Embed Size (px)

Citation preview

LIQUIDITY PROVISION DURING THE CRISIS OF 1914:

PRIVATE AND PUBLIC SOURCES

BY MARGARET M. JACOBSON*

ELLIS W. TALLMAN**

For presentation at: the Workshop on Monetary and Financial History held at the Federal Reserve Bank of Atlanta, June 24-27, 2013 *Federal Reserve Bank of Cleveland ** Oberlin College and Federal Reserve Bank of Cleveland Disclaimer: These are the views of the authors and not those of the Federal Reserve Bank of Cleveland or the Federal Reserve System.

INTRODUCTION

• Compares 1914 to the outcomes of the National Banking Era panics of 1873, 1893, and 1907

• Explores why crisis prevention mechanisms were better in 1914 than in the other crises

• 1914 supported stable deposit levels to promote the expansion of the aggregate money supply

• Investigates the previously overlooked palliative role of clearing house loan certificates in the New York City

OUTLINE

• Background

• Data

• Empirical Methods and Results

• Discussion/Extensions

• Conclusions

BACKGROUND

• Crisis of 1914 in the United States

• Not a major event

• But could have been

• Before the Federal Reserve System was operational

• Fed “operational” in mid-November 1914

• Liquidity crisis – but no banking panic

• Intervention by policymakers and market participants

• Policymaker intervention (public liquidity provision)

• Issuance of Aldrich-Vreeland emergency currency

• Market participants (private liquidity provision)

• Clearing house loan certificates (CHLCs)

CONDITIONS IN JULY 1914

• Trepidations in European financial markets

• Political situation – impending war

• July 27-July 30 European stock markets, bourses close

• Prevent stock market dislocations and gold outflows

• July 31 New York Exchange closed by Secretary of the Treasury William McAdoo

• After consulting with and with support from the New York Stock Exchange

NEW YORK STOCK EXCHANGE

• Financial conditions in New York were benign

• Compared to Europe

• Stock market closure prevented:

• Liquidation of the US gold supply

• Throughout July, foreign investors were liquidating US stocks into gold and shipping the gold to London

• Gold standard implied that gold outflows could induce a contraction the base money supply

• Stock liquidations

• Policymakers feared fire sales of assets

• Silber (2007) suggests that fears were unwarranted

CRISIS CONDITIONS

• Structure of the National Banking System

• No explicit lender of last resort

• No mechanism to adjust base money supply rapidly

• Financial system prone to runs by banks, depositors

• New York national banks - reserve depositories

• Pyramid structure of bank reserves

• New York City national banks held their excess reserves in the call loan market at the New York Stock Exchange

• “Demand” loans as ‘liquid’

• Closure of the New York Stock Exchange

• Made call loans illiquid – clear risk of cash scramble

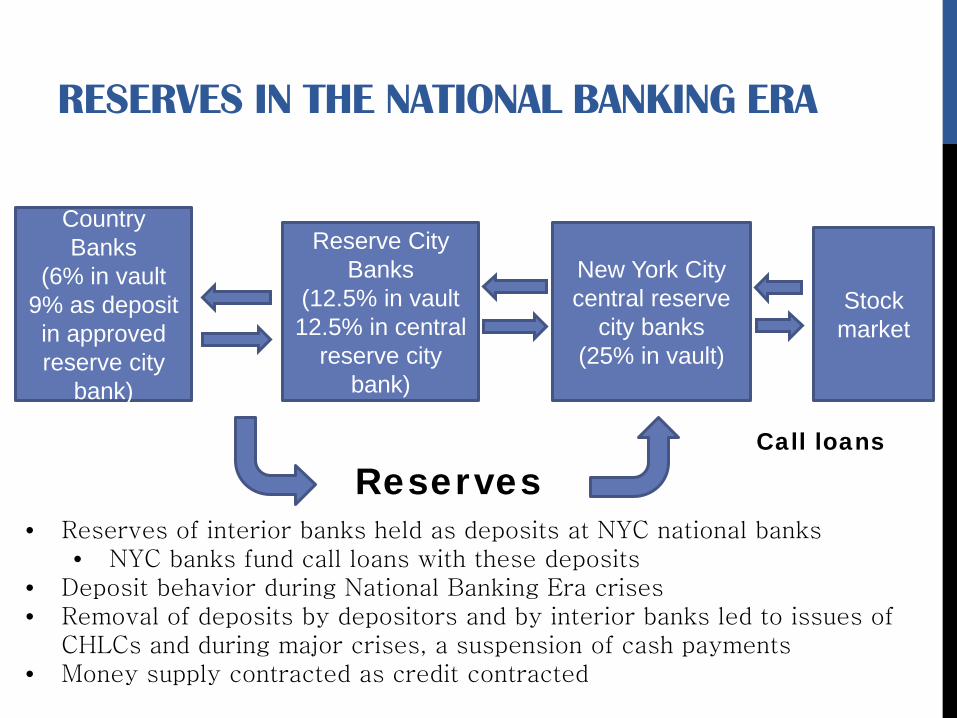

RESERVES IN THE NATIONAL BANKING ERA

Country Banks

(6% in vault 9% as deposit in approved reserve city

bank)

Reserve City Banks

(12.5% in vault 12.5% in central

reserve city bank)

New York City central reserve

city banks (25% in vault)

Stock market

Reserves Call loans

• Reserves of interior banks held as deposits at NYC national banks • NYC banks fund call loans with these deposits

• Deposit behavior during National Banking Era crises • Removal of deposits by depositors and by interior banks led to issues of

CHLCs and during major crises, a suspension of cash payments • Money supply contracted as credit contracted

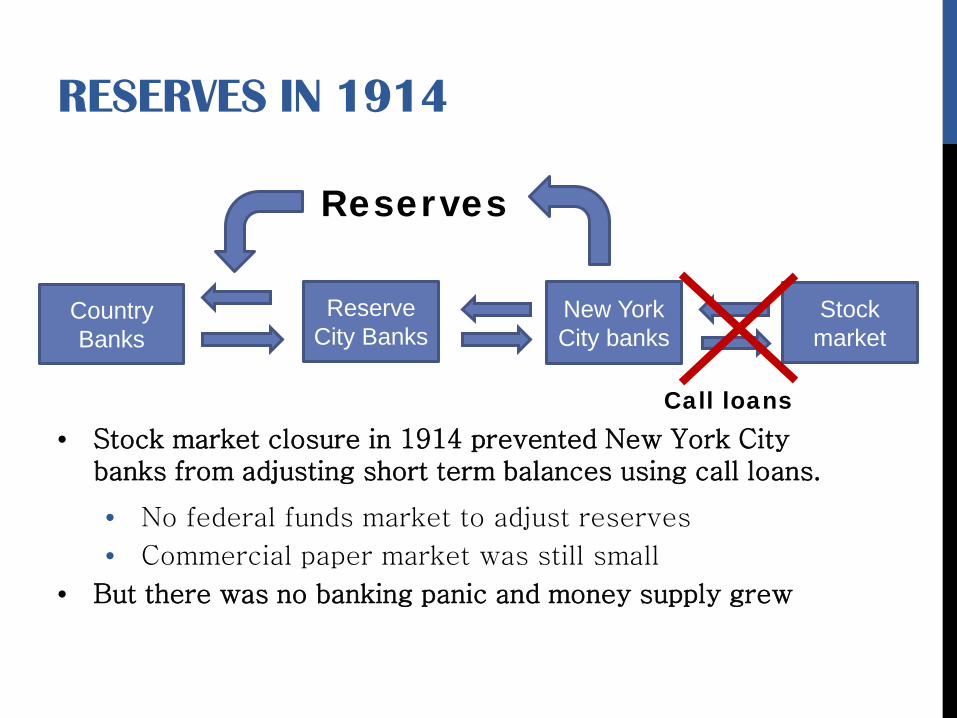

RESERVES IN 1914

Country Banks

Reserve City Banks

New York City banks

Stock market

• Stock market closure in 1914 prevented New York City banks from adjusting short term balances using call loans.

• No federal funds market to adjust reserves

• Commercial paper market was still small

• But there was no banking panic and money supply grew

Reserves

Call loans

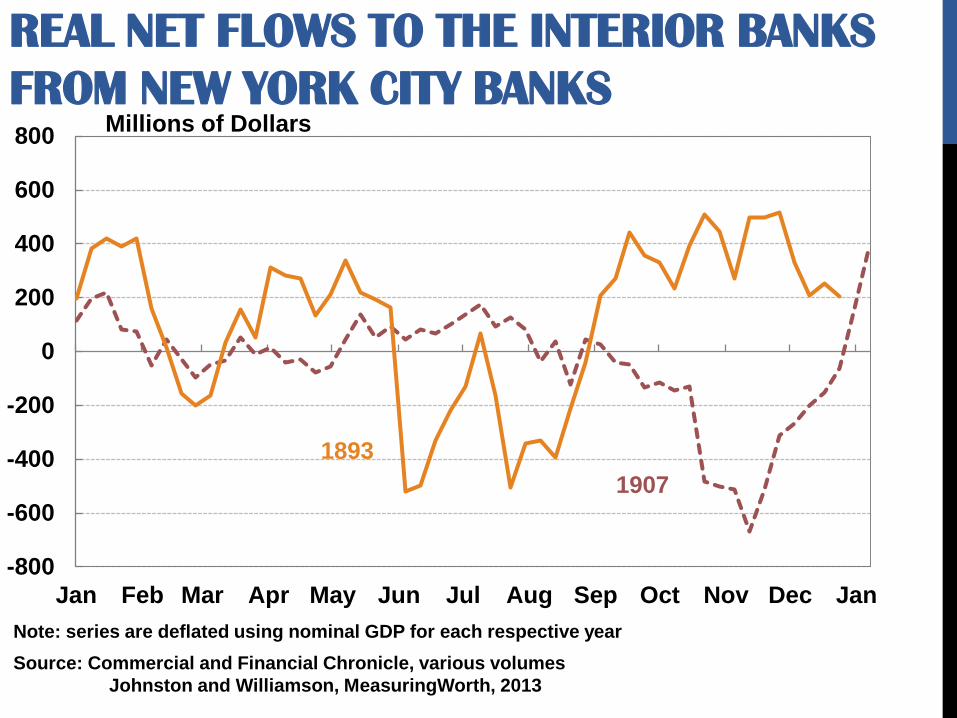

REAL NET FLOWS TO THE INTERIOR BANKS FROM NEW YORK CITY BANKS

-800

-600

-400

-200

0

200

400

600

800

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan

Millions of Dollars

Source: Commercial and Financial Chronicle, various volumes Johnston and Williamson, MeasuringWorth, 2013

Note: series are deflated using nominal GDP for each respective year

1893 1907

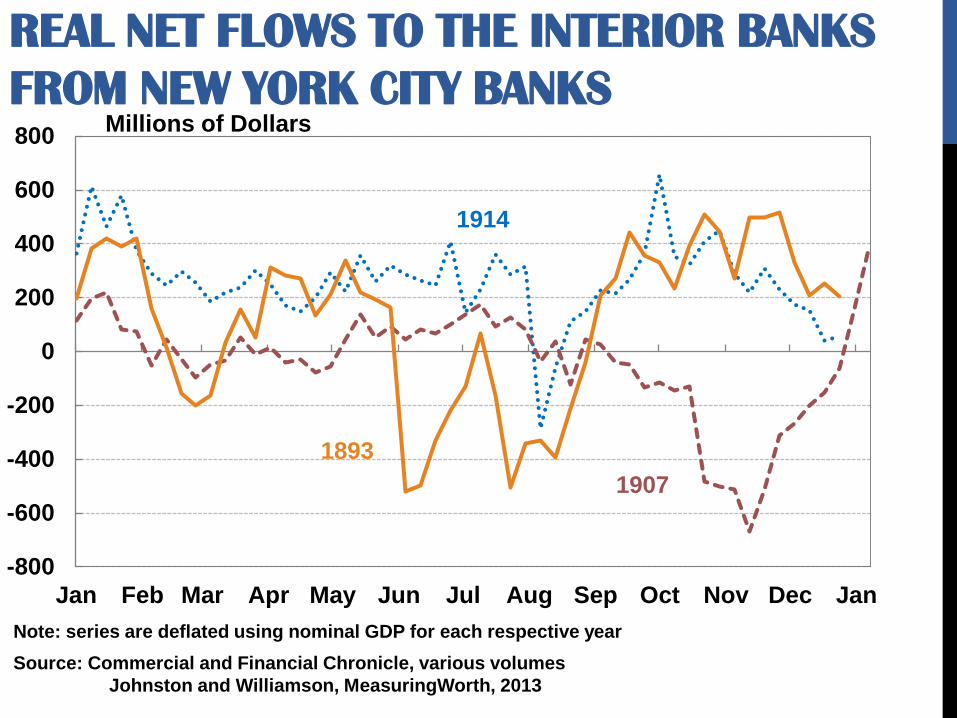

REAL NET FLOWS TO THE INTERIOR BANKS FROM NEW YORK CITY BANKS

-800

-600

-400

-200

0

200

400

600

800

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan

1914

Millions of Dollars

Source: Commercial and Financial Chronicle, various volumes Johnston and Williamson, MeasuringWorth, 2013

Note: series are deflated using nominal GDP for each respective year

1893 1907

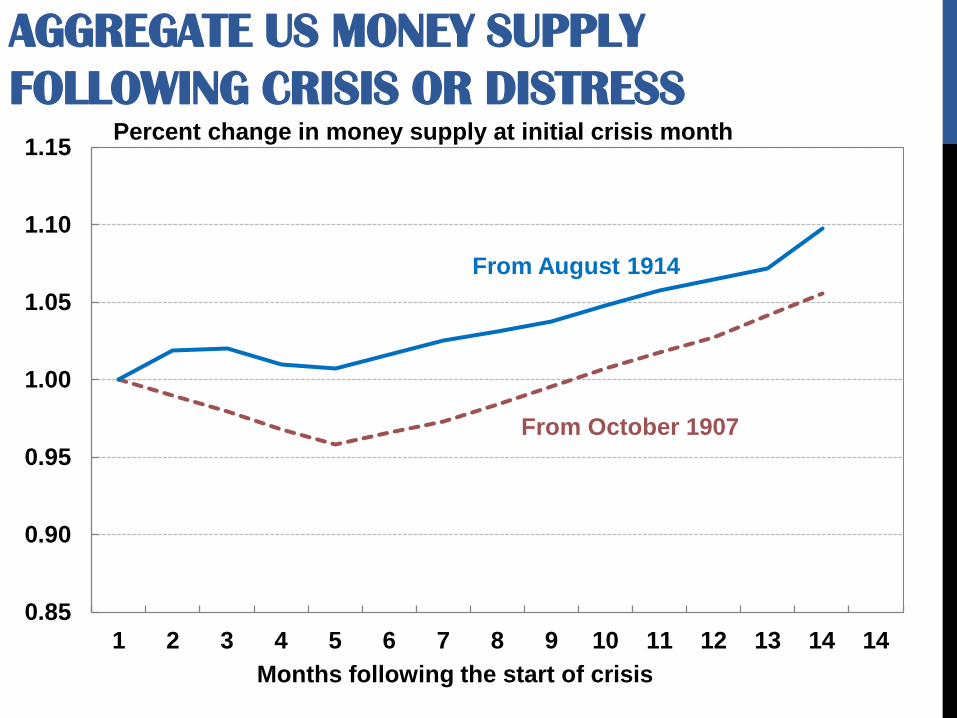

AGGREGATE US MONEY SUPPLY FOLLOWING CRISIS OR DISTRESS

0.85

0.90

0.95

1.00

1.05

1.10

1.15

1 2 3 4 5 6 7 8 9 10 11 12 13 14 14Months following the start of crisis

Percent change in money supply at initial crisis month

From August 1914

From October 1907

QUESTIONS TO BE ADDRESSED

• New York City banks were shut off from their main source of financial liquidity in 1914

• Why was there no banking panic in 1914?

• Why was the outcome of 1914 so different from the previous panics of the National Banking Era?

EXISTING LITERATURE • The success in 1914 associated with:

• Actions of policymakers (Silber 2007)

• The invention of emergency currency (Friedman and Schwartz 1963, Wicker 2005, Silber 2007)

• Clearing house loan certificates seen as a relics

• But contemporary observers of the 1914 distress attribute success to both forms of liquidity

• Noyes (1916)

• Commercial and Financial Chronicle (1915)

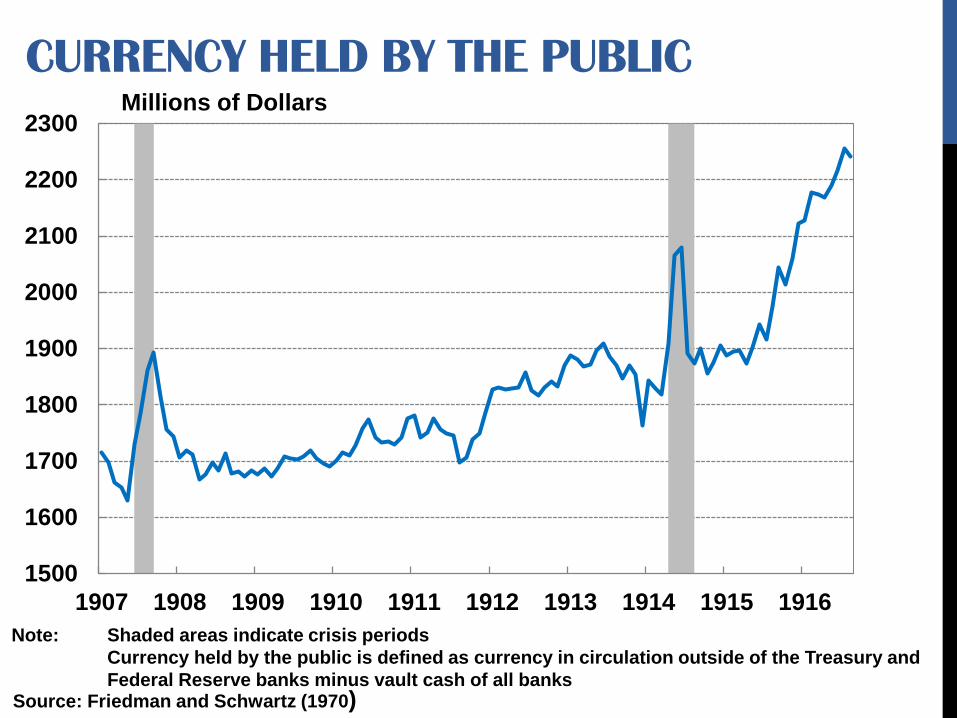

CURRENCY HELD BY THE PUBLIC

1500

1600

1700

1800

1900

2000

2100

2200

2300

1907 1908 1909 1910 1911 1912 1913 1914 1915 1916

Millions of Dollars

Source: Friedman and Schwartz (1970)

Note: Shaded areas indicate crisis periods Currency held by the public is defined as currency in circulation outside of the Treasury and Federal Reserve banks minus vault cash of all banks

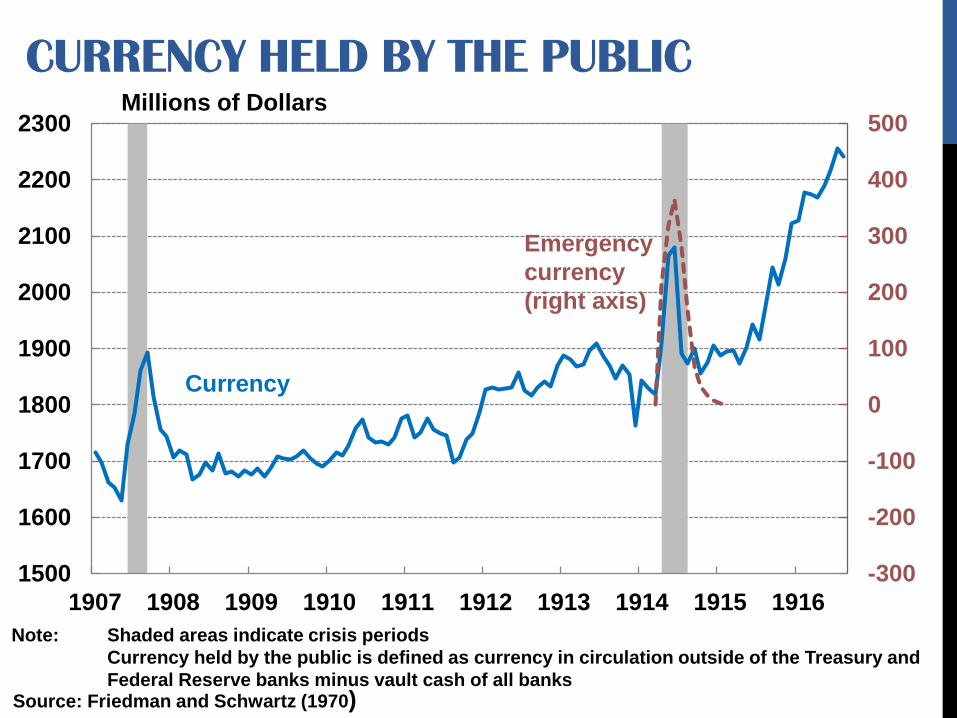

CURRENCY HELD BY THE PUBLIC

-300

-200

-100

0

100

200

300

400

500

1500

1600

1700

1800

1900

2000

2100

2200

2300

1907 1908 1909 1910 1911 1912 1913 1914 1915 1916

Millions of Dollars

Source: Friedman and Schwartz (1970)

Note: Shaded areas indicate crisis periods Currency held by the public is defined as currency in circulation outside of the Treasury and Federal Reserve banks minus vault cash of all banks

Currency

Emergency currency (right axis)

DATA

• New York City clearing house member banks

• New York Clearing House banks represented:

• Nearly half of U.S. banking assets in 1914

• Most acutely affected by stock market closure

• What we have:

• Daily data on emergency currency and clearing house loan certificates requested and received by bank

• Weekly balance sheet items (a subset) for each bank leading up to and following the onset of the distress

• Aggregate banking data weekly for clearing house member banks during the distress

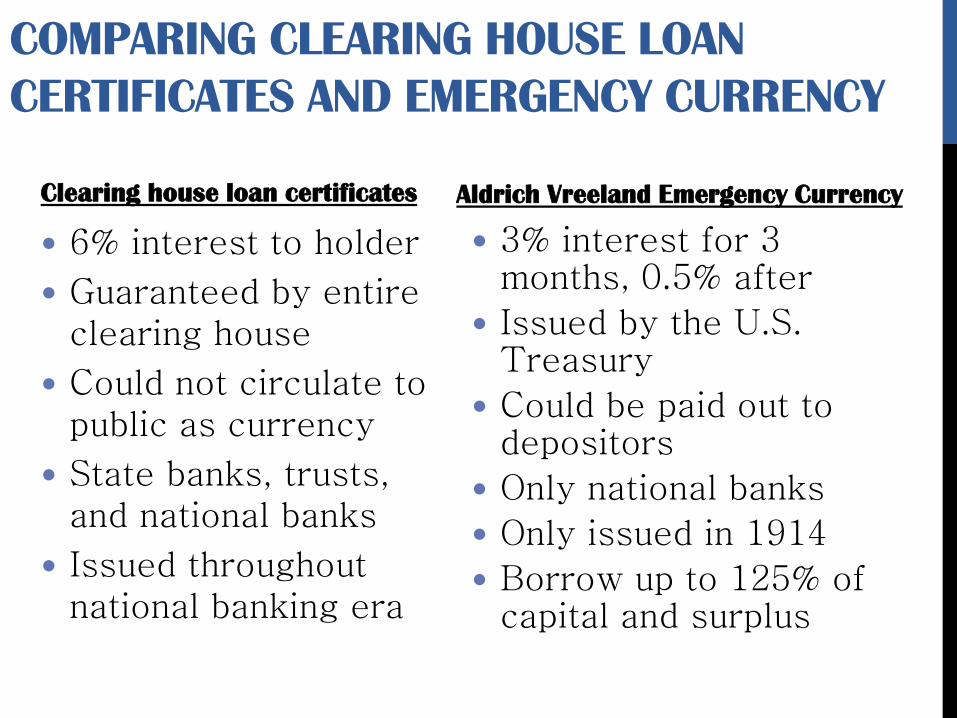

COMPARING CLEARING HOUSE LOAN CERTIFICATES AND EMERGENCY CURRENCY

6% interest to holder

Guaranteed by entire clearing house

Could not circulate to public as currency

State banks, trusts, and national banks

Issued throughout national banking era

3% interest for 3 months, 0.5% after

Issued by the U.S. Treasury

Could be paid out to depositors

Only national banks

Only issued in 1914

Borrow up to 125% of capital and surplus

Clearing house loan certificates Aldrich Vreeland Emergency Currency

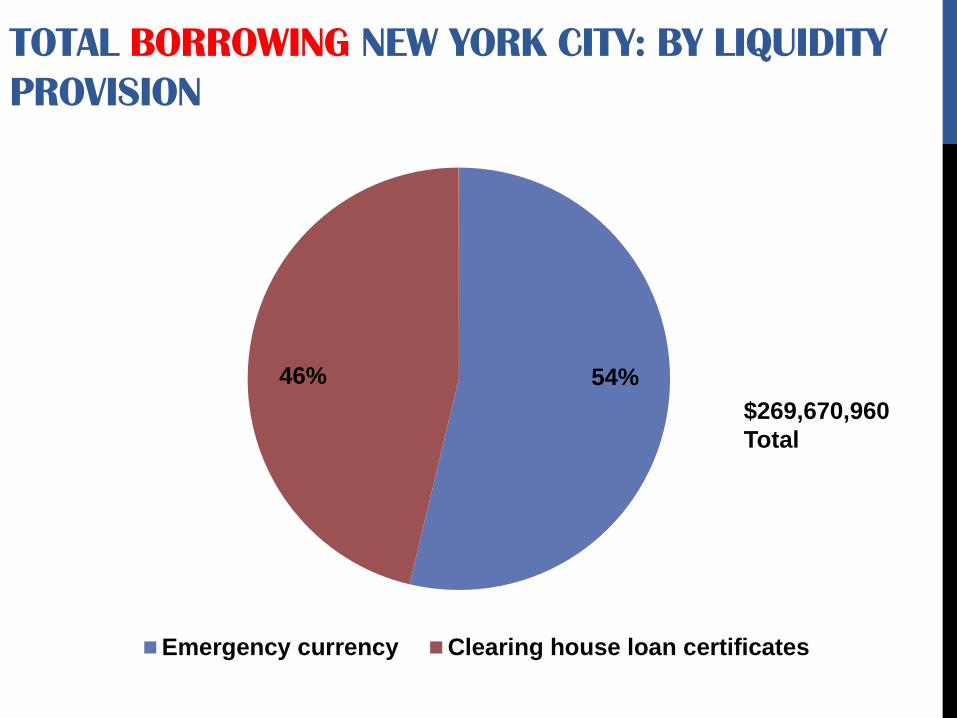

TOTAL BORROWING NEW YORK CITY: BY LIQUIDITY PROVISION

54% 46%

Emergency currency Clearing house loan certificates

$269,670,960 Total

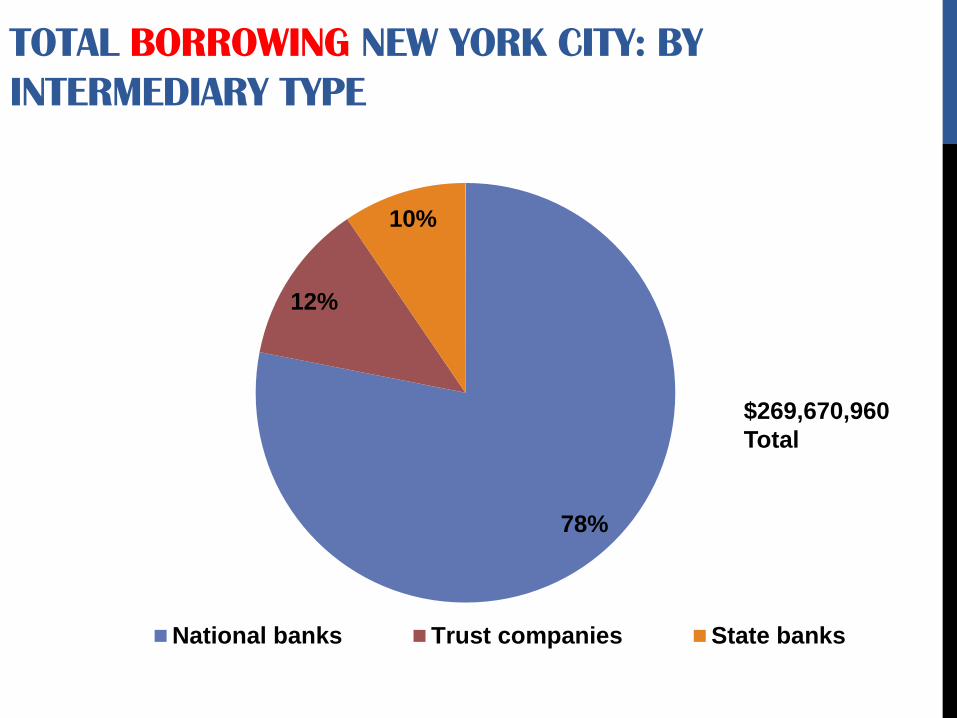

TOTAL BORROWING NEW YORK CITY: BY INTERMEDIARY TYPE

78%

12%

10%

National banks Trust companies State banks

$269,670,960 Total

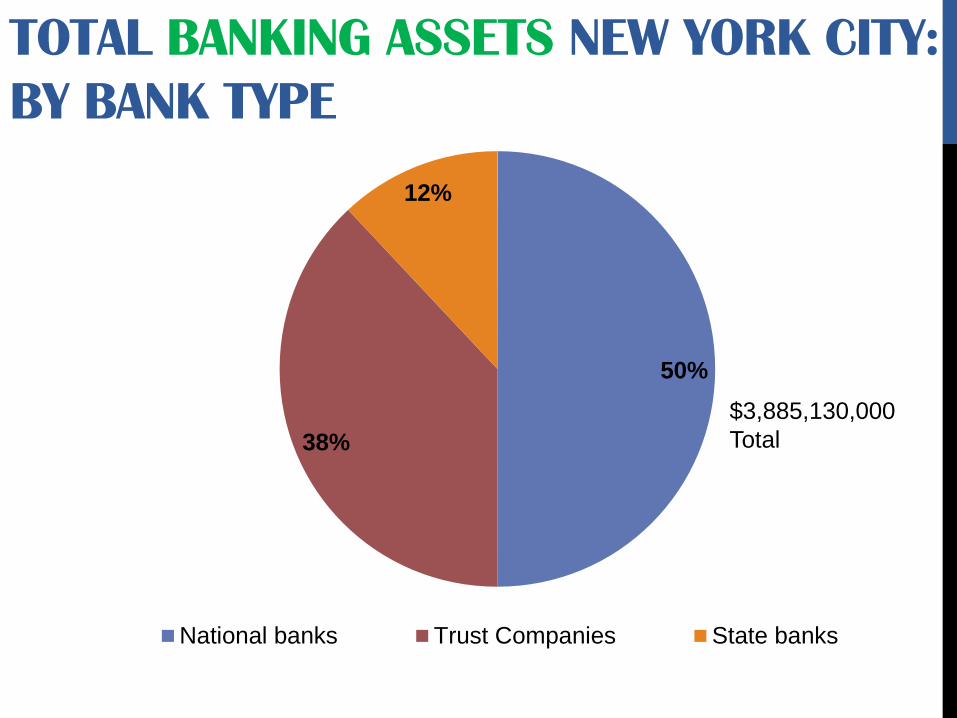

TOTAL BANKING ASSETS NEW YORK CITY: BY BANK TYPE

50%

38%

12%

National banks Trust Companies State banks

$3,885,130,000 Total

0

20

40

60

80

100

120

140

160

Aug-1914 Sep-1914 Oct-1914 Nov-1914 Dec-1914 Jan-1915 Feb-1915

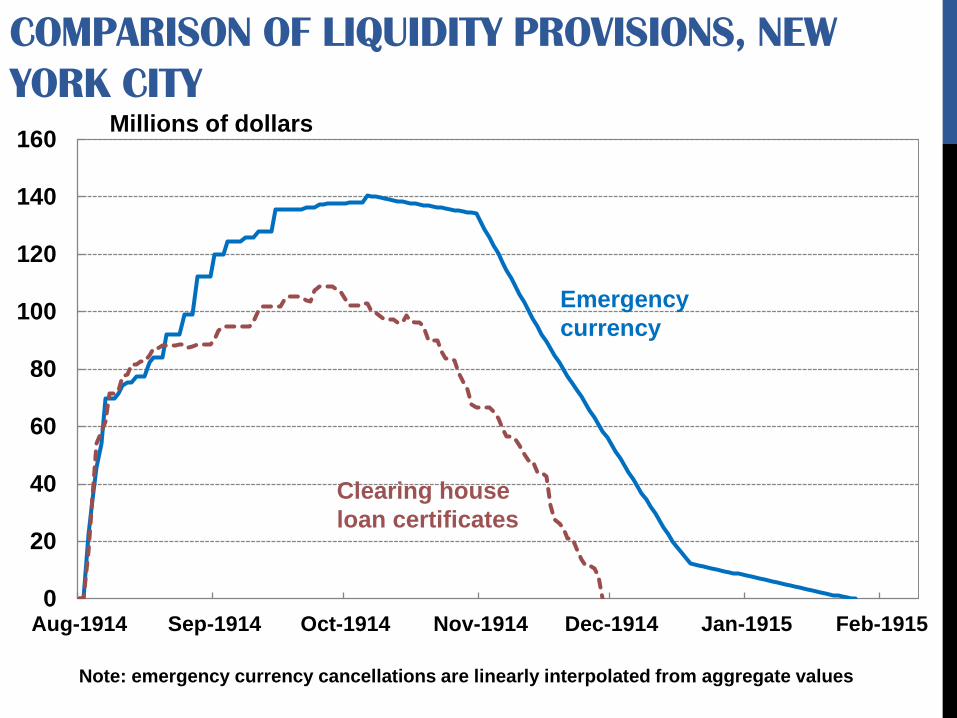

COMPARISON OF LIQUIDITY PROVISIONS, NEW YORK CITY

Emergency currency

Clearing house loan certificates

Millions of dollars

Note: emergency currency cancellations are linearly interpolated from aggregate values

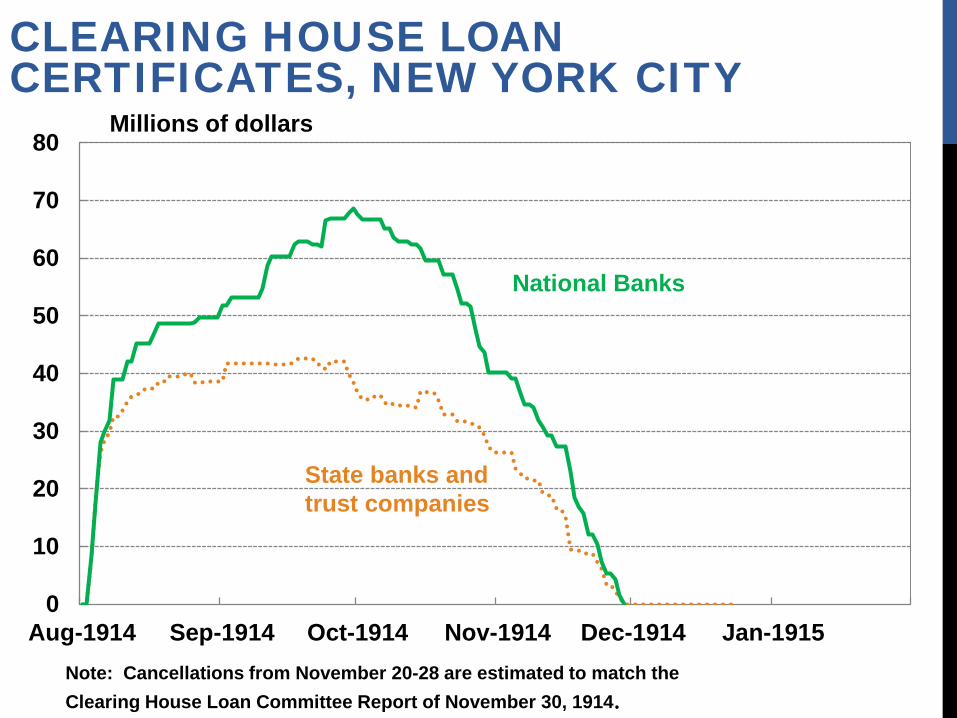

CLEARING HOUSE LOAN CERTIFICATES, NEW YORK CITY

Millions of dollars

0

10

20

30

40

50

60

70

80

Aug-1914 Sep-1914 Oct-1914 Nov-1914 Dec-1914 Jan-1915

National Banks

State banks and trust companies

Note: Cancellations from November 20-28 are estimated to match the Clearing House Loan Committee Report of November 30, 1914.

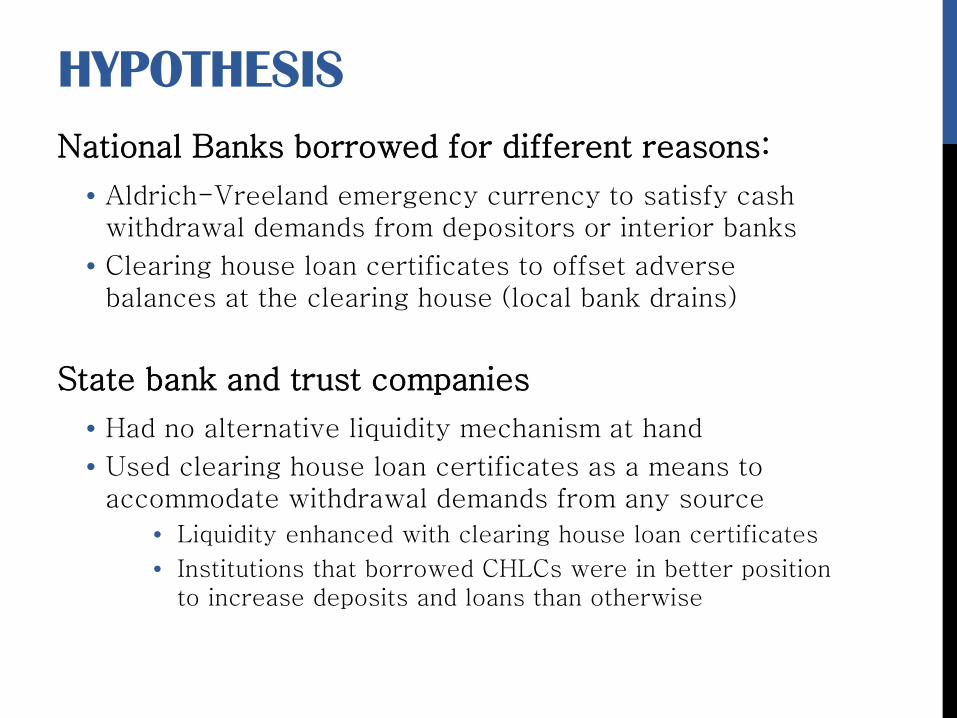

HYPOTHESIS National Banks borrowed for different reasons:

• Aldrich-Vreeland emergency currency to satisfy cash withdrawal demands from depositors or interior banks

• Clearing house loan certificates to offset adverse balances at the clearing house (local bank drains)

State bank and trust companies

• Had no alternative liquidity mechanism at hand

• Used clearing house loan certificates as a means to accommodate withdrawal demands from any source

• Liquidity enhanced with clearing house loan certificates

• Institutions that borrowed CHLCs were in better position to increase deposits and loans than otherwise

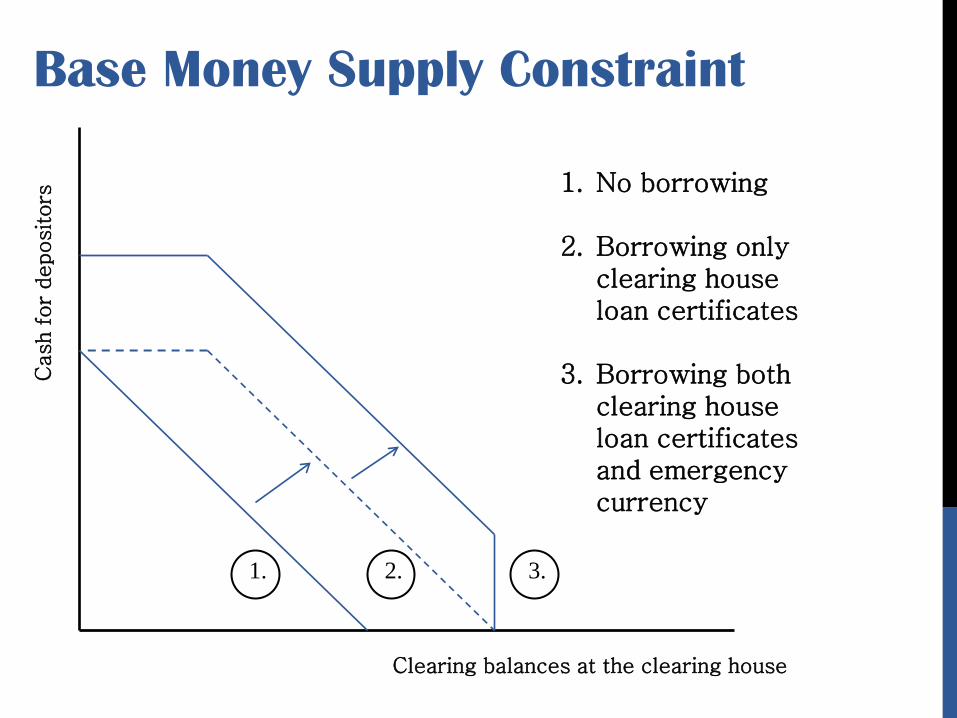

Cash f

or

depositors

Clearing balances at the clearing house

Base Money Supply Constraint

1. 2. 3.

1. No borrowing

2. Borrowing only clearing house loan certificates

3. Borrowing both clearing house loan certificates and emergency currency

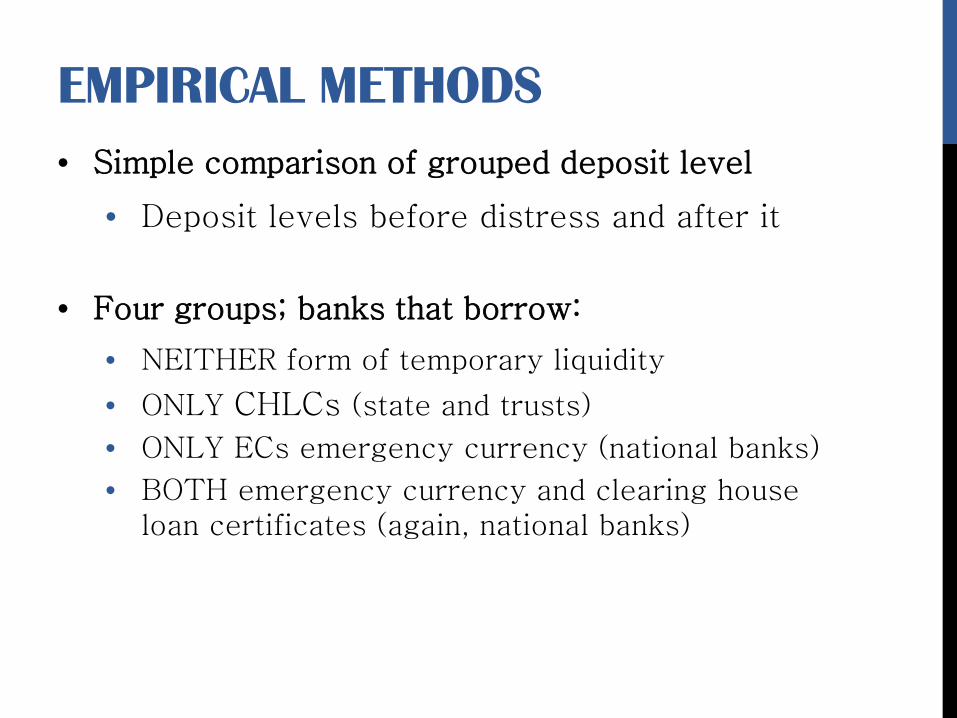

EMPIRICAL METHODS • Simple comparison of grouped deposit level

• Deposit levels before distress and after it

• Four groups; banks that borrow:

• NEITHER form of temporary liquidity

• ONLY CHLCs (state and trusts)

• ONLY ECs emergency currency (national banks)

• BOTH emergency currency and clearing house loan certificates (again, national banks)

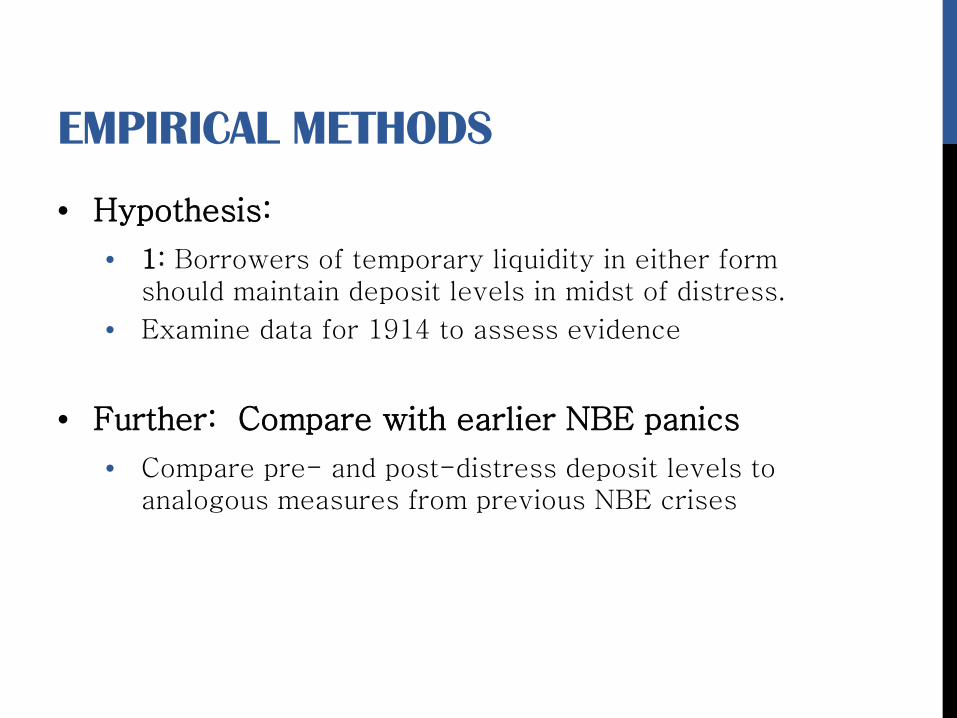

EMPIRICAL METHODS

• Hypothesis:

• 1: Borrowers of temporary liquidity in either form should maintain deposit levels in midst of distress.

• Examine data for 1914 to assess evidence

• Further: Compare with earlier NBE panics

• Compare pre- and post-distress deposit levels to analogous measures from previous NBE crises

800

900

1000

1100

1200

1300

1400

1500

1600

1700

Jul-1914 Oct-1914 Jan-1915 Apr-1915 Jul-1915

Loans

Net Deposits

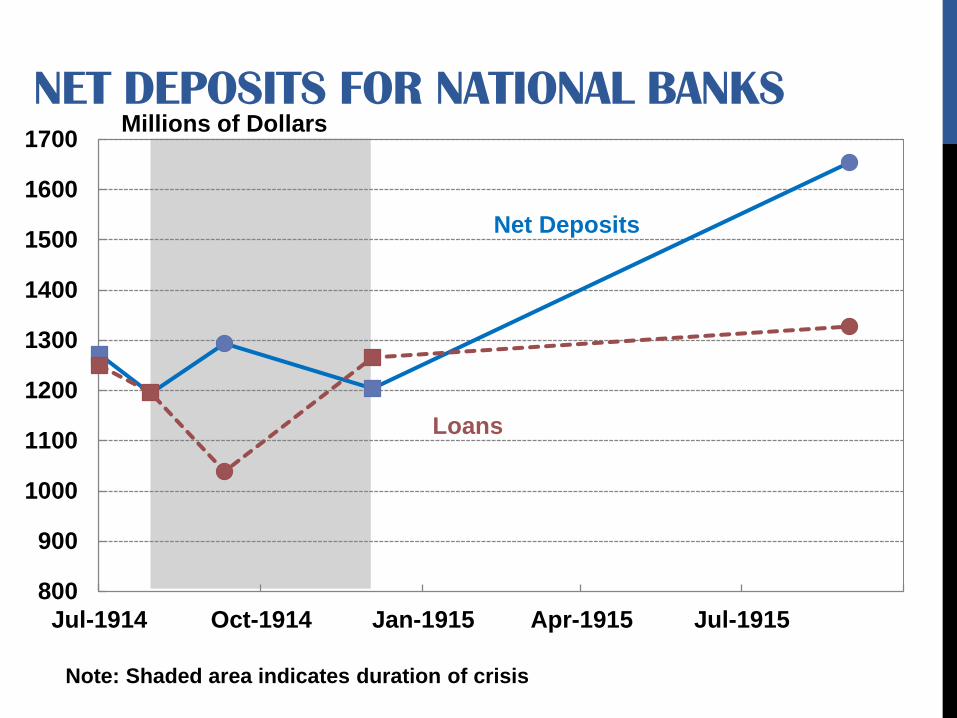

NET DEPOSITS FOR NATIONAL BANKS Millions of Dollars

Note: Shaded area indicates duration of crisis

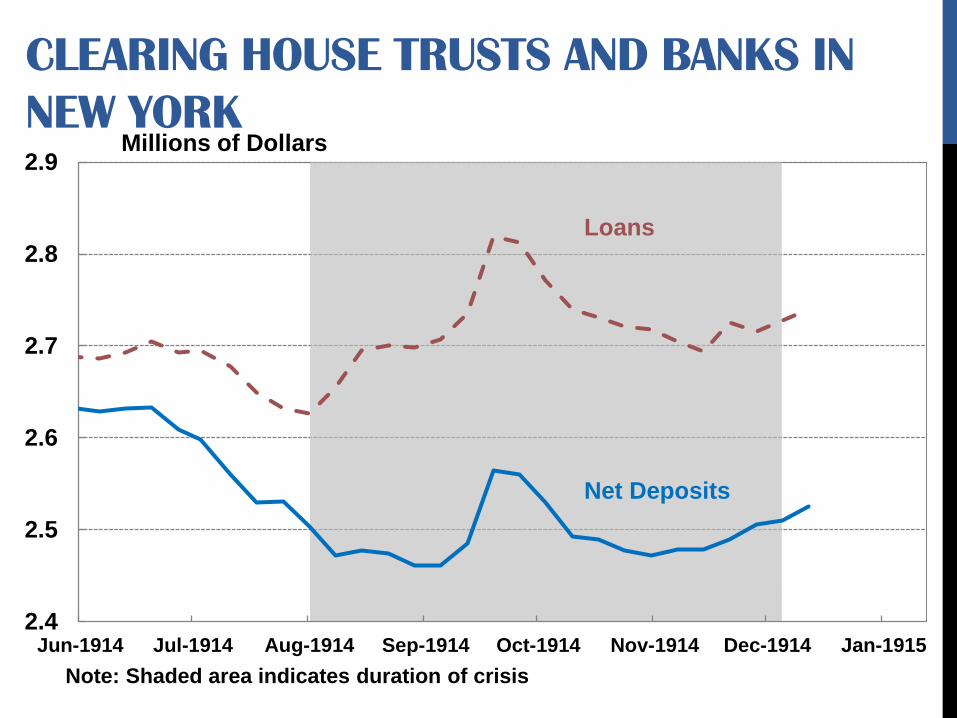

CLEARING HOUSE TRUSTS AND BANKS IN NEW YORK

2.4

2.5

2.6

2.7

2.8

2.9

Jun-1914 Jul-1914 Aug-1914 Sep-1914 Oct-1914 Nov-1914 Dec-1914 Jan-1915

Millions of Dollars

Loans

Net Deposits

Note: Shaded area indicates duration of crisis

-400

-300

-200

-100

0

100

200

300

400

500

800

900

1000

1100

1200

1300

1400

1500

1600

1700

Jul-1914 Oct-1914 Jan-1915 Apr-1915 Jul-1915

NET DEPOSITS FOR NATIONAL BANKS Millions of Dollars

Loans

Net Deposits

Total borrowing (right axis)

Note: Shaded area indicates duration of crisis

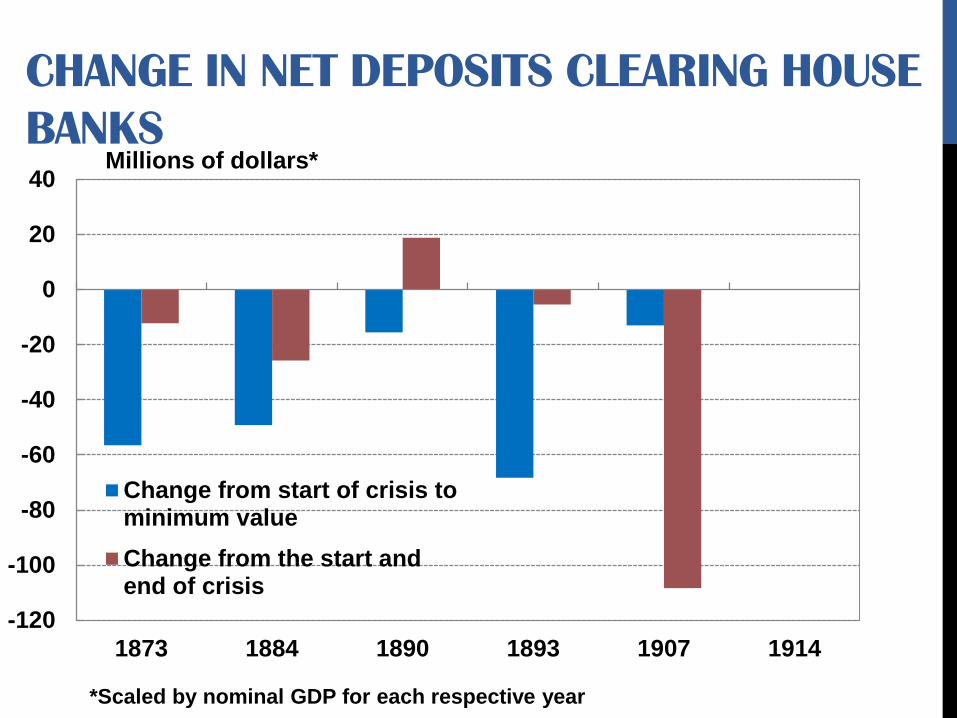

CHANGE IN NET DEPOSITS CLEARING HOUSE BANKS

-120

-100

-80

-60

-40

-20

0

20

40

1873 1884 1890 1893 1907 1914

Change from start of crisis tominimum valueChange from the start andend of crisis

Millions of dollars*

*Scaled by nominal GDP for each respective year

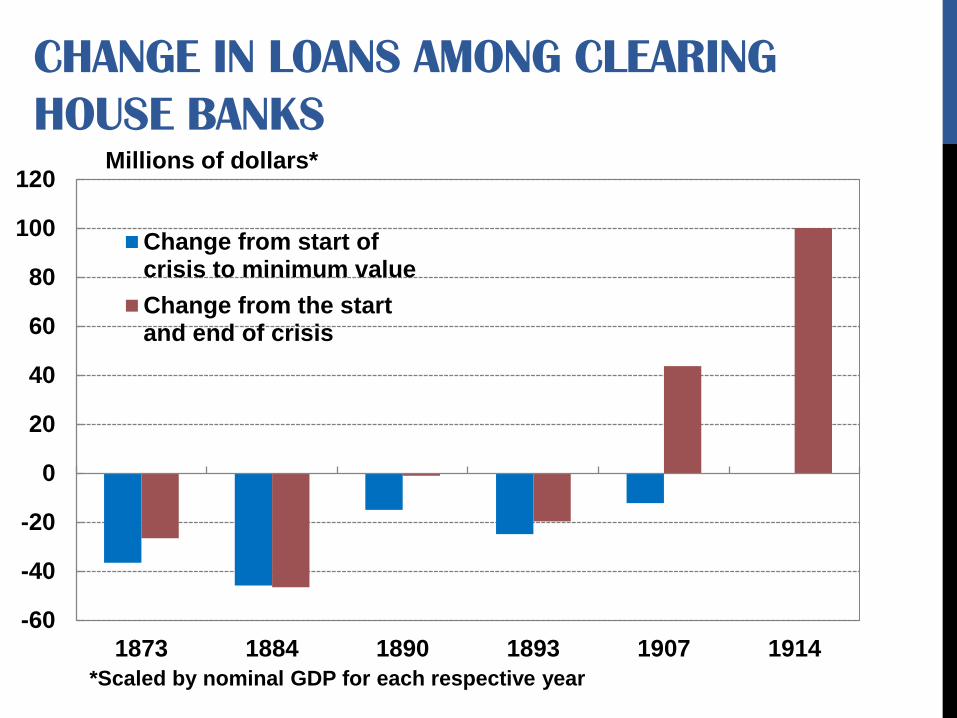

CHANGE IN LOANS AMONG CLEARING HOUSE BANKS

-60

-40

-20

0

20

40

60

80

100

120

1873 1884 1890 1893 1907 1914

Change from start ofcrisis to minimum valueChange from the startand end of crisis

Millions of dollars*

*Scaled by nominal GDP for each respective year

DATA SUMMARY

• Banking activity and intermediation

• Contracted during the three major NBE panics

• Remained flat in 1914.

• Is borrowing status associated with deposit level changes?

• Examine net deposit levels from the August and December weekly reports in the Commercial and Financial Chronicle

• Group data by borrowing status – four groups

TOTAL NET DEPOSITS BY BORROWING STATUS

9.29

15.28

-3.06

2.09

-5

0

5

10

15

20

Emergencycurrency only

Clearing houseloan certificates

only

Both No borrowing

%

%

%

%

December 1914 – August 1914 percent change

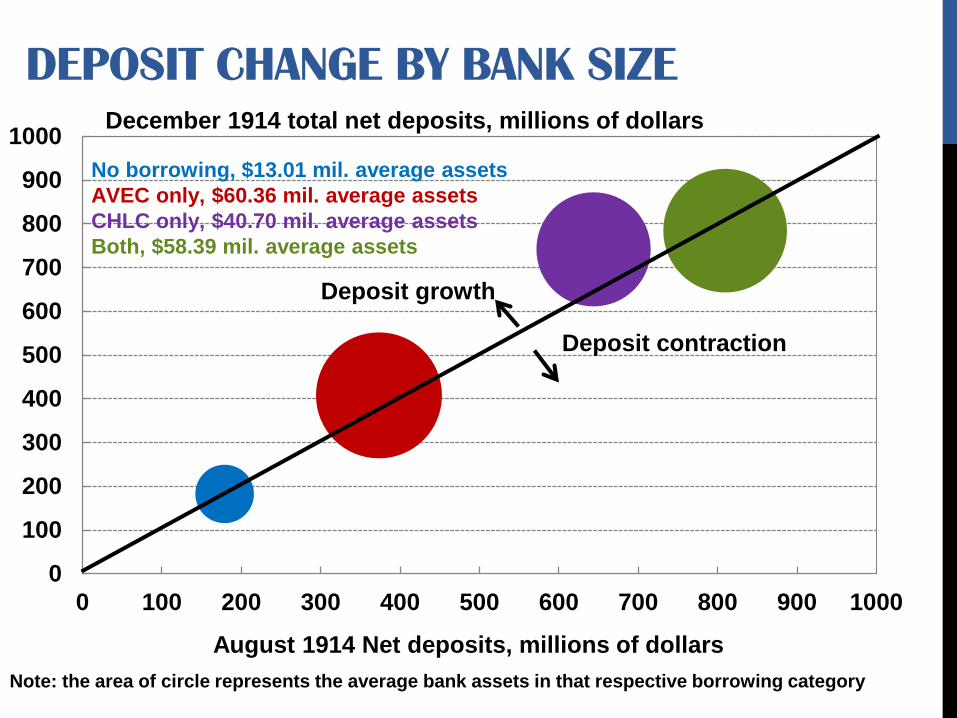

DEPOSIT CHANGE BY BANK SIZE

0

100

200

300

400

500

600

700

800

900

1000

0 100 200 300 400 500 600 700 800 900 1000

No borrowing, $13.01 mil. average assets AVEC only, $60.36 mil. average assets CHLC only, $40.70 mil. average assets Both, $58.39 mil. average assets

Deposit growth

Deposit contraction

December 1914 total net deposits, millions of dollars

August 1914 Net deposits, millions of dollars Note: the area of circle represents the average bank assets in that respective borrowing category

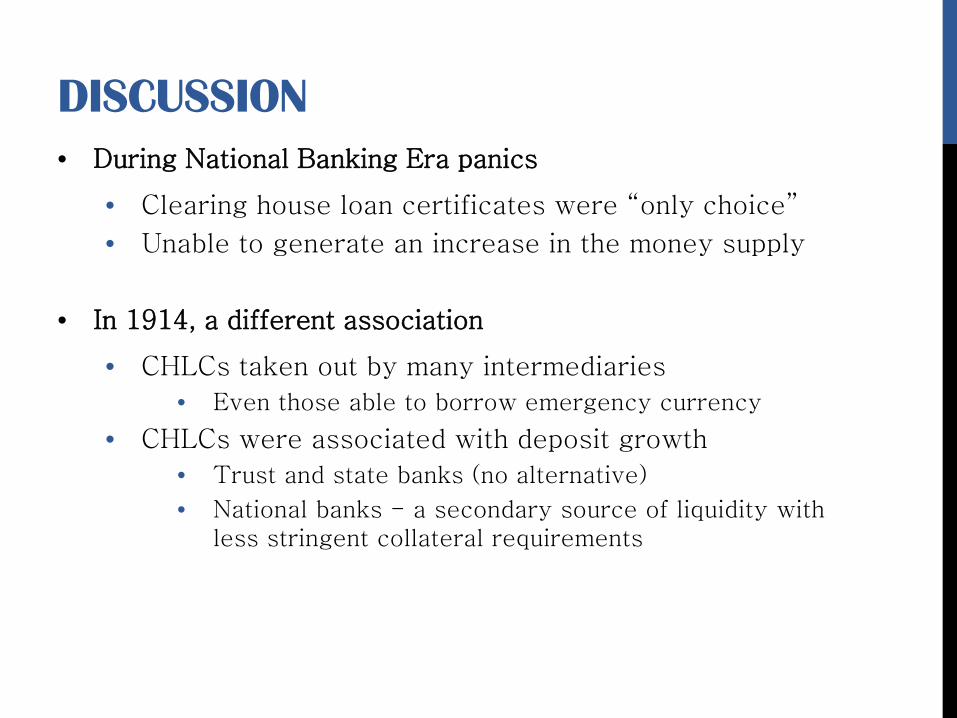

DISCUSSION • During National Banking Era panics

• Clearing house loan certificates were “only choice”

• Unable to generate an increase in the money supply

• In 1914, a different association

• CHLCs taken out by many intermediaries

• Even those able to borrow emergency currency

• CHLCs were associated with deposit growth

• Trust and state banks (no alternative)

• National banks - a secondary source of liquidity with less stringent collateral requirements

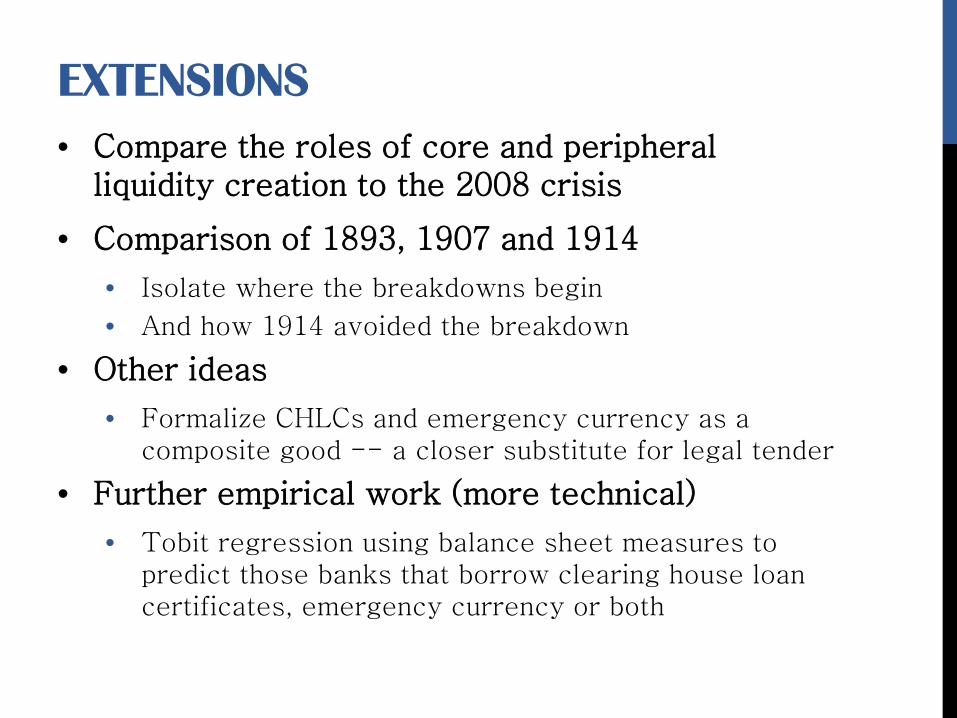

EXTENSIONS • Compare the roles of core and peripheral

liquidity creation to the 2008 crisis

• Comparison of 1893, 1907 and 1914

• Isolate where the breakdowns begin

• And how 1914 avoided the breakdown

• Other ideas

• Formalize CHLCs and emergency currency as a composite good -- a closer substitute for legal tender

• Further empirical work (more technical)

• Tobit regression using balance sheet measures to predict those banks that borrow clearing house loan certificates, emergency currency or both

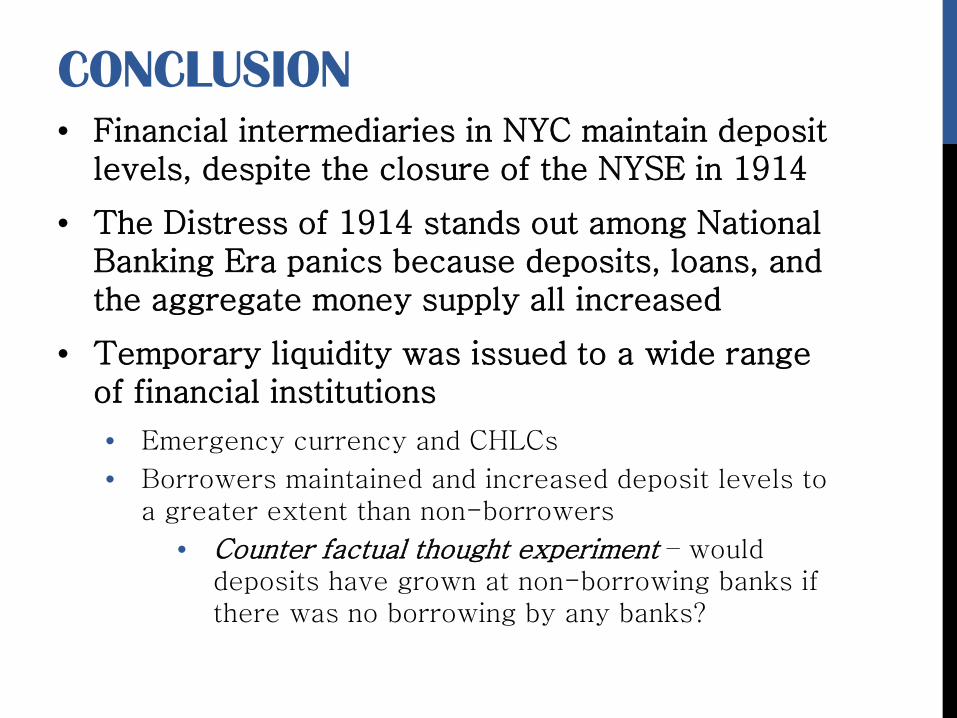

CONCLUSION • Financial intermediaries in NYC maintain deposit

levels, despite the closure of the NYSE in 1914

• The Distress of 1914 stands out among National Banking Era panics because deposits, loans, and the aggregate money supply all increased

• Temporary liquidity was issued to a wide range of financial institutions

• Emergency currency and CHLCs

• Borrowers maintained and increased deposit levels to a greater extent than non-borrowers

• Counter factual thought experiment – would deposits have grown at non-borrowing banks if there was no borrowing by any banks?