Embed Size (px)

Citation preview

The financial services industry has experienced drastic changes over the past few years. The global financial crisis has resulted in massive government interventions, uncovered major frauds, and caused uncertainty among consumers, investors, intermediaries, and regulators. The failures of several significant financial institutions have put greater focus on the important role that prime brokers play in the primary capital markets and the importance of enhanced transparency, strong custody, and internal risk management controls at prime brokers. Financial regulation is a form of regulation or supervision, which subjects financial institutions to certain requirements, restrictions and guidelines, aiming to maintain the integrity of the financial system. This may be handled by either a government or non-government organization. So, financial systems of a country most probably strong player to react with such economic demolition like economic recession, financial crisis, inflation & deflation etc. In my Whole report I have tried to focus the financial structures of Bangladesh, the most common way to respond with financial motives with their terminologies.

A financial system is a system that to channels funds from lenders to borrowers, to create liquidity and money, to provide a payments mechanism, to provide financial services such as insurance and pensions and to offers portfolio adjustment facilities. A developed financial system is one that has a secure and efficient payment system, security market and financial intermediaries that arrange financing and derivative markets and financial institutions that provide access to risk management instruments.

The present structure of the financial system in Bangladesh comprises of various types of banks, insurance companies, and non-bank financial institutions. Bangladesh Bank is at the top of the banking system and is accountable for assuring prudential administration and central banking activities for all types of banks operating within the banking industry. On the other hand, the Securities and Exchange Commission (SEC) of Bangladesh is the regulatory body for stock-market related activities.

The Financial System in Bangladesh

Abstract

The financial system of Bangladesh is comprised of three broad fragmented sectors:

Financial System in Bangladesh

Formal Sector Semi Formal Informal Sector

Financial Market Regulators & Institution

Money Market (Banks, NBFIs,Primary

Dealers)

Capital Market (Investment banks, Stock Exchanges, Credit Rating

Companies etc.)

Foreign Exchange Market

(Authorized Dealers)

Bangladesh Bank (Central Bank)

Banks47 scheduled & 4 non-

scheduled banks

NBFIs31 NBFIs

Insurance Development & Regulatory Authority

(Insurance Authority)

Insurance Companies18 Life and 44 Non-Life Insurance

Companies

Securities & Exchange Commission (Regulatory of capital market Intermediaries)

Stock Exchanges, Stock Dealers & Brokers, Merchants Banks, AMC s,

Credit Rating Agencies etc.

Microcredit Regulatory Authority (MFI Authority)

Micro Finance Institutions 599 MFIs

Specialized Financial Institutions

1. House Building Financial Corporation (HBFC)

2. Palli Karma Sahayak Foundation (PKSF)

3. Samabay bank

4. Grameen Bank

The sectors have been categorized in accordance with their degree of regulation.The formal sector includes all regulated institutions like Banks, Non-Bank Financial Institutions (FIs), Insurance Companies, Capital Market Intermediaries like Brokerage Houses, Merchant Banks etc Micro Finance Institutions (MFIs). It includes financial market and Regulators & Institution.

The financial market in Bangladesh is mainly of following types:

Money Market : The primary money market is comprised of banks, FIs and primary dealers as intermediaries and savings & lending instruments, treasury bills as instruments. There are currently 15 primary dealers (12 banks and 3 FIs) in Bangladesh. The only active secondary market is overnight call money market which is participated by the scheduled banks and FIs. The money market in Bangladesh is regulated by Bangladesh Bank (BB), the Central Bank of Bangladesh.

Capital market: The primary segment of capital market is operated through private and public offering of equity and bond instruments. The secondary segment of capital market is institutionalized by two (02) stock exchanges-Dhaka Stock Exchange and Chittagong Stock Exchange. The instruments in these exchanges are equity securities (shares), debentures, corporate bonds and treasury bonds. The capital market in Bangladesh is governed by Securities and Commission (SEC).

Foreign Exchange Market : In the foreign exchange market banks are free to buy and sale foreign currency in the spot and also in the forward markets. However, to avoid any unusual volatility in the exchange rate, Bangladesh Bank, the regulator of foreign exchange market remains vigilant over the developments in the foreign exchange market and intervenes by buying and selling foreign currencies whenever it deems necessary to maintain stability in the foreign exchange market.

Formal Sector

Financial Market

Central bank

Bangladesh Bank,

Head Office: Motijheel, Dhaka-1000 Tele: 7125850-79, 7126280-95 7126101-20 Fax: 880-2-9566212

Pursuant to Bangladesh Bank Order, 1972 the Government of Bangladesh reorganized the Dhaka branch of the State Bank of Pakistan as the central bank of the country, and named it Bangladesh Bank with retrospective effect from 16 December 1971.

BanksAfter the independence, banking industry in Bangladesh started its journey with 6 nationalized commercialized banks, 2 State owned specialized banks and 3 Foreign Banks. In the 1980s banking industry achieved significant expansion with the entrance of private banks. Now, banks in Bangladesh are primarily of two types:

Scheduled Banks: The banks which get license to operate under Bank Company Act, 1991 (Amended in 2003) are termed as Scheduled Banks. State-owned commercial banks, private commercial banks, Islamic commercial banks, foreign commercial banks and some specialized banks are Scheduled Banks.

State-owned are functioning as nationalist. Here is the list -

1. Sonali bank Limited www.sonalibank.com.bd

Head office: 35-42, 44 Motijheel Commercial Area, Dhaka-1000

2. Rupali bank Limited www.rupalibank.org

Head office: Computer division, 9th floor, 34 Dilkusha C/A, Dhaka1000

3. Agrani Bank Limited www.agranibank.org

Head Office: Motijheel Dhaka-1000 Tele: 9566153-4, Fax: 9563662, 9563658

4. Janata Bank Limited www.janatabank-bd.com

Head Office: Motijheel, Dhaka-1000

REGULATORS

&

INSITUTION

Private Banks are the highest growth sector due to the dismal performances of government banks (above). They tend to offer better service and products. Here is the list -

1. Uttara Bank Limited www.uttarabank-bd.com

Head Office: 90 Motijheel C/A Dhaka-1000

2. Mutual Trust Bank Limited www.mutualtrustbank.com

Head Office: Ispahani Bhaban 23 Dilkusha C/A, Dhaka-1223

3. Dhaka Bank Limited www.dhakabankltd.com

Head office: Biman Bhaban(1st floor), Motijheel C/A, Dhaka-1000

4. Eastern Bank Limited www.ebl-bd.com

Jiban Bima Bhaban10, Dilkusha C/A, Dhaka 100

5. Dutch Bangla Bank Limited www.dutchbanglabank.com

Head Office: 1, Dilkusha C/A Dhaka-1223

6. Pubali Bank Limited www.pubalibangla.com

Head Office: 26 Dilkusha C/A, Dhaka-1223

7. IFIC Bank Limited www.ificbank.com.bd

Head office: 8, Rajuk Avenue, Dhaka-1000

8. National Bank Limited www.nblbd.com

Head Office: 18, Dilkusha C/A, Dhaka-1223

9. The City Bank Limited www.thecitybank.com.bd

Private Commercial Bank

10. NCC Bank Limited www.nccbank.com.bd

Head Office: 7-8, Motijheel C/A, Dhaka-1000

11. Mercantile Bank Limited www.mblbd.com

Head office: 61, Dilkusha C/A, Dhaka-1223

12. Prime Bank Limited www.primebank.com.bd

Head Offiice: Adamjee Court 119-120, Motijheel C/ADhaka-1000

13. Southeast Bank Limited www.southeastbank.com.bd

Head Off.: 1, Dilkusha C/A (Floor 3), Dhaka-1223

14. Standard Bank Limited www.standardbankbd.com

Head Office: 19, Dilkusha C/A (Fl. 7), Dhaka-1223

15. One Bank Limited www.onebankbd.com

Head office: Zaman Court 45, Dilkusha C/A, Dhaka-1223

16. Bangladesh Commerce Bank Limited www.bcblbd.com

17. The Premier Bank Limited www.premierbankltd.com

Head Offiice: Iqbal Centre, 42, Kamal Ataturk Avenue, Banani, Dhaka-1213

18. Bank Asia Limited www.bankasia-bd.com

Head office: Rangs Bhaban (Floor 112-116, Old Airport Road, Dhaka-1215

19. Trust Bank Limited www.trustbank.com.bd

Head office: Building No-98, Principal Rd. Dhaka Cantonment, Dhaka

20. Jamuna Bank Limited www.jamunabankbd.com

21. AB Bank Limited www.abbl.com

22. NRB Commercial Bank Limited www.nrbcommercialbank.com

23. NRB Bank Limited www.nrbbankbd.com

24. Meghna Bank Limited www.meghnabank.com.bd

25. Farmers Bank Limited www.famersbanklimited.com

26. Modhumoti Bank Limited www.modhumotbankltd.com

27. South Bangla Agriculture and Commerce Bank Ltd www.sbacbank.com

28. Midland Bank Limited www.midlandbankbd.net

29. United Commercial Bank Ltd www.ucbl.com

30. BRAC Bank Limited www.bracbank.com

1. 1. Islami Bank Bangladesh Limited www.islamibankbd.com

Head office: 71, Dilkusha C/A, Dhaka-1223

2. Shahjalal islami bank Limited www.shahajalalbank.com.bd

Head office: 58, Dilkusha C/A, Dhaka-1223

3. First Security Islami Bank Limited www.fsiblbd.com

Head Office: 23, Dilkusha C/A, Dhaka-1223

4. Export Import Bank of Bangladesh Limited www.eximbd.com

Head Office: Printers Building5, Rajuk Avenue, Dhaka-100

5. Al-Arafah Islami Bank Limited www.al-arafahbank.com

Rahman Mansion 161, Motijheel C/A, Dhaka-1000

6. Social Islami Bank Limited www.siblbd.com

7. ICB Islamic Bank www.icbislamic-bd.com

8. Union Bank Limited www.unionbank.com.bd

There are 8 Islamic Commercial Banks

1. Citibank NA www.asia.citibank.com/bangladesh/corporate

2. HSBC www.hsbc.com.bd

3. Standard Chartered Bank www.standardchartered.com.bd

4. Commercial Bank of Ceylon www.combank.net

5. State Bank of India www.sbibd.com

6. Habib Bank Limited www.hbl.com/bangladesh

7. National Bank of Pakistan www.npb-bd.com

8. Woori Bank www.bd.wooribank.com

9. Bank Alfalah www.bankalfalah.com

4 specialized banks are now operating which were established for specific objectives like agricultural or industrial development. These banks are also fully or majorly owned by the Government of Bangladesh.

1. . Bangladesh Krishi Bank www.krishibank.org.bd

Head Office: Krishi Bhaban, 83-84, Motijheel, Dhaka-1000

2. Rajshahi Krishi Unnayan Bank www.rkub.org.bd

These are 9 foreign commercial banks are operating in Bangladesh

Specialized Banks

3. Bangladesh Development Bank Ltd www.bdbl.com.bd

Head office: Amin Court, 62-63, Motijheel, Dhaka-1000

4. BASIC Bank Limited www.basicbanklimited.com

Head Office: 7-8 Motijheel C/A, Dhaka-1000

The banks which are established for special and definite objective and operate under the acts that are enacted for meeting up those objectives, are termed as Non-Scheduled Banks. These banks cannot perform all functions of scheduled banks.

1. Grameen Bank

Head Office: Mirpur-2, Dhaka

2. Probashi Kallyan Bank

3. Karmasangsthan Bank

4. Progoti Co-operative Land Development Bank Limited (progoti Bank) and

5. Answer VDP Unnayan Bank

Non-banking financial institutions, which are not, banks. These institutions cannot perform all functions of banks, which get license to operate under Financial Institution Act, 1993 are termed as Non-banking financial institutions. Here are list of non-banking financial institution.

1. Uttara Finance and Investments Limited2. United Leasing Company Limited (ULCL)3. Union Capital Limited4. The UAE-Bangladesh Investment Co. Ltd5. Saudi-Bangladesh Industrial & Agricultural Investment Company Limited (SABINCO)6. Reliance Finance Limited7. Prime Finance & Investment Ltd8. Premier Leasing & Finance Limited9. Phoenix Finance and Investments Limited

Non-Scheduled Banks

10. People's Leasing and Financial Services Ltd11. National Housing Finance and Investments Limited12. National Finance Ltd13. MIDAS Financing Ltd. (MFL)14. LankaBangla Finance Ltd.15. Islamic Finance and Investment Limited16. International Leasing and Financial Services Limited17. Infrastructure Development Company Limited (IDCOL)18. Industrial Promotion and Development Company of Bangladesh Limited(IPDC)19. Industrial and Infrastructure Development Finance Company (IIDFC) Limited20. IDLC Finance Limited21. Hajj Finance Company Limited22. GSP Finance Company (Bangladesh) Limited (GSPB)23. First Lease Finance & Investment Ltd.24. FAS Finance & Investment Limited25. Fareast Finance & Investment Limited26. Delta Brac Housing Finance Corporation Ltd. (DBH)27. Bay Leasing & Investment Limited28. Bangladesh Industrial Finance Company Limited (BIFC)29. Bangladesh Finance & Investment Co. Ltd.

30. Agrani SME Finance Co. Ltd.

Here are18 Life Insurance Company of Bangladesh

1.American Life Insurance Co.Alico Building18-20, Motijheel C/ADhaka-1000Tele: 9561791Fax:880-2-9558682, 9558683

2. Popular Life Insurance Co. Ltd.9/E, Motijheel C/ADhaka-1000Tele: 9554058, 9570696Fax: 9564795

3. Jiban Bima Corporation24, Motijheel C/ADhaka-1000Tele: 9551414, 9551423-24Fax: 880-2-9561325

4. Delta Life Insurance Co. Ltd.Uttara Bank Bhaban90-91 Motijheel C/ADhaka-1000Fax: 880-2-9562219

5. Shandhani Life Insurance Co. Ltd.Taranga Complex19, Rajuk AvenueDhaka-1000Fax: 880-2-9554847

6. Meghna Life Insurance Co. Ltd.Biman Bhaban100, Motijheel C/ADhaka-1000.Fax: 880-2-9555802

7. Pragati Life Insurance Co. Ltd.Uttara Bank Bhaban90-91 Motijheel C/ADhaka-1000Tele: 7113243-45Fax: 880-2-7113249

8. Padma Life Insurance Co. Ltd.Rupali Bima Bhaban7, Rajuk Avenue (Floor-10)Dhaka-1000Tele: 7110816

Insurance Development & Regulatory Authority

Here are 44 Non life insurance companies list

9. Sunlife Insurance Co. Ltd.BTA Tower (12th fl.)29 Kemal Ataturk AvenueRoad # 17, Banani C/ADhaka – 1213Phone: 9887511, 9892983

10. Prime Life Insurance Co. Ltd.29, Dilkusha C/ADhaka-1223 Tele: 956088911. National Life Insurance CO. LTD.

N.L.I. Tower, 54, Kazi Nazrul Islam Avenue, Karwan Bazar, Dhaka-1215, Bangladesh Phone : PABX-8158171, 8158189, 8158190. Fax: 88-02-8144237.

12. Progressive Life Insurance Company LtdNational Scout Bhaban (4th,5th,6th,7th & 11th Floor), 70/1 Inner Circular Road, Kakrail, Dhaka-1000. Fax: 880-2-8315373

13. Rupali Life Insurance Co. Ltd.Rupali Bima Bhaban, 7 Rajuk Avenue,Dhaka-1000Tel: 9565628

14. Jamuna Life Insurance Co. Ltd.15. Baira Life Insurance Company Ltd.16. Farest Islami life Insurance co. Ltd.17. Golden Life Insurance Ltd.18. Homeland Life Insurance Company Ltd.

1. Bangladesh Co-Operative Insurance Ltd. no siteSena Kalyan Bhaban, 195, Motijheel C/A, Dhaka- 1000Tel: 9561121, 9555645

2. Bangladesh Genaral Insurance Co. Ltd.42, Dilkusha C/A, Dhaka-1000.Tel: 9550379, 9564213

3. Bangladesh National Insurance Co. Ltd 21, Rajuk Avenue, Motijheel C/A,Dhaka-1000.Tel: 9559547

4. Central Insurance Co. Ltd. no siteUttara Bank Bhaban, 90-91, Motijheel C/A, Dhaka-1000.Tel: 9560254, 9567421-2

5. City General Insurance Co. Ltd.Baitul Hossain Building (3rd Floor), 27, Dilkusha C/A, Dhaka- 1000Tel: 9564033

6. Eastern Insurance Co. Ltd.44, Dilkusha C/A, Dhaka-1000.Tel: 9552759, 9563033-4

7. Eastland Insurance Co. Ltd.13, Dilkusha C/A, Dhaka-1000.Tel: 9563928, 9560048-9

8. Express Insurance Ltd.58 Dilkusha C/A (2nd Floor)Dhaka 1000, Bangladesh. Phone: 88-02-9552672, 9569546 Fax: 880-2-9568616

9. Federal Insurance Co. Ltd.122-124, Motijheel C/A, Dhaka-1000.Tel: 9562877, 9560003-4

10. Green Delta Insurance Co. Ltd.Hadi Mansion (4th Floor), 2, Dilkusha C/A, Dhaka-1000.Tel: 9552188, 9560005-6

11. Janata Insurance Co. Ltd.125, Motijheel C/A, Dhaka-1000.Tel: 9560141, 9563438

12. Karnaphuli Insurance Co. Ltd.Sena Kallyan Bhaban, 195, Motijheel C/A, Dhaka-1000.Tel: 9561150, 9564808-9

13. Mercantile Insurance Company Ltd.61, Motijheel C/A, Dhaka- 1000Tel: 9557662-4, 9557665

14. Meghna Insurance Co. Ltd.73, Motijheel C/A, Dhaka- 1000Tel: 9554989, 9557796

15. Northern General Insurance Co. Ltd.128, Motijheel C/A, Malek Mansion (2nd Floor), Dhaka-1000.Tel: 9559077

16. Paramount Insurance Company LimitedSummit Centre (3rd floor)18, Kawran Bazar C/A. Dhaka-1215, BangladeshPhone :- 8118982, 9137554, 8127189, 9144346

17. People's Insurance Co. Ltd.Senakalyan Bhaban, 195, Motijheel C/A, Dhaka-1000.Tel: 9564797-8

18. Phoenix Insurance Co. Ltd.Purbani Annexe Building, 1/A, Dilkusha C.A, Dhaka 1000Tel: 9563608

19. Pioneer Insurance Co. LtdJiban Bima Tower,(6th floor), 10 Dilkusha C.A.,Dhaka 1000Tel: 9557674-5

20. Pragati Insurance LimitedUttara Bank Bhaban, 90-91, Motijheel C/A, Dhaka-1000.Tel: 9561385

21. Prime Insurance Company Ltd.63 Dilkusha C.A., Dhaka 1000Tel: 9552742

22. Provati Insurance Co.Ltd.Khan Mansion, (11th floor), 107 Motijheel C.A, Dhaka 1000Tel: 9559561-3

23. Purabi General Insurance Co. Ltd.23 Motijheel C.A., Dhaka- 1000Tel: 9566006-7

24. Reliance Insurance LimitedBSB Building, 8 Rajuk Avenue, Dhaka-1000.Tel: 9560105-6

25. Rupali Insurance Co. LtdRupali Bima Bhaban, 7 Rajuk Avenue,Dhaka-1000Tel: 9565628

26. Sadharan Bima Corporation 33, Dilkusha C/A, Dhaka-1000.

27. United Insurance Co. Ltd.Camellia House, 22 Kazi Nazrul Islam Avenue, Dhaka-1000Tel: 862159

28. Agrani Insurance Company Ltd29. Asia Insurance Ltd30. Asia pacific Gen Insurance Company Ltd31. Bangladesh National Insurance Company Ltd32. Central Insurance Company Ltd33. Islami Insurance Bangladesh Ltd.34. Crystal Insurance Company Ltd35. Desh Gen. Insurance Company Ltd

35. Global Insurance36. Islami Commercial Insurance co. Ltd37. Nitol Insurance Company Ltd38. Peoples Insurance Company Ltd39. Pramount Insurance Company Ltd40. Republic Insurance Company Ltd41. Takaful Islami Insurance Ltd.42. Union Insurance Company Ltd

At a time when the financial sector needs further consolidation and tight supervision, the government has issued license for 11 insurance companies. There have nine life & two general insurance companies.

New insurance companies1. Sonali Life Insurance, 7. Mercantile Islami Life Insurance,2. Taiyo Summit Life Insurance, 8. NRB Global Life Insurance,3. Protective Life Insurance, 9. Guardian Life Insurance,4. Chartered Life Insurance, 10. Best Life Insurance,5. Zenith Islami Life Insurance, 11. Sikder General Insurance Company and,6. Sena Kalyan General Insurance Company.

The Bangladesh Securities and Exchange Commission (BSEC) is the regulator of the capital market of Bangladesh, comprising Dhaka Stock Exchange and Chittagong Stock Exchange (CSE).

The commission is statutory body and attached to the Ministry of Finance.

SECURITIES & EXCHANGE

COMMISSION

(REGULATORY OF CAPITAL

MARKET INTERMEDIAR

IES)

Newly Licensed Insurance

Companies

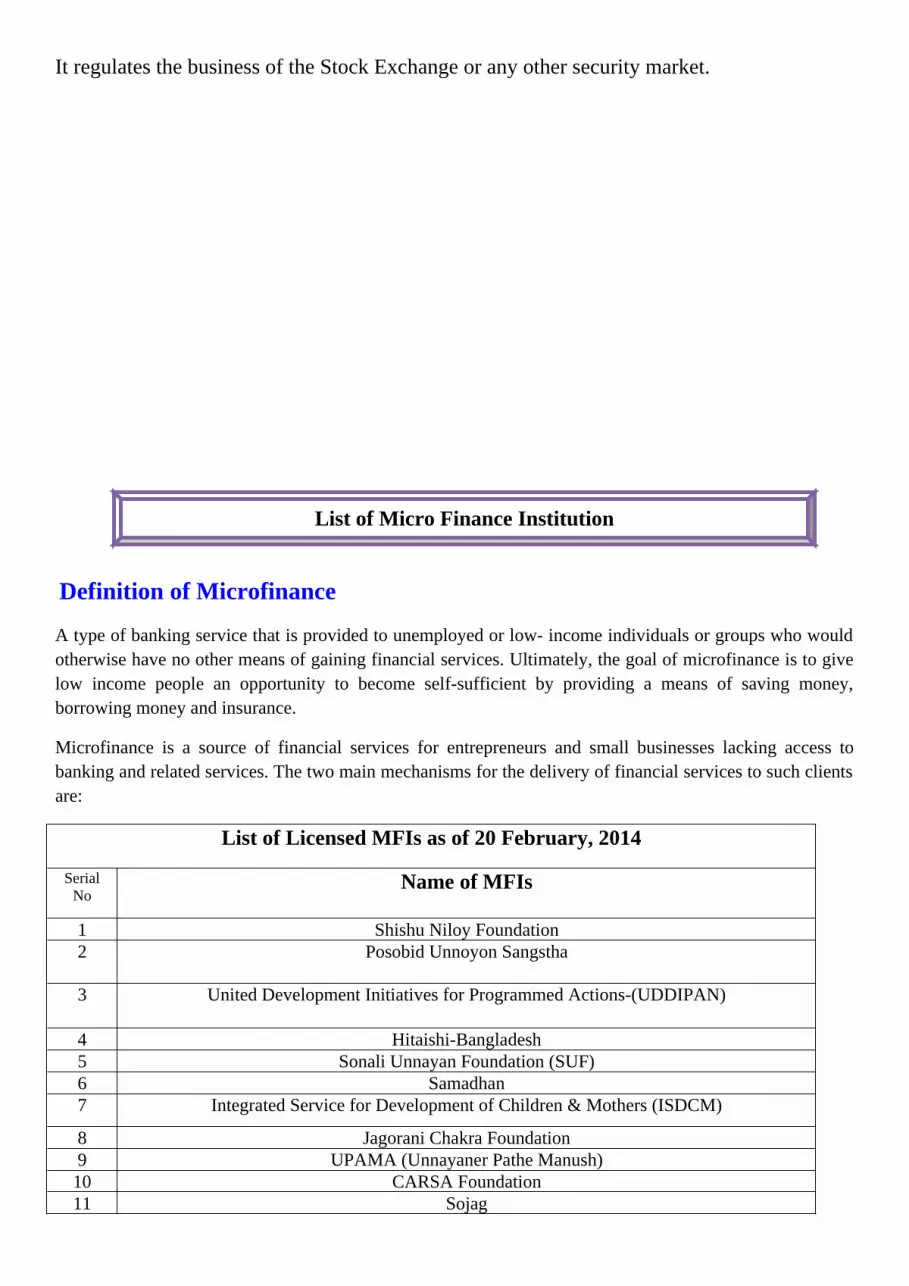

It regulates the business of the Stock Exchange or any other security market.

Definition of Microfinance

A type of banking service that is provided to unemployed or low- income individuals or groups who would otherwise have no other means of gaining financial services. Ultimately, the goal of microfinance is to give low income people an opportunity to become self-sufficient by providing a means of saving money, borrowing money and insurance.

Microfinance is a source of financial services for entrepreneurs and small businesses lacking access to banking and related services. The two main mechanisms for the delivery of financial services to such clients are:

List of Licensed MFIs as of 20 February, 2014

Serial No

Name of MFIs

1 Shishu Niloy Foundation2 Posobid Unnoyon Sangstha

3 United Development Initiatives for Programmed Actions-(UDDIPAN)

4 Hitaishi-Bangladesh5 Sonali Unnayan Foundation (SUF)6 Samadhan7 Integrated Service for Development of Children & Mothers (ISDCM)

8 Jagorani Chakra Foundation9 UPAMA (Unnayaner Pathe Manush)10 CARSA Foundation11 Sojag

List of Micro Finance Institution

12 Bajitpur Rural Advancement Society (BRAS)13 Charcha14 Social Upliftment Society (SUS)15 Grameen Unnayan Sangstha (GUS)16 BEDO17 Village Education Resource Center18 Shakti Foundation for Disadvataged women19 Bridge M.F.I

20 Prottoy Unnyan Sangstha21 Dabi Moulik Unnayan Sangstha22 Wave Foundation23 Development Initative for Social Advancement (DISA)24 Society for Social Service (SSS)25 Rural Reconstruction Foundation26 DRISHTIDAN27 Page Development Centre

28 Bangladesh Association of Women for Self Empowrment (BAWSE)

29 ENDEAVOUR(Ensure Development Activities for Vulnerable Under Privileged Rural People )

The semi-formal sector includes those institutions which are regulated otherwise but do not fall under the jurisdiction of Central Bank, Insurance Authority, Securities and Exchange Commission or any other enacted financial regulator. This sector is mainly represented by Specialized Financial Institutions like House Building Finance Corporation (HBFC), Palli Karma Sahayak Foundation (PKSF), Samabay Bank, Grameen Bank etc., Non-Governmental Organizations (NGOs and discrete government programs.

The informal sector includes private intermediaries which are completely unregulated.

Before liberation of Bangladesh, the banking and finance industries in erstwhile East Pakistan was owned and controlled by erstwhile West Pakistani owners. Bangladesh inherited a narrow and thin financial sector with six commercial banks which were nationalized, a few foreign banks and two Govt. owned specialized financial institutions. The banking system was operating until the end of 1980s with the directives of monetary authorities aiming at achieving objectives of supplying cheap money to the State Owned Enterprises (SOEs) and priority sector like Agriculture, Export and Small and Cottage Industries in the private sector. The two important instruments at the armory of monetary authority to execute monetary

Informal Sector

Semi formal sector

Criticism of Financial institutions:

policy was selective credit control measures and administered interest rate. One consequence of Central Bank’s regulated deposit and lending rates at that time without consideration of market clearing rate was that in real terms, interest rates appeared to be negative in view of high rates of inflation during the mid-70s and up to the end of 1980s. The policy of arbitrarily fixed low interest rate brought about undesirable consequences of distortion in allocation of resources between different sectors. Consequently, the financial interrelations ratio (Goldsmith, 1969) measured in terms of ratio of total financial assets to National Wealth remained abysmally low in Bangladesh ranging between 10%-20% between 1973-1983 compared to 40% - 65% in Pakistan, India, Sri Lanka, Thailand, Philippines and Malaysia (IMF Financial Statistics, 1980 - 1984). During the decade up to mid-1980, the banking sector was characterized by a ”financially repressed” regime scenario of low interest rate, distortion in resource allocation, low rate of savings leading to financial disintermediation and the financial sector was being used to service the need of the Govt. sector and a few business houses with concomitant consequence of shallow financial system. The demand management aspect of macro-economic variables was not taken care of. The loanable fund at the disposal of the banks were disbursed mostly in publicly directed sectors without commercial consideration. The internal control system of commercial banks was weak, the books of accounts did never reflect the actual financial health of the banks, the quality of assets of the banks was never evaluated on strict accounting principles, the MIS was virtually non-existent in the banking sector, profitability and liquidity aspect of portfolio management was unfamiliar concept among the management personnel, the elements of capital adequacy for banking operation were never given due weightage. The pervasive weakness in the money market was observed in the capital market also. The only stock exchange of the country, namely the Dhaka Stock Exchange was almost inoperative with only a few enlisted companies. Bangladesh Shilpa Bank (BSB) & Bangladesh Shilpa Rin Shangastha (BSRS) were financing projects out of loans from IDA, ADB credit lines to projects which were hardly appraised from the point of view of cost benefit analysis. Cumulative effect of mismanagement in money and capital market led to huge accumulation of non-performing loans for our financial sector which has risen to about 40% - 42% of the total advances of our banking sector in recent period. The total scenario of financial sectors was in a state of disarray. Hence the need for overhauling of the financial sector was felt and in order to bring about structural, institutional and policy changes in the fragile financial sector, a National Commission of Money, Banking and Credit was constituted in 1984. The Commission submitted report to the Govt. in 1986 identifying the problem areas in our financial sector with specific recommendations to bring about the structural, institutional, policy and legal reforms. Accordingly, the Financial Sector Reforms Project (FSRP) was launched in 1990 under Financial Sector Adjustment Credit of IDA the 1st phase of which was completed in June, 1996. The financial sector reform has become a continuous process which is being carried out in its second phase under the style of commercial banks restructuring project. Moreover, like almost every country of Asia, Bangladesh has committed to introduce market forces into its financial system - but slowly, so as not to make bankrupt borrowers, destabilize lenders, displace workers or otherwise upset the established order of things. The crises of 1997 which began in the foreign exchange market and spread quickly through the banking sector of most of the Asian countries challenged the slow moving style of reform. As such although Bangladesh has not been directly affected by the recent financial turmoil of Asian tigers, yet the financial reform heads the agenda of the present Government. Accordingly the Government has constituted a Bank Reform Committee with an eminent economist of the country as chairman, along with experienced professional bankers as members including the Governor of Bangladesh Bank to make pragmatic recommendations to overhaul and strengthen the fragile financial sector of the country.

Conclusion