Embed Size (px)

Citation preview

The University of Melbourne

Faculty of Architecture, Building & Planning

ABPL 90026 Property Development

Assignment 2

Lecturer: Dr Georgia Warren-Myers

Tutor: Kusal Kusal Nanayakkara

Semestre 1, 2016

Team: X Investments Property Group

Miguel Angel Garcia Escobar (733188)

Daniel Acheampong (723452)

Chen Zhe (812286)

XiXi Zhou (794728)

THIS PAGE IS INTENTIONALLY LEFT BLANK

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

I

Table of Contents

Assignment 2 ........................................................................................................................................ 1

1 Executive Summary ....................................................................................................................... 1

2 Project Overview ............................................................................................................................ 2

3 Feasibility Assessment. Residual land value analysis .................................................................. 5

4 Comparative analysis .................................................................................................................. 16

5 Feasibility Assessment - Profit analysis ...................................................................................... 18

6 Scenario analysis ......................................................................................................................... 20

6 SWOT analysis ............................................................................................................................. 28

7 RISK ANALYSIS ........................................................................................................................... 30

8 Conclusions & recommendation ................................................................................................. 32

9 Bibliography ................................................................................................................................. 33

Appendix ......................................................................................................................................... 34

Appendix a - Sales in Carlton ......................................................................................................... 35

Appendix B - Sensitivity of assumptions ........................................................................................ 38

Appendix C - Sensitivity of costs .................................................................................................... 40

Appendix D - Case Scenario: Sustainability ................................................................................... 42

Appendix E - Case Scenario: Affordable Housing ......................................................................... 47

Appendix F - Case Scenario: Government Intervention ................................................................. 56

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

II

THIS PAGE IS INTENTIONALLY LEFT BLANK

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

1

Assignment 2

1 Executive Summary

This report is a financial analysis and a development proposal for the property at the site of

227-229 and 231 Queensberry Street, Carlton VIC. We propose the development for 12

floors within 2 floors of parking spaces. The land is 442m². There are five types of

apartments. The size of each type is from 35m² to 70m² and the sales price is from 6500$/m²

to 9200/m².

A residual land value was undertaken by reviewing the different costs associated with these

development. Comparable properties were analyzed to review this RLV, and then a profit

analysis was made using this new information.

The following table shows the expected values for the development

Land residual value $3,873,181

Net land value from comparable $2,500,000

Gross Revenue $27,651,000

Net Realization Value $26,268,450

Construction Cost $16,277,939

Total Cost $19,303.641

Developer’s Profit $6,964,809

Profit Margin 27%

Floors 12 stories

Parking Space 2 underground parking levels

No. of Apartments 67

Sellable Square Metres 3865 m²

Gross Building Area 4547m²

Building Efficiency 85%

Gearing 80%

Image 1. Financial Summary.

A sensitivity analysis was made were we have found that the profit margin of our

development is highly sensitive to the building efficiency, the construction and sales price.

Three additional scenarios were studied, where sustainable features were added, affordable

housing was in place and government intervention reduces our building size. This scenarios

were analyzed separately, and financially evaluated. We’ve found that they not have a

hazardous impact, and can be addressed strategically.

After this analysis we recommend to proceed with these development given the

recommendations stated in the body of this report.

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

2

2 Project Overview

Introduction

The project proposal explores planning opportunities, market demand for possible uses,

and the highest and best use options for Apartment units, Student Accommodation, Office

and a mixed -use development. The site includes an obsolete structure which is currently

ripe for redevelopment. The property is located at 227-229 and 231 Queensberry St. with an

area of 442 square meters. The property currently has a subsisting commercial lease but it

is on the market. Subjecting to the Capital City Zone, the project site is allowed for office

use, residential, and retail; but are subject to design, heritage and parking overlays.

Project Name

The Youth Union

Limitations

There are limited restrictions on size of the site as well as car parking space, both issues

would influence the use of property. The height of each floor and the whole building also

limit the future development options.

Design Considerations

Special care should be taken for the proposal of a building that protects the importance of

the façade of 227-229 Queensberry St which subject to Heritage Overlay (HO).

Market Evaluation

Residential market has made a significant contribution to property growth over the past year,

but in the long term, the residential market would face fierce competition and policy

restriction in the coming year, which may to some extent influence the development and

selling process in the future. According to the ANZ-PCA survey reveals the increasing

mortgage rate and expected tighter debt finance would happen in the coming year.

Meanwhile, the foreign buyers continue to play a key role in Australia’s real estate market

and the proportion of overseas investors remains higher in NSW and Victoria, even though

the restriction of FRIB and mortgage limitation revealed, the highly demand for foreign

buyers would not falling dramatically.

In respect to the market in project site, Carlton, which is likely to be an ideal place for both

independent people and students since it is located near the inner city and close to

universities, parks and medical systems. There are 44% residential apartment and about

62% occupied private dwellings rented which mean the apartment is the main market here,

and the demand of renting an apartment is high, which with a slight increasing price from

last year at 2.54%.

However, the commercial property experiences relatively lower rise and higher vacancy rate

(office market in Australia is at 10.5%).

While, through trough investigation abound the project site, the retail market there is facing

a highly vacant situation, except for a coffee bar around the corner and several motor repair

shops. Lack of footfall is the main problem there for retail.

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

3

Target Market

Users

Students nearby who study at the universities, and young professionals who work in Carlton

but not live here, most of them do not have a high weekly income.

Buyers

Investors (especially those international investors from China and Singapore), and First

Home Occupiers (currently renting) who work nearby but still living in a leasing room.

Marketing Strategy

Target the price of apartments to achieve Median Market Price, using a strategy for “young

generations”, in order to give the idea that these homes are better than the existing stock,

but not as luxurious as the other upcoming apartments.

Highest and best use analysis

The following chart is the summary of the analysis of four potential options of the project

site.

Image 2. Highest and best use analysis summary

Based on this information, and doing a comparison of the benefits and complications of all

the options. We have synthesized our decision ranked each of the options on a scale that

goes from the best option (4 stars) to the least good option (1star) for every part of the

feasibility study (physical, legal & financial). Among all of the options, the mid-rise apartment

shares all the convenient and positive conditions of the site without a restrict demand for

car parking spaces and construction request on the physically possible; also with a legally

permission of residential use; and the financial possibility is higher than others due to a

steady increase of population and international students in Carlton, which will induce a rise

of demand for apartments.

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

4

Development strategy

According to the market analysis and HBU, the X property development limited decided to

redevelop the current properties to cost-effectively mid-rise apartment units for sale with few

retail space at the ground floor in line with the perceived market demand and demographic

features of Carlton, through which we could get the highest return with mixed applicable

options of each floor.

Opportunities: the steadily increasing demand on cost- effectively apartments for leasing or

purchasing, through selling off the plan, there is demand and available financing options.

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

5

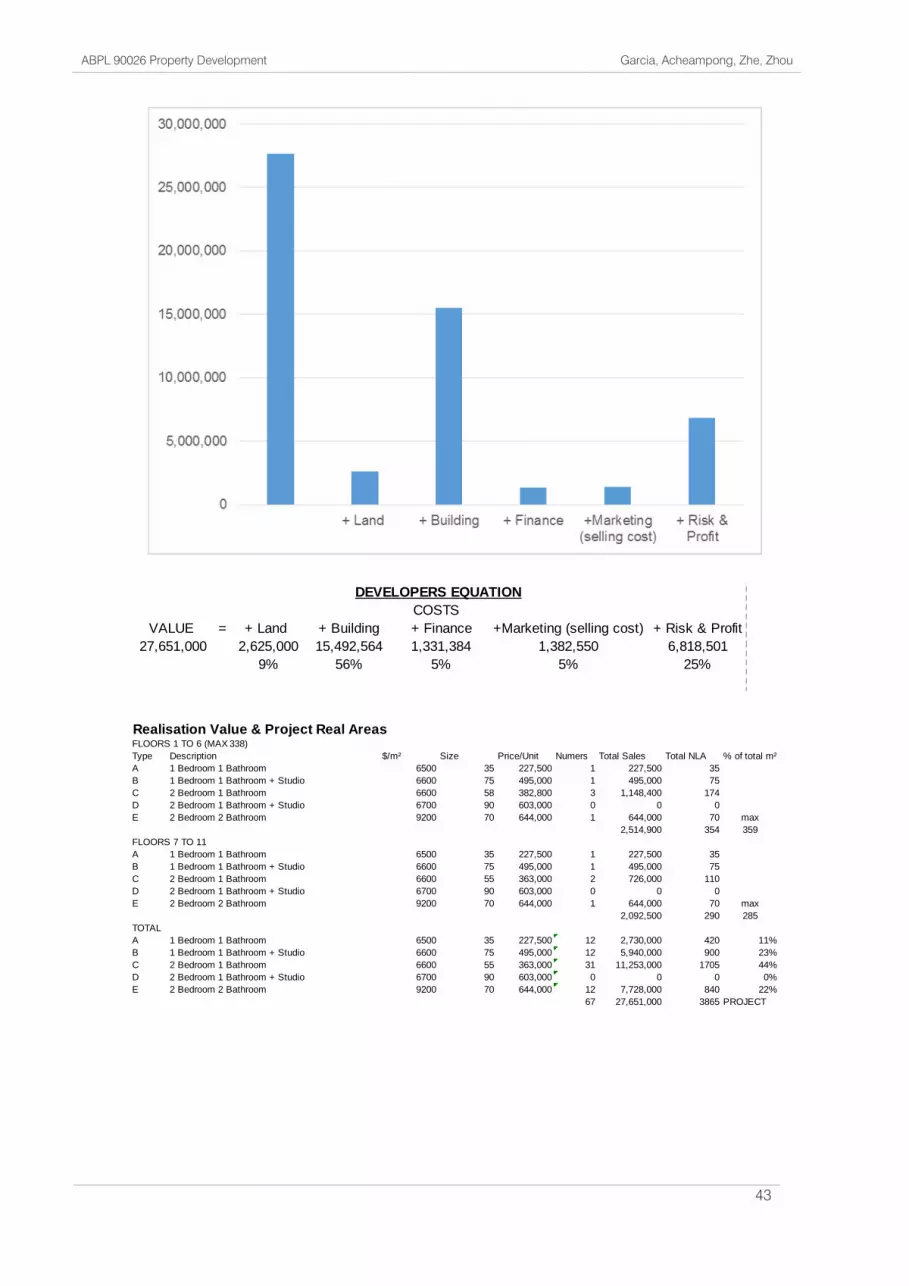

3 Feasibility Assessment. Residual land value analysis

A residual land value financial is been made for our property in order to get the residual land

value at the minimum accepted rate of return.

Residual land value calculation summary

Image 3. Land Residual Value. According to the assumptions made in the body of this report.

The project is yielding $A 26.2 million of Net Realisation Value. Subtracting the cost of

construction at $16.2 million and a developer's profit and risk margin of $5.2 million gives

us a gross residual land value of $ 4.71 million, which includes land finance and purchasing

cost. Calculating land finance at 16% of the total net land value and purchasing costs at 5%

we get a Net Land Value of $3.87 million.

The following is a set of explanations of where this costs were drawn to arrive to this

numbers:

Sales

In order to arrive at the sales, the first step is to calculate the maximum number of sellable

square metres per floor.

Assuming if that both sites are fully used, that we have a building efficiency of 85%, and that

the floor to floor height of the building will be 4m for the ground level and 3.4m for all levels

above, the following schedule can be made.

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

6

Image 4. List of maximum sellable area per floor.

Sellable floor area of each level from ground floor to level 6 will be at a maximum of 359 m²

and 63 m² of common space. After level 7 (passing the 24 m threshold) a setback of 6

metres is required. With a frontage of 14.5m the required setback will lessen our total floor

area by 87m², at which point we will have 285 m² of sellable area and 50 of common area.

This set of areas are based on the assumptions (land use, building efficiency) and will be

subject to change according to the design proposal. But this will gave us the base for the

tenant mix in every floor.

Apartment size and price

In order to get the current market price of the project, the selling price of different properties

have been assessed. The following is a summary of the property listings of Appendix A. In

which we obtain a sell rate per square metre of the different types of properties that will be

used for our site.

Image 5. Summary of the properties analyzed to get the selling rates. Refer to Appendix A.

From this information above the following rates have been assumed for our project.

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

7

Image X. Summary of the assumptions for property selling rates based on the comparable properties

in Appendix A.

The assumption is that this properties will not have balconies and any benefit that arises

from the architect’s design will give us a better indication of the value added by the design.

It will be up to the architects’ design to achieve maximum benefit possible within the

constraints of the project.

Gross realisation value

Based on the maximum sellable area per floor, the current rates, and the size proposed for

this apartments the following tenant mix was assumed.

Image 6. Detail figure of gross realisation values used in feasibility studies.

It is worth noting that although there were other options that would yield higher gross sales,

some of this options didn't aligned with our market strategy and we chose the mix that we

believe will have the best gross realisation and will not increase the difficulty of sales. i.e.

We’ve found that only using 1 bedroom+1 bathroom apartments will yield the most gross

profit based on our assumptions, however this will give us a building with nearly a hundred

apartments, which increases the problems in the buildings for the residents and also

increases the time and difficulty of sale. Also, all of the cost in included in the report are GST

exclusive.

Developers profit and risks

For the purpose of the Residual Land Value model the risk and profit margin required for

this project was set at 25%. This is considering that the project characteristics, some of

them include the land size, the heritage and planning risks, have some particular issues that

will increase the risk premium component of this margin, compared to similar projects. This

characteristics are described in detail in the risk management section of this report.

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

8

Construction costs

Construction costs for this part is divided in 3 major areas: demolition, main building and

underground parking.

PART 1 DEMOLITIONS

Image 7. Estimate of demolition costs.

The demolition costs for this site will add up to around $A 100,000. For the purposes of this

model this prices will not considering the additional costs that may arise from trying to

preserve the facade of the building in order to comply with the design of the building that

will help the heritage overlay. It is advised that an estimate of this costs will be addressed

with a chartered quantity surveyor once the design phase is finished in order to adjust

accordingly. ,

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

9

PART 2 MAIN BUILDING.

Image 8. Estimate of main building costs.

The building price for this project will cost. A$ 11.3 million. This includes a contingency cost

of $A 283K. The type of materials included in this project will include the mid-range finishes,

as the project is not aimed to be luxury apartments.

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

10

PART 3 UNDERGROUND PARKING

Image 9 Estimate of car parking construction costs

Summary of construction costs

Although the underground parking is part of the main building, it is separated in order to

consider removing it in the financial options, as the price of the apartments stated above

does not include any parking space but is still consider on the cost. This is an important

assumption because the base case we are modelling is a relatively conservative

approach. Statutory costs are set at 1% of the total construction costs, this will include cost

of applying for permits related to the development.

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

11

Image 10. Summary of construction costs.

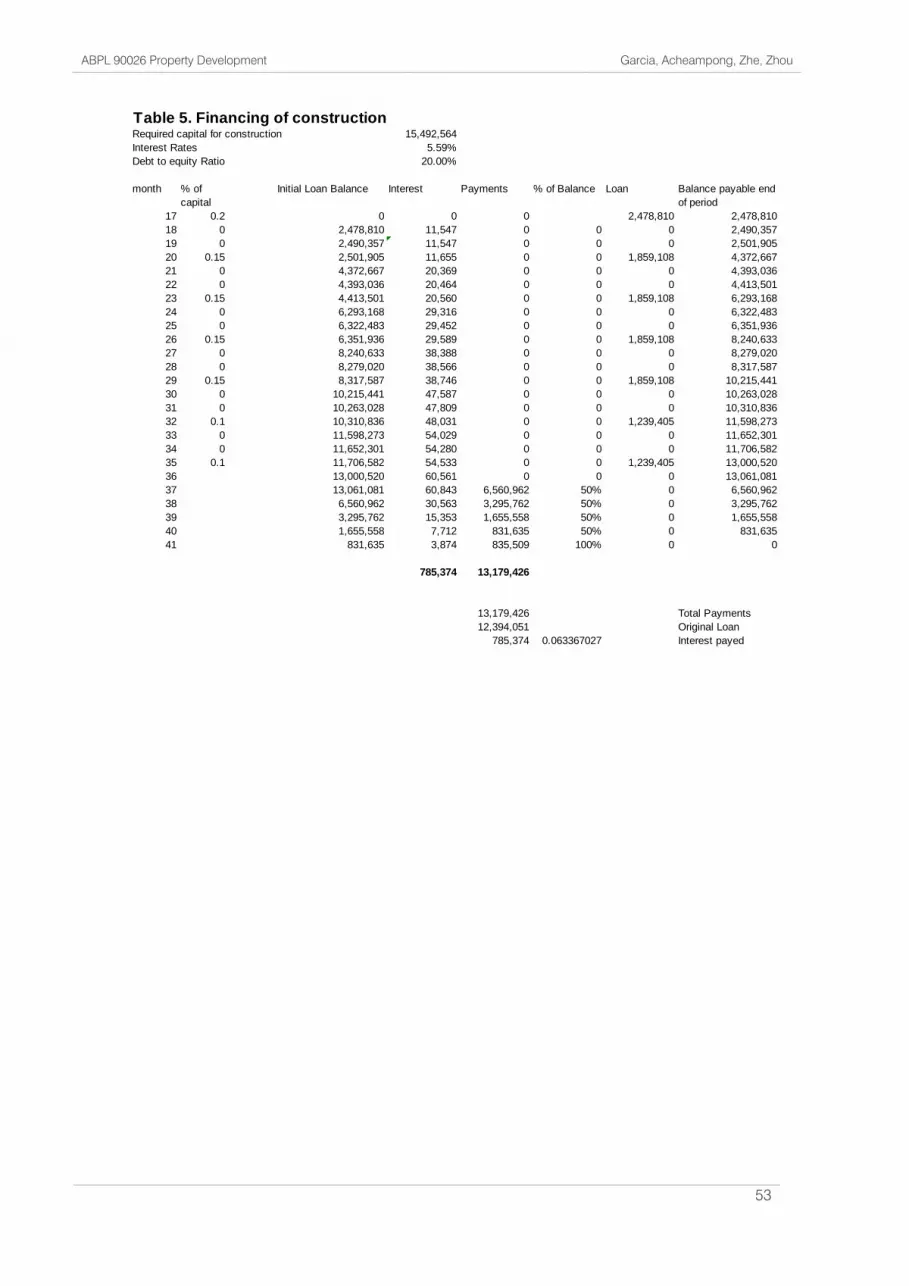

Construction finance

The assumed interest of the project was 5.59%, which is slightly above of the land finance

due to the lack of security for the loan. The project will be debt financed by 80%. For this

financial model we have used an estimated schedule of payments for the project. Where

the loan borrowings are made quarterly. After month 36 of this where practical completion

of the project is achieved, the income from pre sales will be available. However, in order for

the firm not to run out of cash, after practical completion it is recommended to make

payments of 50% of the loan balance per month until all units have been sold.

Image 11. Schedule of financing of construction. Where the amount is borrowed every 3 months.

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

12

Image 12. Graph that shows the loan balance (y axis) at the end of the month (x axis).

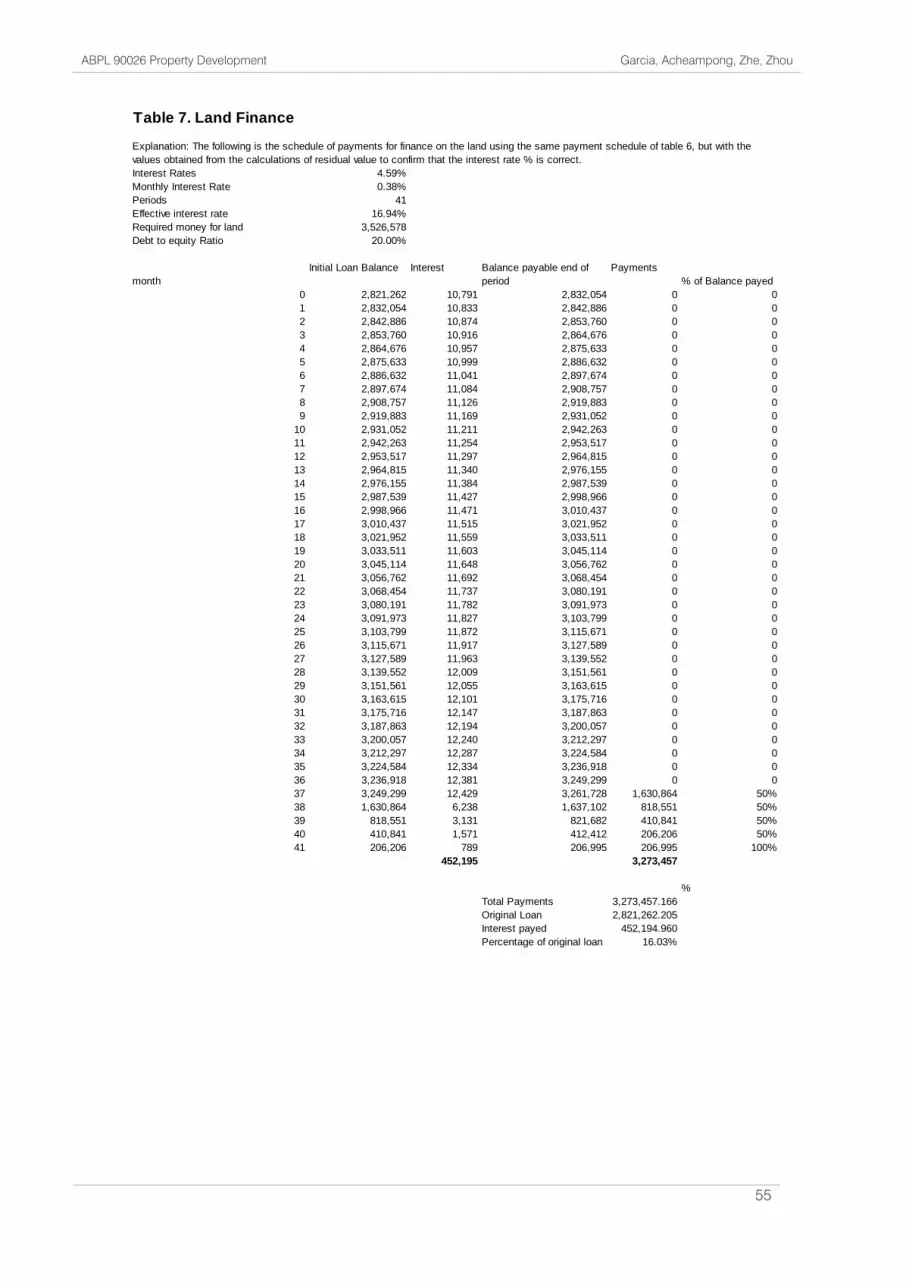

Land finance

Explanation: The following is the schedule of payments for finance on the land. A value of

one dollar has been used in order to get the % of real interest payed in relation to the original

loan amount. So that, we can get the total percentage over the land costs using this

schedule.

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

13

Image 13. Schedule of financing of construction for $1, in order to obtain the percentage of interest

paid over the balance required.

With this percentage we can get the interest from the gross realisation value. (GRV/(1+real

interest on land). The actual amount of Gross Land Value without finance is placed in the

same schedule and calculated in order to corroborate this information.

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

14

Image 14. Schedule of financing of construction using the calculated values.

Other assumptions

The schedule presented below is the set of inputs and assumptions made in the financial

model that lead to the results stated above. The interest rate of land is assumed at 5%

based on the costs at different banks at current times. Cost for financing construction is

considered riskier and therefore has a slightly higher rate.

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

15

Image 15. Schedule of assumptions made for the proposal

Building efficiency is currently estimated at 85% however this may be subject to change

depending on the different design proposals made by the architects. We believe a more

efficient design can be achieved.

Selling costs is currently at 2.5% for agents, however an additional 2.5% is considered due

to the additional marketing material that might be required (advertisements, brochures,

design models, website, etc.) Similarly and as a reference CBRE considers 5% average

selling costs.

The equity put in the project is assumed to be at 20%. We consider that the property being

in such a favourable site allows the project to be slightly leveraged.

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

16

4 Comparative analysis

This analysis is based on development sites that have recently exchanged hands in Carlton and around the fringes of the Melbourne city centre. In essence, we focused on similar properties which has been sold recently, and using the evidence of those transactions to access the value of our development site. The sales data was obtained from various Estate Agency and internet sources (Refer to Reference list).

Trend of values in Carlton and environs: evidence of comparable

1. 202 - 204 Drummond street, Carlton VIC 3053 ; a terrace dwelling which is ripe for

redevelopment, was sold through private treaty for an estimated price of $2,200,000.00 in

February,2016.It has similar features to the subject property and the land area is 536 m² .

2. 128 - 130 Lygon Street, Carlton VIC 3053 is also a retail property which has a

redevelopment potentials. The property was auctioned for $ 1,870,000.00 subject to a 5

years lease which commenced in November, 2012. The Land area is 230 m² and the

property was sold in June, 2015.

3. 140-142 Station Street, Carlton VIC 3053 is a residential premises which was auctioned in

May 2016 for an estimated price of $ 1,800,000.00. The property has a Land area of 352

m².

4. 12 / 121 Cardigan Street, Carlton VIC 3053 is an office property with an existing long term

lease which will expire in 2021. The property has a land area of 214 m² and it was auctioned

for an estimated price of $1,200, 000.00 in September, 2015. The comparable has a

redevelopment potentials.

5. 605 - 609 King Street, West Melbourne is a residential property which has a redevelopment

potential. It was sold through a private treaty for a price of $ 1,800,000.00 in February, 2016.

The property has a Land area of 781 m².

Assumptions essential for effective comparison

Adjustments on the units of comparison are made relative to the development site (227-

229,231 Queensberry St., Carlton VIC 3053); that is the comparable data are adjusted as

though we want to make the comparable development sites identical to the subject. Factors

that are considered for adjustments are similarities and dissimilarities in regards to:

Location; accessibility

Physical features; land area, existing use and facilities.

Time of transaction; changes in market indicators.

Conditions of sale; private treaty or auction.

Development potentials.

Positive features that the comparable possess relative to the subject are negatively adjusted

and negative features are given positive adjustments. Rates for adjustments are subjective

and based on the level of similarity.

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

17

Comparable data analysis

Item Subject

Property

Comparable Properties

1 2 3 4 5

Location Carlton Carlton Carlton Carlton Carlton West

Melbourne

Date of sale February

2016

June 2015 May 2016 September

2015

February

2016

Existing use Commercial Residential Retail Residential Mixed Residential

Land area (m²) 442 536 230 352 214 781

Price $ 2,200,000 1,870,000 1,800,000 1,200,000 1,800,000

Adjustments

Sales date 2% 6% +5% +2%

Size 2% 5% 2% +4% 8%

Accessibility 2% -1%

Condition of sale +5% +5% +5%

Interest rates/

Market condition

+1% +4% +4% +1%

Existing Lease +2% +4%

Net +1% +20% +7% +22% -6%

Adjusted Price $ 2,222,000 2,244,000 1,926,000 1,464,000 1,692,000

Image 16.Table of comparable properties.

Average of Adjusted prices = $1,909,600

Opinion of value

It is our considered opinion that the Value of the subject is $1,909,600. But comparing this

value with the value obtained using the Residual approach, we will be prepared to pay

$2,500,000.00 for the proposed development site.

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

18

5 Feasibility Assessment - Profit analysis

Image 17.Graph using the developers’ equation for the base proposal. (Percentages are based on Gross Sales.)

Based on the information from the comparative Analysis, we have determine a value for the

land, then we use this information using the same information in our Residual Model to

calculate our profit analysis. And get more accurate information of the profit margin of the

development.

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

19

Image 18. Summary of profit analysis.

From the summary above the total profit of the development will be $6.9 million AUD. That

means that the profit margin is 27% as a percentage of the net realisation value. Based on

the expectations of profit margin, the proposal will exceed slightly the expected profit

margin.

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

20

6 Scenario analysis

Sensitivity analysis

In order to assess the impact of the assumptions made in the base case scenario a

sensitivity analysis was made. The information is detailed in appendix B and C. This

appendix show in detail the sensitivity of the assumptions made and the costs and revenues

calculated in the base case respectively.

Sensitivity of the assumptions

Assuming a 10% change positively and negatively in the input value of the assumptions

made on the base model we can recalculate the model in order to get the new profit margin.

The following graph shows in the y axis, the new profit margin if the assumption is changed

(in the x axis). The most sensitive assumption, using this method, is the Building Efficiency,

which was calculated at 85%. As in the appendix B, a change in 10% of the building

efficiency (93.5% efficiency) would give us a Profit Margin of 31.8%.

The change in the levels of parking (which implicates an impact in the building costs) is the

next sensitive assumption, followed by consultant fees and selling costs.

Image 19.Sensitivity analysis of the assumptions made in the model. For more detail refer to Appendix B & C

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

21

Sensitivity of the costs (revenues)

The same methodology was used to assess the sensitivity of the costs in the project, where

the input values were modified by an increase and a decrease in 10% ceteris paribus, to

assess the impact that any possible variations would have on the Profit Margin.

Image 20. Table of sensitivity analysis of the costs made by the project. For more detail refer to Appendix B & C

As expected, the most sensitive elements where the Sales Revenue and the cost of construction of construction. A 10% increase in the sales revenue of the project, ceteris paribus, leads to an increase in profit margin up to 33. %.

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

22

Sustainability scenario

Sustainability has become more and more important for the modern society to think the

environment that we live around. However, it is a challenge to promote a sustainable

building and increase its market value as well. In general, sustainable construction is more

practical than other action. As the buyers’ awareness of sustainability has been improved

significantly in recent years, people may know that sustainability would have the positive

impact on the health, productivity and efficiency. These features would lead to a monetary

savings in the operation of the building. As a result, the property value would be improved

in that case. According to the Moran (2010), the market demand for sustainable buildings

has increased to 40% in 2008 in America. For the property value, decreased operating costs

is one of the most significant value to the use of the green building. Even the property price

for the green building may be a little higher for the potential buyer, they will save the money

as a long-time view, because they may spend less on operating costs. Basically, green

building can reduce 30% utility bills than conventional one. Based on this we are assumed

that added features in sustainability can increase our sales price by 6%.

However, this features will increase the cost of construction and the time required for the

proposal. Studies has shown that an increase due to sustainability components in the

building can increase the price of the construction by 10 up to 20%.

Image 21. Summary of profit analysis using a sustainable scenario. 6% increase in revenue. 10% increase in cost.

And 2 additional months which are reflected in the interest costs.

Although time vary from project to project, we have factored sustainability in our

development timelines and strategy. In the static model that is been presented it will not

have a high impact as time will only affect the interest costs. We have basically considered

an allowance for any construction or design variations as well as overheads.

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

23

Affordable housing scenario

Image 22. Table of total apartments in the building, including an allowance of 29.37% of the building, via 25

apartments in the “Social Housing” table. Which is equivalent to 7.4 million dollars.

Some city councils in the Melbourne metropolitan area have considered government polices

where affordable housing is contained in this project. Recently, the council of Melbourne

aim to create about 1700 new affordable homes in the inner-city by 2021. How to well

managed and cost effective with the ability to meet low-income community need, without

adding an excessive burden on the taxpayer could be a problem the policy maker should

to tackle with. We are to consider a scenario where the government require us to give 30%

of the project as affordable housing.

Under this scenario, the new apartments valued almost 7.4 million will be taken by

government or social housing communities, which will be rented or brought by low-income

residents. As a compensation, the government or communities may pay the cost prices of

these 25 apartments to the developer. As a result, the profit of this scenario will be negative

(-2%) and rarely developer will undertake that project.

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

24

Image 23.Summary of the project using a full allowance of 30% of the building, ceteris paribus. Losses would be

500K.

Alternatively, the newest document issued by Victorian Public Tenants Association on

February 2016 stipulated a possible strategy for a development site includes a certain

percentage of affordable housing, which will be more acceptable by developers,

government is offering land to developer free of charge and the developer affords the

completed apartments as same value as the provided land to the government or housing

associations.

We are to assume this strategy for our project.

Under this circumstance, the government pays the land cost about $2,500,000 to acquire

this parcel in Carlton, after the completion of this apartment tower, 13 apartments of one

bedroom & one bathroom and 1 apartment with one bedroom & one studio & one bathroom

which valued $3,225,000 in the market then could be taken by government. X still make 29%

profit as well. This will be the win-win scenario for council and the developer, also benefiting

the low-income residents. This can also give us a reputation and improves our social

citizenship and responsibility image.

Image 23. Table using the new strategy. Where the governments buys the land (equivalent to $2.5 million) and 13

apartments are given in exchange, with an equivalent value of $3.2 million. A win-win situation. The government

receives more than what is paying, and our project saves Purchasing costs and land finance in exchange.

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

25

Image 24. Summary of the profit analysis. Where the governments buys the land (equivalent to $2.5 million) and 13

apartments are given in exchange, with an equivalent value of $3.2 million. A win-win situation. The government

receives more than what is paying, and our project saves Purchasing costs and land finance in exchange.

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

26

Government intervention scenario

Image 25. Table of total apartments using a discount in size of 20% in size. 3 storeys were reduced in the building.

During the real development process, stage of getting planning permit might be a dominant

consideration by any developer. While several specific regulations or limitations might occur

within that stage. Related to this project located in Carlton, the city of Melbourne discounted

20% of net leasable area of project site. Under this scenario, 3 floors area would be took off

and the NLA reduced from 3865m² to 2995m², which may saving 4 months construction

period for the whole project, lowering construction costs and financial costs. Given this

circumstance, we loss 16 apartments for selling, reducing sales revenue and project profit

to 22%.

Image 26. Summary of profit analysis, using a reduction in size of the project of 20%. For more detail, refer to the

appendix.

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

27

Scenario comparison

Image 27. Synthesis of the different case scenarios. A percentage change is set to the right of each with respect to

the base case.

The information presented above is a synthesis of the different scenarios. Adding

sustainability features will not decrease our profits by much, assuming that the 6% increase

in sales is achieved. This also has the benefit of improving our branding.

Affordable housing strategies can be a win-win scenario depending on the negotiations with

the council, as providing them with affordable houses while still making the highest profits

in the scenarios. We highly recommend considering this option.

Government intervention will have an impact in our project, as the overall sales, construction

and time will be reduced. However this reduction is bearable and we believe that the risk of

this event happening can be reduced by a good brief with the design team in order to

respect the planning policies.

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

28

6 SWOT analysis

A careful consideration of all the possible scenario show that our project is viable, although

we will be faced with some surmountable minor challenges (see SWOT below). The team

have thoroughly considered and examined the negative possible situations and made

provisions for them.

This analysis depicts the possible strengths, challenges, and opportunities associated with

the proposed development project is presented below.

STRENGTHS (what is good about our project)

WEAKNESSES (what is bad about our project)

Market opportunity

Good location.

CBD Fringe

Cost effectively

Small land area

Sensitive for sales, construction and land value

Planning issues such as height limit

OPPORTUNITIES (what can happened that makes our project better)

THREATS (what can happen that makes our project worse)

Increase in number of students will increase demand for units; that is low vacancy rate.

Constant steady economic growth in Australia

Increased immigrations to Melbourne

Overseas investigation limitation

Unstable Australian dollars

Strengths

The commercial and residential building still have a fierce demand in Melbourne. Apart from

that, good location and CBD Fringe attract international students and young professional to

be the potential buyers. Also, cost effective dwelling benefits for first home buyer and young

generations.

Weaknesses

Small land areas limit the further property development. The project schedule would be over

4 years. It is unclear about how is the market and land value trend during this period. The

property would be sensitive for sales, construction and land value. From the other

perspective, there are also several planning issues. For example, height limit and heritage

overlay would limit the development options in the property development process.

Opportunities

Melbourne is one of the most attractive education places for international students and

Melbourne is top 5 best immigration cities in the world. The property demand for

international students in Carlton is still strong in the next few years, especially for Chinese

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

29

students and other Asian students. Moreover, the constant economic growth in Australia

creates a healthful demand and supply environment for the real estate. We can design the

development project to create a green community in the middle levels which will attract high

demand and enhance our ability to sell -off-the plan, since the bottom line of the

development is closing a deal to meet our expectations.

Threats

According to the Economist (2016), the housing market in Australia is 40% overvalued,

which measured by price to income measures. The Australian banks such as ANZ,

Commonwealth have already ceased to offer loans for overseas’ buyers since April 2016.

Moreover, Australian dollars has experienced depreciation since the second quarter and

the depreciated trend is still going on. Thus, the real purchasing power of local buyers has

plummeted.

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

30

7 RISK ANALYSIS

As a business activity, property development is filled with risks, the greater risk always along

with a bigger project. As a developer, the risks should be taken into consideration not only

the commencement and progress risks like planning risk, land holding cost, construction

risks, market risk, financial risk, etc., but also think about the settlement risks at the end of

the project building progress. While, there are a number of ways to evade or reduce the

risks in whole development program.

Planning risks

Planning risk which will be happened during the planning application period, such as the

repeatedly amended design plan which would bring out the delay of planning permit. So

before commence the subject site project, due diligence of the background and relative

regulations are key roles to smooth the process after. This site belongs to Council, medical,

consultant and education systems as supplement infrastructures to Carlton are preferred.

Meanwhile, the particular consideration about heritage façade may produces different

requests on building design. What’s more, the restriction of car parking space and building

height need more time to plan and get permit. More time and repeat applies for planning

permit would put off the following developing scheme.

Before the proposed period, the thorough due diligence should be taken and the specified

requests and regulations had been figure out. Secondly, the schedule of planning approval

need includes at least 15 days as reserved time for modifications and changes would

happen. This stage usually takes up between 6 and 12 months before achieve development

approval.

Landholding risks

A downturn in the property market, the interest rates rising, and unexpected delay during

the development may leading to increased holding costs until the project is sold. As our site

contains two tenant contracts there, that means before start the actual construction process,

the rent received offsets the holding costs partially during the planning stage.

At the same time, the condition of this site like land contamination would induce a high risk

of developing, not just increase the building time but the cost of investing and solving the

pollution. The soil condition research could not be neglected.

Market demand risks

Once is the development process started, it is fixed in time and location, and the design

aims at a very narrow target market which within an uncertain economic climate. The

demand for residential units in Carlton is expected to rise steadily since the sustaining

increase population and students here. An accurate orientation of target market as the

“young generation” which preferred cost-effective dwellings, which with well-designed

apartment (less space with sufficient and changeable function), well-quality construction

and high-standard marketing effort would dramatically reduce the market risk for our site.

Financial risks

As before mentioned in the report, the potential risk of interest rate rises during the life of

the project over the future 41 months, and any reduction of project life time would lower this

risk.

Lowering the loan-to-value ratio (LVR) on the developer or buyers which means the lender

need to pay more the purchase the land or property and lend less than before, which may

significant impact on the settlement activity, since the site may be using the sell-off-plan

marketing strategy, means during the settlement period, the lowering LVR may increase the

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

31

cost of buyers. Usually, the settlement dispute may be triggered under this circumstance,

which directly influenced on the profit return of this project. Therefore, unlike other agencies

make a promises to buyers they can get a debt as 90%, and only need to pay 10% deposit

at first, our marketing team should inform purchasers of the loan risk in the future, they may

experience 10-15% decrease of the loan proportion, to some extent, mitigate the settlement

risk and financial risk then.

Site risks

Our site is the combined two subject properties 227-229 and 231 Queensberry St, and the

construction area is designed to use the whole area of both parcels, which with 15% area

as the common space and 85% as the net saleable area. There is a building risk if the

construction design utilize more space as the common area, the efficiency may decrease.

In effect, reducing our expected returns.

Construction risks

In respect to the pricing, design, quality and possible delays would lead to variation of

construction cost. Like increasing costs in materials and labors recent years led to higher

construction costs. Or the contractors or builders’ changes during the half way of the

development project. These situations could be relieved by drawn up contracts with a fixed

price carefully as well as the quality and criteria of materials and process. There are a variety

of on-site construction work. On-site work can be highly influenced by the materials overdue,

the workers’ experiences and skills and even weather. Also, occupational health and safety

is another part which have high risk in the construction industry. Any accident on the

construction would stop the whole project. For traditional construction process, poor

communication always exists between design and construction. The construction overdue

would happen in this situation because of several reasons such as wrong documentation

and redesign.

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

32

8 Conclusions & recommendation

This studies have informed our decision to develop a Mid-rise residential development for

sale, after a thorough survey and investigation into what is the best option for the site as

well as the viability of the proposed development project. The market, highest and best use

analysis as well as the feasibility analysis, prove that our intended project will be viable. Meanwhile, we have made provisions for any design, construction, cost and market

variations and these are inherent in our cost estimates, feasibility studies as well as

development strategy. The team examined various scenarios, assessed inherent risks, as

well as predict an unforeseeable market eventualities that may ignite any considerable

variations to our expectations and timelines. In this event, the team have outlined the following recommendations:

1. The team should equip the project manager with management tools and technique

to ensure smooth delivery of the project and work within scope especially financial

(overheads) and timelines.

2. The team should strengthen the marketing base of the project so as to enhance

the presales, a prerequisite for residential development project financing.

3. The planning applications should be facilitated so as to avoid delays and obtain

permits within the timelines scheduled for the entire development process.

4. Through the analysis of three scenarios about sustainability, affordable housing

and government issues, the following outcomes should be considered:

o Sustainability scenario does not affect the project much;

o Government requests about reducing storeys will impact on our project

mildly;

o The affordable housing scenario might be a win-win recommendation if the

government in accordance with our strategy, which will benefit triple-sides:

low-income residents, developer and council (City of Melbourne)

5. We highly recommend negotiations with the council to provide for affordable

housing strategies. To maximize our profits and reputation. From the report we have

confirmed that is a viable option.

6. Sustainability improvements will not have a high impact in cost, but can have a

good impact in reputation. We recommend detailed studies about what

improvements can be design and build, as well as assessing detailed costs

depending on the design.

7. Maximizing the building efficiency will have a great impact in our financial returns,

we recommend to try to achieve a high efficiency by addressing this issue with the

architecture team. Keeping in mind not to sacrifice potential value (loss of

amenities) due to this efficiency objective. A balance is to be achieved.

8. Sell price of the apartments is highly sensitive. In the static model that we

presented, it is not including price escalations, trying to achieve a higher price on

the project as soon as practical completion is achieved is a sound strategy to

maximize our returns.

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

33

9 Bibliography

Australia, C. H. (n.d.). Current funding framework. Retrieved from http://www.chfv.org.au/current-

funding-framework/

City of Port Phillip. (n.d.). Affordable Housing Development Models. Melborune: Commonwealth of

Australia .

Office, S. R. (2016). Metropolitan Planning Levy. Retrieved from State Goverment Victoria:

http://www.sro.vic.gov.au/mpl

Real Estate.com.au. (n.d.). 12/121 Cardigan Street Carlton Vic 3053. Retrieved from Real

Estate.com.au: https://www.realestate.com.au/property/12-121-cardigan-st-carlton-vic-

3053

Real Estate.com.au. (2016, Feb). 202-204 Drummond Street, Carlton, Vic 3053. Retrieved from

Realestate.com.au: http://www.realcommercial.com.au/property-land+development-vic-

carlton-501767386

Realestate.com.au. (2016, June). 128-130 lygon St, Carlton, Vic 3053. Retrieved from

http://www.realcommercial.com.au/property-retail-vic-carlton-501160299

The Age Victoria. (2014, November 14). Melbourne has given away bargaining power to developers

. The Age Victoria.

Victoria Public Tenants Association. (Ferbruary of 2016). A blueprint for Affordable Housing in Victoria.

Melbourne.

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

34

Appendix

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

35

Appendix A - Sales in Carlton

No Picture AddressSize(m2

)Bedroom Bathroom

Car

parking

Bed/Study

roomBalcony Sold Price Sold time Agent Category Floor plan

1

3/26 Little

Cardigan Street

Carlton Vic 3053

1 1 1 1 1 $455,000 16-Apr-16 Hockingstuart Full packaged

2

S1812/570

Lygon Street

Carlton Vic 3053

2 1 1 $255,000 03-May-16EJ Love Real

Estatebasic furnitured

3

301/475

Cardigan Street

Carlton Vic 3053

2 2 1 1 $629,000 16-Apr-16

Nelson

Alexander Real

Estate

Full packaged

4

2005/28

Bouverie Street

Carlton Vic 3053

62 2 2 $555,000 08-Apr-16Royaland Real

EstateFull packaged

5

720/800

Swanston Street

Carlton Vic 3053

1 1 $195,000 21-May-16Lucas Real

Estatebasic furnitured

6

206/101 Grattan

Street Carlton

Vic 3053

2 1 1 1 $545,000 19-May-16Woodards

NorthernFull packaged

7

702/95 Berkeley

Street Carlton

Vic 3053

1 1 1 1 $399,000 04-Apr-16

Nelson

Alexander Real

Estate

Furnitured

http://www.realestate.co

m.au/property-apartment-

vic-carlton-121993902

http://www.realestate.co

m.au/property-apartment-

vic-carlton-121366026

http://www.realestate.co

m.au/property-apartment-

vic-carlton-121502370

http://www.realestate.co

m.au/property-apartment-

vic-carlton-122233578

Website

http://www.realestate.co

m.au/property-apartment-

vic-carlton-120796781

http://www.realestate.co

m.au/property-apartment-

vic-carlton-122205346

http://www.realestate.co

m.au/property-apartment-

vic-carlton-121658386

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

36

8

417/528

Swanston Street

Carlton Vic 3053

1 1 $219,500 30-May-16 Dingle Partners basic furnitured

9

303/70

Queensberry

Street Carlton

Vic 3053

1 1 $159,000 17-May-16

Nelson

Alexander Real

Estate

basic furnitured

10

28/36

Drummond

Street Carlton

Vic 3053

2 1 1 1 $610,000 27-Feb-16Stockdale &

Leggo Full packaged

11

1515/570 Lygon

Street Carlton

Vic 3053

53.7 2 1 1 $275,000 24-Feb-16UniLodge

Australia Pty Ltdbasic furnitured

12

873/488

Swanston Street

Carlton Vic 3053

2 1 2 $260,000 16-Feb-16Brady

Residentialbasic furnitured

13

110/151 Princes

Street Carlton

Vic 3053

2 2 1 1 $478,000 16-Feb-16Stockdale &

Leggo basic furnitured

14

501/488

Swanston Street

Carlton Vic 3053

32(land

size)2 1 1 $225,000 26-Jan-16 Dingle Partners basic furnitured

15

7/264

Drummond

Street Carlton

Vic 3053

2 2 1 1 $630,000 19-Dec-15

Scott Banks

Real Estate

Group

Full packaged

http://www.realestate.co

m.au/property-apartment-

vic-carlton-122199738

http://www.realestate.co

m.au/property-apartment-

vic-carlton-121655326

http://www.realestate.co

m.au/property-apartment-

vic-carlton-121775894

http://www.realestate.co

m.au/property-apartment-

vic-carlton-120407977

http://www.realestate.co

m.au/property-apartment-

vic-carlton-121602710

http://www.realestate.co

m.au/property-apartment-

vic-carlton-118499991

http://www.realestate.co

m.au/property-apartment-

vic-carlton-121669398

http://www.realestate.co

m.au/property-apartment-

vic-carlton-121412190

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

37

16

600B/640

Swanston Street

Carlton Vic 3053

84 2 2 1 1 $670,000 10-Dec-15Golden Hills

Property Groupbasic furnitured

http://www.realestate.co

m.au/property-apartment-

vic-carlton-120033985

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

38

Appendix B - Sensitivity of assumptions

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

39

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

40

Appendix C - Sensitivity of costs

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

41

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

42

Appendix D - Case Scenario: Sustainability

Profit Analysis Sustainability Scenario Description: $

REVENUE

Sales 27,651,000

Increase due to sustainability 1,659,060

Less Selling costs 1,382,550

NET REALISATION VALUE 27,927,510

.

Construction cost

Construction Cost * 13,957,265 50%

Consultant Fees * 1,395,727 10%

Construction Finance 908,449 7%

Statutory Costs * 139,573

Developers' Contribution 18,144

16,419,157

Add. Sutainability 1,641,916

Total Construction Costs 18,061,073.03

Land Cost

Net Land Value * 2,500,000

Purchasing costs * 125,000 5%

Land finance 422,936

3,047,936

TOTAL COST 21,109,009

PROFIT & RISK

Developer's Profit 6,818,501

Profit Margin (profit / net realisation) 24%

(*) used for IRR calculation * debt service ratio

Static IRR calculation:

Total equity required (pv) 3,598,513

Profit (fv) 6,818,501

months required (n) 41

Monthly Interest rate (i) 1.571%

Annual interest rate ( i * 12) 18.85%

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

43

VALUE = + Land + Building + Finance +Marketing (selling cost) + Risk & Profit

27,651,000 2,625,000 15,492,564 1,331,384 1,382,550 6,818,501

9% 56% 5% 5% 25%

DEVELOPERS EQUATION

COSTS

Realisation Value & Project Real AreasFLOORS 1 TO 6 (MAX 338)

Type Description $/m² Size Price/Unit Numers Total Sales Total NLA % of total m²

A 1 Bedroom 1 Bathroom 6500 35 227,500 1 227,500 35

B 1 Bedroom 1 Bathroom + Studio 6600 75 495,000 1 495,000 75

C 2 Bedroom 1 Bathroom 6600 58 382,800 3 1,148,400 174

D 2 Bedroom 1 Bathroom + Studio 6700 90 603,000 0 0 0

E 2 Bedroom 2 Bathroom 9200 70 644,000 1 644,000 70 max

2,514,900 354 359

FLOORS 7 TO 11

A 1 Bedroom 1 Bathroom 6500 35 227,500 1 227,500 35

B 1 Bedroom 1 Bathroom + Studio 6600 75 495,000 1 495,000 75

C 2 Bedroom 1 Bathroom 6600 55 363,000 2 726,000 110

D 2 Bedroom 1 Bathroom + Studio 6700 90 603,000 0 0 0

E 2 Bedroom 2 Bathroom 9200 70 644,000 1 644,000 70 max

2,092,500 290 285

TOTAL

A 1 Bedroom 1 Bathroom 6500 35 227,500 12 2,730,000 420 11%

B 1 Bedroom 1 Bathroom + Studio 6600 75 495,000 12 5,940,000 900 23%

C 2 Bedroom 1 Bathroom 6600 55 363,000 31 11,253,000 1705 44%

D 2 Bedroom 1 Bathroom + Studio 6700 90 603,000 0 0 0 0%

E 2 Bedroom 2 Bathroom 9200 70 644,000 12 7,728,000 840 22%

67 27,651,000 3865 PROJECT

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

44

Table 4. Construction Costs

SUMMARY

Construction Cost

Demoltion 102,770.00

Apartment B. 12,458,941.18

Parking 1,395,554.00

Total Construction Cost 13,957,265.18

Consultant Fees 1,395,727

Statutory Costs 139,573

Total capital required for construction 15,492,564.35

Table 5. Financing of construction Required capital for construction 15,492,564

Interest Rates 5.59%

Debt to equity Ratio 20.00%

month % of

capital

Initial Loan Balance Interest Payments % of Balance Loan Balance payable end

of period

17 0.2 0 0 0 2,478,810 2,478,810

18 0 2,478,810 11,547 0 0 0 2,490,357

19 0 2,490,357 11,547 0 0 0 2,501,905

20 0.15 2,501,905 11,655 0 0 1,859,108 4,372,667

21 0 4,372,667 20,369 0 0 0 4,393,036

22 0 4,393,036 20,464 0 0 0 4,413,501

23 0.15 4,413,501 20,560 0 0 1,859,108 6,293,168

24 0 6,293,168 29,316 0 0 0 6,322,483

25 0 6,322,483 29,452 0 0 0 6,351,936

26 0.15 6,351,936 29,589 0 0 1,859,108 8,240,633

27 0 8,240,633 38,388 0 0 0 8,279,020

28 0 8,279,020 38,566 0 0 0 8,317,587

29 0.15 8,317,587 38,746 0 0 1,859,108 10,215,441

30 0 10,215,441 47,587 0 0 0 10,263,028

31 0 10,263,028 47,809 0 0 0 10,310,836

32 0.1 10,310,836 48,031 0 0 1,239,405 11,598,273

33 0 11,598,273 54,029 0 0 0 11,652,301

34 0 11,652,301 54,280 0 0 0 11,706,582

35 0.1 11,706,582 54,533 0 0 1,239,405 13,000,520

36 0 13,000,520 60,561 0 0 0 13,061,081

37 0 13,061,081 60,843 0 0 0 13,121,924

38 13,121,924 61,126 0 0 0 13,183,050

39 13,183,050 61,411 6,622,230 50% 0 6,622,230

40 6,622,230 30,849 3,326,540 50% 0 3,326,540

41 3,326,540 15,496 1,671,018 50% 0 1,671,018

42 1,671,018 7,784 839,401 50% 0 839,401

43 839,401 3,910 843,311 100% 0 0

908,449 13,302,500

13,302,500 Total Payments

12,394,051 Original Loan

908,449 0.073297138 Interest payed

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

45

Table 6. Land Finance of $1 dollar

Interest Rates 4.59%

Monthly Interest Rate 0.38%

Periods 41

Effective interest rate 16.94%

Required money for land 1

Debt to equity Ratio 20.00%

month

Initial Loan Balance Interest Balance payable end

of period

Payments

% of Balance payed

0 0.80 0.003 0.803 0.000 0

1 0.80 0.003 0.806 0.000 0

2 0.81 0.003 0.809 0.000 0

3 0.81 0.003 0.812 0.000 0

4 0.81 0.003 0.815 0.000 0

5 0.82 0.003 0.819 0.000 0

6 0.82 0.003 0.822 0.000 0

7 0.82 0.003 0.825 0.000 0

8 0.82 0.003 0.828 0.000 0

9 0.83 0.003 0.831 0.000 0

10 0.83 0.003 0.834 0.000 0

11 0.83 0.003 0.838 0.000 0

12 0.84 0.003 0.841 0.000 0

13 0.84 0.003 0.844 0.000 0

14 0.84 0.003 0.847 0.000 0

15 0.85 0.003 0.850 0.000 0

16 0.85 0.003 0.854 0.000 0

17 0.85 0.003 0.857 0.000 0

18 0.86 0.003 0.860 0.000 0

19 0.86 0.003 0.863 0.000 0

20 0.86 0.003 0.867 0.000 0

21 0.87 0.003 0.870 0.000 0

22 0.87 0.003 0.873 0.000 0

23 0.87 0.003 0.877 0.000 0

24 0.88 0.003 0.880 0.000 0

25 0.88 0.003 0.883 0.000 0

26 0.88 0.003 0.887 0.000 0

27 0.89 0.003 0.890 0.000 0

28 0.89 0.003 0.894 0.000 0

29 0.89 0.003 0.897 0.000 0

30 0.90 0.003 0.901 0.000 0

31 0.90 0.003 0.904 0.000 0

32 0.90 0.003 0.907 0.000 0

33 0.91 0.003 0.911 0.000 0

34 0.91 0.003 0.914 0.000 0

35 0.91 0.003 0.918 0.000 0

36 0.92 0.004 0.921 0.000 0

37 0.92 0.004 0.925 0.000 0

38 0.92 0.004 0.928 0.000 0

39 0.93 0.004 0.932 0.466 50%

40 0.47 0.002 0.468 0.234 50%

41 0.23 0.001 0.235 0.117 50%

42 0.12 0.000 0.118 0.059 50%

43 0.06 0.000 0.059 0.059 100%

0 0.935

Total Payments 0.935

Original Loan 0.800

Interest payed 0.135 16.9174%

Explanation: The following is the schedule of payments for finance on the land. A value of one dollar has

been used in order to get the % of real interest payed in relation to the original loan ammount. So that,

instead of using the 50% rule, the payment schedule is used.

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

46

Table 7. Land Finance

Interest Rates 4.59%

Monthly Interest Rate 0.38%

Periods 41

Effective interest rate 16.94%

Required money for land3,946,159

Debt to equity Ratio 20.00%

month

Initial Loan Balance Interest Balance payable end of

period

Payments

% of Balance payed

0 3,156,927 12,075 3,169,002 0 0

1 3,169,002 12,121 3,181,124 0 0

2 3,181,124 12,168 3,193,292 0 0

3 3,193,292 12,214 3,205,506 0 0

4 3,205,506 12,261 3,217,767 0 0

5 3,217,767 12,308 3,230,075 0 0

6 3,230,075 12,355 3,242,430 0 0

7 3,242,430 12,402 3,254,832 0 0

8 3,254,832 12,450 3,267,282 0 0

9 3,267,282 12,497 3,279,779 0 0

10 3,279,779 12,545 3,292,324 0 0

11 3,292,324 12,593 3,304,918 0 0

12 3,304,918 12,641 3,317,559 0 0

13 3,317,559 12,690 3,330,249 0 0

14 3,330,249 12,738 3,342,987 0 0

15 3,342,987 12,787 3,355,774 0 0

16 3,355,774 12,836 3,368,610 0 0

17 3,368,610 12,885 3,381,494 0 0

18 3,381,494 12,934 3,394,429 0 0

19 3,394,429 12,984 3,407,412 0 0

20 3,407,412 13,033 3,420,446 0 0

21 3,420,446 13,083 3,433,529 0 0

22 3,433,529 13,133 3,446,662 0 0

23 3,446,662 13,183 3,459,846 0 0

24 3,459,846 13,234 3,473,080 0 0

25 3,473,080 13,285 3,486,364 0 0

26 3,486,364 13,335 3,499,699 0 0

27 3,499,699 13,386 3,513,086 0 0

28 3,513,086 13,438 3,526,523 0 0

29 3,526,523 13,489 3,540,012 0 0

30 3,540,012 13,541 3,553,553 0 0

31 3,553,553 13,592 3,567,145 0 0

32 3,567,145 13,644 3,580,790 0 0

33 3,580,790 13,697 3,594,486 0 0

34 3,594,486 13,749 3,608,235 0 0

35 3,608,235 13,801 3,622,036 0 0

36 3,622,036 13,854 3,635,891 0 0

37 3,635,891 13,907 3,649,798 0 0

38 3,649,798 13,960 3,663,759 0 0

39 3,663,759 14,014 3,677,772 1,838,886 50%

40 1,838,886 7,034 1,845,920 922,960 50%

41 922,960 3,530 926,490 463,245 50%

42 463,245 1,772 465,017 232,509 50%

43 232,509 889 233,398 233,398 100%

534,071 3,690,998

%

Total Payments 3,690,997.717

Original Loan 3,156,927.078

Interest payed 534,070.640

Percentage of original loan 16.92%

Explanation: The following is the schedule of payments for finance on the land using the same payment

schedule of table 6, but with the values obtained from the calculations of residual value to confirm that the

interest rate % is correct.

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

47

Appendix E - Case Scenario: Affordable Housing

Residual Land Value Calculation. Option Social Housing From: Description: $

VALUE

Table 3 Sales 27,651,000

Table 1 Less Selling costs 1,382,550

NRV withouth allowances 26,268,450

- Social Housing Allowance -3,225,000 .

Net Realization Value 29,493,450

PROFIT & RISK

Table 1 Developer's Profit 5,898,690 28.96%

DEVELOPING COSTS 16,277,939

Table 4 Construction Cost 13,957,265 53%

Table 1 Consultant Fees 1,395,727 10%

Table 5 Construction Finance 785,374 6%

Table 1 Statutory Costs 139,573

Gross Landing Value 4,091,821

LAND COSTS 4,091,821

Table 7 Land finance 565,244

Table 1 Purchasing costs 167,932 5%

Net Land Value 3,358,645

Site m² 422

$/m² 7,959

Static IRR calculation:

Total equity required (pv) 3,803,828

Profit (fv) 5,898,690

months required (n) 41

Monthly Interest rate (i) 1.076%

Annual interest rate ( i * 12) 12.91%

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

48

VALUE = + Land + Building + Finance +Marketing (selling cost) + Risk & Profit

27,651,000 0 15,492,564 785,374 1,382,550 6,747,367

0% 56% 3% 5% 24%

DEVELOPERS EQUATION

COSTS

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

49

Inputs or assumptions

Item From:

A Data Land size 1 242

B Data Land Size 2 180

C = A + B Total Land size 422

D Data GBA of current premises 1195

E Table 3 NLA 3,865

F = D / E GBA 4,547

G = E - F Common Areas 682

H Table 8 Land Value 2,500,000

I Table 6 Interest payed for Land 16.03%

J Input Building Efficiency 85%

K Input Selling Cost 5%

L Input Developers Profit 25%

M Input Consultant Fees 10%

N Input Construction Loan interest Rate 6%

O Input Land Interest Rate 5%

P Input Loan to cost ratio 20%

Q Input Purchasing Costs 5%

R Input Statutory costs 1%

S Input Levels of parking 2.00

T Input Developers' Contribution 0.13%

Table 3 . Realisation Value & Project Real AreasFLOORS GF TO LEVEL 6 (MAX 338)

Type Description $/m² Size Price/Unit Numers Total Sales Total NLA

A 1 Bedroom 1 Bathroom 6500 35 227,500 1 227,500 35

B 1 Bedroom 1 Bathroom + Studio 6600 75 495,000 1 495,000 75

C 2 Bedroom 1 Bathroom 6600 58 382,800 3 1,148,400 174

D 2 Bedroom 1 Bathroom + Studio 6700 90 603,000 0 0 0

E 2 Bedroom 2 Bathroom 9200 70 644,000 1 644,000 70

2,514,900 354

FLOORS 7 TO 11

A 1 Bedroom 1 Bathroom 6500 35 227,500 1 227,500 35

B 1 Bedroom 1 Bathroom + Studio 6600 75 495,000 1 495,000 75

C 2 Bedroom 1 Bathroom 6600 55 363,000 2 726,000 110

D 2 Bedroom 1 Bathroom + Studio 6700 90 603,000 0 0 0

E 2 Bedroom 2 Bathroom 9200 70 644,000 1 644,000 70

2,092,500 290

TOTAL

A 1 Bedroom 1 Bathroom 6500 35 227,500 12 2,730,000 420

B 1 Bedroom 1 Bathroom + Studio 6600 75 495,000 12 5,940,000 900

C 2 Bedroom 1 Bathroom 6600 55 363,000 31 11,253,000 1705

D 2 Bedroom 1 Bathroom + Studio 6700 90 603,000 0 0 0

E 2 Bedroom 2 Bathroom 9200 70 644,000 12 7,728,000 840

67 27,651,000 3865

SOCIAL HOUSING : GOV PAYS LAND STRATEGY

A 1 Bedroom 1 Bathroom 6500 35 227,500 12 2,730,000 420

B 1 Bedroom 1 Bathroom + Studio 6600 75 495,000 1 495,000 75

C 2 Bedroom 1 Bathroom 6600 55 363,000 0 0 0

D 2 Bedroom 1 Bathroom + Studio 6700 90 603,000 0 0 0

E 2 Bedroom 2 Bathroom 9200 70 644,000 0 0 0

13 3,225,000 495

12.81%

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

50

Table 4. Construction Costs

SUMMARY

Construction Cost

Demoltion 102,770.00

Apartment B. 12,458,941.18

Parking 1,395,554.00

Total Construction Cost 13,957,265.18

Consultant Fees 1,395,727

Statutory Costs 139,573

Total capital required for construction 15,492,564.35

PART 1 - DEMOLITIONS

Total square metres for parking

(from table 1) 1,195.00

Phase $/m² % $ total price

Demolitions: Retail premises, two

storrey ditto with reinforced concrete

slab

86

102,770.00

Total 102,770.00

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

51

PART 2 - APARTMENT BUILDING

Apartment type Size Number Total m²

A 35 12 420

B 75 12 900

C 55 31 1705

D 90 0 0

E 70 12 840

Net lettable area 3865

Building Efficiency 85%

Gross building Area 4,547

Phase $/m² % $ total price

PRELIMINARIES 392.25 14.32% 1,783,584

SUBSTRUCTURE 37.00 1.35% 168,241

SUPERSTRUCTURE

Columns 50.25 1.83% 228,490

Upper floors 260.75 9.52% 1,185,646

Staircase 33.00 1.20% 150,053

Roof 36.50 1.33% 165,968

External Walls & Windows 317.75 11.60% 1,444,828

External doors 29.75 1.09% 135,275

Internal Walls 100.75 3.68% 458,116

Internal Screens 10.25 0.37% 46,607

Internal Doors 36.25 1.32% 164,831

FINISHES

Walls 76.00 2.77% 345,576

Floor 88.50 3.23% 402,415

Cielings 49.75 1.82% 226,216

FITTINGS

Firments 166.25 6.07% 755,949

Special 0.00 0.00% -

SERVICES

Plumbing 326.25 11.91% 1,483,478

Mechanical 328.25 11.98% 1,492,572

Fire 48.75 1.78% 221,669

Electrical 112.25 4.10% 510,407

Transportation 146.50 5.35% 666,144

Special 23.50 0.86% 106,856

EXTERNAL SERVICES 1.00 0.04% 4,547

CONTINGENCY 68.50 2.50% 311,474

TOTAL 2,740.00 100.00% 12,458,941

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

52

PART 3 - UNDER GROUND PARKING

Total square metres for parking

(from table 1) 844.00

Phase $/m² % $ total price

PRELIMINARIES 294.25 10.74% 248,347.00

SUBSTRUCTURE 317.00 11.57% 267,548.00

SUPERSTRUCTURE

Columns 68.25 2.49% 57,603.00

Upper floors 151.00 5.51% 127,444.00

Staircase 16.75 0.61% 14,137.00

Roof 226.00 8.25% 190,744.00

External Walls & Windows 152.25 5.56% 128,499.00

External doors 17.50 0.64% 14,770.00

Internal Walls 36.50 1.33% 30,806.00

Internal Screens 0.00 0.00% -

Internal Doors 9.25 0.34% 7,807.00

FINISHES

Walls 16.75 0.61% 14,137.00

Floor 15.00 0.55% 12,660.00

Cielings 15.00 0.55% 12,660.00

FITTINGS

Firments 1.25 0.05% 1,055.00

Special 0.00 0.00% -

SERVICES

Plumbing 39.75 1.45% 33,549.00

Mechanical 104.75 3.82% 88,409.00

Fire 109.00 3.98% 91,996.00

Electrical 61.00 2.23% 51,484.00

Transportation 0.00 0.00% -

Special 0.00 0.00% -

EXTERNAL SERVICES 1.00 0.04% 844.00

CONTINGENCY 1.25 0.05% 1,055.00

TOTAL 1,653.50 60.35% 1,395,554.00

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

53

Table 5. Financing of construction Required capital for construction 15,492,564

Interest Rates 5.59%

Debt to equity Ratio 20.00%

month % of

capital

Initial Loan Balance Interest Payments % of Balance Loan Balance payable end

of period

17 0.2 0 0 0 2,478,810 2,478,810

18 0 2,478,810 11,547 0 0 0 2,490,357

19 0 2,490,357 11,547 0 0 0 2,501,905

20 0.15 2,501,905 11,655 0 0 1,859,108 4,372,667

21 0 4,372,667 20,369 0 0 0 4,393,036

22 0 4,393,036 20,464 0 0 0 4,413,501

23 0.15 4,413,501 20,560 0 0 1,859,108 6,293,168

24 0 6,293,168 29,316 0 0 0 6,322,483

25 0 6,322,483 29,452 0 0 0 6,351,936

26 0.15 6,351,936 29,589 0 0 1,859,108 8,240,633

27 0 8,240,633 38,388 0 0 0 8,279,020

28 0 8,279,020 38,566 0 0 0 8,317,587

29 0.15 8,317,587 38,746 0 0 1,859,108 10,215,441

30 0 10,215,441 47,587 0 0 0 10,263,028

31 0 10,263,028 47,809 0 0 0 10,310,836

32 0.1 10,310,836 48,031 0 0 1,239,405 11,598,273

33 0 11,598,273 54,029 0 0 0 11,652,301

34 0 11,652,301 54,280 0 0 0 11,706,582

35 0.1 11,706,582 54,533 0 0 1,239,405 13,000,520

36 13,000,520 60,561 0 0 0 13,061,081

37 13,061,081 60,843 6,560,962 50% 0 6,560,962

38 6,560,962 30,563 3,295,762 50% 0 3,295,762

39 3,295,762 15,353 1,655,558 50% 0 1,655,558

40 1,655,558 7,712 831,635 50% 0 831,635

41 831,635 3,874 835,509 100% 0 0

785,374 13,179,426

13,179,426 Total Payments

12,394,051 Original Loan

785,374 0.063367027 Interest payed

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

54

Table 6. Land Finance of $1 dollar

Interest Rates 4.59%

Monthly Interest Rate 0.38%

Periods 41

Effective interest rate 16.94%

Required money for land 1

Debt to equity Ratio 20.00%

month

Initial Loan Balance Interest Balance payable end

of period

Payments

% of Balance payed

0 0.80 0.003 0.803 0.000 0

1 0.80 0.003 0.806 0.000 0

2 0.81 0.003 0.809 0.000 0

3 0.81 0.003 0.812 0.000 0

4 0.81 0.003 0.815 0.000 0

5 0.82 0.003 0.819 0.000 0

6 0.82 0.003 0.822 0.000 0

7 0.82 0.003 0.825 0.000 0

8 0.82 0.003 0.828 0.000 0

9 0.83 0.003 0.831 0.000 0

10 0.83 0.003 0.834 0.000 0

11 0.83 0.003 0.838 0.000 0

12 0.84 0.003 0.841 0.000 0

13 0.84 0.003 0.844 0.000 0

14 0.84 0.003 0.847 0.000 0

15 0.85 0.003 0.850 0.000 0

16 0.85 0.003 0.854 0.000 0

17 0.85 0.003 0.857 0.000 0

18 0.86 0.003 0.860 0.000 0

19 0.86 0.003 0.863 0.000 0

20 0.86 0.003 0.867 0.000 0

21 0.87 0.003 0.870 0.000 0

22 0.87 0.003 0.873 0.000 0

23 0.87 0.003 0.877 0.000 0

24 0.88 0.003 0.880 0.000 0

25 0.88 0.003 0.883 0.000 0

26 0.88 0.003 0.887 0.000 0

27 0.89 0.003 0.890 0.000 0

28 0.89 0.003 0.894 0.000 0

29 0.89 0.003 0.897 0.000 0

30 0.90 0.003 0.901 0.000 0

31 0.90 0.003 0.904 0.000 0

32 0.90 0.003 0.907 0.000 0

33 0.91 0.003 0.911 0.000 0

34 0.91 0.003 0.914 0.000 0

35 0.91 0.003 0.918 0.000 0

36 0.92 0.004 0.921 0.000 0

37 0.92 0.004 0.925 0.462 50%

38 0.46 0.002 0.464 0.232 50%

39 0.23 0.001 0.233 0.116 50%

40 0.12 0.000 0.117 0.058 50%

41 0.06 0.000 0.059 0.059 100%

0 1

Total Payments 0.928

Original Loan 0.800

Interest payed 0.128 16.0281%

Explanation: The following is the schedule of payments for finance on the land. A value of one dollar has

been used in order to get the % of real interest payed in relation to the original loan ammount. So that,

instead of using the 50% rule, the payment schedule is used.

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

55

Table 7. Land Finance

Interest Rates 4.59%

Monthly Interest Rate 0.38%

Periods 41

Effective interest rate 16.94%

Required money for land 3,526,578

Debt to equity Ratio 20.00%

month

Initial Loan Balance Interest Balance payable end of

period

Payments

% of Balance payed

0 2,821,262 10,791 2,832,054 0 0

1 2,832,054 10,833 2,842,886 0 0

2 2,842,886 10,874 2,853,760 0 0

3 2,853,760 10,916 2,864,676 0 0

4 2,864,676 10,957 2,875,633 0 0

5 2,875,633 10,999 2,886,632 0 0

6 2,886,632 11,041 2,897,674 0 0

7 2,897,674 11,084 2,908,757 0 0

8 2,908,757 11,126 2,919,883 0 0

9 2,919,883 11,169 2,931,052 0 0

10 2,931,052 11,211 2,942,263 0 0

11 2,942,263 11,254 2,953,517 0 0

12 2,953,517 11,297 2,964,815 0 0

13 2,964,815 11,340 2,976,155 0 0

14 2,976,155 11,384 2,987,539 0 0

15 2,987,539 11,427 2,998,966 0 0

16 2,998,966 11,471 3,010,437 0 0

17 3,010,437 11,515 3,021,952 0 0

18 3,021,952 11,559 3,033,511 0 0

19 3,033,511 11,603 3,045,114 0 0

20 3,045,114 11,648 3,056,762 0 0

21 3,056,762 11,692 3,068,454 0 0

22 3,068,454 11,737 3,080,191 0 0

23 3,080,191 11,782 3,091,973 0 0

24 3,091,973 11,827 3,103,799 0 0

25 3,103,799 11,872 3,115,671 0 0

26 3,115,671 11,917 3,127,589 0 0

27 3,127,589 11,963 3,139,552 0 0

28 3,139,552 12,009 3,151,561 0 0

29 3,151,561 12,055 3,163,615 0 0

30 3,163,615 12,101 3,175,716 0 0

31 3,175,716 12,147 3,187,863 0 0

32 3,187,863 12,194 3,200,057 0 0

33 3,200,057 12,240 3,212,297 0 0

34 3,212,297 12,287 3,224,584 0 0

35 3,224,584 12,334 3,236,918 0 0

36 3,236,918 12,381 3,249,299 0 0

37 3,249,299 12,429 3,261,728 1,630,864 50%

38 1,630,864 6,238 1,637,102 818,551 50%

39 818,551 3,131 821,682 410,841 50%

40 410,841 1,571 412,412 206,206 50%

41 206,206 789 206,995 206,995 100%

452,195 3,273,457

%

Total Payments 3,273,457.166

Original Loan 2,821,262.205

Interest payed 452,194.960

Percentage of original loan 16.03%

Explanation: The following is the schedule of payments for finance on the land using the same payment schedule of table 6, but with the

values obtained from the calculations of residual value to confirm that the interest rate % is correct.

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

56

Appendix F - Case Scenario: Government Intervention

Residual Land Value Calculation. Government Intervention

From: Description: $

REVENUE

Sales 21,291,500

Less Selling costs 1,064,575

NET REALISATION VALUE 20,226,925

.

Construction cost

Construction Cost * 11,023,853 55%

Consultant Fees * 1,102,385 10%

Construction Finance 491,686 4%

Statutory Costs * 110,239

Developers' Contribution 14,331

12,742,494

Land Cost

Net Land Value * 2,500,000

Purchasing costs * 125,000 5%

Land finance 356,743

2,981,743

TOTAL COST 15,724,238

PROFIT & RISK

Developer's Profit 4,502,687

Profit Margin (profit / net realisation) 22%

(*) used for IRR calculation * debt service ratio

Static IRR calculation:

Total equity required (pv) 2,947,295

Profit (fv) 4,502,687

months required (n) 41

Monthly Interest rate (i) 1.039%

Annual interest rate ( i * 12) 12.47%

ABPL 90026 Property Development Garcia, Acheampong, Zhe, Zhou

57

VALUE = + Land + Building + Finance +Marketing (selling cost) + Risk & Profit

21,291,500 2,625,000 12,236,477 848,429 1,064,575 4,502,687

12% 57% 4% 5% 21%

DEVELOPERS EQUATION

COSTS

Inputs or assumptions

Item From:

A Data Land size 1 242

B Data Land Size 2 180

C = A + B Total Land size 422

D Data GBA of current premises 1195

E Table 3 NLA 2,955

F = D / E GBA 3,476

G = E - F Common Areas 521

H Table 8 Land Value 2,500,000