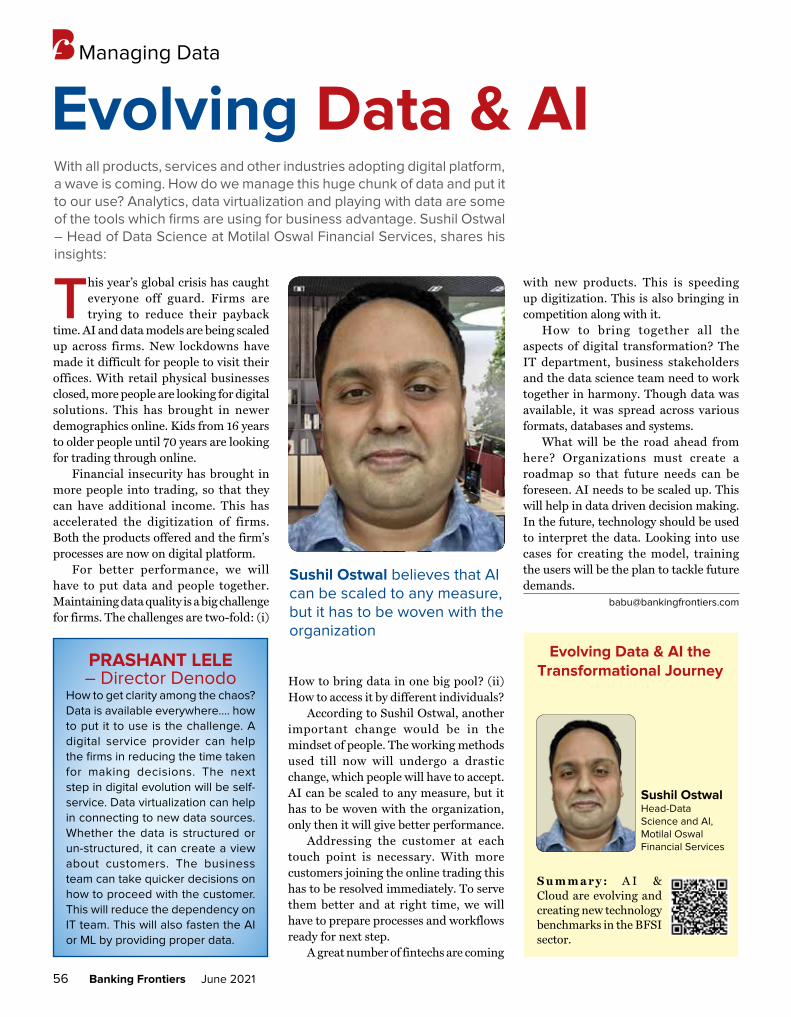

Embed Size (px)

Citation preview

Vol. 20 No. 2 June 2021 `75

Pages 68

www.bankingfrontiers.comwww.bankingfrontiers.live

Health insurance pg 6

Digital Transformation pg 8

India Infoline pg 19

Mandeshi Mahila Bank pg 24

Th

eRisk Sentinels

Call for Nomination

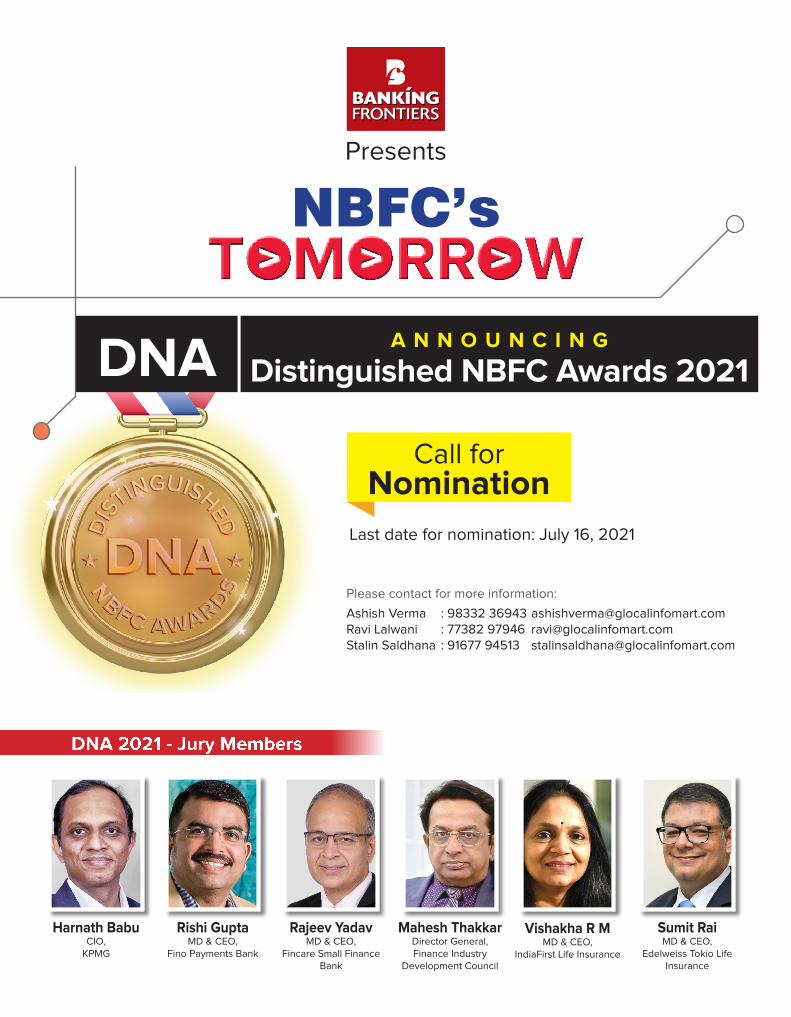

Rajeev YadavMD & CEO,

Fincare Small Finance Bank

Vishakha R MMD & CEO,

IndiaFirst Life Insurance

Rishi GuptaMD & CEO,

Fino Payments Bank

Mahesh ThakkarDirector General, Finance Industry

Development Council

Sumit RaiMD & CEO,

Edelweiss Tokio Life Insurance

Harnath BabuCIO,

KPMG

DNA 2021 - Jury Members

Please contact for more information:

Ashish Verma : 98332 36943 [email protected] Ravi Lalwani : 77382 97946 [email protected] Stalin Saldhana : 91677 94513 [email protected]

A N N O U N C I N G

Distinguished NBFC Awards 2021

Last date for nomination: July 16, 2021

DNA

Presents

NBFC’s

Banking Frontiers June 2021 3

June 2021 - Vol. 20 No. 2

Group Publisher : Babu Nair

Group Editor : Manoj Agrawal

Editor : N. Mohan

Editorial Mehul Dani, Ravi Lalwani, V. Raghuraman

Research Editors V. Babu, Ratnakar Deole, W.A. Wijewardena, Sanchit Gogia, K.C. Shashidhar, Dr L.S. Subramanian, Ajay Kumar

Advisor-Alliances Ateeq Siddique

Marketing Kailash Purohit, Dhara Thobani, Rohit Kahar, Aditya Arya

Events & Operations Shirish Joshi, Stalin Saldhana, Pramod Jadhav, Ashish Verma, Wilhelm Singh, Sneha Agrawal, Ramesh Vishwakarma, Sushant Tulapurkar

Design Somnath Roy Choudhury, Sudarshan Herle

Published By Glocal Strategies & Services D-312, Twin Arcade, Military Road, Marol, Andheri (E), Mumbai 400059, India. Tel: +91-22-29250166 / 29255569 Fax: +91-22-29207563

Printed & Published by Babu Nair on behalf of Glocal Strategies & Services and Printed at Indigo Presss (India) Pvt Ltd., Plot No. 1C/716, Off Dadoji Konddeo Cross Road, Between Sussex and Retiwala Indl.Estate, Byculla (E), Mumbai 400027.

Editor: Manoj Agrawal (Responsible for selection of news under PRB Act)

There is lot of buzz these days about neobanks. Banking industry analysts say they may if not one day replace traditional banks, become what Amazon is to the supermarkets. They have proved that

technology can indeed make big difference and bring in convenience factor, especially for the customer. One of their offerings is that customers will have complete control of their finances using apps. This is not just a sop for the customers but a means for the neobanks to lower their overheads and thereby allowing them to waive fees or service charges that traditional banks usually levy on their customers.

In markets where neobanks have firmly established themselves, like in the US, the customer service they offer is far superior to those given by traditional banks. And for them, digital is all-pervading. For example, their high- profile chat systems ensure that there is no way a resolution will not be found. In comparison, the apps offered by the highly technology driven banks are often stuck by poor functionality and security concerns.

Studies have indicated that even when neobanks own less than 5% of the retail market, they appeal up to 35% of new customers per year. Their market size was valued at $34.77 billion in 2020 and it is expected to expand at a CAGR of 47.7% from 2021 to 2028.

It is not a wishful thinking that neobanks will, if not render traditional banks redundant, come to stay and offer competition, thereby pushing the latter to evolve, modernize and become customer-centric. They will also be pushed into taking up technology for what it is and not just because others too are using it.

Neobanks have facilitated the creation of a new tech course that has completely changed the services, products and speed of delivery. And this makes them highly impactful, transparent, low cost and easy to access. They are assuming the role of digital challengers to the traditional financial services institutions, proving to be the real people-oriented institutions to the people who need them.

Editor’s BlogN. MohanMobile : 9322895820Email : [email protected]

Neobanks a boon for customers

N E W S Regulator

4 Banking Frontiers June 2021

Project Jura to experiment on wCBDC The Bank for International Settlements’ (BIS) Innovation Hub, Swiss National Bank and Bank of France will be working with a private sector consortium on an experiment using wholesale central bank digital currency (wCBDC) for cross-border settlement. BIS said the project, called Project Jura, will look into the potential benefits and challenges of

wCBDC in settling cross-border payments and digital financial instruments. It will involve 2 wCBDCs and a French digital financial instrument on a distributed ledger technology platform. The private sector consortium is led by Accenture and includes Credit Suisse, Natixis, R3, SIX Digital Exchange and UBS. The project is an expansion on central bank experimentation investigating the effectiveness of wCBDC for cross-border settlement. Several central banks are exploring the scope of launching CBDCs as a virtual form of a country’s fiat currency.

HKMA to set up fintech groupThe Hong Kong Monetary Authority (HKMA) is setting up a new Fintech Cross-Agency Coordination Group to formulate supportive policies for the local fintech ecosystem. This is part of the central bank’s Fintech 2025 strategy plan. The project involves local commercial banks, blockchain-based data sharing, talent supply and the central bank’s own work in exploring the outer boundaries of digital currency creation. The regulator is proposing to start study on a possible retail e-HK$ to understand its use cases, benefits, and related risks. It is also intending to roll-out a Tech Baseline Assessment to take stock of banks’ current and planned adoption of fintech in the coming years, to identify fintech business areas or specific technology types which may be underdeveloped, and would benefit from HKMA support.

Malaysia regulator sets up new funding facilityBank Negara Malaysia has established a 1-billion-ringgit financing facility, called the High-Tech Facility - National Investment Aspirations (HTF-NIA) to support local high-tech and innovation-driven small and medium-sized enterprises impacted by the pandemic. Eligible companies can receive up to 1 million ringgit as working capital and up to 5 million ringgit for capital expenditure. HTF-NIA is available until 31 December 2021, or until the funding has been fully utilized (whichever comes first). SMEs that are not eligible for the HTF-NIA can apply for other financing facilities from BNM, such as the SME Automation and Digitalization Facility (ADF). Under this scheme, businesses can receive up to 3 million ringgit for the purchase of equipment and software that accelerates the automation and digitalization of business operations.

BIS to open innovation hub in LondonThe Bank of International Settlements (BIS) has opened a London innovation hub in collaboration with the Bank of England. This is the fourth innovation center that the BIS has launched in the past 2 years, having already established innovation partnerships with the Hong Kong Monetary Authority, the Monetary Authority of Singapore and the Swiss National Bank. It now plans to open such hubs in Toronto with the Bank of Canada, with the European Central Bank and the Eurosystem in Frankfurt and Paris, and with 4 central banks in the Nordic region. It has also entered into a memorandum of understanding with the US Federal Reserve in this regard.

Saudi women can operate children’s bank accounts

Ravi Menon gets 2-year term at MAS

Singapore President Halimah Yacob has re-appointed Ravi Menon as the Managing Director of the Monetary Authority of Singapore for a further period of 2 years. He will now have his tenure until May 2023. Menon has also been reappointed to the MAS’s board for the same length of time. The central bank said in a statement it has appointed 2 new members and reappointed 5 existing members to its board. Menon has seen his global profile rise since he took the job in 2011. Under his leadership, MAS has adopted a multi-pronged strategy to build what is now regarded by many as one of the most vibrant fintech ecosystems in the world. The 2 new members of the board are Lawrence Wong, Minister for Finance, as deputy chairman, and Deborah Ong, a retired partner at PricewaterhouseCoopers. They will have a term of 3 years. Tharman Shanmugaratnam, Senior Minister and Coordinating Minister for Social Policies, has been re-appointed as Chairman until 31 May 2024.

The Saudi Central Bank (SAMA) said it will allow mothers to open bank accounts on behalf of their children, so long as they are minors. The regulator said it is keen to contribute to empowering maternal clients to manage their children’s affairs. Children’s account will be in the name of the minor but a subsidiary of the mother’s account. Saudi Arabia was the top reformer and improver among 190 economies in the World Bank’s Women, Business and the Law 2021 report, getting a score of 80 out of 100, compared with last year’s 70.6.

Banking Frontiers June 2021 5

Sri Lanka

Covid Maneuver: Banks & Regulator RespondDr W.A. Wijewardena, former deputy governor of the Central Bank of Sri Lanka, shares interesting insights on measures taken by Sri Lankan banks to stay afloat in the aftermath of the pandemic:

Babu Nair: How has the Sri Lankan

banking sector been able to be resilient

in the pandemic scenario?

W.A. Wijewardena: The Sri Lankan banking sector had taken the technological path since some time. The pandemic came as a shock as face-to-face transactions took a hit. The banks could not render services in the usual way. Some leading banks moved to the digital platforms more easily than others. Some banks introduced banking via vehicles. This allowed the banks to give cash to their customers. This way the customers did not face liquidity problem and could buy essential goods.

When it came to other banking services like account opening, the systems were already in place. An automated clearing house has been introduced by the Sri Lanka National Payments Platform, called LankaPay. Through LankaPay, customers could log in to their respective bank accounts and make payments to government departments. This way, with just a click of a button anyone could pay their bills, income tax, etc.

The central bank introduced QR codes for use by retail shops. The customers could make payments just by scanning the QR codes. The Sri Lankan banking system will not have any problems even if the lockdown is to be extended.

Have the changes in banking methods

affected the business of banks? The government of Sri Lanka

is trying to stimulate the economy by giving lower interest rates. The lending rates have been brought down considerably. However, the government is supporting the banks fully. Several taxes like VAT, nation-building tax etc have been eliminated for the current financial year. The negative impact of the reduction in interest rates has been offset by the removal of expenses. Hence, the banks’ profits remain the same. The

banks will have to provide for upcoming businesses. They will also have to seed the capital for new startups and invest in newer technology to ease the banking system.

Have there been any changes in the

non-performing assets? NPAs have gone up as customers have

not been able to repay.

Has the government given a moratorium

on repayment of loans?

The Central Bank had announced a moratorium of 6 months which was further extended by 3 months.

The phygital system has worked so far.

What is the road ahead for the banks?

Sri Lankan banks are taking many steps. The important ones are:1. The use of APIs is coming up. Data

collected through APIs will be used to develop internal banking products.

The sharing of data between the banks is bringing transparency in the banking sector.

2. The Central Bank’s initiative to introduce blockchain technology for customer services is also being implemented.

3. Cryptocurrency is being promoted by the Central Bank. The aim is to reduce physical currency by replacing it with digital currency.

How is the banking industry going to

take business to next level?

The new normal is setting in. The banks will have to train their staff for the new technologies. Most of the banks are going for AI technology for processes. The law does not allow the banker to share the data unless they have the consent of the customer.

Revolutionising workplaces

Summary: When enterprises have adopted some solution or the other to optimize productivity during the pandemic times, how can they have better systems and processes?

Prajit NairDirector, Sales, VMware

W.A. Wijewardena highlights an initiative by Central Bank of Sri Lanka to introduce QR codes for use by retail shops

Health Insurance

6 Banking Frontiers June 2021

Data drives Health & Treatment AnalyticsUdayan Joshi, President - Claims & Personal Lines Underwriting, Liberty General Insurance and Dr Sudha Reddy, Head - Health and Travel, Digit Insurance, speaks about issues relating to data for the health insurance sector:

Ravi Lalwani: What are the new types of

data that health insurers are seeking?

Udayan Joshi: A revolution has been sweeping the insurance industry for a few years now, to improve the management and utilization of data. Data is critical for designing new products, offering better service, improving customer experience and eliminating frauds. An established new trend is wearable technology that enables customers to track their routine, calorie intake and manage their lifestyle choices. This data can help insurers design better products that can reward customers maintaining healthy habits. Technologies like machine learning and artificial intelligence are now widely used - assessing fewer complex claims and deploying chatbots to manage customer relations better are some of the examples. Similarly, predictive models built based on richer data collated from various sources are helping in several business areas such as renewals management, cross-selling, fraud filtration, etc.

Dr Sudha Reddy: Health insurers look for both customer level data as well as overall trends in the health and well-being space across the world. For policy issuance, insurers are more and more looking at personal details, family history, lifestyle patterns etc, to gauge the overall health score of a person. Insurers also keep looking at overall health trends to understand what would be needed from a product level.

What are the sources of data for health

insurance companies? What is the quality

of the data?

Udayan Joshi: With this movement from the traditional structure to the unstructured data of today, there has been an evolution in the sources of data such as mobile applications, providers of wearable technologies and even web search providers. Many fintech companies specialize in providing data related to specific use cases and demographic/psychographic

analytics. The quality of this data has improved significantly over the last few years. Also, the use of technologies like OCR is helping insurers improve the quality of input data coming from various documents.

Dr Sudha Reddy: Health insurance companies either look at trends from customer data or use open-source data from IIB, GIC or other authentic research intermediaries. For instance, when we were curating India’s first covid insurance product, with no earlier references and evolving treatments, pricing was a real challenge. We improvised and used data from public domains globally - like the John Hopkins Report, Worldometer, research studies published by medical societies, hospital accounts, third-party databases and hospital expenses reports. This helped us understand the main levers of higher/ lower risks and develop our product accordingly. The quality of such data is generally high as they are curated by research bodies, health ministries or healthcare bodies.

What new functionality and analytics health

insurance companies are developing for

leveraging the data?

Udayan Joshi: The goal of any insurance company is to build a sustainable book. This can be done through precise risk selection, which in turn is enabled by data models determining accurate customer profiles and pricing – and right pricing helps in maximizing customer delight. While analytics can help in mitigating the risk of fraud and cancellation thus benefiting the company, it can also aid in designing better customer and partner journeys. Predictive tools can churn data to create personalized experiences and machine learning and artificial intelligence is used to improve turnaround time during

claims and endorsement. These together result in increased customer and partner retention.

Dr Sudha Reddy: H e a l t h i n s u r a n c e companies are developing predictive analysis for

claims, especially to gauge claim predictions that can help in scaling up claims processes, in looking at underwriting ratios and in being ready for any sudden increase in claims. These are relevant especially in such times with more and more covid claims coming in.

What kinds of queries are coming from

customers? How are health insurers

handling vernacular language data?

Udayan Joshi: While customers continue to interact with insurance companies with queries about their policy and to highlight challenges faced during their policy servicing, now, in addition to the traditional call center option, the mode of this interaction has expanded to include social and digital media. There has been a recent growth in technologies that can not only read, translate and organize data in any language from the written text but also analyze and respond through automated text and voice communication – and all this in the customer’s language.

Dr Sudha Reddy: Queries are usually on covid related claims. Customers usually want to know about expenses that are covered, whether consumables and preventive devices like thermometers and oximeters are covered and the kind of hospitals that are treating covid. Customers are also seen to be enquiring about digital claims processes and seeking guidance on the same.

More and more insurers are examining use of vernacular languages to help customers from across the country. We also have our documents in vernacular languages and our website is translated in multiple vernacular languages.

Dr. Sudha ReddyUdayan Joshi

Banking Frontiers June 2021 7

Paradigm Shift

Key to Lending Growth - Speed & ScalabilityThe transformation that is happening in the lending space is enormous. Rajesh Krishnia, Head of Enterprise BFSI at Nutanix India, and D. Venkatesh, Director, Lentra AI, explain the nuances:

Babu Nair: What can banks do to reduce

the turnaround time for proposals? What

are the business opportunities in this?

D. Venkatesh: eKYC has been a game-changer. With the adoption of such initiatives, there has been a paradigm shift in running the lending business. Lending has moved from branch to online. Banks, due to lack of technology, are lagging behind in fulfilling business needs. We are empowering them with the right tools to cope with the demands.

Credit off-take has been hit during the

pandemic. How can technology help

banks?

Venkatesh: Our tools help to collate data and allow the banks to decide on further steps that will have to be taken. The product’s name is ‘GoNoGo’, and we believe that it helps banks to make faster decisions on loan approvals. The speed at which the data is collected from various sources and presented will change the way business will be run in the future.

The foundation must be compliance-

driven, secure and must perform in real-

time. What is the technical support that is

being given to lenders to reduce uptime? Rajesh Krishnia: The bank’s

application would work on a 3-tier architecture. Nutanix has brought in a new platform. We have tried to converge various storage and network aspects of banking. It is scalable and completely configurable. The availability of the data to the various tools makes it even more user-friendly. It is fully compliant with RBI regulations.

There are multiple applications running on

multiple clouds. How do you ensure the

governance of such platforms? Rajesh: Hybrid clouds will be adopted

in the future. We are helping clients with customer use cases. We are trying to move existing applications of clients to the cloud without disrupting their business.

Most of the demands are in the realm of WFH and how the employees’ work experience can be made smoother. Security and compliance are built at the first level so that it becomes easier to move to cloud computing from the mainframe.

What technology paradigms will create

further efficiency in lending?

Venkatesh: We enable the firms with tools that can aggregate the data and help run the business. The platform offers digital-first solutions.

RBI is proactive in reducing the NPAs. What

has been the role of technology in this?

Venkatesh: Early warning systems can be implemented in a 2-pronged approach. The first will be to review the portfolio. The best approach will be at the origination point. The data collected by our tools from various sources give a clear picture to the business rule engine. It can be further enriched by other ecosystems. We have found that under 1% of the cases had flaws and needed intervention.

Open APIs are making inroads in BFSIs.

What is the best way to integrate different

APIs?

Ve n k at e s h : T h e t ra d i t i o n a l lending system was very rigid. Now the government is opening the data portal for anyone to access the data; it is a game-changer. The new lending system allows banks to connect to outside systems. We are allowing the banks to choose the APIs which best suit their business. One of the revolutionary API-led frameworks initiated by the government is OCEN.

This is going to reach the gram panchayat level. This will allow the village-level entrepreneurs to get discounts a n d l o a n s without any physical intervention.

How can banks aggregate the lending

with the help of fintechs?

Venkatesh: Fintechs create niche products. We are dealing with both fintechs and techfin. We try to provide solutions to the banks using our collaborations. We have over 300 ready-to-use integrations. So, solutions are already there for the customers to choose from.

What are the challenges while working in

an open API environment?

Rajesh: Our products are API-driven. We want to remain invisible in the whole process. The customers are wanting to modernize the applications.

What are the technologies which are yet

to be seen in the lending space?

Venkatesh: Credit off-take is going to grow. SEHMATI is a framework that is coming up for lending. This will allow investigation of the accounts of the person and also credit bureau for any defaults. This means good customers will get loans at cheaper rates of interest, and bad customers will not be able to hide. All the banks are doing away with paperwork.

What will be the world of lending look like

post covid?

Venkatesh: There is going to be strong growth once the world reopens. The lenders are going to see increases in loans. There will be all types of lenders.

D. Venkatesh Rajesh Krishnia

Digital Banking

8 Banking Frontiers June 2021

Tie-ups for digitization to drive business growthKarnataka Bank has set up ‘Digital Centre of Excellence’ in its quest for focus on improvement in technology, digitization and building values:

Karnataka Bank has deployed the most modern IT tools to deliver products and services for customers’ benefit

with an aim to develop effective long-term relationship with them. Mahabaleshwara M S, MD & CEO, lists the several digital initiatives in this regard:

Mehul Dani: What are the various tie-ups

Karnataka Bank has entered into and the

perspectives of such partnering? What

are the steps taken towards digitization

through such tie-ups?

Mahabaleshwara M S: We had embarked on a strategic transformation journey, namely ‘KBL Vikaas’ in 2017, complete with a vision, milestones, roadmap revolving around digitization and customer centricity. In the last 2 years, we have tied up with fintech companies for digital banking products, like Fin Wizard Technologies (FISDOM) for mutual funds platform, with IIFL Securities for demat and trading facilities for our bank customers and Corpository for sourcing corporate leads and business.

We have also tied up with companies like Karza Service, Perfios, Jocato, NSDL, Experian, Hunter, etc. to strengthen, automate and digitize the journeys, which include processes like onboarding of customers, recovery automation, data analytics and risk assessment, lending automation, etc.

In all tie-ups, customer is in the center as we all are moving towards ‘paperless, cashless, faceless’ Digital India economy. I am of the view that tie-ups with service platforms facilitates delivery, ease of access of the bank’s products to customers, whereas sales platforms are for customer onboarding, engagements, sales and retentions.

Our KBL Mobile Plus App is well loaded with features that varies from payment of

utility bills, credit card payments, UPI, scan & pay, mutual funds, insurance solutions and our aim is to bring complete banking at the fingertips of our customers.

We are witnessing digital adoption and customer delight through customer engagements. We will continue to focus end-to-end digital solutions for almost all banking activities so as to take customer engagement to a new high.

One more very strategic initiative and a milestone for us has been establishing non-financial, fully owned subsidiary of the bank, KBL Services, which is a big step for us in realigning business strategies with the objectives of improving efficiency, results and valuation in the long run for the bank.

What new initiatives the bank has

undertaken in the last 2 years to

augment business, like for example, lead

generation, business sourcing, cross-

selling and profitability? How do you view

cross-selling of third-party products?

Banks are increasingly becoming intermediary marketplaces in the digital era, and each prospective event in the customer journey presents a new opportunity. We already have our own infrastructure, resources and networking, para-banking tie-ups and activities, including bancassurance, depository service, insurance, MFs, credit cards, etc, that have helped increase the reach of the bank and bring a vast customer segment into the fold of varied financial services.

Our branches are supported by our lead management system (LMS) and analytical leads from the system facilitate identifying, engagement with prospective customers and help us offer additional banking services. This actually helps to build value to our relationships.

In retail asset segment, we have tied up with various builders for pre-approved housing projects that not only help customers in their decision making for house purchase, but reduces the loan processing turnaround time in the bank.

Similarly in motor insurance segment, we have entered into corporate arrangements with Tata Motors and Maruti Suzuki, wherein interested car buyers can avail finance from the bank through our ‘Xpress Digital Car Loan’ process. Our branches and loan processing units now have a strong retail marketing and sales force that facilitates end to end journey for customers.

Cross selling of products is undertaken as per RBI’s master directions on para banking or financial services as issued from time to time. It is in the nature of corporate agency, distribution, referral tie-ups etc. In the para banking segment, we have been offering various third-party

Mahabaleshwara M S claims that Karnataka Bank is ambitiously poised to become the Digital Bank of Future

Banking Frontiers June 2021 9

Dhira - Digital Human Interactive Relationship Assistant

products, which provide one stop financial solutions to the needy customers.

In life insurance we function as a corporate agency of PNB MetLife India Insurance, LIC of India and Bharti Axa Life Insurance. For general insurance products we have tied up with Universal Sompo General Insurance and Bajaj Allianz General Insurance.

Our other arrangements with BFSIs include tie-ups with Way 2 Wealth Brokers and IIFL Securities for equity trading and co-branded credit card facility for our customers through SBI Card. We have partnered with FISDOM, an online platform for sale and management of mutual funds, which digitally enables our customers to invest and track mutual fund investments on KBL Mobile Plus App at their convenience.

The collaboration for third party products helps to improve revenue in the non-core income segment and there also exists a positive correlation to ROA in the longer run. In collaboration lies success.

How has the process of onboarding of

customers changed in the last 2 years in

terms of ease for customers?

We have set up an inhouse ‘Digital Centre of Excellence (DCOE)’, in our quest for reimagining customer journey and continuous focus on improvement in technology, digitization and building values. For example, digital loan underwriting products such as KBL Xpress Car Loan, Express Home Loans, Xpress Ghar Nivesh, Xpress Home Top Up, Xpress Easy Ride, Xpress Cash Loan, Xpress MSME etc, have been successfully launched and implemented by our bank in the last 1 year.

We have tied up with appropriate fintech players for these purposes. The application helps us to speed up account opening and approval of loan application by real-time data extraction and ID verification. These new age applications

automate many manual tasks to increase accuracy and hence, efficiency with automatic data entry. It is noteworthy that

we have already achieved the retail digital loan process adoption and 75% of the total/ number of retail loans have been sanctioned in such a way as on date.

Another tech product is ‘Tab Banking’, which is

flexible and reliable and empowers our field agents to initiate the on-boarding process on-the-fly. They can capture customer information on their tablet devices and initiate the e-KYC process to validate it and then upload this information to the core banking system in real-time. Using this solution, we can ensure the agile processing of savings bank applications and opening of accounts.

These customized banking applications have enabled us

to provide better customer experience by delivering flexibility and convenience of the essential banking operations right at the customer’s doorstep.

What steps have you taken in popularising

and marketing of digital products and

what is the visible impact?

Creating a robust digital platform and integrating all customer touch points across all channels is what we have ambitiously set into. We believe API integration is critical to business and so also our collaboration with newer and non-traditional players are to open up their APIs in order to remain competitive and witness growth. We are continuously engaged with the customers through social media marketing, mobile marketing, email marketing etc. to stay connected, build relationships, value and brand.

We also have contact center tie- up for providing tele marketing services and also popularising our digi-products and solutions. At the branch level, digital adoption campaigns are held to popularise and hand hold the customers for digital adoption.

As a part of indirect endorsement of the bank, you will find our bank’s products promoted in various blogging sites, bookmarking sites and classified sites such as Quora, Tumblr, etc. Customer experience, reviews and recommendations are found here, which affirms our customer centricity.

Also, the covid pandemic has accelerated digital adoptions and we have witnessed this, as our alternate delivery channel penetration crossed 90% this year. Such channel transactions have also increased 3.5-fold and today 90% of overall banking transactions are taking place through alternate delivery channels. We may say, that branch banking has shifted to mobile banking. This is enabling us, as there is a rationale to downsize 25-40% area in the branches, to reduce expenses on rentals, maintenance and other recurring costs.

We feel, we are on a right path to strengthen our technology and digital culture at all levels including business, managing of risk, compliance and governance, and is ambitiously poised to become the digital bank of future.

Collections

10 Banking Frontiers June 2021

From bucket-based to risk-basedCollection systems are increasingly getting digitized and various approaches by financial services institutions make them more and more efficient:

When it comes to collection effic iency for MSMEs, a situational, 360-degree approach

is the most effective. For example, U GRO Capital, being a sector-specific lender, is focusing on leveraging knowledge and experience to understand the cash flows of the entire ecosystem in which a business operates and of the customer’s business as well at a granular level. In situations involving temporary cash flow issues, the company’s approach is to intensify the collection process. For varied situations, it utilizes other tailored solutions.

According to Anuj Pandey, Chief Operating Officer, in the collection process it is crucial to define clearly each milestone and ensure close monitoring of the required actions that need to be taken when such individual milestones are met or missed.

On its part, Fincare Small Finance Bank has built loan collection tools that not only enhance the customer experience but also lower the cost of operations, thus impacting the bottom line. The bank follows a hybrid analytics-driven collection approach, where extensive benchmarking is done and these are validated at the field level through pilots at select markets.

“Post evaluation of the pilot results, suitable collection models are launched across all markets,” says Soham Shukla, Chief Operating Officer - Rural Banking at the bank, adding: “In a nutshell, the combination of expertise and experience has helped us fine-tune our collection strategy - leading to best-in-class collection efficiency, despite the disruption caused by the pandemic.”

Clix Capital has adopted both efficiency and a top-down vs. bottom-up approach to work in tandem to improve collection efficiency. Vishal Jain, Head – Collections,

explains: “First is mind and later is the body and the 2 must work in a synchronized way to function effectively and efficiently.”

He adds: “A top-down approach defines the basic ground rules and direction to a bottom-up approach to ensure MIMO (Minimum Input and Maximum Output) and the bottom-up approach gives the feedback to a top-down approach to fine-tune the basic ground rules and direction to make it realistic and feasible to implement. Our adoption of both the approaches has helped us to segment the portfolio in a sharper and realistic manner to improve our collection efficiency as it was backed by field flavour.”

COLLABORATION WITH OTHER DEPARTMENTS Clix Capital’s collection team is in touch with borrowers throughout the loan tenor - in EWS, bounce and delinquency management activities. This structure feedbacks have been infused in all the key decision-making processes like defining the souring scorecard, loss prediction of the portfolio and in refining the organizational structure with right reward

and recognition program to manage the portfolio quality. Says Vishal: “Even in the current challenging environment where the regulator had declared various relief packages like restructuring, ECLGS, etc to the borrowers to come out from the difficult situation, collections learning has played a key role to identify the right customer segment to offer these packages to manage the portfolio in short and long terms.”

The appropriate collaborations between varied departments are critical to ensure high collection efficiency. Especially, teams from underwriting, collections and risk-analytics departments must work in tandem over the long term to ensure sustainable portfolio management. Anuj of U GRO Capital explains this feature: “At U GRO Capital, these departments work very closely. This collaboration is particularly instrumental in identifying portfolio and collection triggers at an early stage, post data analysis. The cooperation further extends to sales and product teams, which are key elements in the feedback loop, helping and refining the product proposition.”

Soham states that Fincare Small Finance

Anuj Pandey Vinod P

Banking Frontiers June 2021 11

Bank is in the business of ‘collecting money, not giving loans.’ There is a strong alignment between business, support, and control functions for ensuring robust growth and portfolio quality, he says, adding the risk team helps highlight the operating and credit risks, the audit team ensures strong adherence to processes and support teams provide the required manpower, training, technology, back-office support to help the business teams fulfil their goals.

He also shares an example where the risk team put together concentration risk analysis and loss estimation modelling that helped the business teams navigate the way forward in a smarter way.

Speridian Intelligent Collection System provides a holistic view of the scenario about collections. It helps collate the results from various departments such as HR, risk, finance, etc. utilizing the capability of EWS, analytics, AI/ML, etc. Vinod mentions that with the impact of the pandemic, there has been a drastic change in the approach where digitization got a major thrust and the digital adoption has been swift to everybody’s surprise. “Here comes the real benefit of collaboration,” he says, adding: “Our Beacon collection solution synthesizes the data from various channels, analyses, and provides valuable insights to the collection team, dashboards to the managers such that they can approach their customers proactively as well as be more informed.”

He also maintains that this has provided good results to the company’s financial services customers. “The alerts, reminders, collection team dashboards, etc provide updated information so that these companies can take productive action. Also, the manager’s dashboards and escalations provide help to take proactive steps and improve the results.”

FINAL RATING/SCOREU GRO Capital has a distinctive scorecard-based underwriting model, for which the company has filed a patent as well. The model takes into consideration the historical loan delinquency patterns and cash flow within each focused business segment. In this approach, the application score, generated at the sourcing stage, and the behaviour score, reflecting the customer

repayment behaviour, are critical. Says Anuj: “Both scores are used as inputs in the collection strategy and process. These scores are dynamic and vary with time and circumstances. This process then dictates our collection strategy, to resonate with the posed situation, to achieve the best possible collection efficiency.”

Fincare Bank conducts Portfolio Quality Review (PQR) periodically by synthesizing internal and external data of each customer to understand the risk and evaluate future repayment behaviour. Basis this analysis, the bank creates customer segmentation and applies appropriate collection methodologies to reduce leakages.

Over a period, collection has also moved from the conventional way of bucket-based treatment to risk-based treatment, hence score plays an important role in defining the risk in the early MOB (Month on Book). As the MOB increases, the borrower’s internal and external behaviours gain higher influence in defining the risk score. Vishal explains this: “Even recent risk score helps to identify the improvement or deterioration in the portfolio, compared to souring score and to take corrective measure in new souring as well as the future loss prediction.”

According to Vinod, while NACH and e-NACH are extremely popular, other channels are getting more and more traction. Financial institutions are eager to utilize such ever-evolving facilities to reach out to customers, he says, pointing out that previously there were limited options for a customer to pay such as cash or cheque.

But, more than the underlying technology, it is the convenience and acceptability of the end customers which is driving the adoption of systems.

CUSTOMER BEHAVIOUR ANALYSIS Fincare Small Finance Bank recently launched a collection application that enables the loan office to update customer ratings at the time of collection. By gathering this data continually, the bank aims to create Early Warning Signals (EWS) for its field force and help them define bespoke collection strategy.

Customer behaviour score holds high importance in devising a collection strategy, believes Anuj of U GRO Capital. He says this is particularly essential to gauge the risk associated. Customer behaviour, being dynamic, impacts the score as well. “It is essential to appropriately analyze the behaviour to generate the most effective scores, to ensure efficient collection,” says he.

Collection has evolved in the past few years and the borrowers’ behaviour parameters are being used for the risk scorecard, which in turn helps to define the key input metrics like collection channel, collection intensity, engagement scripts and review mechanism for the institutions to improve collection. Vishal concludes the discussion: “Collection can be improved if we reach to the customer at the right time through the right channel with right communication script and all can be defined with the help of customer behaviour analysis.”

Soham Shukla Vishal Jain

Small Finance Bank

12 Banking Frontiers June 2021

Roadmap to Achieve 50% GrowthShivalik Small Finance Bank will be adopting varied technologies and has engaged top-notch IT companies:

Shivalik Small Finance Bank is the first small finance bank to have transitioned from an urban

cooperative bank. It was first registered as a cooperative society in 1997 and was granted a banking license by the Reserve Bank of India to operate from Saharanpur district. The bank has Suveer Kumar Gupta as its MD & CEO, who is an engineer by qualification and has experience in computing and related activities with Tata Consultancy Services. He joined the bank in 1998 an he has been responsible for the all-round growth of the bank, which is the first and largest multi-state urban cooperative bank in Uttar Pradesh. With his deep focus on technology, he has brought in automation and technology drive services in the bank.

1000 TOUCHPOINTS With a strong technology infrastructure and a solid customer base, developed over 23 years, the bank today has 340 customer touch points, which includes 31 branches, 57 ATMs and 250 banking agents spread across western Uttar Pradesh, Lucknow and Madhya Pradesh.

Suveer has ambitious plans for the future: “We plan to add 40 customer touchpoints in FY 2021-22. In the next 5 years, we also aim to INCREASE the touch points to 1000. The aim is to expand through physical and digital channels and we are therefore looking at various skills including branch banking, digital sales, information technology, information security, compliance, risk management.”

DIGITAL ADOPTION DOUBLEDShivalik Small Finance Bank has made significant efforts in technology induction in the last 3 years to enable it to scale up rapidly. It completed a major technology transformation in 2017. And the pandemic accelerated digital adoption by the customers. Suveer says digital adoption more than doubled and the number of

digital transactions crossed 3.5 million. There was 20% rise in mobile banking adoption. There was a 150% yoy growth in mobile and internet banking transactions. More than 40% of the eligible customers already has debit cards and this segment is transacting using micro-ATMs or handheld devices. And 25% of the eligible customer base is on mobile and internet banking.”

LOAN ORIGINATION PLATFORMThe total business of the bank has grown by 10% in FY 2020-21 to `20 billion, with deposits at `12.45 billion and advances at `8.05 billion. This is despite extraordinary situation caused by the pandemic. The bank offers instant sanctioning of loans on digital channels.

It has a unique 2-wheeler insurance plan offered through BQR code, which is offered with the support of Bajaj Allianz General Insurance Co. The customer can just scan a QR code and enter the registration number of the vehicle. Details get populated and the premium amount

is displayed. Customers can just pay the amount at the press of button and the policy is also issued instantly.

DIGITAL ONBOARDING: E-KYCThe bank has introduced paperless account opening using e-KYC for savings bank accounts. Says Suveer: “95% of all savings accounts in our bank are opened digitally. We have plans to enable new account opening via website to drive customer acquisition digitally.”

The bank also offers business correspondent banking. In FY 2020/21, it introduced an app for employees, distributors, agents and BCs to onboard customers digitally and enable payment services. “We are currently working on video KYC and an integration sandbox for third parties to partner with us,” says Suveer

PAYMENTS & CLOUDTechnology has been a key focus area of the bank. Digital channels offered by the bank include mobile banking on both iOS and Android, internet banking, micro-ATMs for doorstep banking and Aadhaar-enabled payments. Says Suveer: “We are live on all retail payment platforms including UPI, IMPS, NEFT and RTGS and we are a direct member of the National Financial Switch. While 80% of all transactions in the bank are happening via digital channels, all our branches are equipped with cash recyclers, which perform the dual role of ATMs and cash deposit machines.”

Shivalik Small Finance Bank has been a pioneer in the adoption of cloud way back in 2013, even while it was a UCB. “We were the first bank in India to host the Infosys Finacle solutions on the cloud using a hybrid cloud architecture. The cloud-based architecture provides the bank with unmatched agility to cost effectively manage scale and power its growth,” says Suveer.

TECH VENDORSThe bank has a number of established

Suveer Kumar Gupta aims to offer online fixed deposits and digital loans in the current FY itself

Banking Frontiers June 2021 13

technology vendors. The CBS is Finacle from Infosys and it has a digital banking suite including internet and mobile banking. The data is hosted at CtrlS data centers which are classified as tier-4 data centers. Other technology partners include FIS Global for Payments and Switching Services, FSS for UPI payments and Bharti Airtel for networking solutions. The bank is about to go live on Oracle’s Middleware and API Gateway solutions both of which also utilize Oracle Cloud Services.

CAPEX, OPEX, TEAM SIZEThe IT capital expenditure of the bank as a proportion of the total income has on an average been 5.1% over the last 5 years, which is higher than the industry standard of 2-3%. It touched a peak of about 16% in FY 19-20, when the bank completed a large digital transformation project. IT opex represented 8.5% of all operating expenses in FY 20-21. IT opex (excluding staff expenses) have increased by 42% yoy on average over the last 5 years especially because the bank’s IT infrastructure is hosted on a cloud-based model. The size of the bank’s IT team continues to grow and is about 10% of the total workforce, ie around 50 people.

CUSTOMER ENGAGEMENTShivalik Small Finance Bank has been using customer behavior analysis to offer products and solutions to existing customers and drive digital adoption. This is done via an assisted digital approach whereby contact center teams of the bank are in touch with customers. The bank has been able to increase mobile banking adoption through dedicated calling to customers where the teams guide the customers on how to onboard on the bank’s app.

The bank is also present on all major social media platforms including LinkedIn, Facebook, and Twitter. “We will continue investing in latest technology to keep pace with the changing nature of digital banking with a key focus on our extended target customer segment,” says Suveer.

DIGITAL FIRST VISIONWith over 450,000 customers, the bank has been leveraging technology to extend its

reach into the last mile and offer financial services for the masses and MSMEs. “If the year 2020 has taught us anything,” says Suveer, “it is that technology and digitization is the only way to progress. Our vision is to be a new age bank being digital first in its mindset and provide best in class banking services to the underserved and underbanked sections of the population, which they may be unable to get from other larger banks. The focus is on doing this through a combination of personalized, respectful customer service and superior technology offering for our target customers.”

SECURITY ENHANCEMENTShivalik Small Finance Bank has migrated to a new enterprise fraud risk management (EFRM) solution to monitor high risk transactions. “We have implemented Dynamic Key Exchange (DKE) as a security enhancement measure for payment systems. Any investments in technology have to be accompanied by investments into cyber and information security initiatives and fraud prevention tools,” says Suveer

HELP FROM FINTECHSuveer believes in having a clear vision to create a brick and click bank. The bank has API enabled architecture, which will allow partnerships with fintechs and other players. It currently has partnerships in place with India Gold, a fintech which offers doorstep delivery of gold loans; it has arrangements with Airtel Payments Bank and Atyati Technologies for retail and microfinance loans. It is actively engaged in discussions with multiple fintech partners to reach newer customer segments like entrepreneurial and underbanked women,

kirana stores, millennials in need of neo-banking services and individuals looking for gold loans.

In the next 12 months, the bank aims to offer online fixed deposits, customized savings accounts for millennials, digital loans against fixed deposits and insurance policies, loans against e-warehouse receipts, etc. Says Suveer: “With a razor-sharp focus on small businesses, we plan to grow our current loan book of `8.05 billion and deposits of `12.45 billion by 50% over next 12 months. Backed by significant investments made in building a robust digital interface to complement its physical touch points, our new entity aims to grow the business by `10 billion and significantly expand its current base of 450,000 customers in the next 12 months.”

TECHNOLOGY ROADMAP The pandemic has certainly accelerated digital adoption at a much faster pace than would have been organically possible. Suveer expects the trend of transacting through digital channels to continue and cross 90% from present 80% in the coming years. “Almost 65% of our customer base is using digital channels. We plan to push this up further by another 10-15 percentage points. We also plan to invest in building capabilities around digital sales, especially on customer on-boarding and insurance, integration capabilities to partner with the external eco-system including fintechs, data analytics to assist customer acquisition and business process automation to ensure that customer journeys can be simplified and time to service any requests are reduced. These are an integral part of our technology roadmap,” he says.

Shivalik Bank recently launched its Rupay Debit Card

Digitization Initiatives

14 Banking Frontiers June 2021

Pillars of Transformation - AI & AutomationCity Union Bank is also building middleware platform that would help third party systems and fintechs to connect with core banking and internal legacy systems:

City Union Bank has been a pioneer in implementing IT enabled solutions for the benefit

of customers who could avail banking products and services at their convenience anytime, anywhere. One of the most innovative technology products of the bank is ‘CUB All in One Mobile App’.

Sankaran G., General Manager, Computer Systems Department, describes the solution: “This is a multilingual voice enabled interactive chat bot launched by Finance Minister Nirmala Sitharaman. The bot can converse in Tamil, English, Hindi and Telugu. We were the first bank to launch such a product in the Indian banking industry. Customers can converse with this bot for their general banking needs, including transactions like balance enquiry, mini statement, fund transfer over voice/text instructions, wealth management services, utility payments etc.”

‘CUB Lakshmi’ is the bank’s banking robot. It leverages AI techniques and is integrated with the core banking solution. It provides information on accounts, answer generic banking queries, last 5 transactions, 15G submission, cheque book request, etc.

AI BASED LOAN PROCESSING The bank is also planning some key digital initiatives during the current financial year. One of them is an AI-based loan processing solution, which will digitally accept KYC document, documents like IT returns, balance sheet, salary slips, GST returns etc and facilitate approval and sanction of the loans digitally. Says Sankaran: “The project is expected to go live by September 2021. It significantly enhances user experience by reducing TAT as application processing is done in 2 working days instead of the current 5-7 working days.”

OPEN BANKING PLATFORM The bank has set out on a digital

transformation journey to adopt open banking and partnerships. Sankaran says it is building an enterprise-wide middleware platform that would help third party systems and fintechs to connect with the core banking / internal legacy systems. This would enable them to distribute the banks products to potential customers and build products on top of it. “We expect to go live by July 2021 and will open up banking for fintechs to partner with us,” he adds.

SAVING FORMS, DOCUMENTSThe bank is also implementing a low-code content document management and workflow automation platform allowing the bank to create, share and save forms and inter-office documents quickly without building them from scratch and allow for digital execution. The project is expected to go live in 2 months by August 2021.

The platform is expected to help the bank in reducing manual processes and time delays. Also, it will help in going digital without paper. Says Sankaran: “In all the above cases, the vendors were selected basis due diligence on product capability, lower cost, company profile, feedback from peer banks and faster time to market as the metrics.”

AI BASED UNDERWRITINGThe bank has engaged a data analytics partner to make use of big data available with the bank on transactions, demographics and financials of the borrowers to deliver risk-based pricing on gold loans and SME loans. This is expected to help creditworthy borrowers to get credit at a lower rate / discount compared to ordinary borrowers. It will also identify potential NPAs and reduce the risk exposure of such accounts for the bank. This project is also expected to go live in 2 months.

AUTOMATING CHEQUE PASSINGUsually, cheque clearing at the 3 CTS grids is done after verifying the customer’s signature and payment details. Sankaran says the bank is proposing to automate the comparison process of verifying the signatures in the cheques and those in the bank’s records. “The passing of cheques is done during the night. The staff doing the comparison at night are bound to make mistakes due to fatigue. Hence, we have started procedure for procuring a solution for system-based comparison of signature, which will speed up the clearing process,” says Sankaran.

CONNECTING BANKING WITH ERP To provide better customer service to its corporate clients, the bank is developing an API service that will facilitate integration with the ERP system of the clients so that payables can be managed more efficiently. “With this

Sankaran G. reveals that 90% of City Union Bank’s accounts are now opened digitally via e-KYC or video KYC

Banking Frontiers June 2021 15

service, customers can transact with their linked accounts on their ERP platform. Customers can also manage their cash management services with this API. The project will be live soon,” says Sankaran.

TAB BANKING, VIDEO KYCCity Union Bank has a number of new projects with their existing vendors. It has already implemented eKYC for opening of accounts with Aadhaar based identification of customers. It has also rolled out tab banking through which the bank’s staff meet customers at their places and using the eKYC process, open the accounts. The bank has also introduced video KYC process through which customer identification is done. Customers can open their accounts through the bank’s mobile banking application from their places. They can book a slot for video KYC and the staff will initiate a video call and verify KYC documents and signatures. Once this is done the account is opened and the customer can do all transactions. “Nearly 90% of our accounts are now opened digitally via eKYC or video KYC,” says Sankaran.

TRADE FINANCE AUTOMATIONAs of now, the bank’s trade finance

application is a static and transaction-oriented solution. The bank proposes to implement an AI based solution for trade finance. Sankaran says that the proposed solution will be capable of reading the documents submitted by customers online and automate the process of generating recommendations of LC/guarantee opening, bill payments, retiring of LCs etc.

CARD-LESS CASH WITHDRAWAL The bank has launched inter-operable card-less cash withdrawal enabling customers to withdraw cash in all its NCR ATMs by using the UPI QR code. Sankaran claims the bank is the first bank in India to launch this facility and once other banks launch this facility, customers of all banks can use this card-less withdrawal from any bank’s ATMs.

Fintrend Setters NEXT – New tech trends amidst the pandemic (Technoviti 2021)

Technology

leaders, CEOs

of payment

processing firms

fintechs

Summary: While it has been a disappointing year that had passed off, fintechs see a big future tapping into an impending era of mobile payments.

Customer Management

16 Banking Frontiers June 2021

Who, When, What, How - CRM Embraces AllSpecialists discuss the changing role of CRM, personalized communication, power of social media channels, measures & special projects:

Finance companies are focusing on increasing customer engagement and enhancing customer experience.

Communication plays a critical role in terms of timing, relevance and what organizations want to communicate or to engage with their customers.

PERSONALIZED COMMUNICATION Canara HSBC Oriental Bank of Commerce Life Insurance Co has invested in a customer communication management system that ensures customized and interact ive communication with customers through varied delivery modes. This tool is further supported by a CRM solution that provides a 360-degree view of the customer and has analytical capabilities that the company is starting to unlock to deliver experiential and targeted customer experience.

Sachin Dutta, Chief Operating Officer at the insurance company, believes that there is immense opportunity to leverage on communication platforms already available via social media. This reduces the time that one normally takes to get familiar with new communication. “Therefore, our WhatsApp bot and chatbots provide platforms for customers to converse with us as per their convenience and device and time of choice. We made our IVR flexible and highly customized to cater to the needs of customers. We will be investing in more bots like voice bots and email bots to expand our servicing avenues and continue to pursue excellence in this area,” says Sachin.

Kotak Mahindra Life Insurance Co uses Send Time Optimization (STO) to reach out to the customers at their most preferred time. Everyone has a different pattern when it comes to checking emails. Over the few months, the insurer has identified a pattern for each customer and the best time to send out a communication to them which will ensure that they have enough time to read the email as well as

get the maximum benefit from it. This has helped the company to increase its delivery percentage and overall open rates.

According to Subhasis Ghosh, Senior Executive Vice President & Head – Marketing & Group Insurance at Kotak Life, every customer has his preference of consuming information - some prefer SMS (short content) and other email (more detailed). Sending communication to the customer on their preferred channel has helped the company to minimize wastage and create a higher engagement, he says.

SPECIALIZED SOLUTIONS To personalize the customer experience, Kotak Mahindra Bank has been issuing persona-based communications. For example, messaging on fixed deposits is a short-term goal-based communication for millennial customers, while for women customers, the same messaging is customized to saving money for emergencies and ease of investment.

Puneet Kapoor, President - Products, Alternate Channels & Customer Experience Delivery at the bank, says: “Our net banking home page experience can be hyper customized by each customer according to his interests. For example, if a customer uses bill payments, fund transfers and FDs the most, then he can customize the home page widgets for the most-used services to get easy and quick access.

Speridian CRM, which is built on Next Best Action (NBA) framework, uses AI for recommendations, business intelligence and to synthesize tactics, strategies, and business insights which considers all the possible actions during a customer interaction and recommends the optimal offer.

Mohammad Omer Kundi, Practice Manager - Global Banking SME at Speridian Beacon, says: “By continuously suggesting ‘what to do next to a customer, CRM NBA allows iterative and interactive forms of dialogue that customers identify as natural thereby delivering a first-class customer-centric experience. CRM NBA is a paradigm shift from being product-centric to becoming customer-centric. NBA is not necessarily about knowing the best product or message to serve up to a customer, but when to offer it and how to communicate it.”

SOCIAL INTERACTIONS The levels of adoption for social media have increased and customers are more familiar with the social media platforms compared to earlier times. BFSI companies are seeing this as a good opportunity to stay engaged with the customers.

Sachin says: “Social media has connected people digitally and has emerged as a platform where customers can do a lot of research, go through blogs and make themselves aware of new market trends, etc. It is also emerging as a tool to exchange views. We do provide WhatsApp as a mode of communication if the customer opts for such services.”

Sachin Dutta recommends IVR should be flexible & highly customized to cater to the needs of customers

Banking Frontiers June 2021 17

Social media has been the place where irate customers would go when the traditional channels of approaching the company would fail. However, in recent months, Kotak Life has noticed an increase in the number of customers approaching the company via online to tell positive stories.

Says Subhasis: “We have noticed that as platforms have matured, customers have become more comfortable with interacting about private policy details in that environment. There are lesser requests for call-backs once the customers notice that such avenues are working. We use a third-party application to aggregate all these multi-channel tickets into one dashboard for easier and quicker handling. This single view approach has helped us reduce both first response and resolution times.”

Puneet maintains that at Kotak Mahindra Bank, interactions with customers on social media result in the staff getting a sense that inclusivity will matter more than ever. “To facilitate this, we are using stories as a content format,” says he.

Concurring, Mohammad Omer says: “CRM uses the objections info to improve ad campaigns on search engines and social

media platforms. A useful tactic is to create custom ads based on customer objections. Speridian CRM offers templates that meet all quality requirements, and which can be optimized for optimal results.”

INBOUND & OUTBOUND Call centres will have to elevate communication through digital channels to thrive in the post-covid world. Scalability being the key, organizations will need to adopt solutions powered by advanced automation which not only offers data security but also provides stability to human operators. The ongoing pandemic has opened newer channels for customer interaction. Kotak Life’s newly launched digital platforms account for a whopping 67% servicing, easing out the pressure on its traditional channels - namely call center and email desk.

Sachin expects the IVRs to become more responsive and intelligent with technologies like voice recognition-based verification becoming norm. Use cases for insurance are currently less but companies are experimenting. “Also, we believe that IVRs are perfect use cases for voice bots or virtual assistants provided by all technology leaders getting integrated and powering the IVRs in the future. We are also seeing increased adoption of video calls, video-based verifications including KYC which is helping businesses do well during covid times. Such reliance on voice and video-based technology shall emerge even stronger in the next 12 months,” says he.

With inbound calls forced to seek alternatives, consumers too have adopted a mobile-first approach and have turned to net banking. Kotak Mahindra Bank’s customer experience center is receiving a lesser number of calls. There has been a reduction in the number of calls to agents. Puneet provides details: “We have witnessed a huge change in customer behavior. The nature of calls is no longer only for seeking simple information. Customers now call for resolving multiple and complex queries. A total of 43% of calls and conversations are complemented with WhatsApp communication. This has led to a 9-11 points higher Net Promoter Score (NPS) for us.”

He maintains that in outbound calls digital processes/ products assisted by employees get sold on calls. If the effort is low, customers are quite comfortable engaging with virtual relationship managers. Besides, long conversations are not a deterrent if they add value, and video is still the future.

MEASURES Due to the pandemic, the Kotak Life team had decided to ensure that even though they were not able to meet customers face to face, they still are with them throughout. This led to focussing the attention of the customer on online mediums for any assistance they need. The company constantly communicated its digital tools through its campaign called ‘Ease hai ….hamesha’ across multiple channels - KAYA (chatbot), WhatsApp, OPM (policy manager app), and easy claim’s process online.

Subhasis shares the details: “The campaign was successful in reducing calls on our toll-free number and footfall to the branches. We went one step ahead and added this campaign as a part of our welcome and onboarding communication, which helped educate our customers from

Mohammad Omer Kundi advocates CRM NBA to deliver a first-class customer-centric experience

Subhasis Ghosh reveals that communicating in the right channel helped them create a higher customer engagement

Customer Management

18 Banking Frontiers June 2021

the start about the various digital tools at their disposal to ensure that we stick by our promise of ‘Hum hai….hamesha’.”

Canara HSBC OBC Insurance Co used a video calling facility where in addition to normal inbound, customers can interact with its agent virtually over a video session. The company comes up with initiatives like video-based verifications to make the experience seamless for the customers who prefer to interact with them digitally. Sachin added: “We interact via social media platforms for business as well as in creating awareness. All such facilities have helped us, and our customers operate and engage with us digitally. We expect the trend to continue and gain further momentum and shape the way companies communicate and engage with our customers.”

FOR GEN X, GEN Y, GEN ZCanara HSBC OBC is focussing on working with the millennial age group to drive increased uptake of insurance. The company understands and foresees that future generations will consider technology and baseline services as given and would want the insurer to interact with them on how they interact with all other companies over the web.

According to Sachin, investments in technology are driven largely by keeping the future in mind and hence are being developed with the intent of making it fit for purpose for any generation. “We understand the needs of people who have opted for pension plans with us and understand the needs of millennials who may be interested in protection or savings proposition. That is the range we operate in and our solutions, therefore, need to be flexible and brutally simple to each of these generations,” he says.

Kotak Mahindra Bank has been using WhatsApp as a complement to voice conversations. “Last year, we were the first bank to integrate the video KYC process in the account opening journey. Additionally, we have also been using live chats with customers,” says Puneet.

CRM FUNCTIONSSperidian’s CRM system helps to generate

leads, segment them and qualify them so salespeople can customize their outreach. The optimum offer rejection is handled in CRM by Sales Objection Process; next, it provides sales reps with a historical overview of all customer interactions and valuable intelligence on how to approach every objection. The CRM system has its ways of handling sales objections before they have happened, while they are happening, and after they have happened.

Says Mohammad Omer: “Preventing sales objections is a function in our CRM system, it creates a database, including previous customer objections, regardless of whether the objections were successfully handled or not. This way, agents have enough saved information to deal with new objections, even if they deal with a client for the very first time. Another important thing CRM does is link leads to objections. This will help the agent customize his approach to a particular customer.”

He shares details of other functions like automating handling of sales objections. He says the CRM does not simply drive customers your way, but it examines their buying capacity (foremost

in terms of budget and influence), giving salespeople a more or less clear picture of the objection they might have. In relating leads to the common objections function, the CRM generates emails and messages for each of the tagged objections, allowing the salesperson to prepare just the right content for each target audience.

CRM & MARKETING Kotak Life has started promoter referral campaigns that piggyback on its Net Promoter System framework. These are directly integrated with its CRM.

Kotak Mahindra Bank offers segmented communications basis p r o p e n s i ty a n a l y s i s . C u s t o m e r propensity is analyzed to understand which offer will provide the most value to a particular customer and he receives communication basis that analysis. This is further augmented for cross-selling opportunities.

Explains Puneet: “Our CRM was effectively mobilized during the lockdown. It enables pre-qualified offers uniquely tailored for individual customers and MSMEs, thereby helping us boost new acquisitions as well as cross-selling of products and services. In addition, it provides a powerful lead management system on a customer’s transaction behaviour, thereby giving a 360-degree view of a customer’s profile to our banking relationship managers. This helps us offer the right product at the right time to the right customer.”

Speridian CRM omnichannel insights and reports provide comprehensive information on how overall support is performing across channels. The reports provide a rich visualization and ability to filter across channels, queues, agents and date ranges to better understand performance and troubleshoot problem areas.

Mohammad Omer says: “Some of the useful KPIs include conversation engaged based on channels, abandoned rate based on channels, transfer rate based on channels, average wait time based on channels, reports based on how the agent is performing on channels and sentiment zones by channels.”

Puneet Kapoor supports effective mobilization of CRM for individual customers & MSMEs

Banking Frontiers June 2021 19

CX and Technology

Innovation & Tech that boost CXDharmender Narang, Chief Customer Experience Officer at India Infoline, speaks about CX innovations and technologies:

Babu Nair: What are the remarkable

innovations that you have brought about

in the last few months? What has the

customer response been?

Dharmender Narang: We always try to give superlative customer experience. Building trust and being proactive keep us ahead and progressing. Not constraining to the channels gives us an edge over others. We noticed the growing trend of ‘do-it-yourself ’. Customers want to be independent. AI and chat bots have helped us in achieving that. Many peers provide chat bot facility. We have gone one step further by adding AI to the chat bot. This gives clients a more realistic answer. We proactively provide solutions to the customers.

Irrespective of the channel the customer is using, he should get uniform customer experiences. We have implemented a common CRM platform across all channels of communication. This allows companies to address the queries of the customers.

This way (i) there is no disconnect between the channels (ii) AI is equipped with a large database of questions. However, if the customer is not satisfied, he has the option to chat with the agent live.

The customer can connect to us through multiple channels 24x7 and irrespective of the channel chosen, he gets the same experience in real-time.

It is observed that customers don’t

shy away from paying for better

customer services. Along with the

product differentiator, if an experience

differentiator were to be made, what

would be the criteria?

Undercutting will never result in the best customer experiences. The customer always looks for the value added to the product. There may be many companies selling products with the same technology, but the added value is what

entices the customer. For example, there may be many stock broking agents, but the well-researched agent, with whom wealth growth is possible, is the most sought after.

Many times, the customer may not know this upfront. The expertise of the person is valuable. This is what gives value to the product. We provide this expertise and allow the customer to create wealth for themselves.

What are the new and innovative tools

that you have planned for good customer

experience?

Voice bot is picking up. It will have to cross the language barrier. Chat bots are now giving language options. A lot of work is happening on voice analytics. During real-time chat the agent can identify an irate customer and provide solutions accordingly. Technology is moving very fast and new ideas are coming up equally

fast. This will help in reaching out to customers in small cities. This will in turn add to the customer base.

Is it possible to preempt customer

needs with technology? Will process

automation help the companies?

When the backend is completely automated it is easier to provide the analysis. If a customer query is not being resolved by AI, it indicates a process gap. Automating the processes and providing consistent output will help reduce the cost of service. Combined efforts of AI and service agents will take customer service to a higher level. We are always interested in exploring new products in the Fintech sector.

Collections - It’s like Chess

Summary: Collections function in a BFSI organization involves making intelligent moves to maximize returns per customer, maximize number of customers, minimize the number of calls, focus on the high-risk cases.

Business Leaders from Fintech Companies

Dharmender Narang believes that technology is moving very fast and new ideas are coming up equally fast

Anil PinAPAlA

Abhijit RAy SReekumAR m

Alok ChAdhAAnAnt deShPAnde

kunAl VeRmA

Digital Journey

20 Banking Frontiers June 2021

Becoming a Data First CompanyMyMoneyMantra is building robust technology infrastructure constituting AI, Data Analytics and Machine Learning to ensure a seamless customer experience:

MyMoneyMantra (MMM) is a finserve marketplace, helping customers compare products

across 100+ financial institutions and opt for the most suited one. Over the last 5 years, it has originated more than $5 billion worth of financial services products through its platform. It currently serves about 7 million customers across 60 cities with more than 100+ banking partners and 3000 employees. Raj Khosla, Founder & MD, traces the digital journey.

Mehul Dani: How has MyMoneyMantra

implemented its digital strategy in

2020-21?

Raj Khosla: Digital has opened up new avenues for creating competitive advantage and driving business growth for MyMoneyMantra. We have tied digital to our strong delivery and distribution platform to give us an edge over competitors. Recently, our website has been revamped with new design and functionalities keeping customer transactional convenience as the main objective. Our digital infrastructure has expanded our geographic and demographic distribution multi-fold.