Embed Size (px)

Citation preview

Assist.Anurak ThongsukhowongAssist.Anurak Thongsukhowong

Faculty of Management ScienceFaculty of Management ScienceKhon Kean UniversityKhon Kean UniversityTel.Tel. 043043--202401202401 Ext.Ext. 164164Tel. Tel. 043043 202401 202401 Ext. Ext. 164164

Fax. Fax. 043043--202402202402EE--mail:mail: [email protected]@kku.ac.thEE mail: mail: [email protected]@kku.ac.th

Website: http://home.kku.ac.th/anutonWebsite: http://home.kku.ac.th/anuton

1

Energy project appraisal and management

2

Financial AnalysisFinancial AnalysisCommon Size AnalysisCommon Size Analysis

Trend Percentage Analysisg y

Ratio Analysis

Method of Evaluating Capital Investment

3

Common Size Analysis

Common Size Analysis

เปนการลดตวเลขของแตล รายการทปรากฏในงบ เปนการลดตวเลขของแตละรายการทปรากฏในงบแสดงฐานะการเงนและงบกาไรขาดทนใหเปนอตรารอยละของสนทรพยรวม หนสนและทนรวม หรอตอยอดขายสทธ เพอเนนใหเหนถงการเปลยนแปลงในสวนผสมหรอสทธ เพอเนนใหเหนถงการเปลยนแปลงในสวนผสมหรอโครงสรางงบการเงน ซงจะชวยใหเหนถงการเปลยนแปลงในโครงสรางของงบการเงนไดเปนอยางด

4

Common Size Analysis

บรษท ตวอยาง จากดงบแสดงฐานะการเงนเปรยบเทยบและการยอสวนตามแนวดง

ณ วนท 31 ธนวาคม 2550 - 2555

สนทรพย

รายการ 31 ธนวาคม (พนบาท) 31 ธนวาคม (%)2550 2551 2552 2553 2554 25552550 2551 2552 2553 2554 2555

สนทรพยหมนเวยน เงนสด เงนลงทนชวคราว

6.1 2.6 4.3 4.0 4.7 5.262.1 28.2 58.6 59.0 74.2 83.4

3 4 9 7 2 9 2 7 2 5 2 833 7 105 1 39 6 39 8 39 5 44 9 เงนลงทนชวคราว ลกหนการคา (สทธ) สนคา

3.4 9.7 2.9 2.7 2.5 2.833.7 105.1 39.6 39.8 39.5 44.9

25.7 42.1 14.9 15.6 17.1 18.2263.1 261.1 203.3 230.3 269.9 291.9

17.8 18.2 16.1 16.4 17.0 15.8182.4 197.2 219.6 219.6 268.3 253.4

ป

สนทรพยหมนเวยนอน ๆรวมสนทรพยหมนเวยน

2.5 5.6 3.7 3.5 3.3 2.225.6 60.7 50.5 51.6 52.1 35.2

55.5 60.2 41.9 42.2 44.6 44.2566.9 652.3 571.6 622.6 704.0 708.8 ทดน อาคาร และอปกรณ สนทรพยอน ๆ

รวมสนทรพย

42.4 39.4 50.0 46.8 45.3 44.9433.5 426.9 682.2 690.4 715.1 720.1

2.1 0.4 8.1 11.0 10.1 10.921.6 4.3 110.5 162.3 159.4 174.8

100 0 100 0 100 0 100 0 100 0 100 01 022 0 1 083 5 1 364 3 1 475 3 1 578 5 1 603 7

5

รวมสนทรพย 100.0 100.0 100.0 100.0 100.0 100.01,022.0 1,083.5 1,364.3 1,475.3 1,578.5 1,603.7

Common Size Analysis

หนสนและสวนของผถอหนรายการ 31 ธนวาคม (พนบาท) 31 ธนวาคม (%)

2550 2551 2552 2553 2554 25552550 2551 2552 2553 2554 2555หนสนและสวนของผถอหนหนสนหมนเวยนเจาหนการคา

18.0 17.3 13.3 11.7 9.6 10.0184.4 187.5 181.4 172.6 151.5 160.4ตวเงนจายหนสนหมนเวยนอนรวมหนสนหมนเวยน

5.2 5.2 7.7 6.0 3.9 2.752.7 56.3 105.1 88.5 61.6 43.3

2.6 6.8 1.4 1.7 2.2 1.826.3 73.7 19.1 25.1 34.7 28.8

25.8 29.3 22.4 19.4 15.7 14.5263.4 317.5 305.6 286.2 247.8 232.5

หนสนระยะยาวรวมหนสนหมนเวยน

รวมหนสน

25.8 29.3 22.4 19.4 15.7 14.5263.4 317.5 305.6 286.2 247.8 232.5

14.7 15.0 19.5 16.3 14.5 12.5150.0 162.5 266.0 240.5 228.9 200.5

40.5 44.3 41.9 35.7 30.2 27.0413.4 480.0 571.6 526.7 475.7 433.0 สวนของผถอหนหนสามญ (100 บาท)สวนเกนมลคาหนสามญ

39.1 39.2 38.5 42.0 39.3 38.7400.0 425.0 525.0 620.0 620.0 620.0

5 9 6 5 8 8 10 8 10 1 10 060 0 70 0 120 0 160 0 160 0 160 0สวนเกนมลคาหนสามญกาไรสะสมรวมสวนของผถอหน

5.9 6.5 8.8 10.8 10.1 10.060.0 70.0 120.0 160.0 160.0 160.014.5 10.0 10.8 11.5 20.4 24.3148.6 108.5 147.7 168.6 321.8 390.7

59.5 55.7 58.1 64.3 69.8 73.0608.6 603.5 792.7 948.6 1,101.8 1,170.7

6รวมหนสนและสวนของผถอหน

100.0 100.0 100.0 100.0 100.0 100.01,022.0 1,083.5 1,364.3 1,475.3 1,578.5 1,603.7

พนบาท1 600

Common Size Analysis

1 200

1,400

1,600

800

1,000

1,200

%800

600

%100

Year

200

400

0

75

2550 2551 2552 2553 2554 2555Year0

สนทรพยหมนเวยน

50

สนทรพยหมนเวยน

ทดน อาคาร และอปกรณ

สนทรพยอน

25

72550 2551 2552 2553 2554 2555Year0

พนบาท1 600

Common Size Analysis

1 200

1,400

1,600

800

1,000

1,200

%800

600

%100

Year

200

400

0

75

Year0

หนสนหมนเวยน

502550 2551 2552 2553 2554 2555

หนสนหมนเวยน

หนสนระยะยาว

สวนของผถอหน

25

8

Year0

2550 2551 2552 2553 2554 2555

Trend Percentage Analysis

Trend Percentage Analysis เปนการวเคราะหทศทางความเปนไปไดของรายการตาง ๆ ท เปนการวเคราะหทศทางความเปนไปไดของรายการตาง ๆ ทปรากฏในงบการเงน ซงตองอาศยงบการเงนของชวงเวลาหลาย

ป ป ป โ ๆ ปตอเนองกน เพอนามาสรปเปนขอคดเหนวาแนวโนมทางการเงนและการดาเนนงานเปนทนาพอใจหรอไมวเคราะหแนวโนมจากขอมลเดม

เปนการศกษาแนวโนมจากขอมลทใหมาโดยตรง เชน เปน

วเคราะหอตรารอยละของแนวโนม

เปนการศกษาแนวโนมจากขอมลทใหมาโดยตรง เชน เปนจานวนเงน (บาท) นาหนก (กโลกรม) เปนตน

วเคราะหอตรารอยละของแนวโนมเปนการศกษาแนวโนมโดยปรบขอมลเปนรอยละกอนการ

9

เปรยบเทยบ

วเคราะหแนวโนมจากขอมลเดมTrend Percentage Analysisวเคราะหแนวโนมจากขอมลเดม

Net Sales 813 854 860 1,201 1,341 1,4922550 2551 2552 2553 2554 2555

Change of Net Sales, , ,

41 6 341 140 151

1 500

Bahts

1,400

1,500

1,200

800

1,000

2550 2551 2552 2553 2554 2555Year0

10

2550 2551 2552 2553 2554 2555

วเคราะหอตรารอยละของแนวโนมTrend Percentage Analysisวเคราะหอตรารอยละของแนวโนม

อตรารอยละของปฐานเคลอนท (Progressive year horizontal trend analysis)horizontal trend analysis)เปนการคานวณอตรารอยละของการเพมหรอลดของรายการนน ๆ ใ ในแตละชวงเวลาทผานมา

gtXt Xt-1

X= (100)-

Xt-1

g2546X2546 X2545

X= (100) = 5%854 813

813(100)- -

=X2545

g2547X2547 X2546= (100) = 1%

813

- =860 854 (100)-g2547

X2546= (100) = 1%= 854

(100)

11

Trend Percentage Analysis

Net Sales 813Increase Rate (%)

854 860 1,201 1,341 1,4925 1 40 12 11

2550 2551 2552 2553 2554 2555

40

%

30

20

10

Year2551 2552 2553 2554 2555

12

วเคราะหอตรารอยละของแนวโนมTrend Percentage Analysisวเคราะหอตรารอยละของแนวโนม

อตรารอยละของปฐาน (Simple base year horizontal trend analysis)horizontal trend analysis)

XgtXtXb

= (100)

g X2546 (100) 105%854 (100)g2546X2546X2545

= (100) = 105%854813

(100) =

g X2547 (100) 106%860 (100)g2547X2547X2545

= (100) = 106%860813

(100) =

13

Trend Percentage Analysis

Net Sales 813Base year Rate (%)

854 860 1,201 1,341 1,492105 106 148 165 184100

2550 2551 2552 2553 2554 2555

%

Base year Rate (%) 105 106 148 165 184100

175

125

150

100

Year02550 2551 2552 2553 2554 2555

14

นาความสมพนธของงบการเงนมาเทยบRatio Analysis

Liquidity Rations

Ratio Analysis นาความสมพนธของงบการเงนมาเทยบสดสวน และอธบายผล

Current RatiosLiquidity RationsQuick/Acid test RatiosInventory Turnover RatioDays Sales Outstanding (DSO)Asset Management Ratios Days Sales Outstanding (DSO)Fixed Assets Turnover RatioTotal Assets Turnover Ratio

Debt Management RatiosTotal Debt to Total AssetsTimes Interest Earned (TIE)EBITDA Coverage Ratio

Profitability Ratios

EBITDA Coverage RatioProfit Margin on SalesBasic Earning Power (BEP)Return on Total Assets (ROA)Return on Total Assets (ROA)Return on Common Equity (ROE)

Price Earnings Ratios (P/E Ratio)15

Market Value Ratios Price Earnings Ratios (P/E Ratio)Price/Cash Flow RatioMarket/Book Ratio (M/B Ratio)

Liquidity Ratios Debt Management Ratios

Ratio Analysisq yCurrent Ratios

Current AssetsCurrent Liabilities

gTotal Debt to Total Assets

Total DebtTotal Assets

Quick/Acid test RatiosCurrent Assets - Inventories

Current Liabilities

Times Interest Earned (TIE)Earnings Before Interest and Taxes

Interest ChargeEBITDA Coverage Ratio

Asset Management RatiosInventory Turnover Ratio

Sales

EBITDA Coverage RatioEBITDA + Lease payments

Interest + Loan repayments + Lease paymentsP fit bilit R ti

Days Sales Outstanding (DSO)Inventories

Account Receivables

Profitability RatiosProfit Margin on SalesNet income available to Common Stockholder

SalesAverage sales per dayFixed Assets Turnover Ratio

Sales

Basic Earning Power (BEP)Sales

EBITTotal Assets

R t T t l A t (ROA)Total Assets Turnover RatioNet Fixed Assets

SalesT t l A t

Return on Total Assets (ROA)

Return on Common Equity (ROE)

Net IncomeTotal Assets

16

Total Assets Return on Common Equity (ROE)Net income Available to Common Stockholder

Common equity

Market Value Ratios

Ratio AnalysisMarket Value Ratios

Price Earnings Ratios (P/E Ratio)Price per share

Earning per sharePrice/Cash Flow RatioEarning per share

Price per shareC fCash flow per shareMarket/Book Ratio (M/B Ratio)Market price per share Common equityMarket price per share

Book value per shareCommon equity

Share outstanding

17

Ratio AnalysisABC Co.,Ltd.

2011 2010

,Income Statement

For the year Ending December 31, 2010-2011 Unit: millions of Bahts

Net sales 3,000.0 2,850.0Operating costs excluding depreciation and amortizationEarnings before interests. Taxes. Depreciation, and amortization (EBITDA)DepreciationAmortization

, ,2,616.2 2,497.0

383.8 353.0100.0 90.0

0.0 0.0Depreciation and amortizationEarnings before interest and taxes (EBIT, or operating income)Less InterestEarning before taxes (EBT)

100.0 90.0283.8 263.088.0 60.0

195.8 203.0Earning before taxes (EBT)Less Taxes (40%)Net income before preferred dividendsLess Preferred dividendsNet income

195.8 203.078.3 81.0

117.5 122.04.0 4.0

113.5 117.8Net incomeCommon dividendsAddition to retained earningsPer-share data:

Common stock price

113.5 117.857.5 53.056.0 64.8

23.00 26.00Common stock priceEarnings per share (EPS)Dividends per share (DPS)Book value per share (BVPS)Cash flow per share (CFPS)

23.00 26.002.27 2.361.15 1.06

17.92 16.804.27 4.16

18

Cash flow per share (CFPS) 4.27 4.16

**Loan repayments 20.0

Ratio Analysis

Earnings per share (EPS)Net income

= Common shares outstanding113 500 000

Dividends per share (DPS) =Dividends paid to common stockholders

113,500,00050,000,000

= 2.27

Dividends per share (DPS) = Common shares outstanding57,500,00050,000,000

= 1.15

Book value per share (BVPS) =Total common equity

Common shares outstanding896,000,00050 000 000

= 17.92

Cash flow per share (CFPS) =Net income + Depreciation + Amortization

Common shares outstanding

50,000,000

213,500,00050,000,000

= 4.27

19

Ratio AnalysisABC Co.,Ltd.,

Statement of Retained EarningsFor the year Ending December 31, 2011

Balance of retained earnings, 12/31/05 710.0 Add N t i 2006 113 5Add: Net income, 2006 113.5Less: Dividends paid (57.5)

Balance of retained earnings, 12/31/06 766.0

Assets 2011 2010 Liabilities and Equity 2011 2010

ABC Co.,Ltd.Balance Sheet

December 31, 2010-2011 Unit: millions of Bahts

Cash and marketable securities

Assets 2011 2010 Liabilities and Equity 2011 2010

Accounts receivableInventories

Accounts payableNotes payableAccruals

10 80375 315615 415

3060110 60140 130

Total current assetsNet plant and equipment

AccrualsTotal current liabilities

Long-term bondsTotal Debt

615 4151,000 8101,000 870

140 130310 220754 580

1,064 800Total DebtPreferred stock (400,000 shares)Common stock (50,000,000 shares)

Retained earnings

1,064 80040 40

130 130766 710

20Total common equityTotal liabilities and equityTotal assets 2,000 1,680

896 8402,000 1,680

Ratio AnalysisLiquidity Ratios Calculation Ratio Industry Ave.Liquidity Ratios

Current RatiosQuick/Acid test Ratios

Asset Management Ratios

1,000/310385/310

=3.2x=1.2x

4.2x2.1x

Inventory Turnover RatioDays Sales Outstanding (DSO)Fixed Assets Turnover Ratio

g3,000/615375/8.3333,000/1,000

=4.9x=45days=3.0x

9.0x36days

3.0xTotal Assets Turnover Ratio

Debt Management RatiosTotal Debt to Total Assets

3,000/2,000

1,604/2,000

=1.5x

=53.2%

1.8x

40.0%Times Interest Earned (TIE)EBITDA Coverage Ratio

Profitability Ratios

283.8/88411.8/136

=3.2x=3.0x

6.0x4.3x

o tab ty at osProfit Margin on SalesBasic Earning Power (BEP)Return on Total Assets (ROA)

113.5/3,000283.8/2,000113.5/2,000

=3.8%=14.2%=5.7%

5.0%17.2%

9.0%Return on Total Assets (ROA) 113.5/2,000 5.7% 9.0%

Market Value RatiosPrice Earnings Ration (P/E Ratio) 23.0/2.27 =10.1x 12.5x

Return on Common Equity (ROE) 113.5/896 =12.7% 15.0%

21

Price Earnings Ration (P/E Ratio)Price/Cash Flow RatioMarket/Book Ratio (M/B Ratio)

23.0/2.2723.0/4.2723.0/17.92

10.1x=5.4x=1.3x

12.5x6.8x

17x

Ratio Analysis

Du Pont ChartReturn on Equity 12.7%

Return on Assets 5.7% Asset/Equity 2.23Multiplied by

Profit Margin 3.8% Total Assets Turn over 1.5Multiplied by

Sales Net incomeDividend Sales Total AssetsDividend3,000 113.5into

Net incomeSubtractedTotal Costs

3,000 2,000into

Current Add Fixed Assets113.5from2,886.5

Other Operating Interest plus Preferred

Assets 1,000to1,000

Cash and Accounts Inventory Costs 2,616.2 Dividends 92

Depreciation 100 Taxes 78.3

Marketable Securities 10

Receivable 375

615

22

Method of Evaluating Capital Investment

Method of Evaluating Capital Investment

Average rate of return methodCash payback methodCash payback methodNet preset value methodInternal rate of return method

Cash payback method

Average rate ofreturn method

46%

71% Source : Robert A. Howell, J D B St h R

Internal rate of return method

Net present value method

p y

64%

69%

James D. Brown, Stephen R. Soucy, and Allen H. Seed, Management Accounting in the New/Manufacturing Environment, National Association of Accountants and Computer Aided Manufacturing I t ti l M t l N

230 10 20 30 40 50 60 70 80 90 100Percentage of Respondents Using the Method

International, Montvale, New Jersey, 1987.

Method of Evaluating Capital InvestmentAverage Rate of Return MethodThe average rate of return, sometimes called the accounting rate of return, is a measure of the average income as a per cent of the

Average Rate of Return Method

average investment in fixed assets. The average rate of return is determined by using the following equation:

Estimated average annual incomeAverage rate of return =

Estimated average annual income

Average investment

To illustrate, assume that management is considering the purchase of a machine at a cost of $500,000. The machine is expected to have a useful life of 4 years, with no residual value, p y , ,and to yield total income of $200,000.

Average rate of return = $200,000/4 = 20%Average rate of return = ,($500,000+$0)/2

= 20%

24

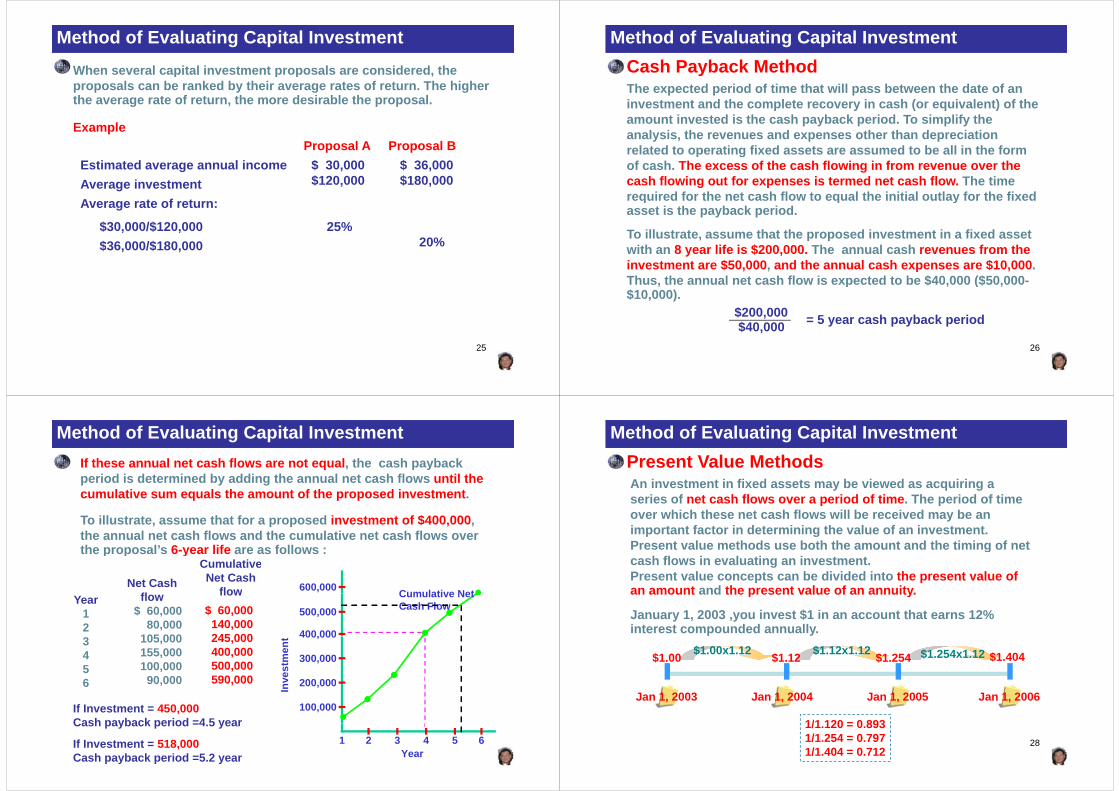

Method of Evaluating Capital InvestmentWhen several capital investment proposals are considered theWhen several capital investment proposals are considered, the proposals can be ranked by their average rates of return. The higher the average rate of return, the more desirable the proposal.

ExampleProposal A Proposal B

Estimated average annual incomeAverage investment

$ 30,000 $ 36,000$120,000 $180,000

Average rate of return:

$30,000/$120,000$36 000/$180 000

25%20%$36,000/$180,000 20%

25

Method of Evaluating Capital InvestmentCash Payback MethodThe expected period of time that will pass between the date of an investment and the complete recovery in cash (or equivalent) of the

Cash Payback Method

amount invested is the cash payback period. To simplify the analysis, the revenues and expenses other than depreciation related to operating fixed assets are assumed to be all in the form p gof cash. The excess of the cash flowing in from revenue over the cash flowing out for expenses is termed net cash flow. The time required for the net cash flow to equal the initial outlay for the fixedrequired for the net cash flow to equal the initial outlay for the fixed asset is the payback period.

To illustrate, assume that the proposed investment in a fixed asset with an 8 year life is $200,000. The annual cash revenues from the investment are $50,000, and the annual cash expenses are $10,000. Thus, the annual net cash flow is expected to be $40,000 ($50,000-us, t e a ua et cas o s e pected to be $ 0,000 ($50,000$10,000).

$200,000$40 000 = 5 year cash payback period

26

$40,000

Method of Evaluating Capital InvestmentIf these annual net cash flows are not equal the cash paybackIf these annual net cash flows are not equal, the cash payback period is determined by adding the annual net cash flows until the cumulative sum equals the amount of the proposed investment.

To illustrate, assume that for a proposed investment of $400,000, the annual net cash flows and the cumulative net cash flows over the proposal’s 6-year life are as follows :the proposal s 6-year life are as follows :

Net Cash fl

Cumulative Net Cash

flow 600,000 Cumulative NetYear12

flow$ 60,000

80,000105 000

flow$ 60,000140,000245 000 400,000

500,000

Cumulative Net Cash Flow

3456

105,000155,000100,000

90 000

245,000400,000500,000590 000 ve

stm

ent

200 000

300,000

400,000

6 90,000 590,000

If Investment = 450,000Cash payback period =4 5 year

100,000

Inv 200,000

27

Cash payback period =4.5 year

If Investment = 518,000Cash payback period =5.2 year

1 2 3 4 5 6Year

Method of Evaluating Capital InvestmentPresent Value MethodsPresent Value MethodsAn investment in fixed assets may be viewed as acquiring a series of net cash flows over a period of time. The period of time over which these net cash flows will be received may be an important factor in determining the value of an investment. Present value methods use both the amount and the timing of net gcash flows in evaluating an investment. Present value concepts can be divided into the present value of an amount and the present value of an annuity.an amount and the present value of an annuity.

January 1, 2003 ,you invest $1 in an account that earns 12% interest compounded annually.

$1.00x1.12 $1.12x1.12 $1.254x1.12$1.00 $1.12 $1.254 $1.404

Jan 1, 2003 Jan 1, 2004 Jan 1, 2005 Jan 1, 2006

1/1 120 = 0 89328

1/1.120 = 0.8931/1.254 = 0.7971/1.404 = 0.712

Method of Evaluating Capital InvestmentPresent Value of $1 at Compound InterestPresent Value of $1 at Compound Interest

Year 6% 10% 12% 15% 20%

1 0.943 0.909 0.893 0.870 0.833Example2 0.890 0.826 0.797 0.756 0.694

3 0.840 0.751 0.712 0.658 0.5794 0.792 0.683 0.636 0.572 0.4825 0.747 0.621 0.567 0.497 0.4026 0 705 0 564 0 507 0 432 0 335

January 1, 2003 ,Present value of a $100 annuity for five periods at 12%

Example

6 0.705 0.564 0.507 0.432 0.3357 0.665 0.513 0.452 0.376 0.2798 0.627 0.467 0.404 0.327 0.2339 0.592 0.424 0.361 0.284 0.19410 0.558 0.386 0.322 0.247 0.162

could be determined by using the present value factors.

Jan 1, 2003 Dec 1, 2003 Dec 1, 2004 Dec 1, 2005 Dec 1, 2006 Dec 1, 2007

Present value of amount $100$100 $100 $100 $100

$89.30 $100x0.893$100 0 797

$79.70$71.20$63.60

$100x0.712

$100x0.636

$100x0.797

29

$63 60$56.70

$360.50

$100x0.567

$100x3.605

Method of Evaluating Capital Investment

Present Value of $1 at Compound Interest

Year 6% 10% 12% 15% 20% Present Value of an Annuity of$1 at Compound Interest

1 0.943 0.909 0.893 0.870 0.8332 0.890 0.826 0.797 0.756 0.6943 0 840 0 751 0 712 0 658 0 579

Year 6% 10% 12% 15% 20%

1 0.943 0.909 0.893 0.870 0.8333 0.840 0.751 0.712 0.658 0.5794 0.792 0.683 0.636 0.572 0.4825 0.747 0.621 0.567 0.497 0.4026 0.705 0.564 0.507 0.432 0.335

2 1.833 1.736 1.690 1.626 1.5283 2.673 2.487 2.402 2.283 2.1064 3.465 3.170 3.037 2.855 2.5895 4.212 3.791 3.605 3.353 2.991

7 0.665 0.513 0.452 0.376 0.2798 0.627 0.467 0.404 0.327 0.2339 0.592 0.424 0.361 0.284 0.19410 0.558 0.386 0.322 0.247 0.162

6 4.917 4.355 4.111 3.785 3.3267 5.582 4.868 4.564 4.160 3.6058 6.210 5.335 4.968 4.487 3.8379 6 802 5 756 5 328 4 772 4 0319 6.802 5.756 5.328 4.772 4.03110 7.360 6.145 5.650 5.019 4.192

30

Method of Evaluating Capital InvestmentNet Present Value MethodsThe net present value method analyzes capital investment proposals by comparing the initial cash investment with the present value of

Net Present Value Methods

by comparing the initial cash investment with the present value of the net cash flows. It is sometimes called the discounted cash flow method. The interest rate (return) used in net present value analysis is set by management This rate is often based upon such factors asis set by management. This rate is often based upon such factors as the nature of the business, the purpose of the investment, the cost of securing funds for the investment, and the minimum desired rate of return If the net present value of the cash flows expected from areturn. If the net present value of the cash flows expected from a proposed investment equals or exceeds the amount of the initial investment, the proposal is desirable.Jan 1, 2003, assume a proposal to acquire $200,000 of equipmentwith an expected useful life of 5 years (no residual value) and minimum desired rate of 10%Net cash flows for the years Dec 31, 2003 $70,000

Dec 31, 2004 $60,000Dec 31 2005 $50 000

31

Dec 31, 2005 $50,000Dec 31, 2006 $40,000Dec 31, 2007 $40,000

Method of Evaluating Capital Investment

Jan 1, 2003Dec 1, 2003 Dec 1, 2004 Dec 1, 2005Dec 1, 2006 Dec 1, 2007

$$ $ $ $$

$$4949 560560

$40,000$70,000 $60,000 $50,000 $40,000$$6363,,630630 $70,000x0.909

$60,000x0.826

$200,000

$$4949,,560560$$3737,,550550$$2727 320320

$50,000x0.751$40,000x0.683

$60,000 0 8 6

$$2727,,320320$$2424,,840840

$$202202,,900900

$40,000x0.621

$$202202,,900900Net present value

Present value index = Total present value of net cash flowAmount to be invested

$$22,,900900

Amount to be invested

= $202,900$200,000

= 1.0145

32

$200,000

Method of Evaluating Capital InvestmentIf a business is considering three alternative proposals and hasIf a business is considering three alternative proposals and has determined their net present values, the present value index for each proposal is as follows:

Proposal A Proposal BTotal present value of net cash flowAmount to be invested

$107,000 $86,400$100 000 $80 000

Proposal C$93,600$90 000Amount to be invested $100,000 $80,000 $90,000

Net present value $ 7,000 $ 6,400 $ 3,600

1 07 1 08 1 04Present value index 1.07(107,000/100,000)

1.08(86,400/80,000)

1.04(93,600/90,000)

33

Method of Evaluating Capital InvestmentInternal Rate of Return MethodThe internal rate of return method uses present value concepts to compute the rate of return from the net cash flows expected from

Internal Rate of Return Method

capital investment proposals. This method is sometimes called the time-adjusted rate of return method. It is similar to the net present value method, in that it focuses on the present value of the net , pcash flows. However, the internal rate of return method starts with the net cash flows and, in a sense, works backwards to determine the rate of return expected from the proposalthe rate of return expected from the proposal

Assume that management is evaluating a proposal to acquire equipment costing $33,530. The equipment is expected to provide q p g q p p pannual net cash flows of $10,000 per year for five years. If we assume a rate of return of 12%, we can calculate the present value of the net cash flows, using the present value of an annuity tablethe net cash flows, using the present value of an annuity table

Annual net cash flow (at the end of each of five years)$10,000Present value of an annuity of $1 at 12% for 5 year 3.605P t l f l t h fl $36 050

34

Present value of annual net cash flows $36,050Less amount to be invested $33,530Net present Value $ 2,520

Method of Evaluating Capital Investment$36 050 present value of the cash inflows based on a 12% rate of$36,050 present value of the cash inflows, based on a 12% rate of return, is greater than the $33,530 to be invested. Therefore, the internal rate of return must be greater than 12%. Through trial-and-error procedures the rate of return that equates the $33 530 cost oferror procedures, the rate of return that equates the $33,530 cost of the investment with the present value of the net cash flows is determined to be 15%, as shown below.

Jan 1, 2003 Dec 1, 2003 Dec 1, 2004 Dec 1, 2005 Dec 1, 2006 Dec 1, 2007

$33,530

$10,000$10,000 $10,000 $10,000 $10,000$33,530

10 000x3 353 (15% 5 year)Net present value0

10,000x3.353 (15%, 5 year)

35

Method of Evaluating Capital InvestmentExample : To illustrate assume that management is considering aExample : To illustrate, assume that management is considering a proposal to acquire equipment costing $97,360. The equipment is expected to provide equal annual net cash flows of $20,000 for seven yearsseven years.

Present value factor for an annuity of $1 =Amount to be invested

Equal annual net cash flowsq

=$97,360$20,000

= 4.868

Present Value of an Annuity of$1 at Compound Interest

Year 6% 10% 12% 15% 20%

1 0.943 0.909 0.893 0.870 0.8332 1.833 1.736 1.690 1.626 1.5283 2.673 2.487 2.402 2.283 2.1064 3 465 3 170 3 037 2 855 2 5894 3.465 3.170 3.037 2.855 2.5895 4.212 3.791 3.605 3.353 2.9916 4.917 4.355 4.111 3.785 3.3267 5.582 4.868 4.564 4.160 3.605

36

7 5.582 4.868 4.564 4.160 3.6058 6.210 5.335 4.968 4.487 3.8379 6.802 5.756 5.328 4.772 4.03110 7.360 6.145 5.650 5.019 4.192

Method of Evaluating Capital Investmentassume that management is considering a proposal to acquireassume that management is considering a proposal to acquire equipment costing $97,360. The equipment is expected to provide equal annual net cash flows of $21,000 for seven years.

Present value factor for an annuity of $1 =Amount to be invested

Equal annual net cash flows$97,360 = 4 636=$21,000

4.636Present Value of an Annuity of$1 at Compound Interest

Year 6% 10% 12% 15% 20%

1 0.943 0.909 0.893 0.870 0.8332 1.833 1.736 1.690 1.626 1.5283 2 673 2 487 2 402 2 283 2 106 10%+ 12%-10% x(4 868-4 636)[ ]3 2.673 2.487 2.402 2.283 2.1064 3.465 3.170 3.037 2.855 2.5895 4.212 3.791 3.605 3.353 2.9916 4.917 4.355 4.111 3.785 3.326

10%+ (4.868-4.564)x(4.868-4.636)[ ]

10%+ 10%+ ((2/0.304) X0.232)[ ]6 4.917 4.355 4.111 3.785 3.3267 5.582 4.868 4.564 4.160 3.6058 6.210 5.335 4.968 4.487 3.8379 6.802 5.756 5.328 4.772 4.03110 7.360 6.145 5.650 5.019 4.192

11.523%

[ ]

37

10 7.360 6.145 5.650 5.019 4.192

Method of Evaluating Capital InvestmentUnequal Proposal LivesThe alternative proposals may have unequal lives. To illustrate, assume that alternative investments. A truck and computers, are

Unequal Proposal Lives

being compared. The truck has a useful life of 8 years, and the computer network has a useful life of 5 years. Each proposal requires an initial investment of $100,000, and the company q $ , , p ydesires a rate of return of 10%.

T k 8 lifAssuming truck is to be sold at

Truck 8-year life

Compare

gthe end of 5 year $40,000

Computer network 5-year life

Compare

38

Method of Evaluating Capital InvestmentThe expected cash flows and net present value of each alternative shows:The expected cash flows and net present value of each alternative shows:

TruckPresent Value Net Cash Present Value of

Of $1 at 10% Flow Net Cash FlowYear

ComputerPresent Value Net Cash Present Value of

Of $1 at 10% Flow Net Cash FlowYearOf $1 at 10% Flow Net Cash Flow1 0.909 $ 30,000 $ 27,2702 0.826 30,000 24,7803 0.751 25,000 18,7754 0.683 20,000 13,6605 0 621 15 000 9 315

Of $1 at 10% Flow Net Cash Flow1 0.909 $ 30,000 $ 27,2702 0.826 30,000 24,7803 0.751 30,000 22,5304 0.683 30,000 20,490

5 0.621 15,000 9,3156 0.564 15,000 8,4607 0.513 10,000 5,1308 0.467 10,000 4,670Total $ 155,000 $112,060

5 0.621 35,000 21,735Total $ 155,000 $116,805Amount to be invested 100,000Net present value $ 16,805

Amount to be invested 100,000Net present value $ 12,000

Truck-Revised t o 5 year lifePresent Value Net Cash Present Value of

Of $1 at 10% Flow Net Cash FlowYear

1 0.909 $ 30,000 $ 27,2702 0.826 30,000 24,7803 0.751 25,000 18,775, ,4 0.683 20,000 13,6605 0.621 15,000 9,315

Total $ 160 000 $118 640

5(Residual value)0.621 40,000 24,840

Truck NPV >Computers NPV

39

Total $ 160,000 $118,640Amount to be invested 100,000Net present value $ 18,640

Method of Evaluating Capital InvestmentLease versus Capital InvestmentLeasing fixed assets has become common in many industries. Leasing allows a business to use fixed assets without spending

Lease versus Capital Investment

large amounts of cash to purchase them. In addition, management may believe that a fixed asset has a high risk of becoming obsolete. This risk may be reduced by leasing rather than y y gpurchasing the asset. Also, the Internal Revenue Code allows the lesser (the owner of the asset) to pass tax deductions on to the lessee (the party leasing the asset) These provisions of the taxlessee (the party leasing the asset). These provisions of the tax law have made leasing assets more attractive.

UncertaintyAll capital investment analyses rely on factors that are uncertain. The long-term nature of capital investments suggests that some

Uncertainty

The long term nature of capital investments suggests that some estimates are likely to involve uncertainty. Error in one or more of the estimates could lead to incorrect decisions.

40

Method of Evaluating Capital InvestmentChange in Price LevelsIn performing investment analysis, management must be concerned about changes in price levels. Price levels may

Change in Price Levels

change due to inflation, which occurs when general price levels are rising. Price levels may also change for foreign investments as the y g gresult of currency exchange rates. Currency exchange rates are the rates at which currency in another country can be exchanged.

Q lit ti C id tiSome benefits of capital investments are qualitative in nature and

t b il ti t d i d ll t If t d

Qualitative Considerations

cannot be easily estimated in dollar terms. If management does not consider these qualitative considerations, the quantitative analyses may suggest rejecting a worthy investment.

Funding for capital projects may be obtained from issuing bonds or stock or from operating cash. Capital rationing is the process by which management allocates these funds among competing capital

41

which management allocates these funds among competing capital investment proposals. In this process, management often uses a combination of the methods described in this chapter.

NoAlternative Capital

Investment Proposals

Minimum CashPayback and Average Rate of

Return Standards Met?

RejectedProposals

Decision

Yes

Proposals forFurther Analysis

No

Net PresentValue and Internal Rate

of Return StandardsRejectedProposals

YesMet?

Proposals forF th A l i

p

Further Analysis

Yes NoDo Qualitative

Considerations Change theDo Qualitative

Considerations Change the RejectedRejected

AcceptedProposals

Decision? Decision? ProposalsProposals

U f d d P l

Ranking ofProposals

42Funded

Proposals

Unfunded ProposalsReconsider If Funds

Subsequently BecomeAvailable

NoYes Capital Funds Available?

Question??Question??

43

Modifying Accounting data forStatement of Cash flows

Modifying Accounting data for Managerial decisions

Operating Assets and Operating Capital

Balance SheetAssets LiabilitiesAssetsOperate Operating Assets

Working Capital

LiabilitiesCharge InterestDo not charge Interest

Nonoperating AssetsFixed Assets Equities

44

Statement of Cash flows

Net Operating Working Capital (NOWC)= All current asset – All current liabilities the do not charge interest

ABC Co.,Ltd. =(Cash & marketable securities + AR + Inventories) – (AP + Accruals)Y 2006

g

Year 2006=(10 + 375 + 615) – (60 + 140)=800Year 2005=(80 + 315 + 415) – (30 + 130)=650650

Total Operating Capital=Net Operating Working Capital + Net Fixed AssetsYear 2006Year 2006=800 + 1,000=1,800Y 2005

45

Year 2005=650 +870=1,520

Statement of Cash flows

Net Operating Profit After Taxes (NOPAT)

กาไรทกจการควรไดรบจากการดาเนนงานโดยไมรวมกาไรทกจการควรไดรบจากการดาเนนงานโดยไมรวมคาจายในการจดหาเงนทน และสนทรพยทางการเงนทไมเกยวของกบการดาเนนงานตามปกต

Net Operating Profit After Taxes (NOPAT)E i b f i t t d t (1 T t )= Earning before interest and taxes x (1 – Tax rate)

ABC Co.,Ltd.Y 2006Year 2006=283.8(1 – 0.40) = 170.3Year 2005=263(1-0.40) = 157.8

46

Statement of Cash flows

Free Cash Flow (FCF)กระแสเงนสดทพรอมจะนาไปจายใหผลงทนได หลงจากทกนเงนไวเพอลงทน และกนไวเปนเงนทนหมนเวยน

Free Cash Flow (FCF)= Operating Cash Flow – Gross investment in Operating Capital

Operating Cash Flow = NOPAT + Depreciation= 283.8(1-0.40) + 100= 270.30

Gross investment in Operating Capital= Net investment + Depreciation= Net investment + Depreciation= (1,800 – 1,520) + 100= 380

47

380Free Cash Flow = 270 – 380

= -109.70

Measuring Cash FlowsStatement of Cash flows

Measuring Cash Flows

Operating freecash flows

Financing freecash flows=

Free Cash Flows:An Operating Perspective

Free Cash Flows:A Financing Perspective=

48

Tona Co Ltd

Statement of Cash flowsTona Co.,Ltd.

Income StatementDecember 31, 2006

ยอดขาย 11,508Unit: millions of Bahts

ยอดขายตนทนสนคาขายกาไรขนตนคาใชจายในการบรหารและการตลาด

11,5086,5374,971

1 832คาใชจายในการบรหารและการตลาดคาเสอมราคา คาใชจายในการดาเนนงานรวม

ไ

1,832 345

2,177กาไรจากการดาเนนงานดอกเบยจายกาไรกอนภาษ

2,794387

2,407ภาษจายกาไรกอนเงนปนผลหนบรมสทธเงนปนผลหนบรมสทธ

,765

1,64225เงนปนผลหนบรมสทธ

กาไรสทธกาไรสทธสวนของผถอหนสามญ

ป

251,6171,617

49เงนปนผลหนสามญการเปลยนแปลงในกาไรสะสม

688929

Tona Co.,Ltd.

Statement of Cash flows,

Balance SheetDecember 31, 2005-2006

2006 2005 การเปลยนแปลงสนทรพย 2006 2005 การเปลยนแปลงเงนสดลกหนสนคาคงเหลอ

สนทรพย33249570

34148471

9(11)

1สนคาคงเหลอคาใชจายจายลวงหนารวมสนทรพยหมนเวยน

70208

1,10519 134

71247

1,14320 088

13938

954สนทรพยถาวรคาเสอมราคาสนทรพยถาวรรวมสนทรพยถาวร

19,134(4,782)14,352

20,088(5,127)14,961

954(345)

609การลงทนสนทรพยอนรวมสนทรพยอน

7791,152

17 388

7021,436

18 242

(77)284854รวมสนทรพยอน 17,388 18,242 854

50

Tona Co.,Ltd.

Statement of Cash flows,

Balance SheetDecember 31, 2005-2006

2006 2005 การเปลยนแปลงหนสนและสวนของผถอหน

หนสนตวเงนระยะสนเจาหนการคา

693638

1,629651

93613เจาหนการคา

ภาษคางจายคาใชจายคางจายรวมหนสนหมนเวยน

63823

7822 136

65153

6522 985

1330

(130)849รวมหนสนหมนเวยน

หนสนระยะยาวรวมหนสน

2,1366,5338,669

2,9856,3259,310

849(208)

641สวนของผถอหนหนบรมสทธหนสามญ (มลคาและสวนเกน)

165583

80708

(85)125หนสามญ (มลคาแล สวนเกน)

กาไรสะสมการซอหนกลบคนสวนของผถอหนสามญ

58310,998(3,027)

8 554

70811,927(3,783)

8 852

125929

(756)298

51

สวนของผถอหนสามญรวมสวนของผถอหนสามญรวมหนสนและสวนของผถอหนสามญ

8,5548,719

17,388

8,8528,932

18,242

298213854

F C h Fl A O ti P ti

Statement of Cash flows

Free Cash Flows: An Operating Perspective

Step 1: Income statement Accrual Basis Cash BasispEBIT+ Depreciation

EBITDA= EBITDA- Tax (Cash)= Cash flows after Operatingp g

Step 2: Compute investing in net current assetsChange in Current assets

Ch i i t t b i t li biliti- Change in non-interest-bearing current liabilitiesStep 3: Compute investing in Fixed assets and Others assets

52

F C h Fl A O ti P ti

Statement of Cash flows

Free Cash Flows: An Operating Perspective

Step 1: Income statement Accrual Basis Cash Basisp

กาไรจากการดาเนนงาน (EBIT)คาเสอมราคา

2,794345

กาไรกอนดอกเบย ภาษ คาเสอมราคาและรายการตดบญช (EBITDA)ภาษจายหก การเปลยนแปลงในภาษคางจาย

3,139765 30

ภาษจายทเปนเงนสดกระแสเงนหลงภาษจากการดาเนนงาน

7352,404

53

F C h Fl A O ti P ti

Statement of Cash flows

Free Cash Flows: An Operating Perspective

Step 2: Compute investing in net current assetsp p gการเปลยนแปลงในสนทรพยหมนเวยน: การเปลยนแปลงในเงนสด

การเปลยนแปลงในลกหน9

(11) การเปลยนแปลงในลกหน การเปลยนแปลงในสนคาคงเหลอ การเปลยนแปลงในคาใชจายจายลวงหนา

(11) 1

39 การเปลยนแปลงในสนทรพยหมนเวยนการเปลยนแปลงในหนสนหมนเวยน:

การเปลยนแปลงในเจาหน

38

13 การเปลยนแปลงในเจาหน การเปลยนแปลงในคาใชจายคางจาย การเปลยนแปลงในหนสนหมนเวยนทไมตองชาระดอกเบย

13 (130)

(117)การเปลยนแปลงในเงนทนหมนเวยนสทธจาการดาเนนงาน(สนทรพยหมนเวยน – หนสนหมนเวยนทไมตองชาระดอกเบย)

155

54

F C h Fl A O ti P ti

Statement of Cash flows

Free Cash Flows: An Operating Perspective

Step 3: Compute investing in Fixed assets and Others assetsp p gการเปลยนแปลงในสนทรพยระยะยาว การลงทนในสนทรพยถาวร

การเปลยนแปลงในการลงทน954 (77) การเปลยนแปลงในการลงทน

การเปลยนแปลงในสนทรพยอน เงนสดสทธทใชในการลงทน

(77) 284

1,161กระแสเงนสดจากการดาเนนงาน(2,404-155-1,161)

1,088

55

F C h Fl A Fi i P ti

Statement of Cash flows

Free Cash Flows: A Financing Perspective

Step 1: Compute the real interestStep 1: Compute the real interestInterest paid – Accrued Interest (change)

Step 2: Compute the change of liabilitiesStep 2: Compute the change of liabilitiesStep 3: Compute Dividend paidStep 4: Compute the change of stocksStep 4: Compute the change of stocks

56

Statement of Cash flows

2006 2005MVAPrice per shareNumber of shares (millions)Market value of equity

23.0 26.050.0 50.0

1 150 0 1 300 0Market value of equityBook value of equity

1,150.0 1,300.0896.0 840.0

MVA = Market value – Book value 254.0 460.0MVA Market value Book value 254.0 460.0EVAEBIT 283.8 263.0Tax rate(%)NOPAT = EBIT(1-Tax rate)Total investor Supplied operating capital

40 40170.3 157.8

1 800 0 1 520 0Total investor – Supplied operating capital 1,800.0 1,520.0After tax cost of capital(%) 10.0 10.3Dollar cost of capital(%) 180 156.6

57

p (%)EVA = NOPAT – Capital cost (9.7) (1.2)

Market Value Added (MVA) andStatement of Cash flows

Market Value Added (MVA) and Economic Value Added (EVA)

MVAมลคาเพมทางการตลาด ซงเกดจากผลตางระหวางมลคาทางการตลาดของเจาของกจการกบเงนทนทมาจากเจาของ

MVA = Market value of equity – Equity capital supply by investors= (Shares outstanding x Stock price) – Total Common equity

EVA

มลคาเพมทางเศรษฐศาสตร เปนการวดประสทธภาพการจดการซงกอใหเกดการเพมมลคาของผถอหนในปใ ป ไ ใดปหนงทกาหนดไว

EVA = NOPAT – After tax cost of capital used to support operationsEBIT (1 T t ) (O ti C it l) (Aft t t

58

= EBIT – (1 – Taxes rate) – (Operating Capital) – (After tax percentage cost of capital)

F C h Fl A Fi i P ti

Statement of Cash flows

Free Cash Flows: A Financing Perspective

ดอกเบยจายใหแกเจาหน 387ดอกเบยจายใหแกเจาหนหก การเปลยนแปลงในดอกเบยคางจายดอกเบยจายใหแกเจาหน

387 0

387ดอกเบยจายใหแกเจาหนบวก หนสนระยะยาวลดลงหก หนสนระยะสนเพมขน

387208

(936)หก หนสนร ย สนเพมขนบวก เงนปนผลหนบรมสทธบวก เงนปนผลหนสามญ

(936)25

688บวก เงนปนผลหนสามญบวก การลดลงในหนบรมสทธบวก การลดลงในหนสามญ

68885

631ว รล ลงใน นส มญกระแสเงนสดจายใหแกผถอหน

631,088

59