Embed Size (px)

Citation preview

Consolidation in the European banking industry: how effectiveis it?

Ana Lozano-Vivas • Subal C. Kumbhakar •

Meryem Duygun Fethi • Mohamed Shaban

Published online: 6 April 2011

� Springer Science+Business Media, LLC 2011

Abstract The European banking industry is becoming

increasingly consolidated as banks engage in domestic and

cross-border merger and acquisition (M&A) activities. Due

to cultural differences in cross-border consolidations, the

benefits of domestic and cross-border consolidations are

likely to differ. This paper examines the effectiveness of

merger processes, with a detailed analysis of both domestic

and cross-border consolidations in Europe from 1998 to

2004. Effectiveness is measured via several criteria:

improvement in costs, return on assets (ROA), and return

on equity (ROE). To analyze potential cost efficiency

improvement, we use a stochastic cost frontier approach.

The same methodology is used for ROA and ROE to

estimate efficiency in profitability. Finally, considering

cross-border mergers as a form of entry, we carry out an

analysis of the entry effect in response to the performance

and profitability of the incumbent market participants.

Results show that mergers in the European banking

industry have been effective. Although domestic M&As

are more common than cross-border M&As, banks

involved in cross-border M&As are more efficient. More-

over, cross-border merged banks seem to outperform

incumbent banks.

Keywords Cross-border and in-border merger and

acquisitions � Stochastic frontier � Return on assets �Return on equity

JEL Classification D24 � G21 � G34

1 Introduction

The last three decades have witnessed significant consoli-

dations in the European banking sector and the rest of the

world. In particular, the globalization of international

financial systems, technological advances, and enhance-

ments in the cross-border regulatory environment con-

nected to the single-market program (SMP) and the

introduction of the euro have facilitated consolidation

activities through merger and acquisitions (M&As) within

the European Union (EU) banking sector. These consoli-

dation activities have changed the structure of the banking

industry throughout Europe and the rest of the world.

Since increases in market share, improvements in effi-

ciency and profitability, and the diversification of portfolios

are expected outcomes after bank consolidations, both

academicians and policy makers are interested in knowing

the impact of bank consolidation on (1) market power, (2)

bank performance, and (3) the creation of value for

shareholders. However, there are only a few studies in the

literature that analyze M&As in the EU, compared to the

numerous studies on the US experience (e.g., Berger et al.

1999; Amel et al. 2004, among many others).

A. Lozano-Vivas

Dpto. de Teorıa e Historia Economica, Universidad de Malaga,

Plza. El Ejido s/n., 29013 Malaga, Spain

e-mail: [email protected]

S. C. Kumbhakar

Department of Economics, State University of New York,

Binghamton, NY 13902, USA

e-mail: [email protected]

M. D. Fethi (&) � M. Shaban

School of Management, University of Leicester, Leicester,

England, UK

e-mail: [email protected]

M. Shaban

e-mail: [email protected]

123

J Prod Anal (2011) 36:247–261

DOI 10.1007/s11123-011-0212-8

In the last two decades, a growing body of empirical

literature seeking to measure the effects of bank consoli-

dation on performance has emerged, including studies that

analyze changes in merged banks’ performance using

accounting measurements, return on assets (ROA) and

return on equity (ROE), cost and profit frontier analyses,

and so forth, to quantify gains in profitability and effi-

ciency (Berger et al. 1999). Nevertheless, most of the

available knowledge on the performance of bank consoli-

dation comes from the US banking market (Pilloff and

Santomero 1998). In contrast, much less attention has been

paid to the European banking market (Vander Vennet

2002).

The standard hypothesis is that M&As boost the effi-

ciency and profitability of consolidating banks, and good

performance and profitability contribute toward the safety

and stability of financial institutions. This paper seeks to

evaluate the effectiveness of consolidation not only on cost

efficiency but also on profitability. Moreover, given that

consolidation is a natural outcome of integration (Abraham

and Van Dijcke 2002; Vander Vennet 2002; Altunbas and

Ibanez 2004), it is quite important to investigate its efficacy

within the EU context. Furthermore, since cross-border

consolidations can strengthen competition, in the sense that

market entry is facilitated, providing a possible avenue for

achieving integration through cross-border banking activi-

ties may be refreshing and innovative. Thus, exploring

these issues for both domestic and cross-border M&As in

Europe is an important task.

Our study analyzes the effectiveness of domestic and

cross-border consolidations in Europe. We use a sample of

commercial banks from 14 European countries during

1998–2004 and measure effectiveness via several criteria,

namely, improvements in costs, ROA, and ROE, using the

stochastic frontier approach (SFA). Analyzing within-border

(domestic) as well as cross-border consolidations allows us

to extend our study and to examine the entry effect in

response to the performance and profitability of incumbent

market participants. Our results suggest that consolidated

banks have higher cost efficiency and higher profitability (in

terms of ROA and ROE) compared to those that are not

involved in consolidation. Moreover, although domestic

M&As are more common than cross-border ones, banks

involved in cross-border M&As are more efficient. Addi-

tionally, the entry effect results seem to suggest that banks

involved in cross-border mergers have a higher chance of

survival in the long run.

The rest of the paper is organized as follows. Section 2

reviews the relevant empirical literature. Section 3 explains

the model and the methodology. Data and variable selec-

tion are discussed in Sect. 4. Empirical results are pre-

sented in Sect. 5. Finally, Sect. 6 presents a summary of the

results and makes some concluding remarks.

2 Literature

Berger et al. (1999) and Amel et al. (2004) present excel-

lent international surveys on consolidation studies in

financial services industries. In particular, these studies

evaluate the causes, consequences, and future implications

of banking consolidations. Overall, they show that there is

an extensive empirical literature on US banking consoli-

dation, whereas such studies are limited for Europe. Fur-

thermore, these surveys disclose that there are two

methodological strands that analyze the impact of consol-

idation on bank performance.

One strand of the empirical literature uses an event

study methodology, mainly to examine shareholders wealth

creation, whereby the effect of merger deal announcements

is measured against any price change in specific financial

market assets. Cornett and Tehranian (1992), Houston and

Ryngaert (1994), Pilloff (1996), Kane (2000), and Houston

et al. (2001), among others, use this methodology for

studying US cases, while Cybo-Ottone and Murgia (2000),

Beitel and Schiereck (2001), Beitel et al. (2004), and

Campa and Hernando (2004, 2006), among others, apply it

to European situations. Although it is worth noting that

there is a widespread skepticism in the financial markets

regarding the potential of bank mergers for creating value,

the above studies reveal that there is some evidence to

suggest that value creation occurs when both the acquirer

and target banks involved in the M&A process are from the

same country (Campa and Hernando 2004) or headquar-

tered in the same state (Kane 2000). Thus, it seems that

merged banks do not have to go through the complexities

in integrating banks from different regions or countries.

The second strand of research measures pre- and post-

merger bank performance. This approach mainly analyzes

changes in the post-merger and pre-merger performances of

merged banks, using accounting measurements (including

ROA/ROE and cost/profit) and various functional forms,

mainly in the frontier approach. Berger et al. (1999) classify

these studies into static and dynamic categories. Studies

from the United States that utilize accounting ratios with

data sets from the 1980s produce varied results. For

instance, Cornett and Tehranian (1992) find that the profit-

ability ratios improve with M&As, whereas Berger and

Humphrey (1992) find no such improvement. Another study

on large US banks finds little change in cost efficiency after

M&As, and an improvement in profit efficiency, particularly

for large banks that were relatively inefficient prior to

mergers (Akhavein et al. 1997).

The evidence for European banks using similar meth-

odologies is broadly consistent with the US experience.

Vander Vennet (1996) uses cost and profit to examine

performance for a sample of 492 European takeovers over

the period 1988–1993 and finds that only domestic mergers

248 J Prod Anal (2011) 36:247–261

123

among equal-sized firms tend to have a positive impact on

profitability. However, Dıaz et al. (2004) find an increase in

the acquirers’ long-term profitability for a sample of 181

acquisitions carried out in Europe between 1993 and 2000.

Individual country studies in Europe also produce dif-

ferent results. For instance, Resti (1998) uses DEA to

analyze 67 Italian deals and concludes that merged banks

seem to improve their efficiency in the post-merger period.

Likewise, Vander Vennet (1996) finds that efficiency

increases more when two different-sized banks merge. A

study on Spanish savings banks over the period 1985–1998

by Cuesta and Orea (2002) uses a stochastic output

distance function and finds that non-merged banks are, on

average, more efficient than merged ones. Moreover, Lang

and Welzel (1999) find no evidence of efficiency gains

from mergers in German cooperative banks for 283

mergers from 1989 to 1997.

Most of the European studies reviewed above focus on

domestic bank consolidations; there is little research on the

performance effects of cross-border consolidations in

Europe. Belonging to the first strand of the literature but

considering cross-border consolidations, Abraham and Van

Dijcke (2002) find that domestic M&As perform better

than cross-border merged banks or those not involved in

any kind of merger. However, included in the second

strand of the literature and analyzing cross-border consol-

idations, Altunbas and Ibanez (2004) find that bank

mergers in Europe, particularly cross-border mergers,

result in improved ROE over the period 1992–2001.

Additionally, Vander Vennet (2002) finds that before

M&A transactions take place, acquirer banks outperform

target ones in terms of profit and cost efficiencies. Vander

Vennet (2002) also finds that in cross-border mergers there

is a partial profit improvement in ex post performance, with

no gains in terms of cost efficiency. The author argues that

these results suggest the existence of various types of

barriers to operational efficiency in cross-border deals.

Finally, recent research using international data sets

including both US and European banks investigates

potential efficiency gains from cross-border consolidations

and examines trends in international financial integration

and international M&As. For example the study of Berger

et al. (2000) is the most exhaustive and examines the profit

and cost efficiency differences between the United States

and four European countries, using more than 2,000 banks.

The authors find that domestic banks are generally more

efficient than foreign banks, suggesting that cross-border

consolidations in Europe are significantly affected by

‘‘efficiency’’ barriers such as geographical distance, lan-

guage and cultural differences, currency, and regulatory or

supervisory structures (Berger et al. 2001).

It is clear from the above that little effort has been

directed toward analyzing the overall trend of the effect

on the performance of European bank consolidations and

the real effectiveness of merger processes, with a

detailed examination of both domestic and cross-border

consolidations. This study aims to fill this gap and shed

light on the effectiveness of consolidations in the EU

commercial banking sector, using various performance

measures.

3 Methodology

Our objective is to measure the overall cost and profit-

ability gains resulting from within-border (domestic) and

cross-border consolidations. We model such overall gains

through (1) changes (shifts) in technology and (2)

improvements in managerial efficiency (management). We

use several criteria (cost, ROA, and ROE) to examine the

effectiveness of both types of consolidations in the Euro-

pean banking industry.

We use cost, ROA, and ROE frontiers to analyze

changes in technology, and the SFA to estimate

improvements in managerial efficiency. Gains in terms of

technology change are examined by testing whether

within and cross-border mergers lead to a shift in the cost,

ROA, or ROE frontiers (improvement in technology

labeled as the direct effect of within- and cross-border

mergers on cost and profitability); that is, we examine

whether the shift in the cost (ROA, ROE) frontier leads to

a reduction (increase) in cost (ROA, ROE), ceteris pari-

bus. We also examine whether within- and cross-border

mergers lead to an improvement in managerial efficiency.

This is done via the SFA, in which the one-sided ineffi-

ciency term is made a function of within- and cross-border

mergers. We label this as the indirect effect of within- and

cross-border mergers on cost and profitability (ROA,

ROE). More specifically, we estimate a cost (ROA, ROE)

frontier in which the inefficiency term is made a function

of within- and cross-border mergers, among other

covariates.

To measure the overall gains on cost from the consoli-

dation of within- and cross-border mergers, we introduce

within- and cross-border variables, along with input prices,

outputs, and other control variables (i.e., time trend, a

quasi-fixed input variable, and country dummies) in the

cost function. The coefficients associated with the merger

variables show whether the technology for merged (within-

or cross-border) banks is different from those that are not

involved with mergers. Similarly, the coefficients of the

within- and cross-border variables in the inefficiency

function show whether or not mergers decrease

inefficiency.

Assuming a Cobb–Douglas (CD) functional form, the

cost function with inefficiency is written as

J Prod Anal (2011) 36:247–261 249

123

ln C ¼ b0 þX

bj ln wj þX

am ln ym þX

kqzq þ v

þ u

ð1Þ

where C is total cost and w, y, and z are, respectively, input

prices, outputs, and other control variables (such as quasi-

fixed inputs, time, and country dummies, as well as within-

and cross-border mergers). Finally, v is the noise term and

u C 0 is inefficiency. Note that all these variables have

both bank and time subscripts but are skipped to avoid

notational clutter (to be introduced later when absolutely

necessary). In the inefficiency term we introduce determi-

nants of inefficiency through the variance of the ineffi-

ciency component u, which is assumed to be distributed

half-normally with non-constant variance. Specifically,

we assume that the variance is a function of covariates

(which are often labeled as determinants of inefficiency);

that is, we specify the variance of u r2u

� �as r2

u ¼ exp

c0 þP

n¼1 cnzn

� �, where z includes the within- and cross-

border merger variables (among others), which are also

bank- and time-specific. We assume v to be normally

distributed with mean zero. To control for possible heter-

oskedasticity in the noise component (v), we specify the

variance of v r2v

� �as r2

v ¼ exp d0 þP

s¼1 dsqs

� �, where

the q variables are determinants of heteroskedasticity in the

noise term, and are bank- and time-specific.1 If the variance

of u decreases due to mergers, inefficiency will decrease

(efficiency will increase).2 This follows from the fact that

EðuðzÞÞ ¼ffiffiffiffiffiffiffiffi2=p

pruðzÞ, and therefore the marginal effect of

z on mean inefficiency is directly related to ru(z). Thus,

anything that increases ru(z) will increase (decrease) mean

inefficiency (efficiency). SinceoEðuðzÞÞ

ozn¼

ffiffiffiffiffiffiffiffi2=p

poruðzÞ

ozn, the

mean inefficiency will decrease (increase) iforuðzÞ

ozn\0 ð[ 0Þ.

We estimate the model using the maximum likelihood

(ML) method based on the above distributional assump-

tions. To estimate the inefficiency for each observation, we

use the estimator proposed by Jondrow et al. (1982), i.e.,

u ¼ EðujeÞ, which has a nice algebraic form because the

distribution of u|e is truncated normal. In implementing this

formula, we replace the unknown parameters by their

estimates and e is replaced by the corresponding ML

residuals, viz.,

u ¼ Eðu ej Þ ¼ lþ r�/ðl=r�ÞUðl=r�Þ

� �ð2Þ

where l ¼ e r2u= r2

u þ r2v

� �, r2

� ¼ r2ur

2v= r2

u þ r2v

� �, and

e ¼ uþ v. Note that, although not explicitly specified, both

l and r� are functions of covariates (the z and q variables)

because r2u is a function of the z variables and r2

v is a

function of the q variables. The parameters in Eq. 2 are the

ML estimates (MLEs) of the unknown parameters and e is

the residual of Eq. 1 obtained by using the estimated

(MLE) parameter values. Finally, /(�) and U(�) are the

standard normal probability and cumulative distribution

functions, respectively. One can interpret u as the per-

centage increase in cost due to inefficiency, given that the

cost function is logarithmic. Alternatively, 1� u �expð�uÞ� 1 can be interpreted as cost efficiency, which is

the ratio of the frontier cost to the actual cost. Note that u

is observation specific because it is a function of e, which is

observation specific. Moreover, if the z and q variables are

observation specific, then r� will be observation specific

because both r2u and r2

v will also be observation specific

(via the z and q variables). One can compute the marginal

effect of these z and q variable covariates on cost efficiency

(Wang 2002). This allows us to compute explicitly the

indirect effect of within- and cross-border mergers on cost

fromoEðuðzÞÞ

ozn¼

ffiffi2p

qoruðzÞ

ozn, where E(u(z)) is given in Eq. 2.

Note that E(u(z)) is the same as u in Eq. 2. Wang (2002)

derives the algebraic expression of the above marginal

effects for each z variable.

Besides cost, we are interested in evaluating the effect of

consolidation on profitability. Since ROA and ROE are

often viewed as measures of profitability, we consider these

measures to model the impact of within- and cross-border

variables on profitability. However, ROA and ROE, mea-

sured from raw data, are likely to be affected by random

noise and therefore cannot measure a bank’s true perfor-

mance. Thus, to make sure that managerial efficiency is

reflected in ROA and ROE, it is necessary to estimate them

in such a way that the noise component is eliminated. We

label these as profitability efficiency measures.3 If a bank is

not fully efficient, its ROA (ROE) will be less that the

‘‘optimum’’ ROA (ROE). Therefore this optimum should

be defined as the maximum ROA (ROE) the bank could

have achieved. Consequently, we can write the ROA

1 Since all the variables introduced so far change across banks and

over time, there is no need to introduce bank and time subscripts.2 We introduce determinants of inefficiency through the mean of the

inefficiency term by using a truncated normal distribution. However,

either these models do not converge or the mean function is found to

be not statistically different from zero.

3 In particular, we focus on profitability instead of profit, since

profitability tells us more about the efficiency and performance of

banks than profit. Increasing profitability is one of the most important

tasks of bank managers, who are constantly looking for ways to

change the business to improve profitability (Demirguc-Kunt and

Huizinga 1998). Moreover, without profitability, banks would not

survive in the long run. Thus, the evaluation of bank profitability

seems to be relevant when the effectiveness of the consolidation

process is to be analyzed.

250 J Prod Anal (2011) 36:247–261

123

(ROE) computed from raw data as the true ROA (ROE)

minus a one-sided inefficiency term plus a two-sided noise

term:

ROA ¼ ROA� þ v� u ð3aÞROE ¼ ROE� þ v� u ð3bÞ

where ROA* (ROE*) is the maximum ROA (ROE) that can

be achieved, ceteris paribus. Alternatively, ROA* (ROE*)

can be viewed as the ROA (ROE) frontier. The u term in

Eqs. 3a and 3b can be interpreted as ROA (ROE)

inefficiency—that is, failure to attain the maximum return

on average assets (equity) due to managerial incompetence,

inertia, laziness, and other such things. Although this has

never been done before, there is no reason why one cannot

define an ROA (ROE) frontier and decompose ROA (ROE)

into its maximum value ROA* (ROE*), ceteris paribus, and

the shortfall of ROA (ROE) from its maximum value,

which we label ROA (ROE) inefficiency. If one can use a

production frontier in which case the implicit objective is

to maximize output, the use of ROA (ROE) frontier can be

justified by making the assumption that the objective of

banks is to maximize ROA. This idea can also be justified

from a cost/profit frontier. Consider the alternative profit

function model of Berger and Mester (1997) in which profit

is a function of output and input prices (plus other control

variables such as assets, time, etc.). If this is accepted, then

ROA can be specified as a function of the same variables,

since ROA is profits divided by total assets. The same

holds for ROE. The only issue is whether one wants to

specify ROA (ROE) in the exact same way as cost and/or

alternative profit functions are specified. Here we specify

ROA* (or ROE*) in Eq. 3a (or Eq. 3b) as a function of

some bank-specific covariates:

ROA ¼ b0 þX

q

kqzq þ v� u ð4aÞ

ROE ¼ b0 þX

q

kqzq þ v� u ð4bÞ

where the z variables include within- and cross-border

merger variables, as well as some other variables that can

explain ROA (ROE). The majority of studies on bank

profitability, such as those of Short (1979), Bourke (1989),

Molyneux and Thornton (1992), Demirguc-Kunt and

Huizinga (1998), and Goddard et al. (2004), use linear

models to estimate the impact of various factors that may

be important in explaining profitability. In this literature,

bank profitability is usually expressed as a function of

internal and external determinants. We follow this litera-

ture, since our interest is to analyze the association of ROA

(ROE) with some variables of interest (particularly within-

and cross-border merger variables). The advantage of using

the ROA (ROE) frontier is that, apart from the usual z

variables explaining ROA (ROE), there may be unobserved

management variables that affect the ROA (ROE). This can

be captured by the u term. If certain management attributes

are observed, we can allow them to affect u through the

mean and/or variance of u. The v term is the usual random

noise component that can affect ROA (ROE) positively as

well as negatively, and it is not within any bank’s control.

We therefore assume it to be symmetric with zero mean but

heteroskedastic.

The assumptions on u and v are similar to those in the

cost model, except for the negative sign of u. The param-

eters are estimated using the ML procedure. Finally, the

point estimate of u is obtained from its conditional mean.

Empirically, we replace the unknowns in the conditional

mean function by their estimated/predicted values. The

formula is similar to Eq. 2:

u ¼ lþ r�/ðl=r�Þ

Uð�l=r�Þ

� �ð2aÞ

where e is calculated from the residuals of the ROA (ROE)

function (i.e., e ¼ �uþ v) and l ¼ �e r2u= r2

u þ r2v

� �.

4 Data and variables

4.1 Data

The sample used in this study includes commercial banks

from 14 EU countries covering the period 1998–2004.

These banks are from Austria, Belgium, Finland, France,

Germany, Greece, Ireland, Italy, Luxembourg, the Neth-

erlands, Portugal, Spain, Sweden, and the United Kingdom.

The data used in the study were collected in two phases. In

the first stage, we used data from Thomson’s SDC Plati-

num Database on domestic and cross-border M&A deals

over the period 1998–2004. In the second stage, we used

data on the annual financial statements of the banks from

Fitch IBCA’s BankScope database. This was done to

compile information on input and output variables over the

period 1998–2004.

The SDC Platinum database is provided by Thomson

Corporation, a leading global provider of integrated

information-based solutions for business and professional

customers. The data extracted include essential information

for analysis, that is, the completion dates of M&A trans-

actions and the full names and countries of origin of target

and acquirer banks. Since our interest is on targets and

acquirers within the EU, we extract only completed and

unconditional M&A transactions that occurred during the

period under analysis. These M&A transactions did not

involve any failing banks or mergers carried out by gov-

ernment assistance.

J Prod Anal (2011) 36:247–261 251

123

The criterion we use to extract the relevant M&A

transaction data is that the acquirer’s pre-acquisition

ownership in the target capital is less than 50% and post-

acquisition ownership is greater than or equal to 51%.4 In

the 14 selected European countries, the total numbers of

banks involved in domestic M&A deals as acquirers and

targets from 1998 to 2004 are 84 and 125, respectively.

However, banks involved in cross-border M&A activities

during the same period comprise 33 acquirers and 63 target

banks. We then use the BankScope database to extract

more detailed financial information, not only for the banks

involved in the M&A deals but also for those not involved

in such deals. Our search criterion is to include financial

data from active banks only. We collect relevant data on

the inputs and outputs used in the estimation.

BankScope is a financial database compiled by Fitch

IBCA containing financial information, mostly from bal-

ance sheets, income statements, and applicable notes in the

audited annual reports of banks and depository institutions.

As a result, we gather data from annual financial data on

the inputs and outputs of 4,310 commercial banks from 14

European countries starting in 1998. We conduct an

exhaustive process to amalgamate the information from the

two data sets into one final data set. We use individual bank

names and any previous bank names or nicknames pro-

vided by SDC Platinum Data as search tools with which to

find matching banks within the whole sample of 4,310

banks collected from the BankScope database.

In our sample, Italy is the most active country in

domestic M&A transactions, with 62% of the total, fol-

lowed by France and Spain, with 22.5 and 14%, respec-

tively. However, Belgium’s cross-border M&As account

for 6% of the total number, placing Belgium at the top of

the list of countries involved in cross-border M&As.

4.2 Variables

To estimate the cost frontier, banking outputs and input

prices are needed. For this, one has to first decide on a

particular approach. This study uses the value-added

approach of Berger and Humphrey (1992), which considers

deposits as both inputs and outputs at the same time. The

inputs include borrowed funds, labor, and physical capital.

The price of borrowed funds is defined as interest paid

divided by all borrowed funds. The price of labor is mea-

sured as personnel expenses divided by total assets, since

data on employee numbers are not available (for this

approach see, e.g., Altunbas et al. 2001; Weill 2003).

Finally, the price of physical capital is defined as the ratio

of non-interest expenses other than personnel expenses to

fixed assets. The output variables include loans, deposits,

and other earning assets. Total cost is the sum of paid

interest, personnel expenses, and non-interest expenses

other than personnel expenses. Following Berger and

Mester (1997) we specify equity as a quasi-fixed input,

because insolvency risk affects banks’ costs.5 Additionally,

time trend and country dummies are included as covariates

in the cost function to accommodate technical change and

to control country-specific fixed effects such as culture and

work habits. Finally, to control for merger effects follow-

ing our methodology, we introduce within- and cross-bor-

der merger variables in the cost frontier, as well as in the

inefficiency component.

Two measures of profitability, ROA and ROE, are used

in this study: ROA is net income to total assets and ROE is

net income to total equity.6 While ROA tells us how suc-

cessfully a bank’s assets are being used to generate profits,

ROE provides a measure of how much banks are earning

on their equity investment. Following the literature on

bank profitability (e.g., Short 1979; Goddard et al. 2004;

Athanasoglou et al. 2008), we express profitability as a

function of internal and external factors. While the internal

factors are bank-specific determinants of profitability, the

external factors are those that are not related to bank

management but reflect the economic and legal environ-

ment that affects bank operations and performance. In our

study, the profitability measures ROA and ROE are defined

as functions of a set of seven variables that are internal

determinants of bank profitability when a merger process

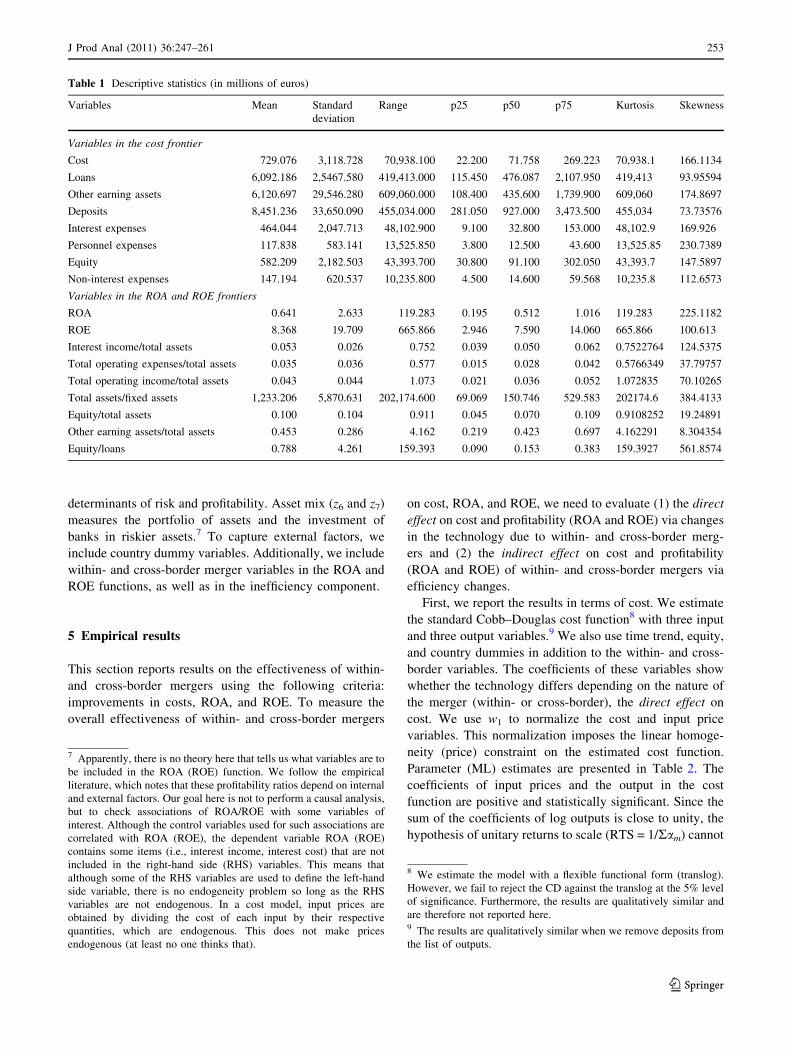

is at hand (Knapp et al. 2005). Table 1 contains the

descriptive statistics of the variables used in the empirical

exercise.

The variables used as internal determinants in the ROA

and ROE functions can be divided into four groups:

(1) revenue-related variables (interest earning assets to

total assets, z1, and non-interest income to total assets, z2),

(2) expense-related variables (operating expenses to total

assets, z3, and fixed assets to total assets, z4), (3) asset

quality-related variables (equity to total assets, z5), and

(4) asset mix (other earning assets to total assets), z6, and

loan to equity, z7. Revenue-related variables (z1 and z2)

measure how the traditional lending business is supple-

mented by fee-based revenue. One of the most important

causes of poor bank performance after a merger is the

generation of inadequate fee income (Knapp et al. 2005).

Expense-related variables (z3 and z4) are very important

determinants of profitability and are closely related to

the notion of efficient management. Asset quality (z5)

measures bank capitalization and is one of the major

4 We follow the same criteria that Lozano-Vivas and Weill (2009)

use.

5 We use fixed capital as a proxy for size in the variance of the noise

component.6 Net income in the definition of ROA and ROE is profit before tax.

252 J Prod Anal (2011) 36:247–261

123

determinants of risk and profitability. Asset mix (z6 and z7)

measures the portfolio of assets and the investment of

banks in riskier assets.7 To capture external factors, we

include country dummy variables. Additionally, we include

within- and cross-border merger variables in the ROA and

ROE functions, as well as in the inefficiency component.

5 Empirical results

This section reports results on the effectiveness of within-

and cross-border mergers using the following criteria:

improvements in costs, ROA, and ROE. To measure the

overall effectiveness of within- and cross-border mergers

on cost, ROA, and ROE, we need to evaluate (1) the direct

effect on cost and profitability (ROA and ROE) via changes

in the technology due to within- and cross-border merg-

ers and (2) the indirect effect on cost and profitability

(ROA and ROE) of within- and cross-border mergers via

efficiency changes.

First, we report the results in terms of cost. We estimate

the standard Cobb–Douglas cost function8 with three input

and three output variables.9 We also use time trend, equity,

and country dummies in addition to the within- and cross-

border variables. The coefficients of these variables show

whether the technology differs depending on the nature of

the merger (within- or cross-border), the direct effect on

cost. We use w1 to normalize the cost and input price

variables. This normalization imposes the linear homoge-

neity (price) constraint on the estimated cost function.

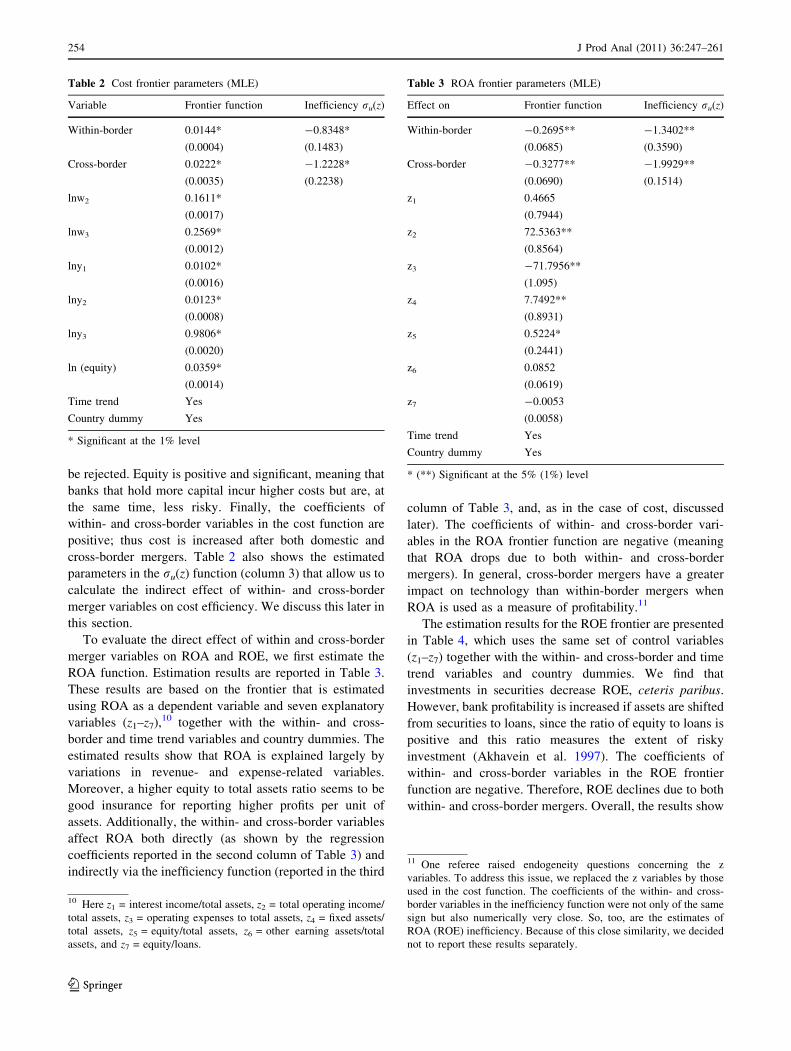

Parameter (ML) estimates are presented in Table 2. The

coefficients of input prices and the output in the cost

function are positive and statistically significant. Since the

sum of the coefficients of log outputs is close to unity, the

hypothesis of unitary returns to scale (RTS = 1/Ram) cannot

Table 1 Descriptive statistics (in millions of euros)

Variables Mean Standard

deviation

Range p25 p50 p75 Kurtosis Skewness

Variables in the cost frontier

Cost 729.076 3,118.728 70,938.100 22.200 71.758 269.223 70,938.1 166.1134

Loans 6,092.186 2,5467.580 419,413.000 115.450 476.087 2,107.950 419,413 93.95594

Other earning assets 6,120.697 29,546.280 609,060.000 108.400 435.600 1,739.900 609,060 174.8697

Deposits 8,451.236 33,650.090 455,034.000 281.050 927.000 3,473.500 455,034 73.73576

Interest expenses 464.044 2,047.713 48,102.900 9.100 32.800 153.000 48,102.9 169.926

Personnel expenses 117.838 583.141 13,525.850 3.800 12.500 43.600 13,525.85 230.7389

Equity 582.209 2,182.503 43,393.700 30.800 91.100 302.050 43,393.7 147.5897

Non-interest expenses 147.194 620.537 10,235.800 4.500 14.600 59.568 10,235.8 112.6573

Variables in the ROA and ROE frontiers

ROA 0.641 2.633 119.283 0.195 0.512 1.016 119.283 225.1182

ROE 8.368 19.709 665.866 2.946 7.590 14.060 665.866 100.613

Interest income/total assets 0.053 0.026 0.752 0.039 0.050 0.062 0.7522764 124.5375

Total operating expenses/total assets 0.035 0.036 0.577 0.015 0.028 0.042 0.5766349 37.79757

Total operating income/total assets 0.043 0.044 1.073 0.021 0.036 0.052 1.072835 70.10265

Total assets/fixed assets 1,233.206 5,870.631 202,174.600 69.069 150.746 529.583 202174.6 384.4133

Equity/total assets 0.100 0.104 0.911 0.045 0.070 0.109 0.9108252 19.24891

Other earning assets/total assets 0.453 0.286 4.162 0.219 0.423 0.697 4.162291 8.304354

Equity/loans 0.788 4.261 159.393 0.090 0.153 0.383 159.3927 561.8574

7 Apparently, there is no theory here that tells us what variables are to

be included in the ROA (ROE) function. We follow the empirical

literature, which notes that these profitability ratios depend on internal

and external factors. Our goal here is not to perform a causal analysis,

but to check associations of ROA/ROE with some variables of

interest. Although the control variables used for such associations are

correlated with ROA (ROE), the dependent variable ROA (ROE)

contains some items (i.e., interest income, interest cost) that are not

included in the right-hand side (RHS) variables. This means that

although some of the RHS variables are used to define the left-hand

side variable, there is no endogeneity problem so long as the RHS

variables are not endogenous. In a cost model, input prices are

obtained by dividing the cost of each input by their respective

quantities, which are endogenous. This does not make prices

endogenous (at least no one thinks that).

8 We estimate the model with a flexible functional form (translog).

However, we fail to reject the CD against the translog at the 5% level

of significance. Furthermore, the results are qualitatively similar and

are therefore not reported here.9 The results are qualitatively similar when we remove deposits from

the list of outputs.

J Prod Anal (2011) 36:247–261 253

123

be rejected. Equity is positive and significant, meaning that

banks that hold more capital incur higher costs but are, at

the same time, less risky. Finally, the coefficients of

within- and cross-border variables in the cost function are

positive; thus cost is increased after both domestic and

cross-border mergers. Table 2 also shows the estimated

parameters in the ru(z) function (column 3) that allow us to

calculate the indirect effect of within- and cross-border

merger variables on cost efficiency. We discuss this later in

this section.

To evaluate the direct effect of within and cross-border

merger variables on ROA and ROE, we first estimate the

ROA function. Estimation results are reported in Table 3.

These results are based on the frontier that is estimated

using ROA as a dependent variable and seven explanatory

variables (z1–z7),10 together with the within- and cross-

border and time trend variables and country dummies. The

estimated results show that ROA is explained largely by

variations in revenue- and expense-related variables.

Moreover, a higher equity to total assets ratio seems to be

good insurance for reporting higher profits per unit of

assets. Additionally, the within- and cross-border variables

affect ROA both directly (as shown by the regression

coefficients reported in the second column of Table 3) and

indirectly via the inefficiency function (reported in the third

column of Table 3, and, as in the case of cost, discussed

later). The coefficients of within- and cross-border vari-

ables in the ROA frontier function are negative (meaning

that ROA drops due to both within- and cross-border

mergers). In general, cross-border mergers have a greater

impact on technology than within-border mergers when

ROA is used as a measure of profitability.11

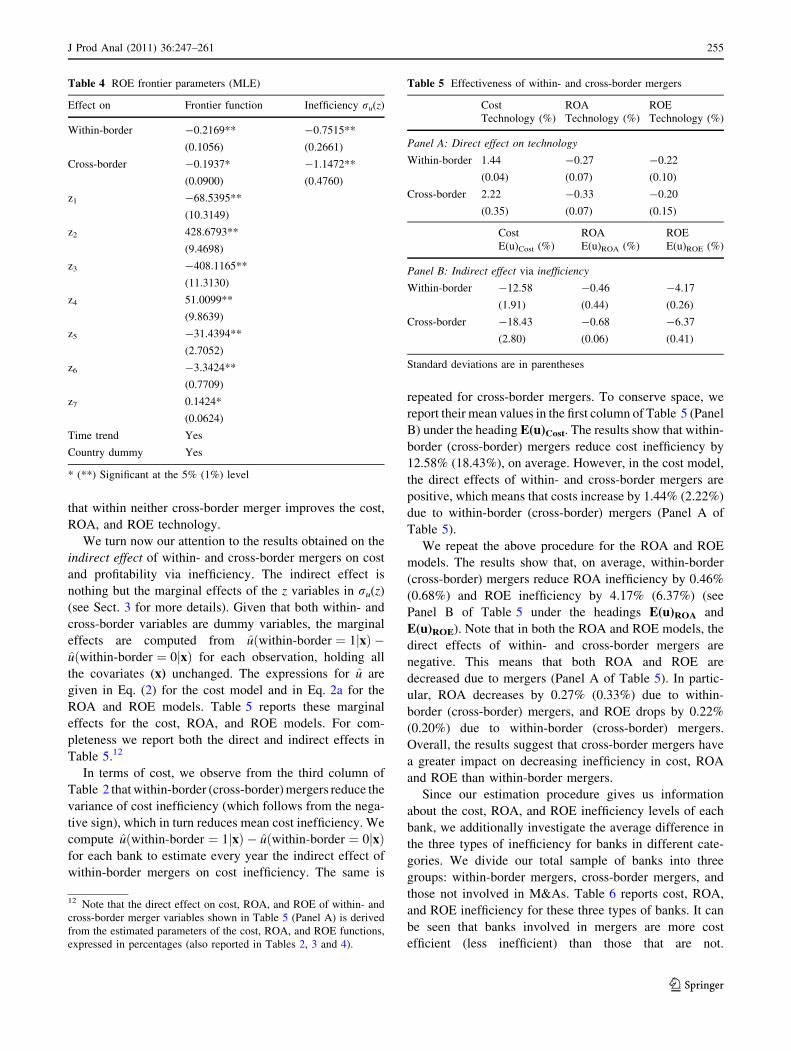

The estimation results for the ROE frontier are presented

in Table 4, which uses the same set of control variables

(z1–z7) together with the within- and cross-border and time

trend variables and country dummies. We find that

investments in securities decrease ROE, ceteris paribus.

However, bank profitability is increased if assets are shifted

from securities to loans, since the ratio of equity to loans is

positive and this ratio measures the extent of risky

investment (Akhavein et al. 1997). The coefficients of

within- and cross-border variables in the ROE frontier

function are negative. Therefore, ROE declines due to both

within- and cross-border mergers. Overall, the results show

Table 2 Cost frontier parameters (MLE)

Variable Frontier function Inefficiency ru(z)

Within-border 0.0144*

(0.0004)

-0.8348*

(0.1483)

Cross-border 0.0222*

(0.0035)

-1.2228*

(0.2238)

lnw2 0.1611*

(0.0017)

lnw3 0.2569*

(0.0012)

lny1 0.0102*

(0.0016)

lny2 0.0123*

(0.0008)

lny3 0.9806*

(0.0020)

ln (equity) 0.0359*

(0.0014)

Time trend Yes

Country dummy Yes

* Significant at the 1% level

Table 3 ROA frontier parameters (MLE)

Effect on Frontier function Inefficiency ru(z)

Within-border -0.2695**

(0.0685)

-1.3402**

(0.3590)

Cross-border -0.3277**

(0.0690)

-1.9929**

(0.1514)

z1 0.4665

(0.7944)

z2 72.5363**

(0.8564)

z3 -71.7956**

(1.095)

z4 7.7492**

(0.8931)

z5 0.5224*

(0.2441)

z6 0.0852

(0.0619)

z7 -0.0053

(0.0058)

Time trend Yes

Country dummy Yes

* (**) Significant at the 5% (1%) level

10 Here z1 = interest income/total assets, z2 = total operating income/

total assets, z3 = operating expenses to total assets, z4 = fixed assets/

total assets, z5 = equity/total assets, z6 = other earning assets/total

assets, and z7 = equity/loans.

11 One referee raised endogeneity questions concerning the z

variables. To address this issue, we replaced the z variables by those

used in the cost function. The coefficients of the within- and cross-

border variables in the inefficiency function were not only of the same

sign but also numerically very close. So, too, are the estimates of

ROA (ROE) inefficiency. Because of this close similarity, we decided

not to report these results separately.

254 J Prod Anal (2011) 36:247–261

123

that within neither cross-border merger improves the cost,

ROA, and ROE technology.

We turn now our attention to the results obtained on the

indirect effect of within- and cross-border mergers on cost

and profitability via inefficiency. The indirect effect is

nothing but the marginal effects of the z variables in ru(z)

(see Sect. 3 for more details). Given that both within- and

cross-border variables are dummy variables, the marginal

effects are computed from uðwithin-border ¼ 1jxÞ �uðwithin-border ¼ 0jxÞ for each observation, holding all

the covariates (x) unchanged. The expressions for u are

given in Eq. (2) for the cost model and in Eq. 2a for the

ROA and ROE models. Table 5 reports these marginal

effects for the cost, ROA, and ROE models. For com-

pleteness we report both the direct and indirect effects in

Table 5.12

In terms of cost, we observe from the third column of

Table 2 that within-border (cross-border) mergers reduce the

variance of cost inefficiency (which follows from the nega-

tive sign), which in turn reduces mean cost inefficiency. We

compute uðwithin-border ¼ 1jxÞ � uðwithin-border ¼ 0jxÞfor each bank to estimate every year the indirect effect of

within-border mergers on cost inefficiency. The same is

repeated for cross-border mergers. To conserve space, we

report their mean values in the first column of Table 5 (Panel

B) under the heading E(u)Cost. The results show that within-

border (cross-border) mergers reduce cost inefficiency by

12.58% (18.43%), on average. However, in the cost model,

the direct effects of within- and cross-border mergers are

positive, which means that costs increase by 1.44% (2.22%)

due to within-border (cross-border) mergers (Panel A of

Table 5).

We repeat the above procedure for the ROA and ROE

models. The results show that, on average, within-border

(cross-border) mergers reduce ROA inefficiency by 0.46%

(0.68%) and ROE inefficiency by 4.17% (6.37%) (see

Panel B of Table 5 under the headings E(u)ROA and

E(u)ROE). Note that in both the ROA and ROE models, the

direct effects of within- and cross-border mergers are

negative. This means that both ROA and ROE are

decreased due to mergers (Panel A of Table 5). In partic-

ular, ROA decreases by 0.27% (0.33%) due to within-

border (cross-border) mergers, and ROE drops by 0.22%

(0.20%) due to within-border (cross-border) mergers.

Overall, the results suggest that cross-border mergers have

a greater impact on decreasing inefficiency in cost, ROA

and ROE than within-border mergers.

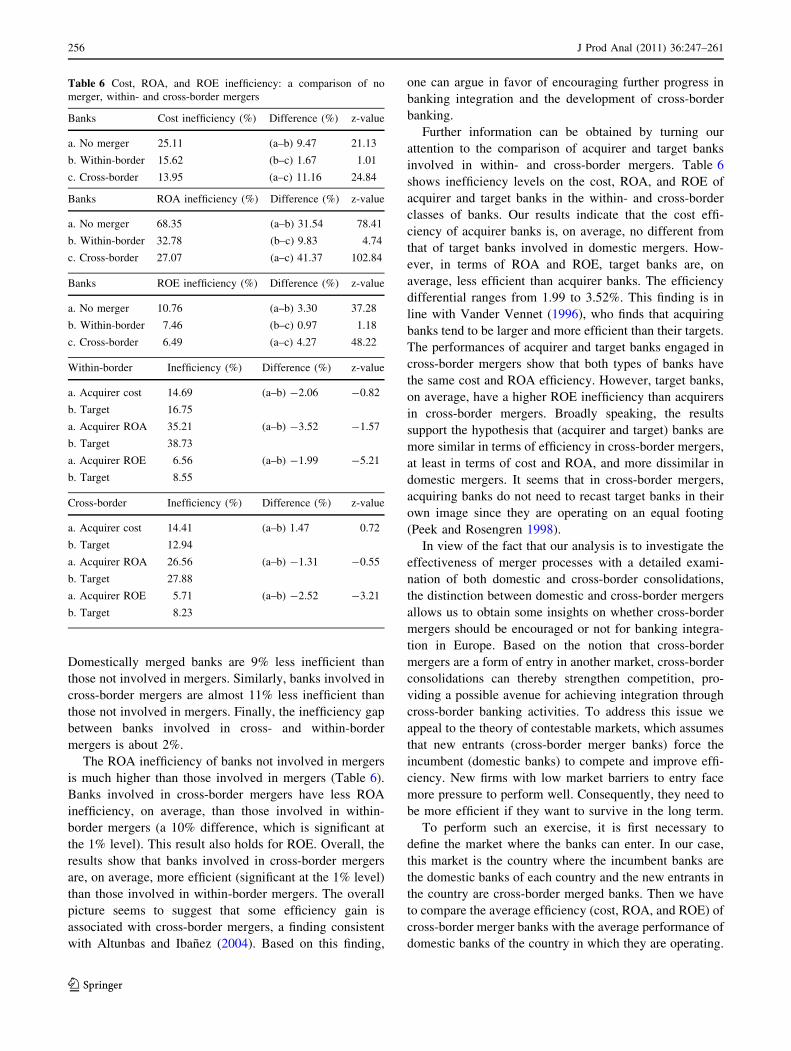

Since our estimation procedure gives us information

about the cost, ROA, and ROE inefficiency levels of each

bank, we additionally investigate the average difference in

the three types of inefficiency for banks in different cate-

gories. We divide our total sample of banks into three

groups: within-border mergers, cross-border mergers, and

those not involved in M&As. Table 6 reports cost, ROA,

and ROE inefficiency for these three types of banks. It can

be seen that banks involved in mergers are more cost

efficient (less inefficient) than those that are not.

Table 5 Effectiveness of within- and cross-border mergers

Cost ROA ROE

Technology (%) Technology (%) Technology (%)

Panel A: Direct effect on technology

Within-border 1.44 -0.27 -0.22

(0.04) (0.07) (0.10)

Cross-border 2.22 -0.33 -0.20

(0.35) (0.07) (0.15)

Cost ROA ROE

E(u)Cost (%) E(u)ROA (%) E(u)ROE (%)

Panel B: Indirect effect via inefficiency

Within-border -12.58 -0.46 -4.17

(1.91) (0.44) (0.26)

Cross-border -18.43 -0.68 -6.37

(2.80) (0.06) (0.41)

Standard deviations are in parentheses

Table 4 ROE frontier parameters (MLE)

Effect on Frontier function Inefficiency ru(z)

Within-border -0.2169**

(0.1056)

-0.7515**

(0.2661)

Cross-border -0.1937*

(0.0900)

-1.1472**

(0.4760)

z1 -68.5395**

(10.3149)

z2 428.6793**

(9.4698)

z3 -408.1165**

(11.3130)

z4 51.0099**

(9.8639)

z5 -31.4394**

(2.7052)

z6 -3.3424**

(0.7709)

z7 0.1424*

(0.0624)

Time trend Yes

Country dummy Yes

* (**) Significant at the 5% (1%) level

12 Note that the direct effect on cost, ROA, and ROE of within- and

cross-border merger variables shown in Table 5 (Panel A) is derived

from the estimated parameters of the cost, ROA, and ROE functions,

expressed in percentages (also reported in Tables 2, 3 and 4).

J Prod Anal (2011) 36:247–261 255

123

Domestically merged banks are 9% less inefficient than

those not involved in mergers. Similarly, banks involved in

cross-border mergers are almost 11% less inefficient than

those not involved in mergers. Finally, the inefficiency gap

between banks involved in cross- and within-border

mergers is about 2%.

The ROA inefficiency of banks not involved in mergers

is much higher than those involved in mergers (Table 6).

Banks involved in cross-border mergers have less ROA

inefficiency, on average, than those involved in within-

border mergers (a 10% difference, which is significant at

the 1% level). This result also holds for ROE. Overall, the

results show that banks involved in cross-border mergers

are, on average, more efficient (significant at the 1% level)

than those involved in within-border mergers. The overall

picture seems to suggest that some efficiency gain is

associated with cross-border mergers, a finding consistent

with Altunbas and Ibanez (2004). Based on this finding,

one can argue in favor of encouraging further progress in

banking integration and the development of cross-border

banking.

Further information can be obtained by turning our

attention to the comparison of acquirer and target banks

involved in within- and cross-border mergers. Table 6

shows inefficiency levels on the cost, ROA, and ROE of

acquirer and target banks in the within- and cross-border

classes of banks. Our results indicate that the cost effi-

ciency of acquirer banks is, on average, no different from

that of target banks involved in domestic mergers. How-

ever, in terms of ROA and ROE, target banks are, on

average, less efficient than acquirer banks. The efficiency

differential ranges from 1.99 to 3.52%. This finding is in

line with Vander Vennet (1996), who finds that acquiring

banks tend to be larger and more efficient than their targets.

The performances of acquirer and target banks engaged in

cross-border mergers show that both types of banks have

the same cost and ROA efficiency. However, target banks,

on average, have a higher ROE inefficiency than acquirers

in cross-border mergers. Broadly speaking, the results

support the hypothesis that (acquirer and target) banks are

more similar in terms of efficiency in cross-border mergers,

at least in terms of cost and ROA, and more dissimilar in

domestic mergers. It seems that in cross-border mergers,

acquiring banks do not need to recast target banks in their

own image since they are operating on an equal footing

(Peek and Rosengren 1998).

In view of the fact that our analysis is to investigate the

effectiveness of merger processes with a detailed exami-

nation of both domestic and cross-border consolidations,

the distinction between domestic and cross-border mergers

allows us to obtain some insights on whether cross-border

mergers should be encouraged or not for banking integra-

tion in Europe. Based on the notion that cross-border

mergers are a form of entry in another market, cross-border

consolidations can thereby strengthen competition, pro-

viding a possible avenue for achieving integration through

cross-border banking activities. To address this issue we

appeal to the theory of contestable markets, which assumes

that new entrants (cross-border merger banks) force the

incumbent (domestic banks) to compete and improve effi-

ciency. New firms with low market barriers to entry face

more pressure to perform well. Consequently, they need to

be more efficient if they want to survive in the long term.

To perform such an exercise, it is first necessary to

define the market where the banks can enter. In our case,

this market is the country where the incumbent banks are

the domestic banks of each country and the new entrants in

the country are cross-border merged banks. Then we have

to compare the average efficiency (cost, ROA, and ROE) of

cross-border merger banks with the average performance of

domestic banks of the country in which they are operating.

Table 6 Cost, ROA, and ROE inefficiency: a comparison of no

merger, within- and cross-border mergers

Banks Cost inefficiency (%) Difference (%) z-value

a. No merger 25.11 (a–b) 9.47 21.13

b. Within-border 15.62 (b–c) 1.67 1.01

c. Cross-border 13.95 (a–c) 11.16 24.84

Banks ROA inefficiency (%) Difference (%) z-value

a. No merger 68.35 (a–b) 31.54 78.41

b. Within-border 32.78 (b–c) 9.83 4.74

c. Cross-border 27.07 (a–c) 41.37 102.84

Banks ROE inefficiency (%) Difference (%) z-value

a. No merger 10.76 (a–b) 3.30 37.28

b. Within-border 7.46 (b–c) 0.97 1.18

c. Cross-border 6.49 (a–c) 4.27 48.22

Within-border Inefficiency (%) Difference (%) z-value

a. Acquirer cost 14.69 (a–b) -2.06 -0.82

b. Target 16.75

a. Acquirer ROA 35.21 (a–b) -3.52 -1.57

b. Target 38.73

a. Acquirer ROE 6.56 (a–b) -1.99 -5.21

b. Target 8.55

Cross-border Inefficiency (%) Difference (%) z-value

a. Acquirer cost 14.41 (a–b) 1.47 0.72

b. Target 12.94

a. Acquirer ROA 26.56 (a–b) -1.31 -0.55

b. Target 27.88

a. Acquirer ROE 5.71 (a–b) -2.52 -3.21

b. Target 8.23

256 J Prod Anal (2011) 36:247–261

123

This comparison should provide some insight about what

the response of an incumbent bank facing a new entrant

(cross-border merged bank) should be. In this first exercise,

we consider domestic banks, that is, incumbent banks not

involved in M&As and banks involved in domestic M&As.

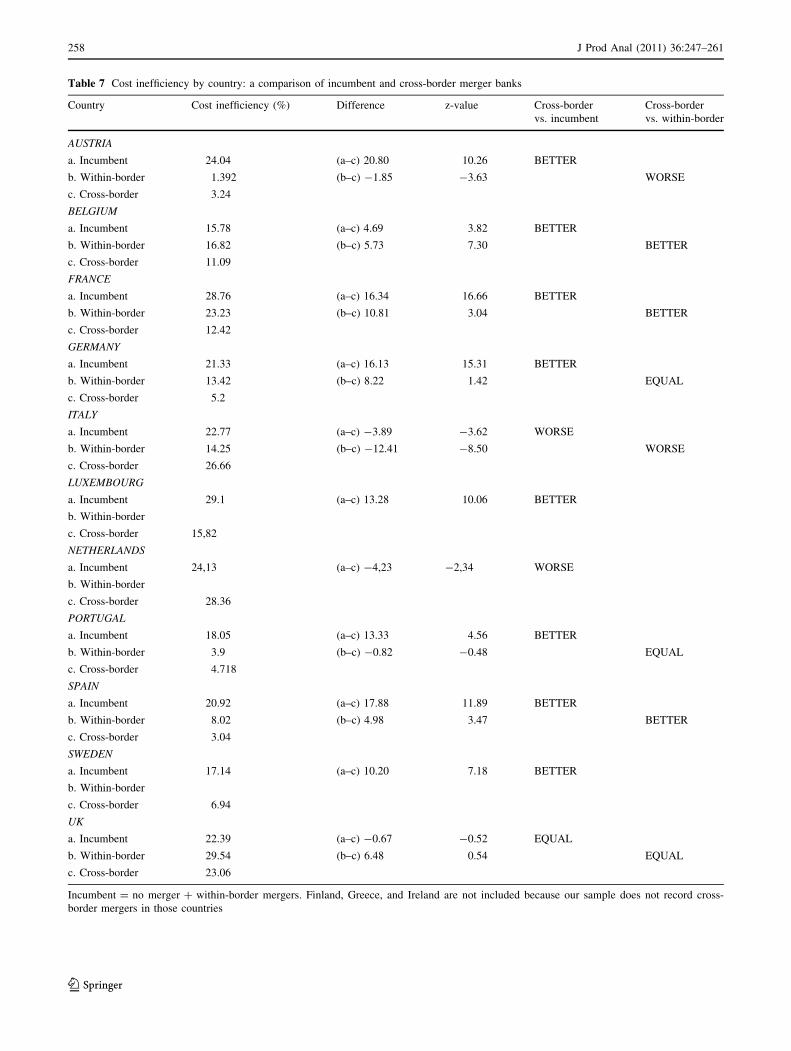

We do this for each country. Table 7 shows that cross-

border merged banks outperform incumbent banks in terms

of average cost efficiency in all countries, except for Italy,

the Netherlands, and the United Kingdom.

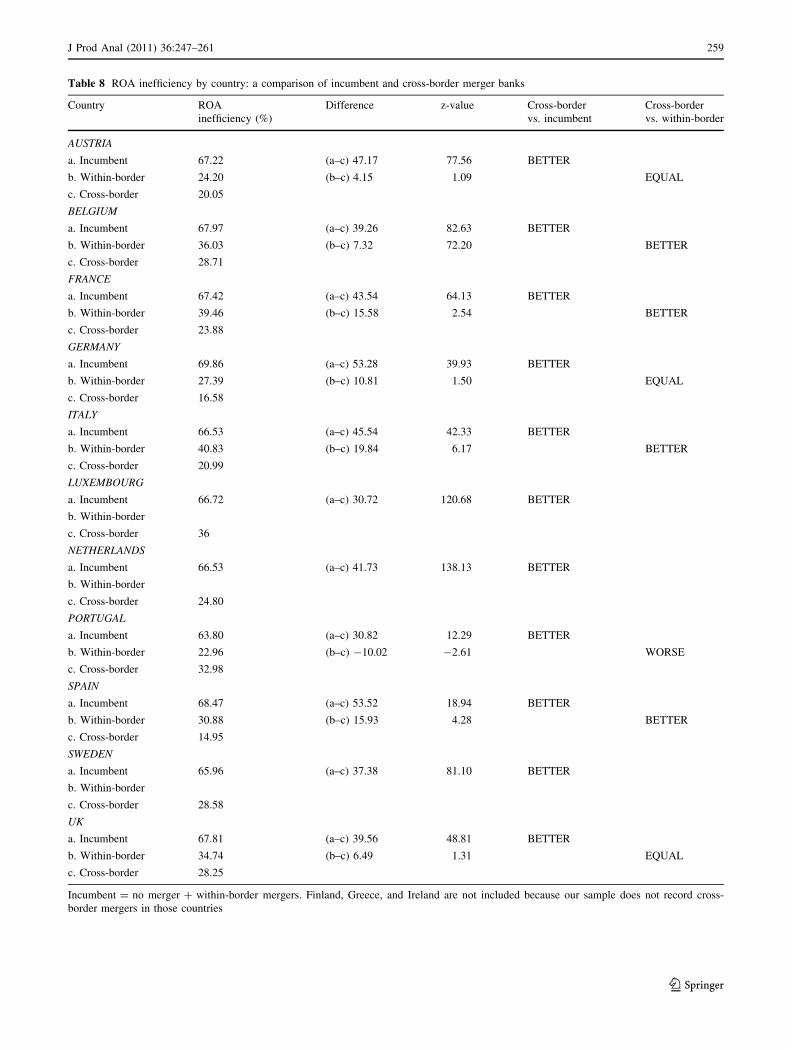

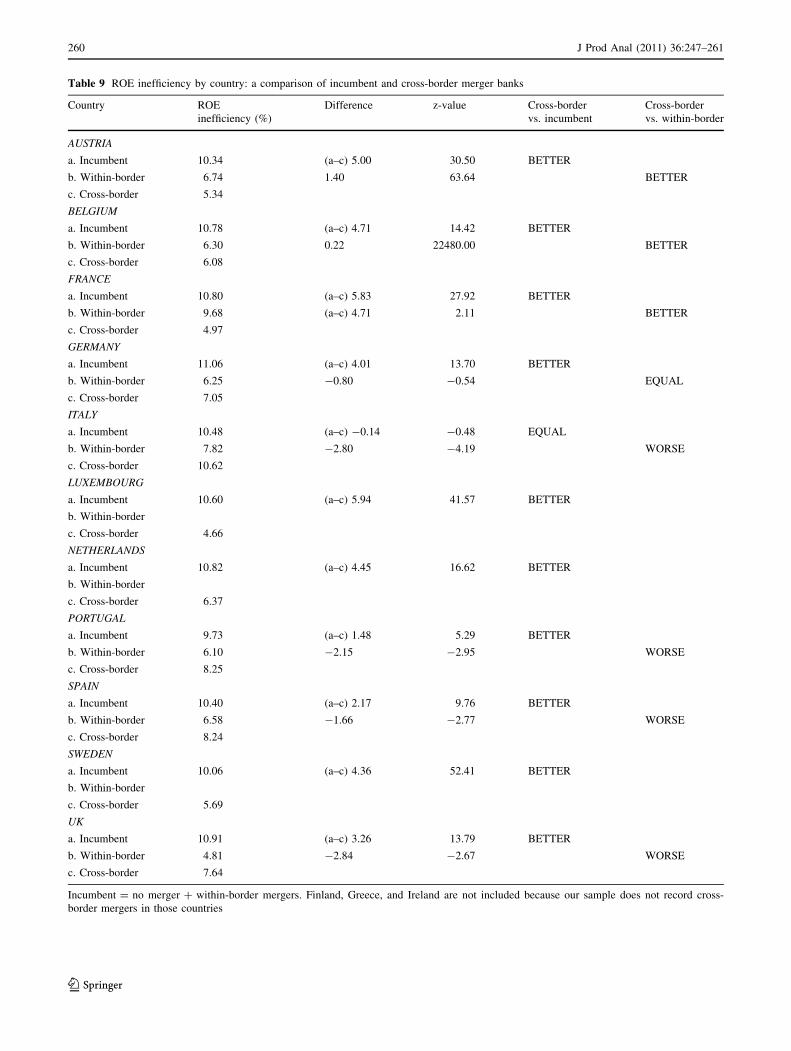

The results for ROA and ROE inefficiency, reported in

Tables 8 and 9, show that, except for Italy (which performs

equally regarding ROE inefficiency), cross-border merged

banks outperform incumbent banks.

If we consider only the within-border banks as incum-

bent banks, based on the idea that those banks are the

largest banks in the country and close competitors to the

cross-border entrant banks, then we find (1) countries

where cross-border mergers show greater effectiveness

than within-border mergers, (2) countries where cross-

border mergers outperform in cost and/or profitability

efficiency, and (3) countries where cross-border mergers

are less effective than within-border mergers. Only in the

case of Belgium and France do cross-border merged banks

outperform their within-border counterparts in all three

performance measures. In Spain, cross-border merged

banks outperform in terms of cost and ROA but not in

terms of ROE. This is because Spanish banks are charac-

terized by strong solvency and high profit per unit of equity

investment. On the other hand, in Germany, banks are on

an equal footing, and in the case of Italy and the United

Kingdom cross-border merged banks underperform in

terms of cost and ROE, and perform equally in terms of

ROA. These findings suggest that this last group of coun-

tries needs to make a greater effort to boost competition. In

general, our findings on the significance of cross-border

mergers in enhancing efficiency gains provide insights into

the development of cross-border banking in Europe.

6 Summary and conclusions

This paper examines the effectiveness of mergers, with a

detailed analysis of both domestic and cross-border con-

solidations in Europe during 1998–2004. Effectiveness is

measured via several criteria: improvement in costs, ROA,

and ROE. We use stochastic frontier models that allow us

to evaluate the effect of within- and cross-border mergers

on technology (direct effect) and on efficiency (indirect

effect). Using a sample of commercial banks from 14

European countries, we estimate cost, ROA, and ROE

frontiers where within- and cross-border variables are used

as explanatory variables, as well as determinants of

inefficiency.

Overall, we find that, on average, although there are no

improvements in cost, ROA, or ROE (direct effect) due to

within- and cross-border mergers, both types of mergers

reduce cost inefficiency. Furthermore, our findings in terms

of ROA and ROE confirm that within- and cross-border

mergers decrease inefficiency. These results suggest that

merger processes in the European banking industry have

been effective, since both the cost efficiency and profit-

ability efficiency of merged banks have improved. Judging

from these findings, one can argue that the European bank

consolidation process has been successful during the period

of our study.

Additionally, our findings on the comparison of banks

involved in domestic and cross-border mergers as well as

those not involved in such activities reveal that banks

involved in mergers are more cost efficient than those not

involved in mergers. The ROA and ROE inefficiencies of

banks also confirm this finding. On average, the ROA and

ROE efficiencies for banks involved in cross-border

mergers are greater than for banks involved in in-border

mergers. These results show that although domestic M&As

are more common than cross-border M&As, banks

involved in cross-border M&As are more efficient.

We also examine the differences between acquirers and

target banks involved in merger processes (domestic and/or

cross-border) and find that there are similarities between

acquirer and target banks in cross-border mergers. How-

ever, we find dissimilarities between acquirer and target

banks involved in domestic mergers. Acquirer and target

banks involved in cross-border mergers have similar per-

formances in terms of efficiency, suggesting that they

operate on an equal footing and there is no need for the

target bank to undergo any changes after the merger. It can

be concluded that efficiency is more important for cross-

border mergers.

Finally, we investigate the entry effect, the average

performance of incumbent market participants, in each

country market where cross-border merged banks operate.

In terms of cost efficiency, cross-border merged banks

outperform incumbent banks in all countries, except Italy,

the Netherlands, and the United Kingdom. With the

exception of Italy, which shows equal performance in terms

of ROE efficiencies, we find results supporting the idea that

cross-border merged banks outperform incumbent banks.

We find that the cross-border banks have a higher

chance of survival in the long term in the new environment

than the other banks in the sample due to their better per-

formance. Extending this finding further, we can say that

these banks are in a good position for competing outside.

Given the effectiveness of cross-border mergers found in

our results, banking integration and the development of

cross-border banking mergers should be encouraged in

European countries.

J Prod Anal (2011) 36:247–261 257

123

Table 7 Cost inefficiency by country: a comparison of incumbent and cross-border merger banks

Country Cost inefficiency (%) Difference z-value Cross-border

vs. incumbent

Cross-border

vs. within-border

AUSTRIA

a. Incumbent 24.04 (a–c) 20.80 10.26 BETTER

b. Within-border 1.392 (b–c) -1.85 -3.63 WORSE

c. Cross-border 3.24

BELGIUM

a. Incumbent 15.78 (a–c) 4.69 3.82 BETTER

b. Within-border 16.82 (b–c) 5.73 7.30 BETTER

c. Cross-border 11.09

FRANCE

a. Incumbent 28.76 (a–c) 16.34 16.66 BETTER

b. Within-border 23.23 (b–c) 10.81 3.04 BETTER

c. Cross-border 12.42

GERMANY

a. Incumbent 21.33 (a–c) 16.13 15.31 BETTER

b. Within-border 13.42 (b–c) 8.22 1.42 EQUAL

c. Cross-border 5.2

ITALY

a. Incumbent 22.77 (a–c) -3.89 -3.62 WORSE

b. Within-border 14.25 (b–c) -12.41 -8.50 WORSE

c. Cross-border 26.66

LUXEMBOURG

a. Incumbent 29.1 (a–c) 13.28 10.06 BETTER

b. Within-border

c. Cross-border 15,82

NETHERLANDS

a. Incumbent 24,13 (a–c) -4,23 -2,34 WORSE

b. Within-border

c. Cross-border 28.36

PORTUGAL

a. Incumbent 18.05 (a–c) 13.33 4.56 BETTER

b. Within-border 3.9 (b–c) -0.82 -0.48 EQUAL

c. Cross-border 4.718

SPAIN

a. Incumbent 20.92 (a–c) 17.88 11.89 BETTER

b. Within-border 8.02 (b–c) 4.98 3.47 BETTER

c. Cross-border 3.04

SWEDEN

a. Incumbent 17.14 (a–c) 10.20 7.18 BETTER

b. Within-border

c. Cross-border 6.94

UK

a. Incumbent 22.39 (a–c) -0.67 -0.52 EQUAL

b. Within-border 29.54 (b–c) 6.48 0.54 EQUAL

c. Cross-border 23.06

Incumbent = no merger ? within-border mergers. Finland, Greece, and Ireland are not included because our sample does not record cross-

border mergers in those countries

258 J Prod Anal (2011) 36:247–261

123

Table 8 ROA inefficiency by country: a comparison of incumbent and cross-border merger banks

Country ROA

inefficiency (%)

Difference z-value Cross-border

vs. incumbent

Cross-border

vs. within-border

AUSTRIA

a. Incumbent 67.22 (a–c) 47.17 77.56 BETTER

b. Within-border 24.20 (b–c) 4.15 1.09 EQUAL

c. Cross-border 20.05

BELGIUM

a. Incumbent 67.97 (a–c) 39.26 82.63 BETTER

b. Within-border 36.03 (b–c) 7.32 72.20 BETTER

c. Cross-border 28.71

FRANCE

a. Incumbent 67.42 (a–c) 43.54 64.13 BETTER

b. Within-border 39.46 (b–c) 15.58 2.54 BETTER

c. Cross-border 23.88

GERMANY

a. Incumbent 69.86 (a–c) 53.28 39.93 BETTER

b. Within-border 27.39 (b–c) 10.81 1.50 EQUAL

c. Cross-border 16.58

ITALY

a. Incumbent 66.53 (a–c) 45.54 42.33 BETTER

b. Within-border 40.83 (b–c) 19.84 6.17 BETTER

c. Cross-border 20.99

LUXEMBOURG

a. Incumbent 66.72 (a–c) 30.72 120.68 BETTER

b. Within-border

c. Cross-border 36

NETHERLANDS

a. Incumbent 66.53 (a–c) 41.73 138.13 BETTER

b. Within-border

c. Cross-border 24.80

PORTUGAL

a. Incumbent 63.80 (a–c) 30.82 12.29 BETTER

b. Within-border 22.96 (b–c) -10.02 -2.61 WORSE

c. Cross-border 32.98

SPAIN

a. Incumbent 68.47 (a–c) 53.52 18.94 BETTER

b. Within-border 30.88 (b–c) 15.93 4.28 BETTER

c. Cross-border 14.95

SWEDEN

a. Incumbent 65.96 (a–c) 37.38 81.10 BETTER

b. Within-border

c. Cross-border 28.58

UK

a. Incumbent 67.81 (a–c) 39.56 48.81 BETTER

b. Within-border 34.74 (b–c) 6.49 1.31 EQUAL

c. Cross-border 28.25

Incumbent = no merger ? within-border mergers. Finland, Greece, and Ireland are not included because our sample does not record cross-

border mergers in those countries

J Prod Anal (2011) 36:247–261 259

123

Table 9 ROE inefficiency by country: a comparison of incumbent and cross-border merger banks

Country ROE

inefficiency (%)

Difference z-value Cross-border

vs. incumbent

Cross-border

vs. within-border

AUSTRIA

a. Incumbent 10.34 (a–c) 5.00 30.50 BETTER

b. Within-border 6.74 1.40 63.64 BETTER

c. Cross-border 5.34

BELGIUM

a. Incumbent 10.78 (a–c) 4.71 14.42 BETTER

b. Within-border 6.30 0.22 22480.00 BETTER

c. Cross-border 6.08

FRANCE

a. Incumbent 10.80 (a–c) 5.83 27.92 BETTER

b. Within-border 9.68 (a–c) 4.71 2.11 BETTER

c. Cross-border 4.97

GERMANY

a. Incumbent 11.06 (a–c) 4.01 13.70 BETTER

b. Within-border 6.25 -0.80 -0.54 EQUAL

c. Cross-border 7.05

ITALY

a. Incumbent 10.48 (a–c) -0.14 -0.48 EQUAL

b. Within-border 7.82 -2.80 -4.19 WORSE

c. Cross-border 10.62

LUXEMBOURG

a. Incumbent 10.60 (a–c) 5.94 41.57 BETTER

b. Within-border

c. Cross-border 4.66

NETHERLANDS

a. Incumbent 10.82 (a–c) 4.45 16.62 BETTER

b. Within-border

c. Cross-border 6.37

PORTUGAL

a. Incumbent 9.73 (a–c) 1.48 5.29 BETTER

b. Within-border 6.10 -2.15 -2.95 WORSE

c. Cross-border 8.25

SPAIN

a. Incumbent 10.40 (a–c) 2.17 9.76 BETTER

b. Within-border 6.58 -1.66 -2.77 WORSE

c. Cross-border 8.24

SWEDEN

a. Incumbent 10.06 (a–c) 4.36 52.41 BETTER

b. Within-border

c. Cross-border 5.69

UK

a. Incumbent 10.91 (a–c) 3.26 13.79 BETTER

b. Within-border 4.81 -2.84 -2.67 WORSE

c. Cross-border 7.64

Incumbent = no merger ? within-border mergers. Finland, Greece, and Ireland are not included because our sample does not record cross-

border mergers in those countries

260 J Prod Anal (2011) 36:247–261

123

Acknowledgments Ana Lozano-Vivas and Subal C. Kumbhakar

acknowledge the financial support from the Ministerio de Educacion

y Ciencias and FEDER grant with reference ECO2008-04424. The

authors thank the participants of the ‘‘Tor Vergata’’ conference on

Banking and Finance (Rome, Italy), Tenth European Workshop on

Efficiency and Productivity Analysis (Lille, France) and North

American Productivity Workshop, New York University, the Editor,

Robin Sickles and three anonymous referees for many suggestions.

References

Abraham J-P, Van Dijcke P (2002) European financial cross-border

consolidation: at the cross-roads in Europe? By exception,

evolution or revolution? SUERF Studies No. 22

Akhavein JD, Berger AN, Humphrey DB (1997) The effects of bank

megamergers on efficiency and prices: evidence from the profit

function. Rev Ind Organ 12:95–139

Altunbas Y, Ibanez DM (2004) Mergers and acquisitions and bank

performance in Europe: the role of strategic similarities. ECB

Working Paper Series No. 398

Altunbas Y, Gardener EPM, Molyneux P, Moore B (2001) Efficiency

in European banking. Eur Econ Rev 45(10):1931–1955

Amel D, Barnes C, Panetta F, Salleo C (2004) Consolidation and

efficiency in the financial sector: a review of the international

evidence. J Bank Finance 28:2493–2519

Athanasoglou PP, Brissimis SN, Delis MD (2008) Bank-specific,

industry-specific and macroeconomic determinants of bank

profits. J Int Finance Mark Inst Money 18:121–136

Beitel P, Schiereck D (2001) Value creation at the ongoing

consolidation of the European banking market. Institute for

Mergers and Acquisitions, Working Paper 05/01

Beitel P, Schiereck D, Wahrenburg M (2004) Explaining M&A

success in European banks. Eur Finan Manag 10:109–140

Berger AN, Humphrey DB (1992) Megamergers in banking and the

use of cost efficiency as an antitrust defense. Antitrust Bull 37:

541–600

Berger AN, Mester L (1997) Inside the black box: what explain

differences in the efficiency in financial institutions. J Bank

Finance 21:895–947

Berger AN, Demsetz RS, Strahan PE (1999) The consolidation of the

financial services industry: causes, consequences, and implica-

tions for the future. J Bank Finance 23:135–194

Berger AN, DeYoung R, Genay H, Udell GF (2000) Globalization of

financial institutions: evidence from cross-border banking per-

formance. Brookings–Wharton Papers on Financial Services 3:

23–158

Berger AN, DeYoung R, Udell GF (2001) Efficiency barriers to the

consolidation of the European financial services industry. Eur

Financ Manag 7:117–130

Bourke P (1989) Concentration and other determinants of bank

profitability in Europe. North America and Australia. J Bank

Finance 13:65–79

Campa JM, Hernando I (2004) Shareholder value creation in

European M&As. Eur Financ Manag 10:47–81

Campa JM, Hernando I (2006) M&As performance in the European

financial industry. J Bank Finance 30:3367–3392

Cornett MM, Tehranian H (1992) Changes in corporate performance

associated with bank acquisitions. J Financ Econ 31:211–234

Cuesta RA, Orea L (2002) Mergers and technical efficiency in

Spanish savings banks: a stochastic distance function approach.

J Bank Finance 26:2231–2247

Cybo-Ottone A, Murgia M (2000) Mergers and shareholder wealth in

European banking. J Bank Finance 24:831–859

Demirguc-Kunt A, Huizinga H (1998) Determinants of commercial

bank interest margins and profitability. Policy Research Working

Paper, World Bank, WPS 1900

Dıaz B, Garcıa M, Sanfilippo S (2004) Bank acquisitions and

performance: evidence from a panel of European credit entities.

J Econ Bus 56:377–404

Goddard JA, Molyneux P, Wilson JOS (2004) The profitability of

European banks: a cross-sectional and dynamic panel analysis.

Manch School 72:363–381

Houston JF, Ryngaert MD (1994) The overall gains from large bank

mergers. J Bank Finance 18:1155–1176

Houston JF, James CM, Ryngaert MD (2001) Where do merger gains

come from? Bank mergers from the perspective of insiders and

outsiders. J Financ Econ 60:285–331

Jondrow J, Lovell CAK, Materow IS, Schmidt P (1982) On the

estimation of technical inefficiency in the stochastic frontier

production function model. J Econom 14(2/3):233–238

Kane E (2000) Incentives for banking megamergers: what motives

might regulators infer from event-study evidence? J Money

Credit Banking 32:671–701

Knapp M, Gart A, Becher D (2005) Post-merger performance of bank

holding companies, 1987–1998. Financ Rev 40:549–574

Lang G, Welzel P (1999) Mergers among German cooperative banks:

a panel-based stochastic frontier analysis. Small Bus Econ

13:273–286

Lozano-Vivas A, Weill L (2009) How does cross-border activity

affect the EU banking market? European Financial Management.

doi:10.111/J.1468-036X2009.00534.X

Molyneux P, Thornton J (1992) Determinants of European bank

profitability: a note. J Bank Finance 16:1173–1178

Peek J, Rosengren E (1998) Bank consolidation and small business

lending: it’s not just bank size that matters. J Bank Finance

22(6–8):799–819

Pilloff SJ (1996) Performance changes and shareholder wealth

creation associated with mergers of publicly traded banking

institutions. J Money Credit Banking 28:294–310

Pilloff SJ, Santomero AM (1998) The value effects of bank mergers

and acquisitions. In: Amihud Y, Miller G (eds) Bank mergers

and acquisitions. Kluwer Academic, Boston, pp 59–78

Resti A (1998) Regulation can foster mergers: can mergers foster

efficiency? The Italian case. J Econ Bus 50:157–169

Short BK (1979) The relation between commercial bank profit rates

and banking concentration in Canada, Western Europe and

Japan. J Bank Finance 3:209–219

Vander Vennet R (1996) The effect of mergers and acquisitions on

the efficiency and profitability of EC credit institutions. J Bank

Finance 20:1531–1558

Vander Vennet R (2002) Cross-border mergers in European banking

and bank efficiency. Universiteit Gent, Working Paper, No.

2002/152

Wang H-J (2002) Heteroscedasticity and non-monotonic efficiency

effects of a stochastic frontier model. J Prod Anal 18:241–253

Weill L (2003) Banking efficiency in transition economies, the

economics of transition. Eur Bank Reconstr Dev 11(3):569–592

J Prod Anal (2011) 36:247–261 261

123