Embed Size (px)

Citation preview

Migrant Workers and the Financial Services Sector in Ireland

A preliminary report from the Migrant Careers and Aspirations research project

Justyna Salamonska, Elaine Moriarty, James Wickham, Alicja Bobek

Trinity Immigration Initiative

10 June, 2008

Trinity Immigration Initiative Trinity College Dublin

Employment Research Centre Trinity College Dublin

Contents

List of Tables ..........................................................................................................2

List of Charts..........................................................................................................2

Introduction............................................................................................................3

An Overview of the Financial Services Sector in Ireland ..................................4

Employment in the Financial Services Sector: The Role of Migrants ..............6 Migrants and Employment...........................................................................6 Nationality and Gender ................................................................................7 Occupational Structure and Education.........................................................8 Earnings, Gender and Nationality..............................................................11 Age, Nationality and Gender .....................................................................13 Trade Union Membership ..........................................................................14

Issues for Research: Employers’ Strategies and Migrants’ Careers ..............16 Employers’ Strategies: Issues for Research...............................................16

Regulation and Recruitment ..........................................................16 Skills Shortages and Potential Employment ..................................17 Soft Skills.......................................................................................17 Turnover and Retention of Workers ..............................................18

Employees’ Careers and Aspirations: Issues for research .........................19 Geographical Mobility of Migrants ...............................................19 Qualifications and Opportunities ...................................................20 Job or Career? ................................................................................20

References.............................................................................................................22 Appendix: Statistical Sources ...............................................................................24

1

List of Tables Table 1 Employment and Nationality in Banking and Financial Services 2006 .....7 Table 2 Nationality and Gender 2006 ......................................................................7 Table 3 Employment, Gender and Geographical Location 2006.............................8 Table 4 Occupational Structure 2007.......................................................................8 Table 5 Education 2001, 2006 .................................................................................9 Table 6 Third Level Education 2006 .......................................................................9 Table 7 Occupational Groups 2006 .......................................................................10 Table 8 Occupation, Gender and Nationality 2006................................................11 Table 9 Earnings, Gender and Nationality 2003, 2006..........................................12 Table 10 Earnings, Hours Worked and Nationality 2006........................................12 Table 11 Age and Nationality, 2006 ........................................................................13 Table 12 Age, Nationality and Gender, 2006 ..........................................................14 Table 13 Trade Union Membership 2001, 2006 ......................................................14 Table 14 Trade Union Membership, Gender and Nationality 2006 ........................15 List of Charts Chart 1 Occupation, Wage Dispersion 2005, 2007 ...............................................13

2

Introduction The financial services sector in Ireland employed almost 85,000 workers in 2006 which accounted for 4% of the total workforce in Ireland (C.S.O. 2006). The number of immigrants1 active in this sector is low at 6,525 employees, representing 8% of the labour force in financial services, which is a smaller share than immigrant employment in the Irish economy as a whole (12%).

However, the financial services sector remains an interesting area to study as the sector provides an overview of migrant employment in a plethora of occupational positions, from high-skilled and well paid to low-skilled and poorly remunerated jobs. Existing literature tends to focus on the high-skilled work force in the sector, overlooking the vast area of low-skilled and low-paid jobs that compose an important part of employment in the financial services sector in Ireland.

This report is the second in a series of sectoral reports compiled by the Migrant Careers and Aspirations (MCA) project, one of six projects within the research programme of the Trinity Immigration Initiative. These reports seek to examine the situation of migrant workers in different sectors of the Irish economy. We are particularly interested in evaluating the significance of accession state nationals to particular sectors of the Irish economy which contribute background and context to the core aspect of the MCA project, namely, a longitudinal study of Polish workers who have migrated to Ireland and are active in the labour market.

The report is based primarily on secondary data analysis of relevant and available statistical sources and an overview of existing literature. In addition, six employees working in the sector and a number of key stakeholders were interviewed for the report.

The report begins with an overview of the financial services sector in Ireland followed by an analysis of relevant data on employment in the sector. Finally, it sketches the research issues concerning employers’ strategies and migrant careers and aspirations in the financial services sector in Ireland.

1 In this report we use the terms ‘immigrants’, ‘migrants’ and ‘other nationalities’ inter-changeably. This simply reflects the practice of the Central Statistics Office and other official statistical accounts of the contemporary Irish labour market. For these purposes someone living in Ireland for thirty years with UK citizenship and someone arriving yesterday from Poland are both ‘immigrants’; an Irish citizen returning from the USA after an absence of thirty years and a naturalised arrival from Nigeria are both defined as ‘Irish’. The terms have nothing to do with ‘ethnicity’ or ‘ethnic origin’ as used in many other national censuses such as that of the UK.

3

An Overview of the Financial Services Sector in Ireland The financial services sector as we discuss it in this report includes banking and financial services, insurance and pension funds companies and activities auxiliary to banking and financial services (or financial intermediation as the sector is defined by the Central Statistics Office). Depending on the data sources being reviewed, these categorisations will be used interchangeably.

There are a number of employer and employee representative organisations concerned with employment and migration issues with regard to financial services in Ireland, including the Irish Banking Officials Associations (IBOA), the Irish Bankers Federation (IBF) and the Irish Insurance Federation (IIF).

An overview of the financial services sector in Ireland needs to take into account the fact that

…financial markets and the associated institutions differ from national economies: financial markets tend to be global markets, and the financial system can arguably be considered a global system (Knorr Cetina and Preda, 2005: 5). Such an understanding requires consideration of developments at a number of

levels. Firstly, it is widely accepted that the global financial services industry has lost a level of momentum due to the current global credit crunch (Soros, 2008). Secondly, the global financial market is affected by privatisation and deregulation which can be particularly observed at European level (Webster, 2001: 2). Finally, the specificities of the national state structure plays a key role in enabling a particular environment for financial services development.

Liberalisation of the market at EU level has opened up opportunities for non-domestic businesses and the transnational supply of financial services (Webster, 2001). Deregulation has been driven by state authorities interested in reducing the number of regulations financial services are subject to, with the exception of security regulations. Such deregulation has, however, been ratified and reinforced at EU level. The integration of European financial markets and financial services is an illustration of such trends. In 1999, the EU Commission launched The Financial Services Action Plan with the objective of creating a single financial services market within the EU.

However, single state regulation is not without significance and the creation of the International Financial Services Centre (IFSC) in Dublin in 1987 is a good example of such state influence. Since the early 1990s, Ireland has developed a reputation as a leading global financial services centre. Dublin has, in fact, been ranked 13th in the Global Financial Centres Index (City of London, 2007). It is estimated that there are approximately 450 international institutions operating from Ireland, representing more than half of the top 50 global financial companies which offer a vast range of financial services including fund/asset management, banking and insurance (Deloitte, 2004: 28). Many of the top global financial services companies have chosen to locate in Ireland including Citigroup, JP Morgan Chase, ABN AMRO and Merrill Lynch amongst others.

Varying reasons have been put forward to explain the attraction for such global institutions including an attractive fiscal and regulatory environment, the availability of a highly skilled educated population (IDA, 2004), strategic location to world markets, English language capacity, consensus governance which facilitated wage restraint and industrial relations stability (EGFSN, 2007). However, Sokol argues that Dublin’s IFSC can be described as a “glorified back office” (Murphy 1998 cited in Sokol, 2007: 247) or “enclave economy” (White 2005 cited in Sokol, 2007: 247).

4

Employment within the IFSC is compared with that within domestic banking “for which Dublin serves as a base for sophisticated head office operations” (Sokol, 2007: 247).

Regardless of such debates, the size and importance of the financial services sector to the Irish economy, with €1.2 trillion in banking assets alone in 2006 compared to €422 billion in 2001 and insurance business worth €15 billion (Expert Group on Future Skills Needs, 2007: 37), is considered crucial. This expansion has impacted on firstly, the employment growth within the sector as we will examine in the next section and secondly, the structural composition of the sector.

With the transformation of the financial services sector (Webster, 2001), defining banking becomes more challenging as the banks take up activities that were not traditionally their core area of business (like mortgages, insurances, etc.) (Sokol, 2007: 236). In Ireland, there are three main types of activity: global organisations which have a dominant presence in their own local markets but with a large presence overseas (Citigroup, JP Morgan Chase, HSBC); local/niche organisations which have a strong presence in their own local markets with a limited presence overseas (Allied Irish Bank, Bank of Ireland); new entrants to the market, which include non financial services organisations who specialise in a single product strategy such as credit cards (Virgin, Tesco) which this report will not be focusing on.

Each of these business types has a variety of what Sokol (2007: 237) refers to as delivery channels, namely, branch-based networks, agent networks and branch-less banking. These new forms of business have generated new firm practices including decentralisation, consolidation, the widespread use of ICTs and internet banking. Such developments have had a particular influence on “the organisation of work within firms and for the working lives of financial services employees” (Webster, 2001: 2) as we will discuss later in the report.

On the one hand, the fiscal environment continues to retain its reputation as relatively favourable, and the Building on Success report (CHG, 2006) highlighted Ireland’s potential to be

…a major player in international financial services focused on niche opportunities, recognised as being a world class location for innovation and transaction execution by leveraging key competitive strengths (CHG, 2006: ).

On the other hand, concerns have been expressed around a number of issues. These include the cost of skilled labour, the availability of appropriately educated graduates, the development of specialist knowledge in certain disciplines, an attractive living and working environment and obtaining work permits were also essential to both retaining Ireland’s competitive position globally and enhancing it to reach Ireland’s potential as outlined.

A recent EGFSN report (2007) which was commissioned in response to such challenges has confirmed the issues identified above but contributed to two primary responses from relevant interested parties; firstly is the identification of “a shortage of particular skills sets” (EGFSN, 2007: 8) in the financial services sector and recommendations around meeting such shortages through education, training and research. Secondly and connected to the first shortfall, the financial services sector has looked to international workers as a key source of labour as will be discussed in the next section which profiles the financial services sector workforce.

5

Employment in the Financial Services Sector: The Role of Migrants In this section, we outline some basic information on the financial services sector (or financial intermediation) workforce in Ireland. In particular, we document the small but growing role of migrants in the financial services sector. We also highlight a pronounced gender difference, particularly when examined in the context of earnings. Emphasis in also placed on the high level of educational qualification amongst migrants when compared with Irish workers.

The key data sources for this section include the Quarterly National Household Survey (QNHS), the Earnings and Labour Cost Survey and the National Employment Survey (NES). While we have already highlighted the two dominant sub-sectors of the financial services sector in Ireland, namely, global financial companies in the IFSC and domestic banking, the statistics we analyse in this section tend to aggregate these sub-sectors in terms of employment. Appendix 1 provides more background information on how the data presented here has been obtained. Migrants and Employment

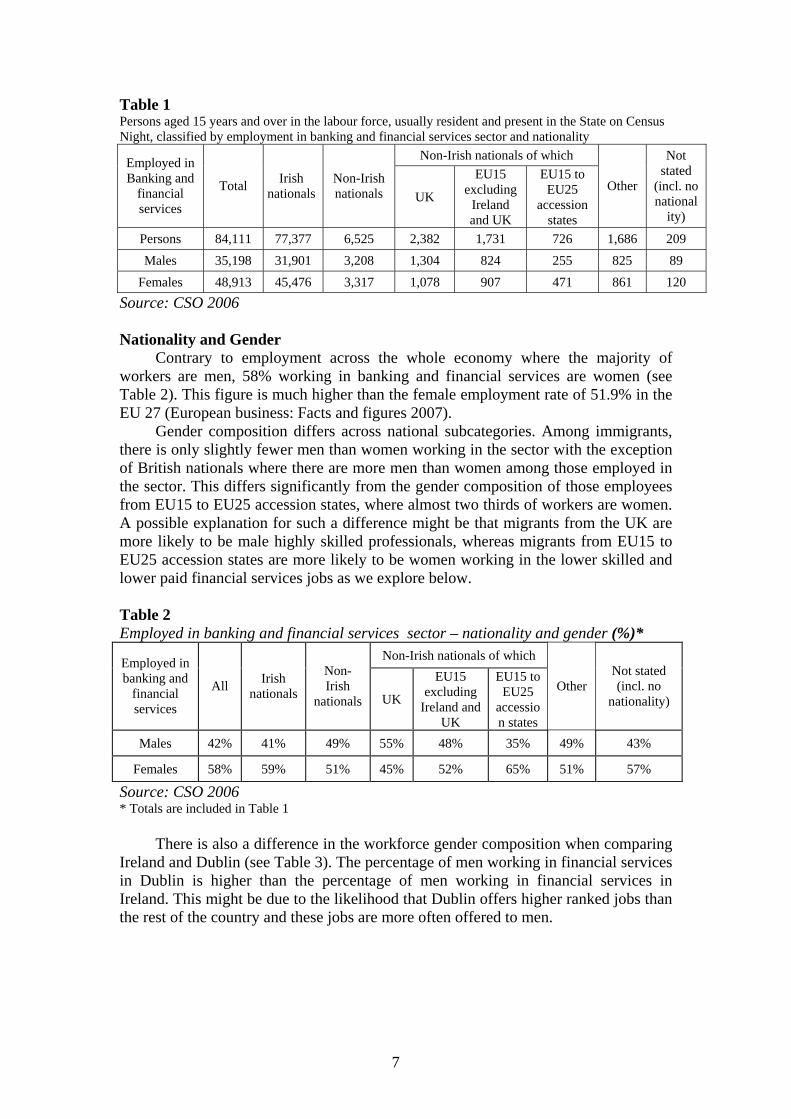

Total employment in the sector reached 84,000 according to the most recent census figures (see Table 1). Data from the Irish Labour Market Review 2007 (Q3 2007) shows that employment growth in Ireland occurred mainly in the services area of the economy. While other sectors’ employment levels were decreasing, particularly the construction sector, employment in financial and business services was actually growing at a strong pace (+ 10.7%).

At December 2006, the IFSC employed 22,177 people (Finance Dublin Yearbook 2007 cited in www.financedublin.com, 2007). Employment in the IFSC comprises investment management jobs (over 9,000), banking and capital markets jobs (almost 10,000) and positions in the insurance area (over 3,000) (Expert Group on Future Skills Needs, 2007). In 2006 alone there was a 16% growth in employment in the IFSC, generating up to 3,000 new jobs. Such employment growth was observable mainly in banking and funds companies (Finance Dublin Yearbook 2007 cited in www.financedublin.com, 2007). Over half of the total workforce in the financial services sector in Ireland is concentrated in Dublin indicating that around 50% of those working in Dublin are IFSC company employees.

Banks in Ireland employ 41,000 people of which 31,700 (77%) work for major retail banks (including AIB, Bank of Ireland, National Irish Bank, Permanent tsb, Ulster Bank, Bank of Scotland (Ireland)). Thus, approximately half of the workforce in the financial services sector work for banks (IBF, 2006) of which around 9,000 employees work in the international banking area (Expert Group on Future Skills Needs, 2007). Bank employees account for two percent of total at work in Ireland, positioning Ireland as a country with the third largest share of its population working in banks in Europe (Sokol, 2007).

In 2006, 6,525 employees with non-Irish nationalities were working in the banking and financial services sector which accounted for almost 8% of the workforce in the sector. However, EU15 to EU25 figures accounted for just 11% of the non-Irish national workforce in the sector.

6

Table 1 Persons aged 15 years and over in the labour force, usually resident and present in the State on Census Night, classified by employment in banking and financial services sector and nationality

Non-Irish nationals of which Employed in Banking and

financial services

Total Irish nationals

Non-Irish nationals UK

EU15 excluding

Ireland and UK

EU15 to EU25

accession states

Other

Not stated

(incl. no national

ity)

Persons 84,111 77,377 6,525 2,382 1,731 726 1,686 209 Males 35,198 31,901 3,208 1,304 824 255 825 89

Females 48,913 45,476 3,317 1,078 907 471 861 120 Source: CSO 2006 Nationality and Gender

Contrary to employment across the whole economy where the majority of workers are men, 58% working in banking and financial services are women (see Table 2). This figure is much higher than the female employment rate of 51.9% in the EU 27 (European business: Facts and figures 2007).

Gender composition differs across national subcategories. Among immigrants, there is only slightly fewer men than women working in the sector with the exception of British nationals where there are more men than women among those employed in the sector. This differs significantly from the gender composition of those employees from EU15 to EU25 accession states, where almost two thirds of workers are women. A possible explanation for such a difference might be that migrants from the UK are more likely to be male highly skilled professionals, whereas migrants from EU15 to EU25 accession states are more likely to be women working in the lower skilled and lower paid financial services jobs as we explore below. Table 2 Employed in banking and financial services sector – nationality and gender (%)*

Non-Irish nationals of which Employed in banking and

financial services

All Irish nationals

Non-Irish

nationals UK

EU15 excluding

Ireland and UK

EU15 to EU25

accession states

Other Not stated (incl. no

nationality)

Males 42% 41% 49% 55% 48% 35% 49% 43%

Females 58% 59% 51% 45% 52% 65% 51% 57%

Source: CSO 2006 * Totals are included in Table 1

There is also a difference in the workforce gender composition when comparing Ireland and Dublin (see Table 3). The percentage of men working in financial services in Dublin is higher than the percentage of men working in financial services in Ireland. This might be due to the likelihood that Dublin offers higher ranked jobs than the rest of the country and these jobs are more often offered to men.

7

Table 3 Employed in banking and financial services (B&FS) sector in Ireland and Dublin –gender

Persons, males and females aged 15 years and over at work in each Regional Authority Area, employed in banking and Financial Services

Ireland

Ireland B&FS

workforce by sex

%

Dublin

Dublin B&FS

workforce as a % of Ireland B&FS

workforce

Dublin B&FS

workforce by sex

%

Persons, males and females aged 15 years and over at work in each Regional Authority Area, employed in banking and Financial Services

85,413 100% 44,461 52% 100%

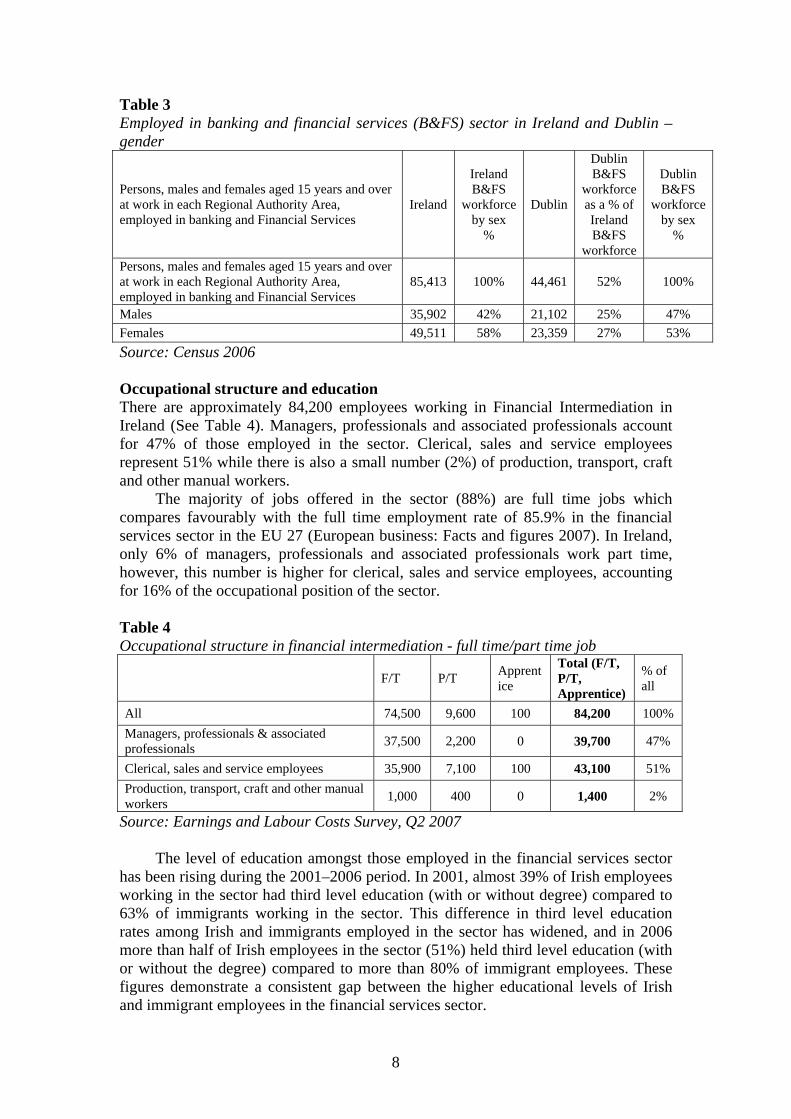

Males 35,902 42% 21,102 25% 47% Females 49,511 58% 23,359 27% 53% Source: Census 2006 Occupational structure and education There are approximately 84,200 employees working in Financial Intermediation in Ireland (See Table 4). Managers, professionals and associated professionals account for 47% of those employed in the sector. Clerical, sales and service employees represent 51% while there is also a small number (2%) of production, transport, craft and other manual workers.

The majority of jobs offered in the sector (88%) are full time jobs which compares favourably with the full time employment rate of 85.9% in the financial services sector in the EU 27 (European business: Facts and figures 2007). In Ireland, only 6% of managers, professionals and associated professionals work part time, however, this number is higher for clerical, sales and service employees, accounting for 16% of the occupational position of the sector. Table 4 Occupational structure in financial intermediation - full time/part time job

F/T P/T Apprentice

Total (F/T, P/T, Apprentice)

% of all

All 74,500 9,600 100 84,200 100% Managers, professionals & associated professionals 37,500 2,200 0 39,700 47%

Clerical, sales and service employees 35,900 7,100 100 43,100 51% Production, transport, craft and other manual workers 1,000 400 0 1,400 2%

Source: Earnings and Labour Costs Survey, Q2 2007

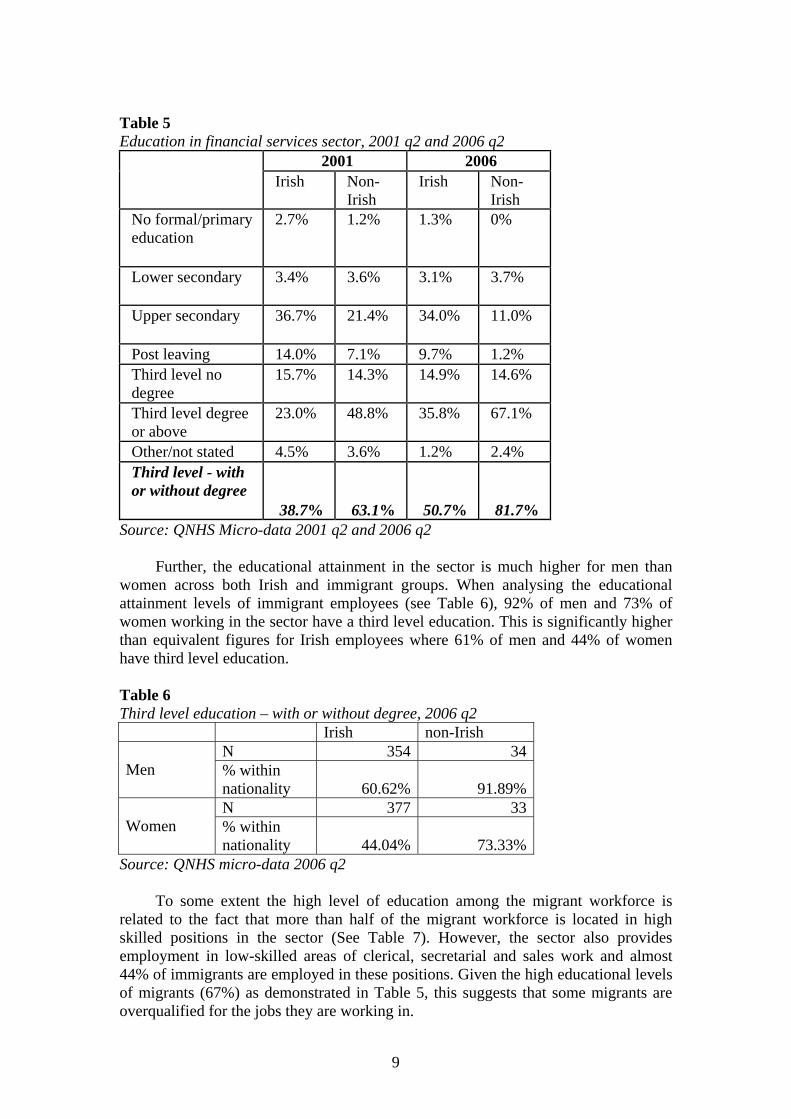

The level of education amongst those employed in the financial services sector has been rising during the 2001–2006 period. In 2001, almost 39% of Irish employees working in the sector had third level education (with or without degree) compared to 63% of immigrants working in the sector. This difference in third level education rates among Irish and immigrants employed in the sector has widened, and in 2006 more than half of Irish employees in the sector (51%) held third level education (with or without the degree) compared to more than 80% of immigrant employees. These figures demonstrate a consistent gap between the higher educational levels of Irish and immigrant employees in the financial services sector.

8

Table 5 Education in financial services sector, 2001 q2 and 2006 q2

2001 2006 Irish Non-

Irish Irish Non-

Irish No formal/primary education

2.7% 1.2% 1.3% 0%

Lower secondary 3.4% 3.6% 3.1% 3.7%

Upper secondary 36.7% 21.4% 34.0% 11.0%

Post leaving 14.0% 7.1% 9.7% 1.2% Third level no degree

15.7% 14.3% 14.9% 14.6%

Third level degree or above

23.0% 48.8% 35.8% 67.1%

Other/not stated 4.5% 3.6% 1.2% 2.4% Third level - with or without degree

38.7% 63.1% 50.7% 81.7% Source: QNHS Micro-data 2001 q2 and 2006 q2

Further, the educational attainment in the sector is much higher for men than women across both Irish and immigrant groups. When analysing the educational attainment levels of immigrant employees (see Table 6), 92% of men and 73% of women working in the sector have a third level education. This is significantly higher than equivalent figures for Irish employees where 61% of men and 44% of women have third level education. Table 6 Third level education – with or without degree, 2006 q2 Irish non-Irish

N 354 34Men % within

nationality 60.62% 91.89%N 377 33

Women % within nationality 44.04% 73.33%

Source: QNHS micro-data 2006 q2

To some extent the high level of education among the migrant workforce is related to the fact that more than half of the migrant workforce is located in high skilled positions in the sector (See Table 7). However, the sector also provides employment in low-skilled areas of clerical, secretarial and sales work and almost 44% of immigrants are employed in these positions. Given the high educational levels of migrants (67%) as demonstrated in Table 5, this suggests that some migrants are overqualified for the jobs they are working in.

9

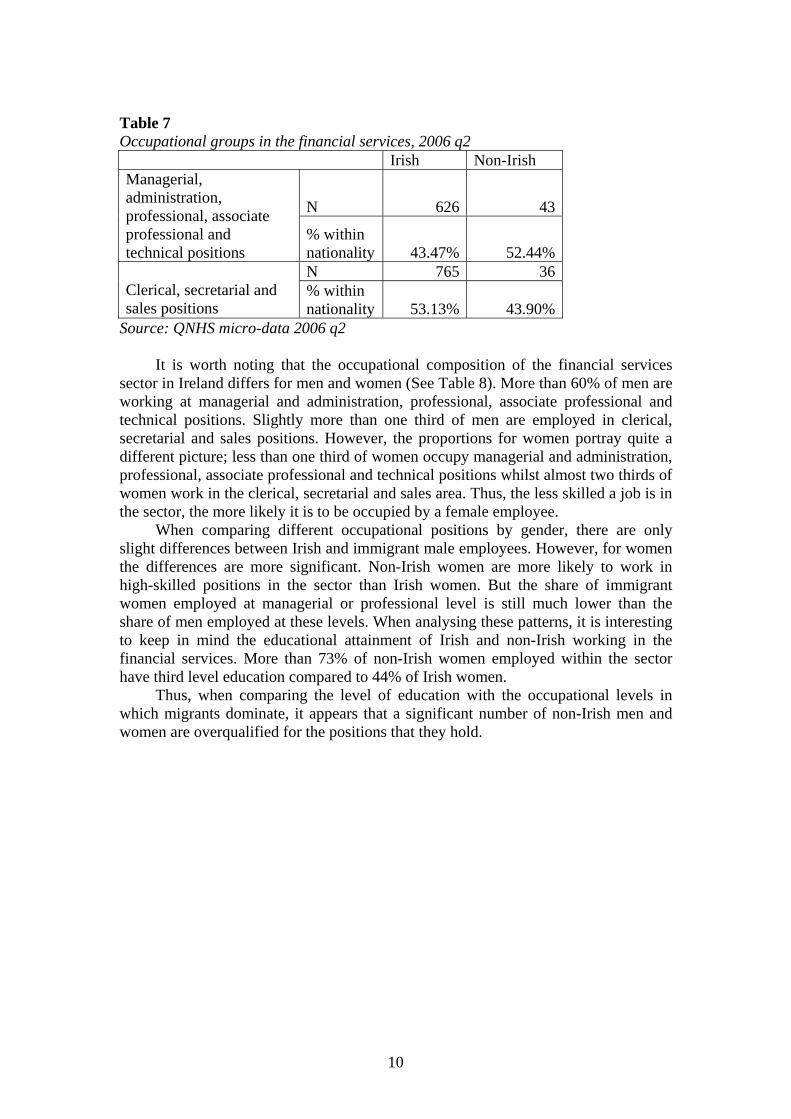

Table 7 Occupational groups in the financial services, 2006 q2 Irish Non-Irish

N 626 43

Managerial, administration, professional, associate professional and technical positions

% within nationality 43.47% 52.44%N 765 36

Clerical, secretarial and sales positions

% within nationality 53.13% 43.90%

Source: QNHS micro-data 2006 q2

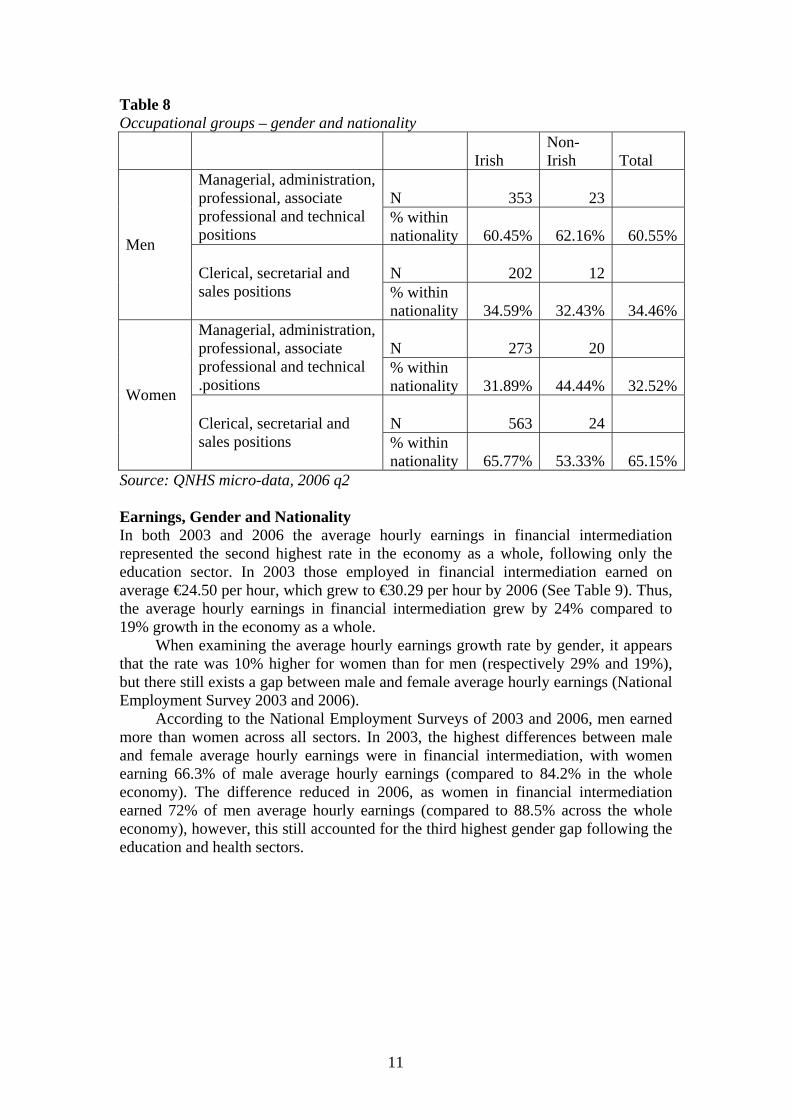

It is worth noting that the occupational composition of the financial services sector in Ireland differs for men and women (See Table 8). More than 60% of men are working at managerial and administration, professional, associate professional and technical positions. Slightly more than one third of men are employed in clerical, secretarial and sales positions. However, the proportions for women portray quite a different picture; less than one third of women occupy managerial and administration, professional, associate professional and technical positions whilst almost two thirds of women work in the clerical, secretarial and sales area. Thus, the less skilled a job is in the sector, the more likely it is to be occupied by a female employee.

When comparing different occupational positions by gender, there are only slight differences between Irish and immigrant male employees. However, for women the differences are more significant. Non-Irish women are more likely to work in high-skilled positions in the sector than Irish women. But the share of immigrant women employed at managerial or professional level is still much lower than the share of men employed at these levels. When analysing these patterns, it is interesting to keep in mind the educational attainment of Irish and non-Irish working in the financial services. More than 73% of non-Irish women employed within the sector have third level education compared to 44% of Irish women.

Thus, when comparing the level of education with the occupational levels in which migrants dominate, it appears that a significant number of non-Irish men and women are overqualified for the positions that they hold.

10

Table 8 Occupational groups – gender and nationality

Irish Non-Irish Total

N 353 23 Managerial, administration, professional, associate professional and technical positions

% within nationality 60.45% 62.16% 60.55%

N 202 12

Men

Clerical, secretarial and sales positions % within

nationality 34.59% 32.43% 34.46%

N 273 20 Managerial, administration, professional, associate professional and technical .positions

% within nationality 31.89% 44.44% 32.52%

N 563 24

Women

Clerical, secretarial and sales positions % within

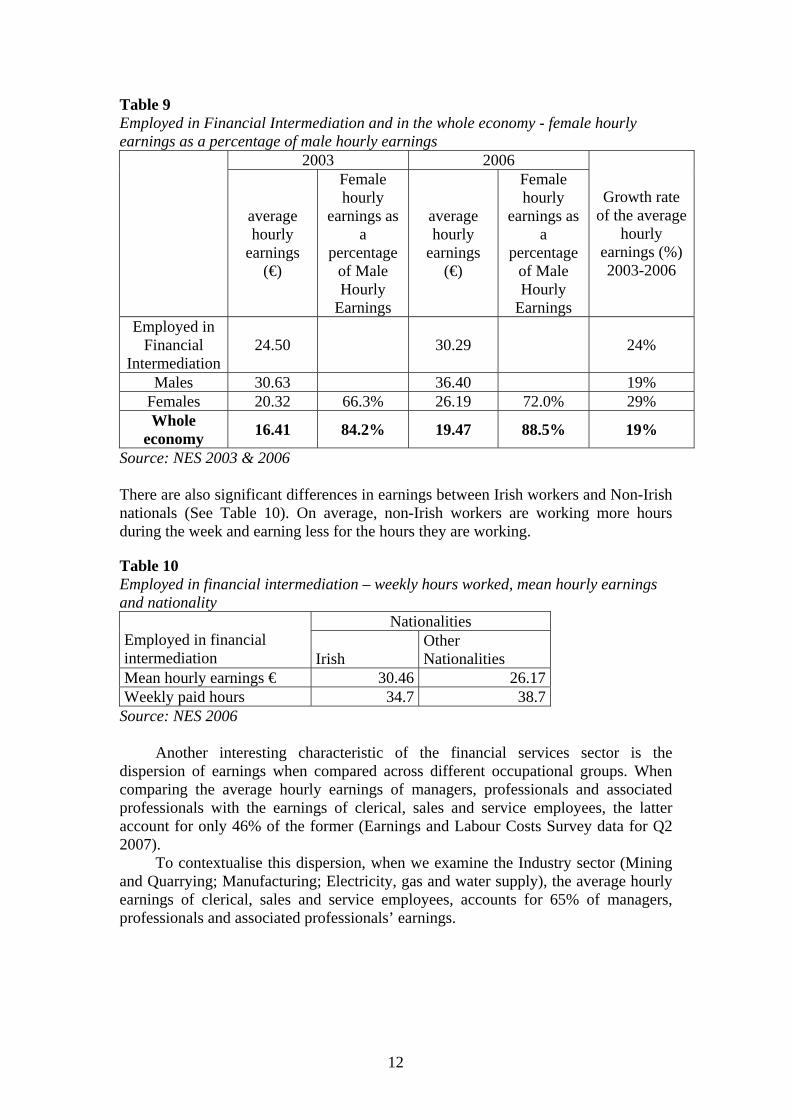

nationality 65.77% 53.33% 65.15%Source: QNHS micro-data, 2006 q2 Earnings, Gender and Nationality In both 2003 and 2006 the average hourly earnings in financial intermediation represented the second highest rate in the economy as a whole, following only the education sector. In 2003 those employed in financial intermediation earned on average €24.50 per hour, which grew to €30.29 per hour by 2006 (See Table 9). Thus, the average hourly earnings in financial intermediation grew by 24% compared to 19% growth in the economy as a whole.

When examining the average hourly earnings growth rate by gender, it appears that the rate was 10% higher for women than for men (respectively 29% and 19%), but there still exists a gap between male and female average hourly earnings (National Employment Survey 2003 and 2006).

According to the National Employment Surveys of 2003 and 2006, men earned more than women across all sectors. In 2003, the highest differences between male and female average hourly earnings were in financial intermediation, with women earning 66.3% of male average hourly earnings (compared to 84.2% in the whole economy). The difference reduced in 2006, as women in financial intermediation earned 72% of men average hourly earnings (compared to 88.5% across the whole economy), however, this still accounted for the third highest gender gap following the education and health sectors.

11

Table 9 Employed in Financial Intermediation and in the whole economy - female hourly earnings as a percentage of male hourly earnings

2003 2006

average hourly

earnings (€)

Female hourly

earnings as a

percentage of Male Hourly

Earnings

average hourly

earnings (€)

Female hourly

earnings as a

percentage of Male Hourly

Earnings

Growth rate of the average

hourly earnings (%) 2003-2006

Employed in Financial

Intermediation 24.50 30.29 24%

Males 30.63 36.40 19% Females 20.32 66.3% 26.19 72.0% 29% Whole

economy 16.41 84.2% 19.47 88.5% 19%

Source: NES 2003 & 2006 There are also significant differences in earnings between Irish workers and Non-Irish nationals (See Table 10). On average, non-Irish workers are working more hours during the week and earning less for the hours they are working. Table 10 Employed in financial intermediation – weekly hours worked, mean hourly earnings and nationality

Nationalities Employed in financial intermediation Irish

Other Nationalities

Mean hourly earnings € 30.46 26.17Weekly paid hours 34.7 38.7

Source: NES 2006

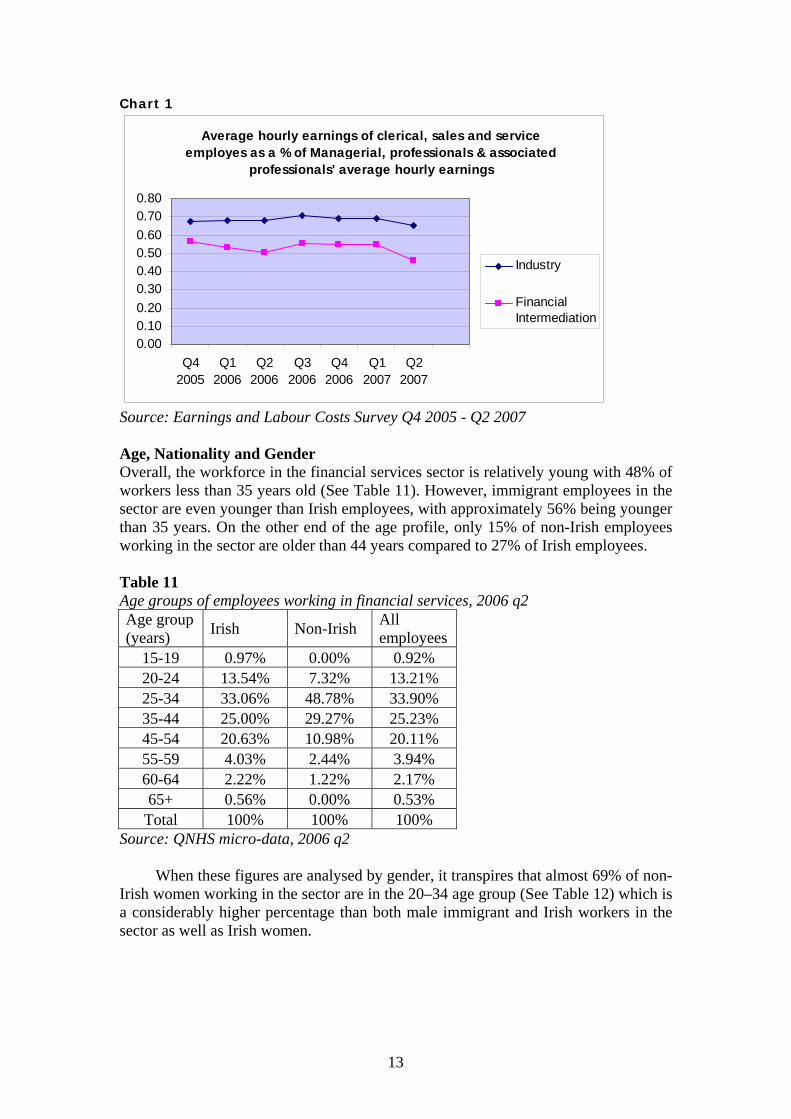

Another interesting characteristic of the financial services sector is the dispersion of earnings when compared across different occupational groups. When comparing the average hourly earnings of managers, professionals and associated professionals with the earnings of clerical, sales and service employees, the latter account for only 46% of the former (Earnings and Labour Costs Survey data for Q2 2007).

To contextualise this dispersion, when we examine the Industry sector (Mining and Quarrying; Manufacturing; Electricity, gas and water supply), the average hourly earnings of clerical, sales and service employees, accounts for 65% of managers, professionals and associated professionals’ earnings.

12

Chart 1

Average hourly earnings of clerical, sales and service employes as a % of Managerial, professionals & associated

professionals' average hourly earnings

0.000.100.200.300.400.500.600.700.80

Q42005

Q12006

Q22006

Q32006

Q42006

Q12007

Q22007

Industry

FinancialIntermediation

Source: Earnings and Labour Costs Survey Q4 2005 - Q2 2007

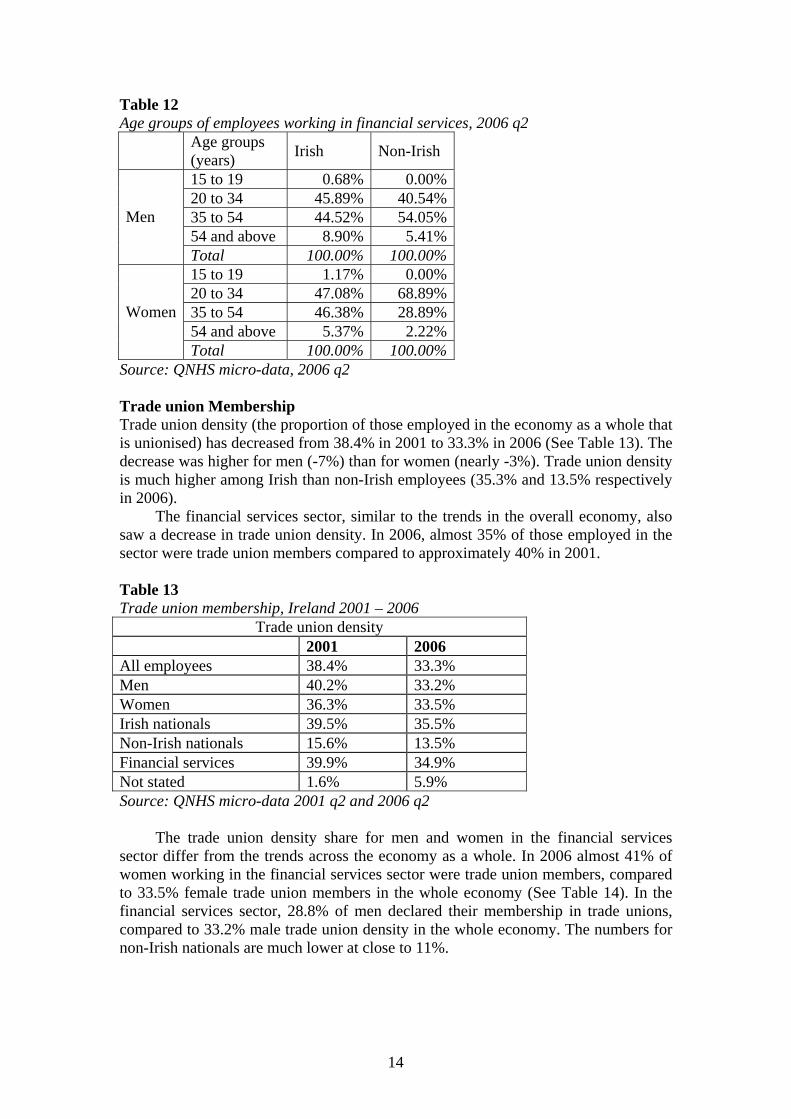

Age, Nationality and Gender Overall, the workforce in the financial services sector is relatively young with 48% of workers less than 35 years old (See Table 11). However, immigrant employees in the sector are even younger than Irish employees, with approximately 56% being younger than 35 years. On the other end of the age profile, only 15% of non-Irish employees working in the sector are older than 44 years compared to 27% of Irish employees. Table 11 Age groups of employees working in financial services, 2006 q2 Age group (years) Irish Non-Irish All

employees 15-19 0.97% 0.00% 0.92% 20-24 13.54% 7.32% 13.21% 25-34 33.06% 48.78% 33.90% 35-44 25.00% 29.27% 25.23% 45-54 20.63% 10.98% 20.11% 55-59 4.03% 2.44% 3.94% 60-64 2.22% 1.22% 2.17% 65+ 0.56% 0.00% 0.53%

Total 100% 100% 100% Source: QNHS micro-data, 2006 q2

When these figures are analysed by gender, it transpires that almost 69% of non-

Irish women working in the sector are in the 20–34 age group (See Table 12) which is a considerably higher percentage than both male immigrant and Irish workers in the sector as well as Irish women.

13

Table 12 Age groups of employees working in financial services, 2006 q2

Age groups (years) Irish Non-Irish

15 to 19 0.68% 0.00%20 to 34 45.89% 40.54%35 to 54 44.52% 54.05%54 and above 8.90% 5.41%

Men

Total 100.00% 100.00%15 to 19 1.17% 0.00%20 to 34 47.08% 68.89%35 to 54 46.38% 28.89%54 and above 5.37% 2.22%

Women

Total 100.00% 100.00%Source: QNHS micro-data, 2006 q2 Trade union Membership Trade union density (the proportion of those employed in the economy as a whole that is unionised) has decreased from 38.4% in 2001 to 33.3% in 2006 (See Table 13). The decrease was higher for men (-7%) than for women (nearly -3%). Trade union density is much higher among Irish than non-Irish employees (35.3% and 13.5% respectively in 2006).

The financial services sector, similar to the trends in the overall economy, also saw a decrease in trade union density. In 2006, almost 35% of those employed in the sector were trade union members compared to approximately 40% in 2001. Table 13 Trade union membership, Ireland 2001 – 2006

Trade union density 2001 2006 All employees 38.4% 33.3% Men 40.2% 33.2% Women 36.3% 33.5% Irish nationals 39.5% 35.5% Non-Irish nationals 15.6% 13.5% Financial services 39.9% 34.9% Not stated 1.6% 5.9% Source: QNHS micro-data 2001 q2 and 2006 q2

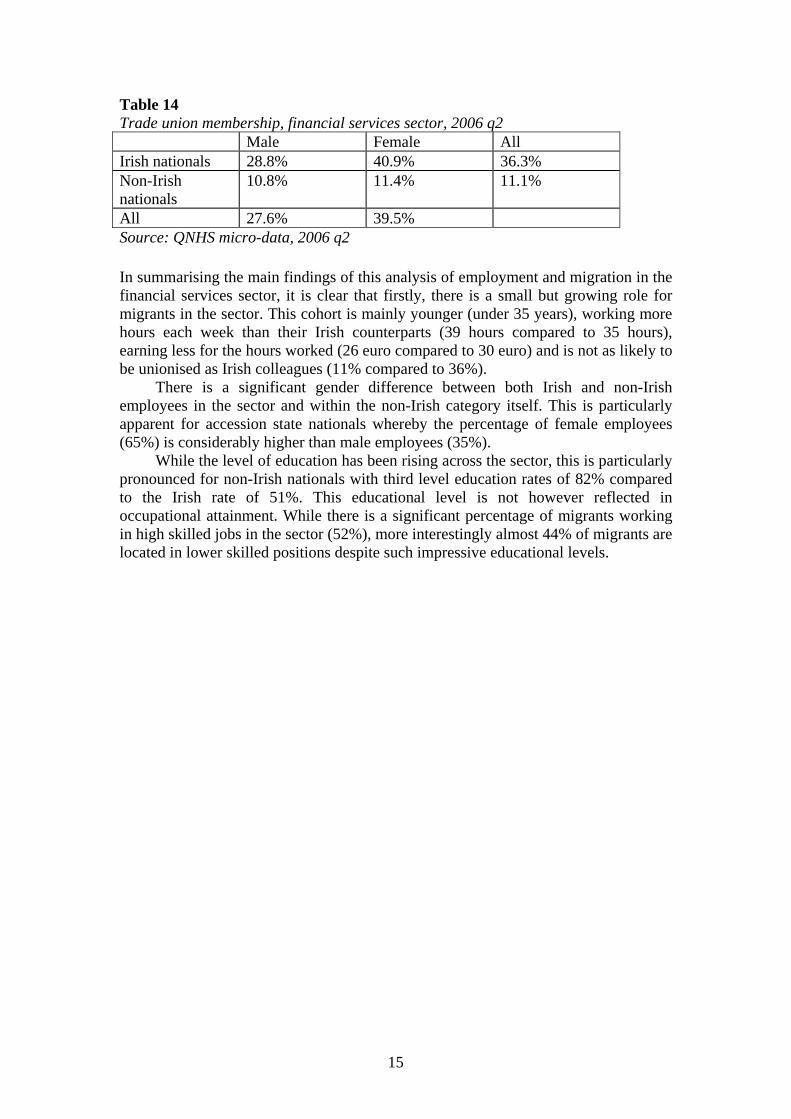

The trade union density share for men and women in the financial services sector differ from the trends across the economy as a whole. In 2006 almost 41% of women working in the financial services sector were trade union members, compared to 33.5% female trade union members in the whole economy (See Table 14). In the financial services sector, 28.8% of men declared their membership in trade unions, compared to 33.2% male trade union density in the whole economy. The numbers for non-Irish nationals are much lower at close to 11%.

14

Table 14 Trade union membership, financial services sector, 2006 q2 Male Female All Irish nationals 28.8% 40.9% 36.3% Non-Irish nationals

10.8% 11.4% 11.1%

All 27.6% 39.5% Source: QNHS micro-data, 2006 q2 In summarising the main findings of this analysis of employment and migration in the financial services sector, it is clear that firstly, there is a small but growing role for migrants in the sector. This cohort is mainly younger (under 35 years), working more hours each week than their Irish counterparts (39 hours compared to 35 hours), earning less for the hours worked (26 euro compared to 30 euro) and is not as likely to be unionised as Irish colleagues (11% compared to 36%).

There is a significant gender difference between both Irish and non-Irish employees in the sector and within the non-Irish category itself. This is particularly apparent for accession state nationals whereby the percentage of female employees (65%) is considerably higher than male employees (35%).

While the level of education has been rising across the sector, this is particularly pronounced for non-Irish nationals with third level education rates of 82% compared to the Irish rate of 51%. This educational level is not however reflected in occupational attainment. While there is a significant percentage of migrants working in high skilled jobs in the sector (52%), more interestingly almost 44% of migrants are located in lower skilled positions despite such impressive educational levels.

15

Issues for Research: Employers’ Strategies and Migrants’ Careers The final sections of this report overview the key issues which form the basis of our research agenda with regard to migrant workers and the financial services sector in Ireland. These involve a discussion of employers’ workplace strategies and migrants’ career aspirations in the context of relevant international literature. Employers’ Strategies: Issues for Research In order to understand employers’ strategies in the financial services sector, it is useful to mention the primary characteristics of work in the sector which are both mobile and global. The regulatory context shapes the rules in the sector on different levels. There are still some state peculiarities, even if the European financial services market is becoming integrated into a single market and the institutions are interlinked even further in the global marketplace.

A number of issues have been mentioned in earlier sections as potential challenges to Ireland’s continued success in financial services. These include the availability of skilled graduates, the development of specialist knowledge in certain disciplines, an attractive living and working environment and obtaining work permits. We have also highlighted how many financial services companies have responded to the new challenges of globalisation and liberalisation by processes of consolidation and diversification. In Ireland, local niche companies have responded to such pressures with branch closures, staff reductions, adoption of new technologies such as on-line banking reducing face to face contact and call centres (Webster, 2001: 18).

During recent decades, work in the sector has undergone a significant transformation. Regini (1999) offers an overview of the development of the Human Resource Management and industrial relations practices in the banking subsector, observing that there is a growing distinction between staff employed in the front and back offices. The introduction of technology has also reduced the amount of work performed in the back office. Traditionally bureaucratic institutions were developed into sales-oriented organisations. A focus on the market and customer demands implied use of new Human Resource Management practices, among them a redefinition of the role of the managers, emphasis on soft skills, introduction of job rotation and horizontal career movements and development of performance based remuneration packages. Regulation and Recruitment

Even with such changing patterns in banking employment, career paths in the banking sector appear to remain highly institutionalised. The financial market as a global institution provides occupational categories that are similar around the world. Employers are thus provided with a framework of comparable occupational structures in different countries. This is of importance as international qualifications make the candidates’ skills comparable and possible to assess.

However, the recruitment of international candidates requires engaging with state regulations which in turn open the labour market to international skills. In Ireland, the introduction of the green card system was warmly welcomed by the employers group, IBEC (IBEC, 2007) and the importance of this green card system was underlined by the Expert Group on Future Skills Needs (2007). The significance of the green card system was particularly highlighted by the Expert Group in the context of both a shortage of appropriate skills in the sector as well as a lack of capacity by the Irish education system in the short term to provide the sector with

16

some of the high skills required. In short, this has driven many Irish based employers to search for such skills abroad.

The Green Card system is crucial for a sector that endeavours to attract highly skilled professionals from jurisdictions outside the EU, particularly because some of the main financial centres and high skills are based in the US and Asia. Another mechanism available to employers in the sector is the intra-company transfer scheme which was again reinforced through the immigration legislation of 2007. This scheme is important for the IFSC as it opens the way to relocate existing expertise to Dublin.

In the less skilled and consequently less well paid area of financial services, there are a small number of work permits that are issued to companies operating in the sector, often located in the domestic banking sector. However, candidates for less skilled and less well paid positions are expected to be sourced from the broader European or EEA labour market. Indeed in order to expand the pool of skills to choose from, since May 2004, employers and recruitment agencies have been particularly targeting candidates through recruitment campaigns based in Eastern and Central European countries (interview with recruitment consultant, 25/1/08). However, this recruitment practice has now reversed and recruitment agencies are actively seeking Eastern European financial service sector employees who have gained experience in the Irish market and who may be willing to return to fill skills shortages in the Polish financial sector (interview with consultant, 25/1/08). Skills Shortages and Potential Employment

According to Global Financial Employment Monitor (2007-2008) published by Robert Half International, the main skills shortages in the financial services sector in Ireland include executive level, operational, financial analysis and general accounting positions. FAS (2007) outlined how employers in the services sector economy reported problems with filling financial and insurance personnel and managers vacancies.

The IDA in 2004 claimed that the availability of skilled labour, particularly “the availability of a quality graduate pool…[along with] the development of specialist knowledge in certain disciplines” (IDA, 2004: 32) was essential in building a competitive and successful financial centre.

Referring to such skills shortages in the financial services sector, The Expert Group on Future Skills Needs (2007) asserted that the Irish education system was producing ‘skilled generalists’ possessing vast but general knowledge which is not specific to the financial services sub-sectors. Another problem discussed in the report related to the fact that such general knowledge amongst students was not accompanied by practical experience. It appears that Irish students prefer casual summer employment abroad to taking up apprenticeships in the financial services sector.

However, there are strong preferences amongst graduates when it comes to identifying particular financial sector companies as potential employers. In The Ireland Graduate Careers Survey 2007, AIB and Bank of Ireland appeared in the first five positions while Anglo Irish Bank and Ulster Bank were classified in the first 30. However, traditionally rigid corporate cultures of financial institutions might disappoint young professionals. Soft Skills

In our previous report on the hospitality sector (Wickham et al, 2008) we mentioned the importance of ‘good attitude’ in the selection process for customer

17

18

service positions. Surprisingly, we find that similar processes might also be occurring in the financial sector. In the context of skills shortages, companies appear to employ candidates for lower to medium level positions with perceived potential. However, unlike the hospitality sector, employers value the ability and willingness to learn and progress up the financial services career ladder. This might happen while hiring overqualified candidates for simple jobs, thus creating a potential reserve of skills that can be activated by the company as required.

There are a number of examples of migrants holding MA degrees in banking and finances that are performing the most basic tasks in the sector. As demonstrated in the last section, a large majority of the migrant workforce (82%) in the sector has third level education (compared to only half (51%) of the Irish workforce), but at the same time almost 44% of immigrants work in the low skilled, clerical, secretarial and sales jobs. This raises a key research question around migrants’ chances of progressing from clerical and secretarial jobs to more senior positions.

Moreover, with the opening of the Irish labour market to immigrants from the new accession states, a variety of skills was attracted to Ireland. This provided employers with wide choices when sourcing candidates for sector vacancies and raises another research issue in terms of the impact of this new situation on employers’ expectations in the future. This question is of particular relevance in the context of the current debate around the temporary or permanent character of migration to Ireland. Turnover and Retention of Workers in the sector In addition to the skills shortages emphasized by both the Expert Group on Future Skills Needs and FAS, the problem of high turnover in the financial services sector is also highlighted. These challenges are faced by both sub-sectors of the financial services sector in Ireland.

In order to attract and retain staff, global financial companies in the IFSC offer more attractive salary packages, but this has important implications in terms of the related rise in labour costs and consequent reduction of competitiveness. In the domestic banking sector, along with salaries and bonuses, some companies have introduced what they describe as work-life balance strategies to create family friendly or equal opportunity work environments. Such strategies include, for example, flexible working arrangements and maternity leave. Thus AIB and IBOA have an agreed ‘Partnership Approach to Family Friendly Working Arrangements’; BoI has had an Equal Opportunities Policy and Programme of Action since 1985.

These work-life balance strategies are particularly important for women working in the sector. However, in a study of sex equality issues in Turkish and British banking, Özbilgin and Woodward (2004) argued there are very few cases of successful work-life balance schemes and there is extensive evidence of sexual discrimination. These findings may be of interest for the Irish case. In the companies examined, the predominantly male managers’ views on ‘the ideal worker’ were represented in the selection of candidates for jobs and the promotional opportunities offered to employees. These views also functioned as part of the dominant corporate culture and consequently shaped the everyday organisational reality experienced by workers. The authors also describe the exclusion of women due to ‘innocent’ practices like male dominated sporting activities and argue that the existence of a ‘glass ceiling’ is one of the examples of female discrimination in the financial services and may be experienced by immigrant employees.

Employees’ Careers and Aspirations: Issues for Research The literature on migrants in the financial services sector is rather extensive. However, it focuses on one side of the labour market, namely on the highly skilled professionals working for transnational companies located in international financial centres (IFC). The debate on financial services centres is embedded in the vaster literature on mobility. Flows of capital and the international elite dealing with that capital are some of the main manifestations of what Castells (2001) describes as the ‘space of flows’. The flows of highly skilled professionals take place between different IFCs located in different global cities (Sassen, 2004). Dublin, ranked tenth in the global financial centres ranking in 2003 (FCI cited in Sokol, 2007: 246), is regarded as an emerging global city.

According to Beaverstock (2002), the temporary migration of high-skilled workers is enhanced by employers whose strategy is to relocate knowledge. This has an effect on the choices of employees working in the sector. Indeed a number of studies reveal the highly skilled professionals strategies of building a multinational curricula with career histories in different companies (e.g. Beaverstock 2002). Mobility in the financial world is important as the financial knowledge is concentrated in clusters, leading to the intertwining of geographical and career mobilities, or space and knowledge.

However, in the IFCs there are not just transnational elites that move back and forward. Sassen (2004) argues that a polarisation is taking place in the global city. On the one hand there are highly skilled professionals; on the other the entrance of women and migrants to professional jobs in the global cities creates a demand for low-paid service jobs (McDowell et al., 2005). The literature focusing on this increasing polarisation within global cities apparently overlooks the fact that the IFCs are not homogenous themselves. There is a huge area of financial services jobs that consist of performing mainly routine, clerical tasks and these are often performed by an immigrant workforce.

However, we can also recognise such workforce changes as creating opportunities for employers to develop a pool of highly skilled and educated workers, thus creating a possible reserve of potential that might be activated by the company as needed. Employers therefore retain a relatively low paid, highly educated workforce in reserve. For example, our preliminary research (interview, 30/1/2008) suggests that while migrants have accessed low to medium level jobs in the sector, there is a perception that they may ‘get stuck’ at these levels. One issue worth exploring would involve the extent of possible career movements in the sector from the lower to top level jobs.

Geographical mobility of migrants

Another area of research is the extent to which work with hypermobile capital affects the geographical career mobility of employees with low to medium level jobs. We know that the previously mentioned highly skilled professionals perceive the labour market as global, but another interesting question would focus on how lower level workers in the sector perceive the labour market within which they would like to move (if they would like to do so). The statistical evidence in Ireland suggests that, although capital in the sector is global, the labour force in the sector is not (as reported above, migrants only comprise 8% of the workforce in the financial services sector in Ireland, a smaller proportion than in the workforce as a whole).

19

However, there is also evidence that migrant employees in the domestic banking sector in Ireland are identifying potential opportunities for return to Poland or to move elsewhere through intra-company transfers with particular banks which have a presence overseas. For example, it has been highlighted by participants in our preliminary research (interview, 24/5/08) that the AIB brand is recognised internationally, including in the Polish labour market. The AIB group owns BZ WBK bank which is based in Poland and it seems that migrants perceive opportunities to move to Poland through such transnational employment structures.

Qualifications and Opportunities An important feature of the sector is the presence of both national and international regulations. These affect the market of qualifications. Some of them are obviously specific to the local labour market, such as the Qualified Financial Adviser (QFA) certificate which is specific to the Irish market for financial products. Others are recognised internationally, like the ACCA in accounting or the CFA (Chartered Financial Analyst). The migrants’ choices of training, acquiring the qualifications specific to local or global markets will affect future career opportunities. They also provide an indication of the migrant perception of the labour market: in local, European or even global terms.

With training, migrants achieve some skills that might be, but not necessarily are, regarded as an asset by international employers in different labour markets. For example, in our preliminary research (interview, 30/1/08) the IFSC is perceived as offering a wide range of both clerical and management skills that provides employees with internationally recognised experience and potentially opens the gates to further financial services labour markets. Similarly at the domestic banking level, it is perceived that employers will invest in their employees’ development and provide promotion opportunities which will enhance both curriculum vitae and experience (interview, 19/4/08).

Given that a number of our participants in both global finance companies and domestic banking companies are considering the possibility of returning to Poland at some time in the future (interviews 30/1/08, 19/4/08) this would appear a coherent strategy. However, there is also a recognition that depending on the area of financial services one is located, there can be both limitations (insurance and pensions being seen as more domestic) and opportunities (investment banking) in terms of career opportunities. This is another research question worth exploring.

Job or Career? The concepts of job and career suggested by Westergaard (1984) seem to be a fruitful analytical tool with which to examine migrant employees’ strategies in the host labour market. McDowell et al (2005) used the concepts in their study of women working in the financial services sector. While female employment within the financial sector is broadly recognised as representing secure white collar jobs, nevertheless, the sector does not seem women friendly in terms of employers’ strategies (Özbilgin and Woodward, 2004). However, long working hours would not necessarily create a problem for migrant women who decided to migrate on the basis of economic motivations. In this case, it might actually be an advantage.

Connected to such motivations, it would also be interesting to compare female and male migrants’ strategies in the labour market. For women, employment in the sector provides a relatively high status job and indeed in Ireland, the sector attracts more women than men. The majority of the female workforce is employed in clerical,

20

21

secretarial and sales positions, however, immigrant women (44%) are more widely represented at managerial level than Irish women (32%). This achievement must still be analysed in terms of the high educational attainment of immigrant women (73%) who are often overqualified for the jobs they occupy.

For male migrants who identify financial accumulation as their primary motivation in entering the Irish labour market, the financial services sector is not an obvious route. Unskilled work on building sites is likely to be better paid than lower or medium skilled jobs in the financial services sector. Apart from migrants having their jobs in the sector simply to earn money, there are also some migrants with specific career orientations. For those with longer-term career goals, the financial services sector in considered a worthwhile employment option. Indeed, our preliminary research (interview 9/5/08) demonstrates that migrants are willing to take considerable wage cuts, at least in the short term, in order to invest in their longer term career strategy.

The boundaryless career (Arthur, 1994) becomes a useful concept here as it incorporates an understanding of inter-organisational mobility. This is important in the financial sector as the multi-organisational CV is a key factor in highly skilled professional careers (Beaverstock, 2002). Also for the less skilled migrant, career progress is possible at a more rapid pace when changing employers in the sector: faced with the skills shortages discussed already, employers will consider hiring candidates with less experience.

It is also interesting to follow the way recruitment agencies operate in different European labour markets, using employers’ difficulties with staffing and the migrants’ strategies. As mentioned in the previous section, some of the recruitment agencies that sought to source candidates in Eastern and Central Europe for positions in Western Europe are now in the process of launching recruitment campaigns attracting migrants to return to their countries of origin. Employers ‘back home’ seem to value the skills and English language knowledge acquired abroad. Thus another research question might focus on migrants decisions to return to their country of origin; and if they do, how their situation in the labour market changes.

References Arthur, M. B. 1994. ‘The boundaryless career: a new perspective for organizational

inquiry. Journal of Organizational Behavior 15: 295 - 306.

Beaverstock, J. V. and J. T. Boardwell. 2000. ‘Negotiating globalisation, transnational corporations and global city financial centres in transient migration studies.’ Applied Geography 20: 277-304.

Beaverstock, J. V. 2002. ‘Transnational elites in global cities: British expatriates in Singapore's financial district.’ Geoforum 33: 525-538.

Castells, M. 2000. The Information Age: Economy, Society and Culture, Vol. 1: The Rise of the Network Society. Oxford: Blackwell.

Cetina, K. K. and A. Preda 2005. ‘Introduction’. In K. K. Cetina and A. Preda. The Sociology of Financial Markets. Oxford, Oxford University Press. pp. 1 - 16.

CSO 2006. National Employment Survey 2003. Dublin: CSO.

CSO 2007a. Census 2006, Principal Economic Status and Industries. Dublin: CSO.

CSO 2007b. Census 2006, Principal Socio-Economic Results. Dublin: CSO.

CSO 2007c. Earnings and Labour Costs, CSO. Quarter 4 2005 - Quarter 3 2006 (Final), Quarter 4 2006 (Preliminary Estimates).

CSO 2007d. Earnings and Labour Costs, CSO. Quarter 4 2006 - Quarter 1 2007 (Final), Quarter 2 2007 (Preliminary Estimates).

CSO 2007e. National Employment Survey 2006. CSO. Dublin.

Deloitte 2004. Study on the Future of the International Financial Services Sector in Ireland. Dublin: Deloitte and IDA Ireland.

European Business: Facts and figures - 2007 edition. 2007 Luxembourg, Office for Official Publications of the European Communities.

FAS. 2007. Irish Labour Market Review 2007. Dublin: FAS.

Finance Dublin Yearbook. 2007. Ireland's International Financial Services Industry 2007. (Retrieved 10 January 2008) http://financedublin.com/yearbook/ifs_and_economy.php.

High Fliers Research. 2007. The Ireland Graduate Careers Survey 2007. Dublin: High Fliers Research Ltd & Irish Times.

IBEC. 2007. ‘FSI welcomes reform of migration procedures.’ (Retrieved 18 February 2008), http://www.ibec.ie/ibec/press/presspublicationsdoclib3.nsf/wvPCICCC/9488A8C905935D128025726D00558107?OpenDocument.

Irish Bankers Federation. 2007. Employment Statistics, IBF. (Retrieved 18 February 2008) http://www.ibf.ie/researchset.html

Keenan, B. 2007. ‘Reports of the services sector's demise are greatly exaggerated..’ Irish Independent.

McDowell, L., D. Perrons, et al. 2005. ‘The contradictions and intersections of class and gender in a global city: placing working women's lives on the research agenda.’ Environment and Planning 37: 441 - 461.

22

Expert Group on Future Skills Needs. 2007. Future Skills and Research Needs of the International Financial Services Industry. Dublin: Expert Group on Future Skills Needs.

O’Toole, R. 2008. National Irish Bank Economic Focus report, Spring 2008. Dublin: National Irish Bank.

Özbilgin, M. F. and D. Woodward. 2004. ‘'Belonging' and 'Otherness': Sex Equality in Banking in Turkey and Britain.’ Gender, Work and Organization 11(6): 668 - 688.

Regini, M. 1999. ‘Comparing Banks in Advanced Economies: The Role of Markets, Technology, and Institutions in Employment Relations.’ In M. Regini, J. Kitay and M. Baethge (eds) From Tellers to Sellers. Changing Employment Relations in Banks. Massachusetts: The MIT Press.

Robert Half International. 2007. Global Financial Employment Monitor 2007 - 2008, (Retrieved 18 February 2008) http://www.roberthalf.net/GfxUser/RHI/GFEM_UK.pdf.

Sassen, S. 2004. ‘The Global City. Strategic Site/New Frontier.’ In L. Benería and S. Bisnath (eds) Global Tensions. Challenges and Opportunities in the World Economy. New York and London: Routledge. pp 259-274.

Sokol, M. 2007. ‘Space of Flows, Uneven Regional Development, and the Geography of Financial Services in Ireland. Growth and Change 38(2): 224 - 259.

Soros, G. 2008. ‘The worst market crisis in 60 years’. Financial Times. http://www.ft.com/cms/s/0/24f73610-c91e-11dc-9807-000077b07658.html

Webster, J. 2001. Final Thematic Report - Retail Financial Services. SERVEMPLOI – Innovations in Information Society Sectors: Implications for Women’s Work. (Retrieved 20 February 2008) http://www.tcd.ie/ERC/pastprojects/servemploidownloads/Servemploi%20Financial%20Services.pdf

Westergaard, J. 1984. The Once and Future Class. In J. Curran. The Future of the Left. Cambridge: Polity Press & New Socialist. pp 77 – 89.

Wickham, J. et al. 2008. ‘Migrant Workers and the Irish hospitality sector’. (Retrieved 20 March 2008) http://www.tcd.ie/immigration/css/downloads/MCA110208Report.pdf

Yeandle, M. M. Mainelli and I. Harris. 2008. The Global Financial Services Index – 3. City of London Corporation. (Retrieved 20 March 2008) http://www.zyen.com/Knowledge/Research/GFCI%203%20March%202008.pdf

23

24

Appendix: Statistical Sources

All statistics presented in this report on employment in the financial services sector derive from four primary sources from the Central Statistics Office: the Census (2002, 2006), the Quarterly National Household Survey (QNHS) (2001, 2006), the National Employment Survey (2003, 2006) and the Earnings and Labour Costs Survey (various years).

Tables where the source is given as ‘QNHS micro-data’ are derived from our own analysis of the QNHS micro-data provided by the Irish Social Survey Data Archive; we acknowledge permission for the use of the Central Statistics Office - QNHS Microdata Files © Government of Ireland. All other tables are derived from the published tabulations by the CSO.

• Census 2002 & Census 2006 The Census offers comparative data between 1996, 2002 and 2006, though gives only general numbers on those employed within the sector. The categories relevant for this report include 65 - 67 Banking and Financial Services (65 Banking and financial services, except insurance and pension funding; 66 Insurance and pension funding; 67 Activities auxiliary to banking and financial services)

• Quarterly National Household Survey (QNHS) The QNHS is a sample survey of Irish households carried out by the CSO four times a year. The data used include Quarter 2 of 2001 and Quarter 2 of 2006. The CSO has re-weighted the QNHS data in line with the 2006 Census, since comparison of the Census and the QNHS suggests that the QNHS, as a household survey, systematically under-counts immigrants. However, the QNHS micro-data which was available to us for analysis for this report had not been re-weighted. The 2006 QNHS micro-data analysed in this report therefore under-estimates the number of migrants.

• National Employment Survey (NES) from March 2003 and March 2006 NES is a workplace survey conducted by the CSO. Survey results are weighted to the population of employees from the Quarterly National Household Survey (QNHS).

• Earnings and Labour Costs Survey Two main reports from the Earnings and Labour Costs Survey were drawn on for analysis in this report.

1) Quarter 4 2005 – Quarter 3 2006 (Final) Quarter 4 2006 (Preliminary Estimates)

2) Quarter 4 2006 – Quarter 1 2007 (Final) Quarter 2 2007 (Preliminary Estimates)

The survey includes NACE Sections: C (Mining & quarrying), D (Manufacturing), E (Electricity, gas and water supply) and J (Financial intermediation).