Embed Size (px)

Citation preview

Sales Audit, Sales Analysis & Sales Audit, Sales Analysis & Marketing Cost AnalysisMarketing Cost Analysis

Sales Force ManagementSales Force ManagementChapter 8Chapter 8

11

Control Mechanism in Control Mechanism in Sales Management Sales Management

Sales organisation is integrated with many other Sales organisation is integrated with many other departments like sales promotion, public relations, departments like sales promotion, public relations, personal selling and physical distribution. personal selling and physical distribution. Excepting the "sales volume objective" most of the Excepting the "sales volume objective" most of the sales persons are not able to give full justice to other sales persons are not able to give full justice to other functional aspects. functional aspects. A properly designed and carefully implemented A properly designed and carefully implemented control mechanism, emphasise not only the "sales control mechanism, emphasise not only the "sales volume objective" but also on "sales profit objective" volume objective" but also on "sales profit objective" and "cost control aspects" of activities.and "cost control aspects" of activities.

Sales Audit, Sales Analysis & Sales Audit, Sales Analysis & Marketing Cost AnalysisMarketing Cost Analysis

Sales Force ManagementSales Force ManagementChapter 8Chapter 8

22

Methods of Control Methods of Control

There are two types of control devices:There are two types of control devices:Control Devices during Planning Phase: Control Devices during Planning Phase:

Design of sales territories,Design of sales territories,Planning of sales budgetsPlanning of sales budgetsAllocation of sales quotas. Allocation of sales quotas.

Control Devices during Implementation PhaseControl Devices during Implementation PhaseSales AuditSales AuditSales Analysis, Sales Analysis, Marketing Cost AnalysisMarketing Cost Analysis

Sales Audit, Sales Analysis & Sales Audit, Sales Analysis & Marketing Cost AnalysisMarketing Cost Analysis

Sales Force ManagementSales Force ManagementChapter 8Chapter 8

33

Sales Audit Sales Audit

Sales audit focus on design and Sales audit focus on design and implementation of strategies and policies of implementation of strategies and policies of sellingsellingSales audit is to identify the strength and Sales audit is to identify the strength and weakness of the organisation. weakness of the organisation. The purpose is to maximise the opportunities The purpose is to maximise the opportunities and minimize its weaknesses.and minimize its weaknesses.

Sales Audit, Sales Analysis & Sales Audit, Sales Analysis & Marketing Cost AnalysisMarketing Cost Analysis

Sales Force ManagementSales Force ManagementChapter 8Chapter 8

44

Sales Analysis Sales Analysis Sales analysis brings out the details which Sales analysis brings out the details which otherwise remain dormant. otherwise remain dormant. This analysis identifies the following:This analysis identifies the following:

Strong and weak territoriesStrong and weak territoriesHigh volume and low volume productsHigh volume and low volume productsSatisfactory and unsatisfactory "Customer Satisfactory and unsatisfactory "Customer Accounts"Accounts" etc.etc.

Sales analysis, thus provides data and Sales analysis, thus provides data and information which enables company to information which enables company to allocate the resources optimally and distribute allocate the resources optimally and distribute sales efforts effectively.sales efforts effectively.

Sales Audit, Sales Analysis & Sales Audit, Sales Analysis & Marketing Cost AnalysisMarketing Cost Analysis

Sales Force ManagementSales Force ManagementChapter 8Chapter 8

55

Marketing Cost Analysis Marketing Cost Analysis

Sales budgets and sales quota identify various sales Sales budgets and sales quota identify various sales activities and estimate their respective costs. activities and estimate their respective costs. Success of sales operation depends on faithful Success of sales operation depends on faithful implementation of these plans.implementation of these plans.Sales persons must execute their assigned task within Sales persons must execute their assigned task within the "time frame" and "cost frame" envisaged therein.the "time frame" and "cost frame" envisaged therein.The principle followed here is "management by The principle followed here is "management by exceptions" so that corrective actions are initiated in exceptions" so that corrective actions are initiated in time, only if these go beyond pretime, only if these go beyond pre--fixed limits.fixed limits.

Sales Audit, Sales Analysis & Sales Audit, Sales Analysis & Marketing Cost AnalysisMarketing Cost Analysis

Sales Force ManagementSales Force ManagementChapter 8Chapter 8

66

Sales AuditSales Audit--Nature and ScopeNature and Scope

A sales audit is a systematic, critical and unbiased A sales audit is a systematic, critical and unbiased review and appraisal of basic objectives and policies review and appraisal of basic objectives and policies of selling, functions and of the organisation methods, of selling, functions and of the organisation methods, procedure and personnel employed to implement procedure and personnel employed to implement those policies and achieve those objectives.those policies and achieve those objectives.The scope of sales audit is quite wide and include the The scope of sales audit is quite wide and include the critical introspection of objective performance and critical introspection of objective performance and self appraisal.self appraisal.The purpose is to maximise the "strength" and The purpose is to maximise the "strength" and minimise the illminimise the ill--effects of "weaknesseseffects of "weaknesses”” uncovered uncovered by sales audit.by sales audit.

Sales Audit, Sales Analysis & Sales Audit, Sales Analysis & Marketing Cost AnalysisMarketing Cost Analysis

Sales Force ManagementSales Force ManagementChapter 8Chapter 8

77

Sales AuditSales Audit-- Form and Content Form and Content Sales audit, examines the following aspects of Sales audit, examines the following aspects of business:business:

The ObjectiveThe ObjectiveStrategies and PoliciesStrategies and PoliciesOrganisation DesignOrganisation DesignOrganisational MethodsOrganisational MethodsSystems and ProcedureSystems and ProcedureMorale and MotivationMorale and MotivationProduct MixProduct MixMarket ConditionsMarket Conditions

Sales Audit, Sales Analysis & Sales Audit, Sales Analysis & Marketing Cost AnalysisMarketing Cost Analysis

Sales Force ManagementSales Force ManagementChapter 8Chapter 8

88

Sales AnalysisSales Analysis--PurposePurpose

The focus is on analysis of "sales volume" and "sales The focus is on analysis of "sales volume" and "sales profitprofit””. Sales analysis serves following purposes:. Sales analysis serves following purposes:

Analysing specific problems of sales.Analysing specific problems of sales.Identifying 'strengths' and 'weaknesses' of the firmIdentifying 'strengths' and 'weaknesses' of the firmTo provide timely warning to management based on "iceTo provide timely warning to management based on "ice--berg principles." berg principles."

'Sales Analysis' does not answer the question of 'why' 'Sales Analysis' does not answer the question of 'why' of the problems.of the problems.With data, interpretation and analysis, it is possible With data, interpretation and analysis, it is possible for managers to identify the reasons and apply for managers to identify the reasons and apply corrections.corrections.

Sales Audit, Sales Analysis & Sales Audit, Sales Analysis & Marketing Cost AnalysisMarketing Cost Analysis

Sales Force ManagementSales Force ManagementChapter 8Chapter 8

99

Specific Problems of Sales Specific Problems of Sales Firm faces a number of specific problems Firm faces a number of specific problems which require sales analysis such as:which require sales analysis such as:

Inadequate growth rate of salesInadequate growth rate of sales--volumevolumeShortfall of sales profitShortfall of sales profitWhile sales volume shows increasing rate of While sales volume shows increasing rate of growth, sales profit shows decreasing rate of growth, sales profit shows decreasing rate of increase. increase. Profit comes down for a given sales volumeProfit comes down for a given sales volumeSales quotas are not metSales quotas are not metShortfall of sales volume objectiveShortfall of sales volume objectiveShortfall of "sales profit" objectiveShortfall of "sales profit" objective

Sales Audit, Sales Analysis & Sales Audit, Sales Analysis & Marketing Cost AnalysisMarketing Cost Analysis

Sales Force ManagementSales Force ManagementChapter 8Chapter 8

1010

Strengths and Weaknesses Strengths and Weaknesses Sales Analysis is also necessary to identify Sales Analysis is also necessary to identify strengths and weaknesses of an organisation in strengths and weaknesses of an organisation in different areas: different areas:

Product lineProduct line--range. quality, price etcrange. quality, price etcSales effortsSales efforts--advertisement. sales promotion, advertisement. sales promotion, distribution etc.distribution etc.Sales territoriesSales territoriesSales persons.Sales persons.Class of accounts (customers).Class of accounts (customers).Expenses and distribution of overheads.Expenses and distribution of overheads.

Sales Audit, Sales Analysis & Sales Audit, Sales Analysis & Marketing Cost AnalysisMarketing Cost Analysis

Sales Force ManagementSales Force ManagementChapter 8Chapter 8

1111

Iceberg Principles Iceberg Principles No consideration is given during planning phaseNo consideration is given during planning phase

To different sales efforts, to suit different territories, produTo different sales efforts, to suit different territories, products, cts, customer accounts or competence level of salesperson. customer accounts or competence level of salesperson. This is because detailed information on such aspects are, This is because detailed information on such aspects are, simply, not available. simply, not available.

Sales efforts and sales expenses are evenly distributed Sales efforts and sales expenses are evenly distributed over territories.over territories.This is called "iceberg principle" where only a small part This is called "iceberg principle" where only a small part of total situation is known (above water) while the of total situation is known (above water) while the details are unknown (submerged). details are unknown (submerged). Sales analysis reverses this situation and increases the Sales analysis reverses this situation and increases the profit by selecting optimum, strategy of allocating profit by selecting optimum, strategy of allocating resources and arranging efforts. resources and arranging efforts.

Sales Audit, Sales Analysis & Sales Audit, Sales Analysis & Marketing Cost AnalysisMarketing Cost Analysis

Sales Force ManagementSales Force ManagementChapter 8Chapter 8

1212

Sales AnalysisSales Analysis--Methods Methods

Sales analysis is a systematic process of Sales analysis is a systematic process of finding answers to the following questions.finding answers to the following questions.

"What' is sold?"What' is sold?"Where" is it sold?"Where" is it sold?By "whom" it is sold? By "whom" it is sold? "Who" are the buyers?"Who" are the buyers?

Analysis is carried out when there is a purpose Analysis is carried out when there is a purpose to do so which is to solve a problem.to do so which is to solve a problem.

Sales Audit, Sales Analysis & Sales Audit, Sales Analysis & Marketing Cost AnalysisMarketing Cost Analysis

Sales Force ManagementSales Force ManagementChapter 8Chapter 8

1313

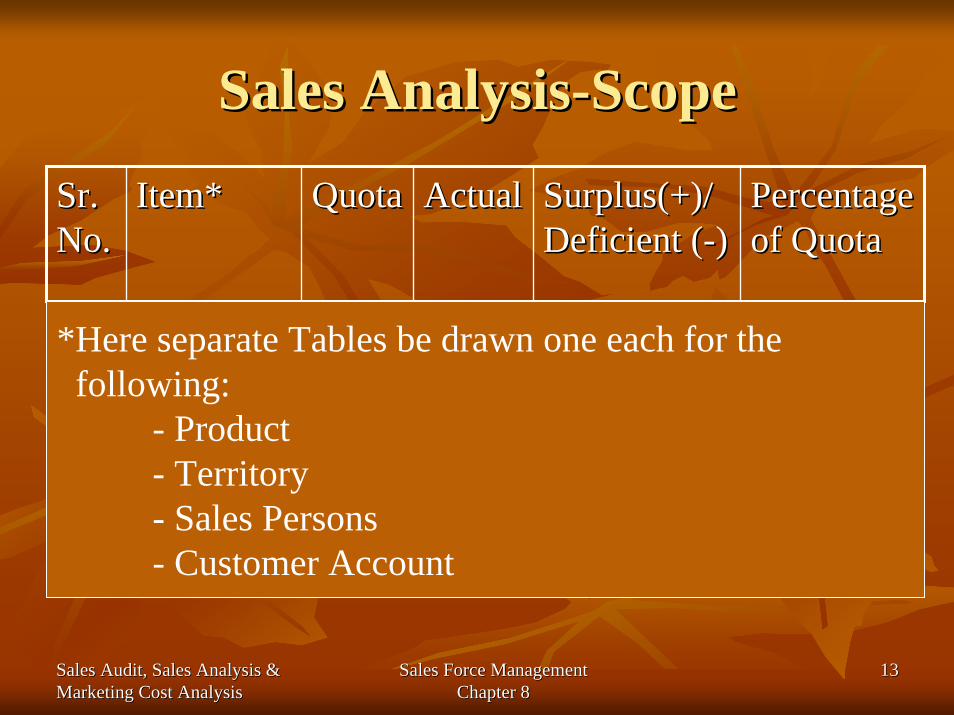

Sales AnalysisSales Analysis--Scope Scope

Sr. Sr. No.No.

Item*Item* QuotaQuota ActualActual Surplus(+)/Surplus(+)/Deficient (Deficient (--))

Percentage Percentage of Quotaof Quota

*Here separate Tables be drawn one each for the following:

- Product- Territory- Sales Persons- Customer Account

Sales Audit, Sales Analysis & Sales Audit, Sales Analysis & Marketing Cost AnalysisMarketing Cost Analysis

Sales Force ManagementSales Force ManagementChapter 8Chapter 8

1414

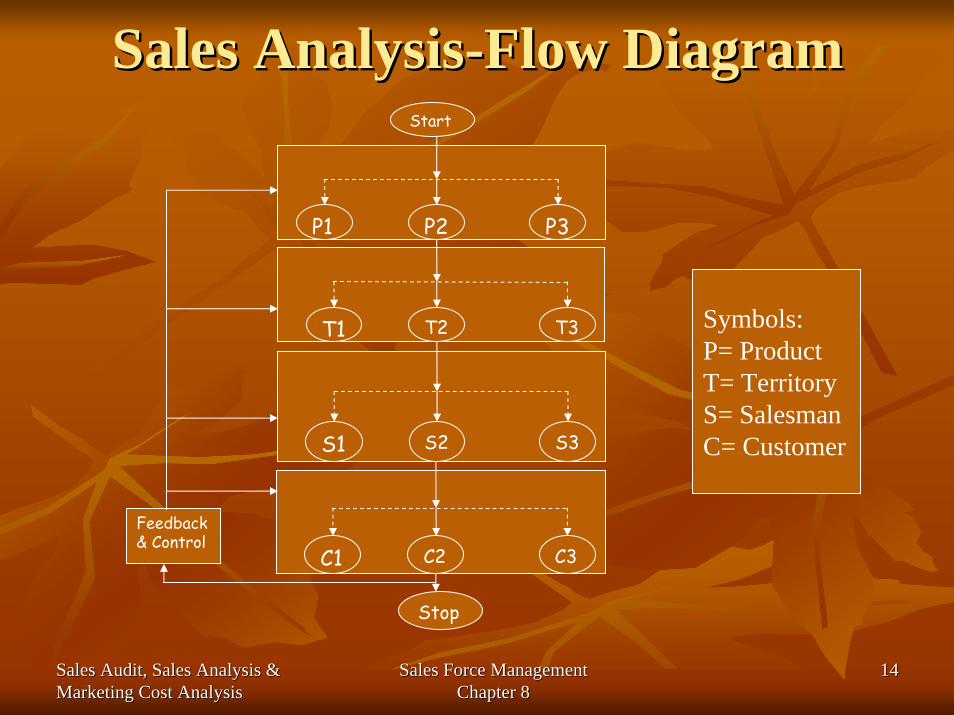

Sales AnalysisSales Analysis--Flow Diagram Flow Diagram

T1 T2 T3

Start

P1 P2 P3

Stop

C1 C2 C3

Feedback& Control

S1 S2 S3

Symbols:P= ProductT= TerritoryS= SalesmanC= Customer

Sales Audit, Sales Analysis & Sales Audit, Sales Analysis & Marketing Cost AnalysisMarketing Cost Analysis

Sales Force ManagementSales Force ManagementChapter 8Chapter 8

1515

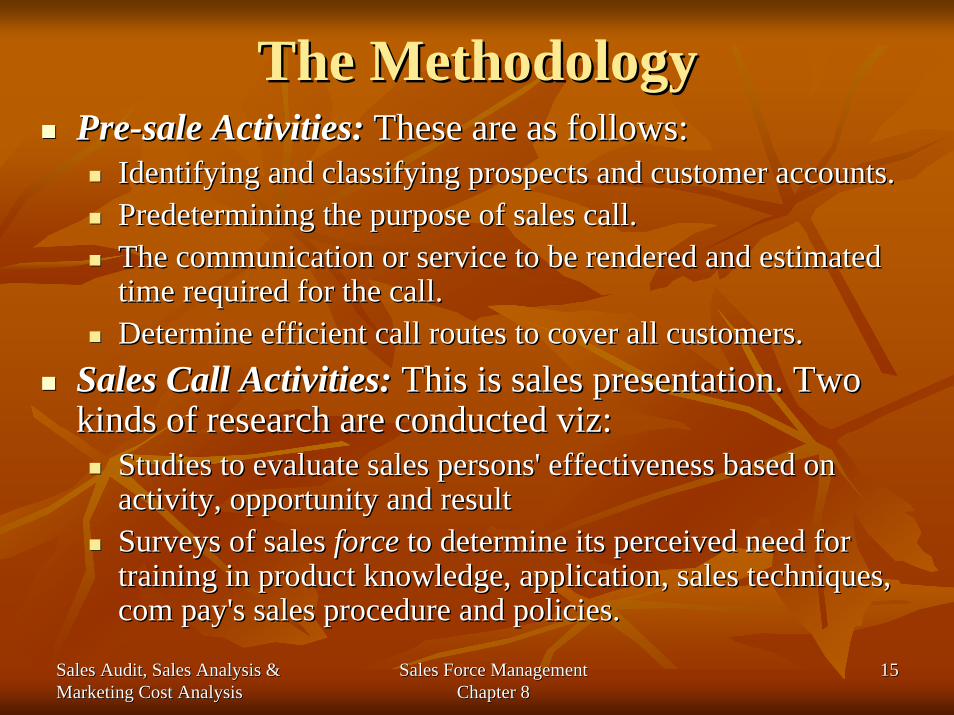

The Methodology The Methodology PrePre--sale Activities:sale Activities: These are as follows:These are as follows:

Identifying and classifying prospects and customer accounts.Identifying and classifying prospects and customer accounts.Predetermining the purpose of sales call.Predetermining the purpose of sales call.The communication or service to be rendered and estimated The communication or service to be rendered and estimated time required for the call.time required for the call.Determine efficient call routes to cover all customers.Determine efficient call routes to cover all customers.

Sales Call Activities:Sales Call Activities: This is sales presentation. Two This is sales presentation. Two kinds of research are conducted viz:kinds of research are conducted viz:

Studies to evaluate sales persons' effectiveness based on Studies to evaluate sales persons' effectiveness based on activity, opportunity and resultactivity, opportunity and resultSurveys of sales Surveys of sales force force to determine its perceived need for to determine its perceived need for training in product knowledge, application, sales techniques, training in product knowledge, application, sales techniques, com pay's sales procedure and policies.com pay's sales procedure and policies.

Sales Audit, Sales Analysis & Sales Audit, Sales Analysis & Marketing Cost AnalysisMarketing Cost Analysis

Sales Force ManagementSales Force ManagementChapter 8Chapter 8

1616

Conclusion Conclusion

Better the knowledge on sales potential of an Better the knowledge on sales potential of an area, greater the accuracy of forecasting sales area, greater the accuracy of forecasting sales volume objective. volume objective. Similarly, better knowledge of market Similarly, better knowledge of market condition and sales territories yield, more condition and sales territories yield, more accurate is the assessment of sales expenditure accurate is the assessment of sales expenditure and and forecast forecast of sales profit objective. of sales profit objective. Sales research is not only a science but also an Sales research is not only a science but also an art.art.

Sales Audit, Sales Analysis & Sales Audit, Sales Analysis & Marketing Cost AnalysisMarketing Cost Analysis

Sales Force ManagementSales Force ManagementChapter 8Chapter 8

1717

Marketing Cost AnalysisMarketing Cost Analysis--Objective Objective

The bottom line of any commercial venture is the profit. The bottom line of any commercial venture is the profit. While sales volume and market share are important, While sales volume and market share are important, profitability decides survivability of the firm. profitability decides survivability of the firm. Marketing cost analysis link the two objectives "Sales Marketing cost analysis link the two objectives "Sales volume objective" and "Sales profit objective" together. volume objective" and "Sales profit objective" together. Cost analysis, analyses sales volume and selling Cost analysis, analyses sales volume and selling expenses so as to estimate the sales profit based on the expenses so as to estimate the sales profit based on the following formula.following formula.Sales profit = Sales volume in Rupees Sales profit = Sales volume in Rupees --Selling Expenses Selling Expenses

Sales Audit, Sales Analysis & Sales Audit, Sales Analysis & Marketing Cost AnalysisMarketing Cost Analysis

Sales Force ManagementSales Force ManagementChapter 8Chapter 8

1818

Marketing Cost AnalysisMarketing Cost Analysis--Nature and Scope Nature and Scope

Cost Analysis find answers to the following Cost Analysis find answers to the following questions.questions.

Which products contribute the maximum profit?Which products contribute the maximum profit?What are the contributions or others?What are the contributions or others?Which territories are profitable or otherwise?Which territories are profitable or otherwise?What are the levels of profit contribution by different sales What are the levels of profit contribution by different sales persons? persons? What are the relative profitWhat are the relative profit--contribution by different accounts?contribution by different accounts?What is the minimum size of accounts which is profitable?What is the minimum size of accounts which is profitable?Which marketing channel provides most profitable operations Which marketing channel provides most profitable operations for a given sales volume?for a given sales volume?

Sales Audit, Sales Analysis & Sales Audit, Sales Analysis & Marketing Cost AnalysisMarketing Cost Analysis

Sales Force ManagementSales Force ManagementChapter 8Chapter 8

1919

Marketing Cost AnalysisMarketing Cost Analysis--Techniques Techniques

Classification Classification of of selling Expenses:selling Expenses: under the following under the following two categories.two categories.

Indirect Expenses (Overheads): Indirect Expenses (Overheads): These are common expenses These are common expenses allocated based on degree of utilization by each allocated based on degree of utilization by each territory/salesman.territory/salesman.Direct Expenses: Direct Expenses: Expenses such as salesmen's salaries, Expenses such as salesmen's salaries, commissions, travel and entertainment expenses.commissions, travel and entertainment expenses.

Grouping Grouping of of "Activity Heading"Activity Heading““: : all expenses related to all expenses related to a particular sales person or territory are grouped together a particular sales person or territory are grouped together irrespective of their accounting heads.irrespective of their accounting heads.Allocation Allocation of of Overheads:Overheads: are made logically, not on are made logically, not on products but on sales territory, or sales person or on products but on sales territory, or sales person or on customer accounts. customer accounts.

Sales Audit, Sales Analysis & Sales Audit, Sales Analysis & Marketing Cost AnalysisMarketing Cost Analysis

Sales Force ManagementSales Force ManagementChapter 8Chapter 8

2020

Marketing Cost AnalysisMarketing Cost Analysis--TechniquesTechniques

Contribution MarginContribution Margin: As marketing cost : As marketing cost analysis, focuses on 'activity heading' of expenses analysis, focuses on 'activity heading' of expenses and allocation is made on logical bases, relative and allocation is made on logical bases, relative profitability is measured as contribution margin. profitability is measured as contribution margin. Contribution margin (CM) = Net sales (R) Contribution margin (CM) = Net sales (R) -- Cost Cost of goods sold (C)of goods sold (C)-- Direct Expenses (D)Direct Expenses (D)--(OH(OH11+OH+OH22) Overheads allocated to sales on ) Overheads allocated to sales on logical basis.logical basis.CM=RCM=R--CC--DD--(OH)(OH)11--(OH)(OH)22+P+P where P=Profitwhere P=Profit

Sales Audit, Sales Analysis & Sales Audit, Sales Analysis & Marketing Cost AnalysisMarketing Cost Analysis

Sales Force ManagementSales Force ManagementChapter 8Chapter 8

2121

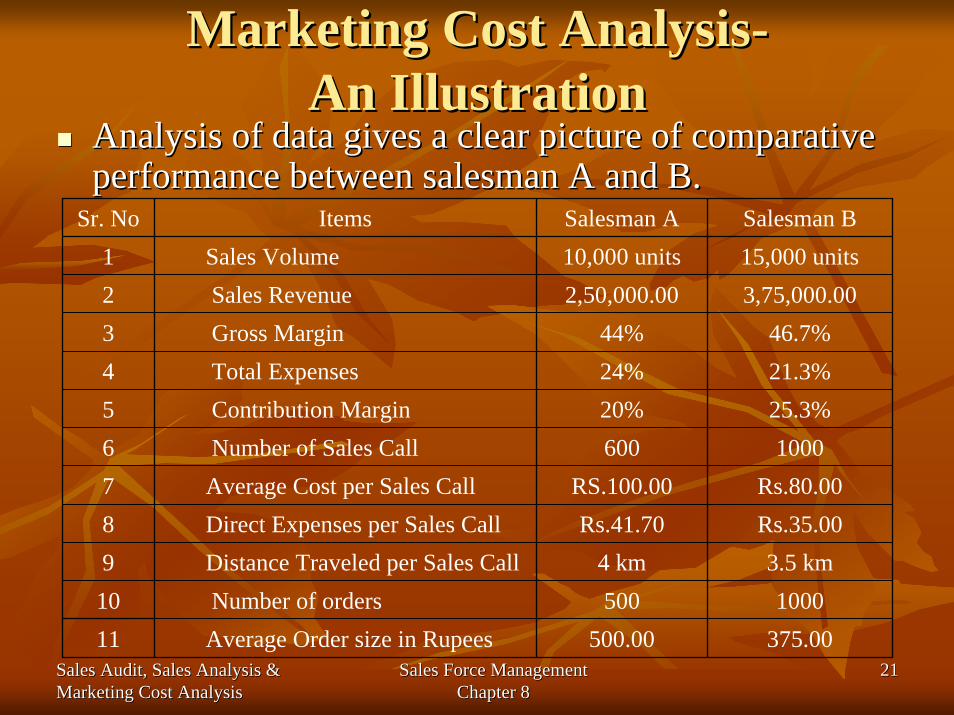

Marketing Cost AnalysisMarketing Cost Analysis--An IllustrationAn Illustration

Analysis of data gives a clear picture of comparative Analysis of data gives a clear picture of comparative performance between salesman A and B.performance between salesman A and B.

Sr. No Items Salesman A Salesman B1 Sales Volume 10,000 units 15,000 units2 Sales Revenue 2,50,000.00 3,75,000.003 Gross Margin 44% 46.7%4 Total Expenses 24% 21.3%5 Contribution Margin 20% 25.3%6 Number of Sales Call 600 10007 Average Cost per Sales Call RS.100.00 Rs.80.008 Direct Expenses per Sales Call Rs.41.70 Rs.35.009 Distance Traveled per Sales Call 4 km 3.5 km10 Number of orders 500 100011 Average Order size in Rupees 500.00 375.00

Sales Audit, Sales Analysis & Sales Audit, Sales Analysis & Marketing Cost AnalysisMarketing Cost Analysis

Sales Force ManagementSales Force ManagementChapter 8Chapter 8

2222

Marketing Research Marketing Research -- ObjectiveObjectiveMarketing research may be defined as "the process of Marketing research may be defined as "the process of organizing, interpreting and integrating data so as to organizing, interpreting and integrating data so as to provide marketing intelligence which will improve provide marketing intelligence which will improve the quality of managerial decisions." the quality of managerial decisions." Primary objectives of marketing research are to Primary objectives of marketing research are to identify information needs of top management and identify information needs of top management and provide them the same to take correct decisions. provide them the same to take correct decisions. In other words, marketing research should be In other words, marketing research should be regarded as a supplement to executive judgement.regarded as a supplement to executive judgement.Marketing research focuses its efforts towards the Marketing research focuses its efforts towards the needs of marketing system to solve the problem.needs of marketing system to solve the problem.

Sales Audit, Sales Analysis & Sales Audit, Sales Analysis & Marketing Cost AnalysisMarketing Cost Analysis

Sales Force ManagementSales Force ManagementChapter 8Chapter 8

2323

Marketing ResearchMarketing Research--Functions Functions

Control Function:Control Function: Provides the organisation Provides the organisation with market feedback of own performance in with market feedback of own performance in terms of sales targets, customer satisfaction terms of sales targets, customer satisfaction and competitive position. and competitive position. Development Function:Development Function: Provides information Provides information on market needs/wants of product and on market needs/wants of product and customers characteristics so as to enable the customers characteristics so as to enable the organisation new direction to open up new organisation new direction to open up new market opportunities.market opportunities.

Sales Audit, Sales Analysis & Sales Audit, Sales Analysis & Marketing Cost AnalysisMarketing Cost Analysis

Sales Force ManagementSales Force ManagementChapter 8Chapter 8

2424

Marketing Research Marketing Research Nature and ScopeNature and Scope

Is marketing research an art or a science? Is marketing research an art or a science? As a scientific study, it passes through steps like As a scientific study, it passes through steps like

Identification of problem (curiosity), Identification of problem (curiosity), An assumption (hypothesis) data collection, An assumption (hypothesis) data collection, Analysis (testing) and Analysis (testing) and Conclusions from the findings (rejection or acceptance of Conclusions from the findings (rejection or acceptance of hypothesis). hypothesis).

It needs conceptual skill and creative mind. Both lead It needs conceptual skill and creative mind. Both lead to artistic approach in marketing research. to artistic approach in marketing research. In other words marketing research is an art as well as In other words marketing research is an art as well as a science.a science.

Sales Audit, Sales Analysis & Sales Audit, Sales Analysis & Marketing Cost AnalysisMarketing Cost Analysis

Sales Force ManagementSales Force ManagementChapter 8Chapter 8

2525

Market Research Verses Market Research Verses Marketing Research Marketing Research

Scope:Scope: Market research is concerned with size, Market research is concerned with size, composition and structure of market, whereas marketing composition and structure of market, whereas marketing research is concerned with solving specific problem in research is concerned with solving specific problem in the marketing system. the marketing system. Focus:Focus: Market research emphasizes on quantitative Market research emphasizes on quantitative dimensions about market like market potential, market dimensions about market like market potential, market share etc. Marketing research emphasizes qualitative share etc. Marketing research emphasizes qualitative aspects like needs and wants of market, unsatisfaction or aspects like needs and wants of market, unsatisfaction or frustration of customers, motivation and morale level of frustration of customers, motivation and morale level of sales persons. sales persons.

Sales Audit, Sales Analysis & Sales Audit, Sales Analysis & Marketing Cost AnalysisMarketing Cost Analysis

Sales Force ManagementSales Force ManagementChapter 8Chapter 8

2626

Marketing ResearchMarketing Research--LimitationsLimitationsPreponderance with Present:Preponderance with Present: Marketing research Marketing research focuses on present problem. focuses on present problem.

Work out longWork out long--term strategic "marketing plan" which will term strategic "marketing plan" which will enable individual studies to provide information which is enable individual studies to provide information which is useful not only for shortuseful not only for short--term solution but also for longterm solution but also for long--term term applications.applications.

Narrow Scope:Narrow Scope: Data collection and analysis is often Data collection and analysis is often related to isolated cases. related to isolated cases.

Knowledge gained can be codified and stored to enrich the Knowledge gained can be codified and stored to enrich the "body of knowledge." "body of knowledge." AdAd--hocism can be substituted by predictive research using hocism can be substituted by predictive research using hypothesis by encouraging creativity and innovation.hypothesis by encouraging creativity and innovation.

Obsession with Techniques:Obsession with Techniques: Too much attention on Too much attention on O.R. techniques often lead to "inwardO.R. techniques often lead to "inward--looking" looking" approach. approach.

Sales Audit, Sales Analysis & Sales Audit, Sales Analysis & Marketing Cost AnalysisMarketing Cost Analysis

Sales Force ManagementSales Force ManagementChapter 8Chapter 8

2727

Functions Of Marketing Research Functions Of Marketing Research Control Functions Control Functions

Short Term Control:Short Term Control:Sales performance Vs. targets (quotas)Sales performance Vs. targets (quotas)Market share/penetration strategy and achievementMarket share/penetration strategy and achievementFirm's competitive positioning visFirm's competitive positioning vis--àà--vis the competitor's vis the competitor's products.products.

Long Term Control:Long Term Control:Bringing out necessary changes in the sales targets in the Bringing out necessary changes in the sales targets in the original plan based on experience, data and analysis.original plan based on experience, data and analysis.Take actions necessary to bring about long term brand Take actions necessary to bring about long term brand privilege (loyalty) by customersprivilege (loyalty) by customersBy getting market intelligence, bring about necessary changes By getting market intelligence, bring about necessary changes in product mix, product technology and product attributes.in product mix, product technology and product attributes.

Sales Audit, Sales Analysis & Sales Audit, Sales Analysis & Marketing Cost AnalysisMarketing Cost Analysis

Sales Force ManagementSales Force ManagementChapter 8Chapter 8

2828

Functions Of Marketing Research Functions Of Marketing Research Development FunctionsDevelopment Functions

Marketing R&DMarketing R&D: : Need and Want Analysis: To find out unsolved problems Need and Want Analysis: To find out unsolved problems (need) and unsatisfied wants to discover new opportunities.(need) and unsatisfied wants to discover new opportunities.Concept testing: To examine feasibility of an "idea" to Concept testing: To examine feasibility of an "idea" to capitalize an opportunity. capitalize an opportunity. Product Testing: Having developed product, one must Product Testing: Having developed product, one must satisfy whether the product have all desirable attributes satisfy whether the product have all desirable attributes envisaged in the original concept.envisaged in the original concept.Test Marketing: Test Marketing is to examine, how far the Test Marketing: Test Marketing is to examine, how far the market/customer accepts the product, to meet firm's market/customer accepts the product, to meet firm's objective in terms of sales volume and sales profit.objective in terms of sales volume and sales profit.

Sales Audit, Sales Analysis & Sales Audit, Sales Analysis & Marketing Cost AnalysisMarketing Cost Analysis

Sales Force ManagementSales Force ManagementChapter 8Chapter 8

2929

Functions Of Marketing ResearchFunctions Of Marketing Research--Development FunctionsDevelopment Functions

Consumer CharacteristicsConsumer Characteristics: : Consumer Consumer promotion steps include advertisement, public promotion steps include advertisement, public relations exercise, personal selling and other relations exercise, personal selling and other consumer and dealer promotion steps consumer and dealer promotion steps Demand of a product depends on :Demand of a product depends on :

Product attributes and sales performanceProduct attributes and sales performanceEffectiveness of advertisement through mass Effectiveness of advertisement through mass media media Consumer perception and buying behaviour etc.Consumer perception and buying behaviour etc.

Sales Audit, Sales Analysis & Sales Audit, Sales Analysis & Marketing Cost AnalysisMarketing Cost Analysis

Sales Force ManagementSales Force ManagementChapter 8Chapter 8

3030

Monitoring Environmental Change Monitoring Environmental Change

Monitoring environmental changes are most essential Monitoring environmental changes are most essential for both the functions given above for both the functions given above viz., viz., control function control function and development function.and development function.Changes occur on social, economic and fiscal policies as Changes occur on social, economic and fiscal policies as well as changes of perception by consumers which are well as changes of perception by consumers which are difficult to detectdifficult to detectControl and development functions must keep a constant Control and development functions must keep a constant vigil in discovering, diagnosing and providing vigil in discovering, diagnosing and providing suggestions to solve problems and commercially exploit suggestions to solve problems and commercially exploit fully the opportunities offered by the environment.fully the opportunities offered by the environment.

Sales Audit, Sales Analysis & Sales Audit, Sales Analysis & Marketing Cost AnalysisMarketing Cost Analysis

Sales Force ManagementSales Force ManagementChapter 8Chapter 8

3131

Research On Industrial Products Research On Industrial Products And ServicesAnd Services--Nature & ScopeNature & Scope

Research on industrial products and services Research on industrial products and services covers the following types of studies covers the following types of studies

Long range/short range sales forecastingLong range/short range sales forecastingMarket potential and shareMarket potential and shareMarket characteristicsMarket characteristicsConsumer characteristicsConsumer characteristicsAnalysis of sales performanceAnalysis of sales performance

The focus of industrial research is to assist The focus of industrial research is to assist managerial decisions. managerial decisions.

Sales Audit, Sales Analysis & Sales Audit, Sales Analysis & Marketing Cost AnalysisMarketing Cost Analysis

Sales Force ManagementSales Force ManagementChapter 8Chapter 8

3232

Market ResearchMarket Research--Organisation Organisation Centralised OrganisationCentralised Organisation:: In this case, the organisation is of In this case, the organisation is of centralized structure and O.R. team can be organised in the centralized structure and O.R. team can be organised in the following two patterns.following two patterns.

Single Research Team: Single Research Team: Attached to each division, tackling all problems in Attached to each division, tackling all problems in that divisionthat divisionMultiple Team: Multiple Team: Each specialized on a specific area like "demand Each specialized on a specific area like "demand forecasts," "consumer behaviour," "performance evaluation" etc. forecasts," "consumer behaviour," "performance evaluation" etc. All such All such teams report to a centralized authorityteams report to a centralized authority

Matrix Type OrganisationMatrix Type Organisation:: Here R&D team is attached to each Here R&D team is attached to each division. Divisional manager control them administratively. division. Divisional manager control them administratively. However, they hold functional relationship with central R&D However, they hold functional relationship with central R&D chief.chief.Decentralised OrganisationDecentralised Organisation:: In this case, the R&D team is In this case, the R&D team is decentralized and reporting to divisional head both decentralized and reporting to divisional head both administratively and functionally.administratively and functionally.

Sales Audit, Sales Analysis & Sales Audit, Sales Analysis & Marketing Cost AnalysisMarketing Cost Analysis

Sales Force ManagementSales Force ManagementChapter 8Chapter 8

3333

Method of Investigation and Method of Investigation and Analysis Analysis

Identification of problemIdentification of problemDevelopment of objectives Development of objectives PrePre--planning activities like research design, sampling planning activities like research design, sampling design, deciding on type, source and method of design, deciding on type, source and method of collecting data etc.collecting data etc.Data collection Data collection -- Primary, secondary, questionnaire, Primary, secondary, questionnaire, display technique, expert opinion, etc.display technique, expert opinion, etc.Data Analysis Data Analysis -- textual discussion and interpretation textual discussion and interpretation of data of data Report presentation. Report presentation. FollowFollow--up and feedback.up and feedback.

Sales Audit, Sales Analysis & Sales Audit, Sales Analysis & Marketing Cost AnalysisMarketing Cost Analysis

Sales Force ManagementSales Force ManagementChapter 8Chapter 8

3434

Types of Market Research Studies Types of Market Research Studies

The most popular market research studies are The most popular market research studies are the following:the following:

Sales control researchSales control researchSales/Demand forecastSales/Demand forecastCustomer analysisCustomer analysisCompetitor analysisCompetitor analysisSales control research consists of "Market Sales control research consists of "Market Analysis" and "Sales Analysis". Analysis" and "Sales Analysis".

Sales Audit, Sales Analysis & Sales Audit, Sales Analysis & Marketing Cost AnalysisMarketing Cost Analysis

Sales Force ManagementSales Force ManagementChapter 8Chapter 8

3535

Sales Control Research Sales Control Research

Sales control research may be defined as "a research Sales control research may be defined as "a research designed to enable sales manager to achieve sales designed to enable sales manager to achieve sales goal." goal." Sales control research consists of the following steps.Sales control research consists of the following steps.

Market Analysis.Market Analysis.Sales Analysis.Sales Analysis.

Sales analysis breaks down sales activity into small Sales analysis breaks down sales activity into small manageable units for the manager to achieve sales manageable units for the manager to achieve sales targets for each territory, customer and product range.targets for each territory, customer and product range.

Sales Audit, Sales Analysis & Sales Audit, Sales Analysis & Marketing Cost AnalysisMarketing Cost Analysis

Sales Force ManagementSales Force ManagementChapter 8Chapter 8

3636

Market Analysis Market Analysis

Sales target of products: Sales target of products: This is derived out of sales forecastThis is derived out of sales forecastSales forecast forms the basis of planning. Sales forecast forms the basis of planning. By breaking down the forecast of entire By breaking down the forecast of entire market into small manageable groups, we market into small manageable groups, we get sales target of product for each market get sales target of product for each market segment. segment.

Sales Audit, Sales Analysis & Sales Audit, Sales Analysis & Marketing Cost AnalysisMarketing Cost Analysis

Sales Force ManagementSales Force ManagementChapter 8Chapter 8

3737

Market AnalysisMarket AnalysisSales Target for Market Segment :Market analysis is the Sales Target for Market Segment :Market analysis is the process of breaking down large markets into smaller market process of breaking down large markets into smaller market segments and determining the relative sales potential in each.segments and determining the relative sales potential in each.Market Potential: Market Potential: This is defined as the "total possible sales of This is defined as the "total possible sales of a given product in a given area at a given time, under, given a given product in a given area at a given time, under, given marketing conditions."marketing conditions."Sales Potential: Sales Potential: This is the "estimate of maximum possible This is the "estimate of maximum possible sales opportunities present in a particular market segment sales opportunities present in a particular market segment opened to specified company selling a product for a given opened to specified company selling a product for a given period."period."Relative Sales Potential: Relative Sales Potential: Relative sales potential is defined as Relative sales potential is defined as "the potential sales of a given seller's product in a given "the potential sales of a given seller's product in a given market segment as compared to other market segments under market segment as compared to other market segments under the conditions existing at that time."the conditions existing at that time."

Sales Audit, Sales Analysis & Sales Audit, Sales Analysis & Marketing Cost AnalysisMarketing Cost Analysis

Sales Force ManagementSales Force ManagementChapter 8Chapter 8

3838

The Process of Market Analysis The Process of Market Analysis The analytical process of market analysis starts with The analytical process of market analysis starts with forecast of total sales of a given product for the entire forecast of total sales of a given product for the entire market and determine what portion or percentage of market and determine what portion or percentage of total sale be possible for each of the market segments. total sale be possible for each of the market segments. Market segments can be made based on a number of Market segments can be made based on a number of criteria. Geographic basis is most popular among criteria. Geographic basis is most popular among them. them. Two methods used here are the following:Two methods used here are the following:

Corollary Data MethodCorollary Data MethodDirect Data Method.Direct Data Method.

Sales Audit, Sales Analysis & Sales Audit, Sales Analysis & Marketing Cost AnalysisMarketing Cost Analysis

Sales Force ManagementSales Force ManagementChapter 8Chapter 8

3939

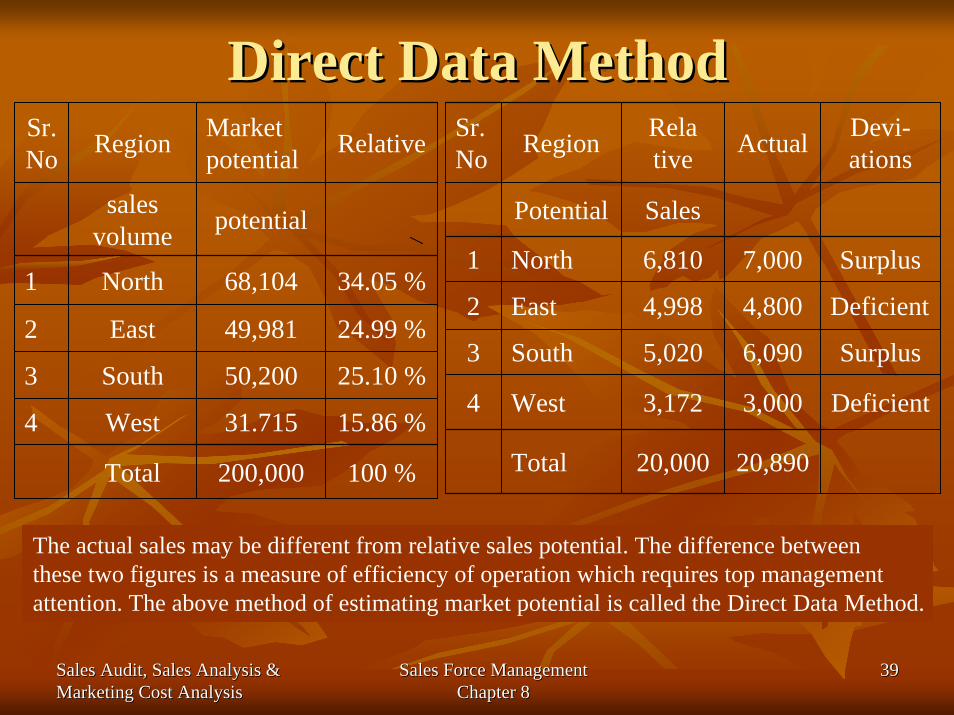

Direct Data Method Direct Data Method Sr. No Region Market

potential Relative

sales volume potential

1 North 68,104 34.05 %

2 East 49,981 24.99 %

3 South 50,200 25.10 %

4 West 31.715 15.86 %

Total 200,000 100 %

Sr. No Region Rela

tive Actual Devi-ations

Potential Sales

1 North 6,810 7,000 Surplus

2 East 4,998 4,800 Deficient

3 South 5,020 6,090 Surplus

4 West 3,172 3,000 Deficient

Total 20,000 20,890

The actual sales may be different from relative sales potential. The difference between these two figures is a measure of efficiency of operation which requires top management attention. The above method of estimating market potential is called the Direct Data Method.

Sales Audit, Sales Analysis & Sales Audit, Sales Analysis & Marketing Cost AnalysisMarketing Cost Analysis

Sales Force ManagementSales Force ManagementChapter 8Chapter 8

4040

Corollary Data Method Corollary Data Method Total industry sales by geographical areas are available for Total industry sales by geographical areas are available for major industries and products like gasoline. However, such major industries and products like gasoline. However, such statistics are not available for a number of products and statistics are not available for a number of products and smaller industries.smaller industries.As a result, most firms resort to using general or related data As a result, most firms resort to using general or related data of other products to derive demand of own products.of other products to derive demand of own products.Weightages of general data such as disposable income, retail Weightages of general data such as disposable income, retail sales and population are used in the ratio of 5, 3 and 2 in sales and population are used in the ratio of 5, 3 and 2 in determining demand of a number of consumer products in determining demand of a number of consumer products in various regions, in buying power index (BPI) method.various regions, in buying power index (BPI) method.This method is also called "multiple factor index" method. This method is also called "multiple factor index" method. Special multiple factor indexes are also used to forecast Special multiple factor indexes are also used to forecast demand. demand. These methods are called corollary data methodThese methods are called corollary data method