Embed Size (px)

Citation preview

India Investment Opportunities for NRIs/OCIs

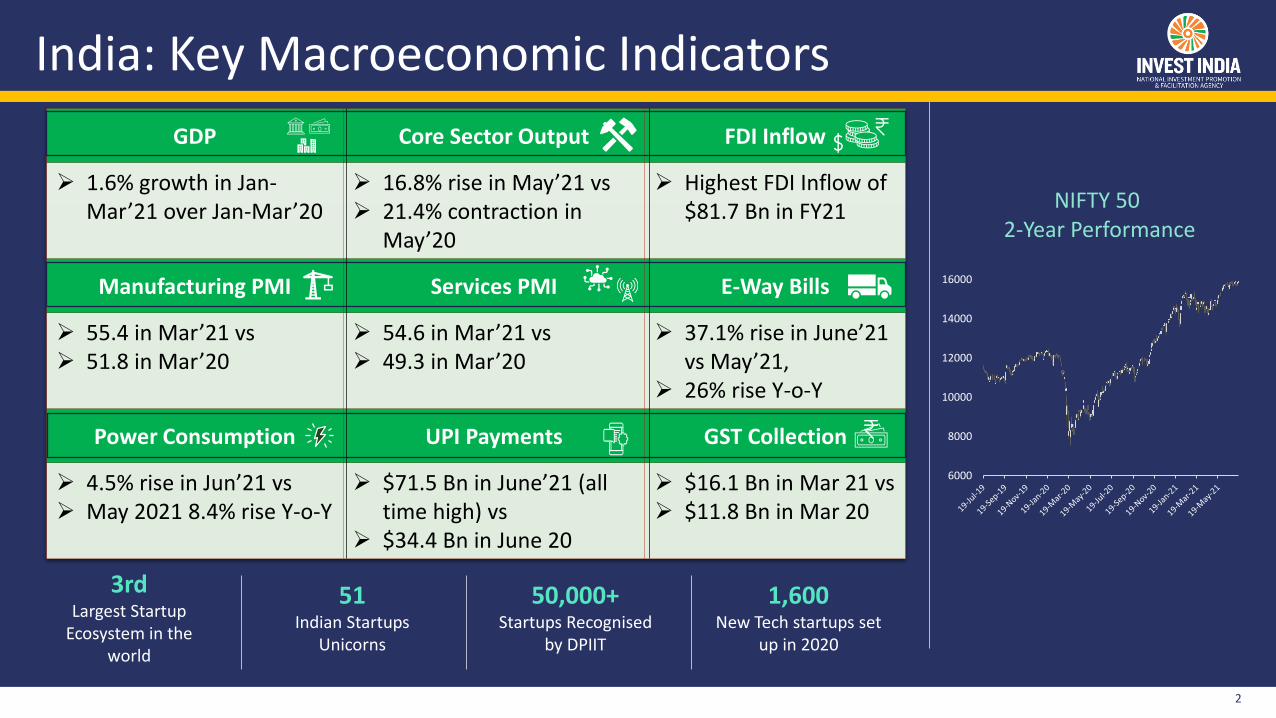

India: Key Macroeconomic Indicators

2

GDP Core Sector Output FDI Inflow

➢ 1.6% growth in Jan-Mar’21 over Jan-Mar’20

➢ 16.8% rise in May’21 vs➢ 21.4% contraction in

May’20

➢ Highest FDI Inflow of $81.7 Bn in FY21

Manufacturing PMI Services PMI E-Way Bills

➢ 55.4 in Mar’21 vs ➢ 51.8 in Mar’20

➢ 54.6 in Mar’21 vs ➢ 49.3 in Mar’20

➢ 37.1% rise in June’21 vs May’21,

➢ 26% rise Y-o-Y

Power Consumption UPI Payments GST Collection

➢ 4.5% rise in Jun’21 vs➢ May 2021 8.4% rise Y-o-Y

➢ $71.5 Bn in June’21 (all time high) vs

➢ $34.4 Bn in June 20

➢ $16.1 Bn in Mar 21 vs➢ $11.8 Bn in Mar 20

6000

8000

10000

12000

14000

16000

NIFTY 502-Year Performance

3rdLargest Startup

Ecosystem in the world

51Indian Startups

Unicorns

50,000+Startups Recognised

by DPIIT

1,600New Tech startups set

up in 2020

Critical Structural Reforms: Accelerating Growth

3

Investor friendly laws• 64 penal provisions under

Companies Act amended to decriminalize procedural lapses

• Corporate insolvency enactment recovery time reduced to 1.6 years in 2019 vs 4.3 years in 2018

Business friendly labor reforms• 41 labor laws subsumed under 4

codes easing compliance burden

Competitive tax regime• Corporate Income tax lowest in SE

Asia reduced from 30% to 17% (vs. 25% in China, Indonesia)

Competitive factor cost • Electricity made available at $0.07

per kWh; lowest in entire region

Hassle-free land acquisition• 3000+ Industrial parks with 0.5+

million hectare readily available

Production Linked Incentives• ~5% average incentive on total

production of 5 years

Simplified existing processes • Single form for company information;

Single window at Indian customs

Provide fast track clearances • Empowered Group of Secretaries &

Project development cell for handholding investors

SOE bank reform

• Bank reform merging & allocated capital in most efficient institutions

Cost of Doing Business Ease of Doing Business Risk of Doing Business

#142

2014

#63

2019

33 PlacesGlobal Innovation Index#48 (2020)

10 PlacesLogistics Performance Index #44 (2018)

79 PlacesWorld Bank’s Ease of Doing Business

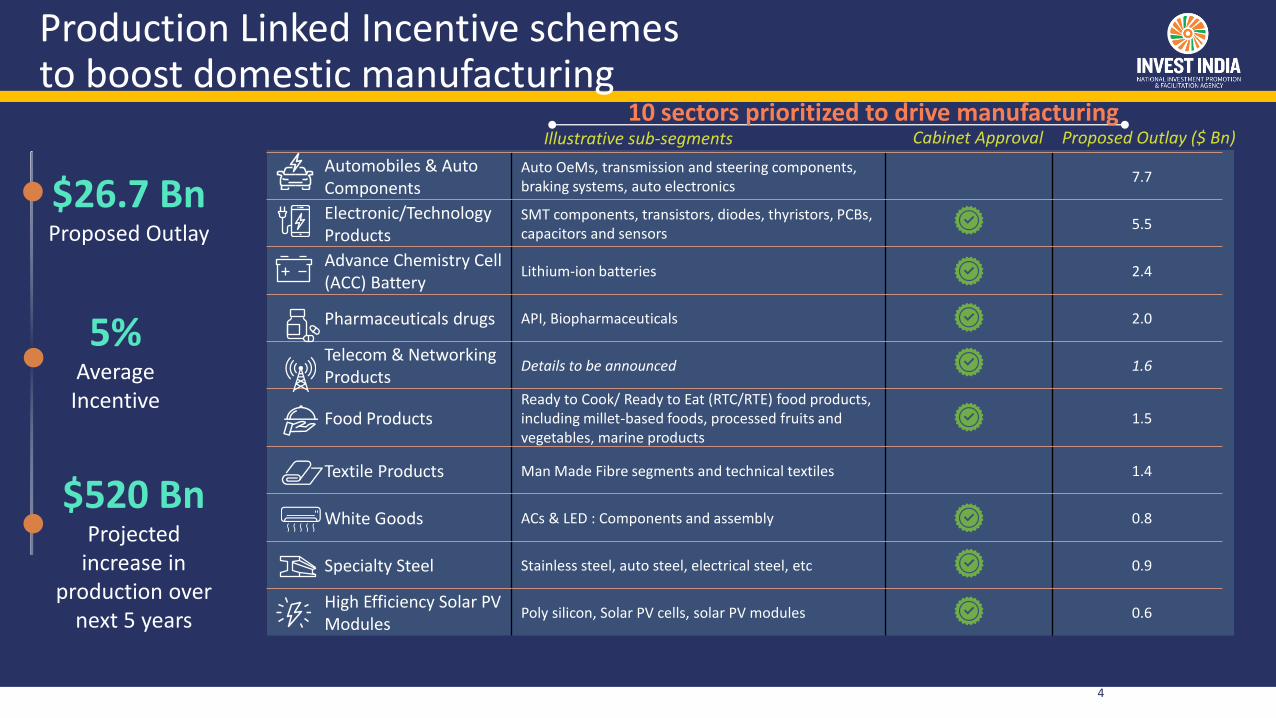

Production Linked Incentive schemes to boost domestic manufacturing

4

Automobiles & Auto Components

Auto OeMs, transmission and steering components, braking systems, auto electronics

7.7

Electronic/Technology Products

SMT components, transistors, diodes, thyristors, PCBs, capacitors and sensors

5.5

Advance Chemistry Cell (ACC) Battery

Lithium-ion batteries 2.4

Pharmaceuticals drugs API, Biopharmaceuticals 2.0

Telecom & Networking Products

Details to be announced 1.6

Food ProductsReady to Cook/ Ready to Eat (RTC/RTE) food products, including millet-based foods, processed fruits and vegetables, marine products

1.5

Textile Products Man Made Fibre segments and technical textiles 1.4

White Goods ACs & LED : Components and assembly 0.8

Specialty Steel Stainless steel, auto steel, electrical steel, etc 0.9

High Efficiency Solar PV Modules

Poly silicon, Solar PV cells, solar PV modules 0.6

Illustrative sub-segments

Cost of Doing Business

10 sectors prioritized to drive manufacturingCabinet Approval Proposed Outlay ($ Bn)

$26.7 BnProposed Outlay

5%Average

Incentive

$520 BnProjected

increase in production over

next 5 years

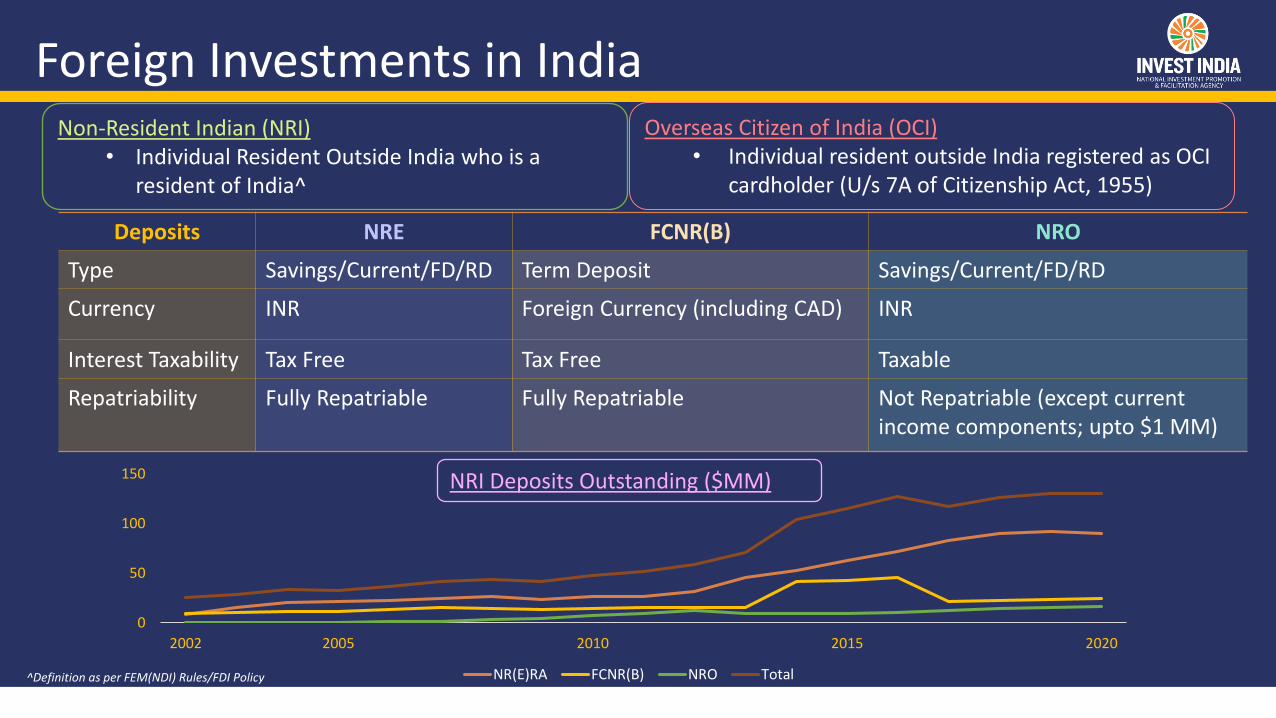

Foreign Investments in India

5

^Definition as per FEM(NDI) Rules/FDI Policy

NRI Deposits Outstanding ($MM)

Overseas Citizen of India (OCI)• Individual resident outside India registered as OCI

cardholder (U/s 7A of Citizenship Act, 1955)

Deposits NRE FCNR(B) NRO

Type Savings/Current/FD/RD Term Deposit Savings/Current/FD/RD

Currency INR Foreign Currency (including CAD) INR

Interest Taxability Tax Free Tax Free Taxable

Repatriability Fully Repatriable Fully Repatriable Not Repatriable (except current income components; upto $1 MM)

0

50

100

150

2002 2005 2010 2015 2020

NR(E)RA FCNR(B) NRO Total

Non-Resident Indian (NRI)• Individual Resident Outside India who is a

resident of India^

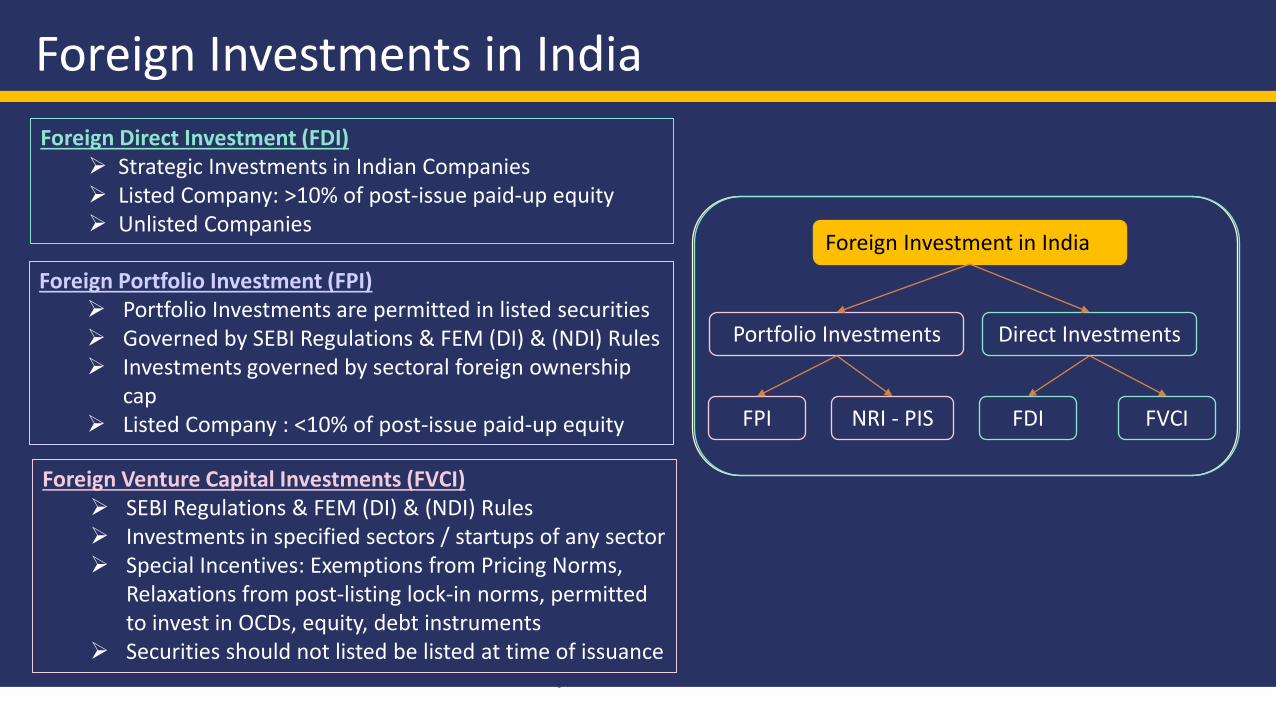

Foreign Investments in India

6

Foreign Direct Investment (FDI)➢ Strategic Investments in Indian Companies➢ Listed Company: >10% of post-issue paid-up equity➢ Unlisted Companies

Foreign Investment in India

NRI - PIS

Direct Investments

FPI

Portfolio Investments

FDI FVCI

Foreign Portfolio Investment (FPI)➢ Portfolio Investments are permitted in listed securities➢ Governed by SEBI Regulations & FEM (DI) & (NDI) Rules➢ Investments governed by sectoral foreign ownership

cap➢ Listed Company : <10% of post-issue paid-up equity

Foreign Venture Capital Investments (FVCI)➢ SEBI Regulations & FEM (DI) & (NDI) Rules➢ Investments in specified sectors / startups of any sector➢ Special Incentives: Exemptions from Pricing Norms,

Relaxations from post-listing lock-in norms, permitted to invest in OCDs, equity, debt instruments

➢ Securities should not listed be listed at time of issuance

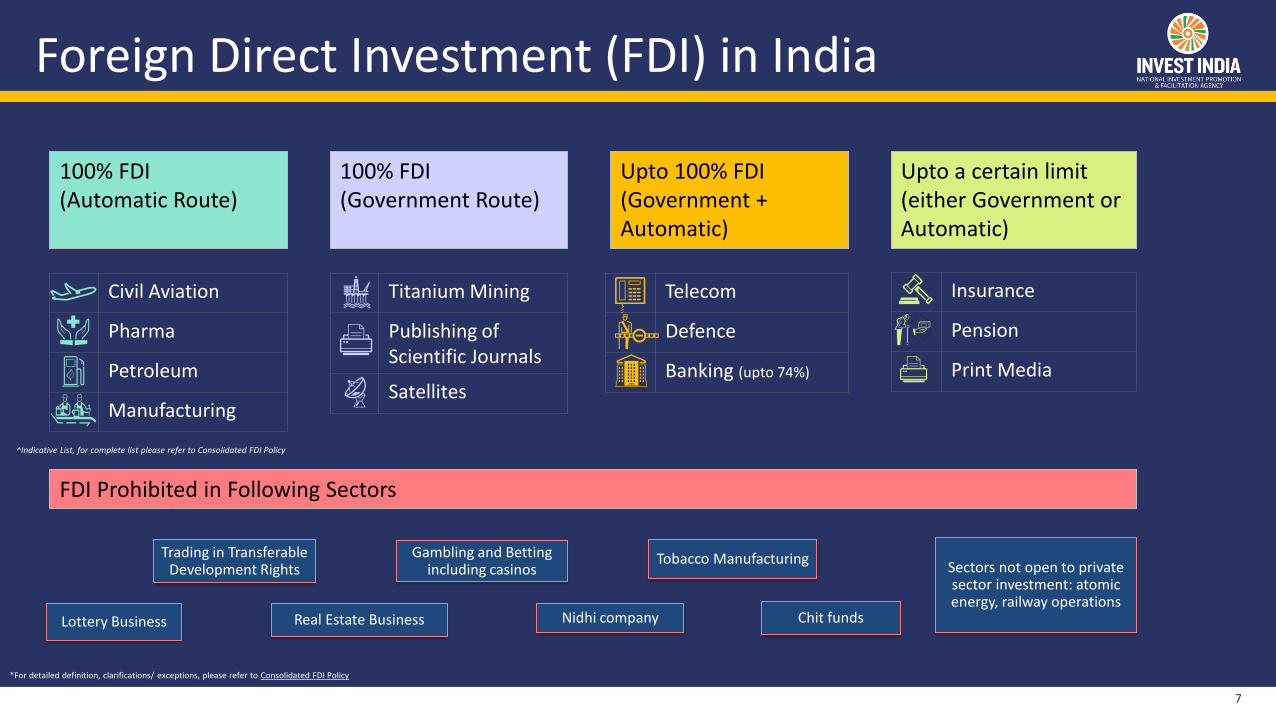

Foreign Direct Investment (FDI) in India

7

100% FDI (Automatic Route)

*For detailed definition, clarifications/ exceptions, please refer to Consolidated FDI Policy

Civil Aviation

Pharma

Petroleum

Manufacturing

100% FDI (Government Route)

Titanium Mining

Publishing of Scientific Journals

Satellites

Upto 100% FDI (Government + Automatic)

Telecom

Defence

Banking (upto 74%)

Upto a certain limit (either Government or Automatic)

Insurance

Pension

Print Media

FDI Prohibited in Following Sectors

Lottery Business

Gambling and Betting including casinos

Chit fundsNidhi company

Trading in Transferable Development Rights

Real Estate Business

Tobacco ManufacturingSectors not open to private sector investment: atomic energy, railway operations

^Indicative List, for complete list please refer to Consolidated FDI Policy

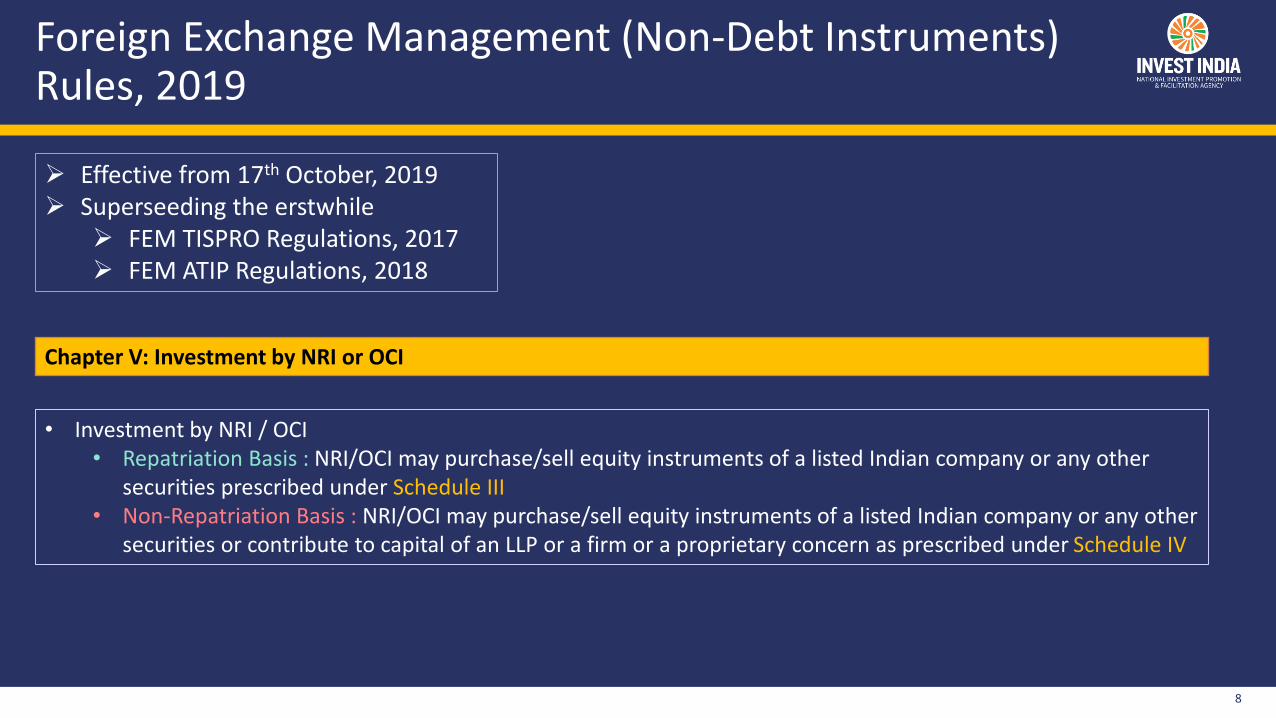

Foreign Exchange Management (Non-Debt Instruments) Rules, 2019

8

➢ Effective from 17th October, 2019➢ Superseeding the erstwhile

➢ FEM TISPRO Regulations, 2017➢ FEM ATIP Regulations, 2018

Chapter V: Investment by NRI or OCI

• Investment by NRI / OCI• Repatriation Basis : NRI/OCI may purchase/sell equity instruments of a listed Indian company or any other

securities prescribed under Schedule III• Non-Repatriation Basis : NRI/OCI may purchase/sell equity instruments of a listed Indian company or any other

securities or contribute to capital of an LLP or a firm or a proprietary concern as prescribed under Schedule IV

9

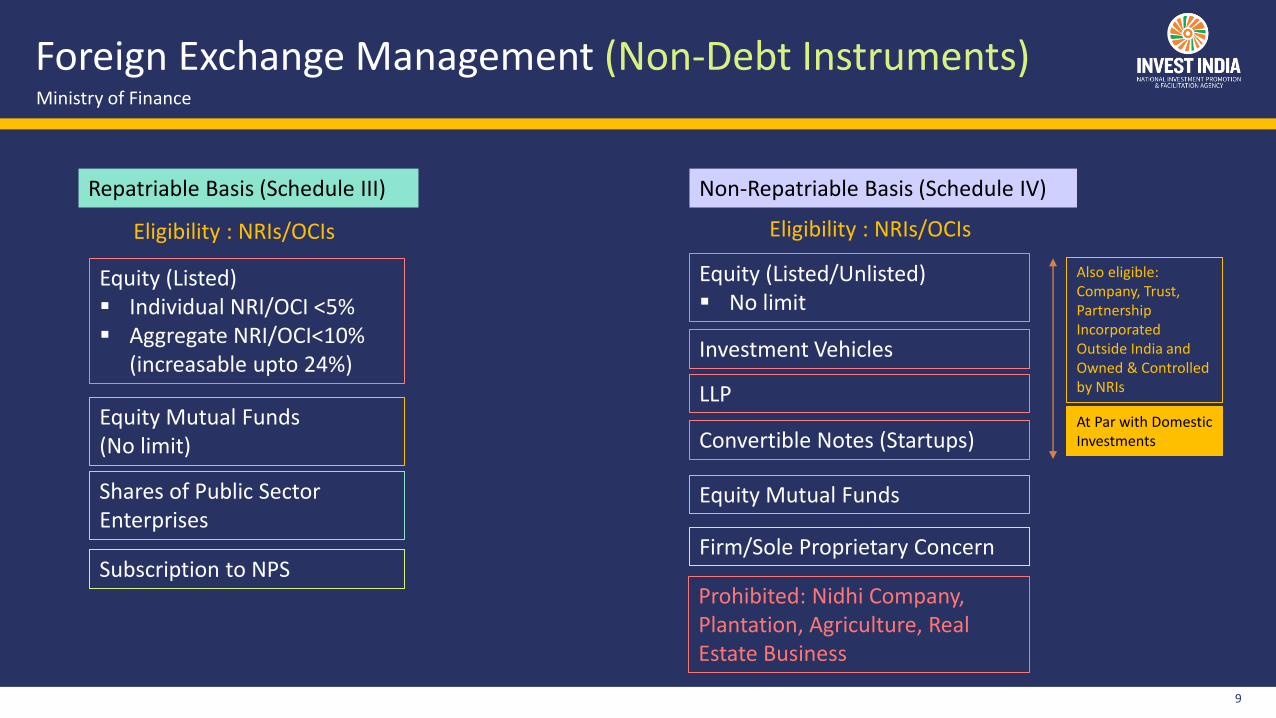

Foreign Exchange Management (Non-Debt Instruments)

Equity (Listed)▪ Individual NRI/OCI <5%▪ Aggregate NRI/OCI<10%

(increasable upto 24%)

Equity Mutual Funds(No limit)

Shares of Public Sector Enterprises

Subscription to NPS

Repatriable Basis (Schedule III)

Equity (Listed/Unlisted)▪ No limit

Prohibited: Nidhi Company, Plantation, Agriculture, Real Estate Business

Firm/Sole Proprietary Concern

Non-Repatriable Basis (Schedule IV)

Eligibility : NRIs/OCIs Eligibility : NRIs/OCIs

Investment Vehicles

LLP

Convertible Notes (Startups)

Also eligible: Company, Trust, Partnership Incorporated Outside India and Owned & Controlled by NRIs

At Par with Domestic Investments

Equity Mutual Funds

Ministry of Finance

10

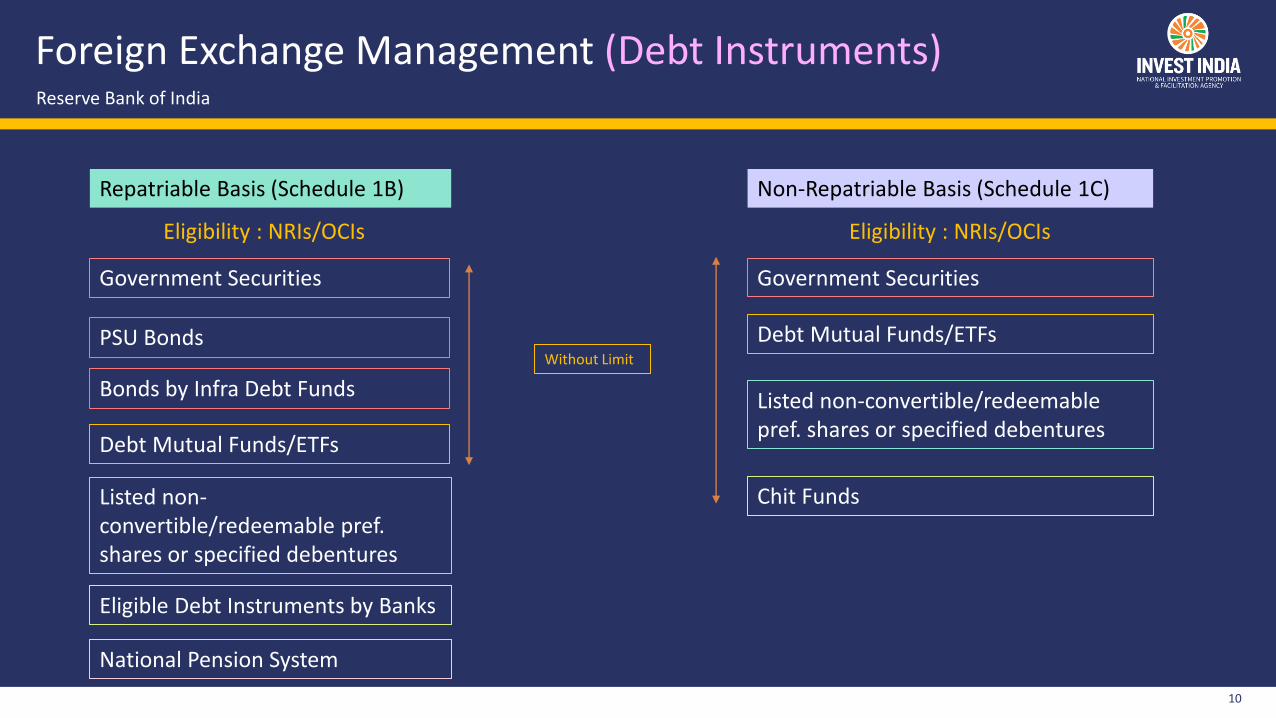

Foreign Exchange Management (Debt Instruments)

Government Securities

Debt Mutual Funds/ETFs

Listed non-convertible/redeemable pref. shares or specified debentures

Eligible Debt Instruments by Banks

Repatriable Basis (Schedule 1B)

Eligibility : NRIs/OCIs

Reserve Bank of India

PSU Bonds

Bonds by Infra Debt Funds

National Pension System

Government Securities

Debt Mutual Funds/ETFs

Listed non-convertible/redeemable pref. shares or specified debentures

Chit Funds

Non-Repatriable Basis (Schedule 1C)

Eligibility : NRIs/OCIs

Without Limit

Recent Announcements

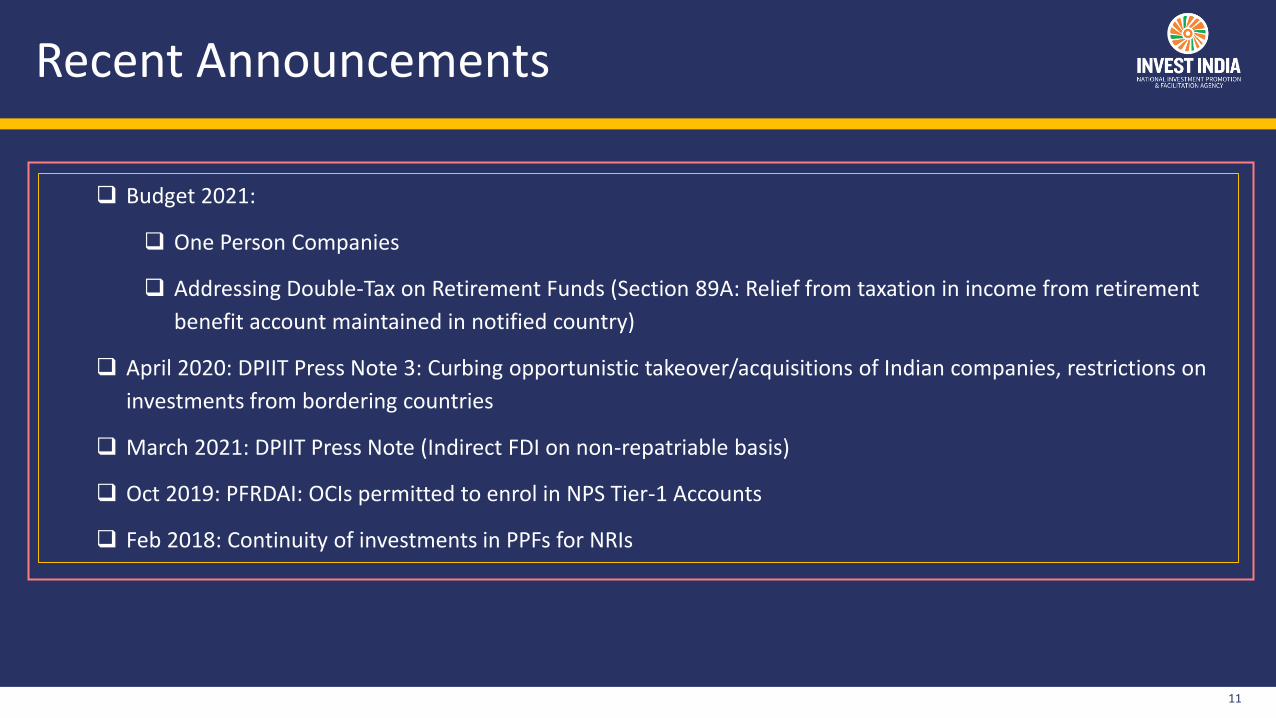

11

❑ Budget 2021:

❑ One Person Companies

❑ Addressing Double-Tax on Retirement Funds (Section 89A: Relief from taxation in income from retirement

benefit account maintained in notified country)

❑ April 2020: DPIIT Press Note 3: Curbing opportunistic takeover/acquisitions of Indian companies, restrictions on

investments from bordering countries

❑ March 2021: DPIIT Press Note (Indirect FDI on non-repatriable basis)

❑ Oct 2019: PFRDAI: OCIs permitted to enrol in NPS Tier-1 Accounts

❑ Feb 2018: Continuity of investments in PPFs for NRIs

India-Canada Double Taxation Avoidance Agreement

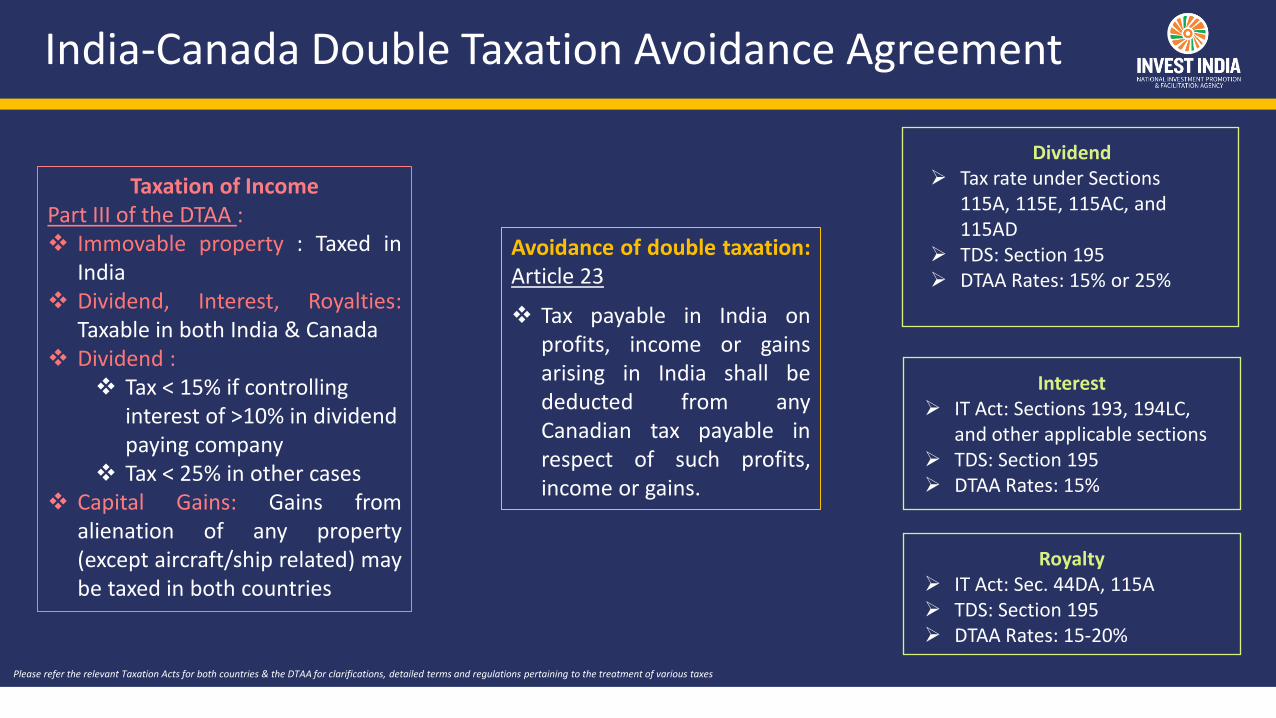

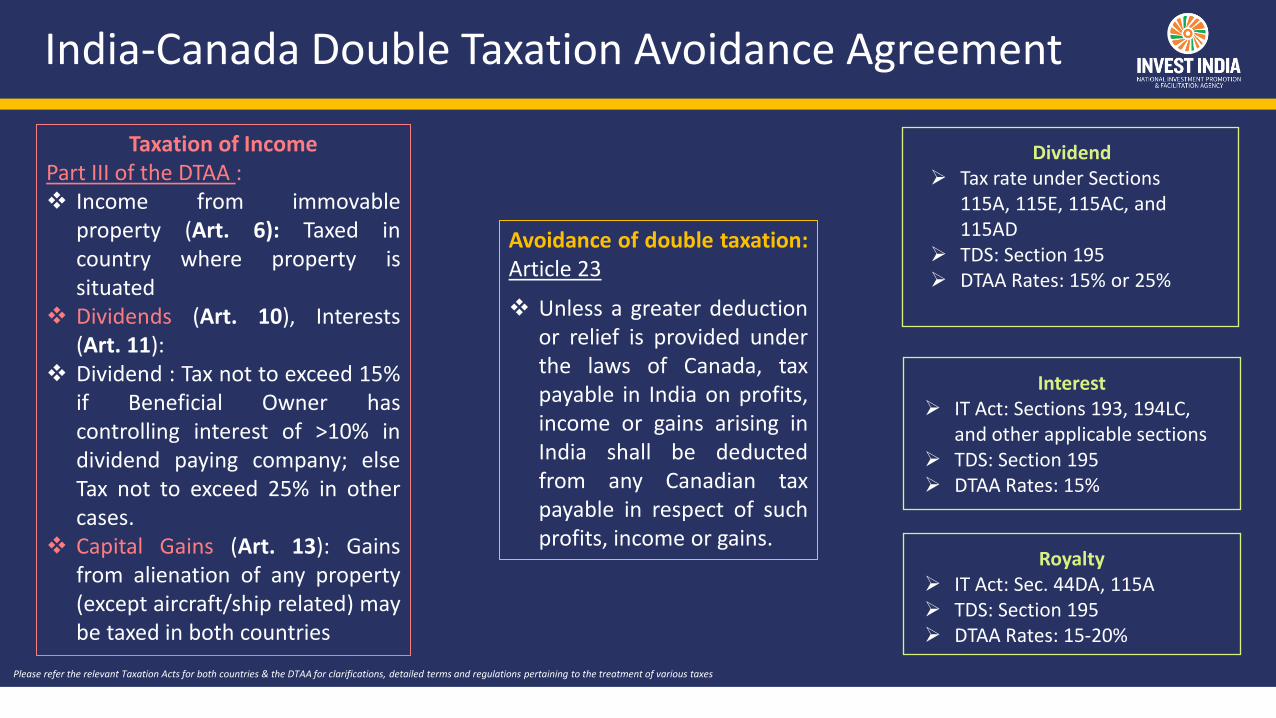

Avoidance of double taxation:Article 23

❖ Tax payable in India onprofits, income or gainsarising in India shall bededucted from anyCanadian tax payable inrespect of such profits,income or gains.

Taxation of IncomePart III of the DTAA :❖ Immovable property : Taxed in

India❖ Dividend, Interest, Royalties:

Taxable in both India & Canada❖ Dividend :

❖ Tax < 15% if controlling interest of >10% in dividend paying company

❖ Tax < 25% in other cases❖ Capital Gains: Gains from

alienation of any property(except aircraft/ship related) maybe taxed in both countries

Please refer the relevant Taxation Acts for both countries & the DTAA for clarifications, detailed terms and regulations pertaining to the treatment of various taxes

Dividend➢ Tax rate under Sections

115A, 115E, 115AC, and 115AD

➢ TDS: Section 195➢ DTAA Rates: 15% or 25%

Interest➢ IT Act: Sections 193, 194LC,

and other applicable sections ➢ TDS: Section 195➢ DTAA Rates: 15%

Royalty➢ IT Act: Sec. 44DA, 115A➢ TDS: Section 195➢ DTAA Rates: 15-20%

Equity

Investment Avenues

13

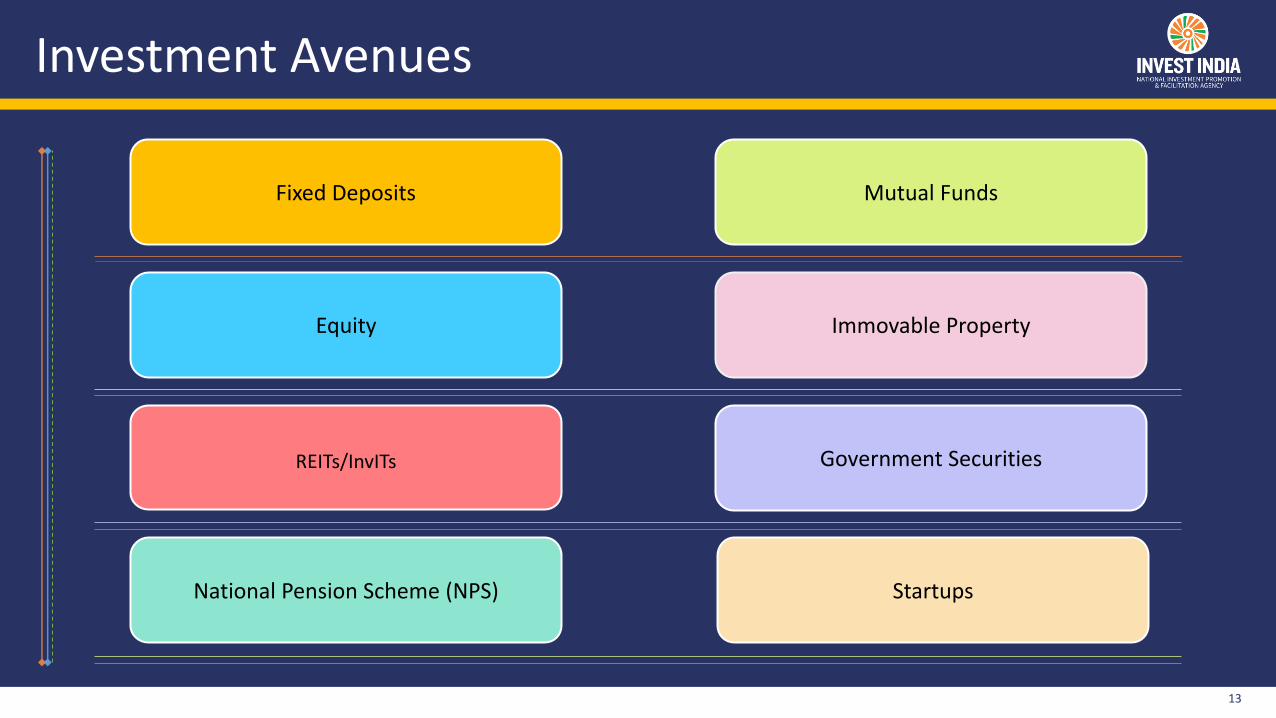

Fixed Deposits

REITs/InvITs

National Pension Scheme (NPS)

Mutual Funds

Immovable Property

Government Securities

Startups

1414

Mutual Funds

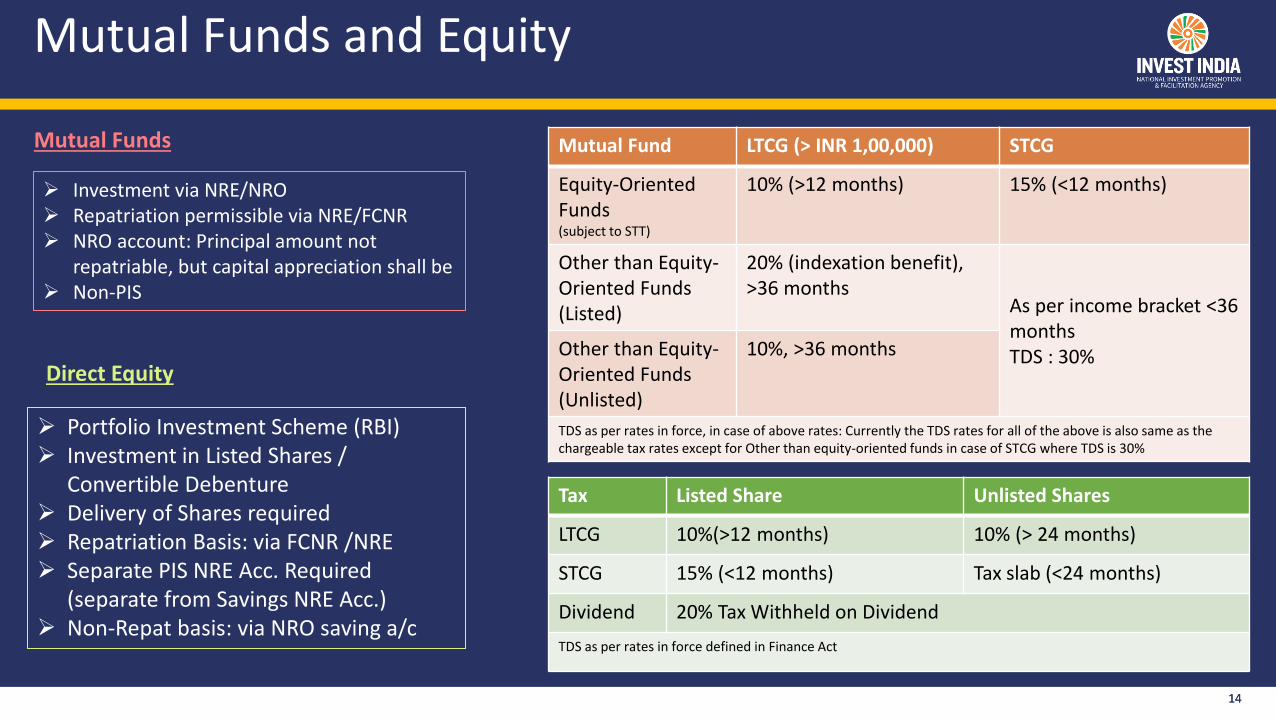

Mutual Funds and Equity

Mutual Fund LTCG (> INR 1,00,000) STCG

Equity-Oriented Funds (subject to STT)

10% (>12 months) 15% (<12 months)

Other than Equity-Oriented Funds (Listed)

20% (indexation benefit), >36 months

As per income bracket <36 monthsTDS : 30%Other than Equity-

Oriented Funds (Unlisted)

10%, >36 months

TDS as per rates in force, in case of above rates: Currently the TDS rates for all of the above is also same as the chargeable tax rates except for Other than equity-oriented funds in case of STCG where TDS is 30%

Direct Equity

Tax Listed Share Unlisted Shares

LTCG 10%(>12 months) 10% (> 24 months)

STCG 15% (<12 months) Tax slab (<24 months)

Dividend 20% Tax Withheld on Dividend

TDS as per rates in force defined in Finance Act

➢ Investment via NRE/NRO➢ Repatriation permissible via NRE/FCNR➢ NRO account: Principal amount not

repatriable, but capital appreciation shall be➢ Non-PIS

➢ Portfolio Investment Scheme (RBI)➢ Investment in Listed Shares /

Convertible Debenture➢ Delivery of Shares required➢ Repatriation Basis: via FCNR /NRE➢ Separate PIS NRE Acc. Required

(separate from Savings NRE Acc.)➢ Non-Repat basis: via NRO saving a/c

15

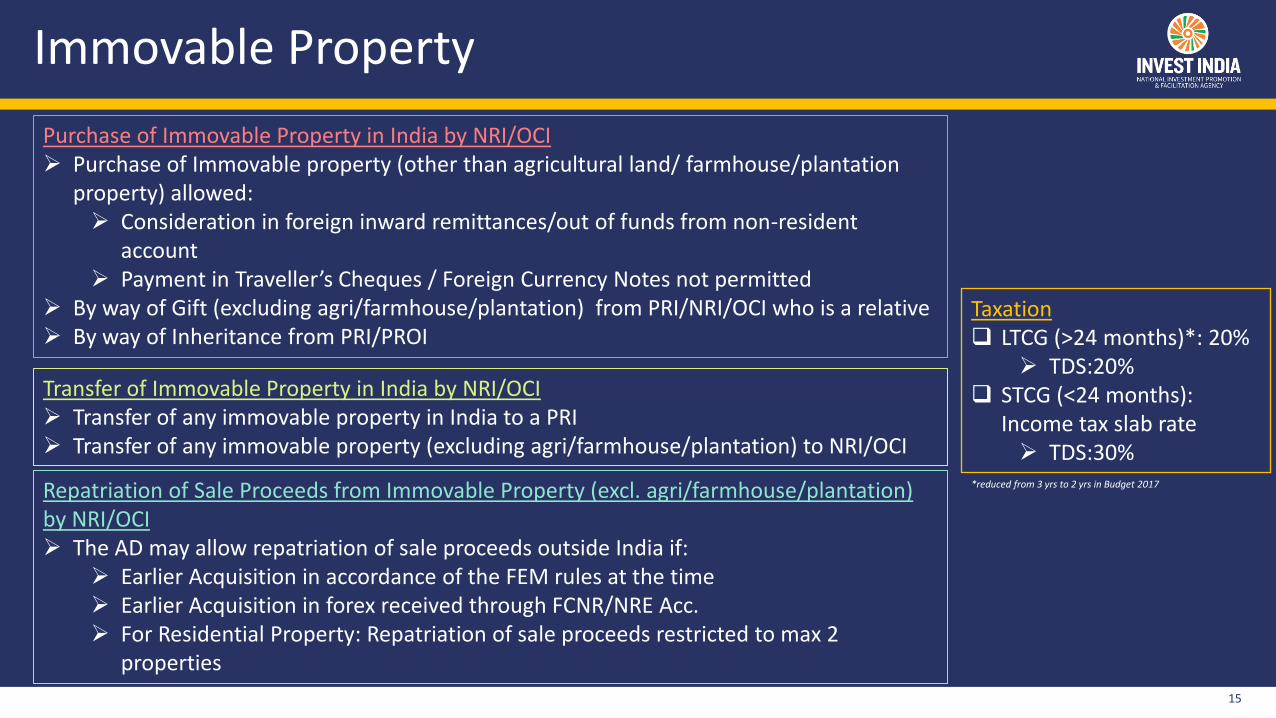

Immovable Property

Purchase of Immovable Property in India by NRI/OCI➢ Purchase of Immovable property (other than agricultural land/ farmhouse/plantation

property) allowed:➢ Consideration in foreign inward remittances/out of funds from non-resident

account➢ Payment in Traveller’s Cheques / Foreign Currency Notes not permitted

➢ By way of Gift (excluding agri/farmhouse/plantation) from PRI/NRI/OCI who is a relative ➢ By way of Inheritance from PRI/PROI

Taxation❑ LTCG (>24 months)*: 20%

➢ TDS:20%❑ STCG (<24 months):

Income tax slab rate➢ TDS:30%

*reduced from 3 yrs to 2 yrs in Budget 2017

Transfer of Immovable Property in India by NRI/OCI➢ Transfer of any immovable property in India to a PRI➢ Transfer of any immovable property (excluding agri/farmhouse/plantation) to NRI/OCI

Repatriation of Sale Proceeds from Immovable Property (excl. agri/farmhouse/plantation) by NRI/OCI➢ The AD may allow repatriation of sale proceeds outside India if:

➢ Earlier Acquisition in accordance of the FEM rules at the time➢ Earlier Acquisition in forex received through FCNR/NRE Acc.➢ For Residential Property: Repatriation of sale proceeds restricted to max 2

properties

16

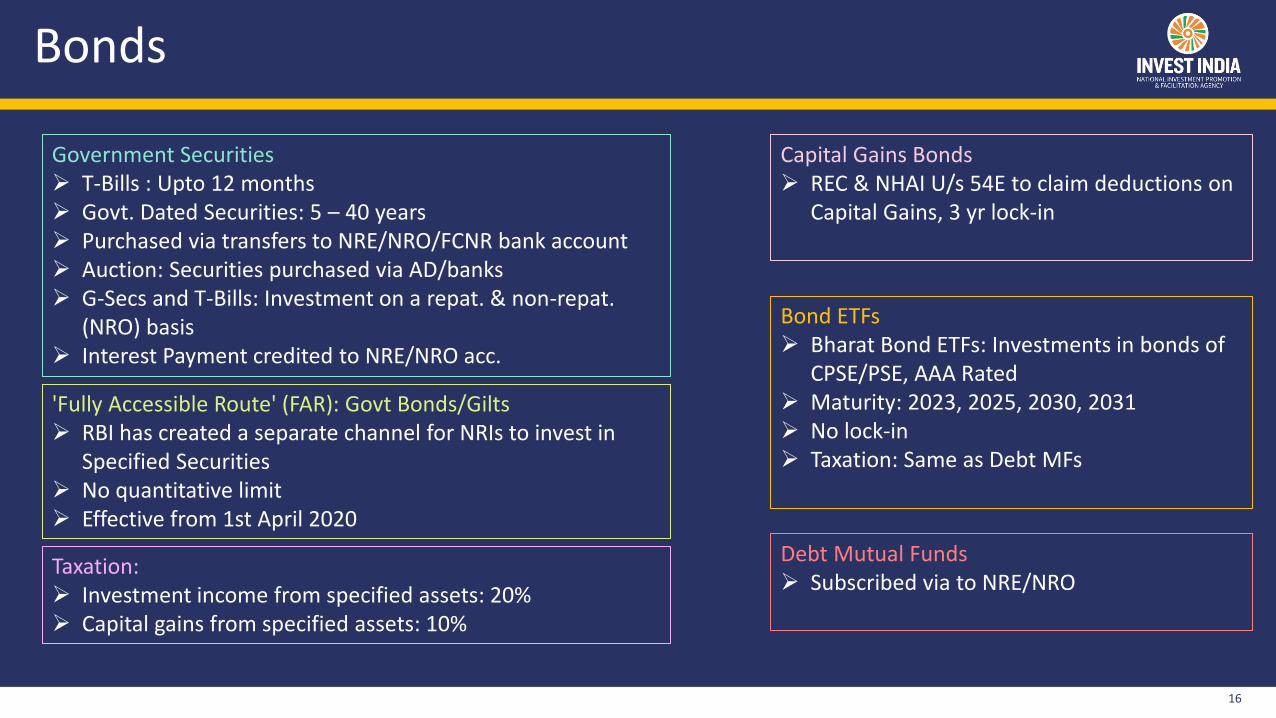

Bonds

Taxation:➢ Investment income from specified assets: 20%➢ Capital gains from specified assets: 10%

'Fully Accessible Route' (FAR): Govt Bonds/Gilts➢ RBI has created a separate channel for NRIs to invest in

Specified Securities➢ No quantitative limit➢ Effective from 1st April 2020

Capital Gains Bonds➢ REC & NHAI U/s 54E to claim deductions on

Capital Gains, 3 yr lock-in

Bond ETFs➢ Bharat Bond ETFs: Investments in bonds of

CPSE/PSE, AAA Rated➢ Maturity: 2023, 2025, 2030, 2031➢ No lock-in➢ Taxation: Same as Debt MFs

Debt Mutual Funds➢ Subscribed via to NRE/NRO

Government Securities➢ T-Bills : Upto 12 months➢ Govt. Dated Securities: 5 – 40 years➢ Purchased via transfers to NRE/NRO/FCNR bank account➢ Auction: Securities purchased via AD/banks ➢ G-Secs and T-Bills: Investment on a repat. & non-repat.

(NRO) basis➢ Interest Payment credited to NRE/NRO acc.

17

National Pension Scheme

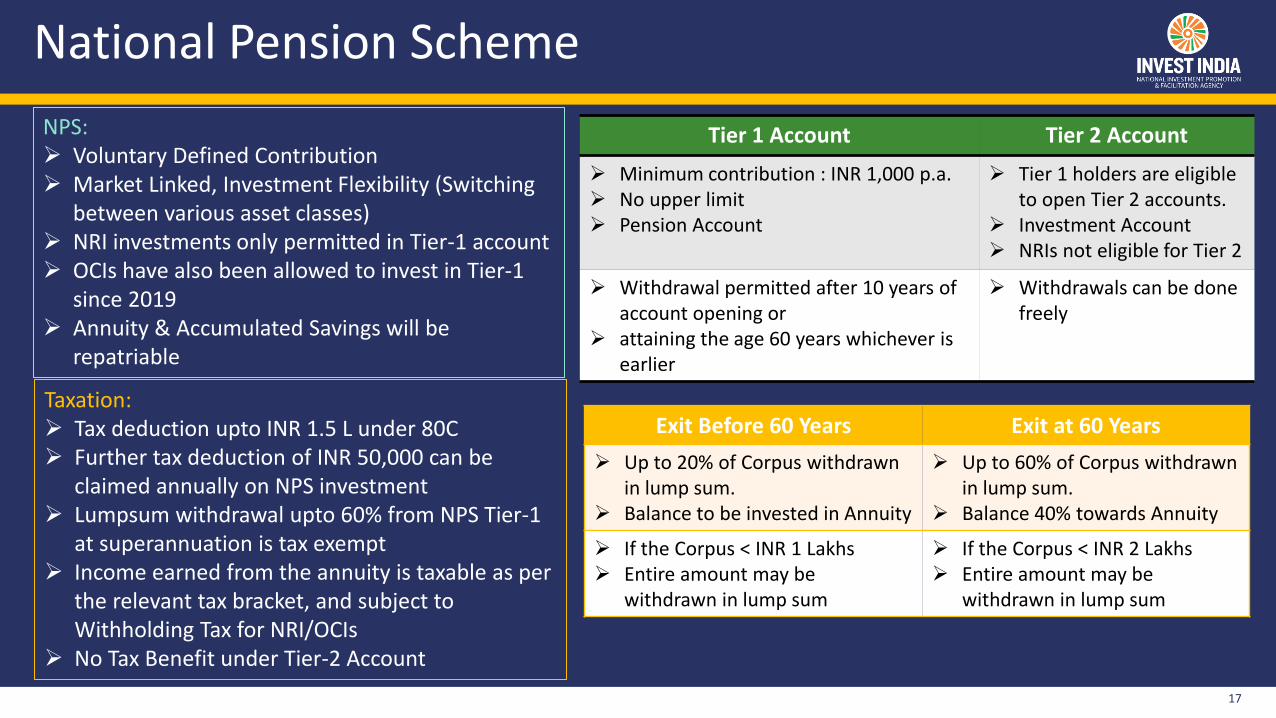

Tier 1 Account Tier 2 Account

➢ Minimum contribution : INR 1,000 p.a. ➢ No upper limit ➢ Pension Account

➢ Tier 1 holders are eligible to open Tier 2 accounts.

➢ Investment Account➢ NRIs not eligible for Tier 2

➢ Withdrawal permitted after 10 years of account opening or

➢ attaining the age 60 years whichever is earlier

➢ Withdrawals can be done freely

Taxation: ➢ Tax deduction upto INR 1.5 L under 80C➢ Further tax deduction of INR 50,000 can be

claimed annually on NPS investment➢ Lumpsum withdrawal upto 60% from NPS Tier-1

at superannuation is tax exempt➢ Income earned from the annuity is taxable as per

the relevant tax bracket, and subject to Withholding Tax for NRI/OCIs

➢ No Tax Benefit under Tier-2 Account

NPS:➢ Voluntary Defined Contribution➢ Market Linked, Investment Flexibility (Switching

between various asset classes)➢ NRI investments only permitted in Tier-1 account➢ OCIs have also been allowed to invest in Tier-1

since 2019➢ Annuity & Accumulated Savings will be

repatriable

Exit Before 60 Years Exit at 60 Years

➢ Up to 20% of Corpus withdrawn in lump sum.

➢ Balance to be invested in Annuity

➢ Up to 60% of Corpus withdrawn in lump sum.

➢ Balance 40% towards Annuity

➢ If the Corpus < INR 1 Lakhs➢ Entire amount may be

withdrawn in lump sum

➢ If the Corpus < INR 2 Lakhs➢ Entire amount may be

withdrawn in lump sum

1818

REITs/InvITs

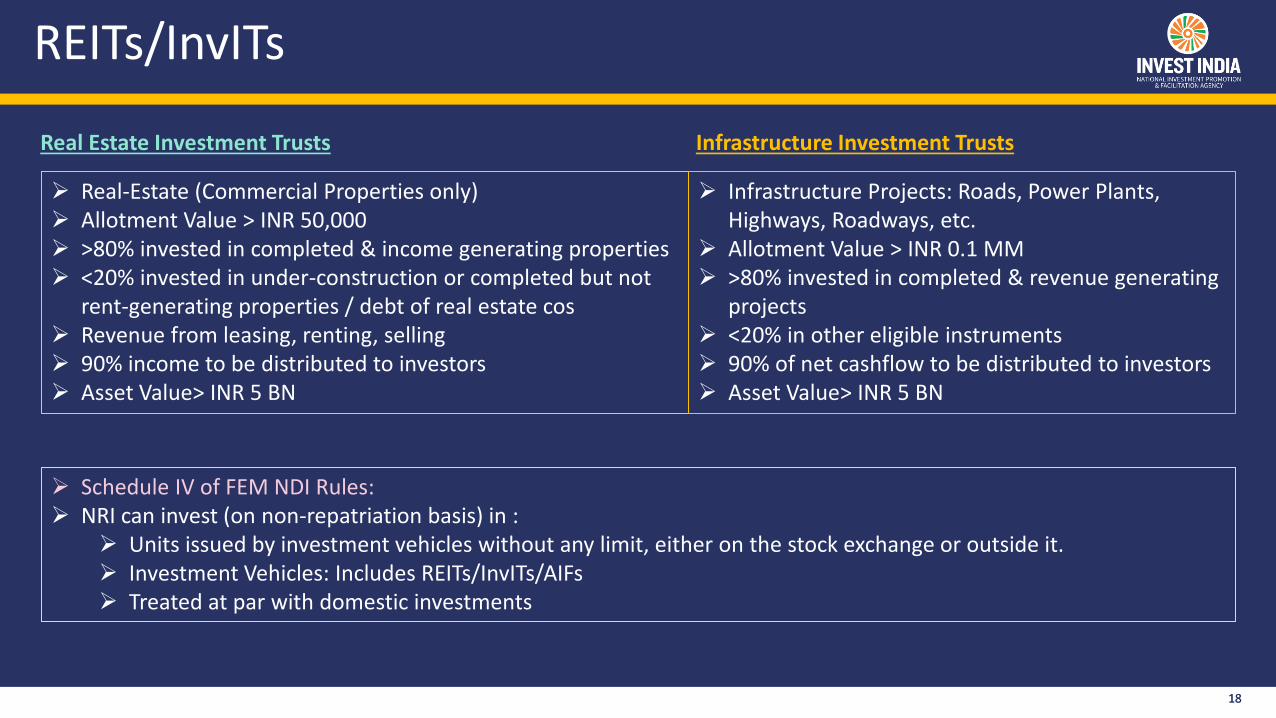

Real Estate Investment Trusts Infrastructure Investment Trusts

➢ Real-Estate (Commercial Properties only)➢ Allotment Value > INR 50,000➢ >80% invested in completed & income generating properties➢ <20% invested in under-construction or completed but not

rent-generating properties / debt of real estate cos➢ Revenue from leasing, renting, selling➢ 90% income to be distributed to investors➢ Asset Value> INR 5 BN

➢ Infrastructure Projects: Roads, Power Plants, Highways, Roadways, etc.

➢ Allotment Value > INR 0.1 MM➢ >80% invested in completed & revenue generating

projects➢ <20% in other eligible instruments➢ 90% of net cashflow to be distributed to investors➢ Asset Value> INR 5 BN

➢ Schedule IV of FEM NDI Rules: ➢ NRI can invest (on non-repatriation basis) in :

➢ Units issued by investment vehicles without any limit, either on the stock exchange or outside it.➢ Investment Vehicles: Includes REITs/InvITs/AIFs➢ Treated at par with domestic investments

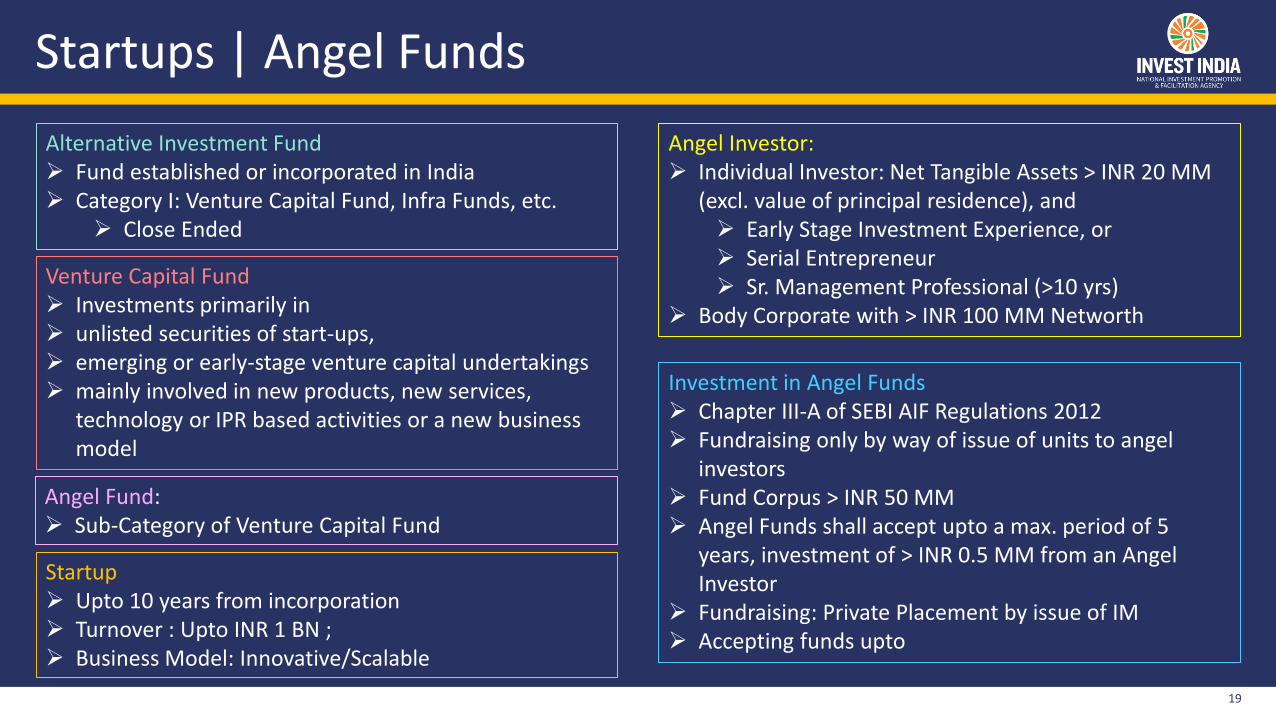

Startups | Angel Funds

19

Angel Investor:➢ Individual Investor: Net Tangible Assets > INR 20 MM

(excl. value of principal residence), and➢ Early Stage Investment Experience, or➢ Serial Entrepreneur➢ Sr. Management Professional (>10 yrs)

➢ Body Corporate with > INR 100 MM Networth

Alternative Investment Fund➢ Fund established or incorporated in India➢ Category I: Venture Capital Fund, Infra Funds, etc.

➢ Close Ended

Angel Fund: ➢ Sub-Category of Venture Capital Fund

Startup➢ Upto 10 years from incorporation➢ Turnover : Upto INR 1 BN ; ➢ Business Model: Innovative/Scalable

Venture Capital Fund➢ Investments primarily in ➢ unlisted securities of start-ups, ➢ emerging or early-stage venture capital undertakings➢ mainly involved in new products, new services,

technology or IPR based activities or a new business model

Investment in Angel Funds➢ Chapter III-A of SEBI AIF Regulations 2012➢ Fundraising only by way of issue of units to angel

investors➢ Fund Corpus > INR 50 MM➢ Angel Funds shall accept upto a max. period of 5

years, investment of > INR 0.5 MM from an Angel Investor

➢ Fundraising: Private Placement by issue of IM➢ Accepting funds upto

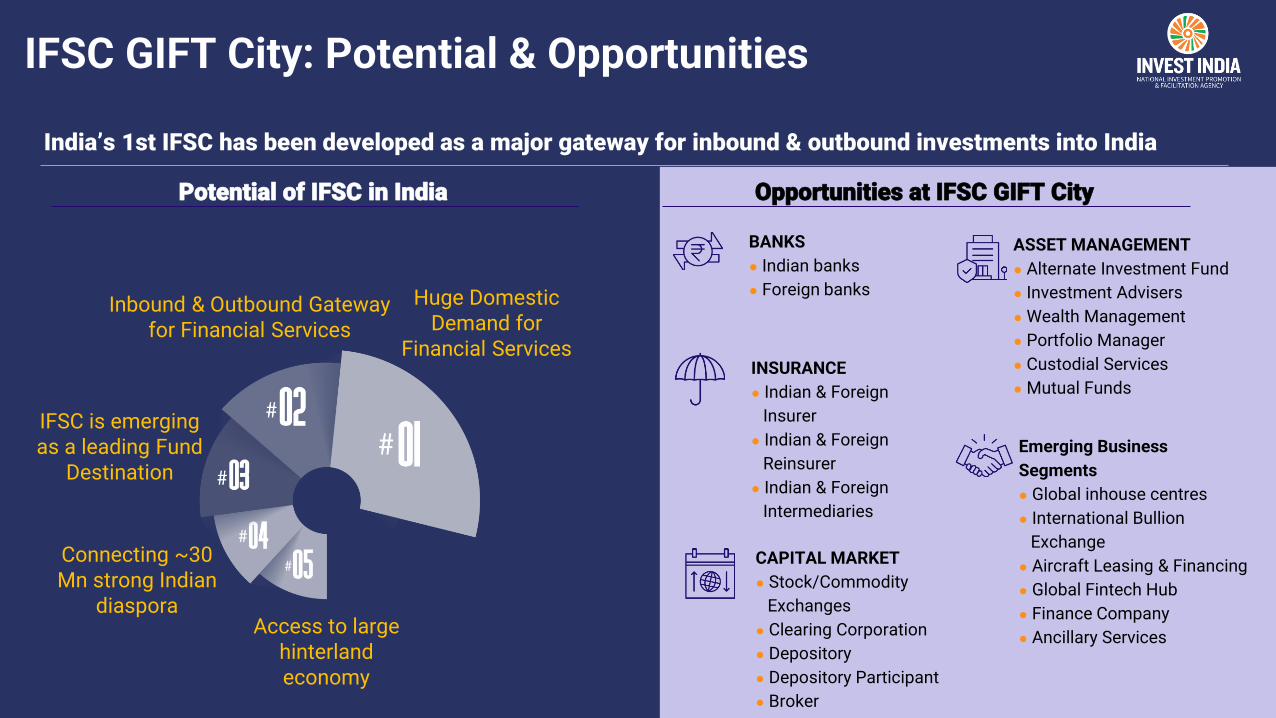

IFSC GIFT City: Potential & Opportunities

Huge Domestic Demand for

Financial Services

Connecting ~30 Mn strong Indian

diasporaAccess to large

hinterland economy

Inbound & Outbound Gateway for Financial Services

IFSC is emerging as a leading Fund

Destination

India’s 1st IFSC has been developed as a major gateway for inbound & outbound investments into India

Potential of IFSC in India Opportunities at IFSC GIFT City

BANKS

● Indian banks

● Foreign banks

CAPITAL MARKET

● Stock/Commodity

Exchanges

● Clearing Corporation

● Depository

● Depository Participant

● Broker

INSURANCE

● Indian & Foreign

Insurer

● Indian & Foreign

Reinsurer

● Indian & Foreign

Intermediaries

Emerging Business

Segments

● Global inhouse centres

● International Bullion

Exchange

● Aircraft Leasing & Financing

● Global Fintech Hub

● Finance Company

● Ancillary Services

ASSET MANAGEMENT

● Alternate Investment Fund

● Investment Advisers

● Wealth Management

● Portfolio Manager

● Custodial Services

● Mutual Funds

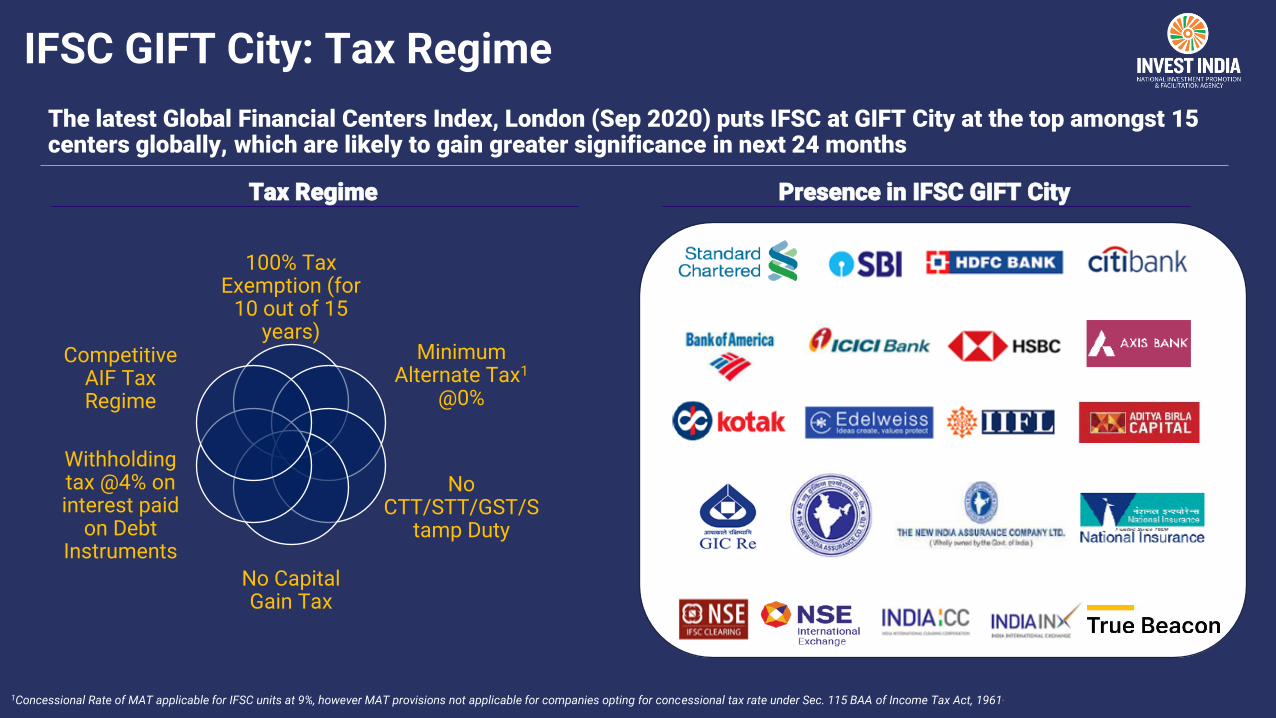

IFSC GIFT City: Tax Regime

The latest Global Financial Centers Index, London (Sep 2020) puts IFSC at GIFT City at the top amongst 15 centers globally, which are likely to gain greater significance in next 24 months

100% Tax Exemption (for

10 out of 15 years)

Minimum Alternate Tax1

@0%

No CTT/STT/GST/S

tamp Duty

No Capital Gain Tax

Withholding tax @4% on interest paid

on Debt Instruments

Competitive AIF Tax Regime

1Concessional Rate of MAT applicable for IFSC units at 9%, however MAT provisions not applicable for companies opting for concessional tax rate under Sec. 115 BAA of Income Tax Act, 1961.

Tax Regime Presence in IFSC GIFT City

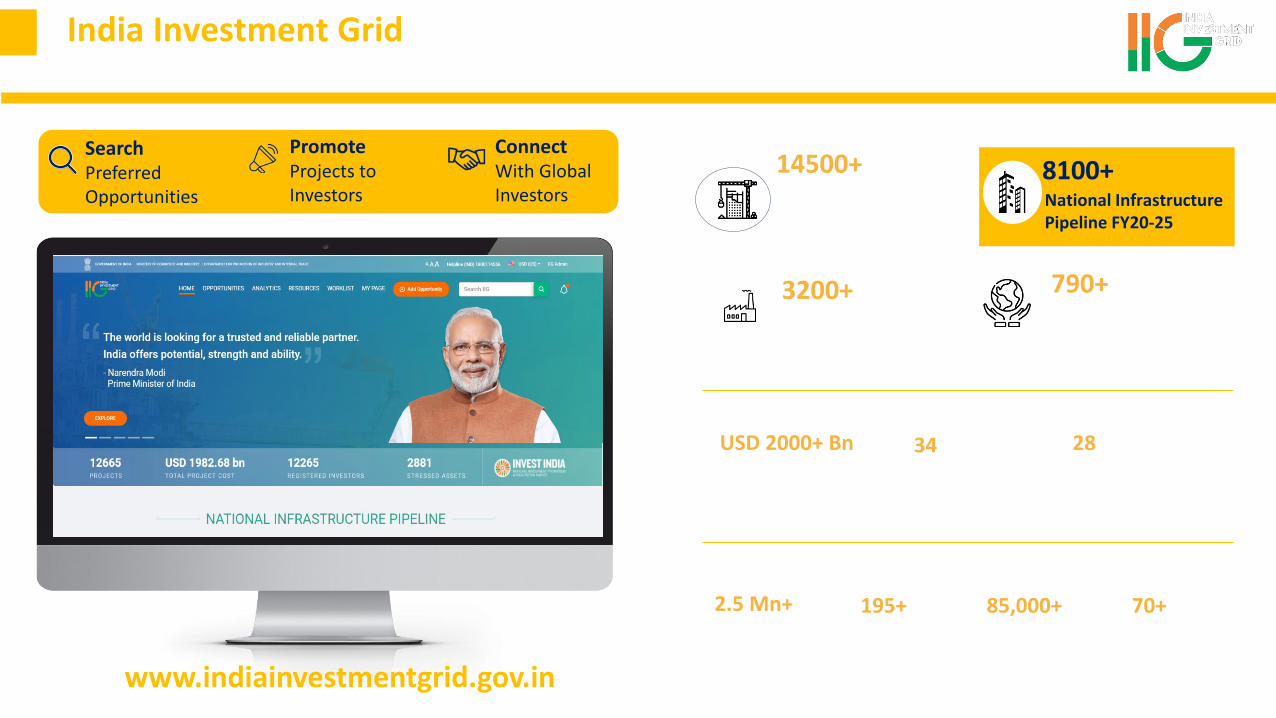

India Investment Grid

Stressed AssetsIncl. companies under IBC

14500+ Projects

3200+ 790+

8100+ National InfrastructurePipeline FY20-25Greenfield & Brownfield

USD 2000+ BnProject Cost

2.5 Mn+Page Views

195+Countries

CSR Projects

SDG projects

85,000+Twitter Followers

www.indiainvestmentgrid.gov.in

70+Embassies& Missions

Connect With GlobalInvestors

SearchPreferred Opportunities

Promote Projects to Investors

A Pan-India Repository of Opportunities

34Infra sub-sectors

28Non-infra sub-sectors

Invest India: National Investment Promotion & Facilitation Agency

23

Government Industry

Centre / States

Foreign Missions / Agencies

Associations / Corporates

Professional Advisors / Academia

Awareness & Engagement

Business AdvisoryStrategy &

ImplementationInvestor Aftercare Long term partnership

Opportunity AssessmentPartner / Location Search

Market StrategyRegulatory Clearances

Policy GuidanceIssue Redressal Continuous Engagements

UNCTAD Award 2016, 2018, 2020

Indian Ocean Rim Association

Investment Award 2016

AIM UAE : Best Investment Project

Award : 2016 - 2020

Annexure

24

India Investment Grid Finding an Opportunity

Foreign Direct Investment In India

26

Notes*For detailed definition, clarifications/ exceptions, please refer to Consolidated FDI Policy**Activities under this included sector are as follows: a) Floriculture, Horticulture, and Cultivation of Vegetables & Mushrooms under controlled conditions; b) Development and Production of seeds and planting material; c) Animal Husbandry (including breeding of dogs), Pisciculture, Aquaculture, Apiculture; and d) Services related to agro and allied sectors. Other than the activities provided under this head in the FDI Policy (as listed above), foreign investment is not allowed in any other agricultural sector/ activity.***FDI up to 100% has been permitted under the automatic route for sale of coal, for coal mining activities including associated processing and now, foreign players would be permitted to mine coal and sell the same. This change shall become effective as on the date of the respective FEMA notification****Construction Development: development of townships, construction of residential/commercial premises, roads or bridges, hotels, resorts, hospitals, educational institutions, recreational facilities, city and regional level infrastructure, townships, Real estate Broking business*****Air Transport Services- Non Scheduled Air Transport Service / Helicopters services/ seaplane services requiring DGCA approval (please refer PN2, 2020), FEMA Notification has been released as on 27 July 2020******Other services include ground Handling Services subject to sectoral regulations and security clearance & Maintenance and Repair organizations; flying training institutes; and technical training institutions*******Market place model of e-commerce’ means providing of an information technology platform by an e-commerce entity on a digital & electronic network to act as a facilitator between buyer and seller********Any financial services activity which are regulated by any Financial Sector Regulator, foreign investment up to 100% will be allowed under Automatic route*********This sector has now been removed per the FEMA notification and subsumed under the Financial Services sector, but the same continues to exist under the FDI Policy. Both are permitted under the 100% automatic route**********Per Press Note No. 4 (2019), contract manufacturing has been specifically covered under manufacturing and accordingly, manufacturing activities is now permitted under 100% automatic route, which can be undertaken either by the investee entity itself or through contract manufacturing in India under a legally tenable contract, whether on Principal to Principal or Principal to Agent basis. This change shall become effective as on the date of the respective FEMA notification***********Per Press Note No. 1 (2020), Intermediaries or Insurance Intermediaries including insurance brokers, re-insurance brokers, insurance consultants, corporate agents, third party administrators, Surveyors and Loss Assessors and such other entities, as may be notified by the Insurance Regulatory Authority of India

from time to time. Refer to the Press Note 1 (2020) & Press Note 2 (2021)

Category 1 : 100% FDI permitted through Automatic route*

Pharmaceuticals – Greenfield Sector and Medical device manufacturing

Industrial Park

Check for FDI routing procedures in India

Railway Infrastructure (as defined under Para 5.2.16 of

the Consolidated FDI Policy )

Other Services at Airport ******

Exploration of Petroleum & Natural Gas (including marketing of

petroleum products & natural gas)

Up-link of non-’News & Current Affairs’ TV Channels, Down linking

of TV channel

Other Financial Services (registered/

regulated entity)********

Agriculture & Animal Husbandry**

Plantation (FDI is allowed only in Tea, Coffee, Rubber, Cardamom, Palm oil tree, Olive oil tree

and not in any other plantation activity)

Mining & Exploration of metals & non-metals ores excluding titanium bearing

minerals and its ores

Coal & Lignite mining in respect of

eligible activities (including captive

consumption)***

Cash & Carry Wholesale Trading

Construction Development projects****

Transport services*****

Broadcasting Carriage Services

Market Place E-commerce Activities*******

Asset Reconstruction & Credit Information Companies

White Label ATM Operations*********

Single Brand Retail Trading, Duty Free

Shops

Civil Aviation – Greenfield & Brownfield

Manufacturing**********Insurance intermediaries

***********

Foreign Direct Investment In India

Category 2 : 100% FDI permitted through Government Route

Publishing/ printing of scientific and technical magazines/specialty journals/ periodicals

Mining and minerals separation of titanium bearing minerals & ores

and its value addition & integrated activities

Retail Trading including through e-commerce in respect of food products manufactured and/ or produced in

India

Satellites-establishment and operations

Publication of facsimile edition of foreign newspapers

Government Route (Approval from various Administrative Ministries/ Government Department)*

*For detailed definition, clarifications/ exceptions, please refer to Consolidated FDI Policy

Foreign investment in core investment companies (CIC) and other investing companies, engaged in the activity of investing in the capital of other company/ies/LLP, is permitted under Govt. approval route. CICs will additionally have to follow RBI regulatory framework

Check for FDI routing procedures in India

Foreign Direct Investment In India

Telecom Services*

Defence industry**

Pharmaceutical -Brownfield

Air Transport Services ***

Banking –Private Sector

Private Security Agencies****

Up to

Up to

Up to

Up to

Up to

Up to

49% Automatic route Above 49% Government route

74% Automatic route Above 74% Government route

74% Automatic route Above 74% Government route

49% Automatic route Above 49% Government route

49% Automatic route Above 49% Government route

49% Automatic route Above 49% Government route

Up to 74%

Up to 74%

For detailed definition, clarifications/ exceptions, please refer to Consolidated FDI Policy.

* All telecom services including Telecom Infrastructure Providers Category-I, viz. Basic, Cellular, United Access Services, Unified License (Access Services), Unified License, National/International Long Distance, Commercial V-Sat, Public Mobile Radio Trunked Services (PMRTS), Global Mobile Personal Communications Services (GMPCS), All types of ISP licenses, Voice Mail/Audio text/UMS, Resale of IPLC, Mobile Number Portability Services, Infrastructure Provider Category-I (providing dark fibre, right of way, duct space, tower) except Other Service Providers.**Government route beyond 74% wherever it is likely to result in access to modern technology or for other reasons to be recorded. Refer the egazette notification

*** Air Transport Services- Scheduled Air Transport Service/ Domestic Scheduled Passenger Airline; Regional Air Transport Service. Up to 100% allowed under automatic route for NRI’s (Refer to PN2, 2020), FEMA Notification has been released as on 27 July 2020**** FDI in Private Security Agencies is subject to compliance with Private Security Agencies (Regulation) (PSAR) Act, 2005, as amended from time to time. Please note that this sector has not been notified per the FEMA notification and currently only appears in the Consolidated FDI Policy. This change shall become effective as on the date of the respective FEMA notification.

Category 3 : Up to 100% FDI permitted through Government + Automatic routeCheck for FDI routing procedures in India

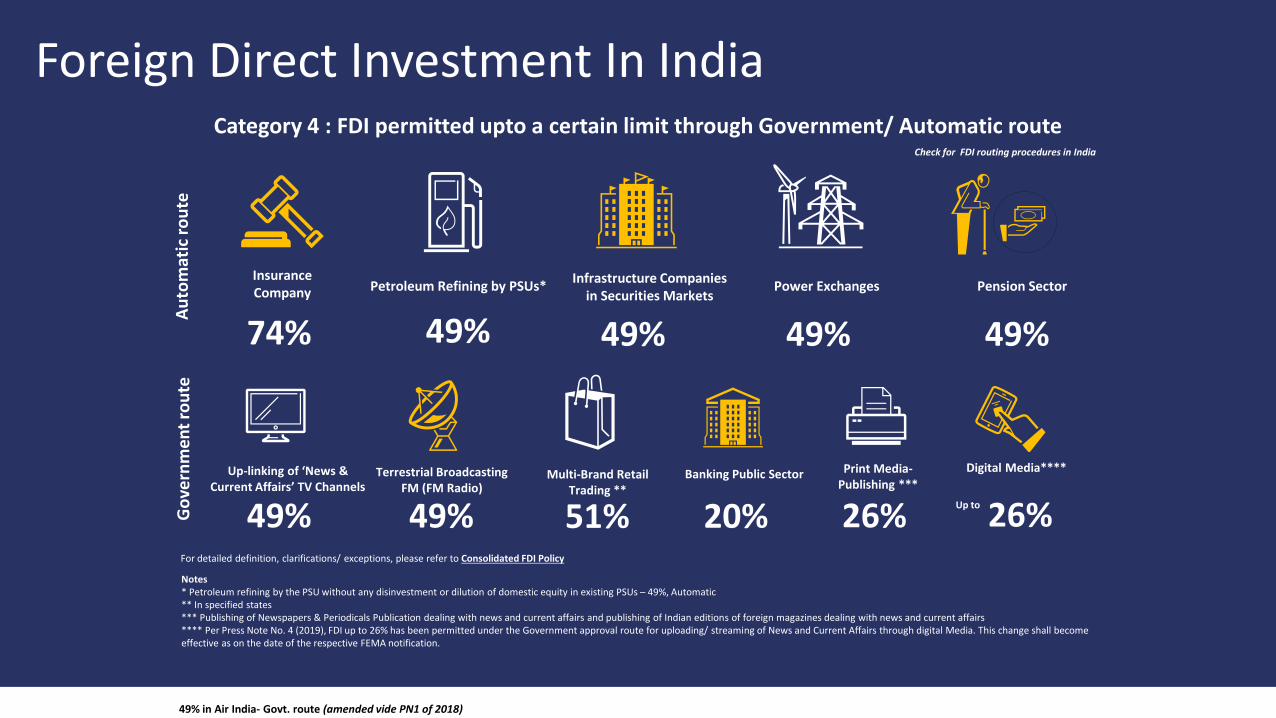

Foreign Direct Investment In India

Au

tom

atic

ro

ute

Insurance Company Petroleum Refining by PSUs*

Infrastructure Companies in Securities Markets

Power Exchanges Pension Sector

74% 49% 49% 49% 49%

Up-linking of ‘News & Current Affairs’ TV Channels

Terrestrial Broadcasting FM (FM Radio)

Multi-Brand Retail Trading **

Banking Public Sector Print Media-Publishing ***

49% 49% 51% 20% 26%Go

vern

men

t ro

ute

For detailed definition, clarifications/ exceptions, please refer to Consolidated FDI Policy

Category 4 : FDI permitted upto a certain limit through Government/ Automatic route

Notes* Petroleum refining by the PSU without any disinvestment or dilution of domestic equity in existing PSUs – 49%, Automatic ** In specified states *** Publishing of Newspapers & Periodicals Publication dealing with news and current affairs and publishing of Indian editions of foreign magazines dealing with news and current affairs**** Per Press Note No. 4 (2019), FDI up to 26% has been permitted under the Government approval route for uploading/ streaming of News and Current Affairs through digital Media. This change shall become effective as on the date of the respective FEMA notification.

49% in Air India- Govt. route (amended vide PN1 of 2018)

Check for FDI routing procedures in India

Digital Media****

26%Up to

Foreign Direct Investment In India

Lottery Business including Government/private lottery,

online lotteries , etc.*

Gambling and Betting including casinos* Chit funds Nidhi company

Trading in Transferable Development Rights (TDR)

Real Estate Business or Construction of farm

houses**

Manufacturing of cigars, cheroots, cigarillos and

cigarettes, of tobacco or of tobacco substitutes

Sectors not open to private sector investment- atomic energy, railway operations

(other than permitted activities mentioned under

the Consolidated FDI policy)

Notes

*Foreign technology collaboration in any form including licensing for franchise, trademark, brand name, management contract is also prohibited for Lottery Business and Gambling andBetting activities

**Real estate business shall not include development of townships, construction of residential/ commercial premises, roads or bridges and Real Estate Investment Trusts (REITs)registered and regulated under the SEBI (REITs) Regulations, 2014

A non-resident entity can invest in India, subject to the FDI Policy except in those sectors/activities which are prohibited. However, an entity of a country, which shares a land border withIndia or where the beneficial owner of investment into India is situated in or is a citizen of any such country, can invest only under the Government route. Further, a citizen of Pakistan oran entity incorporated in Pakistan can invest, only under the Government route, in sectors/activities other than defence, space, atomic energy and sectors/activities prohibited for foreigninvestment. Please refer Press Note 3.

Prohibited Sectors

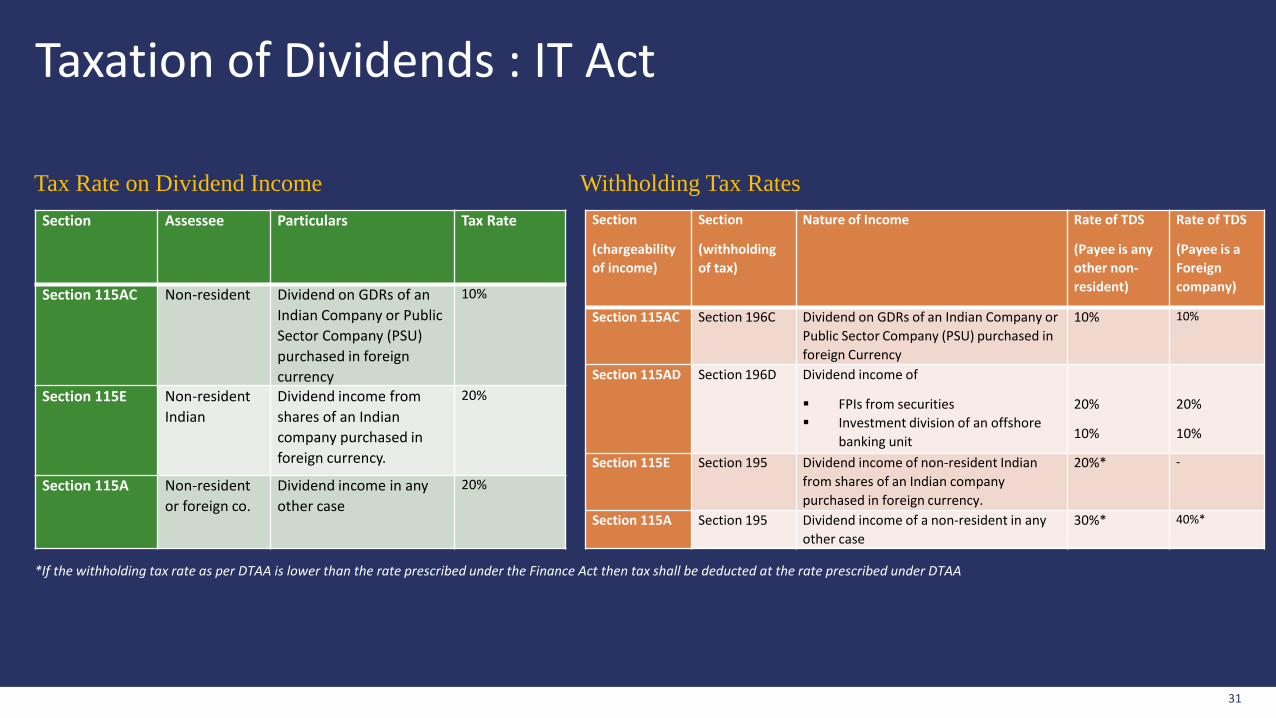

Taxation of Dividends : IT Act

31

Section Assessee Particulars Tax Rate

Section 115AC Non-resident Dividend on GDRs of an

Indian Company or Public

Sector Company (PSU)

purchased in foreign

currency

10%

Section 115E Non-resident

Indian

Dividend income from

shares of an Indian

company purchased in

foreign currency.

20%

Section 115A Non-resident

or foreign co.

Dividend income in any

other case

20%

Tax Rate on Dividend Income

Section

(chargeability

of income)

Section

(withholding

of tax)

Nature of Income Rate of TDS

(Payee is any

other non-

resident)

Rate of TDS

(Payee is a

Foreign

company)

Section 115AC Section 196C Dividend on GDRs of an Indian Company or

Public Sector Company (PSU) purchased in

foreign Currency

10% 10%

Section 115AD Section 196D Dividend income of

▪ FPIs from securities

▪ Investment division of an offshore

banking unit

20%

10%

20%

10%

Section 115E Section 195 Dividend income of non-resident Indian

from shares of an Indian company

purchased in foreign currency.

20%* -

Section 115A Section 195 Dividend income of a non-resident in any

other case

30%* 40%*

Withholding Tax Rates

*If the withholding tax rate as per DTAA is lower than the rate prescribed under the Finance Act then tax shall be deducted at the rate prescribed under DTAA

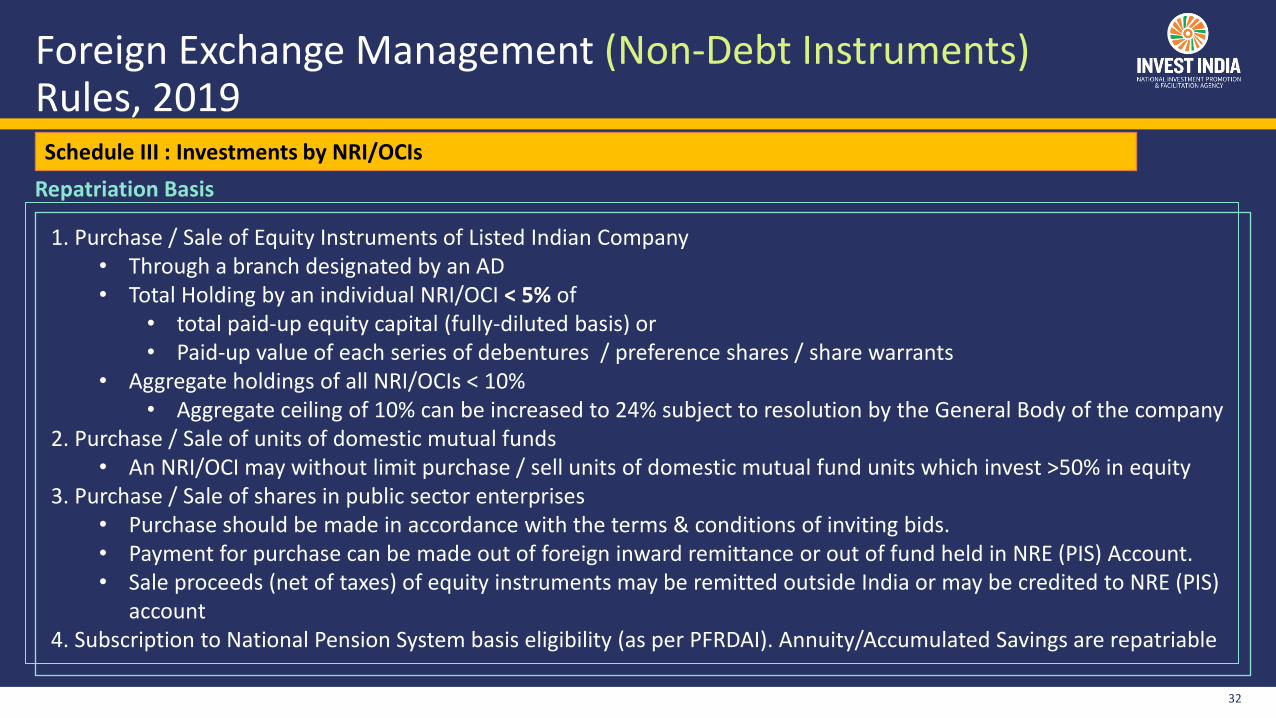

Foreign Exchange Management (Non-Debt Instruments) Rules, 2019

32

Schedule III : Investments by NRI/OCIs

1. Purchase / Sale of Equity Instruments of Listed Indian Company• Through a branch designated by an AD • Total Holding by an individual NRI/OCI < 5% of

• total paid-up equity capital (fully-diluted basis) or• Paid-up value of each series of debentures / preference shares / share warrants

• Aggregate holdings of all NRI/OCIs < 10%• Aggregate ceiling of 10% can be increased to 24% subject to resolution by the General Body of the company

2. Purchase / Sale of units of domestic mutual funds• An NRI/OCI may without limit purchase / sell units of domestic mutual fund units which invest >50% in equity

3. Purchase / Sale of shares in public sector enterprises• Purchase should be made in accordance with the terms & conditions of inviting bids. • Payment for purchase can be made out of foreign inward remittance or out of fund held in NRE (PIS) Account. • Sale proceeds (net of taxes) of equity instruments may be remitted outside India or may be credited to NRE (PIS)

account4. Subscription to National Pension System basis eligibility (as per PFRDAI). Annuity/Accumulated Savings are repatriable

Repatriation Basis

Foreign Exchange Management (Non-Debt Instruments) Rules, 2019

33

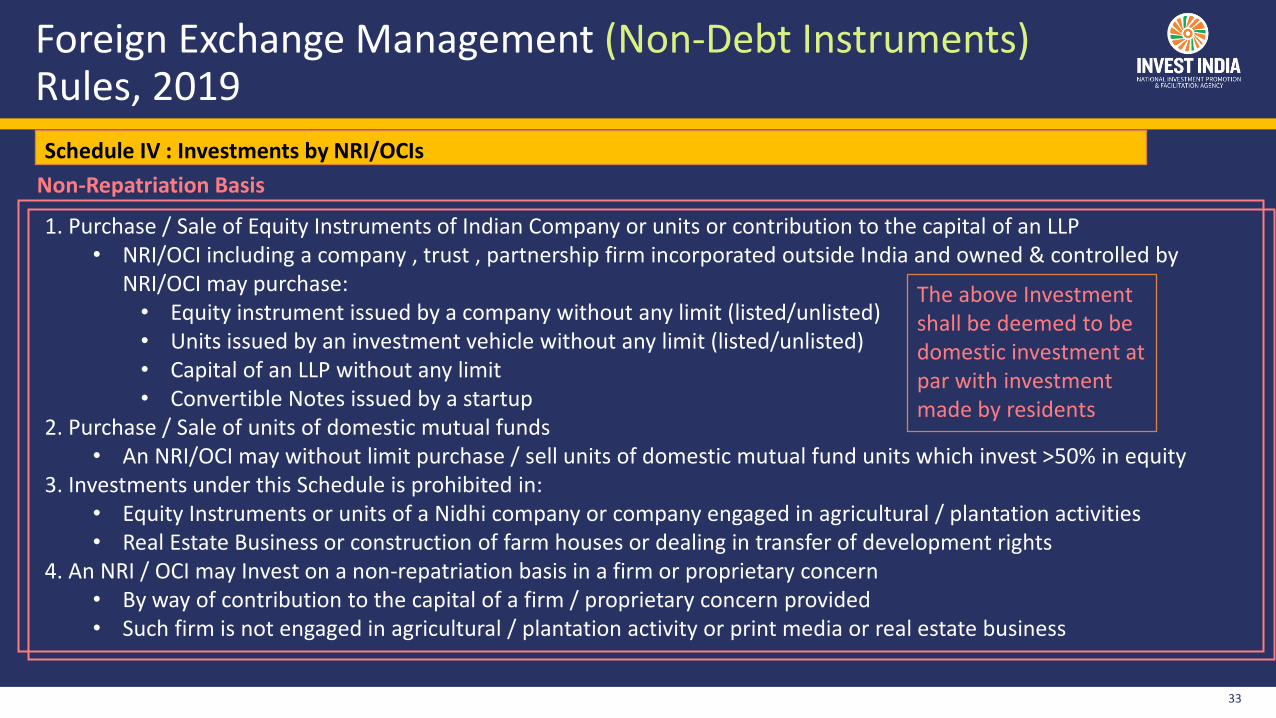

Schedule IV : Investments by NRI/OCIs

1. Purchase / Sale of Equity Instruments of Indian Company or units or contribution to the capital of an LLP• NRI/OCI including a company , trust , partnership firm incorporated outside India and owned & controlled by

NRI/OCI may purchase:• Equity instrument issued by a company without any limit (listed/unlisted)• Units issued by an investment vehicle without any limit (listed/unlisted)• Capital of an LLP without any limit• Convertible Notes issued by a startup

2. Purchase / Sale of units of domestic mutual funds• An NRI/OCI may without limit purchase / sell units of domestic mutual fund units which invest >50% in equity

3. Investments under this Schedule is prohibited in:• Equity Instruments or units of a Nidhi company or company engaged in agricultural / plantation activities• Real Estate Business or construction of farm houses or dealing in transfer of development rights

4. An NRI / OCI may Invest on a non-repatriation basis in a firm or proprietary concern• By way of contribution to the capital of a firm / proprietary concern provided• Such firm is not engaged in agricultural / plantation activity or print media or real estate business

The above Investment shall be deemed to be domestic investment at par with investment made by residents

Non-Repatriation Basis

Foreign Exchange Management (Debt Instruments) Regulations, 2019 - RBI

34

1. NRI/OCI may without limit purchase the following instruments• Government dated securities (other than bearer securities) or treasury bills or units of domestic

mutual funds or Exchange-Traded Funds (ETFs) which invest less than or equal to 50 percent in equity;• Bonds issued by a Public Sector Undertaking (PSU) in India;• Bonds issued by Infrastructure Debt Funds;• Listed non-convertible/ redeemable preference shares or debentures issued in terms of Regulation 6

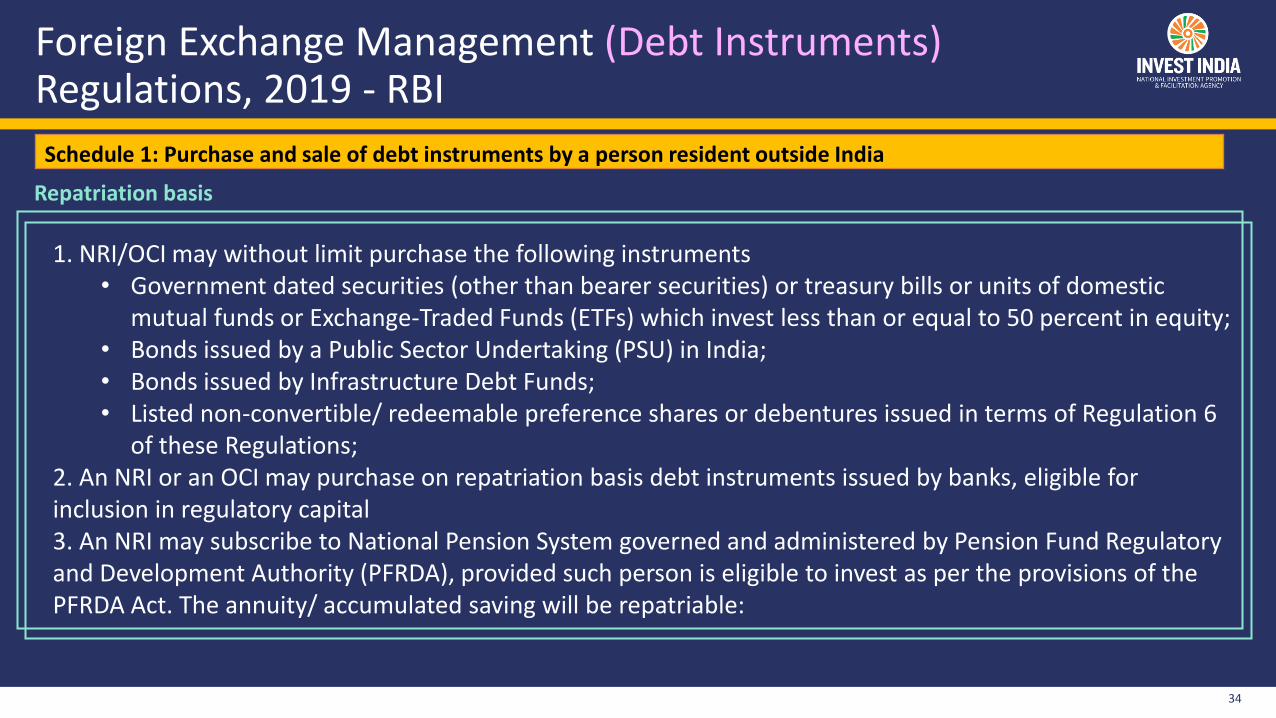

of these Regulations;2. An NRI or an OCI may purchase on repatriation basis debt instruments issued by banks, eligible for inclusion in regulatory capital3. An NRI may subscribe to National Pension System governed and administered by Pension Fund Regulatory and Development Authority (PFRDA), provided such person is eligible to invest as per the provisions of the PFRDA Act. The annuity/ accumulated saving will be repatriable:

Schedule 1: Purchase and sale of debt instruments by a person resident outside India

Repatriation basis

Foreign Exchange Management (Debt Instruments) Regulations, 2019 - RBI

35

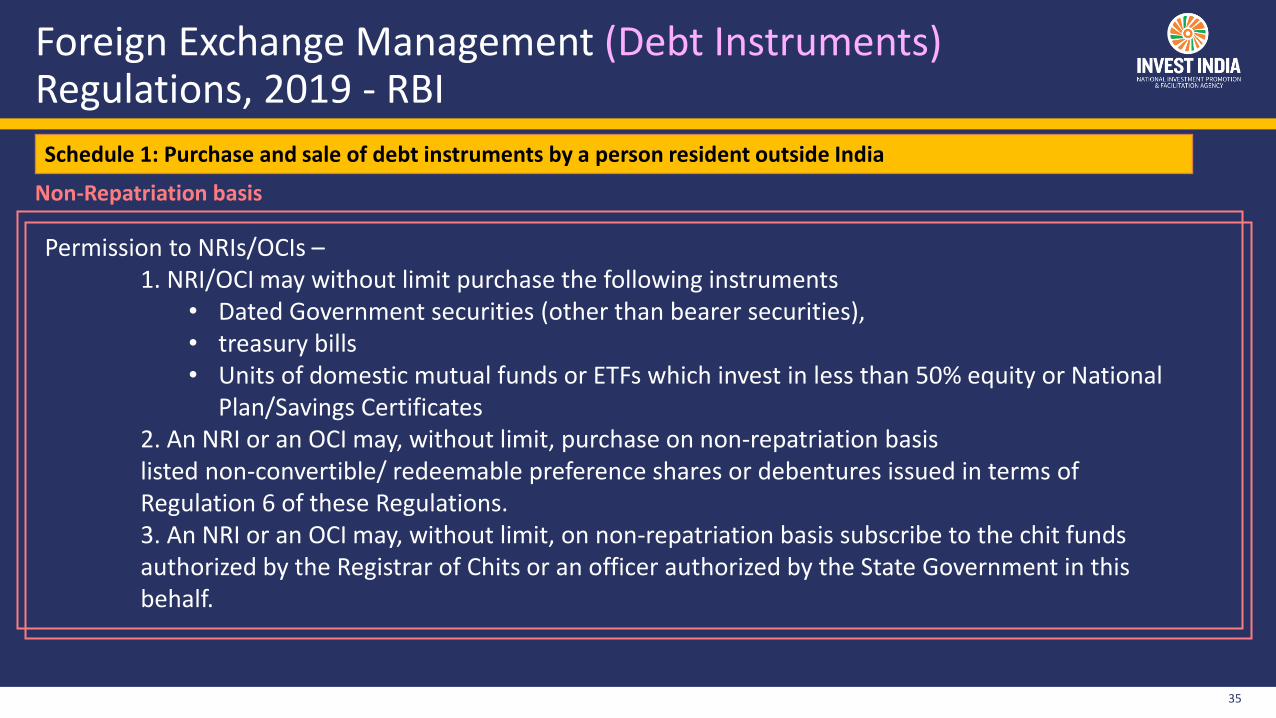

Permission to NRIs/OCIs –1. NRI/OCI may without limit purchase the following instruments

• Dated Government securities (other than bearer securities), • treasury bills• Units of domestic mutual funds or ETFs which invest in less than 50% equity or National

Plan/Savings Certificates 2. An NRI or an OCI may, without limit, purchase on non-repatriation basislisted non-convertible/ redeemable preference shares or debentures issued in terms of Regulation 6 of these Regulations.3. An NRI or an OCI may, without limit, on non-repatriation basis subscribe to the chit funds authorized by the Registrar of Chits or an officer authorized by the State Government in this behalf.

Schedule 1: Purchase and sale of debt instruments by a person resident outside India

Non-Repatriation basis

India-Canada Double Taxation Avoidance Agreement

Avoidance of double taxation:Article 23

❖ Unless a greater deductionor relief is provided underthe laws of Canada, taxpayable in India on profits,income or gains arising inIndia shall be deductedfrom any Canadian taxpayable in respect of suchprofits, income or gains.

Taxation of IncomePart III of the DTAA :❖ Income from immovable

property (Art. 6): Taxed incountry where property issituated

❖ Dividends (Art. 10), Interests(Art. 11):

❖ Dividend : Tax not to exceed 15%if Beneficial Owner hascontrolling interest of >10% individend paying company; elseTax not to exceed 25% in othercases.

❖ Capital Gains (Art. 13): Gainsfrom alienation of any property(except aircraft/ship related) maybe taxed in both countries

Please refer the relevant Taxation Acts for both countries & the DTAA for clarifications, detailed terms and regulations pertaining to the treatment of various taxes

Dividend➢ Tax rate under Sections

115A, 115E, 115AC, and 115AD

➢ TDS: Section 195➢ DTAA Rates: 15% or 25%

Interest➢ IT Act: Sections 193, 194LC,

and other applicable sections ➢ TDS: Section 195➢ DTAA Rates: 15%

Royalty➢ IT Act: Sec. 44DA, 115A➢ TDS: Section 195➢ DTAA Rates: 15-20%

37

@investindia @invest-india investindiaofficial @investindia2017

Rohan Goyal

Asst. Manager

Ishaan Jain

Manager

Shruti Chandra

Sr. AVP

Raghav Dhanuka

Manager

Invest India | Canada Desk: [email protected]

Priya Rawat

Vice President

www.investindia.gov.in/country/canada