Embed Size (px)

Citation preview

Internal governance mechanisms and firm performancein China

Helen Wei Hu & On Kit Tam & Monica Guo-Sze Tan

Published online: 12 February 2009# Springer Science + Business Media, LLC 2009

Abstract Corporate governance issues arising from concentrated ownershipstructure in emerging economies have received growing attention. Adopting aprincipal–principal perspective, this paper employs structural equation modeling toevaluate the independent and interdependent effects of internal governancemechanisms in enhancing firms’ value in China. Based on a 3-year dataset covering304 publicly listed companies over 2003–2005, our findings suggest that ownershipconcentration has the most significant governance effect and has impactednegatively on firm performance. Furthermore, the governance role of the board ofdirectors and supervisory boards is found to have been hindered by ownershipconcentration, rendering them unable to improve firm performance at present.

Keywords Internal governance mechanisms . Ownership concentration . Controllingshareholder . Board of directors . Supervisory board

The traditional Anglo-American corporate governance model has evolved to dealwith the principal–agent issues stemming from the separation of ownership andcontrol in modern corporations with highly dispersed ownership structure. To

Asia Pac J Manag (2010) 27:727–749DOI 10.1007/s10490-009-9135-6

We thank the editors, Mike Peng (Editor-in-Chief), Rae Pinkham (Managing Editor) and two anonymousreviewers for constructive and helpful comments. This research has been financially supported by alinkage research grant awarded by the Australian Research Council.

H. W. Hu (*)Department of Management and Marketing, University of Melbourne, Parkville, Melbourne,Victoria 3010, Australiae-mail: [email protected]

O. K. TamRMIT University, 239 Bourke Street, Melbourne, Victoria 3001, Australiae-mail: [email protected]

M. G.-S. TanDeloitte Touch Tohmatsu, 180 Lonsdale St, Melbourne, Victoria 3000, Australiae-mail: [email protected]

mitigate the conflict of interest associated with the principal–agent problem,appropriate governance structures, including formal regulations, markets forcorporate control, managerial incentive alignment contracts, and board of directors,must function effectively to ensure value maximization in firms (Jensen & Meckling,1976; Shleifer & Vishny, 1997). However, it is now widely recognized that theconventional principal–agent perspective is of less significance in emergingeconomies where concentrated ownership is predominant. In such an environment,the conflict of interest between the controlling shareholders and minority share-holders has given rise to a principal–principal problem (Dharwadkar, George, &Brandes, 2000; Young, Peng, Ahlstrom, Bruton, & Jiang, 2008). As a result, “adifferent bundle of governance mechanisms” is required in such emergingeconomies because of their weak legal protection for shareholders and ineffectiveexternal governance mechanisms (Young et al., 2008: 199). In these circumstances,internal governance mechanisms (IGMs) are expected to play a more prevalent rolein these countries in addressing the principal–principal problem.

Like most emerging economies, China’s publicly listed companies are character-ized by highly concentrated ownership structure. External governance mechanismssuch as competitive markets for corporate control and for CEOs are underdeveloped.On the other hand, ownership by family, individual or institutional investors inChina’s listed firms is not yet significant. Rather, the controlling interest in Chinesecompanies is primarily through direct state ownership at both central and localgovernment levels and indirect state ownership through shareholding in companiesby state-owned enterprises (SOEs) and domestic organizations. As a result, complexcorporate governance issues have arisen from the dominance of direct and indirectstate ownership. While IGMs such as ownership structure and board of directors areto play a vital role at this juncture of China’s governance development, most studieson Chinese companies have focused on examining the impact of a single governancemechanism on firm performance. In order to provide a broader empirical evaluationof the independent and interdependent effects of different IGMs, this study aims toaddress the key research question: How do internal governance mechanismsindependently and jointly affect firm performance in China?

Three major IGMs—namely, (1) ownership structure, (2) board of directors, and(3) supervisory board—are examined for the purpose of this study on account oftheir formal responsibilities mandated by the country’s corporate governance system(China Company Law, 1994; CSRC, 2001, 2002). For the first time, these IGMs areinvestigated both individually and jointly. The examination of an individual IGMenables us to uncover the effect of a single governance mechanism on shareholderprotection, and also to provide comparable results to past studies such as Peng(2004), Tam and Hu (2006), and Wei and Varela (2003). However, as Rediker andSeth (1995) point out, studies on a single governance mechanism often neglect thebroader linkage of various governance mechanisms and their joint impacts onvarious governance issues. Rediker and Seth (1995) suggest that different levels ofsubstitution effects exist among IGMs. Similarly, Agrawal and Knoeber (1996) showthat a focus on a single governance mechanism does not detect the interdependenceof different mechanisms. Even among different governance mechanisms, Berglöfand Claessens (2006) argue that ownership concentration might exert an over-powering influence especially in countries where the regulatory environment and

728 H. W. Hu et al.

legal enforcement are weak. Thus, by examining IGMs jointly, this study canexplore their influences on each other.

This study contributes to the literature in three ways. First, Peng, Wang, and Jiang(2008) point out that conventional approaches of evaluating corporate governancesystem under dispersed ownership structure are inappropriate for understandingemerging economies. Therefore, this study makes a theoretical contribution byextending the literature in a Chinese context with a focus on the joint impact of threemajor IGMs on firm performance. Second, this study makes an empiricalcontribution by employing a structural equation model (SEM) to provide an analysisof both the independent and interdependent impacts of IGMs on firm performance ina single model. As applied in a number of studies, SEM offers a more in-depth andcomprehensive view than multivariate regression techniques for such integratedassessment (Buck, Filatotchev, Demina, & Wright, 2003; Tam & Tan, 2007). Lastly,as China launched two major corporate governance reforms in 2001 and 2002,1 thisstudy incorporates more recent data on 304 listed companies with 912 company-years over the subsequent period of 2003 to 2005. The post-reform data in the studycontribute significantly to the understanding of the latest development of practicesand effectiveness of IGMs in China’s corporate sector.

Theoretical discussion and hypotheses development

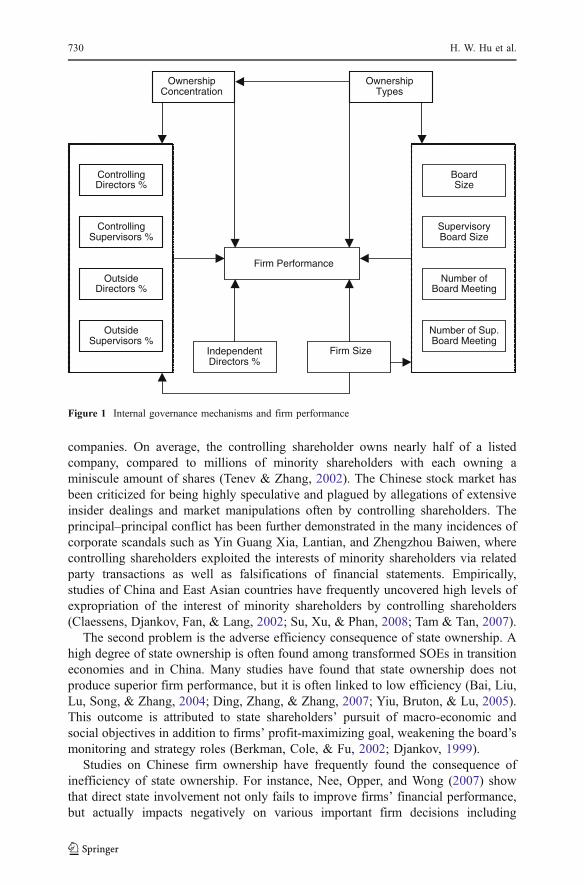

IGMs and their efficiency to mitigate the principal–principal conflict are recognizedto be vital to the development of corporate governance in emerging economies. InChina’s listed firms, the dual board system of the board of directors and supervisoryboard is a primary governance structure to protect the interest of minorityshareholders. Nevertheless, controlling shareholders can, through one IGM,particularly the ownership concentration, affect other IGMs such as the appointmentof directors and supervisors of their choice. It is therefore important to gain a betterunderstanding of the interconnectedness of these IGMs. That is, to examine howwell IGMs may affect each other in terms of their governance effect and how muchvariance in firm performance can be explained by these IGMs. Figure 1 is developedon the basis of our conceptual framework discussed in the sections below.

Ownership structure

In transition and emerging economies, concentration of ownership is oftenprominent. Two major problems have arisen as a result of corporatization ofChinese SOEs. The first problem is what Chinese observers have typically called theone-dominant controlling shareholder phenomenon (yigududa) in most listed

1 China introduced two major corporate governance reforms in 2001 and 2002, which placed strongemphasis on IGMs in an attempt to institute better corporate governance. The two reforms were based on(1) the “Guidelines for introducing independent directors to the board of directors of listed companies,”released by China Securities Regulatory Commission (CSRC) on 16 August 2001 (CSRC, 2001) and (2)the “Code of corporate governance for listed companies in China” that was jointly introduced by CSRCand State Economic and Trade Commission on 7 January 2002 (CSRC, 2002).

Internal governance mechanisms and firm performance in China 729

companies. On average, the controlling shareholder owns nearly half of a listedcompany, compared to millions of minority shareholders with each owning aminiscule amount of shares (Tenev & Zhang, 2002). The Chinese stock market hasbeen criticized for being highly speculative and plagued by allegations of extensiveinsider dealings and market manipulations often by controlling shareholders. Theprincipal–principal conflict has been further demonstrated in the many incidences ofcorporate scandals such as Yin Guang Xia, Lantian, and Zhengzhou Baiwen, wherecontrolling shareholders exploited the interests of minority shareholders via relatedparty transactions as well as falsifications of financial statements. Empirically,studies of China and East Asian countries have frequently uncovered high levels ofexpropriation of the interest of minority shareholders by controlling shareholders(Claessens, Djankov, Fan, & Lang, 2002; Su, Xu, & Phan, 2008; Tam & Tan, 2007).

The second problem is the adverse efficiency consequence of state ownership. Ahigh degree of state ownership is often found among transformed SOEs in transitioneconomies and in China. Many studies have found that state ownership does notproduce superior firm performance, but it is often linked to low efficiency (Bai, Liu,Lu, Song, & Zhang, 2004; Ding, Zhang, & Zhang, 2007; Yiu, Bruton, & Lu, 2005).This outcome is attributed to state shareholders’ pursuit of macro-economic andsocial objectives in addition to firms’ profit-maximizing goal, weakening the board’smonitoring and strategy roles (Berkman, Cole, & Fu, 2002; Djankov, 1999).

Studies on Chinese firm ownership have frequently found the consequence ofinefficiency of state ownership. For instance, Nee, Opper, and Wong (2007) showthat direct state involvement not only fails to improve firms’ financial performance,but actually impacts negatively on various important firm decisions including

OwnershipConcentration

OwnershipTypes

ControllingDirectors %

ControllingSupervisors %

OutsideDirectors %

OutsideSupervisors %

BoardSize

SupervisoryBoard Size

Number ofBoard Meeting

Number of Sup.Board Meeting

IndependentDirectors %

Firm Size

Firm Performance

Figure 1 Internal governance mechanisms and firm performance

730 H. W. Hu et al.

personnel, strategic and financial decisions. Other research suggest privately-ownedlisted companies outperform listed companies with significant state ownership (Dinget al., 2007). In essence, three distinct types of controlling shareholders aremandatorily disclosed in China’s company annual reports. They are (1) state-ownedshares, (2) legal person shares and (3) state-owned legal person shares.2 Both state-owned shares and state-owned legal person shares have state involvement, with theformer 100% owned by the state but the latter has the state as the majority owner. Incontrast, legal person shares are represented by domestic institutions. Studies onvarious governance effects of ownership types have reported that, compared to state-owned shares, state-owned legal person shares hire more outside directors formonitoring purposes while legal person shares are able to achieve better firmperformance (Hovey, Li, & Naughton, 2003; Tenev & Zhang, 2002; Xu & Wang,1997). The negative efficiency implication of state-owned shares could be explainedby the conflicting role played by the state, who is the regulator as well as theabsolute owner. Conversely, if firms are not directly controlled by state-ownedshares, they are more inclined to be driven by the profit motive to achieve betterfinancial performance. Therefore, apart from the potentially greater principal–principal conflicts as a result of ownership concentration, we predict thatconcentrated ownership via direct state-owned shares will give rise to higher levelof inefficiency. Two hypotheses are formulated:

Hypothesis 1a Ownership concentration of the controlling shareholder is negativelyrelated to firm performance.

Hypothesis 1b Firms controlled by state-owned shares would produce inferiorperformance compared to firms controlled by state-owned legal person shares andlegal person shares.

Board of directors

As the primary IGM, the key governance role of the board of directors is tosafeguard the interest of the firm by improving the firm’s corporate governancestandard. Owing to the high ownership concentration, the strategic influence bycontrolling shareholders through directors on the board makes the investigation of boardeffectiveness a more complex issue. To explore the governance influence of controllingshareholders, we identify the Chinese board of directors as consisting of four mutually

2 The three types of controlling shareholders are mutually-exclusive and their official definitions are:

Ownership type DefinitionState-owned shares (guoyou gu) Shares owned by the central government, local governments, or an

entity that represents the central or local governments.Legal person shares (faren gu) Shares owned by a non-individual legal entity or institution.State-owned legal person shares(guoyou faren gu)

Shares owned by an entity in which the state is the majority owner buthas less than 100% shareholding.

Internal governance mechanisms and firm performance in China 731

exclusive director types, which are (1) executive directors, (2) outside directors, (3)independent directors and (4) controlling directors.

A controlling director is someone who is a full-time employee of the largestshareholder of the listed company.3 Though controlling directors and executivedirectors are often regarded as insiders, the presence of controlling directors on boardshas far reaching ramifications in the Chinese context. On the one hand, they need toprotect the interest of all shareholders, including both controlling and minorityshareholders. On the other hand, they would face potential conflicts of interest whenthe principal–principal problem arises between the two shareholder groups (Young etal., 2008). Studies of companies in Asia show that having representatives ofcontrolling shareholders on the board is common in highly concentrated firms, withthese directors playing a pivotal role in board decisions (Claessens, Djankov, Fan, &Lang, 1999; Heidrick & Struggles, 2007; Yeh, Lee, & Woidtke, 2001). Therefore, thegovernance implication of controlling directors is central to the understanding of theconflicts between controlling and minority shareholders.

Although information asymmetry between shareholders and managers may bereduced through board presence, the detrimental effects of having controlling directorscould outweigh the benefits of their presence. First, controlling directors activelyinfluence the development of company objectives with a focus on the interest ofcontrolling shareholders, not necessarily the minority shareholders (Claessens,Djankov, & Lang, 2000; Faccio, Lang, & Young, 2001; Young et al., 2008). Second,the presence of controlling directors could potentially weaken the governance role ofother directors, making the board less effective. For instance, Yeh et al. (2001)discover that family representation on the board leads to centralization in authority anddecision-making power, and a similar finding was also documented by Tong (1996).In the case of state ownership, research suggests that controlling directors whorepresent the state with political backgrounds are not effective in performing theirmonitoring role (Chang & Wong, 2004; Dong & Gao, 2002). Nevertheless, thecomposition of controlling directors and their governance effect on firm performancehave not been explored in past studies. Therefore, this study pioneers the empiricalexamination of these important issues with two respective hypotheses:

Hypothesis 2a The proportion of controlling directors on the board is positivelyrelated to the degree of ownership concentration of controlling shareholders.

Hypothesis 2b The proportion of controlling directors on the board is negativelyrelated to firm performance.

Board independence is supposed to provide defense against the exploitativebehavior by the controlling shareholders and directors. Thus, independent directorsplay a critical role. Different definitions of “independence” have been adopted bycorporate governance codes around the world. A common view of independence is

3 Controlling directors are different from executive directors who are full-time employees of the listedcompany. There is no overlapping between controlling directors and executive directors according toCSRC Corporate Governance Code (Article 23, CSRC, 2002). In fact, our study is the first to examine“controlling directors,” whose data come from companies’ annual reports (CSRC, 2003).

732 H. W. Hu et al.

defined as having “no relationships or circumstances which could affect thedirector’s judgment” (Mallin, 2007: 102). From an agency perspective, independentdirectors are expected to play a more active and effective monitoring role thanexecutive (inside) directors (Fama & Jensen, 1983; Johnson, Daily, & Ellstrand,1996). However, empirical research on the effectiveness of independent directors hasbeen on the whole inconclusive. Meta-analyses by Dalton, Daily, Ellstrand, andJohnson (1998) and others have not found convincing evidence to suggest that agreater number of independent directors necessarily results in better firmperformance. Although empirical findings on the governance and performance linkare mixed, the importance of having independent directors is widely accepted. Forinstance, Uzun, Szewczyk, and Varma (2004) show that the presence of independentdirectors does help to reduce corporate frauds in US companies. In an empirical teston Chinese companies, Kato and Long (2006) reveal that, after controlling for firmperformance, the appointment of independent directors increases CEO turnover,suggesting a stronger governance role by a more independent board.

In a situation where insiders may dominate the board, instead of focusing onindependent directors, the more broadly defined notion of outside directors hassometimes been used as another yardstick for measuring board independence(Johnson et al., 1996). Outside directors are found to be more assertive inconfronting board decisions and can therefore act as a counterweight to insidedirectors (Johnson et al., 1996; Mallin, 2007). Moreover, they can bring in expertiseand knowledge external to the firm, and more importantly, that resource dependencerole allows them to provide advice and resources in helping the firm to succeed(Hillman & Dalziel, 2003; Pfeffer & Salancik, 1978; Yoshikawa & McGuire, 2008).Studies on China using the notion of outside directors have found that institutionaloutside directors have a positive impact on firm performance, implying an effectiveresource role played by these directors (Peng, 2004). Chen, Firth, Gao, and Rui(2006) also produce findings that outside directors are effective monitors particularlyin deterring corporate frauds in China’s companies. However, earlier studies ofChinese firms have been unable to differentiate the monitoring efficacy betweenoutside directors and independent directors since regulatory requirement of havingindependent directors only started in 2001. Utilizing new data that have becomeavailable since 2001, we can now more accurately test the governance function ofoutside directors by separating them from independent directors.4 Since bothindependent and outside directors are expected to mitigate the principal–principalconflict, their presence and potential monitoring effectiveness might be tempered bythe level of ownership concentration. Given that a Chinese board is legally requiredto have at least one third of independent directors, the interrelationship betweenownership concentration and board of directors can be expected to be reflected bythe proportion of outside directors. On the basis of the above discussion, wetherefore hypothesize that:

Hypothesis 3a The proportion of outside directors on the board is negatively relatedto the degree of ownership concentration of controlling shareholders.

4 China’s securities regulator CSRC has clearly defined criteria for independent directors. Refer to CSRC(2001) for the official definition of independent directors.

Internal governance mechanisms and firm performance in China 733

Hypothesis 3b The proportion of outside directors on the board is positively relatedto firm performance.

Hypothesis 3c The proportion of independent directors on the board is positivelyrelated to firm performance.

Supervisory board

In Chinese listed companies, a dual board structure is mandatory. Unlike the superior-subordinate relationship between the supervisory board and management board inEuropean countries, the Chinese dual board structure is parallel under theirshareholders. Officially, the key responsibilities of supervisory board are to examinethe company’s financial affairs, and to check legal compliance of directors andmanagers (China Company Law, 1994). However, Chinese supervisors are found tohave played little role in determining corporate strategies, merger and acquisitiondecisions, appointing board directors and selecting company CEOs. Therefore, thesupervisory board has received less attention in previous studies such as Peng (2004)and Peng, Zhang, and Li (2007). Although a few studies have examined thesupervisory board, they have consistently reported the inefficiency of the performanceof supervisory boards. For instance, Tam (1999: 86) found that “about one-quarter ofsupervisors did not regularly inspect company activities and financial affairs, and 78%of supervisors were not prepared to investigate company affairs.” Similar findings arealso reported by Dahya, Karbhari, Xiao, and Yang (2003) and Xiao, Dahya, and Lin(2004). Certainly, without effective monitoring by the supervisory board, thelikelihood of attenuating the principal–principal problem will be limited.

A typical Chinese supervisory board composes of three mutually exclusivegroups of supervisors, which are (1) controlling supervisors (full-time employees ofthe largest shareholder of the listed company), (2) executive supervisors (companyemployees), and (3) outside supervisors. Xu and Wang’s (1997) study of supervisoryboards has found that almost none of the Chinese supervisors represented individualshareholders, with the super-majority of them being executive supervisors orcontrolling supervisors. The recent drive for board independence initiated by China’sregulatory authorities is aimed only at the board of directors, whereas supervisoryboard membership is mandated to include shareholder and employee representativesso that the independence of the supervisory board is inherently constrained (ChinaCompany Law, 1994; CSRC, 2002).5 Similarly, Tam and Hu (2006) and Dahya et al.(2003) suggest that supervisory boards are unlikely to play an active role in Chinesecorporate governance due to its weak independence from the company and itscontrolling shareholders.

In a study of European supervisory boards in OECD countries, Andres, Azofra,and Lopez (2005) argue that supervisors associated with block-holders do not

5 Our study of 304 listed companies shows that none of them has actually appointed any independentsupervisors, thus indicating companies’ reluctance to engage actively in promoting independence at thesupervisory board level.

734 H. W. Hu et al.

monitor the management as effectively as outside supervisors not associated withblock-holders, since the former may have a special interest in the company. Incontrast, outside supervisors can be expected to be more effective in performing theirmonitoring role as they have less potential conflicts of interest compared to insiders,with a greater willingness to challenge other board members (Johnson et al., 1996).In the Chinese context, Tam and Hu (2006) find that outside supervisors are moreeffective in performing their duties than inside supervisors though the Chinesesupervisory boards are overwhelmingly controlled by the latter. We argue that withhigh ownership concentration and weak external governance mechanisms in China,supervisory board could help achieve better governance outcomes. However,whether or not the supervisory board can perform its monitoring function effectivelyhinges largely on its independence. We posit that in the absence of independentsupervisors at the current stage of corporate governance development, the presenceof outside supervisors as the only outsiders may play a role in safeguarding minorityshareholders’ interest. Specifically:

Hypothesis 4a The proportion of controlling supervisors on the supervisory boardis positively related to the degree of ownership concentration of controllingshareholders.

Hypothesis 4b The proportion of controlling supervisors on the supervisory board isnegatively related to firm performance.

Hypothesis 4c The proportion of outside supervisors on the supervisory board isnegatively related to the degree of ownership concentration of controllingshareholders.

Hypothesis 4d The proportion of outside supervisors on the supervisory board ispositively related to firm performance.

Methodology and data

Sample

As of 31 December 2003, there were 1,271 companies listed on the Shanghai andShenzhen Stock Exchanges. In order to better capture representative samples of thelisted companies, a stratified random sampling technique is used. A total of 381companies were initially selected based on 30% sampling in each category of firmsize, covering large, medium and small firms, constituting a final sample size of 304firms after data cleaning.6 Starting from the year 2003, which was the first year afterChina’s corporate governance code was released and the requirement for one thirdindependent directors was implemented, this data set arguably signals the beginning

6 The classification of firm size is adopted from Xu and Wang (1997), who classified small-sized firms ashaving total assets lower than RMB500 million, medium-sized firms as having total assets betweenRMB500 million and RMB1.5 billion, and large-sized firms as having total assets above RMB1.5 billion.

Internal governance mechanisms and firm performance in China 735

of the new development of IGMs in China. Therefore, IGMs data are collected fromcompany annual reports of year 2003. To cater for time lag effect, data on marketcapitalization and financial performance are collected from 2003 to 2005, and anaverage value is used to reduce the noise in yearly data.

Variables

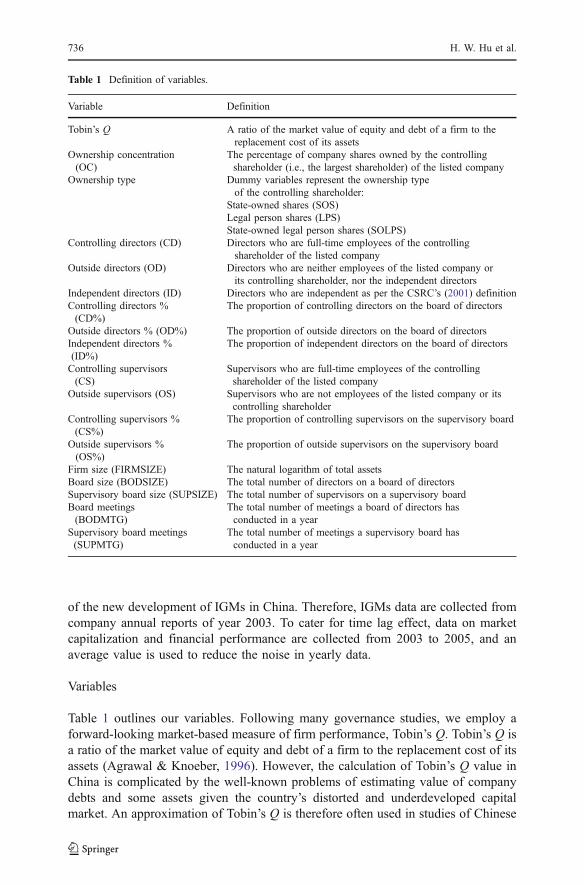

Table 1 outlines our variables. Following many governance studies, we employ aforward-looking market-based measure of firm performance, Tobin’s Q. Tobin’s Q isa ratio of the market value of equity and debt of a firm to the replacement cost of itsassets (Agrawal & Knoeber, 1996). However, the calculation of Tobin’s Q value inChina is complicated by the well-known problems of estimating value of companydebts and some assets given the country’s distorted and underdeveloped capitalmarket. An approximation of Tobin’s Q is therefore often used in studies of Chinese

Table 1 Definition of variables.

Variable Definition

Tobin’s Q A ratio of the market value of equity and debt of a firm to thereplacement cost of its assets

Ownership concentration(OC)

The percentage of company shares owned by the controllingshareholder (i.e., the largest shareholder) of the listed company

Ownership type Dummy variables represent the ownership typeof the controlling shareholder:

State-owned shares (SOS)Legal person shares (LPS)State-owned legal person shares (SOLPS)

Controlling directors (CD) Directors who are full-time employees of the controllingshareholder of the listed company

Outside directors (OD) Directors who are neither employees of the listed company orits controlling shareholder, nor the independent directors

Independent directors (ID) Directors who are independent as per the CSRC’s (2001) definitionControlling directors %(CD%)

The proportion of controlling directors on the board of directors

Outside directors % (OD%) The proportion of outside directors on the board of directorsIndependent directors %(ID%)

The proportion of independent directors on the board of directors

Controlling supervisors(CS)

Supervisors who are full-time employees of the controllingshareholder of the listed company

Outside supervisors (OS) Supervisors who are not employees of the listed company or itscontrolling shareholder

Controlling supervisors %(CS%)

The proportion of controlling supervisors on the supervisory board

Outside supervisors %(OS%)

The proportion of outside supervisors on the supervisory board

Firm size (FIRMSIZE) The natural logarithm of total assetsBoard size (BODSIZE) The total number of directors on a board of directorsSupervisory board size (SUPSIZE) The total number of supervisors on a supervisory boardBoard meetings(BODMTG)

The total number of meetings a board of directors hasconducted in a year

Supervisory board meetings(SUPMTG)

The total number of meetings a supervisory board hasconducted in a year

736 H. W. Hu et al.

companies. This study follows the approximation approach by Chen (2001) and Weiand Varela (2003).7

The first IGM, ownership concentration (OC), is measured by the proportion ofshares owned through different types of the controlling shareholding—state-ownedshares (SOS), legal person shares (LPS), and state-owned legal person shares (SOLPS)of a listed company. Consistent with Ding et al. (2007) and Xu and Wang (1997), we donot expect endogeneity to be a problem in the testing of ownership and performancerelationship.8 The second IGM, the composition of the board of directors, isrepresented by the proportion of controlling directors (CD), outside directors (OD)and independent directors (ID). The third IGM, the supervisory board, is to be testedthrough the proportion of controlling supervisors (CS) and outside supervisors (OS).

Control variables including firm size (FIRMSIZE) and board characteristics aretested in this study.9 Firm size is measured by the natural logarithm of total assets,which is often found to have significant impact on IGMs. One type of boardcharacteristics are the size of the board of directors (BODSIZE) and the supervisoryboard (SUPSIZE). One view is that a larger board will have more diversified andknowledgeable board members, which will in turn increase the problem-solvingcapabilities and enhance board efficiency (Haleblian & Finkelstein, 1993; van denBerghe & Levrau, 2004). On the other hand, several empirical findings point out thatthe size of a board is negatively correlated to firm performance (Ees, Postma, &Sterken, 2003; Yermack, 1996), especially an oversized board (Andres et al., 2005).The other type of board characteristics are frequency of board meetings (BODMTG)and supervisory board meetings (SUPMTG). Empirical studies on these variables arerelatively scant in Chinese research, therefore, this study can fill a gap in the literature.

Findings

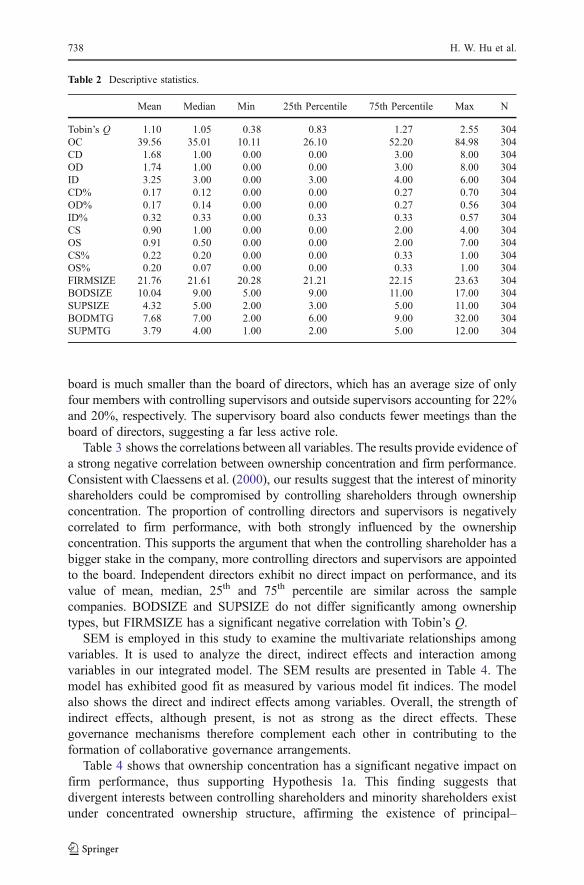

Descriptive statistics are presented in Table 2. The average ownership concentration is40% among the 304 companies in the sample, compared to 47% among 257companies listed in 1999 examined by Tenev and Zhang (2002). This suggests that theownership concentration is high in Chinese firms and relatively stable. A board ofdirectors has an average size of ten members, with controlling directors accounting for17%. On average, a board has three independent directors that accounts for 32% of theoverall size. The result indicates that most of the companies have complied with theindependent director requirement set by the CSRC within 2 years. The supervisory

9 An industry control variable has been used but test results are indifferent. Only the model controllingfirm size and board characteristics is presented as a result of a good fit.

8 Since it was the state that determined which company could be listed, coupled with the low proportion oftradable shares on the market (35% found by Su et al., 2008), firm performance would have limited impacton ownership structure as Xu and Wang point out (1997). Study by Tian and Estrin (2008) affirms thatendogeneity issue of ownership is not a big concern in testing for firm performance in Chinese companies.

7 Chen (2001) used “total liabilities” as the “replacement costs of total debt” and “book value of totalassets” as the “replacement costs of total assets” as a result of the difficulties in calculating the marketvalue of Chinese companies’ debt (2001: 58). Same estimation method is also used in Chinese studies byWei and Varela (2003), and Hovey et al. (2003). For further discussion of the calculation of the Q value,see Lang and Stulz (1994) and Chung and Pruitt (1994).

Internal governance mechanisms and firm performance in China 737

board is much smaller than the board of directors, which has an average size of onlyfour members with controlling supervisors and outside supervisors accounting for 22%and 20%, respectively. The supervisory board also conducts fewer meetings than theboard of directors, suggesting a far less active role.

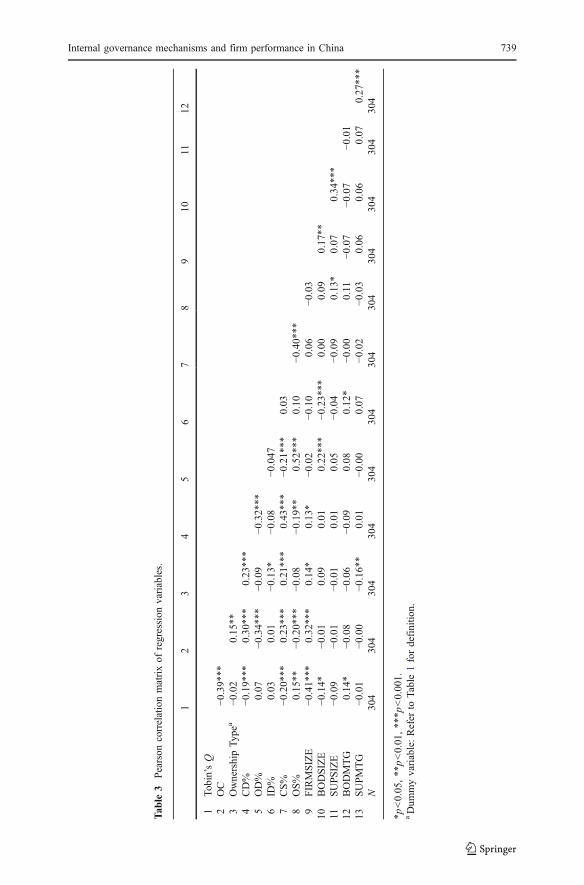

Table 3 shows the correlations between all variables. The results provide evidence ofa strong negative correlation between ownership concentration and firm performance.Consistent with Claessens et al. (2000), our results suggest that the interest of minorityshareholders could be compromised by controlling shareholders through ownershipconcentration. The proportion of controlling directors and supervisors is negativelycorrelated to firm performance, with both strongly influenced by the ownershipconcentration. This supports the argument that when the controlling shareholder has abigger stake in the company, more controlling directors and supervisors are appointedto the board. Independent directors exhibit no direct impact on performance, and itsvalue of mean, median, 25th and 75th percentile are similar across the samplecompanies. BODSIZE and SUPSIZE do not differ significantly among ownershiptypes, but FIRMSIZE has a significant negative correlation with Tobin’s Q.

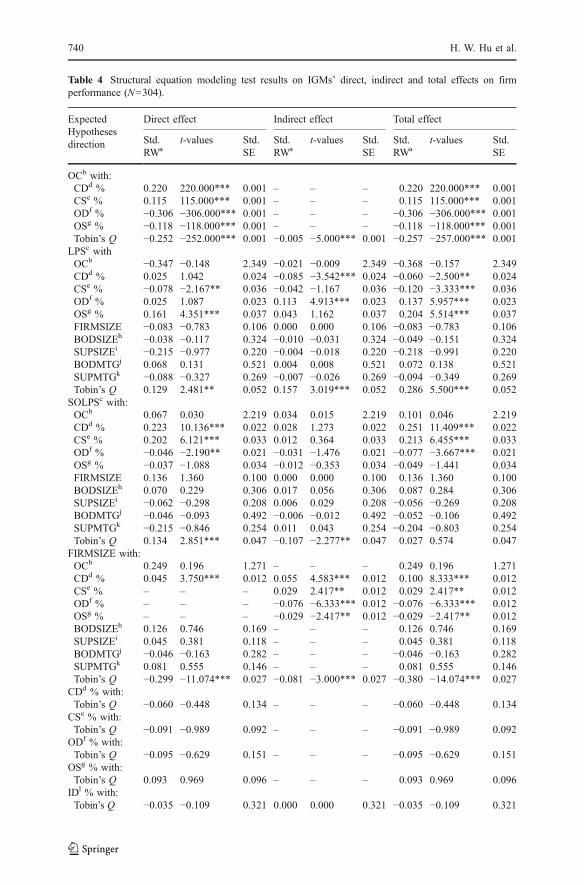

SEM is employed in this study to examine the multivariate relationships amongvariables. It is used to analyze the direct, indirect effects and interaction amongvariables in our integrated model. The SEM results are presented in Table 4. Themodel has exhibited good fit as measured by various model fit indices. The modelalso shows the direct and indirect effects among variables. Overall, the strength ofindirect effects, although present, is not as strong as the direct effects. Thesegovernance mechanisms therefore complement each other in contributing to theformation of collaborative governance arrangements.

Table 4 shows that ownership concentration has a significant negative impact onfirm performance, thus supporting Hypothesis 1a. This finding suggests thatdivergent interests between controlling shareholders and minority shareholders existunder concentrated ownership structure, affirming the existence of principal–

Table 2 Descriptive statistics.

Mean Median Min 25th Percentile 75th Percentile Max N

Tobin’s Q 1.10 1.05 0.38 0.83 1.27 2.55 304OC 39.56 35.01 10.11 26.10 52.20 84.98 304CD 1.68 1.00 0.00 0.00 3.00 8.00 304OD 1.74 1.00 0.00 0.00 3.00 8.00 304ID 3.25 3.00 0.00 3.00 4.00 6.00 304CD% 0.17 0.12 0.00 0.00 0.27 0.70 304OD% 0.17 0.14 0.00 0.00 0.27 0.56 304ID% 0.32 0.33 0.00 0.33 0.33 0.57 304CS 0.90 1.00 0.00 0.00 2.00 4.00 304OS 0.91 0.50 0.00 0.00 2.00 7.00 304CS% 0.22 0.20 0.00 0.00 0.33 1.00 304OS% 0.20 0.07 0.00 0.00 0.33 1.00 304FIRMSIZE 21.76 21.61 20.28 21.21 22.15 23.63 304BODSIZE 10.04 9.00 5.00 9.00 11.00 17.00 304SUPSIZE 4.32 5.00 2.00 3.00 5.00 11.00 304BODMTG 7.68 7.00 2.00 6.00 9.00 32.00 304SUPMTG 3.79 4.00 1.00 2.00 5.00 12.00 304

738 H. W. Hu et al.

Tab

le3

Pearson

correlationmatrixof

regression

variables.

12

34

56

78

910

1112

1To

bin’sQ

2OC

−0.39*

**3

OwnershipTy

pea

−0.02

0.15**

4CD%

−0.19*

**0.30**

*0.23**

*5

OD%

0.07

−0.34***

−0.09

−0.32***

6ID

%0.03

0.01

−0.13*

−0.08

−0.047

7CS%

−0.20*

**0.23**

*0.21**

*0.43**

*−0

.21***

0.03

8OS%

0.15

**−0

.20***

−0.08

−0.19**

0.52**

*0.10

−0.40***

9FIRMSIZE

−0.41*

**0.32**

*0.14*

0.13*

−0.02

−0.10

0.06

−0.03

10BODSIZE

−0.14*

−0.01

0.09

0.01

0.22**

*−0

.23*

**0.00

0.09

0.17**

11SUPSIZE

−0.09

−0.01

−0.01

0.01

0.05

−0.04

−0.09

0.13*

0.07

0.34

***

12BODMTG

0.14

*−0

.08

−0.06

−0.09

0.08

0.12

*−0

.00

0.11

−0.07

−0.07

−0.01

13SUPMTG

−0.01

−0.00

−0.16**

0.01

−0.00

0.07

−0.02

−0.03

0.06

0.06

0.07

0.27**

*N

304

304

304

304

304

304

304

304

304

304

304

304

*p<0.05,**p<0.01

,**

*p<0.001.

aDum

myvariable:Refer

toTable1fordefinitio

n.

Internal governance mechanisms and firm performance in China 739

Table 4 Structural equation modeling test results on IGMs’ direct, indirect and total effects on firmperformance (N=304).

ExpectedHypothesesdirection

Direct effect Indirect effect Total effect

Std.RWa

t-values Std.SE

Std.RWa

t-values Std.SE

Std.RWa

t-values Std.SE

OCb with:CDd % 0.220 220.000*** 0.001 – – – 0.220 220.000*** 0.001CSe % 0.115 115.000*** 0.001 – – – 0.115 115.000*** 0.001ODf % −0.306 −306.000*** 0.001 – – – −0.306 −306.000*** 0.001OSg % −0.118 −118.000*** 0.001 – – – −0.118 −118.000*** 0.001Tobin’s Q −0.252 −252.000*** 0.001 −0.005 −5.000*** 0.001 −0.257 −257.000*** 0.001

LPSc withOCb −0.347 −0.148 2.349 −0.021 −0.009 2.349 −0.368 −0.157 2.349CDd % 0.025 1.042 0.024 −0.085 −3.542*** 0.024 −0.060 −2.500** 0.024CSe % −0.078 −2.167** 0.036 −0.042 −1.167 0.036 −0.120 −3.333*** 0.036ODf % 0.025 1.087 0.023 0.113 4.913*** 0.023 0.137 5.957*** 0.023OSg % 0.161 4.351*** 0.037 0.043 1.162 0.037 0.204 5.514*** 0.037FIRMSIZE −0.083 −0.783 0.106 0.000 0.000 0.106 −0.083 −0.783 0.106BODSIZEh −0.038 −0.117 0.324 −0.010 −0.031 0.324 −0.049 −0.151 0.324SUPSIZEi −0.215 −0.977 0.220 −0.004 −0.018 0.220 −0.218 −0.991 0.220BODMTGj 0.068 0.131 0.521 0.004 0.008 0.521 0.072 0.138 0.521SUPMTGk −0.088 −0.327 0.269 −0.007 −0.026 0.269 −0.094 −0.349 0.269Tobin’s Q 0.129 2.481** 0.052 0.157 3.019*** 0.052 0.286 5.500*** 0.052

SOLPSc with:OCb 0.067 0.030 2.219 0.034 0.015 2.219 0.101 0.046 2.219CDd % 0.223 10.136*** 0.022 0.028 1.273 0.022 0.251 11.409*** 0.022CSe % 0.202 6.121*** 0.033 0.012 0.364 0.033 0.213 6.455*** 0.033ODf % −0.046 −2.190** 0.021 −0.031 −1.476 0.021 −0.077 −3.667*** 0.021OSg % −0.037 −1.088 0.034 −0.012 −0.353 0.034 −0.049 −1.441 0.034FIRMSIZE 0.136 1.360 0.100 0.000 0.000 0.100 0.136 1.360 0.100BODSIZEh 0.070 0.229 0.306 0.017 0.056 0.306 0.087 0.284 0.306SUPSIZEi −0.062 −0.298 0.208 0.006 0.029 0.208 −0.056 −0.269 0.208BODMTGj −0.046 −0.093 0.492 −0.006 −0.012 0.492 −0.052 −0.106 0.492SUPMTGk −0.215 −0.846 0.254 0.011 0.043 0.254 −0.204 −0.803 0.254Tobin’s Q 0.134 2.851*** 0.047 −0.107 −2.277** 0.047 0.027 0.574 0.047

FIRMSIZE with:OCb 0.249 0.196 1.271 – – – 0.249 0.196 1.271CDd % 0.045 3.750*** 0.012 0.055 4.583*** 0.012 0.100 8.333*** 0.012CSe % – – – 0.029 2.417** 0.012 0.029 2.417** 0.012ODf % – – – −0.076 −6.333*** 0.012 −0.076 −6.333*** 0.012OSg % – – – −0.029 −2.417** 0.012 −0.029 −2.417** 0.012BODSIZEh 0.126 0.746 0.169 – – – 0.126 0.746 0.169SUPSIZEi 0.045 0.381 0.118 – – – 0.045 0.381 0.118BODMTGj −0.046 −0.163 0.282 – – – −0.046 −0.163 0.282SUPMTGk 0.081 0.555 0.146 – – – 0.081 0.555 0.146Tobin’s Q −0.299 −11.074*** 0.027 −0.081 −3.000*** 0.027 −0.380 −14.074*** 0.027

CDd % with:Tobin’s Q −0.060 −0.448 0.134 – – – −0.060 −0.448 0.134

CSe % with:Tobin’s Q −0.091 −0.989 0.092 – – – −0.091 −0.989 0.092

ODf % with:Tobin’s Q −0.095 −0.629 0.151 – – – −0.095 −0.629 0.151

OSg % with:Tobin’s Q 0.093 0.969 0.096 – – – 0.093 0.969 0.096

IDl % with:Tobin’s Q −0.035 −0.109 0.321 0.000 0.000 0.321 −0.035 −0.109 0.321

740 H. W. Hu et al.

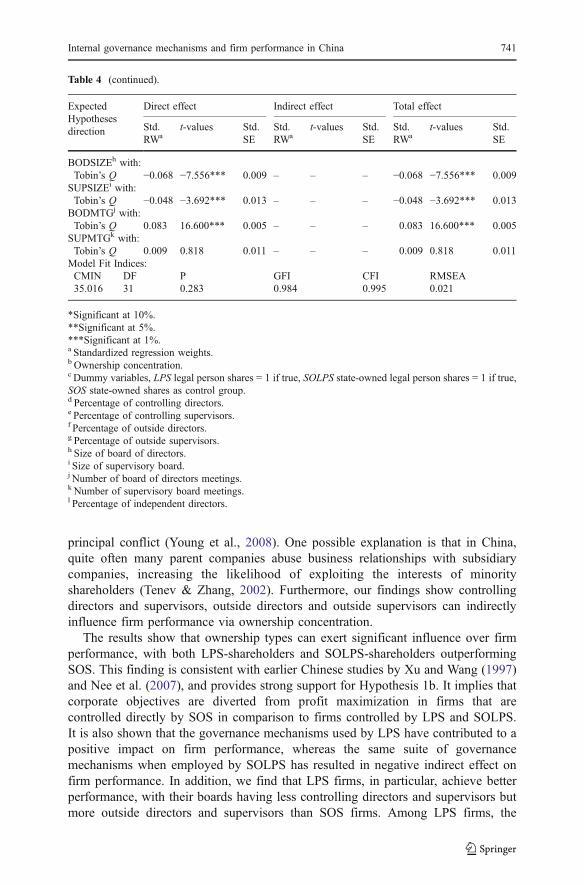

principal conflict (Young et al., 2008). One possible explanation is that in China,quite often many parent companies abuse business relationships with subsidiarycompanies, increasing the likelihood of exploiting the interests of minorityshareholders (Tenev & Zhang, 2002). Furthermore, our findings show controllingdirectors and supervisors, outside directors and outside supervisors can indirectlyinfluence firm performance via ownership concentration.

The results show that ownership types can exert significant influence over firmperformance, with both LPS-shareholders and SOLPS-shareholders outperformingSOS. This finding is consistent with earlier Chinese studies by Xu and Wang (1997)and Nee et al. (2007), and provides strong support for Hypothesis 1b. It implies thatcorporate objectives are diverted from profit maximization in firms that arecontrolled directly by SOS in comparison to firms controlled by LPS and SOLPS.It is also shown that the governance mechanisms used by LPS have contributed to apositive impact on firm performance, whereas the same suite of governancemechanisms when employed by SOLPS has resulted in negative indirect effect onfirm performance. In addition, we find that LPS firms, in particular, achieve betterperformance, with their boards having less controlling directors and supervisors butmore outside directors and supervisors than SOS firms. Among LPS firms, the

Table 4 (continued).

ExpectedHypothesesdirection

Direct effect Indirect effect Total effect

Std.RWa

t-values Std.SE

Std.RWa

t-values Std.SE

Std.RWa

t-values Std.SE

BODSIZEh with:Tobin’s Q −0.068 −7.556*** 0.009 – – – −0.068 −7.556*** 0.009

SUPSIZEi with:Tobin’s Q −0.048 −3.692*** 0.013 – – – −0.048 −3.692*** 0.013

BODMTGj with:Tobin’s Q 0.083 16.600*** 0.005 – – – 0.083 16.600*** 0.005

SUPMTGk with:Tobin’s Q 0.009 0.818 0.011 – – – 0.009 0.818 0.011

Model Fit Indices:CMIN DF P GFI CFI RMSEA35.016 31 0.283 0.984 0.995 0.021

*Significant at 10%.**Significant at 5%.***Significant at 1%.a Standardized regression weights.b Ownership concentration.c Dummy variables, LPS legal person shares = 1 if true, SOLPS state-owned legal person shares = 1 if true,SOS state-owned shares as control group.d Percentage of controlling directors.e Percentage of controlling supervisors.f Percentage of outside directors.g Percentage of outside supervisors.h Size of board of directors.i Size of supervisory board.j Number of board of directors meetings.k Number of supervisory board meetings.l Percentage of independent directors.

Internal governance mechanisms and firm performance in China 741

observed lower ownership concentration has indirectly impacted on the positiverelationship between outside directors and firm performance, and the negativerelationship between controlling directors and firm performance. However, none ofthese indirect relationships was significant with SOLPS. These results suggest thatwith less state involvement, LPS firms are more capable of utilizing their IGMs forachieving better performance than other types of controlling shareholder.

In terms of board composition, Table 4 shows that ownership concentration ispositively related to the proportion of controlling directors and supervisors, butnegatively associated with the proportion of outside directors and supervisors.Hypotheses 2a, 3a, 4a and 4c are supported. This indicates that there are stronginterdependent relationships among the IGMs in which ownership structure directlyaffects the composition of the board of directors and supervisory board, andsubsequently the IGMs’ joint impact on Tobin’s Q. This also raises the notion thatthe different objectives and strategy of controlling shareholders might drive corporateresults in different directions even by employing the same governance mechanisms.

In addition, Table 4 shows the proportion of controlling directors, controllingsupervisors is negatively correlated to firm performance though the relationshipswere not strong, and the findings relating to outside directors and supervisors andindependent directors were also not significant. Thus, the board compositionfindings do not support Hypotheses 2b, 3b, 3c, 4b and 4d. In other words, theboard of directors has not shown its effectiveness in ensuring value maximization infirms. Nevertheless, the result of FIRMSIZE shows a negative impact on firmperformance, which is consistent with Peng (2004) and Wei and Varela (2003).Controlling directors and controlling supervisors have a significantly positiveindirect impact while outside directors and supervisors have significant negativeindirect impact on the relationship between FIRMSIZE and performance. One of thepossible explanations is that larger firms may have more room for appropriation andexploitation of firm value by controlling shareholders via controlling directors/supervisors representation on boards. Lastly, the size of the two corporate boards areinversely related to performance, supporting the view of O’Regan and Oster (2005)that monitoring capability is reduced in a large board. In contrast, board meetings, asone of the most important measures of board activities according to Vafeas (1999),are found to be positively associated with Tobin’s Q. Since the frequency of boardmeetings reflects the time and efforts directors put in, this study suggests that highernumber of board meetings leads to a better performed board.

Discussion

Contributions

The growing wealth of research on the performance ramifications from theownership structure of firms has enhanced significantly our understanding of theachievements and weaknesses in the development of an effective corporategovernance system in various types of economies. However, in an emergingeconomy such as China where the state continues to dominate corporate ownership,it is increasingly accepted that an alternative to the traditional principal–agent model

742 H. W. Hu et al.

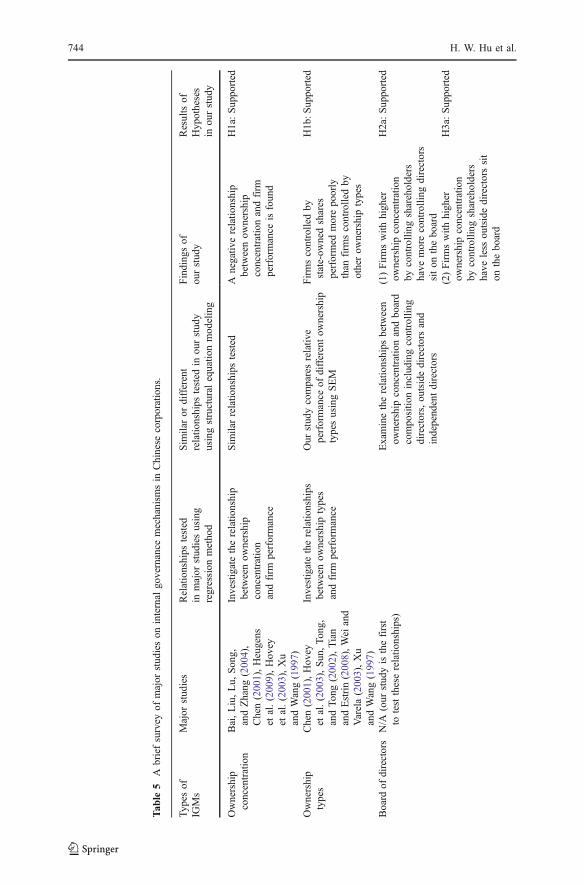

to examine the development of corporate governance is required. This study adoptsthe newly emerged principal–principal perspective (Young et al., 2008) to developan analysis of the governance effectiveness of multiple IGMs in reducing the conflictbetween controlling shareholders and minority shareholders in Chinese companies.The major findings presented in this study affirm the theoretical relevance ofemploying this new perspective and the significant empirical benefits of applyingSEM to go beyond single governance mechanism studies by providing new evidencehighlighting the complex relationships between ownership structure, board ofdirectors, supervisory board and firm performance. Our results show that of theIGMs investigated, ownership concentration has the most significant governanceimpact and has fundamentally shaped the principal–principal conflict prevalent inChinese firms. Overall, how our study contributes to the growing literature oncorporate governance in China is outlined in Table 5.

Our empirical findings provide clear evidence that ownership concentration not onlyimpacts negatively on firm performance, but also strongly influences board operationsthrough director/supervisor selection. It is notable that when ownership concentration ishigh, more controlling directors and supervisors were appointed but less outsidedirectors and supervisors were put on the board. The finding is consistent with ourexpectation that, out of self-interest, controlling shareholders tend to prefer feweroutsiders. Unfortunately, this situation exacerbates the principal–principal problemgiven the poor legal protection of shareholders in the country. Not surprisingly,outsiders, including independent directors and outside directors/supervisors who aresupposed tomitigate principal–principal conflicts, are found in this study to be incapableof effectively performing their expected function.

Using the technique of SEM, this study has analyzed the interdependence ofmultiple IGMs, and has documented the existence of the interconnectedness amongthese IGMs. Of the three IGMs, ownership concentration has the greatest impact onfirm performance though the effect is negative. Ownership concentration is also foundto indirectly affect firm performance through the other two IGMs. The results on thegovernance impacts of controlling directors and supervisors on firm performanceindicate negative direct relationships even though they are not significant. However,indirectly via ownership concentration, the joint impacts are negative and significant.In other words, the joint impacts of IGMs document stronger relationships on firmperformance than what an evaluation of a single board level evaluation would show.These findings therefore reinforce Berglöf and Claessens’ (2006) study on corporategovernance enforcement, which suggests that highly concentrated ownershipstructure has indeed weakened the governance role of other IGMs, particularly incountries such as China with poorly functioning external governance mechanisms.

In summary, this study not only provides support to the existing literature, butalso adds new perspective and findings that are not found in previous studies onlisted firms in China. First, extending the findings of Su et al. (2008) of higheragency costs under ownership concentration, this study suggests that poor firmperformance is also a result of the concentrated ownership structure. Second,instead of the conventional approach of searching for a relationship betweenownership types and firm performance in most of the earlier studies (Hovey et al.,2003; Wei & Varela, 2003; Xu & Wang, 1997), we compare the performanceimpact of different types of ownership, thus adding depth to the existing literature.

Internal governance mechanisms and firm performance in China 743

Tab

le5

Abriefsurvey

ofmajor

studieson

internal

governance

mechanism

sin

Chinese

corporations.

Typesof

IGMs

Major

studies

Relationships

tested

inmajor

stud

iesusing

regression

method

Sim

ilaror

different

relatio

nships

tested

inourstudy

usingstructural

equatio

nmodeling

Finding

sof

ourstud

yResultsof

Hyp

otheses

inou

rstud

y

Ownership

concentration

Bai,Liu,Lu,

Son

g,andZhang

(200

4),

Chen(200

1),Heugens

etal.(200

9),Hov

eyet

al.(200

3),Xu

andWang(199

7)

Investigatetherelatio

nship

betweenow

nership

concentration

andfirm

performance

Sim

ilarrelatio

nships

tested

Anegativ

erelatio

nship

betweenow

nership

concentrationandfirm

performance

isfoun

d

H1a:Suppo

rted

Ownership

types

Chen(200

1),Hov

eyet

al.(200

3),Sun,To

ng,

andTo

ng(200

2),Tian

andEstrin(200

8),W

eiand

Varela(200

3),Xu

andWang(199

7)

Investigatetherelatio

nships

betweenow

nershiptypes

andfirm

performance

Our

stud

ycomparesrelativ

eperformance

ofdifferentow

nership

typesusingSEM

Firmscontrolledby

state-ow

nedshares

performed

morepo

orly

than

firm

scontrolledby

otherow

nershiptypes

H1b

:Suppo

rted

Board

ofdirectors

N/A

(our

stud

yisthefirst

totesttheserelatio

nships)

Examinetherelatio

nships

between

ownershipconcentrationandboard

compositio

nincludingcontrolling

directors,outsidedirectorsand

independentdirectors

(1)Firmswith

high

erow

nershipconcentration

bycontrolling

shareholders

have

morecontrolling

directors

siton

thebo

ard

H2a:Suppo

rted

(2)Firmswith

high

erow

nershipconcentration

bycontrolling

shareholders

have

less

outsidedirectorssit

onthebo

ard

H3a:Suppo

rted

744 H. W. Hu et al.

Tab

le5

(con

tinued).

Typesof

IGMs

Major

studies

Relationships

tested

inmajor

stud

iesusing

regression

metho

d

Sim

ilaror

different

relatio

nships

tested

inourstudy

usingstructural

equatio

nmodeling

Finding

sof

ourstud

yResultsof

Hyp

otheses

inou

rstud

y

Bai

etal.(200

4),Chang

andWon

g(200

4),Chen

etal.(200

6),Peng(200

4)

Investigatetherelatio

nships

betweenboardcompositio

nandfirm

performance

Based

onthenew

analytical

perspectiveof

thisstudy,

similar

relatio

nships

tested

butwith

new

director

grouping

(nam

ely

controlling

directors,outside

directorsandindepend

entd

irectors)

Found

norelatio

nshipbetween

theproportio

nof

controlling

directors,outsidedirectors,

independentdirectorsand

firm

performance

H2b

,3b

,3c:

Rejected

Supervisory

board

N/A

(our

stud

yisthe

firstto

testthese

relatio

nships)

Examinetherelatio

nships

between

ownershipconcentrationand

supervisoryboardcompositio

nincludingcontrolling

supervisors

andou

tsidesupervisors

(1)Firmswith

high

erow

nership

concentrationby

controlling

shareholders

have

more

controlling

supervisorssit

onthesupervisoryboard

H4a:Sup

ported

(2)Firmswith

high

erow

nership

concentrationby

controlling

shareholders

have

less

outside

supervisorssiton

the

supervisorybo

ard

H4c:Suppo

rted

Tam

andHu(200

6)Investigatetherelatio

nships

betweensupervisor

board

compo

sitio

nandfirm

performance

Based

onthenew

analytical

perspectiveof

thisstudy,

similar

relatio

nships

tested

butwith

new

supervisor

grouping

(nam

ely

controlling

supervisorsand

outsidesupervisors)

Found

norelatio

nshipbetween

theproportio

nof

controlling

supervisors,outside

supervisors

andfirm

performance

H4b

,4d

:Rejected

Thissurvey

isnotintended

tobe

comprehensive.Rather,itisareferenceforcontrastinghow

ourstudyadds

totheexistin

gliteratureon

thistopic.

Internal governance mechanisms and firm performance in China 745

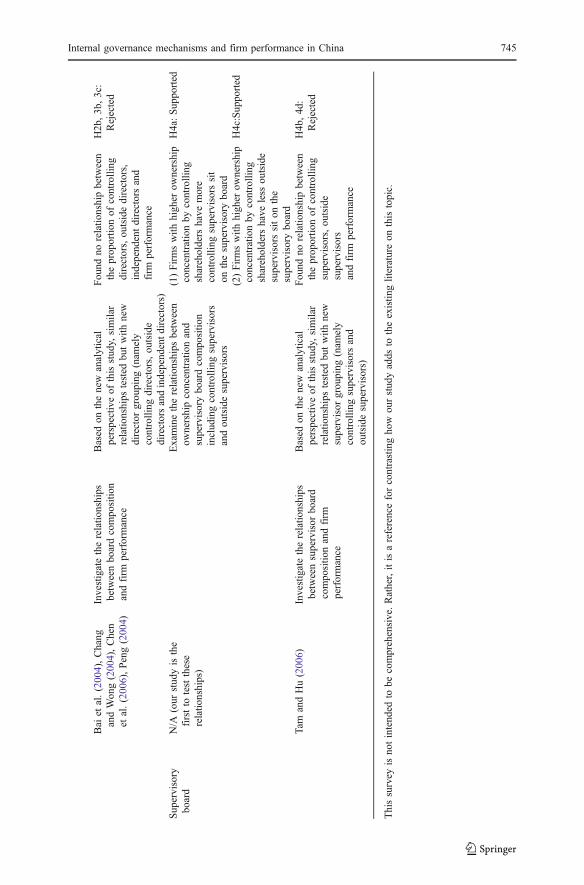

Third, existing research on board of directors (Peng, 2004; Tian & Lau, 2001) wasmostly conducted before the official introduction of independent directors. Differentinterpretations of director types, particularly independent directors, were used in thesestudies which have constrained the overall compatibility of their findings. Fourth, thisstudy has systematically examined the performance effect of supervisory board, anarea that has often been neglected in the past. Lastly, the integrative researchframework used in the study also adds insights to the understanding of the interactionsamong these multiples IGMs. Through the examination of the combined effects ofdifferent governance mechanisms, this contributes to the literature by producing betterknowledge of the interplay of the key governance forces in China.

Limitations and future research directions

Several issues can however be identified for future research. As China’s reform in2005 to gradually freeing the non-tradable state-owned shareholding in listedcompanies has been scheduled to be completed over the next few years, there willbe good opportunities to investigate the impact on the long existing concentratedownership problem. Although the reform implementation and its effects might take 4to 5 years to become apparent, evaluating the changes of the most important IGM (i.e.,ownership structure) and its impacts along the way will have analytical and empiricalsignificance for China and beyond. Also, owing to the relatively short period of timein having independent directors on Chinese boards, their governance impact in thecontext of firm performance is probably still too early to be captured as this study hasshown. As scholars such as Peng (2004) and Tenev and Zhang (2002) have questionedthe true independence of Chinese independent directors, there is indeed a need formore empirical and qualitative studies on board practices and dynamics in order togain a better understanding of these directors.

Conclusion

Research on the relationship between ownership and performance will continue to be afocus of the corporate governance literature in the future. For developing economiesexperiencing processes of ownership transformation, innovative analysis of the impactsof corporate ownership structure on the effectiveness of their currently available IGMsand firm performance is of particular interest. Through SEM, this study has producednew insights by extending the principal–principal perspective to China’s evolving IGMsand corporate governance landscape. Before conditions for developing effectiveexternal governance mechanisms mature, a better understanding of how IGMs work iscritical not only for scholars, but also for both regulators and practitioners.

References

Agrawal, A., & Knoeber, C. R. 1996. Firm performance and mechanisms to control agencyproblems between managers and shareholders. Journal of Financial and Quantitative Analysis, 31(3): 377–397.

746 H. W. Hu et al.

Andres, P. D., Azofra, V., & Lopez, F. 2005. Corporate boards in OECD countries: Size,composition, functioning and effectiveness. Corporate Governance: An International Review, 13(2): 197–210.

Bai, C., Liu, Q., Lu, J., Song, F. M., & Zhang, J. 2004. Corporate governance and market valuation inChina. Journal of Comparative Economics, 32(4): 599–616.

Berglöf, E., & Claessens, S. 2006. Enforcement and good corporate governance in developing countriesand transition economies. The World Bank Research Observer, 21(1): 123–150.

Berkman, H., Cole, R., & Fu, J. 2002. From state to state: Improving corporate governance when thegovernment is a large block holder. Working paper, University of Auckland.

Buck, T., Filatotchev, I., Demina, N., & Wright, M. 2003. Insider ownership, human resource strategiesand performance in a transition economy. Journal of International Business Studies, 34(6): 530–549.

Chang, E. C., & Wong, S. M. L. 2004. Political control and performance in China’s listed firms. Journalof Comparative Economics, 32(4): 617–636.

Chen, J. 2001. Ownership structure as corporate governance mechanism: Evidence from Chinese listedcompanies. Economics of Planning, 34(1–2): 53–72.

Chen, G., Firth, M., Gao, D. N., & Rui, O. M. 2006. Ownership structure, corporate governance and fraud:Evidence from China. Journal of Corporate Finance, 12(3): 424–448.

China Company Law. 1994. The Company Law of the People’s Republic of China.Chung, K. H., & Pruitt, S. W. 1994. A simple approximation of Tobin’s Q. Financial Management, 23(3):

70–74.Claessens, S., Djankov, S., Fan, J. P. H., & Lang, L. H. P. 1999. Expropriation of minority shareholders:

Evidence from East Asia. Policy Research working paper no. 2088, World Bank.Claessens, S., Djankov, S., & Lang, L. H. P. 2000. The separation of ownership and control in East Asian

corporations. Journal of Financial Economics, 58(1,2): 81–112.Claessens, S., Djankov, S., Fan, J. P. H., & Lang, L. H. P. 2002. Disentangling the incentive and

entrenchment effects of large shareholdings. Journal of Finance, 57(6): 2741–2771.CSRC. 2001. Guidelines for introducing independent directors to the board of directors of listed

companies. People’s Republic of China: China Securities Regulatory Commission.CSRC. 2002. Code of corporate governance for listed companies in China. People’s Republic of China:

China Securities Regulatory Commission.CSRC. 2003. Guidelines on contents and formats of information disclosure of annual report for listed

companies—2002 version (gongkai faixing zhenquan de gongsi xingxi pilu neirong yu geshi zhunze—2002 nian xiouding gao). People’s Republic of China: China Securities Regulatory Commission.

Dahya, J., Karbhari, Y., Xiao, J. Z., & Yang, M. 2003. The usefulness of the supervisory board report inChina. Corporate Governance: An International Review, 11(4): 308–321.

Dalton, D. R., Daily, C. M., Ellstrand, A. E., & Johnson, J. L. 1998. Meta-analytic reviews of boardcomposition, leadership structure, and financial performance. Strategic Management Journal, 19(3):269–290.

Dharwadkar, R., George, G., & Brandes, P. 2000. Privatization in emerging economies: An agency theoryperspective. Academy of Management Review, 25(3): 650–669.

Ding, Y., Zhang, H., & Zhang, J. 2007. Private vs. state ownership and earnings management:Evidence from Chinese listed companies. Corporate Governance: An International Review, 15(2):223–238.

Djankov, S. 1999. Ownership structure and enterprise restructuring in six newly independent states. PolicyResearch working paper no. 2047, World Bank.

Dong, X. L., & Gao, F. 2002. Ownership structure of the listed companies: Questions and solutions.Modern Economics Research (Dangdai Jingji Yanjiou), 3: 24–28.

Ees, H. V., Postma, T. J. B. M., & Sterken, E. 2003. Board characteristics and corporate performance inthe Netherlands. Eastern Economic Journal, 29(1): 41–58.

Faccio, M., Lang, L. H. P., & Young, L. 2001. Dividends and expropriation. The American EconomicReview, 91(1): 54–78.

Fama, E. F., & Jensen, M. C. 1983. Separation of ownership and control. Journal of Law and Economics,26(2): 301–325.

Haleblian, J., & Finkelstein, S. 1993. Top management team size, CEO dominance, and firm performance:The moderating roles of environmental turbulence and discretion. Academy of Management Journal,36(4): 844–863.

Heidrick, & Struggles. 2007. Benchmarking corporate governance in China. Chicago: Heidrick &Struggles International.

Internal governance mechanisms and firm performance in China 747

Heugens, P. P. M. A. R., van Essen, M., & van Oosterhout, J. 2009. Meta-analyzing ownershipconcentration and firm performance in Asia: Towards a more fine-grained understanding. Asia PacificJournal of Management, 26. doi:10.1007/s10490-008-9109-0.

Hillman, A. J., & Dalziel, T. 2003. Boards of directors and firm performance: Integrating agency andresource dependence perspectives. Academy of Management Review, 28(3): 383–396.

Hovey, M., Li, L., & Naughton, T. 2003. The relationship between valuation and ownership of listed firmsin China. Corporate Governance: An International Review, 11(2): 112–122.

Jensen, M. C., & Meckling, W. H. 1976. Theory of the firm: Managerial behavior, agency costs, andownership structure. Journal of Financial Economics, 3(4): 305–360.

Johnson, J. L., Daily, C. M., & Ellstrand, A. E. 1996. Board of directors: A review and research agenda.Journal of Management, 22(3): 409–438.

Kato, T., & Long, C. 2006. CEO turnover, firm performance, and enterprise reform in China: Evidencefrom micro data. Journal of Comparative Economics, 34(4): 796–817.

Lang, L. H. P., & Stulz, R. 1994. Tobin’s Q, corporate diversification, and firm performance. Journal ofPolitical Economy, 102(6): 1248–1280.

Mallin, C. A. 2007. Corporate governance. New York: Oxford University Press.Nee, V., Opper, S., & Wong, S. 2007. Developmental state and corporate governance in China.

Management and Organization Review, 3(1): 19–53.O’Regan, K., & Oster, S. M. 2005. Does the structure and composition of the board matter? The case of

nonprofit organizations. The Journal of Law, Economics, & Organization, 21(1): 205–227.Peng, M. W. 2004. Outside directors and firm performance during institutional transitions. Strategic

Management Journal, 25(5): 453–471.Peng, M. W., Zhang, S., & Li, X. 2007. CEO duality and firm performance during China’s institutional

transitions. Management and Organization Review, 3(2): 205–225.Peng, M. W., Wang, D. Y., & Jiang, Y. 2008. An institutional-based view of international business

strategy: A focus on emerging economies. Journal of International Business Studies, 39(5): 920–936.Pfeffer, J., & Salancik, G. R. 1978. The external control of organizations: A resource dependence

perspective. New York: Harper and Row.Rediker, K. J., & Seth, A. 1995. Board of directors and substitution effects of alternative governance

mechanisms. Strategic Management Journal, 16(2): 85–99.Shleifer, A., & Vishny, R. W. 1997. A survey of corporate governance. The Journal of Finance, 52(2):

737–783.Su, Y., Xu, D., & Phan, P. H. 2008. Principal–principal conflict in the governance of the Chinese public

corporation. Management and Organization Review, 4(1): 17–38.Sun, Q., Tong, W. H. S., & Tong, J. 2002. How does government ownership affect firm performance?

Evidence from China’s privatization experience. Journal of Business Finance and Accounting, 29(1/2): 1–27.

Tam, O. K. 1999. The development of corporate governance in China. Cheltenham: Edward Elgar.Tam, O. K., & Hu, H. W. 2006. Supervisory boards in Chinese corporate governance. In L. S. Ho & R.

Ash (Eds.). China, Hong Kong and the world economy: Study on globalization: 327–347. US:Macmillan.

Tam, O. K., & Tan, M. G.-S. 2007. Ownership, governance and firm performance in Malaysia. CorporateGovernance: An International Review, 15(2): 208–222.

Tenev, S., & Zhang, C. 2002. Corporate governance and enterprise reform in China: Building theinstitutions of modern markets. Washington: World Bank.

Tian, J. J., & Lau, C. 2001. Board composition, leadership structure and performance in Chineseshareholding companies. Asia Pacific Journal of Management, 18(2): 245–263.

Tian, L., & Estrin, S. 2008. Retained state shareholding in Chinese PLCs: Does government ownershipalways reduce corporate value? Journal of Comparative Economics, 36(1): 74–89.

Tong, C. K. 1996. Centripetal authority, differentiated networks: The social organization of Chinese firmsin Singapore. In G. G. Hamilton (Ed.). Asian business networks. Berlin: Walter de Gruyter.

Uzun, H., Szewczyk, S. H., & Varma, R. 2004. Board composition and corporate fraud. FinancialAnalysts Journal, 60(3): 33–43.

Vafeas, N. 1999. Board meeting frequency and firm performance. Journal of Financial Economics, 53(1):113–142.

van den Berghe, L., & Levrau, A. 2004. Evaluating boards of directors: What constitutes a good corporateboard? Corporate Governance: An International Review, 12(4): 461–478.

Wei, Z., & Varela, O. 2003. State equity ownership and firm market performance: Evidence from China’snewly privatized firms. Global Finance Journal, 14(1): 65–82.

748 H. W. Hu et al.

Xiao, J. Z., Dahya, J., & Lin, Z. 2004. A grounded theory exposition of the role of the supervisory boardin China. British Journal of Management, 15(1): 39–55.

Xu, X. N., & Wang, Y. 1997. Ownership structure, corporate governance, and corporate performance: Thecase of Chinese stock companies. Policy Research working paper no. 1794, World Bank.

Yeh, Y. H., Lee, T. S., & Woidtke, T. 2001. Family control and corporate governance: Evidence fromTaiwan. International Review of Finance, 2(1/2): 21–48.

Yermack, D. 1996. Higher market valuation of companies with a small board of directors. Journal ofFinancial Economics, 40(2): 185–211.

Yiu, D., Bruton, G. D., & Lu, Y. 2005. Understanding business group performance in an emergingeconomy: Acquiring resources and capabilities in order to prosper. Journal of Management Studies,42(1): 183–206.

Yoshikawa, T., & McGuire, J. 2008. Change and continuity in Japanese corporate governance. AsiaPacific Journal of Management, 25(1): 5–24.

Young, M. N., Peng, M. W., Ahlstrom, D., Bruton, G. D., & Jiang, Y. 2008. Corporate governance inemerging economies: A review of the principal–principal perspective. Journal of ManagementStudies, 45(1): 196–220.

Helen Wei Hu (PhD, Monash University) is a lecturer at the Department of Management and Marketing,University of Melbourne, Australia. Her research interests are corporate governance, with a focus onemerging economies, and Chinese business and management. She is also an Honorary Research Fellow atMonash University, Australia.

On Kit Tam (PhD, La Trobe University) is a professor of economics and Deputy Pro Vice-Chancellor atRMIT University, Australia. He was previously Deputy Dean of the Faculty of Business and Economics,Monash University, Australia. His research interests include corporate governance, financial and corporatedevelopment in Asia Pacific, and foreign direct investment and economic development. He currentlyserves as an independent director of a financial joint venture between two major Australian and Chinesefinancial institutions.

Monica Guo-Sze Tan (PhD, Monash University) is a manager at Deloitte Touch Tohmatsu, Australia,specializing in Risk Services. Her research interests are corporate governance and firm valuation. Sheholds a BA from the University of Western Ontario, Canada, and a Master of Management from MonashUniversity, Australia.

Internal governance mechanisms and firm performance in China 749