Embed Size (px)

Citation preview

LIQUIDITY ANALYSIS OF NEPAL INVESTMENT BANK LTD.

Contents

Acknowledgement …………………………………………………….I Table of content……………………………………………………………II List of table………………………………………………………………...III

Table of ContentsChapter- one

1. Introduction1.1. concept of banking1.2. The banking in Nepal1.3. List of commercial bank in Nepal 1.3.1. List of licensed commercial bank in Nepal 1.3.2. Functions of commercial bank1.4. Overview of Nepal investment bank ltd. 1.4.1. Board of directors 1.4.2. Management team 1.4.3. Branches and Counters 1.4.4. Products and Services1.5. Strategies and future plans of Nepal investment

Page No.1112345567889

bank ltd.1.6. Statement of problem1.7. objectives of the study1.8. Significance of the study1.9. Limitations of the study1.10. Scope and importance of the study

9101010

Chapter -two2. Review of Literature 2.1. Conceptual framework 2.1.1. Liquid Assets 2.1.2. Cash Reserve ratio(CRR) 2.1.3. Statutory Liquidity ratio(SLR) 2.1.4. Importance of the liquidity for thebank 2.1.5. Need of the liquidity for the bank 2.1.6. Demand for the liquidity 2.1.7. Supply for the bank liquidity 2.1.8.Criteria of measuring the bank liquidity 2.1.9. Liquidity to be maintained with thecentral bank 2.1.10. penalty for non-compliances 2.1.11. Applicable penalty rates

11111111111212121212121313

2.1.12. Composition 2.1.13 Basis for the liquidity Requirement prediction 2.1.14Review of related study

131414

Chapter three3. Research methodology 3.1. Research design15 3.2. Data collection techniques15 3.3. Data analysis tools 15

3.3.1. Ratios

Chapter Four4.Data presentation and analysis 4.1. Participation of all deposits in the total deposit liability 17 4.2. Liquidity Ratio 17 4.2.1. saving deposit to total deposit ratio 18 4.2.2. fixed deposit to total deposit ratio 19 4.2.3. Cash and bank balance to current deposit ratio20 4.2.4. Cash and bank balance to total deposit ratio 20 4.2.5. Cash and bank balance to total deposit21 (Excluding fixed deposit ) ratio 4.2.6. Balance with NRB to current and saving22 deposit ratio 4.2.7. Balance with NRB to fixed deposit ratio 23 4.2.8. Total investment to total deposit ratio 24 4.2.9. Liquid asset to total deposit ratio 25

Chapter five

5. Summary, Conclusion and Recommendation 5.1. Summary27 5.2 Conclusion

27 5.3. Recommendation 28

Bibliography

List of table

Table No. Table Name Pege no.

1. Participation of the all the deposits in the total deposit liability 17

2. Saving deposit to total deposit ratio 18

3. Fixed deposit to total deposit ratio 19

4. Cash and bank balance to current deposit ratio 20

5. Cash and bank balance to total deposit ratio 20

6. Cash and bank balance to total deposit(excluding fixed deposit) ratio 21

7. Balance with NRB to current and saving deposit 22

8. Balance with NRB to fixed deposit ratio23

9. Total investment to total deposit ratio 24

10. Liquid assets to total deposit ratio 25

CHAPTER – ONE

INTRODUCTION

1.1. CONCEPT OF BANKING:

Generally, bank is an institution which accepts deposits, makes business loans, and offers related services. Commercial banks also allow for a variety of deposit accounts, such as checking, saving, and time deposit. There institutions are run to make a profit and owned by a group of individuals, yet some may be members of the Federal Reserve System. While commercial banks offer services to individuals, they are primary concernedwith receiving deposits and lending to businesses. In an economy the bank is regarded as one of the economic backbone of the country for its development. Bank is a financial institution that deals inmoney. The basic function of bank is collecting deposit and granting the loans. It involves in credit creation that in related to creation of deposit and loan. In the economy, the banks collects small saving of general people, accumulative it and lends the productive sectors of the society for the overall economic development.

Various writers have been defined the word “bank” in different ways.

According to Scholars, “The bank is defined as factory of money for creditwhere it does not purchase goods and sells it rather produces credit inform of deposit and sells it inform of loans.”

According to C.R. Crowther,”A banks collects money from those who have it to spare or who are saving it out of their income and lends this money to those who required it.”Thus in conclusion, we can say that bank is an organization which deals with the monetary transactions for the mobilization of idle money or deposits in productive sectors, is essentially essential for the development of the whole net.

1.2. THE BANKING IN NEPAL

In the context of Nepal, like as in other country the goldsmiths and landlord was the ancient banker. The Nepalese people were highly exploited by shahu mahajan by charging higher interest rate that iscompound interest rate and even by manipulating the principle amounts. If we try to see the history of banking transaction in depth then evidence ofmoney landing function are found in practice before 8th century in 780 B.S. 1

gunakamdev the ruler of Kathmandu reconstructed Kathmandu valley by borrowing dept from the people. In 14th century tankdhari system had been running in the period of ranodip shing inKathmandu established and office called tejarath adda. From the office the government distributed salary totheir employees and provided loan to government employment @5% of interestagainst the security gold, silver etc.

Because of the development of economy activities in Nepal the above institutions could not be fulfilled the need of people. Soin kartik 30, 1994 B.S. Nepal bank was established as one of the semi government commercial bank which had 10 million authorized capital and 842000 paid of capital. it has done the pioneering function in function spreading the banking habits among the people. Having felt a need of central bank to control and direct the commercial bank and help the government for making monitory polices Nepal rastra bank was set up in 14 baishakht, 2013 B.S.

To fulfill the growing credit requirement of the country. The commercial bank i.e. Rastraya Banijya bank was establishes in 10th bhadra 2022 B.S. this bank also provides facility for the economy welfare of the general public. Nepal is an agricultural country to develop agriculture system. Industry agriculture development bank and Nepal industrial development corporation was established in 2024 B.S. 2016 B.S. respectively.

The initiation of the financial sector; liberalization policy by Nepal rastra bank, a board of joint venture banks entered with the view to accelerate the race of development of nation. At present, there are many joint venture banks which are running successfully in a

competitive environment. His majesty government deliberates policy of allowing foreign joint venture banks to operate in Nepal basically targeted, to encourage local tradition commercial bank to enhance their capacity through competitor’s efficiencies mechanization modernization prompt customer service. Nepal Arab bank ltd was established in 2041 as a first foreign joint venture bank.

Now in our country there are 31 commercial bank, 87 development bank, 79 finance company and 21 micro credit development banks after mid July 2011(licensed by NRB)

1.3. LIST OF COMMERCIAL BANKS IN NEPAL:

The history of financial and economic development in Nepal is not very old. It has gone through different stages, during the PM Ranodip shingh around 1972 A.D. “TEJARATH ADDA” was introduced, which brought a reform ineconomic and financial section. The main purpose of “TEJARATH ADDA” was toprovide credit facilities to the general public at confessional rate. However the installment of “KHUSI KHANA” as a banking agency during the king Prithivi Narayan Shah could also be regarded as the first step towards banking in Nepal.

2 After that the first commercial bank of Nepal, Nepal bank

Limited (NBL) was lunched with the cooperation of imperial bank of India in November 1937. holding 51% government equity. The second commercial bank, Rastriya Banijya bank come into existence in 1966 A.D. with 100% government ownership. In early 1980, to meet the need of health completion in the financial system, Nepal allowed to entry of foreign banks as joint ventures with up to maximum of 50% equity participation.

Nepal arab bank limited was the first joint venture bank which wasestablished with the joint venture of arab bank emirates in 1984. in 1986, Nepal grind lays bank limited (now chartered bank limited) entered in nepali financial market as a joint venture with ANZ-Grind lays.

1.3.1 LIST OF LICESCED COMMERCIAL BANK IN NEPAL:S.No. Name of commercial banks

1 Nepal Bank ltd.2 Rastriya Banijya Bank Ltd.3 Agriculture Development Bank Ltd.4 Nabil Bank Ltd.5 Nepal Investment Bank Ltd.6 Standard Chartered Bank Nepal Ltd.7 Himalayan Bank Ltd.8 Nepal SBI Bank Ltd.9 Nepal Banladesh Bank Ltd.10 Everest Bank Ltd.11 Bank of Kathmandu Ltd.12 Nepal Credit and Commercial Bank ltd.13 Lumbini Bank Ltd.14 Nepal Industrial and Commercial Bank Ltd.15 Machhapuchre Bank Ltd.16 Kumari Bank Ltd.17 Laxmi Bank Ltd.18 Siddhartha Bank Ltd.19 Global Bank Ltd.20 Citizens Bank International Ltd.21 Prime Commercial Bank Ltd.22 Sunrise Bank Ltd.23 Bank of Asia Nepal Ltd.24 DCBL Bank Ltd.25 NMB Bank Nepal Ltd.26 Kist Bank Ltd.27 Janata Bank Nepal Ltd.28 Mega Bank Nepal Ltd.

329 Commerce and Trust Bank Nepal Ltd.

30 Civil Bank Ltd.31 Century Commercial Bank Ltd.Source:” www.nrb.org.np”

1.3.2 FUNCTIONS OF COMMERCIAL BANKS:

Although profit maximization is a major objective of commercial bank, to achieve this objectives commercial bank performs various functions under the mandatory rules and registrations and directives of NRB and commercialBank Act 2031(1974) which are:

Primary functionsa) accepting Deposits:

Accepting deposits is the main function of commercial banks. Commercial banks collects money from those who want to deposit in different types of deposits accounts such as: Fixed deposit account Current deposit account Saving deposit account

b) Advancing of Loans:Commercial banks provide the required loan or credit to various sectors ofeconomy such as industry, trade, agriculture, business deprived sector etc. in this way bank creates facilities. It provides loans from various procedures in different form such as: Overdraft Cash credit Direct loan with collateral Discounting bill of exchange Loans of money at call and notice

General Utility functionsCommercial banks also form general utility functions such

Issuing of letters of credit to customers Issuing of bank draft and travels cheque etc for transfer of funds from

one place to another. Dealing in foreign exchange and financial foreign trade by accepting or

collecting foreign bill of exchange. Underwriting loans to be raised public bodied and corporations. Providing safety vaults or lock for the safe custody of valuables and

securities of the customers. Remittance of money

4

Agency FunctionsApart from the above function, commercial banks also perform agency functions for which they act as agent and claim commission on some facilities such as:

Collection of customer’s money from other banks. Receipt and payment of dividend and interest. Security brokerage service Financial advisory services To underwrite the government and private securities.

1.4. OVERVIEW OF NEPAL INVESTMENT BANK LTD.

Nepal investment Bank Ltd. (NIBL), previously Nepal Indosuez bank Ltd., was established in 1986 as a joint venture between neplise and French partners. The French partner (holing 50% of the capital of NIBL) was credit agricole Indosuez, a subsidiary of one the largest banking group inthe world. With the decision of credit agricole Indosuez to divest, a group of companies comprising of bankers, professionals, industrialists and business man, had acquired on april 2002 the 50% share holding of credit agricole Indosuez in Nepal Indosuez bank Ltd.

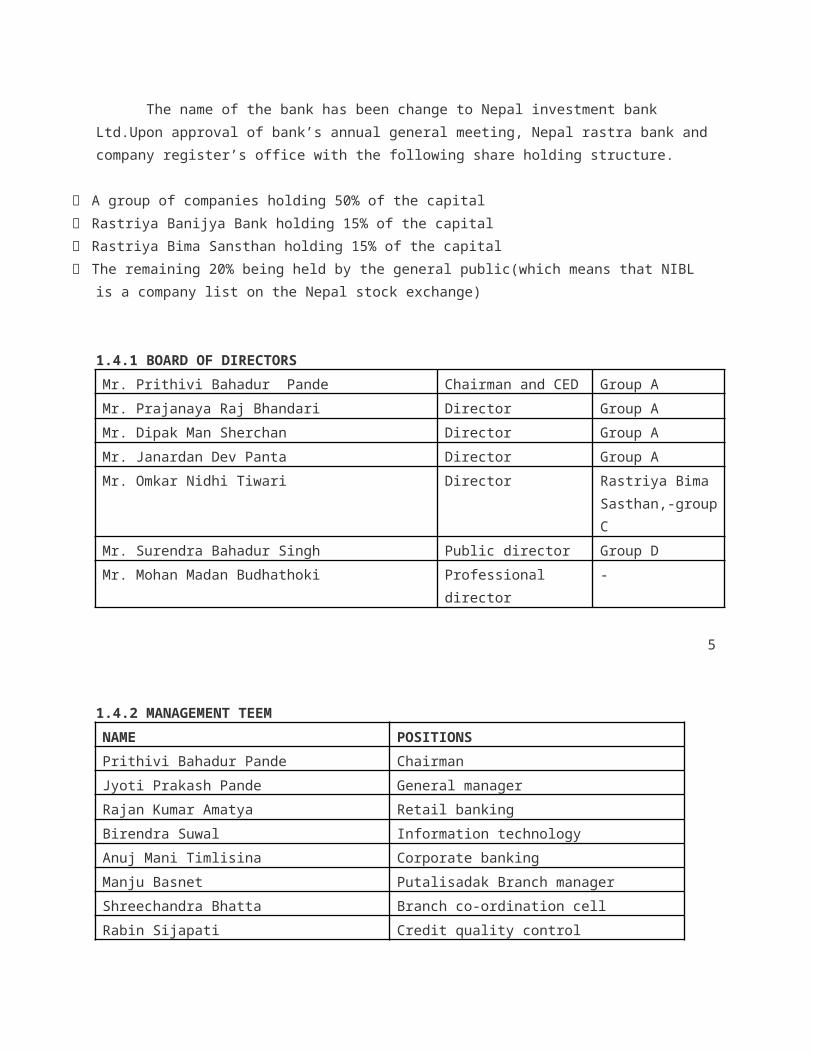

The name of the bank has been change to Nepal investment bank Ltd.Upon approval of bank’s annual general meeting, Nepal rastra bank and company register’s office with the following share holding structure.

A group of companies holding 50% of the capital Rastriya Banijya Bank holding 15% of the capital Rastriya Bima Sansthan holding 15% of the capital The remaining 20% being held by the general public(which means that NIBL

is a company list on the Nepal stock exchange)

1.4.1 BOARD OF DIRECTORS Mr. Prithivi Bahadur Pande Chairman and CED Group AMr. Prajanaya Raj Bhandari Director Group AMr. Dipak Man Sherchan Director Group AMr. Janardan Dev Panta Director Group AMr. Omkar Nidhi Tiwari Director Rastriya Bima

Sasthan,-groupC

Mr. Surendra Bahadur Singh Public director Group DMr. Mohan Madan Budhathoki Professional

director-

5

1.4.2 MANAGEMENT TEEMNAME POSITIONSPrithivi Bahadur Pande ChairmanJyoti Prakash Pande General managerRajan Kumar Amatya Retail bankingBirendra Suwal Information technologyAnuj Mani Timlisina Corporate bankingManju Basnet Putalisadak Branch managerShreechandra Bhatta Branch co-ordination cellRabin Sijapati Credit quality control

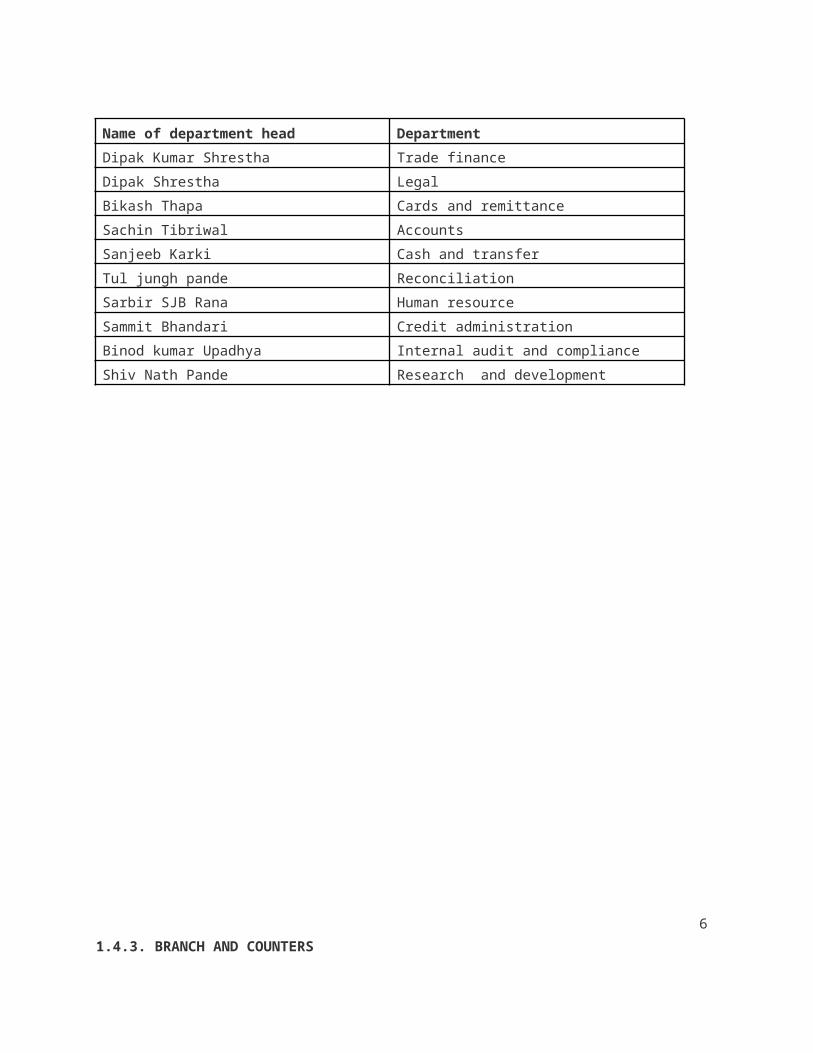

Name of department head DepartmentDipak Kumar Shrestha Trade financeDipak Shrestha LegalBikash Thapa Cards and remittanceSachin Tibriwal AccountsSanjeeb Karki Cash and transferTul jungh pande ReconciliationSarbir SJB Rana Human resourceSammit Bhandari Credit administrationBinod kumar Upadhya Internal audit and complianceShiv Nath Pande Research and development

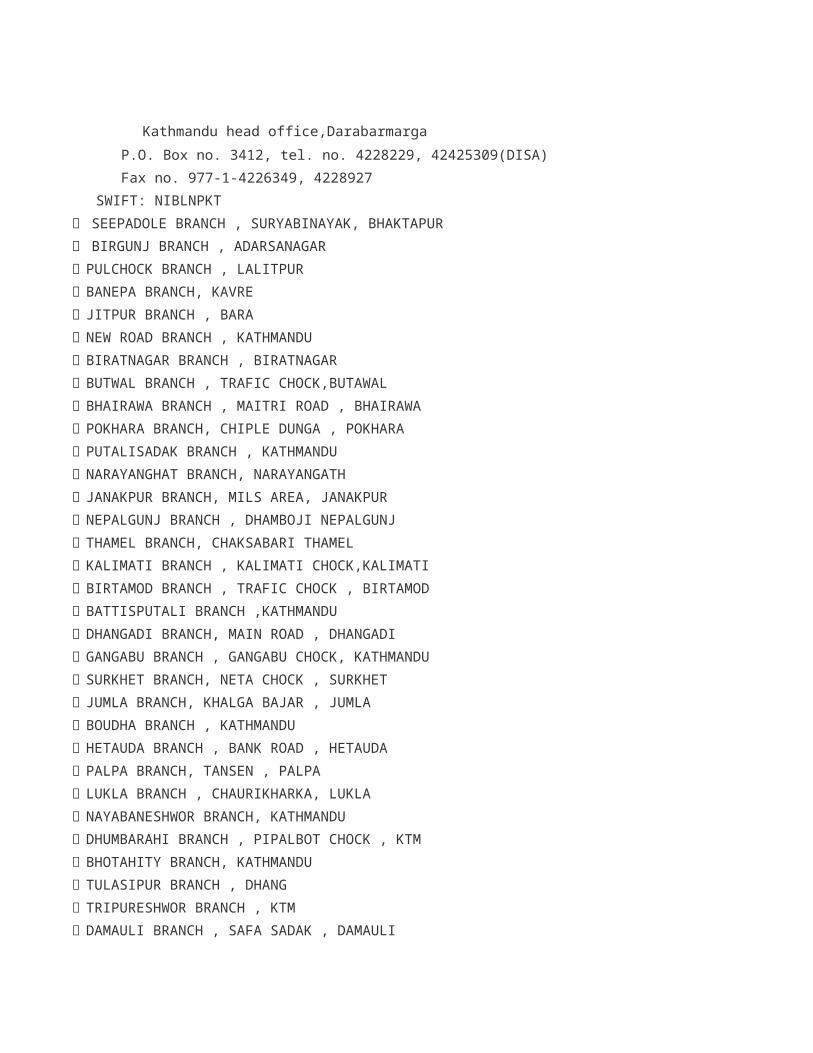

61.4.3. BRANCH AND COUNTERS

Kathmandu head office,Darabarmarga P.O. Box no. 3412, tel. no. 4228229, 42425309(DISA) Fax no. 977-1-4226349, 4228927SWIFT: NIBLNPKT

SEEPADOLE BRANCH , SURYABINAYAK, BHAKTAPUR BIRGUNJ BRANCH , ADARSANAGAR PULCHOCK BRANCH , LALITPUR BANEPA BRANCH, KAVRE JITPUR BRANCH , BARA NEW ROAD BRANCH , KATHMANDU BIRATNAGAR BRANCH , BIRATNAGAR BUTWAL BRANCH , TRAFIC CHOCK,BUTAWAL BHAIRAWA BRANCH , MAITRI ROAD , BHAIRAWA POKHARA BRANCH, CHIPLE DUNGA , POKHARA PUTALISADAK BRANCH , KATHMANDU NARAYANGHAT BRANCH, NARAYANGATH JANAKPUR BRANCH, MILS AREA, JANAKPUR NEPALGUNJ BRANCH , DHAMBOJI NEPALGUNJ THAMEL BRANCH, CHAKSABARI THAMEL KALIMATI BRANCH , KALIMATI CHOCK,KALIMATI BIRTAMOD BRANCH , TRAFIC CHOCK , BIRTAMOD BATTISPUTALI BRANCH ,KATHMANDU DHANGADI BRANCH, MAIN ROAD , DHANGADI GANGABU BRANCH , GANGABU CHOCK, KATHMANDU SURKHET BRANCH, NETA CHOCK , SURKHET JUMLA BRANCH, KHALGA BAJAR , JUMLA BOUDHA BRANCH , KATHMANDU HETAUDA BRANCH , BANK ROAD , HETAUDA PALPA BRANCH, TANSEN , PALPA LUKLA BRANCH , CHAURIKHARKA, LUKLA NAYABANESHWOR BRANCH, KATHMANDU DHUMBARAHI BRANCH , PIPALBOT CHOCK , KTM BHOTAHITY BRANCH, KATHMANDU TULASIPUR BRANCH , DHANG TRIPURESHWOR BRANCH , KTM DAMAULI BRANCH , SAFA SADAK , DAMAULI

KRISHNA NAGAR BRANCH, KAPILBASTU GHAIGHAT BRANCH, UDAYAPUR LAZIMPAT BRANCH , KTM PARSA BRANCH , CHITAWAN MAHARAJGUNJ BRANCH ,KTM LALBANDI BRANCH, LALBANI,SARLAHI LAGANKHEL BRANCH,LALITPUR

7

WALING BRANCH , SYANJA

1.4.4. Products and services:Some products and services of Nepal Investment Bank Ltd Are given below:

Deposit Saving deposit Current deposit Fixed deposit Call deposit Lending Documentary credits Guarantee Collections (agency functions) Credit card Safe deposit locker Fund transfer Remittance SWIFT member ATM Fast cash Withdrawal Pin change Enquiry

1.5. STRATEGIES AND FUTURE PLANS OF THE NEPAL INVESTMENT BANK LTD.

The Nepal investment Bank Ltd.’s mission is to be the “Bank of the first choice” to attain the goal to be the “Bank of the first choice”, bank is concerting into the service of its customers and social issues. So Nepal investment is the customer focus and goal oriented.

NIBL’s strategies and future plans: To develop a customer oriented service culture with special emphasis on

customer care and convenience To increase its market share by following a disciplined growth strategy. To leverage its technology platform and pen scalable system to achieve

cost effective operation, efficient MIS, improved delivery capability and high service standards.

To develop innovative products and service that attracts its targets customer and market segments

To continue to develop products and service that reduces its cost of funds.

To maintain a high quality assets portfolio to achieve strong and sustainable returns and to continuously build share holders value.

To explore new avenues for growth and profitability. 8

1.6. STATEMENT OF THE PROBLEMS: Liquidity is the status and part of the assets which can be used to meet the obligation. Liquidity can be viewed in term of liquidity stored in the balance sheet and in term of liquidity available through purchased fund. The degree of liquidity depends upon the relationship between cash assets plus those assets which can be quickly turned into cash and liability awaiting payments.

Bank needs to maintenance some seasonable level of liquidity to fulfill different commitments such as provide money to depositors when they demand for administrative expenses, for maintaining cash reserve ratio in the central bank etc. so, liquidity is defined as the bank’s capacity to pay cash in exchange of deposits. Liquidity is crucial in the business like banking. Because if the bank has the high liquidity it can no on a desired profit and if the bank has the shortfall of the liquidity

it can not satisfy its customers. Inadequate liquidity may lead to collapse of the bank while excess liquidity is determinant to bank’s profitability in order to remove demerits associated with maintaining inadequate and excess liquidity, bank should maintained and optimum level of liquidity. This possible only when bank’s liquidity needs is correctly predicted. Prediction covers inflows and outflows of liquidity. If prediction shows more outflows, bank should be prepared to cover the shortfall by borrowing or by liquidating assets. If inflow is greater thanoutflows, bank should plan where to invest so that income can be increase.Banks attach great importance short terms and long terms predictions. Prediction of liquidity need should be in the form of primary and secondary reserve so that bank generates income and at the same time does not compromise to liquidity. Banks got failure because of wrongly analyzedliquidity position and wrongly predicated liquidity requirement and management policy of liquidity. Thus to gain the trust of the customers and be success on the operation, the bank should maintain and forecast the liquidity need for the period and optimum level of liquidity based on the past liquidity position.

1.7. OBJECTIVES THE STUDY: The main objective of the study is to analyze the Nepal investment bank’s liquidity position. Based on the analyzed liquidity position, the study will suggest the liquidity need and its management for the current year. Other objectives can be listed below:

To check the liquidity position of the NIBL To analyze the financial performance To check the NIBL bank’s profitability To suggest the amount of the optimum level of liquidity To suggest the liquidity management policies To fulfill the partial requirement of T.U. (department of management) for

the degree of bachelor of business study.

9

1.8. SIGNIFICANCE OF THE DTUDY: This report is prepared to analyze the liquidity position of Nepal investment bank. This report comprises the date from 2005 to 2010. This would help the bank to observe the trend of the liquidity position hold in those periods. Besides that, this study also evaluates the role of short term obligation and the bank ability to pay the currently maturity obligation. Moreover, the study will check the profitability of the bank. This will help the bank to take the corrective actions if there are any errors on the past performance and the study aimsto recommend correcting the division if the standard has not been met.

1.9. LIMITATION OF THE STUDY This study is simply conducted for the partial fulfillmentof the requirement for the degree of the bachelor in business studies (BBS). And only the secondary data is used and analyzed which could not disclose the actual result. And being the first endeavor, the report can comprise some mistakes which may cause to misinterpretation of the results. The other limitation of the study is listed below:

i. Data contains mostly of the annuals reports of the bank through fiscal year2005/2006 to 2009/2010.

ii. Only five years observation covering from fiscal year 2005/2006 to 2009/2010 is analyzed.

iii. Analysis is based on the ratio and trend lines of the corresponding ratios only.

iv. For the forecast of the liquidity requirement, daily and monthly data is needed. But due to time and cost constraints, only the annual datais used for analysis.

v. Only the secondary data is used.vi. The study is only fulfill the requirement for the degree of

bachelor in business studies, which can not cover all the dimension of theall subjects matter and resource and time period is also limited.

1.10. SCOPE AND IMPORTANCE OF THE STUDY:

This study will be useable and valuable to the various parties, which can be mentioned as follow:

a) To the investorsb) To the creditorsc) To management of the bankd) To the customerse) To the other partiesf)

And this study will be equally useful to the other readers, students of related subjects and other people who are concern with bankingfield.

CHAPTER – TWO

Review of Literature

This chapter deals with the theoretical aspects of the topic of financial analysis of Nepal investment bank Ltd. in more detail and descriptive manner. For this study, journals, articles, and some research reports related with this topic have been reviewed. This study has to refer almost all books related with this topic published. Some of the prior reports by students of BBS regarding this topic have also been reviewed.

2.1. Conceptual framework: One of the sensitive factor or element in the bank is liquidity. Liquidity refers to the convertibility assets into cash. It means how fast the assets can be change into cash. There are many assets which are easily converted into cash by the bank. Such as cash in hand, cash at bank, cash at central bank, investment in government securities. But some assets are difficult to get converted into cash such as loan and fixed assets.

Liquidity is also defined as the position or capability of a bank to meet the current obligation of customers such as payment of cheque. Payment of demand drafts, disbursement of approved loan etc. Bank needs to maintain some reasonable level of liquidity to fulfill different commitments such as provide money to depositors when they demand for administrative expenses, for maintaining cash bank’s capacity to pay cash in exchange of deposits. Liquidity is crucial in the business like banking. Because if the bank has high liquidity, it can no earn a desire profit and if the bank has the shortfall of the liquidity it cannot satisfy its customers. Inadequate liquidity may lead to collapse of the banks while excess liquidity is detrimental to bank’s profitability. In order to remove demerits associated with maintaining inadequate and excessliquidity, banks should maintain an optimum level of liquidity. This

possible only when bank’s liquidity needs is correctly predicted. Prediction covers in present outflows of liquidity. If prediction shows more outflows, bank should be prepared to cover the shortfall by borrowingor by liquidating assets. If inflow greater than outflow, bank should planwhere to invest so that income can be increase. Banks attach great importance short term and long term predictions. Prediction of liquidity need should be in the firm of primary and secondary reserves so that bank generates income and at the same time does not compromise to liquidity.

2.1.1. Liquidity assets: the assets which can be converted into cash immediately with or without a nominal loss of value. Liquidity can be in the firm of treasury bills, investments in government securities, gold andsilvers, inventories and marketable securities etc.

2.1.2. Cash reserve Ratio (CRR): Central banks the world over make banks maintains the certain level of liquidity to total deposit liabilities in the form of the cash and bank balance. This ratio is known as the cash reserve ratio or primary reserve.

2.1.3. Statutory liquidity ratio (SLR): Central bank orders to the banks to maintain the certain level of liquidity to total deposit liabilities inthe form of the cash and bank 11balance and treasury bills and government securities and bonds. Such liquidity requirement is called the statutory liquidity ratio.

2.1.4. Importance of liquidity for the bank: The liquidity is important for the bank for the motives cited as follow: Transaction motive Speculative motive Precautionary motive

2.1.5. Need of liquidity for the bank: a) To meet the expenses for the bank’s administrative works b) To pay all sorts of deposit on demand c) To repay the dept d) To gain trust or faith

e) To provide the security to the bank

2.1.6. Demand for the liquidity: Withdrawal of customer deposit Acceptable loan request Repayment of non-deposit borrowing Payment of interest on deposit Payment of dividends Expansion and growth Miscellaneous liabilities

2.1.7. Supply of bank liquidity: Capital issue Retained earning Borrowings Bond issue Repayments of loans Other incomes

2.1.8. Criteria of the measuring the bank liquidity: Criteria of measuring of the bank liquidity denotes

- attributes required being bank liquidity- compliance test of liquidity requirement

In words criteria area bank liquidity refers to:i. What conditions the assets have to meet to be bank liquidity?ii. Whether CRR and SLR have been maintained as per instruction of

the central bank?

2.1.9. Liquidity to be maintained with the central bank: Nepal Rastra Bank, as the central bank of Nepal, had made it mandatory for commercial bankers to maintain liquidity as under: 12 Balance at Nepal Rastra bank – 7% current and saving deposit liabilities. 4.5% of fixed deposit liabilities. Cash in vault – 2 % of deposit liabilities

2.1.10. Penalty for non-compliance: Penalty will be levied for failing to maintain the adequate liquidity as above under any of the following conditions:

1) In the case of shortfall in maintenance of balance with Nepal Rastra bank but maintenance of cash at vault more than 2%, then on such shortfallamount.

2) In the case shortfall in maintenance of balance with Nepal Rastra bank but maintenance of cash at vault more than 2%, up to 1% excess cash of total deposit is added in the balance with NRB, than on such shortfall amount (after adding up to 1% excess)

3) In the case of shortfall in maintenance of cash in vault as well as shortfall in balance held with Nepal Rastra bank, than on total shortfall amount.

2.1.11. Applicable penalty rates:1. first time shortfall Equivalent to bank rate/highest

refinance (currently 5.5%)2. for second time shortfall Equivalent to 2 times of bank rate3.for third time shortfall and all subsequent shortfalls

Equivalent to 3 times of bank rate.

The penalty is imposed on the shortfall amount on weekly basis.

2.1.12. Composition:

a. Total deposit means current, saving and fixed deposit account as well as call money deposit and certificate of deposit. For the purpose, deposits held in convertible foreign currency, employees guarantee amount and margin account will not be included.

b. Fixed deposit means a deposit in local currency accepted under the condition to repay on completion so stipulated time period.

c. Current and saving deposit means all deposit accounts other than thefixed deposits.

d. Cash in vault shall include only the local currency and foreign currency (except clearing cheque etc.)

e. Balance held with Nepal rastra bank in ordinary account only will beeligible for liquidity calculation. Special accounts opened

with Nepal rastra bank for specific purpose and foreign currency designated accounts will not be included for the purpose.

f. For the purpose of liquidity examination, all branches of the bank shall constitute one unit.

13

2.1.13. Basis for liquidity requirement prediction:a. Maturity of deposits g. seasonal

need of liquidityb. Maturity of borrowings h capital

purchasesc. Maturity of placement i. central

banks requirementsd. Maturity of bill payment j market

situatione. Repayment of the debt. k bonus to the

staffsf. Letter of credit outstanding l investment

2.1.14. Review from related studies: Bank needs to maintain some reasonable amount of liquidity tofulfill different commitments. Such as provide money to depositors when they demand for administrative expenses, for maintaining cash reserve ratio in the central bank etc. so, liquidity is define bank’s capacity to pay cash in exchange of deposits. Liquidity needs of commercial banks are unique because in no other types of business there will be such large portion of deposits payable on demand. Inadequate liquidity does damage credits standing of other organization as well but a banks fails to pay

the deposits on demands, the bank loose the faith of the public. Bank may maintain the liquidity in the form of :

Cash and bank balance Placement money at short calls or short notice Investments in gov. securities and other securities convertible into

cash

International federation of accountants has recommended the measuring the liquidity of bank by:

Cash and liquid securities Interbank money deposit liabilities

Liquidity of the bank should be maintained according to standard; excel liquidity as well as lack of the liquidity indicates that a bank is serious financial problems. The implication of the financial problem results losing of deposits, which erodes its supply of cash and forces theinstitutions to dispose of its safer and more liquid assets. On the other hand, other banks that are strong in liquidity will be increasingly reluctant to lend the problem bank liquid funds at higher interest rates. Thus, we can say that it is optimism necessity of the bank to maintain a proper balance between high liquidity and low liquidity. The tools used for analysis are:

Cash and bank balance to total deposit ratio Current deposit to total deposit ratio Saving deposit to total deposit ratio Investment to total deposit ratio And fund fluctuation trend line

CHAPTER – THREE

Research Methodology

The method which is use in the research is called research methodology. How the data is collected and which source the research use for getting the data is under the research methodology. Research methodology covers the data analysis tools as well.

3.1. Research Design: A research design is the arrangement conditions, for the collectionand analysis of data in a manner that aims to combined relevance to the research purpose with economy in procedures. This study aims on the financial analysis of the Nepal investment bank Ltd. This study is mainly based on primary data and secondary data. The primary data, which are collected directly from the question answer, direct interview with customer and office staffs. Thesecondary data are collected from respective annual reports especially from the Nepalinvestment bank’s web sites and various other journals and from security bond Nepal (SUBO) and Nepal stock exchange (NEPSE).

3.2. Data collection techniques: I went to the main office of Nepal investment bank ltd. Darbarmarga, Kathmandu, and get the important information. I collected themain annual reports of this bank directly from the web site. And other various articles and journals from various publication and some others from the SEBO, NEPSE and previous field reports are also taken in to accounts.

3.3 DATA ANALYSIS TOOLS: Data analysis tools means which tools the research used for presentand analyzed the data. The main tools of analysis are mathematical and statistical tools. In this reports statistical and financial ratio tools

is used for data analysis. Mean and correlation is calculated for analysisthe data as statistical tools.

3.3.1. Ratios: An arithmetical relationship between two figures is called ratio.It is the most useful and analytical tools to evaluate in respect to one variable over another. Here, for our purpose, only the liquidity related ratios are calculated.

1) Liquidity ratio2) Cash and bank balance to current deposit ratio3) Saving deposit to total deposit ratio4) Cash and bank to total deposit ratio5) Fixed deposit to total deposit ratio6) Cash and bank balance to total deposit ratio(excluding fixed deposit)7) NRB balance to total deposit(excluding fixed deposit)8) NRB balance to fixed deposit ratio9) Deposit to investment ratio

15

3.3.2. Statistical tools: Mean Standard deviation Coefficient of variance Correlation of coefficient Trend analysis

CHAPTER – FOUR

Data Presentation and Analysis:

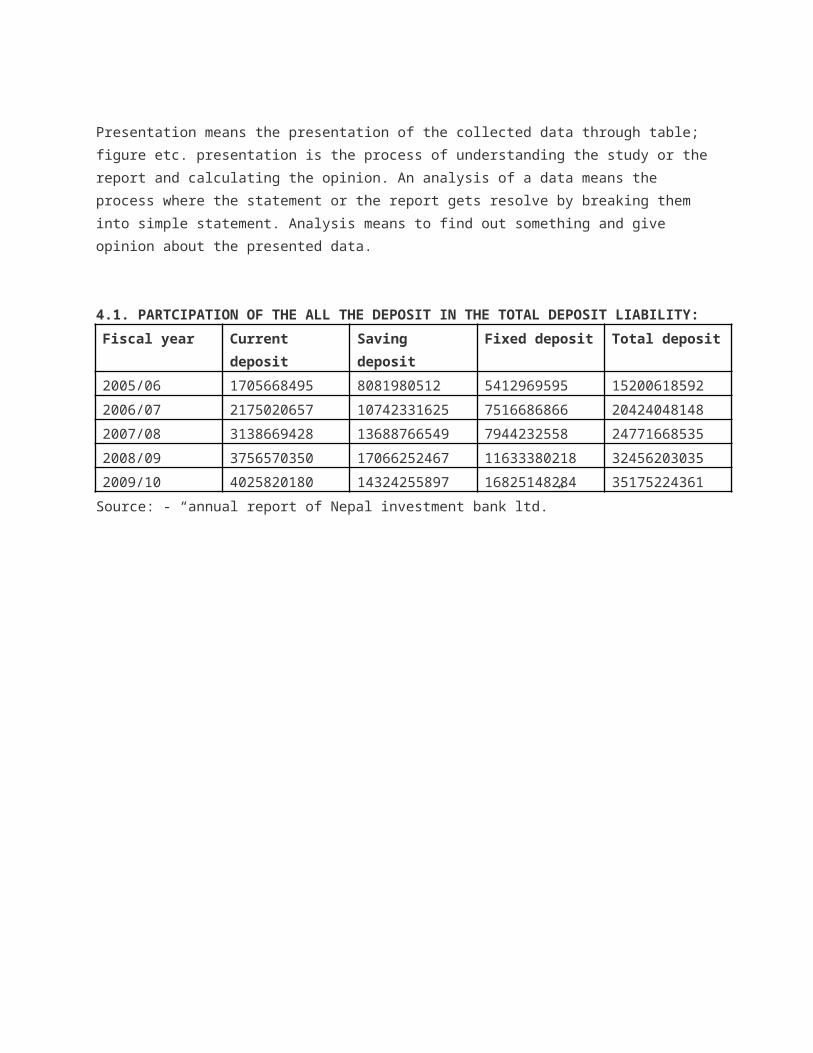

Presentation means the presentation of the collected data through table; figure etc. presentation is the process of understanding the study or the report and calculating the opinion. An analysis of a data means the process where the statement or the report gets resolve by breaking them into simple statement. Analysis means to find out something and give opinion about the presented data.

4.1. PARTCIPATION OF THE ALL THE DEPOSIT IN THE TOTAL DEPOSIT LIABILITY:Fiscal year Current

depositSaving deposit

Fixed deposit Total deposit

2005/06 1705668495 8081980512 5412969595 152006185922006/07 2175020657 10742331625 7516686866 204240481482007/08 3138669428 13688766549 7944232558 247716685352008/09 3756570350 17066252467 11633380218 324562030352009/10 4025820180 14324255897 16825148284 35175224361Source: - “annual report of Nepal investment bank ltd.”

17In the above table and chart, we see that, in fiscal year 2005/06, the current deposit account occupied 11%, saving deposit account 53%, fixed deposit account 37%.in fiscal year 2006/7 the current deposit account occupied 10%, saving deposit account53%, fixed deposit account 36% occupied. In fiscal year 2007/08 the saving deposit account occupied 13%, saving deposit account 53%, fixed deposit account 37% occupied. In fiscal year 2008/09 the current deposit account occupied 13% saving deposit account55%, fixed deposit account32% occupied. In fiscal year 2009/10 the current deposit account occupied 11%, saving deposit account42%, fixed deposit account occupied 48%.

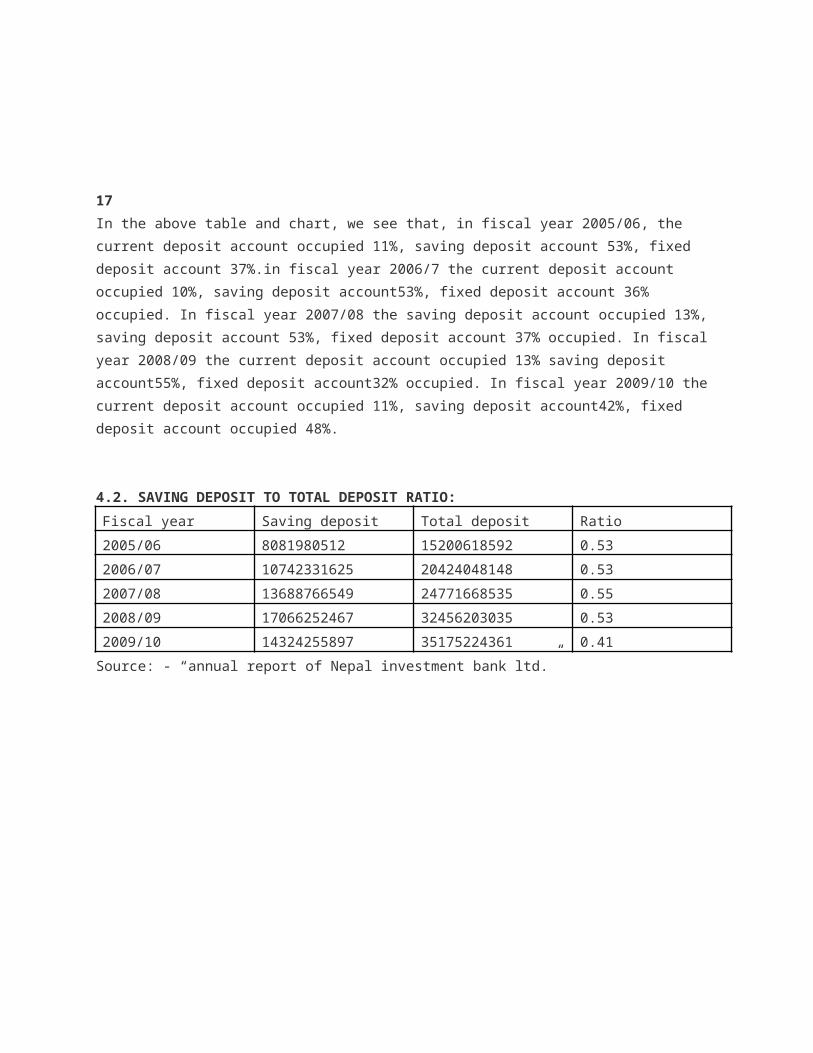

4.2. SAVING DEPOSIT TO TOTAL DEPOSIT RATIO:Fiscal year Saving deposit Total deposit Ratio2005/06 8081980512 15200618592 0.532006/07 10742331625 20424048148 0.532007/08 13688766549 24771668535 0.552008/09 17066252467 32456203035 0.532009/10 14324255897 35175224361 0.41Source: - “annual report of Nepal investment bank ltd.”

Fiscalyear

From the above table and trend line chart, the ratio is fluctuating state.In the fiscal year 2005/06, the bank has the saving deposit of 0.53 times of total deposit liability. And 0.53, 0.55, 0.53, 0.41 times of total deposit liability in fiscal year 2006/07, 2007/08, 2008/09, 2009/10 respectively. 18

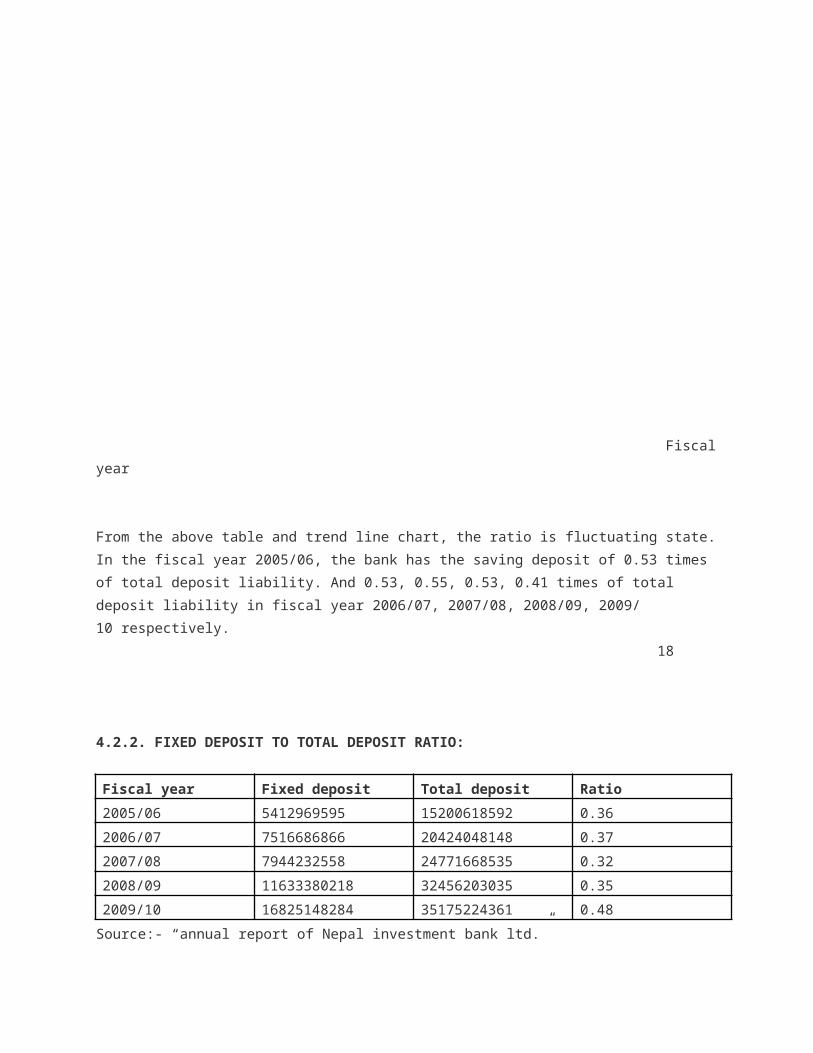

4.2.2. FIXED DEPOSIT TO TOTAL DEPOSIT RATIO: Fiscal year Fixed deposit Total deposit Ratio2005/06 5412969595 15200618592 0.362006/07 7516686866 20424048148 0.372007/08 7944232558 24771668535 0.322008/09 11633380218 32456203035 0.352009/10 16825148284 35175224361 0.48Source:- “annual report of Nepal investment bank ltd.”

Fiscal year

From the above table and trend line chart, the ratio is fluctuating in increasing and decreasing trend. The highest ratio is 0.48 times in year 2009/10 and lowest ratio is 0.32 times in fiscal year 2007/08. And 0.36 times, 0.37 times and 0.35 times in year 2005/06, 2006/07, and 2008/09 respectively.

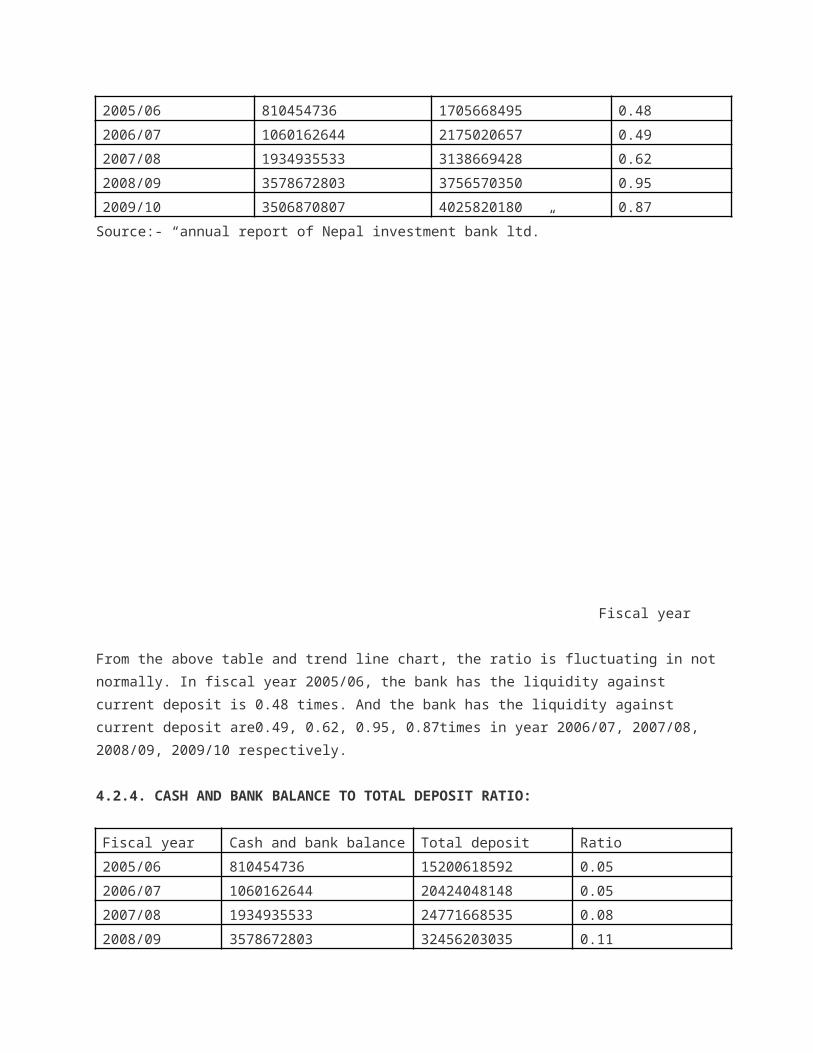

194.2.3 CASH AND BANK BALANCE TO CURRENT DEPOSIT RATIO:

Fiscal year Cash and bank balance

Current deposit Ratio

2005/06 810454736 1705668495 0.482006/07 1060162644 2175020657 0.492007/08 1934935533 3138669428 0.622008/09 3578672803 3756570350 0.952009/10 3506870807 4025820180 0.87Source:- “annual report of Nepal investment bank ltd.”

Fiscal year

From the above table and trend line chart, the ratio is fluctuating in notnormally. In fiscal year 2005/06, the bank has the liquidity against current deposit is 0.48 times. And the bank has the liquidity against current deposit are0.49, 0.62, 0.95, 0.87times in year 2006/07, 2007/08, 2008/09, 2009/10 respectively.

4.2.4. CASH AND BANK BALANCE TO TOTAL DEPOSIT RATIO:

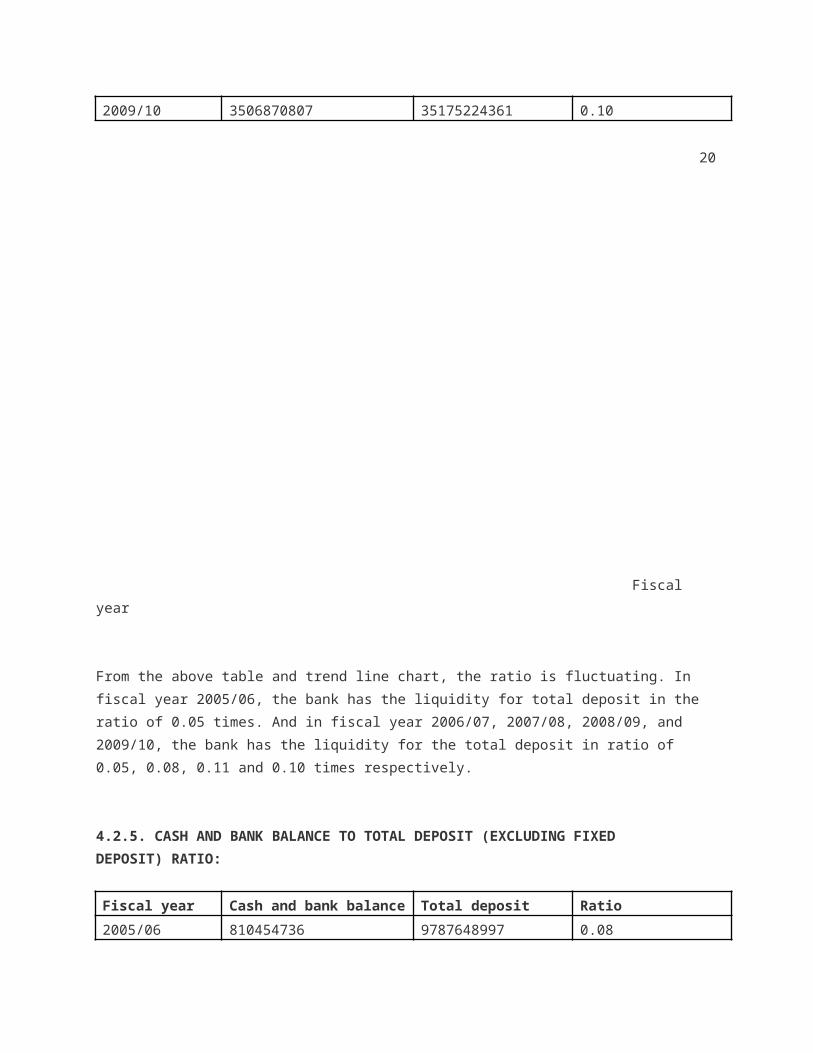

Fiscal year Cash and bank balance Total deposit Ratio2005/06 810454736 15200618592 0.052006/07 1060162644 20424048148 0.052007/08 1934935533 24771668535 0.082008/09 3578672803 32456203035 0.11

2009/10 3506870807 35175224361 0.10 20

Fiscal year

From the above table and trend line chart, the ratio is fluctuating. In fiscal year 2005/06, the bank has the liquidity for total deposit in the ratio of 0.05 times. And in fiscal year 2006/07, 2007/08, 2008/09, and 2009/10, the bank has the liquidity for the total deposit in ratio of 0.05, 0.08, 0.11 and 0.10 times respectively.

4.2.5. CASH AND BANK BALANCE TO TOTAL DEPOSIT (EXCLUDING FIXEDDEPOSIT) RATIO:

Fiscal year Cash and bank balance Total deposit Ratio2005/06 810454736 9787648997 0.08

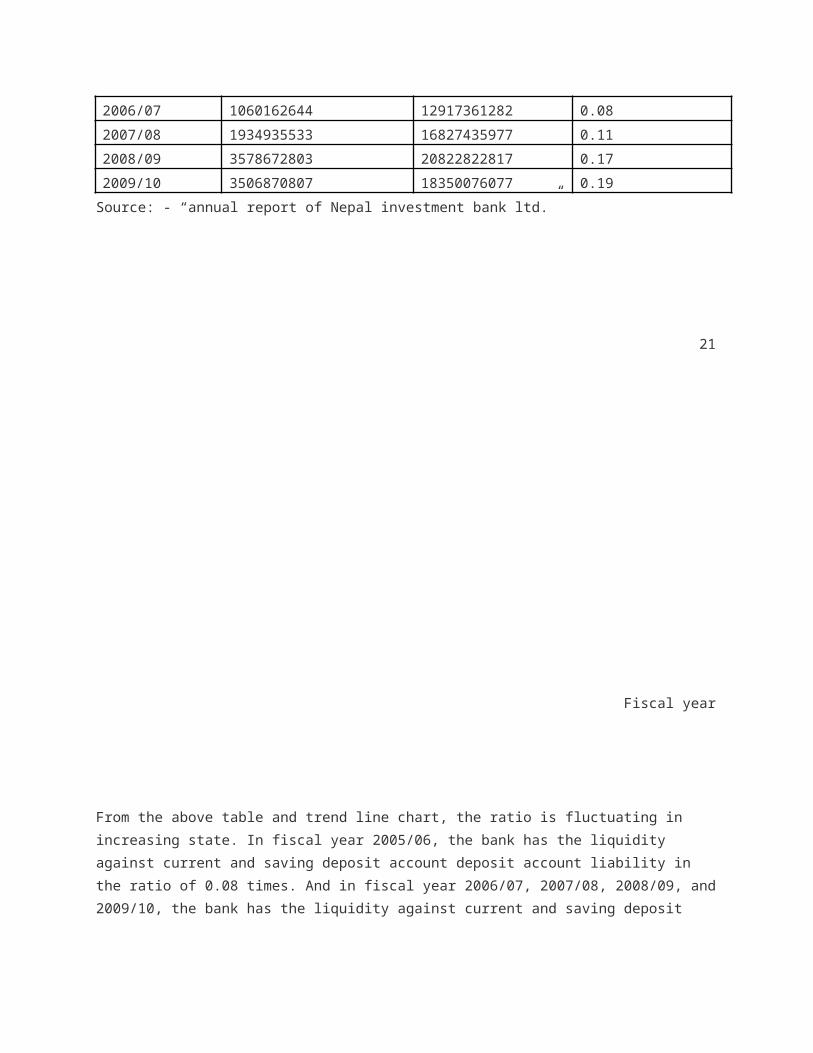

2006/07 1060162644 12917361282 0.082007/08 1934935533 16827435977 0.112008/09 3578672803 20822822817 0.172009/10 3506870807 18350076077 0.19Source: - “annual report of Nepal investment bank ltd.”

21

Fiscal year

From the above table and trend line chart, the ratio is fluctuating in increasing state. In fiscal year 2005/06, the bank has the liquidity against current and saving deposit account deposit account liability in the ratio of 0.08 times. And in fiscal year 2006/07, 2007/08, 2008/09, and2009/10, the bank has the liquidity against current and saving deposit

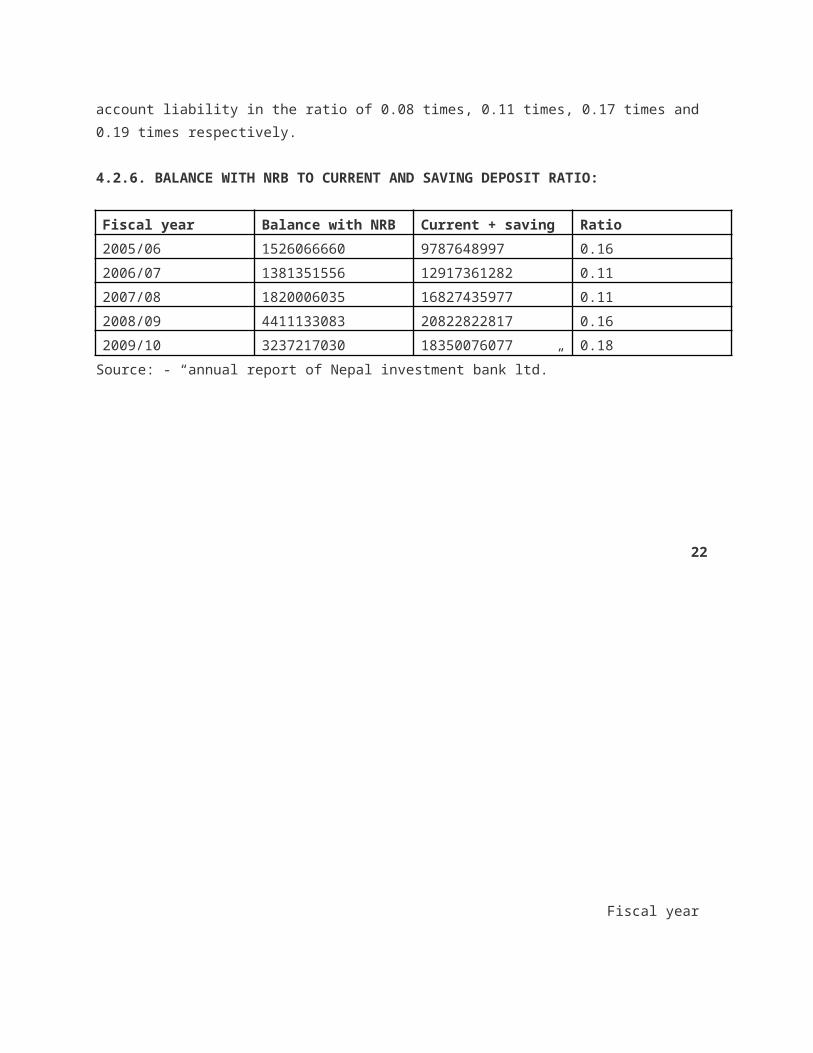

account liability in the ratio of 0.08 times, 0.11 times, 0.17 times and 0.19 times respectively.

4.2.6. BALANCE WITH NRB TO CURRENT AND SAVING DEPOSIT RATIO:

Fiscal year Balance with NRB Current + saving Ratio2005/06 1526066660 9787648997 0.162006/07 1381351556 12917361282 0.112007/08 1820006035 16827435977 0.112008/09 4411133083 20822822817 0.162009/10 3237217030 18350076077 0.18Source: - “annual report of Nepal investment bank ltd.”

22

Fiscal year

From the above table and trend line chart, the ratio has been maintained in fiscal year 2005/06 by 0.16 times. And the bank has been maintained itsratio in fiscal year 2006/07, 2007/08, 2008/09, 2009/10 by 0.11 times, 0.11 times, 0.16 times and 0.18 times respectively.

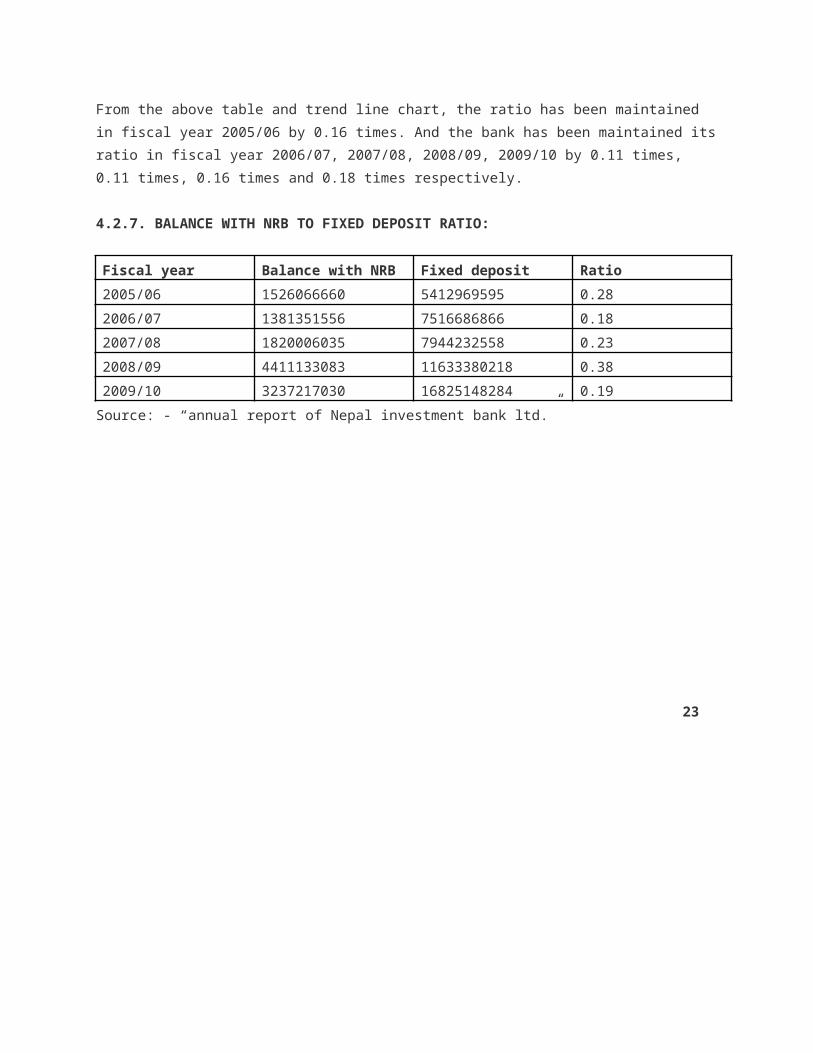

4.2.7. BALANCE WITH NRB TO FIXED DEPOSIT RATIO:

Fiscal year Balance with NRB Fixed deposit Ratio2005/06 1526066660 5412969595 0.282006/07 1381351556 7516686866 0.182007/08 1820006035 7944232558 0.232008/09 4411133083 11633380218 0.382009/10 3237217030 16825148284 0.19Source: - “annual report of Nepal investment bank ltd.”

23

Fiscal year

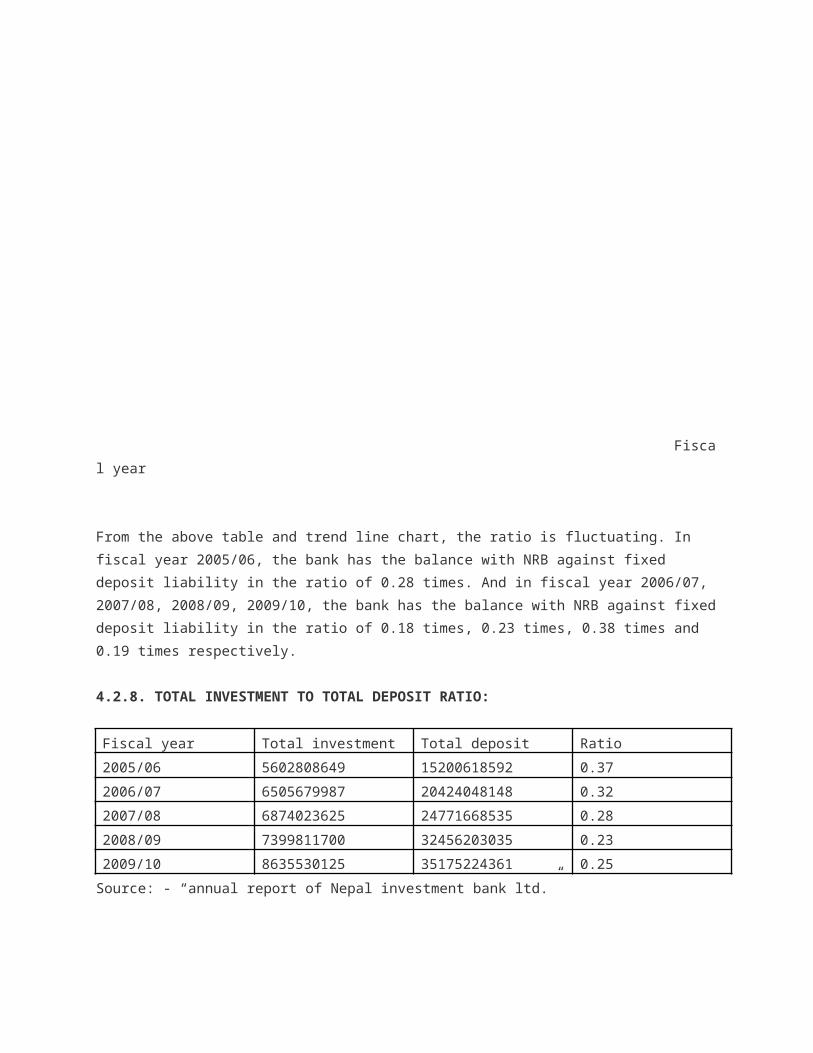

From the above table and trend line chart, the ratio is fluctuating. In fiscal year 2005/06, the bank has the balance with NRB against fixed deposit liability in the ratio of 0.28 times. And in fiscal year 2006/07, 2007/08, 2008/09, 2009/10, the bank has the balance with NRB against fixeddeposit liability in the ratio of 0.18 times, 0.23 times, 0.38 times and 0.19 times respectively.

4.2.8. TOTAL INVESTMENT TO TOTAL DEPOSIT RATIO:

Fiscal year Total investment Total deposit Ratio2005/06 5602808649 15200618592 0.372006/07 6505679987 20424048148 0.322007/08 6874023625 24771668535 0.282008/09 7399811700 32456203035 0.232009/10 8635530125 35175224361 0.25Source: - “annual report of Nepal investment bank ltd.”

24

Fiscal year

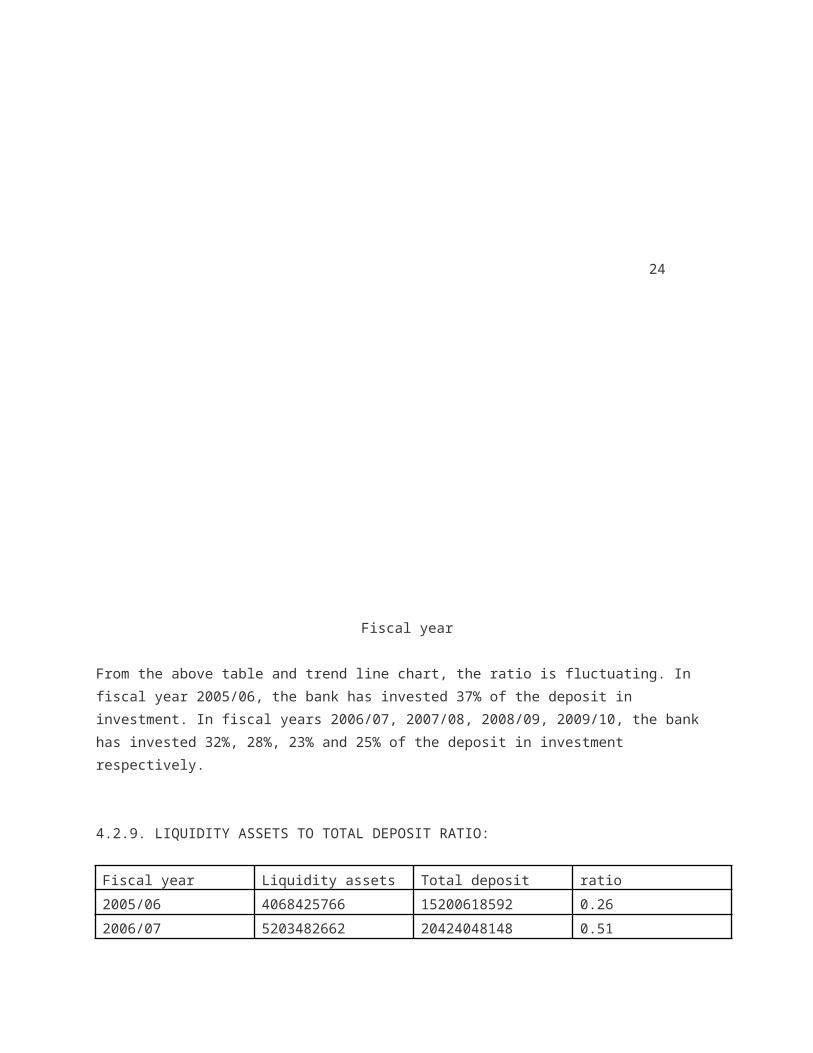

From the above table and trend line chart, the ratio is fluctuating. In fiscal year 2005/06, the bank has invested 37% of the deposit in investment. In fiscal years 2006/07, 2007/08, 2008/09, 2009/10, the bank has invested 32%, 28%, 23% and 25% of the deposit in investment respectively.

4.2.9. LIQUIDITY ASSETS TO TOTAL DEPOSIT RATIO:

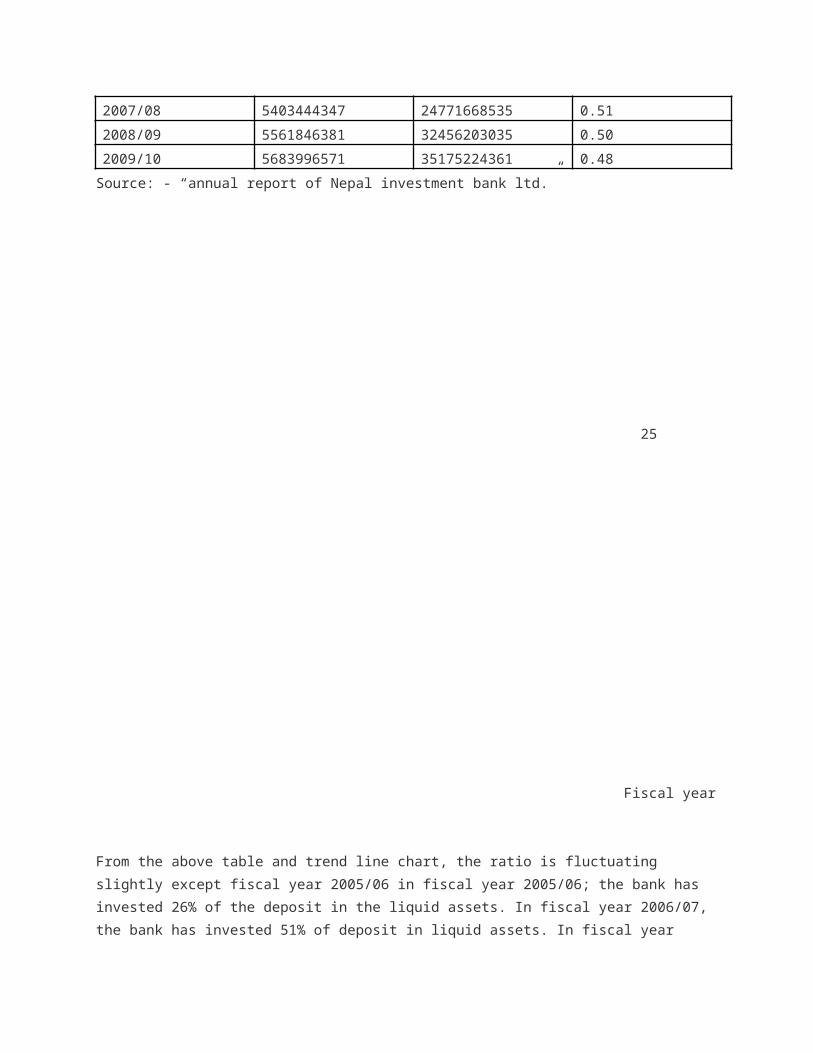

Fiscal year Liquidity assets Total deposit ratio2005/06 4068425766 15200618592 0.262006/07 5203482662 20424048148 0.51

2007/08 5403444347 24771668535 0.512008/09 5561846381 32456203035 0.502009/10 5683996571 35175224361 0.48Source: - “annual report of Nepal investment bank ltd.”

25

Fiscal year

From the above table and trend line chart, the ratio is fluctuating slightly except fiscal year 2005/06 in fiscal year 2005/06; the bank has invested 26% of the deposit in the liquid assets. In fiscal year 2006/07, the bank has invested 51% of deposit in liquid assets. In fiscal year

2007/08, 2008/09 and 2009/10, the bank has invested 51%, 50%, and 48% of the deposit in the liquid assets respectively.

CHAPTER – FIVE

Summary, Conclusion and Recommendation

5.1. SUMMARY

Nepal is one of the least developed countries of the world. For most of the developing process, it is financially depending upon the foreign countries. It is economically too weak. Thus, the economic condition of the people is weak. In Nepal 85% of the people are depended upon agricultural sector which is unable to provide full employment to thepeople. Nepal government has to activate people in the nation’s development through overall industrialization of nation. For this purpose,development of sound banking system is essential.

In neplese banking sector, commercial banks including ventures banks are operating at present. In the absences of modern bankingany country cannot develop the economic activity. Therefore, it is essential to find out whether or not the banks are serving an important contribution to develop sectors of economy. Liquidity is said to be general business of fund, which shows the bank ability to meet cash requirement. In this record, this study has been based upon the objective to evaluate the liquidity position of Nepal investment bank ltd.

5.2. CONCLUSION

a) The saving deposit account is nearly constant trend. The highest ratio is 0.55 times in fiscal year 2007/08 and the lowest ratio is 0.41 times infiscal year 2009/10. But the ratio is not satisfactory due to the last year ratio was decline.

b) Fixed deposit is fluctuated. The lowest ratio is 0.32 times and highestratio is 0.48 times. It is decrease up to fiscal year 2007/08 and grows upthen. And it is 0.48 times on 2009/10. It is satisfactory. Bank made good ratio after 2007/08.

c) From the cash and bank balance to current deposit liability is fluctuating. The ratio is moving around between 0.48 times to 0.95 times. It is satisfactory.

d) Cash and bank balance to total deposit ratio is fluctuating. But the ratio is somehow satisfactory even though the ratio is higher than the central banks prescription. The ratio is moving around the between 0.05 times to 0.11 times.

e) Cash and bank balance to total deposit (excluding fixed deposit) ratio is fluctuating in increasing state. The ratio is satisfactory. It is moving around between 0.08 times to 0.19 times.

f) The ratio of balance with the NRB to current and saving deposit has been fluctuating. The ratio is declined in year 2006/07 and constant in 2007/08 and then it is grow up. so, the ratio is satisfactory.

g) The balance with the NRB to fixed deposit ratio is fluctuating. It is moving around between 0.18 times to 0.39 times.

h) The investment to total deposit ratio is fluctuating adversely. Since the ratio is fluctuating the bank has unsatisfactory result. However the investment from source of deposit is 27higher. It will give a higher return without risk only if the ratio is stabilized.

i) The liquid assets to total deposit ratio is fluctuating slightly except fiscal year 2005/06. However the ratio is higher and somehow may beconsidered satisfactory.

5.3 RECOMMENDATION

a) The overall results are satisfactory. But in some case the Nepal investment Bank should take certain steps to improve the bank current financial condition. Therefore some recommendations are being put forward for its improvement along with its development of the country.

b) The proportion of the saving deposit account is high in total deposit liability. So, it is recommended that the bank should utilize the amount collected from the saving deposit account carefully. It should be investedin the higher yielding areas.

c) The cash and bank balance in the Nepal investment bank is satisfactory.It is higher a bit though. Bank should analyze the opportunities for shortterm investment.

d) Balance with NRB to current plus saving deposit should be maintained atthe below than 0.11 times.

e) Investment to deposit ratio is fluctuating adversely. It may harm the operation of the bank. So, the investment from the deposit source should

always be aware of liquidity need and keep in mind to maintain the optimumliquidity.

f) Bank should not spend too much in the fixed assets because it yields only a nominal portion, almost no yield.

28 BIBLIOGRAPHY

Bajracharya, B.C. (2053), Business statistics & mathematics, M.K. publishers and Wistributors.

Brigham, Weston, Essentials of Managerial Finance”, Eleventh Edition, University Publishers, USA.

Kothari, C.R., Research Methodology”, Mc. Grow Hill Company, second Edition.

Shekhar and Shekhar “Banking Theory & Practice”, Eighteenth Revised Edition, 1996.

Nepal Rastra Bank, Banking and Financial Statistics,

Nepal investment Bank Ltd., “annual report 2006-2010