Embed Size (px)

Citation preview

Pergamon

Tekmafics and Informtics, Vol. 14, No. 2, pp. 159-171, 1997 % 1997 Elsevier Science Ltd. All rights reserved

Printed in Great Britain 0736-5853/97 $17.00 + 0.00

PII: so736-5853(%)ooo31-7

GAINING COMPETITIVE ADVANTAGE IN THE

U.S. WIRELESS TELEPHONY MARKET:

THE MARKETING CHALLENGE

Manoj K. Agarwal Barry E. Goodstadt

Abstract - Wireless telephony in the U.S. is undergoing a major change due to Federal Communications Commission regulations and the new telecommuni- cations bill. This paper identifies some of the major strategic and environ- mental factors associated with this change. Some strategies for gaining sustainable competitive advantage are discussed along with their marketing implications. 0 1997 Elsevier Science Ltd

Keywords - Wireless, wireless telephony, marketing strategy, telecommuni- cations, competitive advantage.

The worldwide telecommunications market is expected to reach an annual $3 trillion volume per year by the year 2010, with 20% of this market being for wireless equipment and services (Schneiderman, 1994). While cellular service currently has over 35 million subscribers in the U.S., a new digital service, Personal Communi- cations Services (PCS), promises to provide superior voice quality, increased security and more advanced calling features than cellular service. Cellular and PCS services will be close wireless competitors in the next decade.

In preparation for PCS, The Federal Communications Commission (FCC) has recently accumulated $18 billion in PCS licensing fees (Hardy, 1996). Building the ser- vice and technological infrastructure and introducing PCS to the market will take considerably more investment on the part of licensees. By way of comparison, the cel- lular industry spent about $21 billion to build the cellular infrastructure and introduce its services between 1983 and 1995 (CTIA, 1996).

The marketing challenges facing the wireless telecommunications industry will change rapidly over the next few years as the competitive and regulatory landscape evolves. Aron (1995) posits that an “ice age” is coming to the wireless industry such that not all market participants will survive a period of rapid change and highly com- petitive market conditions.

In this paper we identify a number of environmental changes that will pose new challenges to the marketing of wireless telecommunications. At the present time, the

Manoj K. Agarwal is with the School of Management, Binghamton University,

Binghamton, New York 13902-6015, U.S.A. and Barry E. Goodstadt is with ITRON

Inc., Spokane, Washington, U.S.A.

159

160 Manoj K. Agatwal and Barry E. Goodstadt

wireless market consists primarily of analog cellular service, paging, mobile data, and specialized mobile radio (SMR) offerings. This market will soon be joined by PCS voice services, digital cellular service, two-way paging and messaging services, voice and data mobile satellite services (like IRIDIUM and Orbcomm) and enhanced spe- cialized mobile radio services (ESMR) which is a digital version of SMR. In the U.S. market, the number of wireless subscriptions is expected to grow from about 50 million in 1994 to almost 200 million in 2005 (PCIA, 1995). In this paper we focus our analysis primarily on mass market voice services including cellular and PCS.

EXTERNAL MARKET LANDSCAPE

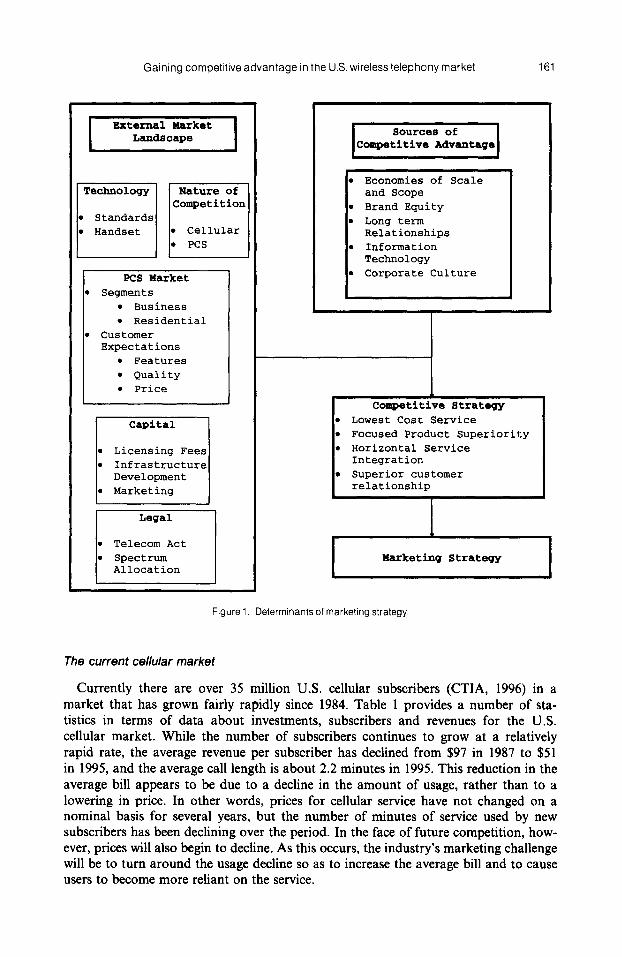

We first discuss the external market landscape of the wireless market. As part of this analysis, we examine the underlying technology, the current cellular market, the recent telecommunication bill, the potential PCS market, the nature of competition in this market and the capital requirements. Next, we explore potential sources of competitive advantage that firms can employ to attain necessary market share, and then draw out corresponding implications for marketing strategy. Figure 1 illustrates the relationship between the various elements.

Technology

A number of technologies are available to provide wireless voice services. Cellular service in the U.S. is heavily based on the Analog Mobile Phone Service (AMPS) standard which uses spectrum allocated in the 800 MHz band. New digital standards for cellular rely on either time division multiplex technology (TDMA) or code division multiplex technology (CDMA) and will use the same spectrum currently allotted for analog cellular usage.

A number of PCS standards are available in the U.S. These include versions of TDMA, CDMA, and General System for Mobile (GSM) standards adapted to the spectrum in the 1.9-2.1 GHz band. In the rest of the world the European GSM stan- dard is becoming most common. GSM has been adopted in 80 countries (Arnold, 1996) and is used both in digital cellular (at 900 MHz) and in PCS bands (at 1.8-2.2 GHz).

In the U.S., there is currently a debate raging among CDMA, TDMA and GSM proponents to win over the PCS providers to their point of view but it is likely that these multiple standards will co-exist in this country for some time to come. However, unless universal standards are adopted, the potential for seamless PCS roaming in the U.S. will not be easily realized. Firms that have obtained PCS licenses have now or will soon have to decide which of the available technical solutions they will imple- ment.

Advances in battery technology and in computer chip technology have made it pos- sible to dramatically reduce the size of handsets and to increase the length of time that users can talk on the phone without recharging. These advances make the handsets much more acceptable to consumers. Accordingly, the pace of adoption of wireless communications services will increase. Bear, Steams and Company (Keller, 1996a) forecasts that there will be nearly 27 million PCS users and 60 million cellular users in the U.S. by the end of the year 2000.

Gaining competitive advantage in the U.S. wireless telephony market 161

L

I External Market Landscape I

PCS Market.

b Segments l Business

l Residential

b Customer Expectations

l Features

l Quality

l Price

l Licensing Fees

l Infrastructure Development

I Legal

I

Economies of Scale and Scope

Brand Equity

Long term Relationships

Information Technology

Corporate Culture

l Lowest Cost Service

l Focused Product Superiority

l Horizontal Service Integration

l Superior customer relationship

Marketing Strategy

Figure 1. Determinants of marketing strategy.

The current cellular market

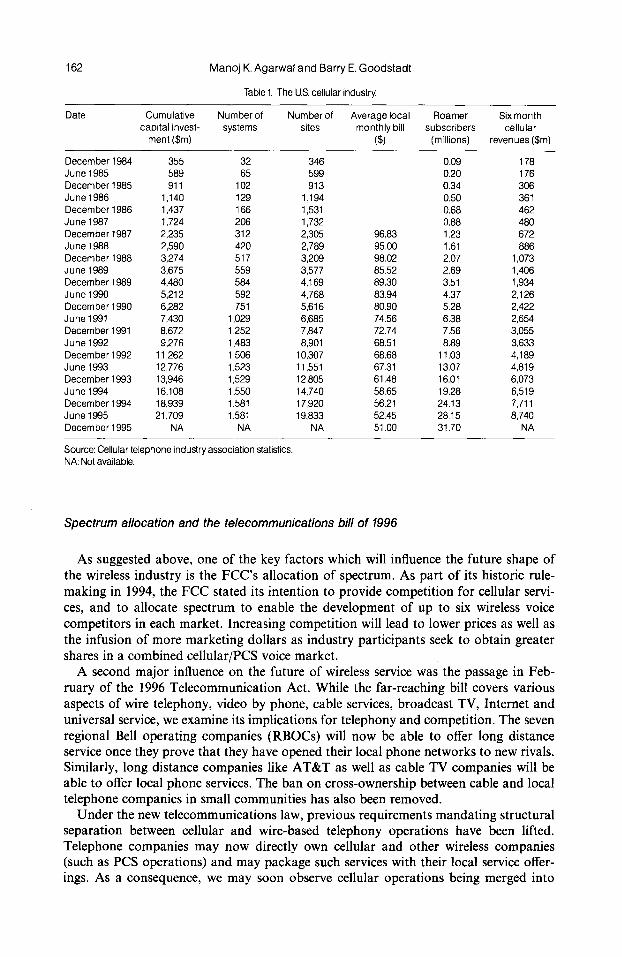

Currently there are over 35 million U.S. cellular subscribers (CTIA, 1996) in a market that has grown fairly rapidly since 1984. Table 1 provides a number of sta- tistics in terms of data about investments, subscribers and revenues for the U.S. cellular market. While the number of subscribers continues to grow at a relatively rapid rate, the average revenue per subscriber has declined from $97 in 1987 to $51 in 1995, and the average call length is about 2.2 minutes in 1995. This reduction in the average bill appears to be due to a decline in the amount of usage, rather than to a lowering in price. In other words, prices for cellular service have not changed on a nominal basis for several years, but the number of minutes of service used by new subscribers has been declining over the period. In the face of future competition, how- ever, prices will also begin to decline, As this occurs, the industry’s marketing challenge will be to turn around the usage decline so as to increase the average bill and to cause users to become more reliant on the service.

162 Manoj K. Agarwal and Barry E. Goodstadt

Tablel. The U.S.cellularindustry

Date Cumulative Numberof Numberof Averagelocal Roamer Sixmonth capitalinvest- systems sites monthly bill subscribers cellular ment($m) (S) (millions) revenues($m)

December1984 355 32 346 June1985 589 65 599 December1985 911 102 913 June1986 1,140 129 1,194 December1986 1,437 166 1,531 June1987 1,724 206 1,732 December1987 2,235 312 2,305 June1988 2,590 420 2,789 December1988 3,274 517 3,209 June1989 3,675 559 3,577 December1989 4,480 584 4,169 June1990 5,212 592 4,768 December1990 6,282 751 5,616 June1991 7,430 1,029 6,685 December1991 8,672 1,252 7,847 June1992 9,276 1,483 8,901 December1992 11,262 1,506 10,307 June1993 12,776 1,523 11,551 December1993 13,946 1,529 12,805 June1994 16,108 1,550 14,740 December1994 18,939 1,581 17,920 June1995 21,709 1,581 19,833 December1995 NA NA NA

96.83

95.00 98.02 85.52 89.30 83.94 80.90 74.56 72.74 68.51 68.68 67.31 61.48 58.65 56.21 52.45 51.06

0.09 178 0.20 176 0.34 306 0.50 361 0.68 462 0.88 480 1.23 672 1.61 886 2.07 1,073 2.69 1,406 3.51 1,934 4.37 2,126 5.28 2,422 6.38 2,654 7.56 3,055 8.89 3,633 11.03 4,189 13.07 4,819 16.01 6,073 19.28 6,519 24.13 7.711 28.15 8,740 31.70 NA

- Source:Cellulartelephoneindustryassociation statistics NA:Notavailable.

Spectrum allocation and the telecommunications bill of 1996

As suggested above, one of the key factors which will influence the future shape of the wireless industry is the FCC’s allocation of spectrum. As part of its historic rule- making in 1994, the FCC stated its intention to provide competition for cellular servi- ces, and to allocate spectrum to enable the development of up to six wireless voice competitors in each market. Increasing competition will lead to lower prices as well as the infusion of more marketing dollars as industry participants seek to obtain greater shares in a combined cellular/PCS voice market.

A second major influence on the future of wireless service was the passage in Feb- ruary of the 1996 Telecommunication Act. While the far-reaching bill covers various aspects of wire telephony, video by phone, cable services, broadcast TV, Internet and universal service, we examine its implications for telephony and competition. The seven regional Bell operating companies (RBOCs) will now be able to offer long distance service once they prove that they have opened their local phone networks to new rivals. Similarly, long distance companies like AT&T as well as cable TV companies will be able to offer local phone services. The ban on cross-ownership between cable and local telephone companies in small communities has also been removed.

Under the new telecommunications law, previous requirements mandating structural separation between cellular and wire-based telephony operations have been lifted. Telephone companies may now directly own cellular and other wireless companies (such as PCS operations) and may package such services with their local service offer- ings. As a consequence, we may soon observe cellular operations being merged into

Gaining competitive advantage in the US. wireless telephony market 163

traditional telephone company operations. This trend is already apparent as South- western Bell has merged Southwestern Bell Mobile back into its wireline operation, and BellSouth is marketing both wireless and wireline products through its regulated tele- phone operations.

The potential PCS market

PCS is not one single service, but an array of services. They are a “set of capabilities that allow terminal mobility, and personal mobility” (Hemmady, 1995). As described by Hemmady (1995) terminal mobility is the ability of the terminal to access telecom- munications services from different locations while in motion. Personal mobility allows the user to access telecommunications services from any terminal on the basis of a personal identifier. The network has to be able to identify and locate the terminal or user at any point.

Compared to analog cellular, PCS may be characterized as a lower powered service. That is, the service operates by means of smaller, low power micro-cells with antennas every 1,000 feet or so which communicate by digital signaling techniques. This low power requirement permits the use of smaller handsets, with longer battery life, more advanced features such as messaging services, and voice quality which approaches that of landline service.

As PCS networks are built, PCS will attract new subscribers (due to its higher func- tionality and array of services) as well as converting some current cellular users. The penetration of wireless voice service is forecast to be 40% of the U.S. population in the next 10 years, with 15% penetration for PCS and 25% for cellular (Hardy, 1996). Current wireless penetration is about 13% of the U.S. population (CTIA, 1996).

Based on a large number of proprietary focus groups conducted by us in the last several years, we find that potential customers know what they want in PCS offerings. Most consumers want the handset to be small, to be durable and waterproof, to fit in the pocket or to be of wristwatch size, to have eight plus hours of talk time, and to also provide integrated two-way text messaging. Some even want hands-free operations (with an earpiece and lapel mike) and voice-activated dialing. Consumers would like to have call screening and call blocking services, to be reachable anywhere, and to have a lower price than cellular. Two-way communications are essential to this group and it will be important to have pricing packages that allow for predictable expenses. The underlying communication needs of residential customers are to be able to coordinate family activities as well as to provide communications services that help alleviate safety, emergency, and health concerns.

It is amazing to note that PCS is not treated as a new innovation, but as a service where customer needs are driving technology, a technology that which is finally catch- ing up to user requirements. Thus, we anticipate that the diffusion of PCS will be much more a function of the supply and the pricing rather than requiring the education of the customers, as is typical in innovative products. Perhaps this is due to the existence of cellular which has served to educate consumers regarding the application and use of wireless voice services.

Business customers want their mobile employees to have convenient two-way com- munications with the office information systems, as well as to having access to key personnel for decision inputs. Some primary business information needs include mes- sages from the office, electronic mail, faxes, client information, travel related informa- tion, and data from their own desktop. They also desire access to this information from various locations including their own home, in town away from office, in meetings,

164 Manoj K. Agatwal and Barry E. Goodstadt

while traveling, and during down time and so on. Seamless integration between other services like wireless PBXs, pagers and e-mail networks will also be desirable.

As the entrance of new PCS operators broadens the market, the expectations of the customers are going to evolve. These customers are used to local exchange carrier ser- vice quality levels (e.g. near 100% reliability, good sound quality, responsive repair service, credit for mis-dialed calls and so on), and will expect the same from new wire- less services.

Nature of competition

For cellular firms. In the early years of this industry, the FCC licensed only two competing cellular operators in any given market with 25 MHz of spectrum each. That competitive environment could be characterized as a duopoly with only limited price competition. Usually one cellular carrier was a wireline company (i.e. owned by an existing local exchange carrier), while the other was a non-wireline provider - a new, non-telephone company competitor. However, the non-wireline companies have gone through an extensive series of consolidations through alliances and buyouts. They are now also largely owned either by wireline telephone companies (e.g. Southwestern Bell, Bell Atlantic, BellSouth) from other regions of the country, or by AT&T.

The cellular industry, while showing high growth rates, has also been characterized by a high rate of customer churn. (It is common knowledge in the industry that churn has been running at 2% or more per month and in some markets has been as high as 3.5% per month.) Until recently, the competition between the firms has not been based on service differentiation, but rather on coverage and roaming differentiation. Most of the price competition between the firms was based on handset subsidies (i.e. to subsi- dize the cost of the handset so that the customer acquires a handset for free or for a very nominal fee) rather than on air time prices. The cellular industry has a poor reputation in terms of quality of services (e.g. a large number of dropped calls, the existence of holes in the coverage, poor voice quality, inadequate or poor customer service, etc.).

With the FCC’s recent allocation of spectrum for PCS, a number of new competitors are expected to enter the wireless arena in different markets across the country. Argu- ments have been made by some authors (Naik, 1995) that by the time PCS is intro- duced in the market, cellular service providers will have migrated to digital offerings, and may be able to offer most of the benefits that can be delivered by PCS. It should be noted, however, that cellular carriers have had the technology available to make the transition from analog to digital services for a number of years yet they have not been able to migrate a substantial portion of the customer base to digital cellular. The migration to digital is not an easy one due to the need to transition a large imbedded base of analog users, and the need to simultaneously operate both analog and digital systems till the transition is complete. The appearance of digital PCS offerings may well speed up the cellular digital migration process as cellular operators fight to retain their customers rather than lose them to PCS.

This will make it likely that churn rates will increase, and that the marketing chal- lenge for existing wireless voice providers will be to retain current customers in the face of new competitors. Cellular firms, for example, will have to change their corporate culture and try to focus on providing excellent service to customers if they are to retain customers whose handsets they have so heavily subsidized.

Gaining competitive advantage in the U.S. wireless telephony market 165

For PCS firms. The first time entry costs for PCS firms entering the wireless voice market are considerable. These costs generally include a variety of operating expenses (including local telephone access and interconnect charges), selling and marketing expenses (including customer care, customer activation, and subsidies to “buy down” the cost of wireless terminals), general and administrative expenses, and capital expen- ses. The capital expenses costs include FCC licensing fees, base site radios, optical fiber, switches, and the expenses for relocating spectrum incumbents from the 1.9-2.1 GHz band to other blocks of spectrum.

Some business simulations have been performed recently by EDS (Aron, 1995) to estimate break-even market shares for PCS firms. Assumptions were made about the cost items outlined above, license costs determined based on average actual FCC spectrum auction bids in different size markets, the buildout rates, and when, where and which markets will be served first. The simulations show that for PCS firms to just survive, they will need market shares of between 17% and 35% (in terms of number of customers) in large markets and shares of between 33% and 83% in small markets (at an optimistic average monthly revenue per subscriber of $45, compared to $51 for current cellular subscribers). This implies that not more than three competitors can survive in the small markets. Up to nine competitors may theoretically exist in each market (two cellular companies, six PCS operators and one Enhanced Specialized Mobile Radio or ESMR operator). It should be noted that these simulations were quite conservative in their approach and did not take into account the much higher license fees paid in recent auctions in the C band (or small/minority business). Thus, the like- lihood of multiple providers surviving would be even lower than predicted in the Aron (1995) analysis. Given this situation, there will be intense competition for market share to ensure survival.

Capital requirements

From 1983 to 1995, the cellular industry invested approximately $21 billion in the development of network infrastructure. This does not include the cost of marketing, sales and handset subsidies or of operating losses experienced by cellular carriers in their early years. Capital for this development has generally been available in signifi- cant amounts as the cellular divisions of wireline firms had corporate parents as a source of funding. Non-wireline firms have raised capital from a range of sources including venture capitalists, debt markets, and initial public offerings of stock. Equipment manufacturers also financed part of the expansion by providing “pay as you go” schemes. These schemes enabled the cellular operators to buy equipment from them at reduced costs in the early years of operation when the cash flow is tight.

As noted earlier, the PCS industry has already invested $18 billion in spectrum license fees alone. The infrastructure costs for the PCS buildout will potentially be as much as $25 billion in additional investments (Donaldson, Lufkin & Jenrette Securities Corporation, 1996). What this means is that FCC licensing fees have created extensive financial strains on industry participants who will still have need to build the PCS infrastructure. Furthermore, these operators will need to competitively market their services against entrenched cellular incumbents who have already begun to reduce their rate of infrastructure investment. In effect, the high cost of acquiring a license will financially weaken potential PCS operators and reduce their potential for survival over the long run. Many of the winners of PCS licenses are now actively trying to develop new sources of funding through initial public offerings (IPOs) and the future of these firms will depend heavily on how they perform in these markets.

166 Manoj K. Agarwal and Barry E. Goodstadt

SOURCES OF COMPETITIVE ADVANTAGE

In service industries, the major potential sources of sustainable competitive advan- tage have been discussed by Bharadwaj, Varadarajan and Fahy, (1993). We focus here on five of these sources that seem relevant for telecommunication firms to gain com- petitive advantage: (a) economies of scale and scope, (b) brand equity, (c) long term relationships, (d) information technology, and (e) corporate culture and organizational expertise.

A firm will choose among some of these based on the external environment that it faces and its own internal resources.

Economies of scale and scope

With the entry of larger competitors and firms with multiple service lines, economies of scale and scope will become extremely important. Once a corporate infrastructure is in place, the cost of providing additional services to customers is small. For example, the cost of providing call screening, voice mail and caller ID to a customer who has already bought basic PCS service is minimal. Companies that can provide a full range of services like local, long distance, wireless voice and data, TV, and internet access are likely to be more successful due to economies of scope and the ability to market a whole bundle of services. This, of course, has been facilitated by the deregulation of the market. Hill (1996) calls this situation the “battle of the bundle”. Wireless companies will be able to offer bundled local, long distance and wireless services. However, inter- exchange carriers and others also have the capability to offer “service bundles” and may have larger existing customer bases to which they can offer this service. In addi- tion, multi-product firms can better bear the financial burden of marketing PCS pro- ducts as large amounts have already been invested in license costs.

It appears to us that bundling of services is preferred by many customers. In pro- prietary studies that we have undertaken, customers prefer bundles of local, long dis- tance, and wireless services from one company, rather than buying separate services from two or three different firms. Having a single point of contact for customer service, billing and service activation provides additional utility for customers.

An example of the value of bundling for local and long distance service is provided by Hill (1996). Between 41% and 54% of the customers in the various regions want AT&T to be their sole provider for local and long distance services. The RBOCs are second in this contest and expect to garner between 18% and 3 1% of bundled local and long distance service in their respective territories. MCI and Sprint are projected to get about 5% each of these bundled local, long distance offerings (Hill, 1996).

Larger firms can achieve these economies of scope through acquisition and mergers, while other firms will obtain this advantage through partnering arrangements. For example, AT&T has acquired McCaw Cellular, offers internet services, has ownership interest in Direct TV, and has a credit card business in addition to their long distance business. MCI is now offering a “bundle” of long distance, cellular, paging and internet services. In order to achieve economies of scope and provide themselves with a larger customer base for providing bundled service offerings, smaller firms like Bell Atlantic and NYNEX, and Southwestern Bell and Pactel will merge in 1997. Bell Atlantic and NYNEX have already combined their cellular operations.

Similarly, within the wireless industry, the combination of four RBOC-derived PCS wireless operations (Bell Atlantic, NYNEX, U.S. WEST and AirTouch) into PCS

Gaining competitive advantage in the U.S. wlreless telephony market 167

PrimeCo has resulted in an entity with extensive geographic coverage of the market and the ability to leverage assets across that broad base. Likewise, Sprint Spectrum, which is a partnership of Sprint, TCI, Cox and Comcast (three cable TV firms), pro- vides a good example of an effort to amass greater scale and scope of resources.

Brand equity

Aaker (1991) defines brand equity as “a set of brand assets and liabilities linked to a brand”. In the telecom market, some of these assets are brand awareness, brand loy- alty, and perceived quality. AT&T, MCI and Sprint have strong national brand names and will bring these assets to their wireless ventures. AT&T has a strong competitive edge in terms of its brand equity that was built on the basis of extensive advertising over a long period of time.

Since many firms are entering the wireless markets only now, the level of brand equity in the market can be judged by examining the strength of the brands in the local and long distance markets. A report by Morgan Stanley and Company (1995) shows that if prices were the same, in the local phone market, AT&T will get 30% of the market, the RBOCs 35%, Cable 19% and others (including Sprint and MCI) the rest. In long distance services, AT&T gets a phenomenal 46%, MCI, Sprint and RBOCs share 48% equally, while cable gets 6% market share. In the business market, while the long distance results are similar, the RBOCs’ share in the local phone market is much larger at 53%.

These results highlight the critical importance of brand equity, not only in the pre- sent telephony market but also in the upcoming competitive wireless markets. For example, PCS PrimeCo, a consortium of RBOCs, has no name recognition at present although its member companies are well known in their regional service areas. This organization will therefore need to use its considerable capital base to create and build brand recognition. Sprint Spectrum will have some built-in advantage due to the use of Sprint’s name but, as the third provider of long distance, its existing customer base is somewhat limited.

Long term relationships

Long term relationships will be extremely valuable to firms in this market. Retaining current customers is much less expensive than acquiring new ones. Churn is a major problem in the industry. Strategies have to be adopted to reduce churn by increasing the transaction cost to the customers and providing more value. One way to do this is to provide a bundle of services, including both wireless and land line telecommunica- tions and other related services. This will improve the relationships with the customers and also increase the implicit cost of switching for the customer. This strategy will be effective if the bundle of potential services offered is much wider for one firm over the others. As mentioned earlier, MCI recently began to offer a bundle of long distance, cellular, paging and internet services as part of its nationwide advertising campaign in September 1996. We anticipate that AT&T will shortly announce a similar program and may also provide satellite television in its bundle.

Rather than adopting short term strategies to grab market share, firms will have to use a long term strategy of providing value and retaining customers. AT&T is already adopting this long term view by looking at the value of a customer in terms of his/her net present value and aggressively going after the high value customers (Hill, 1996).

168 Manoj K. Agarwal and Barry E. Goodstadt

Information technology

Having comprehensive data bases of customers will be a major asset to players in the wireless market. MCI was able to develop its “Friends and Family” campaign because its billing system could match the numbers called with the numbers in the circle. AT&T’s information technology was not able to match this capability and, as a result, AT&T could not make a comparable offer and lost market share.

Even today, while AT&T has the broadest array of services available, its efforts to build a unified system of billing is behind schedule (Keller, 1996b). When a unified system for billing is ready, it will obviously provide a competitive advantage in the marketplace.

Sprint still suffers from the image it had several years ago of having an inadequate billing system, despite the fact that its historical billing problems are no longer present. Accordingly, Sprint has focused much of its strategy on price, offering ten cents per minute, rather than on more innovative technology-driven product offerings. Thus having state-of-the-art information technology can provide tremendous competitive advantages to firms in this industry.

Corporate culture and organizational expertise

In mobile telephony, some firms will have superior management skills. AT&T has high quality personnel in marketing and technical areas. Cable companies do not gen- erally have strong marketing programs, neither do most of the cellular operators. In recent years, cellular marketing departments have had difficulty processing a large volume of orders for service and have found it problematic to deal with a high volume of customer care inquiries. Since there have been more than enough customers coming to the carriers and seeking their services, little attention has been paid to innovative marketing and branding programs. This situation, however, will have to change as competition for customers becomes more intense.

Other new PCS players may have smaller, more agile organizations, and may be better able to take quick action. Agile firms can gain from the first mover advantage by rapidly bringing new services to market. Constantly being in touch with the market will therefore be important. Innovation in packaging and marketing will need to be used to provide positional advantage.

STRATEGIES FOR COMPETITIVE ADVANTAGE

Firms that leverage some of these bases of potential competitive advantage will see potential results in terms of strong customer satisfaction, a high degree of loyalty, larger market share and profitability.

Early adopters of these services will also have to be identified. Some of our proprie- tary research shows that early adopters of PCS in the residential sector are likely to be buyers of other high technology products such as pagers, compact disc players and video cameras. Those who are single, male, younger and with higher expenditures on telephone services are also more likely to acquire wireless services early. Early adopters in the business sector will likely be current users of cellular, paging, private mobile radio, and voice mail. In addition, they are likely to be drawn from larger establish- ments in business services.

Aron (1995) identifies four generic strategies for survival in the “wireless ice age”. These strategies have some overlap with those suggested by Porter (1980). They are:

Gaining competitive advantage in the U.S. wireless telephony market 169

(a) lowest cost service, offering acceptable quality at the lowest competitive cost, and thus being best able to meet commodity type price competition,

(b) focused product superiority, by providing superior value through product inno- vation and leadership,

(c) horizontal service integration, being able to offer a broad range of bundled mobility and non-mobility type services, e.g. local, long distance, wireless, video, internet, etc.

(d) superior customer relationships, by focusing on satisfying the customer, building long term relationships and thus reducing churn.

Based on the individual sources of advantage available to the firm, any one of these strategies may prove to be viable. We now discuss the marketing implications of these strategies in more depth.

The lowest cost provider does not need to focus as heavily on customers or innova- tive service, but on cost management. The firm’s size, economies of scale and infor- mation resources can provide comparative advantage. The segments for this strategy will clearly be the price-sensitive ones. Acceptable customer service will have to be provided. Products offered will be limited.

The focused product superiority strategy will involve continuous innovation in products and services. Strong brand equity will be needed to maintain its name in the marketplace. While relationship management will be important, product inno- vations will be key. For example, some firms could provide offer single number offerings, allowing the subscriber to give one number for callers to reach them any- time, anywhere. He or she can program the system to develop a calling protocol in case there is no answer. For example, it may say first try home, then office, then car and, finally, if there is no other option, revert to voice mail. User control will be enhanced by providing call management features. These will include call screening, call blocking, voice mail, and concierge type features in an integrated package. On the hardware side, multi-mode terminals that are able to function both with cellular and PCS networks could be marketed. Since 100% national coverage may not be a reality for several years for any one air interface standard, this feature may allow service providers to offer virtually seamless roaming from the first day. Indeed, a number of the carriers employing a particular technology standard (e.g. DCS 1900 operators) are signing memoranda of understanding with regard to roaming between markets.

Horizontal integration will need strategic alliances with other service providers and an in-depth understanding of the needs of the customers. Economies of scope will be critical here, as well as good information technology to integrate the various services into one bill, customer service, etc. Marketing personnel also will need to be well trained in diverse products and services. A key marketing challenge will be to decide which features and bundles are valuable for which segments at what prices, and to be able to provide it more efficiently than competitors.

As the competition intensifies, average air-time prices are bound to decline. Various pricing strategies may be relevant: lowest cost per minute, high fixed cost with low per minute cost, or no fixed cost with high per minute cost for emergency uses. In addition, we are likely to see “free” off-peak and bundled-in free minutes that are part of the basic monthly service charge. The challenge will be to provide value to the customer. For example, AT&T is considering offering flat-rate bundled prices for local, in-state long distance, and long distance services that will not have the usual peak off-peak rate structure. They may extend this to their cellular customers (Keller, 1996b). While

170 Manoj K. Agarwal and Barry E. Goodstadt

lower prices will not necessarily be a winning strategy, understanding the needs of the customers and what they value will help provide the needed features at the right price.

For some firms it will be possible to bundle various other services into a package price. Cable TV, seamless mobile telephony including voice and data, all at different prices, may be included in these packages. Firms can try to maximize profits on bun- dles rather than on each of the constituent services. For example, Sprint Spectrum could offer a deep discount on its PCS phone service and recoup its losses by better profitability on cable TV services (Hardy, 1996). Understanding the elasticities and cross-elasticities of demand at various prices will be critical to proper pricing. Market research methods like conjoint analysis and discrete choice analysis will be extremely useful in assessing these values (Bolton, 1994).

The superior customer relationship strategy requires an existing base of customers and strong marketing and customer care programs to maintain and grow the customer base. Superior training of personnel and delegation of authority to customer contact employees will be critical for delivering this superior service. A strong corporate culture and a good information technology infrastructure will help provide this superior cus- tomer relationship.

THE MARKETING CHALLENGE

The marketing landscape for mobile telephony is changing rapidly. Cellular opera- tors will have to quickly upgrade their marketing personnel and skills to be able to compete in this evolving environment. Old strategies that used to work in a relatively secure, duopoly market may no longer enable profitability. New PCS competitors will have to determine their strategic postures and fashion a marketing strategy to meet those goals. Three major marketing challenges will be: (a) to develop a compelling buying proposition beyond low price, (b) identifying and capturing distribution chan- nels, and (c) developing and maintaining brand equities.

The main marketing challenge in the near term will be one of defining the needs of different segments, differentiating the offerings competitively, and overcoming barriers associated with less-than-ideal services in the early years. We feel that creating brand equity, and providing bundled services to reduce churn in the market are going to be key ingredients in this new environment.

As the mobile telephony market becomes more broad-based, distribution will become key in the fight for survival and prosperity. Retail re-sellers who can provide information to potential subscribers have to be recruited. Companies may not have the time or the resources to establish in-house direct sales forces. Existing telemarketers may be used, perhaps with strategic alliances and equity participation, to provide wide coverage of the markets. Franchising opportunities may also arise.

One key to success in the market will be brand equity. With similar technology available to all players, it will be difficult to differentiate the services being offered. Brand equity may therefore emerge as a key to this market. Players with existing brand awareness will have to make much lower investments in entering mobile telephony. Newer firms with PCS licenses like PCS PrimeCo and American Portable Telecommu- nications will have the opportunity, albeit at a higher cost, to create and establish their unique brand image.

Given the changes in the wired and wireless telephony environment outlined above, the market will become extremely competitive in the next few years. The market opportunities are tremendous, but so are the challenges.

Gaining competitive advantage in the U.S. wireless telephony market

REFERENCES

171

Aaker, D. A. (1991). Managing Brand Equity: Capitalizing on the Value of a Brand Name. New York: Free Press.

Arnold, W. (1996). Cracking the Code. Wall Street Journal Reports. September 16, 1996, pp. R18. Aron, C. R. (1995). An Ice Age is Coming to the Wireless World. Communications and Electronics Industries

Consulting 1995 Thought Leadership Series. EDS Management Consulting Services. Bharadwaj, S. G., Rajan Varadarajan P., & Fahy, J. (1993). Sustainable Competitive Advantage in Service

Industries: A Conceptual Model and Research Propositions. Journal of Marketing, 57,4, 83-99. Bolton, R. N. (1994). Evaluating Pricing Strategies for New Residential Customer Services in the Telecom-

munications Industry. In R. R. Dholakia, (Ed.), Advances in Telecommunications Management (pp. 177- 196), 4, Jai Press Inc.

CTIA (1996). Cellular Technology Industry Association Statistics. Washington, D.C. Donaldson, Lufkin & Jenrette Securities Corporation (1996). The Wireless Communications Industry. New

York. Hardy, Q. (1996). Wireless Wagers. Wall Street Journal Reports, 1996, pp R18. Hemmady, J. G. (1995). Wireless Communication Services. In R. K. Heldman (Ed.), Telecommunications

Information Millennium: A Vision and Plan for the Global Information Society, McGraw Hill, 162-178. Hill, G. C. (1996). Its War. Wall Street Journal Reports, September 16, 1996, pp Rl. Keller, J. J. (1996a). Home Court. Wall Street Journal Reports, September 16, 1996, pp R4. Keller, J. J. (1996b). The New AT&T Faces Daunting Challenges. Wall Street Journal, September 19, 1996,

pp. Bl. Morgan Stanley and Company (1995). Telecommunications Services: Customer Preference Survey: Results

Say . . . Jump Ball!. Working Paper, Morgan Stanley and Company, NY. Naik, G. (1995). No Big Deal. Wall Street Journal, March 20, 1995, pp R16. PCIA (1995). PCIA 1995 PCS Technologies Market Demand Forecast Update. Personal Communications

Industry Association, Washington, D.C. Porter, M. (1980). Competitive Strategy: Techniques for Analyzing Industries and Competitors. New York,

Free Press. Schneiderman, R. (1994). Wireless Personal Communications: The Future of Talk. IEEE Press, Piscataway,

N.J.

Acknowledgement-We would like to thank Ruby Dholakia for her comments and suggestions.