Embed Size (px)

Citation preview

15588/1561/6201176v1

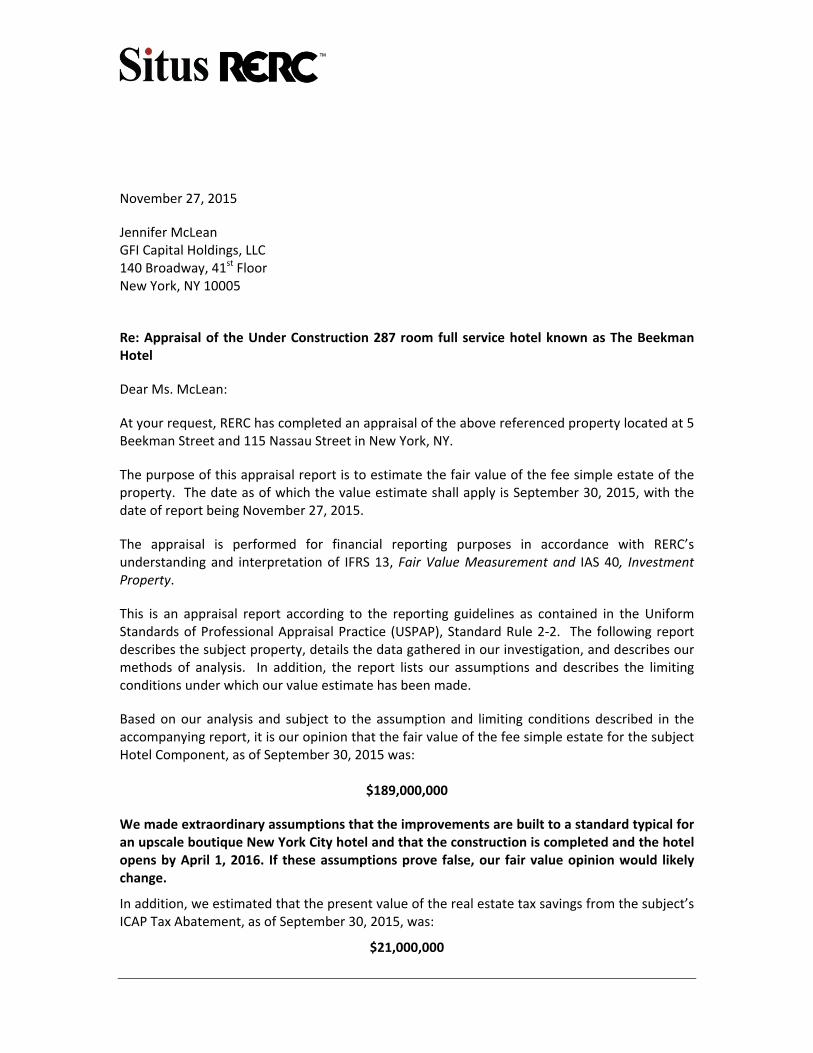

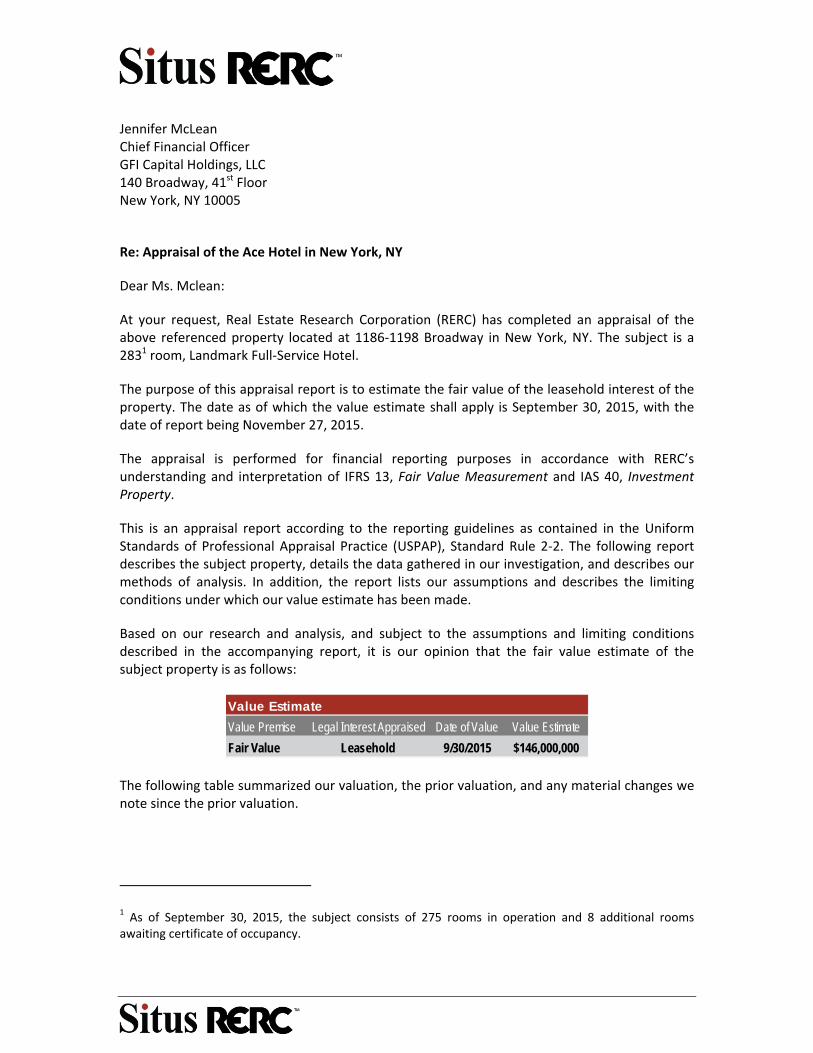

November 27, 2015 GFI Real Estate Limited 140 Broadway, 41st Floor New York, NY 10005 USA

Re: Fair Value Appraisals – Consent to include within Financial Statements

Dear Sirs, We hereby give our full consent to GFI Real Estate Limited (the "Company") to the inclusion of our Appraisal Reports dated November 17, 2015, November 27, 2015, and November 27, 2015 (Effective date – September 30, 2015) regarding Harbour Club at 49000 Denton Road, Belleville, MI, Ace Hotel at 1186-1198 Broadway, New York, NY, and The Beekman Hotel at 5 Beekman and 115 Nassau Streets, New York, NY in their entirety, within the Company's Financial Statements for September 30, 2015, to be published by the Company no later than November 30, 2015, and any ensuing financial statements, and within any other filing to be filed and/or disclosed by the Company to the Israel Securities Authority and/or to be published by the Company. In addition, we hereby give our full consent to the inclusion of a copy of this letter within the Company's Financial Statements and other filings as aforesaid. Yours faithfully, __________ Kenneth P. Riggs, Jr. President

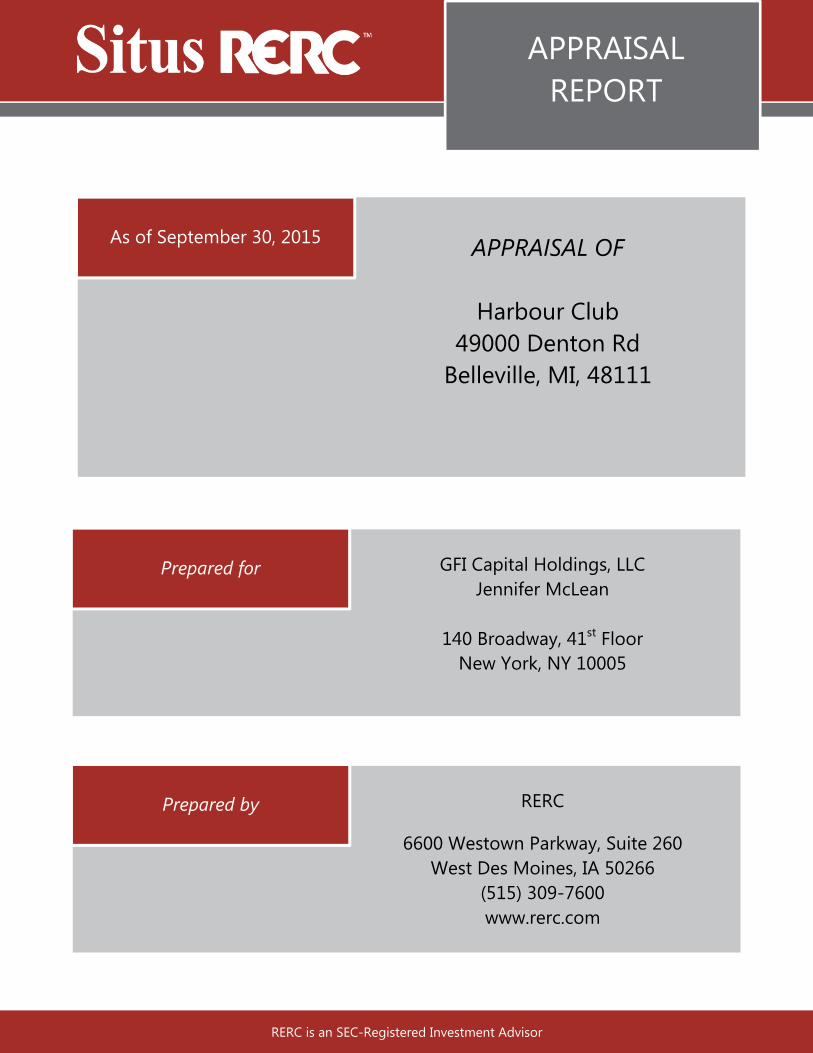

APPRAISAL OF

Harbour Club 49000 Denton Rd

Belleville, MI, 48111

As of September 30, 2015

GFI Capital Holdings, LLC Jennifer McLean

140 Broadway, 41st Floor

New York, NY 10005

Prepared for

RERC

6600 Westown Parkway, Suite 260 West Des Moines, IA 50266

(515) 309-7600 www.rerc.com

Prepared by

APPRAISAL REPORT

RERC is an SEC-Registered Investment Advisor

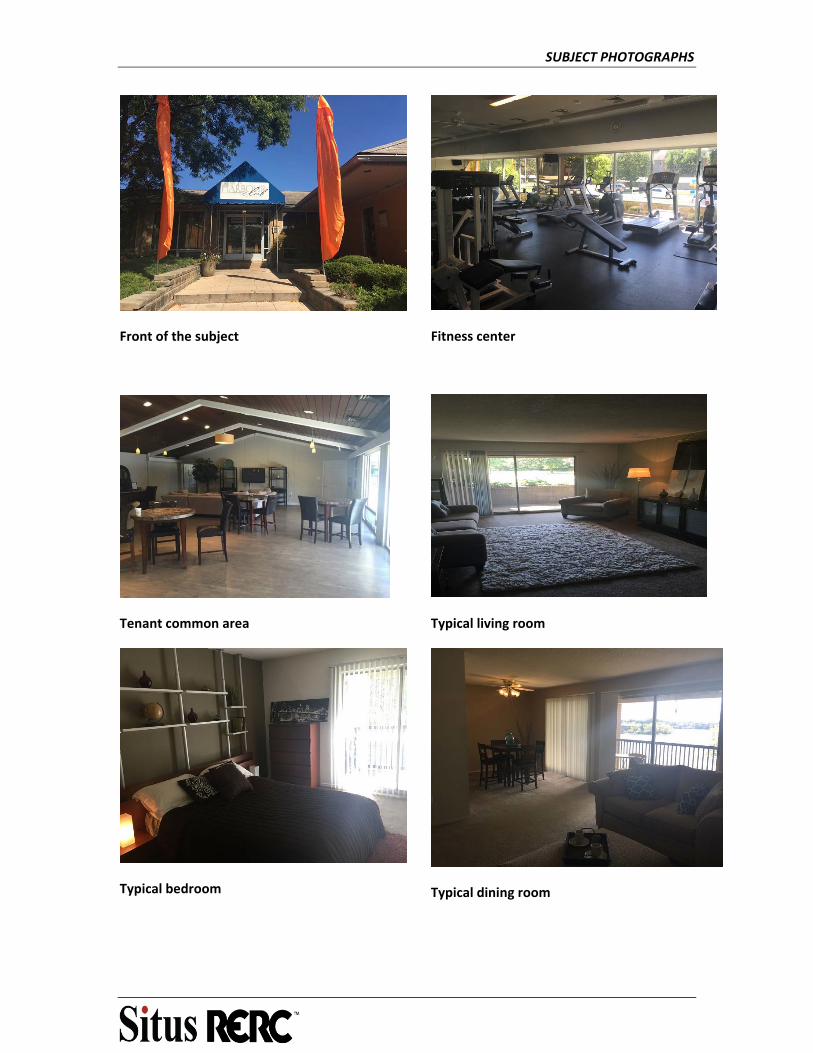

SUBJECT PHOTO Clubhouse Entrance

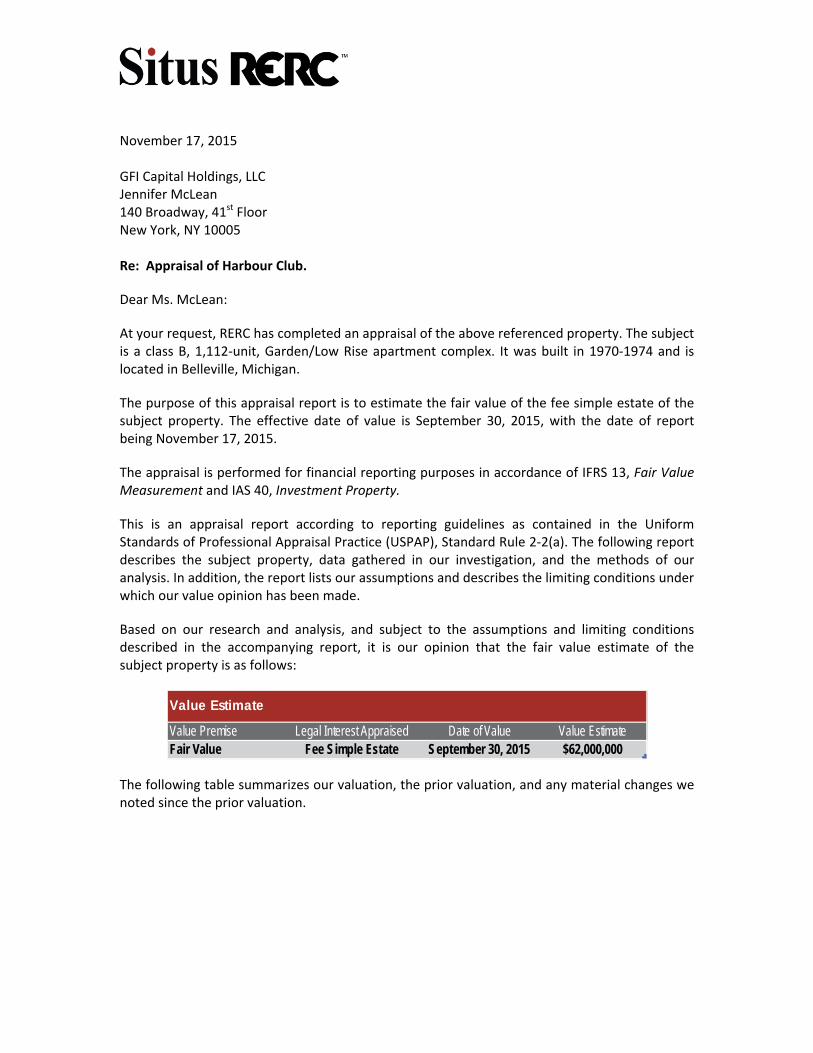

November 17, 2015 GFI Capital Holdings, LLC Jennifer McLean 140 Broadway, 41st Floor New York, NY 10005 Re: Appraisal of Harbour Club.

Dear Ms. McLean:

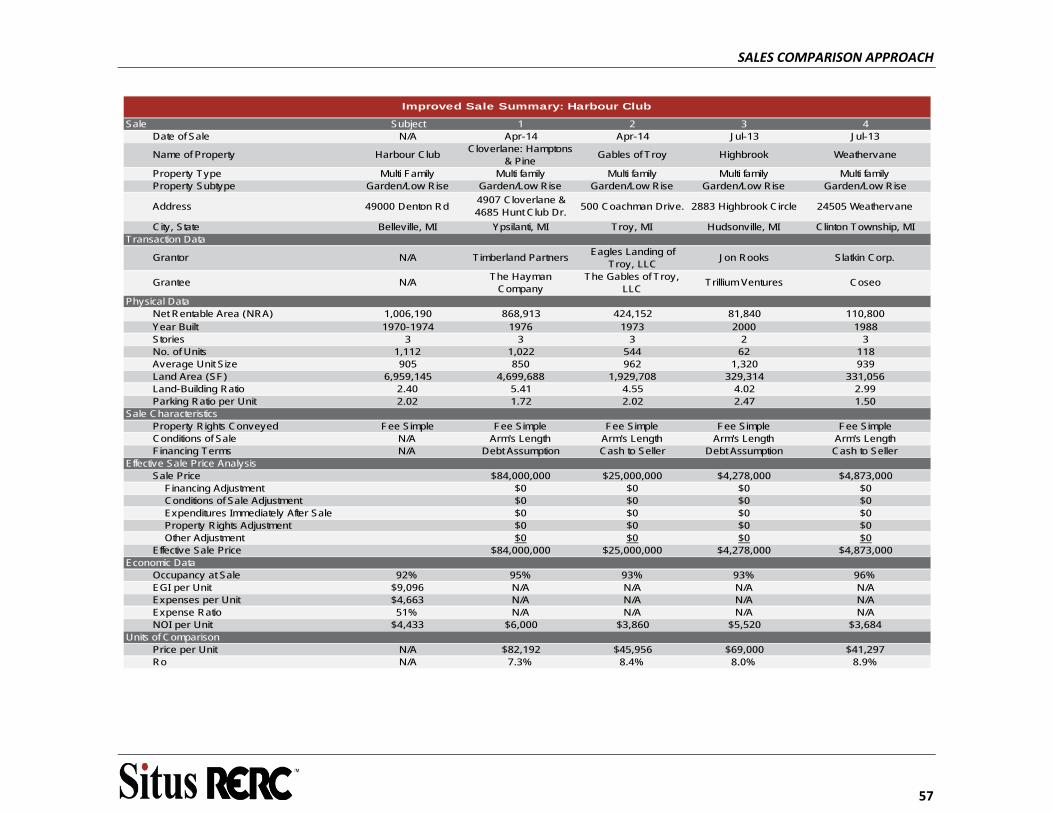

At your request, RERC has completed an appraisal of the above referenced property. The subject is a class B, 1,112‐unit, Garden/Low Rise apartment complex. It was built in 1970‐1974 and is located in Belleville, Michigan.

The purpose of this appraisal report is to estimate the fair value of the fee simple estate of the subject property. The effective date of value is September 30, 2015, with the date of report being November 17, 2015.

The appraisal is performed for financial reporting purposes in accordance of IFRS 13, Fair Value Measurement and IAS 40, Investment Property.

This is an appraisal report according to reporting guidelines as contained in the Uniform Standards of Professional Appraisal Practice (USPAP), Standard Rule 2‐2(a). The following report describes the subject property, data gathered in our investigation, and the methods of our analysis. In addition, the report lists our assumptions and describes the limiting conditions under which our value opinion has been made.

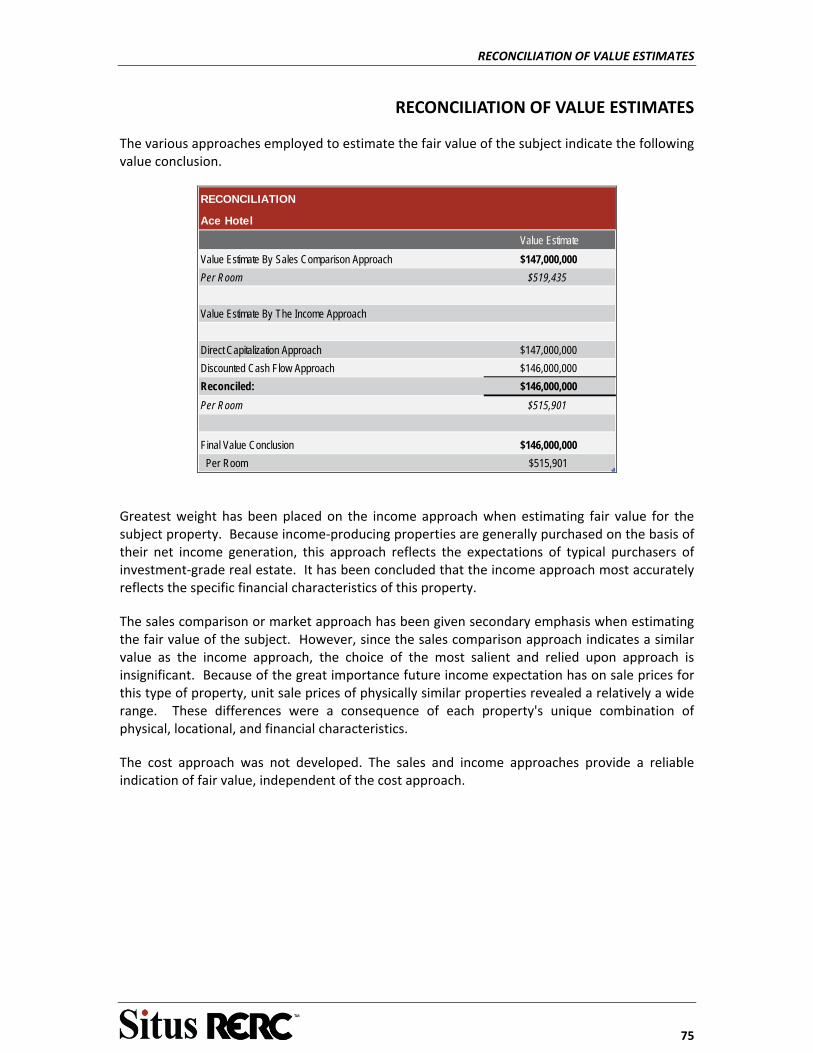

Based on our research and analysis, and subject to the assumptions and limiting conditions described in the accompanying report, it is our opinion that the fair value estimate of the subject property is as follows:

Value Premise Legal Interest Appraised Date of Value Value EstimateFair Value Fee Simple Estate September 30, 2015 $62,000,000

Value Estimate

The following table summarizes our valuation, the prior valuation, and any material changes we noted since the prior valuation.

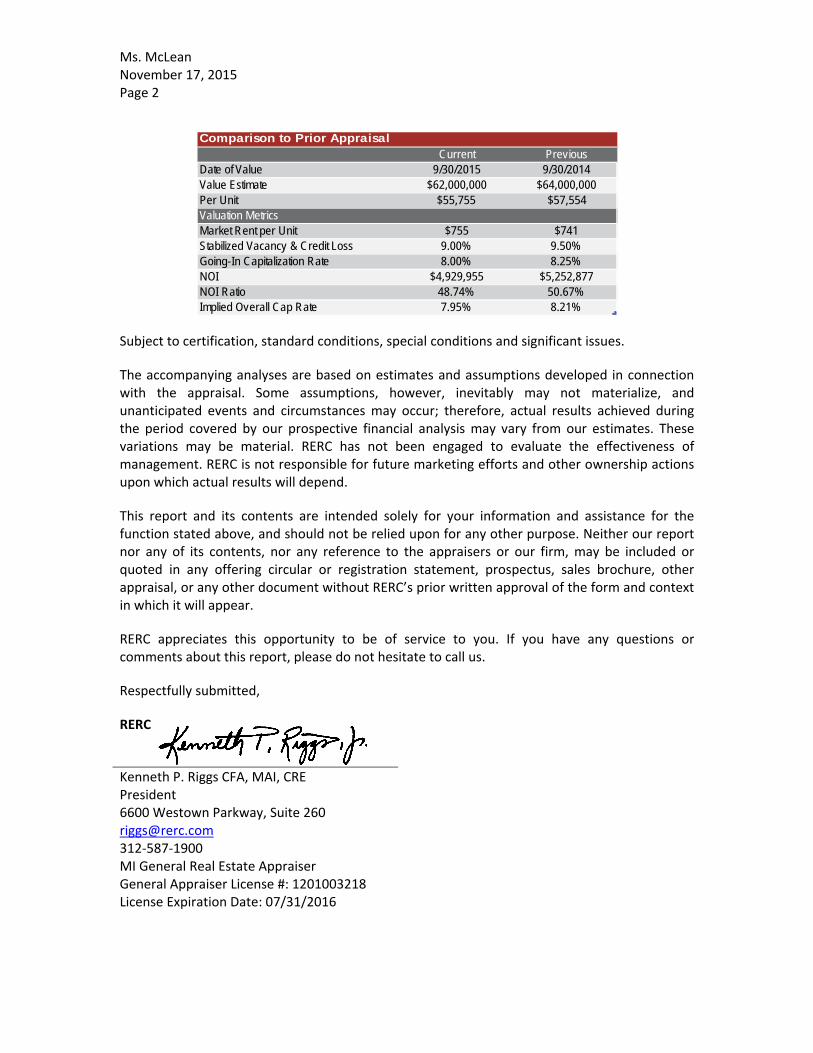

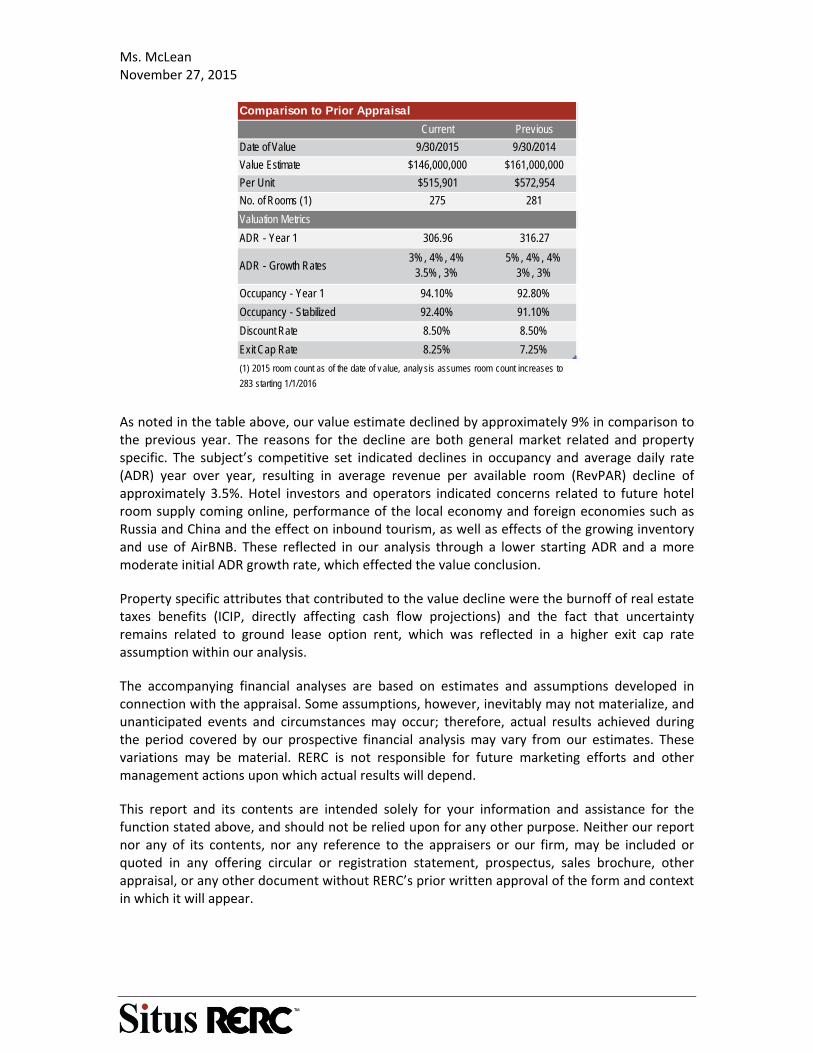

Ms. McLean November 17, 2015 Page 2

Current PreviousDate of Value 9/30/2015 9/30/2014Value Estimate $62,000,000 $64,000,000Per Unit $55,755 $57,554Valuation MetricsMarket Rent per Unit $755 $741Stabilized Vacancy & Credit Loss 9.00% 9.50%Going-In Capitalization Rate 8.00% 8.25%NOI $4,929,955 $5,252,877NOI Ratio 48.74% 50.67%Implied Overall Cap Rate 7.95% 8.21%

Comparison to Prior Appraisal

Subject to certification, standard conditions, special conditions and significant issues.

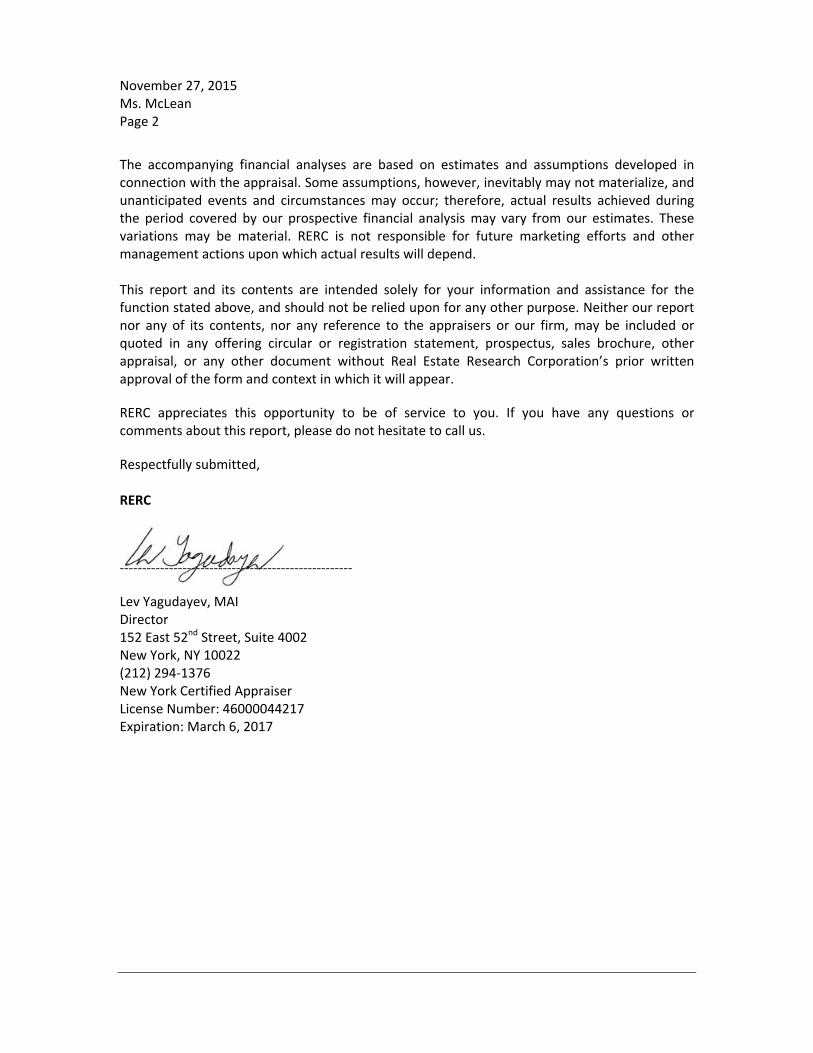

The accompanying analyses are based on estimates and assumptions developed in connection with the appraisal. Some assumptions, however, inevitably may not materialize, and unanticipated events and circumstances may occur; therefore, actual results achieved during the period covered by our prospective financial analysis may vary from our estimates. These variations may be material. RERC has not been engaged to evaluate the effectiveness of management. RERC is not responsible for future marketing efforts and other ownership actions upon which actual results will depend.

This report and its contents are intended solely for your information and assistance for the function stated above, and should not be relied upon for any other purpose. Neither our report nor any of its contents, nor any reference to the appraisers or our firm, may be included or quoted in any offering circular or registration statement, prospectus, sales brochure, other appraisal, or any other document without RERC’s prior written approval of the form and context in which it will appear.

RERC appreciates this opportunity to be of service to you. If you have any questions or comments about this report, please do not hesitate to call us.

Respectfully submitted,

RERC

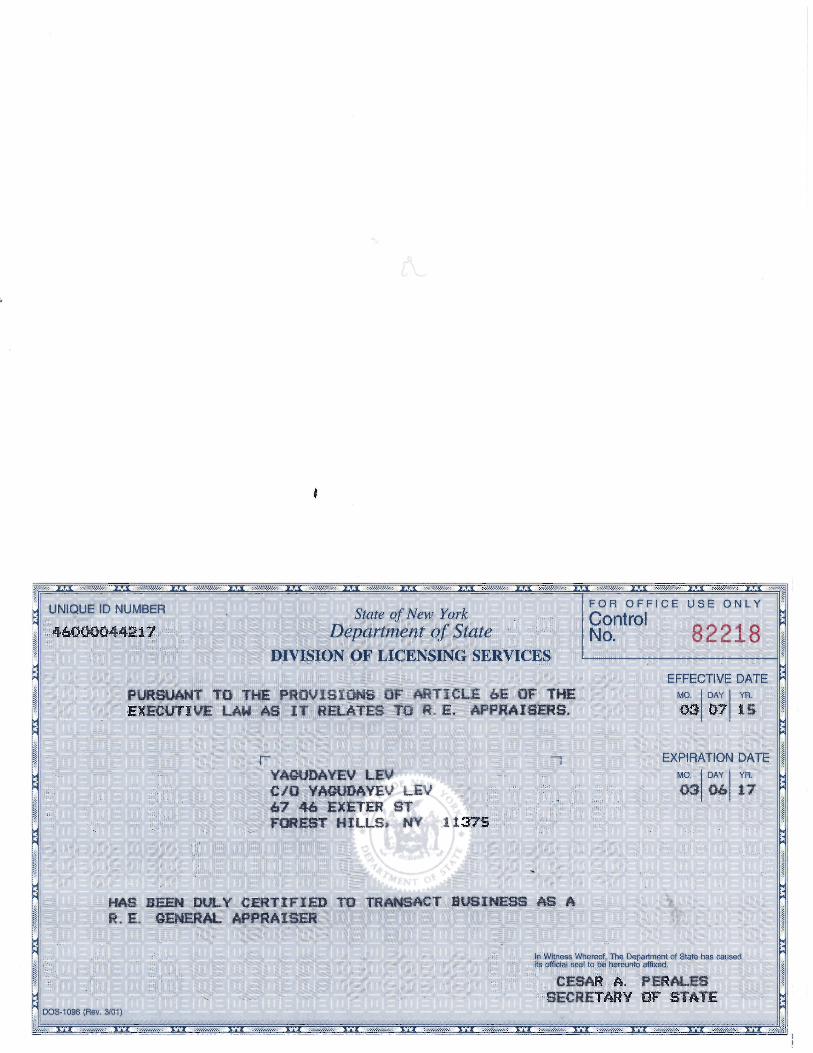

Kenneth P. Riggs CFA, MAI, CRE President 6600 Westown Parkway, Suite 260 [email protected] 312‐587‐1900 MI General Real Estate Appraiser General Appraiser License #: 1201003218 License Expiration Date: 07/31/2016

TABLE OF CONTENTS

TABLE OF CONTENTS

EXECUTIVE SUMMARY ...................................................................................................................... 6

INTRODUCTION ................................................................................................................................ 8

THE REGION .................................................................................................................................... 14

THE NEIGHBORHOOD ..................................................................................................................... 21

THE PROPERTY ................................................................................................................................ 25

REAL ESTATE TAXES ........................................................................................................................ 33

NATIONAL APARTMENT MARKET ANALYSIS .................................................................................. 35

APARTMENT MARKET ANALYSIS .................................................................................................... 44

HIGHEST AND BEST USE ................................................................................................................. 51

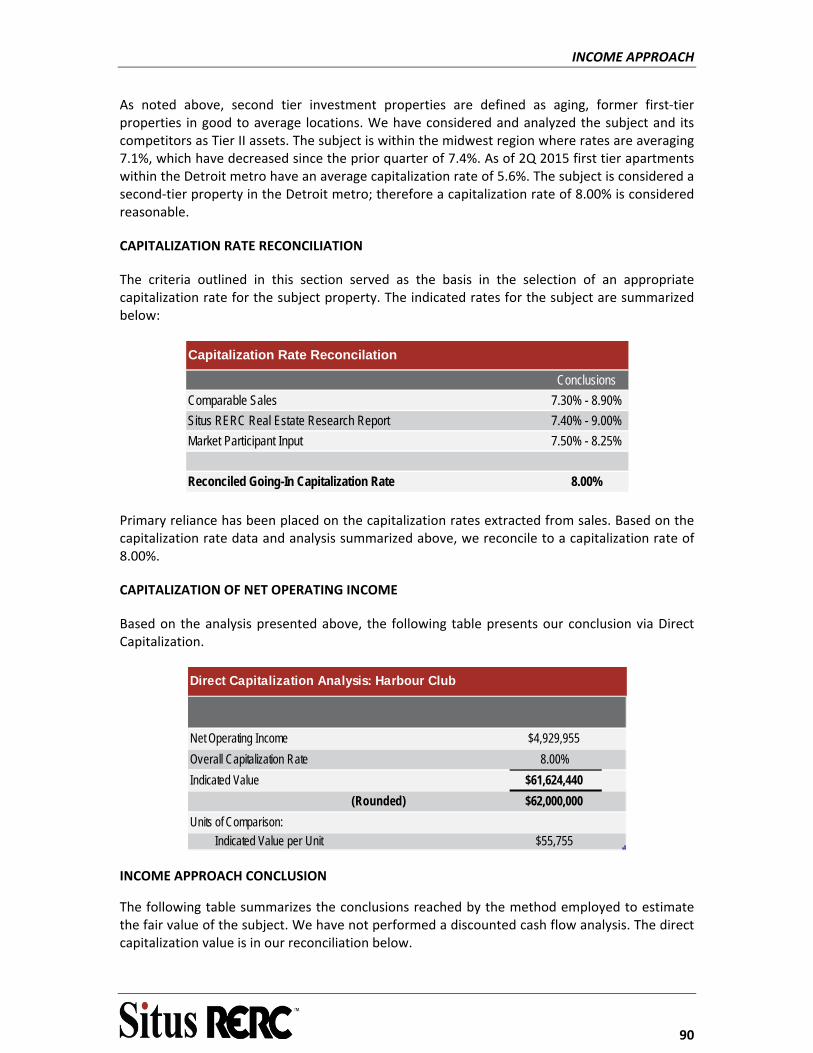

VALUATION METHODOLOGY ......................................................................................................... 54

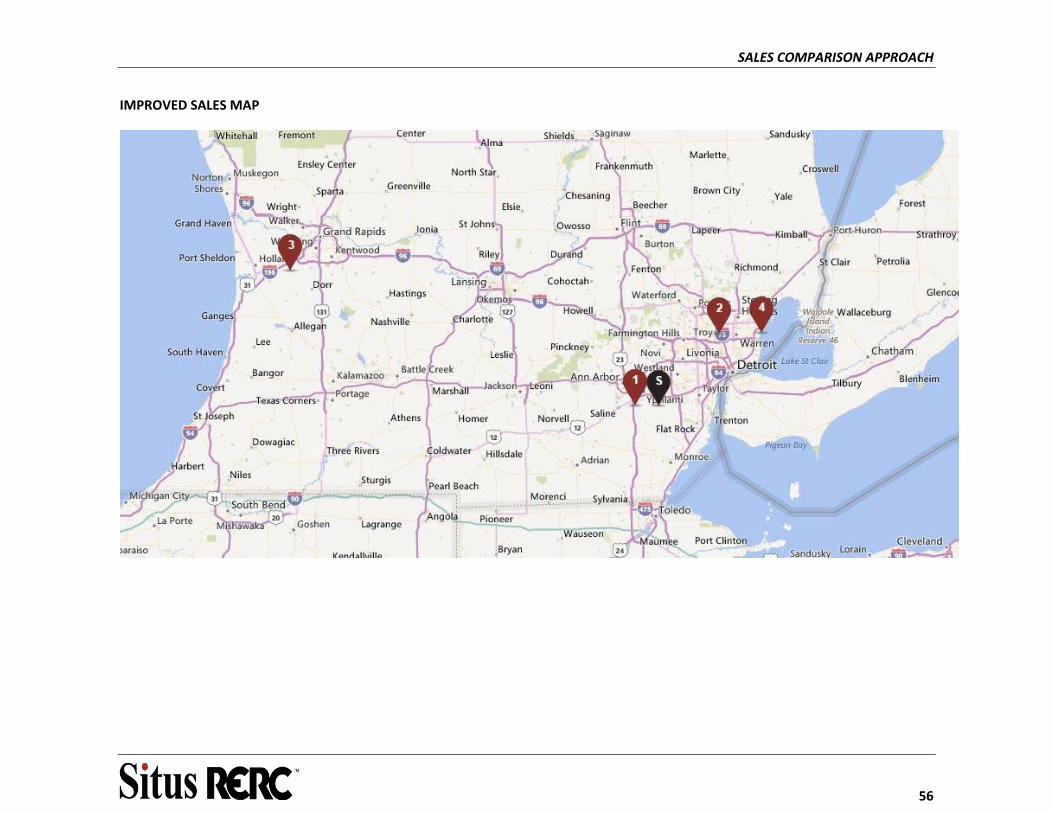

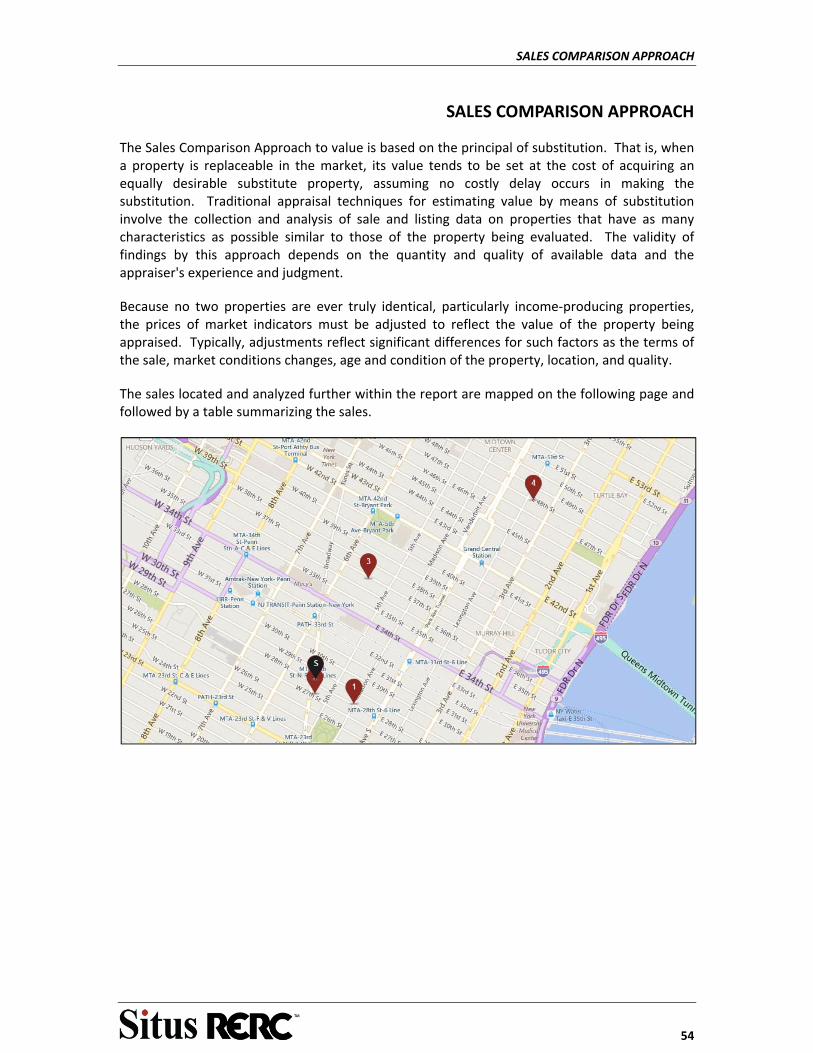

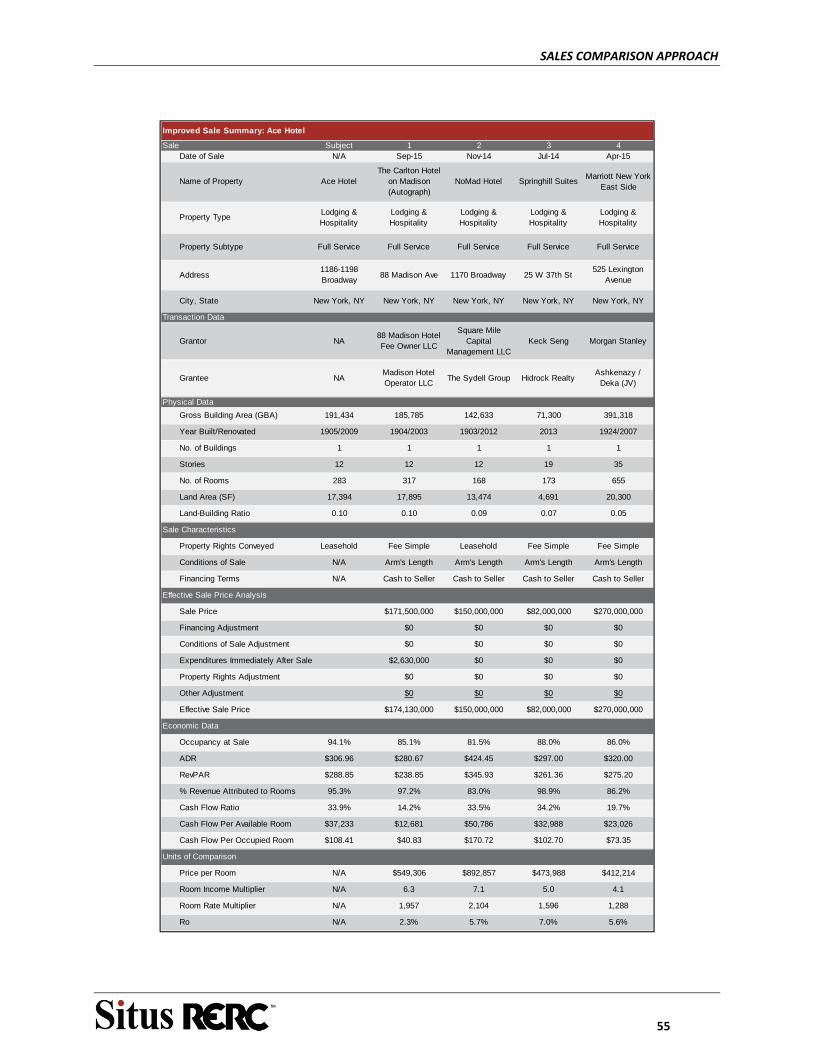

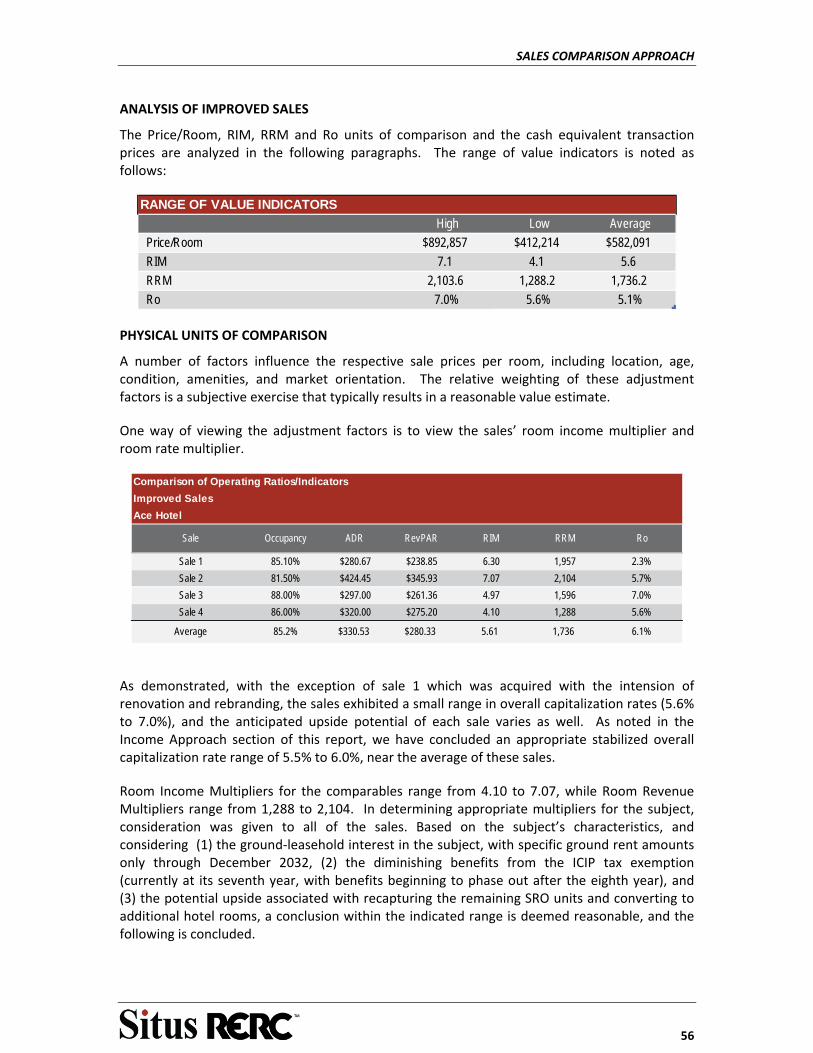

SALES COMPARISON APPROACH .................................................................................................... 55

INCOME APPROACH ....................................................................................................................... 65

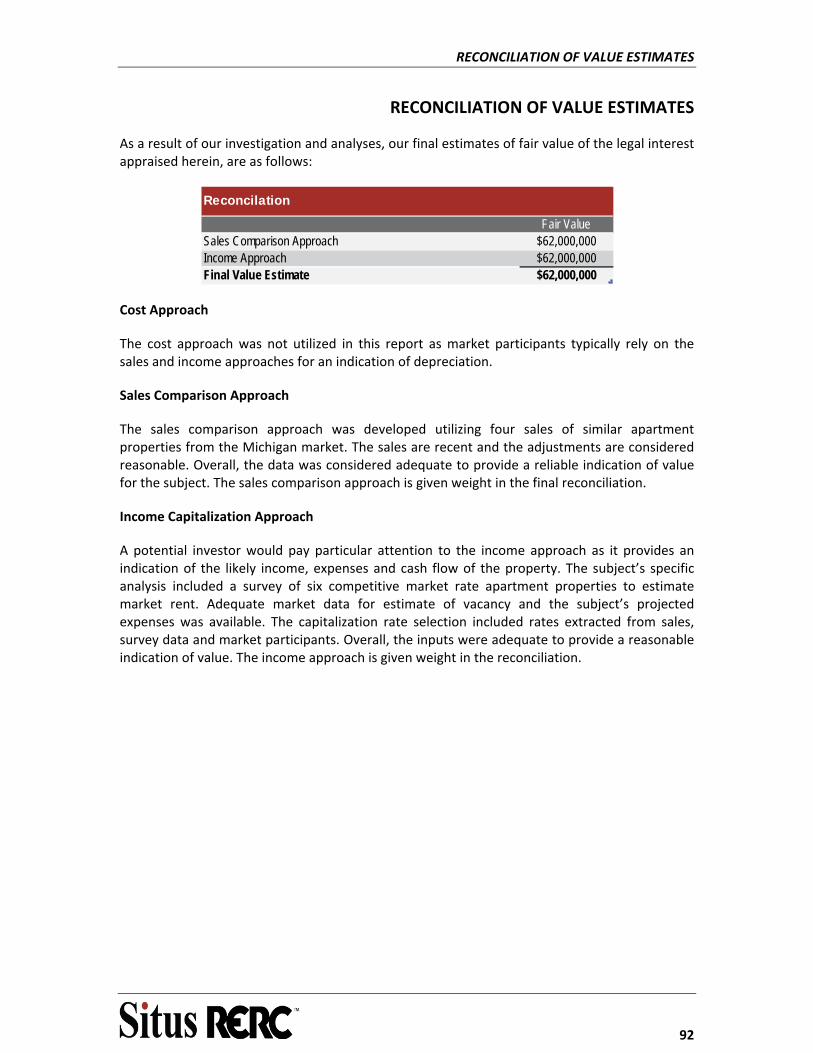

RECONCILIATION OF VALUE ESTIMATES ........................................................................................ 92

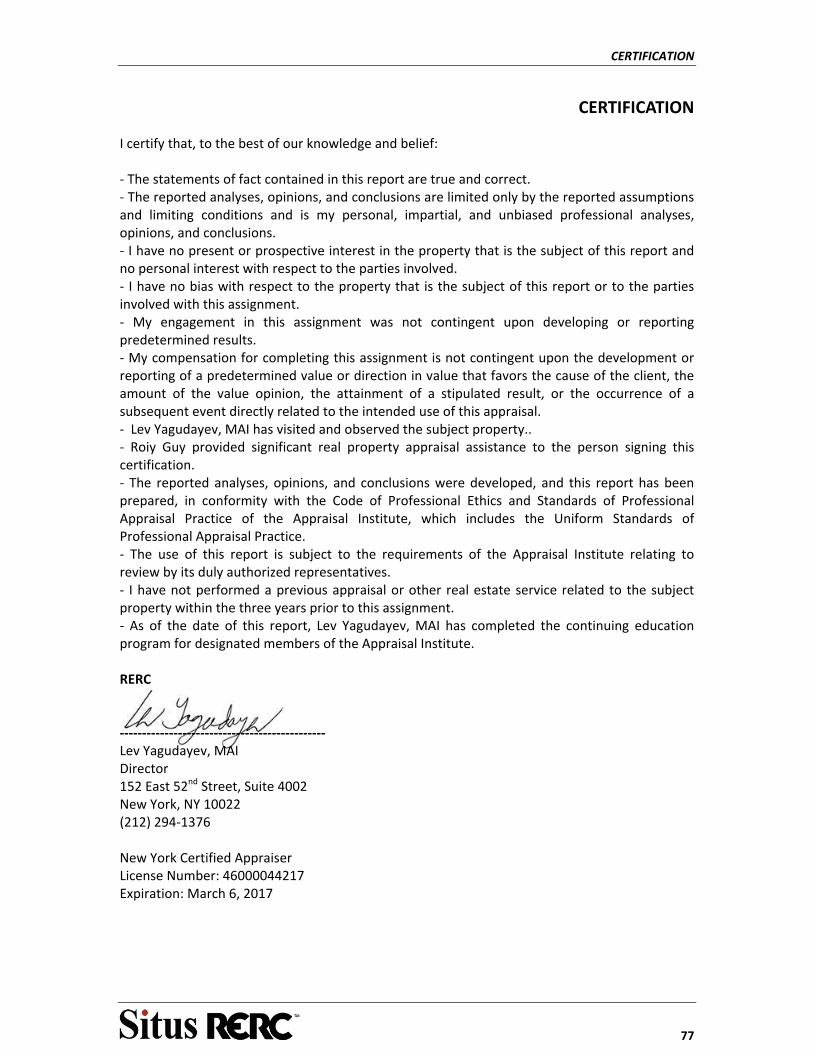

CERTIFICATION ............................................................................................................................... 94

ASSUMPTIONS AND LIMITING CONDITIONS .................................................................................. 95

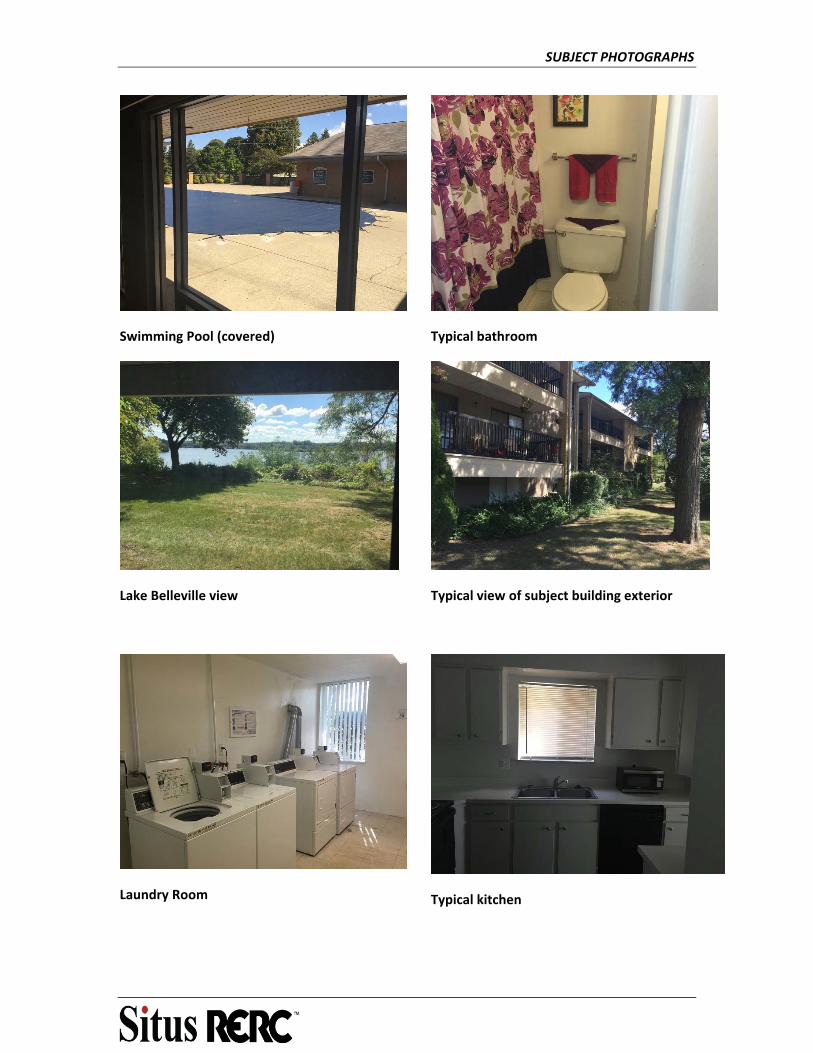

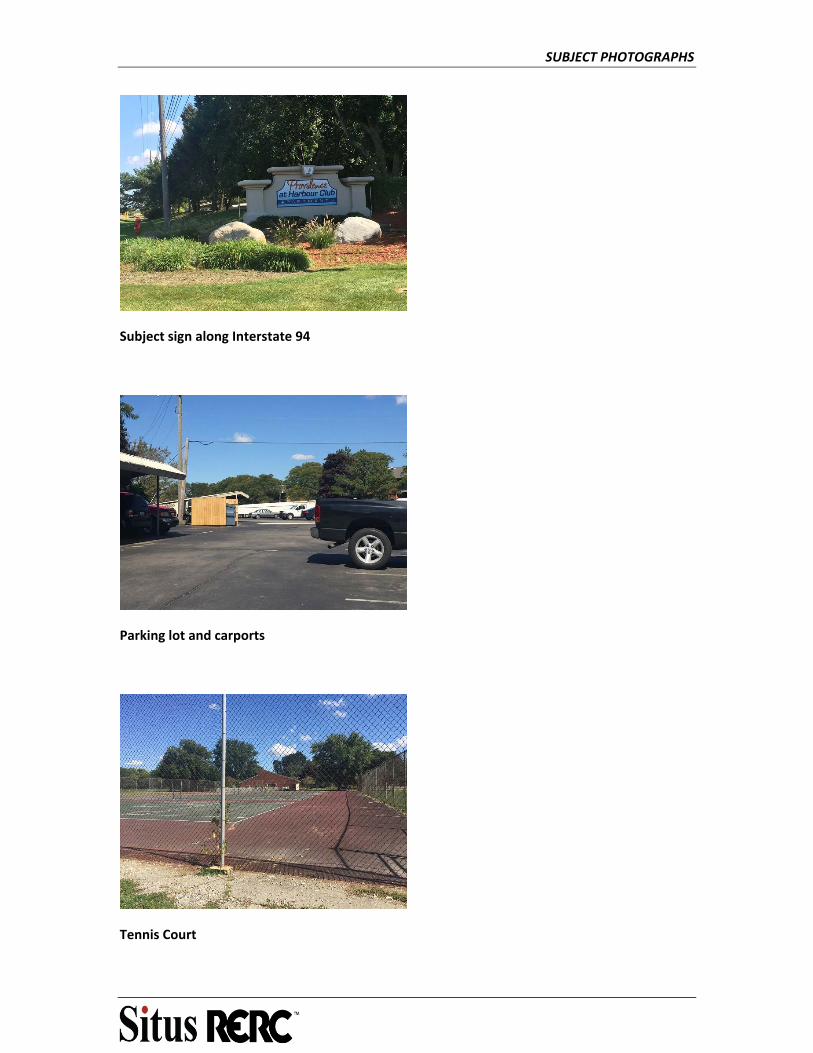

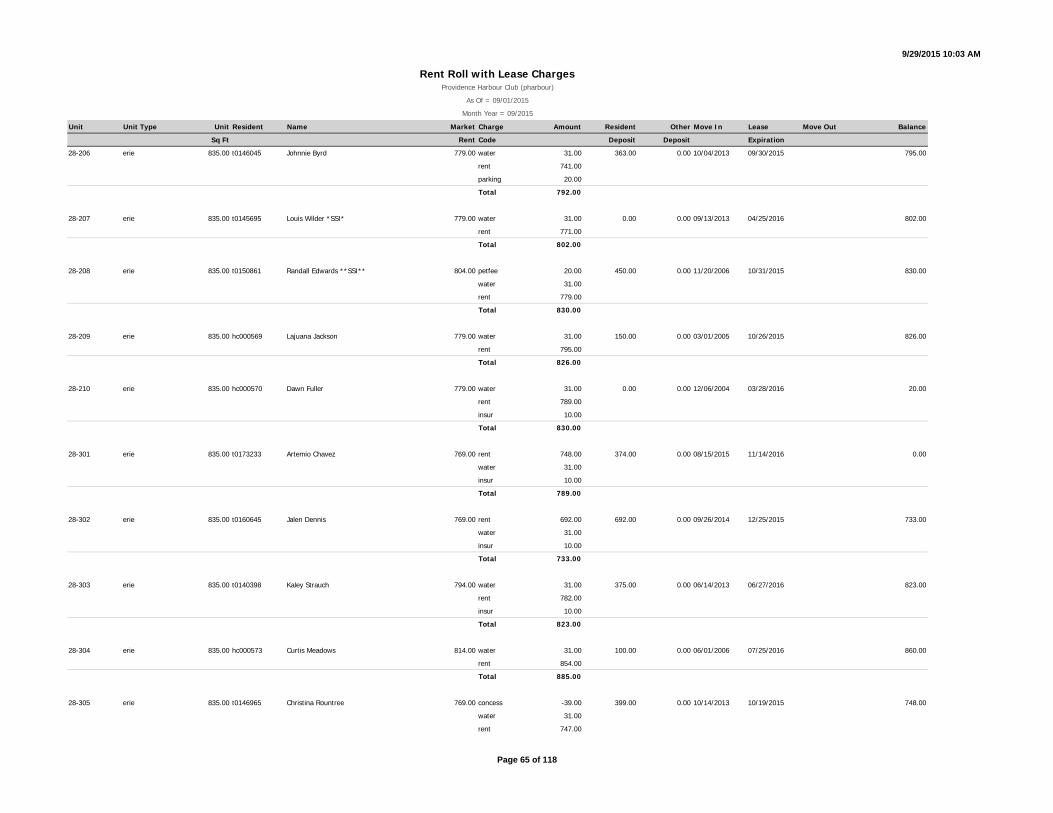

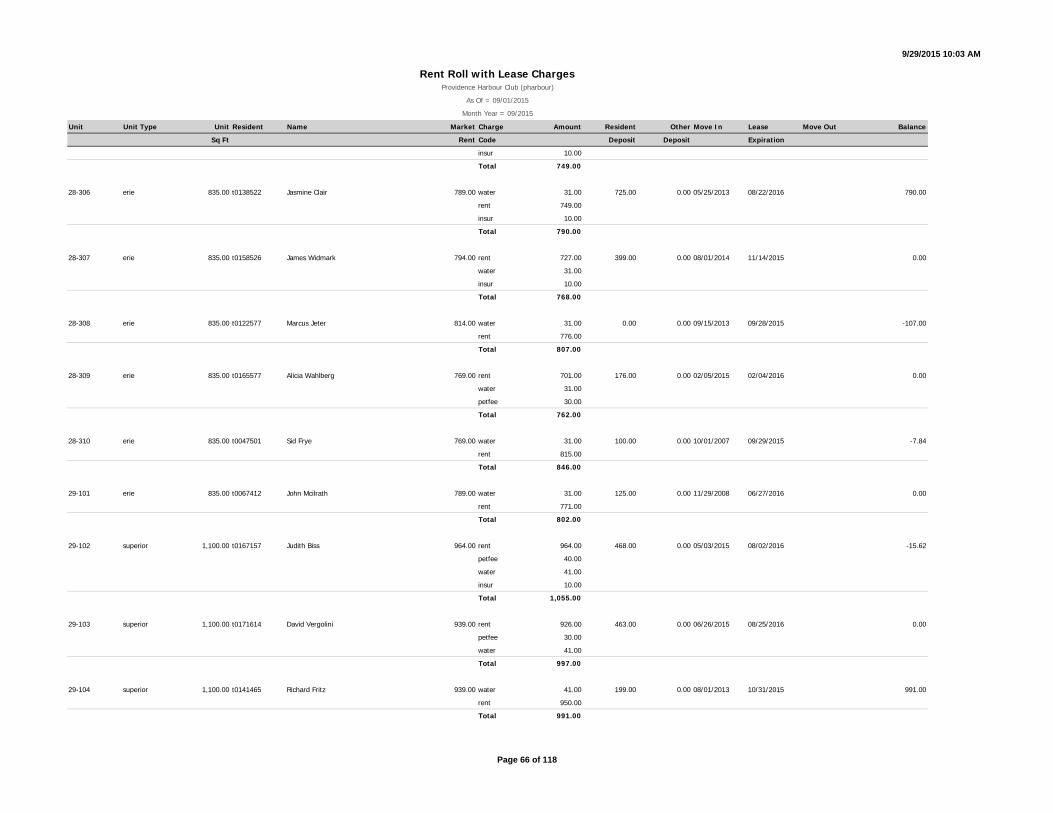

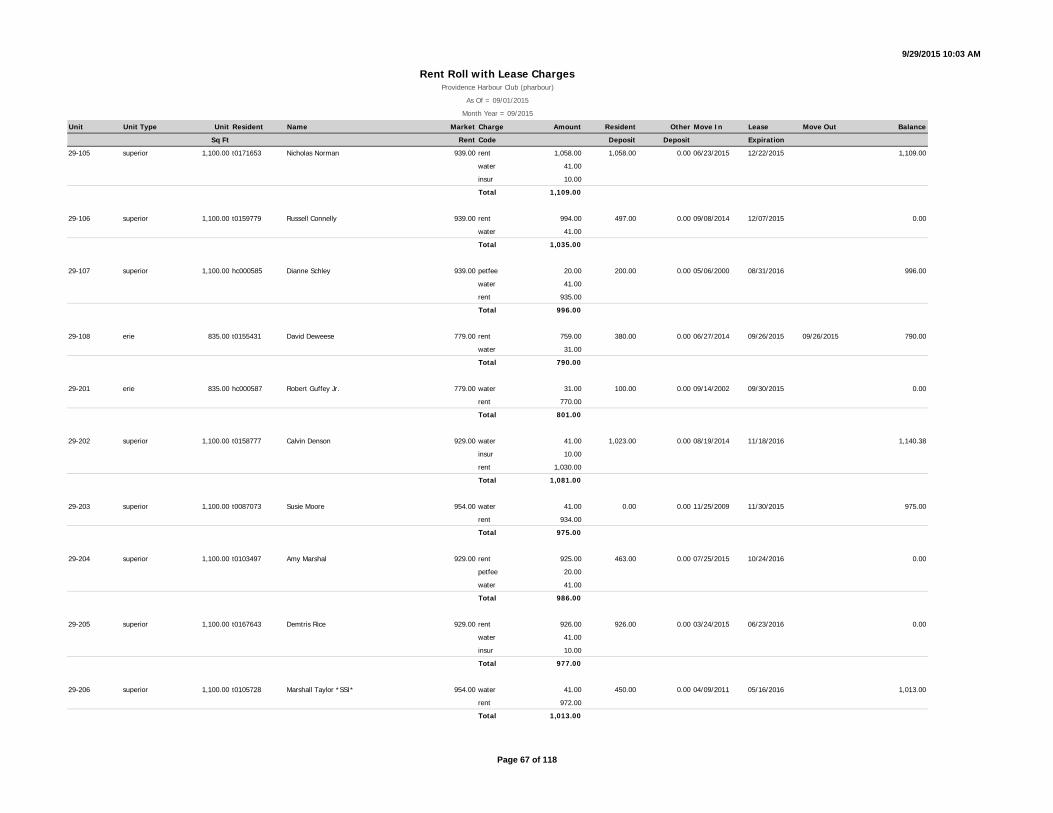

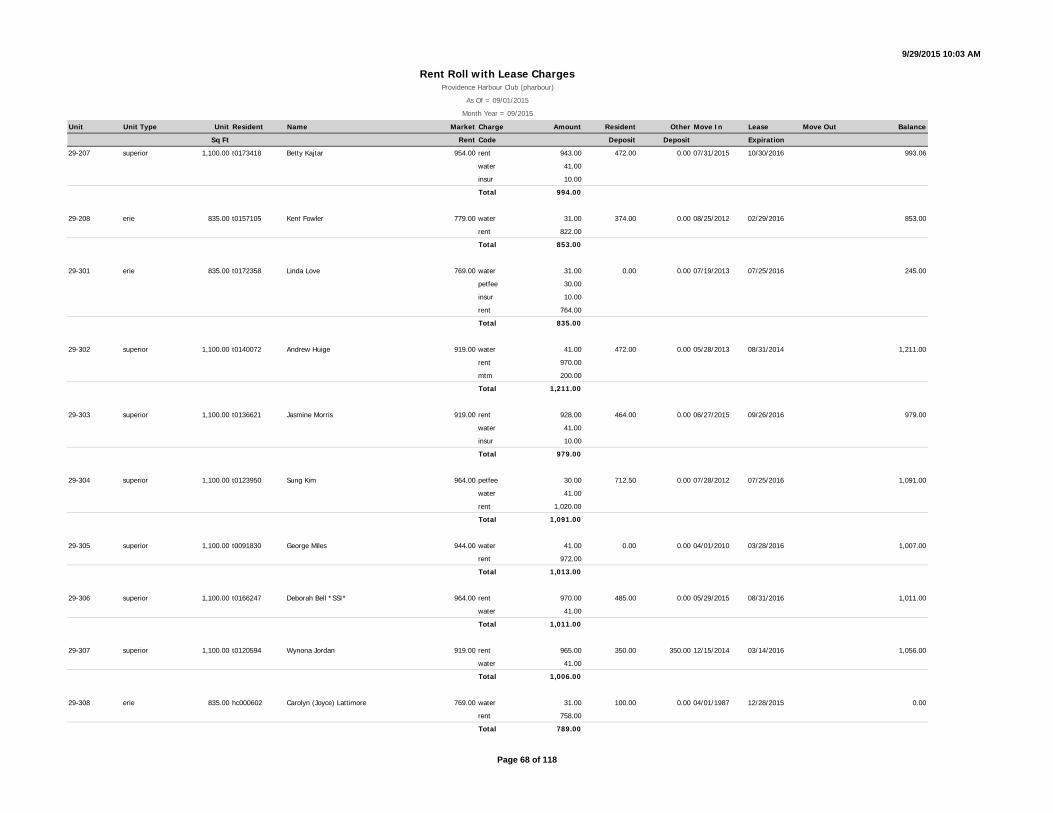

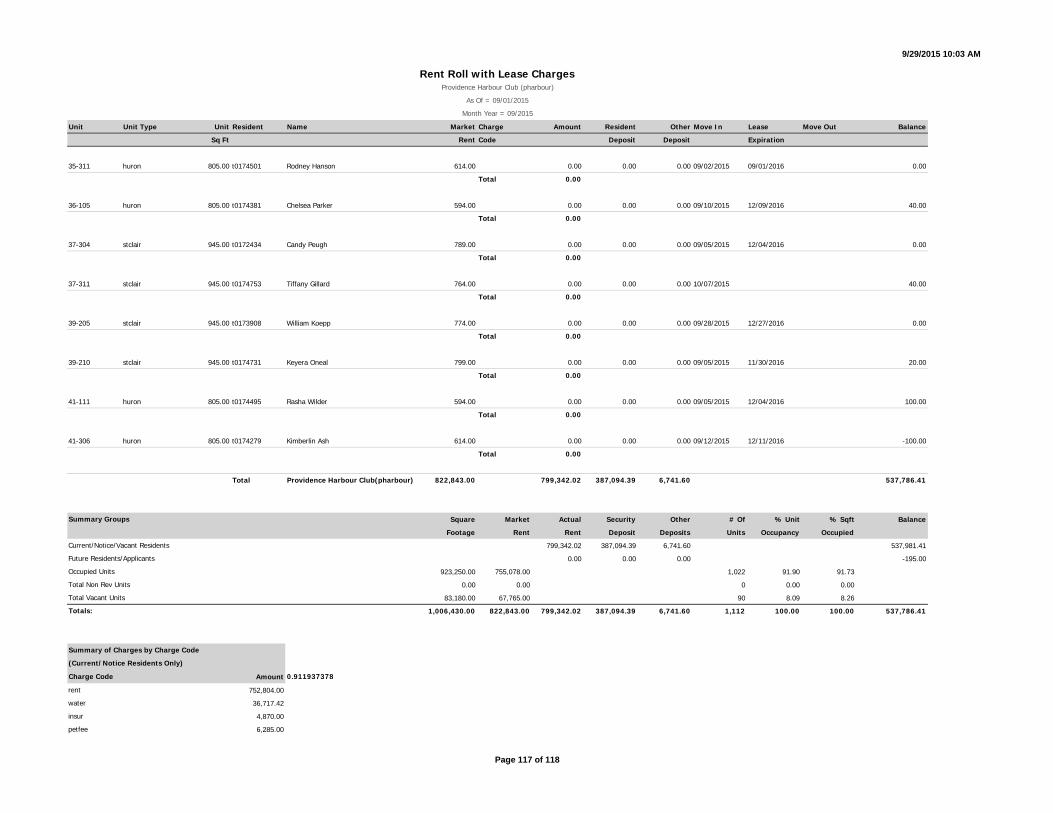

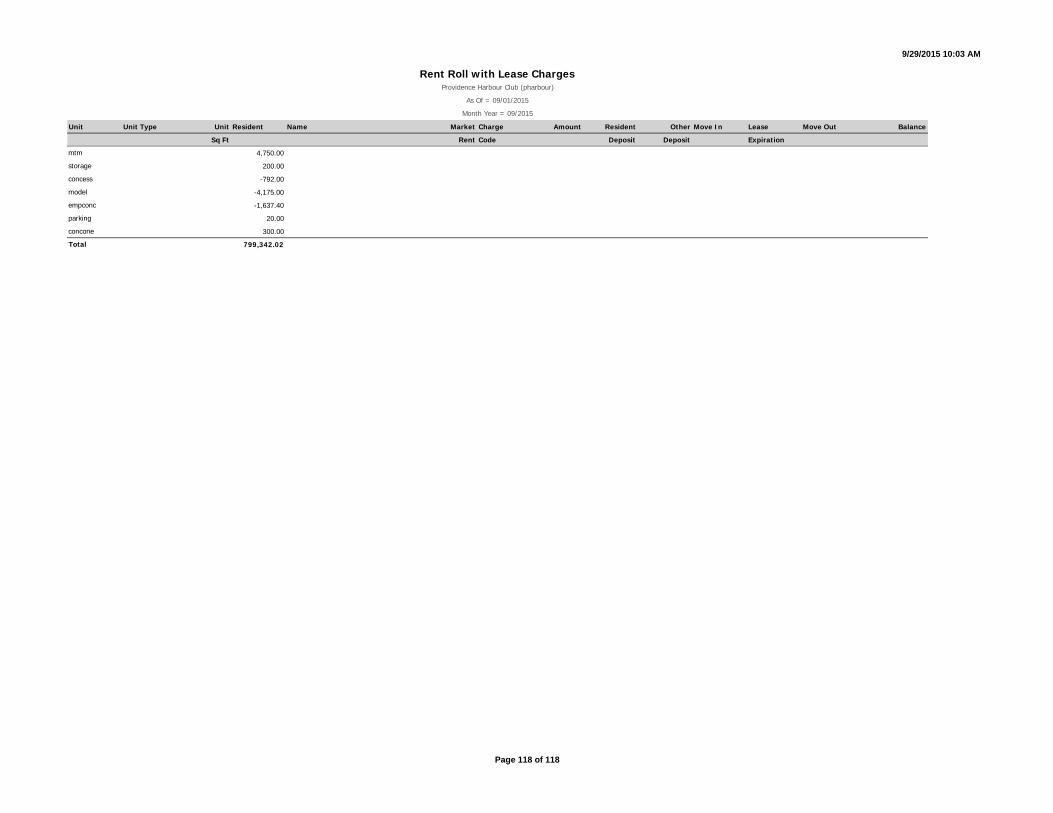

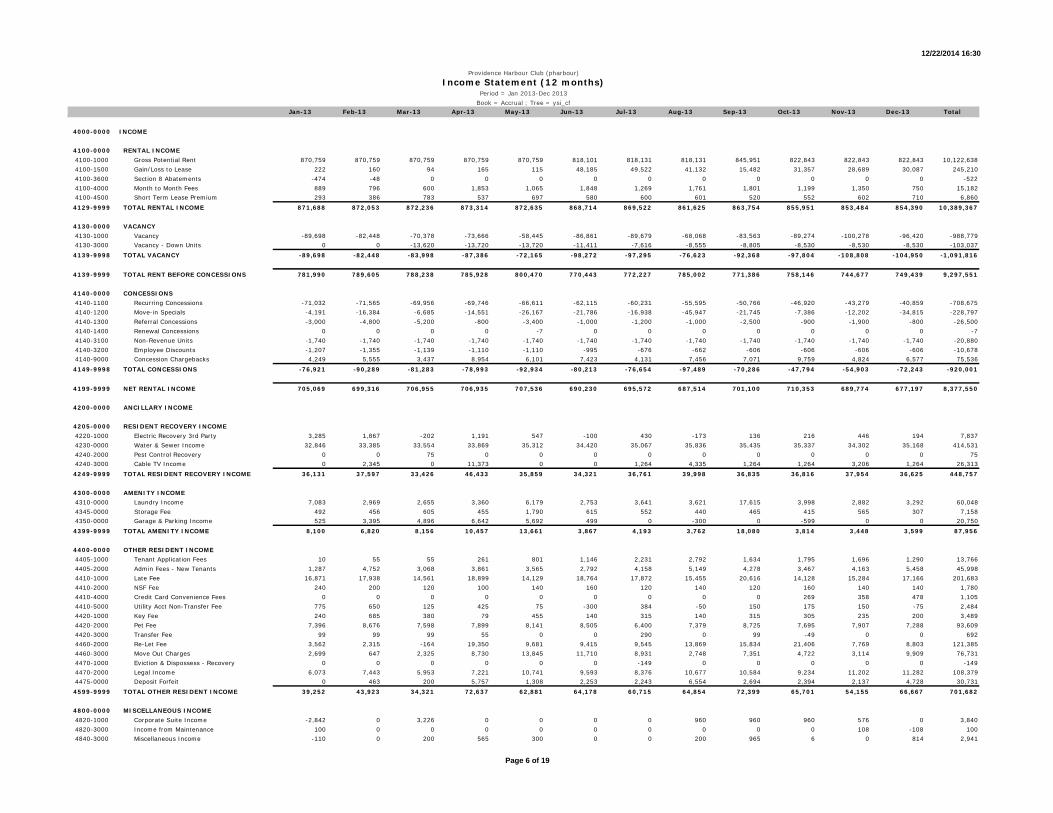

ADDENDA Subject Photographs Improved Sales Rent Roll Operating Statements Qualifications Licenses

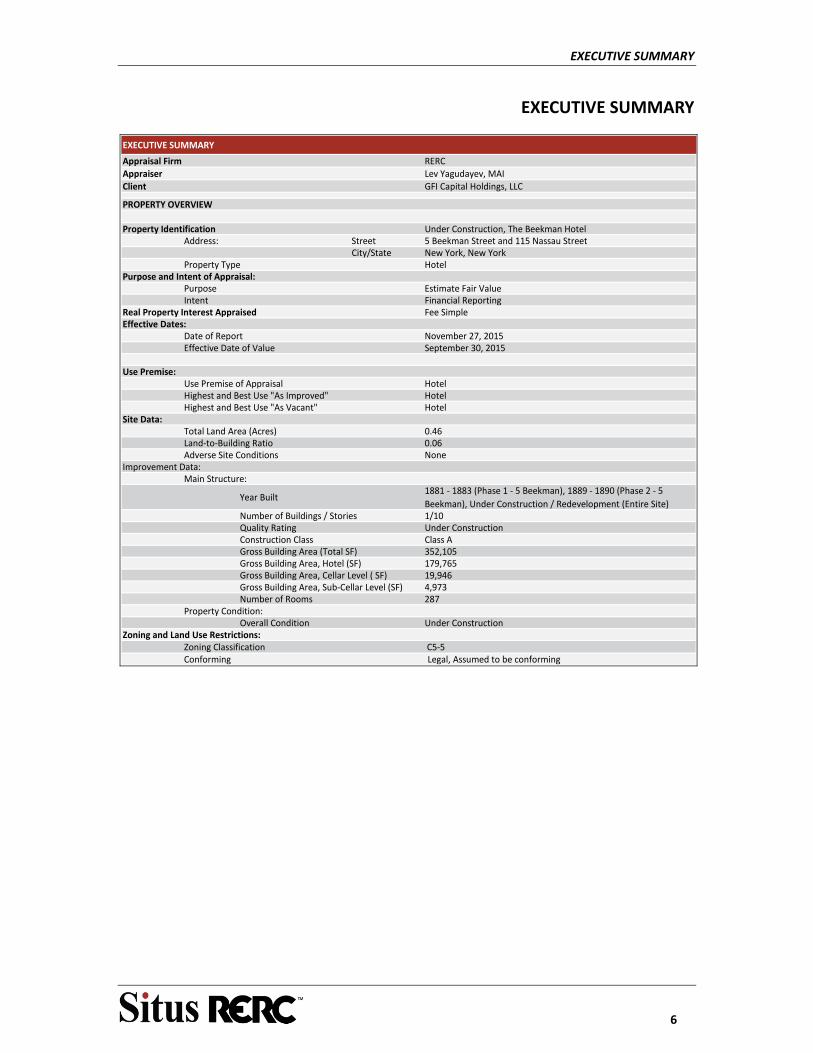

EXECUTIVE SUMMARY

6

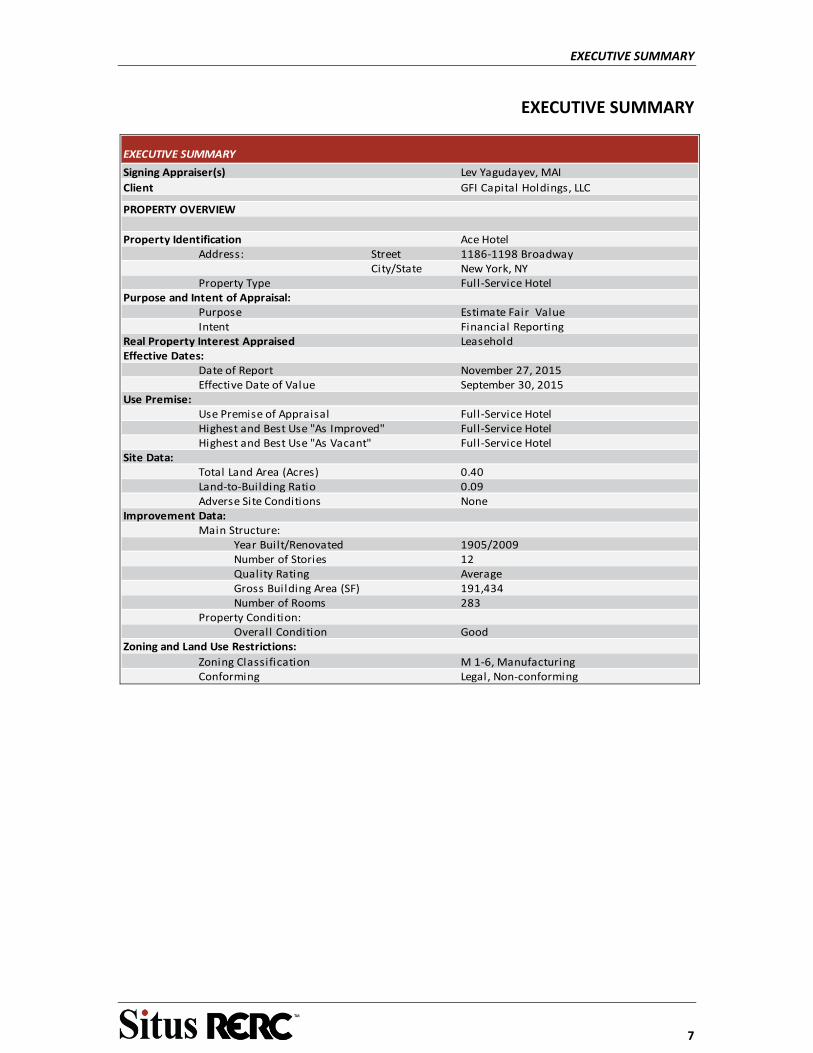

EXECUTIVE SUMMARY

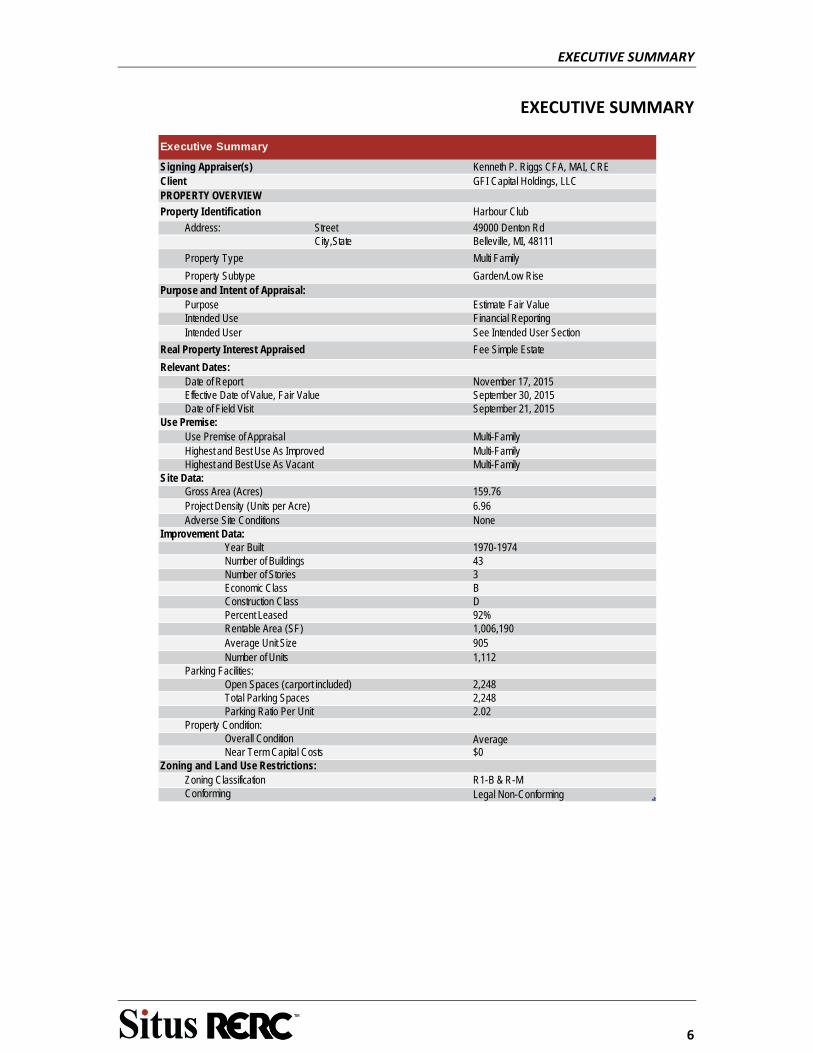

Signing Appraiser(s) Kenneth P. Riggs CFA, MAI, CREClient GFI Capital Holdings, LLCPROPERTY OVERVIEW

Property Identification Harbour Club

Address: Street 49000 Denton RdCity,State Belleville, MI, 48111

Property Type Multi Family

Property Subtype Garden/Low RisePurpose and Intent of Appraisal:

Purpose Estimate Fair ValueIntended Use Financial ReportingIntended User See Intended User Section

Real Property Interest Appraised Fee Simple Estate

Relevant Dates:Date of Report November 17, 2015Effective Date of Value, Fair Value September 30, 2015Date of Field Visit September 21, 2015

Use Premise:Use Premise of Appraisal Multi-FamilyHighest and Best Use As Improved Multi-FamilyHighest and Best Use As Vacant Multi-Family

Site Data:Gross Area (Acres) 159.76Project Density (Units per Acre) 6.96Adverse Site Conditions None

Improvement Data:Year Built 1970-1974Number of Buildings 43Number of Stories 3Economic Class BConstruction Class DPercent Leased 92%Rentable Area (SF) 1,006,190Average Unit Size 905Number of Units 1,112

Parking Facilities:Open Spaces (carport included) 2,248Total Parking Spaces 2,248Parking Ratio Per Unit 2.02

Property Condition:Overall Condition AverageNear Term Capital Costs $0

Zoning and Land Use Restrictions:Zoning Classification R1-B & R-MConforming Legal Non-Conforming

Executive Summary

EXECUTIVE SUMMARY

7

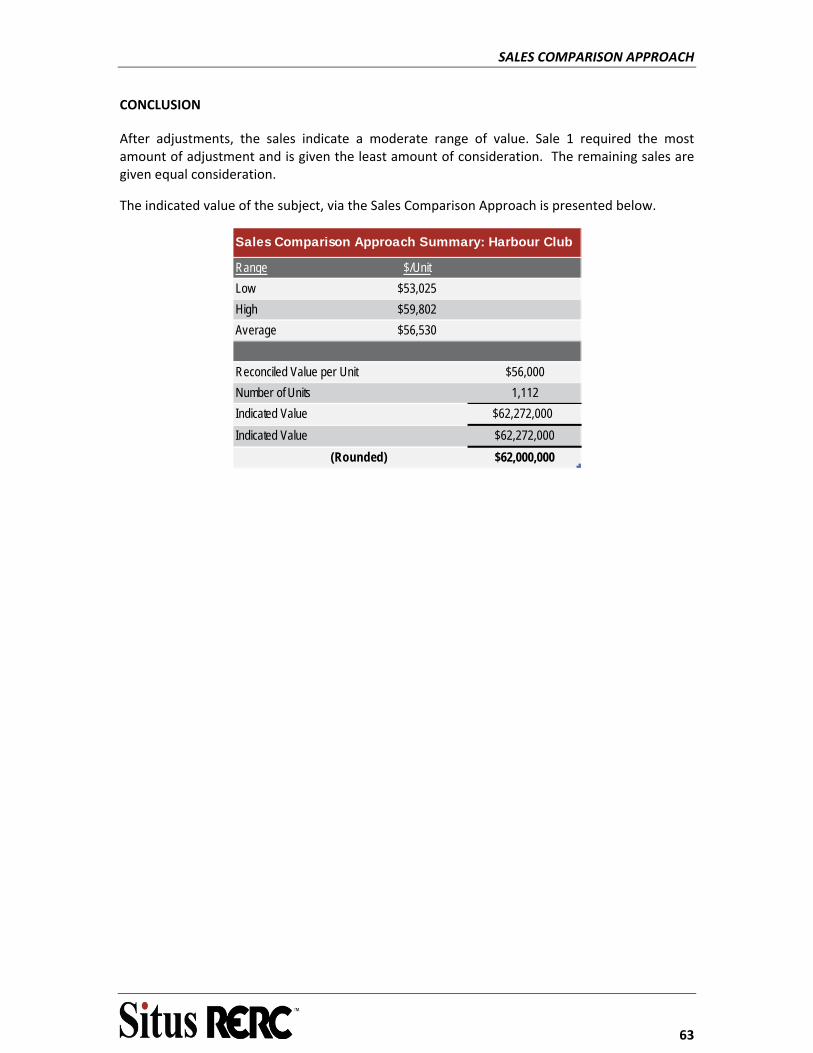

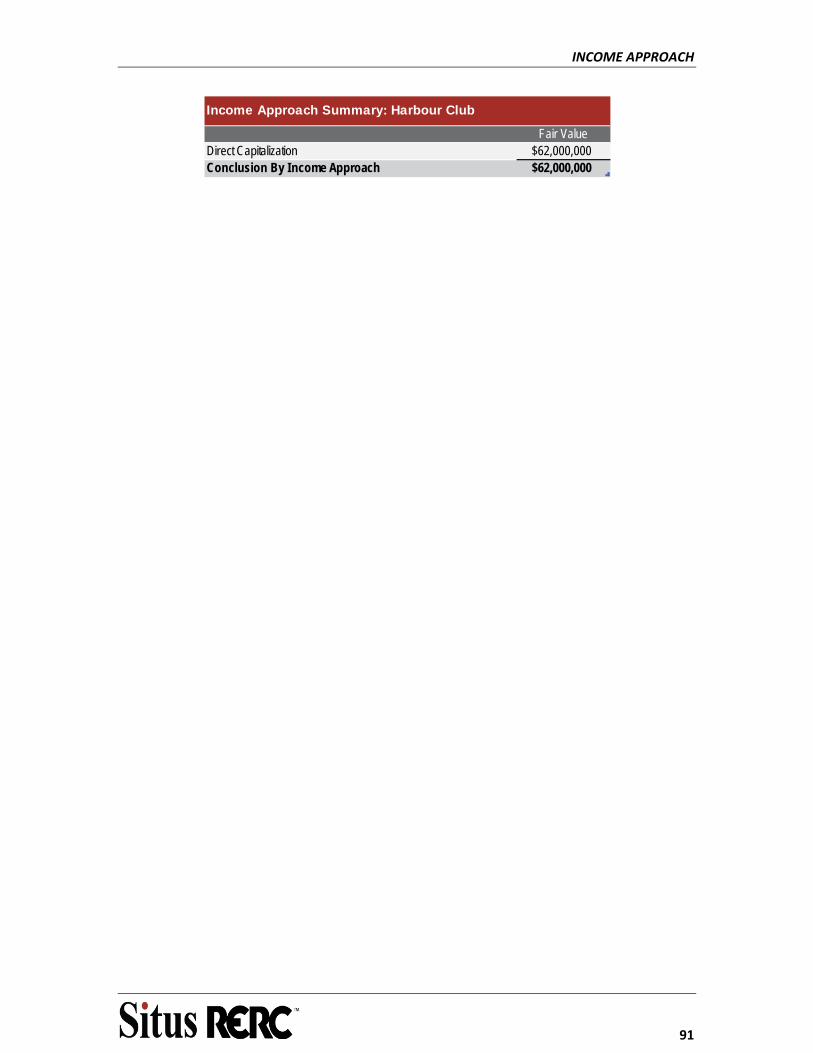

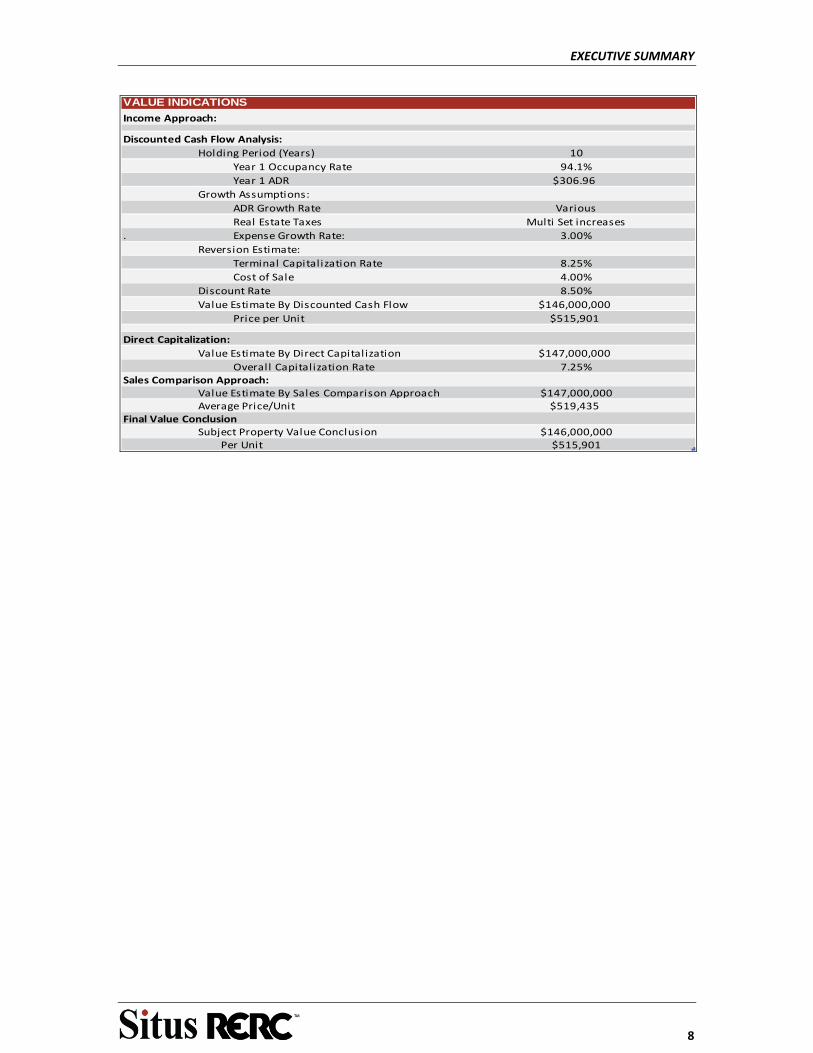

Sales Comparison Approach:Indicated Value $62,000,000Indicated Value per Unit $55,755

Income Capitalization Approach:Direct Capitalization Analysis:

Capitalization Rate 8.00%Indicated Value Estimate $62,000,000Indicated Value per Unit $55,755

Final Value EstimateValue Estimate $62,000,000

Indicated Value per Unit $55,755

Implied EGIM 6.13Implied Overall Cap Rate 7.95%

Value Indications

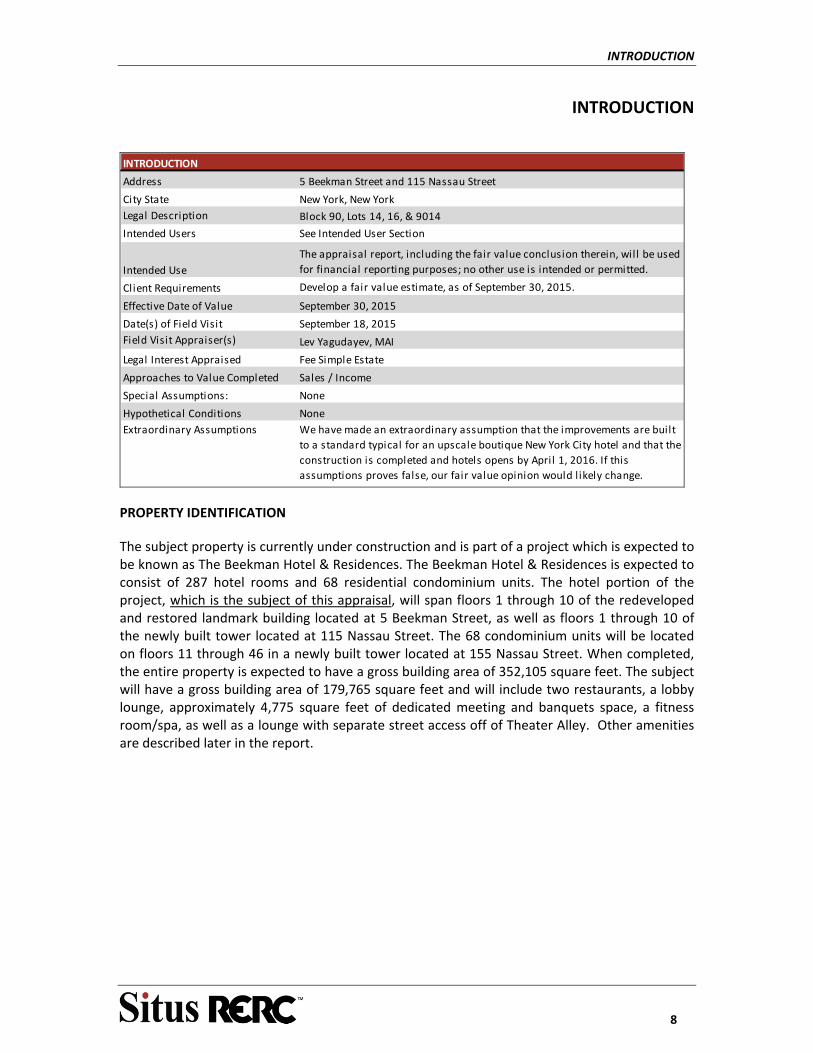

INTRODUCTION

8

INTRODUCTION

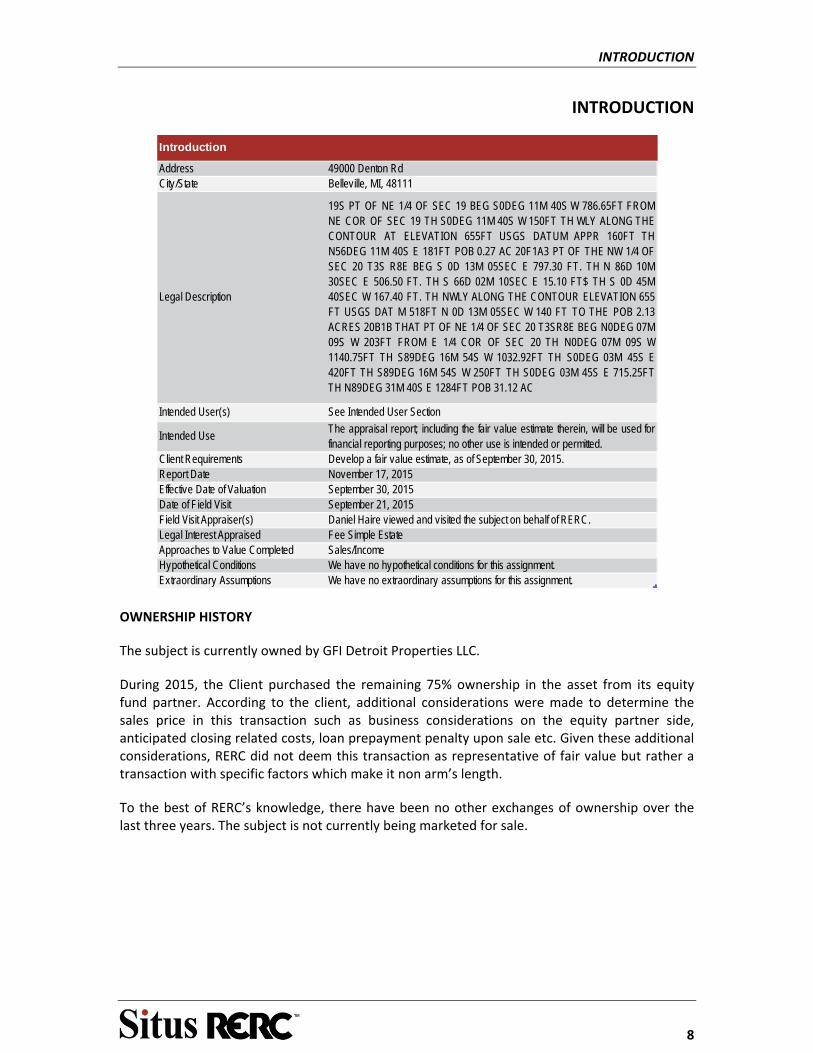

Address 49000 Denton RdCity/State Belleville, MI, 48111

Legal Description

19S PT OF NE 1/4 OF SEC 19 BEG S0DEG 11M 40S W 786.65FT FROMNE COR OF SEC 19 TH S0DEG 11M 40S W 150FT TH WLY ALONG THECONTOUR AT ELEVATION 655FT USGS DATUM APPR 160FT THN56DEG 11M 40S E 181FT POB 0.27 AC 20F1A3 PT OF THE NW 1/4 OFSEC 20 T3S R8E BEG S 0D 13M 05SEC E 797.30 FT. TH N 86D 10M30SEC E 506.50 FT. TH S 66D 02M 10SEC E 15.10 FT$ TH S 0D 45M40SEC W 167.40 FT. TH NWLY ALONG THE CONTOUR ELEVATION 655FT USGS DAT M 518FT N 0D 13M 05SEC W 140 FT TO THE POB 2.13ACRES 20B1B THAT PT OF NE 1/4 OF SEC 20 T3SR8E BEG N0DEG 07M09S W 203FT FROM E 1/4 COR OF SEC 20 TH N0DEG 07M 09S W1140.75FT TH S89DEG 16M 54S W 1032.92FT TH S0DEG 03M 45S E420FT TH S89DEG 16M 54S W 250FT TH S0DEG 03M 45S E 715.25FTTH N89DEG 31M 40S E 1284FT POB 31.12 AC

Intended User(s) See Intended User Section

Intended UseThe appraisal report; including the fair value estimate therein, will be used forfinancial reporting purposes; no other use is intended or permitted.

Client Requirements Develop a fair value estimate, as of September 30, 2015.Report Date November 17, 2015Effective Date of Valuation September 30, 2015Date of Field Visit September 21, 2015Field Visit Appraiser(s) Daniel Haire viewed and visited the subject on behalf of RERC.Legal Interest Appraised Fee Simple EstateApproaches to Value Completed Sales/IncomeHypothetical Conditions We have no hypothetical conditions for this assignment.Extraordinary Assumptions We have no extraordinary assumptions for this assignment.

Introduction

OWNERSHIP HISTORY

The subject is currently owned by GFI Detroit Properties LLC.

During 2015, the Client purchased the remaining 75% ownership in the asset from its equity fund partner. According to the client, additional considerations were made to determine the sales price in this transaction such as business considerations on the equity partner side, anticipated closing related costs, loan prepayment penalty upon sale etc. Given these additional considerations, RERC did not deem this transaction as representative of fair value but rather a transaction with specific factors which make it non arm’s length.

To the best of RERC’s knowledge, there have been no other exchanges of ownership over the last three years. The subject is not currently being marketed for sale.

INTRODUCTION

9

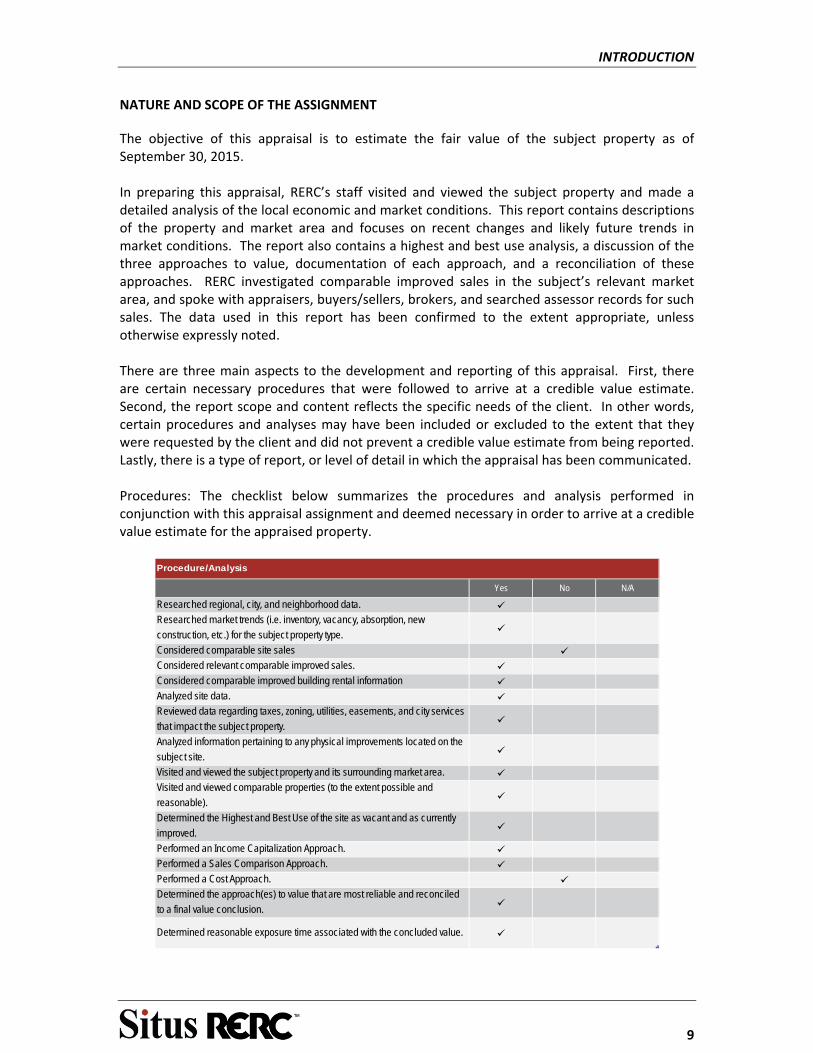

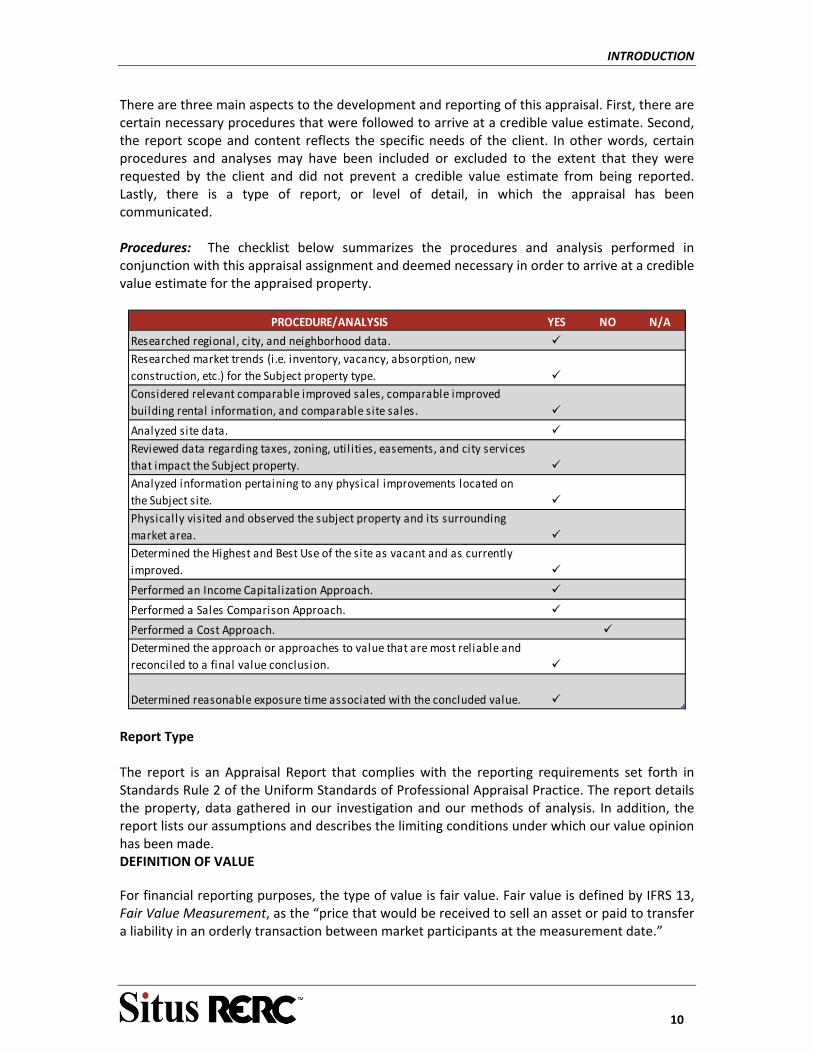

NATURE AND SCOPE OF THE ASSIGNMENT

The objective of this appraisal is to estimate the fair value of the subject property as of September 30, 2015. In preparing this appraisal, RERC’s staff visited and viewed the subject property and made a detailed analysis of the local economic and market conditions. This report contains descriptions of the property and market area and focuses on recent changes and likely future trends in market conditions. The report also contains a highest and best use analysis, a discussion of the three approaches to value, documentation of each approach, and a reconciliation of these approaches. RERC investigated comparable improved sales in the subject’s relevant market area, and spoke with appraisers, buyers/sellers, brokers, and searched assessor records for such sales. The data used in this report has been confirmed to the extent appropriate, unless otherwise expressly noted. There are three main aspects to the development and reporting of this appraisal. First, there are certain necessary procedures that were followed to arrive at a credible value estimate. Second, the report scope and content reflects the specific needs of the client. In other words, certain procedures and analyses may have been included or excluded to the extent that they were requested by the client and did not prevent a credible value estimate from being reported. Lastly, there is a type of report, or level of detail in which the appraisal has been communicated. Procedures: The checklist below summarizes the procedures and analysis performed in conjunction with this appraisal assignment and deemed necessary in order to arrive at a credible value estimate for the appraised property.

Yes No N/A

Researched regional, city, and neighborhood data. Researched market trends (i.e. inventory, vacancy, absorption, new

construction, etc.) for the subject property type.

Considered comparable site sales Considered relevant comparable improved sales. Considered comparable improved building rental information Analyzed site data. Reviewed data regarding taxes, zoning, utilities, easements, and city services

that impact the subject property.

Analyzed information pertaining to any physical improvements located on the

subject site.

Visited and viewed the subject property and its surrounding market area. Visited and viewed comparable properties (to the extent possible and

reasonable).

Determined the Highest and Best Use of the site as vacant and as currently

improved.

Performed an Income Capitalization Approach. Performed a Sales Comparison Approach. Performed a Cost Approach. Determined the approach(es) to value that are most reliable and reconciled

to a final value conclusion.

Determined reasonable exposure time associated with the concluded value.

Procedure/Analysis

INTRODUCTION

10

Report Type: The report is an appraisal report that complies with the reporting requirements set forth in Standards Rule 2 of the Uniform Standards of Professional Appraisal Practice. The report details the property, data gathered in our investigation and our methods of analysis. In addition, the report lists our assumptions and describes the limiting conditions under which our value opinion has been made.

DEFINITION OF VALUE

For financial reporting purposes, the type of value is fair value. Fair value is defined by IFRS 13, Fair Value Measurement, as the “price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.”

Implicit in this definition is the definition of market value. The market value definition used in this analysis is used by agencies that regulate federally insured financial institutions in the United States. Market value means the most probable price that a property should bring in a competitive and open market under all conditions requisite to a fair sales, the buyer and seller each acting prudently and knowledgably, and assuming the price is not affected by undue stimulus. Implicit in this definition is the consummation of a sale as of a specified date and the passing of title from seller to buyer under conditions whereby

Buyer and seller are typically motivated;

Both parties are well informed or well advised, and acting in what they consider their best interests;

A reasonable time is allowed for exposure in the open market;

Payment is made in terms of cash in U.S. dollars or in terms of financial arrangements comparable thereto; and

The price represents the normal consideration for the property sold unaffected by special or creative financing or sales concessions granted by anyone associated with the sale.1

1(12 C.F.R Part 34.42(g); 55 Federal Register 34696, August 24, 1990, as amended at 57 Federal Register 12202, April 9, 1992; 59 Federal Register 29499, June 7, 1994)

INTEREST APPRAISED

The real property interest appraised is considered to be the fee simple estate of the subject property.

The Dictionary of Real Estate Appraisal, 5th edition defines the fee simple estate as:

“Absolute ownership unencumbered by any other interest or estate, subject only to the limitations imposed by the governmental powers of taxation, eminent domain, police power, and escheat.”

INTRODUCTION

11

INTENDED USER

As specified in the engagement agreement between RERC and GFI Capital Holdings, LLC dated October 9, 2015, the Services (defined in the engagement agreement) and the Report (defined in the engagement agreement) are for the use and benefit of, and may be relied upon solely by the GFI Capital Holdings, LLC (the “Company”), its Affiliates (defined in the engagement agreement), and GFI Real Estate Limited. The Report shall remain confidential, but for the purposes of its Intended Use (defined in the engagement agreement), RERC understands that the Report will be disclosed to the following:

a. Independent auditors, accountants, attorneys and other professionals acting on behalf of the Company its Affiliates, and GFI Real Estate Limited;

b. Governmental agencies having regulatory authority over the Company, its Affiliates, and GFI Real Estate Limited; and

c. Designated persons pursuant to an order or legal process of any court or governmental agency having jurisdiction over the Company, its Affiliates, and GFI Real Estate Limited.

RERC understands that the Report is to be used to aid GFI Capital Holdings, LLC and its Affiliates in the preparation of Financial Statements for the GFI Real Estate Limited. The Report is to be used in whole and not in part. No part of the Report shall be used in conjunction with any other analysis. Except as otherwise stated herein, the Report may not be used by any person other than the parties to whom it is addressed or for purposes other than that for which it was prepared. No part of the Report shall be conveyed to the public through advertising, or used in any sales, promotion, offering or SEC material without RERC’s prior written consent.

In providing any consent RERC will note that an appraisal: (1) is an estimate of value as of a point in time, (2) is not a guarantee of financial results, (3) is not a due diligence document beyond the estimate of value. No matter the care exercised, the results achieved in an actual transaction may be different than the appraisal results, as the appraisal is an estimate of value. Any opinion of value is inherently subjective and the results speculative, as they are based on information available at the time the value opinion was being prepared, and are influenced by matters relating to operations, projections of the future, as well as the appraisers’ interpretation of the market. As such, relying on an appraisal is subject to risks and uncertainties. The appraisal report is prepared for the specifically identified use and user and not intended, permitted, nor appropriate to be relied on for other uses or by other users. The reader and user must rely on their own due diligence and analysis of the subject property in evaluating the overall security transaction, and not rely on the appraisal for their final decision making. In addition, the reader and user is/are encouraged to refer to the definition of fair value (previously defined).

INTRODUCTION

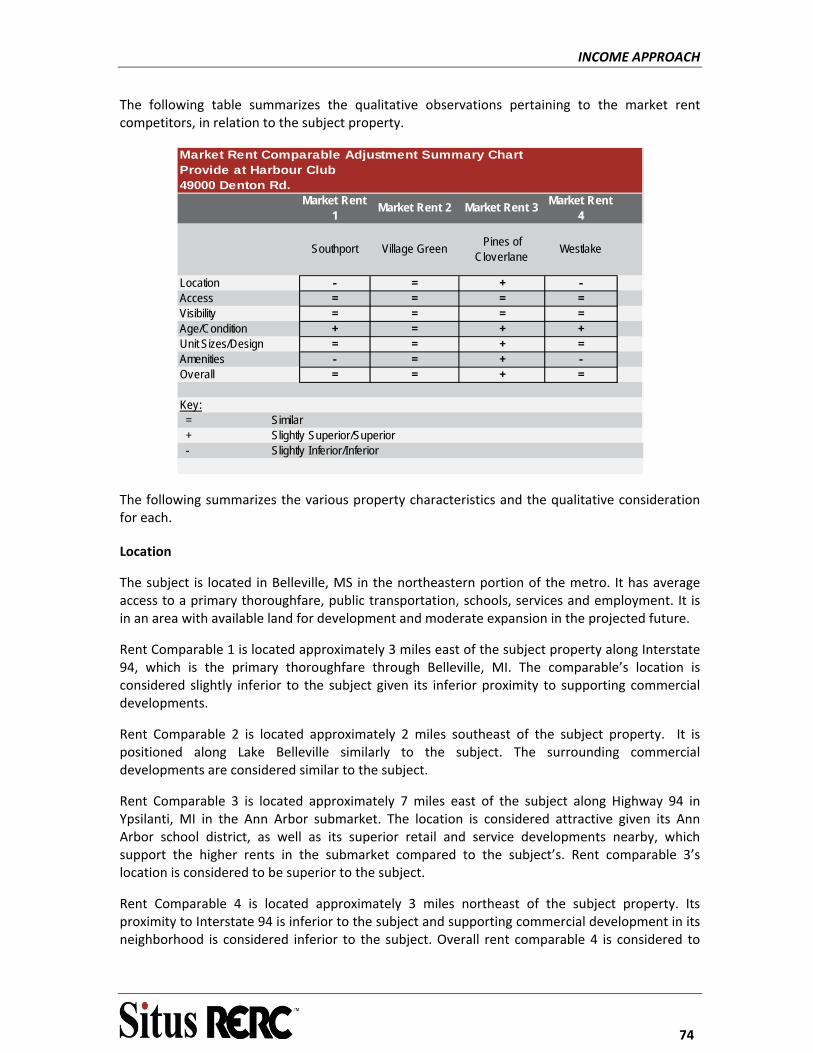

12

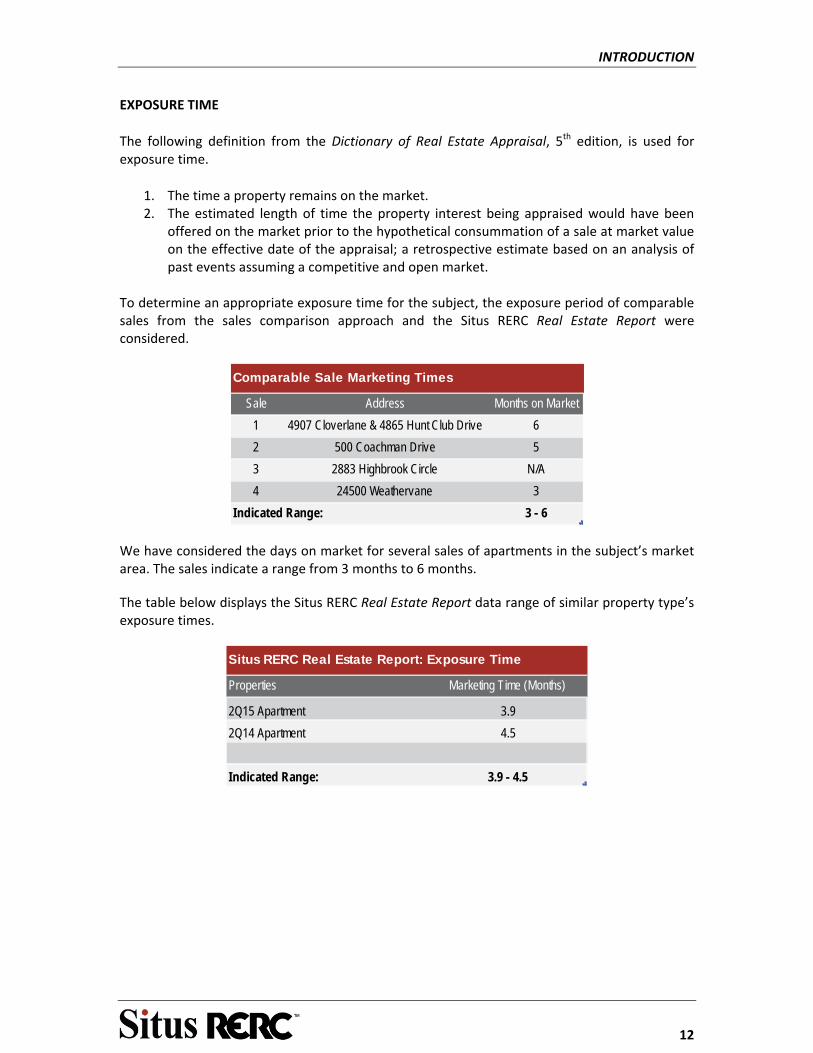

EXPOSURE TIME

The following definition from the Dictionary of Real Estate Appraisal, 5th edition, is used for exposure time.

1. The time a property remains on the market. 2. The estimated length of time the property interest being appraised would have been

offered on the market prior to the hypothetical consummation of a sale at market value on the effective date of the appraisal; a retrospective estimate based on an analysis of past events assuming a competitive and open market.

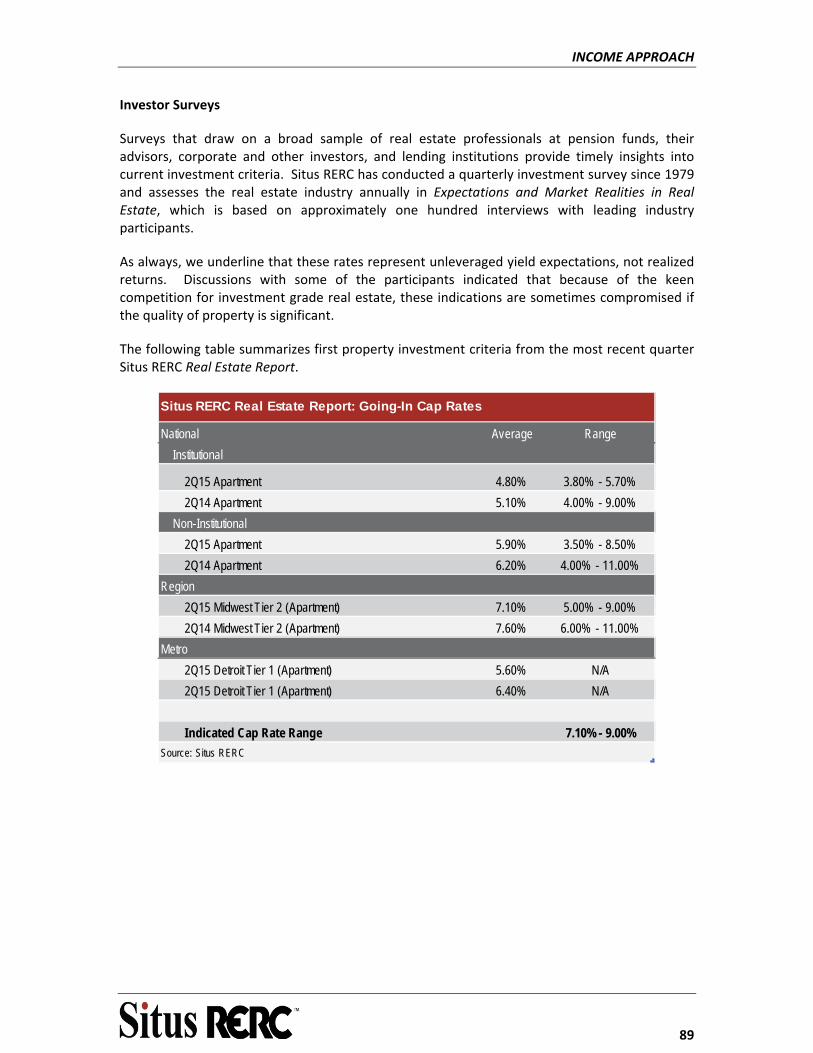

To determine an appropriate exposure time for the subject, the exposure period of comparable sales from the sales comparison approach and the Situs RERC Real Estate Report were considered.

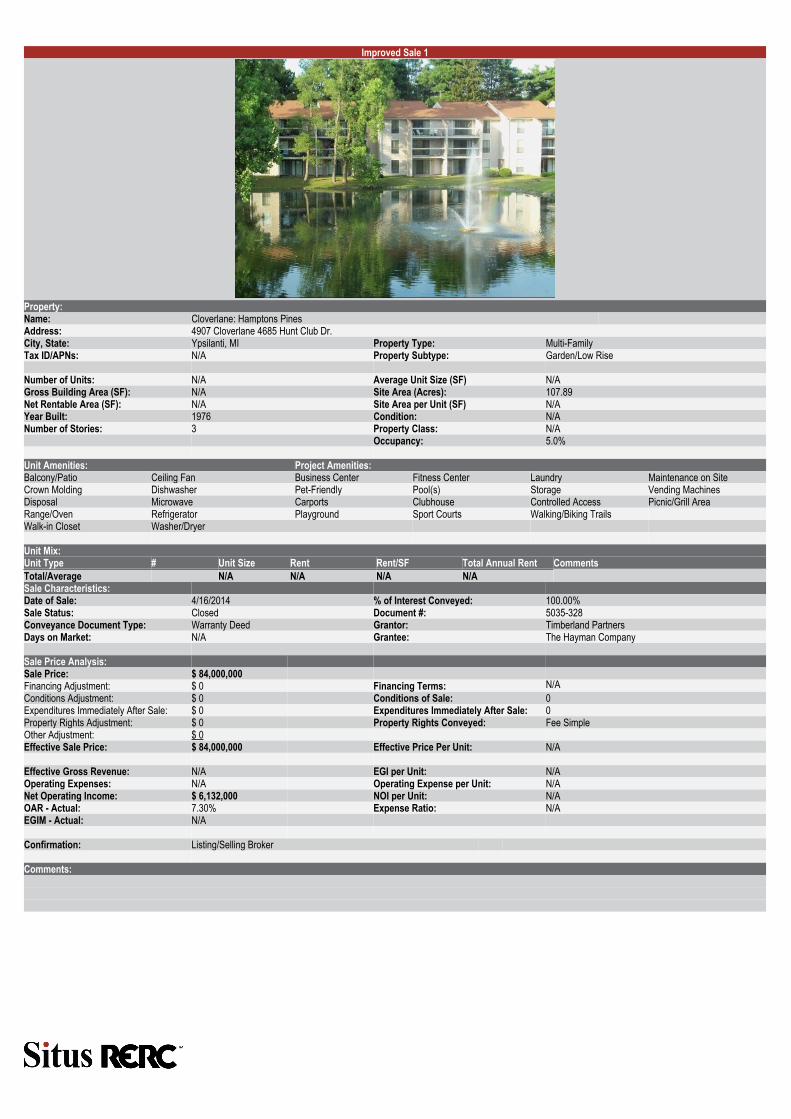

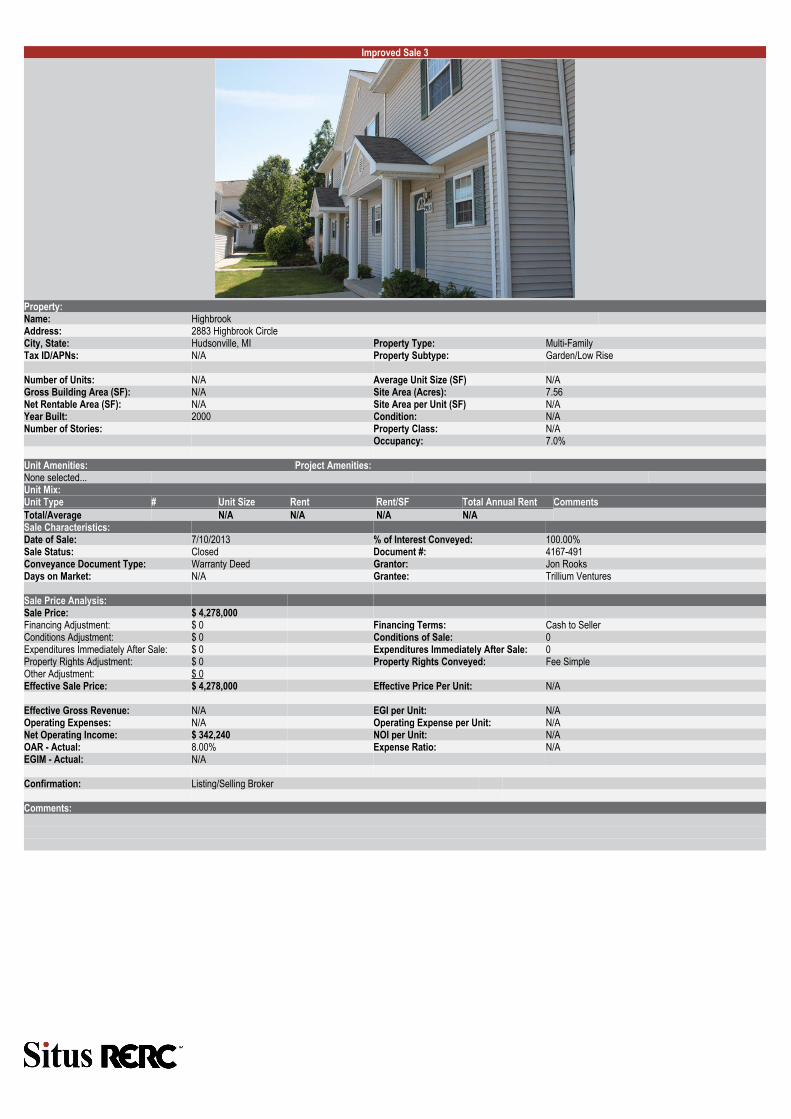

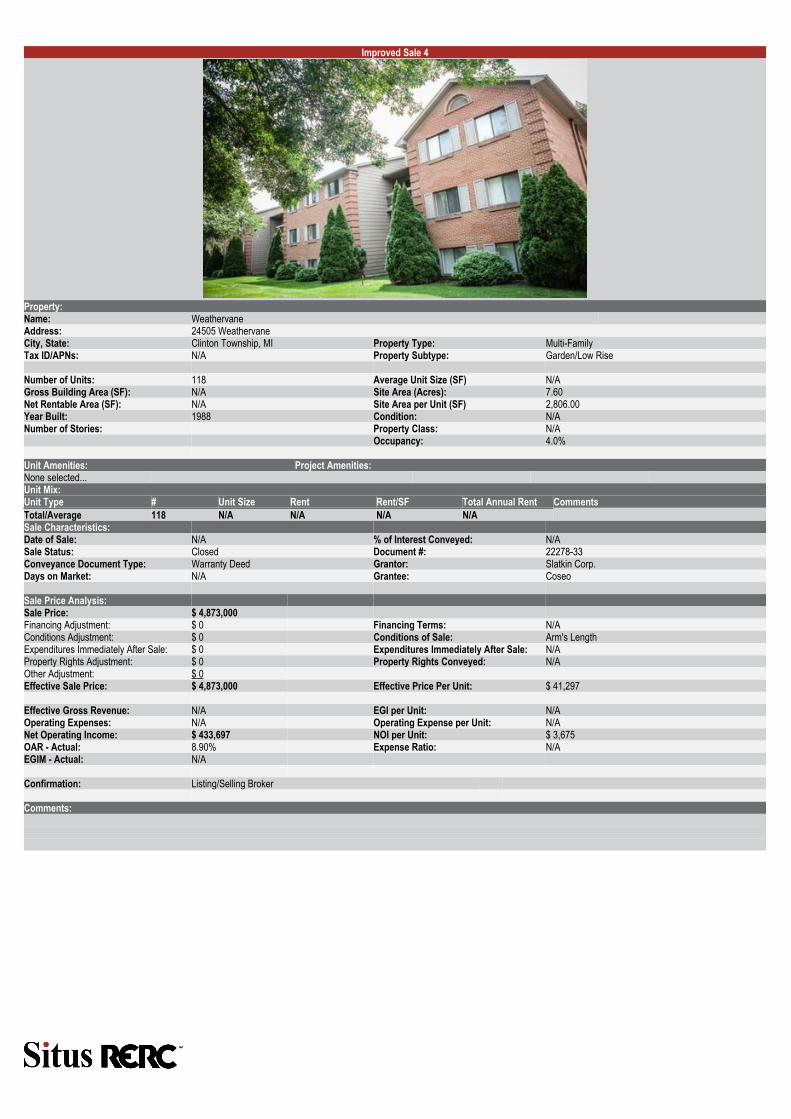

Sale Address Months on Market

1 4907 Cloverlane & 4865 Hunt Club Drive 6

2 500 Coachman Drive 5

3 2883 Highbrook Circle N/A

4 24500 Weathervane 3

Indicated Range: 3 - 6

Comparable Sale Marketing Times

We have considered the days on market for several sales of apartments in the subject’s market area. The sales indicate a range from 3 months to 6 months.

The table below displays the Situs RERC Real Estate Report data range of similar property type’s exposure times.

Properties Marketing Time (Months)

2Q15 Apartment 3.9

2Q14 Apartment 4.5

Indicated Range: 3.9 - 4.5

Situs RERC Real Estate Report: Exposure Time

INTRODUCTION

13

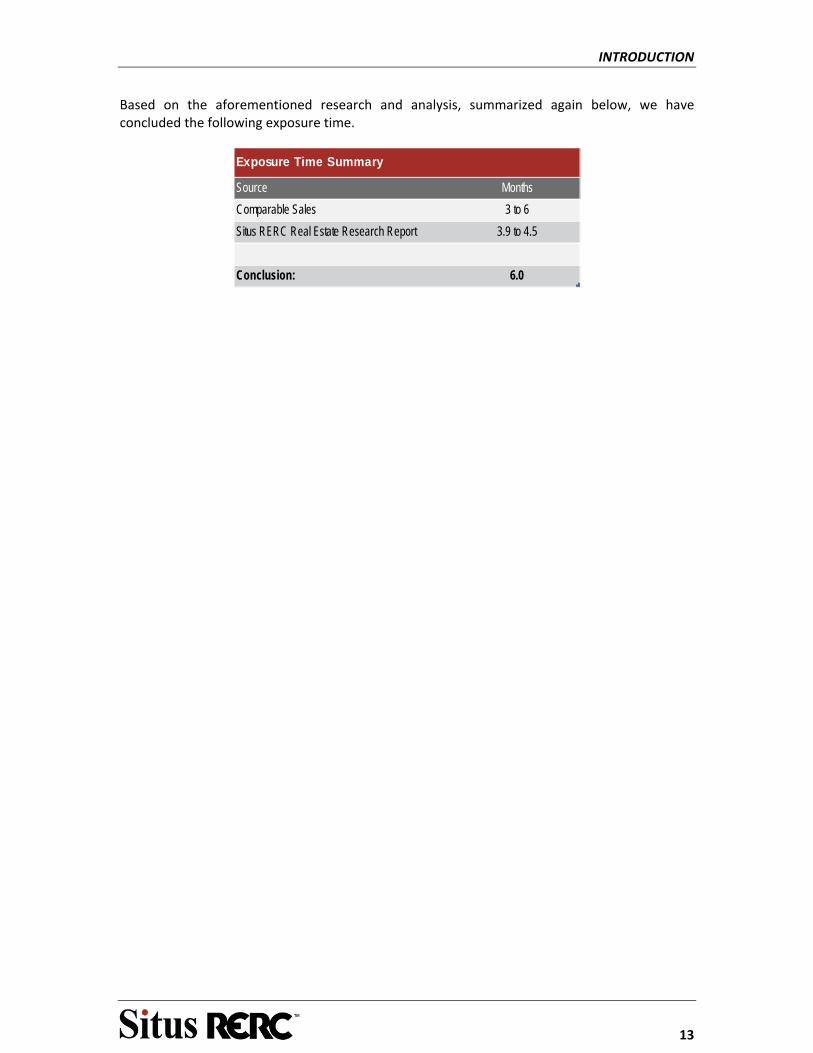

Based on the aforementioned research and analysis, summarized again below, we have concluded the following exposure time.

Source Months

Comparable Sales 3 to 6

Situs RERC Real Estate Research Report 3.9 to 4.5

Conclusion: 6.0

Exposure Time Summary

THE REGION

14

THE REGION

Regional Analysis: A survey of the industries and businesses that generate employment and income in a community as well as the rate of population growth and levels of income, both of which are functions of employment. Economic base analysis is used to forecast the level and composition of future economic activity. (The Dictionary of Real Estate Appraisal, 5th edition)

OVERVIEW

The value of the subject property is affected by various influences of the surrounding region. Infrastructure, base employment, and overall social, economic, and political conditions in the area form the background against which the property is considered. Primary sources of data include the Site To Do Business Online and The Bureau of Labor Statistics.

The subject property is located in Belleville, Wayne County, Michigan in the Detroit‐Warren‐Dearborn, MI Metro Area. The MSA is located in Southeast Michigan, consisting of the city of Detroit and its surrounding area. The area includes a variety of natural landscapes, parks, and beaches, with a recreational coastline linking the Great Lakes. The subject’s location within the region is displayed in the map below.

Subject

THE REGION

15

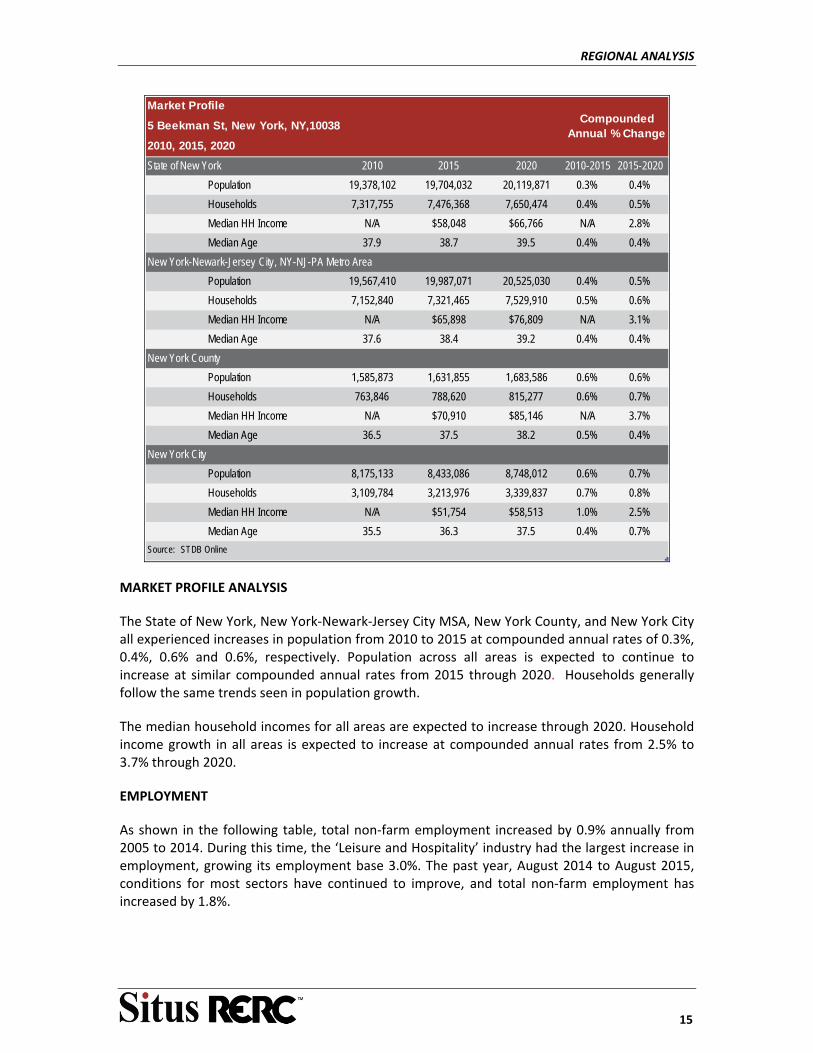

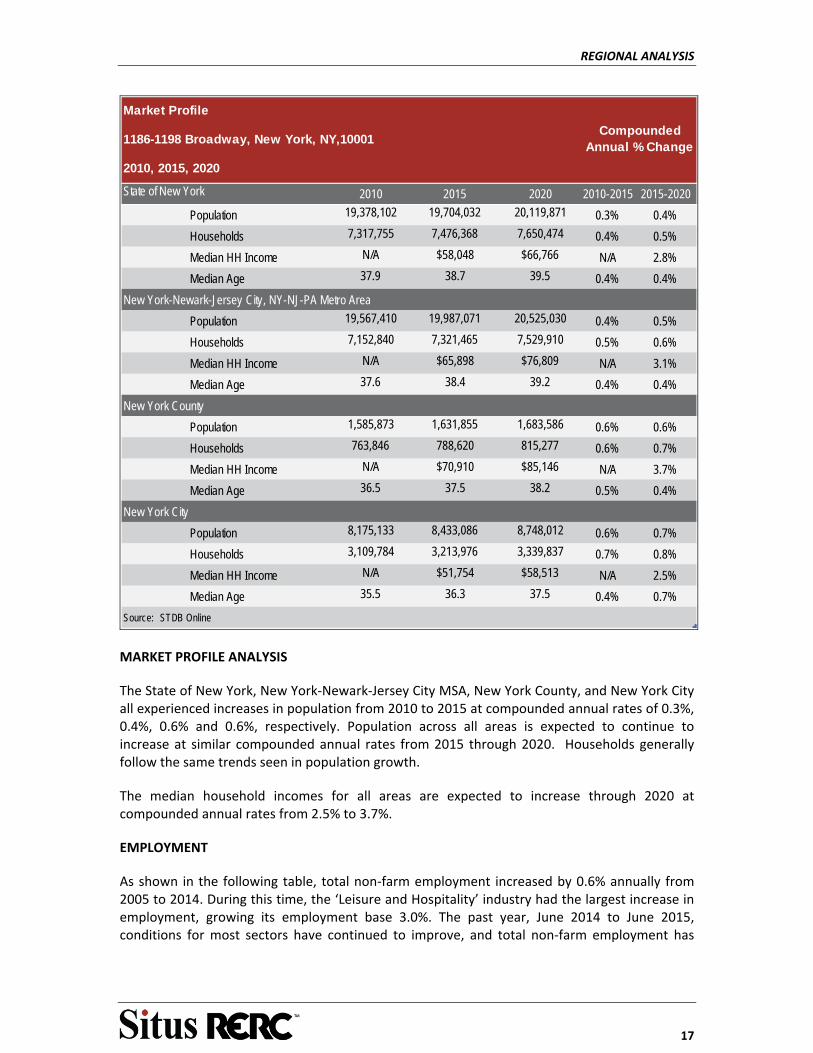

MARKET PROFILE

The following market profile indicates that the subject market is healthy with sustainable, moderate population, household and income growth.

State of Michigan 2010 2015 2020 2010-2015 2015-2020

Population 9,883,640 9,870,786 9,944,000 0.0% 0.1%

Households 3,872,508 3,902,559 3,943,165 0.2% 0.2%

Median HH Income N/A $49,402 $56,701 N/A 2.8%

Median Age 38.8 39.9 40.7 0.6% 0.4%

Detroit-Warren-Dearborn, MI Metro Area

Population 4,296,250 4,261,580 4,278,482 -0.2% 0.1%

Households 1,682,111 1,682,649 1,694,370 0.0% 0.1%

Median HH Income N/A $52,839 $62,034 N/A 3.3%

Median Age 39.0 40.3 41.2 0.7% 0.4%

Wayne County

Population 1,820,584 1,751,579 1,709,289 -0.8% -0.5%

Households 702,749 682,376 668,376 -0.6% -0.4%

Median HH Income N/A $41,008 $48,578 N/A 3.4%

Median Age 37.2 38.4 39.2 0.6% 0.4%

Belleville

Population 3,991 3,927 3,855 -0.3% -0.4%

Households 1,755 1,728 1,698 -0.3% -0.3%

Median HH Income N/A $40,179 $48,791 N/A 4.0%

Median Age 40.1 40.8 41.7 0.3% 0.4%

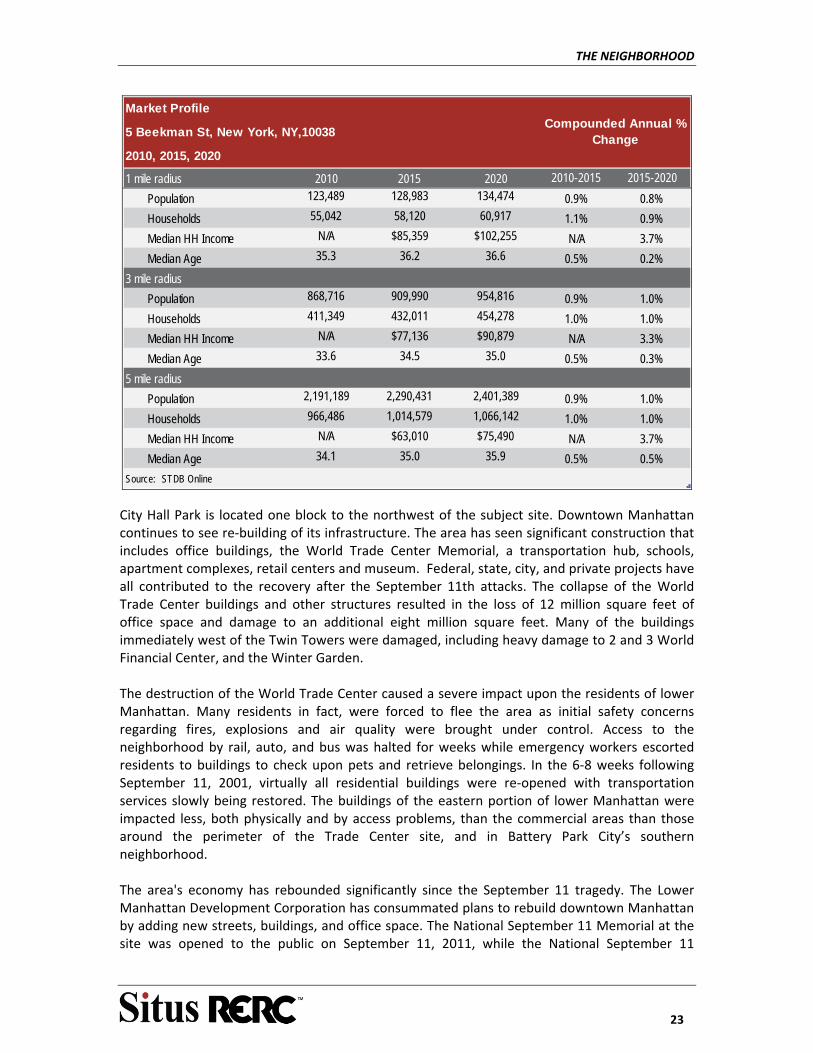

Source: STDB Online

Market Profile

49000 Denton Rd

2010, 2015, 2020

Compounded Annual % Change

MARKET PROFILE ANALYSIS

The market profile indicates that the Detroit‐Warren‐Dearborn MSA experienced growth rate decreases from 2010 to 2015 at ‐0.2% for population, while households remained stagnant. Negative growth rates for Wayne County were higher than the MSA at ‐0.8% for the population and ‐0.6% for households. Population growth for the State of Michigan remained materially unchanged at 0.0%, while households increased 0.2%. The City of Belleville experienced a negative growth rate from 2010 to 2015 of ‐0.3% for population and ‐0.3% for households. The State of Michigan and Detroit‐ Warren‐ Dearborn, MI MSA are projected to experience a slight increase in population from 2015 to 2020, while all other observed geographical areas are expected to continue to experience negative growth.

THE REGION

16

ECONOMIC FORCES

The Greater Detroit Region has a strong and currently revitalizing economic base. Since 2006, the Detroit Region has seen in excess of $12 billion invested in commercial, industrial, and residential properties. Moreover, major American corporations including Quicken Loans and Blue Cross Blue Shield have added over 12,000 jobs in downtown Detroit alone in the past 4 years. Recent metrics further elucidate the revitalization occurring in the Detroit Region as gross domestic product has increased 14% since the beginnings of the nation’s economic recovery from recession in 2009. These effects have been felt in a major way among the working class population as personal incomes are up over 6% relative to 2010 figures.

To catalyze private sector growth and small business generation Michigan replaced its Michigan Business Tax with a simpler corporate income tax effective January 2012. This less complicated business taxation structure reduced business taxes by approximately 86%, reducing operations costs, and resulting in continued investment in Michigan as a whole, with significant investments taking place in the Detroit Metro. Personal property taxes on business have also begun their phase‐out in Michigan effective January 2014. The Tax Foundation ranks Michigan’s overall business tax climate 12th in the nation, with corporate taxation specifically ranking as high as 7th in the nation.

Beyond incentivizing taxation and the upshot economic growth, varieties of grant, loan, and other economic assistance monies are available for competitive start‐ups and projects in the Detroit Metro. These include the Michigan Business Development Program from the Michigan Strategic Fund in cooperation with the Michigan Economic Development Corporation, and the Industrial Property Tax Abatement for new business investment in manufacturing, renovation of existing plants, and technology operations. Moreover, rehabilitation projects have newly been awarded 100% abatement by the State of Michigan pursuant to the Commercial Rehabilitation Act P.A. 210, provided the commercial properties are at a minimum of 15 years old.

The culmination of positive economic indicators and actively evolving programs for business incentives, as well as the strong unemployment trends elucidated in the employment section of this report, Detroit appears well positioned for continued recovery. EMPLOYMENT

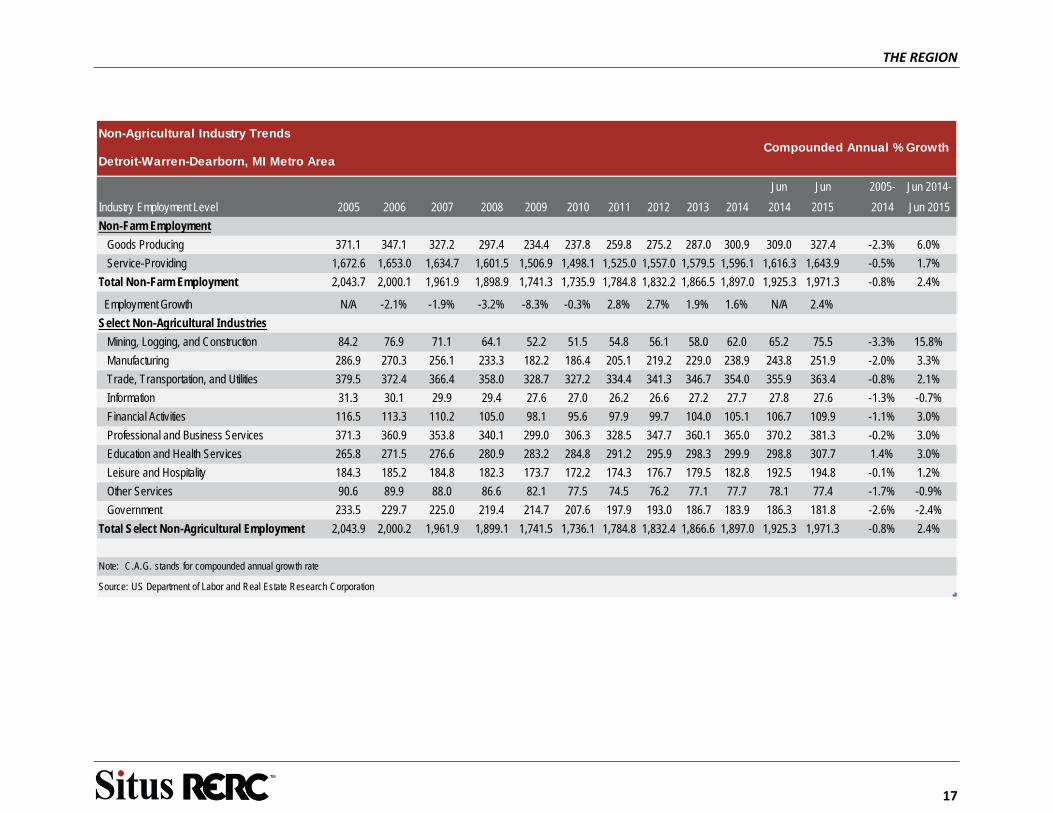

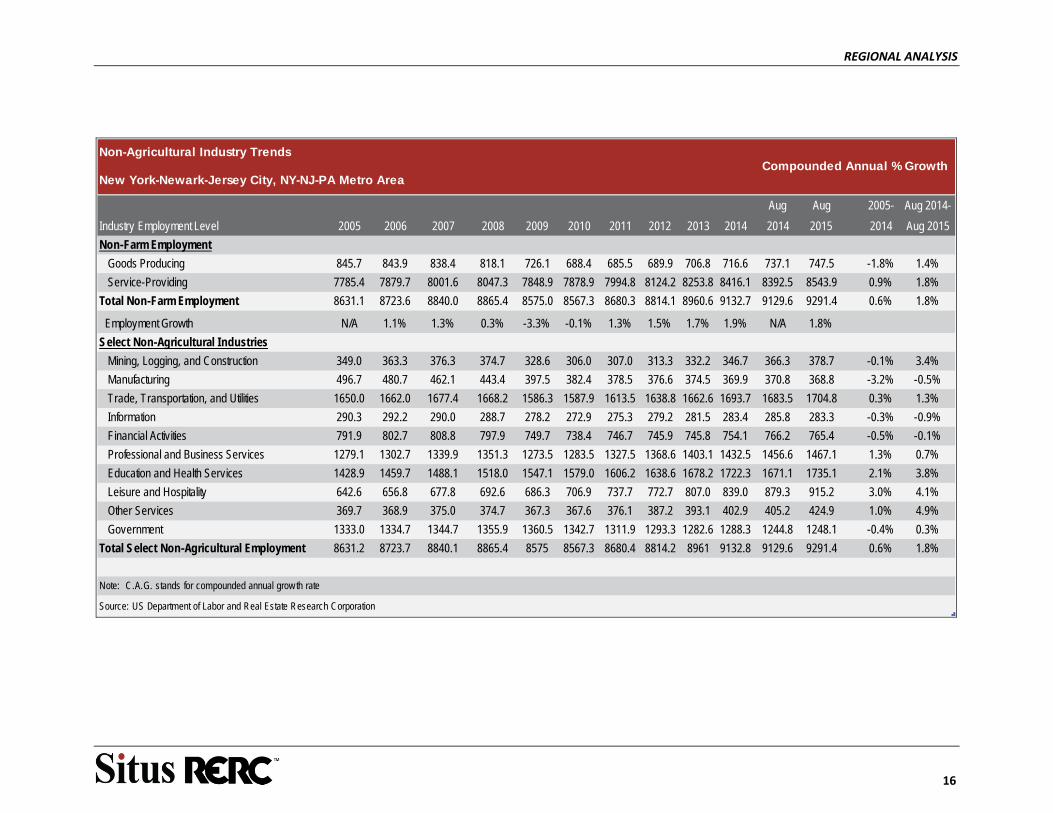

An overview of the total civilian labor force in the Detroit‐Warren‐Dearborn, MI Metro Area from 2005 through 2014 is included in the following chart supplied by the Bureau of Labor Statistics. From June 2014 to June 2015, the trend shows an increase of 2.4%. When looking at the industries separately, over the past ten years all sectors reported negative growth with Mining, Logging, and Construction reporting the largest negative growth.

The following table presents a more detailed picture of the non‐agricultural industry trends from 2005 to June 2015.

THE REGION

17

Non-Agricultural Industry Trends

Detroit-Warren-Dearborn, MI Metro Area

Jun Jun 2005- Jun 2014-

Industry Employment Level 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2014 2015 2014 Jun 2015

Non-Farm Employment

Goods Producing 371.1 347.1 327.2 297.4 234.4 237.8 259.8 275.2 287.0 300.9 309.0 327.4 -2.3% 6.0%

Service-Providing 1,672.6 1,653.0 1,634.7 1,601.5 1,506.9 1,498.1 1,525.0 1,557.0 1,579.5 1,596.1 1,616.3 1,643.9 -0.5% 1.7%

Total Non-Farm Employment 2,043.7 2,000.1 1,961.9 1,898.9 1,741.3 1,735.9 1,784.8 1,832.2 1,866.5 1,897.0 1,925.3 1,971.3 -0.8% 2.4%

Employment Growth N/A -2.1% -1.9% -3.2% -8.3% -0.3% 2.8% 2.7% 1.9% 1.6% N/A 2.4%

Select Non-Agricultural Industries

Mining, Logging, and Construction 84.2 76.9 71.1 64.1 52.2 51.5 54.8 56.1 58.0 62.0 65.2 75.5 -3.3% 15.8%

Manufacturing 286.9 270.3 256.1 233.3 182.2 186.4 205.1 219.2 229.0 238.9 243.8 251.9 -2.0% 3.3%

Trade, Transportation, and Utilities 379.5 372.4 366.4 358.0 328.7 327.2 334.4 341.3 346.7 354.0 355.9 363.4 -0.8% 2.1%

Information 31.3 30.1 29.9 29.4 27.6 27.0 26.2 26.6 27.2 27.7 27.8 27.6 -1.3% -0.7%

Financial Activities 116.5 113.3 110.2 105.0 98.1 95.6 97.9 99.7 104.0 105.1 106.7 109.9 -1.1% 3.0%

Professional and Business Services 371.3 360.9 353.8 340.1 299.0 306.3 328.5 347.7 360.1 365.0 370.2 381.3 -0.2% 3.0%

Education and Health Services 265.8 271.5 276.6 280.9 283.2 284.8 291.2 295.9 298.3 299.9 298.8 307.7 1.4% 3.0%

Leisure and Hospitality 184.3 185.2 184.8 182.3 173.7 172.2 174.3 176.7 179.5 182.8 192.5 194.8 -0.1% 1.2%

Other Services 90.6 89.9 88.0 86.6 82.1 77.5 74.5 76.2 77.1 77.7 78.1 77.4 -1.7% -0.9%

Government 233.5 229.7 225.0 219.4 214.7 207.6 197.9 193.0 186.7 183.9 186.3 181.8 -2.6% -2.4%

Total Select Non-Agricultural Employment 2,043.9 2,000.2 1,961.9 1,899.1 1,741.5 1,736.1 1,784.8 1,832.4 1,866.6 1,897.0 1,925.3 1,971.3 -0.8% 2.4%

Note: C.A.G. stands for compounded annual grow th rate

Source: US Department of Labor and Real Estate Research Corporation

Compounded Annual % Growth

THE REGION

18

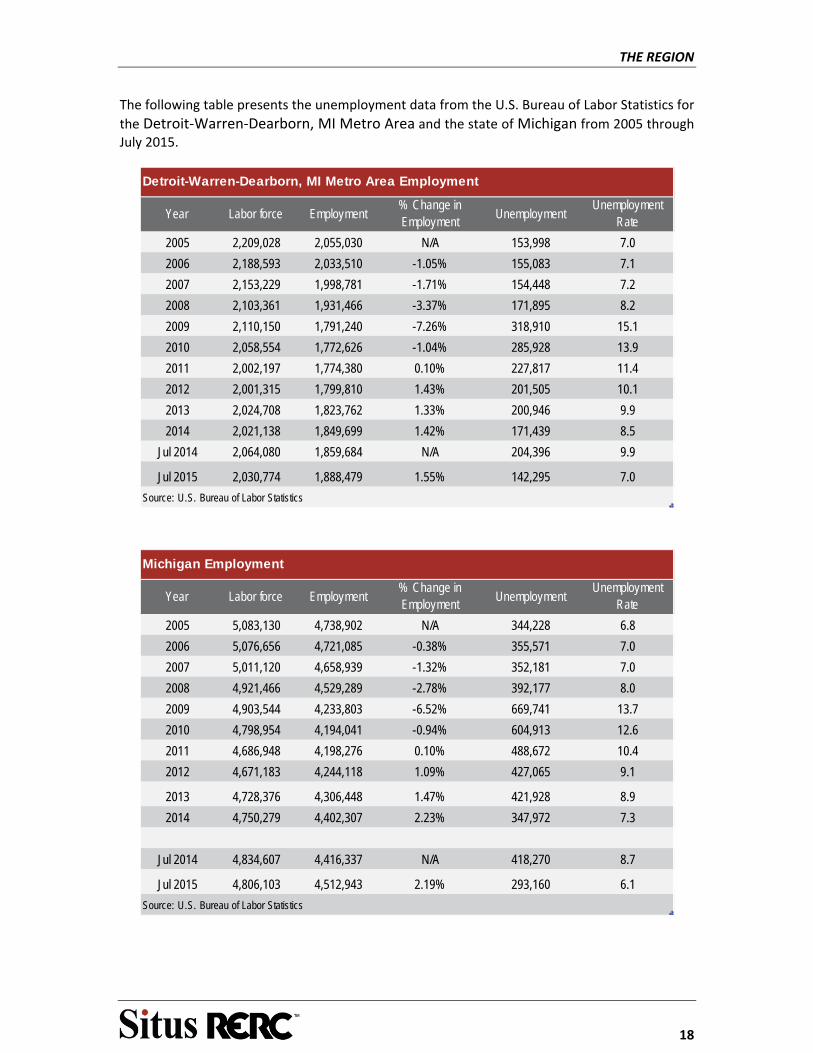

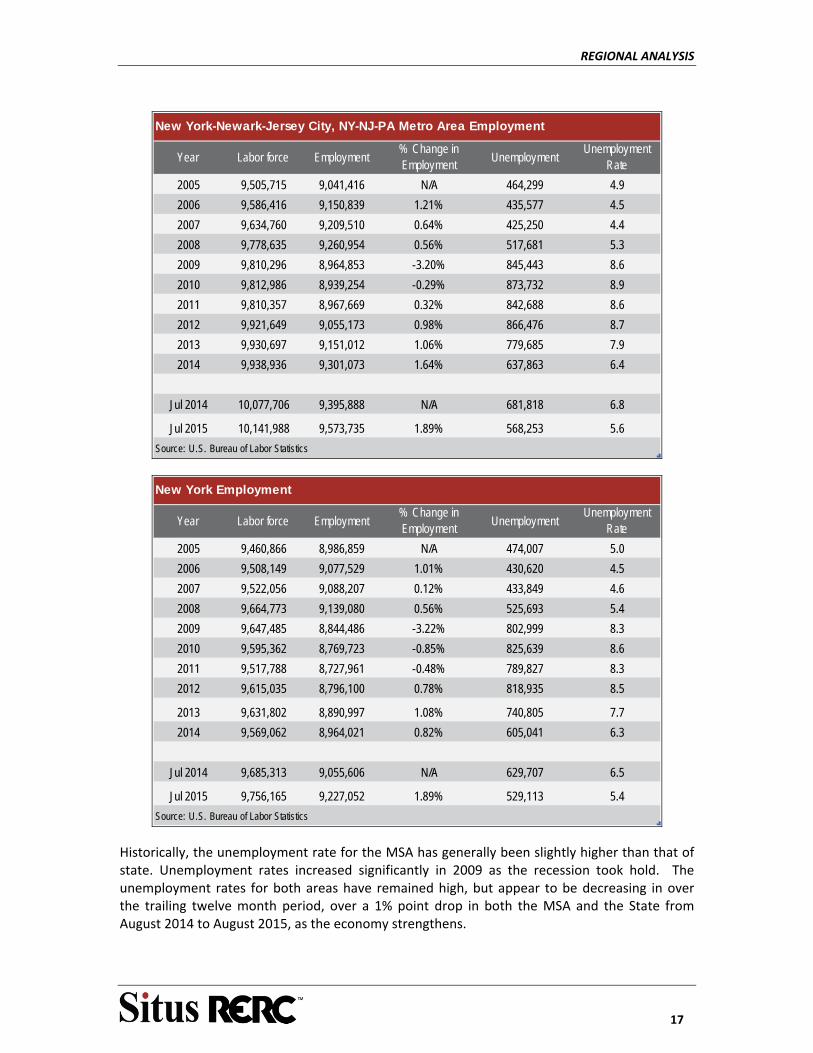

The following table presents the unemployment data from the U.S. Bureau of Labor Statistics for

the Detroit‐Warren‐Dearborn, MI Metro Area and the state of Michigan from 2005 through July 2015.

Year Labor force Employment% Change in Employment

UnemploymentUnemployment

Rate

2005 2,209,028 2,055,030 N/A 153,998 7.0

2006 2,188,593 2,033,510 -1.05% 155,083 7.1

2007 2,153,229 1,998,781 -1.71% 154,448 7.2

2008 2,103,361 1,931,466 -3.37% 171,895 8.2

2009 2,110,150 1,791,240 -7.26% 318,910 15.1

2010 2,058,554 1,772,626 -1.04% 285,928 13.9

2011 2,002,197 1,774,380 0.10% 227,817 11.4

2012 2,001,315 1,799,810 1.43% 201,505 10.1

2013 2,024,708 1,823,762 1.33% 200,946 9.9

2014 2,021,138 1,849,699 1.42% 171,439 8.5

Jul 2014 2,064,080 1,859,684 N/A 204,396 9.9

Jul 2015 2,030,774 1,888,479 1.55% 142,295 7.0

Source: U.S. Bureau of Labor Statistics

Year Labor force Employment% Change in Employment

UnemploymentUnemployment

Rate

2005 5,083,130 4,738,902 N/A 344,228 6.8

2006 5,076,656 4,721,085 -0.38% 355,571 7.0

2007 5,011,120 4,658,939 -1.32% 352,181 7.0

2008 4,921,466 4,529,289 -2.78% 392,177 8.0

2009 4,903,544 4,233,803 -6.52% 669,741 13.7

2010 4,798,954 4,194,041 -0.94% 604,913 12.6

2011 4,686,948 4,198,276 0.10% 488,672 10.4

2012 4,671,183 4,244,118 1.09% 427,065 9.1

2013 4,728,376 4,306,448 1.47% 421,928 8.9

2014 4,750,279 4,402,307 2.23% 347,972 7.3

Jul 2014 4,834,607 4,416,337 N/A 418,270 8.7

Jul 2015 4,806,103 4,512,943 2.19% 293,160 6.1

Source: U.S. Bureau of Labor Statistics

Detroit-Warren-Dearborn, MI Metro Area Employment

Michigan Employment

THE REGION

19

Unemployment rates for the MSA and the state have historically mirrored one another fairly closely. In 2009 and 2010, unemployment rates increased for the state of Michigan and the Detroit‐ Warren‐ Dearborn, MI MSA, reaching a 10‐year high in 2009, with unemployment rates at 13.7% and 15.1% respectively. Since 2011, unemployment rates have seen a steady decrease reaching as low as 6.1% in July 2015 for the State and 7.0% for the MSA.

TRANSPORTATION

The Detroit‐Warren‐Dearborn area is served by Interstate 75, Interstate 94, Interstate 96, Interstate 275 and U.S. Highway 23.

Interstate 75 is the second longest north‐south highway from northwest of Miami, Florida to Sault Ste. Marie, Michigan and passes through the states of Florida, Georgia, Tennessee, Kentucky, Ohio, and Michigan. It enters Michigan near Lake Erie until Monroe where it continues northeastward to enter Detroit and its surrounding areas. The highway has intersections with other interstates including Interstate 375 (Chrysler Freeway), Interstate 94, Interstate 96, Michigan Highway 10 and Michigan Highway 8 (Davison Freeway). Other intersections within the state include Interstate 475, Interstate 69. After crossing the Detroit metropolitan area, the freeway reaches Pontiac, heads north towards Saginaw, travels north to Bay City before a major interchange with U.S. Route 127, and then crosses over to Mackinac Bridge continuing t the Canadian border in Sault Ste. Marie. Interstate 275 provides north south connectivity, connecting the cities of Carleton, Romulus, Livonia and Farmington Hills, and the counties of Monroe and Wayne. U.S. Highway 23 runs from Jacksonville, Florida to Mackinaw City, Michigan. In Michigan, it is a major north–south state trunk line highway that runs through the Lower Peninsula serving as a freeway bypass to the west of Metro Detroit and a scenic highway through the northern portion of the state along Lake Huron. It runs concurrently with Interstate 75 from Flint to Bay City.

Interstate 94 is an east–west highway from Billing, Montana to Port Huron, Michigan. The highway connects Interstate 90 to the west providing connectivity to the cities of Butte and Seattle in Washington. The highway connects the states of Montana, North Dakota, Minnesota, Wisconsin, Illinois, Indiana and Michigan. In Michigan, Interstate 94 runs north along Lake Michigan to St. Joseph before heading east toward Detroit. The highway serves as a connecting link to major cities including Madison in Wisconsin, Chicago in Illinois, and Fargo in North Dakota.

Interstate 96 runs east‐west through traverses the state of Michigan and serves to connect the cities of Grand Rapids, Brighton, Lancing and Detroit.

Air Transportation is provided by Detroit Metropolitan Wayne County Airport, the busiest airport in Michigan is served by 13 passenger airlines connecting the region to 180 destinations through its non‐stop services. The airport provides connectivity to domestic and international destinations. The airport handled 32,513,555 passengers in 2014. The airport transported air cargo of 202,066 tons in 2014. Detroit Metropolitan Wayne County Airport is a hub for Delta Air Lines and Spirit Airlines. Other airports serving the area are Ann Arbor Municipal Airport (ARB), Oakland County International Airport (PTK) and Willow Run Airport (YIP).

THE REGION

20

Rail Transportation to the region is provided by Amtrak through its Wolverine service between Chicago, Illinois, and Pontiac.

Water transportation is provided by Port of Detroit. The Port of Detroit is located along the west side of the Detroit River, and is the largest seaport in the state of Michigan. The port consists of multiple marine terminals handling general, liquid, and bulk cargo as well as passengers.

CONCLUSION

In summary, the economic base of the Detroit Metro Region is concentrated in a variety of industries, but primarily automotive manufacturing. Other strong sectors include government, healthcare, and education. The community and overall state have decreasing unemployment and Detroit specifically has a rapidly expanding downtown employment base. Commercial development is being catalyzed by a multitude incentive programs including attractive corporate tax regulations, availability of state monies for start‐up companies and the rehabilitation of existing commercial properties.

THE NEIGHBORHOOD

21

THE NEIGHBORHOOD

Neighborhood Analysis: The objective analysis of observable and/or quantifiable data indicating discernible patterns of urban growth, structure, and change that may detract from or enhance property values. (The Dictionary of Real Estate Appraisal, 5th edition)

OVERVIEW

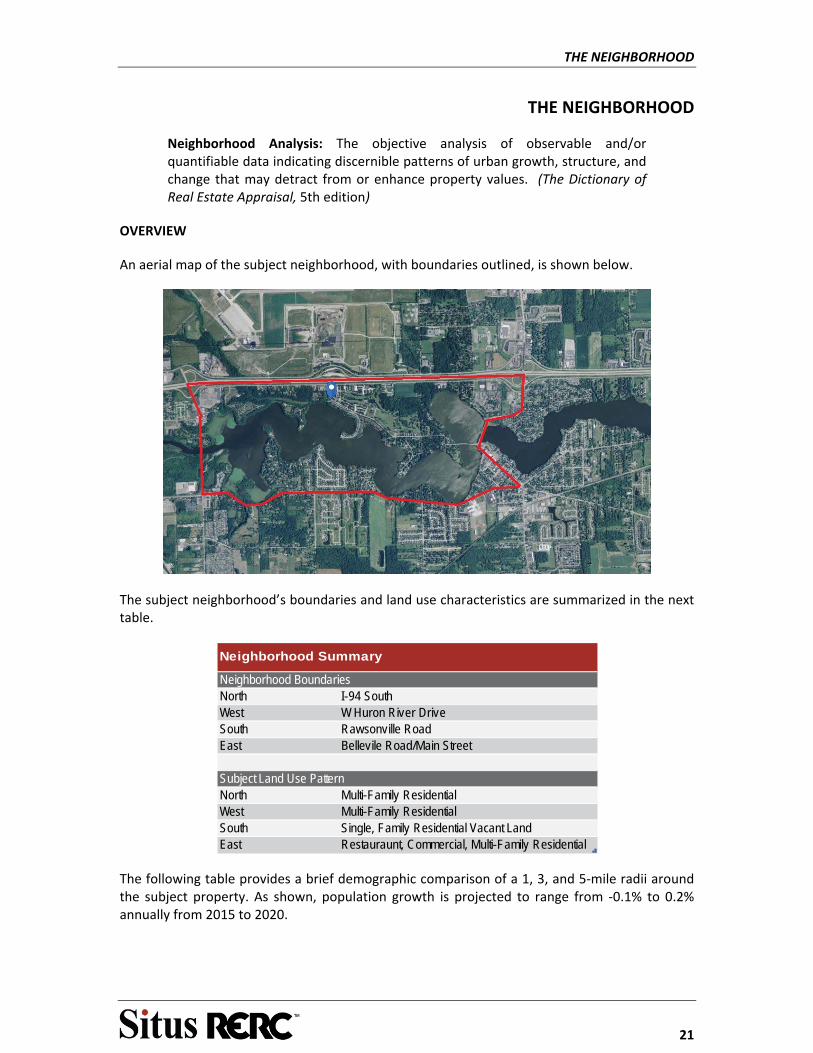

An aerial map of the subject neighborhood, with boundaries outlined, is shown below.

The subject neighborhood’s boundaries and land use characteristics are summarized in the next table.

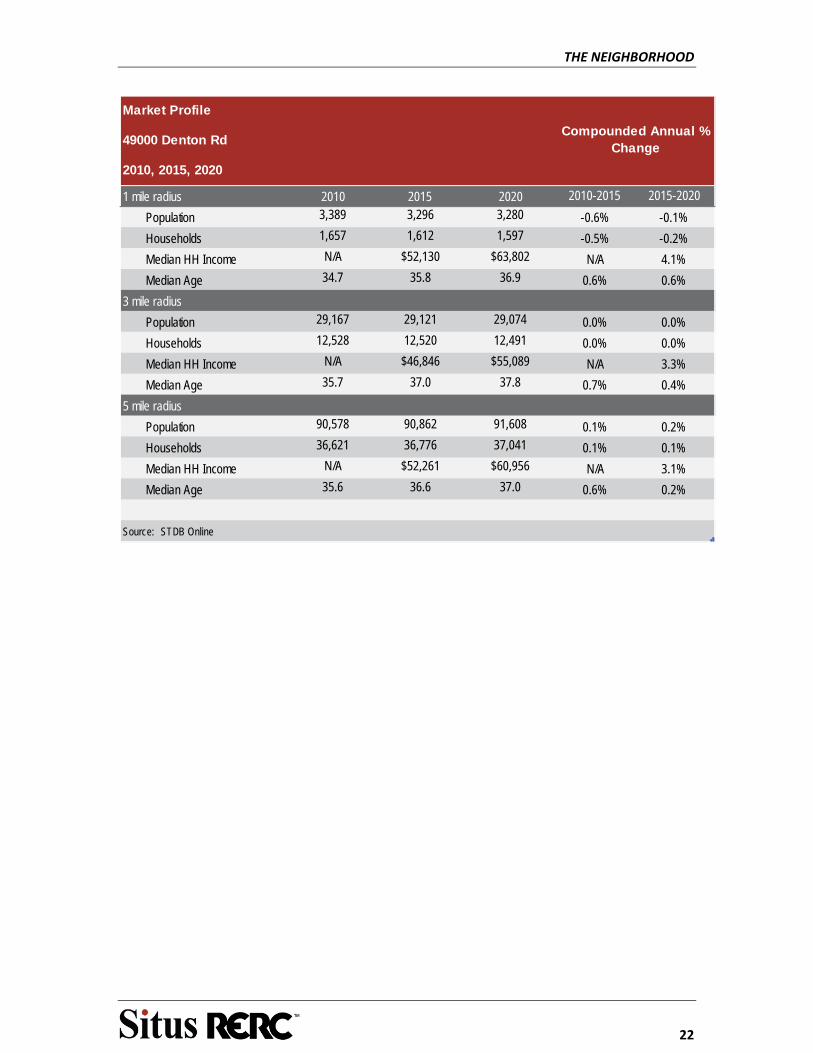

The following table provides a brief demographic comparison of a 1, 3, and 5‐mile radii around the subject property. As shown, population growth is projected to range from ‐0.1% to 0.2% annually from 2015 to 2020.

Neighborhood BoundariesNorth I-94 SouthWest W Huron River DriveSouth Rawsonville RoadEast Bellevile Road/Main Street

Subject Land Use PatternNorth Multi-Family ResidentialWest Multi-Family ResidentialSouth Single, Family Residential Vacant LandEast Restauraunt, Commercial, Multi-Family Residential

Neighborhood Summary

THE NEIGHBORHOOD

22

Market Profile

49000 Denton Rd

2010, 2015, 2020

1 mile radius 2010 2015 2020 2010-2015 2015-2020

Population 3,389 3,296 3,280 -0.6% -0.1%

Households 1,657 1,612 1,597 -0.5% -0.2%

Median HH Income N/A $52,130 $63,802 N/A 4.1%

Median Age 34.7 35.8 36.9 0.6% 0.6%

3 mile radius

Population 29,167 29,121 29,074 0.0% 0.0%

Households 12,528 12,520 12,491 0.0% 0.0%

Median HH Income N/A $46,846 $55,089 N/A 3.3%

Median Age 35.7 37.0 37.8 0.7% 0.4%

5 mile radius

Population 90,578 90,862 91,608 0.1% 0.2%

Households 36,621 36,776 37,041 0.1% 0.1%

Median HH Income N/A $52,261 $60,956 N/A 3.1%

Median Age 35.6 36.6 37.0 0.6% 0.2%

Source: STDB Online

Compounded Annual % Change

THE NEIGHBORHOOD

23

INCOME CHARACTERISTICS

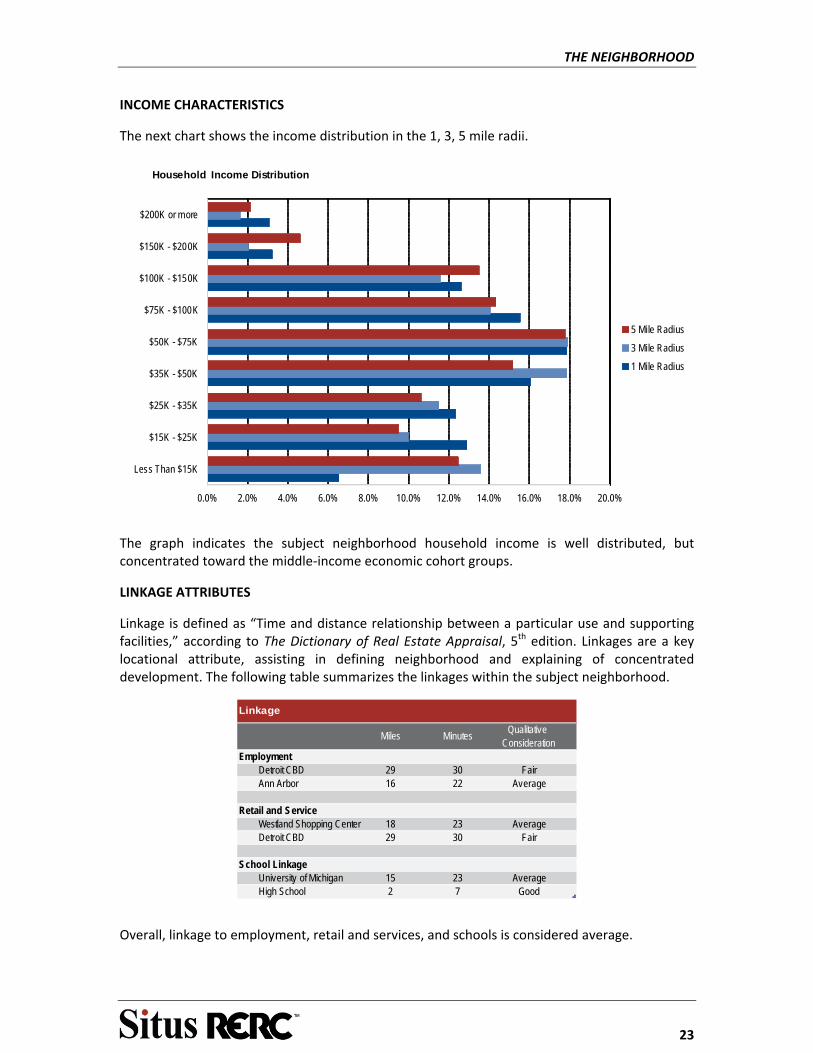

The next chart shows the income distribution in the 1, 3, 5 mile radii.

0.0% 2.0% 4.0% 6.0% 8.0% 10.0% 12.0% 14.0% 16.0% 18.0% 20.0%

Less Than $15K

$15K - $25K

$25K - $35K

$35K - $50K

$50K - $75K

$75K - $100K

$100K - $150K

$150K - $200K

$200K or more

Household Income Distribution

5 Mile Radius

3 Mile Radius

1 Mile Radius

The graph indicates the subject neighborhood household income is well distributed, but concentrated toward the middle‐income economic cohort groups.

LINKAGE ATTRIBUTES

Linkage is defined as “Time and distance relationship between a particular use and supporting facilities,” according to The Dictionary of Real Estate Appraisal, 5th edition. Linkages are a key locational attribute, assisting in defining neighborhood and explaining of concentrated development. The following table summarizes the linkages within the subject neighborhood.

Overall, linkage to employment, retail and services, and schools is considered average.

Miles MinutesQualitative

ConsiderationEmployment

Detroit CBD 29 30 FairAnn Arbor 16 22 Average

Retail and ServiceWestland Shopping Center 18 23 AverageDetroit CBD 29 30 Fair

School LinkageUniversity of Michigan 15 23 AverageHigh School 2 7 Good

Linkage

THE NEIGHBORHOOD

24

EDUCATION

Schools in the immediate area of the subject property include the Van Buren Public School District. The Van Buren Public School District is home to approximately 5,200 students. The University of Michigan is located approximately 15 miles away in Ann Arbor. Overall Linkage to schools is average for the neighborhood.

LAND USE AND DEVELOPMENT PATTERNS

The primary use of land in the neighborhood is multi and single‐family residential. Some portions of the western edge of the neighborhood with residential use as the community continue to expand. Retail and service uses are primarily concentrated along Belleville Road and Main Street along the eastern boundary of the neighborhood. Belleville High School is located along the southeastern boundary of the neighborhood.

The overall trend for the neighborhood is for expansion to the west with primarily residential development. Commercial uses will continue to locate along primary corridors to capitalize on the high traffic visibility. CONCLUSION

Development in the subject neighborhood is likely given the availability of vacant land. With the existing access to primary traffic artery the neighborhood should continue to maintain and attract business and households and remain stable for the mid to long‐term future.

THE PROPERTY

25

THE PROPERTY

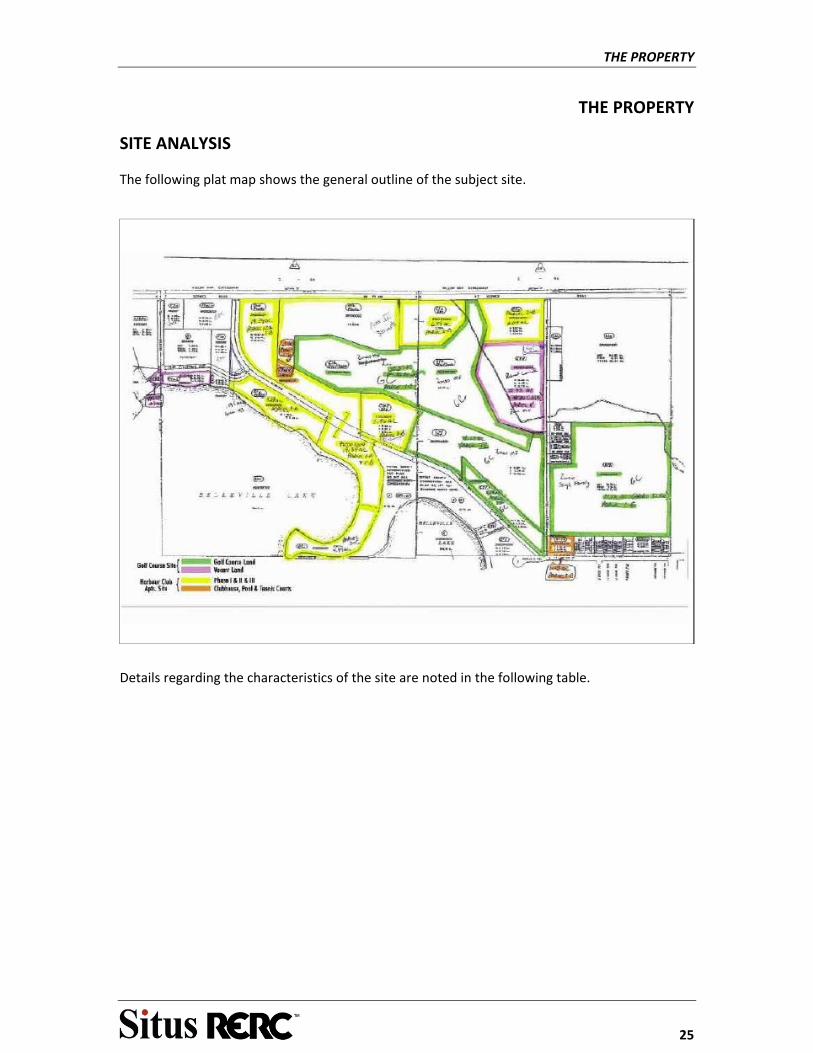

SITE ANALYSIS

The following plat map shows the general outline of the subject site.

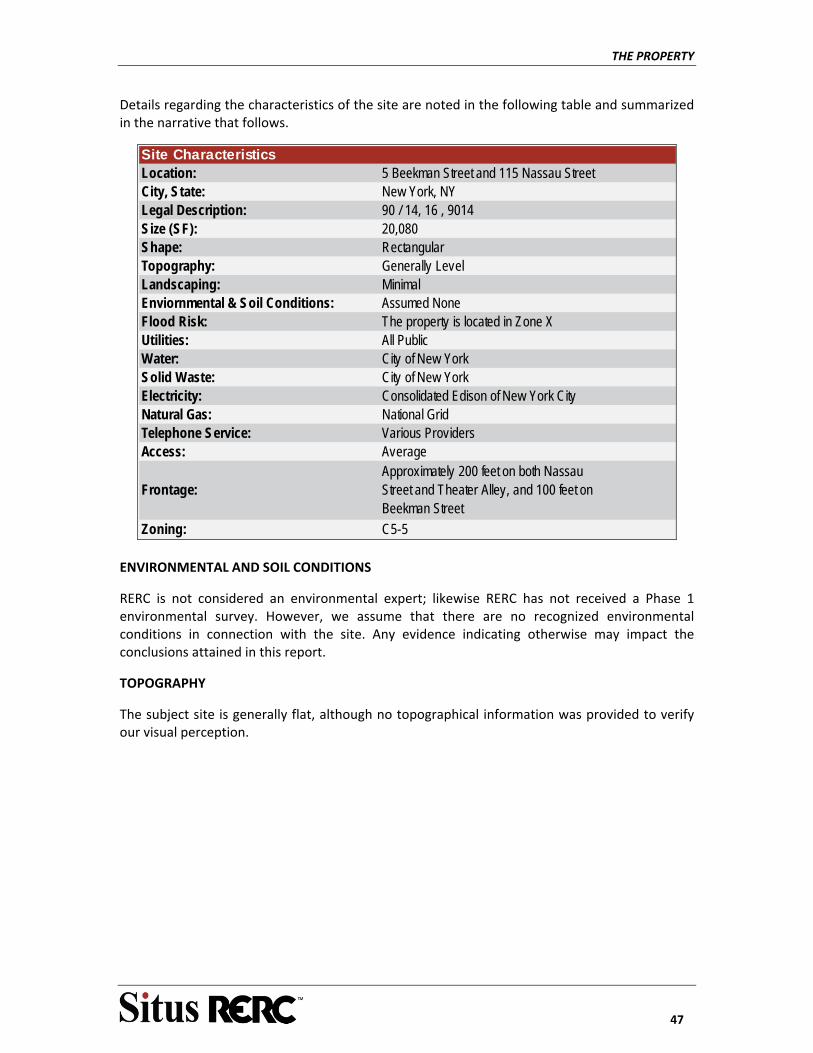

Details regarding the characteristics of the site are noted in the following table.

THE PROPERTY

26

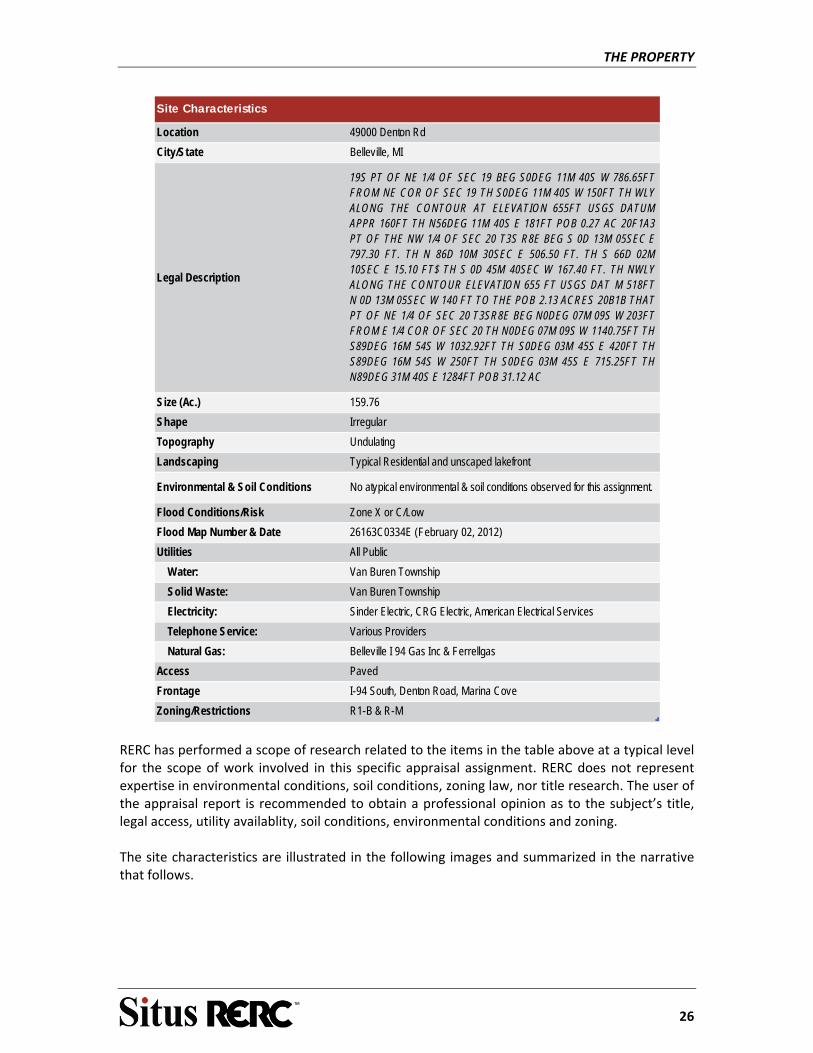

Location 49000 Denton Rd

City/State Belleville, MI

Legal Description

19S PT OF NE 1/4 OF SEC 19 BEG S0DEG 11M 40S W 786.65FTFROM NE COR OF SEC 19 TH S0DEG 11M 40S W 150FT TH WLYALONG THE CONTOUR AT ELEVATION 655FT USGS DATUMAPPR 160FT TH N56DEG 11M 40S E 181FT POB 0.27 AC 20F1A3PT OF THE NW 1/4 OF SEC 20 T3S R8E BEG S 0D 13M 05SEC E797.30 FT. TH N 86D 10M 30SEC E 506.50 FT. TH S 66D 02M10SEC E 15.10 FT$ TH S 0D 45M 40SEC W 167.40 FT. TH NWLYALONG THE CONTOUR ELEVATION 655 FT USGS DAT M 518FTN 0D 13M 05SEC W 140 FT TO THE POB 2.13 ACRES 20B1B THATPT OF NE 1/4 OF SEC 20 T3SR8E BEG N0DEG 07M 09S W 203FTFROM E 1/4 COR OF SEC 20 TH N0DEG 07M 09S W 1140.75FT THS89DEG 16M 54S W 1032.92FT TH S0DEG 03M 45S E 420FT THS89DEG 16M 54S W 250FT TH S0DEG 03M 45S E 715.25FT THN89DEG 31M 40S E 1284FT POB 31.12 AC

Size (Ac.) 159.76

Shape Irregular

Topography Undulating

Landscaping Typical Residential and unscaped lakefront

Environmental & Soil Conditions No atypical environmental & soil conditions observed for this assignment.

Flood Conditions/Risk Zone X or C/Low

Flood Map Number & Date 26163C0334E (February 02, 2012)

Utilities All Public

Water: Van Buren Township

Solid Waste: Van Buren Township

Electricity: Sinder Electric, CRG Electric, American Electrical Services

Telephone Service: Various Providers

Natural Gas: Belleville I 94 Gas Inc & Ferrellgas

Access Paved

Frontage I-94 South, Denton Road, Marina Cove

Zoning/Restrictions R1-B & R-M

Site Characteristics

RERC has performed a scope of research related to the items in the table above at a typical level for the scope of work involved in this specific appraisal assignment. RERC does not represent expertise in environmental conditions, soil conditions, zoning law, nor title research. The user of the appraisal report is recommended to obtain a professional opinion as to the subject’s title, legal access, utility availablity, soil conditions, environmental conditions and zoning. The site characteristics are illustrated in the following images and summarized in the narrative that follows.

THE PROPERTY

27

FLOOD HAZARD

The subject’s flood hazard risk was noted in the site characteristics table and displayed on the following flood map.

THE PROPERTY

28

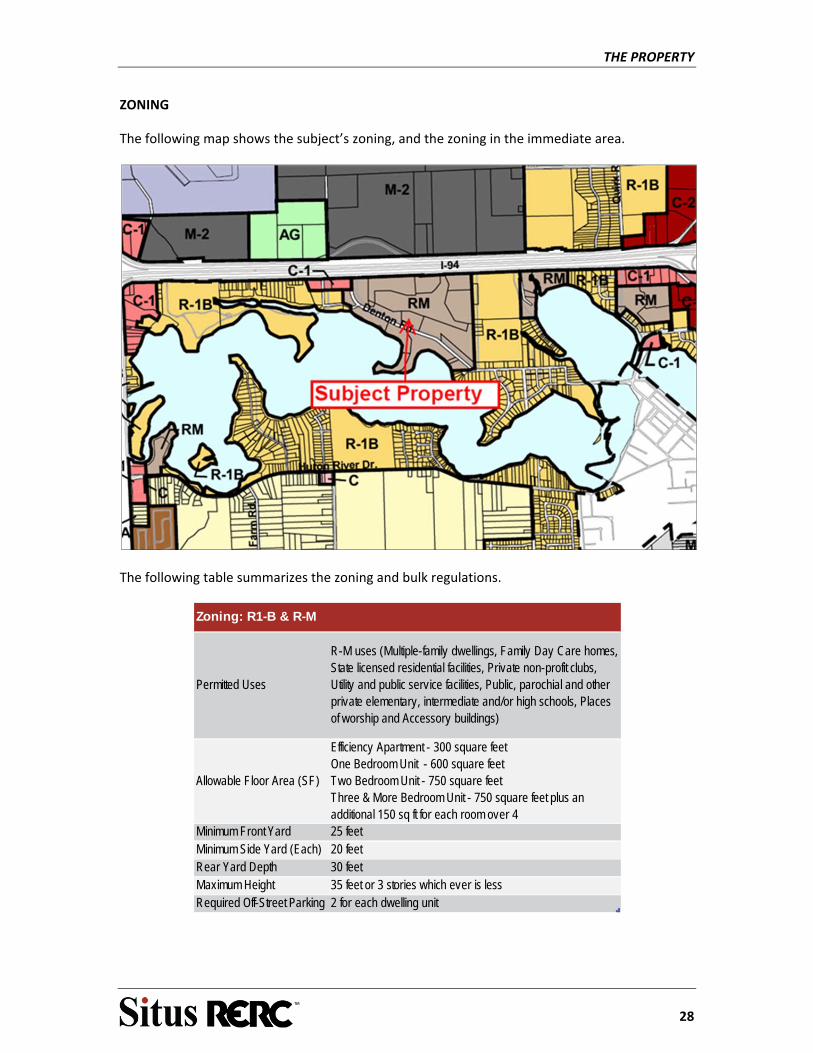

ZONING

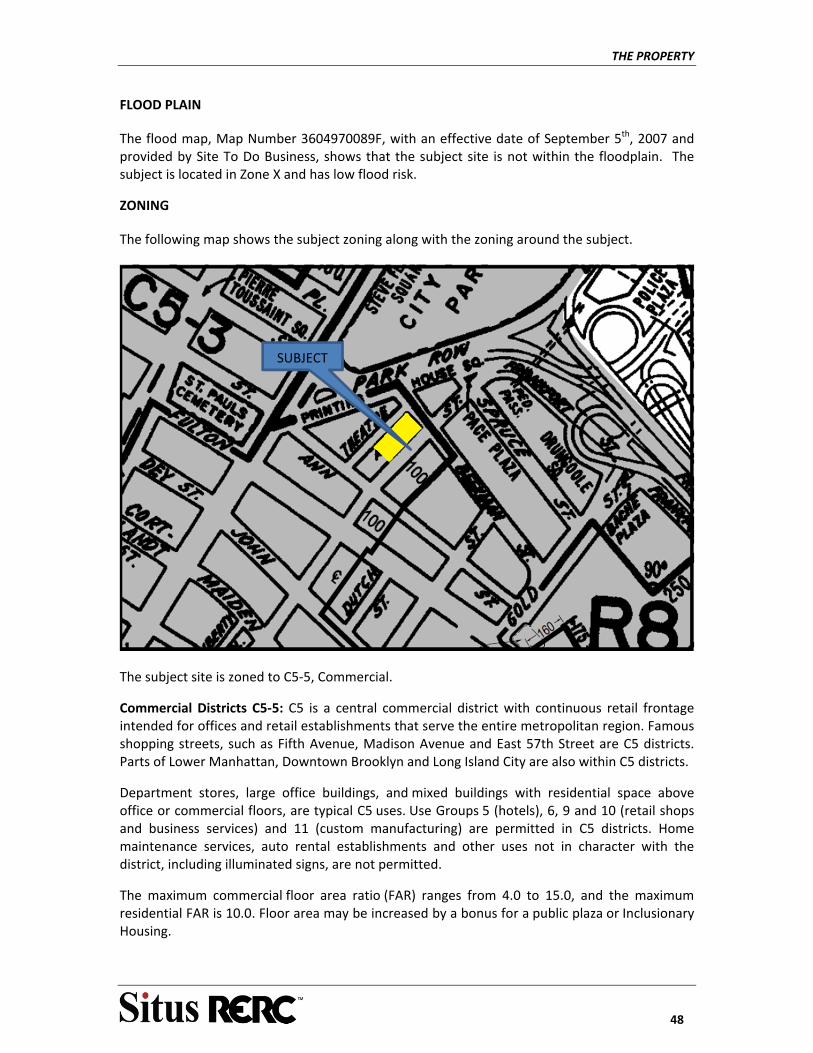

The following map shows the subject’s zoning, and the zoning in the immediate area.

The following table summarizes the zoning and bulk regulations.

Permitted Uses

R-M uses (Multiple-family dwellings, Family Day Care homes, State licensed residential facilities, Private non-profit clubs, Utility and public service facilities, Public, parochial and other private elementary, intermediate and/or high schools, Places of worship and Accessory buildings)

Allowable Floor Area (SF)

Efficiency Apartment - 300 square feetOne Bedroom Unit - 600 square feetTwo Bedroom Unit - 750 square feetThree & More Bedroom Unit - 750 square feet plus anadditional 150 sq ft for each room over 4

Minimum Front Yard 25 feetMinimum Side Yard (Each) 20 feetRear Yard Depth 30 feetMaximum Height 35 feet or 3 stories which ever is lessRequired Off-Street Parking 2 for each dwelling unit

Zoning: R1-B & R-M

THE PROPERTY

29

RERC is unaware of any deed restrictions impacting the subject. The subject appears to be a legal, non‐conforming use to the zoning ordinance as portions of the subject site are zoned for single‐family use, but are improved with apartments. Property management indicated that portions of the golf course land at the subject may be utilized as single‐family homes as portions of the subject’s golf course land were zoned to single‐family prior to the construction of the golf course.

ACCESS AND VISIBILITY

The site is situated along Denton Road, I‐94 Service Road and Marina Cove with adequate curb cuts from each road.

FUNCTIONAL UTILITY

For a multi‐family development parcel, the subject has typical utility. The size, shape, utility availability and access are typical for a property like the subject.

EASEMENTS

No atypical easements appear to exist based on our physical observation of the subject. A title report was not provided to confirm or identify atypical easements. The user of the appraisal report is recommended to obtain a professional opinion as to the subject’s title and potential restrictions or benefits of easement.

CONCLUSION ‐ SITE

The subject site is situated north of Lake Belleville along I‐94 Service Road, Denton Drive, and Marina Cove. The surrounding area is improved with single‐family residences, multi‐family residences, churches, schools, retail & service developments, and recreational facilities.

The size, shape, and topography of the site appear adequate to support multi‐family development. All of the required utilities are available to the site. The site and its characteristics appear to be adequate to support multi‐family use.

THE PROPERTY

30

IMPROVEMENT ANALYSIS

The following table summarizes the pertinent information on the subject improvements.

Property Attributes

Year Built 1970-1974

Number of Buildings 43

Number of Stories 3

Number of Units 1,112

Economic Class B

Construction Class D

Style Garden Apartment

Property Condition Average

Construction Quality Average

Gross Building Area 1,106,809

Occupancy 92%

Total Parking Spaces 2,248

Property Overview

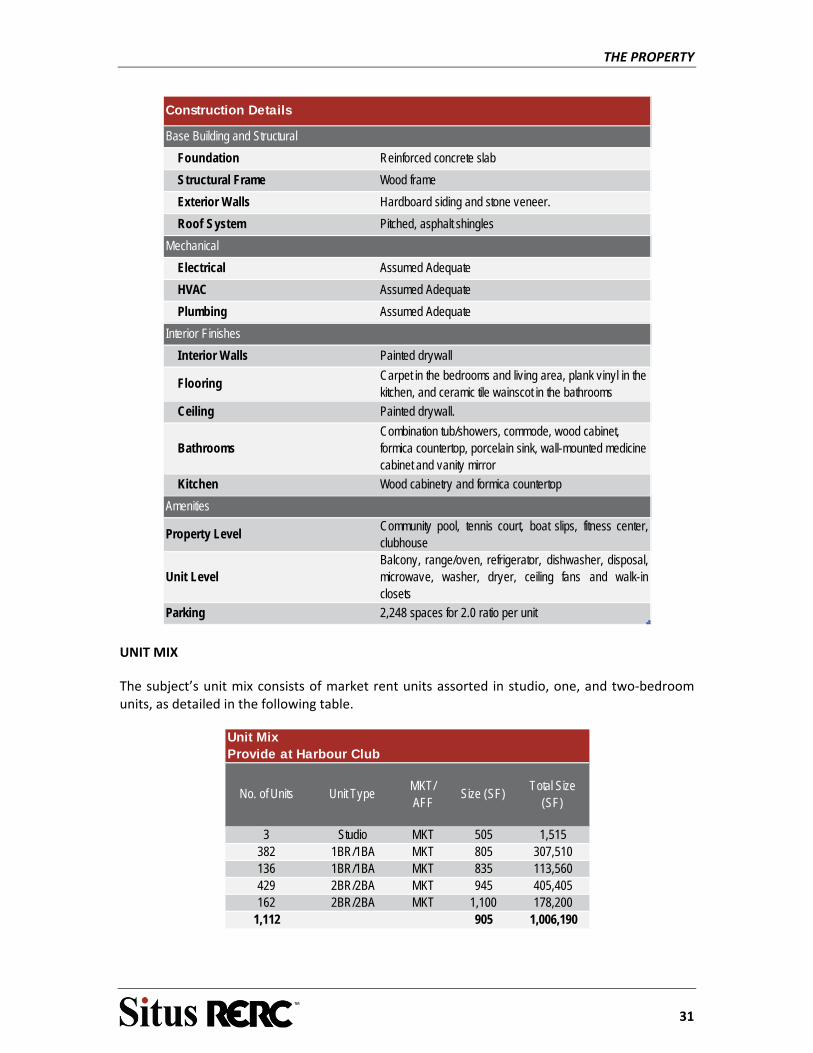

CONSTRUCTION DETAILS

Construction details for the improvements are noted as follows.

THE PROPERTY

31

Base Building and Structural

Foundation Reinforced concrete slab

Structural Frame Wood frame

Exterior Walls Hardboard siding and stone veneer.

Roof System Pitched, asphalt shingles

Mechanical

Electrical Assumed Adequate

HVAC Assumed Adequate

Plumbing Assumed Adequate

Interior Finishes

Interior Walls Painted drywall

FlooringCarpet in the bedrooms and living area, plank vinyl in the kitchen, and ceramic tile wainscot in the bathrooms

Ceiling Painted drywall.

BathroomsCombination tub/showers, commode, wood cabinet, formica countertop, porcelain sink, wall-mounted medicine cabinet and vanity mirror

Kitchen Wood cabinetry and formica countertop

Amenities

Property LevelCommunity pool, tennis court, boat slips, fitness center,clubhouse

Unit LevelBalcony, range/oven, refrigerator, dishwasher, disposal,microwave, washer, dryer, ceiling fans and walk-inclosets

Parking 2,248 spaces for 2.0 ratio per unit

Construction Details

UNIT MIX

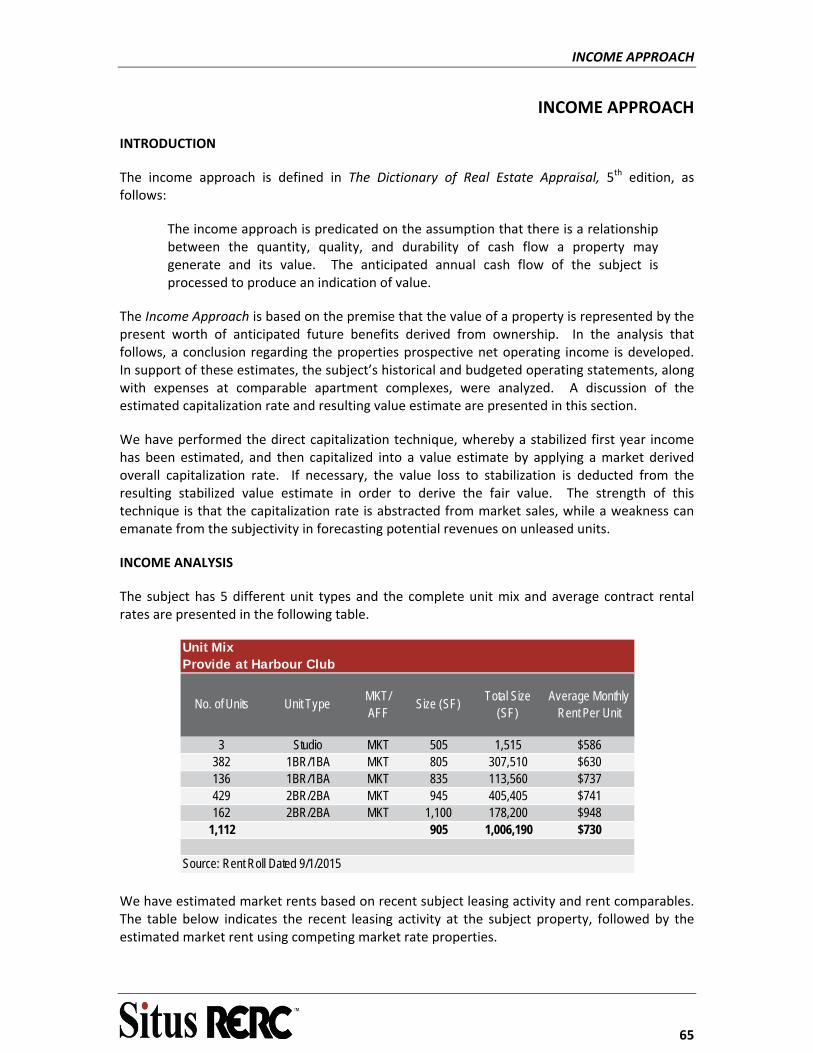

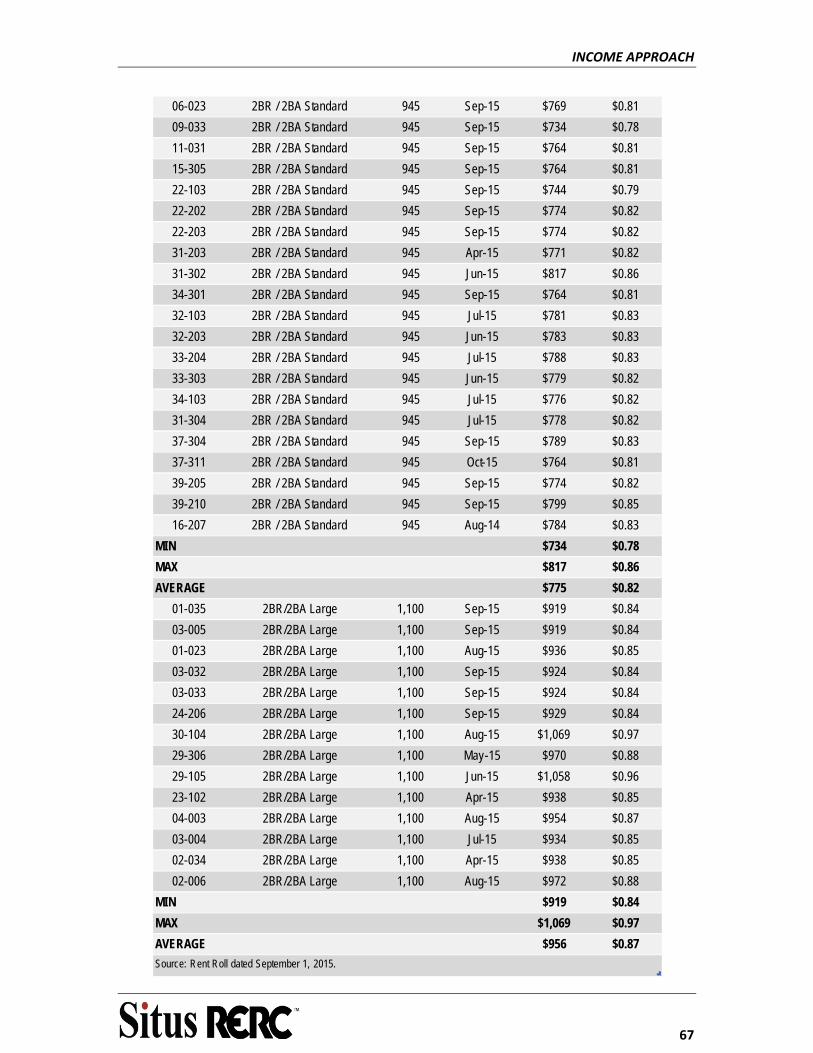

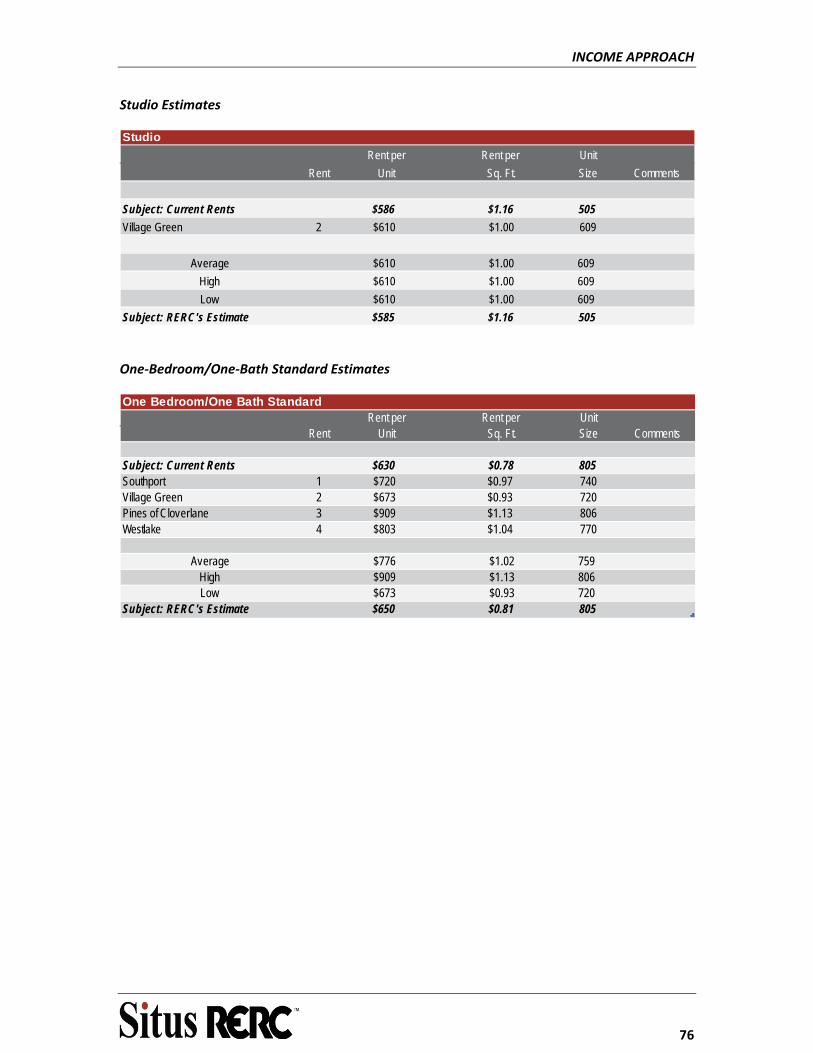

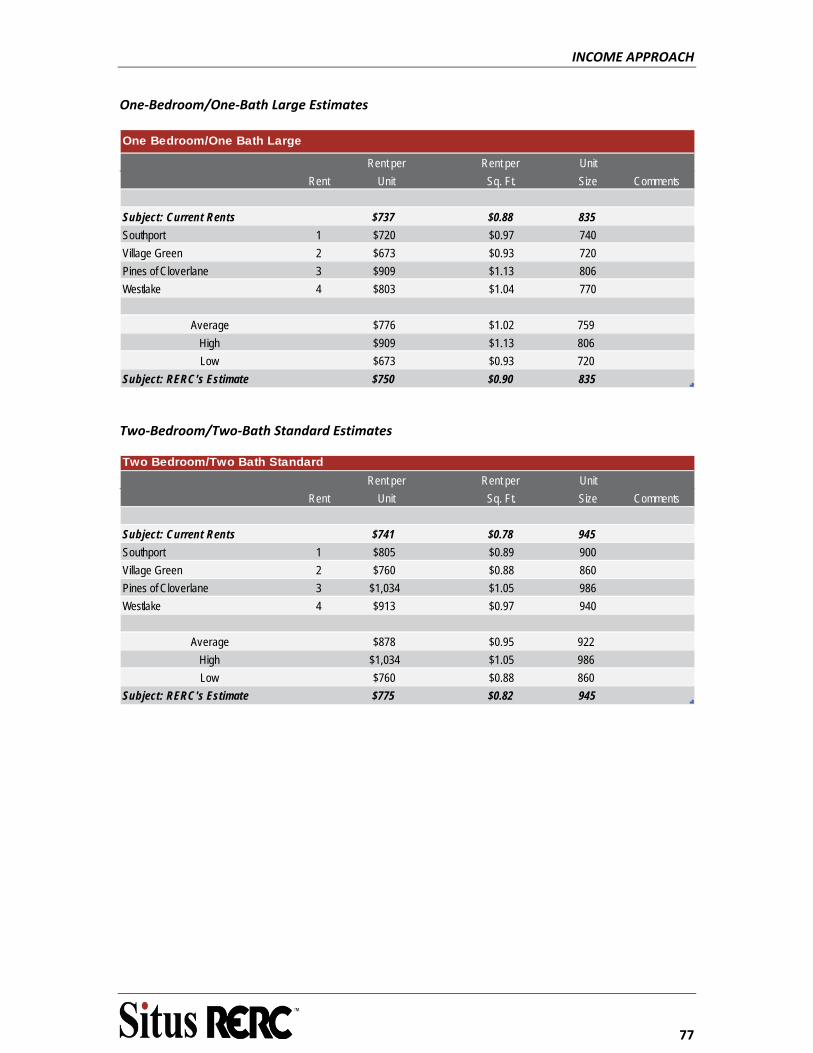

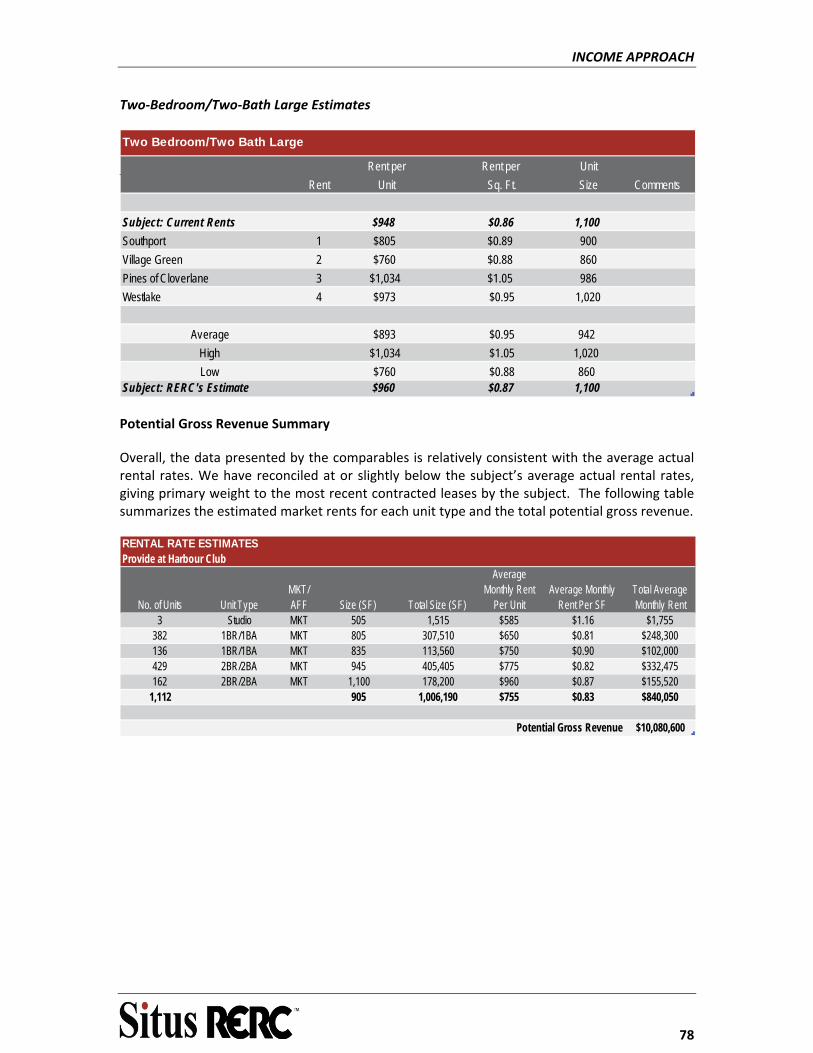

The subject’s unit mix consists of market rent units assorted in studio, one, and two‐bedroom units, as detailed in the following table.

Unit MixProvide at Harbour Club

No. of Units Unit TypeMKT/AFF

Size (SF)Total Size

(SF)

3 Studio MKT 505 1,515382 1BR/1BA MKT 805 307,510136 1BR/1BA MKT 835 113,560429 2BR/2BA MKT 945 405,405162 2BR/2BA MKT 1,100 178,200

1,112 905 1,006,190

THE PROPERTY

32

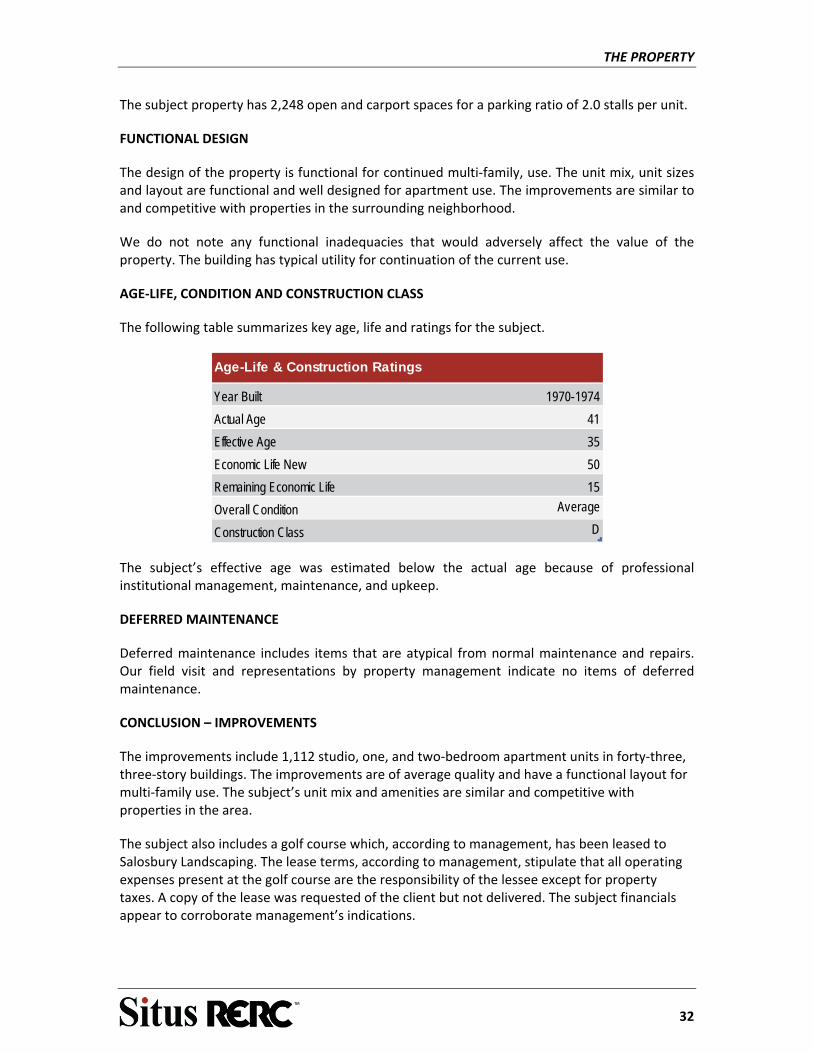

The subject property has 2,248 open and carport spaces for a parking ratio of 2.0 stalls per unit.

FUNCTIONAL DESIGN

The design of the property is functional for continued multi‐family, use. The unit mix, unit sizes and layout are functional and well designed for apartment use. The improvements are similar to and competitive with properties in the surrounding neighborhood.

We do not note any functional inadequacies that would adversely affect the value of the property. The building has typical utility for continuation of the current use.

AGE‐LIFE, CONDITION AND CONSTRUCTION CLASS

The following table summarizes key age, life and ratings for the subject.

Year Built 1970-1974

Actual Age 41

Effective Age 35

Economic Life New 50

Remaining Economic Life 15

Overall Condition Average

Construction Class D

Age-Life & Construction Ratings

The subject’s effective age was estimated below the actual age because of professional institutional management, maintenance, and upkeep.

DEFERRED MAINTENANCE

Deferred maintenance includes items that are atypical from normal maintenance and repairs. Our field visit and representations by property management indicate no items of deferred maintenance.

CONCLUSION – IMPROVEMENTS

The improvements include 1,112 studio, one, and two‐bedroom apartment units in forty‐three, three‐story buildings. The improvements are of average quality and have a functional layout for multi‐family use. The subject’s unit mix and amenities are similar and competitive with properties in the area.

The subject also includes a golf course which, according to management, has been leased to Salosbury Landscaping. The lease terms, according to management, stipulate that all operating expenses present at the golf course are the responsibility of the lessee except for property taxes. A copy of the lease was requested of the client but not delivered. The subject financials appear to corroborate management’s indications.

REAL ESTATE TAXES

33

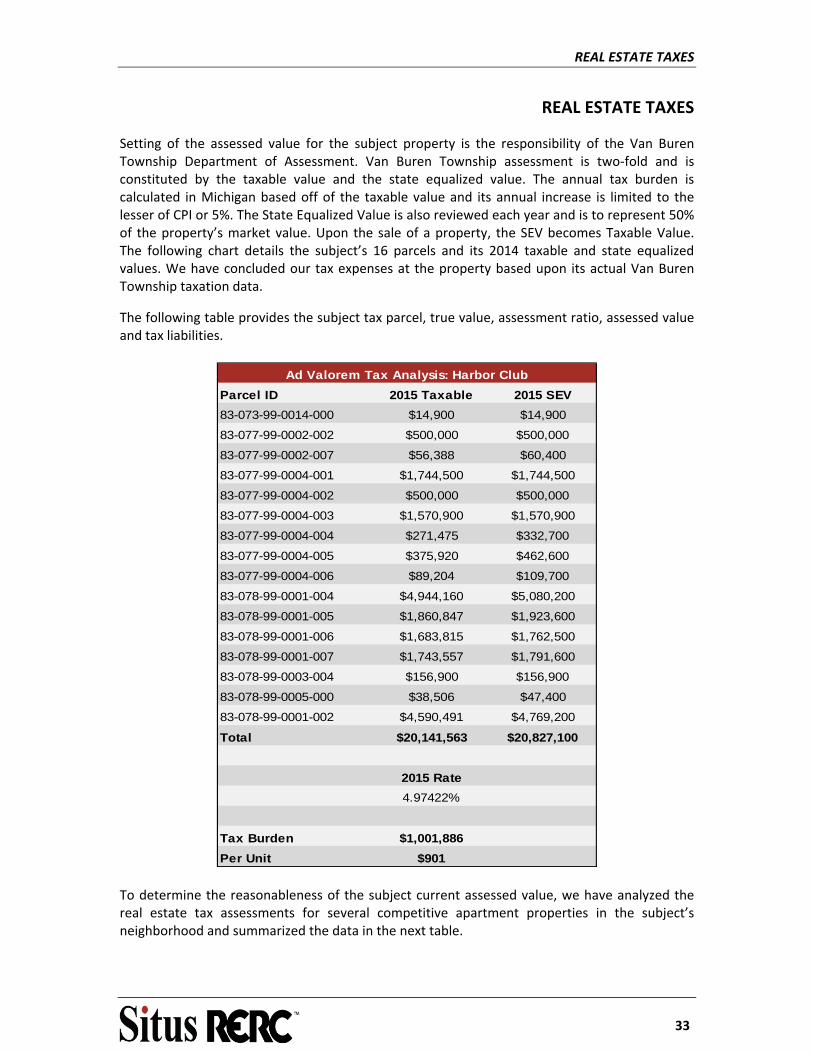

REAL ESTATE TAXES

Setting of the assessed value for the subject property is the responsibility of the Van Buren Township Department of Assessment. Van Buren Township assessment is two‐fold and is constituted by the taxable value and the state equalized value. The annual tax burden is calculated in Michigan based off of the taxable value and its annual increase is limited to the lesser of CPI or 5%. The State Equalized Value is also reviewed each year and is to represent 50% of the property’s market value. Upon the sale of a property, the SEV becomes Taxable Value. The following chart details the subject’s 16 parcels and its 2014 taxable and state equalized values. We have concluded our tax expenses at the property based upon its actual Van Buren Township taxation data.

The following table provides the subject tax parcel, true value, assessment ratio, assessed value and tax liabilities.

Parcel ID 2015 Taxable 2015 SEV

83-073-99-0014-000 $14,900 $14,900

83-077-99-0002-002 $500,000 $500,000

83-077-99-0002-007 $56,388 $60,400

83-077-99-0004-001 $1,744,500 $1,744,500

83-077-99-0004-002 $500,000 $500,000

83-077-99-0004-003 $1,570,900 $1,570,900

83-077-99-0004-004 $271,475 $332,700

83-077-99-0004-005 $375,920 $462,600

83-077-99-0004-006 $89,204 $109,700

83-078-99-0001-004 $4,944,160 $5,080,200

83-078-99-0001-005 $1,860,847 $1,923,600

83-078-99-0001-006 $1,683,815 $1,762,500

83-078-99-0001-007 $1,743,557 $1,791,600

83-078-99-0003-004 $156,900 $156,900

83-078-99-0005-000 $38,506 $47,400

83-078-99-0001-002 $4,590,491 $4,769,200

Total $20,141,563 $20,827,100

2015 Rate

4.97422%

Tax Burden $1,001,886

Per Unit $901

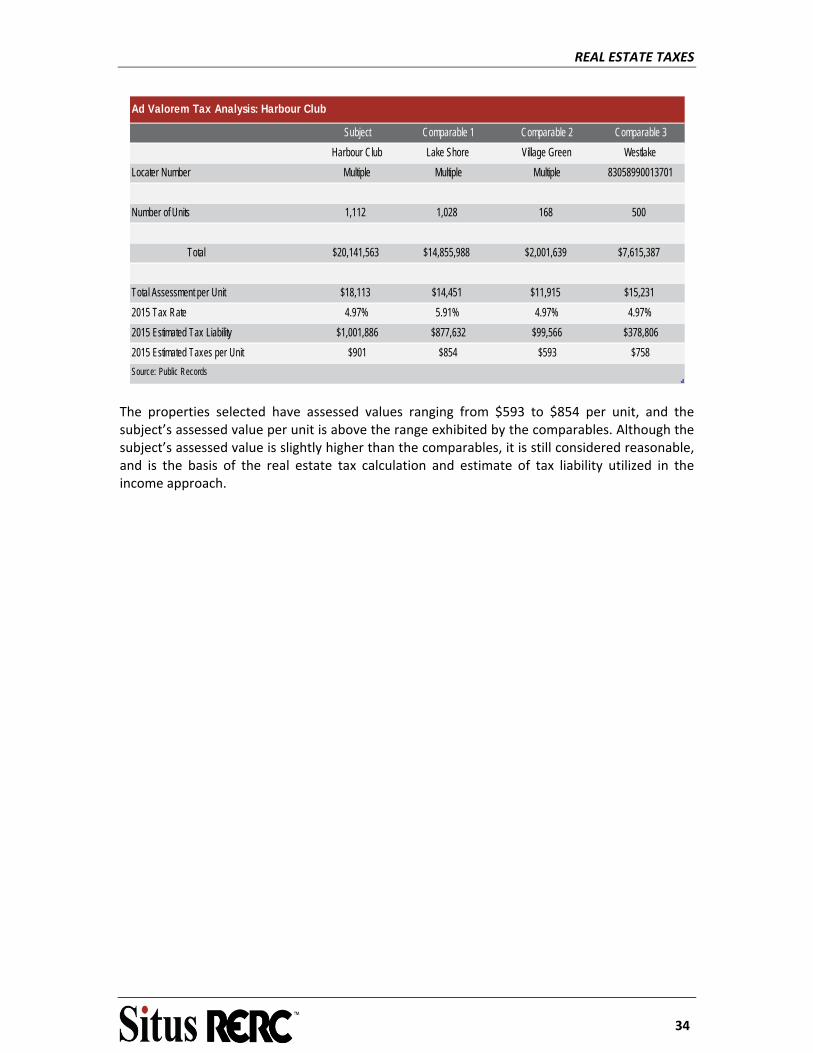

Ad Valorem Tax Analysis: Harbor Club

To determine the reasonableness of the subject current assessed value, we have analyzed the real estate tax assessments for several competitive apartment properties in the subject’s neighborhood and summarized the data in the next table.

REAL ESTATE TAXES

34

Subject Comparable 1 Comparable 2 Comparable 3

Harbour Club Lake Shore Village Green Westlake

Locater Number Multiple Multiple Multiple 83058990013701

Number of Units 1,112 1,028 168 500

Total $20,141,563 $14,855,988 $2,001,639 $7,615,387

Total Assessment per Unit $18,113 $14,451 $11,915 $15,231

2015 Tax Rate 4.97% 5.91% 4.97% 4.97%

2015 Estimated Tax Liability $1,001,886 $877,632 $99,566 $378,806

2015 Estimated Taxes per Unit $901 $854 $593 $758

Source: Public Records

Ad Valorem Tax Analysis: Harbour Club

The properties selected have assessed values ranging from $593 to $854 per unit, and the subject’s assessed value per unit is above the range exhibited by the comparables. Although the subject’s assessed value is slightly higher than the comparables, it is still considered reasonable, and is the basis of the real estate tax calculation and estimate of tax liability utilized in the income approach.

NATIONAL APARTMENT MARKET ANALYSIS

35

NATIONAL APARTMENT MARKET ANALYSIS

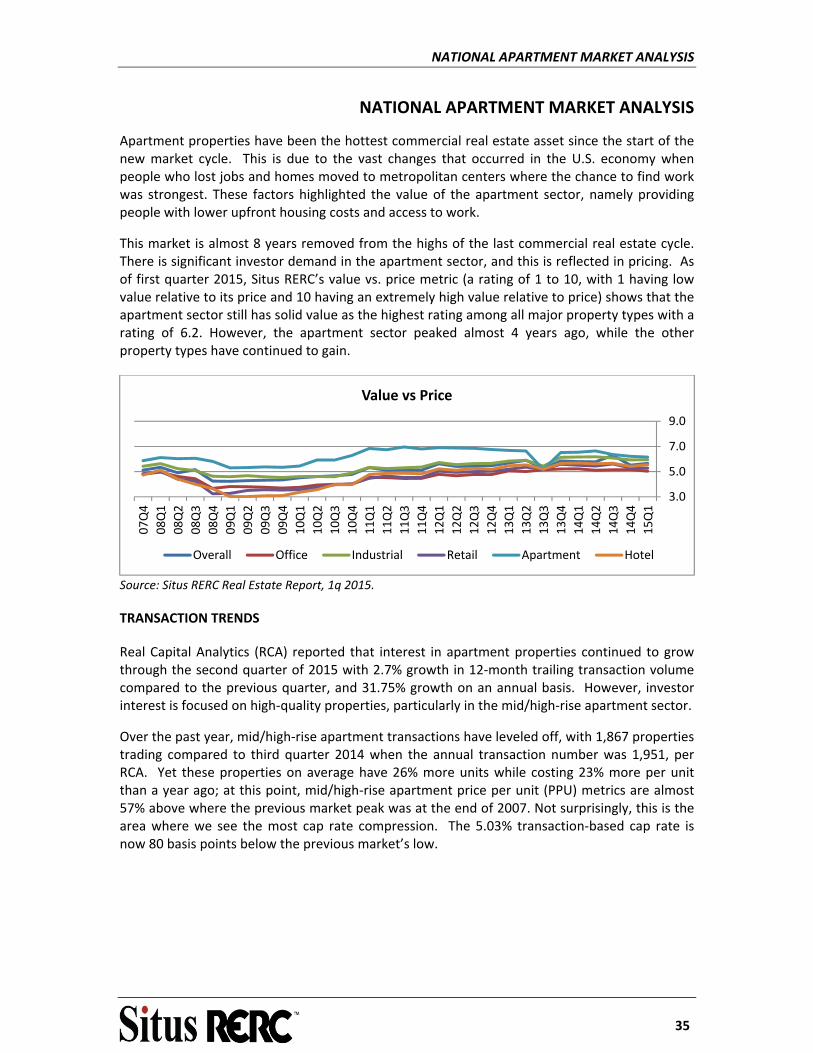

Apartment properties have been the hottest commercial real estate asset since the start of the new market cycle. This is due to the vast changes that occurred in the U.S. economy when people who lost jobs and homes moved to metropolitan centers where the chance to find work was strongest. These factors highlighted the value of the apartment sector, namely providing people with lower upfront housing costs and access to work.

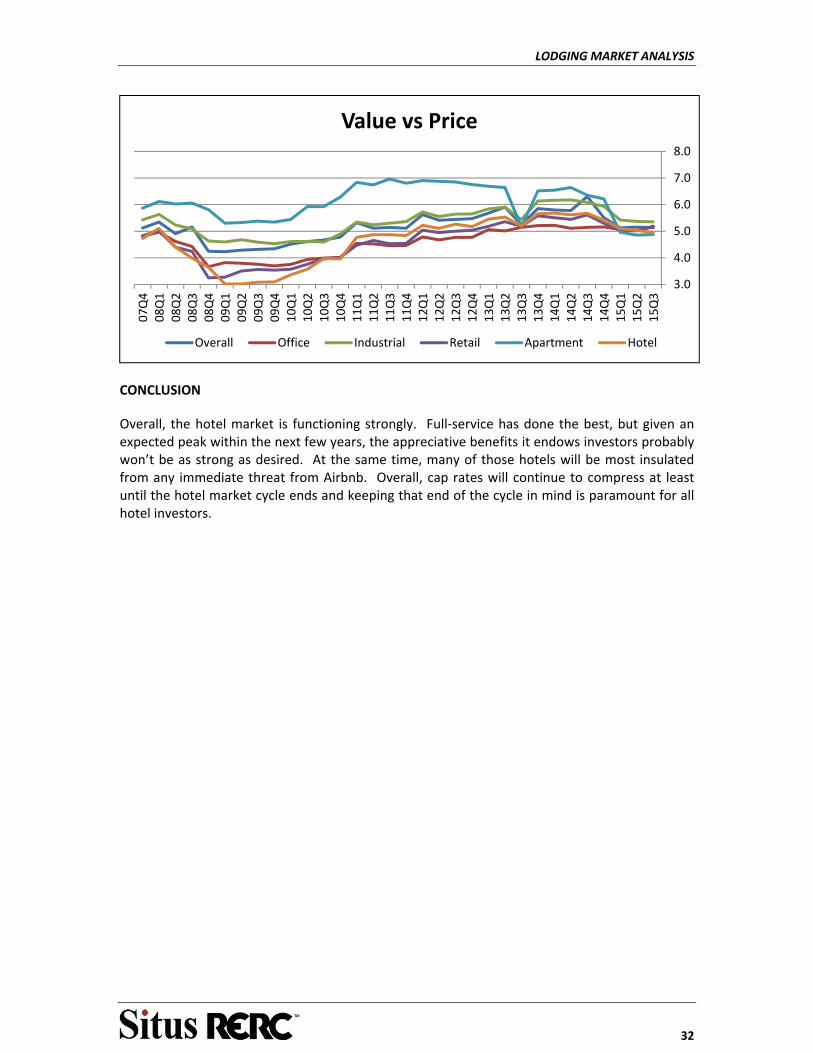

This market is almost 8 years removed from the highs of the last commercial real estate cycle. There is significant investor demand in the apartment sector, and this is reflected in pricing. As of first quarter 2015, Situs RERC’s value vs. price metric (a rating of 1 to 10, with 1 having low value relative to its price and 10 having an extremely high value relative to price) shows that the apartment sector still has solid value as the highest rating among all major property types with a rating of 6.2. However, the apartment sector peaked almost 4 years ago, while the other property types have continued to gain.

Source: Situs RERC Real Estate Report, 1q 2015.

TRANSACTION TRENDS

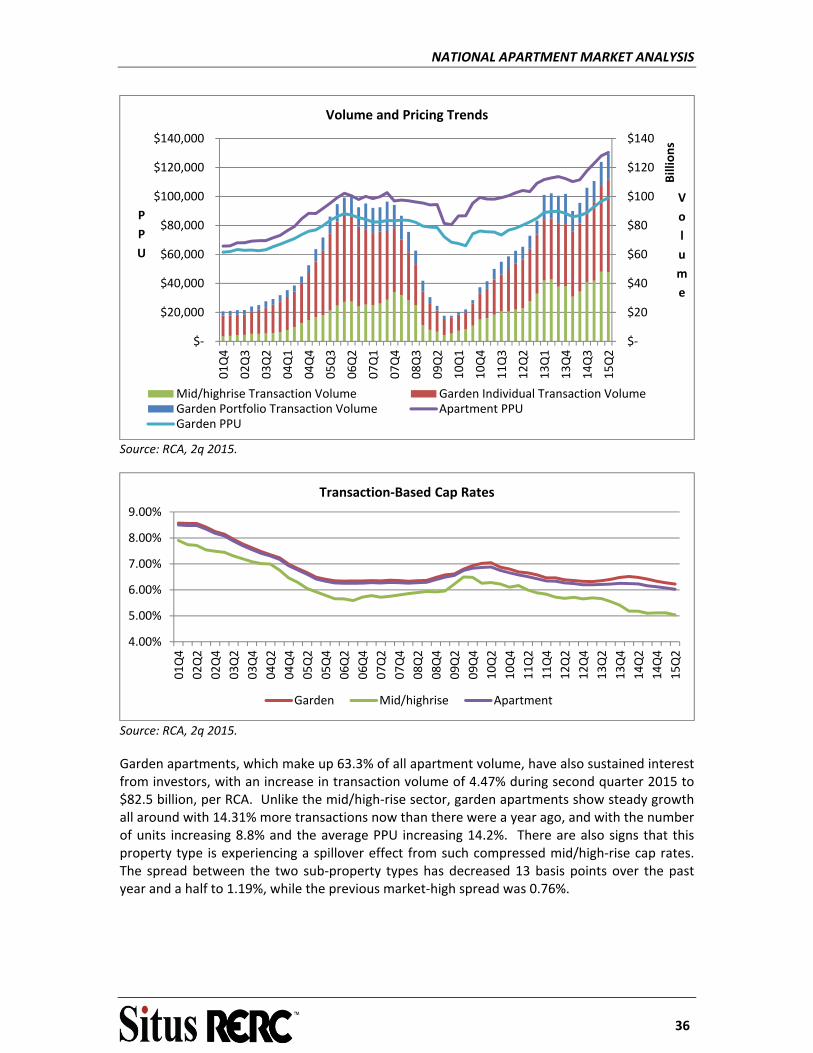

Real Capital Analytics (RCA) reported that interest in apartment properties continued to grow through the second quarter of 2015 with 2.7% growth in 12‐month trailing transaction volume compared to the previous quarter, and 31.75% growth on an annual basis. However, investor interest is focused on high‐quality properties, particularly in the mid/high‐rise apartment sector.

Over the past year, mid/high‐rise apartment transactions have leveled off, with 1,867 properties trading compared to third quarter 2014 when the annual transaction number was 1,951, per RCA. Yet these properties on average have 26% more units while costing 23% more per unit than a year ago; at this point, mid/high‐rise apartment price per unit (PPU) metrics are almost 57% above where the previous market peak was at the end of 2007. Not surprisingly, this is the area where we see the most cap rate compression. The 5.03% transaction‐based cap rate is now 80 basis points below the previous market’s low.

3.0

5.0

7.0

9.0

15Q1

14Q4

14Q3

14Q2

14Q1

13Q4

13Q3

13Q2

13Q1

12Q4

12Q3

12Q2

12Q1

11Q4

11Q3

11Q2

11Q1

10Q4

10Q3

10Q2

10Q1

09Q4

09Q3

09Q2

09Q1

08Q4

08Q3

08Q2

08Q1

07Q4

Value vs Price

Overall Office Industrial Retail Apartment Hotel

NATIONAL APARTMENT MARKET ANALYSIS

36

Source: RCA, 2q 2015.

Source: RCA, 2q 2015.

Garden apartments, which make up 63.3% of all apartment volume, have also sustained interest from investors, with an increase in transaction volume of 4.47% during second quarter 2015 to $82.5 billion, per RCA. Unlike the mid/high‐rise sector, garden apartments show steady growth all around with 14.31% more transactions now than there were a year ago, and with the number of units increasing 8.8% and the average PPU increasing 14.2%. There are also signs that this property type is experiencing a spillover effect from such compressed mid/high‐rise cap rates. The spread between the two sub‐property types has decreased 13 basis points over the past year and a half to 1.19%, while the previous market‐high spread was 0.76%.

$‐

$20

$40

$60

$80

$100

$120

$140

$‐

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

$140,000

01Q4

02Q3

03Q2

04Q1

04Q4

05Q3

06Q2

07Q1

07Q4

08Q3

09Q2

10Q1

10Q4

11Q3

12Q2

13Q1

13Q4

14Q3

15Q2

V

o

l

u

m

e

Billions

P

P

U

Volume and Pricing Trends

Mid/highrise Transaction Volume Garden Individual Transaction VolumeGarden Portfolio Transaction Volume Apartment PPUGarden PPU

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

01Q4

02Q2

02Q4

03Q2

03Q4

04Q2

04Q4

05Q2

05Q4

06Q2

06Q4

07Q2

07Q4

08Q2

08Q4

09Q2

09Q4

10Q2

10Q4

11Q2

11Q4

12Q2

12Q4

13Q2

13Q4

14Q2

14Q4

15Q2

Transaction‐Based Cap Rates

Garden Mid/highrise Apartment

NATIONAL APARTMENT MARKET ANALYSIS

37

Source: RCA, 2q 2015.

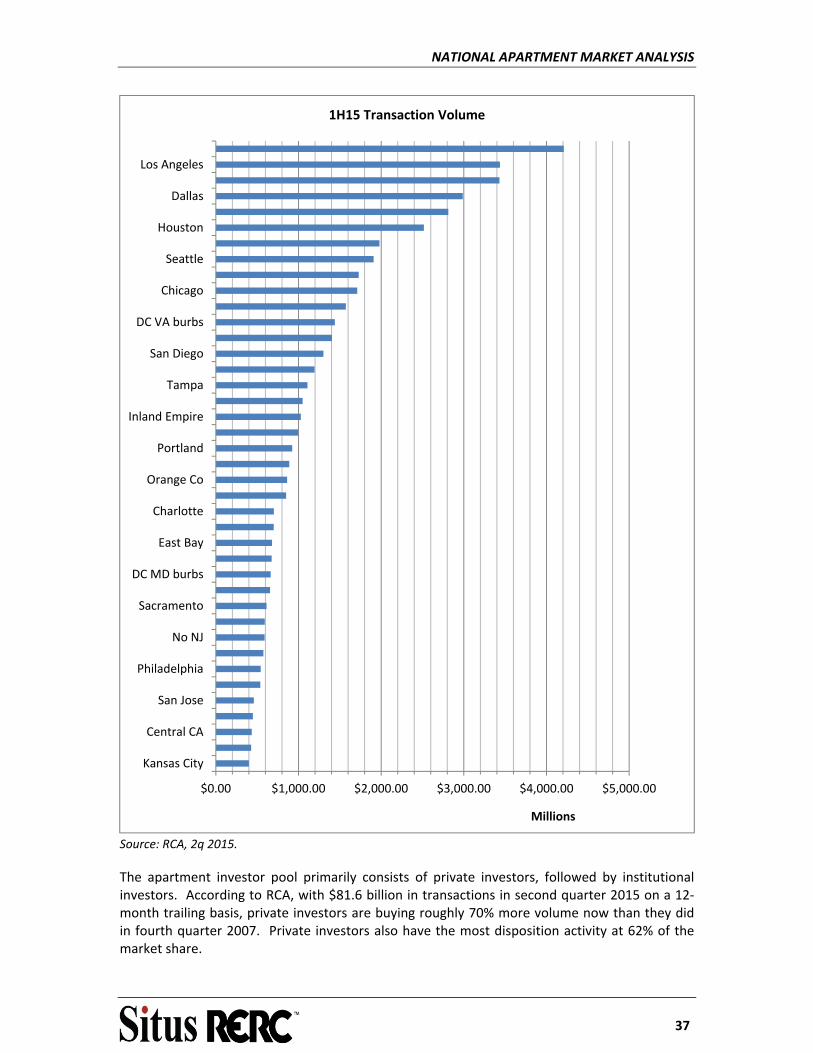

The apartment investor pool primarily consists of private investors, followed by institutional investors. According to RCA, with $81.6 billion in transactions in second quarter 2015 on a 12‐month trailing basis, private investors are buying roughly 70% more volume now than they did in fourth quarter 2007. Private investors also have the most disposition activity at 62% of the market share.

$0.00 $1,000.00 $2,000.00 $3,000.00 $4,000.00 $5,000.00

Kansas City

Central CA

San Jose

Philadelphia

No NJ

Sacramento

DC MD burbs

East Bay

Charlotte

Orange Co

Portland

Inland Empire

Tampa

San Diego

DC VA burbs

Chicago

Seattle

Houston

Dallas

Los Angeles

Millions

1H15 Transaction Volume

NATIONAL APARTMENT MARKET ANALYSIS

38

Source: RCA, 2q 2015.

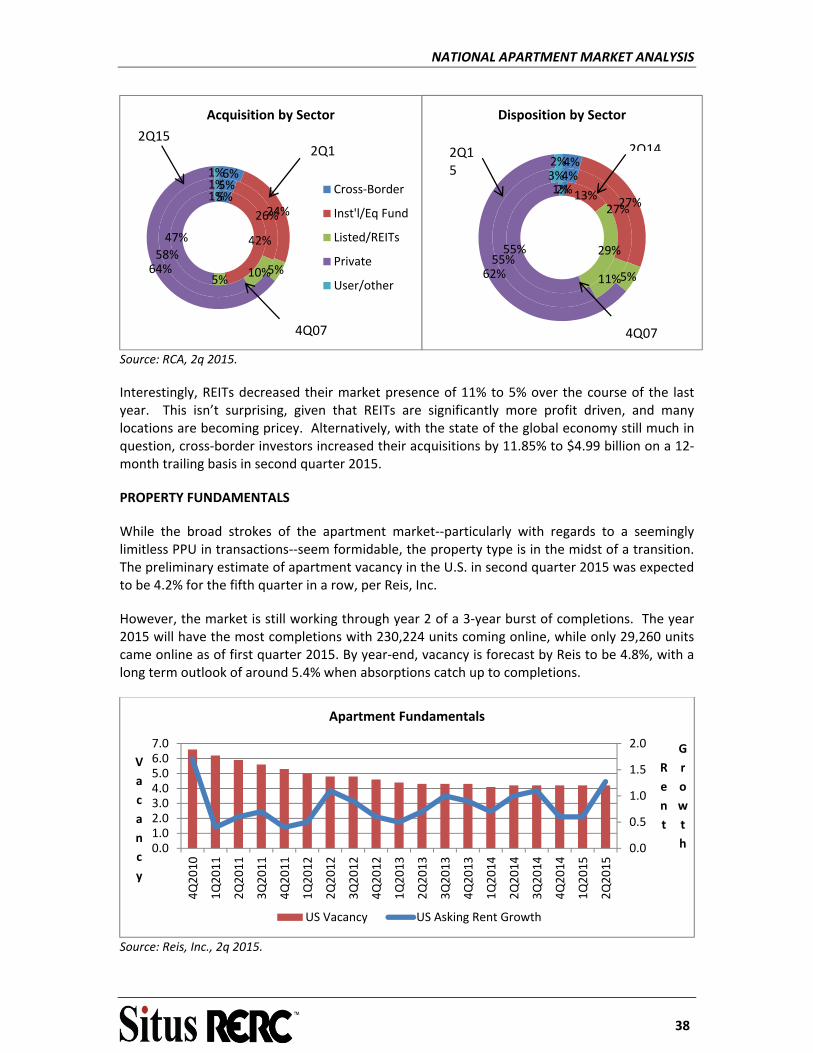

Interestingly, REITs decreased their market presence of 11% to 5% over the course of the last year. This isn’t surprising, given that REITs are significantly more profit driven, and many locations are becoming pricey. Alternatively, with the state of the global economy still much in question, cross‐border investors increased their acquisitions by 11.85% to $4.99 billion on a 12‐month trailing basis in second quarter 2015.

PROPERTY FUNDAMENTALS

While the broad strokes of the apartment market‐‐particularly with regards to a seemingly limitless PPU in transactions‐‐seem formidable, the property type is in the midst of a transition. The preliminary estimate of apartment vacancy in the U.S. in second quarter 2015 was expected to be 4.2% for the fifth quarter in a row, per Reis, Inc.

However, the market is still working through year 2 of a 3‐year burst of completions. The year 2015 will have the most completions with 230,224 units coming online, while only 29,260 units came online as of first quarter 2015. By year‐end, vacancy is forecast by Reis to be 4.8%, with a long term outlook of around 5.4% when absorptions catch up to completions.

Source: Reis, Inc., 2q 2015.

5%

42%

5%

47%

1%5%

26%

10%

58%

1%6%

24%

5%64%

1%

Acquisition by Sector

Cross‐Border

Inst'l/Eq Fund

Listed/REITs

Private

User/other

2Q12Q15

4Q07

0.0

0.5

1.0

1.5

2.0

0.01.02.03.04.05.06.07.0

4Q2010

1Q2011

2Q2011

3Q2011

4Q2011

1Q2012

2Q2012

3Q2012

4Q2012

1Q2013

2Q2013

3Q2013

4Q2013

1Q2014

2Q2014

3Q2014

4Q2014

1Q2015

2Q2015

R

e

n

t

G

r

o

w

t

h

V

a

c

a

n

c

y

Apartment Fundamentals

US Vacancy US Asking Rent Growth

2%13%

29%55%

1%4%

27%

11%

55%

3%4%

27%

5%62%

2%

Disposition by Sector

2Q142Q15

4Q07

NATIONAL APARTMENT MARKET ANALYSIS

39

Source: Reis, Inc., 2q 2015.

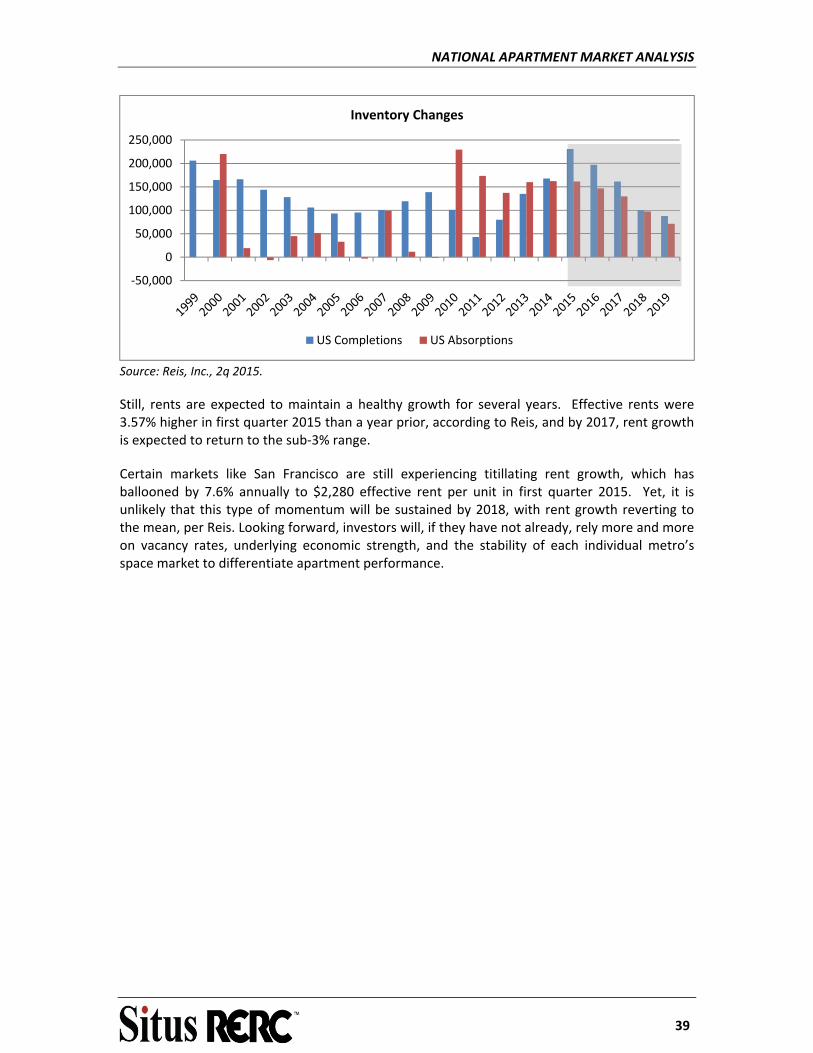

Still, rents are expected to maintain a healthy growth for several years. Effective rents were 3.57% higher in first quarter 2015 than a year prior, according to Reis, and by 2017, rent growth is expected to return to the sub‐3% range.

Certain markets like San Francisco are still experiencing titillating rent growth, which has ballooned by 7.6% annually to $2,280 effective rent per unit in first quarter 2015. Yet, it is unlikely that this type of momentum will be sustained by 2018, with rent growth reverting to the mean, per Reis. Looking forward, investors will, if they have not already, rely more and more on vacancy rates, underlying economic strength, and the stability of each individual metro’s space market to differentiate apartment performance.

‐50,000

0

50,000

100,000

150,000

200,000

250,000

Inventory Changes

US Completions US Absorptions

NATIONAL APARTMENT MARKET ANALYSIS

40

Source: Reis, Inc., 2q 2015.

2 4 6 8 10

Sacramento

San Diego

Hartford

Detroit

Cleveland

Minneapolis

Cincinnati

New York

Philadelphia

Los Angeles

Pittsburgh

Portland

Chicago

San Francisco

Miami

Baltimore

Salt Lake City

Newark

Richmond

St Louis

Kansas City

Seattle

Denver

Nashville

Phoenix

Boston

Tampa

Dallas

Columbus

Las Vegas

New Orleans

Atlanta

Charlotte

Orlando

Austin

San Antonio

Houston

Indianapolis

Washington DC

Raleigh

Memphis

Vacancy Rate Distribution

0.0% 5.0% 10.0%

San…

Denver

Seattle

Nashville

Houston

Miami

Dallas

Boston

Austin

Orlando

Raleigh

Phoenix

Portland

Atlanta

Charlotte

Salt Lake…

Las Vegas

Pittsburgh

Sacramento

Columbus

Minneapolis

St Louis

Kansas City

Cleveland

San Antonio

Philadelphia

Tampa

Baltimore

Cincinnati

Chicago

New York

Los Angeles

Indianapolis

Detroit

Memphis

Newark

San Diego

Richmond

Hartford

New Orleans

Washingto…

Rent Growth Distribution

1Q2015

2018

NATIONAL APARTMENT MARKET ANALYSIS

41

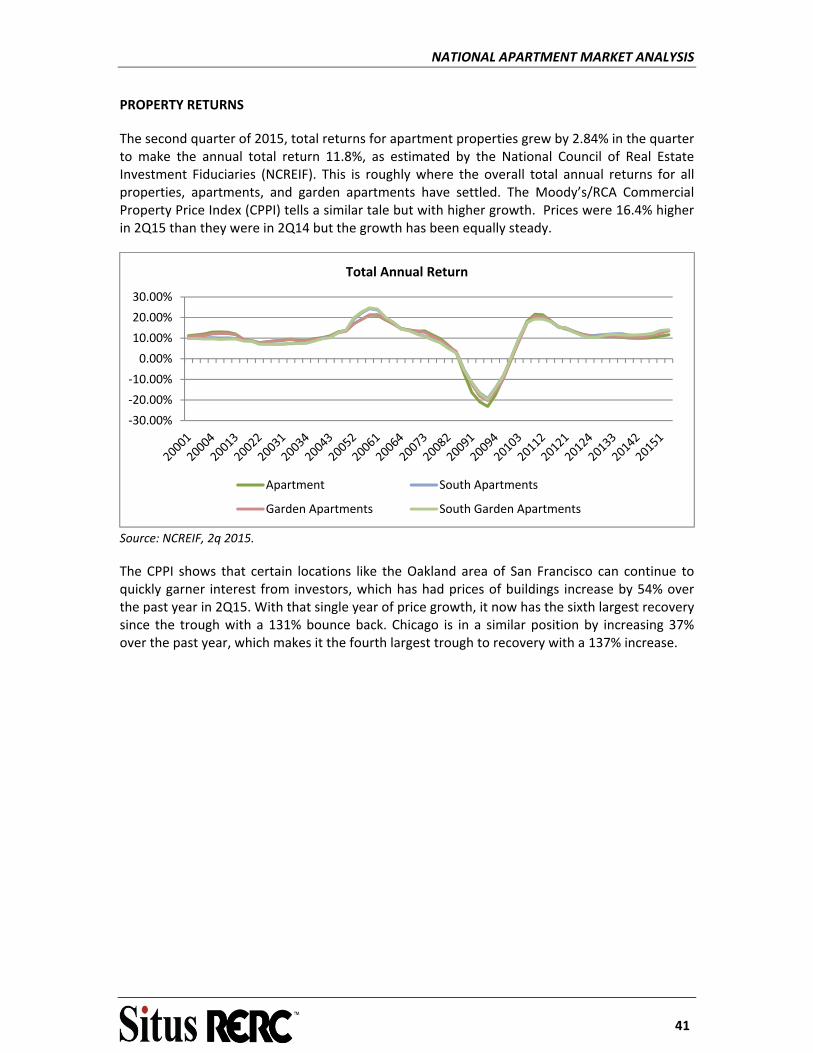

PROPERTY RETURNS

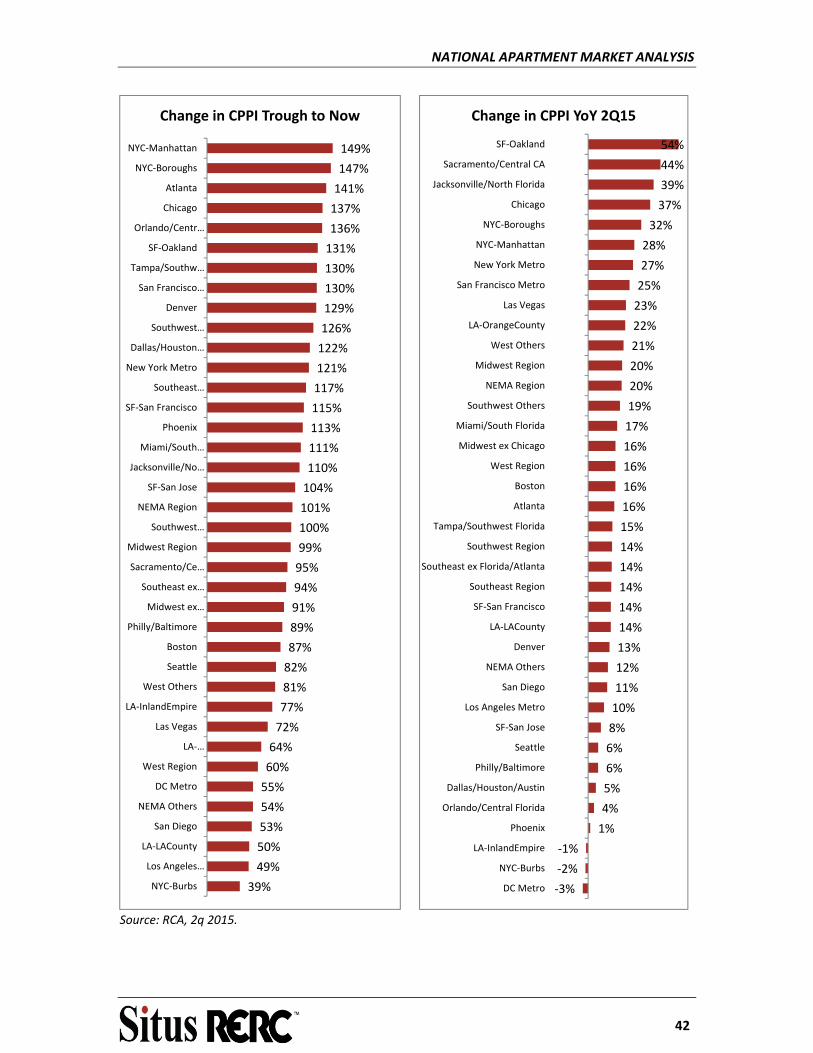

The second quarter of 2015, total returns for apartment properties grew by 2.84% in the quarter to make the annual total return 11.8%, as estimated by the National Council of Real Estate Investment Fiduciaries (NCREIF). This is roughly where the overall total annual returns for all properties, apartments, and garden apartments have settled. The Moody’s/RCA Commercial Property Price Index (CPPI) tells a similar tale but with higher growth. Prices were 16.4% higher in 2Q15 than they were in 2Q14 but the growth has been equally steady.

Source: NCREIF, 2q 2015.

The CPPI shows that certain locations like the Oakland area of San Francisco can continue to quickly garner interest from investors, which has had prices of buildings increase by 54% over the past year in 2Q15. With that single year of price growth, it now has the sixth largest recovery since the trough with a 131% bounce back. Chicago is in a similar position by increasing 37% over the past year, which makes it the fourth largest trough to recovery with a 137% increase.

‐30.00%

‐20.00%

‐10.00%

0.00%

10.00%

20.00%

30.00%

Total Annual Return

Apartment South Apartments

Garden Apartments South Garden Apartments

NATIONAL APARTMENT MARKET ANALYSIS

42

Source: RCA, 2q 2015.

149%

147%

141%

137%

136%

131%

130%

130%

129%

126%

122%

121%

117%

115%

113%

111%

110%

104%

101%

100%

99%

95%

94%

91%

89%

87%

82%

81%

77%

72%

64%

60%

55%

54%

53%

50%

49%

39%

NYC‐Manhattan

NYC‐Boroughs

Atlanta

Chicago

Orlando/Centr…

SF‐Oakland

Tampa/Southw…

San Francisco…

Denver

Southwest…

Dallas/Houston…

New York Metro

Southeast…

SF‐San Francisco

Phoenix

Miami/South…

Jacksonville/No…

SF‐San Jose

NEMA Region

Southwest…

Midwest Region

Sacramento/Ce…

Southeast ex…

Midwest ex…

Philly/Baltimore

Boston

Seattle

West Others

LA‐InlandEmpire

Las Vegas

LA‐…

West Region

DC Metro

NEMA Others

San Diego

LA‐LACounty

Los Angeles…

NYC‐Burbs

Change in CPPI Trough to Now

54%

44%

39%

37%

32%

28%

27%

25%

23%

22%

21%

20%

20%

19%

17%

16%

16%

16%

16%

15%

14%

14%

14%

14%

14%

13%

12%

11%

10%

8%

6%

6%

5%

4%

1%

‐1%

‐2%

‐3%

SF‐Oakland

Sacramento/Central CA

Jacksonville/North Florida

Chicago

NYC‐Boroughs

NYC‐Manhattan

New York Metro

San Francisco Metro

Las Vegas

LA‐OrangeCounty

West Others

Midwest Region

NEMA Region

Southwest Others

Miami/South Florida

Midwest ex Chicago

West Region

Boston

Atlanta

Tampa/Southwest Florida

Southwest Region

Southeast ex Florida/Atlanta

Southeast Region

SF‐San Francisco

LA‐LACounty

Denver

NEMA Others

San Diego

Los Angeles Metro

SF‐San Jose

Seattle

Philly/Baltimore

Dallas/Houston/Austin

Orlando/Central Florida

Phoenix

LA‐InlandEmpire

NYC‐Burbs

DC Metro

Change in CPPI YoY 2Q15

NATIONAL APARTMENT MARKET ANALYSIS

43

CONCLUSION

For investors, the current apartment market is still strong without a lot of weaknesses to suggest otherwise. And yet, there are hints that the underlying apartment market could be brittle. The apartment market may be unable to make a fluid transition while confronting hurdles such as extreme upward price pressures on top tier assets, the absorption of a burst of new apartment properties, improving outlook of other commercial real estate property types, or an increase in the Federal Funds Rate that could be larger than anticipated. The consequence of the latter will ultimately be an increased lending rate for commercial real estate making current compressed cap rates harder to justify. The apartment market is not devoid of opportunities or gems in the rough, but the boom this property type has experienced, in large part, may be over sooner than later.

APARTMENT MARKET ANALYSIS

44

APARTMENT MARKET ANALYSIS

This Detroit macro market overview is followed by an overview of the subject's immediate micro market, Westland. Data presented herein has been sourced from REIS and Site To Do Business Online. REIS do not make projections for individual property classes.

State Michigan

MSADetroit-Warren-Dearborn, MI Metro Area

County Wayne County

City Belleville

Reis Macro Market Detroit

Reis Micro Market Westland

Market Segmentation

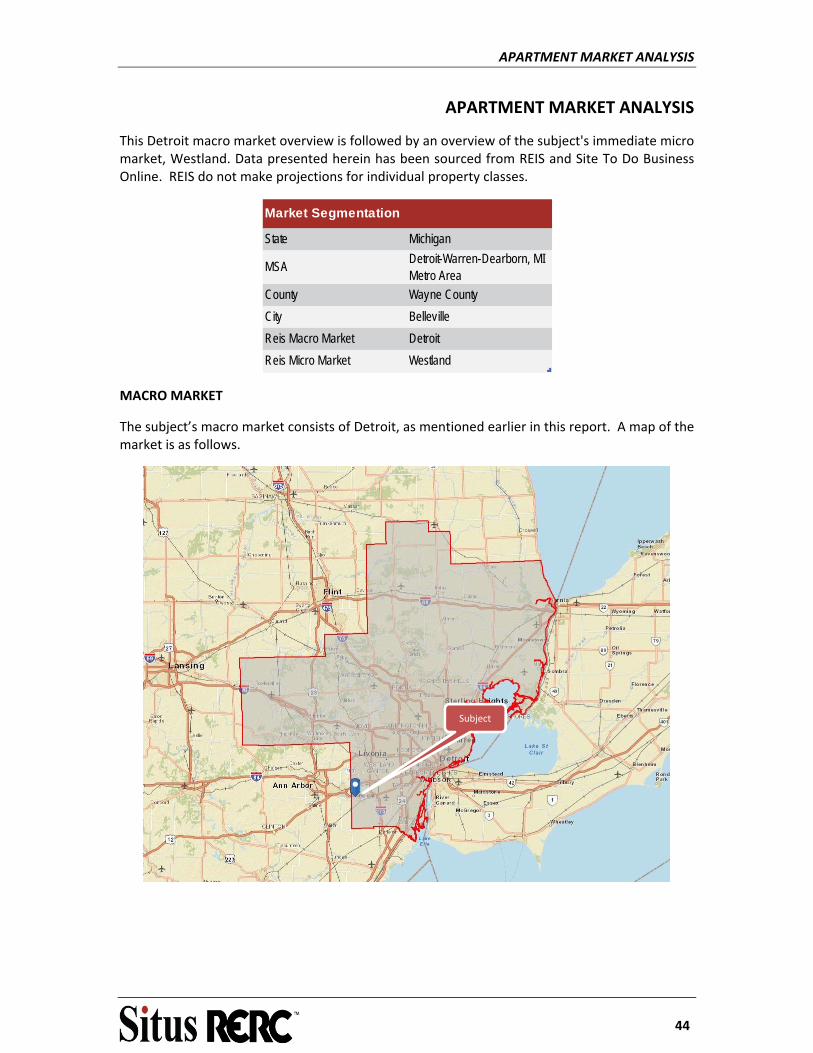

MACRO MARKET

The subject’s macro market consists of Detroit, as mentioned earlier in this report. A map of the market is as follows.

Subject

APARTMENT MARKET ANALYSIS

45

Inventory

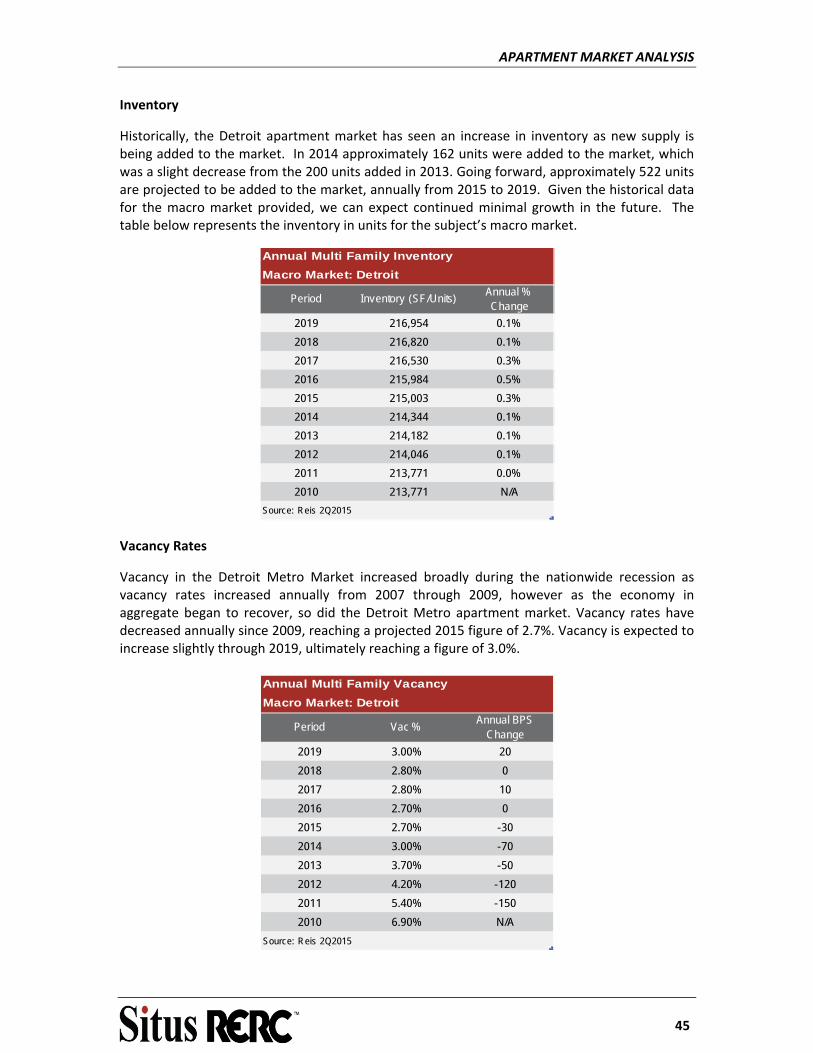

Historically, the Detroit apartment market has seen an increase in inventory as new supply is being added to the market. In 2014 approximately 162 units were added to the market, which was a slight decrease from the 200 units added in 2013. Going forward, approximately 522 units are projected to be added to the market, annually from 2015 to 2019. Given the historical data for the macro market provided, we can expect continued minimal growth in the future. The table below represents the inventory in units for the subject’s macro market.

Annual Multi Family Inventory

Macro Market: Detroit

Period Inventory (SF/Units)Annual % Change

2019 216,954 0.1%

2018 216,820 0.1%

2017 216,530 0.3%

2016 215,984 0.5%

2015 215,003 0.3%

2014 214,344 0.1%

2013 214,182 0.1%

2012 214,046 0.1%

2011 213,771 0.0%

2010 213,771 N/A

Source: Reis 2Q2015

Vacancy Rates

Vacancy in the Detroit Metro Market increased broadly during the nationwide recession as vacancy rates increased annually from 2007 through 2009, however as the economy in aggregate began to recover, so did the Detroit Metro apartment market. Vacancy rates have decreased annually since 2009, reaching a projected 2015 figure of 2.7%. Vacancy is expected to increase slightly through 2019, ultimately reaching a figure of 3.0%.

Annual Multi Family Vacancy

Macro Market: Detroit

Period Vac %Annual BPS

Change

2019 3.00% 20

2018 2.80% 0

2017 2.80% 10

2016 2.70% 0

2015 2.70% -30

2014 3.00% -70

2013 3.70% -50

2012 4.20% -120

2011 5.40% -150

2010 6.90% N/A

Source: Reis 2Q2015

APARTMENT MARKET ANALYSIS

46

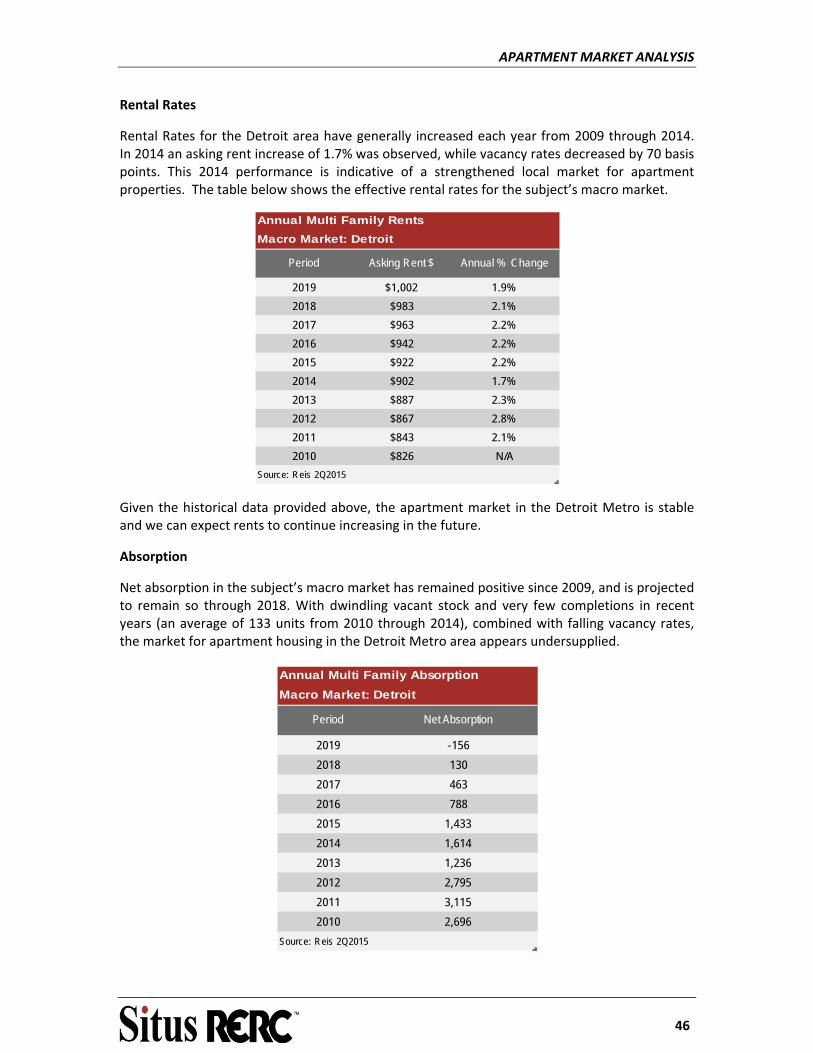

Rental Rates

Rental Rates for the Detroit area have generally increased each year from 2009 through 2014. In 2014 an asking rent increase of 1.7% was observed, while vacancy rates decreased by 70 basis points. This 2014 performance is indicative of a strengthened local market for apartment properties. The table below shows the effective rental rates for the subject’s macro market.

Annual Multi Family Rents

Macro Market: Detroit

Period Asking Rent $ Annual % Change

2019 $1,002 1.9%

2018 $983 2.1%

2017 $963 2.2%

2016 $942 2.2%

2015 $922 2.2%

2014 $902 1.7%

2013 $887 2.3%

2012 $867 2.8%

2011 $843 2.1%

2010 $826 N/A

Source: Reis 2Q2015

Given the historical data provided above, the apartment market in the Detroit Metro is stable and we can expect rents to continue increasing in the future.

Absorption

Net absorption in the subject’s macro market has remained positive since 2009, and is projected to remain so through 2018. With dwindling vacant stock and very few completions in recent years (an average of 133 units from 2010 through 2014), combined with falling vacancy rates, the market for apartment housing in the Detroit Metro area appears undersupplied.

Annual Multi Family Absorption

Macro Market: Detroit

Period Net Absorption

2019 -156

2018 130

2017 463

2016 788

2015 1,433

2014 1,614

2013 1,236

2012 2,795

2011 3,115

2010 2,696

Source: Reis 2Q2015

APARTMENT MARKET ANALYSIS

47

MICRO MARKET

The subject’s micro market consists of the Westland submarket, as mentioned earlier in this report. A map of the submarket is as follows.

Inventory

Over the past 5 years, inventory has remained stagnant in the micro market. From 2009 to 2014, there have been no units added to the market. Given the historical data for the micro market, we can expect minimal growth in the future. The table below represents the inventory in units for the subject’s micro market.

Annual Multi Family Inventory

Westland

Period Inventory (SF/Units)Annual % Change

2019 26,511 0.0%

2018 26,511 0.0%

2017 26,511 0.0%

2016 26,511 0.0%

2015 26,511 0.0%

2014 26,511 0.0%

2013 26,511 0.0%

2012 26,511 0.0%

2011 26,511 0.0%

2010 26,511 N/A

Source: Reis 2Q2015

Subject

APARTMENT MARKET ANALYSIS

48

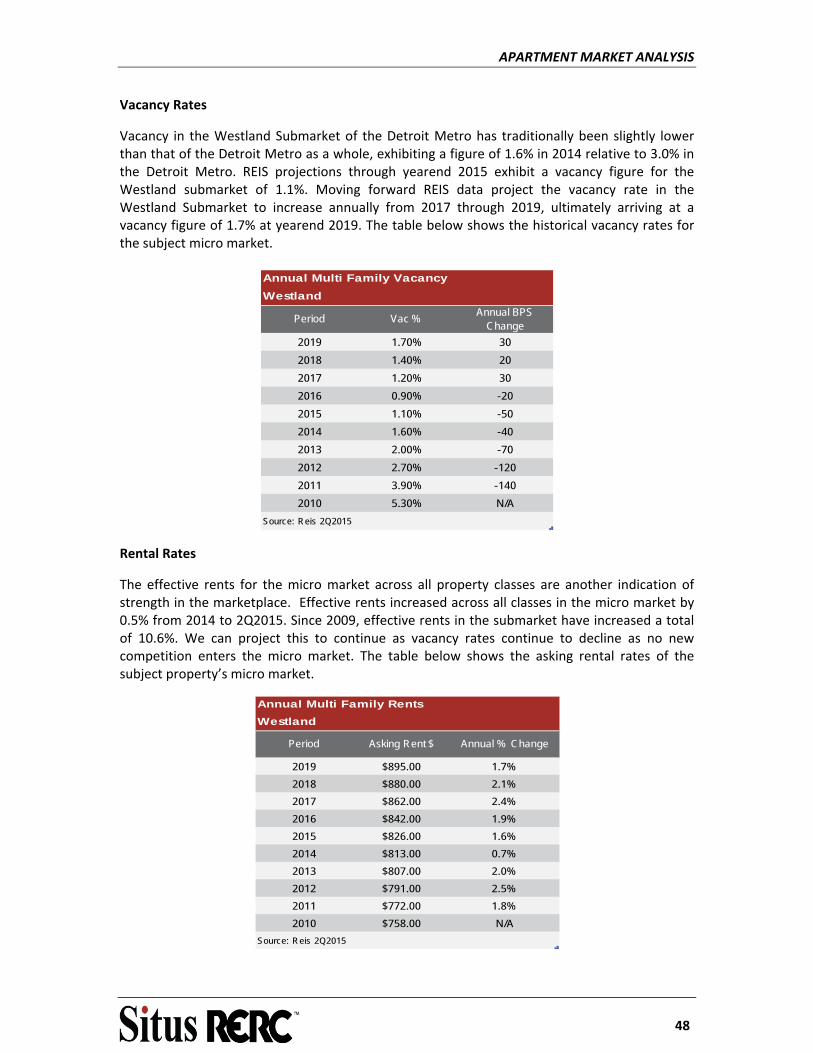

Vacancy Rates

Vacancy in the Westland Submarket of the Detroit Metro has traditionally been slightly lower than that of the Detroit Metro as a whole, exhibiting a figure of 1.6% in 2014 relative to 3.0% in the Detroit Metro. REIS projections through yearend 2015 exhibit a vacancy figure for the Westland submarket of 1.1%. Moving forward REIS data project the vacancy rate in the Westland Submarket to increase annually from 2017 through 2019, ultimately arriving at a vacancy figure of 1.7% at yearend 2019. The table below shows the historical vacancy rates for the subject micro market.

Annual Multi Family Vacancy

Westland

Period Vac %Annual BPS

Change

2019 1.70% 30

2018 1.40% 20

2017 1.20% 30

2016 0.90% -20

2015 1.10% -50

2014 1.60% -40

2013 2.00% -70

2012 2.70% -120

2011 3.90% -140

2010 5.30% N/A

Source: Reis 2Q2015

Rental Rates

The effective rents for the micro market across all property classes are another indication of strength in the marketplace. Effective rents increased across all classes in the micro market by 0.5% from 2014 to 2Q2015. Since 2009, effective rents in the submarket have increased a total of 10.6%. We can project this to continue as vacancy rates continue to decline as no new competition enters the micro market. The table below shows the asking rental rates of the subject property’s micro market.

Annual Multi Family Rents

Westland

Period Asking Rent $ Annual % Change

2019 $895.00 1.7%

2018 $880.00 2.1%

2017 $862.00 2.4%

2016 $842.00 1.9%

2015 $826.00 1.6%

2014 $813.00 0.7%

2013 $807.00 2.0%

2012 $791.00 2.5%

2011 $772.00 1.8%

2010 $758.00 N/A

Source: Reis 2Q2015

APARTMENT MARKET ANALYSIS

49

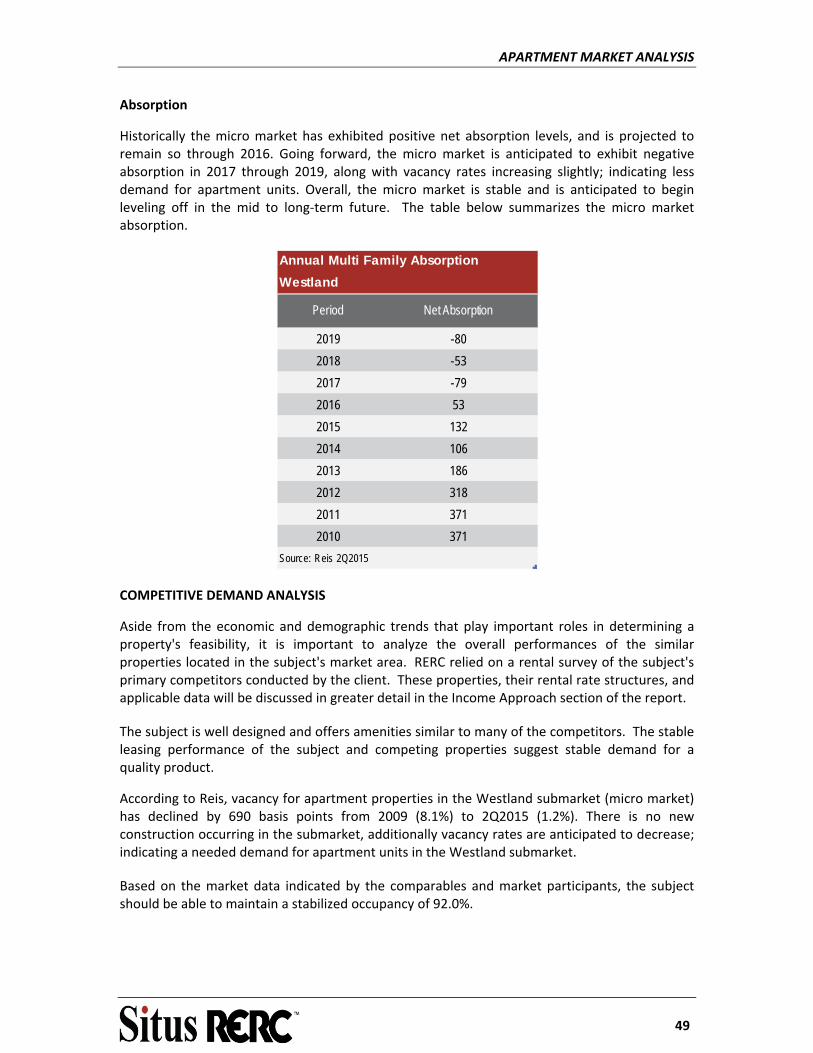

Absorption

Historically the micro market has exhibited positive net absorption levels, and is projected to remain so through 2016. Going forward, the micro market is anticipated to exhibit negative absorption in 2017 through 2019, along with vacancy rates increasing slightly; indicating less demand for apartment units. Overall, the micro market is stable and is anticipated to begin leveling off in the mid to long‐term future. The table below summarizes the micro market absorption.

Annual Multi Family Absorption

Westland

Period Net Absorption

2019 -80

2018 -53

2017 -79

2016 53

2015 132

2014 106

2013 186

2012 318

2011 371

2010 371

Source: Reis 2Q2015

COMPETITIVE DEMAND ANALYSIS

Aside from the economic and demographic trends that play important roles in determining a property's feasibility, it is important to analyze the overall performances of the similar properties located in the subject's market area. RERC relied on a rental survey of the subject's primary competitors conducted by the client. These properties, their rental rate structures, and applicable data will be discussed in greater detail in the Income Approach section of the report.

The subject is well designed and offers amenities similar to many of the competitors. The stable leasing performance of the subject and competing properties suggest stable demand for a quality product.

According to Reis, vacancy for apartment properties in the Westland submarket (micro market) has declined by 690 basis points from 2009 (8.1%) to 2Q2015 (1.2%). There is no new construction occurring in the submarket, additionally vacancy rates are anticipated to decrease; indicating a needed demand for apartment units in the Westland submarket.

Based on the market data indicated by the comparables and market participants, the subject should be able to maintain a stabilized occupancy of 92.0%.

APARTMENT MARKET ANALYSIS

50

MARKET ANALYSIS CONCLUSION

The apartment market in Detroit has shown positive recovery since the recession with increasing rental rates and declines in vacancy. There has been limited construction activity since 2009; we expect this trend to continue to the mid to long‐term future.

The subject’s micro market has experienced similar conditions as the overall metro area. Given the area demographics and continued development activity, it appears demand for comparable apartment properties and the subject improvements will continue to be favorable. The subject and its neighborhood are projected to experience a continued stable existence.

HIGHEST AND BEST USE

51

HIGHEST AND BEST USE

OVERVIEW

Highest and best use is defined by The Dictionary of Real Estate Appraisal, 5th edition as:

The reasonably probable and legal use of vacant land or an improved property, which is physically possible, appropriately supported, financially feasible and that results in the highest value.

Analyzing the site’s highest and best use requires consideration of all legal, physical and economic factors. Economic factors such as supply and demand are especially important. The highest and best use analysis is discussed on the following pages.

HIGHEST AND BEST USE, AS VACANT

Legal Permissibility