Embed Size (px)

Citation preview

Global Issues in the

Airline Industry

By

Syam Dev Mangattu

EAC0613406

i

TABLE OF CONTENTS

Table of Contents i

List of Tables ii

List of Figures iii

1 Introduction 1

2 Research Objective 2

3 Research: The Low Cost Business Model 3

3.1 Characteristics of Low-Cost Carriers (LCCs) 3

3.2 Cost Advantages of Low-Cost Airlines over Traditional Operators 6

4 Analysis: JetBlue Airways (1999-2003) 8

4.1 JetBlue Airways Brief 8

4.2 JetBlue Strategic Approach 8

4.3 JetBlue Operational Highlights 9

4.4 JetBlue Airways: Issues at Hand 12

4.5 JetBlue Business - Opportunities, Threats and Risks 14

5 JetBlue Research Solutions 16

5.1 Can JetBlue continue its spectacular growth? 16

5.2 Were its competitive advantages sustainable? 16

6 Plan of Action 17

6.1 Recommendations 17

7 Conclusions 19

References 20

ii

LIST OF TABLES

Table 1: The basic characteristics of LCA and FSA business models 4, 5

iii

LIST OF FIGURES

Figure 1: Low-cost business model 3

Figure 2: Low-cost carrier activity circle 4

Figure 3: Cost savings of LCA compared to FSA 7

Figure 4: JetBlue’s activity system 9

Figure 5: JetBlue’s Revenue passengers, 2000-2003 9

Figure 6: JetBlue’s revenue passenger miles, 2000-2003 10

Figure 7: JetBlue’s available seat miles, 2000-2003 10

Figure 8: JetBlue’s passenger load factor, 2000-2003 11

Figure 9: JetBlue’s departures, 2000-2003 11

Figure 10: The cost gap with JetBlue, 2004 12

Figure 11: JetBlue’s average fuel cost per gallon, 2000-2004 13

1

CHAPTER 1

INTRODUCTION

A sound corporate business strategy can be stated by defining Michael Porter’s two basic

types of competitive advantage: cost leadership and differentiation. Cost leadership strategy

gave rise to a breed of airlines in the mid 1990’s, the low-cost carriers (LCCs). This report

analyses the characteristics of the low-cost carriers and the key drivers that influence

operations.

In the past decade, the airline industry dynamics have changed which has affected the growth

and sustainability of the market (Sarker et al. 2012). In contrast, the low-cost carriers sector

has experienced growth and significant developments in air transport industry. The low cost

phenomenon has revolutionised the aviation market; guiding the path for success, with cost

efficient and productive innovations.

The global economic crisis, fuel crisis and the increasing operating costs has forced the low-

cost airlines to constantly evolve and adapt their business model to the existing market

conditions. It gave rise to the development of a hybrid of full-service airline (FSA) and low-

cost airline (LCA) business models (Vidović et al. 2013). The pragmatic research objective of

this report is to analyse the business model of the JetBlue Airways and to strategically plan

for the future success and profitability of the airline.

2

CHAPTER 2

RESEARCH OBJECTIVES

1. Conduct an in-depth research about the main characteristics of typical low cost

carriers, highlighting the different cost advantages when compared with typical

equivalent network carriers.

2. Evaluate the current situation of JetBlue Airways, mentioning the impacts of internal

and external factors on the operation and management of the airline, and discuss the

associated opportunities, threats and risks to the business.

3. a) Can JetBlue continue its spectacular growth?

b) Were its competitive advantages sustainable?

4. Recommend a plan of actions for the next 5 years, mentioning the associated likely

risks and outcomes.

3

CHAPTER 3

RESEARCH: THE LOW COST BUSINESS MODEL

Traditionally, LCCs business model focussed on their low-cost principles concept (Aimia

2013). LCCs business strategy now explores new models with significant developments, such

as: forming alliances, codesharing and interline agreements, operating long-haul flights and

offering new products and services.

3.1 Characteristics of Low-Cost Carriers (LCCs)

The characteristics of the low-cost business model rely on two key elements: value

proposition and operating model (Hellqvist et al. 2012), as shown below in figure 1.

Figure 1. Low-cost business model (Kachaner et al. 2011)

4

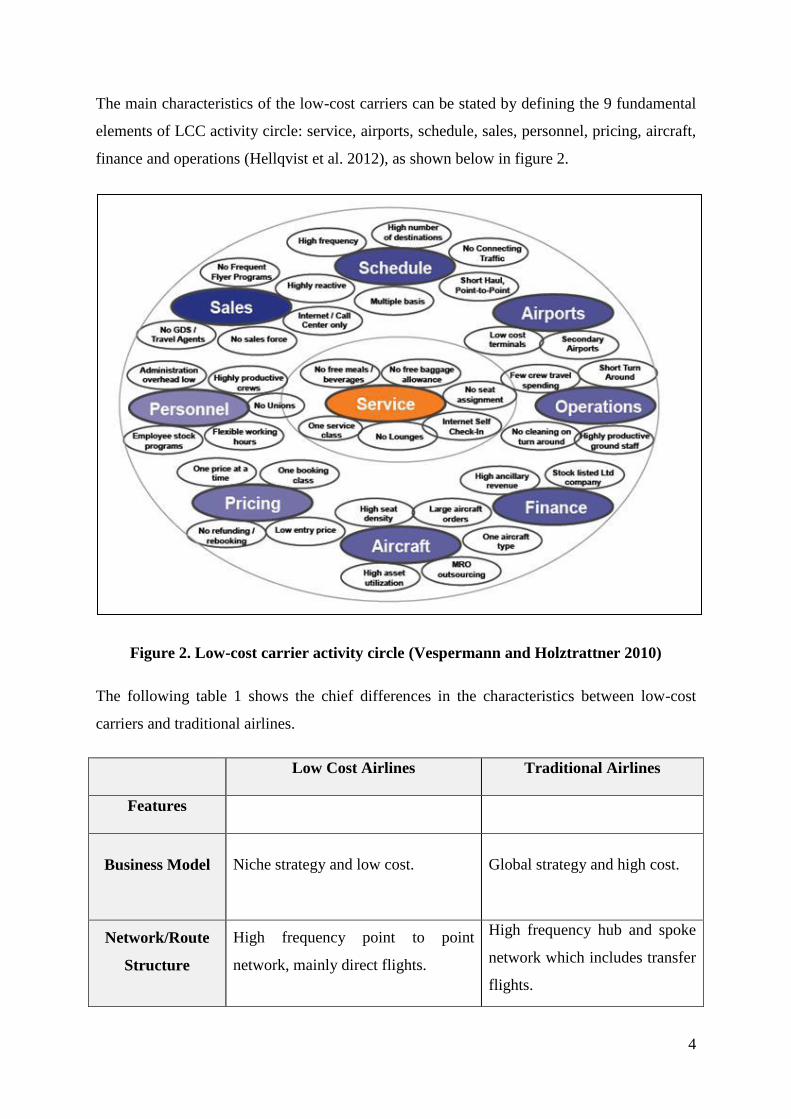

The main characteristics of the low-cost carriers can be stated by defining the 9 fundamental

elements of LCC activity circle: service, airports, schedule, sales, personnel, pricing, aircraft,

finance and operations (Hellqvist et al. 2012), as shown below in figure 2.

Figure 2. Low-cost carrier activity circle (Vespermann and Holztrattner 2010)

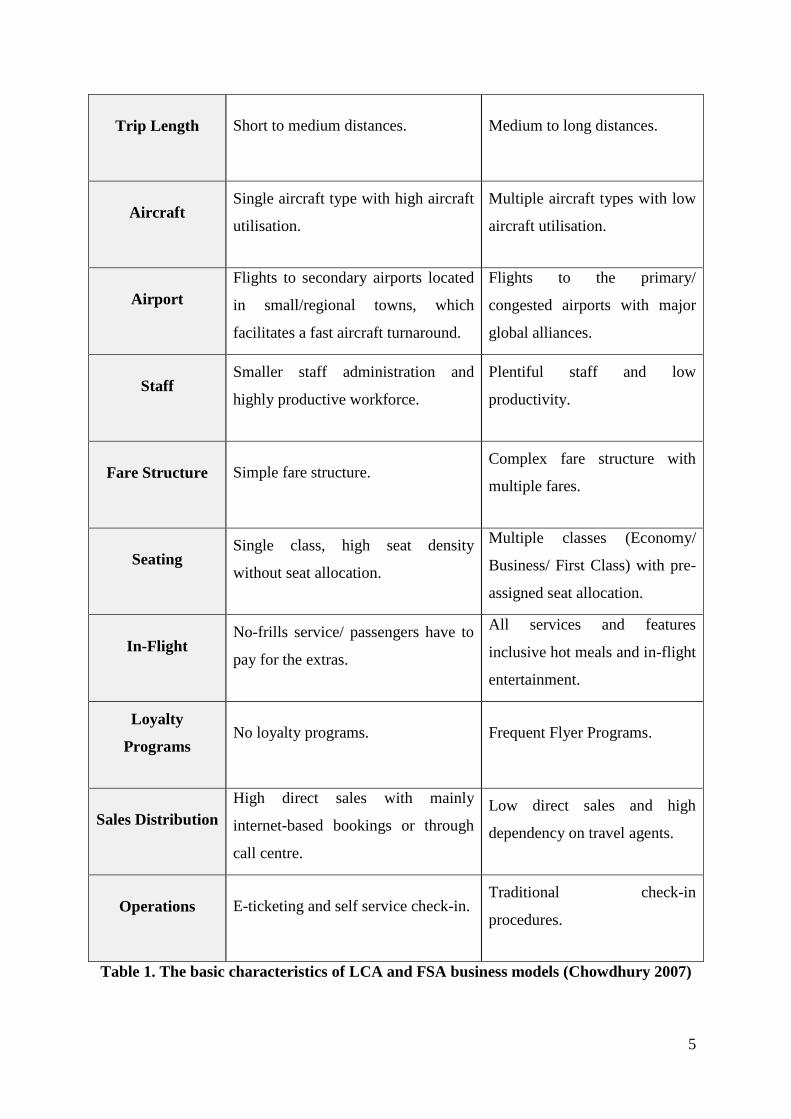

The following table 1 shows the chief differences in the characteristics between low-cost

carriers and traditional airlines.

Low Cost Airlines Traditional Airlines

Features

Business Model Niche strategy and low cost. Global strategy and high cost.

Network/Route

Structure

High frequency point to point

network, mainly direct flights.

High frequency hub and spoke

network which includes transfer

flights.

5

Trip Length Short to medium distances. Medium to long distances.

Aircraft Single aircraft type with high aircraft

utilisation.

Multiple aircraft types with low

aircraft utilisation.

Airport

Flights to secondary airports located

in small/regional towns, which

facilitates a fast aircraft turnaround.

Flights to the primary/

congested airports with major

global alliances.

Staff Smaller staff administration and

highly productive workforce.

Plentiful staff and low

productivity.

Fare Structure Simple fare structure. Complex fare structure with

multiple fares.

Seating Single class, high seat density

without seat allocation.

Multiple classes (Economy/

Business/ First Class) with pre-

assigned seat allocation.

In-Flight No-frills service/ passengers have to

pay for the extras.

All services and features

inclusive hot meals and in-flight

entertainment.

Loyalty

Programs No loyalty programs. Frequent Flyer Programs.

Sales Distribution

High direct sales with mainly

internet-based bookings or through

call centre.

Low direct sales and high

dependency on travel agents.

Operations E-ticketing and self service check-in. Traditional check-in

procedures.

Table 1. The basic characteristics of LCA and FSA business models (Chowdhury 2007)

6

However, with increasing competition from the traditional airlines, the LCCs business

strategy now practices a mix of these features depending on the market conditions.

3.2 Cost Advantages of Low-Cost Airlines over Traditional Operators

The major LCCs in order to achieve cost efficiencies in the areas of growing competition,

have adopted different strategic operations, fewer service offerings and distribution

efficiencies.

The low-cost airlines maximise complementary revenues from sales of refreshments

and for baggage. The airlines also charge for the in-flight facilities and services.

The low-cost airlines operate mainly to the secondary airports, which charge less fees

for landing and other services, thereby saving costs.

The other cost advantage of using secondary airports is that, it is less congested and

often have spare capacity which helps in avoiding delays and thereby helps in

acheiving a fast turnaround (ICAO 2003).

To acheive low-operating costs, the low-cost airlines operate at the highest seating

density with a maximum load factor (Doganis 2006).

The low-cost airlines have a lower average fleet age and a higher aircraft utilisation

rate than the traditional airlines, thereby saving maintenance costs and reducing the

operational costs even further.

The low-cost airlines gain cost advantage over traditional operators in sales

ditribution. Significant cost savings is made through electronic bookings and through

direct sales via internet and call centres (ICAO 2003).

The low-cost airlines workforce requirement is lower than the traditional operators,

thereby reducing the expenses.

The low-cost airlines keep overheads down by operating only a single type of aircraft,

therby reducing operational, maintenance and training costs. It also provides the pilots

and the cabin crew the flexibility to operate on any aircraft in the fleet.

7

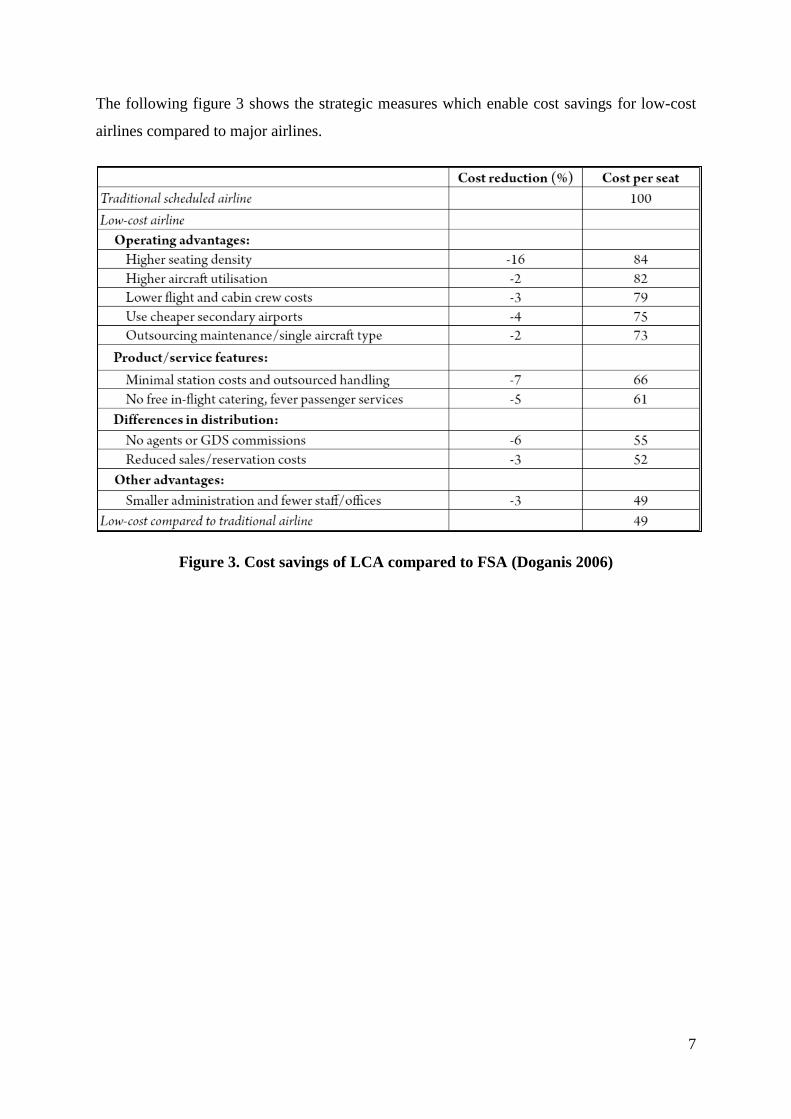

The following figure 3 shows the strategic measures which enable cost savings for low-cost

airlines compared to major airlines.

Figure 3. Cost savings of LCA compared to FSA (Doganis 2006)

8

CHAPTER 4

ANALYSIS: JETBLUE AIRWAYS (1999-2003)

4.1 JetBlue Airways Brief

JetBlue Airways, a low-fare, low-cost domestic airline based in New York, was incorporated

in Delaware in August 1998. JetBlue founded under the chief leadership of David Neeleman;

commenced operations in February 2000, with a mission to offer high-quality customer

service and differentiated products to underserved markets (JetBlue Airways 2005).

4.2 JetBlue Strategic Approach

JetBlue Airways, as part of its business strategy, implements a combination of low-cost

leadership and differentiation strategies.

The low cost strategic approach has brought about great success to JetBlue’s performance. As

for the operations, JetBlue uses paperless cockpit and electronic ticketing which saves time

and reduces cost. Another key aspect of JetBlue’s success has been its differentiated flight

service; providing new aircraft, leather seats, free live satellite TV at every seat and a reliable

operating performance.

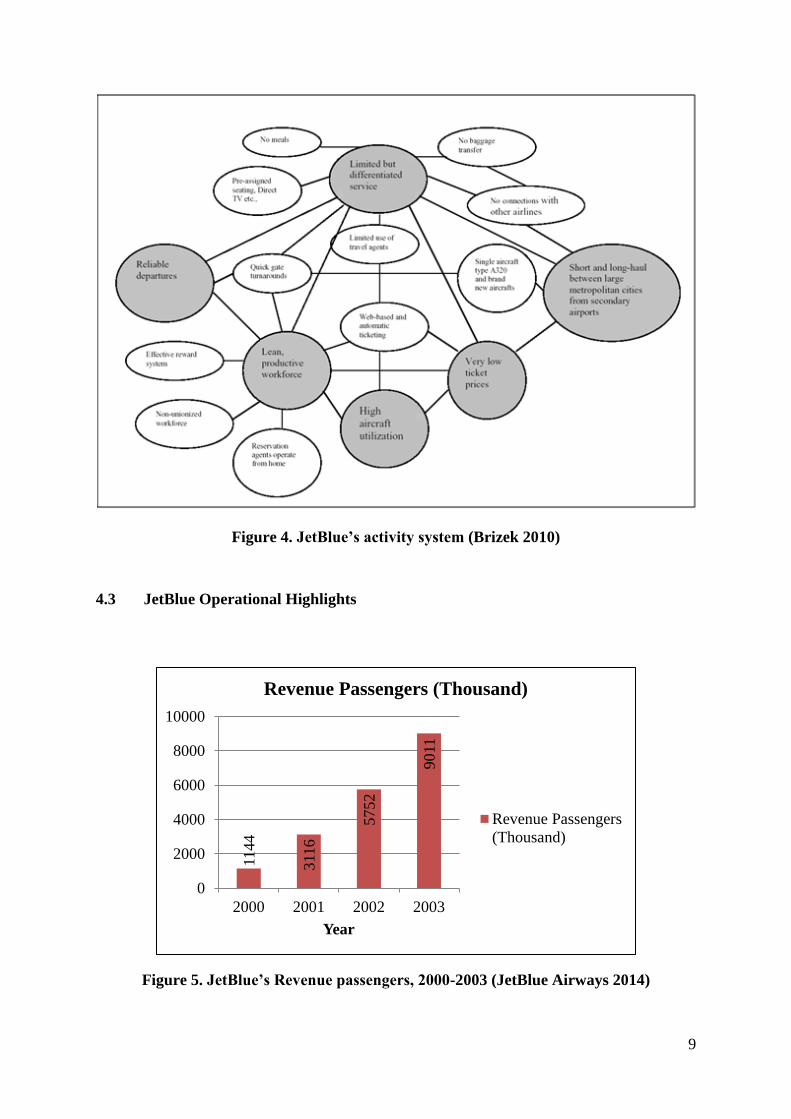

The characteristics of JetBlue’s business model can be stated by defining JetBlue’s activity

system, as shown below in figure 3.

9

Figure 4. JetBlue’s activity system (Brizek 2010)

4.3 JetBlue Operational Highlights

Figure 5. JetBlue’s Revenue passengers, 2000-2003 (JetBlue Airways 2014)

1144

3116

5752

9011

0

2000

4000

6000

8000

10000

2000 2001 2002 2003

Year

Revenue Passengers (Thousand)

Revenue Passengers

(Thousand)

10

Figure 6. JetBlue’s revenue passenger miles, 2000-2003 (JetBlue Airways 2014)

Figure 7. JetBlue’s available seat miles, 2000-2003 (JetBlue Airways 2014)

1004

3281

6835

11526

0

2000

4000

6000

8000

10000

12000

2000 2001 2002 2003

Year

Revenue Passenger Miles (Million)

Revenue Passenger

Miles (Million)1371

4208

82

39

13639

0

2000

4000

6000

8000

10000

12000

14000

2000 2001 2002 2003

Year

Available Seat Miles (Million)

Available Seat Miles

(Million)

11

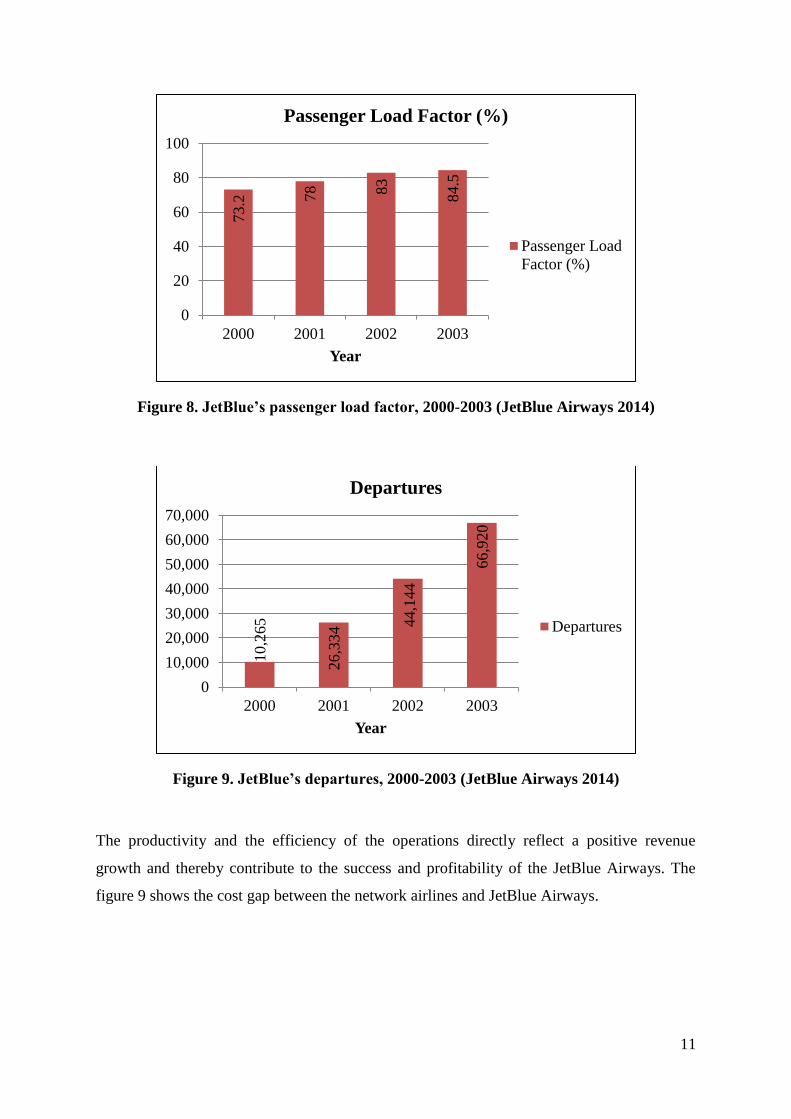

Figure 8. JetBlue’s passenger load factor, 2000-2003 (JetBlue Airways 2014)

Figure 9. JetBlue’s departures, 2000-2003 (JetBlue Airways 2014)

The productivity and the efficiency of the operations directly reflect a positive revenue

growth and thereby contribute to the success and profitability of the JetBlue Airways. The

figure 9 shows the cost gap between the network airlines and JetBlue Airways.

73.2

78

83

84.5

0

20

40

60

80

100

2000 2001 2002 2003

Year

Passenger Load Factor (%)

Passenger Load

Factor (%)10,2

65

26,3

34 44,1

44

66,9

20

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

2000 2001 2002 2003

Year

Departures

Departures

12

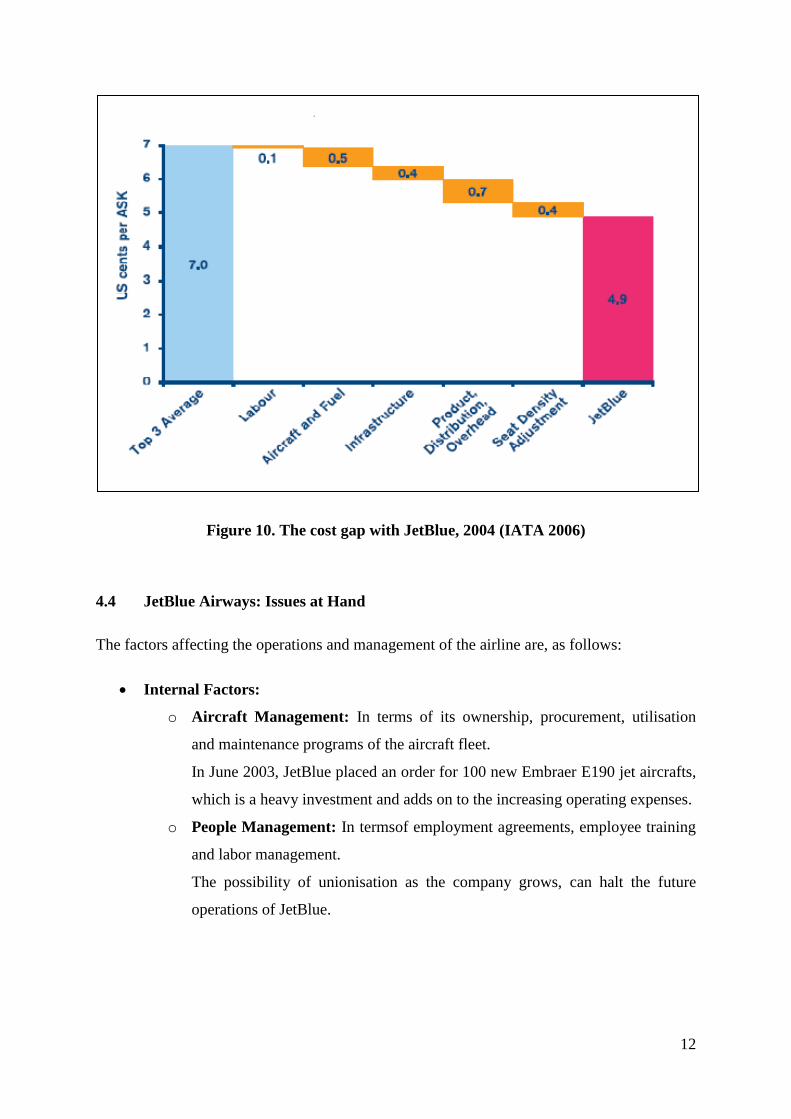

Figure 10. The cost gap with JetBlue, 2004 (IATA 2006)

4.4 JetBlue Airways: Issues at Hand

The factors affecting the operations and management of the airline are, as follows:

Internal Factors:

o Aircraft Management: In terms of its ownership, procurement, utilisation

and maintenance programs of the aircraft fleet.

In June 2003, JetBlue placed an order for 100 new Embraer E190 jet aircrafts,

which is a heavy investment and adds on to the increasing operating expenses.

o People Management: In termsof employment agreements, employee training

and labor management.

The possibility of unionisation as the company grows, can halt the future

operations of JetBlue.

13

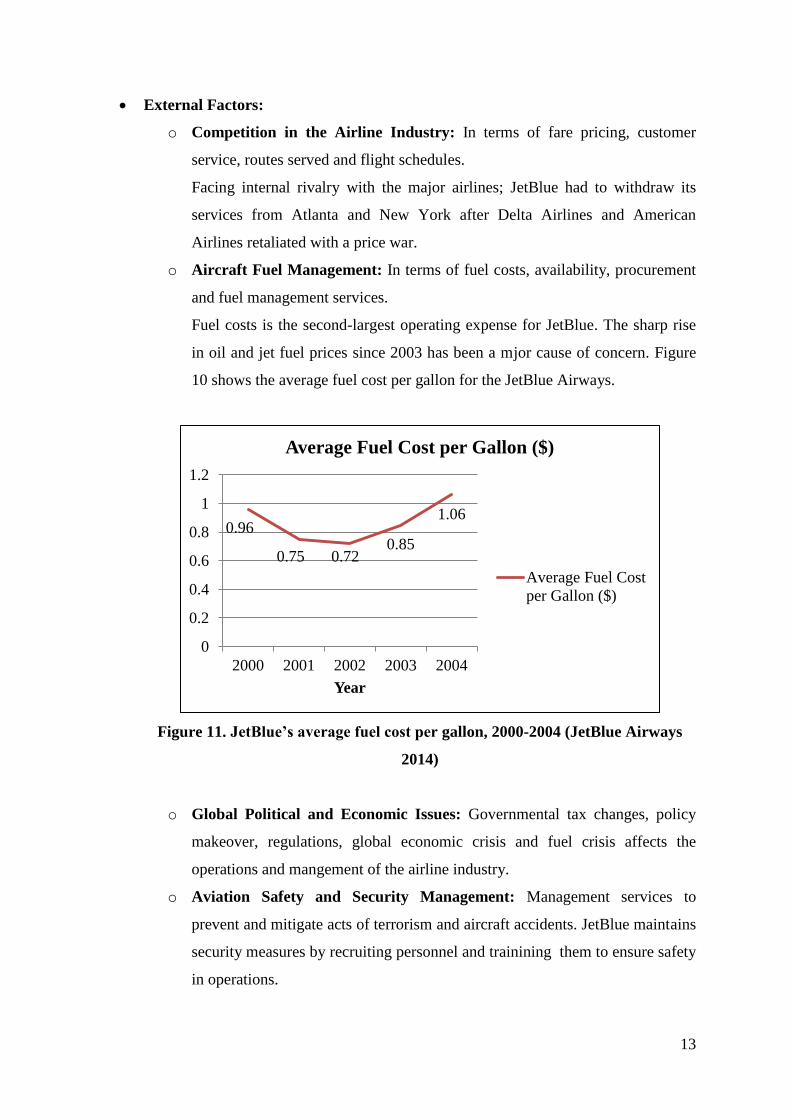

External Factors:

o Competition in the Airline Industry: In terms of fare pricing, customer

service, routes served and flight schedules.

Facing internal rivalry with the major airlines; JetBlue had to withdraw its

services from Atlanta and New York after Delta Airlines and American

Airlines retaliated with a price war.

o Aircraft Fuel Management: In terms of fuel costs, availability, procurement

and fuel management services.

Fuel costs is the second-largest operating expense for JetBlue. The sharp rise

in oil and jet fuel prices since 2003 has been a mjor cause of concern. Figure

10 shows the average fuel cost per gallon for the JetBlue Airways.

Figure 11. JetBlue’s average fuel cost per gallon, 2000-2004 (JetBlue Airways

2014)

o Global Political and Economic Issues: Governmental tax changes, policy

makeover, regulations, global economic crisis and fuel crisis affects the

operations and mangement of the airline industry.

o Aviation Safety and Security Management: Management services to

prevent and mitigate acts of terrorism and aircraft accidents. JetBlue maintains

security measures by recruiting personnel and trainining them to ensure safety

in operations.

0.96

0.75 0.72 0.85

1.06

0

0.2

0.4

0.6

0.8

1

1.2

2000 2001 2002 2003 2004

Year

Average Fuel Cost per Gallon ($)

Average Fuel Cost

per Gallon ($)

14

4.5 JetBlue Business - Opportunities, Threats and Risks

Opportunities:

JetBlue must follow its strategy, by increasing the frequency of flights as

requirements necessitates.

Target the mid-sized market segments using the 100-seat Embraer E190.

Cut the turnaround time of flights and lower the aircraft fuel requirements to increase

revenue and decrease costs.

Increase the use of Internet to reduce the sales and distributions costs.

Increase the use of technology, such as for baggage handling and baggage tracking.

Charge for the in-flight amenities, gaining additional revenue.

Threats:

JetBlue faces stiff competition from the other low-cost and major carriers, with

carriers like Southwest Airlines, Delta Airlines and United Airlines cutting down

ticket prices.

Rising fuel costs and the problem of availability is a concern for JetBlue Airways.

JetBlue, planning to be the launch customer of the Embraer E190, may be exposed to

unexpected problems (technical and/or non-technical) (Smart et al. 2007).

An economic downturn or any safety and/or security lapses will lower the demand for

air travel (Smart et al. 2007).

Shift of political powers and changes to government rules and regulations can affect

the operations of the airline industry.

Limited number of suppliers for the aircraft parts, equipments and other products can

pose as a threat. A high supplier power can limit the options and availability of the

airlines (JetBlue Airways 2004).

Risks:

JetBlue business being highly dependent on New York City market is a high risk.

JetBlue’s plans to purchase the Embraer E190 is a shift from its initial strategy to

operate a single type of aircraft. JetBlue’s usage of multiple aircraft types (A320’s and

15

Embraer E190) will increase the maintenance and service costs (JetBlue Airways

2005).

JetBlue may face unionisation, which may result in work stoppages and increased

labor costs. Unions can strike whenever their demands or agreemanets are not met.

JetBlues’ business will be harmed , if they are not able to attract or retain the services

of the vastly qualified and experienced personnel (JetBlue Airways 2004).

JetBlue’s high level of debt will harm the company’s growth strategy (JetBlue

Airways 2005).

JetBlue’s branding and cost performances will be harmed in the event of a flight

delay/cancellation or an accident/incident involving the aircraft.

16

CHAPTER 5

JETBLUE RESEARCH SOLUTIONS

5.1 Can JetBlue continue its spectacular growth?

In 2003, while the airline industry suffered heavy losses; JetBlue had a net income of $103.9

million. JetBlue generated an operating margin of 16.91% which was higher than all of the

major U.S. airlines (JetBlue Airways 2004).

JetBlue follows a controlled growth plan characterised by cost control diligence, a healthy

balance sheet, and a top-rated product offering delivered by dedicated crewmembers.

JetBlue’s strategy to maintain a low-cost structure can generate continued revenue and

earnings growth provided it adapts to the growing labor costs, fuel costs, aircraft maintenance

and compensation costs.

5.2 Were its competitive advantages sustainable?

The two bases of JetBlue’s competitive advantages are low-cost leadership and

differentiation strategies. JetBlue Airways has successfully achieved superior performance by

integrating the low-cost services with a differentiated offering. However, a small change in

the competitive factors can affect the entire operations and management of activities.

JetBlue will not be able to maintain the low-cost advantages over other airlines in

future, considering:

o The major airlines’ transition to the low-cost strategy

o The increasing operating costs

Maintenance costs with aging fleet

Labor costs, compensation costs etc.

JetBlue will not be able to maintain the differentiation strategy, as the differentiated

product features could easily be imitated.

The other aspect is the investment on the new type of aircraft Embraer E190, which is

a change from JetBlue’s business strategy of operating using only a single type of

aircraft. It could be a risk to JetBlue’s business, as it is not only a financial liability,

but also increases JetBlue’s operating expenses.

17

CHAPTER 6

PLAN OF ACTION

6.1 Recommendations

In order to maintain the growing success and profitability of the airline business, JetBlue has

to define a proper framework both internally and externally. For JetBlue to sustain the

growth, it needs to re-emphasise strategic planning. The main reason to JetBlue’s strategic

success is its efficiency and productivity of operations.

In order to improve the efficiency of the operations, JetBlue must focus on long-term

strategies on increasing PRASM above CASM (Smart et al. 2007).

JetBlue has to continue its low-cost approach by offering low ticket fares to

customers.

Risks: It could slow down overall productivity and casue operational costs to grow.

Outcomes: It is to attract customers, as customer satisfaction is one of the primary

bases of JetBlue airlines to acheive optimal efficiency.

In-flight, the airlines should charge for their offered benefits. The airlines should offer

food-for-purchase and other amenities, and should also charge for extra luggage and

for more legroom.

Risks: It may lead to extra expenses and wastages (food).

Outcomes: It is to gain additional revenue.

JetBlue has to reduce fuel expenditures. JetBlue should adopt the fuel hedging

strategy to mitigate the potential risk of rising crude oil prices. To improve fuel

efficiency, airlines could also reduce the aircraft weight or by including winglet

devices/blended wing body system (Maxim 2013).

Risks: The hedging program may lead to mistakes, if not planned and managed

properly.

Outcomes: It is to reduce fuel consumption, since fuel costs represent one of the

largest operating expense. A proper hedging program can protect against rising fuel

prices.

18

JetBlue should defer the delivery of the Embraer E190s’ as it is risk being the lanuch

customer of the product. Meanwhile, JetBlue should invest in Airbus jets.

Risks: JetBlue’s limited cash source for investment and high level of debt may affect

the growth strategy.

Outcomes: The investmenst supports the expansion plans.

JetBlue has to expand its route network to the underserved Carribean and Latin

American countries. JetBlue should also cancel services of unprofitable routes that

show less demand for future.

Risks: The competition may affect the efficiency and productivity of the operations.

Outcomes: The route network will be well established and will earn the growth.

JetBlue‘s management should implement a monthly incentive performance-based

program for the emplyees by setting targets and goals so as to increase the workforce

efficiency and productivity (Smart et al. 2007).

Risks: Monthly bonuses and rewards will increase the costs.

Outcomes: It is to increase the workforce effciency and productivity, and thereby

improve on-time performance.

JetBlue should also reconsider its passenger boarding plan. JetBlue currently utilises a

random assigned seating pattern. JetBlue has to adopt a back-front or a self-organising

approach boarding plan in order to acheive a fast flight turnaround.

Risks: It may create a negative feedback from a section of customers who prefer

assigned seats.

Outcomes: It is to decrease the average time to takeoff and improve the efficiency,

since the back-fromt and unassigned random system are more efficient methods of

passenger loading (Smart et al. 2007).

19

CHAPTER 7

CONCLUSIONS

The airline industry is in the process of a profound change, with every airline now evolving

to be a lower-cost airline (IATA 2006). The report has identified and analysed the competitve

strategies and advantages of the airline business models, which has helped in identifying how

an airline can further focus its positioning for a sustainable long-term path of growth and

profitability.

The report also discussed the strategic approach of the JetBlue Airways. Basing on the

operating and financial analysis conducted on JetBlue Airways; the higher revenues and

lower unit costs has led to the net income growth. However, considering the future operations

and management, JetBlue’s competitive advantages don’t stand sustainable. The report also

suggests that, JetBlue’s foremost goal should be to alleviate its expenses and increase

available seat miles.

20

REFERENCES

Aimia (2013) The Legacy Effect [online] available from

<http://www.aimia.com/content/dam/aimiawebsite/CaseStudiesWhitepapersResearch/english

/AirlineLoyalty_LowCostCarriers.pdf> [3 July 2014]

Brizek, M. (2010) ‘JetBlue Airways, Trouble in the Sky’ Journal of Aviation Management

and Education [online] 1, 1-13. available from

<http://www.aabri.com/manuscripts/10478.pdf> [5 July 2014]

Chowdhury, E. (2007) Low Cost Carriers: How Are They Changing the Market Dynamics of

the U.S. Airline Industry? [online] Ontario: Carleton University. available from

<http://www.carleton.ca/economics/wp-content/uploads/he-chowdhury-erfan.pdf> [4 July

2014]

Doganis, R. (2006) The Airline Business [online] 2nd

edn. New York: Routledge. available

from <http://sivilhavacilik.files.wordpress.com/2011/10/the-airline-business.pdf> [4 July

2014]

Hellqvist, D., Elison, J., and Karakan, T. M. (2012) Low-Cost Carriers: A Revised Business

Model for Future Success [online] Sweden: Jönköping University. available from

<http://www.diva-portal.org/smash/get/diva2:539537/FULLTEXT01.pdf> [4 July 2014]

IATA (2006) Airline Cost Performance [online] available from

<http://www.iata.org/whatwedo/Documents/economics/airline_cost_performance.pdf> [9

July 2014]

ICAO (2003) The Impact of Low Cost Carriers in Europe [online] available from

<http://www.icao.int/sustainability/CaseStudies/StatesReplies/Europe_LowCost_En.pdf> [4

July 2014]

JetBlue Airways (2014) Annual Reports [online] available from

<http://investor.jetblue.com/phoenix.zhtml?c=131045&p=irol-reportsAnnual> [6 July 2014]

21

JetBlue Airways (2005) JetBlue Airways [online] available from <http://library.corporate-

ir.net/library/13/131/131045/items/211507/200410k.pdf> [6 July 2014]

JetBlue Airways (2004) JetBlue Airways: Analysis of JetBlue Airways Corporation [online]

available from <http://web.mit.edu/wysockip/www/Jetblue.pdf> [6 July 2014]

Kachaner, N., Lindgardt, Z., and Michael, D. (2011) ‘Innovating low-cost business models’

Strategy & Leadership [online] 39 (2), 43-48. available from

<http://syariahmuamalah.blogdetik.com/files/2012/03/93c7bfd05a2f07f7fb8bd1fb17ad544d_

innovating-low-cost-business-models.pdf> [3 July 2014]

Maxim, L. D. (2013) ‘The Development of the Low-Cost Carriers Business Models.

Southwest Airlines Case Study’ Scientific Annals of the Alexandru Ioan Cuza University of

Iaşi Economic Sciences [online] 59 (1), 231-238. available from

<http://www.degruyter.com/dg/viewarticle.fullcontentlink:pdfeventlink/$002fj$002faicue.20

12.59.issue-1$002fv10316-012-0016-7$002fv10316-012-0016-

7.pdf?t:ac=j$002faicue.2012.59.issue-1$002fv10316-012-0016-7$002fv10316-012-0016-

7.xml> [8 July 2014]

Sarker, Md. A. R., Hossan, C. G., and Zaman, L. (2012) ‘Sustainability and Growth of Low

Cost Airlines: An Industry Analysis in Global Perspective’ American Journal of Business and

Management [online] 1 (3), 162-171. available from

<http://wscholars.com/index.php/ajbm/article/viewFile/23/pdf> [2 July 2014]

Smart, R., Saydalikhodjayev, A., and Craig, S. (2007) Strategic Report for JetBlue Airways

[online] California: Harkness Consulting Pomona College Economics. avialable from

<http://economics-

files.pomona.edu/jlikens/SeniorSeminars/harknessconsulting2008/pdfs/Jet_Blue.pdf> [8 July

2014]

22

Vespermann, J., and Holztrattner, S. (2010) ‘The Air Transport System’ Introduction to

Aviation Management 2, 9-24. cited in Hellqvist, D., Elison, J., and Karakan, T. M. (2012)

Low-Cost Carriers: A Revised Business Model for Future Success [online] Sweden:

Jönköping University: 24. available from <http://www.diva-

portal.org/smash/get/diva2:539537/FULLTEXT01.pdf> [4 July 2014]

Vidović, A., Štimac, I., and Vince, D. (2013) ‘Development of Business Models of Low-Cost

Airlines’ International Journal for Traffic and Transport Engineering [online] 3 (1), 69-81.

available from <http://www.ijtte.com/uploads/2013-03-25/5d57e65e-a0a9-

482fIJTTE_Vol%203%281%29_7.pdf> [2 July 2014]