Embed Size (px)

Citation preview

Improving Farmer Agribusiness Market Linkages, the case of Asella Malt Factory and small farmes, Ethiopia

IMPROVING FARMER AGRI BUSINESS MARKET INKAGES THE CASE OF ASELLA MALT FACTORY AND SMALL MALT BARLEY PRODUCER FARMERS, ARSI ZONE, ETHIOPIA

A Research Project Submitted toLarenstein University of Professional Education

in Partial fulfillment of the Requirements for the

Degree of

Master of Management of DevelopmentSpecialization in International Agriculture

By

Beshir Butta

September 2005

Deventer

The Netherlands

© Copyright Beshir Butta Dale, 2005. All right reserved

1

Improving Farmer Agribusiness Market Linkages, the case of Asella Malt Factory and small farmes, Ethiopia

2

Improving Farmer Agribusiness Market Linkages, the case of Asella Malt Factory and small farmes, Ethiopia

DEDICATION

This work is dedicated to my late father Hussein Kel’a, my late brother Ebrahim Butta and my late biological father Butta Dale who have been a protagonist of my study, yet I don’t have a chance to say thank you.

i

Improving Farmer Agribusiness Market Linkages, the case of Asella Malt Factory and small farmes, Ethiopia

ii

Improving Farmer Agribusiness Market Linkages, the case of Asella Malt Factory and small farmes, Ethiopia

Permission to use

In presenting this research project in partial fulfillment of therequirement for a master degree in Management of Development, Iagree that the library of Larenestein University ProfessionalEducation may make it freely available for inspection. I furtheragree that permission for copying of this research project in anymanner, in whole or in part, for scholarly proposes may be grantedby Larenstein Director of Research. It is understood that anycopying or publication or use of this research project or partsthereof for financial gain shall not be allowed without my writtenpermission. It is also understood that due recognition shall begiven to me and to the university in any scholarly use which may bemade of any material in my research project.

Request for permission to copy or make other use of material inthis research project in whole or part should be addressed to:

Coordinator International Education Larenstein University of Professional Education P.O.Box 77416 AA Deventer The Netherlands Fax: +31 570 68 56 08

iii

Improving Farmer Agribusiness Market Linkages, the case of Asella Malt Factory and small farmes, Ethiopia

iv

Improving Farmer Agribusiness Market Linkages, the case of Asella Malt Factory and small farmes, Ethiopia ACKNOWLEDGEMENTS

This study was only possible with a lot of supports I received frommany individuals and institutions. My first sincere gratitude goesto my advisor Prof. A.A.W. van Wulfften Palthe for his constructivecomments, guidance and flexible supervision. I am sincerelygrateful to my co-advisor Dr. Adenine Kutcher for his time,valuable inputs and comments in such a skillful way.

The full flagged scholarship rendered by the Netherlands FellowshipProgram for this study is gratefully acknowledged. I am indebted tomy employer, Ethiopian Agricultural Research Institute, forgranting me leave of absence with pay during my entire two yearsstay overseas.

I would like to express sincere thanks and appreciation to mycolleague Mr.Tessema Abate for his time in coordinating datacollection.

My special thanks and heartfelt gratitude go to my mother WoyaKela, who has raised me and educated me profoundly in the absenceof my father. My mother, you are very special and my hero. Yourlove keeps me going even in difficult situations. Thank you forall. My late father Hussein Kela and late brother Ebrahim Butta,your support and passionate about my study is unforgettableforever. I want also to acknowledge the love and contribution of my twobrothers Amano Butta and Hussein Butta who always love me, careabout me, encourage and support me during all my studies. I gratefully acknowledge all the resource persons of Asella MaltFactory and farmers in Digalu Tijo and Kofale districts for sharingwith me their insightful knowledge without which this thesis wouldbe impossible. Ali Ahmed, I appreciate your friendship of all the time and forbeing with me in Addis during write-up of this thesis project tokeep my company.

i

Improving Farmer Agribusiness Market Linkages, the case of Asella Malt Factory and small farmes, Ethiopia I would like to acknowledge Friends of Foreign Students (FFS)members Ms. Nicole and Mrs. Sjakkelien who made our stay inNetherlands enjoyable and memorable.

My thanks also go to my relatives and friends (Amano Nure, MohammedNure, Hussein Dale, Mohammed Hussein, Jemal Ahmed) for their love,material and moral supports. Above all praise be to almighty ‘Allah’ who is always on my sidewith all my weaknesses by his mercy and graciousness.

Mr. Beshir Butta DALESeptember 2005The Netherlands

ii

Improving Farmer Agribusiness Market Linkages, the case of Asella Malt Factory and small farmes, Ethiopia

TABLE OF CONTENTS

Pages

DEDICATION...............................................................I

PERMISSION TO USE.......................................................II

ACKNOWLEDGEMENTS.........................................................I

LIST OF TABLES...........................................................V

LIST OF FIGURES.........................................................VI

ACRONYMS...............................................................VII

ABSTRACT..............................................................VIII

1. INTRODUCTION..........................................................1

1.1 PROBLEM STATEMENTS....................................................2

1.2 OBJECTIVE OF THE RESEARCH..............................................3

1.3 MAIN RESEARCH QUESTIONS................................................3

1.4 SUB-QUESTIONS........................................................3

1.5 SIGNIFICANCE OF THE STUDY..............................................3

1.6 OUTLINE AND DELINEATION OF THE STUDY....................................4

2. RESEARCH METHODOLOGY..................................................5

2.1 AREA SELECTION.......................................................5

2.2 DATA COLLECTION METHOD................................................5

2.3 CHOICE OF METHODS....................................................6

2.4 DATA ANALYSIS........................................................6

2.5 LIMITATIONS OF THE STUDY...............................................6

3. LITERATURE REVIEW.....................................................7

3.1 GENERAL REVIEW ON AGRICULTURAL MARKETING.................................7

3.1.1 The concept of Agricultural marketing.................................................................................7

3.1.2 Trade in Agricultural commodity...........................................................................................8

3.1.3 Agricultural Commodity Prices..............................................................................................8

iii

Improving Farmer Agribusiness Market Linkages, the case of Asella Malt Factory and small farmes, Ethiopia

3.1.4 The Role of Processors in Commodity Marketing...............................................................9

3.1.5 Marketing Channels for Agricultural Products.................................................................10

3.1.6 The Role of Cooperatives in Agricultural Marketing........................................................10

3.1.7 Infrastructure for Agricultural Marketing.........................................................................10

3.1.8 Market information to Farmers in Developing Countries...............................................11

3.1.8.1 The Benefits of market information to farmers....................11

3.1.8.2 The Weakness of Agricultural Market information in developing

countries................................................................11

3.1.9 The Role of Public Sector in Agricultural and Food Marketing......................................12

3.2 THEORETICAL REVIEW ON FARMER AGRIBUSINESS LINKAGES........................13

3.2.1 Background of Strengthening Farm Agribusiness Linkages..........................................13

3.2.2 Concept and Definition of Farm Agribusiness Linkages.................................................13

3.2.3 Players in Farm-Agribusiness Linkages...................................................................................14

3.2.4 Types of linkages.................................................................................................................... 16

3.2.5 Linking Arrangements between Farmers and Agro-Processors in Africa....................16

3.2.6 Factors Influencing the Strength of the Linkages............................................................18

3.2.7 Benefits on Farmer Agribusiness Linkages........................................................................19

3.2.8 Constraints on Farmer Agribusiness Linkages..................................................................19

3.2.8.1 Internal Constraints on Farmers and Agribusiness.................19

3.2.8.2 External Constraints on Farmers and Agribusiness.................20

3.3 ETHIOPIAN SPECIFIC SITUATIONS.........................................21

3.3.1 Public-Private linkages in Agricultural Development in Ethiopia.................................22

3.3.2 Asella Malt Factory, Research, Farmers partnership in Malt Barley Production.......22

3.3.3 Malt Barley Supply System....................................................................................................23

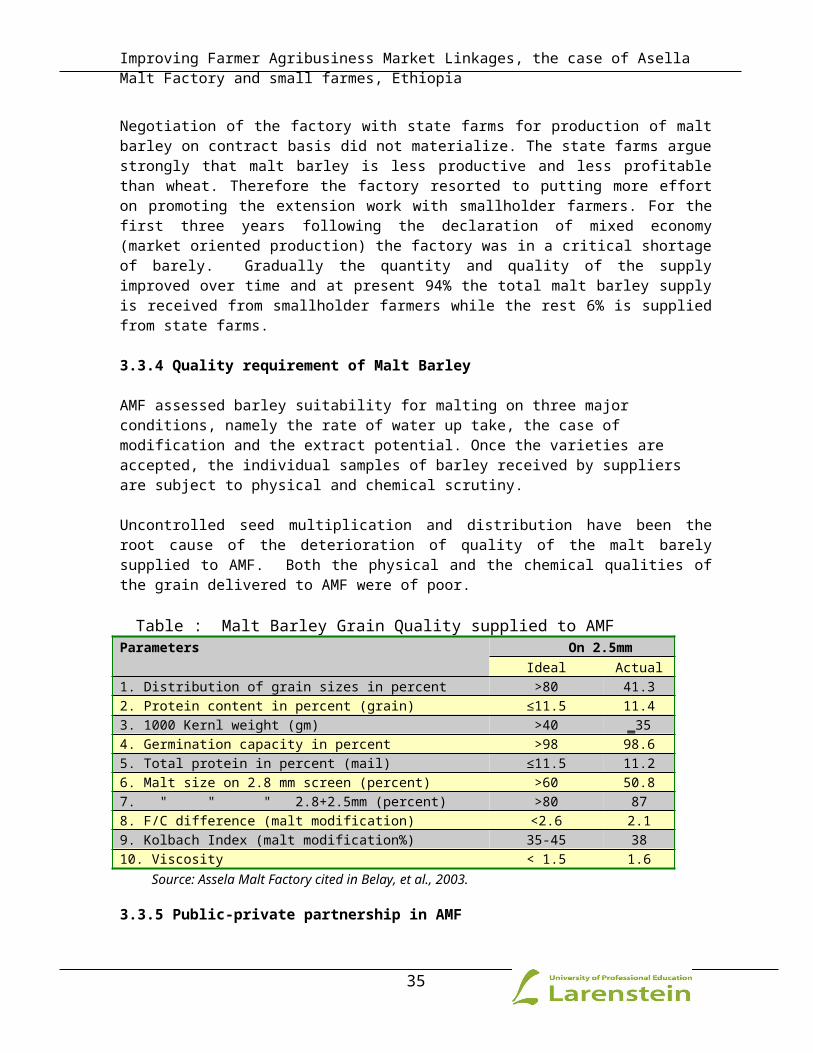

3.3.4 Quality requirement of Malt Barley....................................................................................23

3.3.5 Public-private partnership in AMF...........................................................................................24

4. BACKGROUND AND DISCRIPTION OF THE STUDY AREA.........................25

4.1 COUNTRY BACKGROUND...................................................25

4.1.1 Location and Area................................................................................................................... 25

4.1.2 Socio-economic characteristics............................................................................................25

4.1.3 Agrarian structure (farm size, cash crops/ food crops)...................................................25

4.1.4 Agricultural Marketing..........................................................................................................27

iv

Improving Farmer Agribusiness Market Linkages, the case of Asella Malt Factory and small farmes, Ethiopia

4.1.5 Cooperatives............................................................................................................................ 28

4.1.6 Agro Industry........................................................................................................................... 29

KALITY FOOD PROCESSING FACTORY (KFPF).....................................29

4.2 OVERVIEW OF THE STUDY AREAS...........................................30

4.2.1 Kofale District.......................................................................................................................... 30

4.2.2 Digalu Tijo District.................................................................................................................. 32

4.2.3 Land Tenure System in the study areas.............................................................................33

5. RESULTS AND DISCUSSION...............................................34

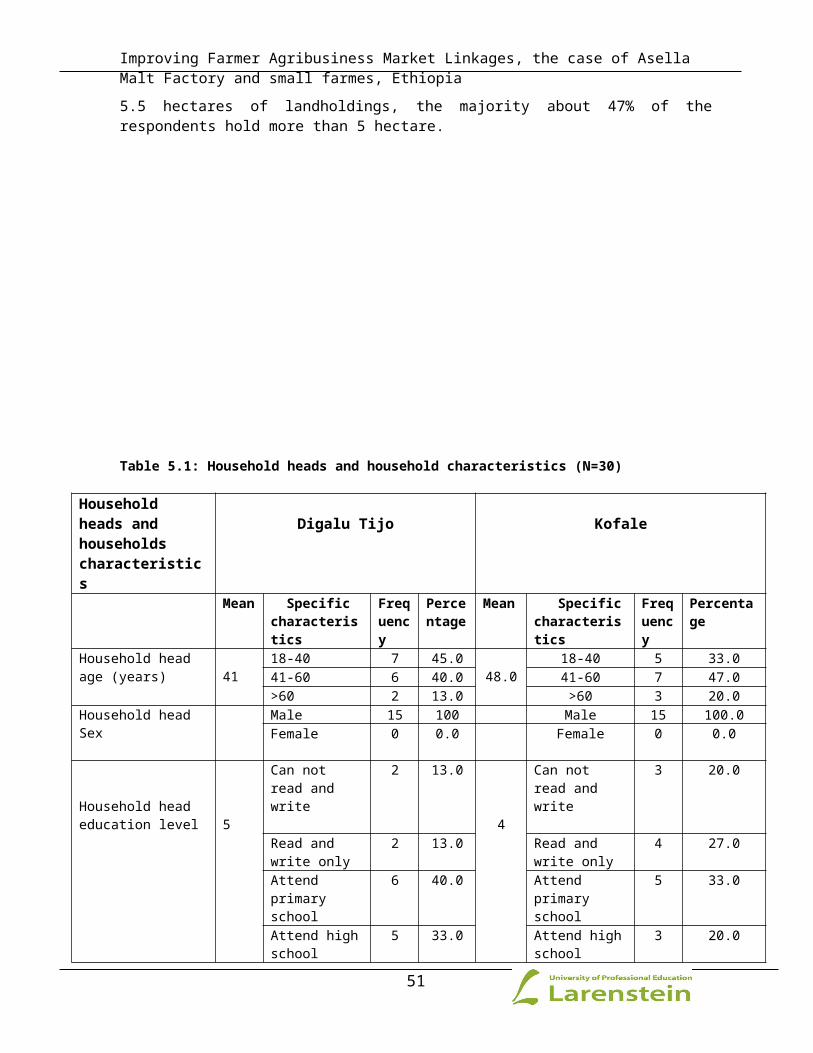

5.1 HOUSEHOLD CHARACTERISTICS.............................................34

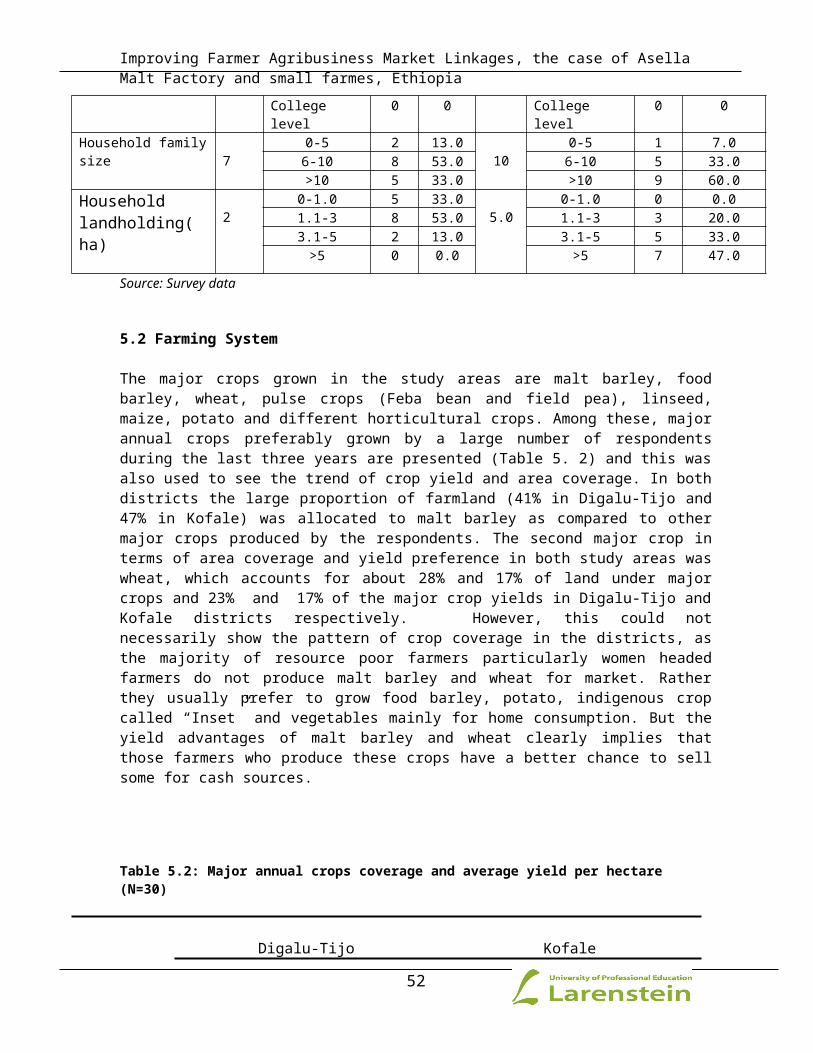

5.2 FARMING SYSTEM......................................................35

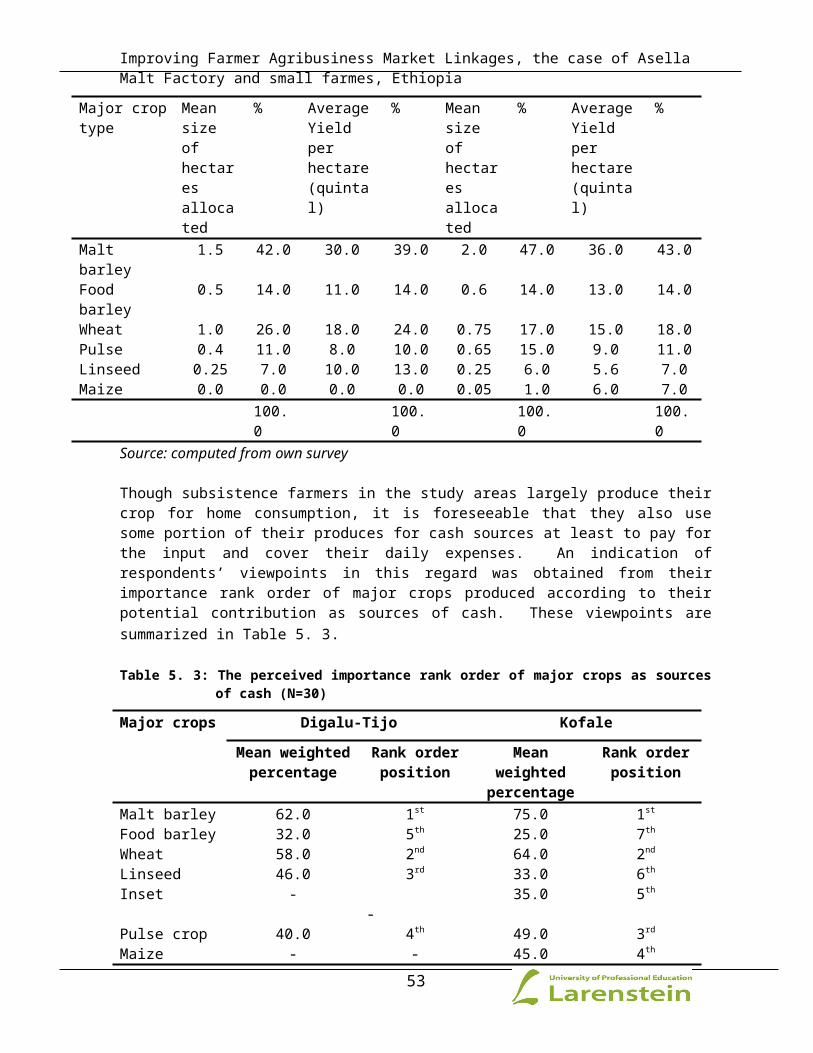

5.3 MALT BARLEY PRODUCTION AND MARKETING PROCESS.............................37

5.4 FARMERS’ MARKET INFORMATION...........................................41

5.5 PROBLEMS WITH MALT BARLEY MARKETING....................................42

5.5.1 External Constraints in Asella Malt Factory......................................................................43

5.5.2 Internal constraints facing farmers and processor.........................................................44

5.6 CAUSAL PROBLEM ANALYSIS ..............................................45

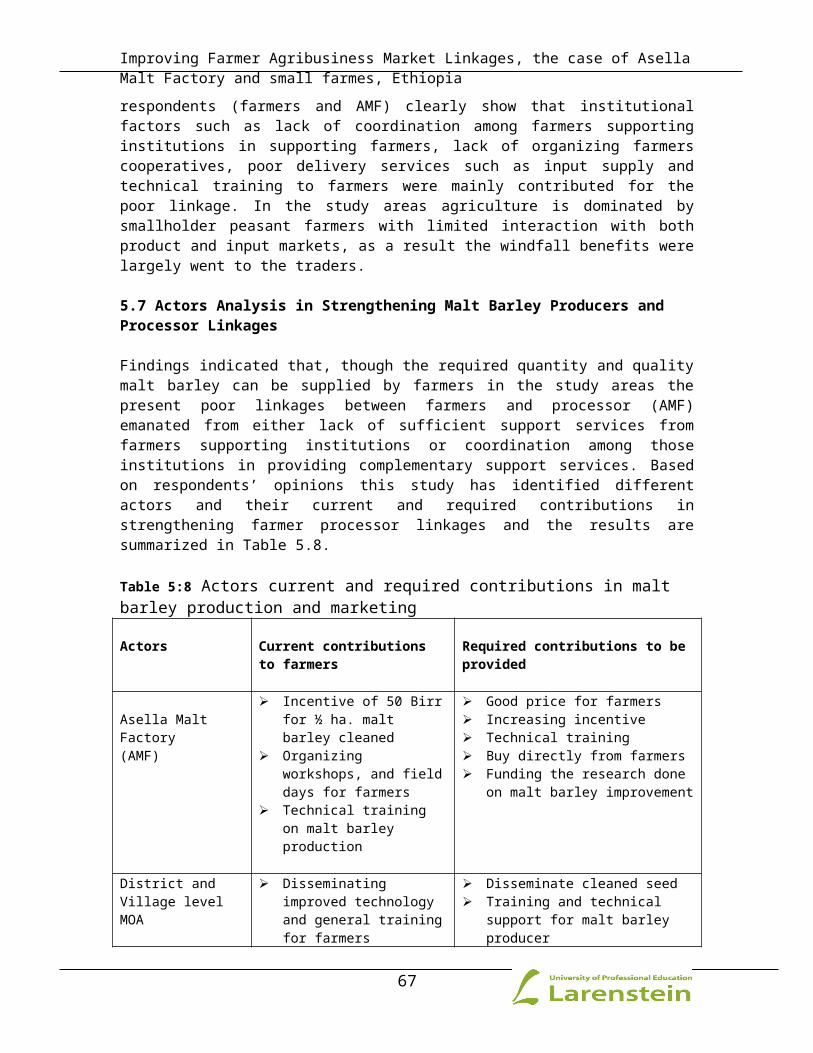

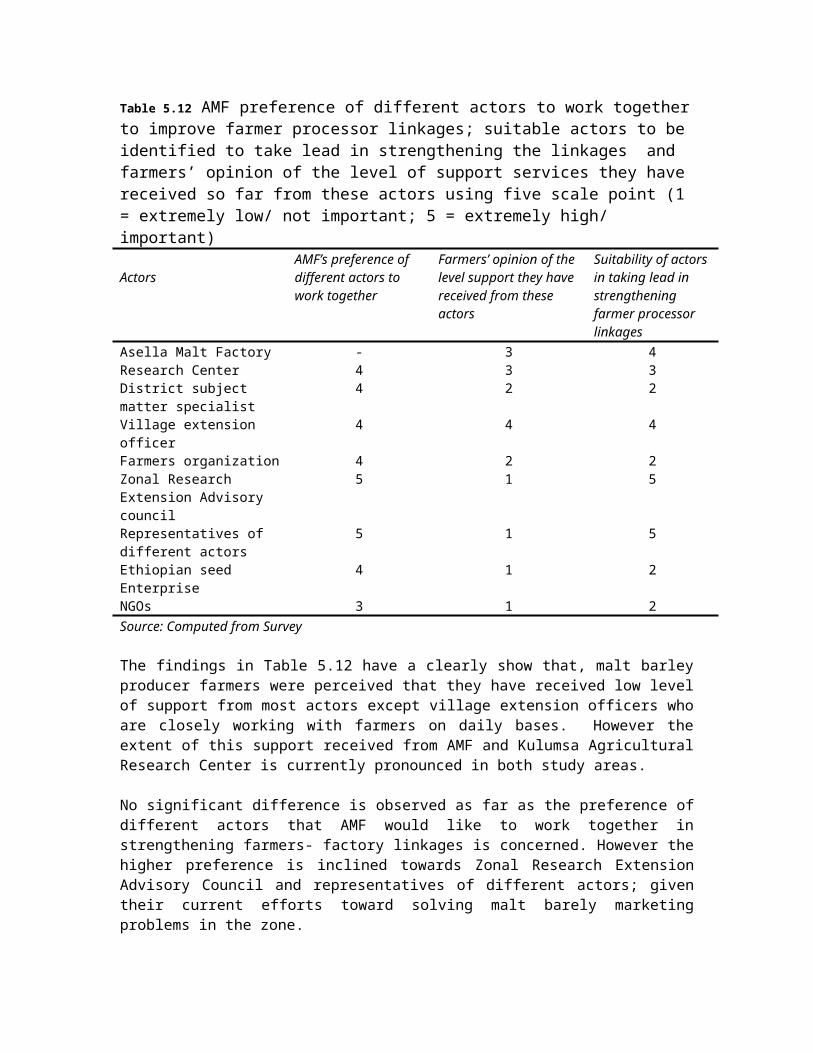

5.7 ACTORS ANALYSIS IN STRENGTHENING MALT BARLEY PRODUCERS AND PROCESSOR LINKAGES.46

5.8 SWOT ANALYSIS IN MALT BARLEY SUPPLY CHAIN..............................48

5.9 OPPORTUNITIES IN THE STRENGTHENING FARMER AGRO PROCESSOR LINKAGES...........49

5.10 STRATEGIES IN IMPROVING FARMER ASELLA MALT FACTORY MARKETING LINKAGES......52

5.10.1 Ways of strengthening linkages........................................................................................52

5.10.2 Actors to be identified.........................................................................................................53

6. CONCLUSIONS AND RECOMMENDATIONS......................................55

6.1 CONCLUSIONS.........................................................55

6.2 RECOMMENDATIONS.....................................................56

REFERENCES..............................................................58

APPENDIX 1: TYPES OF LINKAGES IN THE PRODUCER-PROCESSOR SUPPLY CHAIN....61

v

Improving Farmer Agribusiness Market Linkages, the case of Asella Malt Factory and small farmes, Ethiopia APPENDIX 2. THE SEED SUPPLY SYSTEM ....................................62

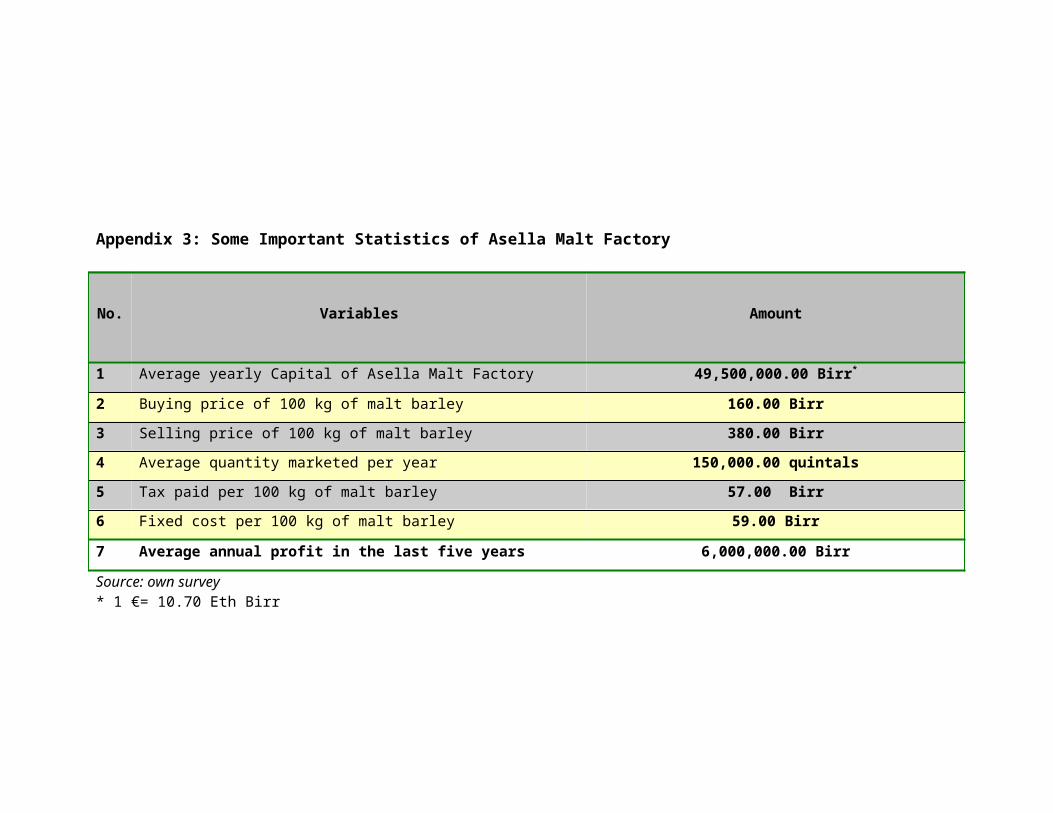

Appendix 3: Some Important Statistics of Asella Malt Factory............63

LIST OF TABLES

Tables Page

Table 4.1 Annual wheat requirements of Kaliti Food Processing Company-------------------------------------

Table 5.1 Household heads and household characteristics

-----------------------------------------------------

2831

Table 5.2 Major annual crops coverage and average yield per hectare

---------------------------------------

32

Table 5. 3 The perceived importance rank order of major crops as 32

vi

Improving Farmer Agribusiness Market Linkages, the case of Asella Malt Factory and small farmes, Ethiopia

sources of cash-------------------------Table 5.4 Malt barley production, consumption and marketing by

respondents------------------------------

33

Table 5.5 Ranking order of different suppliers AMF currently relied

on and its view that the factory should rely on for the

future--------------------------------------------------------------

----------------------------

35

Table 5.6 Percentages of relative frequency respondents showing

major problems with malt barley marketing as perceived by

farmers-------------------------------------------------------------

---------------------

38

Table 5.7 Assessment of perceived of the different external

factors’ impacts on the performance of the AMF using five scale

points--------------------------------------------------------------

---------------------------

39

Table 5:8 Actors current and required contributions in malt barley

production and marketing------------

42

Table 5.9 SWOT

Analysis------------------------------------------------------------

-------------------------------

44

Table 5.10 The amount of malt barley purchased by AMF and the

percentage supplied by different producer during last five

years.--------------------------------------------------------------

------------------------

46

Table 5.11 Assessment of judgments of AMF current focus in assisting

malt barley producer farmers and view where the focus should be and

farmers’ expectation using five point scale-----------------------

48

Table 5.12 AMF preference of different actors to work together to

improve farmer processor linkages; suitable actors to be identified 49

vii

Improving Farmer Agribusiness Market Linkages, the case of Asella Malt Factory and small farmes, Ethiopia

to take lead in strengthening the linkages -------------------------

LIST OF FIGURES

Figures Pag

e

Figure 3.1 : Types of Purchasing Arrangements

--------------------------------------------------------

17

Figure 4. 1 Sectoral composition of GDP, Ethiopia, 1991/92–

2000/01-----------------------------

Figure 4.2 Map of the study

areas-------------------------------------------------------------

-----------------

23

28

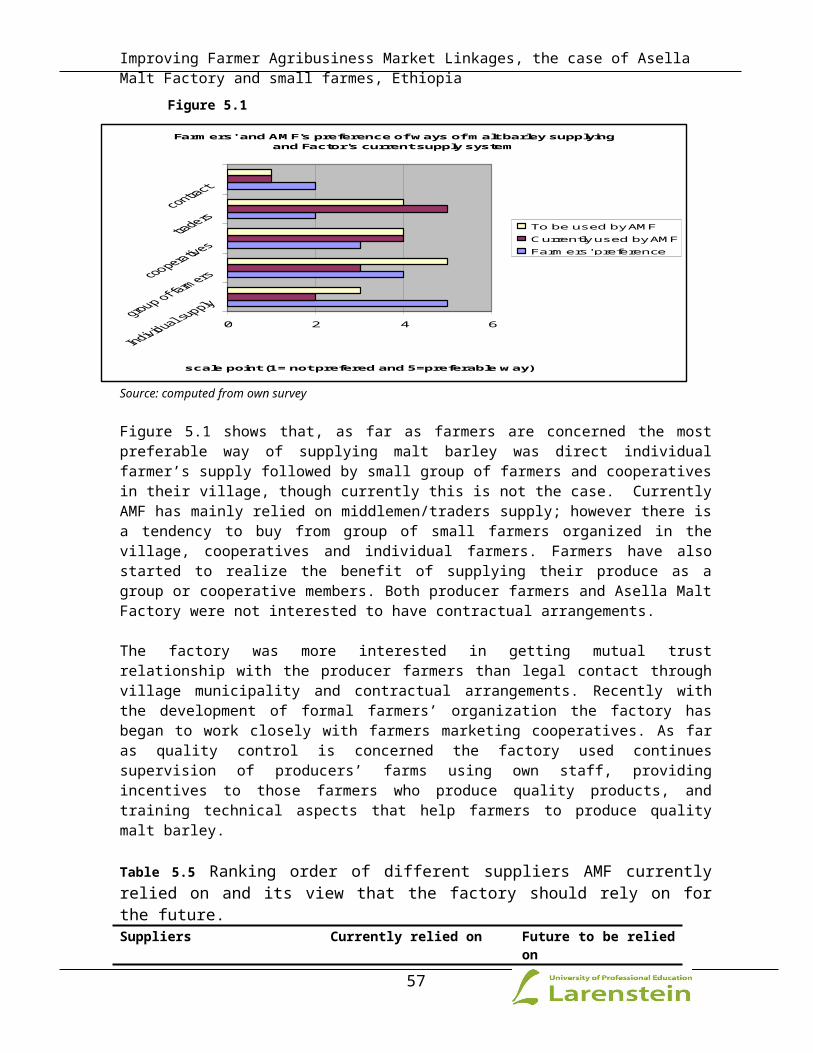

Figure 5.1 Farmers’ and AMF’s preference ways of malt barley

supplying and current

supply system

------------------------------------------------------------------

34

viii

Improving Farmer Agribusiness Market Linkages, the case of Asella Malt Factory and small farmes, Ethiopia -----------------------------------Figure 5.2 Malt Barley Supply Chain

------------------------------------------------------------------

--------

36

Figure 5.3: Respondents Assessment of Source of Market information

----------------------------------

37

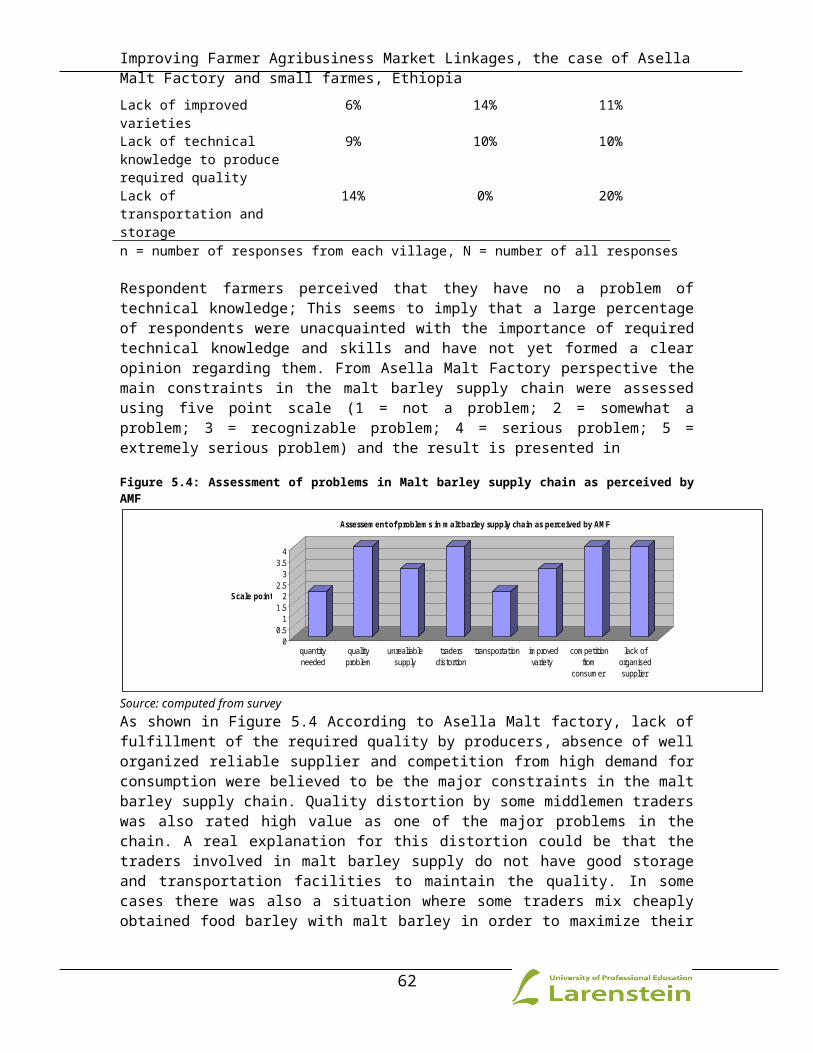

Figure 5.4: Assessment of problems in Malt barley supply chain as

perceived by AMF---------------

38

Figure 5.5 Internal constrains facing

processor---------------------------------------------------------

------

40

Figure 5.6: Causal problem analysis for poor linkages between malt

barley producer

farmers and

AMF---------------------------------------------------------------

-----------------------------------

41

Figure 5.7 Asella Malt Factor’s profit during the last five

years-------------------------------------------

47

Figure 5.8 The amount of processed malt barley used by domestic

brewery factories during the last five

years-------------------------------------------------------------

--------------------------

47

ix

Improving Farmer Agribusiness Market Linkages, the case of Asella Malt Factory and small farmes, Ethiopia

ACRONYMS

ADLI Agricultural Development-Led IndustrializationAMC Agricultural Marketing CooperationAMF Asella Malt FactoryARDU Arsi Rural Development UnitCADU Chilalo Agricultural Development UnitECMC Ethiopian Coffee Marketing CorporationEGTE Ethiopian Grain Trade EnterpriseEOPEC Ethiopian Oilseeds and Pulses Export CorporationETFRUIT

ESE

Ethiopian Fruit and Vegetables Marketing Enterprise

Ethiopian Seed Enterprise

FAO Food and Agricultural Organization

GATT General Agreement on Tariff and Trade

GDP Gross Domestic Product

HDE Horticulture Development Enterprise

IFAD

KFPF

International Fund For Agricultural Development

Kaliti Food Processing Factory

KARC Kulumsa Agricultural Research Center

MIS Market Information Services

x

Improving Farmer Agribusiness Market Linkages, the case of Asella Malt Factory and small farmes, Ethiopia

MOA Ministry of Agriculture

NAFTA North American Free Trade Area

NGOs Non Governmental Organizations

PAs Peasant Associations

REAC Research and Extension Advisory Council

SAP Structural Adjustment Program

SWOT Strength, Weakness, Opportunities and Threat

ABSTRACT

The agricultural led industrial development policy of Ethiopia callfall for the need for higher levels of managed co-ordination amongfarmers, processors and consumers. However, co-operation betweenfarmers and emerging processors is still limited to impersonal spotmarket transactions/ ad hoc linkages. The inability of farmers toaccess markets and market information is one of the major problemsin Ethiopian agriculture. These facts led me to assess how toimprove farmer processor linkages by examining existing marketingsystem of the selected case.

The major focus of this study is to investigate constraints andopportunities in malt barley marketing chain. The study furtheraimed to identify strategies and actors required to improve farmeragro processor market linkages. The study was based on the datacollected through a formal questionnaire administered to 30households selected purposively from two districts. Informalinterview was also used to collect relevant data and informationfrom resource persons in the Asella Malt Factory. Both quantitativeand qualitative data were collected from primary and secondarysources. Descriptive statistics, ranking method, and rating pointscale were employed to quantify the opinion of the respondents.Causal problem analysis, actor analysis and SWOT analysis were used

xi

Improving Farmer Agribusiness Market Linkages, the case of Asella Malt Factory and small farmes, Ethiopia to analyze relevant factors; actor; strength, weakness,opportunities and threat qualitatively.

In the study area cereal crops play a significant role in thelivelihood of the rural community of which malt barley is the mainsource for income generation and home consumption. On average maltbarely contributed 63 percent of annual income in the study areas.In both districts the large proportion of farmland (41% in Digalu-Tijo and 46% in Kofale) was allocated to malt barley as compared toother major crops produced by the respondents. About 40 and 43percent of annual total harvested crop yield was coming from maltbarley in Digalu Tijo and Kofale districts respectively.

Information on market prices, quantities traded, and othermarketing-related matters rarely reach farmers in the study areas.Fellow farmers and visiting market places were identified as themain source of market information in the study area. Other majorproblems facing malt barley producer farmers were lack of access toprocessor market, high cost of production, low price for produce,lack of transportation and storage, Lack of technical knowledge toproduce required quality and lack of improved varieties. Fromprocessor (Asella Malt Factory) perspective, lack of fulfillment ofrequired quality by producers, lack of reliable supply, competitionfrom consumers and absence of organized suppliers were believed tobe the major constraints in the malt barley supply chain. Maltbarley producer farmers preferred to sell their produce directly tothe Asella Malt Factory as it offered them better price of 20-50Birr per 100 kilograms than market price. However due to lack ofaccess to factory market 94%, 78% and 74% of the total malt barleysold out by producer were sold to the traders in the year 2002,2003, and 2004 respectively. Though individual farmer supplythrough middlemen was the dominating way of supply, currently bothfarmers and the processor were convinced that efficient way of maltbarley supply is through organized group of farmers andcooperatives who will directly supply to the factory. The studyrevealed that lack of support services received from supportinginstitutions such as MOA, research institutions, processor andother government and non government institutions were contributedto poor linkages between malt barley producer and processors.

In actor analysis the most important actors found to have apositive effect to strengthen malt barley producer and processorlinkages were Asella Malt Factory, district and village MOA,

xii

Improving Farmer Agribusiness Market Linkages, the case of Asella Malt Factory and small farmes, Ethiopia Kulumsa Research Center, Zonal Research and Extension AdvisoryCouncil (REAC) and farmer cooperatives. Of these Asella MaltFactory was providing at least 70% of the perceived requiredcontributions to farmers through payment of better price to theirproduce, offering incentives, and funding workshop and farmers daysto producer farmers.

xiii

Improving Farmer Agribusiness Market Linkages, the case of Asella Malt Factory and small farmes, Ethiopia

CHAPTER ONE

1. INTRODUCTION

The changes in food and agricultural markets have influenced theneed for higher levels of managed co-ordination. This has resultedin the introduction of different forms of vertical integration andalliances, which have become a dominant feature of agriculturalsupply chains (Kirsten & Sartorius, 2002).

In Ethiopia the emerging of some few agro industries like Asellamalt factory has created market opportunities for smallholdersthough farmers have not yet fully benefited from this market.Asella Malt factory is located in Arsi- one of the leading maltbarley producer zones of the country.

Barley is an important crop in Ethiopia and it accounts for 20percent of all cereal production and covers the third largest areaof any crop--950,000 hectares with total production at 999,610tons, which is 18.3 per cent of the total cereal production. Barleyis used as food and raw material for brewing home-made alcoholicdrinks. Beverage industry (Asella Malt Factory) uses some 10,000tons of barley per annum to prepare malt for breweries (UNDP,2004). Asella Malt Factory is the only malt processor and providerto all brewery factories in the country. Small farmers in districtssuch as Kofale, Lemu Bilbili, Digalu Tijo and Kersa produce a largeamount of malt barley and are directly or indirectly the mainsuppliers of the factory. State farms in Bale and Arsi zone alsoproduced a large amount of malt barley and supplied it to thefactory. However, currently their share is declining followingshrinkage of size of state farms.

The process of industrialization has created opportunities forsmallholders in developing countries to produce agriculturalcommodities under contract according to certain specifics, but hasthe danger that small farmers will be marginalized and excludedfrom high value markets (Reardon and Barret, 2000). The challengeis thus to prevent this from happening and to find ways to linksmall growers in developing countries to these high value markets.It is argued that the major route for continued survival of small-scale farms, would, only be through a reliance on external ratherthan internal economies of scale through networking/clustering and

1

Improving Farmer Agribusiness Market Linkages, the case of Asella Malt Factory and small farmes, Ethiopia other forms of alliances. This could be amongst small firms orthrough establishing links between small firms/growers and largerenterprises who have already overcome the major barriers to marketentry (Delgado, 1999).

In general, stronger linkages between farmers and processors arefound in those economies where the agricultural sector hasundergone some degree of commercialization. In less developedagricultural systems, like in Ethiopia, co-operation betweenfarmers and processors is limited to impersonal spot markettransactions which do not adequately convey information aboutquantity, quality and timing to producers and consumers.

Although some factors such as nature of the product andavailability of support institutions influence farmers’ agroprocessor linkages, studies in Kenya, Ghana, Uganda and SouthAfrica confirmed that linkage arrangements such as serviceprovision, contractual agreements, price determination, purchasingarrangements, and full vertical cooperation helped in strengtheningfarmer agro processor linkages.

1.1 Problem Statements

The dynamic of agricultural trade and marketing in development arewell known. They apply equally to the poor. Even the subsistencesmall-holder must sell some produce if he is to have the cash topay for inputs and services that will raise his output and hislevel of living (Abbot, 1993). Farmers in Ethiopia allocate most oftheir agricultural produce for their own consumption. However thereis a need for farmers’ access to consumer goods. They also need topurchase production tools and inputs. Farmers must producemarketable surplus, saleable in the market and exchanged for othergoods and services.

The inability of farmers to access markets has been identified as amajor weakness in the Ethiopian economy and is blamed forexacerbating perennial food shortages in parts of the country(USAID, 2004). In the current Ethiopian long term agriculturaldevelopment led industrialization economic policy, quite a largenumber of agro-industries are coming up. The growing ofagricultural product processing companies, for small farmersimplies increased participation, or, rather, an improved ability toparticipate, in output markets. However, smallholder farmers find

2

Improving Farmer Agribusiness Market Linkages, the case of Asella Malt Factory and small farmes, Ethiopia it difficult to participate in markets because of a range ofconstraints and barriers reducing the incentives for participation.

In Arsi zone there are some local agro processing industries (oilfood, flour processing), the largest one is Asella Malt Factory,the sole malt processing factory in the country located in theleading barley producer areas of the country.

Asella Malt Factory processes more than 10,000 tons of malt barleyannually and supplies to major brewery factories in the country.The existence of this factory has created market opportunities forsmallholder malt barley farmers in the highland areas of Arsi :Kofale, Diglu Tijo, and Lemu Bilbilo. However, small holder farmerscould not fully benefit from this market. This mainly due to theneed to control the high quality of agricultural product, safehandling, packing and transporting makes difficulties for smallfarmers to be fully benefiting from this market. Therefore due tothese constraints and in some cases lack of enough supply at thepoint, the factory was some years forced to import malt barley fromother countries. The experience of existing supply of malt barleyby small farmers confirmed that, small farmers in Arsi zone havepotential to supply enough amounts of malt barley with the requiredquality. However this can only be achieved through introducingstrong linkages between producers and processors. In the case ofmalt barley producer farmers and Asella Malt factory the linkagearrangements and coordination among agents in the chain are eithernon existent or on an ad hoc basis due to institutional andphysical factors.

Strengthening farmer-agro processor linkages recently promoted byagricultural support organizations doesn’t exist in the area.Evidences in some African countries show that developing strongtrusting relationships between producer and processor are the basisfor producing significant benefits for both parties, leading to‘win-win’ situations through risk reduction for both processors andfarmers or cost saving by better production planning andmanagement.

The level of understanding of quality requirement by producers andtraders is low. Lack of product quality, reliability and commercialorientation are the most commonly criticized features of farmers.Recommended good agricultural practices are often not applied. Abetter understanding by farmers of quality requirements of

3

Improving Farmer Agribusiness Market Linkages, the case of Asella Malt Factory and small farmes, Ethiopia processors will enhance market linkages between producers andprocessor. This in tern resulted in increasing of incomes securedsales of materials for both farmers and factory. The effectivemarket linkages can only be achieved through co-coordinated andintegrated efforts of all actors (zonal MOA, research center, seedenterprise and factory) in marketing chains and alliances. It istherefore important to investigate constraints and opportunities aswell as institutions required to strengthen farmer agro processorlinkages.

1.2 Objective of the research

To identify major challenges and opportunities in the chain ofmalt barley producers, traders and processor marketingchannels.

To identify the strategies and actors required to improvefarmer agro processor market linkages.

To contribute to the appropriate farmer agro processor marketlinkages that can benefit both sectors by identifying relevantappropriate linkage arrangements.

1.3 Main research questions

What is the existing marketing system and constraints involvedin the market system of malt barley producers and processor?

What are the most important actors can be identified ascatalyst to improve market linkage?

What opportunities and benefits can be obtained by introducingrelevant appropriate linkage arrangements?

1.4 Sub-questions

Who are the main suppliers of malt barley to Asella MaltFactory?

What factors restrain the two sectors market linkages? What are the difference advantages and disadvantages among

different domestic supplier from the factory perspective? What possibilities and opportunities can be identified for the

future appropriate market linkages between small farmers andAsella malt factory?

What are the relevant appropriate linkage arrangements can beidentified?

Which actors would play what role to improve market linkage?

4

Improving Farmer Agribusiness Market Linkages, the case of Asella Malt Factory and small farmes, Ethiopia

1.5 Significance of the Study

Various efforts to promote production of small-scale farming havebeen noted in the past decade. Despite of the persistent drought,remarkable results have been achieved in some areas in this regard.However, the challenge remains unsolved is how to deal with themarket problem. The participation of small farmers in marketeconomy is very low in Ethiopia. The investigation identifiesconstraints and possibilities to strengthen farmer agribusinesslinkages and could assist in identifying policy interventionsand/or institutional innovations to alleviate constraints andimprove the ability of small-scale farmers to be part of the marketof the emerging agro- industries.

Moreover, the study will contribute to generate information tosupport policy formation and implementation of improving farmeragribusiness linkages in the agricultural led industrializationeconomic policy programs of the country.

Lastly, the study will hopefully contribute to deeper criticalinsight into the currentendeavor of enhancing food security by improving the capacity ofsubsistence farmers and local agro processors.

1.6 Outline and Delineation of the Study

This study is organized into six main chapters. Chapter one beginswith a general overview of the study. It further describesobjectives and the significance of the study. Chapter two gives anintroduction to some methodological aspects used in this study.

Chapter three introduces the conceptual framework or theoreticalperspective of the study. This chapter is divided into two partswith the first part dealing with general review of agriculturalmarketing and related concepts, while the second part reviewstheoretical framework of the main theme of the study. It reviewsagricultural marketing related concepts, farmer agribusinesslinkage concepts from world perspective in general and developingcountries’ perspective in particular.

Chapter four presents a country profile relevant to this study andgives descriptions for the study areas. It summarizes location,

5

Improving Farmer Agribusiness Market Linkages, the case of Asella Malt Factory and small farmes, Ethiopia socio-economic characteristics, agrarian structures, agriculturalmarketing and agro industry of both at the country and study arealevels.. Chapter five presents the empirical findings of the studyin descriptive and qualitative ways using tables, graphs anddiagrams and gives analysis and discussion of the findingsobjectively.

The thesis report is finalized by giving conclusion and setrecommendation forward for the study.

CHAPTER TWO

2. RESEARCH METHODOLOGY

This section presents the methods that were used in the studyprocess from the time ofcollecting data, analyzing it and eventually in writing the thesis.

6

Improving Farmer Agribusiness Market Linkages, the case of Asella Malt Factory and small farmes, Ethiopia 2.1 Area selection

During the inception of this research design before I had decidedwhere this research would be conducted, relevant institutions andindividuals have formally been contacted to help in selectingappropriate district relevant for the study. Though all districtsin Arsi zone mainly produce barley, only some districts producemalt barley for the processing market; moreover a few of these areaccessible and have some formal marketing linkages with theprocessing company.

Based on information obtained and personal experience in the studyarea, two districts (Kofele & Digalu Tijo) with contrastinggeographic location and farming systems were selected. Kofaledistrict is located far south-west of Arsi zone, while Digalu Tijois just at corner of zone capital Asella 25 km a way (Figure, 4.2).Malt barley producing farmers were sampling unit in this study onthe assumption that the study is focused on malt barley producerand processor linkages. Selection of two Peasants Associations fromeach district and identifying household typologies based on maltbarley producers and non-producers was made. Other criteria used inselecting the respondents were based on the accessibility of thearea and respondents experience with factory’s market. About 15malt barley producer farmers from each Peasant Association wereselected purposively. A total of 30 farmers were interviewedthrough structured and semi-structured questionnaire survey.

2.2 Data Collection Method

This study is built on primary and secondary data collected fromselected farmers and Asella Malt Factory. Primary and secondarydata were collected to support one another. Collection of primarydata involved individual interview, and discussion. The maintechnique used was personal interviewing based upon questionnaireforms. The questionnaire was open and closed ended which providedboth qualitative and quantities data. The questionnaire to thefarmers was focused on household socio-economic characteristics,crop production, malt barley marketing system, constraints theyfaced in malt barley production and marketing, and what possiblestrategies they think to mitigate and how they are going to benefitfrom.

7

Improving Farmer Agribusiness Market Linkages, the case of Asella Malt Factory and small farmes, Ethiopia Discussions and individual interviews with of Asella malt factorymanagers at various levels were made. The necessary informationgathered in this discussion and interviews was addressed to issuessuch as the existing malt barley market system, constraints in maltbarley supply chain, factory market relation with small holderproducer farmers and possible appropriate strategies to improvefarmer agro processor linkages. For the secondary data availableliteratures, reports and documents from Asella malt factory,Kulumsa Agricultural Research Center, zonal MOA and selecteddistricts were consulted and examined. For a conceptual andtheoretical framework of the study recent literatures (books,journals, and webs) in the Larenstein University were mainly used.Triangulation became possible and findings were cross-checkedduring data analysis and interpretation.

2.3 Choice of Methods

Farm agribusiness linkage strategy should emerge from reflectiveand well-informed of all stakeholders. Both quantitative andqualitative methods were used to meet the objective of the study.Qualitative methods concentrate on words and observations toexpress reality and attempt to describe the view and opinions ofpeople in natural situations, while quantitative approach grew outof a strong academic tradition that places considerable trust innumbers that represent opinions or concepts (Krueger 1994:27).Given that the major purpose of this study was to investigateconstraints and opportunities to improve farmer agro processorlinkages from the actors’ point of view as regards theirconception, and understanding, I tried to use methods that wouldefficaciously bring out the actors’ point of view. Hence theresearch methods that were followed in this study are bothqualitative and quantitative approaches. It would not be possibleto answer the research questions set in a rigorous way through asingle approach. The combined use of the methods would enable us tocome up with a credible, realistic and scientifically balancedanalysis in relation to research themes and a problem domain thatis sensitive to subjective perceptions (Legesse, 2003). The use ofcombined methods (qualitative and quantitative) is vital since thecomplexity of rural livelihoods cannot be fully captured using asingle method and/or discipline. A questionnaire was developed insuch a way that it would capture the ideas of respondents in large,using five scale points. Ranking was also used where necessary.

8

Improving Farmer Agribusiness Market Linkages, the case of Asella Malt Factory and small farmes, Ethiopia 2.4 Data Analysis

The collected data were entered into the computer and analyzedusing Excel spread sheet. Simple statistical analyses like average,frequency, mean, and percentages were used. Causal problemanalysis, actor analysis and SWOT analysis were employed to analyzeopinions and perceptions of the respondents qualitatively.

The findings were presented using tables, graphs and figures.Finally the results were then interpreted, discussed and comparedwith relevant literatures.

2.5 Limitations of the study

First and foremost the study was developed in the language of theacademic discipline (English) that is different from the languageof the study subjects (Amharic and Oromiffa) which were the mainmedium of communication in the data collection. Given the languagedifferences, it was often difficult to translate some of theacademic concepts and words from English to the local languages.Besides, the primary data were collected in my absence by my fellowcolleague in my organization. Hence, personal field observation wasmissed. To overcome these problems frequent contacts with theenumerator were made, especial notes were attached to thequestionnaires to make it clear more as much as possible. I alsobelieve that the experience of the enumerator as developmentresearcher in the area will contribute to fill this gap. It isundeniable that selecting only 30 respondents from the twodistricts could not be statistically representative sample, howevergiven the lower number of farmers who have already established somelinkages with the factory, and time and resource limitation, thesample can be reasonable acceptable for the intended studypurpose.

It was almost not possible to come across related work done inEthiopia in general and in study area in particular. However,recent related works done in developing countries like Kenya,Uganda and Nigeria were helpful in this regard.

CHAPTER THREE

3. LITERATURE REVIEW

3.1 General Review on Agricultural Marketing

9

Improving Farmer Agribusiness Market Linkages, the case of Asella Malt Factory and small farmes, Ethiopia

3.1.1 The concept of Agricultural marketing

Agricultural marketing is defined as the performance of businessactivities involved in the flow of food products and services fromthe point of initial agricultural production until they are in thehand of consumer ( Kohls and Uhl 1990, cited in Ritson ,1997). Formuch of the history of mankind, this was relatively insignificant,with most of what was eaten produced in the locality. However,since the industrial revolution there has been a progressiveincrease in the distance between the typical location ofagricultural production and that of food consumption, and in thevalue added to produce as it moves from farmer to consumer. AsCramer, et al., (2001) noted that in USA of the total cost spent byconsumers for food products, less than one-fourth was returned toproducer while over three-fourths of that amount was for marketingconst. Marketing costs include those associated with assembly,transportation, processing and distribution of farm food toconsumers. The cost component of marketing is called marketing billor marketing margin.

Padberg (1997) discussed that in more economically developedcountries, only small percent of the population will be involved inagriculture. This allows agricultural production to undergo oftenextreme geographic specialization. Interregional commodity movementis necessarily much greater. In developing countries, most economicactivity in agricultural sector relates to transaction involvingcommodities. Agricultural commodities refer to unprocessed orminimally processed agricultural materials which handled andmarketed in bulk quantities of which grains are a good example. Theorderly marketing of these commodities requires some public rules,such as grades and standards, food safety policies, marketinformation, features market etc.

Marketing phenomena and marketing systems are growing in importanceas key factors influencing the success or failure of efforts toimprove food production and consumption in developing countries(Zandstra, 1995).Here efficient market is needed. Marketingefficiency is measured by comparing output and input values.Therefore, markets are efficient when the ratio of value of output(based on consumer valuation) to the value of input (costsdetermined by alternative production capability) throughout themarketing system is maximized (Walter, 1979).

10

Improving Farmer Agribusiness Market Linkages, the case of Asella Malt Factory and small farmes, Ethiopia

A well organized market enhances the quality of communicationbetween buyers and sellers. So that market prices can bedetermined. These prices, in turn, guide producers’ productiondecisions and consumers’ purchasing decisions (Cramer, et al.,2001). Though marketing represents one of the most criticallinkages in food system it is neglected in food security analysis(Baulch, 2001).

Zandstra (1995), discussed that with the rise in importance ofcommercial agriculture farmers are no longer interested just inhigher yields, but in more remunerative commercial outlets; directpublic intervention in marketing activities has steadily declined.Therefore, the role of private entrepreneurs and non-governmentalorganization in helping to meet the needs of urban consumers andrural producers is increasingly apparent. He added that giventhese developments, there is a variety of marketing issues fordeveloping countries to address in the years ahead includingovercoming commercial bottlenecks due to inadequate production orpost harvest technology, seizing market opportunities resultingfrom income and demographic changes, and resolving market relatedpolicy problems. Farmers, traders, processors, consumers as well asnational agricultural research institute should need to worktogether to address agricultural marketing problems in developingcountries.

3.1.2 Trade in Agricultural commodity

Down through history, the pattern of agricultural commodity tradehas been restricted by several factors. Agricultural commoditiesare bulky, perishable and expensive to transport. Low incomecountries have much of the population in subsistence agricultureproducing little exportable output. There was a greater tendency toadopt national policies to protect the low income rural sector.National policies are frequently motivated by concerns for foodsecurity or self-sufficiency. These factors led to the erection andmaintenance of significant barriers to agricultural commodity tradehowever major changes in world politics are bringing changes tothis historic impasse. The development of European Union has openedthe boarders of several high-income countries to agriculturalcommodity trade. The North American Free Trade Area (NAFTA) isexpected to have similar effect. The Uruguay round of negotiationof the 130-nation General Agreement on Tariff and Trade (GATT)

11

Improving Farmer Agribusiness Market Linkages, the case of Asella Malt Factory and small farmes, Ethiopia included agricultural commodities in major way for the first time(Padberg ,1997).

In the developing countries, smallholder farmers find it difficultto participate in markets because of a range of constraints andbarriers reducing the incentives for participation. These may bereflected in hidden costs that make access to markets andproductive assets difficult. Transaction costs, that is, observableand non-observable costs associated with exchange, are theembodiment of access barriers to market participation by resourcepoor smallholders. These include the costs of searching for atrading partner with whom to exchange, the costs of screeningpartners, of bargaining, monitoring, enforcement and, eventually,transferring the product to its destination (Kandiwa, 1999).

Agricultural producer rarely sells his output directly toconsumers. Usually there are several stages in the marketingprocess, and it is generally concerned that the middlemen arenecessary in some of the stages (Bauer & Yamey, 1993). Inagricultural commodity distribution where low consumer incomes andsubsistence agricultural conditions prevail, the marketing channelis short and direct.

Van der Laan (1993) reported the undesirable features of graintrade in the villages of developing countries: “many farmers didnot estimate their own requirements properly and sold too much oftheir crop during harvesting. When they discovered that they hadnot enough seed for their farms they turned to the traders toborrow where they had to repay double amount of the same grainduring next harvest.”

3.1.3 Agricultural Commodity Prices

Agricultural commodity prices, particularly their level,variability and determinants, are of central importance in thestudy of agricultural marketing (Carman, 1997). Prices foragricultural commodities are an important determinant of the levelof farm income, the cost of food to consumer, export income forcountries engaged in commodity trade, the profit for agriculturalmarking firms and return to commodity traders and speculators.Because of the importance of agricultural commodity prices toeconomic growth and development, most national governments haveextensive and often complex policies and programs to deal with

12

Improving Farmer Agribusiness Market Linkages, the case of Asella Malt Factory and small farmes, Ethiopia commodity price in both domestic and export market. The nature ofthese policies and programs is politically important because oftheir impact of food prices, farmers’ incomes, and relation withtrading partners (Carman, 1997).

Developing country government often intervene in commodity marketsto achieve various policy objectives such as food self-sufficiencyor food security; providing cheap food for urban consumers;stabilizing producer consumer prices; increasing governmentrevenues and controlling inflation. To achieve these objectives,government often changes the prices producers and marketing agentface (Shapiro and Staal, 1995).

Changes in market price of commodities will cause change in theamount of each product that will be produced (Cramer, et al.,2001). A decrease in the price of one product would cause producersto increase their production of other higher priced product andreduce their production of lower priced product.

Seasonal Price Change: agricultural commodity prices often tend tovary predictably through time as a result of seasonal variations insupply and demand. The harvest period often extends over only one,two or three months, with consumption over the remainder of theyear provided from storage stocks. This result in prices those arelowest at harvest time, with prices increasing inline with chargesof storage over the year. Those businesses that carry largeinventories must evaluate the risk of price changes overtime andpursue strategy for hedging (Morris, 1995).

Price and Product Quality: according to Carman (1997) commoditygrade are often viewed as equivalent to quality, with separategrades reflecting different quality levels. Alternatively, gradesmay reflect different bundles of characteristics that determine endusers possibilities, as distinct from quality. Thus grades andgrade standards convey information about a commodity thatfacilitates communication between buyers and sellers. Grade mayincrease demand, resulting in increased sales at a given price andor increased prices. At consumer and intermediate buyer level, thesorting commodities into grades allow buyers to select particularquality characteristics which they prefer and are willing to payfor, thus increasing utility.

3.1.4 The Role of Processors in Commodity Marketing

13

Improving Farmer Agribusiness Market Linkages, the case of Asella Malt Factory and small farmes, Ethiopia

Agriculture in developing countries is becoming more and morecommercially oriented. And with that trend comes a growing interestin post harvest issue, in particular processing. There are severalreasons for this. Where output is abandoned in the field orunderutilized after harvest, processing can increase the usablephysical volume and economic value of existing production (Scott,1995). If particular commodities have limited usage, processing candiversify their exploitation and thereby create new markets. Indoing so processing activities can also increase the value-added inrural production through transformation of low-priced raw materialsinto higher-priced intermediate or finished products. Processingmay facilitate transportation and handling these commodities aswell. Processing entails a complex set of activities includingprocurement of inputs, transformation, distribution, and sales.Running a processing facility therefore means addressing themarketing problems associated with each of these tasks (Shapiro andStaal, 1995).

3.1.5 Marketing Channels for Agricultural Products

The analysis of marketing channels is intended to providesystematic knowledge of the flow of the goods and services fromtheir origin (producer) to their final destination (consumer)Mendoza (1995). The same author pointed out that, this knowledge isacquired by studying the participants (agents) in the process, i.ethose who perform physical marketing functions in order to obtaineconomic benefits. In carrying out these functions, marketingagents achieve both personal and social goals. Traditionallyaccepted marketing agents involves producers, rural assemblers,wholesalers, retailers, processing companies, producer and consumerassociation, government institutions or agencies and the consumers(Mendoza,1995)

3.1.6 The Role of Cooperatives in Agricultural Marketing

An organizational form that has long been a part of agriculture inmany countries is the cooperative. Farmer cooperatives are anintegral part of agriculture and the free enterprise economy(Cramer, 2001). According to Roy (1964) cited in Cramer et al(2001) cooperative is defined as a business that is organized,

14

Improving Farmer Agribusiness Market Linkages, the case of Asella Malt Factory and small farmes, Ethiopia capitalized, and managed for its member-patrons at cost, furnishingand/or marketing goods and services to the patrons at cost.

Farmer members sell their product through marking cooperatives orbuy their inputs through supply cooperatives. Farris (1997) notesthat cooperative offers opportunities for farmers in order to docollectively what they were unable to do independently within thegenerally prevailing purely competitive structure of agriculture.Among major goals that cooperatives sought to achieve are thefollowing:(i) improve bargaining power in purchasing farm suppliesand selling farm products; (ii) reducing cost of marketing farmproducts; (iii) obtain products or services which are eithercostly or not otherwise available; (iv) obtain better market accessfor cooperative members; (v) improve product or service quality inboth farm inputs purchased or commodities marketed; (vi) increasefarmers’ income; and (vii) provide information and education toincrease agricultural production efficiency and to enhance qualityof life in rural areas.

Farmers associations or cooperatives enables small farmers toeconomize on transport to distant outlets, undertake initialprocessing themselves and increase their bargaining power (Abbot,1993).

3.1.7 Infrastructure for Agricultural Marketing

A major cause of marketing problems often lies in defectiveinfrastructure, particularly road, transport services, seaports,storage facilities, electric utilities, processing facilities,water system and communication system (Mittendorf, 1995). It hasbeen estimated that more than half of the higher marketing costs inAfrica in comparison with those in Asia are due to inadequatemarketing infrastructure (Ahmed & Rustagi, 1987).

Mittendorf (1995) indicates that in the process of strengthening ofmarket infrastructure in African countries greater emphasis hasbeen given to tarred roads that serve urban centers; comparativelyfewer public resources have been allocated to construct simplerural roads; moreover government have invested in physicalmarketing facilities, such as, processing, market centers, andpackaging facilities. Policies have, however, been oriented toomuch toward direct government investment, with often doubtful

15

Improving Farmer Agribusiness Market Linkages, the case of Asella Malt Factory and small farmes, Ethiopia results and much less toward encouraging investment by privatetraders, farmers groups and local communities.

Farris (1997) argues that because of the nature and size of manyinfrastructure investment needs, and the fact that potentialbenefits would be widely distributed; private entrepreneurs areneither generally motivated nor financially capable of undertakingsome of them by themselves. Thus solving several infrastructureinvestment needs requires the joint participation and collaborationof public and private sectors (Patterson et al, 1996).

3.1.8 Market information to Farmers in Developing Countries

Market information services have the function of collecting andprocessing market data systematically and continuously, and ofmaking available to market participants in a form relevant to theirdecision making (Shubert, 1993). Market information can be shown tohave significant benefits for farmers, and also traders.Unfortunately, information on market prices, quantities traded, andother marketing-related matters rarely reach farmers in developingcountries (Shepherd, 2001).

3.1.8.1 The Benefits of market information to farmers

According to Shepherd (2001) farmers can use market information intwo ways. Current, or immediate, information can be used tonegotiate with traders, to decide whether or not to go to marketand, in some cases, to decide which market to visit or supply.Historical information, such as a time series of prices overseveral years, can be used to make decisions regarding productdiversification or the production of out-of-season crops. It mayeven be used to help basically subsistence farmers identifyopportunities for a cash income.

Adequate knowledge of prices, conditions of sale and qualities is,from microeconomics point of view, indispensable for rationalproduction, marketing and consumption decisions (Shubert, 1993). Atthe simplest level, the availability of market information canenable farmers to check on the prices they receive, vis-à-vis theprevailing market prices. Broadcast prices on Radio are also usedas a starting point in negotiations with traders the following dayand the availability of the market information system does enablefarmers to negotiate from a position of relative strength.

16

Improving Farmer Agribusiness Market Linkages, the case of Asella Malt Factory and small farmes, Ethiopia

Rayner and Young (1980) argue that prices for a particular productin one market may differ significantly from prices for the sameproduct in another market. The provision of market information canpermit farmers and traders to take advantage of such pricedifferences.

3.1.8.2 The Weakness of Agricultural Market information indeveloping countries

Most countries have introduced government- run Market InformationServices (MIS) at one time or another. By and large these havefailed to meet their objectives and have experienced problems ofsustainability. MIS have tended to thrive while supported by donorprojects, only to fade away when the donors leave, untilresuscitated by a new donor. Moreover, many MIS function as datacollectors while losing sight of the original purpose of the datacollection, i.e. to assist farmers and traders to make commerciallyuseful decisions. Dissemination is almost always the weakest pointand this is made increasingly difficult by the fact thatgovernment-owned radio stations are increasingly required to becommercially minded (Shepherd, 2001).

Prices of some agricultural products in major markets areconstantly changing but MIS may collect price information onlyweekly or even every two weeks. While such information can be usedfor long-term purposes it does not really help farmers to negotiatewith traders or to decide whether or not to send produce to marketAbbot (1987).

National MIS often disseminate information in a form which isunsuitable for some farmers. Some MIS publish market prices innewspapers but do not broadcast them on the radio. In somecountries newspapers only reach rural areas slowly; in many a largenumber of farmers are illiterate. Where broadcasts are used theseare usually only on national radio and are often only in one or twolanguages, which cannot be understood by all farmers. Broadcastsare often at the wrong times for farmers to be listening, unlessthey take their radios to the fields with them. In years gone by apopular way of disseminating market information was to use noticeboards in villages or markets. However, MIS frequently forgot toupdate the information on the boards, which eventually becamebroken down. Alternatively, they left prices on the boards with no

17

Improving Farmer Agribusiness Market Linkages, the case of Asella Malt Factory and small farmes, Ethiopia date, so that farmers had no idea of the day to which the pricesreferred (Ferris & Muganga, 2000).

Boakye (2000) pointed out that farmers can, of course, obtaininformation from other farmers or from traders but both sources areunreliable, for fairly obvious reasons. Information available torural traders on urban market prices is almost certainly more up-to-date than that provided by market information services as notonly do traders regularly visit these markets, but they also learnabout market conditions from other traders. Increasingly, tradersare now in direct contact with markets by standard telephone and,where available, cell phone. However, it is in a trader’s interestto maximize his or her profits and a strategy to achieve this isunlikely to include giving unbiased information to farmers.

3.1.9 The Role of Public Sector in Agricultural and Food Marketing

Baulch (2001) pointed out that the role of public sector inagricultural and food market development is a highly controversialquestion. Some neo-classical economists argue that the state shouldconfine its activities to the provision of infrastructure andpublic goods that facilitate agricultural marketing. Othereconomists, of a structuralist persuasion, argue that the strategicand political importance of food means that its marketing should becontrolled by the state. A third group argue that selectiveintervention in agricultural and food marketing can be justified ina situations where there are market failures and imperfections,and/or distributional and equity reasons. In this regard, threemain roles can be identified for the public sector in food andagricultural marketing: state trading, price stabilization andmarket development/regulation.

IFPRI's (2003)1,Research on agricultural market reforms has shownthat the liberalization programs adopted by many developingcountries in the past two decades have had limited success indeveloping private, efficient, and competitive agriculturalmarkets. Instead, transactions costs and risks remain high, andpolicies designed to improve incentives for agricultural productionoften have had little impact on small farmers and the rural poor,especially in sub-Saharan Africa.

1 After March 31, 2003, includes research on Global and Regional Trade, formerly associated with the Trade and Macroeconomics Division. http://www.ifpri.org/divs/mtid.htm

18

Improving Farmer Agribusiness Market Linkages, the case of Asella Malt Factory and small farmes, Ethiopia Evidence suggests that a major reason why past reforms have hadlimited impact is that institutional and structural deficiencieshave not been properly addressed. In particular, four main types ofinstitutions can contribute to well-functioning agriculturalmarkets:

i. Marketing institutions such as cooperatives, farmers' andtraders' associations, credit clubs, commodity exchanges andcontract farming;

ii. Infrastructural institutions such as those regulating ormaintaining public goods, including roads, communicationnetworks, extension services, storage facilities, and marketinformation services;

iii. Regulatory institutions such as laws regarding market conductand enforcement of contracts, ownership rules and propertyrights, and grades and standards; and

iv. Government and political institutions that have the capacityto monitor the emergence of markets and support theirdevelopment.

3.2 Theoretical Review on Farmer Agribusiness linkages

3.2.1 Background of Strengthening Farm Agribusiness Linkages

The trend of market-oriented reforms, following multilateral tradeliberalization and especially structural adjustment programs indeveloping countries, have led to the increased integration ofworld markets (Reardon and Barrett, 2000). This has meant thatfarmers in the developing world are now, more than ever, linked toconsumers and corporations of the rich nations. Although most ofthe changes in agricultural and food markets are taking place indeveloped countries, they have far reaching implications foragricultural development efforts in developing countries (Kirstenand Sartorius, 2002).

The changes in food and agricultural markets (the so-calledindustrialization of agriculture) have influenced the need forhigher levels of managed co-ordination. This has resulted in theintroduction of different forms of vertical integration andalliances, which have become a dominant feature of agriculturalsupply chains. Allied to these changes is a worldwide increase inconsumer demand for differentiated agricultural products that arerelatively labor intensive (Rhodes, 1993; Royer, 1995; Pasour, 1998quoted in Kirsten and Sartorius, 2002).

19

Improving Farmer Agribusiness Market Linkages, the case of Asella Malt Factory and small farmes, Ethiopia

Recent studies of the managerial economics of industrializedagriculture have revealed crucial new insights of the economicrationale for higher levels of managed co-ordination as a choice ofgovernance structure (Delgado, 1999). In conjunction with this, thehistory of vertical co-ordination projects in developing countrieshas provided many lessons and a reference framework against whichfuture development can be evaluated. All of these could pioneer anew approach to improve our understanding of market access problemsfacing farmers in developing countries (Kirsten and Sartorius,2002).

3.2.2 Concept and Definition of Farm Agribusiness Linkages

Agribusiness is defined as the sum of total of all operations inthe manufacture and distribution of farm supplies; productionoperation on the farm; and the storage, processing, anddistribution of farm commodities and items made from farm (Cramer,et al., 2001). The same authors argue that some interpret the wordagribusiness narrowly, meaning only very large business withinagricultural industry.

In FAO publication (2004) linkages are defined as direct andindirect interactions of key players in the food chain that resultin an exchange of marketable surplus. Players include producers,processors, traders, wholesalers and retailers, input suppliers, aswell as support organizations such as various support organizationsi.e. producer organizations, NGOs, research and developmentorganizations, and extension services.

Strengthening farm agribusiness linkages was initiated by FAO withthe fundamental purpose to help to transform the agriculturalsector in order to accelerate productivity growth, increase incomeand employment generation, improve food security, and increasecompetitiveness in regional and international trade (FAO, 2004).

Strengthening farm-agribusiness linkages" refers to improvingfarmers' ability to add value by switching from subsistence cropsto marketable crops, by entering into processing activities, or byestablishing raw material supply arrangements with local orinternational processors. In short, the initiative deals withdeveloping long-term and equitable relationships with theagribusiness sector (Santacoloma and Rottge, 2003).

20

Improving Farmer Agribusiness Market Linkages, the case of Asella Malt Factory and small farmes, Ethiopia

Van Rooyen & Esterhuizn (2002) note that linkage between developingagricultural initiatives and agribusiness will render the requiredsupport to industrious emerging agricultural group to produceconsistent quantity and quality as required by contractualarrangements with the supply chain.

3.2.3 Players in Farm-Agribusiness Linkages

In their summery of case studies of farm-agribusiness linkages indifferent African countries, Santacoloma and Rottge (2003) pointedout that the following actors are major players in farm-agribusiness linkages

Farmers:- typically, farmers in developing countries are individualfamily-based seasonal producers. Their focus is on householdeconomics, they operate largely in isolation from the markets fortheir produce, and have little understanding of commercialrealities under which their buyers operate. They have poorlydeveloped business skills and may lack confidence or assertivenesswhen developing linkages with buyers or support agencies.

Farmers’ organizations:- farmers’ associations are fundamentalpillars for smallholders providing a diverse range of services suchas input supplies, training and technical assistance, technologytransfer etc. Other services offered include market information,support in production and marketing planning, laboratory services,access to remote markets, and legal and accounting support. Thesefarmers’ organizations can be savings and credit associations,marketing and producers cooperatives.

Traders:- Traders and other middlemen buy crops from farmers in avariety of ways: some may require delivery (e.g. at rural milkcollection centers or assembly markets) whereas others, includingagro-processing company buyers, may collect produce from the farm.Some buy an entire crop regardless of quality, sort it intodifferent grades, and sell it to a variety of markets that each hastheir own quality standards. Other buyers, includingagribusinesses, may select crops according to particular qualitystandards or varieties. Linkages are usually informal and maychange or evolve. More organized linkages occur where farmersregularly sell to particular traders. Organized but informallinkages between traders, buying agents, wholesalers and retailers,

21

Improving Farmer Agribusiness Market Linkages, the case of Asella Malt Factory and small farmes, Ethiopia are rarely written down, but in effect they are ‘unwrittencontracts’ that are mostly permanent and stable. Linkages oftenextend to form a wide network among players in the distributionchain, and the strength of the relationships is such that it newoperators can be prevented to enter the market.

Agribusiness companies:-These include input suppliers, processorsthat add value to crops for either domestic markets or export,agents/packers that supply fresh foods to international retailingor processing companies, etc. Agribusiness companies may beindependent limited-liability companies with shareholders,companies linked to parent companies or internationalconglomerates, co-operatives or family owned businesses. At the micro- and small-scale, processing companies often have poorlinkages with suppliers, and make ad hoc purchases of raw materials,packaging or ingredients from traders in local retail markets. Atlarger scales of operation they may contract individual farmers orfarmers’ groups and provide support in a variety of ways. They alsohave linkages with wholesalers, retailers, institutional buyers orother commercial buyers of processed foods.

22

Improving Farmer Agribusiness Market Linkages, the case of Asella Malt Factory and small farmes, Ethiopia Publicly funded advisory services:-These include organizationsthat support agribusiness, such as Standards Boards and businessadvisory services. In many countries Standards Boards are movingaway from their traditional role of enforcing food legislation,towards an advisory and support role to improve food qualitystandards. In some countries, staff from the Ministry of Healthinspects food premises and advice on hygiene and sanitation.Extension workers from agricultural ministries or internationalNGOs disseminate information and introduce new ideas to ruralareas, provide training, and help develop linkages to government orprivate sector service providers. When they are adequatelyresourced they can be effective change agents, but in manycountries public sector extension workers are poorly supported andhave limited effectiveness while profitable agribusiness companiesemploy their own extension staff.

NGOs:-For many years these agencies focused on agriculture andrural development in preference to agribusiness support. However,they have recognized the importance of small- and micro-enterprisedevelopment in the food sector and many now operate a wide range ofbusiness and technical training programs, credit schemes andbusiness support programs. They may work directly with smallfarmers and agribusiness entities, but more frequently supportinstitutions and government agencies that promote businessdevelopment. NGOs can be important intermediaries between farmersand agribusiness to assist in the creation and strengthening oflinkages However (Dannson et al, 2004) suggested that NGOs should beaware of not creating unfair competition by offering subsidized(and hence long-term unsustainable) incentives such as subsidizedfarm-gate price, credit, inputs etc..

Private sector support organizations:-These include manufacturers’associations, Chambers of Commerce and consultants or consultancycompanies. Although the focus and membership of these associationsis often larger companies that are able to afford their fees, theyprovide support by dissemination of information (e.g. on marketopportunities, equipment and service suppliers), provide a forumfor discussion of common problems, and lobby governments for fiscalor legislative changes to benefit their members.

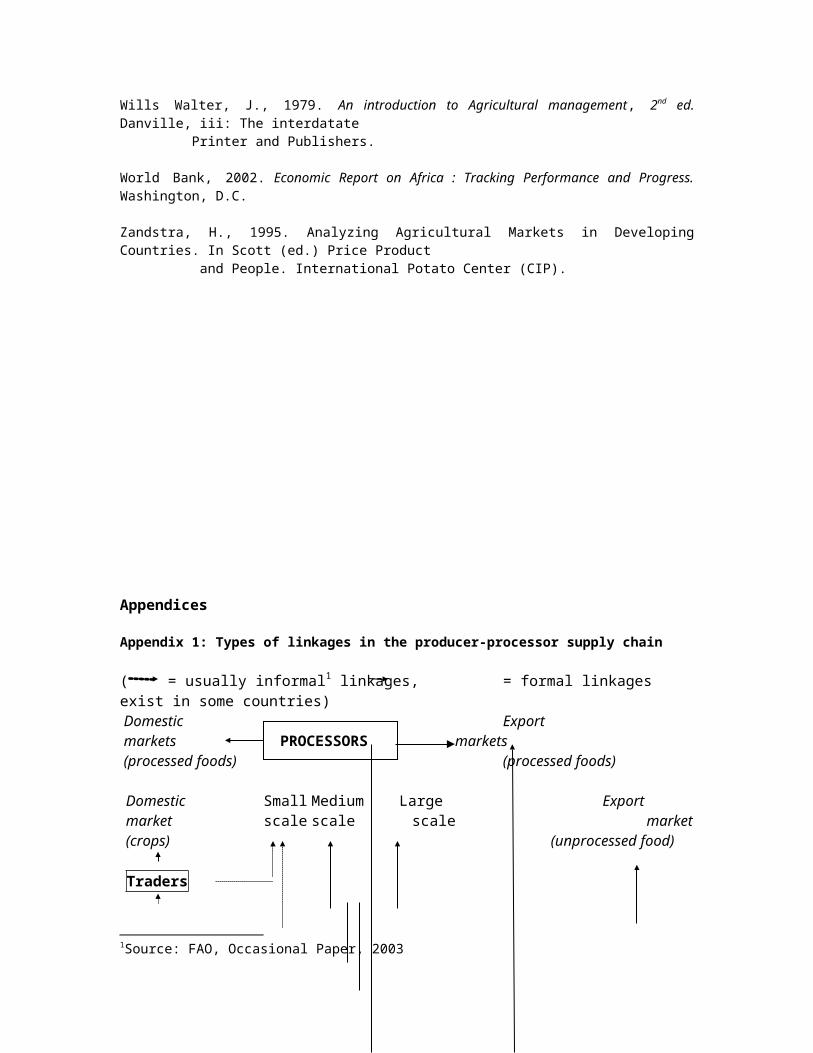

3.2.4 Types of linkages

23

Improving Farmer Agribusiness Market Linkages, the case of Asella Malt Factory and small farmes, Ethiopia Farm-agribusiness linkages evolve around the exchange of rawmaterials between the two parties. These linkages can be classifiedinto primary, secondary and cross-cutting linkages1 (see appendix 1).

Primary linkages: refer to exchanges between main players such asfarmers or farmer's organizations and raw material buyers such asprocessors or traders serving national and international markets.This ranges between simple ad hoc spot market transactions with orwithout the inclusion of intermediaries or informal supplyarrangements to highly managed co-operation such as farming undercontract, asset sharing arrangements between farmers and processorsor fully vertical integration of producing and processingactivities1.

Secondary linkages: are those referring to the supply of supportservices necessary for long-term relationships between farmers andagribusiness. These links traditionally include input supplies suchas seeds, fertilizers, pesticides, rental of agriculturalmachinery, technical assistance, training in good agriculturalpractices, provision of transport and storage facilities etc. Morespecialized secondary linkages develop with higher food safetystandards. These may include cold storage facilities, leasingfacilities, laboratory facilities or business management training1.

Cross cutting linkages: these are complementary to primary andsecondary linkages and address more general needs of key actors infarm-agribusiness linkages such as access to finance and marketinformation or institutional support to agribusiness development.These include financial services and market intelligence servicesand support organizations1.

3.2.5 Linking Arrangements between Farmers and Agro-Processors in Africa

FAO (2004) reported that case studies in selected African countries(Ghana, Kenya, Nigeria, South Africa and Uganda) show that thefollowing are successful farm-agribusiness linkage arrangementsused.

Service Provision:- most agribusiness companies studied provide awide range of extension services to farmers. These services includethe provision of agricultural inputs such as seeds, fertilizer,

1 http://www.fao.org/agribusinesslink/html.

24

Improving Farmer Agribusiness Market Linkages, the case of Asella Malt Factory and small farmes, Ethiopia agrochemicals, veterinary drugs, artificial insemination, animalfeed etc. as well as field preparation services, supply ofirrigation water, produce transport etc. free-of-charge or oncredit. The case studies revealed that the private sector is ableto take over public extension services to primary producers,provided the agro-business is a profitable enterprise.

Price Determination:- prices are normally determined by theprocessor and not by the farmer. In some cases, prices vary fromday to day, according to prevailing market prices, in other cases,like the Mwea rice irrigation scheme and Brookside Dairy Ltd. inKenya, the processor fixes the price on a seasonal basis which thenfluctuate according to market conditions.

Purchasing Arrangements: methods and practices of raw materialexchange can range between simple ad hoc spot market transactionswith or without the inclusion of intermediaries or informal supplyarrangements to highly managed co-operation such as farming undercontract, asset sharing arrangements between farmers and processorsor fully vertical integration of producing and processingactivities.