Embed Size (px)

Citation preview

Euro Credit Pilot

Macro Research June 2021 Strategy Research Credit Research

Credit remains solid

“ ”

June 2021 Credit & Credit Strategy Research

Euro Credit Pilot

UniCredit Research page 2 See last pages for disclaimer

Contents

3 Inflation expectations are in the limelight

4 A lesson from history: credit risk premiums tend to tighten during inflationary periods

5 European credit and inflation expectations

8 Technicals: Issuers are unlikely to accelerate their prefunding

10 Credit quality trend: Improving momentum with rising stars outpacing fallen angels

11 Valuation & Timing: We have adjusted our forecast for NFI and financial seniors

12 Bottom line

13 Sector allocation: we have raised our recommendation on Basic Resources to overweight from marketweight

16 Fundamental Credit Views

16 Telecommunications (Marketweight) 18 Media (Marketweight) 19 Technology (Marketweight) 21 Automobiles & Parts (Overweight) 23 Utilities (Marketweight) 28 Oil & Gas (Overweight) 30 Industrial Goods & Services (Marketweight) 33 Basic Resources (Overweight) 34 Chemicals (Underweight) 36 Construction & Materials (Marketweight) 37 Health Care (Marketweight) 39 Personal & Household Goods (Marketweight) 41 Food & Beverage (Marketweight) 43 Travel & Leisure (Underweight) 44 Retail (Marketweight) 45 Banks (Marketweight) 49 Insurance (Marketweight) 52 Real Estate (Marketweight)

Summary ■ Inflation concerns will remain on investors’ radar screens in

2H. However, high inflation expectations are not necessarily a bad omen for credit. Notably, amid rising inflation expectations, high-yield non-financial bonds and bank AT1s, given their high yield buffers and short durations, are likely to outperform, while investment-grade non-financial seniors and SSAs are most vulnerable.

■ Macro Outlook: While we expect inflation pressure to remain temporarily constrained in 2H21, there is scope for yield volatility to adversely affect long-duration credit, in particular.

■ Credit Quality Trend: Credit quality is improving, with rising stars’ volume in iBoxx indices outpacing the volume of fallen angels YTD.

■ Market Technicals: We continue to see moderate supply in 2H, both in investment-grade and high-yield non-financial bonds, providing support to European credit.

■ Valuation & Timing: We have revised our spread forecast for iBoxx non-financial and financial seniors to 35bp respectively for the end of the year (from 20bp and 20-30bp respectively). We have also adjusted our spread forecast for NFI hybrids to 150bp from 170bp.

■ Sector Allocation & Recommendation Overview: We have revised our recommendation on Basic Resources to overweight from marketweight. This is supported by a strong outlook for commodities on the back of broader economic recovery and demand from government infrastructure programs. We have left other sector recommendations unchanged, i.e. we have an overweight recommendation on Automobiles & Parts and Oil & Gas and an underweight recommendation on Travel & Leisure and Chemicals.

Published on 17 June 2021 Cover picture @ Prajukpunt - Fotolia.com Gianfranco Arcovito, CFA, Credit Analyst Telecoms, Technology, Gaming (UniCredit Bank, Munich), +49 89 378-15449 [email protected] Christian Aust, CFA, Head of Corporate Credit Research, Senior Credit Analyst Industrials, Oil & Gas (UniCredit Bank, Munich), +49 89 378-17564 [email protected] Tobias Keller, Credit Analyst Banks (UniCredit Bank, Munich), +49 89 378-12960 [email protected] Dr. Stefan Kolek EEMEA Corporate Credit Strategist (UniCredit Bank, Munich), +49 89 378-12495 [email protected] Dr. Sven Kreitmair, CFA, Head of Credit Research, Credit Analyst Automotive & Mobility (UniCredit Bank, Munich), +49 89 378-13246, [email protected] Ulrich Scholz, CFA, FRM, Credit Analyst Utilities, Hybrids (UniCredit Bank, Munich) +49 89 378-4184, [email protected] Jonathan Schroer, CFA, Senior Credit Analyst Telecoms, Media/Cable (UniCredit Bank, Munich), +49 89 378-13212 , [email protected] Dr. Silke Stegemann, CEFA, Senior Credit Analyst Health Care & Pharma, Consumer (UniCredit Bank, Munich), +49 89 378-18202 [email protected] Natalie Tehrani Monfared, Senior Credit Analyst Regulatory & Accounting Service, Insurance, Real Estate (UniCredit Bank, Munich), +49 89 378-12242, [email protected] Dr. Michael Teig, Deputy Head of Financials Credit Research, Senior Credit Analyst Banks (UniCredit Bank, Munich), +49 89 378-12429, [email protected]

June 2021 Credit & Credit Strategy Research

Euro Credit Pilot

UniCredit Research page 3 See last pages for disclaimer

Inflation expectations are in the limelight

Prices in major economies have increased substantially recently

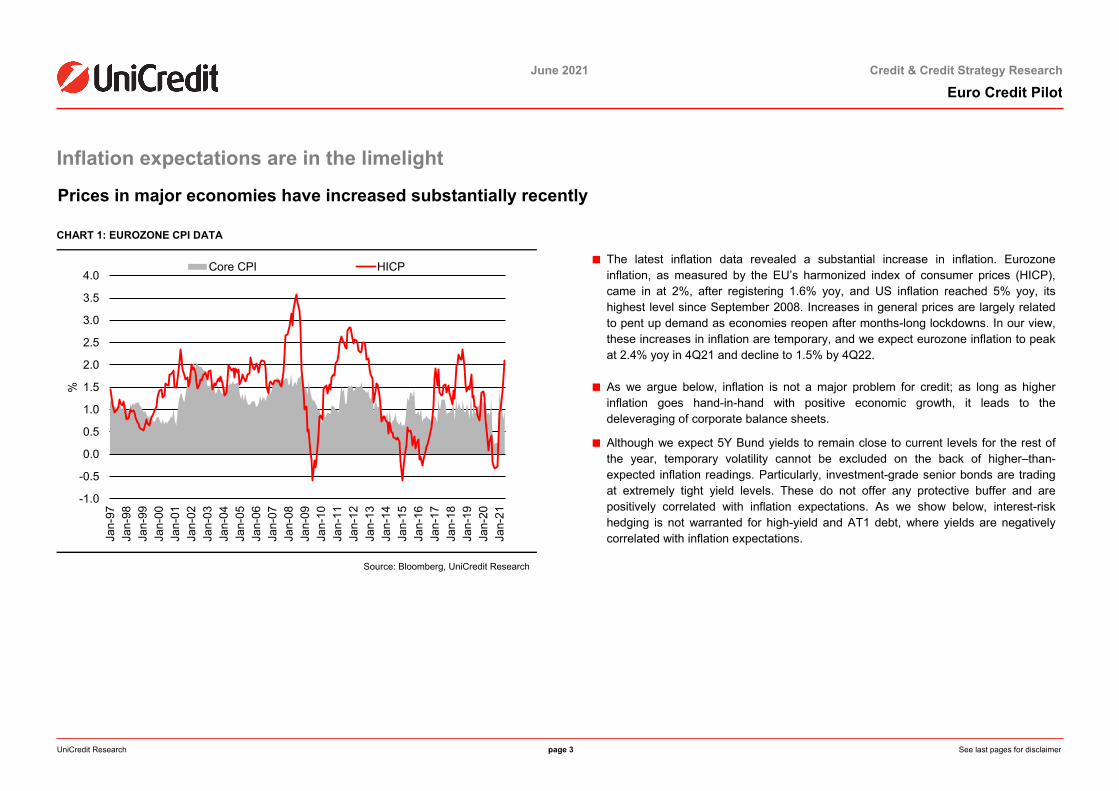

CHART 1: EUROZONE CPI DATA

■ The latest inflation data revealed a substantial increase in inflation. Eurozone inflation, as measured by the EU’s harmonized index of consumer prices (HICP), came in at 2%, after registering 1.6% yoy, and US inflation reached 5% yoy, its highest level since September 2008. Increases in general prices are largely related to pent up demand as economies reopen after months-long lockdowns. In our view, these increases in inflation are temporary, and we expect eurozone inflation to peak at 2.4% yoy in 4Q21 and decline to 1.5% by 4Q22.

■ As we argue below, inflation is not a major problem for credit; as long as higher inflation goes hand-in-hand with positive economic growth, it leads to the deleveraging of corporate balance sheets.

■ Although we expect 5Y Bund yields to remain close to current levels for the rest of the year, temporary volatility cannot be excluded on the back of higher–than-expected inflation readings. Particularly, investment-grade senior bonds are trading at extremely tight yield levels. These do not offer any protective buffer and are positively correlated with inflation expectations. As we show below, interest-risk hedging is not warranted for high-yield and AT1 debt, where yields are negatively correlated with inflation expectations.

Source: Bloomberg, UniCredit Research

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Jan-

97Ja

n-98

Jan-

99Ja

n-00

Jan-

01Ja

n-02

Jan-

03Ja

n-04

Jan-

05Ja

n-06

Jan-

07Ja

n-08

Jan-

09Ja

n-10

Jan-

11Ja

n-12

Jan-

13Ja

n-14

Jan-

15Ja

n-16

Jan-

17Ja

n-18

Jan-

19Ja

n-20

Jan-

21

%

Core CPI HICP

June 2021 Credit & Credit Strategy Research

Euro Credit Pilot

UniCredit Research page 4 See last pages for disclaimer

A lesson from history: credit risk premiums tend to tighten during inflationary periods Credit risk premiums tend to tighten during inflationary periods

CHART 2: MOODY’S BAA US CORPORATE SPREAD INDEX VS. US CPI INFLATION*

CHART 3: ITRAXX XO VS. EUR 5Y5Y INFLATION SWAP*

*Red shading indicates a period of rising inflation. Grey shading indicates a reaction by credit markets to monetary-policy tightening. Source: Moody’s, Bloomberg, UniCredit Research

*Red shading indicates a period of rising inflation. Source: IHS Markit, Bloomberg, UniCredit Research

■ History suggests that inflation does not pose a major problem for credit. As long as higher inflation goes hand-in-hand with economic growth, it leads to the deleveraging of corporate balance sheets. In a positive-growth environment, there is a higher likelihood of corporates passing on higher prices to consumers, which boosts EBITDA. The two major increases in inflation during the 1970s illustrate the relationship between inflation and credit risk premiums. As Chart 2 shows, US corporate-bond spreads actually tightened (red areas).

■ Fed policy tightening ended this period of increasing inflation expectations, although the US economy fell into a recession and spreads widened (gray shading). Although the comparison is not straightforward, as the US economy exhibited a double-digit inflation rate at that time. The lesson from the 1970s is that it is to a lesser degree inflation than monetary-policy tightening (with adverse ramifications on economic growth) that is negative for credit. Similarly, Chart 3 shows that, in the eurozone, recent periods of higher inflation expectations were accompanied by tighter spreads.

-4

-2

0

2

4

6

8

10

12

14

160

100

200

300

400

500

600

700

800

Jan-

65Ju

n-67

Nov

-69

Apr

-72

Sep

-74

Feb-

77Ju

l-79

Dec

-81

May

-84

Oct

-86

Mar

-89

Aug

-91

Jan-

94Ju

n-96

Nov

-98

Apr

-01

Sep

-03

Feb-

06Ju

l-08

Dec

-10

May

-13

Oct

-15

Mar

-18

Aug

-20

% y

oy

bp

Moody's BAA US spread (rev. ls) CPI inflation (rs)

0.5

1.0

1.5

2.0

2.5

3.00

200

400

600

800

1000

1200

May

-08

May

-09

May

-10

May

-11

May

-12

May

-13

May

-14

May

-15

May

-16

May

-17

May

-18

May

-19

May

-20

May

-21

%bp

iTraxx XO (rev. ls) EUR 5Y5Y inflation swap

June 2021 Credit & Credit Strategy Research

Euro Credit Pilot

UniCredit Research page 5 See last pages for disclaimer

European credit and inflation expectations While senior IG NFI debt is most vulnerable to inflation risk, HY NFI debt and bank AT1s offer the best place to stay

CHART 4: IBOXX NFI IG SENIOR AND SUBS YTW VS. 5Y5Y INFLATION FORWARD SWAP*

CHART 5: IBOXX HY NFI AND BANK AT1 YTW VS. 5Y5Y INFLATION FORWARD SWAP*

*past 6M of daily values Source: IHS Markit, Bloomberg, UniCredit Research *past 6M of daily values Source: IHS Markit, Bloomberg, UniCredit Research

■ The impact of inflation expectations on corporate bonds depends mainly on their yield level and duration. We find that NFI IG senior credit is worst-positioned to cope with higher inflation expectations. As Chart 4 shows, the correlation between the latter and YTW is positive, meaning that higher inflationary expectations, as reflected in the 5Y5Y inflation swap, go hand-in-hand with tighter yields in the IG NFI senior credit. As such, investment-grade non-financials seniors are most vulnerable, especially given that we expect to see only limited spread tightening going forward. As Chart 4 also shows, the impact of inflation expectation on hybrids appears neutral.

■ The picture is different for iBoxx HY NFI bonds and bank AT1s (Chart 5) and financial senior bonds (Chart 6), where YTW is negatively correlated with 5Y5Y inflation swaps. These credit-market segments have much lower duration than NFI IG debt and, in the case of HY NFI debt and bank AT1s, higher yield levels. In addition, HY NFI bonds’ rating momentum has stabilized and started to improve; in the year to date, there have been EUR 9bn of rising stars compared to a mere EUR 4bn of fallen angels.

y = 0.4592x - 0.4555R² = 0.7749

y = -0.0473x + 1.4627R² = 0.0069

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

1 1.1 1.2 1.3 1.4 1.5 1.6 1.7

YTW

(%)

5Y5Y forward (%)

NFI IG Senior NFI IG Subs

y = -1.1424x + 4.8684R² = 0.2963

y = -0.6949x + 3.6846R² = 0.5248

2.0

2.5

3.0

3.5

4.0

4.5

1 1.1 1.2 1.3 1.4 1.5 1.6 1.7

YTW

(%)

5Y5Y forward (%)

Bank AT1 HY NFI

June 2021 Credit & Credit Strategy Research

Euro Credit Pilot

UniCredit Research page 6 See last pages for disclaimer

Financial bonds are well protected against higher inflation expectations

CHART 6: IBOXX FINANCIAL SENIOR AND SUBS VS. 5Y5Y INFLATION FORWARD SWAP*

■ Similarly, financial bonds’ yields (both seniors and subs) are negatively correlated with inflation expectations. However, this negative correlation is more pronounced and more consistent among bank AT1s (Chart 5) than financial seniors and subs (Chart 6), where, particularly at higher inflation swap rates (which reflect the most recent values), this relationship is pretty flat. Our preference is for EUR-denominated bank AT1s, which, in our view, at a 330bp ASW spread and 2.9% YTW, offer better value. We expect the ASW spread to end the year between 330bp and 350bp, implying that carry will be a key source of return.

■ From a fundamental point of view, the AT1s of most issuers should benefit from a still-fairly-strong credit-fundamental backdrop. European banks were in much better shape when the pandemic shock hit than they were going into the financial crisis. However, we note that, particularly in the wake of the outbreak of the pandemic (March-April), banks provided a lot of liquidity support to the corporate sector without state guarantees. Banks have been granted material regulatory relief regarding capital. The ECB has estimated that, taken together (excluding flexibility applied to the countercyclical buffer and the CRR quick fix), these relief measures almost doubled banks’ capital headroom. Capital conservation has also been supported by regulators’ recommendations that dividend distributions be suspended. As a consequence, the aggregate CET1 ratio of European banks reached a new all-time high of 15.5% on a fully loaded basis at the end of last year. We therefore think ample room for loss absorption is available to European banks, especially given that regulatory flexibility will remain in place until at least the end of next year. While we expect banks’ NPL ratios to rise gradually from their low levels (the aggregate NPL ratio was 2.6% at year-end 2020) going into 2H21 amid the phasing-out of government support measures, we expect this increase to be manageable.

*past 6M of daily values Source: IHS Markit, Bloomberg, UniCredit Research

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

1 1.1 1.2 1.3 1.4 1.5 1.6 1.7

YTW

(%)

5Y5Y forward (%)

Financials Senior Financials Subs

June 2021 Credit & Credit Strategy Research

Euro Credit Pilot

UniCredit Research page 7 See last pages for disclaimer

EUR-denominated AT1s to benefit from our expectations of further moderate upside in equities

CHART 7: BANK AT1 SPREAD VS. STOXX EUROPE 600 BANKS*

■ From a more-medium-term perspective, we expect to see a steepening of the Bund yield curve in the 10Y-3M segment by 30bp by the end of next year. This is basically supportive of banks’ earnings outlooks. However, the impact of this should not be overestimated. First, the expected steepening is likely to be very moderate. Second, the regulatory framework foresees banks limiting the mismatch in assets’ and liabilities’ durations, which should contain the impact of a steeper curve on earnings outlooks. However, banks have a lot of deposits, whose pricing is sticky, and these are also affected by de facto long-term low interest rates (and, in the case of corporate deposits, negative interest rates). Against this backdrop, a steeper yield curve should be supportive of banks whose assets (loans) are long term.

■ Bank AT1s were closely correlated with the STOXX Europe 600 Banks index in the past (Chart 7). Our outlook for stable-to-slightly-firmer European equities by the end of the year, and given our marketweight recommendation on bank stocks, is supportive of a range-bound move in AT1 spreads in the coming months.

*past 6M of daily values Source: IHS Markit, Bloomberg, UniCredit Research

y = -2.5228x + 686.68R² = 0.6591

200

250

300

350

400

450

500

100 110 120 130 140 150

AT1

spre

ad (b

p)

STOXX Europe 600 Banks

last

June 2021 Credit & Credit Strategy Research

Euro Credit Pilot

UniCredit Research page 8 See last pages for disclaimer

Technicals: Issuers are unlikely to accelerate their prefunding

CHART 8: INVESTMENT-GRADE NON-FINANCIAL ISSUANCE

CHART 9: HIGH-YIELD NON-FINANCIAL ISSUANCE

Source:IHS Markit, UniCredit Research Source: IHS Markit, UniCredit Research

■ We do not expect issuers to accelerate their primary-market activity in 2H. Most issuers are sitting on huge piles of cash reserves accumulated since the beginning of the pandemic, and to a large extent, they have prefunded upcoming maturities.

■ Despite low yield levels, further prefunding activities of maturities in the more-distant future are limited. Thus, we reiterate our forecast of up to EUR 250bn in gross new issuance from iBoxx NFI IG corporates and up to EUR 85bn from iBoxx NFI HY issuers this year. Besides prefunding, HY issuance is driven by inaugural bond issues, i.e. issues from corporates coming to the bond market for the first time, where the YTD volume of EUR 10bn exceeds that of IG NFIs (EUR 8bn) and makes up almost 20% of HY NFI issuance this year.

0

50

100

150

200

250

300

350

400

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

EU

R b

n

2016 2017 2018

2019 2020 2021

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

Jan

Feb

Mar

Apr

May Jun

Jul

Aug

Sep Oct

Nov

Dec

EU

R m

n

2016 2017 2018 2019 2020 2021

June 2021 Credit & Credit Strategy Research

Euro Credit Pilot

UniCredit Research page 9 See last pages for disclaimer

Market liquidity is likely to remain high, issuance is likely to remain low

CHART 10: REDEMPTIONS AND COUPON PAYMENTS AMONG IBOXX IG AND HY NFIS

CHART 11: FRN NON-FINANCIAL ISSUANCE

Source: UniCredit Research Source: UniCredit Research

■ With redemptions (including callable bonds) expected to rise in the coming quarters (Chart 10, which includes coupon payments), liquidity is likely to remain high. Given that corporates have, to a large extent, prefunded upcoming redemptions, this is likely to provide support to the secondary market.

■ As we expect yields to remain close to current levels, we do not expect investor demand for floaters to rise significantly. Corporates are likely to stick to fixed-coupon issuance to a large part, and demand for FRNs is likely to remain moderate given our yield forecasts. Issuance of FRNs has declined to close to historical lows (Chart 11), and we do not expect to see significant potential going forward.

0

10

20

30

40

50

60

Sep

-21

Dec

-21

Mar

-22

Jun-

22

Sep

-22

Dec

-22

EU

R b

n

IG HY

0%

4%

8%

12%

16%

20%

24%

0

5

10

15

20

25

30

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

Issu

ance

vol

ume

in E

UR

bn

FRN % of all IG benchmark bonds (Fix + FRN) (rs)

June 2021 Credit & Credit Strategy Research

Euro Credit Pilot

UniCredit Research page 10 See last pages for disclaimer

Credit quality trend: Improving momentum with rising stars outpacing fallen angels Stay long fallen angels CHART 12: FALLEN ANGELS VS. RISING STARS

CHART 13: YTD PERFORMANCE OF FALLEN ANGELS VS.THAT OF NON-FALLEN ANGELS*

Source: Bloomberg, IHS Markit, UniCredit Research *spreads normalized to 100 at the beginning of the year Source: IHS Markit, UniCredit Research

■ Issuers’ credit quality has started to improve. While downgrades still outweigh upgrades in the IG and HY universe, downward dynamics are less pronounced than they were last year. Similarly, as Chart 12 shows, the volume of rising stars – issues moving from the high-yield to the investment-grade index – has picked up, and at EUR 9bn, it is at its highest level since 2018. At the same time, as rating momentum remains negative, we continue to see fallen angels. However, after a record-high EUR 47bn worth were created last year, the volume of fallen angels is less than EUR 5bn YTD; thus, it is lagging behind that of rising stars.

■ We expect up to EUR 15bn of fallen angels to be created this year and reiterate our hold recommendation on them. Fallen angels have consistently outperformed non-fallen angels YTD (Chart 13), a picture we have observed over the past year and after the recession of 2008-09. The reason remains the same: in terms of size, sector position and corporate policies, fallen angels remain IG names, and this is something investors attach value to despite their having been downgraded to below investment grade.

0

5

10

15

20

25

30

35

40

45

50

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

YTD

EU

R b

n

Fallen angels Rising stars

full-year forecast

70

75

80

85

90

95

100

105

110

115

Jan-

21

Feb-

21

Mar

-21

Apr

-21

May

-21

NFA FA

Outperformance

Underperformance

June 2021 Credit & Credit Strategy Research

Euro Credit Pilot

UniCredit Research page 11 See last pages for disclaimer

Valuation & Timing: We have adjusted our forecast for NFI and financial seniors

We see less scope for spread tightening by the end of the year

CHART 14: IBOXX NFI SENIOR AND SUBS AND IBOXX FINANCIALSENIORS

■ We have revised our spread forecast on iBoxx NFI and Financial seniors to 35bp respectively by the end of the year. This is different from our original expectation that spreads would tighten to 20bp and 20-30bp respectively by the end of the year.

■ Our main argument for spread tightening was technical. We expected the hunt for yield and the combination of ECB corporate-bond purchases with lower net bond supply to drive spreads to those levels. Although in the year to date, corporate purchases have run, on average, at EUR 7.3bn per month. Thus, they are roughly in line with our forecast (of up to EUR 8bn of net purchases per month), and net supply from investment-grade non-financials has declined sharply. Therefore, the impact on spreads has been less pronounced than we forecast. While we expect the aforementioned forces to remain valid throughout the year – and on the back of these, we still expect spreads to tighten – this is likely to happen to a lesser degree than we originally forecast.

■ We have also adjusted our spread forecast on NFI hybrids to 150bp from 170bp, as we expect this segment to benefit from the hunt for yield, stabilized credit metrics and lower expected issuance – notwithstanding hybrid-specific risk factors (e.g. non-call risk, extension risk) – although the latter is highly sector-dependent (e.g. in Utilities we still see scope for issuance).

■ We have left our spread forecasts for HY NFI, at 250bp, and for Bank AT1s, at 300-350bp.

Source: Bloomberg, UniCredit Research

0

100

200

300

400

500

600

Jan-

19

Mar

-19

May

-19

Jul-1

9

Sep

-19

Nov

-19

Jan-

20

Mar

-20

May

-20

Jul-2

0

Sep

-20

Nov

-20

Jan-

21

Mar

-21

May

-21

bp

NFI Sen iBoxx NFI Sub iBoxx € Financials Senior

June 2021 Credit & Credit Strategy Research

Euro Credit Pilot

UniCredit Research page 12 See last pages for disclaimer

Bottom line

Keep duration short

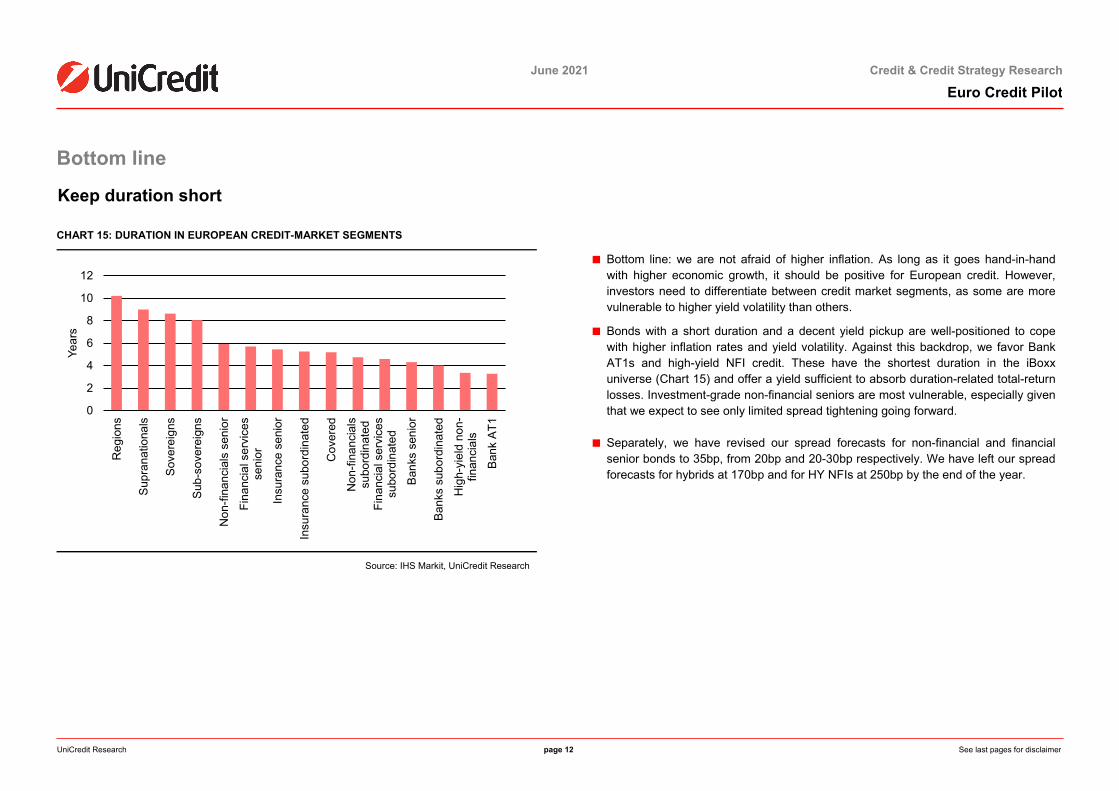

CHART 15: DURATION IN EUROPEAN CREDIT-MARKET SEGMENTS

■ Bottom line: we are not afraid of higher inflation. As long as it goes hand-in-hand with higher economic growth, it should be positive for European credit. However, investors need to differentiate between credit market segments, as some are more vulnerable to higher yield volatility than others.

■ Bonds with a short duration and a decent yield pickup are well-positioned to cope with higher inflation rates and yield volatility. Against this backdrop, we favor Bank AT1s and high-yield NFI credit. These have the shortest duration in the iBoxx universe (Chart 15) and offer a yield sufficient to absorb duration-related total-return losses. Investment-grade non-financial seniors are most vulnerable, especially given that we expect to see only limited spread tightening going forward.

■ Separately, we have revised our spread forecasts for non-financial and financial senior bonds to 35bp, from 20bp and 20-30bp respectively. We have left our spread forecasts for hybrids at 170bp and for HY NFIs at 250bp by the end of the year.

Source: IHS Markit, UniCredit Research

0

2

4

6

8

10

12

Reg

ions

Sup

rana

tiona

ls

Sov

erei

gns

Sub

-sov

erei

gns

Non

-fina

ncia

ls s

enio

r

Fina

ncia

l ser

vice

sse

nior

Insu

ranc

e se

nior

Insu

ranc

e su

bord

inat

ed

Cov

ered

Non

-fina

ncia

lssu

bord

inat

edFi

nanc

ial s

ervi

ces

subo

rdin

ated

Ban

ks s

enio

r

Ban

ks s

ubor

dina

ted

Hig

h-yi

eld

non-

finan

cial

s

Ban

k AT

1

Year

s

June 2021 Credit & Credit Strategy Research

Euro Credit Pilot

UniCredit Research page 13 See last pages for disclaimer

Sector allocation: we have raised our recommendation on Basic Resources to overweight from marketweight ■ Amid continuous economic rebound in 2H21, we have revised our recommendation on

Basic Resources to overweight from marketweight. Basic Resources should benefit from its cyclical nature. Our recommendation is supported by a strong outlook for commodities on the back of broader economic recovery and demand from government infrastructure programs. This is likely to keep sentiment upbeat, particularly towards metals that are supportive of a green transition (such as copper and nickel). Normalization of Chinese metal demand should lead to a stabilization of prices later in the year. At the same time, strong cash generation and robust balance sheets are likely to be maintained for the three names we cover in this sector despite increased shareholder remuneration.

■ We have left other sector recommendations unchanged, i.e. we have an overweight recommendation on Automobiles & Parts and Oil & Gas. Both sectors should benefit from above-average carry and from their cyclical natures. With respect to Oil & Gas, it should benefit from strong oil prices. We have left unchanged our underweight recommendation on Travel & Leisure and Chemicals. With respect to Travel & Leisure, we still think that visibility in the sector is limited. Notably, the business segment of the sector still needs to find its post-pandemic shape, and it still needs to be seen whether vaccination advances will be successful to a degree that will allow a return to pre-crisis travel and leisure activities. Regarding Chemicals, despite being cyclical, this sector is prone to correction given its tight spreads relative to most other cyclical sectors. We have a marketweight recommendation on all other sectors.

■ In terms of ratings, within the IG universe, our preference is for BBB rated credit and hybrids, which offer yield. With regard to bank credit, we reiterate our recommendation to hold AT1s, where we revised our spread forecast to 300-350bp (from 350bp) by the end of the year.

TABLE 1: SECTOR ALLOCATION

As of 16 June 2021 Current

recommendation iBoxx

weight YTD spread

change Current

spread level Macro allocation Sovereigns 58.9% +0.2 11.1 Sub-sovereigns MW 14.0% +0.7 6.6 Covered bonds MW 6.2% -2.1 2.2 Financials MW 8.4% -9.8 55.5 Non-financials OW 12.5% -9.9 50.3 Sector allocation NFI Telecommunications TEL MW 10.7% -6.4 52.8 Media MDI MW 2.1% -18.7 45.6 Technology THE MW 4.6% -7.9 38.9 Automobiles & Parts ATO OW 10.7% -25.2 53.6 Utilities UTI MW 16.4% -6.3 51.5 Oil & Gas OIG MW 8.6% -0.2 72.9 Industrial Goods & Services IGS MW 13.3% -13.7 43.8 Basic Resources BAS OW 1.0% -7.8 58.4 Chemicals CHE UW 3.4% -16.8 38.5 Construction & Materials CNS OW 2.4% -10.0 44.6 Health Care HCA MW 10.5% -6.4 50.9 Personal & Household Goods PHG MW 4.5% -8.1 48.6 Food & Beverage FOB MW 7.9% -7.2 40.9 Travel & Leisure TAL UW 2.4% -8.2 49.5 Retail RET MW 1.4% -15.1 47.0 Quality allocation NFI AAA UW 0.4% -10.9 17.4 AA UW 6.5% -3.7 25.6 A MW 32.8% -7.5 35.7 BBB OW 60.3% -13.8 61.1 Sector other Banks BAK MW Insurance INN MW Real Estate RES MW

Source: UniCredit Research

June 2021 Credit & Credit Strategy Research

Euro Credit Pilot

UniCredit Research page 14 See last pages for disclaimer

Valuation & Timing: SPREAD FORECAST 2021 (forecast level, minimum and maximum level, in bp) Non-financial senior Financial senior

High yield Corporate hybrids and bank AT1s

Source: Bloomberg, IHS Markit, UniCredit Research

0

20

40

60

80

100

120

140

160

180

200

0

20

40

60

80

100

120

140

160

180

200

Dec-19 Jun-20 Dec-20 Jun-21 Dec-21

iBoxx NFI sen. iTraxx NFI

actual forecast

0

20

40

60

80

100

120

140

160

180

200

220

0

20

40

60

80

100

120

140

160

180

200

220

Dec-19 Jun-20 Dec-20 Jun-21 Dec-21

iBoxx FIN sen. iTraxx FinSen

actual forecast

0

150

300

450

600

750

0

150

300

450

600

750

Dec-19 Jun-20 Dec-20 Jun-21 Dec-21

iBoxx HY iTraxx Xover

actual forecast

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

0

100

200

300

400

500

600

Dec-19 Jun-20 Dec-20 Jun-21 Dec-21

AT1

(in b

p)

iBox

x N

FI H

ybrid

s (in

bp)

iBoxx NFI hybrids AT1 (rs)

actual forecast

June 2021 Credit & Credit Strategy Research

Euro Credit Pilot

UniCredit Research page 15 See last pages for disclaimer

AVERAGE SECTOR ASW SPREAD VS. MODIFIED DURATION AND AVERAGE RATING (BUBBLE SIZE CORRESPONDS TO SIZE OF SECTOR, SECTORS [LS], HYBRIDS [RS])

Source: IHS Markit, UniCredit Research

Automobiles & Parts (BBB+)

Basic Resources (BBB+)

Chemicals (BBB+)

Construction & Materials (BBB)

Food & Beverage (A-)

Health Care (A-)

Industrial Goods & Services (A-)

Media (BBB)

Oil & Gas (A-)

Personal & Household Goods (A)

Retail (BBB)

Technology (A-)

Telecommunications (BBB+)

Travel & Leisure (A)Utilities (BBB+)

Hybrid Bonds (BBB)

0

40

80

120

160

200

240

30

40

50

60

70

80

90

3.4 3.9 4.4 4.9 5.4 5.9 6.4 6.9 7.4 7.9

Sec

tor s

prea

ds (i

n bp

)

mDur

June 2021 Credit & Credit Strategy Research

Euro Credit Pilot

UniCredit Research page 16 See last pages for disclaimer

Fundamental Credit Views

Telecommunications (Marketweight) Jonathan Schroer, CFA, Senior Credit Analyst (UniCredit Bank, Munich) +49 89 378-13212, [email protected]

Weight in iBoxx NFI: Current ASW spread: change mom/YTD: Euro STOXX TEL YTD:

10.7%

53bp -3.6/-7.5

+16.8%

Sector drivers: We have a marketweight recommendation on the telecoms sector. In 2021, we expect the sector to see a partial revenue recovery from the pandemic, but also rising capex, which many companies postponed in 2020. This combination should make deleveraging difficult. As a result, we think rating trends will also be skewed to the negative side, continuing the trend of recent years. The industry remains highly competitive and fragmented, making price increases difficult. We expect companies to post modest revenue and EBITDA increases in 2021, especially due to rising demand for fast broadband products. We also think the outlook for price increases in 2021 looks better due to a recovery in the consumer environment. Some European spectrum auctions for 5G licenses that were postponed in 2020 will continue into 2021, and we expect most 5G product launches to gather intensity in the coming years. However, we think 5G is unlikely to give the companies a revenue boost in the near term.

ESG risks: Most ESG rankings have focused on corporate governance and labor relations within the telecoms sector, with environmental risks playing a subordinate role. However, environmental considerations are significant as telcos account for around 2% of global electricity usage. Various technologies (including fiber and 5G) may help break the link between rising data consumption and energy use. For more information, see Sector Thinking – ESG analysis and green bonds in the telecoms sector, 6 July 2020. Market recap: In the year through 31 May, the iBoxx IG Telecoms index slightly underperformed the broader NFI market, with the spread tightening by 5bp, to 56bp, compared to the EUR iBoxx NFI index, which has tightened by 8bp, to 53bp. We think this reflects the expectation of a stable operating performance in the sector in 2021, but rising capex needs have been a source of credit pressure. Over the last three months, T was the top performer after the company announced a major reorganization of its media business that was credit positive. Long-dated telco bonds have underperformed, in particular long-dated TELIAS bonds, although the company’s 1Q21 report was unspectacular.

Debt ticker Issuer Rec Amount (weight)

within index Credit profile

trend* Rating Latest research (including link) ORAFP Orange OW 21,850 (13.9%) Stable –/BBB+s/BBB+s » Daily Credit Briefing - Orange: CEO discusses various divestment options - 27 May 2021

» Sector Report - IG/HY Telecoms: 2021 telecoms outlook - 5G cycle delayed, pandemic recovery in focus - 1 Feb 21 T AT&T MW 21,548 (13.7%) Stable Baa2/BBBs/BBB+s » Daily Credit Briefing - AT&T: S&P changes outlook to stable from negative - 19 May 2021 DT Deutsche Telekom MW 18,100 (11.5%) Stable Baa1/BB+s/BBB+s » Daily Credit Briefing - Deutsche Telekom: CEO discusses various divestment options - 27 May 2021

» Sector Report - IG/HY Telecoms: 2021 telecoms outlook - 5G cycle delayed, pandemic recovery in focus - 1 Feb 21 VZ Verizon Communications MW 17,385 (11.0%) Stable Baa1/BBB+s/A-s » Daily Credit Briefing - Verizon Communications: Agrees to sell media business - 4 May 2021

» Sector Thinking - Green Bonds/ESG: ESG analysis and green bonds in the telecoms sector- 6 July 2020 TELEFO Telefonica OW 16,100 (10.2%) Stable –/BBn/BBBs » Daily Credit Briefing - Telefonica: Reportedly receives offer for deep-sea cables - 1 Jun 2021

» Sector Report - IG/HY Telecoms: 2021 telecoms outlook - 5G cycle delayed, pandemic recovery in focus - 1 Feb 21 VOD Vodafone OW 10,810 (6.9%) Improving –/BBBs/BBBs » Daily Credit Briefing - Vodafone: FY20/21 results show improving trends, but capex to increase in FY21/22 - 19 May 2021

» Sector Report - IG/HY Telecoms: 2021 telecoms outlook - 5G cycle delayed, pandemic recovery in focus - 1 Feb 21 BRITEL BT UW 8,200 (5.2%) Weakening Baa2/BBBs/BBBs » Daily Credit Briefing - BT-Group: Altice acquires minority stake - 10 Jun 2021

» Sector Report - IG/HY Telecoms: 2021 telecoms outlook - 5G cycle delayed, pandemic recovery in focus - 1 Feb 21 TELNO Telenor UW 6,750 (4.3%) Weakening A3/A-s/– » Daily Credit Briefing - Telenor: 1Q21 results show EBITDA decline with Asia adding pressure - 4 May 2021

» Sector Report - IG/HY Telecoms: 2021 telecoms outlook - 5G cycle delayed, pandemic recovery in focus - 1 Feb 21 TELIAS Telia Company MW 5,153 (3.3%) Weakening Baa1/BBB+s/– » Daily Credit Briefing - Telia Company: 1Q21 figures in line despite continued drag from roaming revenue - 23 Apr 2021

» Sector Report - IG/HY Telecoms: 2021 telecoms outlook - 5G cycle delayed, pandemic recovery in focus - 1 Feb 21

June 2021 Credit & Credit Strategy Research

Euro Credit Pilot

UniCredit Research page 17 See last pages for disclaimer

Debt ticker Issuer Rec Amount (weight)

within index Credit profile

trend* Rating Latest research (including link) AMXLMM America Movil MW 4,550 (2.9%) Weakening A3/BBB+n/A-p » Daily Credit Briefing - America Movil: 1Q21 results show growth slowdown, but tower spin-off is in focus - 29 Apr 2021 CKHGTH CK Hutchison Group

Telecom Holdings Ltd – 4,250 (2.7%) – Baa1/–/– Not covered

TLSAU Telstra UW 3,850 (2.4%) Stable A2/A-s/– » Sector Report - IG/HY Telecoms: 2021 telecoms outlook - 5G cycle delayed, pandemic recovery in focus - 1 Feb 2021 ETISLT Emirates

Telecommunications – 2,200 (1.4%) – Aa3/AA-s/A+s Not covered

VANTOW Vantage Towers – 2,200 (1.4%) – Baa3/BBB-s/– Not covered ETLFP Eutelsat UW 2,000 (1.3%) Stable Baa3/BBB-s/BBBs » Daily Credit Briefing - Eutelsat: 3Q20/21 results show further revenue decline, but in line with ... - 12 May 2021 NTT NTT – 2,000 (1.3%) – –/As/– Not covered KPN KPN MW 1,850 (1.2%) Stable Baa3/BBBs/BBBs » Daily Credit Briefing - KPN: EQT reportedly drops pursuit - 9 Jun 2021

» Sector Report - IG/HY Telecoms: 2021 telecoms outlook - 5G cycle delayed, pandemic recovery in focus - 1 Feb 21 SCMNVX Swisscom UW 1,500 (1.0%) Stable A2/As/– » Daily Credit Briefing - Swisscom: 1Q21 results in line with expectations, announces fiber partnership ... - 29 Apr 2021

» Sector Report - IG/HY Telecoms: 2021 telecoms outlook - 5G cycle delayed, pandemic recovery in focus - 1 Feb 21 TDFINF TDF Infrastructure – 1,400 (0.9%) – –/–/– Not covered PROXBB Proximus UW 1,100 (0.7%) Stable A1/An/– » Sector Flash - HY TMT: Benelux M&A could shift valuations and 1Q21 HY results preview - 5 May 2021

» Sector Report - IG/HY Telecoms: 2021 telecoms outlook - 5G cycle delayed, pandemic recovery in focus - 1 Feb 21 SESGFP SES MW 1,000 (0.6%) Stable Baa2/BBB-s/– » Daily Credit Briefing - SES Global: 1Q21 report shows easing revenue decline, but new buybacks planned - 7 May 2021 TELBSS Tele2 – 1,000 (0.6%) – –/BBBs/– Not covered TKAAV Telekom Austria OW 750 (0.5%) Stable Baa1/BBB+s/– » Daily Credit Briefing - Telekom Austria: 1Q21 results show growth slowdown, but tower spin-off is in focus - 29 Apr 2021

» Sector Report - IG/HY Telecoms: 2021 telecoms outlook - 5G cycle delayed, pandemic recovery in focus - 1 Feb 21 ODGR Telefonica Deutschland MW 600 (0.4%) Stable –/–/BBBs » Daily Credit Briefing - Telefonica Deutschland: 1Q21 results exceed consensus, putting upside pressure ... - 14 May 2021

» Sector Report - IG/HY Telecoms: 2021 telecoms outlook - 5G cycle delayed, pandemic recovery in focus - 1 Feb 21 CNUNZ Chorus – 500 (0.3%) – –/BBBs/– Not covered HTOGA OTE Hellenic Telecom MW 500 (0.3%) Stable –/BBBs/– » Sector Report - IG/HY Telecoms: 2021 telecoms outlook - 5G cycle delayed, pandemic recovery in focus - 1 Feb 2021 SGTOPT SingTel Optus – 500 (0.3%) – A3/A-n/A-s Not covered

*This is the analyst's opinion concerning the development (improving/stable/weakening/developing) of the issuer's credit profile over the next 3-6 months. This can be indicated by, among other things, the rating outlook or expected changes in the business profile or the financial profile, as indicated, for example, by credit protection ratios. Source: UniCredit Research

June 2021 Credit & Credit Strategy Research

Euro Credit Pilot

UniCredit Research page 18 See last pages for disclaimer

Media (Marketweight) Jonathan Schroer, CFA, Senior Credit Analyst (UniCredit Bank, Munich) +49 89 378-13212, [email protected]

Weight in iBoxx NFI: Current ASW spread: change mom/YTD: Euro STOXX MDI YTD:

2.1%

46bp -3.1/-19.7

+15.5%

Sector drivers: The media sector is driven by the close link between advertising spending and GDP growth. The outlook for media companies should improve in 2H21 assuming that the COVID-19 crisis is brought under control. Companies with major exposure to advertising continue to be hit particularly hard by lockdowns and slower economic activity. The pandemic has accelerated structural challenges that were already underway in traditional advertising as more business migrates to digital and subscription revenue models. Traditional media companies have thus been required to invest in new distribution channels, often leading to acquisitions at elevated multiples. Bertelsmann, WPP and Publicis are more advertising-driven and therefore more cyclical. Wolters Kluwer, RELX, SES, Eutelsat and Comcast are less cyclical.

ESG risks: S&P considers the media sector to have the lowest ESG exposure among its ranking of different industries. The most significant ESG risks for media companies pertain to data privacy, especially with regard to how client data is used for marketing purposes, and corporate governance concerns. Governance risks include executive compensation, reporting transparency and corporate complexity. Market recap: Media outperformed the NFI from the start of the year through March as the sector benefitted from optimism about a global recovery from the pandemic. However, the outlook for 2021 looks complicated, especially in Europe, where vaccine rollouts have been slow, and we do not expect a recovery to 2019 levels until 2022, at the earliest. From the start of the year through 31 May, the EUR iBoxx IG Media index significantly outperformed the EUR iBoxx NFI, with a spread tightening of 18bp, to 48bp, compared to tightening of 8bp, to 53bp, for the NFI index. In the last three months, longer-dated media bonds have outperformed, with no clear differentiation by issuer. CMCSA bonds underperformed despite reporting strong results in 1Q21 and may be lagging because they receive no benefit from EU stimulus.

Debt ticker Issuer Rec Amount (weight)

within index Credit profile

trend* Rating Latest research (including link) CMCSA Comcast OW 5,350 (16.8%) Stable A3/A-s/A-s » Daily Credit Briefing - Comcast: DAZN rejects cooperation attempt from Sky - 10 Jun 2021 RELLN RELX Group UW 4,350 (13.7%) Weakening Baa1/BBB+s/BBB+s » Daily Credit Briefing - RELX Group: 1Q21 trading statement confirms weak outlook for Exhibitions - 23 Apr 2021 VIVFP Vivendi UW 4,050 (12.7%) Weakening Baa2/–/BBBn » Daily Credit Briefing - Vivendi: Considering further 10% UMG stake sale - 19 May 2021 PUBFP Publicis MW 3,350 (10.5%) Stable Baa2/BBBs/– » Daily Credit Briefing - Publicis Groupe: Moody's raises outlook to stable - 29 Apr 2021 WPPLN WPP UW 3,350 (10.5%) Stable Baa2/BBBs/– » Daily Credit Briefing - WPP Group: 1Q21 trading statement shows growth rebound - 29 Apr 2021 BERTEL Bertelsmann UW 3,132 (9.9%) Weakening Baa2/BBBs/– » Daily Credit Briefing - Bertelsmann: To merge media units - 18 May 2021

» Daily Credit Briefing - Confirms acquisition of Simon & Schuster - 26 November 2020 WKLNA Wolters Kluwer OW 2,200 (6.9%) Stable Baa1/BBB+s/– » Daily Credit Briefing - Wolters Kluwer: 1Q21 report shows return to pre-pandemic growth - 6 May 2021 DECFP JCDecaux – 1,950 (6.1%) – Baa3/BBB-n/– Not covered INFLN Informa – 1,850 (5.8%) – Baa3/BBB-n/BBB-s Not covered OMC Omnicom – 1,000 (3.1%) – Baa1/BBB+s/– Not covered DISCA Discovery Communications – 600 (1.9%) – Baa3/BBB-s/BBB-s Not covered ITVLN ITV – 600 (1.9%) – Baa3/BBB-n/– Not covered

*This is the analyst's opinion concerning the development (improving/stable/weakening/developing) of the issuer's credit profile over the next 3-6 months. This can be indicated by, among other things, the rating outlook or expected changes in the business profile or the financial profile, as indicated, for example, by credit protection ratios. Source: UniCredit Research

June 2021 Credit & Credit Strategy Research

Euro Credit Pilot

UniCredit Research page 19 See last pages for disclaimer

Technology (Marketweight) Gianfranco Arcovito, CFA, Credit Analyst (UniCredit Bank, Munich) +49 89 378-15449; [email protected]

Weight in iBoxx NFI: Current ASW spread: change mom/YTD: Euro STOXX THE YTD:

4.7%

39bp -2.4/-9.2

+17.3%

Sector drivers: We have a marketweight recommendation on the technology sector. Our recommendation is mainly based on the following factors: 1. the sector has become increasingly non-cyclical – although still growth-oriented – in recent years; 2. the digital transformation in other sectors has been increasing demand for technological components and software solutions; 3. the steady increase in the weight of this sector in bond indices supports its overall economic significance. Technology credit is currently trading tighter than the iBoxx NFI. However, this is somewhat mitigated by the better average rating of the iBoxx Technology index (A+) compared to that of the iBoxx NFI (A-). Credit in the technology sector has some of the longest durations within TMT and overall. Some sub-segments of the technology sector tend to exhibit more cyclicality than others, for example the semiconductor, conventional-software and hardware businesses are subject to discretionary spending. Structural growth drivers in some sub-sectors (e.g. cloud-software and IT-services) not only support volume growth but also affect M&A strategies. Therefore, we expect M&A activity in the sector to remain high. Examples of this are large acquisitions by Capgemini (Altran), IBM (Red Hat) and Infineon (Cypress). A particular mention must go to SAP, which acquired Qualtrics in 2018 and undertook a partial IPO in January, benefiting from a supportive environment and valuations for technology companies.

ESG: The sector is less exposed to environmental considerations than other industries, although energy efficiency will remain a focus for hardware manufacturers, especially those exposed to wireless connectivity and semi-conductors. We see room for improvement in this field, possibly extended to software as a way of optimizing efficiency and reducing consumption. Market recap: Since the start of the year through the end of May, the EUR iBoxx IG Technology index tightened by 7bp to 41bp, in line with the EUR iBoxx NFI, which tightened by 8bp to 53bp. The technology sector continues to trade tight relative to the EUR iBoxx NFI but benefits from structurally higher growth generated by technology companies and credit tends to be shielded by ongoing solid cash generation. Other factors to consider include the development of trade talks between the US and China with the new US administration. In some cases, trade tensions might have positive repercussions on some names in our coverage, such as Ericsson and Nokia, which are benefiting from restrictions being imposed on Huawei. At this point in time, we do not think that the new US administration will relax those restrictions and we do not expect a substantial change of heart in other countries either.

Debt ticker Issuer Rec Amount (weight)

within index Credit profile

trend* Rating Latest research (including link) IBM IBM MW 14,000 (20.0%) Stable A2/A-s/– » Daily Credit Briefing - IBM: S&P downgrades to A- - 7 May 2021

» Sector Flash - Technology: Enterprise software: Mission-critical is key - 24 July 2020 AAPL Apple – 9,300 (13.3%) – Aa1/AA+s/– Not covered SAPGR SAP MW 8,700 (12.4%) Stable A2/As/– » Daily Credit Briefing - SAP: Confirms preliminary figures; cloud revenue and backlog underpin growth - 23 Apr 2021

» Sector Flash - Technology: Enterprise software: Mission-critical is key - 24 July 2020 FIS Fidelity National Information

Services – 6,750 (9.7%) – Baa2/BBBs/BBBp Not covered

CAPFP Cap Gemini MW 6,700 (9.6%) Stable –/BBBs/– » Daily Credit Briefing - CapGemini: 3Q20 revenue in line with consensus expectations - 27 Oct 2020 ASML ASML UW 4,500 (6.4%) Stable A3/–/A-s » Daily Credit Briefing - ASML: Strong 1Q21 sustained by software upgrades to increase production capacity - 21 Apr 2021 DSYFP Dassault Systemes – 3,650 (5.2%) – –/A-s/– Not covered IFXGR Infineon MW 2,900 (4.1%) Improving –/BBB-p/– » Daily Credit Briefing - Infineon: 1Q21 results exceed consensus, guidance increased again - 5 May 2021 AMSSM Amadeus IT MW 2,750 (3.9%) Weakening Baa2/BBB-n/– » Daily Credit Briefing - Amadeus IT: Weak 1Q21 results, but management notes progress in March and April - 10 May 2021 MSFT Microsoft – 2,300 (3.3%) – Aaa/AAAs/AAAs Not covered PRXNA Prosus – 1,600 (2.3%) – –/BBB-p/– Not covered FISV Fiserv – 1,500 (2.1%) – Baa2/BBBs/– Not covered WLNFP Worldline SA – 1,500 (2.1%) – –/BBBs/– Not covered ERICB Ericsson S 1,000 (1.4%) Improving Ba1/BBB-s/BBB-s » Sector Flash - Telecoms: Current themes in the mobile infrastructure and equipment sector - 17 May 2021

June 2021 Credit & Credit Strategy Research

Euro Credit Pilot

UniCredit Research page 20 See last pages for disclaimer

Debt ticker Issuer Rec Amount (weight)

within index Credit profile

trend* Rating Latest research (including link) ATOFP AtoS – 750 (1.1%) – –/BBB+s/– Not covered ORCL Oracle – 750 (1.1%) – Baa2/An/BBB+n Not covered DXC DXC Technology – 650 (0.9%) – Baa2/BBB-s/BBBs Not covered EEFT Euronet Worldwide – 600 (0.9%) – Ba1/BBBn/BBBn Not covered

*This is the analyst's opinion concerning the development (improving/stable/weakening/developing) of the issuer's credit profile over the next 3-6 months. This can be indicated by, among other things, the rating outlook or expected changes in the business profile or the financial profile, as indicated, for example, by credit protection ratios. Source: UniCredit Research

June 2021 Credit & Credit Strategy Research

Euro Credit Pilot

UniCredit Research page 21 See last pages for disclaimer

Automobiles & Parts (Overweight) Dr. Sven Kreitmair, CFA, Head of Credit Research (UniCredit Bank, Munich) +49 89 378-13246, [email protected]

Weight in iBoxx NFI: Current ASW spread: change mom/YTD: Euro STOXX ATO YTD:

10.7%

54bp -6.7/-26.1

+22.2%

Sector drivers: Expectations, as reflected in current company ratings in the sector, are for a recovery of 7-12% yoy in global light-vehicle sales in 2021 and approximately 4-6% yoy in 2022. Industry-specific forecast risks for this scenario are currently supply-chain disruptions like semiconductor shortages, increased raw material prices and subsequent waves of COVID-19 and the resulting lockdowns. In January-April 2021, global car sales were up by 32.4% yoy given base effects from a weak, pandemic-impacted 2020. In the same period, sales in China (+49.6%) again outperformed, followed by the US (+30.0%) and Europe (+23.1%). Given that the recovery towards 2017 global sales figures is expected to take several years, capex plans and capacities at manufacturers and part suppliers have mostly been adjusted, which has led to cost-cutting announcements (including headcount cuts) in the sector. As a result of increased leverage and reduced capacity utilization, consolidation and M&A could again become a topic in the industry, for example at smaller auto-parts suppliers with high powertrain exposure. Captive finance and financial services operations are likely to experience higher residual-value risk and more credit losses but should (as in past crisis periods) display more credit-profile resilience than other segments of the industry. Climate change topics and green policy support, in particular in Europe but also in China, will keep up the growth for electrified vehicles; in the US, the topic is meanwhile also high on the agenda with President Biden’s climate plan. Many countries have pledged to phase out the combustion engine over the coming years, auto manufacturers aim to reduce emissions and EV shares have already increased substantially since 2020, in particular in Europe. Auto parts suppliers are indirectly exposed to climate transition risks through their auto manufacturer customers, in particular if they produce auto parts for combustion engines. Digitalization is another important transformation trend in the auto sector. Trends like connected, shared and autonomous vehicles offer significant business opportunities but come with their own challenges, like necessary technologies, updated infrastructures, 5G standards or questions regarding data ownership or system security.

ESG considerations: Key issues in this sector center around electrification and connected, shared, autonomous vehicle trends. S&P’s qualitative sector listing of the relative environmental exposure (greenhouse gas emissions, waste, pollution and land use) for the auto and auto parts sectors is above average (across all industry sectors), with auto manufacturers having higher exposure and auto suppliers lower exposure. S&P thinks social risks will intensify in the next decade due to changing consumer preferences for transportation as a service and new mobility options that will disrupt car ownership. Market recap: The main outperformers over the last month have been the bonds issued by Nissan and VW (hybrids). The major underperformers have been the senior bonds of Aptiv, as well as longer-dated and better-rated bonds.

Debt ticker Issuer Rec Amount (weight)

within index Credit profile

trend* Rating Latest research (including link) VW Volkswagen OW 49,400 (30.6%) Stable A3/BBB+s/BBB+p » Daily Credit Briefing - Volkswagen: Headlines about possible IPOs of Porsche and battery division - 1 Jun 2021

» Sector Report - Automobiles & Parts/German automakers: Charging batteries - 18 March 2021 DAIGR Daimler OW 30,300 (18.8%) Stable A3/BBB+p/BBB+p » Daily Credit Briefing - Daimler: Sees Automotive EBIT margin now at the upper end of the forecast range ... - 10 May 2021

» Sector Report - Automobiles & Parts/German automakers: Charging batteries - 18 March 2021 BMW BMW MW 21,750 (13.5%) Stable A2/An/– » Daily Credit Briefing - BMW: Partial release of provision with respect to EU antitrust proceedings - 24 May 2021

» Sector Report - Automobiles & Parts/German automakers: Charging batteries - 18 March 2021 STLA Stellantis MW 11,400 (7.1%) Stable Baa3/BBB-s/– » Daily Credit Briefing - Stellantis: 70.5%-owned second-hand car group Aramis plans IPO in 2021 - 1 Jun 2021

» Credit Comment - Stellantis: Positive margin outlook at high available liquidity - 3 Mar 2021 RCIBK RCI Banque OW 8,350 (5.2%) Stable Baa2wn/BBBn/– » Daily Credit Briefing - RCI Banque: FY20 results rather resilient, with low funding needs in 2021 - 16 Jun 2021

» Sector Report - Automotive Credit Conference Handbook - 14 June 2021 TOYOTA Toyota Motor Corp OW 7,050 (4.4%) Stable A1/A+s/A+s » Daily Credit Briefing - Toyota: FY21/22 guidance indicates recovery in credit metrics - 12 May 2021

» Sector Report - Automotive Credit Conference Handbook - 14 June 2021

June 2021 Credit & Credit Strategy Research

Euro Credit Pilot

UniCredit Research page 22 See last pages for disclaimer

Debt ticker Issuer Rec Amount (weight)

within index Credit profile

trend* Rating Latest research (including link) FCABNK FCA Bank MW 5,650 (3.5%) Stable Baa1/BBBs/BBB+n » Daily Credit Briefing - FCA Bank: No dividend payment in FY20 and CET1 was up by 120bp to 15.4% - 14 Jun 2021

» Italian Credit Compendium - Moving along the path to recovery MLFP Michelin UW 4,000 (2.5%) Stable –/A-s/A-s » Daily Credit Briefing - Michelin: Sales in 1Q21 up by 8.3% (before FX) and FY21 guidance confirmed - 27 Apr 2021 HNDA Honda – 3,800 (2.4%) – A3/A-n/As Not covered GMFIN GM Financial MW 3,500 (2.2%) Stable Baa3/BBBn/BBB-s » Daily Credit Briefing - GM Financial/GM: Expects 1H21 results to be significantly better than prior guidance - 4 Jun 2021

» Sector Report - Automotive Credit Conference Handbook - 14 June 2021 CONGR Continental MW 3,225 (2.0%) Stable Baa2/BBBn/BBBs » Daily Credit Briefing - Continental: Excluding Vitesco, FY21 guidance is for FCF of EUR 1.1-1.5bn - 7 May 2021

» Sector Report - Automotive Credit Conference Handbook - 14 June 2021 NSANY NISSAN MOTOR CO., LTD. – 2,000 (1.2%) – Baa3/BBB-n/– Not covered PSABFR PSA Banque France MW 2,000 (1.2%) Stable A3/BBB+n/– » Daily Credit Briefing - PSA Banque France: Resilient FY20 credit metrics, but set-up of Stellantis's ... - 11 Jun 2021

» Sector Report - Automotive Credit Conference Handbook - 14 June 2021 BWA BorgWarner – 1,500 (0.9%) – Baa1/BBBn/BBB+s Not covered RBOSGR Robert Bosch UW 1,500 (0.9%) Stable –/As/– » Daily Credit Briefing - Robert Bosch: FY20 liquidity up to EUR 25.7bn and adjusted gross leverage ... - 26 Apr 2021 HOG Harley-Davidson – 1,250 (0.8%) – Baa3/–/BBB+n Not covered APTV Aptiv MW 1,200 (0.7%) Stable Baa2/BBBs/BBBs » Daily Credit Briefing - Aptiv: Unused USD 2.4bn excess cash position at the end of 1Q21 - 7 May 2021

» Sector Report - Automotive Credit Conference Handbook - 14 June 2021 MGCN Magna OW 1,150 (0.7%) Stable A3/A-n/– » Daily Credit Briefing - Magna International: Net leverage down to 1.74x in 1Q21, above own target of 1-1.5x - 7 May 2021 GM GM MW 750 (0.5%) Stable Baa3/BBBn/BBB-s » Daily Credit Briefing - General Motors (exFinSvcs): Expects 1H21 results to be significantly better than ... - 4 Jun 2021 KNOGR Knorr Bremse UW 750 (0.5%) Stable A2/As/– » Daily Credit Briefing - Knorr Bremse: 2021 guidance confirmed after solid 1Q21 results - 14 May 2021 ALV Autoliv MW 500 (0.3%) Stable Aa3/BBBp/– » Daily Credit Briefing - Autoliv: 1Q21 leverage ratio back at the company's long-term target range - 26 Apr 2021 HELLA Hella MW 500 (0.3%) Stable Baa1/–/– » Daily Credit Briefing - Hella: Hueck family reportedly weighing stake sale - 28 Apr 2021

» Sector Report - Automotive Credit Conference Handbook - 14 June 2021

*This is the analyst’s opinion concerning the development (improving/stable/weakening/developing) of the issuer’s credit profile over the next 3-6 months. This can be indicated by, among other things, the rating outlook or expected changes in the business profile or the financial profile, as indicated, for example, by credit protection ratios. Source: UniCredit Research

June 2021 Credit & Credit Strategy Research

Euro Credit Pilot

UniCredit Research page 23 See last pages for disclaimer

Utilities (Marketweight) Ulrich Scholz, CFA, FRM, Credit Analyst (UniCredit Bank, Munich) +49 89 378-41847, [email protected]

Weight in iBoxx NFI: Current ASW spread: change mom/YTD: Euro STOXX UTI YTD:

16.4%

52bp -3.3/-7.4

+2.0%

Sector drivers: After energy demand weakened in 2020, there has been a recovery in volumes and prices in the current year. At the same time, CO2 prices have reached record levels. Power-generation companies with less-efficient coal power plants will continue to face margin pressure. Within fossil generation, the profitability of gas-fired plants relative to coal-fired plants is expected to further improve. In such a scenario, generators will try to accelerate their transformation strategy and their expansion in renewables. Due to variations in the complexity of approval processes for renewables across Europe, international expansion and regional diversification are increasing. Network operators are facing network-expansion obligations with corresponding investment intensity. To keep credit ratings stable, these transformational processes will require mitigation measures in some cases. The European Green Deal triggers green-bond financing: The EU’s aim to become the world’s first climate-neutral bloc by 2050 will require further increases in capex in renewable-energy generation and electricity networks. The sector’s focus is on investment in renewable energy (in order to replace climate-damaging fuels with more-climate-friendly ones), innovative transport and distribution-network infrastructure and energy efficiency. Most of the 27 EU member states aim to become carbon-neutral by 2050 (Poland has a temporary exemption). Achieving an interim target to reduce greenhouse gases (GHG) by 40% by 2030 will require EUR 260bn of additional investment a year, according to European Commission estimates. In mid-September last year, the European Commission (EC) announced that it would raise its GHG-reduction target to at least 55% by 2030. In April, the EC said that it had reached a provisional agreement to achieve this target. The resulting capex requirements should keep utility companies’ demand for sustainable funding high.

M&A risks: Besides internal growth initiatives, we assume that many utility companies in our coverage are also considering opportunistic M&A transactions. First, in the renewables segment, delays in greenfield projects might be compensated for by M&A deals. Second, utility companies with international growth ambitions might consider M&A transactions to expand outside their home markets. Third, multi-utilities within our coverage could continue to consolidate with smaller players in their respective areas. COVID-19 impact: Though energy volumes and prices are still below pre-COVID-19 levels, we expect to see a significant recovery from 2020’s levels. At the same time, we assume that COVID-19-related one-off charges and bad-debt provisions will come down yoy. Besides the past year’s capacity upgrades in the sector, this will be another major earnings driver in 2021. Market recap: EUR 22.0bn of utility benchmark bonds were issued in the first five months of 2021. This is a 7% increase over EUR 20.6bn issued in the same period in 2020. In the year to date, the iBoxx UTI Sen index has tightened by 8bp to 42bp, while the iBoxx UTI Sub index has tightened to by 13bp to 137bp. Over the last month, bonds in the iBoxx UTI Sub index have widened by 4bp, to 137bp, while bonds in the iBoxx UTI Sen index are unchanged at 42bp.

Debt ticker Issuer Rec Amount (weight)

within index Credit profile

trend* Rating Latest research (including link) ENGIFP Engie MW 19,885 (8.1%) Stable Baa1/BBB+s/A-s » Daily Credit Briefing - Engie: Accelerating renewables expansion to achieve net zero carbon emissions ... - 19 May 2021

» Sector Report - Corporate Hybrids: Moderate further spread tightening despite high new issue activity - 25 Mar 2021 ENELIM Enel OW 18,321 (7.5%) Stable Baa1/BBB+s/A-s » Italian Credit Compendium - Moving along the path to recovery - 12 May 2021

» Sector Report - Corporate Hybrids: Moderate further spread tightening despite high new issue activity - 25 Mar 2021 EOANGR E.ON MW 16,850 (6.9%) Improving Baa2/BBBs/BBB+s » Daily Credit Briefing - E.ON: Outlook 2021 and medium-term delivery plan confirmed - 11 May 2021

» Daily Credit Briefing - E.ON: 2020 results match guidance and confirm progress in debt reduction - 24 Mar 2021 IBESM Iberdrola MW 16,285 (6.6%) Stable Baa1/BBB+s/BBB+s » Daily Credit Briefing - Iberdrola: Alliance with Cummins to develop green hydrogen projects in Iberia - 25 May 2021

» Sector Report - Corporate Hybrids: Moderate further spread tightening despite high new issue activity - 25 Mar 2021 EDF EDF OW 14,092 (5.7%) Weakening A3/BBB+s/A-n » Daily Credit Briefing - EDF: May shut down two more UK nuclear power plants - 14 Jun 2021

» Sector Report - Corporate Hybrids: Moderate further spread tightening despite high new issue activity - 25 Mar 2021 RTEFRA RTE MW 8,900 (3.6%) Stable A3/BBB+s/A-n » Sector Report - Utilities: French utilities - the risks and benefits of a new political landscape - 11 Dec 2017

SEVFP Suez MW 8,303 (3.4%) Weakening Baa1/–/– » Daily Credit Briefing - Suez: Veolia and Suez sign combination agreement - 17 May 2021 » Sector Report - Corporate Hybrids: Moderate further spread tightening despite high new issue activity - 25 Mar 2021

June 2021 Credit & Credit Strategy Research

Euro Credit Pilot

UniCredit Research page 24 See last pages for disclaimer

Debt ticker Issuer Rec Amount (weight)

within index Credit profile

trend* Rating Latest research (including link) VIEFP Veolia Environnement OW 7,600 (3.1%) Weakening Baa1/BBBs/BBBs » Daily Credit Briefing - Veolia Environnement: Veolia and Suez sign combination agreement - 17 May 2021

» Sector Report - Corporate Hybrids: Moderate further spread tightening despite high new issue activity - 25 Mar 2021 TENN Tennet MW 7,350 (3.0%) Stable A3/A-s/– » Daily Credit Briefing - Tennet: Proceeds from green bond issue will back grid expansion plans - 10 Jun 2021

» Sector Report - Corporate Hybrids: Moderate further spread tightening despite high new issue activity - 25 Mar 2021 SRGIM Snam MW 6,654 (2.7%) Stable Baa2/BBB+s/BBB+s » Daily Credit Briefing - Snam: Strategy and full-year guidance confirmed - 14 May 2021

» Daily Credit Briefing - Snam: Raises original 2021 net profit guidance by around 3.5% - 19 Mar 2021 EDPPL EDP OW 6,150 (2.5%) Improving Baa3/BBBs/BBBs » Daily Credit Briefing - EDP: Net debt increase largely due to cash capex and working capital

optimization - 14 May 2021 » Sector Report - Corporate Hybrids: Moderate further spread tightening despite high new issue activity - 25 Mar 2021

NTGYSM Naturgy MW 5,892 (2.4%) Stable Baa2/BBBn/BBBs » Daily Credit Briefing - Naturgy: Resilient 1Q results despite ongoing FX weakness - 29 Apr 2021 » Sector Report - Corporate Hybrids: Moderate further spread tightening despite high new issue activity - 25 Mar 2021

ENBW EnBW MW 5,600 (2.3%) Stable Baa1/A-s/BBB+s » Daily Credit Briefing - EnBW: Downgrade to Baa1 with stable outlook by Moody's - 19 May 2021 » Sector Report - Corporate Hybrids: Moderate further spread tightening despite high new issue activity - 25 Mar 2021

TRNIM Terna MW 5,550 (2.3%) Stable Baa2/BBB+s/– » Daily Credit Briefing - Terna: Committed to delivering on 2021-2025 Industrial Plan - 13 May 2021 » Daily Credit Briefing - Terna: 2021 guidance in line with business plan - 25 Mar 2021

IGIM Italgas OW 4,100 (1.7%) Stable Baa2/–/BBB+s » Daily Credit Briefing - Italgas: Strategic plan to 2027 with stronger focus on network digitization - 16 Jun 2021 » Daily Credit Briefing - Italgas: 2020 results match expectations with capex at new all-time highs - 12 Mar 2021

NGGLN National Grid T 3,750 (1.5%) – –/BBB+s/BBB-s Coverage in transition

SSELN SSE T 3,550 (1.4%) – Baa1/BBB+s/BBBs Coverage in transition » Daily Credit Briefing - SSE: EU antitrust approves innogy takeover by E.ON with conditions, as expected - 18 Sep 2019

FUMVFH Fortum Oyj MW 3,500 (1.4%) Weakening Baa2/BBBn/BBBn » Daily Credit Briefing - Fortum: EBITDA growth includes strong contribution from Uniper - 13 May 2021 » Daily Credit Briefing - Fortum: 2021-2025 business plan targets confirmed - 15 Mar 2021

ACEIM Acea OW 3,400 (1.4%) Stable Baa2/–/BBB+s » Daily Credit Briefing - Acea: Double-digit EBITDA growth and stable net leverage - 13 May 2021 » Daily Credit Briefing - Acea: EBITDA growth supported by regulated activities and is above guidance - 11 Mar 2021

EUROGR Eurogrid MW 3,250 (1.3%) Stable –/BBB+s/– » Daily Credit Briefing - Eurogrid: Higher capex budget for 2021-25 due to accelerated grid expansion - 10 Mar 2021 » Sector Report - Our thoughts on 2021: Transformation strategies driving capex to record levels while ... - 27 Jan 2021

VATFAL Vattenfall UW 3,000 (1.2%) Stable A3/BBB+s/– » Daily Credit Briefing - Vattenfall: Support from higher achieved prices and increased hydropower production - 30 Apr 2021 » Sector Report - Corporate Hybrids: Moderate further spread tightening despite high new issue activity - 25 Mar 2021

VGASDE Vier Gas Transport MW 3,000 (1.2%) Stable –/A-n/– » Vier Gas Transport GmbH – Initiation of coverage - 19 Feb 2021

CTEFRA CTE MW 2,920 (1.2%) Stable –/A-s/– » Sector Report - Utilities: French utilities - the risks and benefits of a new political landscape - 11 Dec 2017

REESM Red Electrica MW 2,900 (1.2%) Stable Baa1/A-s/A-s » Daily Credit Briefing - Red Electrica: 1Q results reflect application of the remuneration parameters ... - 28 Apr 2021 » Daily Credit Briefing - Red Electrica: 2020 results reflect the application of new regulatory parameters - 24 Feb 2021

ORSTED Orsted UW 2,867 (1.2%) Stable –/BBB+s/BBB+s » Daily Credit Briefing - Orsted: Objective to reach 50GW of installed capacity by 2030 - 3 Jun 2021 » Sector Report - Corporate Hybrids: Moderate further spread tightening despite high new issue activity - 25 Mar 2021

ESBIRE Electricity Supply Board – 2,800 (1.1%) – A3/A-s/– Not covered

June 2021 Credit & Credit Strategy Research

Euro Credit Pilot

UniCredit Research page 25 See last pages for disclaimer

Debt ticker Issuer Rec Amount (weight)

within index Credit profile

trend* Rating Latest research (including link) CHGRID State Grid – 2,600 (1.1%) – A1/A+s/A+s Not covered

ENEXIS Enexis – 2,500 (1.0%) – Aa3/A+wn/– Not covered

IREIM Iren MW 2,500 (1.0%) Stable –/–/BBBs » Daily Credit Briefing - Iren: Growth driven by energy and waste activities - 14 May 2021 » Daily Credit Briefing - Iren: Higher 2021 capex budget reflects organic growth leveraging - 26 Mar 2021

ELIATB Elia Transmission Belgium SA – 2,350 (1.0%) – Not covered

ENGSM Enagas UW 2,350 (1.0%) Stable Baa2/BBB+n/BBB+n » Sector Flash - Utilities: Role of gas and nuclear activities in EU taxonomy rules yet to be decided - 27 Apr 2021 » Daily Credit Briefing - Enagas: 2020 results slightly below consensus - 23 Feb 2021

ENAPHO EP Infrastructure OW 2,350 (1.0%) Stable Baa3/BBBs/BBB-s » Sector Flash - Utilities: Role of gas and nuclear activities in EU taxonomy rules yet to be decided - 27 Apr 2021 » Daily Credit Briefing - EP Infrastructure: Successful issuance of EUR 500mn 10Y senior bond - 03 Mar 2021

FIREIT 2i Rete Gas OW 2,330 (0.9%) Stable Baa2/BBBs/– » Italian Credit Compendium - Moving along the path to recovery - 12 May 2021 » Daily Credit Briefing - 2i Rete Gas: Proceeds from bond issue to support growth initiatives - 2 Feb 2021

CEZCP CEZ MW 2,225 (0.9%) Stable Baa1/A-s/A-s » Daily Credit Briefing - CEZ: CEZ targets CZK 80-85bn in EBITDA in 2030, which implies a CAGR of 3.4-4.1% - 21 May 2021 » Daily Credit Briefing - CEZ: 2021 EBITDA guidance reflects planned disposals - 17 Mar 2021

STATK Statkraft MW 2,200 (0.9%) Weakening A3/A-s/BBB+s » Daily Credit Briefing - Statkraft: High Nordic power prices lead to all-time high underlying EBIT - 7 May 2021 » Daily Credit Briefing - Statkraft: Hydro reservoir filling in the Nordics normalized in early 2021 - 19 Feb 2021

FLUVIU FLUVIUS – 2,150 (0.9%) – A3/–/– Not covered

STEDIN Stedin – 2,000 (0.8%) – –/A-s/– Not covered

CDTFIN Cadent Gas – 1,875 (0.8%) – –/BBB+s/BBB-s Not covered

ANVAU AusNet Services – 1,760 (0.7%) – A3/A-s/BBB+s Not covered

HERIM Hera MW 1,641 (0.7%) Stable Baa2/BBB+s/– » Daily Credit Briefing - Hera: Increased cash generation reduces leverage - 14 May 2021 » Daily Credit Briefing - Hera: Focus on sustainable growth initiatives confirmed - 25 Mar 2021

YANTZE China Three Gorges Corporation

– 1,350 (0.6%) – A1/As/A+s Not covered

AQUASM FCC Aqualia – 1,350 (0.6%) – –/–/BB+p Not covered

NEGANV Nederlandse Gas – 1,150 (0.5%) – A1/AA-s/– Not covered

NATUEN NorteGas – 1,125 (0.5%) – –/BBB-s/– Not covered

CZGRID Czech Gas Networks OW 1,100 (0.4%) Stable –/BBB+s/BBBs » Sector Report - Our thoughts on 2021: Transformation strategies driving capex to record levels while ... - 27 Jan 2021 » Sector Report - Czech/Slovak utilities: supportive regulation and modest investment requirements - 30 October 2020

ERGIM ERG MW 1,100 (0.4%) Stable –/–/BBB-s » Daily Credit Briefing - ERG: Business plan with re-leveraging while remaining committed to IG rating - 17 May 2021 » Daily Credit Briefing - ERG: Increasing profitability and investment activity in 2021 - 15 Mar 2021

SO Southern – 1,100 (0.4%) – Baa1/An/BBB+s Not covered

RENEPL REN – 1,050 (0.4%) – Baa3/BBBs/BBBs Not covered

June 2021 Credit & Credit Strategy Research

Euro Credit Pilot

UniCredit Research page 26 See last pages for disclaimer

Debt ticker Issuer Rec Amount (weight)

within index Credit profile

trend* Rating Latest research (including link) TEREGA Terega – 1,050 (0.4%) – Baa3/–/– Not covered

VIESGO Viesgo – 1,050 (0.4%) – –/BBB-s/– Not covered

ALLRNV Alliander (Nuon) T 1,000 (0.4%) – Aa3/AA-wn/– Coverage in transition » Daily Credit Briefing - Alliander: Recommendation changes – 3 Apr 2018

CHGDNU CGNPC International – 1,000 (0.4%) – A2/A-s/As Not covered

ENGALL Engie Alliance – 1,000 (0.4%) – Baa1/BBB+s/– Not covered

SPPEUS Eustream MW 1,000 (0.4%) Stable Baa2/–/A-s » Sector Report - Utilities: Our thoughts on 2021 - Transformation strategies driving capex to record ... - 27 Jan 2021 » Daily Credit Briefing - Eustream: Nebt debt reduction despite decline in transported volumes - 30 Nov 2020

PLNIJ PLN – 1,000 (0.4%) – Baa2/BBBn/BBBs Not covered

REDEXS Redexis Gas – 1,000 (0.4%) – Baa3/–/– Not covered

STATNE Statnett – 1,000 (0.4%) – A2/A+s/– Not covered

VERAV Verbund UW 1,000 (0.4%) Stable A3/As/– » Daily Credit Briefing - Verbund: Completion of acquisition of 51% stake in GCA - 1 Jun 2021 » Daily Credit Briefing - Verbund: New green SLB is a novelty in the green financing segment - 25 Mar 2021

ELIASO Elia – 700 (0.3%) – –/BBB+s/– Not covered

AUSGF Ausgrid – 650 (0.3%) – Baa1/BBBs/– Not covered

CKINF CK Infrastructure Holdings – 600 (0.2%) – –/As/A-s Not covered

GALPNA Galp Gas Natural Distribuicao

– 600 (0.2%) – –/BBB-s/– Not covered

ORGAU Origin Energy – 600 (0.2%) – Baa2/BBBn/BBBs Not covered

AEMSPA A2A MW 500 (0.2%) Stable Baa2/BBBs/– » Daily Credit Briefing - A2A: LGH minority shareholders accept merger proposal - 15 Jun 2021 » Daily Credit Briefing - A2A: Confirms its confidence in its 2021-2030 business plan - 19 Mar 2021

ACQUIU Acquirente Unico – 500 (0.2%) – –/BBBs/– Not covered

BEIENT Beijing Enterprises – 500 (0.2%) – Baa1/BBB+s/– Not covered

BOGAEI Bord Gais Eireann – 500 (0.2%) – A2/As/– Not covered

CNGEST Canal de Isabel II Gestion – 500 (0.2%) – Baa1/–/BBB+s Not covered

CARUNA Caruna Networks – 500 (0.2%) – –/BBB+s/– Not covered

ELEVER Elenia Verkko Oyj – 500 (0.2%) – Not covered

EWE EWE MW 500 (0.2%) Stable Baa1/–/– » Daily Credit Briefing - EWE: Higher capex to be carbon-neutral by 2035 - 29 Apr 2021 » Daily Credit Briefing - EWE: Outlook change to stable by Moody's - 10 Feb 2021

NTPCIN NTPC – 500 (0.2%) – Baa3/BBB-s/BBB-n Not covered

June 2021 Credit & Credit Strategy Research

Euro Credit Pilot

UniCredit Research page 27 See last pages for disclaimer

Debt ticker Issuer Rec Amount (weight)

within index Credit profile

trend* Rating Latest research (including link) SGSPAA SGSP – 500 (0.2%) – A3/A-s/– Not covered TPEPW Tauron Polska Energia – 500 (0.2%) – –/–/BBB-s Not covered

*This is the analyst's opinion concerning the development (improving/stable/weakening/developing) of the issuer's credit profile over the next 3-6 months. This can be indicated by, among other things, the rating outlook or expected changes in the business profile or the financial profile, as indicated, for example, by credit protection ratios. Source: UniCredit Research

June 2021 Credit & Credit Strategy Research

Euro Credit Pilot

UniCredit Research page 28 See last pages for disclaimer

Oil & Gas (Overweight) Christian Aust, CFA, Head of Corporate Credit Research (UniCredit Bank, Munich) +49 89 378-17564, [email protected]

Weight in iBoxx NFI: Current ASW spread: change mom/YTD: Euro STOXX OIG YTD:

8.6%

73bp -0.8/-1.0

+13.0%

Sector drivers: On the back of a YTD average Brent price of above USD 64/bbl and our year-end 2021 forecast of USD 60/bbl, we expect all covered Oil & Gas producers to generate sufficiently positive cash flow, allowing them to reduce leverage and remunerate shareholders via dividends and share buybacks without exerting pressure on metrics. We note that most shareholder-remuneration policies are now linked to certain oil-price levels or the achievement of a certain net-debt or gearing target. On balance, however, we project that the sector will maintain its focus on cash flow and cost-preservation measures in FY21.

ESG considerations: European oil and gas producers have set ambitious targets to reduce net carbon emissions. While many producers aim to achieve net zero carbon emissions by 2050 (or before), we note that near-term initiatives are mainly focused on scope 1 and 2 emissions. COVID-19 has accelerated the energy transformation towards greener energy and the generation of electricity from renewable sources. The transformation also puts pressure on European oil and gas companies to diversify away from traditional, core upstream oil and gas production, also via (medium) M&A or asset rotation. Regulators’ (including central banks), investors’ and the general public’s scrutiny of the European oil and gas industry with regard to necessary improvement of environmental, social and governance (ESG) factors will only tighten, in our view. Rating agencies also started to incorporate the longer-term risk from the energy transition into sector ratings in 1Q21 (although not in a consistent fashion, in our view). Market recap: Since the end of March, the iBoxx EUR Oil & Gas index has widened by 1bp and has thus underperformed the 5bp tightening of the iBoxx EUR NFI index. This underperformance was mainly driven by long-dated sector bonds.

Debt ticker Issuer Rec Amount (weight)

within index Credit profile