Embed Size (px)

Citation preview

European Passport for Islamic Banks:

Regulators’ Concern

M. Fahim Khan1

The present form of Islamic banking is not very different in

substance from the conventional interest-based banking. This

is not by choice. Since the Islamic banking has to operate

within the European institutional framework, necessary

modifications are made in the concept and operational

modalities of Islamic banking to conform to the prevailing

institutional framework, which is basically geared towards

promoting, regulating and monitoring the conventional

interest-based banking. In this perspective, introducing

Islamic banking is no more a serious regulatory challenge in

Europe. It is also evident from the fact that conventional

institutions are entering the Islamic financial market

easily without leaving their own conventional (interest

based) business. They are doing this in several ways. They

are opening subsidiaries to do Islamic finance business

only. They are opening Islamic windows, carrying out

conventional and Islamic business under the same roof,

utilizing the certificate of Shari'ah scholars about the

1 Author is currently chairman, Riphah Centre for Islamic Business and Finance, Riphah International University, Islamabad. Email: [email protected]

Shari'ah compatibility of their Islamic operations. They are

selling Islamic products exactly similar to those of Islamic

banks on the backing of their Shari'ah consultants. This is

all happening within the conventional systems of banking

regulations and supervision.

It cannot, however, be denied that the Islamic banking may

require not only a higher degree of monitoring, supervision

and regulations but also a different type of regulatory

framework than what exists for the existing conventional

banking institutions, in case they want to use their

distinct Islamic products. Two areas need attention from the

regulatory authorities in this respect. These are:

1. Risk Management

2. Corporate Governance

Risk management is an issue for regulatory authorities even

for the conventional banking institutions because these

institutions handle other people’s money, which cannot be

subjected to bearing risk. Despite that banking institutions

guarantee the principal and a fixed return determined in

advance, regulatory authorities still monitor the financial

institutions’ operations. Regulatory authorities remain

vigilant so that the banking institutions do not make

adverse selection while choosing their clients for deploying

depositors’ fund or make weakly secured (also called

subprime) loans, as this may lead to the failure of banking

institutions and ultimately cause depositors to suffer a

loss on their deposits. Also the failure of a bank may lead

to a contagion effect and may cause a run on the banking

system and hence putting the entire financial system at

stake. European union of course would not like to take this

risk if permission of Islamic banks to operate in European

Union can lead them to such situation. This apprehension is

not unfounded.

This apprehension arises out of a unique a unique and

distinct feature of Islamic banking that the European

regulatory authorities have never dealt with in the context

of their banking system. The unique feature relates to the

fact that depositors give the Islamic banks their

willingness to bear the risk of loss if it arises out of the

investments made from their deposits. According to Islamic

law, no one can make its money grow without letting it go

through real economic activity and without being willing to

bear the risk of loss associated with the activity. This

willingness of depositors to bear risk, in order to earn a

Shari'ah permissible return on their deposits, generates a

distinct and very important regulatory issue. The

depositors’ willingness to bear the risk may lead the

banking institutions to use the depositors’ money for more

risky economic activities exposing depositors’ money to

bearing the risk more than the depositors would like to

bear. This calls for the attention of regulatory

authorities. Regulatory authorities would like to make sure

that banking institutions are not only doing enough to

manage risk but also they are not taking the risks beyond

what depositors are willing to afford. This is indeed a

complex issue, but definitely not beyond the capacity of

regulatory authorities.

The willingness of depositors to bear the risk on investment

of their deposits raises another important issue for the

regulatory authorities. The issue arises out of the fact

that banks may choose such risky activities to invest

depositors’ money that may benefit the owners/shareholders

of the banking institutions rather than the providers. This

is the issue of corporate governance, which is also on the

agenda of the regulatory authorities. This too will be a

complex issue for the regulatory authorities monitoring

Islamic financial institutions.

Both these issues, risk management and corporate governance,

in respect of Islamic banking become more sensitive in the

context of European union in view of the fact that

regulatory officials are not trained to understand and deal

such operational peculiarities of Islamic banking

institutions. How to understand what risks are necessary to

fulfill Shari'ah compliance and what are not necessary is a

complex issue unless there is complete awareness of the

concept and philosophy underlying the operational details of

Islamic banking institutions.

Wherever Islamic banking is available on the globe, the

tools to regulate conventional financial institutions are

being used for the regulation of Islamic financial

institutions too. This puts the Islamic financial

institutions, when competing with the conventional

institutions, at disadvantage. The Challenge for the

regulatory authorities is to understand the peculiarities of

operational modalities of Islamic financial institutions and

develop a distinct regulatory mechanism that would be more

relevant and friendlier to the concept of Islamic finance.

Encouraging Islamic banking institutions in Europe would be

a welcome step in the interest of making the financial

system socially more inclusive. The absence of the Islamic

financial institutions keeps a large part of the Muslim

population and their economic and financial activities in

European out side the formal financial system.

This article discusses the nature of these issues and how to

take care of them so that Islamic banking institutions’

entry to European Union is facilitated without putting the

objectives and principles of European financial system at

stake.

Risk Management

In the context of allowing Islamic banking in the European

Union, the European regulatory authorities need to worry

about those dimensions of risk that arise out of the

particular nature of contractual relationships with the

clients on assets side as well as liabilities side. The

distinct dimensions of risk in Islamic banking emerge from

following sources:

1) Contractual relationship with the depositors

2) Choice of the modes of financing

3) Risk taking as a part of investing in a real sector

activity

The other dimensions of risk that are common with the

conventional banking do not need to be discussed here as

Islamic banks are equally amenable to any such regulations

and prudent rules that regulatory authorities prescribe for

conventional banking institutions from time to time.

Risks arising out of the contractual relationship with the

depositors: The contract of depositors with the Islamic

banks requires the willingness of depositors to share the

loss of the bank, in case the eventuality arises. The

depositors, thus, are neither guaranteed any predetermined

rate of return nor are guaranteed their full amount of

deposits. The depositors will get back the principal amount

of their deposit and return on their deposits only if bank

makes a profit. If bank bears a loss then the depositors

will get their money back after adjustment of the losss.

Banking laws in Europe may not authorize an institution to

take deposits without guaranteeing principal amount of

deposits and without guaranteeing some return on the

deposits. Presently, Islamic banks have only one choice to

comply with the law. They can offer the guarantee and leave

it to the depositors whether or not they want to invoke the

guarantee. If this is the case, no challenge is posed to

regulatory authorities to devise extra regulations and

prudent rules to protect the depositors’ money. Even if

banking laws allow the Islamic banks not to provide the

guarantees, to comply with the Shari'ah principles, even

then this does not pose a problem for the regulatory

authority, which is concerned with the stability of the

banking institutions. Since the depositors are willing to

bear the losses of the bank, there is no chance of

liabilities exceeding the assets. It can be noted that in

conventional banking any shock on assets side of immediately

creates imbalance in assets and liabilities because

liabilities remain fixed. In case of Islamic banks,

liabilities are linked with the performance on the asset

side and any loss on asset side reduces the liabilities too

to the same extent. Hence, the stability of Islamic banks is

not at stake because of the peculiar contractual

relationship between depositors and Islamic banks.

With respect to the stability, a concern can be raised in

the light of an IMF study claiming that small Islamic banks

are more stable than small conventional bank but large

Islamic banks are not as stable as the large conventional

banks2. “Plausible explanation for the contrast between the

higher stability in small Islamic banks and the relatively

lower stability in larger entities is that it is

significantly more complex for Islamic banks to adjust their

credit risk monitoring system as they become bigger. For

example, the PLS modes, used by Islamic banks, are more

diverse and more difficult to standardize than loans used by

commercial banks”3. If this is true then this is something

that the regulatory authorities can take care of as part of

their normal duties. It does not require any special

concern.

There is, however, a serious issue that arises out of the

contractual relationship of Islamic banks with their

depositors, when they offer risk-bearing savings account to

make profit for the depositors. This adds a new dimension in

the context of managing risk that regulatory bodies may get

more concerned with. This relates to the risk management

relating to managing the profit-sharing Investment Account

(PSIA). The depositors who want to earn a return on their

2 Martin Čihák and Heiko Hesse IMF Working Paper No. 08/16, "Islamic Banks and Financial Stability: An Empirical Analysis," http://www.imf.org/external/pubs/ft/survey/so/2008/RES051908A.htm3 (http://www.imf.org/external/pubs/ft/survey/so/2008/RES051908A.htm).

deposits have to open profit sharing investment accounts.

The Islamic banks thus have authorization from the

depositors to invest their deposits in risk bearing

activities. This suits Islamic banks because they do not

bear any risk in investing these deposits in risky projects

because under the contract (which is called Mudarabah

Contract) bank does not bear any loss that may arise from

the investment of the deposits in risky projects. Depositors

will bear all the loss (the amount of their deposit will be

reduced to the extent of their deposits. Though Islamic

banks would not like to be unscrupulous in managing the risk

bearing deposits because if they end up making a loss on

PSIAs, they will lose their clients who are the major source

of their funds and hence of profit to their share holders.

Yet it cannot be denied that PSIAs potentially do entail

displaced commercial risks for Islamic banks. It is the

existence of this type of risk that necessitated the

enforcement of Glass Steagall Act. The regulatory bodies may

need to formulate not only rules and legal provisions to

stop Islamic banks from speculating on commodity and real

estate prices but may also require different set of

prudential rules to discourage the Islamic banks getting

into risky activities.

Risks arising out of choice of modes of financing

Islamic banks have to make sure that the money passes

through a real activity to justify a return on the use of

their money. There can be several ways to deploy depositors’

money in real economic activities. Islamic banks have to

choose mode of financing that will involve a real activity

(rather than simply advancing money to the clients). Towards

this end, Islamic banks can make a choice from a variety of

modes of financing. These modes of financing4 are either in

the nature of

1) Direct investment with the clients (Called Mudarabah or

partnership between labor and capital and Musharakah

partnership in business, also called profit/loss

sharing-PLS- modes of financing) or

2) Doing Trade directly or indirectly for the clients

(called Bai’ Mujjal bi Thaman Aajil or markup based

trade financing and Bai’ Salam or purchasing foreign

delivery by making advance payment).

3) Leasing assets, directly or indirectly for the clients

(called Ijarah or leasing based modes of financing)

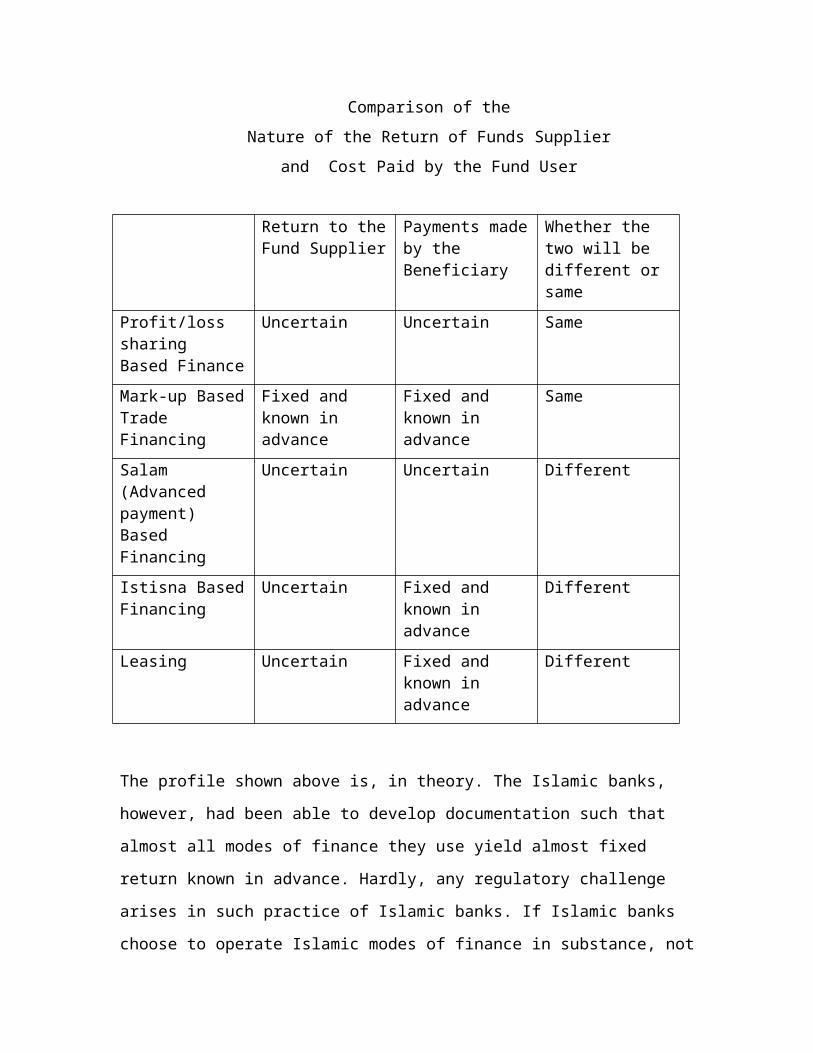

The risk profile of these different types of modes of

financing can be seen in the following table.

Table

4 See Khan and Khan (1), for details of these modes in terms of their counter parts in the contemporary world of trade, finance and investment

Comparison of theNature of the Return of Funds Supplier

and Cost Paid by the Fund User

Return to theFund Supplier

Payments madeby the Beneficiary

Whether the two will be different or same

Profit/loss sharing Based Finance

Uncertain Uncertain Same

Mark-up BasedTrade Financing

Fixed and known in advance

Fixed and known in advance

Same

Salam (Advanced payment) Based Financing

Uncertain Uncertain Different

Istisna BasedFinancing

Uncertain Fixed and known in advance

Different

Leasing Uncertain Fixed and known in advance

Different

The profile shown above is, in theory. The Islamic banks,

however, had been able to develop documentation such that

almost all modes of finance they use yield almost fixed

return known in advance. Hardly, any regulatory challenge

arises in such practice of Islamic banks. If Islamic banks

choose to operate Islamic modes of finance in substance, not

merely in form, then the adoption of Profit/loss sharing

(PLS) based, Leasing based, Istisna based and Salam based

modes of finance, may pose substantial challenge for the

regulatory bodies. This challenge, however, will arise only

if the regulatory bodies are willing to give a chance to

Islamic banks to do Islamic banking in real substance and

spirit5 to show what difference the new paradigm makes on

the frontier of their financial system. This will be a

matter of choice for the regulatory authorities.

Risk taking as a part of undertaking real sector activity

According to Islamic law, financing can earn return only if

it passes through real activity. In other words financing

has to be either a part of a trade or leasing or direct

investment in equity of a business. This takes the concept

of Islamic banking closer to what is known in Europe as

universal banking which has been considered as exposing the

banking institution to get involved in speculative and risky

activities in trading, leasing and stock market activities.

So far Islamic banks are avoiding getting involved directly

in real activity. They are depending on trading based modes

of financing methods where client seeking financing is

required to make the purchase on behalf of the bank and then

to repurchase it from the bank, getting the repurchase

5 The PLS modes of financing are considered reflecting the true spirit of Islamic finance. See M. Fahim Khan, Comparative Economics of Islamic Financing Techniques, Islamic Research and Training Institute,Islamic Development Bank, Jeddah.

financed by the bank. This may have implications but not for

regulators seeking stability of banking institutions, as

discussed earlier. Now that Universal banking is gaining

support in Europe and regulators are already dealing with

the issue, Islamic banking itself does not pose any new

issue.

The fact that Islamic banks may be carrying out more risky

operations on the money of the depositors than conventional

banks do, may be true in theory but the practice of last

more than 35 did not show as a norm. There are only one or

two such instances and those too were not the result of

policy but of unscrupulous management. In general, Islamic

bank do not pose any serious challenge to the regulatory

bodies, even if they are allowed to get into universal

banking. They have been found amenable to suggestions to

reduce risks inherent in their operations. Since they are

competing with the conventional banks, their survival

requires being prudent so that they do not take risks more

than what conventional banks are taking.

Corporate Governance

Though the regulatory authorities in Europe are fully aware

of this issue, particularly in view of the current global

financial crisis yet Islamic banking raises one unique

aspect of corporate governance that is new for the

regulatory authorities in Europe. As already mentioned, the

commitment of Islamic banks to provide Islamically

acceptable modes of finance require a totally different

approach on the part of the regulatory authorities than what

they are faced with in the context of conventional banking.

The sources that generate new issue for governance are also

the sources that generate new issues for risk management.

Taking care of governance will take care of the interest of

the depositors as well. Before discussing what can be done

to ensure good governance in Islamic banking let us see the

sources that create new aspects of the governance to be

faced by regulatory bodies in Europe.

The new issue for corporate governance also arises from the

contractual relationship with the depositors according to

which depositors stand committed to share the profits with

the banks and bear loss of their deposits if eventuality

arises.

Islamic banks offer two types of profit-sharing

investment accounts (PSIA) to the depositors:

a) Restricted Profit Sharing Investment Accounts.

b) Unrestricted Profit Sharing Investment Accounts.

The deposits received under the restricted accounts are

used in pre-specified projects using pre-specified modes.

For such accounts, Islamic banks have succeeded in

developing products that will ensure a return to the

depositors varying only in a very narrow range and almost

non-existing possibility of loss. Thus, despite being

profit-loss sharing accounts, the depositors can have their

deposits in Islamic banks with same risk profile that a

client of conventional bank will get on their savings

account. Whether Islamic banks will be able to provide same

return profile as conventional banks provide to their

depositors is an empirical question. Such accounts thus

pose no risk management issue and no corporate governance

issue significantly different from what is involved in

conventional banking institution.

Unrestricted profit-sharing investment accounts, however, is

an Islamic banking product that offers major and most

complicated regulatory challenge. This is an account where

the depositors authorize bank to invest their deposits in

any investment that banks find suitable and the depositors

agree ex-ante to share the profits/losses arising from these

investments. The spirit of Islamic banking requires

increasing the share of such accounts in mobilizing

resources. It is the existence of these accounts that

distinguish the Islamic banking insititutions from

conventional banking institutions.

Islamic Bank use the deposits of account holders in

investments selected by the bank and account holders will

not have any say in this choice. The possibility of moral

hazard may arise in the use of depositor’s money, which

arise when deposits may be used more in the interest of the

bank management and equity holders than in the interest of

depositors. When bank is making good profits, no corporate

governance issue arises with respect to the interest of the

depositors. Depositors share the profits made by the bank as

the shareholders do. But when banks incur loss on the use of

the deposits, the entire loss is passed on to the

depositors. Here the governance issue comes. There will be

temptation on the part of the management of bank to use the

depositors’ money to increase profits of equity holders who

determine the emolument of the managers. Islamic banking

provides this opportunity. Since Islamic banks are free to

choose where to invest, they may investment in high-risk

high-return projects without caring for the risk-return

preference of depositors. Investing depositors’ money in

high-risk/high-return projects means that if there is high

return, both depositors and equity holders will get higher

return but if the investment ends up incurring loss then the

entire loss will be passed on to the depositors.

Islamic banks have not been able to develop a mechanism of

internal controls strong enough to take care of the interest

of investment account holders vis-à-vis the interests of

shareholders and bank management. In the disciplined

financial and investment environment of Europe, will this

issue be a serious challenge to the regulators?

This governance issue may not be resolved simply by

regulations. There are aspects that relate to ethical

issues also in this respect. Protection of interests of

PSIAs, without adversely affecting the performance of

Islamic banks, will require strict adherence to a carefully

designed code of ethics. Islam gives its own code of ethics

to take care of governance issues. The current practice of

Islamic banking, however, does not have a mechanism to

ensure adherence of Islamic ethics in the conduct of Islamic

banking business.

Similar to the regulations and supervision in stocks and

securities market, Islamic banking industry also requires

more emphasis on developing a system of checks and balances

in respect of fiduciary responsibility with respect to use

of PSIAs. This system has yet to be developed and

implemented as a means to improve the image of the Islamic

banks.

Another issue relating to governance arises on account

of ensuring Shari'ah compliance in the use of different

modes of financing. There is diversity of opinion among

Islamic jurists in the application of Shari'ah rules and

there is flexibility in Islamic system in adopting the

jurist opinion that suits. Islamic banks to enhance their

profits rather than satisfy depositors’ preference for any

particular jurist opinion are utilizing this diversity and

flexibility. Furthermore, since the Islamic banking industry

is still developing, Islamic banking institutions do not

like to reveal all details of their products to avoid free

rider problem. The banks therefore are not very transparent

in declaring all such details that will satisfy account

holders that their religious concerns are being respected in

deploying their funds. Transparency in business deals is

essential ethical requirement in the Islamic system but

maintaining transparency, however, is not simple in view of

the diversity of opinion in religious perceptions of what is

Islamic and what is un-Islamic. This would require a

religious board to specify clear rules and ethical standards

to make the appropriate declarations. The significance of

this issue from the regulators point of view is that if

Islamic banks lose the confidence of their depositors and

fail to establish that they are using the depositors’ money

in Shari'ah compatible way to the satisfaction of the

depositors, the depositors will withdraw their deposits and

the banks will become immediately insolvent. Depositors stay

with Islamic banks only for the satisfaction of Shari'ah

compatibility, otherwise conventional banks are more

convenient, less costly and better equipped to serve their

clients because of their size and experience. This

possibility of losing the confidence of the clientele makes

the Islamic banks vulnerable. A fatwa (verdict) from a

religious scholar enjoying the trust and confidence in the

community can destabilize an Islamic bank. This would be a

genuine concern for the regulatory authority. This concern

becomes more serious when they find that there is no central

Shari'ah body where they could get advice on issues arising

out of diversity of juristic opinions on the application of

Islamic law in developing Shari'ah compatible banking

products. The solution for the problems arising out

diversity of Juristic opinion does not lie in the banking

laws. The solution is in developing independent body that

would set standards for the application of Shari'ah rules

and adherence to ethical standards for Islamic financial

institutions. This will be a self-sustaining body

collectively supported by the Islamic financial institutions

and Islamic businesses in the community. Certification from

this body can be the basis of ensuring stability of Islamic

banks on Shari'ah grounds6.

Another source of generating governance issue is the item of

Reserves in the balance sheet of Islamic bank. This is

similar to the Reserves in the balance sheet of a

conventional bank with only one distinction. Islamic banks

like to keep part of the bank’s profit (before sharing it

with the depositors) as “Profit-Equalization Reserve”.

Islamic banks intend to use these reserves to smooth out

wide fluctuations in the return on profit sharing investment6 See M. Fahim Khan, “Setting Shari'ah Standards for Shari'ah Application in Islamic Finance Industry”, Thunderbird International Business Review, Special Issue, 2006

account. They use the reserves to compensate the depositors

for abnormal decline in profits in any year. Some

prudential and ethical standards are needed to ensure that

no moral hazards takes place on this account and that the

depositors are not compensated from what is genuinely due

for other depositors, or reserves are not used to the

benefit of shareholders what is genuinely required to be

distributed to the depositors.

Islamic banks are not insensitive to governance issue. There

is effort on their own part to show good governance and

hence improve their national and global image. Some of their

efforts are described below:

1. Banks adopt two approaches towards investing the

Investment Accounts. They make PSIA to earn almost

fixed-return, no-risk account by investing in the fixed

return modes of financing and if still there is some

risk of loss the shareholders are willing to bear it

from the reserve account of the bank. The governance

issue of benefitting shareholders at the cost of

deposit holders is diffused to a great extent.

2. Capital adequacy requirements, asset-liability

management and product pricing policies are being

adopted to make the operations not only transparent but

also to build up cushion to fall back on in case of any

unexpected shock.

3. Diversity in Fiqh opinion also has been a potential

source of malpractice on account of corporate

governance. The diversity can potentially be used (and,

in some cases, has actually been used) by the Islamic

banks to increase share holders’ profits rather than

providing the products to satisfy clientele for fulling

their commitment to adhere to Islamic principles in

financial prinicples in lettr and spirit. It is

generally believed that Shari’a Supervisory Board (SSB)

are being used by Islamic banks as an effective organ

ensuring good governance in Islamic banks. But

regulatory body become cautious when seeing SSB taking

decisions which are the prerogative of the management.

Decision making is prerogative of management. Sharing

this prerogative with SSB may generate issues with the

regulating and monitoring agencies such as the central

banks reponsible for overseeing the performance of the

banking industry. This would be a genuine concern of

the regulators in Europe. They would like to be clear

about who is taking the decisions in the Islamic

banking institutions. The Islamic banks, however, have

taken several steps during last decade to clearly

delineate the role of their Shari'ah scholars or

shariah services board in the line of authority

responsible for managing the Islamic banking

operations.

4. Still another area where Islamic banks have made

substantial improvement in their governess structure in

Islamic financial institutions relates to improving

transparency in financial reporting. About two decades

earlier, Islamic banking institutions had no specific

system of financial reporting to provide adequate

information to their PSIA holders with respect to the

revenues and expenses and profit sharing ratios making

up the profit in their investment account. This

information asymmetry made regulatory authorities

rightly concerned about moral hazards on the part of

the banks as well as on the part of their clients with

whom they invest the money of PSIA holders. The

financial reporting system on this account, however,

has improved substantially over time and is still

improving improving. The emergence of institutions like

Accounting and Auditing Organization for Islamic

financial institutions (based in Bahrain) and the

Islamic Financial Services Board (based in Malaysia)

are helping Islamic banks in improving their financial

reporting and transparency and hence improving their

governance structure. The Islamic banks are working

hard to adopt standards for financial reporting that

may meet the requirements of European regulatory

authorities.

5. The solution to governance issue relating to Islamic

banking operations lies to a large extent in the

institutionalization of Islamic business ethics which

specifically aim at not only removing information

asymmetry between banks and the depositors by making it

religious obligations to be transparent to the maximum

possible extent, but also ensuring not to usurp

property of others. There are specific verses in the

Quran. “And do not eat one another's wealth wrongly

[2:188]. “O you who have believe, do not consume one

another's wealth unjustly but only in [lawful] business

by mutual consent. And do not kill yourselves [or one

another” [4:29]. These verses comprehesively prohibit

bad governance and moral hazard. How to

institutionalize such moral values is the issue that

Islamic Financial Institutions are seriously trying to

grapple on priority to minimize the interference of

regulatory authorities to check their governance

standards.

Role of Shari'ah Scholars in Ensuring Good Governance

A Shari'ah scholar or a team of Shari'ah scholars engaged by

Islamic bank has a vital role in the contemporary practice

of Islamic banking. There are following dimensions for this

role. First dimension is related to assuring the clients

that the operations of Islamic bank conform to Islamic law.

Only Shari'ah scholars have the authority to give this

certificate. If a Shari'ah scholar declares that the

management of the bank has violated the Shari'ah in preparing

any product or in conducting any business, it would quickly

lose the confidence of the majority of its investors and

clients.

Second dimension relates to overseeing the operations

whether or not they strictly adhere to Islamic law as the

Shari'ah scholars advised. The third dimension relates to

the adherence to Islamic code of morals and ethics. There is

a specific system of ethics and morals given by Islam for

running a business or a commercial institution. Shari'ah

scholars will identify the practices of Islamic banks, which

are ethically and morally unsound. In this role, Shari'ah

scholars help not only minimizing the transaction costs,

possibility of moral hazards and making adverse selection

but also will help in identifying the situations leading to

bad governance.

There are two points that may be kept in view about the role

of Shari'ah scholars and Shari'ah boards of individual

banks.

1. The Shari'ah scholars are hired by Islamic banks to

help them develop products that are not only Shari'ah

compliant but also make the Islamic banks compete with

conventional banks. They, thus, play the role of

financial engineers for which they are not properly

qualified. They are qualified to supervise, monitor and

help regulatory bodies to keep Islamic bank on the

track it has adopted for its operations which is to

conduct their business according to Islamic law. They

are on pay roll of Islamic banks and hence issue of

conflict of interest may exist. They are often

criticized that being on pay role of Islamic banks they

may be unable to play an objective role in ensuring the

adherence to Shari'ah principles and code of ethics in

the bank employing them7.

2. Diversity of opinion on the application of Shari'ah

gives Islamic banks to choose scholars of their own

choice that may help them in preserving the form of

their products that can earn more profits to them in

the name of Shari'ah rather than preserving the spirit

and substance of Islamic law which is the concern of

the clients of the banks. Benefitting from Shari'ah

scholars’ ability to exploit diversity of opinion in

Islamic juristic literature for increasing profits of

Islamic banks may prove to be counter productive, if

their clientele becomes dissatisfied with the

operations of Islamic banks. This may have serious

7 They place excessive emphasis on contract forms rather than thesubstance, thus sacrificing economy and efficiency to preservation of form. (Mahmoud A el- Gamal, Islamic Finance: Law, Economics and Practic, Cambridge University Press, Cambridge, New York, 2006

repercussions on the long run stability of Islamic

banks. An organization known as Auditing and Accounting

Organization of Islamic Financial Institutions (AAOIFI)

based in Bahrain is carrying out the functions in the

dimensions mentioned above. Another body known as

Islamic Financial Services Board (IFSB) consisting of

the regulatory authorities where Islamic banking exists

is working on developing standards for various

dimensions of Islamic banking operations, corporate

governance, market discipline, risk management being

some of the areas where IFSB has completed the work on

setting standards. However, neither the accounting and

auditing standards set by AAOIFI nor the operational

standards set by IFSB are binding on Islamic banks. If

a body can be developed in Europe to set standards on

Shari'ah application and operational modalities of

Islamic banks and to certify the adherence to these

standards, much of the burden of regulatory authorities

with respect to supervising Islamic banks may be

reduced. The help from the Jeddah based Islamic

Development Bank that played a catalytic role in the

establishment of AAOIFI and IFSB can be solicited to

establish such a Shari'ah regulatory body.

Institutional Infrastructure

As mentioned earlier, most Islamic banks have operated inenvironment, which are conducive to protection and

promotion of conventional interest based banks. Islamic banks cannot benefit from this. The infrastructural institutions to give support to Islamic banking operations and products are non-existent. For example, interbank market is nonexistent for Islamic banks. Shari'ah compatible money market though is developing butis still extremely in formative stage. There are not enough instruments to meet the contemporary financing needs of Muslims to be met from money market. Shari'ah compatible government securities are not available even in Muslim countries. There is limited availability of andaccess to lender-of-last-resort facilities of central banks. Lack of institutional infrastructure to give support to Islamic banks, however puts them in disadvantaged position while managing risk and achieving good governance in competition with the conventional banks whohave strong infrastructure to facilitate their efforts inthese two directions. Development of such infrastructure for Islamic banking institutions, however, is a matter oftime and the market share that Islamic banks carry in thefinancial market of a country. If regulatory bodies in Europe are convinced of the usefulness of the concept of Islamic banking, then the Islamic banks need to be given opportunity to exist and grow and steps need to be taken for infrastructural institutions to emerge for the support of Islamic financial institutions. The infrastructural institutions will emerge in a disciplinedmarket like that of European union more easily to lead and force the Islamic banks to adopt best practices.

Significance of Prudential Regulations

The need and significance of prudential regulations in the

context of allowing Islamic banks in a country or region

like European Union is more pronounced on two accounts.

Firstly, all aspects of Islamic banking practice cannot be

legislated as large part of it depends on good perception of

and commitment to religious spirit of the concept. This can

be assured more by prudential rules than by the legislative

procedures. If Islamic banks deviate from the religious

spirit of the concept of Islamic finance they will lose the

roots in their clientele and hence will lose stability.

Secondly, the corporate governance issue is an issue that

can best be handled by adherence to relevant ethical and

moral norms. Islamic system of life has a strong system of

business ethics specially referring to good governance.

Need for Research

There is no proper educational, research and training

facility preparing concerned officials to develop

methodology and systems to monitor, supervise, and regulate

Islamic financial market. The conventional market has

developed instruments and institutions for risk management

that are not Shari'ah compatible and hence not so relevant

for Islamic finance industry. Islamic finance industry is

not yet mature enough to develop its own methods of risk

management and it does not have the means (because of its

relative size vis-à-vis interest based institutions) to

develop methodology and institutional setup that will help

the industry to have its own mechanism of taking risk and

managing it. Conventional finance industry is better

equipped to manage risk using the institutional arrangements

that they developed.

The entry of Islamic banks in European Union requires

regulatory authorities to research and understand the need

of the Islamic banking industry. The academia and the

research institutions dealing with financial and monetary

system are required to attend to the needs of the Islamic

banking industry in Europe and hence guide regulatory bodies

how and in what directions to regulate the industry.

The Bank of International Settlements has noted the need for

innovations in Islamic banking activities in three

directions: liquidity enhancement, risk transfer and revenue

generation. Islamic banks have to focus on revenue

generation, as it had to compete with conventional finance

and show comparable returns. The need to enhance liquidity,

and hence to move towards greater securitization of assets,

is already recognized as evidenced by the developments in

Malaysia.

An important area for research is integrating Zakah

(obligatory charity) and Waqf (charitable endowments) in the

operations of Islamic banking institutions. At present only

an insignificant fraction of the Zakah payments passes

through Islamic financial institutions. Making Islamic

financial institutions a trustworthy medium to access the

poor and deprived sections of the population meet their

needs from the contributions to Zakah Fund maintained by

Islamic banks will reflect the Islamic financial institution

to be an institution of poor as well. This feature will

attract the, population that pays Zakah, to shift to Islamic

banking institutions as these institutions can help them

discharge their Zakah and similar obligations in a better

way. Islamic financial institutions can also explore the

possibility to include in their activities development of

Awqaf properties and hence contributing to social

development. Securitizing Awqaf properties to mobilize

resources for the development of Awqaf properties and

helping them perform their social development programs is

one example of enhancing the image of Islamic financial

institutions.

All innovations need a base in research and development,

which in turn draw on fundamental research in universities

and laboratories. Islamic finance became a subject of

research in universities in 1980s. The subject is discussed

every year at high profile conferences in Bahrain, Harvard,

and other places. Yet the resources devoted and the

facilities available hardly match the challenges facing the

industry.

Conclusion

Islamic banks need European passport on their own merit.

They are needed tto meet the banking needs of the Muslim

communities and they are also needed for introducing

diversity in the financial system in European Union. The

Islamic institutions will certainly be able to make positive

contribution to the financial system particularly in the

context of the international movement of ethical banking.

There are institutions in Europe that are trying to practise

some sort of “without interest” or zero interest financing.

Islamic banking may provide them a working model. There is

no significant regulatory challenge involved in allowing

Islamic banks to practice in Europe. There are, however, two

areas that require attention of policy makers if they grant

Islamic banks entry into Europe.

1) Facilitating the development of infrastructural

institutions

2) Training the officials of regulating bodies to

understand the Shari'ah background of Islamic banks in

relation to the banking laws in Europe

Institutional Development

Following institutional developments need to be encouraged:

Firstly institutions are required to give access to Islamic

banks to a special inter-bank market that may enable to

acquire liquidity or deploy access liquidity in Shari'ah

compatible way.

Secondly Shari'ah compatible methods need to be developed to

provide effective link with the national central banks to

provide not only support the regular support that is

provided to conventional banks but also to develop external

control of the Islamic banks.

Thirdly, an independent body (on lines of Association of

Investment Management Research-AIMR) consisting of Shari'ah

scholars and finance experts to develop uniform procedures

of internal control and provide training in Shari'ah

diversity in Fiqh opinions and Islamic system of business

ethics. This body will also provide certification adherence

to Shari'ah standards and Islamic ethics, will monitor the

operations of Islamic banks and publish report on state of

adherence to Islamic law and ethics.

Need for Training of officials in regulatory bodies

This is the fundamental conclusion of the paper. If any

European country wants to consider granting license to

Islamic banking, the apprehensions about regulatory

challenge will be substantially alleviated if officials of

regulatory bodies get themselves trained in the Shari'ah and

Fiqh rules underlying the theory of Islamic banking. There

is no shortage of reliable institutions to provide such

training. Islamic Research and Training Institute (IRTI) of

Islamic Development Bank would be a good place to seek such

training.