Embed Size (px)

Citation preview

Inte

rnat

ion

al F

inan

ce a

nd

Gro

wth

in D

evel

opin

g C

oun

trie

s: W

hat

Hav

e W

e Le

arn

ed? Mau

rice

Obs

tfel

dU

nive

rsity

of C

alifo

rnia

, Ber

kele

yAp

ril 9

, 200

7

Out

line

of t

his

pres

enta

tion

!Tr

ends

in g

loba

l fin

anci

al in

tegr

atio

n!

Why

do

coun

trie

s se

em t

o pr

efer

fin

anci

al

open

ing?

!Th

e ris

k of

cris

es!

Evid

ence

on

gain

s fr

om f

inan

cial

ope

ning

?!

The

criti

cal i

mpo

rtan

ce o

f th

e in

stitu

tiona

l se

ttin

g!

Com

plem

enta

ry m

acro

econ

omic

and

ex

chan

ge-r

ate

polic

ies

How

is f

inan

cial

inte

grat

ion

mea

sure

d?

"D

e ju

re m

easu

res

�e.

g., b

ased

on

expl

icit

regu

latio

ns

reco

rded

in t

he I

MF�

s AR

EAER

"Ca

n bi

ndin

g co

ntro

ls b

e de

sign

ed?

"H

ow s

tric

t is

enf

orce

men

t?"

Subj

ectiv

ity o

f co

ding

"D

e fa

cto

mea

sure

s"

Pric

e m

easu

res

"Q

uant

ity m

easu

res

(oft

en t

hese

are

com

posi

te P

and

Q)

"As

set

stoc

ks"

Savi

ng-in

vest

men

t co

rrel

atio

ns"

Volu

me

of f

inan

cial

flo

ws

"M

arke

t ca

pita

lizat

ion

shar

es (

e.g.

, Edi

son-

War

nock

)

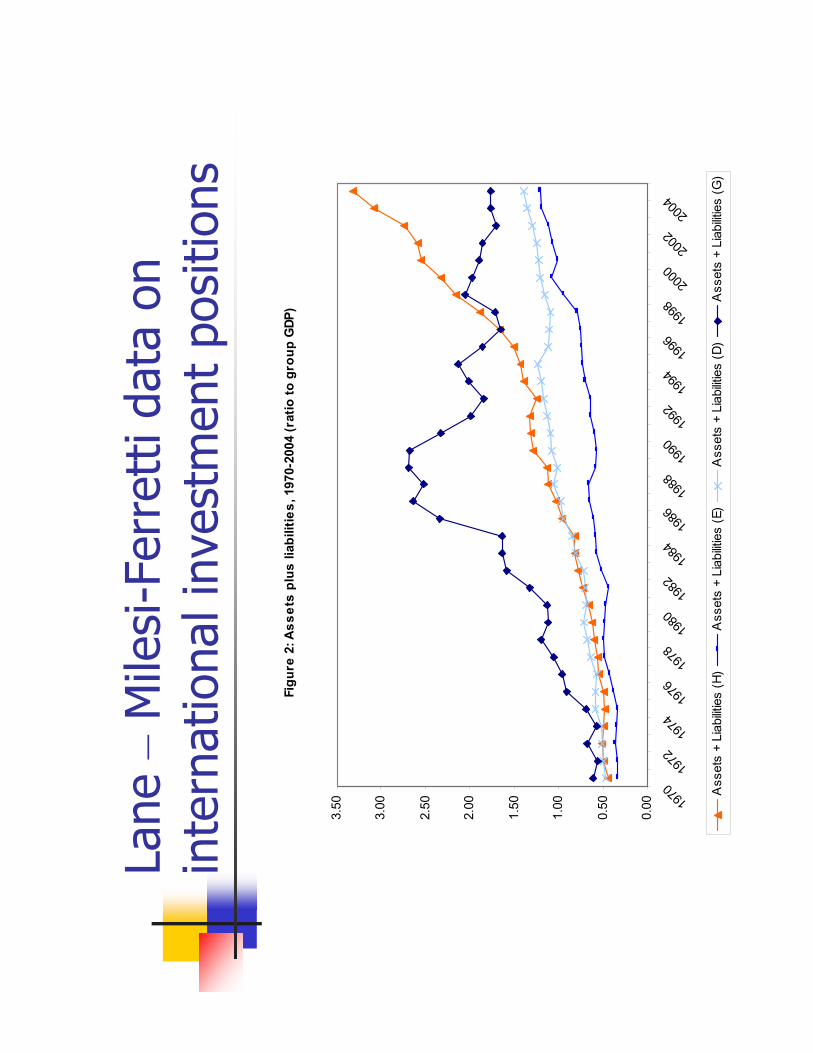

Lane

�M

ilesi

-Fer

rett

i dat

a on

in

tern

atio

nal i

nves

tmen

t po

sitio

ns

Figu

re 2

: Ass

ets

plus

liab

ilitie

s, 1

970-

2004

(rat

io to

gro

up G

DP)

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50 19

7019

7219

7419

7619

7819

8019

8219

8419

8619

8819

9019

9219

9419

9619

9820

0020

0220

04

Ass

ets

+ Li

abilit

ies

(H)

Ass

ets

+ Li

abilit

ies

(E)

Ass

ets

+ Li

abilit

ies

(D)

Ass

ets

+ Li

abilit

ies

(G)

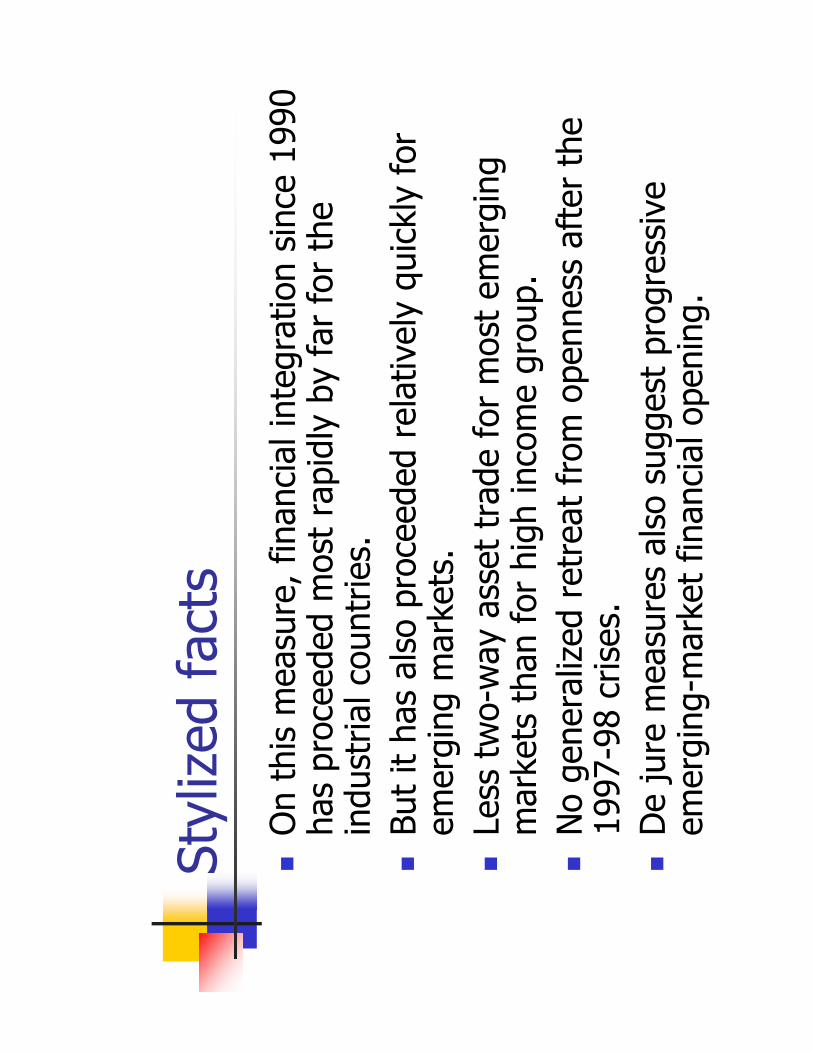

Styl

ized

fac

ts!

On

this

mea

sure

, fin

anci

al in

tegr

atio

n si

nce

1990

ha

s pr

ocee

ded

mos

t ra

pidl

y by

far

for

the

in

dust

rial c

ount

ries.

!Bu

t it

has

also

pro

ceed

ed r

elat

ivel

y qu

ickl

y fo

r em

ergi

ng m

arke

ts.

!Le

ss t

wo-

way

ass

et t

rade

for

mos

t em

ergi

ng

mar

kets

tha

n fo

r hi

gh in

com

e gr

oup.

!N

o ge

nera

lized

ret

reat

fro

m o

penn

ess

afte

r th

e 19

97-9

8 cr

ises

.!

De

jure

mea

sure

s al

so s

ugge

st p

rogr

essi

ve

emer

ging

-mar

ket

finan

cial

ope

ning

.

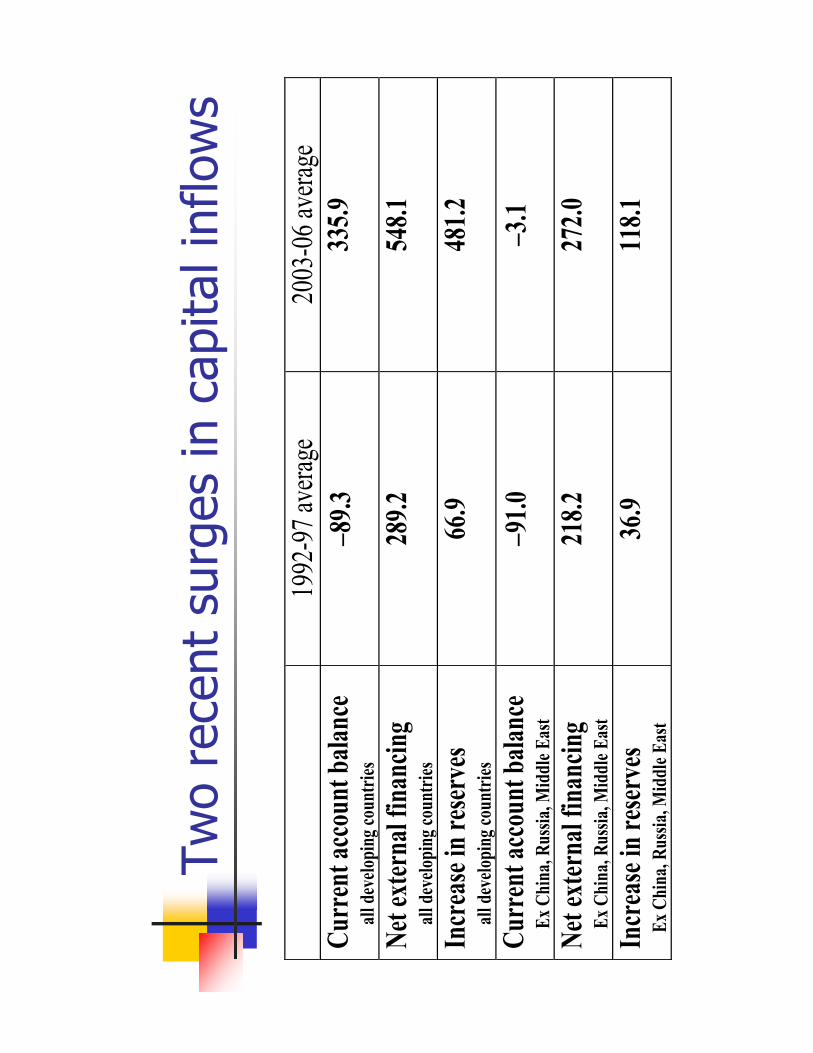

Two

rece

nt s

urge

s in

cap

ital i

nflo

ws

19

92-9

7 ave

rage

2003

-06 a

verag

e Cu

rren

t acc

ount

balan

ce

all

deve

loping

coun

tries

−8

9.3

335.9

Net e

xter

nal f

inan

cing

all

deve

loping

coun

tries

28

9.2

548.1

Incr

ease

in re

serve

s

all de

velop

ing co

untri

es

66.9

481.2

Curr

ent a

ccou

nt ba

lance

Ex C

hina

, Rus

sia, M

iddl

e Eas

t −9

1.0

−3.1

Net e

xter

nal f

inan

cing

Ex

Chi

na, R

ussia

, Mid

dle E

ast

218.2

27

2.0

Incr

ease

in re

serve

s

Ex C

hina

, Rus

sia, M

iddl

e Eas

t 36

.9 11

8.1

Why

cho

ose

inte

rnat

iona

lfin

anci

al

inte

grat

ion?

As

a co

mpl

emen

t to

do

mes

ticfin

anci

al d

evel

opm

ent

�A g

row

ing

body

of

empi

rical

ana

lyse

s, in

clud

ing

firm

-leve

l stu

dies

,indu

stry

-leve

l stu

dies

, ind

ivid

ual

coun

try-

stud

ies,

tim

e-se

ries

stud

ies,

pan

el

inve

stig

atio

ns, a

nd b

road

cro

ss-c

ount

ry

com

paris

ons,

dem

onst

rate

a s

tron

g po

sitiv

e lin

k be

twee

n th

e fu

nctio

ning

of

the

finan

cial

sys

tem

an

d lo

ng-r

un e

cono

mic

gro

wth

.�R

oss

Levi

ne, H

andb

ook

of E

cono

mic

Gro

wth

(200

5).

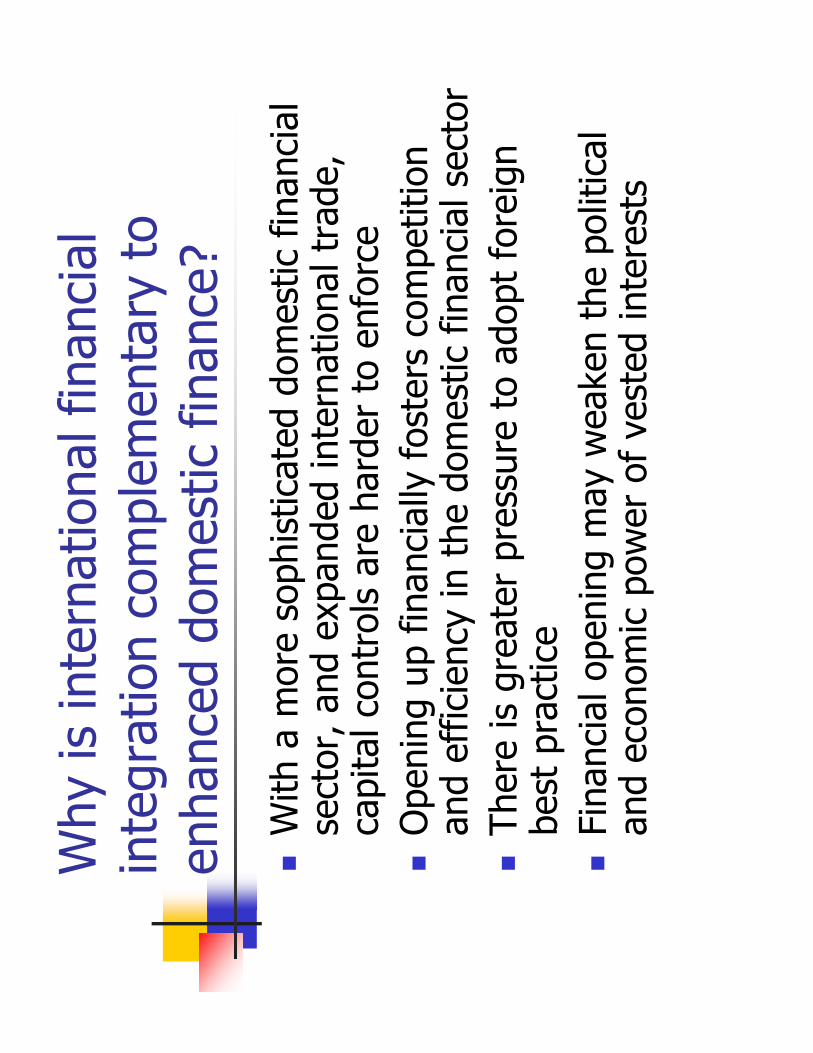

Why

is in

tern

atio

nal f

inan

cial

in

tegr

atio

n co

mpl

emen

tary

to

enha

nced

dom

estic

fin

ance

?

!W

ith a

mor

e so

phis

ticat

ed d

omes

tic f

inan

cial

se

ctor

, and

exp

ande

d in

tern

atio

nal t

rade

, ca

pita

l con

trol

s ar

e ha

rder

to

enfo

rce

!O

peni

ng u

p fin

anci

ally

fos

ters

com

petit

ion

and

effic

ienc

y in

the

dom

estic

fin

anci

al s

ecto

r!

Ther

e is

gre

ater

pre

ssur

e to

ado

pt f

orei

gn

best

pra

ctic

e!

Fina

ncia

l ope

ning

may

wea

ken

the

polit

ical

an

d ec

onom

ic p

ower

of

vest

ed in

tere

sts

Inst

itutio

nal s

caff

oldi

ng m

atte

rs

!Ex

pand

ed d

omes

tic f

inan

ce m

ay b

e de

stab

ilizi

ng

abse

nt s

ound

inst

itutio

ns, e

.g. t

hose

rel

atin

g to

!

Gov

erna

nce

and

rule

of

law

!Pr

uden

tial o

vers

ight

!M

acro

econ

omic

sta

bilit

y!

Thes

e in

stitu

tions

are

als

o ne

cess

ary

to s

afel

y em

brac

e fin

anci

al o

peni

ng;

but

we

also

hav

e!

Sove

reig

n ac

tors

!Cu

rren

cies

!Reg

ulat

ory

gaps

The

cris

is p

robl

em 1

!Fi

nanc

ial o

peni

ng, u

nder

the

wro

ng

cond

ition

s, c

an r

aise

the

like

lihoo

d of

cris

es!

We

have

lear

ned

that

vol

atile

cap

ital f

low

s th

emse

lves

can

con

trib

ute

to c

rises

�in

si

tuat

ions

whe

re a

cris

is m

ight

not

hav

e be

en

othe

rwis

e in

evita

ble

!Cr

ises

can

sta

rt w

ith c

urre

ncy,

ban

k se

ctor

, co

rpor

ates

, gov

ernm

ent

debt

�w

ith

mul

tidire

ctio

nal p

ositi

ve f

eedb

ack

loop

s

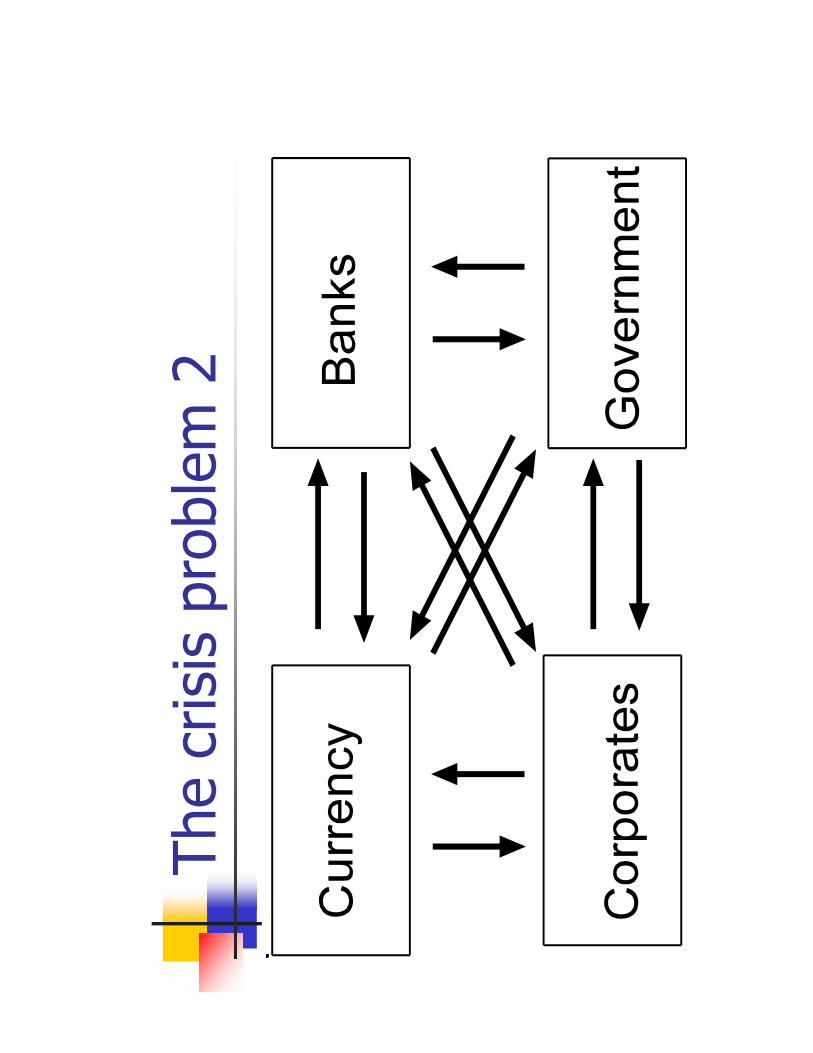

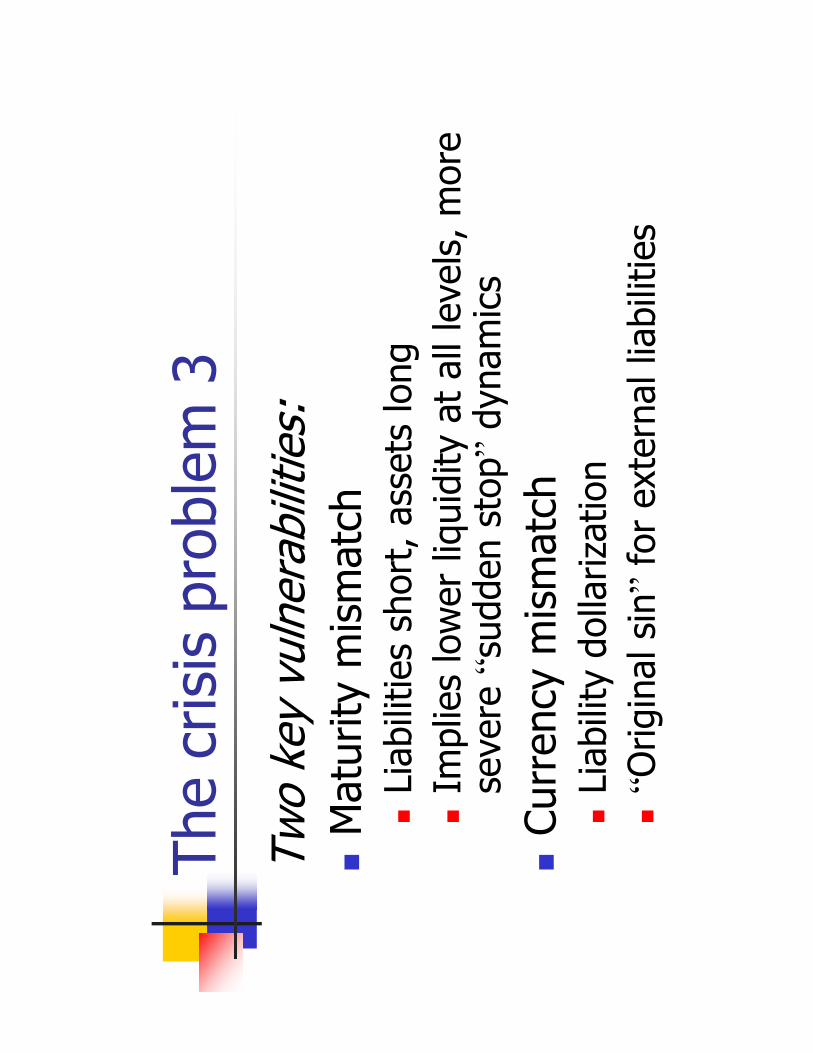

The

cris

is p

robl

em 2

The

cris

is p

robl

em 3

Two

key

vuln

erab

ilitie

s:!

Mat

urity

mis

mat

ch!

Liab

ilitie

s sh

ort,

ass

ets

long

!Im

plie

s lo

wer

liqu

idity

at

all l

evel

s, m

ore

seve

re �

sudd

en s

top�

dyna

mic

s!

Curr

ency

mis

mat

ch!

Liab

ility

dol

lariz

atio

n!

�Orig

inal

sin

�fo

r ex

tern

al li

abili

ties

The

cris

is p

robl

em 4

�Dev

alua

tion

may

pro

duce

ano

ther

typ

e of

wea

lth e

ffec

t w

hen

som

e gr

oups

of

the

coun

try

have

deb

ts t

o fo

reig

ners

ex

pres

sed

in t

erm

s of

for

eign

cur

renc

ies.

A d

eval

uatio

n w

ill

then

incr

ease

the

val

ue o

f th

e de

bt e

xpre

ssed

in d

omes

tic

curr

enci

es a

nd w

ill e

xert

a d

epre

ssin

g in

fluen

ce o

n th

e ex

pen-

ditu

res

of t

hese

gro

ups,

esp

ecia

lly w

hen

the

dom

estic

pric

es

they

rec

eive

for

the

sal

e of

the

ir pr

oduc

ts o

r se

rvic

es d

o no

t in

crea

se p

ropo

rtio

nally

with

the

dev

alua

tion.

Whe

n a

coun

try

has

a ne

t fo

reig

n de

bt, t

his

effe

ct w

ill m

ake

mor

e lik

ely

an

impr

ovem

ent

in t

he t

rade

bal

ance

and

a d

rop

in o

utpu

t fo

llow

ing

deva

luat

ion,

esp

ecia

lly w

hen

the

debt

is h

eld

by t

he

priv

ate

sect

or a

nd is

con

cent

rate

d in

sho

rt-t

erm

mat

uriti

es.�

Carlo

s F.

Día

z-Al

ejan

dro,

Exc

hang

e-Ra

te D

eval

uatio

n in

a S

emi-

Indu

stria

lized

Cou

ntry

: Th

e Ex

perie

nce

of A

rgen

tina,

195

5-19

61(1

965)

.

The

cris

is p

robl

em 5

!W

ith c

urre

ncy

mis

mat

ch, a

n un

expe

cted

de

prec

iatio

n ca

n w

orse

n fir

m b

alan

ce s

heet

s,

harm

ing

inve

stm

ent

!It

can

ham

mer

ban

k ca

pita

l, ei

ther

dire

ctly

or

by r

ende

ring

bank

bor

row

ers

unab

le t

o pa

y de

bts

they

ow

e to

ban

ks!

Rea

l gov

ernm

ent

debt

ris

es, d

irect

ly a

nd d

ue

to im

plic

it or

exp

licit

bailo

ut g

uara

ntee

s !

This

fur

ther

wea

kens

the

cur

renc

y!

But

mon

etar

y tig

hten

ing

wor

sens

the

plig

ht o

f sh

ort-

term

bor

row

ers,

not

ably

ban

ks

Out

put

in c

rises

!Fo

r a

typi

cal i

ndus

tria

l cou

ntry

, out

put

bott

oms

in t

he y

ear

prec

edin

ga

curr

ency

cr

isis

!Bu

t fo

r a

typi

cal d

evel

opin

g co

untr

y, t

he

trou

gh is

the

sam

eye

ar a

s th

e cu

rren

cy c

risis

!H

utch

ison

and

Noy

(20

05)

put

the

aver

age

cost

of

an e

mer

ging

-mar

ket

curr

ency

cris

is a

t a

cum

ulat

ive

5-8%

of

outp

ut, o

f a

bank

ing

cris

is a

t a

cum

ulat

ive

10-1

3%, w

ith t

he

effe

cts

addi

tive

The

open

-eco

nom

y tr

ilem

ma

!An

ope

n ec

onom

y ca

n en

joy

only

tw

o of

: ex

chan

ge s

tabi

lity,

cap

ital m

obili

ty, d

omes

tic

orie

ntat

ion

of m

onet

ary

polic

y (e

.g.,

an

infla

tion

targ

et)

!Bu

t fo

r em

ergi

ng m

arke

ts, c

urre

ncy

mis

mat

ch

mak

es it

diff

icul

t to

flo

at a

s fr

eely

as

indu

stria

l cou

ntrie

s do

!So

the

re c

an b

e �f

ear

of f

loat

ing,

�w

ith f

ree

mon

etar

y po

licy

com

prom

ised

Capi

tal m

obili

ty c

an f

acili

tate

cris

es.

Can

we

mea

sure

its

bene

fits?

!Fo

r po

orer

cou

ntrie

s w

ith lo

w s

avin

g ra

tes,

fin

anci

al g

loba

lizat

ion

can

mak

e sc

arce

cap

ital

avai

labl

e, r

aisi

ng w

elfa

re a

nd g

row

th!

It c

an a

llow

ris

k di

vers

ifica

tion,

low

erin

g th

e va

riabi

lity

of c

onsu

mpt

ion

rela

tive

to o

utpu

t!

It c

an d

isci

plin

e po

licie

s an

d tr

ansf

er v

ario

us

type

s of

kno

w-h

ow, r

aisi

ng T

FP �

!�

in t

heor

y, a

t le

ast

The

allo

catio

n of

ric

h-co

untr

y sa

ving

s

!N

ot m

uch

capi

tal f

low

s fr

om r

ich

to p

oor

coun

trie

s re

lativ

e to

sim

ple

theo

retic

al b

ench

mar

ks (

Luca

s)!

Inde

ed, f

or d

evel

opin

g co

untr

ies,

hig

her

grow

th is

co

rrel

ated

with

hig

her

savi

ng a

nd s

urpl

uses

in t

he

curr

ent

acco

unt

(Pra

sad

et a

l. 20

06;

Aize

nman

et

al.)

!Al

loca

tion

puzz

le o

f G

ourin

chas

and

Jea

nne

(200

7):

the

capi

tal t

hat

does

flo

w t

o de

velo

ping

cou

ntrie

s te

nds

to e

nd u

p in

low

-pro

duct

ivity

loca

les

!FD

I, w

hich

has

the

bes

t-do

cum

ente

d pr

o-gr

owth

ef

fect

s on

rec

ipie

nt c

ount

ries,

doe

s, h

owev

er, s

eem

to

fol

low

the

con

vent

iona

l neo

clas

sica

l pat

tern

of

flow

ing

from

ric

her

to p

oore

r co

untr

ies

Cros

s-se

ctio

nal s

tudi

es o

f fin

anci

al o

peni

ng a

nd g

row

th!

In g

ener

al t

hese

stu

dies

indi

cate

litt

le o

r no

rel

atio

n be

twee

n fin

anci

al o

penn

ess

and

grow

th (

see

Pras

ad e

t al

. 200

3)!

But

they

tak

e no

acc

ount

of

the

timin

g of

libe

raliz

atio

n!

Nor

is t

he t

heor

etic

al b

asis

for

the

pr

edic

tion

bein

g te

sted

ver

y cl

ear

(Hen

ry 2

006)

Stud

ies

of d

ynam

ic e

ffec

ts 1

!Ev

ent

stud

y ap

proa

ch o

f H

enry

sug

gest

s po

sitiv

e ef

fect

s of

sto

ck-m

arke

t lib

eral

izat

ions

on

cos

t of

cap

ital,

equi

ty v

alue

s, in

vest

men

t!

Beka

ert

et a

l. (2

005)

pan

el s

tudy

fin

ds

impl

ausi

bly

larg

e po

sitiv

e gr

owth

eff

ects

fro

m

equi

ty-m

arke

t op

enin

g!

Beka

ert

et a

l. (2

006)

fin

d vo

latil

ity r

educ

tion,

bu

t on

ly in

a b

road

sam

ple

with

ric

h co

untr

ies

!Ca

ptur

es t

he lo

w v

olat

ility

of

indu

stria

l cou

ntrie

s,

whi

ch m

ostly

wer

e op

en in

the

sam

ple

perio

d?

Stud

ies

of d

ynam

ic e

ffec

ts 2

!So

me

maj

or p

robl

ems:

!H

ow t

o m

easu

re li

bera

lizat

ion

date

!Ty

pica

lly f

inan

cial

ope

ning

is a

ccom

pani

ed

by a

pac

kage

of

othe

r re

form

s �

rais

es t

he

iden

tific

atio

n pr

oble

m!

Fina

ncia

l lib

eral

izat

ion

may

occ

ur w

hen

futu

re e

cono

mic

con

ditio

ns lo

ok f

avor

able

!La

tter

tw

o is

sues

ref

lect

tha

t fin

anci

al

liber

aliz

atio

n is

an

endo

geno

usde

cisi

on

Mic

ro-le

vel s

tudi

es!

This

app

roac

h ho

lds

prom

ise

for

solv

ing

the

iden

tific

atio

n pr

oble

m!

If f

irms

face

sam

e m

acro

con

ditio

ns, b

ut o

nly

som

e ga

in f

inan

cial

-mar

ket

acce

ss, w

e ha

ve

trea

tmen

t an

d co

ntro

l gro

ups

of e

nter

pris

es

!Bu

t w

e ne

ed t

he id

entif

ying

con

ditio

n of

ra

ndom

sel

ectio

n in

to t

he t

wo

grou

ps!

Mitt

on (

2006

) fin

ds p

ositi

ve e

ffec

ts u

sing

dat

a w

ith f

irm-s

peci

fic d

ates

for

acc

ess

to f

orei

gn

equi

ty in

vest

ors

The

stru

ctur

al s

ettin

g 1

!Th

e em

piric

al r

ecor

d su

gges

ts li

mite

d ne

t di

rect

gain

s fo

r de

velo

ping

cou

ntrie

s!

Theo

retic

ally

, one

can

rel

ate

this

fin

ding

to

stru

ctur

al s

hort

com

ings

suc

h as

low

sh

areh

olde

r/cr

edito

r pr

otec

tion,

wea

k ru

le o

f la

w, e

tc.;

for

exa

mpl

e, s

ee S

tulz

(20

05)

!Th

ere

is s

tron

g ev

iden

ce, m

uch

of it

an

ecdo

tal,

that

inst

itutio

nal o

r st

ruct

ural

im

perf

ectio

ns c

ontr

ibut

ed t

o ge

nera

ting

cris

es

�fo

r ex

ampl

e, c

haeb

ol in

fluen

ce a

nd f

aulty

lib

eral

izat

ion

in t

he K

orea

n la

te-1

990s

cas

e

The

stru

ctur

al s

ettin

g 2

!Ar

guab

ly, f

ixed

or

heav

ily m

anag

ed e

xcha

nge

rate

s w

ere

a pr

oble

m!

Ther

e is

som

e ec

onom

etric

evi

denc

e th

at a

st

rong

er in

stitu

tiona

l sca

ffol

ding

rai

ses

the

net

bene

fits

from

fin

anci

al o

peni

ng!

Kose

et

al. (

2006

) su

gges

t fo

ur s

truc

tura

l ar

eas

whe

re im

prov

emen

ts c

an e

nhan

ce t

he

net

bene

fits

of c

apita

l inf

low

s:

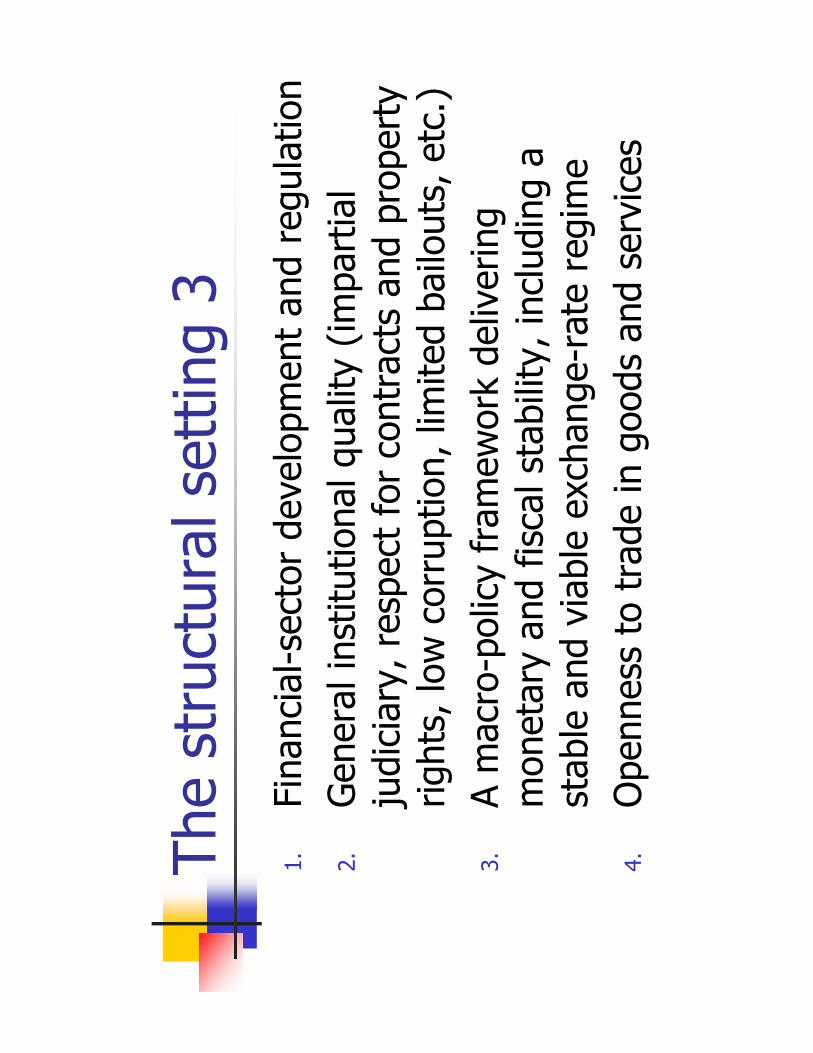

The

stru

ctur

al s

ettin

g 3

1.Fi

nanc

ial-s

ecto

r de

velo

pmen

t an

d re

gula

tion

2.G

ener

al in

stitu

tiona

l qua

lity

(impa

rtia

l ju

dici

ary,

res

pect

for

con

trac

ts a

nd p

rope

rty

right

s, lo

w c

orru

ptio

n, li

mite

d ba

ilout

s, e

tc.)

3.A

mac

ro-p

olic

y fr

amew

ork

deliv

erin

g m

onet

ary

and

fisca

l sta

bilit

y, in

clud

ing

a st

able

and

via

ble

exch

ange

-rat

e re

gim

e4.

Ope

nnes

s to

tra

de in

goo

ds a

nd s

ervi

ces

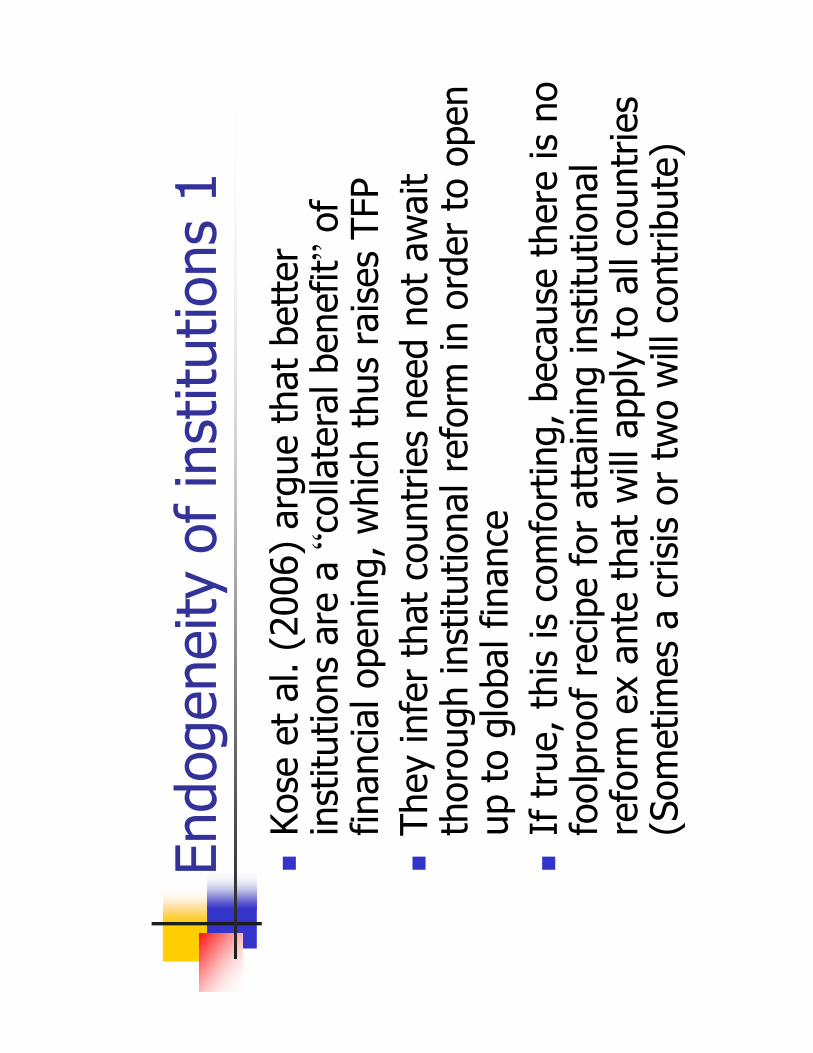

Endo

gene

ity o

f in

stitu

tions

1!

Kose

et

al. (

2006

) ar

gue

that

bet

ter

inst

itutio

ns a

re a

�co

llate

ral b

enef

it�of

fin

anci

al o

peni

ng, w

hich

thu

s ra

ises

TFP

!Th

ey in

fer

that

cou

ntrie

s ne

ed n

ot a

wai

t th

orou

gh in

stitu

tiona

l ref

orm

in o

rder

to

open

up

to

glob

al f

inan

ce!

If t

rue,

thi

s is

com

fort

ing,

bec

ause

the

re is

no

fool

proo

f re

cipe

for

att

aini

ng in

stitu

tiona

l re

form

ex

ante

tha

t w

ill a

pply

to

all c

ount

ries

(Som

etim

es a

cris

is o

r tw

o w

ill c

ontr

ibut

e)

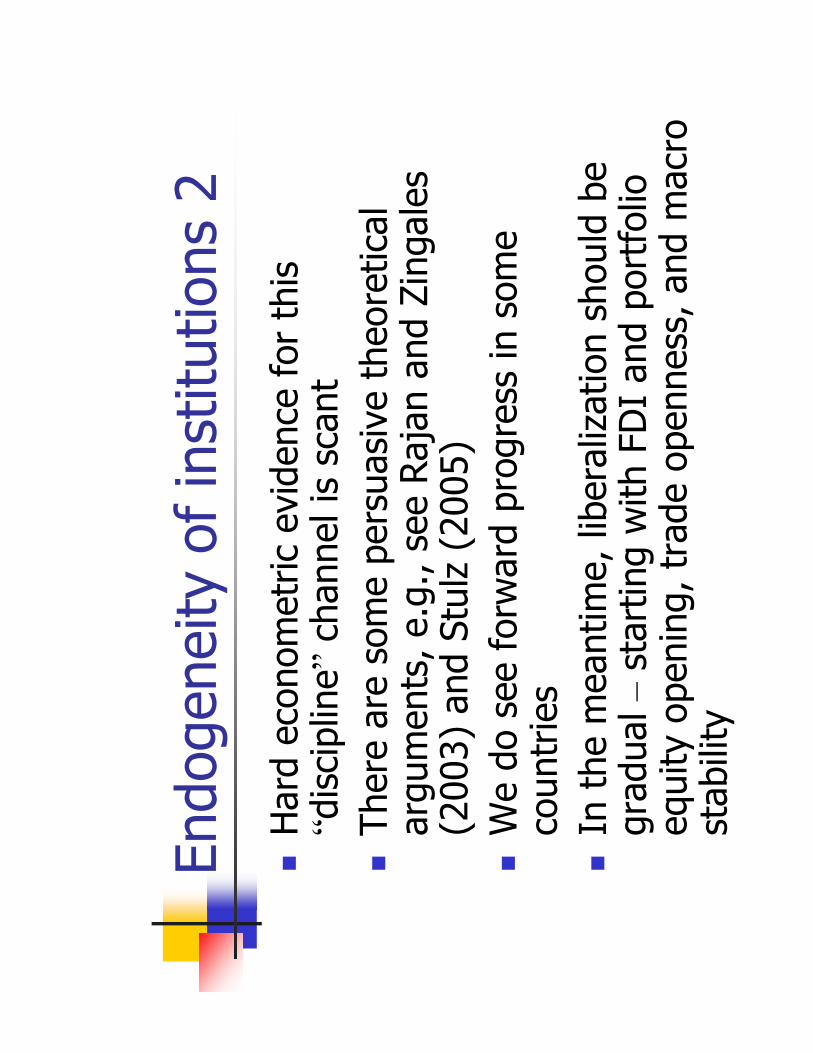

Endo

gene

ity o

f in

stitu

tions

2!

Har

d ec

onom

etric

evi

denc

e fo

r th

is

�dis

cipl

ine�

chan

nel i

s sc

ant

!Th

ere

are

som

e pe

rsua

sive

the

oret

ical

ar

gum

ents

, e.g

., se

e Raj

an a

nd Z

inga

les

(200

3) a

nd S

tulz

(20

05)

!W

e do

see

for

war

d pr

ogre

ss in

som

e co

untr

ies

!In

the

mea

ntim

e, li

bera

lizat

ion

shou

ld b

e gr

adua

l �st

artin

g w

ith F

DI

and

port

folio

eq

uity

ope

ning

, tra

de o

penn

ess,

and

mac

ro

stab

ility

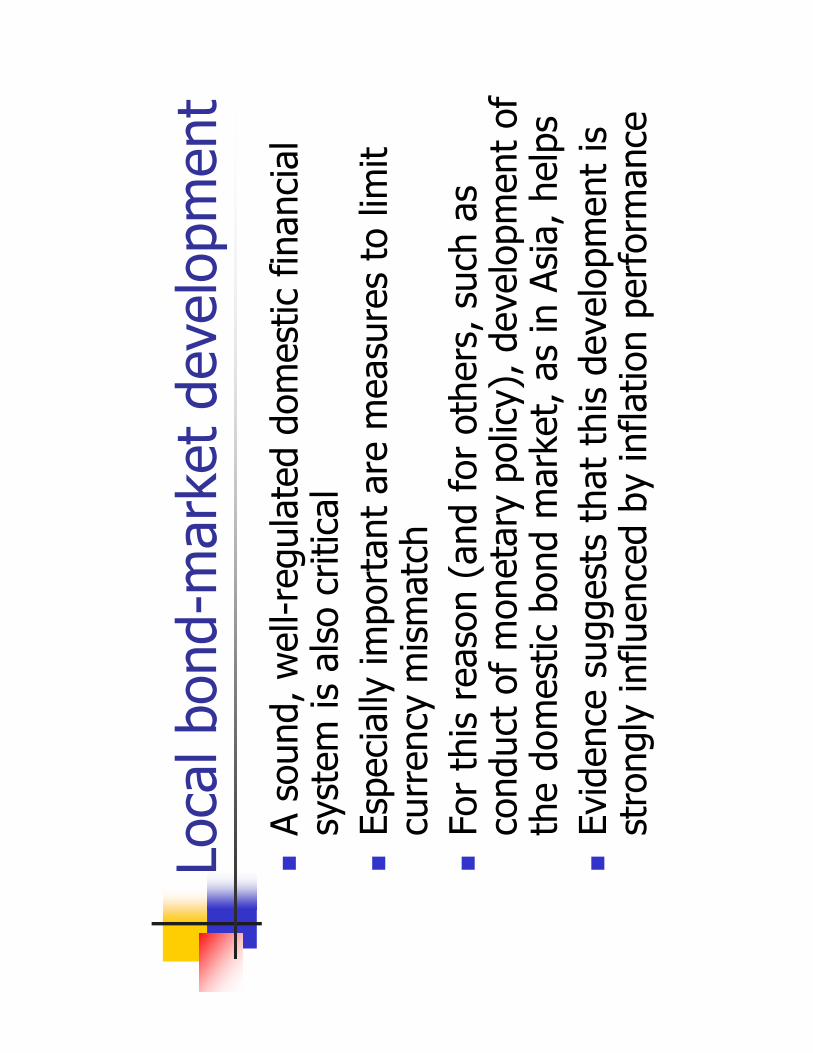

Loca

l bon

d-m

arke

t de

velo

pmen

t!

A so

und,

wel

l-reg

ulat

ed d

omes

tic f

inan

cial

sy

stem

is a

lso

criti

cal

!Es

peci

ally

impo

rtan

t ar

e m

easu

res

to li

mit

curr

ency

mis

mat

ch!

For

this

rea

son

(and

for

oth

ers,

suc

h as

co

nduc

t of

mon

etar

y po

licy)

, dev

elop

men

t of

th

e do

mes

tic b

ond

mar

ket,

as

in A

sia,

hel

ps!

Evid

ence

sug

gest

s th

at t

his

deve

lopm

ent

is

stro

ngly

influ

ence

d by

infla

tion

perf

orm

ance

The

exch

ange

rat

e re

gim

e 1

!Fi

xed

but

adju

stab

le s

yste

ms

are

cris

is-p

rone

w

hen

capi

tal i

s m

obile

: if

you

draw

a li

ne in

th

e sa

nd, y

ou�d

bet

ter

thro

w t

he s

and

in t

he

whe

els

!Co

untr

ies

seem

to

be m

ovin

g to

war

d th

e po

les

of c

urre

ncy

unio

n (f

ull d

olla

rizat

ion

or

the

euro

zon

e) o

r su

bsta

ntia

l dis

cret

iona

ry

flexi

bilit

y, a

void

ing

lines

in t

he s

and

!G

reat

er d

omes

tic f

inan

cial

dev

elop

men

t fa

cilit

ates

hav

ing

mar

ket-

dete

rmin

ed r

ates

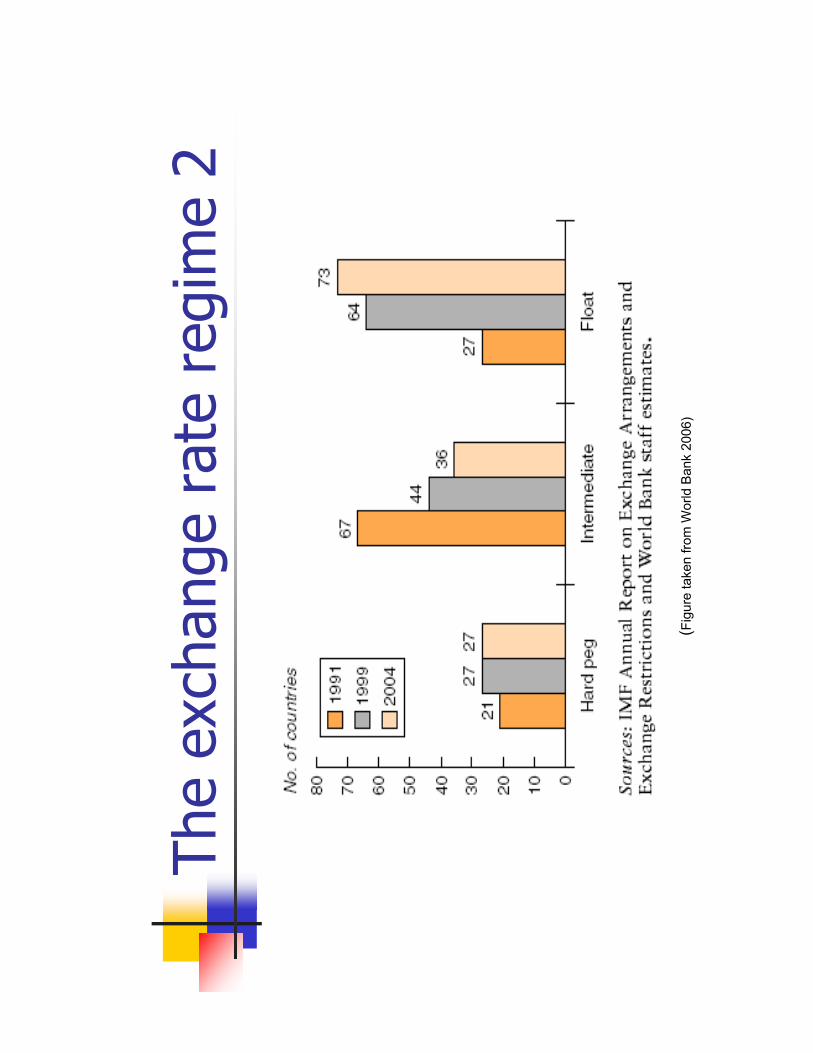

The

exch

ange

rat

e re

gim

e 2

(Fig

ure

take

n fro

m W

orld

Ban

k 20

06)

The

exch

ange

rat

e re

gim

e 3

!If

fin

anci

al o

peni

ng is

a g

oal,

a sy

stem

suc

h as

Gol

dste

in�s

(20

02)

�man

aged

flo

atin

g pl

us�

is d

esira

ble;

it c

ombi

nes:

!Ex

chan

ge-r

ate

flexi

bilit

y, r

educ

ing

cris

is

vuln

erab

ility

and

allo

win

g sh

ock

abso

rptio

n!

Mea

sure

s to

lim

it cu

rren

cy m

ism

atch

!Cr

edib

le in

flatio

n ta

rget

ing

by m

onet

ary

polic

y,

whi

ch m

ay it

self

redu

ce d

olla

rizat

ion

!W

ith c

ontr

ols

still

in p

lace

and

low

fin

anci

al

deve

lopm

ent

(Chi

na),

a b

aske

t, b

and,

cra

wl

(BBC

) à

laW

illia

mso

n m

ay b

e ap

prop

riate

Conc

lusi

on 1

!Em

ergi

ng-m

arke

t po

licym

aker

s sh

ow a

re

veal

ed p

refe

renc

e fo

r fin

anci

al o

peni

ng!

Dom

estic

fin

anci

al li

bera

lizat

ion,

whi

ch is

w

idel

y vi

ewed

as

pro-

grow

th if

don

e rig

ht,

mak

es e

xter

nal l

iber

aliz

atio

n bo

th le

ss

optio

nal a

nd m

ore

likel

y to

del

iver

net

gai

ns!

�Doi

ng it

rig

ht�

impl

ies

putt

ing

in p

lace

pr

econ

ditio

ns t

hat

will

als

o en

hanc

e th

e be

nefit

s fr

om f

inan

cial

glo

baliz

atio

n �

and

then

the

ext

ra s

peci

fic p

robl

ems

of t

he in

ter-

natio

nal m

argi

n sh

ould

be

atta

cked

at

sour

ce

Conc

lusi

on 2

!Fi

nanc

ial o

peni

ng s

houl

d be

gra

dual

and

ph

ased

, how

ever

!Ev

en t

houg

h gl

obal

izat

ion

may

, its

elf, y

ield

co

llate

ral i

nstit

utio

nal b

enef

its, w

e ha

ve li

ttle

ev

iden

ce o

n th

e sp

eed

and

relia

bilit

y of

suc

h ef

fect

s!

The

bene

fits

of e

xter

nal o

peni

ng a

re m

ost

likel

y to

be

real

ized

whe

n it

com

plem

ents

ot

her

pro-

grow

th r

efor

ms

and

an a

ppro

pria

te

mac

ro-m

onet

ary

fram

ewor

k