Embed Size (px)

Citation preview

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

June 2022

As at 30 June 2022

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

Agenda

i. Introduction, Portfolio Manager Profile & Portfolio Strategy

ii. Investment Culture & Team Structure

iii. Portfolio Construction & Risk Management

iv. White Oak India Equity Fund V

v. Case Studies

vi. Summary of Terms

vii. Investment Case for Indian Equities

viii. Appendix

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

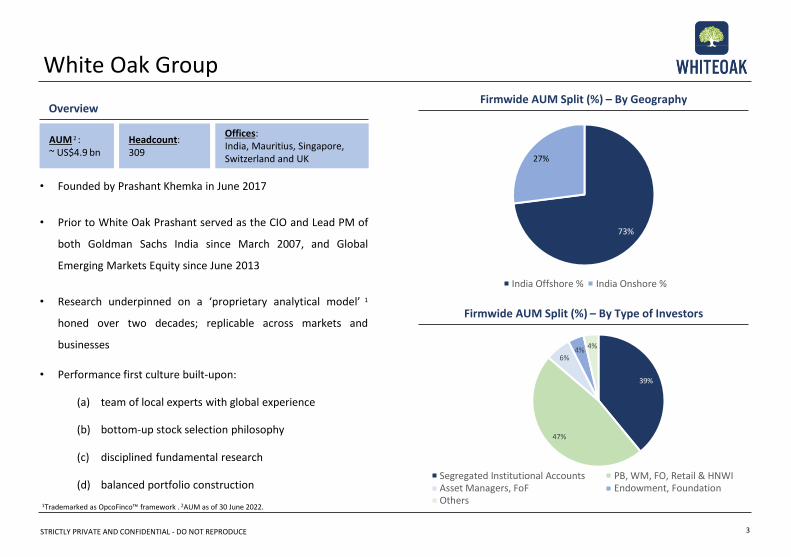

White Oak Group

3

• Founded by Prashant Khemka in June 2017

• Prior to White Oak Prashant served as the CIO and Lead PM of

both Goldman Sachs India since March 2007, and Global

Emerging Markets Equity since June 2013

• Research underpinned on a ‘proprietary analytical model’ 1

honed over two decades; replicable across markets and

businesses

• Performance first culture built-upon:

(a) team of local experts with global experience

(b) bottom-up stock selection philosophy

(c) disciplined fundamental research

(d) balanced portfolio construction

OverviewFirmwide AUM Split (%) – By Geography

Headcount:309

1Trademarked as OpcoFinco™ framework . 2AUM as of 30 June 2022.

AUM 2 :~ US$4.9 bn

Offices:India, Mauritius, Singapore, Switzerland and UK

Firmwide AUM Split (%) – By Type of Investors

73%

27%

India Offshore % India Onshore %

39%

47%

6%4%

4%

Segregated Institutional Accounts PB, WM, FO, Retail & HNWIAsset Managers, FoF Endowment, FoundationOthers

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

▪ Prashant took over as CIO and Lead PM of GS GEM Strategy in 2013with approximately US$600 mn in total assets

▪ Scaled GEM business to US$2.6 bn with distribution across multiplechannels in Europe, Asia and USA

▪ During his tenure, the strategy delivered peer group leadingcumulative 36.3% gross USD returns2 vs. 13.1% for its benchmark

▪ Prashant launched GS India Equity strategy in March 2007 with US$5.0mn seed capital from Goldman Sachs

▪ Scaled GS India Equity business to US$2.5 bn with distributionacross multiple channels in Europe, Asia, and USA

▪ Since inception the strategy delivered peer group leadingcumulative 265.8% gross USD returns1 vs. 66.1% for its benchmark

CIO and Lead PM of GS GEM Equity CIO and Lead PM of GS India Equity

Extensive investing record across India, GEM and the US

Founder’s Profile and Track Record

▪ Prashant joined Goldman Sachs Asset Management (GSAM) in 2000 in the US Growth Equity team

▪ In 2004, he became Senior PM and Co-Chair of the Investment Committee on the US Growth Equity team which managed US$25 bn

▪ Returned to Mumbai in 2006 to start GSAM India business, where he served as CIO and CEO / Co-CEO until 2017

▪ In 2013, Prashant moved to Singapore as CIO and Lead PM of both India and Global Emerging Markets

▪ Directly managed more than US$5.0 bn out of the US$6.5 bn managed by his team

▪ Prashant and the funds managed by him at GSAM earned several awards including Citywire AAA rating and FundCalibre Elite rating

▪ Prashant is AAA rated by Citywire based on the three year risk-adjusted performance across all funds he is managing to 31st May 2022

1Past performance Gross of Fees in US$ for GS India Equity Portfolio. 2Past performance Gross of Fees in US$ for GS EM Equity Portfolio. “Past performance is not a reliable indicator of future results and returns may increase or decrease as a result of currency fluctuations. There can be no assurance that comparable results can be achieved or that similar investment strategy can be implemented or that investment objectives can be achieved.”

4

0

~ 2.5bn

0

500

1000

1500

2000

2500

3000

2007 2017

GSAM India Equity AUM (US$ mn)

~ 675mn

~ 2.6bn

0

500

1000

1500

2000

2500

3000

2013 2017GSAM GEM Equity AUM (US$ mn)

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

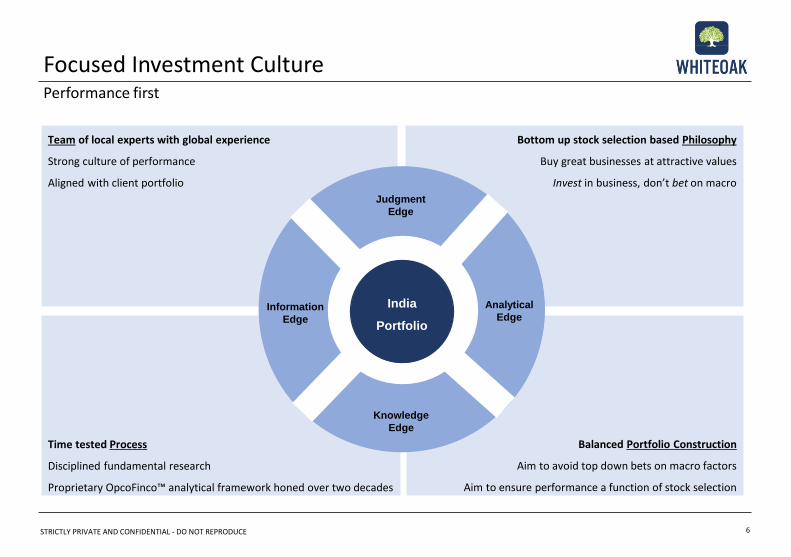

Investment Culture: Team, Philosophy, Process & Portfolio Construction

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

Balanced Portfolio Construction

Aim to avoid top down bets on macro factors

Aim to ensure performance a function of stock selection

Bottom up stock selection based Philosophy

Buy great businesses at attractive values

Invest in business, don’t bet on macro

Time tested Process

Disciplined fundamental research

Proprietary OpcoFinco™ analytical framework honed over two decades

Team of local experts with global experience

Strong culture of performance

Aligned with client portfolio

Information

Edge

Knowledge

Edge

Judgment

Edge

Analytical

EdgeIndia Portfolio

India

Portfolio

Focused Investment CulturePerformance first

6

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

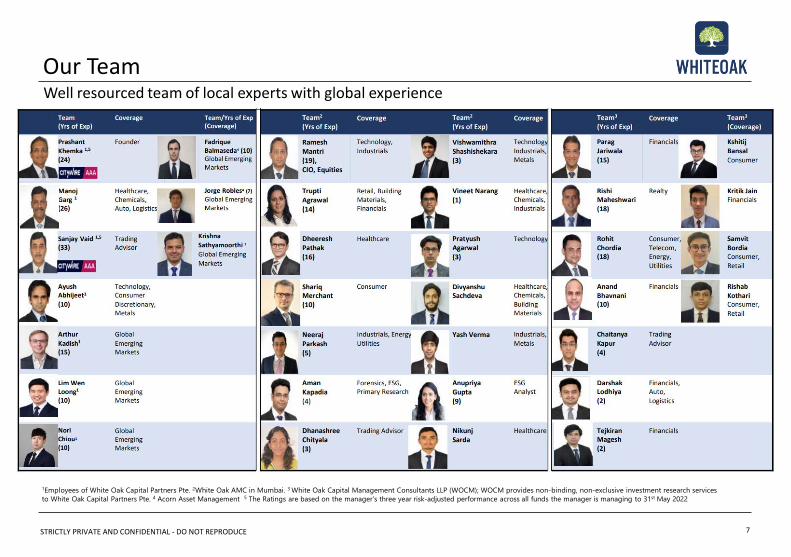

Our TeamWell resourced team of local experts with global experience

7

1Employees of White Oak Capital Partners Pte. 2White Oak AMC in Mumbai. 3 White Oak Capital Management Consultants LLP (WOCM); WOCM provides non-binding, non-exclusive investment research services

to White Oak Capital Partners Pte. 4 Acorn Asset Management 5 The Ratings are based on the manager’s three year risk-adjusted performance across all funds the manager is managing to 31st May 2022

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

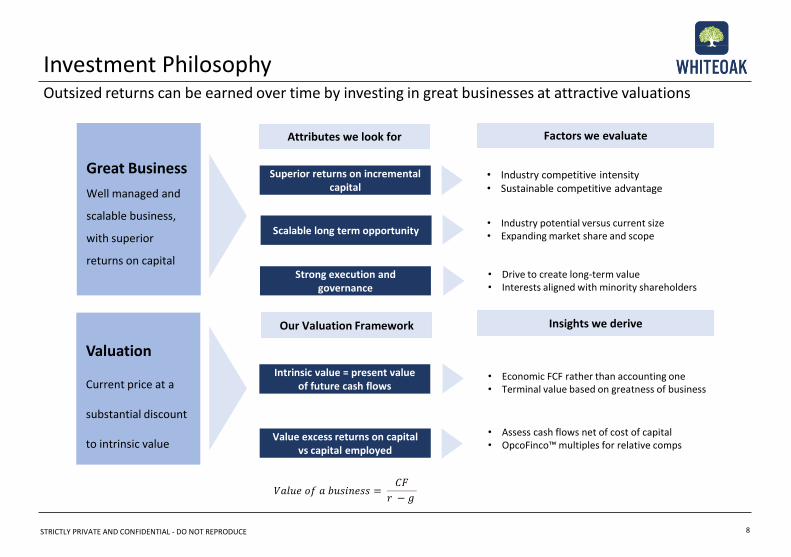

Factors we evaluate

Great Business

Well managed and

scalable business,

with superior

returns on capital

Superior returns on incremental capital

Scalable long term opportunity

Strong execution and governance

Intrinsic value = present value of future cash flows

• Industry competitive intensity• Sustainable competitive advantage

• Industry potential versus current size• Expanding market share and scope

• Drive to create long-term value• Interests aligned with minority shareholders

Attributes we look for

Our Valuation Framework

• Economic FCF rather than accounting one• Terminal value based on greatness of business

• Assess cash flows net of cost of capital• OpcoFinco™ multiples for relative comps

Value excess returns on capital vs capital employed

Insights we derive

Investment PhilosophyOutsized returns can be earned over time by investing in great businesses at attractive valuations

8

Valuation

Current price at a

substantial discount

to intrinsic value

𝑉𝑎𝑙𝑢𝑒 𝑜𝑓 𝑎 𝑏𝑢𝑠𝑖𝑛𝑒𝑠𝑠 =𝐶𝐹

𝑟 − 𝑔

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE 9

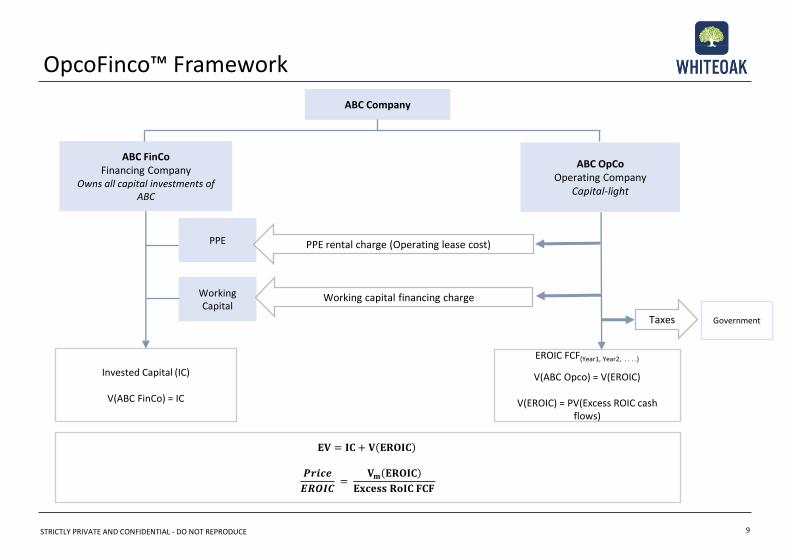

OpcoFinco™ Framework

ABC Company

ABC FinCo Financing Company

Owns all capital investments of ABC

ABC OpCoOperating Company

Capital-light

PPE

Working Capital

PPE rental charge (Operating lease cost)

Working capital financing charge

𝐄𝐕 = 𝐈𝐂 + 𝐕 𝐄𝐑𝐎𝐈𝐂

𝑷𝒓𝒊𝒄𝒆

𝑬𝑹𝑶𝑰𝑪=

𝐕𝐦 𝐄𝐑𝐎𝐈𝐂

𝐄𝐱𝐜𝐞𝐬𝐬 𝐑𝐨𝐈𝐂 𝐅𝐂𝐅

EROIC FCF(Year1, Year2, . . . .)

V(ABC Opco) = V(EROIC)

V(EROIC) = PV(Excess ROIC cash flows)

Taxes Government

Invested Capital (IC)

V(ABC FinCo) = IC

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

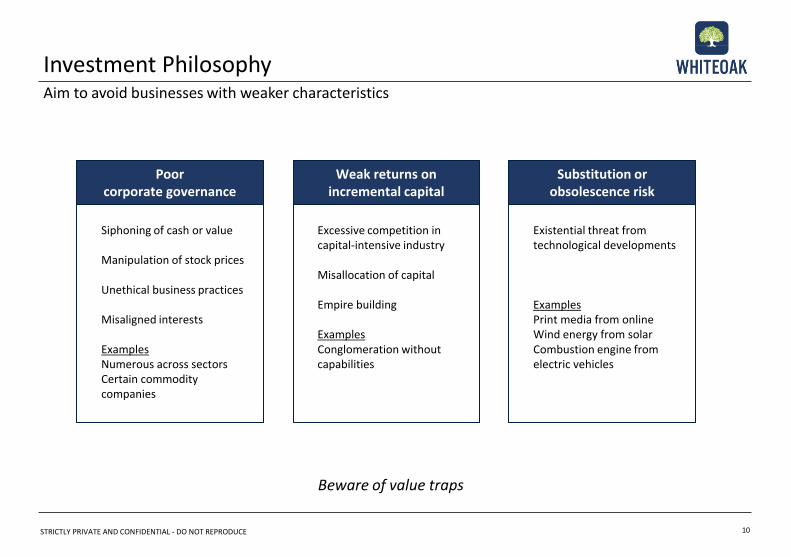

Existential threat from technological developments

ExamplesPrint media from onlineWind energy from solarCombustion engine from electric vehicles

Siphoning of cash or value

Manipulation of stock prices

Unethical business practices

Misaligned interests

ExamplesNumerous across sectorsCertain commodity companies

Beware of value traps

Excessive competition in capital-intensive industry

Misallocation of capital

Empire building

ExamplesConglomeration without capabilities

Substitution or obsolescence risk

Weak returns on incremental capital

Poor corporate governance

Investment PhilosophyAim to avoid businesses with weaker characteristics

10

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

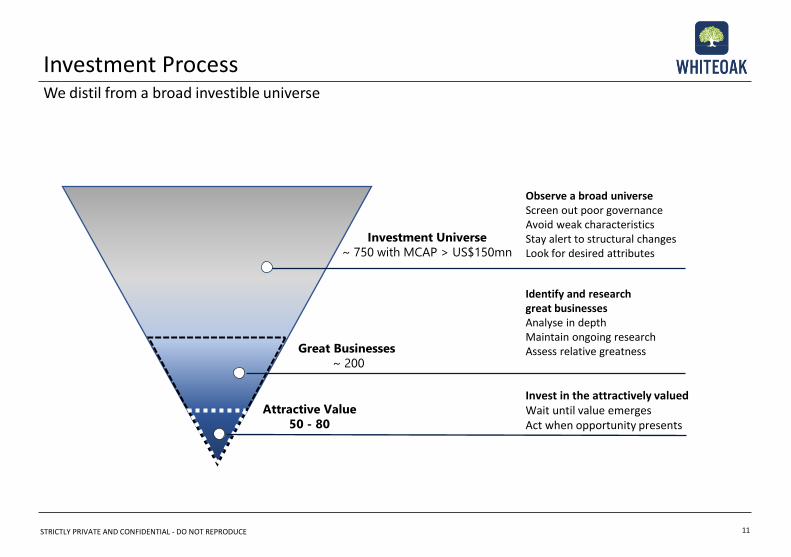

Investment ProcessWe distil from a broad investible universe

11

Observe a broad universeScreen out poor governanceAvoid weak characteristicsStay alert to structural changesLook for desired attributes

Identify and research great businessesAnalyse in depthMaintain ongoing researchAssess relative greatness

Invest in the attractively valuedWait until value emergesAct when opportunity presents

Investment Universe

~ 750 with MCAP > US$150mn

Great Businesses

~ 200

Attractive Value

50 - 80

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

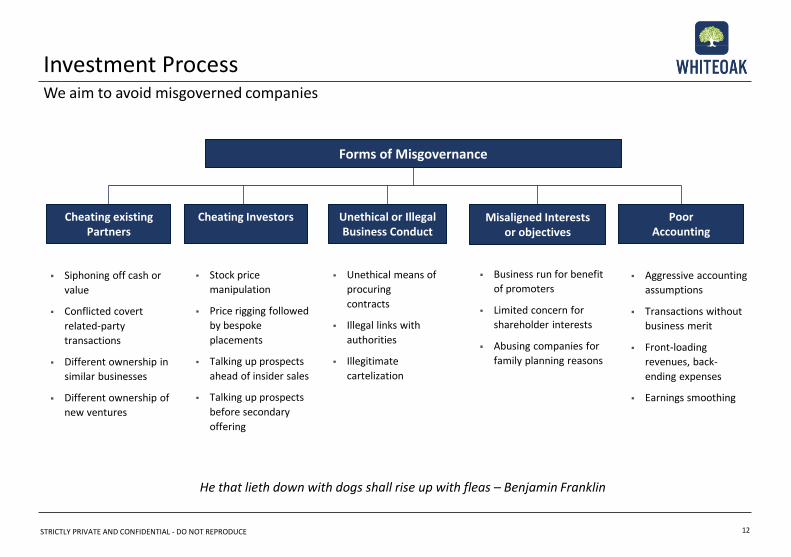

Poor Accounting

Cheating InvestorsCheating existing Partners

Misaligned Interests or objectives

Forms of Misgovernance

Unethical or Illegal Business Conduct

▪ Siphoning off cash or

value

▪ Conflicted covert

related-party

transactions

▪ Different ownership in

similar businesses

▪ Different ownership of

new ventures

▪ Stock price

manipulation

▪ Price rigging followed

by bespoke

placements

▪ Talking up prospects

ahead of insider sales

▪ Talking up prospects

before secondary

offering

▪ Aggressive accounting

assumptions

▪ Transactions without

business merit

▪ Front-loading

revenues, back-

ending expenses

▪ Earnings smoothing

▪ Business run for benefit

of promoters

▪ Limited concern for

shareholder interests

▪ Abusing companies for

family planning reasons

▪ Unethical means of

procuring

contracts

▪ Illegal links with

authorities

▪ Illegitimate

cartelization

He that lieth down with dogs shall rise up with fleas – Benjamin Franklin

Investment ProcessWe aim to avoid misgoverned companies

12

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

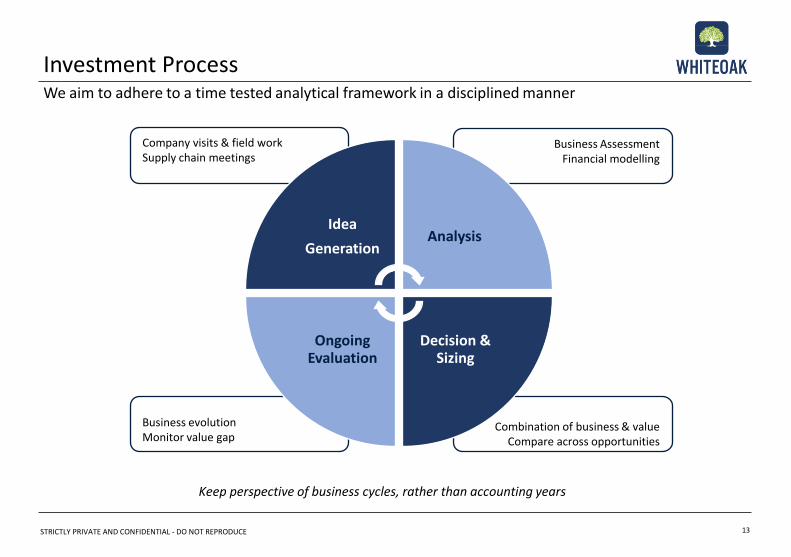

Business AssessmentFinancial modelling

Business evolutionMonitor value gap

Combination of business & valueCompare across opportunities

Keep perspective of business cycles, rather than accounting years

Company visits & field workSupply chain meetings

Investment ProcessWe aim to adhere to a time tested analytical framework in a disciplined manner

13

Idea

GenerationAnalysis

Decision & Sizing

Ongoing Evaluation

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

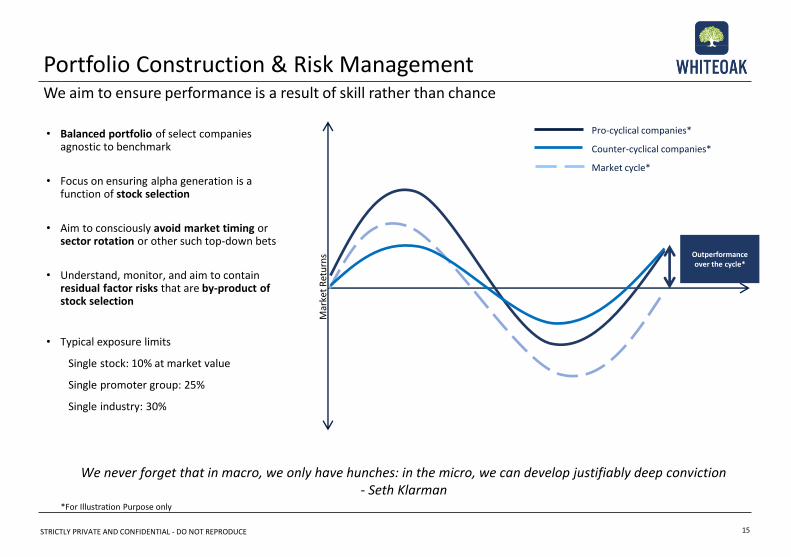

Portfolio Construction & Risk Management

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

• Balanced portfolio of select companies agnostic to benchmark

• Focus on ensuring alpha generation is a function of stock selection

• Aim to consciously avoid market timing or sector rotation or other such top-down bets

• Understand, monitor, and aim to contain residual factor risks that are by-product of stock selection

• Typical exposure limits

Single stock: 10% at market value

Single promoter group: 25%

Single industry: 30%

We never forget that in macro, we only have hunches: in the micro, we can develop justifiably deep conviction- Seth Klarman

Portfolio Construction & Risk ManagementWe aim to ensure performance is a result of skill rather than chance

Outperformance over the cycle*

Pro-cyclical companies*

Counter-cyclical companies*

Market cycle*

Mar

ket

Ret

urn

s

*For Illustration Purpose only

15

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

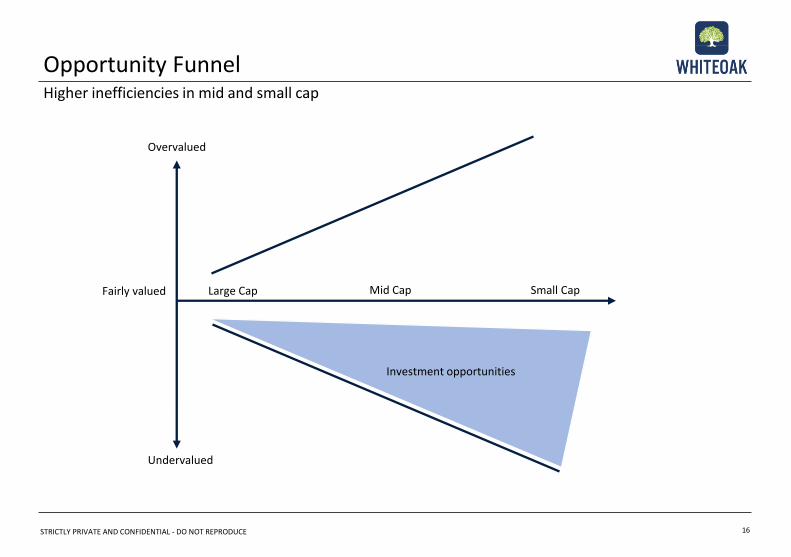

Large Cap

Investment opportunities

Small CapMid Cap

Overvalued

Undervalued

Fairly valued

Opportunity FunnelHigher inefficiencies in mid and small cap

16

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

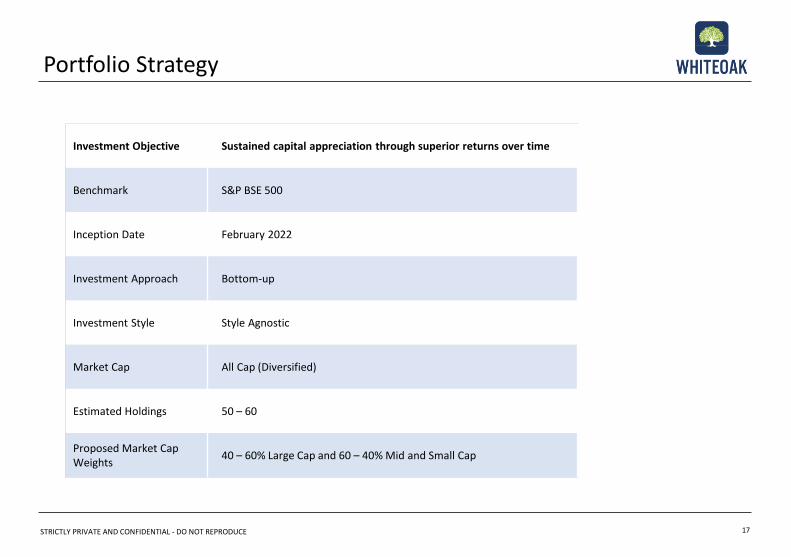

Investment Objective Sustained capital appreciation through superior returns over time

Benchmark S&P BSE 500

Inception Date February 2022

Investment Approach Bottom-up

Investment Style Style Agnostic

Market Cap All Cap (Diversified)

Estimated Holdings 50 – 60

Proposed Market Cap Weights

40 – 60% Large Cap and 60 – 40% Mid and Small Cap

Portfolio Strategy

17

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE 18

White Oak India Equity Fund V

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

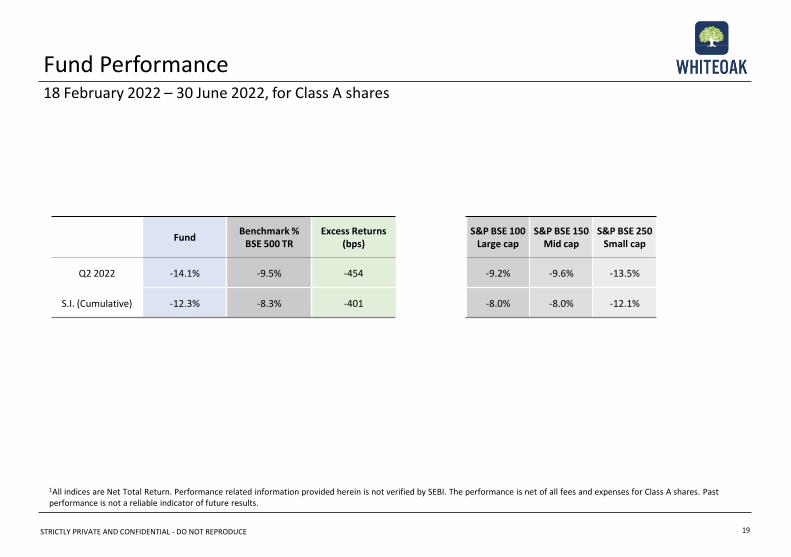

Fund Performance18 February 2022 – 30 June 2022, for Class A shares

19

` FundBenchmark %

BSE 500 TRExcess Returns

(bps)

Q2 2022 -14.1% -9.5% -454

S.I. (Cumulative) -12.3% -8.3% -401

S&P BSE 100 Large cap

S&P BSE 150 Mid cap

S&P BSE 250Small cap

-9.2% -9.6% -13.5%

-8.0% -8.0% -12.1%

1All indices are Net Total Return. Performance related information provided herein is not verified by SEBI. The performance is net of all fees and expenses for Class A shares. Past performance is not a reliable indicator of future results.

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

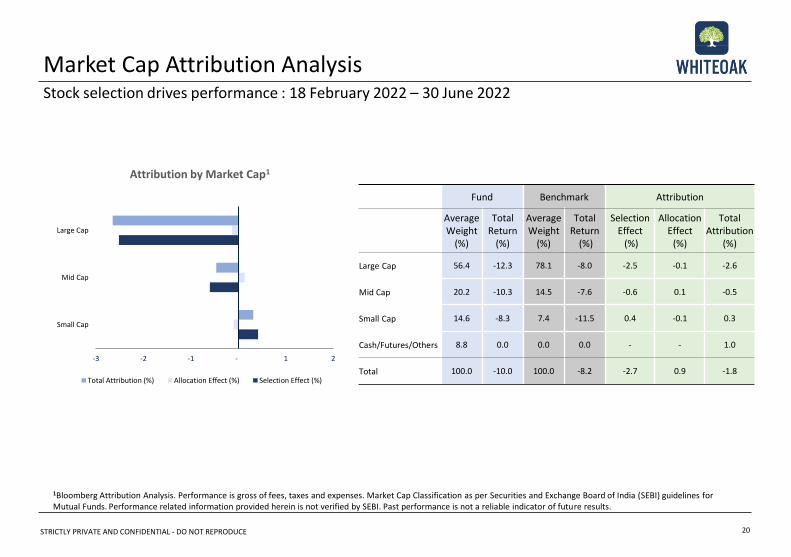

Fund Benchmark Attribution

Average Weight

(%)

Total Return

(%)

Average Weight

(%)

Total Return

(%)

Selection Effect

(%)

Allocation Effect

(%)

Total Attribution

(%)

Large Cap 56.4 -12.3 78.1 -8.0 -2.5 -0.1 -2.6

Mid Cap 20.2 -10.3 14.5 -7.6 -0.6 0.1 -0.5

Small Cap 14.6 -8.3 7.4 -11.5 0.4 -0.1 0.3

Cash/Futures/Others 8.8 0.0 0.0 0.0 - - 1.0

Total 100.0 -10.0 100.0 -8.2 -2.7 0.9 -1.8

Attribution by Market Cap1

Market Cap Attribution AnalysisStock selection drives performance : 18 February 2022 – 30 June 2022

20

1Bloomberg Attribution Analysis. Performance is gross of fees, taxes and expenses. Market Cap Classification as per Securities and Exchange Board of India (SEBI) guidelines for Mutual Funds. Performance related information provided herein is not verified by SEBI. Past performance is not a reliable indicator of future results.

-3 -2 -1 - 1 2

Small Cap

Mid Cap

Large Cap

Total Attribution (%) Allocation Effect (%) Selection Effect (%)

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

Sector Fund Benchmark Attribution

Average Weight

(%)

Total Return

(%)

Average Weight

(%)

Total Return

(%)

Selection Effect

(%)

Allocation Effect

(%)

Total Attributio

n (%)

Comm Services 3.1 -15.5 2.9 -10.4 -0.1 0.0 -0.2

Consumer Disc 14.7 -8.2 8.3 -4.7 -0.6 0.4 -0.2

Consumer Staples 4.7 -3.3 7.6 2.9 -0.3 -0.2 -0.5

Energy 0.0 0.0 10.1 4.5 0.0 -1.2 -1.2

Financials 28.2 -10.9 28.8 -11.6 0.2 0.0 0.2

Health Care 7.0 -9.9 5.4 -9.2 -0.1 0.0 -0.1

Industrials 5.9 -10.9 7.3 -7.6 -0.2 0.0 -0.1

Information Tech 15.7 -16.0 13.5 -15.6 0.2 -0.3 -0.2

Materials 11.2 -15.5 10.5 -16.0 0.1 -0.2 -0.1

Real Estate 0.7 23.4 0.8 -12.6 0.2 0.0 0.3

Utilities 0.0 0.0 4.7 7.2 0.0 -0.6 -0.6

Cash/Futures/Others 8.8 0.0 0.0 0.0 - - 1.0

Total 100.0 -10.0 100.0 -8.2 -0.6 -1.2 -1.8

Sector Attribution AnalysisStock selection drives performance : 18 February 2022 – 30 June 2022

21

Attribution by Sector1

1 Bloomberg Attribution Analysis: GICS Classification. Performance is gross of fees, taxes and expenses. Performance related information provided herein is not verified by SEBI. Past performance is not a reliable indicator of future results.

-2 -1 - 1 2

Utilities

Real Estate

Materials

Information Tech

Industrials

Health Care

Financials

Energy

Consumer Staples

Consumer Disc

Comm Services

Allocation Effect (%) Selection Effect (%)

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

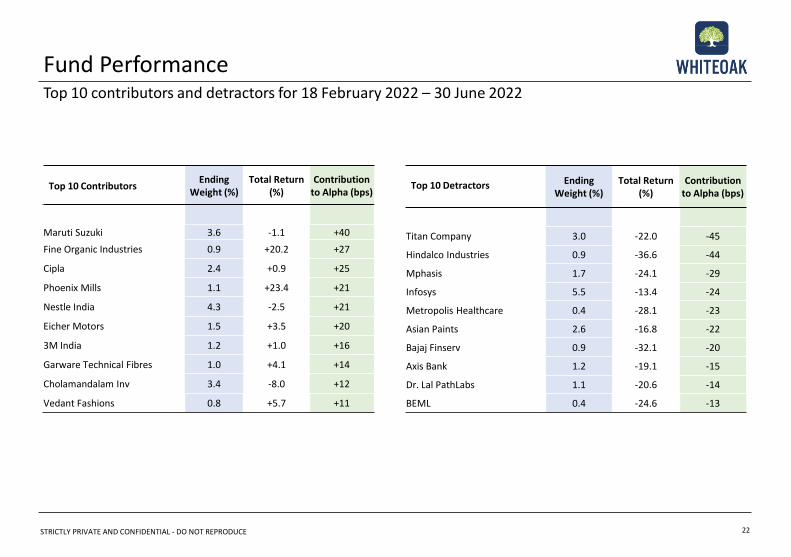

Top 10 ContributorsEnding

Weight (%) Total Return

(%)Contribution

to Alpha (bps)

Maruti Suzuki 3.6 -1.1 +40

Fine Organic Industries 0.9 +20.2 +27

Cipla 2.4 +0.9 +25

Phoenix Mills 1.1 +23.4 +21

Nestle India 4.3 -2.5 +21

Eicher Motors 1.5 +3.5 +20

3M India 1.2 +1.0 +16

Garware Technical Fibres 1.0 +4.1 +14

Cholamandalam Inv 3.4 -8.0 +12

Vedant Fashions 0.8 +5.7 +11

Top 10 Detractors EndingWeight (%)

Total Return (%)

Contribution to Alpha (bps)

Titan Company 3.0 -22.0 -45

Hindalco Industries 0.9 -36.6 -44

Mphasis 1.7 -24.1 -29

Infosys 5.5 -13.4 -24

Metropolis Healthcare 0.4 -28.1 -23

Asian Paints 2.6 -16.8 -22

Bajaj Finserv 0.9 -32.1 -20

Axis Bank 1.2 -19.1 -15

Dr. Lal PathLabs 1.1 -20.6 -14

BEML 0.4 -24.6 -13

Fund PerformanceTop 10 contributors and detractors for 18 February 2022 – 30 June 2022

22

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

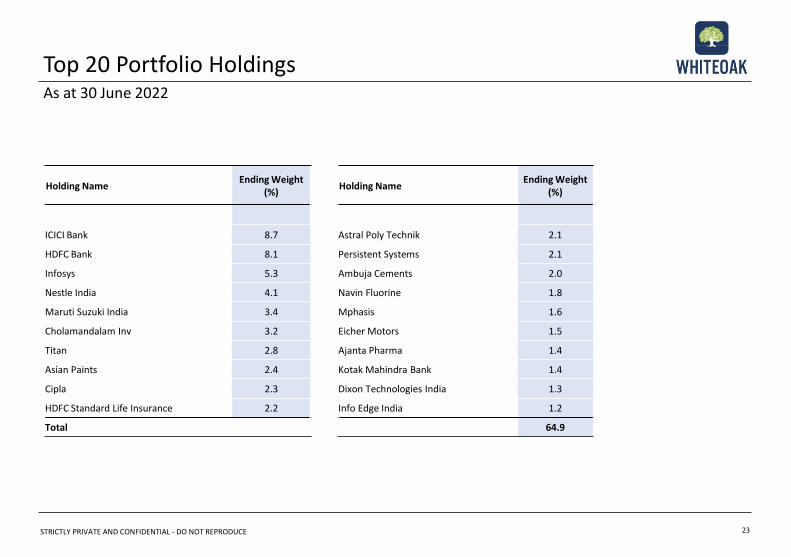

Holding NameEnding Weight

(%)

ICICI Bank 8.7

HDFC Bank 8.1

Infosys 5.3

Nestle India 4.1

Maruti Suzuki India 3.4

Cholamandalam Inv 3.2

Titan 2.8

Asian Paints 2.4

Cipla 2.3

HDFC Standard Life Insurance 2.2

Total

Top 20 Portfolio HoldingsAs at 30 June 2022

23

Holding NameEnding Weight

(%)

Astral Poly Technik 2.1

Persistent Systems 2.1

Ambuja Cements 2.0

Navin Fluorine 1.8

Mphasis 1.6

Eicher Motors 1.5

Ajanta Pharma 1.4

Kotak Mahindra Bank 1.4

Dixon Technologies India 1.3

Info Edge India 1.2

64.9

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

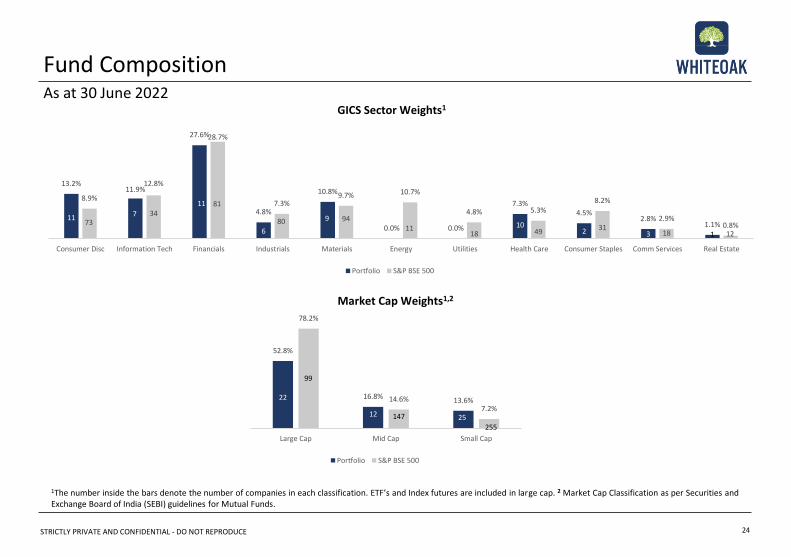

52.8%

16.8%13.6%

78.2%

14.6%7.2%

22

12 25

99

147

255

Large Cap Mid Cap Small Cap

Portfolio S&P BSE 500

13.2%11.9%

27.6%

4.8%

10.8%

0.0% 0.0%

7.3%4.5%

2.8%1.1%

8.9%

12.8%

28.7%

7.3%9.7% 10.7%

4.8% 5.3%8.2%

2.9%0.8%

11 7

11

6

9

0

0

102 3 1

7334

81

80 9411

18 4931

18 12

Consumer Disc Information Tech Financials Industrials Materials Energy Utilities Health Care Consumer Staples Comm Services Real Estate

Portfolio S&P BSE 500

Market Cap Weights1,2

GICS Sector Weights1

1The number inside the bars denote the number of companies in each classification. ETF’s and Index futures are included in large cap. 2 Market Cap Classification as per Securities and Exchange Board of India (SEBI) guidelines for Mutual Funds.

Fund Composition

24

As at 30 June 2022

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE 25

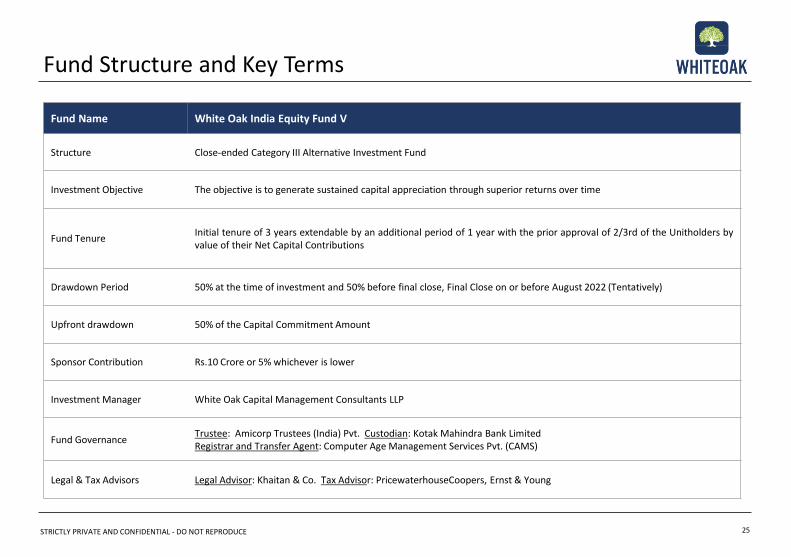

Fund Structure and Key Terms

Fund Name White Oak India Equity Fund V

Structure Close-ended Category III Alternative Investment Fund

Investment Objective The objective is to generate sustained capital appreciation through superior returns over time

Fund TenureInitial tenure of 3 years extendable by an additional period of 1 year with the prior approval of 2/3rd of the Unitholders byvalue of their Net Capital Contributions

Drawdown Period 50% at the time of investment and 50% before final close, Final Close on or before August 2022 (Tentatively)

Upfront drawdown 50% of the Capital Commitment Amount

Sponsor Contribution Rs.10 Crore or 5% whichever is lower

Investment Manager White Oak Capital Management Consultants LLP

Fund GovernanceTrustee: Amicorp Trustees (India) Pvt. Custodian: Kotak Mahindra Bank Limited Registrar and Transfer Agent: Computer Age Management Services Pvt. (CAMS)

Legal & Tax Advisors Legal Advisor: Khaitan & Co. Tax Advisor: PricewaterhouseCoopers, Ernst & Young

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

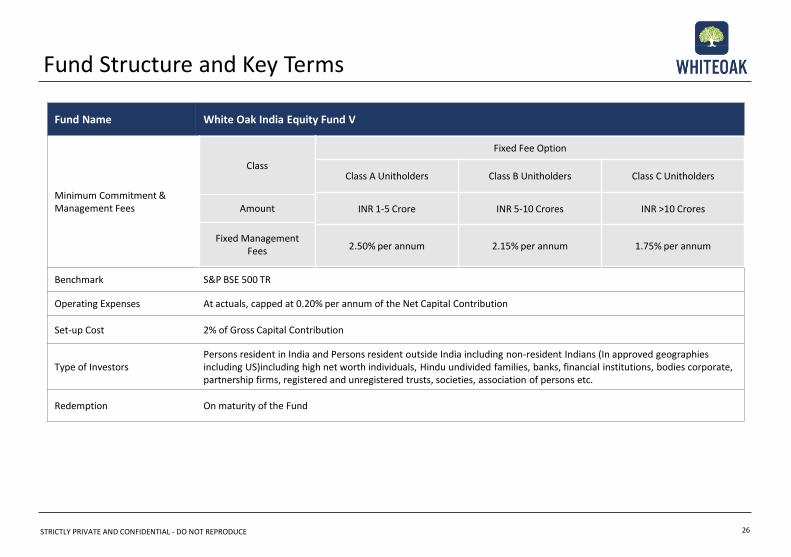

Fund Structure and Key Terms

26

Fund Name White Oak India Equity Fund V

Minimum Commitment & Management Fees

Benchmark S&P BSE 500 TR

Operating Expenses At actuals, capped at 0.20% per annum of the Net Capital Contribution

Set-up Cost 2% of Gross Capital Contribution

Type of InvestorsPersons resident in India and Persons resident outside India including non-resident Indians (In approved geographies including US)including high net worth individuals, Hindu undivided families, banks, financial institutions, bodies corporate,partnership firms, registered and unregistered trusts, societies, association of persons etc.

Redemption On maturity of the Fund

Class

Amount

Fixed Management Fees

Fixed Fee Option

Class A Unitholders Class B Unitholders Class C Unitholders

INR 1-5 Crore INR 5-10 Crores INR >10 Crores

2.50% per annum 2.15% per annum 1.75% per annum

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

Case Studies*

*The following case studies are illustrative examples only. The illustrated companies included here may or may not necessarily be held in any portfolio at any time in the past or currently.

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

Case Studies* - Infoedge

28

*The following case studies are illustrative examples only. The illustrated companies included here may or may not necessarily be held in any portfolio at any time in the past or currently.

India’s leading classifieds company

• Infoedge’s Naukri.com is India’s dominant

online jobs portal with 70%+ traffic share. It also

owns 99acres.com which is the No. 1 online

real-estate classifieds portal with 50% traffic

share

• India’s low internet penetration provides a long

runway of growth for these dominant classified

businesses

• Management has an excellent track record of

execution. It has also made investments in

India’s leading food delivery company (Zomato),

and India’s top online policy aggregator

(Policybazar)

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

Case Studies* - Navin Fluorine International

29

*The following case studies are illustrative examples only. The illustrated companies included here may or may not necessarily be held in any portfolio at any time in the past or currently.

Emerging leader in fluorination

• Established in 1967, NFIL has successfully

transitioned its business model from a domestic

focused, commoditised inorganic fluoride

manufacturer to a well-established specialty

chemical and CRAMS player globally

• Fluorination is one of the fastest growing

chemistry globally owing to its lipophilic

properties which increases the potency and

efficacy of formulations. Development

capabilities (esp. multi-step) in fluorine have a

long gestation period and hence there are only a

handful of players in fluorine chemistry globally

• NFIL has seen renewed aggression under the

leadership of Radhesh Welling who has more

than 25 years of experience in the speciality

chemicals industry. Post his joining, the

management has created the right incentive

structure for employees at all levels to ensure

value accretive growth

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

Investment Case for Indian Equities

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

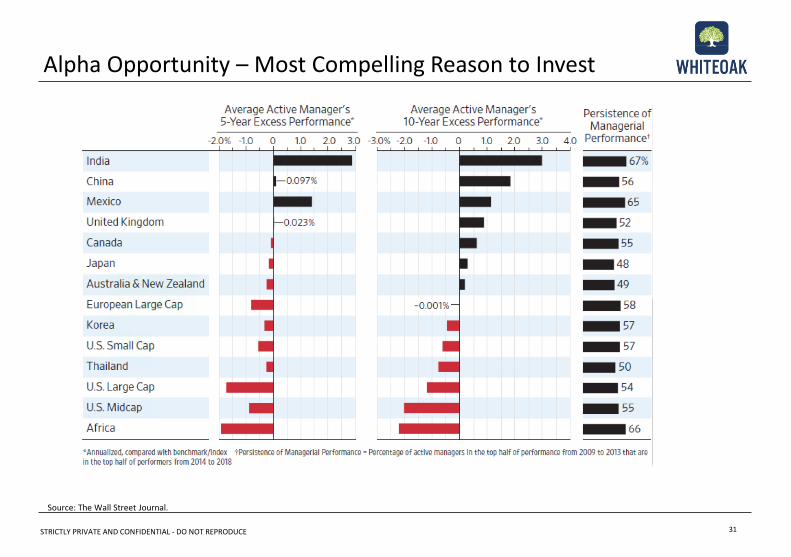

Alpha Opportunity – Most Compelling Reason to Invest

31

Source: The Wall Street Journal.

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

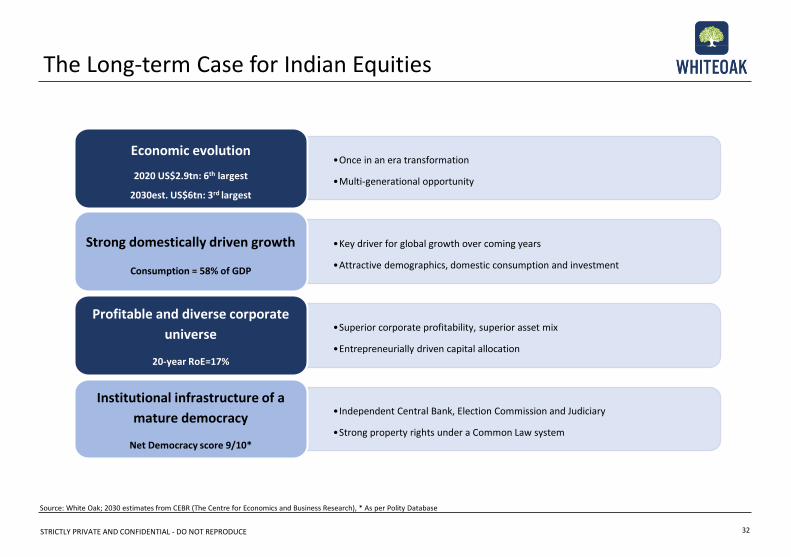

•Once in an era transformation

•Multi-generational opportunity

Economic evolution

2020 US$2.9tn: 6th largest

2030est. US$6tn: 3rd largest

•Key driver for global growth over coming years

•Attractive demographics, domestic consumption and investment

Strong domestically driven growth

Consumption = 58% of GDP

•Superior corporate profitability, superior asset mix

•Entrepreneurially driven capital allocation

Profitable and diverse corporate

universe

20-year RoE=17%

•Independent Central Bank, Election Commission and Judiciary

•Strong property rights under a Common Law system

Institutional infrastructure of a

mature democracy

Net Democracy score 9/10*

The Long-term Case for Indian Equities

32

Source: White Oak; 2030 estimates from CEBR (The Centre for Economics and Business Research), * As per Polity Database

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

FY9

3

FY9

4

FY9

5

FY9

6

FY9

7

FY9

8

FY9

9

FY0

0

FY0

1

FY0

2

FY0

3

FY0

4

FY0

5

FY0

6

FY0

7

FY0

8

FY0

9

FY1

0

FY1

1

FY1

2

FY1

3

FY1

4

FY1

5

FY1

6

FY1

7

FY1

8

FY1

9

FY2

0

FY2

1

FY2

2

FY 93-96: 45% CAGR

FY 96-03: 1% CAGR

FY 03-08: 25% CAGR

FY 08-20: 5.1% CAGR

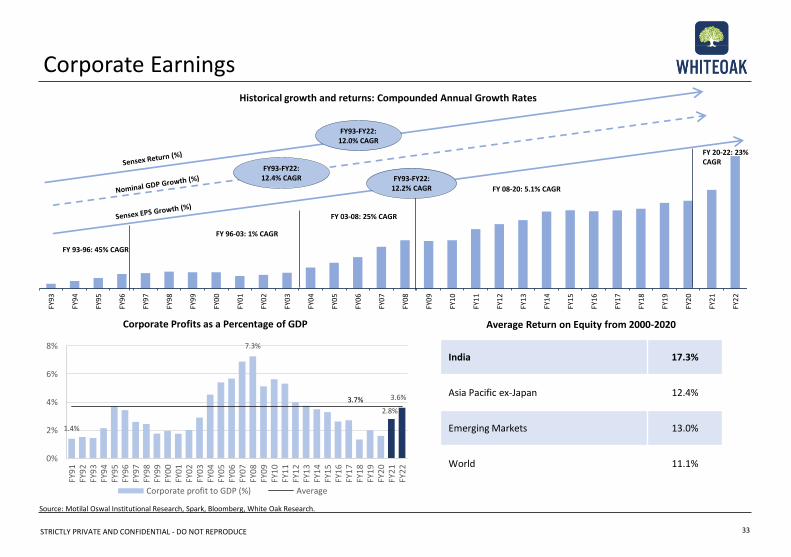

Historical growth and returns: Compounded Annual Growth Rates

Source: Motilal Oswal Institutional Research, Spark, Bloomberg, White Oak Research.

Corporate Profits as a Percentage of GDP Average Return on Equity from 2000-2020

India 17.3%

Asia Pacific ex-Japan 12.4%

Emerging Markets 13.0%

World 11.1%

Corporate Earnings

33

FY93-FY22: 12.2% CAGR

FY93-FY22: 12.4% CAGR

FY93-FY22: 12.0% CAGR

FY 20-22: 23% CAGR

1.4%

7.3%

2.8%

3.6%3.7%

0%

2%

4%

6%

8%

FY9

1FY

92

FY9

3FY

94

FY9

5FY

96

FY9

7FY

98

FY9

9FY

00

FY0

1FY

02

FY0

3FY

04

FY0

5FY

06

FY0

7FY

08

FY0

9FY

10

FY1

1FY

12

FY1

3FY

14

FY1

5FY

16

FY1

7FY

18

FY1

9FY

20

FY2

1FY

22

Corporate profit to GDP (%) Average

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

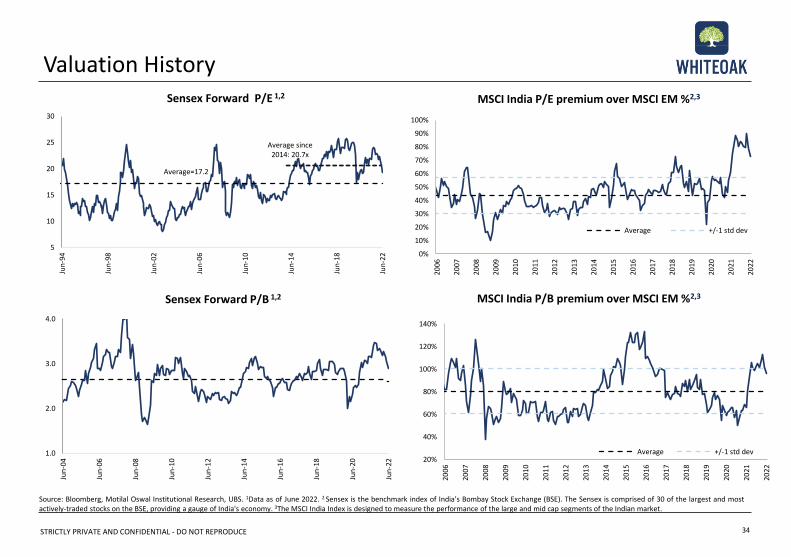

Source: Bloomberg, Motilal Oswal Institutional Research, UBS. 1Data as of June 2022. 2 Sensex is the benchmark index of India's Bombay Stock Exchange (BSE). The Sensex is comprised of 30 of the largest and mostactively-traded stocks on the BSE, providing a gauge of India's economy. 3The MSCI India Index is designed to measure the performance of the large and mid cap segments of the Indian market.

Valuation History

34

Sensex Forward P/B 1,2

Sensex Forward P/E 1,2 MSCI India P/E premium over MSCI EM %2,3

MSCI India P/B premium over MSCI EM %2,3

5

10

15

20

25

30

Jun

-94

Jun

-98

Jun

-02

Jun

-06

Jun

-10

Jun

-14

Jun

-18

Jun

-22

Average since 2014: 20.7x

Average=17.2

1.0

2.0

3.0

4.0

Jun

-04

Jun

-06

Jun

-08

Jun

-10

Jun

-12

Jun

-14

Jun

-16

Jun

-18

Jun

-20

Jun

-22

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

Average +/-1 std dev

20%

40%

60%

80%

100%

120%

140%

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

Average +/-1 std dev

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

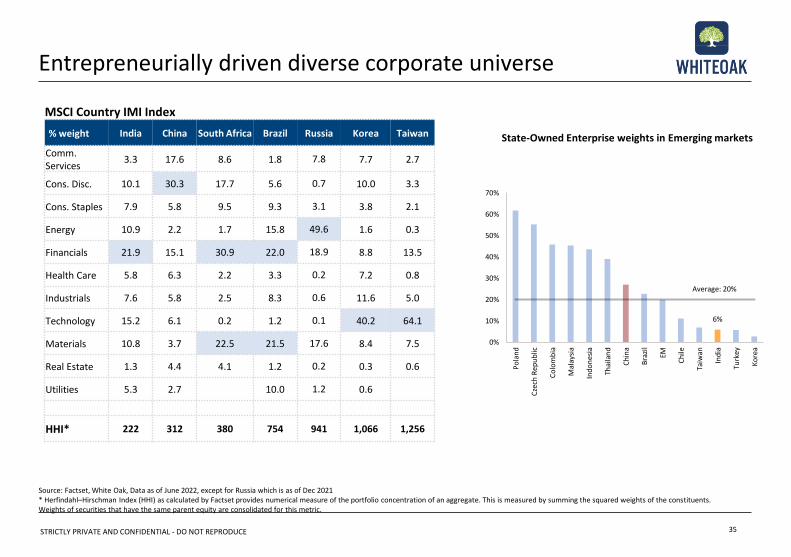

Entrepreneurially driven diverse corporate universe

35

Source: Factset, White Oak, Data as of June 2022, except for Russia which is as of Dec 2021* Herfindahl–Hirschman Index (HHI) as calculated by Factset provides numerical measure of the portfolio concentration of an aggregate. This is measured by summing the squared weights of the constituents. Weights of securities that have the same parent equity are consolidated for this metric.

State-Owned Enterprise weights in Emerging markets

MSCI Country IMI Index

% weight India China South Africa Brazil Russia Korea Taiwan

Comm. Services

3.3 17.6 8.6 1.8 7.8 7.7 2.7

Cons. Disc. 10.1 30.3 17.7 5.6 0.7 10.0 3.3

Cons. Staples 7.9 5.8 9.5 9.3 3.1 3.8 2.1

Energy 10.9 2.2 1.7 15.8 49.6 1.6 0.3

Financials 21.9 15.1 30.9 22.0 18.9 8.8 13.5

Health Care 5.8 6.3 2.2 3.3 0.2 7.2 0.8

Industrials 7.6 5.8 2.5 8.3 0.6 11.6 5.0

Technology 15.2 6.1 0.2 1.2 0.1 40.2 64.1

Materials 10.8 3.7 22.5 21.5 17.6 8.4 7.5

Real Estate 1.3 4.4 4.1 1.2 0.2 0.3 0.6

Utilities 5.3 2.7 10.0 1.2 0.6

HHI* 222 312 380 754 941 1,066 1,256

6%

Average: 20%

0%

10%

20%

30%

40%

50%

60%

70%

Po

lan

d

Cze

ch R

epu

blic

Co

lom

bia

Mal

aysi

a

Ind

on

esia

Thai

lan

d

Ch

ina

Bra

zil

EM

Ch

ile

Taiw

an

Ind

ia

Turk

ey

Ko

rea

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE 36

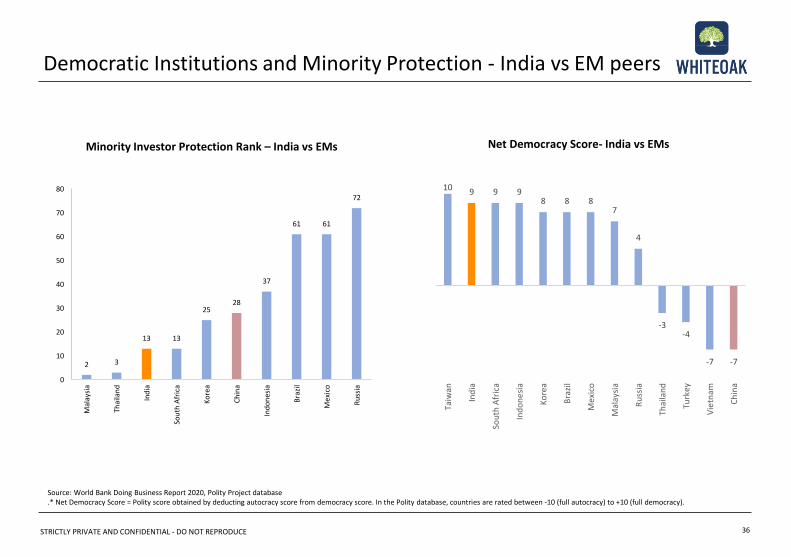

Democratic Institutions and Minority Protection - India vs EM peers

Minority Investor Protection Rank – India vs EMs

Source: World Bank Doing Business Report 2020, Polity Project database.* Net Democracy Score = Polity score obtained by deducting autocracy score from democracy score. In the Polity database, countries are rated between -10 (full autocracy) to +10 (full democracy).

2 3

13 13

2528

37

61 61

72

0

10

20

30

40

50

60

70

80

Mal

aysi

a

Thai

lan

d

Ind

ia

Sou

th A

fric

a

Ko

rea

Ch

ina

Ind

on

esia

Bra

zil

Me

xico

Ru

ssia

Net Democracy Score- India vs EMs

10 9 9 98 8 8

7

4

-3-4

-7 -7

Taiw

an

Ind

ia

Sou

th A

fric

a

Ind

on

esi

a

Ko

rea

Bra

zil

Mex

ico

Mal

aysi

a

Ru

ssia

Thai

lan

d

Turk

ey

Vie

tnam

Ch

ina

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

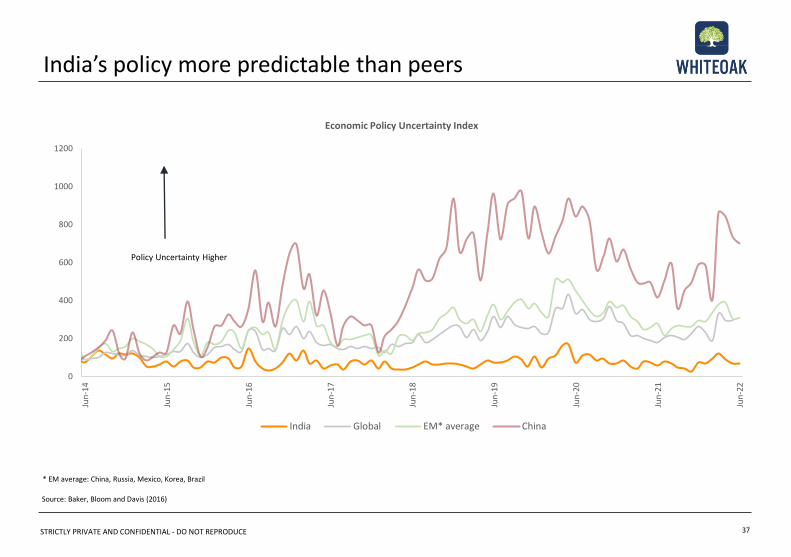

India’s policy more predictable than peers

37

Source: Baker, Bloom and Davis (2016)

* EM average: China, Russia, Mexico, Korea, Brazil

0

200

400

600

800

1000

1200

Jun

-14

Jun

-15

Jun

-16

Jun

-17

Jun

-18

Jun

-19

Jun

-20

Jun

-21

Jun

-22

Economic Policy Uncertainty Index

India Global EM* average China

Policy Uncertainty Higher

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

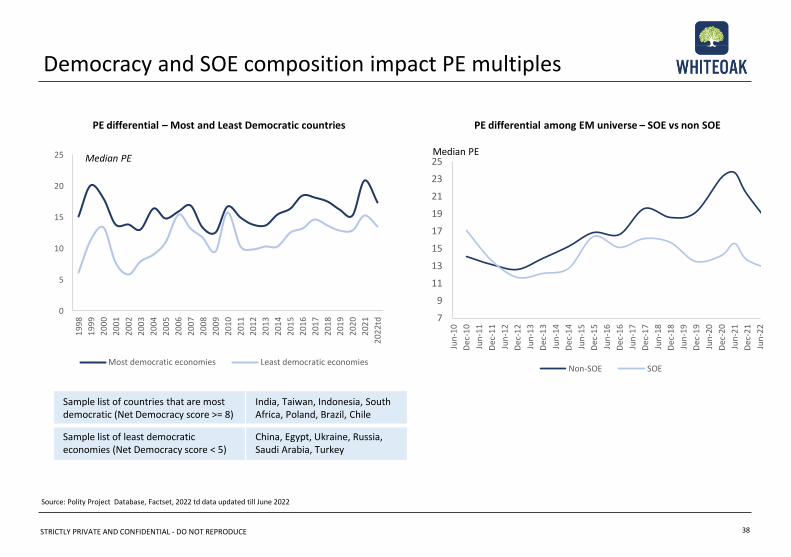

Source: Polity Project Database, Factset, 2022 td data updated till June 2022

PE differential – Most and Least Democratic countries

Democracy and SOE composition impact PE multiples

38

Sample list of countries that are most democratic (Net Democracy score >= 8)

India, Taiwan, Indonesia, South Africa, Poland, Brazil, Chile

Sample list of least democratic economies (Net Democracy score < 5)

China, Egypt, Ukraine, Russia, Saudi Arabia, Turkey

PE differential among EM universe – SOE vs non SOE

Median PE

0

5

10

15

20

25

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7

201

8

201

9

202

0

202

1

202

2td

Most democratic economies Least democratic economies

Median PE

7

9

11

13

15

17

19

21

23

25

Jun

-10

Dec

-10

Jun

-11

Dec

-11

Jun

-12

Dec

-12

Jun

-13

Dec

-13

Jun

-14

Dec

-14

Jun

-15

Dec

-15

Jun

-16

Dec

-16

Jun

-17

Dec

-17

Jun

-18

Dec

-18

Jun

-19

Dec

-19

Jun

-20

Dec

-20

Jun

-21

Dec

-21

Jun

-22

Non-SOE SOE

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

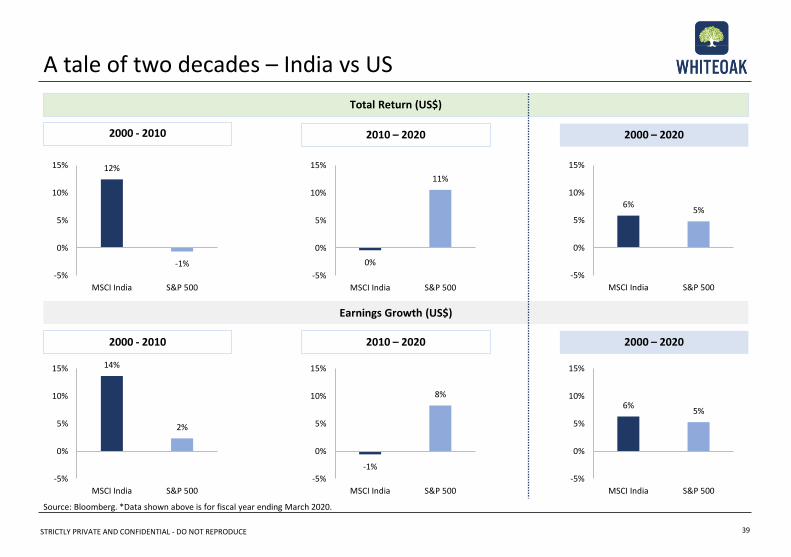

Source: Bloomberg. *Data shown above is for fiscal year ending March 2020.

A tale of two decades – India vs US

2000 - 2010

39

2010 – 2020 2000 – 2020

2000 - 2010 2010 – 2020 2000 – 2020

Earnings Growth (US$)

Total Return (US$)

12%

-1%

-5%

0%

5%

10%

15%

MSCI India S&P 500

0%

11%

-5%

0%

5%

10%

15%

MSCI India S&P 500

6%5%

-5%

0%

5%

10%

15%

MSCI India S&P 500

14%

2%

-5%

0%

5%

10%

15%

MSCI India S&P 500

-1%

8%

-5%

0%

5%

10%

15%

MSCI India S&P 500

6%5%

-5%

0%

5%

10%

15%

MSCI India S&P 500

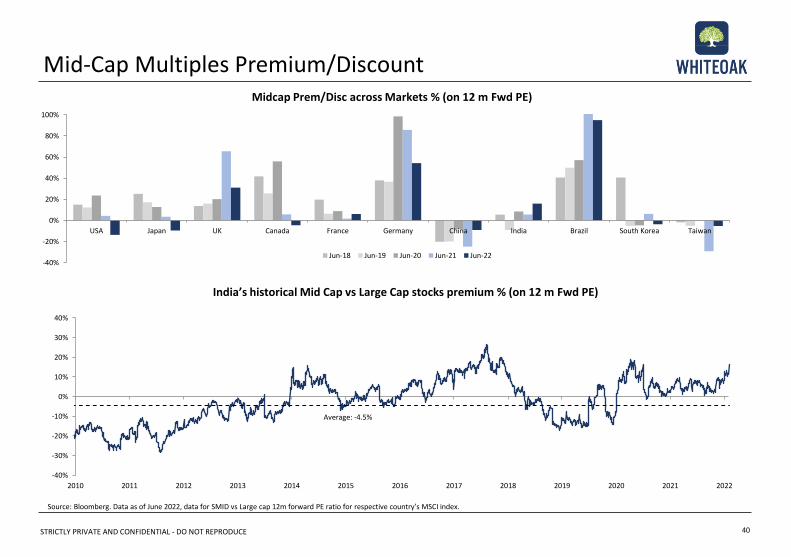

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE 40

Mid-Cap Multiples Premium/Discount

India’s historical Mid Cap vs Large Cap stocks premium % (on 12 m Fwd PE)

Midcap Prem/Disc across Markets % (on 12 m Fwd PE)

Source: Bloomberg. Data as of June 2022, data for SMID vs Large cap 12m forward PE ratio for respective country’s MSCI index.

-40%

-20%

0%

20%

40%

60%

80%

100%

USA Japan UK Canada France Germany China India Brazil South Korea Taiwan

Jun-18 Jun-19 Jun-20 Jun-21 Jun-22

Average: -4.5%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

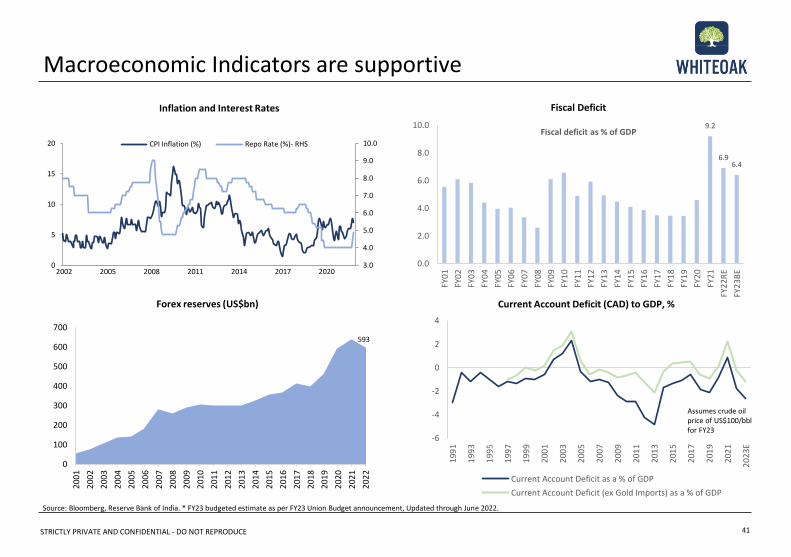

Macroeconomic Indicators are supportive

Inflation and Interest Rates

41

Forex reserves (US$bn) Current Account Deficit (CAD) to GDP, %

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

0

5

10

15

20

2002 2005 2008 2011 2014 2017 2020

CPI Inflation (%) Repo Rate (%)- RHS

Source: Bloomberg, Reserve Bank of India. * FY23 budgeted estimate as per FY23 Union Budget announcement, Updated through June 2022.

Fiscal Deficit

0

100

200

300

400

500

600

700

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7

201

8

201

9

202

0

202

1

202

2

593

9.2

6.96.4

0.0

2.0

4.0

6.0

8.0

10.0

FY0

1

FY0

2

FY0

3

FY0

4

FY0

5

FY0

6

FY0

7

FY0

8

FY0

9

FY1

0

FY1

1

FY1

2

FY1

3

FY1

4

FY1

5

FY1

6

FY1

7

FY1

8

FY1

9

FY2

0

FY2

1

FY2

2RE

FY2

3BE

Fiscal deficit as % of GDP

-6

-4

-2

0

2

4

199

1

199

3

199

5

199

7

199

9

200

1

200

3

200

5

200

7

200

9

201

1

201

3

201

5

201

7

201

9

202

1

202

3E

Current Account Deficit as a % of GDP

Current Account Deficit (ex Gold Imports) as a % of GDP

Assumes crude oil price of US$100/bblfor FY23

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

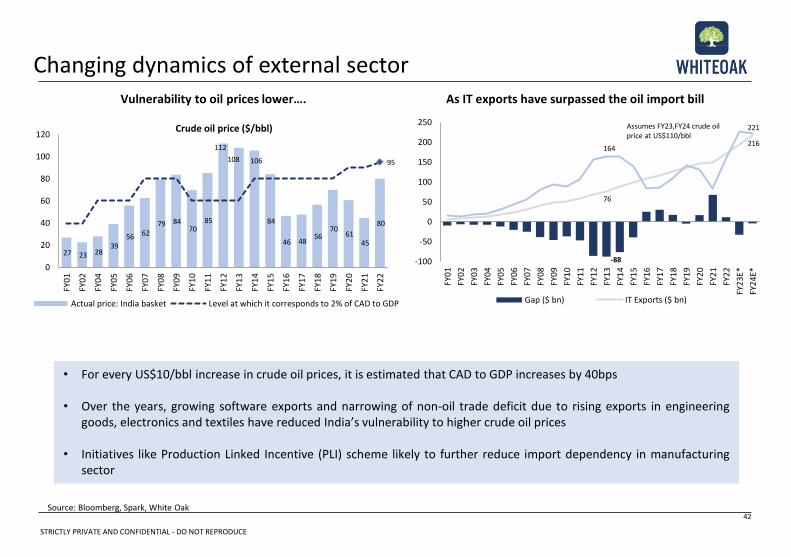

Changing dynamics of external sector

Source: Bloomberg, Spark, White Oak42

Vulnerability to oil prices lower…. As IT exports have surpassed the oil import bill

• For every US$10/bbl increase in crude oil prices, it is estimated that CAD to GDP increases by 40bps

• Over the years, growing software exports and narrowing of non-oil trade deficit due to rising exports in engineeringgoods, electronics and textiles have reduced India’s vulnerability to higher crude oil prices

• Initiatives like Production Linked Incentive (PLI) scheme likely to further reduce import dependency in manufacturingsector

27 23 28 39

56 62 79 84

70 85

112

108 106

84

46 48 56

70 61

45

80

95

0

20

40

60

80

100

120

FY0

1

FY0

2

FY0

4

FY0

5

FY0

6

FY0

7

FY0

8

FY0

9

FY1

0

FY1

1

FY1

2

FY1

3

FY1

4

FY1

5

FY1

6

FY1

7

FY1

8

FY1

9

FY2

0

FY2

1

FY2

2

Crude oil price ($/bbl)

Actual price: India basket Level at which it corresponds to 2% of CAD to GDP

Assumes FY23,FY24 crude oil price at US$110/bbl

-88

76

216164

221

-100

-50

0

50

100

150

200

250

FY0

1

FY0

2

FY0

3

FY0

4

FY0

5

FY0

6

FY0

7

FY0

8

FY0

9

FY1

0

FY1

1

FY1

2

FY1

3

FY1

4

FY1

5

FY1

6

FY1

7

FY1

8

FY1

9

FY2

0

FY2

1

FY2

2

FY2

3E*

FY2

4E*

Gap ($ bn) IT Exports ($ bn)

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

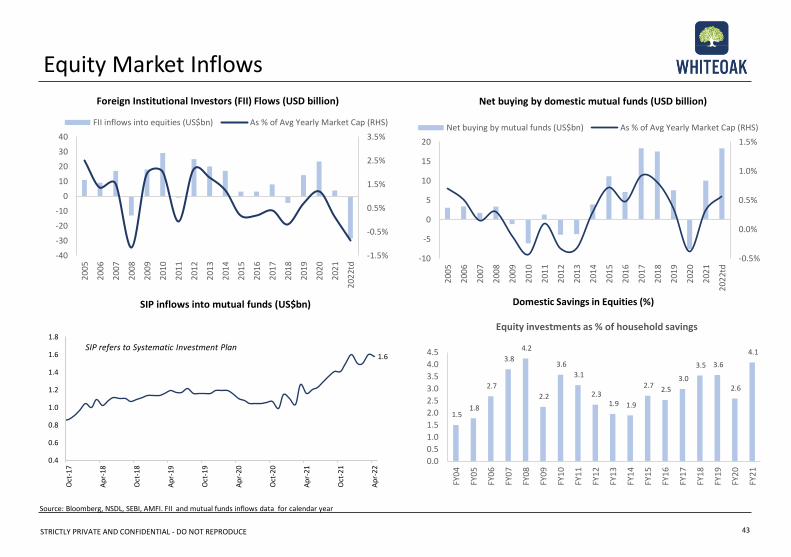

Source: Bloomberg, NSDL, SEBI, AMFI. FII and mutual funds inflows data for calendar year

Equity Market Inflows

Foreign Institutional Investors (FII) Flows (USD billion)

43

SIP inflows into mutual funds (US$bn) Domestic Savings in Equities (%)

-1.5%

-0.5%

0.5%

1.5%

2.5%

3.5%

-40

-30

-20

-10

0

10

20

30

40

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7

201

8

201

9

202

0

202

1

202

2td

FII inflows into equities (US$bn) As % of Avg Yearly Market Cap (RHS)

1.5 1.8

2.7

3.8

4.2

2.2

3.6

3.1

2.3 1.9 1.9

2.7 2.5

3.0

3.5 3.6

2.6

4.1

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

FY0

4

FY0

5

FY0

6

FY0

7

FY0

8

FY0

9

FY1

0

FY1

1

FY1

2

FY1

3

FY1

4

FY1

5

FY1

6

FY1

7

FY1

8

FY1

9

FY2

0

FY2

1

Equity investments as % of household savings

-0.5%

0.0%

0.5%

1.0%

1.5%

-10

-5

0

5

10

15

20

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7

201

8

201

9

202

0

202

1

202

2td

Net buying by mutual funds (US$bn) As % of Avg Yearly Market Cap (RHS)

Net buying by domestic mutual funds (USD billion)

1.6

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

Oct

-17

Ap

r-18

Oct

-18

Ap

r-19

Oct

-19

Ap

r-20

Oct

-20

Ap

r-21

Oct

-21

Ap

r-22

SIP refers to Systematic Investment Plan

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

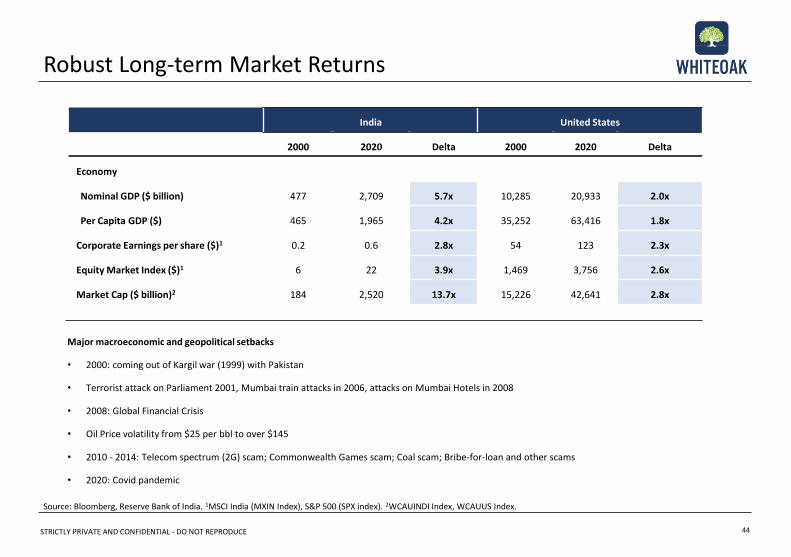

India United States

2000 2020 Delta 2000 2020 Delta

Economy

Nominal GDP ($ billion) 477 2,709 5.7x 10,285 20,933 2.0x

Per Capita GDP ($) 465 1,965 4.2x 35,252 63,416 1.8x

Corporate Earnings per share ($)1 0.2 0.6 2.8x 54 123 2.3x

Equity Market Index ($)1 6 22 3.9x 1,469 3,756 2.6x

Market Cap ($ billion)2 184 2,520 13.7x 15,226 42,641 2.8x

Major macroeconomic and geopolitical setbacks

• 2000: coming out of Kargil war (1999) with Pakistan

• Terrorist attack on Parliament 2001, Mumbai train attacks in 2006, attacks on Mumbai Hotels in 2008

• 2008: Global Financial Crisis

• Oil Price volatility from $25 per bbl to over $145

• 2010 - 2014: Telecom spectrum (2G) scam; Commonwealth Games scam; Coal scam; Bribe-for-loan and other scams

• 2020: Covid pandemic

44

Source: Bloomberg, Reserve Bank of India. 1MSCI India (MXIN Index), S&P 500 (SPX index). 2WCAUINDI Index, WCAUUS Index.

Robust Long-term Market Returns

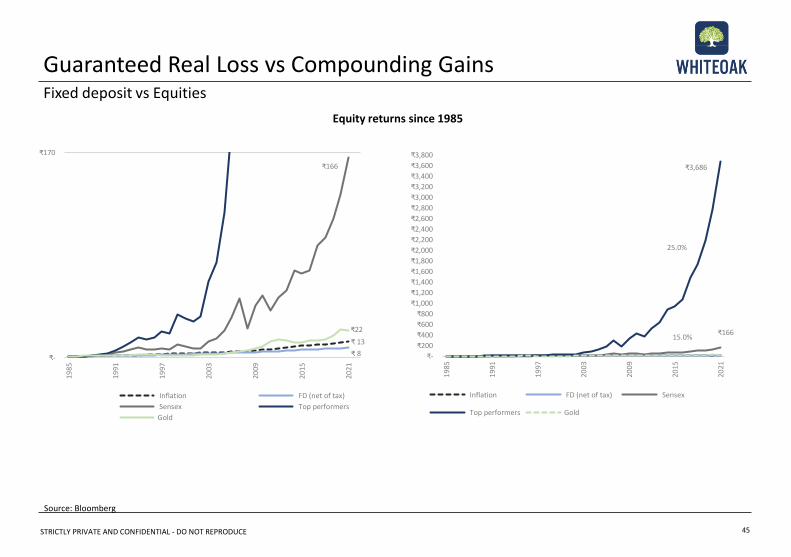

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

Equity returns since 1985

Guaranteed Real Loss vs Compounding GainsFixed deposit vs Equities

Source: Bloomberg

45

₹16615.0%

25.0%

₹3,686

₹-

₹200

₹400

₹600

₹800

₹1,000

₹1,200

₹1,400

₹1,600

₹1,800

₹2,000

₹2,200

₹2,400

₹2,600

₹2,800

₹3,000

₹3,200

₹3,400

₹3,600

₹3,800

1985

1991

1997

2003

2009

2015

2021

Inflation FD (net of tax) Sensex

Top performers Gold

₹ 13

₹ 8

₹166

₹22

₹-

₹170

1985

1991

1997

2003

2009

2015

2021

Inflation FD (net of tax)

Sensex Top performers

Gold

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

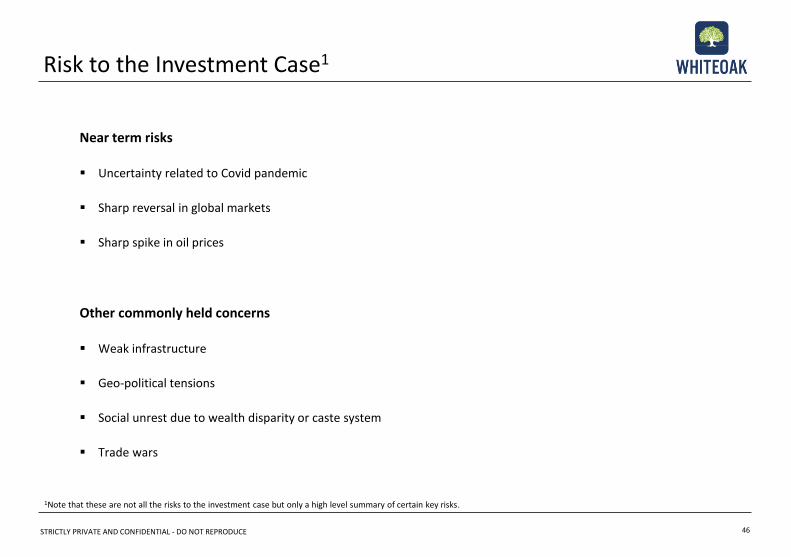

Near term risks

▪ Uncertainty related to Covid pandemic

▪ Sharp reversal in global markets

▪ Sharp spike in oil prices

Other commonly held concerns

▪ Weak infrastructure

▪ Geo-political tensions

▪ Social unrest due to wealth disparity or caste system

▪ Trade wars

46

1Note that these are not all the risks to the investment case but only a high level summary of certain key risks.

Risk to the Investment Case1

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

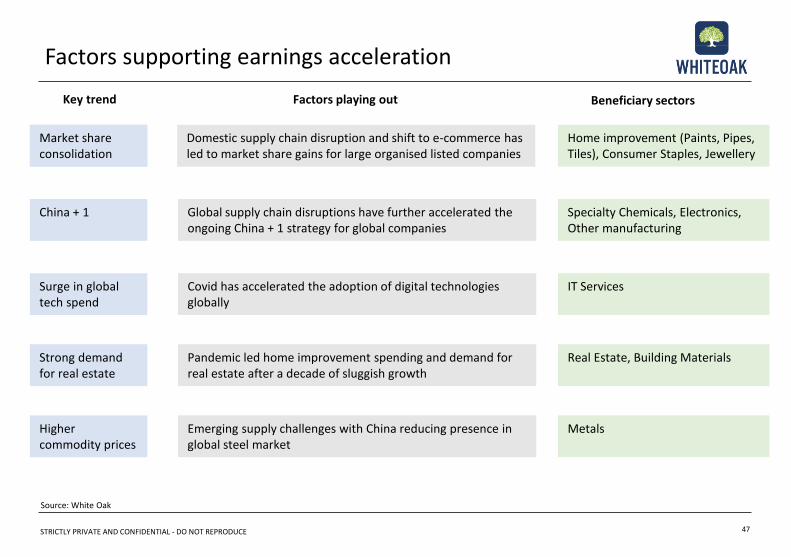

Factors supporting earnings acceleration

47

Source: White Oak

Key trend Factors playing out Beneficiary sectors

Domestic supply chain disruption and shift to e-commerce has led to market share gains for large organised listed companies

Market share consolidation

Home improvement (Paints, Pipes, Tiles), Consumer Staples, Jewellery

Global supply chain disruptions have further accelerated the ongoing China + 1 strategy for global companies

Specialty Chemicals, Electronics, Other manufacturing

Covid has accelerated the adoption of digital technologies globally

Surge in global tech spend

IT Services

Pandemic led home improvement spending and demand for real estate after a decade of sluggish growth

Strong demand for real estate

Real Estate, Building Materials

Emerging supply challenges with China reducing presence in global steel market

Higher commodity prices

Metals

Market share consolidation

China + 1

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

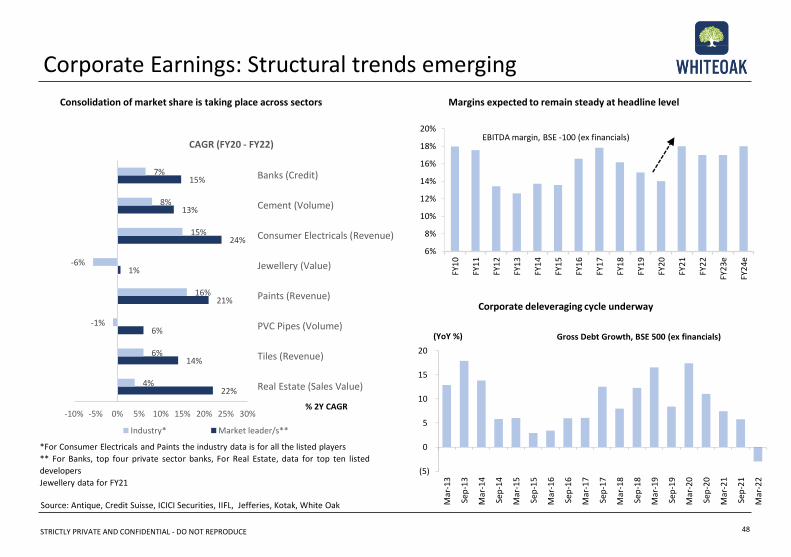

Corporate Earnings: Structural trends emerging

48

*For Consumer Electricals and Paints the industry data is for all the listed players

** For Banks, top four private sector banks, For Real Estate, data for top ten listed

developers

Jewellery data for FY21

Consolidation of market share is taking place across sectors Margins expected to remain steady at headline level

Corporate deleveraging cycle underway

Source: Antique, Credit Suisse, ICICI Securities, IIFL, Jefferies, Kotak, White Oak

6%

8%

10%

12%

14%

16%

18%

20%

FY1

0

FY1

1

FY1

2

FY1

3

FY1

4

FY1

5

FY1

6

FY1

7

FY1

8

FY1

9

FY2

0

FY2

1

FY2

2

FY2

3e

FY2

4e

EBITDA margin, BSE -100 (ex financials)

22%

14%

6%

21%

1%

24%

13%

15%

4%

6%

-1%

16%

-6%

15%

8%

7%

-10% -5% 0% 5% 10% 15% 20% 25% 30%

Real Estate (Sales Value)

Tiles (Revenue)

PVC Pipes (Volume)

Paints (Revenue)

Jewellery (Value)

Consumer Electricals (Revenue)

Cement (Volume)

Banks (Credit)

CAGR (FY20 - FY22)

Industry* Market leader/s**

% 2Y CAGR

(5)

0

5

10

15

20

Mar

-13

Sep

-13

Mar

-14

Sep

-14

Mar

-15

Sep

-15

Mar

-16

Sep

-16

Mar

-17

Sep

-17

Mar

-18

Sep

-18

Mar

-19

Sep

-19

Mar

-20

Sep

-20

Mar

-21

Sep

-21

Mar

-22

Gross Debt Growth, BSE 500 (ex financials)(YoY %)

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

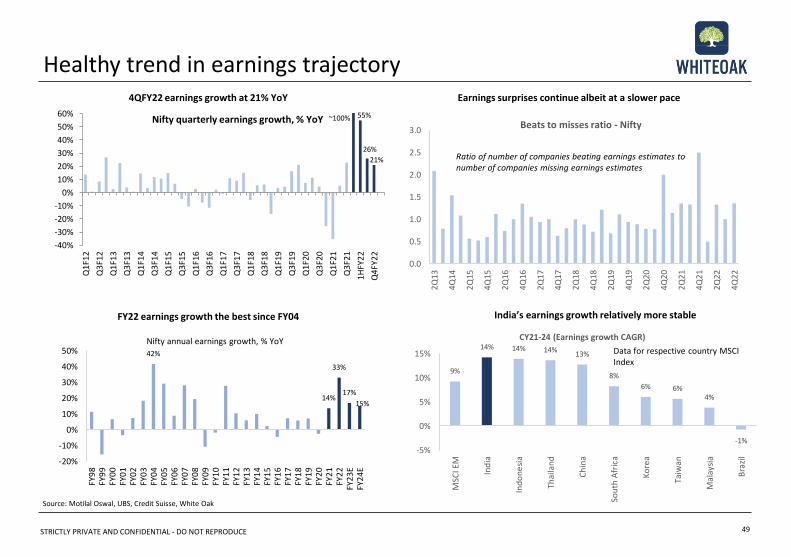

Healthy trend in earnings trajectory

49

Source: Motilal Oswal, UBS, Credit Suisse, White Oak

4QFY22 earnings growth at 21% YoY Earnings surprises continue albeit at a slower pace

FY22 earnings growth the best since FY04 India’s earnings growth relatively more stable

42%

14%

33%

17%

15%

-20%

-10%

0%

10%

20%

30%

40%

50%

FY9

8FY

99

FY0

0FY

01

FY0

2FY

03

FY0

4FY

05

FY0

6FY

07

FY0

8FY

09

FY1

0FY

11

FY1

2FY

13

FY1

4FY

15

FY1

6FY

17

FY1

8FY

19

FY2

0FY

21

FY2

2FY

23E

FY2

4E

Nifty annual earnings growth, % YoY

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2Q

13

4Q

14

2Q

15

4Q

15

2Q

16

4Q

16

2Q

17

4Q

17

2Q

18

4Q

18

2Q

19

4Q

19

2Q

20

4Q

20

2Q

21

4Q

21

2Q

22

4Q

22

Beats to misses ratio - Nifty

Ratio of number of companies beating earnings estimates to number of companies missing earnings estimates

55%

26%

21%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

Q1

F12

Q3

F12

Q1

F13

Q3

F13

Q1

F14

Q3

F14

Q1

F15

Q3

F15

Q1

F16

Q3

F16

Q1

F17

Q3

F17

Q1

F18

Q3

F18

Q1

F19

Q3

F19

Q1

F20

Q3

F20

Q1

F21

Q3

F21

1H

FY2

2

Q4

FY2

2

Nifty quarterly earnings growth, % YoY ~100% 1

9%

14% 14% 14%13%

8%

6% 6%4%

-1%-5%

0%

5%

10%

15%

MSC

I EM

Ind

ia

Ind

on

esi

a

Thai

lan

d

Ch

ina

Sou

th A

fric

a

Ko

rea

Taiw

an

Mal

aysi

a

Bra

zil

CY21-24 (Earnings growth CAGR)

Data for respective country MSCI Index

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

Source: White Oak Research

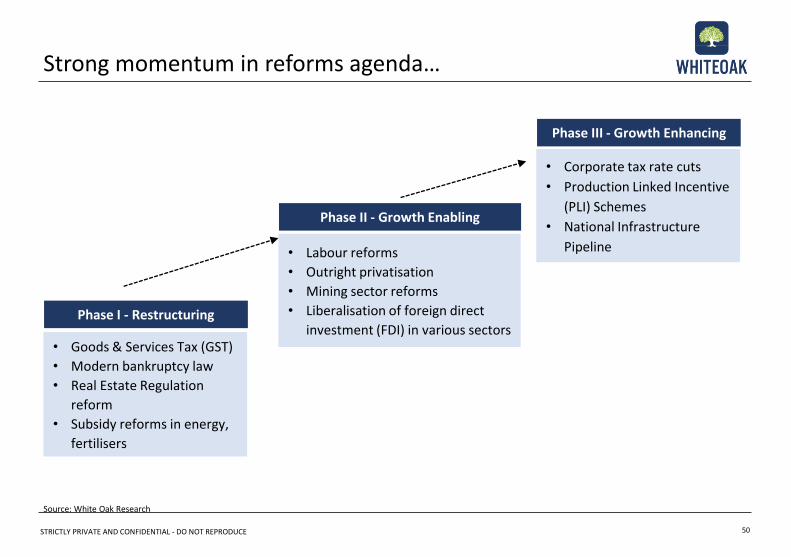

Strong momentum in reforms agenda…

50

• Goods & Services Tax (GST)

• Modern bankruptcy law

• Real Estate Regulation

reform

• Subsidy reforms in energy,

fertilisers

• Labour reforms

• Outright privatisation

• Mining sector reforms

• Liberalisation of foreign direct

investment (FDI) in various sectors

• Corporate tax rate cuts

• Production Linked Incentive

(PLI) Schemes

• National Infrastructure

Pipeline

Phase I - Restructuring

Phase II - Growth Enabling

Phase III - Growth Enhancing

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

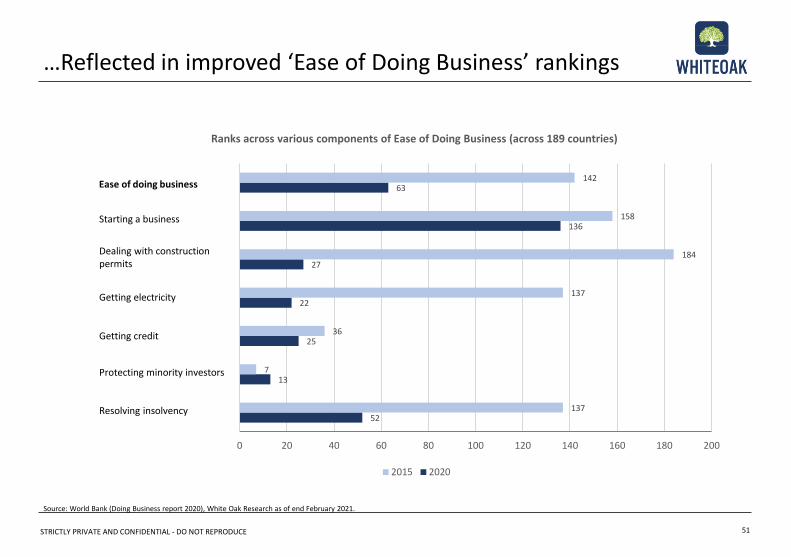

Source: World Bank (Doing Business report 2020), White Oak Research as of end February 2021.

…Reflected in improved ‘Ease of Doing Business’ rankings

51

52

13

25

22

27

136

63

137

7

36

137

184

158

142

0 20 40 60 80 100 120 140 160 180 200

Ranks across various components of Ease of Doing Business (across 189 countries)

2015 2020

Ease of doing business

Starting a business

Dealing with construction permits

Getting electricity

Getting credit

Protecting minority investors

Resolving insolvency

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

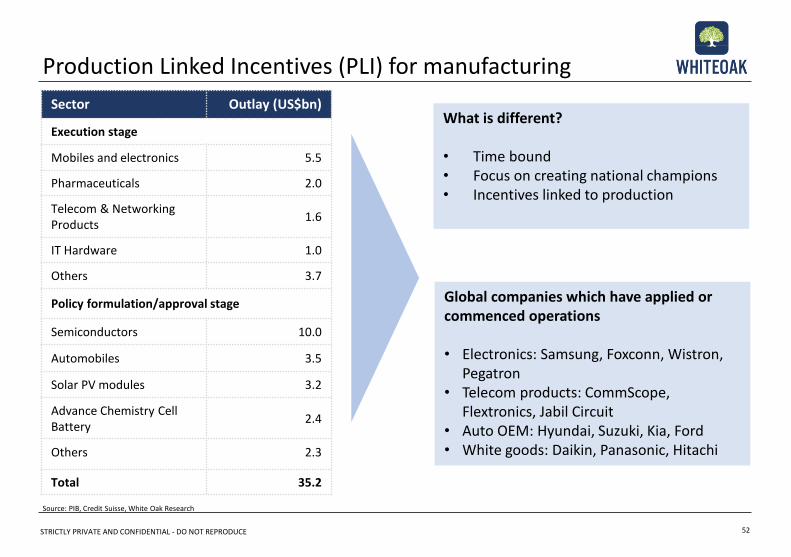

Source: PIB, Credit Suisse, White Oak Research

Production Linked Incentives (PLI) for manufacturing

52

Sector Outlay (US$bn)

Execution stage

Mobiles and electronics 5.5

Pharmaceuticals 2.0

Telecom & Networking Products

1.6

IT Hardware 1.0

Others 3.7

Policy formulation/approval stage

Semiconductors 10.0

Automobiles 3.5

Solar PV modules 3.2

Advance Chemistry Cell Battery

2.4

Others 2.3

Total 35.2

What is different?

• Time bound• Focus on creating national champions• Incentives linked to production

Global companies which have applied or commenced operations

• Electronics: Samsung, Foxconn, Wistron, Pegatron

• Telecom products: CommScope, Flextronics, Jabil Circuit

• Auto OEM: Hyundai, Suzuki, Kia, Ford• White goods: Daikin, Panasonic, Hitachi

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

Source: Credit Suisse, White Oak

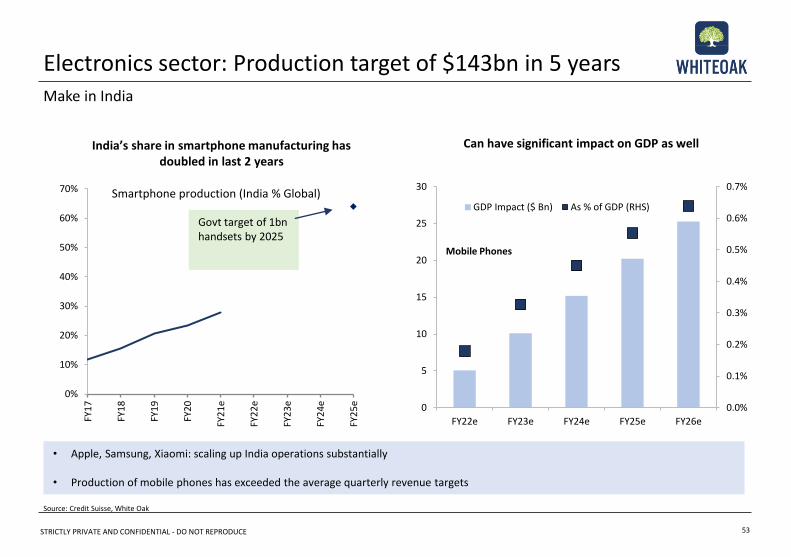

Electronics sector: Production target of $143bn in 5 years

53

India’s share in smartphone manufacturing has doubled in last 2 years

Can have significant impact on GDP as well

• Apple, Samsung, Xiaomi: scaling up India operations substantially

• Production of mobile phones has exceeded the average quarterly revenue targets

0%

10%

20%

30%

40%

50%

60%

70%

FY1

7

FY1

8

FY1

9

FY2

0

FY2

1e

FY2

2e

FY2

3e

FY2

4e

FY2

5e

Smartphone production (India % Global)

Govt target of 1bn handsets by 2025

Make in India

0.0%

0.1%

0.2%

0.3%

0.4%

0.5%

0.6%

0.7%

0

5

10

15

20

25

30

FY22e FY23e FY24e FY25e FY26e

GDP Impact ($ Bn) As % of GDP (RHS)

Mobile Phones

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

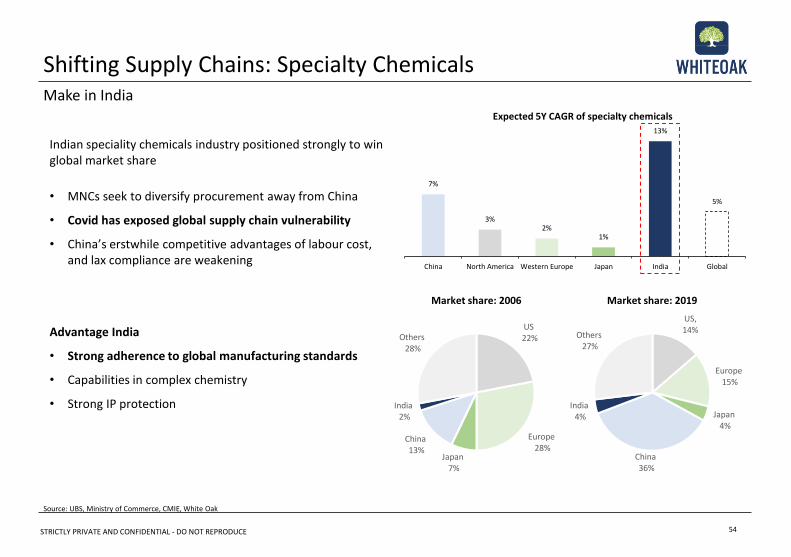

Indian speciality chemicals industry positioned strongly to win global market share

• MNCs seek to diversify procurement away from China

• Covid has exposed global supply chain vulnerability

• China’s erstwhile competitive advantages of labour cost, and lax compliance are weakening

Advantage India

• Strong adherence to global manufacturing standards

• Capabilities in complex chemistry

• Strong IP protection

Shifting Supply Chains: Specialty Chemicals

54

Source: UBS, Ministry of Commerce, CMIE, White Oak

Make in India

7%

3%2%

1%

13%

5%

China North America Western Europe Japan India Global

Expected 5Y CAGR of specialty chemicals

US22%

Europe28%

Japan7%

China13%

India2%

Others28%

Market share: 2006

US,14%

Europe15%

Japan4%

China36%

India4%

Others27%

Market share: 2019

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

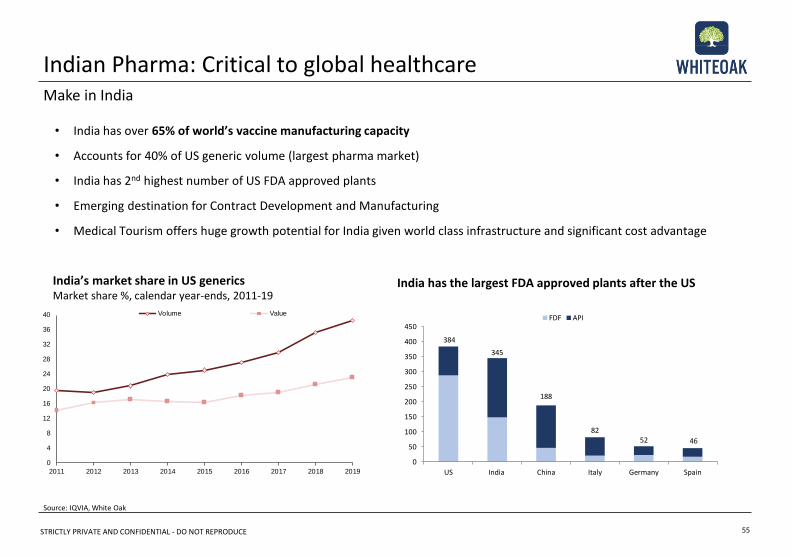

Indian Pharma: Critical to global healthcare

55

Make in India

• India has over 65% of world’s vaccine manufacturing capacity

• Accounts for 40% of US generic volume (largest pharma market)

• India has 2nd highest number of US FDA approved plants

• Emerging destination for Contract Development and Manufacturing

• Medical Tourism offers huge growth potential for India given world class infrastructure and significant cost advantage

India’s market share in US genericsMarket share %, calendar year-ends, 2011-19

Source: IQVIA, White Oak

India has the largest FDA approved plants after the US

384

345

188

8252 46

0

50

100

150

200

250

300

350

400

450

US India China Italy Germany Spain

FDF API

0

4

8

12

16

20

24

28

32

36

40

2011 2012 2013 2014 2015 2016 2017 2018 2019

Volume Value

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

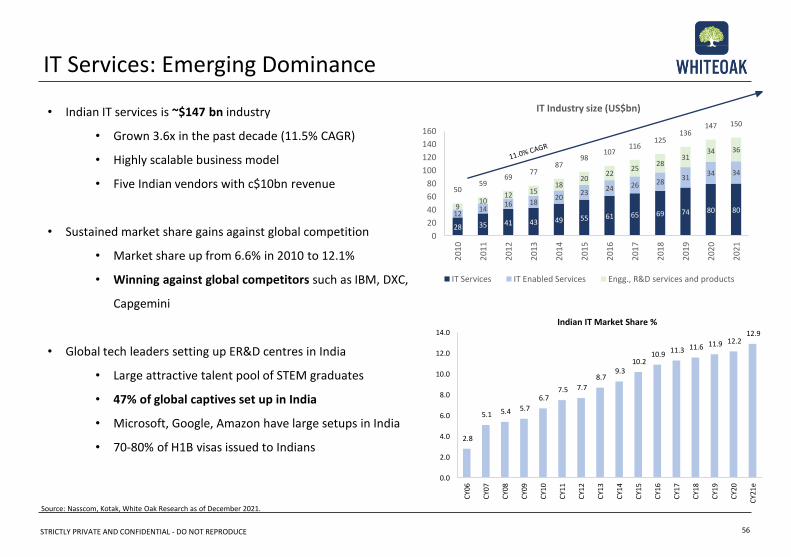

Source: Nasscom, Kotak, White Oak Research as of December 2021.

IT Services: Emerging Dominance

56

• Indian IT services is ~$147 bn industry

• Grown 3.6x in the past decade (11.5% CAGR)

• Highly scalable business model

• Five Indian vendors with c$10bn revenue

• Sustained market share gains against global competition

• Market share up from 6.6% in 2010 to 12.1%

• Winning against global competitors such as IBM, DXC,

Capgemini

• Global tech leaders setting up ER&D centres in India

• Large attractive talent pool of STEM graduates

• 47% of global captives set up in India

• Microsoft, Google, Amazon have large setups in India

• 70-80% of H1B visas issued to Indians2.8

5.1 5.4 5.7

6.7 7.5 7.7

8.7 9.3

10.2 10.9

11.3 11.6 11.9 12.2 12.9

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

CY0

6

CY0

7

CY0

8

CY0

9

CY1

0

CY1

1

CY1

2

CY1

3

CY1

4

CY1

5

CY1

6

CY1

7

CY1

8

CY1

9

CY2

0

CY2

1e

Indian IT Market Share %

28 35 41 43 49 55 61 65 69 74 80 801214

16 1820

2324 26 28

3134 34

910

12 1518

2022

2528

3134 36

5059

6977

8798

107116

125136

147 150

0

20

40

60

80

100

120

140

160

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7

201

8

201

9

202

0

202

1

IT Industry size (US$bn)

IT Services IT Enabled Services Engg., R&D services and products

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

Lessons from 2020

57

Lesson #1

• The usual perennial macroeconomic worries of the well-known unknowns variety are a colossal waste of time • They hardly influence the future returns from equity markets, if any at all

Lesson #2

• Nobody has a crystal ball to forecast cataclysmic risk events of the unknown unknown variety, ex: the pandemic• Market implications remain unpredictable even if one were bestowed with perfect prior knowledge

Lesson #3

• Investment decisions bereft of bottom up analysis, and instead driven by macro considerations, are fraught with high risk of substantial absolute and relative losses

20-20 from 2020: The futility of predicting investment returns based on macroeconomic worries and events

Macro- Shacro

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE 58

Relevance of Macro

• View macros as source of random risks, not as opportunity to add alpha

• Consciously avoid top-down misadventures – market timing, sector rotation

• Stay fully invested, with a bottom up approach to investing in great businesses at attractive valuations

• Maintain a balanced portfolio construction approach at all times

White Oak’s Perspective

The value of the market at any time is present value of aggregate perpetual future cash flows

The market is fairy valued at all times

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

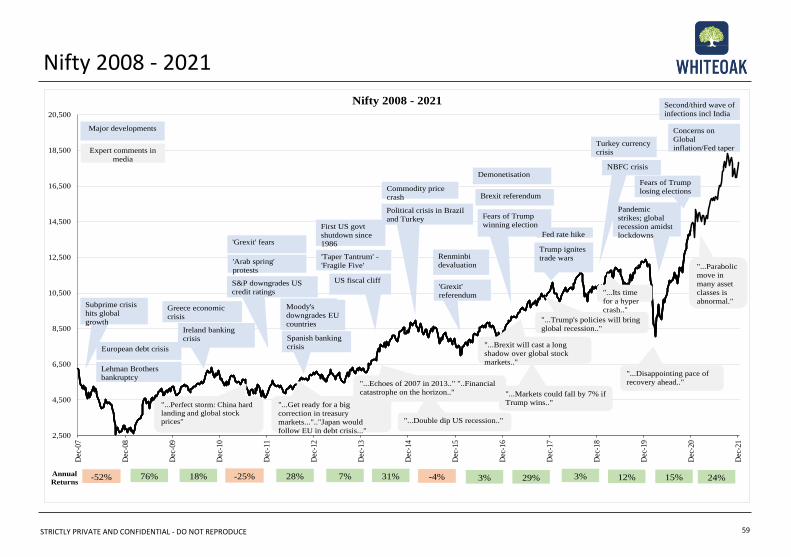

Nifty 2008 - 2021

59

2,500

4,500

6,500

8,500

10,500

12,500

14,500

16,500

18,500

20,500

Dec

-07

Dec

-08

Dec

-09

Dec

-10

Dec

-11

Dec

-12

Dec

-13

Dec

-14

Dec

-15

Dec

-16

Dec

-17

Dec

-18

Dec

-19

Dec

-20

Dec

-21

Nifty 2008 - 2021

Annual

Returns76% 18% -25%-52% 28% 7% 31% -4% 3% 29% 3% 12% 15%

"...Perfect storm: China hard

landing and global stock

prices"

"...Brexit will cast a long

shadow over global stock

markets.."

"...Echoes of 2007 in 2013.." "..Financial

catastrophe on the horizon.."

"...Get ready for a big

correction in treasury

markets...".."Japan would

follow EU in debt crisis..."

"...Double dip US recession.."

"...Markets could fall by 7% if

Trump wins.."

"...Trump's policies will bring

global recession.."

"...Its time

for a hyper

crash.."

"...Disappointing pace of

recovery ahead.."

Ireland banking

crisis

S&P downgrades US

credit ratings

Moody's

downgrades EU

countries

First US govt

shutdown since

1986

'Taper Tantrum' -

'Fragile Five'

US fiscal cliff

Political crisis in Brazil

and Turkey Fears of Trump

winning election

Turkey currency

crisis

Major developments

Expert comments in

media

Moody's

downgrades EU

countries

Commodity price

crash

Demonetisation

Brexit referendum

Fed rate hike

Trump ignites

trade wars

'Grexit' fears

'Arab spring'

protests

Moody's

downgrades EU

countries

Spanish banking

crisis

Renminbi

devaluation

'Grexit'

referendum

Greece economic

crisis

European debt crisis

Subprime crisis

hits global

growth

Lehman Brothers

bankruptcy

Pandemic

strikes; global

recession amidst

lockdowns

NBFC crisis

Second/third wave of

infections incl India

Concerns on

Global

inflation/Fed taper

Fears of Trump

losing elections

"...Parabolic

move in

many asset

classes is

abnormal."

24%

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

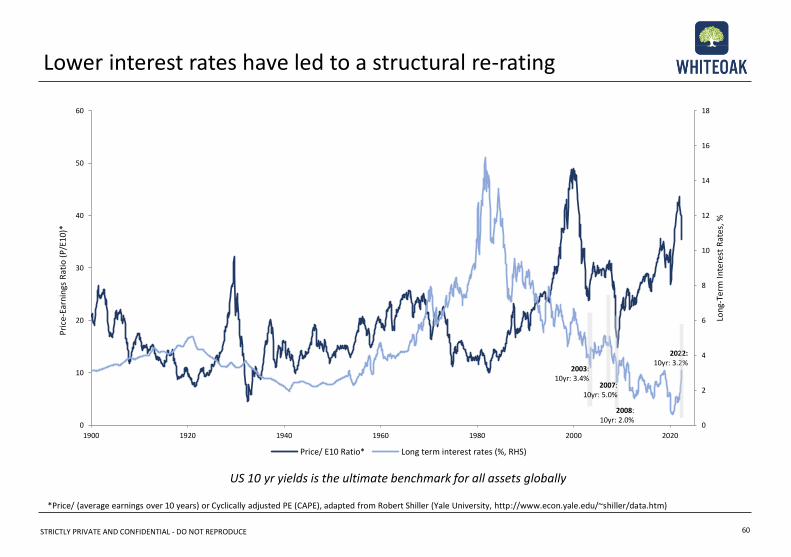

Lower interest rates have led to a structural re-rating

60

*Price/ (average earnings over 10 years) or Cyclically adjusted PE (CAPE), adapted from Robert Shiller (Yale University, http://www.econ.yale.edu/~shiller/data.htm)

US 10 yr yields is the ultimate benchmark for all assets globally

0

2

4

6

8

10

12

14

16

18

0

10

20

30

40

50

60

1900 1920 1940 1960 1980 2000 2020

Lon

g-Te

rm I

nte

rest

Rat

es, %

Pri

ce-E

arn

ings

Rat

io (

P/E

10)*

Price/ E10 Ratio* Long term interest rates (%, RHS)

2007:10yr: 5.0%

2008:10yr: 2.0%

2022:10yr: 3.2%

2003:10yr: 3.4%

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

Appendix

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

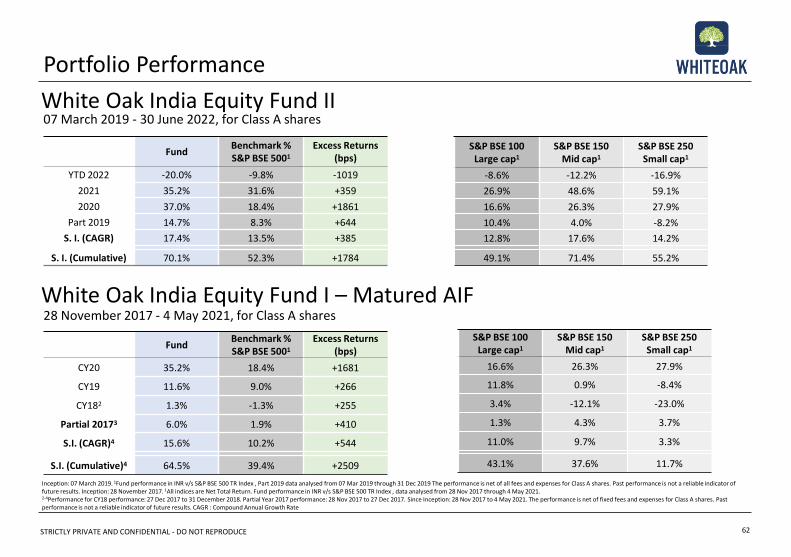

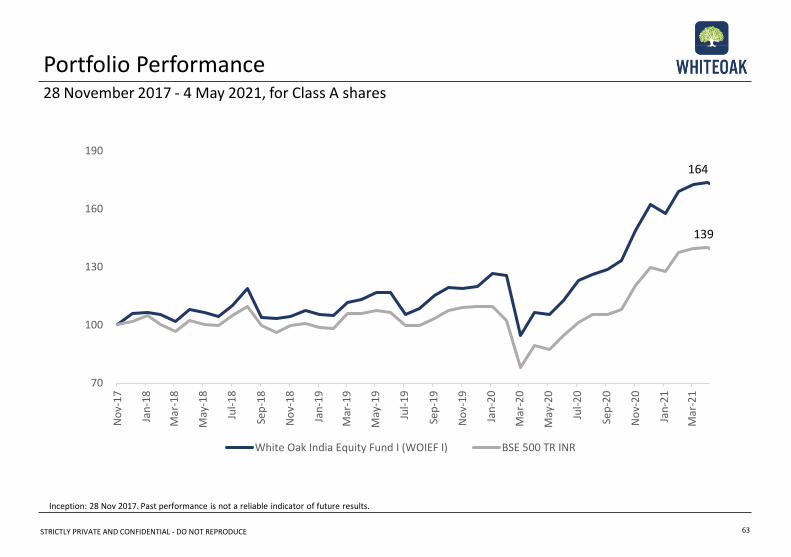

Portfolio Performance

07 March 2019 - 30 June 2022, for Class A shares

62

` FundBenchmark %S&P BSE 5001

Excess Returns (bps)

YTD 2022 -20.0% -9.8% -1019

2021 35.2% 31.6% +359

2020 37.0% 18.4% +1861

Part 2019 14.7% 8.3% +644

S. I. (CAGR) 17.4% 13.5% +385

S. I. (Cumulative) 70.1% 52.3% +1784

S&P BSE 100 Large cap1

S&P BSE 150 Mid cap1

S&P BSE 250Small cap1

-8.6% -12.2% -16.9%

26.9% 48.6% 59.1%

16.6% 26.3% 27.9%

10.4% 4.0% -8.2%

12.8% 17.6% 14.2%

49.1% 71.4% 55.2%

Inception: 07 March 2019. 1Fund performance in INR v/s S&P BSE 500 TR Index , Part 2019 data analysed from 07 Mar 2019 through 31 Dec 2019 The performance is net of all fees and expenses for Class A shares. Past performance is not a reliable indicator of future results. Inception: 28 November 2017. 1All indices are Net Total Return. Fund performance in INR v/s S&P BSE 500 TR Index , data analysed from 28 Nov 2017 through 4 May 2021. 2-4Performance for CY18 performance: 27 Dec 2017 to 31 December 2018. Partial Year 2017 performance: 28 Nov 2017 to 27 Dec 2017. Since Inception: 28 Nov 2017 to 4 May 2021. The performance is net of fixed fees and expenses for Class A shares. Past performance is not a reliable indicator of future results. CAGR : Compound Annual Growth Rate

` FundBenchmark %S&P BSE 5001

Excess Returns (bps)

CY20 35.2% 18.4% +1681

CY19 11.6% 9.0% +266

CY182 1.3% -1.3% +255

Partial 20173 6.0% 1.9% +410

S.I. (CAGR)4 15.6% 10.2% +544

S.I. (Cumulative)4 64.5% 39.4% +2509

S&P BSE 100 Large cap1

S&P BSE 150 Mid cap1

S&P BSE 250Small cap1

16.6% 26.3% 27.9%

11.8% 0.9% -8.4%

3.4% -12.1% -23.0%

1.3% 4.3% 3.7%

11.0% 9.7% 3.3%

43.1% 37.6% 11.7%

White Oak India Equity Fund II

28 November 2017 - 4 May 2021, for Class A sharesWhite Oak India Equity Fund I – Matured AIF

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

Portfolio Performance

63

28 November 2017 - 4 May 2021, for Class A shares

Inception: 28 Nov 2017. Past performance is not a reliable indicator of future results.

70

100

130

160

190

No

v-1

7

Jan

-18

Mar

-18

May

-18

Jul-

18

Sep

-18

No

v-1

8

Jan

-19

Mar

-19

May

-19

Jul-

19

Sep

-19

No

v-1

9

Jan

-20

Mar

-20

May

-20

Jul-

20

Sep

-20

No

v-2

0

Jan

-21

Mar

-21

White Oak India Equity Fund I (WOIEF I) BSE 500 TR INR

164

139

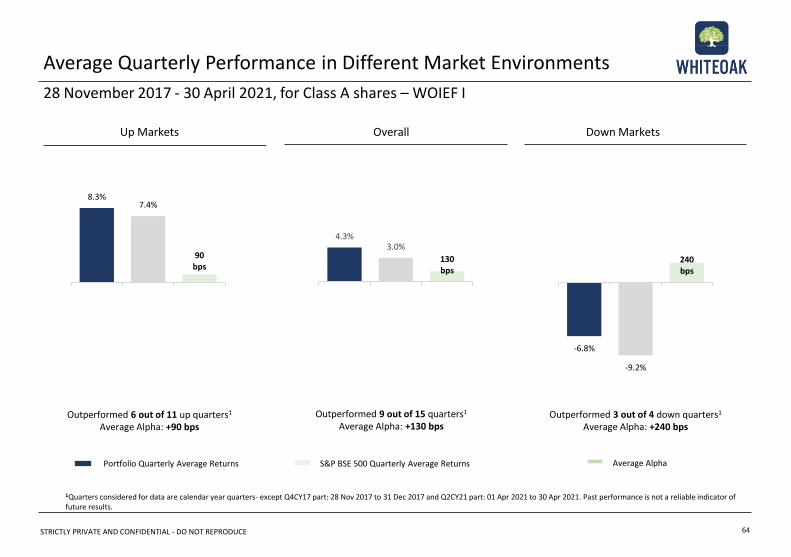

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

-6.8%

-9.2%

240 bps

8.3%7.4%

90 bps

64

Average Quarterly Performance in Different Market Environments

OverallUp Markets Down Markets

Outperformed 9 out of 15 quarters1

Average Alpha: +130 bpsOutperformed 6 out of 11 up quarters1

Average Alpha: +90 bps

Portfolio Quarterly Average Returns S&P BSE 500 Quarterly Average Returns Average Alpha

Outperformed 3 out of 4 down quarters1

Average Alpha: +240 bps

1Quarters considered for data are calendar year quarters- except Q4CY17 part: 28 Nov 2017 to 31 Dec 2017 and Q2CY21 part: 01 Apr 2021 to 30 Apr 2021. Past performance is not a reliable indicator of future results.

28 November 2017 - 30 April 2021, for Class A shares – WOIEF I

4.3%3.0%

130 bps

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

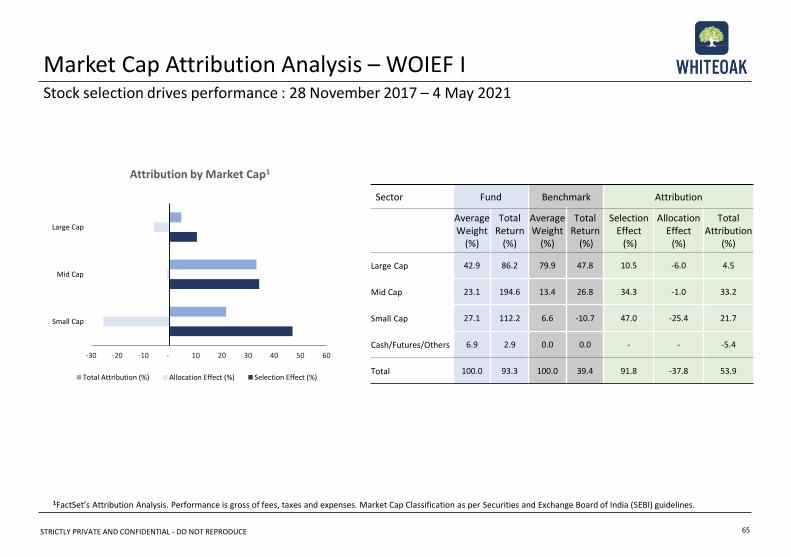

1FactSet’s Attribution Analysis. Performance is gross of fees, taxes and expenses. Market Cap Classification as per Securities and Exchange Board of India (SEBI) guidelines.

Sector Fund Benchmark Attribution

Average Weight

(%)

Total Return

(%)

Average Weight

(%)

Total Return

(%)

Selection Effect

(%)

Allocation Effect

(%)

Total Attribution

(%)

Large Cap 42.9 86.2 79.9 47.8 10.5 -6.0 4.5

Mid Cap 23.1 194.6 13.4 26.8 34.3 -1.0 33.2

Small Cap 27.1 112.2 6.6 -10.7 47.0 -25.4 21.7

Cash/Futures/Others 6.9 2.9 0.0 0.0 - - -5.4

Total 100.0 93.3 100.0 39.4 91.8 -37.8 53.9

Attribution by Market Cap1

Market Cap Attribution Analysis – WOIEF IStock selection drives performance : 28 November 2017 – 4 May 2021

65

-30 -20 -10 - 10 20 30 40 50 60

Small Cap

Mid Cap

Large Cap

Total Attribution (%) Allocation Effect (%) Selection Effect (%)

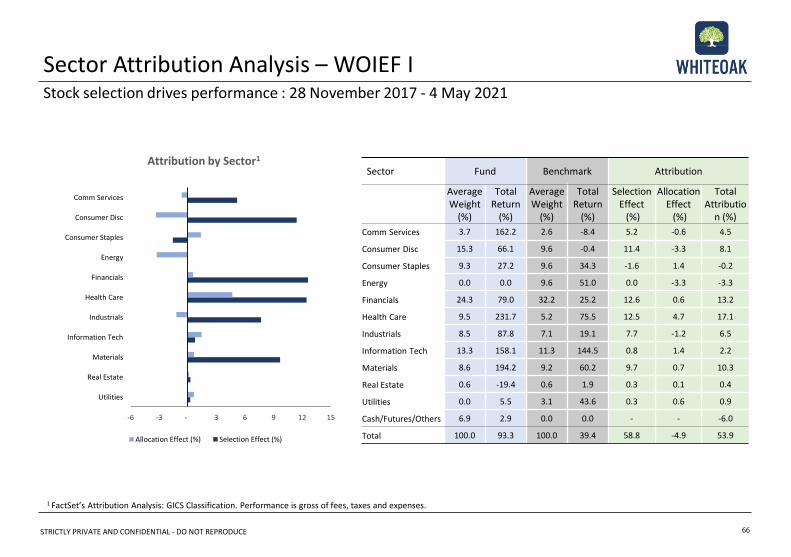

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

Sector Fund Benchmark Attribution

Average Weight

(%)

Total Return

(%)

Average Weight

(%)

Total Return

(%)

Selection Effect

(%)

Allocation Effect

(%)

Total Attributio

n (%)

Comm Services 3.7 162.2 2.6 -8.4 5.2 -0.6 4.5

Consumer Disc 15.3 66.1 9.6 -0.4 11.4 -3.3 8.1

Consumer Staples 9.3 27.2 9.6 34.3 -1.6 1.4 -0.2

Energy 0.0 0.0 9.6 51.0 0.0 -3.3 -3.3

Financials 24.3 79.0 32.2 25.2 12.6 0.6 13.2

Health Care 9.5 231.7 5.2 75.5 12.5 4.7 17.1

Industrials 8.5 87.8 7.1 19.1 7.7 -1.2 6.5

Information Tech 13.3 158.1 11.3 144.5 0.8 1.4 2.2

Materials 8.6 194.2 9.2 60.2 9.7 0.7 10.3

Real Estate 0.6 -19.4 0.6 1.9 0.3 0.1 0.4

Utilities 0.0 5.5 3.1 43.6 0.3 0.6 0.9

Cash/Futures/Others 6.9 2.9 0.0 0.0 - - -6.0

Total 100.0 93.3 100.0 39.4 58.8 -4.9 53.9

Sector Attribution Analysis – WOIEF IStock selection drives performance : 28 November 2017 - 4 May 2021

66

Attribution by Sector1

1 FactSet’s Attribution Analysis: GICS Classification. Performance is gross of fees, taxes and expenses.

-6 -3 - 3 6 9 12 15

Utilities

Real Estate

Materials

Information Tech

Industrials

Health Care

Financials

Energy

Consumer Staples

Consumer Disc

Comm Services

Allocation Effect (%) Selection Effect (%)

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

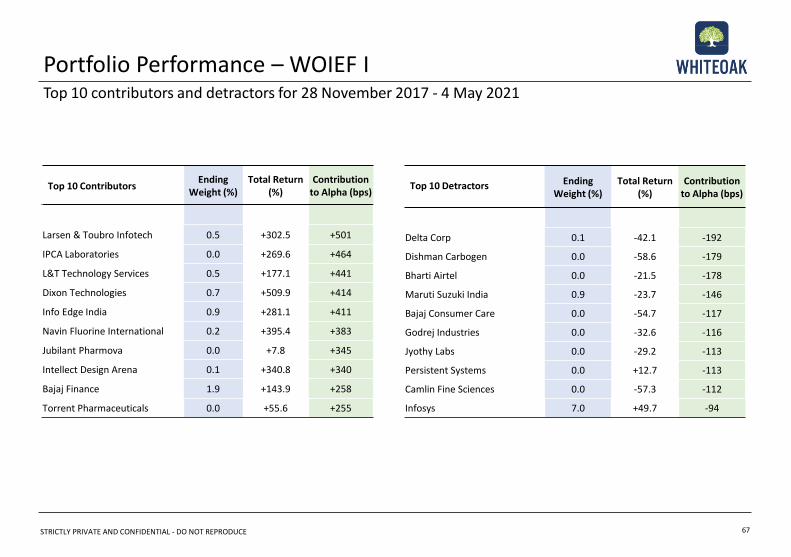

Top 10 ContributorsEnding

Weight (%) Total Return

(%)Contribution

to Alpha (bps)

Larsen & Toubro Infotech 0.5 +302.5 +501

IPCA Laboratories 0.0 +269.6 +464

L&T Technology Services 0.5 +177.1 +441

Dixon Technologies 0.7 +509.9 +414

Info Edge India 0.9 +281.1 +411

Navin Fluorine International 0.2 +395.4 +383

Jubilant Pharmova 0.0 +7.8 +345

Intellect Design Arena 0.1 +340.8 +340

Bajaj Finance 1.9 +143.9 +258

Torrent Pharmaceuticals 0.0 +55.6 +255

Top 10 Detractors EndingWeight (%)

Total Return (%)

Contribution to Alpha (bps)

Delta Corp 0.1 -42.1 -192

Dishman Carbogen 0.0 -58.6 -179

Bharti Airtel 0.0 -21.5 -178

Maruti Suzuki India 0.9 -23.7 -146

Bajaj Consumer Care 0.0 -54.7 -117

Godrej Industries 0.0 -32.6 -116

Jyothy Labs 0.0 -29.2 -113

Persistent Systems 0.0 +12.7 -113

Camlin Fine Sciences 0.0 -57.3 -112

Infosys 7.0 +49.7 -94

Portfolio Performance – WOIEF ITop 10 contributors and detractors for 28 November 2017 - 4 May 2021

67

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

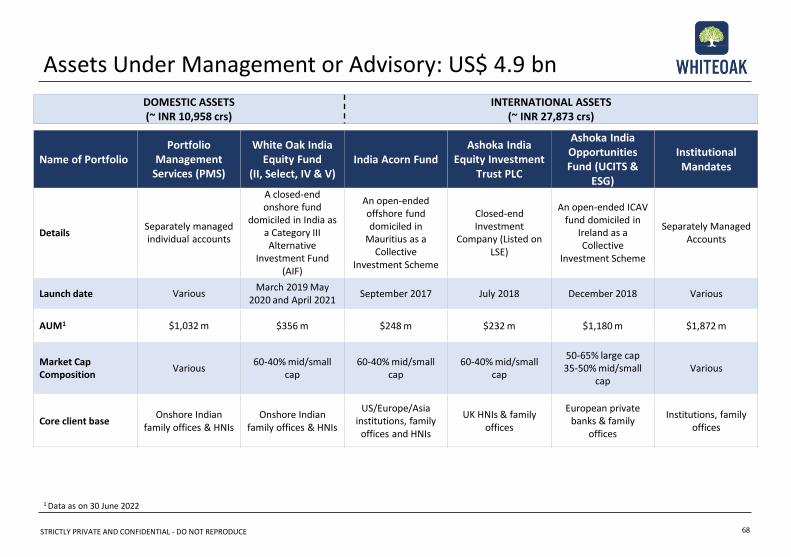

Assets Under Management or Advisory: US$ 4.9 bn

68

1 Data as on 30 June 2022

Name of PortfolioPortfolio

Management Services (PMS)

White Oak India Equity Fund

(II, Select, IV & V)India Acorn Fund

Ashoka India Equity Investment

Trust PLC

Ashoka India Opportunities Fund (UCITS &

ESG)

Institutional Mandates

DetailsSeparately managed individual accounts

A closed-end onshore fund

domiciled in India as a Category III Alternative

Investment Fund (AIF)

An open-ended offshore fund domiciled in

Mauritius as a Collective

Investment Scheme

Closed-end Investment

Company (Listed on LSE)

An open-ended ICAV fund domiciled in

Ireland as a Collective

Investment Scheme

Separately Managed Accounts

Launch date VariousMarch 2019 May

2020 and April 2021September 2017 July 2018 December 2018 Various

AUM1 $1,032 m $356 m $248 m $232 m $1,180 m $1,872 m

Market Cap Composition

Various60-40% mid/small

cap60-40% mid/small

cap60-40% mid/small

cap

50-65% large cap35-50% mid/small

capVarious

Core client baseOnshore Indian

family offices & HNIsOnshore Indian

family offices & HNIs

US/Europe/Asia institutions, family

offices and HNIs

UK HNIs & family offices

European private banks & family

offices

Institutions, family offices

DOMESTIC ASSETS(~ INR 10,958 crs)

INTERNATIONAL ASSETS(~ INR 27,873 crs)

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

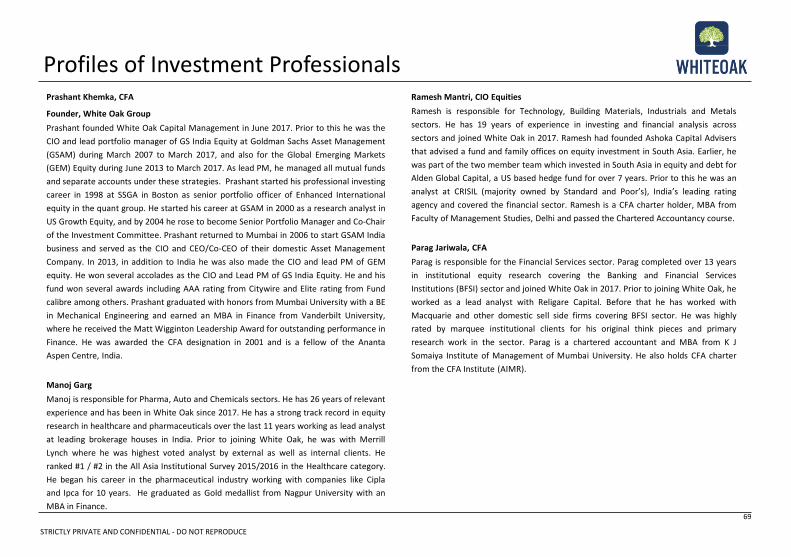

Prashant Khemka, CFA

Founder, White Oak Group

Prashant founded White Oak Capital Management in June 2017. Prior to this he was the

CIO and lead portfolio manager of GS India Equity at Goldman Sachs Asset Management

(GSAM) during March 2007 to March 2017, and also for the Global Emerging Markets

(GEM) Equity during June 2013 to March 2017. As lead PM, he managed all mutual funds

and separate accounts under these strategies. Prashant started his professional investing

career in 1998 at SSGA in Boston as senior portfolio officer of Enhanced International

equity in the quant group. He started his career at GSAM in 2000 as a research analyst in

US Growth Equity, and by 2004 he rose to become Senior Portfolio Manager and Co-Chair

of the Investment Committee. Prashant returned to Mumbai in 2006 to start GSAM India

business and served as the CIO and CEO/Co-CEO of their domestic Asset Management

Company. In 2013, in addition to India he was also made the CIO and lead PM of GEM

equity. He won several accolades as the CIO and Lead PM of GS India Equity. He and his

fund won several awards including AAA rating from Citywire and Elite rating from Fund

calibre among others. Prashant graduated with honors from Mumbai University with a BE

in Mechanical Engineering and earned an MBA in Finance from Vanderbilt University,

where he received the Matt Wigginton Leadership Award for outstanding performance in

Finance. He was awarded the CFA designation in 2001 and is a fellow of the Ananta

Aspen Centre, India.

Manoj Garg

Manoj is responsible for Pharma, Auto and Chemicals sectors. He has 26 years of relevant

experience and has been in White Oak since 2017. He has a strong track record in equity

research in healthcare and pharmaceuticals over the last 11 years working as lead analyst

at leading brokerage houses in India. Prior to joining White Oak, he was with Merrill

Lynch where he was highest voted analyst by external as well as internal clients. He

ranked #1 / #2 in the All Asia Institutional Survey 2015/2016 in the Healthcare category.

He began his career in the pharmaceutical industry working with companies like Cipla

and Ipca for 10 years. He graduated as Gold medallist from Nagpur University with an

MBA in Finance.

Ramesh Mantri, CIO Equities

Ramesh is responsible for Technology, Building Materials, Industrials and Metals

sectors. He has 19 years of experience in investing and financial analysis across

sectors and joined White Oak in 2017. Ramesh had founded Ashoka Capital Advisers

that advised a fund and family offices on equity investment in South Asia. Earlier, he

was part of the two member team which invested in South Asia in equity and debt for

Alden Global Capital, a US based hedge fund for over 7 years. Prior to this he was an

analyst at CRISIL (majority owned by Standard and Poor’s), India’s leading rating

agency and covered the financial sector. Ramesh is a CFA charter holder, MBA from

Faculty of Management Studies, Delhi and passed the Chartered Accountancy course.

Parag Jariwala, CFA

Parag is responsible for the Financial Services sector. Parag completed over 13 years

in institutional equity research covering the Banking and Financial Services

Institutions (BFSI) sector and joined White Oak in 2017. Prior to joining White Oak, he

worked as a lead analyst with Religare Capital. Before that he has worked with

Macquarie and other domestic sell side firms covering BFSI sector. He was highly

rated by marquee institutional clients for his original think pieces and primary

research work in the sector. Parag is a chartered accountant and MBA from K J

Somaiya Institute of Management of Mumbai University. He also holds CFA charter

from the CFA Institute (AIMR).

Profiles of Investment Professionals

69

STRICTLY PRIVATE AND CONFIDENTIAL - DO NOT REPRODUCE

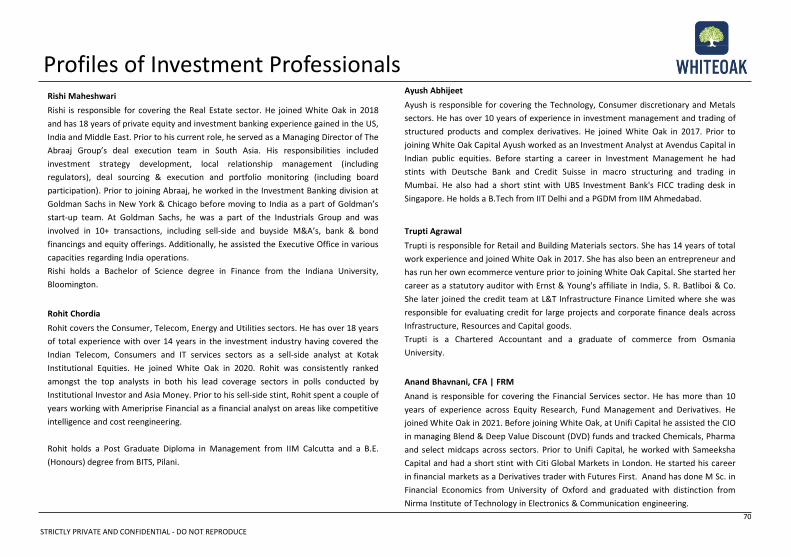

Rishi Maheshwari

Rishi is responsible for covering the Real Estate sector. He joined White Oak in 2018

and has 18 years of private equity and investment banking experience gained in the US,

India and Middle East. Prior to his current role, he served as a Managing Director of The

Abraaj Group’s deal execution team in South Asia. His responsibilities included

investment strategy development, local relationship management (including

regulators), deal sourcing & execution and portfolio monitoring (including board

participation). Prior to joining Abraaj, he worked in the Investment Banking division at

Goldman Sachs in New York & Chicago before moving to India as a part of Goldman’s

start-up team. At Goldman Sachs, he was a part of the Industrials Group and was

involved in 10+ transactions, including sell-side and buyside M&A’s, bank & bond

financings and equity offerings. Additionally, he assisted the Executive Office in various

capacities regarding India operations.

Rishi holds a Bachelor of Science degree in Finance from the Indiana University,

Bloomington.

Rohit Chordia

Rohit covers the Consumer, Telecom, Energy and Utilities sectors. He has over 18 years

of total experience with over 14 years in the investment industry having covered the

Indian Telecom, Consumers and IT services sectors as a sell-side analyst at Kotak

Institutional Equities. He joined White Oak in 2020. Rohit was consistently ranked

amongst the top analysts in both his lead coverage sectors in polls conducted by

Institutional Investor and Asia Money. Prior to his sell-side stint, Rohit spent a couple of

years working with Ameriprise Financial as a financial analyst on areas like competitive

intelligence and cost reengineering.

Rohit holds a Post Graduate Diploma in Management from IIM Calcutta and a B.E.

(Honours) degree from BITS, Pilani.

Ayush Abhijeet

Ayush is responsible for covering the Technology, Consumer discretionary and Metals