Embed Size (px)

Citation preview

Page | 1

Contents

EXECUTIVE SUMMARY ................................................................................................................................................. 3

CHAPTER 1: INTRODUCTION ...................................................................................................................................... 4

1.1 Origin of the Report .............................................................................................................................. 4

1.2 Objectives of the Study ......................................................................................................................... 4

1.3 Methodology ......................................................................................................................................... 4

1.4 Limitations and Restrictions of the Report ........................................................................................... 5

CHAPTER 2: REVIEW OF LITERATURE .................................................................................................................... 6

CHAPTER 3: ISLAMIC BANKING ................................................................................................................................. 8

2.1 Genesis of Islamic Banking in Bangladesh........................................................................................... 8

2.2 What is Islamic Banking ....................................................................................................................... 8

2.3 Why Islamic Banking ........................................................................................................................... 9

2.4 Objectives of Islamic Banking .............................................................................................................. 9

2.5 Why interest is prohibited in Islamic banking system .......................................................................... 9

2.6 Riba (Interest) VS. Profit .................................................................................................................... 10

2.7 Difference between Islamic & Conventional banking ........................................................................ 10

CHAPTER 4: A BRIEF INTRODUCTION OF ISLAMIC BANKS IN BANGLADESH .......................................... 15

CHAPTER 5: INVESTMENT MECHANISM OF ISLAMIC BANKS ....................................................................... 19

1) Bai Mechanism ..................................................................................................................................... 20

2. Ijara Mechanism ................................................................................................................................... 27

3. Share Mechanism.................................................................................................................................. 28

CHAPTER 6: PERFORMANCE ANALYSIS AND DISCUSSION .............................................................................. 29

CHAPTER 7: COMPERATIVE ANALYSIS OF CONVENTIONAL AND ISLAMIC BANKS .............................. 38

6.1 The profitability of Islamic Banking in comparison to Conventional Banking .................................. 38

6.2 Market Share of Islamic Banks ........................................................................................................... 39

6.3 Islamic Banks Liquidity ...................................................................................................................... 40

6.4 Capital adequacy of Islamic Banks and Conventional Banks ............................................................ 41

2 | Performance Analysis: A Study on the Islamic Banks of Bangladesh

6.5 NPL of Conventional Banks and Islamic Banks ................................................................................ 42

CHAPTER 8: MICRO-ECONOMIC AND PROFITIBILITY OF ISLAMIC BANKS OF BANGLADESH ............................ 46

CHAPTER 9: PROBLEMS AND RECOMMENDATIONS ......................................................................................... 48

CONCLUSION .................................................................................................................................................................. 51

REFERENECS

APPENDICES

3 | Performance Analysis: A Study on the Islamic Banks of Bangladesh

EXECUTIVE SUMMARY

Islamic banking system was introduced in Bangladesh more than two decades ago. It

constitutes an important part of the banking system of Bangladesh. This report focuses on

the performance analysis of the Islamic banks working in Bangladesh.

The report contains Eight (8) chapters. The first chapter includes the introductory words

of the internship report and about the methodology used in the preparation thereof. The

second chapter describes concept of Islamic banking and difference between Islamic and

conventional banks. The history of Islamic Banking in Bangladesh and brief knowledge

about Islamic Banks in Bangladesh are included in chapter three. The investment

mechanism of the Islamic banks, modes of investment, its special schemes are described

in chapter four. In chapter five, I have shown some trend analysis on performance on

Islamic Banks. For example deposit growth, investment growth, profit trend, NPL of

Islamic Banks from 2009-2013. From trend analysis I have found that, the Islamic Banks

demonstrated steady growth over the years. Some Ratio analysis for example ROE, ROA,

Net investment income to total investment etc also done here to see which Islamic bank

performed best in respect of profitability among all the Islamic banks of Bangladesh. I

have found here Shahjalal Islami Bank Limited performed best in terms of profitability

and Al Arafah Islami Bank Limited had got the 2nd

position in this case.

In Chapter Six I have shown the comparative analysis of Conventional and Islamic Banks

and found here that Islamic Banks performed better in terms of NPL but conventional

banks performed better in terms of profitability.

In Chapter Seven, I‟ve tried to analyze whether profitability of Islamic banks of

Bangladesh depends on the macroeconomic factor and whether there is any relationship

between these two. This report also shows whether in most of the cases profitability of

Islamic Banks is related with the GDP growth rate of Bangladesh.

The concluding chapter bearing number eight contains findings, recommendations and

the overall conclusion.

During the composition of the report proper care and uninterrupted concentration has

been invested. Moreover, containing some unintentional mistake and printing error is not

usual. I do hope all to be considered in this regard.

4 | Performance Analysis: A Study on the Islamic Banks of Bangladesh

CHAPTER 1: INTRODUCTION

1.1 Origin of the Report

Now a day, education is not just limited to books and classrooms. In today‟s world,

education is not just a tool to understand the real world and apply knowledge for

betterment of the society as well as business. From education the theoretical knowledge is

obtained from courses of study, which is only the half way of the subject matter. Practical

knowledge has no alternative. The perfect coordination between theory and practice is of

paramount importance in the context of the modern business world in order to resolve the

dichotomy between these two areas. Therefore, an opportunity is offered by Department

of Finance, University of Dhaka, for its potential business graduates to get one and a half

months practical experience in a business organization, which is known as “Internship

Program. I have been assigned by the department to prepare my internship report on the

topic “Profitability Analysis: A study on the Islamic Banks of Bangladesh.” I have

prepared the same as the graduation prerequisite of the MBA program.

1.2 Objectives of the Study

The key objectives of the study are:

To review the distinctive concepts of Islamic banking

To analyze the history of Islamic banking

To evaluate the current practice and performances of the Islamic banks of

Bangladesh

To see whether profitability of Islamic banks of Bangladesh depends on the

macroeconomic factor and whether there is any relationship between these

two.

1.3 Methodology

This is a secondary data based report. Information has been collected from various

secondary sources like journal articles, annual reports of different banks, books and

different websites. All the existing Islamic banks of Bangladesh are included in this

study. The first two objectives of the research are subject to be achieved through the

secondary data review and the qualitative discussion. Current Islamic banking practices

and the performances of different Islamic banks are measured and analyzed from the

financial statements of the banks and information from different relevant websites.

5 | Performance Analysis: A Study on the Islamic Banks of Bangladesh

Statistical analysis tool SPSS and MS Excel had been used for analysis and graphical

presentations

1.4 Limitations and Restrictions of the Report

From the beginning to end, the study has been conducted with the intention to making it

as a complete and truthful one. However, many problems appeared in the way of

conducting the study. During the study it was not possible to visit the whole area covered

by the bank although the financial statements and other information regarding the study

have been considered. The study considers following limitations:

Lack of in-depth knowledge and analytical ability for writing such report.

Lack of experience.

The time period for this study was short.

Another limitation of this report is Bank‟s policy of not disclosing some data &

information for obvious reason, which could be very much useful.

6 | Performance Analysis: A Study on the Islamic Banks of Bangladesh

CHAPTER 2: REVIEW OF LITERATURE

A significant level of development had been observed in Islamic banking research since

the last decade. The western analysts and economists demonstrated their emphasis on the

interest-free business transactions. These western economists discovered the connection

between the interest rates and some key macroeconomic instabilities like- unemployment,

inflation or negative growth (Bernante and Gertler, 1990; Fisher, 1933; Greenwald and

Stiglitz, 1988; Hayek, 1933 & 1939; Minsky, 1977; Smith,1904; Wicksell, 1935).

In different parts of the world, Islamic banking researches had been mostly conducted by

Muslims and a small portion by the non-Muslims. The works of Erol and El-Bdour

(1989)and Erol et al (1990) revealed three key selection criteria for Islamic banks: fast

and efficient services, reputation and confidentiality. According to their findings,

religious motivation was not a prime criterion.

On the contrary, Metawa and Almossawi (1998) and Naser et al (1999) found loyalty to

Islamic belief the primary criterion for selecting Islamic banks in countries like Bahrain

and Jordan. Similarly, some other scholars discovered same findings in their studies in

Indonesia, Kuwait and Malaysia (Kader 1993 & 1995; Osman et al, 2009; Othman and

Owen, 2001 & 2002; Wakhid and Efrita, 2007). A study on a large number of

respondents by Dusuki and Abdullah (2006) discovered that Islamic bankers should not

only rely on promoting the Islamic factors but also the necessary service quality. The

three most important factors found in their study were competence, friendliness and

customer service quality.

Hanif & Iqbal (2010) categorized Islamic modes of financing objectively in two heads;

Sharia compliant and Sharia based. Later, Hanif (2011) discussed these terms used for

modes of financing briefly. He explained Sharia compliant products as the modes of

financing where return of financier is predetermined and fixed but within Sharia

constraints. The tools which are relatively harmonizing the operations of Islamic financial

system with conventional banking includes Murabaha (cost plus profit sale), Ijara (a

rental arrangement), Bai Salam (spot payment for future delivery), Bai Muajjal (sale on

deferred payment), Istasna (order to manufacture) and Diminishing Musharaka (house

7 | Performance Analysis: A Study on the Islamic Banks of Bangladesh

financing) are all Sharia compliant products. Sharia based transactions means the

financing modes adopted by IFIs on profit and loss sharing basis including Musharaka

(partnership in capital) and Mudaraba (partnership of capital and skill). Under Sharia

based modes of financing returns of financier are not fixed in advance rather it depends

upon the outcome of the project. However loss is to be shared according to capital

contribution. Following the rule of substance over form one can conclude that the major

difference between conventional and Islamic financing is Sharia based modes of

financing. Mahal & Rahman (2013) made a comparative analysis between conventional

and Islamic banks of Bangladesh. They discussed the distinctions of product or service

and the distinctions in terms of business efficiency between Islamic Banks and

Conventional Banks. Their key findings on the product or service differences are about

the principles of business, variation in goals, variations in deposit etc. The conventional

banks of Bangladesh deal with man-made principles or principles provided by

Bangladesh Bank. But Islamic banks follow Shariah based principles under the

supervision of BB. Conventional banks currently focusing on the CSR activities but

Islamic banks are focusing on the IT development though they also consider the CSR

issues. Conventional deposit schemes are like the fixed deposit, savings or short notice

deposit and current deposit. The Islamic banks offer through Al-Wadeeah principle and

Mudaraba principle. These researchers also discussed the distinctions in terms of business

efficiency. Profitability of conventional banks depends on loans and investments both;

whereas Islamic banks depends on only investments sectors. Conventional banks have to

maintain more SLR19%) than the Islamic banks (10.5%). Islamic banks do not collect

deposits through conventional methods rather on the basis of profit & loss sharing notion.

8 | Performance Analysis: A Study on the Islamic Banks of Bangladesh

CHAPTER 3: ISLAMIC BANKING

2.1 Genesis of Islamic Banking in Bangladesh

Bangladesh is one of the largest Muslim countries in the world. The people of

this country are deeply committed to Islamic way of life as enshrined in the Holy Qur‟an

and the Sunnah. Naturally, it remains a deep cry in their hearts to fashion and design

their economic lives in accordance with the precepts of Islam. Bangladesh is the third

largest Muslim country in the world with around 135 million populations of which 90

percent are Muslim. The hope and aspiration of the people to run banking system on the

basis of Islamic principle came into reality after the OIC recommendation at its Foreign

Ministers meeting in 1978 at Senegal to develop a separate banking system of their own.

After 5 years of that declaration, in 1983, Bangladesh established its first Islamic bank. At

present, out of 49 banks in Bangladesh, 7 full-fledged Islamic Banks and 19 Islamic

Banking branches of 9 conventional banks are working in the private sector on the basis

of Islamic Shariah.

2.2 What is Islamic Banking

Islamic bank is a financial Institution that operates with the objective to

implement and materialize the economic and financial principles of Islam in the banking

area.

The organization of Islamic conference (OIC) defines an Islamic bank as “a financial

institution whose statutes, rules and procedures expressly state its commitment to the

principals of Islamic Shariah and to the banning of the receipt and payment of interest on

any of its operation.”

According Islamic banking Act 1983 of Malaysia Islamic bank is a “company, which

carries on Islamic banking business. Islamic banking business means banking business

whose aims and operations do not involve any element which is not approved by

the religion of Islam.”

It appears from the above definitions that Islamic banking is system of financial

intermediation that avoids receipt and payment of interest in its transactions and

conducts its operations in a way that it helps achieve the objectives of an Islamic

economy. Alternatively, this is a banking system whose operation is based on Islamic

9 | Performance Analysis: A Study on the Islamic Banks of Bangladesh

principles of transactions of which profit and loss sharing (PLS) is a major feature,

ensuring justice and equity in the economy. That is why Islamic banks are often

known as PLS banks.

2.3 Why Islamic Banking

The objective of Islamic banking is not only to earn profit, but also to do good and

welfare to the people. Islam upholds the concept that money, income and property belong

to Allah and this wealth is to be used for the good of the society. Islamic banks operate

on Islamic principles of profit and loss sharing, strictly avoid interest, which is the

root of exploitation and is responsible for large scale information and unemployment.

An Islamic bank is committed to do away with disparity and establish justice in the

economy, trade, commerce and industry, build socio-economic infrastructure and creating

working opportunity.

2.4 Objectives of Islamic Banking

The primary objective of establishing Islamic banks all over the world is to promote,

foster and develop the application of Islamic principles in the business sector. More

specifically, the objectives of Islamic banking when viewed in the context of its role

in the economy are listed as following:

To offer contemporary financial services in conformity with Islamic Shariah;

To contribute towards economic development and prosperity within the

principles of Islamic justice;

Optimum allocation of scarce financial resources; and to help ensure equitable

distribution of income.

2.5 Why interest is prohibited in Islamic banking system

The word used by the Quran concerning „interest‟ is Riba. The literal meanings of„Riba‟ a

re money increase, increase of anything or increment of anything from its original

amount (Maududi 1979, p.84). However, all increases are not considered as Riba in

Islam. Money may increase in business activities as well. This increase is not

at all considered as Riba. Islam prohibits only those increases that are charged on the loan

with a prefixed rate.

10 | Performance Analysis: A Study on the Islamic Banks of Bangladesh

Interest transfers wealth from the poor to the rich, increasing the inequality in the

distribution of income & wealth. Islam stands for cooperation & brotherhood. Interest

creates an idle class of people who receive their income from accumulated wealth. The

society is deprived of the labor & enterprise of these people. Besides interest on

productive loan raises the cost of production, hence the prices of goods increase. The

income generated by the process of production in form of wages, profits & profit-share

are more equitably distributed.

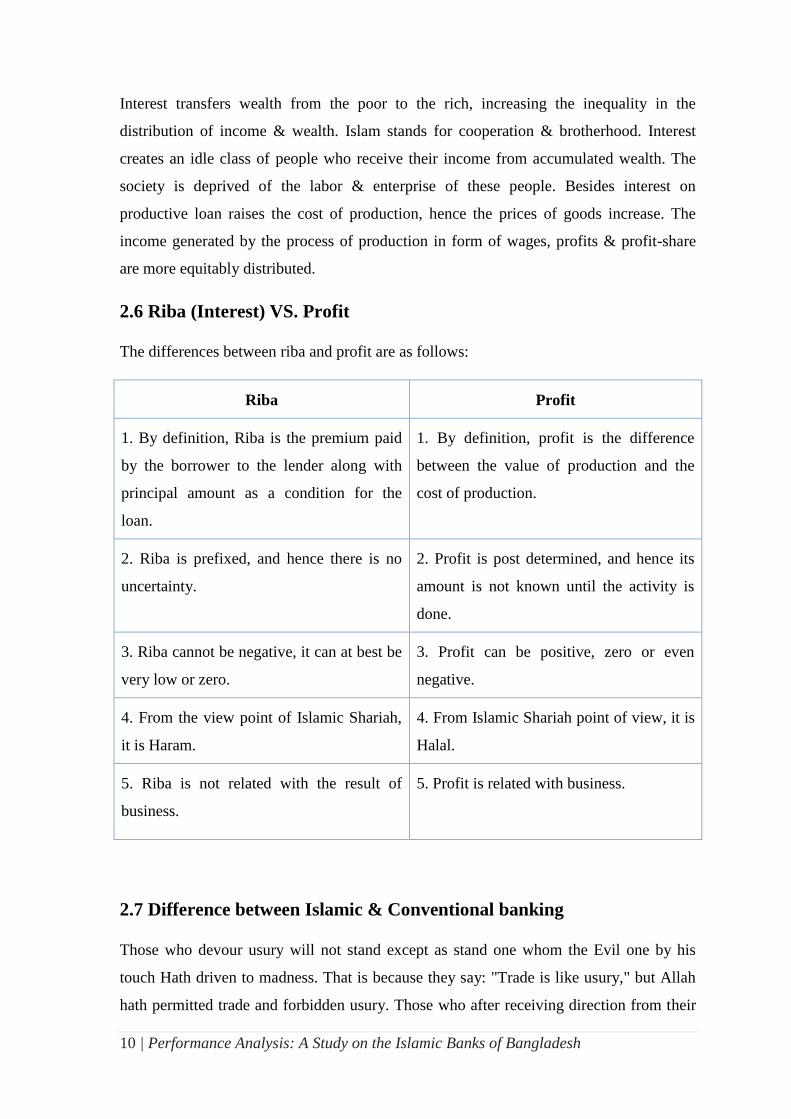

2.6 Riba (Interest) VS. Profit

The differences between riba and profit are as follows:

Riba Profit

1. By definition, Riba is the premium paid

by the borrower to the lender along with

principal amount as a condition for the

loan.

1. By definition, profit is the difference

between the value of production and the

cost of production.

2. Riba is prefixed, and hence there is no

uncertainty.

2. Profit is post determined, and hence its

amount is not known until the activity is

done.

3. Riba cannot be negative, it can at best be

very low or zero.

3. Profit can be positive, zero or even

negative.

4. From the view point of Islamic Shariah,

it is Haram.

4. From Islamic Shariah point of view, it is

Halal.

5. Riba is not related with the result of

business.

5. Profit is related with business.

2.7 Difference between Islamic & Conventional banking

Those who devour usury will not stand except as stand one whom the Evil one by his

touch Hath driven to madness. That is because they say: "Trade is like usury," but Allah

hath permitted trade and forbidden usury. Those who after receiving direction from their

11 | Performance Analysis: A Study on the Islamic Banks of Bangladesh

Lord, desist, shall be pardoned for the past; their case is for Allah (to judge); but those

who repeat (The offence) are companions of the Fire: They will abide therein (for ever).

[2:275]

It‟s clear from the verses of the Holy Quran stated above is that, there is a large

distinction between trade and usury and that‟s why Islamic banking system is totally

different from conventional banking system. The former is based on trade and investment

duly approved by Islamic Shariah and the later is based on usury which is strictly

prohibited under Islamic Shariah. The distinction is shown elaborately in the following:

Islamic Banking Vs. Conventional Banking

One must refrain from making a direct comparison between Islamic banking and

conventional banking. This is because they are extremely different in many ways. The

key difference is that Islamic Banking is based on Shariah foundation. Thus, all dealing,

transaction, business approach, product feature, investment focus, responsibility are

derived from the Shariah law, which lead to the significant difference in many part of the

operations with as of the conventional

The foundation of Islamic bank is based on the Islamic faith and must stay within the

limits of Islamic Law or the Shariah in all of its actions and deeds. The original meaning

of the Arabic word Shariah is 'the way to the source of life' and is now used to refer to

legal system in keeping with the code of behaviour called for by the Holly Qur'an

(Koran). Amongst the governing principles of an Islamic bank are :

The absence of interest-based (riba) transactions;

The avoidance of economic activities involving oppression (zulm)

The avoidance of economic activities involving speculation (gharar);

The introduction of an Islamic tax, zakat;

The discouragement of the production of goods and services which contradict the

Islamic value (haram)

On the other hand, conventional banking is essentially based on the debtor-creditor

relationship between the depositors and the bank on one hand, and between the borrowers

12 | Performance Analysis: A Study on the Islamic Banks of Bangladesh

and the bank on the other. Interest is considered to be the price of credit, reflecting the

opportunity cost of money.

Islamic law considers a loan to be given or taken, free of charge, to meet any

contingency. Thus in Islamic Banking, the creditor should not take advantage of the

borrower. When money is lent out on the basis of interest, more often that it leads to some

kind of injustice. The first Islamic principle underlying for such kind of transactions is

"deal not unjustly, and ye shall not be dealt with unjustly" [2:279] which explain why

commercial banking in an Islamic framework is not based on the debtor-creditor

relationship.

The other principle pertaining to financial transactions in Islam is that there should not be

any reward without taking a risk. This principle is applicable to both labor and capital. As

no payment is allowed for labor, unless it is applied to work, there is no reward for capital

unless it is exposed to business risk. Thus, financial intermediation in an Islamic

framework has been developed on the basis of the above-mentioned principles.

Consequently financial relationships in Islam have been participatory in nature. Lastly,

for the interest of the readers, the unique features of the conventional banking and Islamic

banking are shown in terms of a box diagram as shown below-

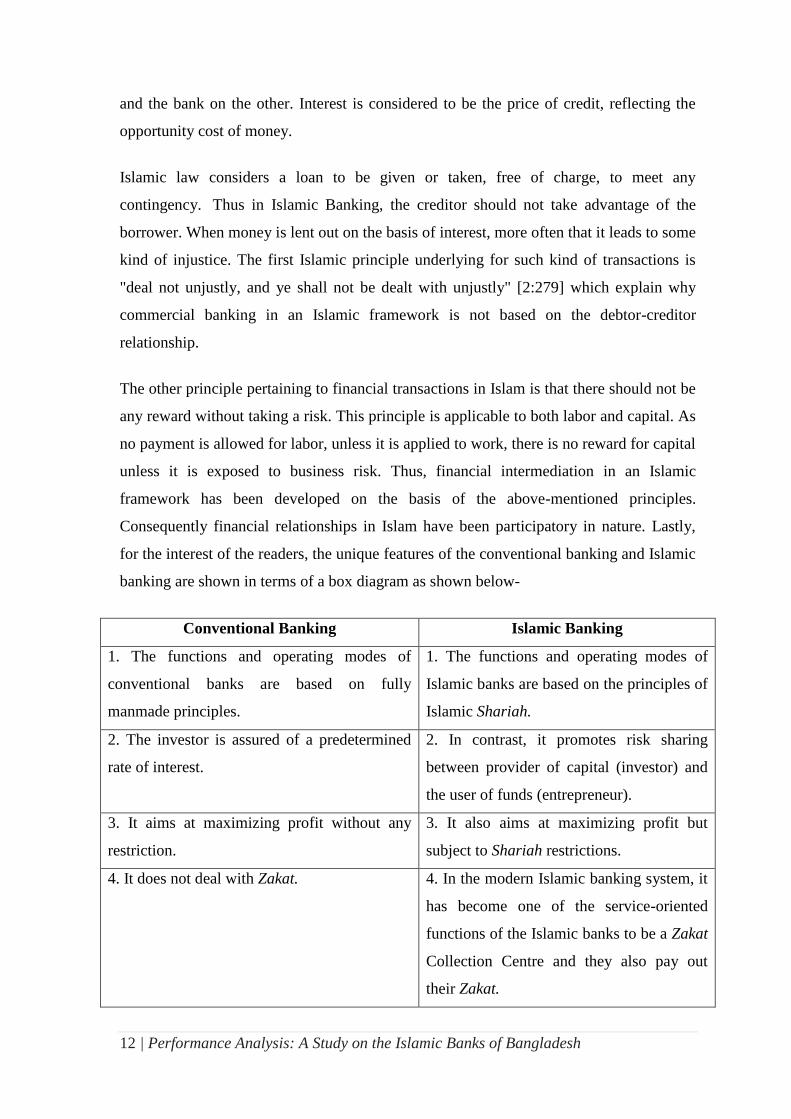

Conventional Banking Islamic Banking

1. The functions and operating modes of

conventional banks are based on fully

manmade principles.

1. The functions and operating modes of

Islamic banks are based on the principles of

Islamic Shariah.

2. The investor is assured of a predetermined

rate of interest.

2. In contrast, it promotes risk sharing

between provider of capital (investor) and

the user of funds (entrepreneur).

3. It aims at maximizing profit without any

restriction.

3. It also aims at maximizing profit but

subject to Shariah restrictions.

4. It does not deal with Zakat. 4. In the modern Islamic banking system, it

has become one of the service-oriented

functions of the Islamic banks to be a Zakat

Collection Centre and they also pay out

their Zakat.

13 | Performance Analysis: A Study on the Islamic Banks of Bangladesh

Conventional Banking Islamic Banking

5. Lending money and getting it back with

compounding interest is the fundamental

function of the conventional banks.

5. Participation in partnership business is

the fundamental function of the Islamic

banks. So we have to understand our

customer's business very well.

6. It can charge additional money (penalty and

compounded interest) in case of defaulters.

6. The Islamic banks have no provision to

charge any extra money from the

defaulters. Only small amount of

compensation and these proceeds is given

to charity. Rebates are given for early

settlement at the Bank's discretion.

7. Very often it results in the bank's own

interest becoming prominent. It makes no

effort to ensure growth with equity.

7. It gives due importance to the public

interest. Its ultimate aim is to ensure growth

with equity.

8. For interest-based commercial banks,

borrowing from the money market is relatively

easier.

8. For the Islamic banks, it must be based

on a Shariah approved underlying

transaction.

9. Since income from the advances is fixed, it

gives little importance to developing expertise

in project appraisal and evaluations.

9. Since it shares profit and loss, the Islamic

banks pay greater attention to developing

project appraisal and evaluations.

10. The conventional banks give greater

emphasis on credit-worthiness of the clients.

10. The Islamic banks, on the other hand,

give greater emphasis on the viability of the

projects.

11. The status of a conventional bank, in

relation to its clients, is that of creditor and

debtors.

11. The status of Islamic bank in relation to

its clients is that of partners, investors and

trader, buyer and seller.

12. A conventional bank has to guarantee all its

deposits.

12. Islamic bank can only guarantee

deposits for deposit account, which is based

on the principle of al-wadiah, thus the

depositors are guaranteed repayment of

their funds, however if the account is based

on the mudarabah concept, client have to

share in a loss position..

14 | Performance Analysis: A Study on the Islamic Banks of Bangladesh

In fine, the main difference between Islamic and conventional banking is that Islamic

teaching says that money itself has no intrinsic value, and forbids people from profiting

by lending it, without accepting a level of risk. wealth can only be generated through

legitimate trade and investment. Any gain relating to this trading are shared between the

person providing the capital and the person providing the expertise. In Islamic Banking

system, bank generates all of their profit through sharia‟a compliant trading and

investment activities and profits are shared with their customers at a pre-agreed ratio.

15 | Performance Analysis: A Study on the Islamic Banks of Bangladesh

CHAPTER 4: A BRIEF INTRODUCTION OF ISLAMIC

BANKS IN BANGLADESH

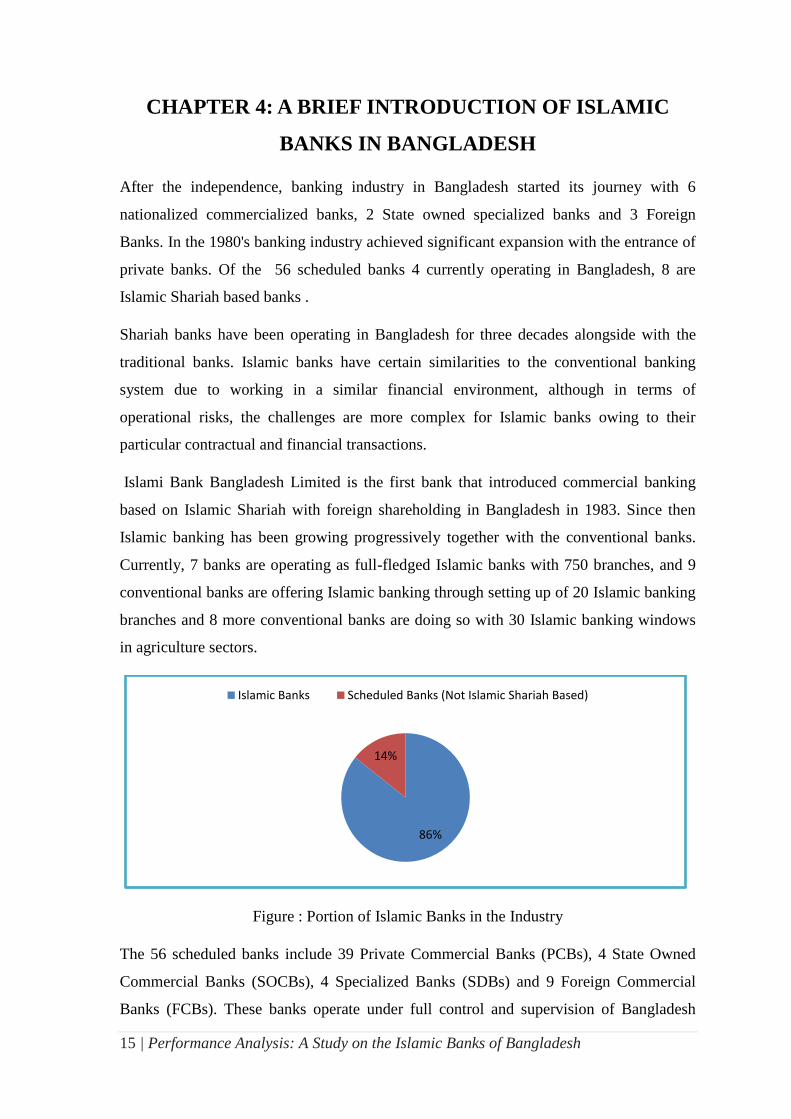

After the independence, banking industry in Bangladesh started its journey with 6

nationalized commercialized banks, 2 State owned specialized banks and 3 Foreign

Banks. In the 1980's banking industry achieved significant expansion with the entrance of

private banks. Of the 56 scheduled banks 4 currently operating in Bangladesh, 8 are

Islamic Shariah based banks .

Shariah banks have been operating in Bangladesh for three decades alongside with the

traditional banks. Islamic banks have certain similarities to the conventional banking

system due to working in a similar financial environment, although in terms of

operational risks, the challenges are more complex for Islamic banks owing to their

particular contractual and financial transactions.

Islami Bank Bangladesh Limited is the first bank that introduced commercial banking

based on Islamic Shariah with foreign shareholding in Bangladesh in 1983. Since then

Islamic banking has been growing progressively together with the conventional banks.

Currently, 7 banks are operating as full-fledged Islamic banks with 750 branches, and 9

conventional banks are offering Islamic banking through setting up of 20 Islamic banking

branches and 8 more conventional banks are doing so with 30 Islamic banking windows

in agriculture sectors.

Figure : Portion of Islamic Banks in the Industry

The 56 scheduled banks include 39 Private Commercial Banks (PCBs), 4 State Owned

Commercial Banks (SOCBs), 4 Specialized Banks (SDBs) and 9 Foreign Commercial

Banks (FCBs). These banks operate under full control and supervision of Bangladesh

86%

14%

Islamic Banks Scheduled Banks (Not Islamic Shariah Based)

16 | Performance Analysis: A Study on the Islamic Banks of Bangladesh

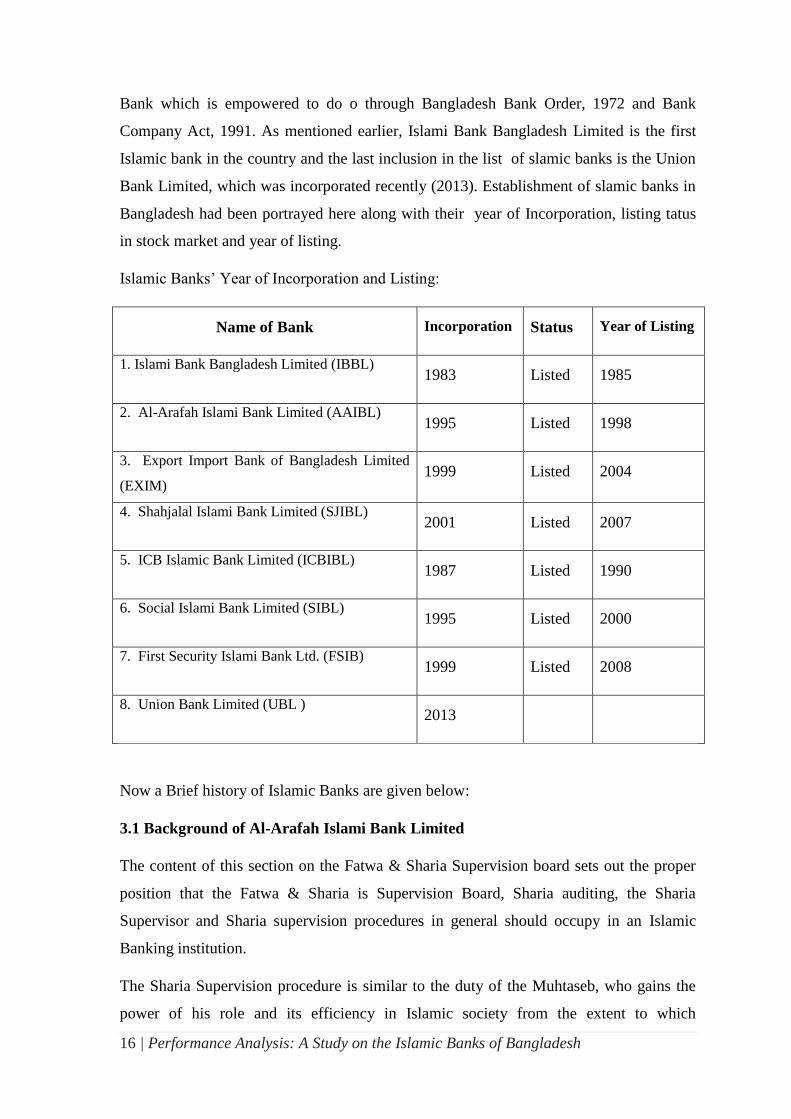

Bank which is empowered to do o through Bangladesh Bank Order, 1972 and Bank

Company Act, 1991. As mentioned earlier, Islami Bank Bangladesh Limited is the first

Islamic bank in the country and the last inclusion in the list of slamic banks is the Union

Bank Limited, which was incorporated recently (2013). Establishment of slamic banks in

Bangladesh had been portrayed here along with their year of Incorporation, listing tatus

in stock market and year of listing.

Islamic Banks‟ Year of Incorporation and Listing:

Name of Bank Incorporation Status Year of Listing

1. Islami Bank Bangladesh Limited (IBBL) 1983 Listed 1985

2. Al-Arafah Islami Bank Limited (AAIBL) 1995 Listed 1998

3. Export Import Bank of Bangladesh Limited

(EXIM) 1999 Listed 2004

4. Shahjalal Islami Bank Limited (SJIBL) 2001 Listed 2007

5. ICB Islamic Bank Limited (ICBIBL) 1987 Listed 1990

6. Social Islami Bank Limited (SIBL) 1995 Listed 2000

7. First Security Islami Bank Ltd. (FSIB) 1999 Listed 2008

8. Union Bank Limited (UBL ) 2013

Now a Brief history of Islamic Banks are given below:

3.1 Background of Al-Arafah Islami Bank Limited

The content of this section on the Fatwa & Sharia Supervision board sets out the proper

position that the Fatwa & Sharia is Supervision Board, Sharia auditing, the Sharia

Supervisor and Sharia supervision procedures in general should occupy in an Islamic

Banking institution.

The Sharia Supervision procedure is similar to the duty of the Muhtaseb, who gains the

power of his role and its efficiency in Islamic society from the extent to which

17 | Performance Analysis: A Study on the Islamic Banks of Bangladesh

compliance, efficiency, and support are provided by the Muslim leader and those of

equivalent status. Otherwise, the Muslim leader would become nothing more than a

trusted adviser who directs to virtue and prohibits wrongdoing. (Whoever believes, it is

for that person's benefit, and whoever misbelieves, it is to that person's account)

3.2 Background of Export Import Bank of Bangladesh Limited

Export Import Bank of Bangladesh Limited was established in the year 1999 under the

leadership of Late Mr. Shahjahan Kabir, Founder Chairman who had a long dream of

floating a commercial bank which would contribute to the socio-economic development

of our country. He had a long experience as a good banker.The Bank starts functioning

from 3rd August, 1999 with its name as Bengal Export Import Bank Limited. On 16th

November 1999, it was renamed as Export Import Bank of Bangladesh Limited with Mr.

Alamgir Kabir as the Founder Advisor and Mr. Mohammad Lakiotullah as the Founder

Managing Director respectively.

3.3 Background of ICB Islamic Bank

The Bank has been incorporated on April, 1987 as a public limited company under the

Companies Act, 1913 to undertake and carry out all kinds of banking, financial and

business activities, transactions and operations in strict compliance with the principles of

Islamic Law (Shariah) relating to business activities in particular avoiding usury in

credit and sales transactions and any practice which amounts to usury. Certificate for

commencement of business has been issued to the bank on April, 30, 1987. The Bank has

been authorized by the Bangladesh Bank to carry on the banking business in Bangladesh

with effect from May 4, 1987. However, actual banking operations commenced on May

20, 1987.

3.4 Background of Islami Bank Bangladesh Limited

Islami Bank Bangladesh Limited is a Joint Venture Public Limited Company engaged in

commercial banking business based on Islamic Shari'ah with 63.09% foreign

shareholding having largest branch network ( total 286 Branches) among the private

sector Banks in Bangladesh. It was established on the 13th March 1983 as the first

Islamic Bank in the South East Asia.It is listed with Dhaka Stock Exchange Ltd. and

Chittagong Stock Exchange Ltd. Authorized Capital of the Bank is Tk. 20,000.00 Million

18 | Performance Analysis: A Study on the Islamic Banks of Bangladesh

and Paid-up Capital is Tk. 14,636.28 Million having 33,686 shareholders as on 31st

December 2013.

3.5 Background of Shahjalal Islami Bank Limited

Shahjalal Islami Bank Limited (SJIBL) commenced its commercial operation in

accordance with principle of Islamic Shariah on the 10th May 2001 under the Bank

Companies Act, 1991. During last thirteen years SJIBL has diversified its service

coverage by opening new branches at different strategically important locations across the

country offering various service products both investment & deposit. Islamic Banking, in

essence, is not only INTEREST-FREE banking business, it carries deal wise business

product thereby generating real income and thus boosting GDP of the economy. Board of

Directors enjoys high credential in the business arena of the country, Management Team

is strong and supportive equipped with excellent professional knowledge under leadership

of a veteran Banker Mr. Farman R. Chowdhury.

3.6 Background of Social Islami Bank Limited

The SOCIAL ISLAMI BANK LTD (SIBL), a second-generation bank, operating since 22

November, 1995 based on Shariah Principles, has now 94 branches all over the country

with two subsidiary companies - SIBL Securities Ltd. & SIBL Investment Ltd. Targeting

poverty, SOCIAL ISLAMI BANK LTD. is indeed a concept of 21st century participatory

three sector banking model in one. in the formal sector, it works as an Islamic

participatory Commercial Bank with human face approach to credit and banking on the

profit and loss sharing: it is a Non-formal banking with informal finance and credit

package that empowers and humanizes real poor family and create local income

opportunities and discourages internal migration; it is a Development Bank intended to

monetize the voluntary sector and management of Waqf, Mosque properties and

introducing cash Waqf system for the first time in the history.

19 | Performance Analysis: A Study on the Islamic Banks of Bangladesh

CHAPTER 5: INVESTMENT MECHANISM OF ISLAMIC

BANKS

Investment operation of a Bank is vital importance the greatest share of total revenue is

generated from it, maximum risk is centered in it and the very existence of a Bank mostly

depends on prudent management of its investment Port-folio.

As such, for efficient deployment of mobilized resources in profitable, safe and liquid

investments, a sound, well-defined, well-planned and appropriate Investment Policy

framework is necessary prerequisite for achieving the goal of the Bank.

The special feature of the investment policy of islamic Banks is to invest on the basis of

profit-loss sharing system in accordance with the tenets and principles of lslami Shariah.

Earning of profit is not the only motive and objective of the Bank‟s investment policy

rather emphasis is given in attaining social good and in creating employment

opportunities.

Objectives and Principles of investment

The objectives and principles of investment operations of the Bank are:

To invest fund strictly in accordance with the principles of Islami Shariah.

To diversity its investment portfolio by size of investment, by sectors (public and

private) by economic purpose, by securities and by geographical area including

industrial, commercial & agricultural.

To ensure mutual benefit both for the Bank and the investment client by

professional appraisal of investment proposals, judicious sanction of investment

close and constant supervision and monitoring thereof.

To make investment keeping the socio economic requirement of the country in

view.

To increase the number of potential investors by making participatory and

productive investment.

20 | Performance Analysis: A Study on the Islamic Banks of Bangladesh

To finance various development schemes for poverty alleviation, income and

employment generation with a view to accelerate sustainable soico-economic

growth and for upliftment of the society.

To invest in the form of goods and commodities rather than give out cash money

to the investment clients.

To encourage social up liftman enterprises.

To shun even highly profitable investment in fields forbidden under Islamic

Shariah and are harmful for the society.

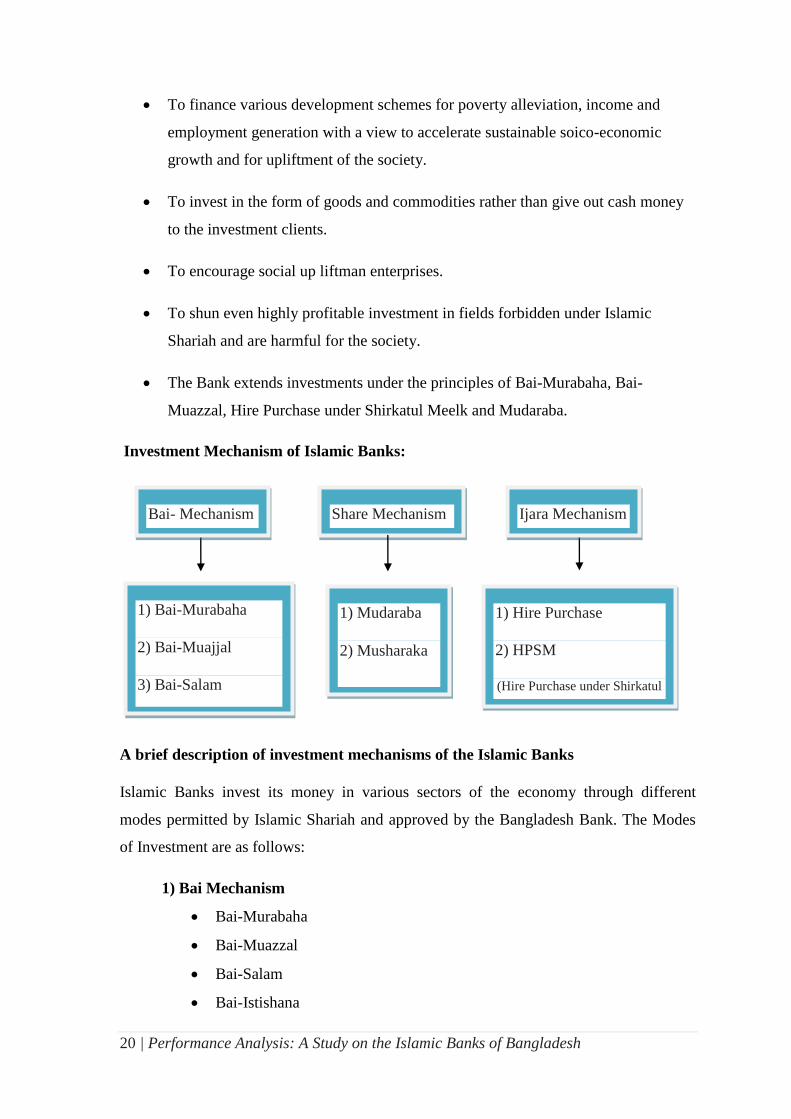

The Bank extends investments under the principles of Bai-Murabaha, Bai-

Muazzal, Hire Purchase under Shirkatul Meelk and Mudaraba.

Investment Mechanism of Islamic Banks:

A brief description of investment mechanisms of the Islamic Banks

Islamic Banks invest its money in various sectors of the economy through different

modes permitted by Islamic Shariah and approved by the Bangladesh Bank. The Modes

of Investment are as follows:

1) Bai Mechanism

Bai-Murabaha

Bai-Muazzal

Bai-Salam

Bai-Istishana

1) Mudaraba

2) Musharaka

1) Hire Purchase

2) HPSM

(Hire Purchase under Shirkatul

Melk)

Share Mechanism Ijara Mechanism Bai- Mechanism

1) Bai-Murabaha

2) Bai-Muajjal

3) Bai-Salam

4) Bai- Istisna‟a

3) Bai-Salam

4) Bai-Istishna‟a

21 | Performance Analysis: A Study on the Islamic Banks of Bangladesh

2) Ijara Mechanism

Hire Purchase (HP)

Hire Purchase under Shirkatul Melk (HPSM)

3) Shirkat Mechanism

Mudaraba

Musharaka

Bai-Mechanism

Bai-Murabaha

Bai- Murabaha may be defined as a contract between a buyer and a seller under which the

seller sells certain specific goods (permissible under Islamic Shariah and the law of the

land) to the buyer at a cost plus agreed profit payable in cash or on any fixed future data

in lump sum or by installments. The marked up profit may be fixed in lump sum or in

percentage of the cost price of the goods.

Important features:

It is permissible for the client to offer an order to purchase by the bank particular

goods deciding its specification and committing him to buy same from the bank

on murabaha, i.e. cost plus agreed upon profit.

It is permissible to make the promise binding upon the client to purchase from the

bank, that is, he is to satisfy the promise or to indemnify the damages caused by

breaking the promise without excuse.

It is also permissible to take cash / collateral security to guarantee the

implementation of the promise or indemnify the damages.

Stock availability of goods is a basic condition for signing a Bai-murabaha

agreement. Therefore, the bank must purchase the goods as per specification of

the client to acquire ownership of the same before signing the Bai-Murabaha

agreement with the Client.

After purchase of goods the Bank must bear the risk of goods until those are

actually sold and delivered to the Client, i.e., after purchase of the goods by the

Bank and before selling of those on Bai-Murabaha to the Client buyer, the bank

bear the consequences of any damages or defects, unless there is an agreement

22 | Performance Analysis: A Study on the Islamic Banks of Bangladesh

with the Client releasing the bank of the defects, that means, if the goods are

damaged, bank is liable, if the goods are defective, (a defect that is not included in

the release) the Bank bears the responsibility.

The Bank must deliver the specified Goods to the Client on specified date and at

specified place of delivery as per Contract.

The bank shall the goods at a higher price (Cost + {profit) to earn profit. The cost

of goods sold and profit markup therewith shall separately and clearly be

mentioned in the Bai-Murabaha agreement. The profit Mark-up may be mentioned

in lump sum or in percentage of the purchase/cost price of the goods. But, under

no circumstance, the percentage of the profit shall have any relation with time or

expressed in relation with time, such as per month, per annum etc.

The price once fixed as per agreement and deferred cannot be further increased.

It is permissible for the bank to authorize any third party to buy and receive the

goods on Bank behalf. The authorization must be in a separated contract.

Bai-Muazzal

Bai-Muajjal may be defined as a contract between a Buyer and a Seller under which the

Seller sells certain specific goods (permissible under Shariah and Law of the Country), to

the Buyer at an agreed fixed price payable at a certain fixed future date in lump sum or

within a fixed period by fixed instalments. The seller may also sell the goods purchased

by him as per order and specification of the Buyer.

In this Bank, Bai-Muajjal is treated as a contract between the Bank and the Client under

which the Bank sells to the Client certain specified goods, purchased as per order and

specification of the Client at an agreed price payable within a fixed future date in lump

sum or by fixed instalments.

Important features

It is permissible for the client to offer an order to purchase by the Bank particular goods

deciding its specification and committing him to buy the same from the Bank on Bai-

Muajjal i.e. deferred payment sale at fixed price.

It is permissible to make the promise binding upon the Client to purchase from the

Bank, that is, he is to either satisfy the promise or to indemnify the damages

caused by breaking the promise without excuse.

23 | Performance Analysis: A Study on the Islamic Banks of Bangladesh

It is permissible to take cash / collateral security to guarantee the implementation

of the promise or to indemnify the damages.

It is also permissible to document the debt resulting from Bai-Muajjal by a

Guarantor, or a mortgage. Or both like any other debt. Mortgage / Guarantee /

Cash security may be obtained prior to the signing of the Agreement or at the time

of signing the Agreement.

Stock and availability of goods is a basic condition for signing a Bai-Muajjal

Agreement, Therefore, the Bank must purchase the goods as per specification of

the Client to acquire ownership of the same before signing the Bai-Muajjal

Agreement with the Client.

After purchase of goods the Bank must bear the risk of goods until those are

actually delivered to the Client.

The Bank must deliver the specified Goods to the Client on specified date and at

specified place of delivery as per Contract.

The Bank may sell the goods at a higher price than the purchase price to earn

profit.

The price once fixed as per agreement and deferred cannot be further increased.

The Bank may sell the goods at one agreed price which will include both the cost

price and the profit. Unlike Bai-Murabaha, the Bank may not disclose the cost

price and the profit mark-up separately to the Client.

Bai-Salam

Bai-Salam may be defined as a contract between a Buyer and a Seller under which the

Seller sells in advance the certain commodity (ies)/ product(s) permissible under Islamic

Shariah and the law of the land to the Buyer at an agreed price payable on execution of

the said contract and the commodity (ies)/ product(s) is/ are delivered as per specification,

size, quality, quantity at a future time in a particular place.

In other words, Bai-Salam is a sale whereby the seller undertakes to supply some specific

Commodity (ies) /Product(s) to the buyer at a future time in exchange of an advanced

price fully paid on the spot. Here the price is paid in cash, but the delivery of the goods is

deferred.

24 | Performance Analysis: A Study on the Islamic Banks of Bangladesh

Important features

Bai-Salam is a mode of investment allowed by Islamic Shariah in which

commodity (ies)/product(s) can be sold without having the said commodity(ies)/

product(s) either in existence or physical/constructive possession of the seller.

If The commodity (ies)/product(s) are ready for sale, Bai-Salam is not allowed in

Shariah. Then the sale may be done either in Bai-Murabaha or Bai-Muajjal mode

of investment.

Generally, Industrial and Agricultural products are purchased/sold in advance

under Bai-Salam mode of Investment to infuse finance so that production is not

hindered due to shortage of fund/cash.

It is permissible to obtain collateral security from the seller client to secure the

investment from any hazards viz. non-supply/partial supply of

commodity(ies)/product(s), supply of low quality commodity(ies)/Product(s) etc.

It is also permissible to obtain Mortgage and/or Personal Guarantee from a third

party as security before the signing of the Agreement or at the time of signing the

Agreement.

Bai-Istishna’a

A contract between a manufacturer/seller and a buyer under which the

manufacturer/seller sells specific product(s) after having manufactured, permissible under

Islamic Shariah and Law of the Country after having manufactured at an agreed price

payable in advance or by installments within a fixed period or on/within a fixed future

date on the basis of the order placed by the buyer. In this contract the buyer is called „Al-

Mustasni‟, the seller „Al-Sani‟ and the goods or the subject matter of the contract „Al-

Masnoo‟.

If the ultimate buyer does not stipulate in the contract that the seller will manufacture the

product(s) by himself, then the seller may enter into a second Istisna'a contract in order to

fulfil his contractual obligations in the first contract. This new contract is known as

Parallel Istisna'a, whereby the obligations of the seller in the first contract are carried out.

Istisna’a in Islami Bank

Islami Bank can utilize Istisna'a in the following ways:

25 | Performance Analysis: A Study on the Islamic Banks of Bangladesh

Islami Bank may buy a commodity under Istisna'a contract and then sell it on cash

or deferred payment basis to a Client of the Bank without receiving prior order

from the Client.

Islami Bank in the capacity of a seller may receive order from a Client for

manufacturing and supplying certain specified goods under an Istisna'a contract

and then enter into a Parallel Istisna'a contract in the capacity of a buyer with a

Manufacturer for having the product(s) manufactured by him i.e. the Islami Bank

may obtain an order from a buyer to supply goods under the obligations of Islami

Bank as a „Seller‟ in the first contract and as a „Buyer‟ in parallel contract are as

under:

Islami Bank as a seller in the first contract will remain solely responsible

for the execution of its obligations as if the parallel contract is non-

existent. Hence, Islami Bank in the first contract would remain liable for

any default, negligence or breach of contract ensuing from the parallel

contract.

In the parallel Istisna'a, the Manufacturer is accountable to Islami Bank in

the way and manner by which he performs his obligations. He has no

direct legal relationship with the ultimate buyer in the first contract.

The second Istisna'a is a parallel contract, but not a contingent transaction

on the first contract. Legally speaking they are different contracts with

respect to rights and obligations.

The Islami Bank as a seller is liable to the ultimate Buyer with regard to

any mal-execution of the sub-contractor and any guarantees arising there

from. It is this very liability that justifies the validity of the Parallel

Istisna'a and which also justifies the charging of profit by the Islami Bank,

if any.

Rules and conditions

1. There must be a contract between the Manufacturer and the Buyer, which shall be

the principal instrument to govern the advance selling and buying under Istisna‟a.

2. The name, specification, brand, quantity, quality, size, etc. of the Product(s) must

be clearly specified in the Contract leaving no ambiguity.

26 | Performance Analysis: A Study on the Islamic Banks of Bangladesh

3. Unit price and total price of the product(s) must be fixed and mentioned in the

Contract.

4. The time and place of delivery should be mentioned in the contract.

5. Mode of transportation, transportation cost, storage charge/godown rent, insurance

etc., if any, should be specified in the Contract.

6. The name of party who will bear the cost of transportation, storage

charge/godown rent, insurance etc. also be mentioned in the contract.

7. The seller shall remain responsible for quantity, quality, and specification of the

product(s) till physical/constructive delivery of the same to the buyer.

8. Under Istisna'a transaction advance payment of price of the Product(s) under order

is not compulsory. The Buyer may pay the price of the goods in advance in full or

part as agreed upon, which should be clearly mentioned in the contract.

9. Remaining price if any, may be paid after receipt of the Product(s) or at any future

date(s) or in installments, if so agreed, and mentioned in the contract.

10. After taking delivery of the Product(s), the Buyer shall be the owner and shall

bear all risks till disposal / sale of the Product(s).

Important features of Istisna’a

Istisna'a is an exceptional mode of investment allowed by Islamic Shariah in

which product(s) can be sold without having the same in existence. If the

product(s) are ready for sale, Istisna'a is not allowed in Shariah. Then the sale may

be done either in Bai-Murabaha or Bai-Muajjal mode of investment. In this mode,

deliveries of goods are deferred and payment of price may also be deferred.

It facilitates the manufacturer sometimes to get the price of the goods in advance,

which he may use as capital for producing the goods.

It gives the buyer opportunity to pay the price in some future dates or by

installments.

It is a binding contract and no party is allowed to cancel the Istisna'a contract after

the price is paid and received in full or in part or the manufacturer starts the work.

Istisna'a is specially practiced in Manufacturing and Industrial sectors. However,

it can be practiced in agricultural and constructions sectors also.

27 | Performance Analysis: A Study on the Islamic Banks of Bangladesh

2. Ijara Mechanism

Hire purchase

It is practiced for procurement of goods which are mainly of fixed nature. Here purchaser

purchases the assets from the seller by paying the price gradually or in lump sum after the

rent period and pay for the assets up until making the full payment.

In this type of contract the hire has the full ownership of the goods. The ownership is only

transferred to the hirer after the price of the goods is fully paid to the Bank. It means

ownership has to be manually transferred in this type of contract. Up until ownership of

the assets is transferred the client has to pay a fixed rental to the Bank according to the

schedule specified in the contract.

Hire Purchase under Shirkatul Melk

Hire Purchase under Shirkatul Melk is a Special type of contract which has been

developed through practice. Actually, it is a synthesis of three contracts:

1. Shirkat

2. Ijarah; and

3. Sale

Shirkat

Shirkat means partnership and Shirkatul Melk means share in ownership. When two or

more persons supply equity, purchase an asset, own the same jointly, and share the

benefit as per agreement and bear the loss in proportion to their respective equity, the

contract is called Shirkatul Melk contract.

Ijara

Ijarah has been defined as a contract between two parties, the Hiree and Hirer where the

Hirer enjoys or reaps a specific service or benefit against a specified consideration or rent

from the asset owned by the Hiree.

Sale

Sale is a sale contract against which the buyer gets the ownership of the goods from the

seller by paying agreed upon price or by agreeing to pay the price at a later date.

28 | Performance Analysis: A Study on the Islamic Banks of Bangladesh

Thus, in Hire Purchase under Shirkatul Melk mode both the Bank and the Client supply

equity in equal or unequal proportion for purchase of an asset like land, building,

machinery, transports etc. Purchase the asset with that equity money, own the same

jointly, share the benefit as per agreement and bear the loss in proportion to their

respective equity. The share, part or portion of the asset owned by the Bank is hired out to

the Client partner for a fixed rent per unit of time for a fixed period. Lastly the Bank sells

and transfers the ownership of its share / part / portion to the Client against payment of

price fixed for that part either gradually part by part or in lump sum within the hire period

or after the expiry of the hire agreement.

3. Share Mechanism

Mudaraba

Mudaraba is a partnership in profit whereby one party provides capital and the other party

provides skill and labour. The provider of capital is called "Shahib Al-Maal" while the

provider of skill and labour is called "Mudarib".

So, Mudaraba may be defined as a contract of partnership where the Shahib al-maal

provides capital to the Mudarib for investing it in a commercial enterprise by applying his

labour and endeavor. Both the parties share the profit as per agreed upon ratio and the

losses, if any, being borne by the provider of funds i.e. Shahib al-maal except if it is due

to breach of trust i.e. misconduct, negligence or violation of the conditions agreed upon

by the Mudarib. If there is any loss incurred due to the reasons mentioned above, the

Mudarib becomes liable for that.

Musharaka

Musharaka may be defined as a contract of partnership between two or more individuals

or bodies in which all the partners contribute capital, participate in the management, and

share the profit in proportion to their capital or as per pre-agreed ratio and bear the loss, if

any, in proportion to their capital/equity ratio.

In Islami Bank Bangladesh Limited (IBBL), the Bank may take part in a business with its

Client(s), where both the Client(s) and the Bank provide capital in fixed proportions, take

part in the management of business and share the profit in proportion to their respective

capital ratio or at pre-agreed ratio and bear the loss, if any, in proportion to their

respective capital/equity ratio.

29 | Performance Analysis: A Study on the Islamic Banks of Bangladesh

CHAPTER 6: PERFORMANCE ANALYSIS AND

DISCUSSION

5.1 Amounts of deposit and total asset of Islamic Banks

This line chart shows the total deposit & total asset of Islamic banks from year 2010 to

year 2013. Both the line has increasing trend. . In FY 2010 the deposit and total asset

amount was 617.1 million respectively and reached at1133.60 and 1359 million

respectively in five years.

5.2 Amounts of Investments of Islamic Banks

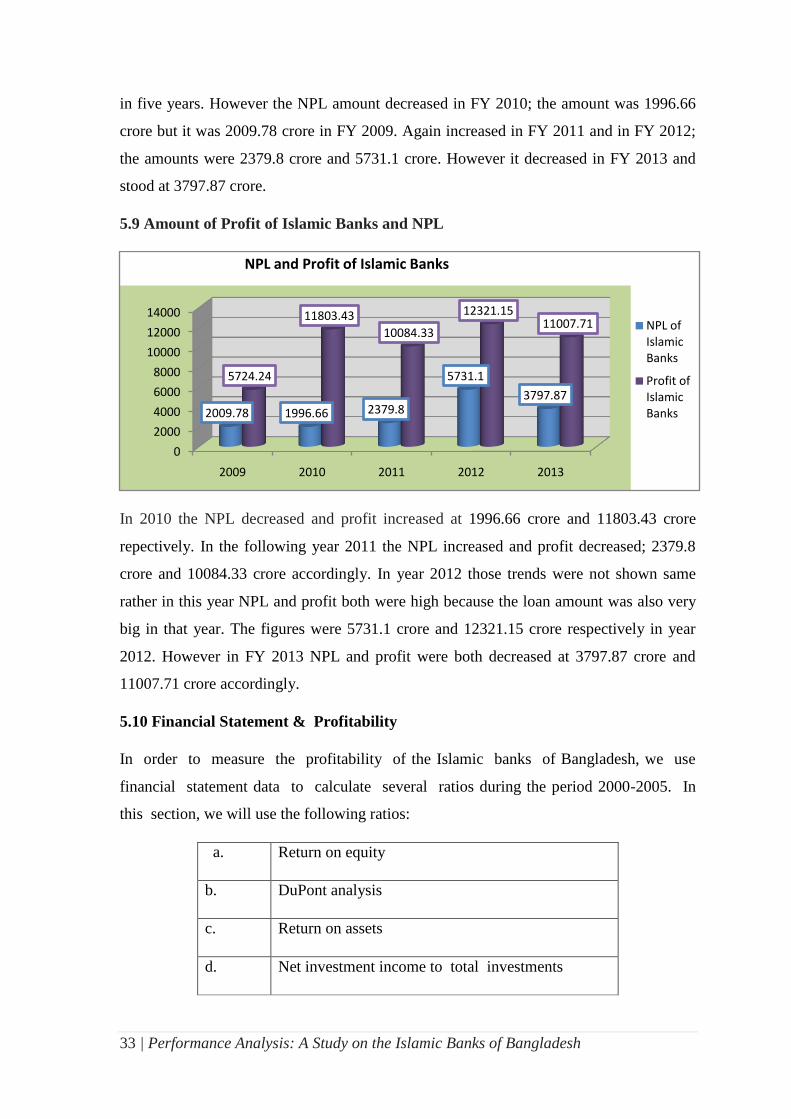

In Islamic banks the investment amount was also increasing every year in these six years.

Here it is clear that Islamic banks are extending their business in Bangladesh banking

industry. In FY 2009 the investment amount was 44204.38 crore and that reached at

103959.843 crore in five years.

0

500

1000

1500

2000

2500

3000

2010 2011 2012 2013

Deposit and total asset

Total deposit

Total asset

0

20000

40000

60000

80000

100000

120000

2008 20092010

20112012

2013

32157.9444204.3857426.04

70144.548 81765.142

103959.843

Total Investments of Islamic Banks

30 | Performance Analysis: A Study on the Islamic Banks of Bangladesh

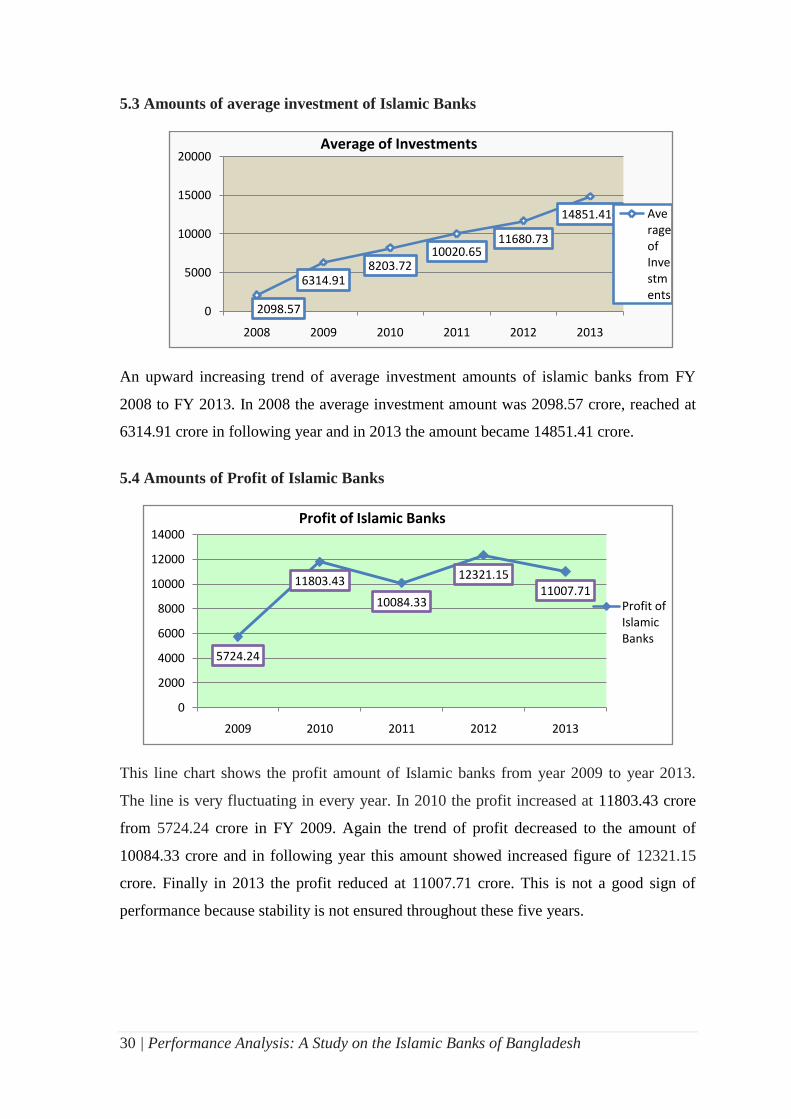

5.3 Amounts of average investment of Islamic Banks

An upward increasing trend of average investment amounts of islamic banks from FY

2008 to FY 2013. In 2008 the average investment amount was 2098.57 crore, reached at

6314.91 crore in following year and in 2013 the amount became 14851.41 crore.

5.4 Amounts of Profit of Islamic Banks

This line chart shows the profit amount of Islamic banks from year 2009 to year 2013.

The line is very fluctuating in every year. In 2010 the profit increased at 11803.43 crore

from 5724.24 crore in FY 2009. Again the trend of profit decreased to the amount of

10084.33 crore and in following year this amount showed increased figure of 12321.15

crore. Finally in 2013 the profit reduced at 11007.71 crore. This is not a good sign of

performance because stability is not ensured throughout these five years.

2098.57

6314.918203.72

10020.6511680.73

14851.414

0

5000

10000

15000

20000

2008 2009 2010 2011 2012 2013

Average of Investments

Average of Investments

5724.24

11803.43

10084.33

12321.1511007.71

0

2000

4000

6000

8000

10000

12000

14000

2009 2010 2011 2012 2013

Profit of Islamic Banks

Profit of Islamic Banks

31 | Performance Analysis: A Study on the Islamic Banks of Bangladesh

5.5 Average Profit in Islamic Banks

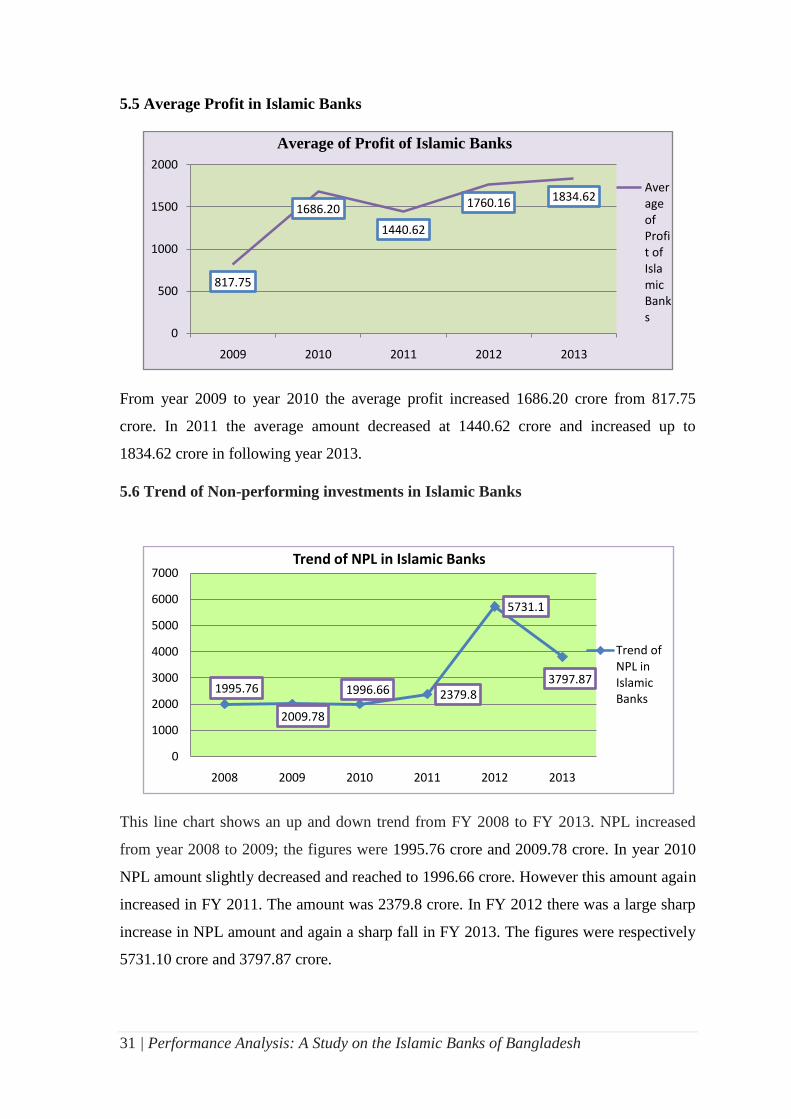

From year 2009 to year 2010 the average profit increased 1686.20 crore from 817.75

crore. In 2011 the average amount decreased at 1440.62 crore and increased up to

1834.62 crore in following year 2013.

5.6 Trend of Non-performing investments in Islamic Banks

This line chart shows an up and down trend from FY 2008 to FY 2013. NPL increased

from year 2008 to 2009; the figures were 1995.76 crore and 2009.78 crore. In year 2010

NPL amount slightly decreased and reached to 1996.66 crore. However this amount again

increased in FY 2011. The amount was 2379.8 crore. In FY 2012 there was a large sharp

increase in NPL amount and again a sharp fall in FY 2013. The figures were respectively

5731.10 crore and 3797.87 crore.

817.75

1686.20

1440.62

1760.16 1834.62

0

500

1000

1500

2000

2009 2010 2011 2012 2013

Average of Profit of Islamic Banks

Average of Profit of Islamic Banks

1995.76

2009.78

1996.66 2379.8

5731.1

3797.87

0

1000

2000

3000

4000

5000

6000

7000

2008 2009 2010 2011 2012 2013

Trend of NPL in Islamic Banks

Trend of NPL in Islamic Banks

32 | Performance Analysis: A Study on the Islamic Banks of Bangladesh

In Islamic banks NPL trend is fluctuating from 2008 to 2013. Among these six years the

NPL was the highest in FY 2012 and the second highest was in FY 2013; this means that

in these two years Islamic banks‟ investment performance was not so good.

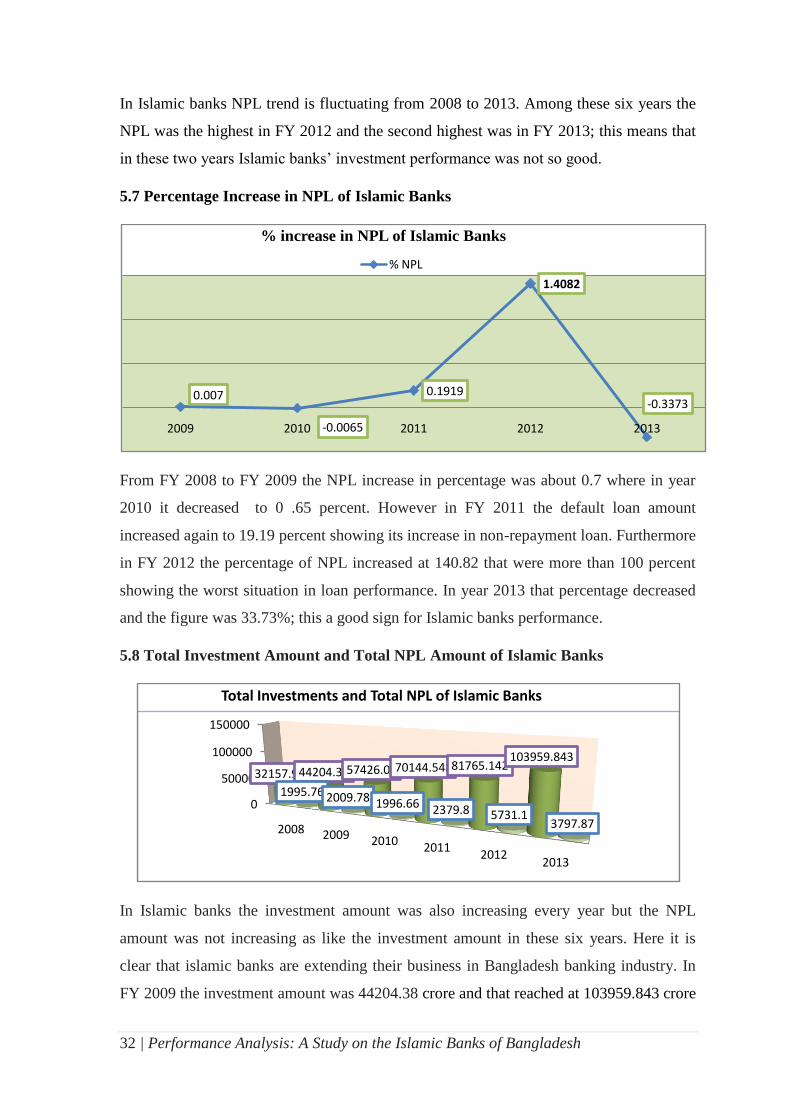

5.7 Percentage Increase in NPL of Islamic Banks

From FY 2008 to FY 2009 the NPL increase in percentage was about 0.7 where in year

2010 it decreased to 0 .65 percent. However in FY 2011 the default loan amount

increased again to 19.19 percent showing its increase in non-repayment loan. Furthermore

in FY 2012 the percentage of NPL increased at 140.82 that were more than 100 percent

showing the worst situation in loan performance. In year 2013 that percentage decreased

and the figure was 33.73%; this a good sign for Islamic banks performance.

5.8 Total Investment Amount and Total NPL Amount of Islamic Banks

In Islamic banks the investment amount was also increasing every year but the NPL

amount was not increasing as like the investment amount in these six years. Here it is

clear that islamic banks are extending their business in Bangladesh banking industry. In

FY 2009 the investment amount was 44204.38 crore and that reached at 103959.843 crore

0.007

-0.0065

0.1919

1.4082

-0.3373

2009 2010 2011 2012 2013

% increase in NPL of Islamic Banks

% NPL

0

50000

100000

150000

2008 2009 2010 20112012

2013

32157.9444204.3857426.0470144.54881765.142103959.843

1995.76 2009.78 1996.66 2379.8 5731.13797.87

Total Investments and Total NPL of Islamic Banks

33 | Performance Analysis: A Study on the Islamic Banks of Bangladesh

in five years. However the NPL amount decreased in FY 2010; the amount was 1996.66

crore but it was 2009.78 crore in FY 2009. Again increased in FY 2011 and in FY 2012;

the amounts were 2379.8 crore and 5731.1 crore. However it decreased in FY 2013 and

stood at 3797.87 crore.

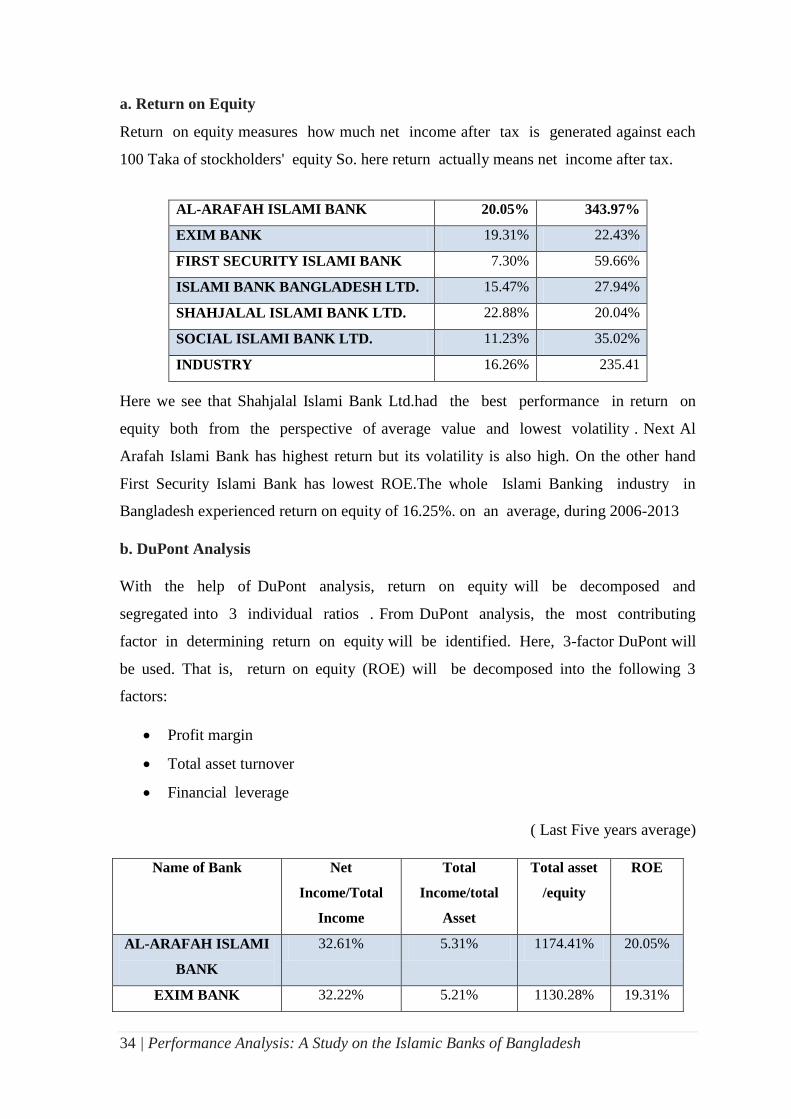

5.9 Amount of Profit of Islamic Banks and NPL

In 2010 the NPL decreased and profit increased at 1996.66 crore and 11803.43 crore

repectively. In the following year 2011 the NPL increased and profit decreased; 2379.8

crore and 10084.33 crore accordingly. In year 2012 those trends were not shown same

rather in this year NPL and profit both were high because the loan amount was also very

big in that year. The figures were 5731.1 crore and 12321.15 crore respectively in year

2012. However in FY 2013 NPL and profit were both decreased at 3797.87 crore and

11007.71 crore accordingly.

5.10 Financial Statement & Profitability

In order to measure the profitability of the Islamic banks of Bangladesh, we use

financial statement data to calculate several ratios during the period 2000-2005. In

this section, we will use the following ratios:

a. Return on equity

b. DuPont analysis

c. Return on assets

d. Net investment income to total investments

0

2000

4000

6000

8000

10000

12000

14000

2009 2010 2011 2012 2013

2009.78 1996.66 2379.8

5731.1

3797.87

5724.24

11803.43

10084.33

12321.1511007.71

NPL and Profit of Islamic Banks

NPL of Islamic Banks

Profit of Islamic Banks

34 | Performance Analysis: A Study on the Islamic Banks of Bangladesh

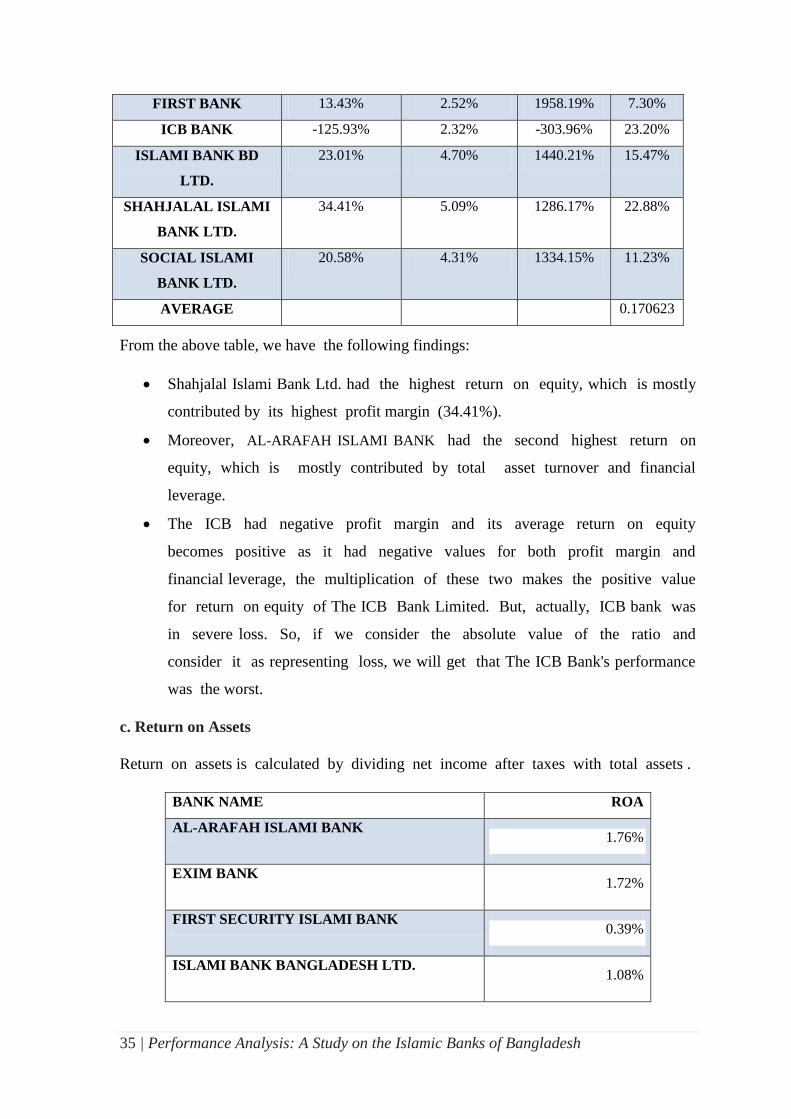

a. Return on Equity

Return on equity measures how much net income after tax is generated against each

100 Taka of stockholders' equity So. here return actually means net income after tax.

AL-ARAFAH ISLAMI BANK 20.05% 343.97%

EXIM BANK 19.31% 22.43%

FIRST SECURITY ISLAMI BANK 7.30% 59.66%

ISLAMI BANK BANGLADESH LTD. 15.47% 27.94%

SHAHJALAL ISLAMI BANK LTD. 22.88% 20.04%

SOCIAL ISLAMI BANK LTD. 11.23% 35.02%

INDUSTRY 16.26% 235.41

Here we see that Shahjalal Islami Bank Ltd.had the best performance in return on

equity both from the perspective of average value and lowest volatility . Next Al

Arafah Islami Bank has highest return but its volatility is also high. On the other hand

First Security Islami Bank has lowest ROE.The whole Islami Banking industry in

Bangladesh experienced return on equity of 16.25%. on an average, during 2006-2013

b. DuPont Analysis

With the help of DuPont analysis, return on equity will be decomposed and

segregated into 3 individual ratios . From DuPont analysis, the most contributing

factor in determining return on equity will be identified. Here, 3-factor DuPont will

be used. That is, return on equity (ROE) will be decomposed into the following 3

factors:

Profit margin

Total asset turnover

Financial leverage

( Last Five years average)

Name of Bank Net

Income/Total

Income

Total

Income/total

Asset

Total asset

/equity

ROE

AL-ARAFAH ISLAMI

BANK

32.61% 5.31% 1174.41% 20.05%

EXIM BANK 32.22% 5.21% 1130.28% 19.31%

35 | Performance Analysis: A Study on the Islamic Banks of Bangladesh

FIRST BANK 13.43% 2.52% 1958.19% 7.30%

ICB BANK -125.93% 2.32% -303.96% 23.20%

ISLAMI BANK BD

LTD.

23.01% 4.70% 1440.21% 15.47%

SHAHJALAL ISLAMI

BANK LTD.

34.41% 5.09% 1286.17% 22.88%

SOCIAL ISLAMI

BANK LTD.

20.58% 4.31% 1334.15% 11.23%

AVERAGE 0.170623

From the above table, we have the following findings:

Shahjalal Islami Bank Ltd. had the highest return on equity, which is mostly

contributed by its highest profit margin (34.41%).

Moreover, AL-ARAFAH ISLAMI BANK had the second highest return on

equity, which is mostly contributed by total asset turnover and financial

leverage.

The ICB had negative profit margin and its average return on equity

becomes positive as it had negative values for both profit margin and

financial leverage, the multiplication of these two makes the positive value

for return on equity of The ICB Bank Limited. But, actually, ICB bank was

in severe loss. So, if we consider the absolute value of the ratio and

consider it as representing loss, we will get that The ICB Bank's performance

was the worst.

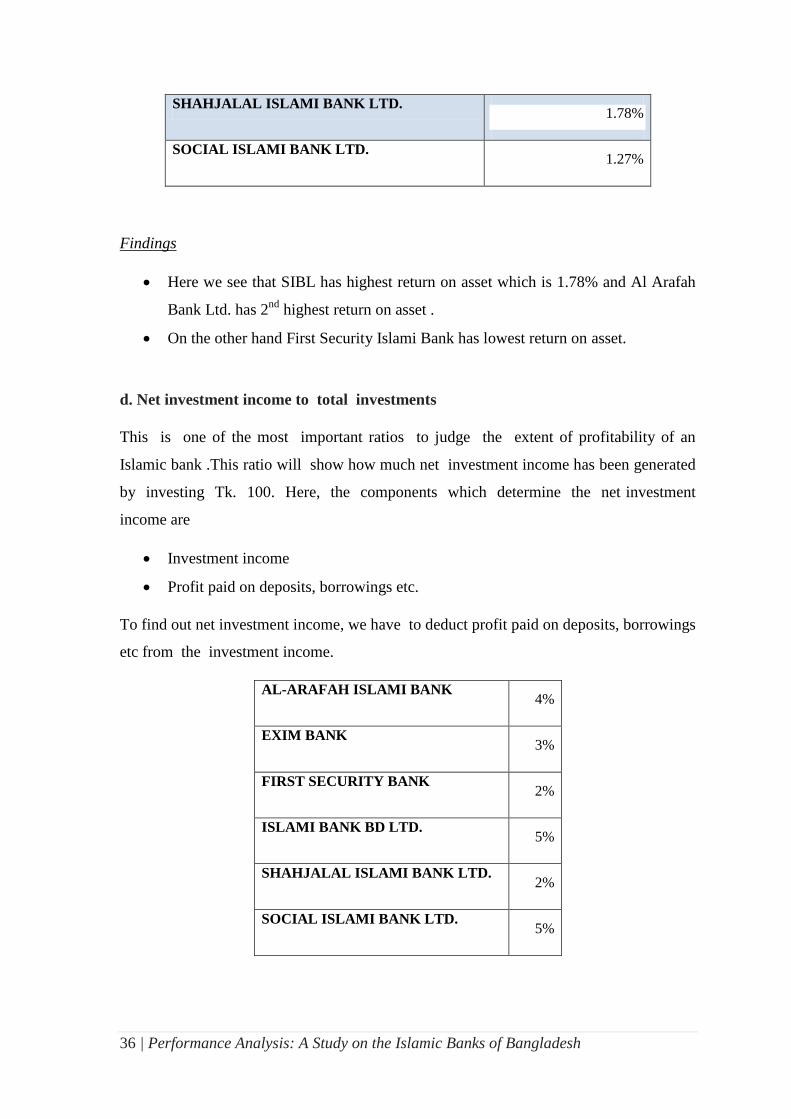

c. Return on Assets

Return on assets is calculated by dividing net income after taxes with total assets .

BANK NAME ROA

AL-ARAFAH ISLAMI BANK 1.76%

EXIM BANK 1.72%

FIRST SECURITY ISLAMI BANK 0.39%

ISLAMI BANK BANGLADESH LTD. 1.08%

36 | Performance Analysis: A Study on the Islamic Banks of Bangladesh

SHAHJALAL ISLAMI BANK LTD. 1.78%

SOCIAL ISLAMI BANK LTD. 1.27%

Findings

Here we see that SIBL has highest return on asset which is 1.78% and Al Arafah

Bank Ltd. has 2nd

highest return on asset .

On the other hand First Security Islami Bank has lowest return on asset.

d. Net investment income to total investments

This is one of the most important ratios to judge the extent of profitability of an

Islamic bank .This ratio will show how much net investment income has been generated

by investing Tk. 100. Here, the components which determine the net investment

income are

Investment income

Profit paid on deposits, borrowings etc.

To find out net investment income, we have to deduct profit paid on deposits, borrowings

etc from the investment income.

AL-ARAFAH ISLAMI BANK 4%

EXIM BANK 3%

FIRST SECURITY BANK 2%

ISLAMI BANK BD LTD. 5%

SHAHJALAL ISLAMI BANK LTD. 2%

SOCIAL ISLAMI BANK LTD. 5%

37 | Performance Analysis: A Study on the Islamic Banks of Bangladesh

Islami Bank Bangladesh Limited& Social Investment Bank Limited (SIBL had the

highest average ratio (5%) for this period (2006-2013). Al Arafah Islami Bank Ltd had

got the second position in this case.

From financial & profitability analysis we can conclude that although IBBL ranks 1st

position in terms of deposit mobilization and investment of fund but in terms of ROE,

ROA and net investment income to total investment income SIBL had got the 1st position

and then Al Arafah Bank Ltd had got the 2nd

position.

38 | Performance Analysis: A Study on the Islamic Banks of Bangladesh

CHAPTER 7: COMPERATIVE ANALYSIS OF

CONVENTIONAL AND ISLAMIC BANKS

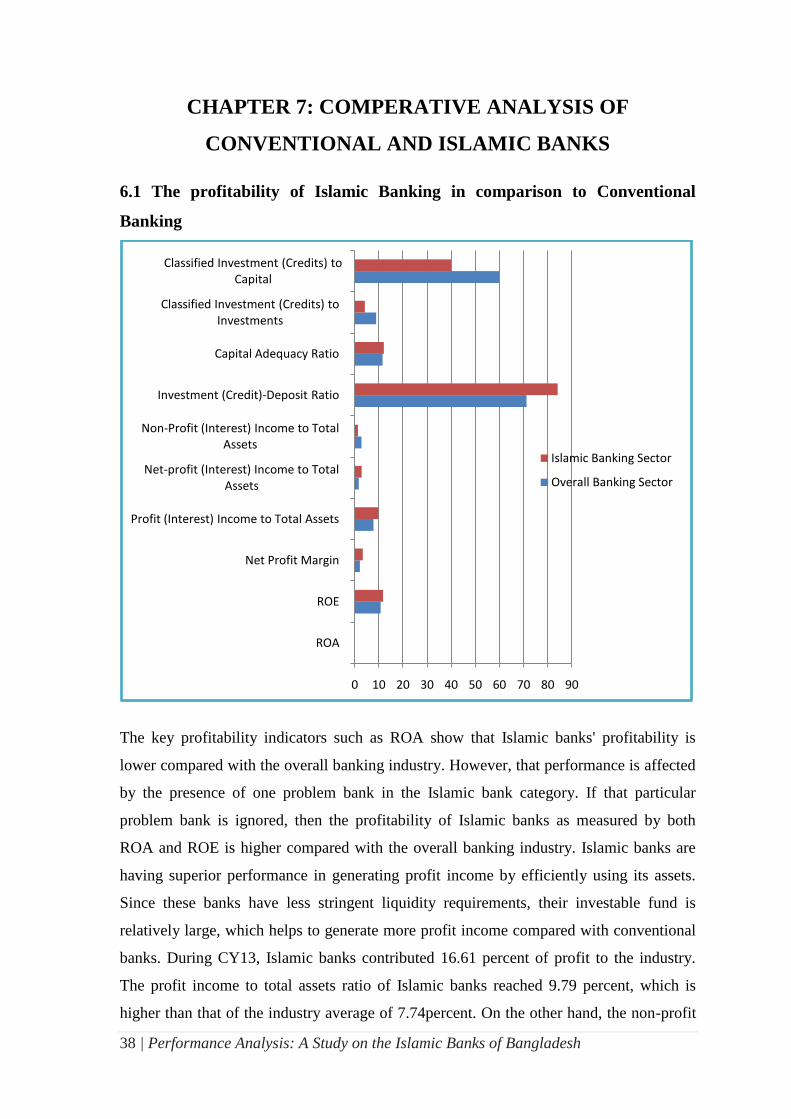

6.1 The profitability of Islamic Banking in comparison to Conventional

Banking

The key profitability indicators such as ROA show that Islamic banks' profitability is

lower compared with the overall banking industry. However, that performance is affected

by the presence of one problem bank in the Islamic bank category. If that particular

problem bank is ignored, then the profitability of Islamic banks as measured by both

ROA and ROE is higher compared with the overall banking industry. Islamic banks are

having superior performance in generating profit income by efficiently using its assets.

Since these banks have less stringent liquidity requirements, their investable fund is

relatively large, which helps to generate more profit income compared with conventional

banks. During CY13, Islamic banks contributed 16.61 percent of profit to the industry.

The profit income to total assets ratio of Islamic banks reached 9.79 percent, which is

higher than that of the industry average of 7.74percent. On the other hand, the non-profit

0 10 20 30 40 50 60 70 80 90

ROA

ROE

Net Profit Margin

Profit (Interest) Income to Total Assets

Net-profit (Interest) Income to Total Assets

Non-Profit (Interest) Income to Total Assets

Investment (Credit)-Deposit Ratio

Capital Adequacy Ratio

Classified Investment (Credits) to Investments

Classified Investment (Credits) to Capital

Islamic Banking Sector

Overall Banking Sector

39 | Performance Analysis: A Study on the Islamic Banks of Bangladesh

income to total assets ratio was only 1.3 percent as compared with the industrial average

of 2.75 percent, representing comparatively lower income from off-balance sheet

transactions and service and fee-based incomes. The ROA of the Islamic banking industry

is lower at 0.89 compared with the overall banking industry of 0.90 in CY13, indicating a

relatively inefficient use of assets by the Shari'ah compliant banks. The relative

inefficiency might be due to the outlier values of one problem bank. If one problem bank

is excluded from the set of Islamic banks, the other Islamic banks as a whole

outperformed the overall banking industry. The ROE of the Islamic banking industry, on

the other hand, stands at 11.71 percent, which is higher than that of the overall banking

industry ROE of 10.70 percent in CY13, indicating the earnings of Islamic banks were

higher compared with their equity position. However, part of it may be due to the

negative equity of an Islamic bank which has been operating under the restructuring

program of Bangladesh Bank. Non-performing investment, the ratio of classified

investment to total investment of Islamic banks, is only 4.2 percent, whereas for the

overall banking industry it is 8.9 percent. However, if only domestic private banks are

considered then the ratio drops to 4.54 percent which indicates that Islamic banks have

only slightly less NPL compared with their closest peer group. Classified investment to

total capital for Islamic banks is 39 percent, while it is 59.8 percent for conventional

banks. These indicators may show better investment management by the Islamic banks in

Bangladesh.

6.2 Market Share of Islamic Banks

Although the Islamic banking industry has been growing faster than the conventional

banks, Shari'ah banks are still a minor proportion of the total banking sector. Compared

with the overall banking industry, the combined share of Islamic banks (excluding

Islamic banking branches/windows of conventional banks) is17 percent in assets, 20.7

percent in investments 18 percent in deposits, 15.2 percent in equity and 17.2 percent in

liabilities as of end-December 2013. There has been a slight increase in most of the ratios

in 2013. Despite the inception of 9 new banks most of which are conventional banks, the

Islamic banks increased their market share in the banking industry.

40 | Performance Analysis: A Study on the Islamic Banks of Bangladesh

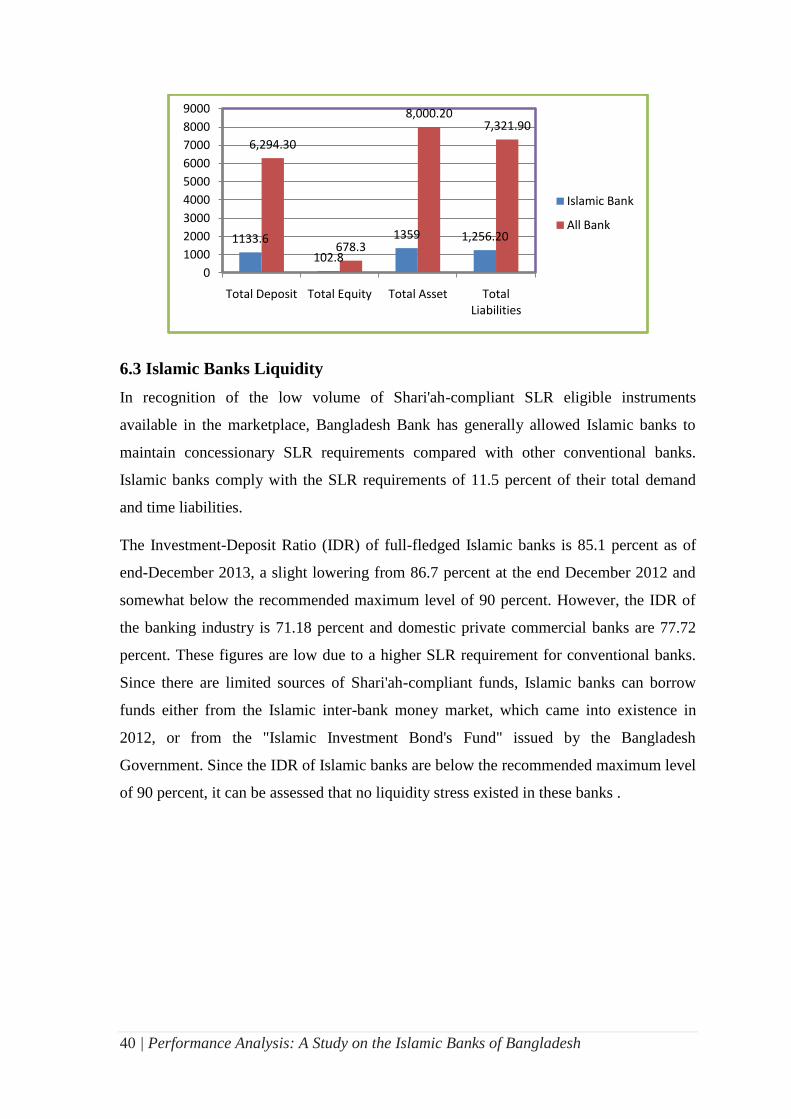

6.3 Islamic Banks Liquidity

In recognition of the low volume of Shari'ah-compliant SLR eligible instruments

available in the marketplace, Bangladesh Bank has generally allowed Islamic banks to

maintain concessionary SLR requirements compared with other conventional banks.

Islamic banks comply with the SLR requirements of 11.5 percent of their total demand

and time liabilities.

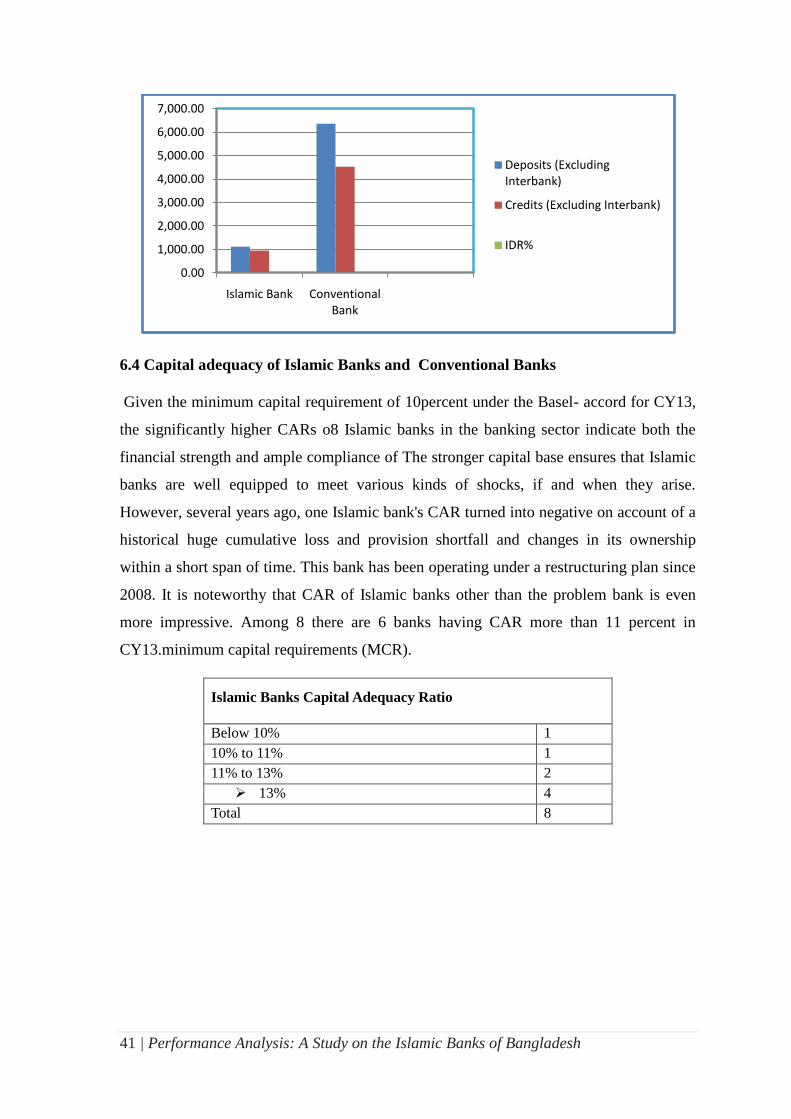

The Investment-Deposit Ratio (IDR) of full-fledged Islamic banks is 85.1 percent as of

end-December 2013, a slight lowering from 86.7 percent at the end December 2012 and

somewhat below the recommended maximum level of 90 percent. However, the IDR of

the banking industry is 71.18 percent and domestic private commercial banks are 77.72

percent. These figures are low due to a higher SLR requirement for conventional banks.

Since there are limited sources of Shari'ah-compliant funds, Islamic banks can borrow

funds either from the Islamic inter-bank money market, which came into existence in

2012, or from the "Islamic Investment Bond's Fund" issued by the Bangladesh

Government. Since the IDR of Islamic banks are below the recommended maximum level

of 90 percent, it can be assessed that no liquidity stress existed in these banks .

1133.6

102.8

1359 1,256.20

6,294.30

678.3

8,000.207,321.90

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

Total Deposit Total Equity Total Asset Total Liabilities

Islamic Bank

All Bank

41 | Performance Analysis: A Study on the Islamic Banks of Bangladesh

6.4 Capital adequacy of Islamic Banks and Conventional Banks

Given the minimum capital requirement of 10percent under the Basel- accord for CY13,

the significantly higher CARs o8 Islamic banks in the banking sector indicate both the

financial strength and ample compliance of The stronger capital base ensures that Islamic

banks are well equipped to meet various kinds of shocks, if and when they arise.

However, several years ago, one Islamic bank's CAR turned into negative on account of a

historical huge cumulative loss and provision shortfall and changes in its ownership

within a short span of time. This bank has been operating under a restructuring plan since

2008. It is noteworthy that CAR of Islamic banks other than the problem bank is even

more impressive. Among 8 there are 6 banks having CAR more than 11 percent in

CY13.minimum capital requirements (MCR).

Islamic Banks Capital Adequacy Ratio

Below 10% 1

10% to 11% 1

11% to 13% 2

13% 4

Total 8

0.00

1,000.00

2,000.00

3,000.00

4,000.00

5,000.00

6,000.00

7,000.00

Islamic Bank Conventional Bank

Deposits (Excluding Interbank)

Credits (Excluding Interbank)

IDR%

42 | Performance Analysis: A Study on the Islamic Banks of Bangladesh

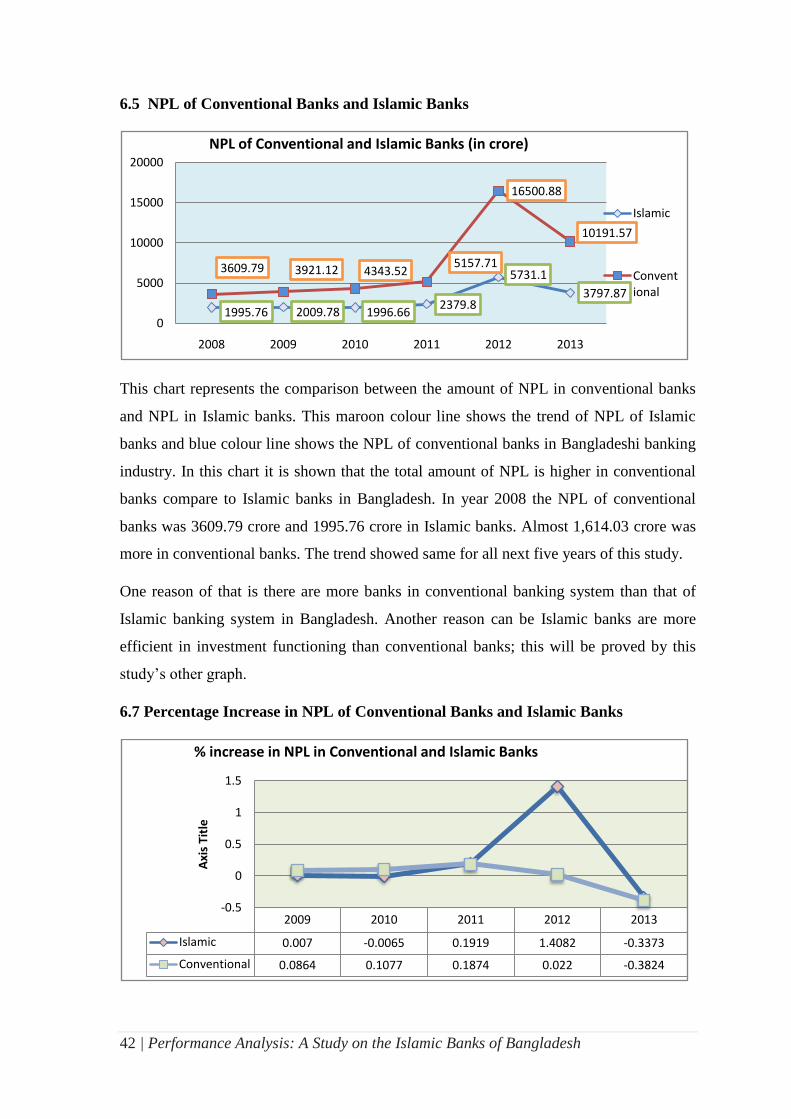

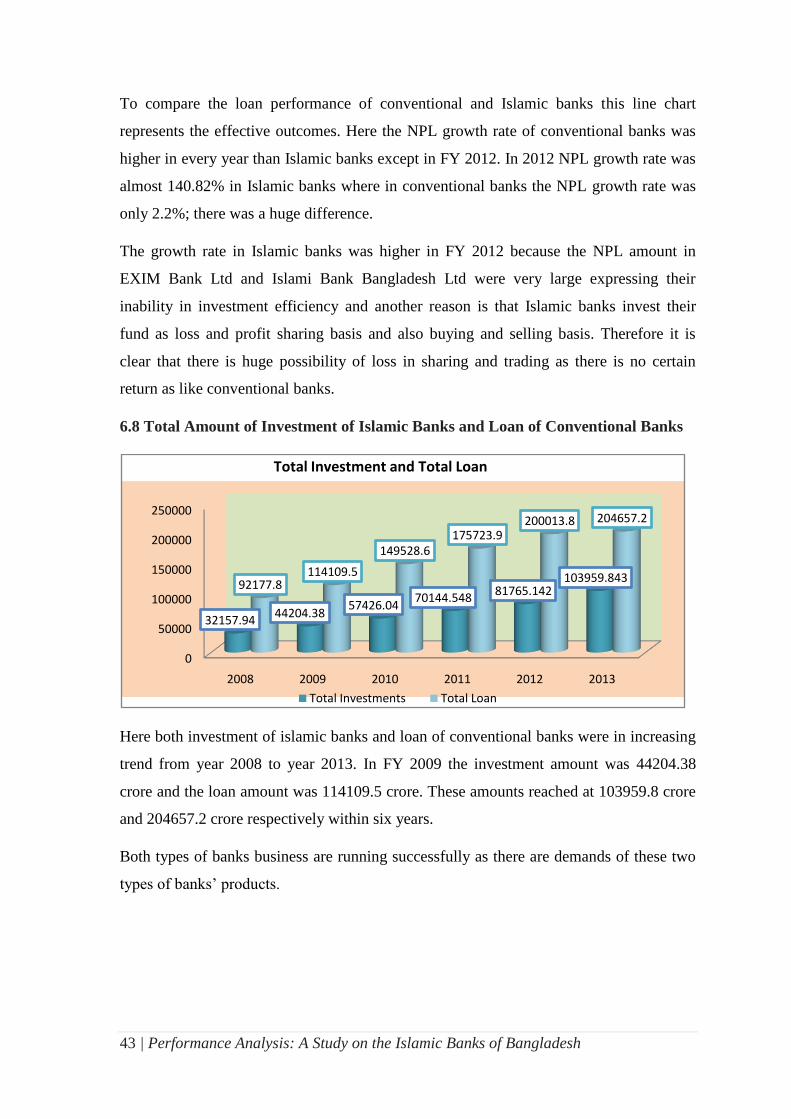

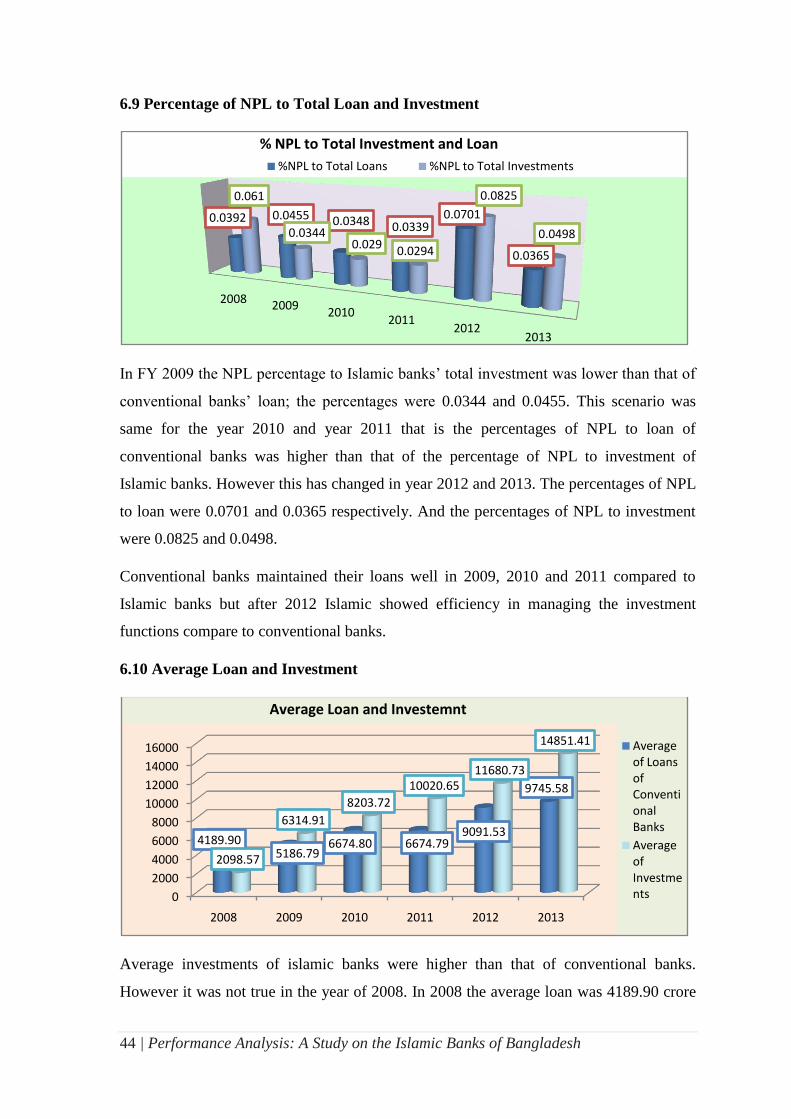

6.5 NPL of Conventional Banks and Islamic Banks

This chart represents the comparison between the amount of NPL in conventional banks

and NPL in Islamic banks. This maroon colour line shows the trend of NPL of Islamic