Embed Size (px)

Citation preview

Technical Paper No. 82December 1997

SD Publication SeriesOffice of Sustainable DevelopmentBureau for Africa

Jim MaxwellRichard GordonAbt Associates

Innovative Approaches toAgribusiness Development inSub-Saharan Africa

Volume 5: Southern Africa

Final Report

Productive Sector Growth and Environment DivisionOffice of Sustainable DevelopmentBureau for AfricaU.S. Agency for International Development

Innovative Approaches to AgribusinessDevelopment in Sub-Saharan Africa

Volume 5: Southern Africa

Final Report

Jim MaxwellRichard GordonAbt Associates

Publication services provided by AMEX International, Inc.pursuant to the following USAID contract:

Project Title: Policy, Analysis, Research, and TechnicalSupport Project

Project Number: 698-0478Contract Number: AOT-C-00-96-90066-00

Technical Paper No. 82December 1997

ii

iii

Contents

Foreword vAcknowledgments viiExecutive Summary ixGlossary of Acronyms and Abbreviations xv

1. General Introduction to the Eight Country Study 1

1.1 Background 11.2 Objective 11.3 Analytical Issues to be Addressed 11.4 The AMIS II Approach to Agribusiness Development Research 11.5 Methodology 21.6 Limitations 31.7 Organization of the Innovative Project Reports 3

2. Introduction to the Southern Africa Study 5

Table 2.1 Size Distribution and Focus of Firms, Associations, and Projects Evaluated 6

3. Key Southern Africa Findings 7

3.1 Non-Traditional Agricultural Export Development 73.2 Indigenous Small and Medium Enterprise Development 10

3.2.1 Overview 103.2.2 Findings 113.2.3 General Observations 133.2.4 Other Indigenous SME Development Findings 133.2.5 Conclusions 14

3.3 Association Development 153.4 Financial Services Development 163.5 Monitoring and Evaluation 183.6 General Recommendations 193.7 Key Issues Deserving Further Study 20

4. Zimbabwe 21

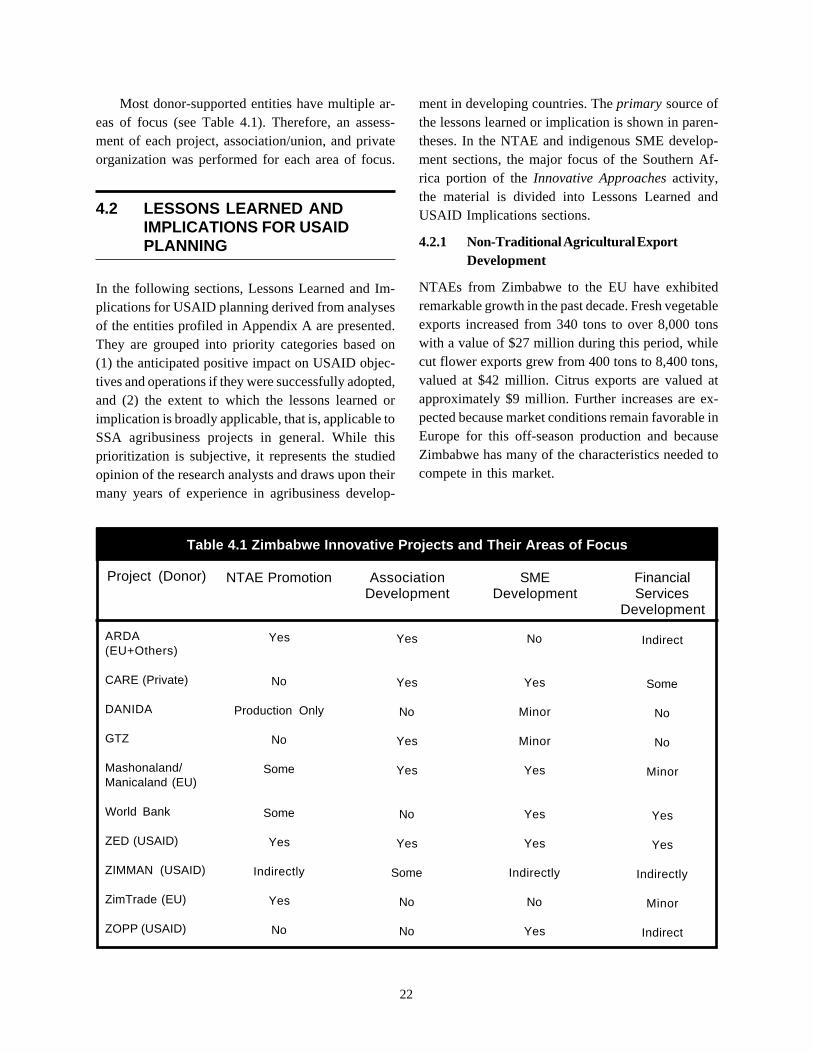

4.1 Entities Selected for Study 214.2 Lessons Learned and Implications for USAID Planning 22

4.2.1 Non-Traditional Agricultural Export Development 224.2.2 Indigenous SME Development 254.2.3 Association Development 284.2.4 Financial Services Development 294.2.5 Monitoring and Evaluation 304.2.6 General Recommendations 304.2.7 Key Issues Deserving Further Study 31

iv

4.3 USAID Zimbabwe Agribusiness Development Recommendations 31

Table 4.1 Zimbabwe Innovative Projects and Their Areas of Focus 22

5. Mozambique 35

5.1 Entities Selected for Study 355.2 Lessons Learned and Implications for USAID Planning 36

5.2.1 Non-Traditional Agricultural Export Development 365.2.2 Indigenous SME Development 375.2.3 Association Development 425.2.4 Financial Services Development 425.2.5 Monitoring and Evaluation 435.2.6 General Recommendations 445.2.7 Key Issues 45

5.3 USAID Mozambique Agribusiness Development Recommendations 45

Table 5.1 Mozambique Innovative Projects/Associations and Their Areas of Focus 36

6. Tanzania 47

6.1 Entities Selected for Study 476.2 Lessons Learned and Implications for USAID Planning 48

6.2.1 Non-Traditional Agricultural Export Development 486.2.2 Indigenous SME Development 516.2.3 Association Development 576.2.4 Financial Services Development 586.2.5 Monitoring and Evaluation 596.2.6 General Recommendations 606.2.7 Key Issues Deserving Further Study 61

6.3 USAID Tanzania Agribusiness Development Recommendations 62

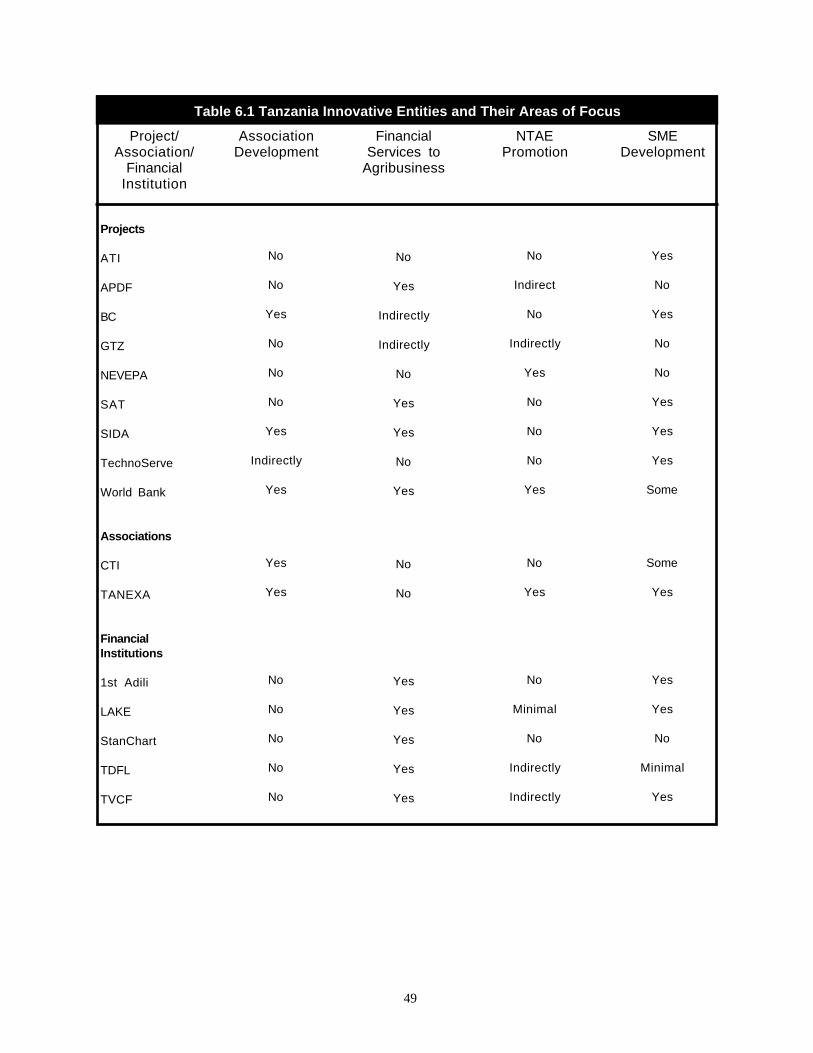

Table 6.1 Tanzania Innovative Entities and Their Areas of Focus 49

Appendixes

Appendix A - Detailed Profiles - Zimbabwe 67Appendix B - Detailed Profiles - Mozambique 95Appendix C - Detailed Profiles - Tanzania 111Appendix D - Contacts 137

Notes 143

v

Foreword

The creation of the Development Funds for Africa(DFA), and, more recently, funding constraints havechallenged the U.S. Agency for International Devel-opment (USAID) to scrutinize vigorously the effec-tiveness and impact of its development assistanceprograms in Africa and to make adjustments neededto improve on the record of the past. Structural Ad-justment programs have been adopted by many sub-Saharan African countries, albeit reluctantly, and somesignificant economic development progress has beenmade. As donor agencies face severe cutbacks andrestructuring of their own and as less assistance be-come available to developing countries, in sub-Sa-haran Africa and elsewhere, new ways must be foundto channel the declining resources to their most effec-tive and productive uses. Donor agencies like USAID,therefore, are increasingly looking at the private sec-tor for new and innovative ways of improving com-petitiveness, and often to agriculture as the potentialcatalyst for generating broad based, sustainable eco-nomic growth. In the light of the DFA and sub-Saharan African countries’ recent development expe-riences under Structural Adjustment Program, theUSAID Africa Bureau’s Office of Sustainable Devel-opment, Division of Productive Sector Growth andEnvironment (formerly ARTS/FARA), has been ex-amining the Agency’s approach to the agriculturalsector.

In January 1991, the Africa Bureau adopted “AStrategic Framework for Promoting AgriculturalMarketing and Agribusiness Development in sub-Saharan Africa” to provide analytical guidance toUSAID/W, REDSOs, and field missions. The frame-work suggested that:

(a) while technical and environmental problems mustcontinue to be addressed, a major cause of poorperformance of the agricultural sector has beenthe inefficiency of the market structures and strat-egies;

(b) improvements in marketing efficiency require agood understanding of the structural arrange-ments, organization and operating strategies avail-able to those entrepreneurs who constitute themajority of the business entities;

(c) such improvements could have a significant ben-eficial impact on incomes, foreign exchange earn-ings, domestic consumption and food security.

To enhance the analytical guidance and technicalsupport that the African Bureau provides to the field,SD/PSGE initiated a series of assessment of donoragencies’ innovative agribusiness projects in a num-ber of sub-Saharan Africa countries to develop casestudies of agribusiness firms targeted by or benefit-ting from these projects. The objective of the assess-ments was to provide the Africa Bureau and FieldMissions with an understanding of the role and sig-nificance of new, innovative agricultural marketingand agribusiness programs being implemented, andto synthesize a cogent set of lessons learned and theirimplications for USAID agribusiness project designand implementation.

This document is Volume 5 of a five-volume setpresenting the Southern Africa (Mozambique, Tan-zania and Zimbabwe) research findings. While theSouthern Africa research addressed all of the keyfocus areas of the Innovative Approaches activity, itplaced special emphasis on SME development andNTAE development. These topics are, therefore, cov-ered in more detail in this report.

Abt Associates, under the Global Bureau’s AMISII project, conducted the field research and reportpreparation. The USAID field mission in each coun-try collaborated with PSGE/PSD and Abt Associates,the contractor, and was particularly helpful in provid-ing counsel and direction of the field research andreviewing of the field draft report.

vi

SD/PSGE believes that the findings and recom-mendations of this report will help the Africa Bureau,field missions, host country governments, and pri-vate sector groups make more informed decisions onfuture project design, implementation, monitoring,and evaluation.

David AtwoodChief, Productive Sector Growthand Environment DivisionOffice of Sustainable DevelopmentAfrica BureauUSAID

vii

Acknowledgments

Abt Associates, the AMIS II team, and the authorswish to thank the many individuals in Zimbabwe,Mozambique, and Tanzania who contributed theirtime and experience to this study. A list of individualsinterviewed is included as Appendix D. Of specialassistance were Robert Armstrong and AlexanderShapleigh at USAID/Zimbabwe, David Newberg andFernando Pixiao at USAID/Mozambique, and DianaPutman and Thomas Tengg at USAID/Tanzania.

John Holtzman of Abt Associates enhanced thereport with his technical review and Jack Hopper didthe final edit. Otilia Santos of Abt Associates spentmany long hours formatting and finalizing the report.

Dr. Charles Whyte of AFR/SD/PSGE/PSD is theInnovative Approaches activity manager and was asubstantial and ongoing contributor to all phases andaspects of the activity, especially analysis and draftenhancement.

The overall Innovative Approaches activity ismanaged by Jim Maxwell of AMIS II/Cargill Tech-nical Services, who was also the principal analyst andauthor of sections of this report other than thoserelating to SME development. Dr. Richard Gordonwas the principal contributor of the material on SMEdevelopment.

viii

ix

The purpose of this activity was to assess donoragencies’ innovative agribusiness projects in a num-ber of Sub-Saharan Africa (SSA) countries and todevelop case studies of agribusiness firms targeted byor benefiting from these projects. The objective is toprovide the Africa Bureau and Field Missions with anunderstanding of the role and significance of new,innovative agricultural marketing and agribusinessprograms being implemented, and to synthesize acogent set of lessons learned and their implicationsfor USAID agribusiness project design and imple-mentation.

The methodology used for this activity consistedof the following four basic steps: (Step 1) identifyand select Key Focus (apparent high-opportunity)Areas for research based on current USAID interestsand the anticipated potential to have a positive affecton agribusiness development. The four Key FocusAreas chosen, based on a literature review, inter-views in Washington, and a field survey, were non-traditional agricultural exports (NTAE) develop-ment, association development, small and mediumenterprise (SME) development, and financial ser-vices to agribusiness; (Step 2) select countries wherethere are projects, associations, and financial institu-tions that are relevant to activity objectives and theKey Focus Areas and that are sufficiently developedto yield lessons learned; (Step 3) complete a field tripto the selected countries to collect detailed informa-tion on the relevant projects and perform case studieson target beneficiaries, primarily via in-depth inter-views with project, association, and financial inter-mediary managers, donor management, and selectedbeneficiaries; and (Step 4) analyze the informationcollected, extract lessons learned, and suggest theimplications for enhancing the design, implementa-tion, and monitoring and evaluation of USAIDagribusiness projects.

The entire Innovative Approaches activity hasfive components, and research findings are reported

in separate volumes. Volume 3 covers East Africa(Kenya and Uganda), Volume 5 Southern Africa(Zimbabwe, Mozambique, and Tanzania), and Vol-ume 4 West Africa (Ghana, Mali, and Senegal). Thereare also separate volumes reporting on the SecondaryResearch Findings (Volume 2) and Overall ProjectSummary and Conclusions (Volume 1).

While the Southern Africa research addressed allof the key focus areas of the Innovative Approachesactivity, it placed special emphasis on SME develop-ment and NTAE development. Therefore, these top-ics are covered in more detail in this report.

SOUTHERN AFRICA FINDINGSSUMMARY– BY KEY FOCUS AREA

Non-Traditional Agricultural Exports Development

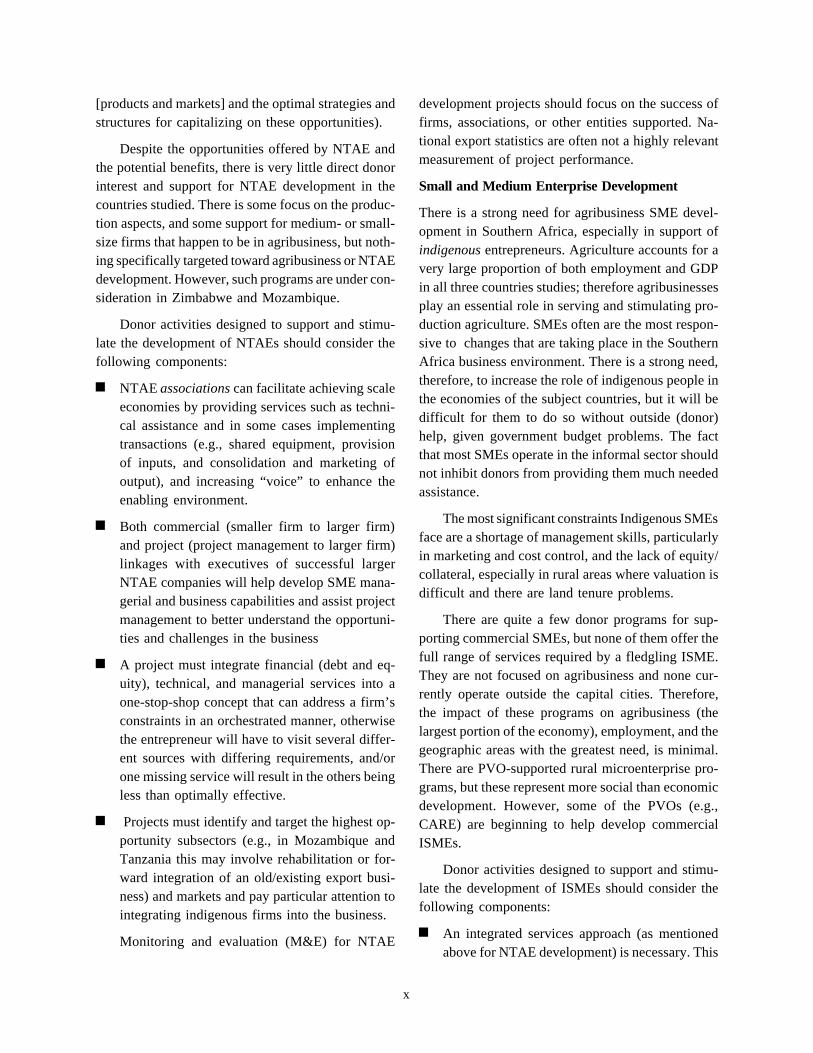

There is significant potential for non-traditional agri-cultural exports (NTAE) development in the coun-tries included in this research. Opportunities in devel-oped country (primarily the EU), second-tier (e.g.,Singapore and the Middle East), and regional marketsare currently being successfully developed by firmsbased in Southern Africa. While the developed coun-try markets are very competitive and require tightcost and quality control, some of the other marketsare less complex, and therefore, more available tosmaller size firms. NTAE promotion also representsan opportunity for broad-based economic develop-ment and for increasing the access of the indigenouspopulation to the commercial economy because, un-der the right conditions, indigenous smallholders andSMEs can successfully participate.

Development of NTAE is constrained by a lackof entrepreneurial equity/collateral, inadequate infra-structure (especially roads, airports, and communica-tions), and poor organization (i.e., the lack of a clearunderstanding of the highest priority opportunities

Executive Summary

x

[products and markets] and the optimal strategies andstructures for capitalizing on these opportunities).

Despite the opportunities offered by NTAE andthe potential benefits, there is very little direct donorinterest and support for NTAE development in thecountries studied. There is some focus on the produc-tion aspects, and some support for medium- or small-size firms that happen to be in agribusiness, but noth-ing specifically targeted toward agribusiness or NTAEdevelopment. However, such programs are under con-sideration in Zimbabwe and Mozambique.

Donor activities designed to support and stimu-late the development of NTAEs should consider thefollowing components:

n NTAE associations can facilitate achieving scaleeconomies by providing services such as techni-cal assistance and in some cases implementingtransactions (e.g., shared equipment, provisionof inputs, and consolidation and marketing ofoutput), and increasing “voice” to enhance theenabling environment.

n Both commercial (smaller firm to larger firm)and project (project management to larger firm)linkages with executives of successful largerNTAE companies will help develop SME mana-gerial and business capabilities and assist projectmanagement to better understand the opportuni-ties and challenges in the business

n A project must integrate financial (debt and eq-uity), technical, and managerial services into aone-stop-shop concept that can address a firm’sconstraints in an orchestrated manner, otherwisethe entrepreneur will have to visit several differ-ent sources with differing requirements, and/orone missing service will result in the others beingless than optimally effective.

n Projects must identify and target the highest op-portunity subsectors (e.g., in Mozambique andTanzania this may involve rehabilitation or for-ward integration of an old/existing export busi-ness) and markets and pay particular attention tointegrating indigenous firms into the business.

Monitoring and evaluation (M&E) for NTAE

development projects should focus on the success offirms, associations, or other entities supported. Na-tional export statistics are often not a highly relevantmeasurement of project performance.

Small and Medium Enterprise Development

There is a strong need for agribusiness SME devel-opment in Southern Africa, especially in support ofindigenous entrepreneurs. Agriculture accounts for avery large proportion of both employment and GDPin all three countries studies; therefore agribusinessesplay an essential role in serving and stimulating pro-duction agriculture. SMEs often are the most respon-sive to changes that are taking place in the SouthernAfrica business environment. There is a strong need,therefore, to increase the role of indigenous people inthe economies of the subject countries, but it will bedifficult for them to do so without outside (donor)help, given government budget problems. The factthat most SMEs operate in the informal sector shouldnot inhibit donors from providing them much neededassistance.

The most significant constraints Indigenous SMEsface are a shortage of management skills, particularlyin marketing and cost control, and the lack of equity/collateral, especially in rural areas where valuation isdifficult and there are land tenure problems.

There are quite a few donor programs for sup-porting commercial SMEs, but none of them offer thefull range of services required by a fledgling ISME.They are not focused on agribusiness and none cur-rently operate outside the capital cities. Therefore,the impact of these programs on agribusiness (thelargest portion of the economy), employment, and thegeographic areas with the greatest need, is minimal.There are PVO-supported rural microenterprise pro-grams, but these represent more social than economicdevelopment. However, some of the PVOs (e.g.,CARE) are beginning to help develop commercialISMEs.

Donor activities designed to support and stimu-late the development of ISMEs should consider thefollowing components:

n An integrated services approach (as mentionedabove for NTAE development) is necessary. This

xi

necessitates an extensive network of alliance part-ners who help to provide the broad range ofservices needed.

n Because an integrated approach is resource in-tensive, significant leveraging is necessary. Thisincludes involving several donors who can con-tribute financial, technical, and managerial assis-tance. Extensive private sector input should beincluded in both project design and implementa-tion, and local consultants should be developedso that they can competently provide services(particularly as related to marketing and costcontrol) on an ongoing basis.

n SME entrepreneurs need significant help to de-velop a highly functional business plan and touse that plan as the basis for an application forfinancing. Therefore, this service should be apart of the services offered.

n The project must provide close monitoring of andproper mentoring for clients, especially after fi-nancial assistance has been provided.

n It is unlikely that an entity that provides servicesto start-up and micro and small clients can everbecome self-supporting, unless such an entity isan umbrella organization.

M&E for this type of project should focus on thefinancial success of clients, the number of clientsassisted, the employment generated, and how well itis able to meet its own agreed budgets.

Association Development

Association development in Southern Africa offersconsiderable positive impact potential because asso-ciations can be an effective and efficient way to helpindigenous small producers and ISMEs leverage sup-port for development of subsectors opportunities. Suc-cessful associations will eventually become self-sup-porting.

The main constraints to association developmentsuccess are: the legacy of former socialist govern-ments’ control of cooperatives in Mozambique andTanzania, the tendency for producer-based associa-tions to be concerned only with production issues, thelow level of training (especially financial) and part-

time status of most association management, mem-bers’ lack of finance and financial viability, and dif-ficulties association management has in determiningmembers’ priority needs and developing programs toeffectively serve their highest priority needs.

Donor involvement in agribusiness associationdevelopment is minimal in the three countries stud-ied. EU donors support chambers of commerce, butthese are usually composed of urban-based traders.USAID is considering support for reorganizing theHorticultural Promotion Council in Zimbabwe, andUSAID supports The Business Center project in Tan-zania, which helped an NTAE association get orga-nized.

Donor activities designed to support and stimu-late the development of agribusiness associationsshould consider the following components:

n Assistance to help determine the priority needs ofmembers and potential members and to developprograms that serve a limited number of theirhighest priority needs.

n Help train association management in how tomanage a sustainable association with a focus onsources and uses of funds, maintaining positivemember relations, and effective lobbying.

n Encourage a vertically integrated structure thatinvolves producers, packers/processors, export-ers, and others to enable a greater number ofmembers and better industry coordination.

n Assist the formation of a multilayer structurewherein small groups of producers form self-help groups, that belong to a subsector associa-tion, which in turn belongs to a sector associa-tion. This will enable donors to support theumbrella sector association, which in turn cansupport and develop the levels below it. Theumbrella association can afford professional man-agement and will have a greater “voice” due tothe large number of members it represents.

M&E for association development projects shouldemphasize the membership-defined success (as de-fined by members) and progress toward sustainabilityof supported associations. The results of an annual

xii

membership satisfaction survey, conducted by a thirdparty, should be one of the most important criteria forcontinued donor support of an association.

Financial Services to Agribusiness

Because the lack of access to financing is widelybelieved to be the greatest initial constraint to busi-ness formation and expansion for all but the largestfirms, there is a major need for financial services tosupport ISMEs, especially in Tanzania andMozambique where the financial sector is nearly non-functional (at least for SMEs). Without financingsupport the agribusiness sector will not develop inthese countries and therefore the development of theagricultural sector will be inhibited.

The main constraints to agribusiness financing,according to the potential borrowers, are lack of eq-uity/collateral (especially in rural areas), poor record-keeping practices, inability to develop a viable busi-ness plan and proper financing application based onthat plan, and missing types of needed financing suchas trade credit or venture capital. Institutional con-straints are a non-supportive legal environment, thehigh cost of experienced financing and fund manag-ers versus the average size and volume of viablefinancing opportunities, the transaction and follow-up costs of small-scale financing, and the generalshortage of investable projects (although there is nota shortage of funds).

Donor supported financing is fairly significant inMozambique and Tanzania. EU donor microenterprisefinancing and World Bank SME financing are nearlythe only formal sources available to those groups inMozambique, and the World Bank SME program isabout to lose its intermediaries since, once privatized,their loan practices will have to be dramataicallyaltered. Donor-supported financial institutions in Tan-zania are also the only sources of finance for microsand SMEs, but none of these institutions focus onagribusiness. The commercial financial sector in Zim-babwe is well developed, but it does not focus onagribusiness ISMEs.

Donor activities designed to support and stimu-late the development of agribusiness financial ser-vices should consider the following components:

n Loan officer training to help them assess financ-ing applications on bases other than theborrower’s balance sheet/collateral.

n Assistance for borrowers to develop viable busi-ness plans and financing applications based onthose plans, and ways to enhance post-financingfollow-up and support. This means providingmanagement and technical services to clients.

n Creative and flexible products such as sweat andin-kind equity, income notes, convertible debt,and so forth.

n Group lending for small borrowers.

n Using existing successful institutions where pos-sible.

n Provide multidonor support due to the minimumsize project needed to afford top-quality manage-ment. Consider making managers responsible formultiple projects/funds in one country or regionalprojects/funds.

The M&E of financial services projects must bevery commercially oriented (i.e., focused on assetgrowth and ROI/ROA).

Monitoring and Evaluation

There are opportunities to enhance the M&E of agri-business projects or project components that supportagribusiness development. However, more benefitwould be derived from a greater focus on more effec-tive design and implementation than on increasedemphasis on formal M&E systems.

USAID agribusiness development projects mostoften have the objective of stimulating firm-leveldevelopment over a usually rather short term (three tofive years). That is insufficient time to have anysignificant effect on macro-level economic growth,employment, or even NTAE volume.

Fortunately, USAID projects are rarely imple-mented through government entities. Other donors,whose policy is to work through such agencies, havea very difficult time assessing the results of theirefforts because the results are heavily dependent onthe effectiveness of the agencies’ implementation,over which the donors have minimal control. This is

xiii

especially true in countries where civil servants aregrossly underpaid and must work two jobs and/or usetheir government position as a source of additionalincome.

The more effectively managed the organization,the more specific its M&E programs will be. M&Efor agribusiness development projects must be pre-dominantly focused on commercial measurementssuch as sales and earnings growth, net asset growth,and return on investment for both the developmententity and its clients. M&E for donor-supported ven-ture capital funds should be based on financial perfor-mance (the fund and that of its investments) as wellas on the number of clients served and investmentsassessed. Over the long term, the ability to sell invest-ments at an acceptable price will also be important.Group lending project M&E considerations shouldinclude: unit transaction costs, repayment rate,sustainability of the credit entity, growth in the capitalbase of entities, and the savings rate of members/clients.

Very few agribusiness projects have been able todevelop effective M&E approaches that can isolatethe effect of external variables such as drought orsignificant changes in the enabling environment or themarket.

General Recommendations

An ongoing, formal, and SSA-wide information ex-change should be established on agribusiness devel-opment lessons learned and the implications for USAIDproject/activity design and implementation. This wouldincorporate the experience of all SSA donors workingin the area and could be initiated based on the findingsof this Innovative Approaches activity.

Multidonor agribusiness development projects (es-pecially if financing focused) should be exploredespecially where cooperatives are responsible for anarea where they have extensive experience. Also,some PVOs (e.g., CARE in Zimbabwe andMozambique) may be able to move beyond produc-tion agriculture and social development into seriouseconomic development, and should therefore be con-

sidered as partners for agribusiness developmentprojects, especially in rural areas.

Agribusiness development projects must be man-aged by individuals with considerable successful com-mercial agribusiness experience. Local staffing shouldtake place from the highest positions downward sothat as much local input as possible can be incorpo-rated into the staffing process. All expatriate posi-tions must have a local counterpart.

Country-level agribusiness opportunities thatUSAID should assist in supporting are an integratedservices horticulture development center focused onISMEs in Zimbabwe, a cashew and coconut rehabili-tation project focused on the role of SMEs inMozambique, and an integrated services, NTAE-fo-cused Food and Agribusiness development Centerlocated in the Arusha/Moshi area in Tanzania.

Key Issues

What is the best way to assess the feasibility of and,if feasible, to install a model of an integrated services,widely supported Agribusiness Development Centerin Southern Africa, and where is the highest opportu-nity location?

Why do Tanzanian cashew producers receive amuch higher portion of the export value per kg thando cashew producers in Mozambique, and how canthe share going to the producer in Mozambique beincreased?

What is the best way to determine the viability ofand to develop highly leveraged (multidonor and ex-tensively networked with the private sector) agribusi-ness projects (especially NTAE) in geographic areasthat apparently have potential for a broad-based,positive impact?

How can the success, future prospects, andspecific agreements of apparently functional outgrowerand subcontractor schemes (e.g., in the Arusha/Moshiarea) be further assessed?

How can the success of CARE’s high-potentialand very innovative “village trader” project in Zimba-bwe be best monitored and evaluated by USAID?

xiv

xv

ACP African Caribbean and Pacific countries (of the Lome Convention)

AFC Agricultural Finance Corporation

AMIS II Agribusiness and Marketing Improvement Strategies Project II

APDF Africa Project Development Facility

ARDA Agricultural and Rural Development Authority (various)

ASC Agribusiness Service Centers

BSBC Barclay’s Small Business Center

CARE Care International in Zimbabwe

CDC Commonwealth Development Corporation

CdZ Companhia da Zambezia

CFU Commercial Farmers Union

DANIDA Danish International Development Authority

DM Deutsche Mark

EDESA Economic Development in Equatorial and Southern Africa Societe Anonyme

EIM Equity Investment Management Ltd.

EU European Union

FADC Food and Agribusiness Development Centers

FAO Food and Agricultural Organization

FAO/AgMin Food and Agricultural Organization of the UN/Mozambique Ministry of Agriculture

GTZ German Technical Assistance

HPC Horticultural Promotion Council

ICFU Indigenous Commercial Farmers Union

IDIL Instituto Nacional de Desenvolvimento de Industria Local

IFAD International Fund for Agricultural Development

IFC International Finance Corporation

ILO International Labor Organization

IRR International Rate of Return

ISME Indigenous small and medium enterprise

Glossary of Acronyms and Abbreviations

xvi

K-MAP Kenya Management Assistance Program

LIBOR London Interbank Offered Rate

M&E Monitoring and Evaluation

NGO Non-Government Organization

NTAE Non-Traditional Agricultural Exports

OCA Operational Constraints Analysis

ODA Overseas Development Administration

PVO Private Voluntary Organization

REDSO Regional Economic Development Support Office of USAID

ROI Return on Investment

SD/PSGE Sustainable Development/Productive Sector Growth & Environment

SHG Self-Help Group

SIDA Swedish International Development Authority

SME Small and Medium Enterprise

SSA Sub-Saharan Africa

TBC The Business Center

TDFL Tanzania Development Finance Limited

TVCF Tanzania Venture Capital Fund

USAID United States Agency for International Development

VCCZ Venture Capital Company of Zimbabwe

WB World Bank

ZED Zimbabwe Enterprise Development Project

ZFU Zimbabwe Farmers Union

ZimBank Zimbabwe Banking Corporation Limited

ZIMMAN Zimbabwe Manpower

ZimTrade Zimbabwe Export Promotion Program

ZOPP Zimbabwe Oil Press Project

1

1. General Introductionto the Eight Country Study

1.1 BACKGROUND

USAID Missions, and to a lesser extent other donors,are designing and implementing programs with theobjective of developing more efficient agriculturalproduct marketing systems. The Africa Bureau’s Ag-ricultural Marketing and Agribusiness DevelopmentStrategic Framework calls for examining marketingconstraints and identifying ways to improve marketingefficiency. USAID does not yet have effective moni-toring and evaluation mechanisms for recently estab-lished agribusiness development programs nor ways todisseminate the lessons learned from these innovativeprojects to Missions in other countries.

USAID’s Africa Bureau therefore requested theAgribusiness and Marketing Improvement Strategies(AMIS II) project to carry out surveys of innovativeagribusiness projects in a number of Sub-SaharanAfrica (SSA) countries for the purpose of providingthe Bureau and Field Missions with: (a) a compilationof lessons learned to assist in developing future mar-keting and agribusiness development activities and (b)an effective monitoring/evaluation mechanism for itspresent and future activities.

1.2 OBJECTIVE

“The objective of this research activity is to increaseunderstanding of the role and significance of new,innovative agricultural marketing and agribusinessprograms that Missions are implementing, and to syn-thesize a cogent set of ‘lessons learned’. In an era ofscarce development resources it is primordial that de-sign innovations and project successes be dissemi-nated rapidly and replicated elsewhere. As agribusi-ness development projects have grown more complex,the need for monitoring and evaluation has risen ac-cordingly. The research activity will focus on twocategories of innovative programs to support agricul-

tural marketing development: supporting services andinstitutions; and financial systems and services.”1

1.3 ANALYTICAL ISSUES TO BEADDRESSED

The research activity calls for the consultant to moni-tor in the targeted countries the impact of new andinnovative programs implemented by any donor agencyand to carry out case studies of agribusiness firmstargeted by a project or benefiting from a project.

As called for in the Statement of Work referencedabove, the major analytical issues to be addressed are:

1. What are the major constraints that the program ormechanism was designed to address?

2. What are the performance indicators to measureimpact and how do they relate to the goal andpurpose of the mechanism/project?

3. What has been the effect of the mechanism/projecton private sector investment levels, export promo-tion, and people-level impacts?

1.4 THE AMIS II APPROACH TOAGRIBUSINESS DEVELOPMENTRESEARCH

The AMIS II Project was designed to provide USAIDaccess to private sector commercial expertise that wouldhelp improve agribusiness marketing efficiency.

The major focus of the project is on stimulatingprivate sector led economic development, not onenabling environment enhancement or social develop-ment. Although enabling environment enhancement/social development is an important aspect of economicdevelopment, the AMIS II project addresses it onlywhen it acts as a constraint to commercial develop-ment. AMIS II focuses primarily on the provision of

2

inputs to production agriculture and all aspects ofagriculture after the farm gate. The project does notlook at production agriculture issues unless so dictatedby market requirements. The project utilizes a marketled or demand pull approach.

The AMIS II approach is to address agribusinessmarketing efficiency improvement and agribusinessproject impact measurement and evaluation from acommercial/analytical perspective. Thus the report ismore prescriptive in nature and less descriptive thana typical USAID project report. In other words, itdeals more with the “so what?” and less with the“what’s so” of agribusiness development activities.

The principal authors of this report (Maxwell andGordon) are first and foremost agribusiness opera-tions and consulting professionals,with between themmore than 50 years of international private sectorfood and agribusiness development experience, muchof which was gained while living and working outsidethe United States. Most of this experience was inmanagement positions with leading food, agribusiness,and agribusiness supply firms such as Beatrice Foods,ConAgra, Cargill, and Monsanto, and was focused onbusiness expansion and market entry in developingcountries. Dr. Gordon is currently Professor ofAgribusiness Studies at the Arizona State UniversityCentre for Agribusiness Policy Analysis. Jim Max-well currently works for Cargill Technical Services,Cargill’s Africa operations include fifteen agribusi-nesses located in eight different African countries.

The result of the above orientation is a presenta-tion style that is not academic, but crisp, authorita-tive, and judgmental. It is based on the authors’intimate and extensive knowledge of agribusinessfirm operations, investor/financier perspectives, andtheir significant business development/market entryconsulting experience. Therefore, the presentationstyle used herein utilizes pointed observations andrepresents the best business judgment of highly expe-rienced and successful practitioners.

1.5 METHODOLOGY

The methodology adopted by the AMIS II team forthis activity consisted of the following steps:

1. Identify and select Key Focus (apparent highopportunity) Areas for research based on majorareas of current USAID interest and the antici-pated potential of a key focus area to positivelyaffect agribusiness development. The four areaschosen, based on a literature review, interviewsin Washington, and a field survey, were Non-traditional Agricultural Export Development,Association Development, Small and MediumEnterprise Development, and Financial Ser-vices. The first three fall into the category of“supporting services,” as mentioned in projectobjectives (see section 1.2), while the fourthrelates to the second category — financial sys-tems and services.

2. Conduct a literature search on all identifiableUSAID and other donor-supported agribusinessprojects in SSA countries.

3. Based on (1) and (2) above, select the SSAcountries that have agribusiness projects or ac-tivities, sponsored by any donor, that relate to theKey Focus Areas. Solicit USAID Mission supportto work in those countries that have both relevantprojects and activities and sizeable agribusinesssectors.

4. Arrange and complete an initial field trip to coun-tries where USAID Missions invited the consult-ants to work, and that have apparently relevantagribusiness projects and activities being imple-mented. Collect additional information on the se-lected projects and on any others suggested byfield personnel. Confirm Mission and REDSO-level Key Focus Area interest.

5. Screen the identified projects or activities andselect those that have aspects relevant to projectobjectives and to the Key Focus Areas and thatare sufficiently developed to start yielding les-sons learned.

6. Arrange and complete a field trip to collect de-tailed information on the most relevant projectsand do case studies on target beneficiaries, pri-marily via in-depth interviews with project man-agers, donor management, and beneficiaries.

7. Analyze the information collected, extract les-

3

sons learned, and suggest the implications forenhancing the design, implementation, and moni-toring and evaluation of USAID agribusinessprojects.

8. Expand the geographic coverage and increase thedepth of analysis in countries and Areas of Focusdetermined to be of high potential to USAID agri-business activity design and implementation.

This Southern Africa report represents the addi-tion of three countries and a particular focus on SMEand NTAE development.

1.6 LIMITATIONS

Research was limited to the countries that respondedpositively to the SD/PSGE/PSD request for collabora-tion. The contractor invested considerable time obtain-ing permission from Missions to travel to their coun-tries.

USAID has been the only donor interested in agri-business development and this interest is quite recent.Therefore there are very few USAID projects with asufficient track record for in-depth evaluation (i.e.,any results are very short term in nature). Very re-cently, the World Bank and some German donor foun-dations have focused on private sector development,which often includes agribusinesses.

1.7 ORGANIZATION OF THEINNOVATIVE PROJECTREPORTS

The entire Innovative Approaches project had twophases. Phase I covered East Africa and Phase IIadded West Africa and Southern Africa, (this report),and three secondary literature studies.

Innovative Approaches research findings are re-ported in separate volumes for East Africa (Kenyaand Uganda-[Volume 3]), Southern Africa (Zimba-bwe, Mozambique, Tanzania-[Volume 5]), and WestAfrica (Ghana, Mali, and Senegal-[Volume 4]). Thereare separate reports on the Secondary Research Find-

ings (Volume 2) and Overall Project Summary andConclusions (Volume 1).

Each of the regional reports are organized asfollows:

n Introduction

n Key Regional Findings (organized by the fourareas of focus plus monitoring and evaluation,general recommendations, and issues deservingfurther study)

n Country-Specific Studies (separate chapters)

— Entities/Case Studies Selected

— Findings on Donor Projects

— Findings on Associations

— Findings on development Finance Organiza-tions

— Findings on Private Agribusiness Firms

— Lessons Learned and Implications for USAIDPlanning

— Each of these sections is organized by thefour Areas of Focus. There are also sectionson Monitoring and Evaluation, General Rec-ommendations, and Issues Deserving Fur-ther Study.

Findings on the larger projects and associationswere analyzed based on the specific research ques-tions listed in the Scope of Work. The research ques-tions, as interpreted by the consultants, are as follows:

1. What project or activity objectives are relevant tothe areas of focus chosen for study?

2. How are these aspects of the activity innovative?

3. What performance indicators were or are beingused to monitor/measure impact of the activity?

4. How are external influences being managed?

5. How successful have the relevant interventionsbeen?

6. What new agribusiness opportunities have resultedfrom the activity?

7. What monitoring and evaluation mechanisms, sys-

4

tems, and indicators can be suggested?

8. What relevant lessons can be learned from thisactivity? What mechanisms worked and did notwork, and how could the impact be improved/enhanced?

9. What are the relevant implications for USAIDproject design and implementation?

10. What new mechanisms or interventions can besuggested to increase the effectiveness of theseprojects or activities?

11. What indicators of project success can be sug-gested, and what is the best way to monitor thoseindicators?

12. What other useful information should be reportedand what are the main unresolved issues?

5

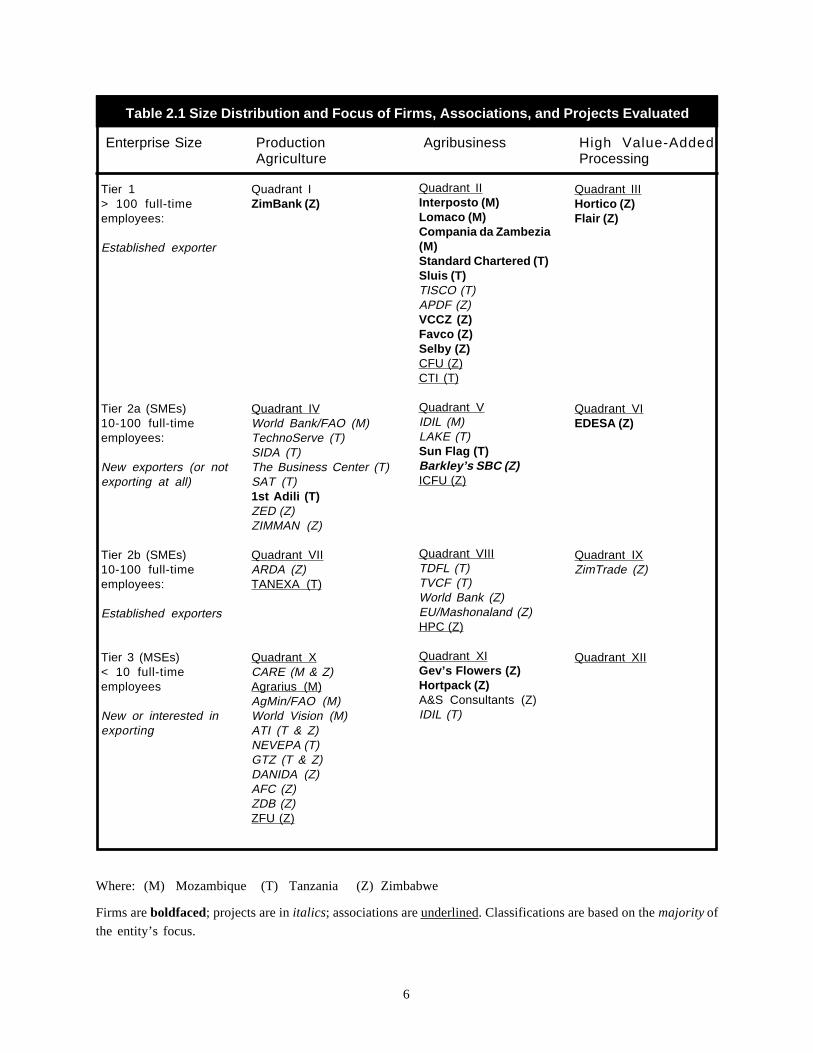

2. Introduction to theSouthern Africa Study

Individuals representing entities from a broad rangeof sizes and stage of participation in the food systemwere interviewed during the fieldwork in Zimbabwe,Mozambique, and Tanzania. A list of these individu-als appears in Appendix D; the entities they representare categorized in Table 2.1. With respect to thistable, please note that:

n The focus of the AMIS II project is on quadrantsV, VI, VIII, IX, and XI.

n In general, the viability of commercial entitiesdecreases from the top right (III) to the bottom left(X) quadrant, with commercial, project, and asso-ciation risks increasing (due to the vagaries of

nature, lack of management capacity, and tightermargins) in a very similar manner.

n One objective of the Innovative Approaches ac-tivity is to identify, based on lessons learned,sustainable interventions that will make agribusi-ness ventures more viable and vibrant, particu-larly in quadrants V, VI, VIII, and IX. However,very few firms, projects, or associations were iden-tified in quadrants VI and IX.

n Given the relatively undeveloped nature of theprivate sector in Mozambique and Tanzania, mostprojects are focused on quadrant X.

6

Table 2.1 Size Distribution and Focus of Firms, Associations, and Projects Evaluated

Enterprise Size

Tier 1> 100 full-timeemployees:

Established exporter

Tier 2a (SMEs)10-100 full-timeemployees:

New exporters (or notexporting at all)

Tier 2b (SMEs)10-100 full-timeemployees:

Established exporters

Tier 3 (MSEs)< 10 full-timeemployees

New or interested inexporting

ProductionAgriculture

Quadrant IZimBank (Z)

Quadrant IVWorld Bank/FAO (M)TechnoServe (T)SIDA (T)The Business Center (T)SAT (T)1st Adili (T)ZED (Z)ZIMMAN (Z)

Quadrant VIIARDA (Z)TANEXA (T)

Quadrant XCARE (M & Z)Agrarius (M)AgMin/FAO (M)World Vision (M)ATI (T & Z)NEVEPA (T)GTZ (T & Z)DANIDA (Z)AFC (Z)ZDB (Z)ZFU (Z)

Agribusiness

Quadrant IIInterposto (M)Lomaco (M)Compania da Zambezia(M)Standard Chartered (T)Sluis (T)TISCO (T)APDF (Z)VCCZ (Z)Favco (Z)Selby (Z)CFU (Z)CTI (T)

Quadrant VIDIL (M)LAKE (T)Sun Flag (T)Barkley’s SBC (Z)ICFU (Z)

Quadrant VIIITDFL (T)TVCF (T)World Bank (Z)EU/Mashonaland (Z)HPC (Z)

Quadrant XIGev’s Flowers (Z)Hortpack (Z)A&S Consultants (Z)IDIL (T)

High Value-AddedProcessing

Quadrant IIIHortico (Z)Flair (Z)

Quadrant VIEDESA (Z)

Quadrant IXZimTrade (Z)

Quadrant XII

Where: (M) Mozambique (T) Tanzania (Z) Zimbabwe

Firms are boldfaced; projects are in italics; associations are underlined. Classifications are based on the majority of

the entity’s focus.

7

3. Key Southern Africa Findings

This section presents the lessons learned and theimplications to enhancing the design and implementa-tion of USAID agribusiness development projects basedon research and analysis in all three Southern Africacountries. Where appropriate, the lessons learned arecategorized. All lessons learned discussed in this chap-ter are relevant to more than one case study and inmany instances more than one country. The implica-tions presented at the end of each section are based onthe lessons learned from the entire Southern Africastudy (i.e., not just those listed in this chapter).

Most of the lessons learned and implications arepresented as brief statements with minimal support orexplanation. More detailed information on the state-ments can be found in the profile of the case studyfrom which the lesson learned was drawn and in thechapter on the country where the entity is located.The entity or entities most relevant to each lessonlearned is shown in parentheses at the end of eachlesson learned. Table 2.1 can be used to identify thecountry for each entity and section X.1 of eachcountry chapter lists the full name of the entity. Referto the Appendix Table of Contents for the location ofthe entity’s profile.

The NTAE development and SME developmentAreas of Focus were of primary interests in the South-ern Africa portion of the Innovative Approaches activ-ity; therefore, these sections are the most developed inthis report. Association development and Financial Ser-vices development Areas of Focus are presented on asurvey basis. In all cases except NTAE development,agribusiness should precede the noted Area of Focus,(e.g., Agribusiness SME development).

3.1 NON-TRADITIONALAGRICULTURAL EXPORTDEVELOPMENT

Non-Traditional Agricultural Exports (NTAEs) arewell developed in Zimbabwe, but need to be redevel-

oped in Mozambique and are embryonic but growingrapidly in Tanzania. All three countries have substan-tial potential for NTAE development because theyhave a current or historical base of NTAE businessand because growing conditions are above averagefor SSA, although water availability problems need tobe resolved in Zimbabwe. There are no major en-abling environment problems that cannot be over-come, but significant transport system–related (air-ports, roads, and ports) constraints exist in all threecountries.

None of the countries have developed an orga-nized and integrated approach to NTAE develop-ment, even though agriculture represents a significantportion of GDP and employment, and additionalsources of foreign exchange and employment arebadly needed. The Horticultural Promotion Council inZimbabwe is currently being restructured to make itmore responsive to the interests of smaller partici-pants. Despite numerous private enterprise–basedefforts to involve indigenous small and medium enter-prises (Indigenous SMEs) in the production, packag-ing/processing, and marketing of NTAEs in Zimba-bwe, the business is still dominated by largecommercial (white) farmers and companies controlledby them. This situation must be resolved to achieveeconomic and political stability.

In Mozambique, rehabilitation of its once largecashew and coconut businesses is as important forits economy as is the development of shrimp aquac-ulture and value-added processing. Tanzania has sig-nificant potential for producing specialty NTAEs,especially in the Arusha/Moshi area.

Lessons Learned

Market Related

n More than 50 percent of the imported vegetablessold in the European Union (EU) are imported bywholesalers for resale to large supermarket chains.

n Successful participation in this large NTAE busi-

8

ness requires strict quality control, large-scaleoperations, and close linkages with the big EUimporters and retail packaging at the site of prod-uct origin.

n EU horticulture and floriculture markets will con-tinue to be well supplied; only those competitorswith high quality, high yields, a consistent supply,and low labor and transport costs will survive.(WB)

n Because transportation costs are a significant pro-portion of the total for NTAEs (30–40% of thelanded price), air freight, and to a lesser extent seafreight, costs must be very competitive. For airfreight, this is significantly dependent on passen-ger traffic volume. (WB)

Although the EU is a large market for NTAEs,there also are viable regional NTAE markets and othernon-African NTAE markets such as the Middle Eastand Singapore. (Favco)

Constraints Related

n Two major constraints to NTAE development arethe shortage of entrepreneur working capital andthe poor transportation system.

n Other important constraints to export develop-ment in general, and to NTAE specifically, arepoor performance (e.g., long delays) of the cus-toms service, inadequate and inconsistent en-forcement of tax laws, and excessive customsduties on inputs that are to be re-exported.

n For Indigenous SMEs, a shortage of high-qualityplanting materials and other input supply inad-equacies, as well as a very limited domestic mar-ket for off-specification production, constrain thedevelopment of NTAE businesses. (CTI/SIDA/WB)

Successful Indigenous SME export horticulturedevelopment requires the following:

n A large number of well organized producers in asmall geographic area with access to irrigation

n Cold storage units at collection points to removefield heat and store the produce

n Producer-owned transport/collection system

n Readily available qualified TA, primarily as relatedto quality control

n Access to a good communications system

n Focus on higher value products

n Shared production-related equipment such assprayers

n Access to a local fresh or processed market foroff-grade product and overproduction (Hortico)

Linkages Related

n When locals producers are risk averse and inex-perienced in NTAE production and marketing, thebest way for them to develop is via outgrower orsubcontractor relationships with large, experi-enced firms. (NEVEPA)

n There is considerable misunderstanding and dis-trust on the part of small producers concerningthe price that packers or exporters pay for pro-duce, especially as related to product grade-outand the appropriate price for the various terms ofsale (e.g., FOB factory versus field pick-up, CODversus consignment, and TA provided versus noTA). Price transparency is important to maintaina credible relationship between small producersand big exporters. (ZFU/Selby)

n Large agribusiness firms may find it easier toestablish their own production in developing coun-tries when technological advances enable inten-sive, commercial agriculture, rather than to de-velop and manage outgrower arrangements. (CdZ)

n Indigenous SMEs will be best able to participatein higher value NTAE business if they shareexpensive fixed assets and consolidate their out-put and marketing efforts. Chances for the finan-cial success of marketing projects involving small-scale producers would be improved if there werea joint packer/small farmer–owned center in agrowing area that was responsible for land prepa-ration, spraying, TA, output consolidation, coldstorage, and transport. (WB/Mashonaland/Hortico)

n Due to high interest costs, it is difficult to useextensive debt to finance new NTAE businessesthat are not fully integrated; that is, can capture

9

most of the margins available between the pro-ducer and the consumer. (ZimBank)

Project Development Related

n Innovative business propositions by entrepreneurswith an intimate knowledge of locally availableraw materials and a reasonable understanding ofinternational markets deserve further evaluation,especially when they can have a significant broad-based local impact. (Sun Flag/Sluis)

n A large up-front investment and significant ongo-ing operating costs are needed for a broad-basedexport promotion and information service.

n Because government funding is unreliable, a smallsurcharge on imports and exports is a good wayto fund an export development entity. (ZimTrade)

n Low literacy significantly increases the cost oftraining farmers and NTAE processing facilityemployees, making it difficult to operate and main-tain these facilities. (Lomaco)

Implications

Before providing support to an NTAE association,donors must determine how much export experienceassociation members have, their export opportunitiesand potential, the status of the export-related enablingenvironment, the extent to which association organiz-ers and leadership understand members’ priority needsand have viable programs to serve these needs, andthe quality of association management.

Because support to Indigenous SMEs for NTAEdevelopment requires considerable, diversified, andongoing “hands-on” assistance, an institution thatoffers the necessary integrated (finance, TA, andmanagement) services (e.g., a horticultural develop-ment center) is needed, especially one that has thesupport of the larger exporting firms.

When an NTAE development project is matureenough for project management to understand whichsubsectors have the best potential to support theirobjectives, managers should have the flexibility totarget some of their resources on these sectors.

Developing local counterparts through the effec-tive transfer of project/activity know-how from for-

eign advisors to locals is essential for projectsustainability and must be a key component of allprojects.

NTAE projects with Indigenous SMEs as theprimary beneficiary should include services that helpIndigenous SMEs join together to:

n Share expensive fixed assets.

n Purchase inputs jointly.

n Consolidate output, at least at the local level.

n Establish linkages with larger exporters to markettheir output.

n Negotiate subcontractor or outgrower relation-ships, especially for lower technology/higher la-bor requirement products.

This type of project also must ensure that whenlarge exporters are buying from small producers ortheir representatives (e.g., an SHG), or from SMEmiddlemen/wholesalers, all participants understandthe basis for establishing prices and terms. This mayrequire donor assistance for communication materialsand meetings to explain the basis for pricing and thedifferent terms, as well as to determine how pricesetting can be made transparent on an ongoing basis.

Projects should investigate, and where viable de-velop, the less difficult to serve regional and mediumsize (e.g., Singapore and the Middle East) exportmarket opportunities, especially for Indigenous SMEexporters. Also, local markets should be assessed fortheir potential as outlets for off-specification andexcess production so that at least some value isrecovered for all production.

Sources for working capital and reasonable costdebt should be made available to NTAE project benefi-ciaries, either by the project itself or from members ofthe project’s support network and/or cooperators. Fi-nancial services are especially important for IndigenousSMEs, and reasonable cost debt is very useful for non-integrated entities, since they are capturing a limitedamount of the total available margin on a product, andfor firms that are not directly exporting and therefore donot have access to debt at offshore rates.

Two very important enabling environment com-

10

ponents that NTAE projects should focus on are:

n Transportation, both domestic roads and ports/airports as well as freight rates, especially airfreight; helping the government stimulate tourist/passenger traffic, deregulate the air cargo busi-ness, and maintain low refueling and airport land-ing fees, which will stimulate air freight availabil-ity and help keep rates competitive.

n Optimization and proper enforcement of customsactivities, including quick clearance of outboundgoods and low/no duties on imported raw materialsthat are used to produce goods that are reexported.

Donor involvement in a major agribusiness exportpromotion project will require substantial funding, along-term commitment, and the development of alterna-tive sources of funding (e.g., a cess on imports and/orexports). The size of commitment needed means thatmultidonor support may be required. Support by donorsfrom countries that are the target market for some of theexports would be very helpful.

A donor-supported mechanism is needed to fi-nance, most likely on a matching grant basis (whichwould be recoverable if the project became success-ful), the assessment of broad-based benefit NTAEpropositions developed by successful local agribusi-ness entrepreneurs. A mechanism should also bedeveloped to tap the experience of the few successfulNTAE entrepreneurs in a given geographic area, andwith their help determine how to accelerate the rateof NTAE development in that area.

Rehabilitation of NTAE industries (e.g., the cashewand coconut industries in Mozambique) that were oncequite large will be very costly and require joint and well-coordinated efforts by donors, the government, privatesector participants, and producers.

3.2 INDIGENOUS SMALL ANDMEDIUM ENTERPRISEDEVELOPMENT

3.2.1 Overview

Reforms being undertaken by the governments of Zim-babwe, Mozambique, and Tanzania have been self-

absorbing to a large degree; that is, occupying all gov-ernment attention to the exclusion of most other activi-ties.

While governments are thus preoccupied, local fi-nancial institutions (originally government owned) are invarious stages of slow restructuring, due largely topressure from donors and the World Bank. These finan-cial institutions, especially the domestic banks, have littleor no liquidity and many, if not most, are technicallyinsolvent. If lending at all, they are almost certainly notlending to food and agribusiness Indigenous SMEs.While business lending centers are being established insome of the major urban centers in the three countriesvisited, there are only nascent plans to do the same atpopulation growth centers in rural areas.

Institutional lending to agriculture-related firms iscomplicated and constrained also by continuing shiftsin land ownership and tenure policies. Even in Zim-babwe, with its tradition of large (white) landhold-ings, the problem of furnishing credit to communallyowned land is still a problem (which the World Bankplans to address). Access to land, determination of itsvalue, and the livelihood that can be derived from it,are crucial issues that must be addressed in each ofthe three countries.

An unexpected finding from recent fieldwork isthat the preoccupation of national governments withdonor-mandated reforms has inadvertently createdgenuine opportunities for entrepreneurship. Concernsthat the regimes would have had with private enter-prise in former years now pale before the demands ofinternational donor groups. Consequently, private sec-tor initiatives are alive and well. Further, where do-nors have consulted with each other and with themore entrepreneurial elements of the business com-munity (particularly in Tanzania and Zimbabwe), theclimate is quite favorable for accelerating the start-upand development of Indigenous SMEs.

Certain constraints to Indigenous SME develop-ment, however, apply across the board:

1. There is no focus on integrated food and agribusi-ness Indigenous SME development per se.

2. The lack of knowledge of modern managementtechniques and the lack of integrated marketing,

11

financial, and technological services to attain spe-cific business objectives is a very large IndigenousSME development constraints.

3. The World Bank and many donors are required towork through government agencies or institutions,which in many cases (especially in Mozambiqueand Tanzania) such services are not effectivelyavailable.

Complete privatization could have one drawbackin that there will be a need for “government endorse-ment” or for donor funds to be channeled directlythrough a government vehicle. It is not clear howthese privatized and commercialized institutions willbe regarded by the World Bank and other agenciesthat traditionally work through governmental struc-tures.

In Mozambique, there is a government-owneddevelopment company (IDIL) that the World Bank,SIDA, and other EU donors are using as a vehicle toevaluate and recommend entrepreneurs for fundingvia state-owned and private commercial banks. How-ever, this approach is not working particularly wellfor two reasons. First, because neither the apex unitat the Bank of Mozambique, the state-owned banks,nor IDIL, are seriously screening projects and therehas been no serious effort to pursue nonperformingloans; and this results in default rates near 80 percenton WB-funded SME loans. Second, private bankslend only to customers they know well, which usu-ally does not include new or growing IndigenousSMEs.

As governments reduce their holdings in andcontrol of large parastatal agribusiness firms, theypay little attention to the entrepreneurial ventures thatneed to take the place of the parastatals. Wheredonors are sponsoring private sector initiatives, thereis very little, if any, direct participation by govern-ment-controlled entities. Therefore, as is pointed outin each country summary, there are many privatesector development approaches that can be pursuedindependently of the governments’ activities.

3.2.2 Findings2

Facilitating Integrated Indigenous SMEAgribusiness Development

For example, a review of past projects (Gordon andShaffer) indicated USAID has added business incu-bation projects to various programs, but these projectsare not far enough along for their results to beevaluated. It has been found that when a venturecapital approach to equity funding is taken, the resultshave been disappointing (Fox, J.W.), and this ap-proach has been especially true in developing coun-tries. The literature suggests several reasons for theinappropriateness of venture capital at the start up formost businesses, among which are:

1. The requirement that the entrepreneur give upboth management control and majority ownershipwhen the venture has high risk or less than spec-tacular payoff possibilities and entrepreneurs typi-cally are not willing to relinquish control.

2. Most enterprises in their early stages of develop-ment need tighter day-to-day oversight and finan-cial control than is provided by venture capitalmanagement or donor staff.

3. The funding required by an individual SME forstart-up or expansion is typically much lowerthan the amount of investment made in any onefirm by venture capital funds.

4. The approach of donor organizations can be quiteantithetical to the way venture capital managersanalyze enterprise potential. Often donor organi-zations, assuming that entrepreneurs are compe-tent and accountable, have exercised lax over-sight, with the result that by the time they learnthat an enterprise is in trouble, it is too late tointervene and help the enterprise back to health.Most enterprises in their early stages of develop-ment need tighter day-to-day oversight and finan-cial control than is provided by venture capitalmanagement or donor staff. This is particularlytrue with inexperienced entrepreneurs and in ar-eas where communication is difficult. Businessincubators/development centers can provide suchday-to-day oversight and control, while at the

12

same time providing technical assistance and train-ing.

5. The funding required by an individual SME forstart-up or expansion is typically much lowerthan the amount of investment made in any onefirm by venture capital funds. Further, venturecapital funds traditionally do not fund start-ups.Business incubators or development centers, how-ever, are well situated to provide small-scale fund-ing in the form of “seed capital” or “bootstraploans” to the SMEs they are assisting.

Fox’s findings certainly apply to private sectordevelopment projects in developing countries spon-sored by USAID and many other donors. Reasons forthis include the following:

1. Donors often do not exercise enough control oversponsored enterprises to ensure that they hireappropriate and qualified staff,

2. Career donor agency staff usually lack privatesector business experience and do not have theexpertise to evaluate the proposed enterprise’sstaff and business plan,

3. USAID has difficulty with a five-year horizon, letalone the up to ten years that enterprise funds andmany venture capital operations may require todemonstrate unequivocal “success.”

The secret of success for incubators/develop-ment centers is that they deal with these well-knownproblems head-on by employing the following guide-lines:

a. Where possible they obtain financial, legal, andother support services (often pro bono in theUnited States), pooling them in a common facilityor operation. This approach, in fact, is beingincorporated in the British-sponsored LAKEproject in Tanzania.

b. Enterprises are given a very short rein from initialfeasibility exploration until they reach profitabil-ity. They are held to objectively measurable, per-formance milestones expressed in terms of time,budgets, output, sales, and so on, which, if notachieved, can terminate any funding commit-ment. Thus, enterprises are judged strictly on a

business development or commercial basis be-cause that is the basis on which they will succeedor fail.

c . Because business incubators/development cen-ters are usually part of a broader local, regional,or national economic development plan, their long-term objectives are usually to achieve a break-even point (where revenues are equal to operatingcosts) within a five-year period. Their goal is tobecome self-sustaining through positive cash flowreceived from rents, royalties, licenses, a spreadon loans, and modest sales of small equity hold-ings in the supported ventures. This is in contrastto the traditional venture capital objective of real-izing an average 30-percent annual return on in-vestment from a portfolio of new enterprises.

d. Investors in business incubators/development cen-ters usually have broader objectives and are morepatient than venture capital investors. For ex-ample, the former are often benevolent donors(foundations, major banks, and local or nationalgovernments) interested in the overall, long-termeconomic development of an area, region, orcountry. Their support typically consist of grantsand seed capital funding. Other such investorsinclude companies (including venture capital firms)interested in observing a development center’soperations, usually with an eye toward contract-ing with or investing in promising individual en-terprises as appropriate; and government pensionfunds, whose investments may be carefully lim-ited to not more than 4-5 percent of total invest-able assets. Funds may make such investments inpart to stimulate local economic development andemployment.

e. Management of an incubator/development centeris vested in at least one senior experienced indi-vidual, with a distinguished business record, whomaintains day-to-day operational oversight of eachventure. This person is also responsible for analy-sis of entrepreneurial proposals and recommendsenterprises he thinks worthy of support to theboard or funding committee of their incubator/development center.

13

f. Entrepreneurs are notoriously independent andself-opinionated, rarely recognizing or acknowl-edging when they have failed to put together acredible management team or practicable busi-ness plan. The incubator/development center man-agement is expected to work step-wise with eachentrepreneur, helping them develop an investableplan, a balanced management team, and sustain-able operations.

All enterprises, whether starting up or expanding,require a “package” of business services that consistsof both long- and short-term debt, equity, and mana-gerial services tailored to fit that specific venture.Some effort should be expended to determine if theSouthern Africa Enterprise development Fund andthe several bureaus with access to USAID loan guar-antees could collaborate with Missions’ TA/manage-ment assistance programs and deal with Africanprojects from a common point of view. This wouldinvolve delivering these Indigenous SME businessdevelopment services in a highly integrated mannerand as appropriate for each individual venture. Ide-ally, a common staff directorate could be developedso that enterprise evaluation and funding could becoordinated through, if not actually integrated into,one decision making process.

3.2.3 General Observations

1. Indigenous SME development projects move fast-est when donors work together, pooling theirresources and agreeing on common procedures.Such donor coordination means that applicantsmust satisfy only one set of requirements (i.e., fillout only one set of forms). While all donor agen-cies must be accountable for their own resources,they must not encumber the enterprises theyassist with “home port” criteria. Whatever theindividual donor requirements, jointly fundedprojects must have one set of performance crite-ria that all donors agree to use.

2. Given the situation in the three countries, donorsshould also work together to enhance and facili-tate communications between the governmentand the private sector. In addition, a united posi-tion by the donors will be useful when donors

must protect their funded agencies or projectsfrom governmental inaction, interference, orthoughtless rule-making.

3.2.4 Other Indigenous SME DevelopmentFindings

Lessons Learned

Market Related

Domestic supply/demand balancing opportuni-ties should be thoroughly investigated, especially thepotential role of indigenous SMEs therein. (A&S)

Constraints Related

Entrepreneurs’ and managers’ lack of experienceand lack of management training are major con-straints in the early stages of private sector develop-ment, especially to SMEs. These constraints are usu-ally more significant than technical skill shortages andmake it very difficult for an entrepreneur to managea business in a way that enables repayment of financ-ing. (StanChart/TechnoServe/ZIMMAN/TBC)

Many donors view very limited equity availabilityand undercapitalization as the major constraint toSME development. However, inadequate infrastruc-ture (especially power, telephones, and roads), highduties on imports of processing inputs, lack of ac-cess to finance (to pay for needed imports), poorlocal business services and input supplies (especiallypackaging), and competition from imports that oftencome in without duties are also important constraintsto SME development. (LAKE/Sluis/World Bank)

Project Development Related

Microenterprises, SMEs, and even local govern-ment entities find it difficult to pay for the full cost ofbusiness advisory services, especially those wherethe provider is not able to leverage expensive staff.(TechnoServe)

Micro and SME development programs managedby indigenous people can succeed, even in verydifficult environments, if they are properly managedand if donor relations so that the programs are care-fully handled, are not perceived as a threat to thegovernment. (IDIL)

14

Implications

If SME entrepreneurs must work with several differ-ent institutions rather than with one institution toobtain their business support needs (e.g., financing,TA and managerial advice), the burden on them ismuch greater, paperwork much more complicated,and coordination problems (e.g., inconsistent require-ments) much more likely. Therefore, a fully inte-grated (financing, TA and management assistance)project is needed.

In environments where there are very few suc-cessful private sector enterprises to use as models,SME development programs that links new entrantsto the few successful enterprises will increase therate of SME development by creating more modelsand mentors. This would include subcontracting re-lationships and other very localized SME develop-ment activities sponsored by successful large privatesector firms. There is also a significant need toenhance the cost competitiveness enhancement, pos-sibly via training or mentoring by successful entre-preneurs. Without donor assistance, achieving sig-nificant tonnage sales via SME linkages/outgrowerschemes will be achieved.

Projects that effectively and successfully supportclients, especially SMEs, at a reasonable cost mayhave difficulty “graduating” these clients as theirbusiness services needs expand along with their com-panies and they face new challenges. Turning thesemore developed clients over to qualified local consult-ants would enable the project to expand its coverageand reach, (i.e., serve new, younger SME clients).However, the more developed the client, especially ifthey are exporting, the more sophisticated their con-sulting needs, and local consultants in these environ-ments are unaccustomed to providing pragmatic busi-ness services, especially regarding ongoing operations.Therefore, a donor can effectively leverage its re-sources in these circumstances by developing localbusiness consulting capacity. Local consultant train-ing should be an ongoing component of SME devel-opment projects.

An institution that helps entrepreneurs prepare afinancing proposal and then operate their businesses

in a manner that ensures financing repayment/in-creasing share values will make a significant contri-bution toward stimulating more new SMEs and thegrowth of existing enterprises. Therefore, there is astrong need for USAID to sponsor an activity to helpdevelop and package proposals and business plansfor entrepreneurs seeking financing. This coulitiesinterested in providing this service, possibly modeledafter USAID-supported training provided to AfricaDevelopment Bank (AfDB) new private sector devel-opment unit officers. Donor-provided special fundsto help SMEs apply for equity investment and todevelop local business services capacity represents apartially integrated approach to SME development.

For donor-supported projects where SMEs areto be the beneficiaries, it is likely that financing willhave to be provided at a preferential rate and that fundmanagement costs will have to be subsidized, be-cause serious “hands-on” management support of theinvestments, both pre- and post-financing, will beneeded.

There is a unique opportunity to help establishSMEs shortly after a change from socialism andparastatal-managed marketing to a private enterprisebased economy. However, “supported” training pro-grams are needed to help entrepreneurs develop theirmanagement and financial skills beyond the limitedscope of their former positions, especially in econo-mies emerging from parastatal control of agribusiness.

3.2.5 Conclusions

Lessons learned and implications of this initial re-search in the three countries are indicated in theindividual country chapters. The following are high-lighted as priorities that emerged from all three of thecountries:

1. Building on and/or Collaborating with Estab-lished Private Sector Development Entities

a. IDIL . USAID in Mozambique should be ableto persuade present donors to give IDIL re-sponsibility for both operational and fundingoversight, including equity investment of anagribusiness development center. Certainlythe Southern Africa Enterprise developmentFund (SAEDF) should explore using IDIL to

15

screen enterprises in which it is consideringinvesting.

b. The Venture Capital Funds in Tanzania andZimbabwe are tightly controlled by their boardsand donors. USAID and SAEDF should con-sider involvement with these operations andthereby gain additional experience in privatesector financial services facilitation. Otherpartners and facilities are available to workwithin support of SME development projectsin all three countries (e.g., the World Bank,which has a substantial private sector invest-ment fund needing near-term placement).

2. Facilitation of Large Processor Indigenous SMELinkage Projects. In Zimbabwe, two of the larg-est processing companies (Hortico and Selby’s)are actively working with small growers to de-velop new sources of higher value, non-tradi-tional food exports. Donor support could acceler-ate establishment of subcontractor arrangementsby both new landowners and communal produc-ers by providing extension personnel, cold stor-age, and trucks. In Mozambique, where the pri-vate sector is just reviving after the long war, theUSAID Mission has already provided funds to acashew processor, who in turn made available tosmall growers cashew trees to replace those dam-aged by the war or by a recent devastating hur-ricane. A large coconut grower and processorwould also like to develop, in collaboration withsmallholders and present plantation employees, awood harvesting and processing enterprise toreclaim land (cut down the old trees) for newplanting. There are likely to be more projects likethese in both countries. More specific investiga-tion should be undertaken and plans of actionformulated with the local Missions to capitalize onthese opportunities to enhance links between largefirms and Indigenous SME agribusinesses.

3. Lack of Entrepreneurial Orientation and “Knowl-edge of Business” Gap. One theme that recursthroughout this report regarding constraints isthat conversion of each economic sector to onefocused on markets and private enterprises can-not be ordered from above. This attitude change