Embed Size (px)

Citation preview

Case Paper

Closing down Organon, what

happened with corporate

governance?

by

P.O. Box 800, 9700 AV Groningen,The Netherlands

October, 2010

Case paper Organon

Date of submitting: October, 2010University of Groningen,

Faculty of Economics and Business.

0

R. Bok

Mail:

Phone: +31 6 46 19 12 11

J.A.W. RAAIJMAKERS

Mail:

Phone: +31 6 48 38 00 83

Master Business Administration,

Specialization Change Management.

Course Corporate Governance, 2010/ 2011

Case Paper

Closing down Organon, what

happened with corporate

governance?

1

ABSTRACT

This paper is a case study about closing down Organon by the Mother

company MSD. Several aspects are discussed and analyzed like history

of Organon, differences in Corporate Governance between the US and The

Netherlands and what makes it, case specific, so difficult for the

board of MSD to close down Organon.

Key words: Case analysis, Corporate Governance, Organon, MSD.

2

Table of ContentsIntroduction 3

1. History of Organon 4

1.1 History from 1887 till 2009......................................4

1.2 Recent history (2010)............................................5

1.2.1 Reorganization at MSD/ Organon...............................5

1.2.2 Resistance...................................................6

1.2.3 Decision chamber of commerce.................................7

2. What are the differences between corporate governance in the US and

The Netherlands 8

2.1 Rijnland approach................................................8

2.2 Anglo-Saxon approach.............................................9

2.3 The main differences between the approaches.....................10

3. Corporate Governance stakeholders 11

3.1 Shareholders....................................................11

3.2 Board of MSD....................................................12

3.3 Organon.........................................................12

3.3.1 Supervisory board of Organon................................12

3.3.2 Union.......................................................12

3.3.3 Works council...............................................13

3.3.4 The Politics................................................13

4. Corporate Governance dilemmas 13

4.1 Board of directors and shareholders.............................13

4.2 The Dutch works council.........................................14

4.3 The supervisory board...........................................14

4.4 Dilemmas for MSD 4.4.1 Dilemmas until 2nd of September 2010......15

5. Discussion and Conclusion15

5.1 Cases that have some relation to Organon........................15

5.2 Dilemmas after 31st of December 2010............................17

5.3 Conclusion and advice...........................................18

3

Bibliography 19

Appendix 1: Differences Netherlands vs United States 22

Appendix 2: Differences in responsibilities 24

4

IntroductionWithin the recent economy corporate governance is getting more and

more important. Factors that lighted up the discussion on corporate

governance are the large scandals from diverse organizations as, for

example Ahold, Stork and ABN Amro. Through these circumstances the

attention for corporate governance increased, not only by the board

members but also in the news and in the economy.

Through the globalization more and more companies are taken over by

foreign holdings. This is also the case in the Netherlands where for

example, KLM that was taken over by air France and many American

companies bought Dutch companies. Organizations that take over

companies in foreign countries have to deal with differences between

corporate governance codes or legislation between the countries.

In this paper the troubles dealing with the differences in corporate

governance between countries is discussed using the MSD/Organon

case. In this particular case an American holding MSD bought Organon

in the Netherlands. The mother holding MSD decided to close down

parts of Organon, but because of the differences in Corporate

Governance between the countries they faced some roadblocks.

5

1. History of Organon

1.1 History from 1887 till 2009Organon is a pharmaceutical company with Dutch roots and best known

from their development of the contraceptive pill. Their main

location is situated in Oss, and four branches located in the

Netherlands and one in Belgium. These days Organon is part of Merck

Sharp & Dohme (MSD). To get a clear view of the company it is

necessary to go far back in the history of the company back to 1887.

At that time Saal van Zwanenberg started an export abattoir. This

abattoir developed diverse sideline activities as a machination,

salting company for bacon and intestines, blood drying company for

black pudding and many more. Later these companies where expanded

with company for producing margarine, a refinery for animal oil and

fat and companies for the production of ice cream and soap etc.

In 1929 Unilever took over the companies that produced margarine,

ice cream, fat and soap and in 1970 they also sold the meat

companies to Unilever. Mr. Zwanenberg wanted to use garbage of the

meat from the abattoir. At that time they already suspected that

animal organs contained useful fabrics for the production of

medicines, but they did not know how to extract and isolate these.

After a finding, in 1921, in Canada where they isolated insulin Mr.

Zwanenberg decided in 1923 to start Organon as Subsidiary company of

Zwanenberg. They managed to find a way to extract insulin on

industrial scale from the pancreas of killed pigs, which was a

unique finding. Later they found that extraction from the pancreas

of a calf gave more insulin.

Under the supervision of Zwanenberg the company kept growing to an

international company which was already represented by sales

organizations in over 40 countries in the year 1934. A third part of

6

the company was started named, Diosynth. Diosynth produced raw

materials for third party companies.

During the Second World War Nazi’s took over the company and they

had to produce for Nazi Germany. After the war, in 1953 the company

received the title Royal. The period after the war brought many take

over’s and the company kept growing. Some of the companies they

bought where Chefaro, a company that produced products for

drugstores and Intervet, a producer of animal medicines. After this

many more companies came e.g. in 1961 Boldoot, and in 1965 Kortman &

Schulte and Noury & Van der Lande

Around 1967 Organon was, with a market of more than 100 countries

the biggest pharmaceutical company in The Netherlands. Units where

situated in Oss, Schaijk, Apeldoorn and Boxtel and they had around

5000 employees under contract of which the most where employed in

Oss. In 1969 AKZO bought Royals Salt Organon (their name at that

moment), and sold activities concerned with meat, to Unilever. A

jump trough time ends in 2002 where AKZO decided to move part of the

Organon headquarters from Oss to Roseland in New Jersey (US),

because the centre of the worlds pharmaceutical companies was

situated there. In 2007 CEO Hans Wijers of AkzoNobel made it public

that they would spin off the Organon BioScience part and bring it to

the stock exchange, in the end this did not happen because Schering-

Plough decided to buy the company, of which the transfer happened in

November 2007. At that moment the company had about 14000 employees’

worldwide.

After a merger in 2009 Scherin-Plough and Merck & Co continued as

Merck Sharp & Dohme (MSD).

7

Organon produces almost forty kinds of medicines. The medicine Deca-

durabolin, produced by Organon, is known in the top sport climate

as the dope Nandrolon. Organon is specialized in some areas:

Gynaecology: the contraceptive pill and other methods;

Psychiatry: including anti-depressants;

Immunology: in particular rheumatism and thrombosis.

1.2 Recent history (2010)This part will show the events that happened from July till about

half October in a chronological order. The history is built on news

facts from different newspapers to verify the information and get an

open-minded view without heroic fancy stories.

1.2.1 Reorganization at MSD/ Organon

Recently, news fact after news fact was published about Organon.

Starting around the 8th of July 2010. At that moment media brought

the news about emotions of employees from Organon in Oss. Knowledge

innovation would stop for the Netherlands with the disappearing of

Organon in Oss, because the new owner MSD had send out a message

that the full research and development department, with 1.100 highly

educated employees, would be transferred to the US. Also the still

existing departments in Schaijk and Boxmeer had to close, and only

the production of medicines should be left in the Netherlands. Where

there was a promise in 2007 from Schering-Plough that the research

departments would stay, but after the merger with MSD there was

clearly not much left of those promises.

Later MSD made clear that they want to reduce the total amount of

employees with 15% to gain synergy benefits of 3.5 milliard dollars

8

in 2012, Organon Oss needs to close together with 7 other research-

and development- units over the world. This meant that instead of

the 1.100, 2.175 would be laid off.

Hans Kortlever, senior president and regional director of Middle

Europe of MSD, stated that: “the decision to close the R&D

department in Oss was very complicated. But this decision is logical

when taken into account the globalization, competition and the

modern dejection in the Pharmaceutical industry”. Besides that the

corporate climate and the admission policy for medicines isn’t

competitive enough in comparison with other countries. In news facts

people, as Dutrée from Nefarma, wonder why the Dutch government

doesn’t interfere in such a situation, because closing down the R&D

department of Organon is not beneficial for the knowledge and

innovation economy of the Netherlands.

Paul Brons (President-commissioner) says1 that in his opinion there

are no good reasons for firing 2175 employees. A few reasons MSD

gives for the reorganization and Mr. Brons comments on it. First,

MSD wanted to place out more research, but than what was the reason

of buying. Next, MSD has many research locations since the takeover

of Schering-Plough, they know that before so again, why are they

buying. Thirdly after the take-over 450 top managers were fired and

not replaced, this is the same as giving a company a handicap. You

create difficulties to come with a clear story and vision for the

outside world when you take away the management. The message from

MSD to their shareholders doesn’t state large job losses or closing

of research departments, “it almost seems deception”. Research shows

that the loss of profits from expiring patents can be compensated

with four new “blockbusters”. Two of them are products of Organon,

this feeds thoughts that MSD just bought Organon for their patents.

1 Brabantsdagblad 27th July 20109

1.2.2 Resistance

At the 1st of August 2010 the supervisory board and the works council

of Organon pronounced that they were against the decision to lay off

2.175 employees, because it isn’t in the best interest of Organon.

Mr. Brons explained (according to the media) in a letter to the

board that their decision about the reorganization cannot be

executed. He explains that the actions of MSD are against the

interest of the company, employees and common interest of The

Netherlands.

The way corporate governance is setup in The Netherlands is

different from that in the US. In the case of MSD/ Organon, Mr.

Wakkie advisor of the supervisory board of Organon, beliefs2 that the

Board of MSD made the decision for the reorganization, and told the

Dutch management simply to do so without thinking about the

differences in corporate governance rules between the US and The

Netherlands. Because of the difference in rules, the supervisory

board had in the weekend of the 31st of July the possibility to

inform the board of the company that they do not give the necessary

permission for the reorganization. Reason for this is that they do

not agree with the argumentation of MSD in which they try to justify

the mass dismissal.

Trying to fire the supervisory board for this decision would lead to

a no go situation. Such a decision has to be announced, according to

the law, thirty days in advance and further the works council has to

be asked for an advice in this situation as well. In this case it is

not very likely that the works council will respond with a positive

reaction on firing the supervisory board.

The possible options left in the current situation would be that MSD

agrees with the ideas of the supervisory board, or they come up with2 Brabantsdagblad 3th August 2010

10

a new plan that they discuss in advance with the works council and

supervisory board. The decision of the supervisory board is there,

the works council will go to the chamber of commerce to try to

destroy MSDs’ decision.

The time till the decision is filled with finding options for the

future, think of a possible management buyout, a restart or a

takeover by another company, all options are looked at. Besides this

there also is a lot of political discussion about the case, minister

of economical businesses is working on the case and visited Organon

to talk with the employees. This all is a pain for MSD, they want to

finish their reorganization before the end of 2012 because at that

moment the current social pact ends.

1.2.3 Decision chamber of commerce

At the second of September 2010 the chamber of commerce would start

the discussion about the MSD/ Organon case, but MSD decided just

before to postpone the closing of Organon till the 31st of December.

The time in-between should give the company enough time to try and

find any possible alternatives, if no alternatives are found they

will stick with the original plans and most logically close the

company in Oss. Postponing does not mean cancelation, but it makes

clear a works council indeed has influence, as also mentioned by Mr.

R. Goodijk3. “Since a couple of years, shareholders have rights. But

in case of conflicts, time after time the chamber of commerce looks

at the company as a whole instead of the shareholder.” As

previously mentioned by mr. Wakie, the American mother MSD, most

likely has underestimated the rights of the employees.

In the meantime news items leak about possible takeovers. A possible

option can be a Japanese company, also there would already be two

Dutch companies that are interested in Organon.3 Brabantsdagblad 3th September 2010

11

2. What are the differences between corporate

governance in the US and The NetherlandsIn the United States the organizations align their corporate

governance system to the Anglo-Saxon approach, while organizations

in the Netherlands follow the Rijnland approach. In this section of

the paper the most important differences, for this paper, between

both the approaches will be discussed and explained. Besides these,

there are more differences mentioned in appendixes one and two.

2.1 Rijnland approachSince 1971, the board structure of Dutch companies has been

regulated by Book 2 of the Civil Code (the so-called “Structure

Act”). This code makes a distinction between private and public

companies, and offers different regimes for various types of

organizations. The key issue of the Civil Code is the structure

regime. This regime applies for companies that meet certain criteria

(Goodijk, 2007):

- at least 100 employees;

- 16 million Euro of capital.

When organizations fulfill the criteria for the structure regime,

they are mandatory to have a structure with a two-tier board. This

two-tier board consists of the board of directors (executive

management) and a supervisory board (independent non-executives)

composed entirely of supervisory directors. In the two-tier

structure it is the supervisory board that has to control and

monitor the board of directors. The supervisory board has the right

to nominate and disregard directors and they have a vote for

important decisions that influence the survival and current state of

the organization. The shareholders are informed of the state, policy

etc. from the organizations’ executive management, during the

12

shareholders’ meeting. During the meeting, the shareholders have the

right to approve or disapprove the annual report (Goodijk, 2007).

Other issues the Civil Code provides are the “mitigated structure

regime” and the “exempted regime”. These regimes apply for most

multinationals, small companies that are part of a holding outside

the Netherlands and for organizations which half of the employees

are working outside the Netherlands. The same as in the “structure

regime” the supervisory board have the legal right to approve or

disapprove important decisions of the management, but unlike the

“structure regime” the shareholders have the right to nominate and

disregard management directors in stead of the supervisory board. In

the Rijnland approach there are a few shareholders, and those few

poses a large percentage of the total shares of the organization

(“high ownership concentration”).

For small and medium-sized organizations the “common regime” is

applicable. In this regime the organization has a choice to have a

two-tier board or only a board of executive directors (Goodijk,

2007).

In the Rijnland approach the management organizations tend to have a

stakeholder orientation. From this view the boards are responsible

for balancing all the different shareholder and stakeholder

interests and gaining their confidence, this is the so called

“balancing act”. It is the Supervisory Board that has to meet the

requirements of independence, quality and trust in order to monitor

and control management decisions on behalf of the entire company;

this is called the “system of countervailing powers”. This means

that the supervisory board has legal right to disapprove decisions

of the management that influence some stakeholders of the

organization (Goodijk, 2007).

13

The organizations in the Rijnland approach are seen as

“institutional firms”, this means that the organization is

considered to be a co-operation of employer and employees with a

longer term perspective and having open relationships with

shareholders and stakeholders.

2.2 Anglo-Saxon approachIn the Anglo-Saxon approach of corporate governance the organization

has an one-tier board system. This board consists of executive and

non-executive board members, which are together in one board

(Goodijk, 2007; Baysinger & Butler, 1985; Hart, 1995). If

organizations are listed, they need to have a greater amount of non-

executive members in their board then there are executive members

(p.4 NYSE). In this one-tier system the chairman of the board works

closely with the CEO, and there are three committees within the

board: audit-, remuneration- and nomination committee (Goodijk,

2007).

In the Anglo-Saxon approach, the organizations have a shareholder

orientation, meaning that the board will try to maximize shareholder

value and look after shareholder interests (Baysinger & Butler,

1985). Because of this shareholder orientation, the share-ownership

is more dispersed (“dispersed share-ownership”). This dispersion

leads to the fact that there are more shareholders that all posses a

smaller percentage of the total of shares of the organization (Hart,

1995).

This is approach is further characterized by the fact that

organizations are “instrumental firms”. In these firms the

stakeholders are part of an environment that must be controlled to

create profits, effectiveness and maximize shareholder value.

14

In firms with an one-tier board there is no place for the

countervailing power system, but there is a strong leadership

culture. This means that the CEO has a lot of power, because in the

one-tier system there isn’t a supervisory board which can counter

the important decisions of the managing board. Additionally the CEO

is more a leader in the Anlgo-Saxon approach, which is the opposite

of the Rijnland approach, because there isn’t as much co-operation

between employer and employees. It is because of this that in the

Anglo-Saxon approach the employees are looking up more against the

CEO than in the other approach. Sometimes the CEO also is the

chairman of the board, than he has a dual role in the company. In

this case that person has a lot of power and there are almost no

countervailing powers (Baysinger & Butler, 1985).

2.3 The main differences between the approachesIn this section the three main differences between the two

approaches will be displayed in three tables. These differences are

also the most important differences in the Organon case. On the

left-side of the tables the Anglo-Saxon approach will be explained

and on the right side the Rijnland approach. One of the main

differences between the Anglo-Saxon and the Rijnland approach is the

different orientation of the management within the organization.

Shareholders orientation Stakeholder orientation

Maximize shareholder value Look after all stakeholder interests

Seek profitability , efficiency and short term

Look for survival, long term growth and stability

15

The second main difference between the two approaches is the

composition of the organization structure, especially that of the

board structure.

One-tier board Two-tier board

Executive and non-executive directors in one board

One board of executive managers and one supervisory board consisting of only non-executive directors

Chairman and CEO work together Supervisory board independent from management board

The third difference is the way the organizations, in the

approaches, view the environment and especially the stakeholders.

Instrumental firm Institutional firm

Stakeholders must be controlled Co-operating and open relationship with stakeholders

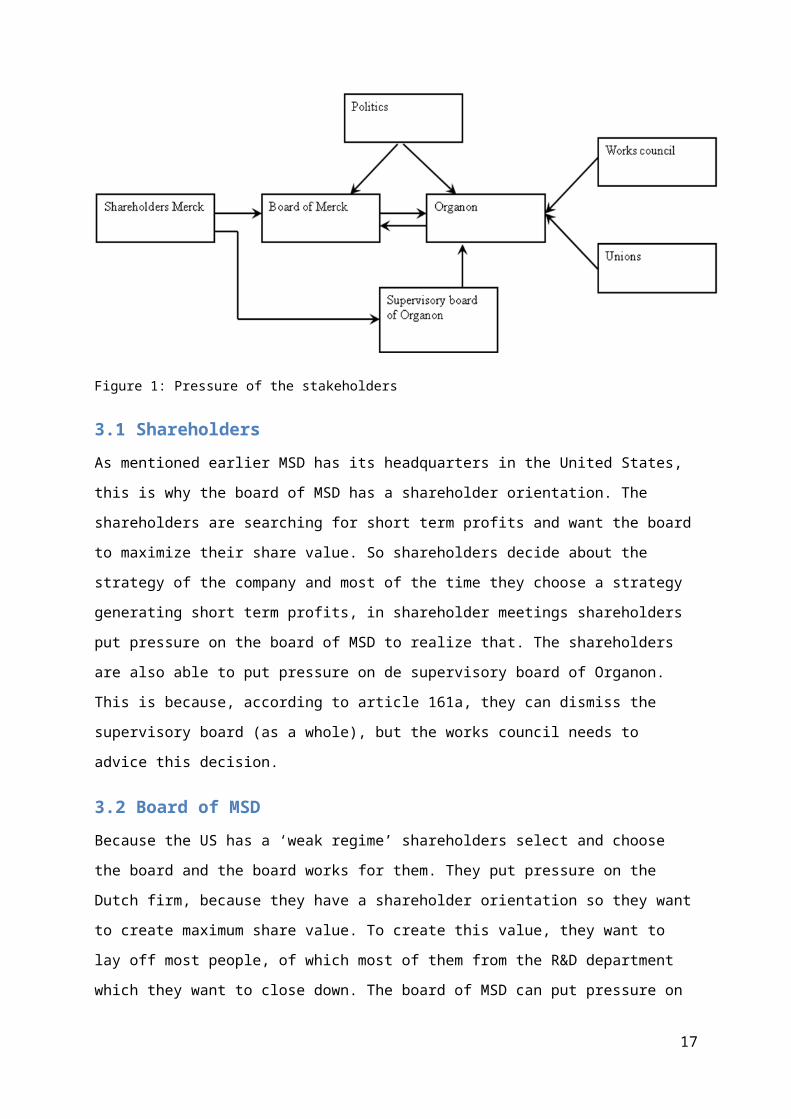

3. Corporate Governance stakeholdersIn this section the stakeholders of Organon are discussed, by making

use of the figure below. This figure displays various stakeholders

that have something to do with Corporate Governance in the case of

Organon and in some way put pressure on other stakeholders. The

arrows within the figure explain which stakeholder puts pressure on

another stakeholder, for example the shareholders put pressure on

the board of MSD. All the arrows in the figure will be explained in

different paragraphs with the corporate governance dilemmas between

those stakeholders.

16

Figure 1: Pressure of the stakeholders

3.1 Shareholders As mentioned earlier MSD has its headquarters in the United States,

this is why the board of MSD has a shareholder orientation. The

shareholders are searching for short term profits and want the board

to maximize their share value. So shareholders decide about the

strategy of the company and most of the time they choose a strategy

generating short term profits, in shareholder meetings shareholders

put pressure on the board of MSD to realize that. The shareholders

are also able to put pressure on de supervisory board of Organon.

This is because, according to article 161a, they can dismiss the

supervisory board (as a whole), but the works council needs to

advice this decision.

3.2 Board of MSDBecause the US has a ‘weak regime’ shareholders select and choose

the board and the board works for them. They put pressure on the

Dutch firm, because they have a shareholder orientation so they want

to create maximum share value. To create this value, they want to

lay off most people, of which most of them from the R&D department

which they want to close down. The board of MSD can put pressure on

17

Organon, because they are the owner of Organon and, according to US

law, working with the one tier board system, they can reorganize

almost always what and whenever they want.

3.3 OrganonThe stakeholders (supervisory board, works council and union)

influencing Organon will be discussed here. They point their arrows

towards Organon and not directly to the board of MSD, because they

can put pressure on the board of MSD through Organon. This means

that the arrow from Organon to the board of MSD includes the arrows

of the stakeholders that will be discussed here.

3.3.1 Supervisory board of Organon

The supervisory board of Organon has the power, by Dutch law, to

approve or disapprove on important decisions off the firm, made by

the management. In this case the decision is not in the best

interest of the company, and according to article 164 of the Civil

law part 2 approval of the supervisory board is, as mentioned,

necessary. It doesn’t matter if the decision is made by a foreign

company, because the decision is about the Dutch part of the

organization. If the board still continues their decision, the

supervisory board is able to stop them in short order. So the

supervisory board can put pressure, countervailing power, on the

board of MSD.

3.3.2 Union

The union of Organon can put pressure on the management by

demonstrations or refusing to work, thereby creating negative media

attention. Further when the dismissal of employees comes closer,

unions have to be notified. In the case of a collective dismissal

(20 or more of the employees) the employer has to explain the unions

why they are firing the employees. If the union does not agree there

18

is a thirty day waiting time to find new places in the company for

employees, further they have to discuss the possibilities of a

social plan with the union(s) and works council. Finally, another

option the unions have is to ask for an inquiry procedure, at the

chamber of commerce, to prove mismanagement of the board. These are

ways for the employees of Organon to make use of the countervailing

powers of the unions.

3.3.3 Works council

The board of MSD is, when making important decisions, obligated

(according to article 25 of the law relating to the works councils)

to ask the works council for advice, but this is only advice. This

advice has to be asked for almost all strategically decisions and

has to be asked beforehand so there is plenty of time for the works

council to have real influence. They also can go to the chamber of

commerce (after the supervisory board turns down the merger) to

prove mismanagement of the board. Further, the works council also

can go to the politicians to ask for their help or advice, if

politics is not supporting the reorganization MSD may get extra

‘bad’ publicity.

Besides the right to advise the board and going to politicians,

another right of the council is to choose one third of the new

supervisory board. Finally, they also have the possibility to

network with the shareholders, like trying to make a deal with the

board. With these points in mind they can put pressure on the board

and they can keep fighting against closing down the R&D department.

3.3.4 The PoliticsAs mentioned earlier, the works council can go to the politicians

for help and or advice. For the politicians closing down Organon can

be a disaster for the knowledge economy in the Netherlands,

especially when politicians want it to be a knowledge economy. When

19

the politicians agree that closing down is not a good idea, it can

strengthen the advice of the works council. They also can, as

mentioned earlier, state in the media that they do not agree with

the closure of Organon, and in this way put pressure on the board of

MSD (creating negative media attention). Finally politicians also

have the possibility to put direct pressure on the board of MSD by

contacting them and try to change their minds or make a deal.

4. Corporate Governance dilemmas In this chapter we take an overview of previously discussed points

to show the dilemmas related to Corporate Governance in the case of

Organon. First some stakeholders will be discussed again to make a

direct relation to the case. Afterward the dilemmas for MSD will be

summed in chronological order, leading to a conclusion.

4.1 Board of directors and shareholdersThe shareholders put pressure on the board of directors to make a

good profit for them. Because of this, it seems that MSD bought

Organon for their patents on medicines, with in mind that their own

patents of medicines where almost expired. The decreasing profit

from older medicine patents leads to decreasing profit margins, to

make sure that this does not happens they need new patents allowing

MSD to produce those medicines, and to continue with the same or

more turnover to keep the shareholders satisfied.

When MSD bought Organon they probably had already in mind that they

wanted to close down the R&D department of Organon, because MSD

already had a R&D department and two research departments doing

double work is a waste of money. The only strange part is that they

never communicated, to their stakeholders, that they wanted to close

all new research facilities.

20

4.2 The Dutch works councilAs mentioned, important decisions have to be discussed with the

works council. Although it is only advice, the board still has to

ask for it in important situations. This way the works council can

put pressure on the board of MSD. In the case of Organon they went

to court, “the commercial chamber”, because MSD did not asked for

advice in the decision to close down different parts of Organon.

Besides the right to advise, the works council is also allowed to

choose one third of the new supervisory board if the old one is

dismissed. This way the new supervisory board can be strong again

against the board of MSD. The works council also has the possibility

to talk with the shareholders to try and convince them of the fact

that closing down research facilities might be bad for them, also

networking with politicians might be of influence. Finally, the

works council can talk with the board about a social plan.

4.3 The supervisory boardAs mentioned, the supervisory board has the right to approve or

disapprove on important decisions. In the case of Organon the

supervisory board disapproved the decision of the board to

reorganize. Reasons for doing so included that MSD could have known

beforehand that with taking over Organon they would have had too

many research facilities but they did not mentioned the

reorganization and never informed the shareholders about it.

Although they disapproved on the reorganization, the supervisory

board does not have to be scared for the board. The board is not

able to send them home on the base of heavy handed arguments neither

is there a case of the delivery of malicious work, one of the two

mentioned is necessary to send the supervisory board home.

21

4.4 Dilemmas for MSD4.4.1 Dilemmas until 2nd of September 2010First dilemma for MSD are their stakeholders, they put pressure on

the board to make profit. This pressure has leaded the board to buy

Organon and some other pharmacy companies over the world. Secondly,

due to the takeovers the board now had many companies but they all

had their own management team, research facilities etcetera so

reorganization was necessary. The first issue they created here was

that, when they took over Organon they promised that there would not

be a large reorganization with the loss of many jobs. The promise

leads us further in the case where the third dilemma rises, to stay

profitable they have to reorganize because they have their own

research en development centers and too many employees only costs

money.

The reorganization is announced, but in The Netherlands they find a

supervisory board and works council that are against the

reorganization. The supervisory board disapproves with the

reorganization, they are not notified early enough, according to the

Dutch law, to try and find any other possible options, for Organon,

instead of closing it down and firing all employees.

Also the works council is against; they go to court because they

have the legal right, according article 161a, to advise the board on

important decisions, and the board did not gave them that right.

The board of MSD, as well as the shareholders were not able to

dismiss the supervisory board because there are no heavy handed

arguments. Neither is there a case of delivering malicious work,

this means that the decision of the supervisory board to reject the

reorganization cannot be ignored. Further, as mentioned the works

council did not have had any opportunity to give advice, and so on

the day that the court would start to discuss the complaint of the

22

works council, the board of MSD decided to give the supervisory

board and works council till the 31st of December 2010 to find any

other options besides closing down the company. After this, if there

are no good solutions they will continue the reorganization.

5. Discussion and ConclusionIn this chapter we will discuss the possibilities for the future of

Organon after the 31st of December, for this we will use information

from the group discussion in our lecture. To create a ground for our

argumentation to the future first two almost similar cases will be

mentioned.

5.1 Cases that have some relation to OrganonThe case of Organon is often compared with cases from Stork or

Corus. To give an example from Corus out of 2003, the old previously

named Hoogovens in IJmuiden. An English mother company had decided

that the Dutch aluminum production part had to be sold and the

profits should flow to the English mother company. The supervisory

board did not agree with that, because it had too many negative

effects on the Dutch part of Corus. So the board of the mother

company went to court (the chamber of commerce) to dismiss the

supervisory board. But in this case the judges did not agree with

the board, because the supervisory board did what they had to do

according to their responsibilities.

A second example is the case of Stork. This is quite a complicated

case of which we will try to simplify, the most important part of

the jurisprudence for this case. Because of a strategy change,

shareholders wanted Stork to focus on just one part of their

processes and sell the rest of the departments. In a meeting between

the shareholders and Stork, the supervisory board showed that they

did not agree with the new strategy and so the shareholders wanted

23

to terminate their trust in the supervisory board and asked the

chamber of commerce to advice for a research concerning the way of

working within Stork including suspension of the supervisory board.

This made that Stork gave the advice to the chamber of commerce to

broaden the research including the shareholder approach related to

the case. The Unions and works council together, on their turn asked

the Chamber to deny the shareholders their voting rights on the

specific point of dismissal of the Supervisory board.

Besides the fact that the judge mentioned that the way of working of

the supervisory board of Stork in this case was not fully correct,

another point mentioned in the court was that the chamber of

commerce is in principle not there to decide about the strategy or

vision and about any correctness in that sense. Discussions about

that have to be done within the company law frame. This states that:

in corporate governance, strategy is the business of the board. A

supervisory board inspects that and shareholders have the

possibility to express their opinions (including the right to

terminating their trust). But this does not mean you have to accept

and it can be tested in relation to existing laws. In the case of

Stork the strategy does not give any reasons for doubt on their

policies. But although the policy might be correct, it might not be

based well enough on strong fundamental argumentation.

The last part can be said, because in decisions you also have to

include fairness and reasonability, as mentioned in article 2:8 8W,

and this cannot be said without outcomes of an external research

focused on the risks for Stork to leave their strategy and choose

for the one of their shareholders.

In the Jurisprudence that means that the chamber of commerce finds

it necessary that Stork cannot be forced to make a radical change in

24

the strategy beforehand. Having this in mind, knowing about the

unstable situation when dismissing the supervisory board and looking

at the importance of a fast reorganization and recovery of the

relationships within Stork, the chamber of commerce forbids the

shareholders to terminate their trust in supervisory board. Further

the chamber also appoints three commissioners that have the right to

set the agenda of the shareholder meetings and have a overruling

voice on subjects about major (de-)investments, strategy changing’s

of Stork and cases that keep Stork and Centaurus divided on strategy

related points.

5.2 Dilemmas after 31st of December 2010What can possibly be the case after the 31st of December? Using the

group discussion and based on the previously mentioned information

about earlier cases we came with the following. According to the

Dutch law the supervisory board still has to approve on the

reorganization, if they do not do that, legally the reorganization

cannot continue.

As showed in the case of Stork there still is a chance for another

court fight. Unions still have the possibility to ask for an inquiry

to prove mismanagement, or a way of working that is beyond

reasonability and fairness. The Jurisprudence in the Stork case can

lead to a decision of the chamber of commerce that Organon cannot be

forced upon a radical change, because of some facts known

beforehand. Again keeping in mind, the unstable situation when

dismissing the supervisory board and looking at the importance for

Organon and MSD of a fast reorganization and recovery, the chamber

might (as in the Stork case) forbid the shareholders to terminate

their trust in supervisory board. Besides that is also possible,

again looking at previous jurisprudence, that the chamber decides to

appoint extra commissioners with the right of setting the

25

shareholder meeting agenda, give them an overruling voice on

subjects about strategy changing’s, (de-investments) and other

strategy related points that MSD and Organon are divided about.

This again could lead to a longer term for Organon to find another

company to buy them.

On the other hand the supervisory board might be dismissed for

disapproving on the reorganization because they have had 4 months to

find any good solutions, and the conclusion after those 4 months can

be that there are no good alternative solutions. To save face, the

best thing they can do than is to step down. Either ways it is

important for MSD is, to finish the reorganization before the end of

2012 because at that time the social plan ends.

26

5.3 Conclusion and adviceTo our judgment there are several options for the outcome of the

Organon case. Till 31ste December the board of Merck has two

options: they have found a partner for the take over or they will

continue closing down Organon. When the board of Merck decides to

continue with the closing down there are again two options: The

supervisory board approves or the supervisory board does not

approve. When the supervisory board does not agree with the decision

of the board of Merck the union has the option to start an inquiry

to declare mismanagement, the only question in this case is: will

the union do that, because it has to be in the interest of the

employees.

To our opinion the best option for Organon ist that Organon is taken

over by another company, which does not have the intention of

closing down the research and development department in The

Netherlands. Another good option will be that the board of Merck

comes up with a social plan where the union and the supervisory

board of Organon can agree upon, for example replacing employees in

other companies, slowly laying off employees or partly closing down

departments. But if the board of Merck does not find a partner and

then continues closing down Organon, the advice for the supervisory

board will be to step down so they make a statement that they do not

agree and are not responsible for the decision of the board of

Merck.

For the Netherlands this is a case out of many. Seen from the

specialization of Corporate Governance it might be good for the

government to take a look at all cases and adapt or write some new

codes for future situations. It might be thinkable that the position

of the supervisory board will be stronger in these situations so

they have to agree on the situation but if they don’t, they cannot

27

be dismissed by the shareholders. This can only be done by the

chamber of commerce, in case their decision is not within the

boundaries of the reasonable. Point is, if you introduce these kinds

of codes it might stop investments from foreign companies which

again have its influence on the economy.

BibliographyAA, E. v. (2010, August 30). De Telegraaf. Opgeroepen op September 24, 2010, van De Telegraaf: http://www.telegraaf.nl/dft/goeroes/finanscoop/7505450/__In_de_loopgraven_om_Organon__.html

ANP. (2010, August 1). NU.nl. Retrieved September 24, 2010, from Nu.nl: http://www.nu.nl/economie/2304141/commissarissen-organon-plannen-msd.html

ANP. (2010, September 4). NU.nl. Retrieved September 24, 2010, from NU.nl: http://www.nu.nl/economie/2326335/japanners-willen-organon.html

Baysinger, B., & Butler, H. (1985). Corporate Governance and the Board of Directors: Performance Effects of Changes in Board. Oxford Journals , 101-124.

Bennaars, J., & Vestering, P. (sd). Beperking van bestuurders beloning in het regenwoud van vennootschapsrecht, arbeidsrecht en gedragscodes. Arbeidsrecht praktijk , 13 - 24.

Bouwmans, A. (2010, September 3). Brabants Dagblad. Retrieved September24, 2010, from Brabants Dagblad: http://www.brabantsdagblad.nl/regios/oss/Organon/7226019/Ondernemingsraad-wint-eerste-slag.ece

28

Brabants Dagblad. (2010, August 16). Retrieved September 24, 2010, fromBrabants Dagblad: http://www.brabantsdagblad.nl/regios/oss/Organon/7072983/Merck-kan-RvC-Organon-niet-negeren.ece

Broek, J. v. (2010, September 2). NOS. Retrieved September 24, 2010,from NOS: http://nos.nl/artikel/182211-msd-stelt-sluiting-organon-oss-uit.html

Budding, J. (2010, August 23). medicalfacts. Retrieved September 24, 2010, from medicalfacts: http://www.medicalfacts.nl/2010/08/23/or-en-rvc-houden-voet-bij-stuk-verslikt-msd-zich-in-organon/

Chhaochharia, V., & Grinstein, Y. (2007, August). Corporate Governance and firm value: the impact of the 2002 Governance rules. The Journal of Finance , 1789-1825.

Code, M. C. (2008). De Nederlandse Coporate governance code. De Nederlandse Coporate governance code . http://corpgov.nl/page/downloads/Dec_2008_Code_NL.pdf.

Committee, C. G. (9/12/2003). Principles of good corporate governance and best practice provisions. Dutch Corporate Governance Committee.

De Telegraaf. (2010, October 12). Retrieved from De Telegraaf: www.telegraaf.nl

de verdieping Trouw. (2010, August 23). Retrieved September 24, 2010, from de verdieping Trouw: http://www.trouw.nl/nieuws/nederland/article3177179.ece/Toekomst_Organon_nog_ongewis.html

de verdieping Trouw. (2010, October 12). Retrieved from de verdieping Trouw: www.trouw.nl

De Volkskrant. (2010, October 12). Retrieved from De Volkskrant: www.volkskrant.nl

FD.nl, Het Financieele Dagblad. (2010, October 12). Retrieved from Het Financieele Dagblad: www.fd.nl

Final NYSE Corporate Governance Rules. (2003, November 4). Final NYSE Corporate Governance Rules . USA.

29

Goodijk, R. (2007). Corporate governance in the Netherlands. Corporategovernance in the Netherlands . Groningen, Groningen, Netherlands: Facultyof Managemetn and Oranization, University of Groningen.

Haas, A. d., & Snijders, H. (2010, July 27). Brabants Dagblad. Retrieved September 2010, 24, from Brabants Dagblad: http://www.brabantsdagblad.nl/regios/oss/Organon/7039874/Brons-vindt-dat-Merck-helemaal-van-zijn-geloof-is-gevallen.ece

Hart, O. (1995). Corporate Governance: Some Theory and implications.The Economic Journal , 678-689.

Merck be well. (2010, October 12). Retrieved from Merck be well: http://merck.com/

Monitoring Commissie Corporate Governance Code. (2010, 9 24). Retrieved fromMonitoring Commissie Corporate Governance Code: http://corpgov.nl/

MSD. (2010, October 12). Retrieved from MSD: http://www.msd.nl/

Nationaal Register Commissarissen en Toezichthouders. (2010, Oktober 25). Retrieved Oktober 15, 2010, from Nationaal Register Commissarissen en Toezichthouders: http://www.nationaalregister.com/page-1731.htm

NOS. (2010, October 12). Retrieved from NOS: www.nos.nl

nrc Handelsblad. (2010, October 12). Retrieved from nrc Handelsblad: www.nrc.nl

Nu.nl. (2010, Ocktober 12). Retrieved from Nu.nl: www.nu.nl

OR-online.nl. (2010, Oktober 25). Retrieved Oktober 16, 2010, from OR-Online.nl: http://www.or-online.nl/naslag/orenpvt/1.0/2.6%20structuur-nv/2.65

redacteuren, e. o. (2010, September 12). nrc Handelsblad. Retrieved September 24, 2010, from nrc Handelsblad: http://www.nrc.nl/economie/article2613032.ece/Sluiting_Organon_Oss_uitgesteld

SEC. (2010, September 24). Retrieved from SEC: http://www.sec.gov/news/press/2009/2009-116.htm

Shivdasani, A., & Yermack, D. (1999). CEO involvement in the selection of new board members: an emperical analysis. The journal of finance , 1829-1853.

30

Snijders, H. (2010, July 29). Brabants Dagblad. Retrieved September 24,2010, from Brabants Dagblad: http://www.brabantsdagblad.nl/regios/oss/Organon/7053173/Ook-delen-Organon-in-de-verkoop.ece

Snijders, H. (2010, August 3). Brabants Dagblad. Retrieved August 24, 2010, from Brabants Dagblad: http://www.brabantsdagblad.nl/regios/oss/Organon/7072983/Merck-kan-RvC-Organon-niet-negeren.ece

Verhoog, J. (1998). N.V. Organon, Oss. Noordwijk: Uitgeverij aan Zee.

Vos, C. (08, July 2010). De Volkskrant. Retrieved September 24, 2010, from De Volkskrant: http://www.volkskrant.nl/economie/article1398630.ece/Massaontslag_Organon_is_mokerslag

31

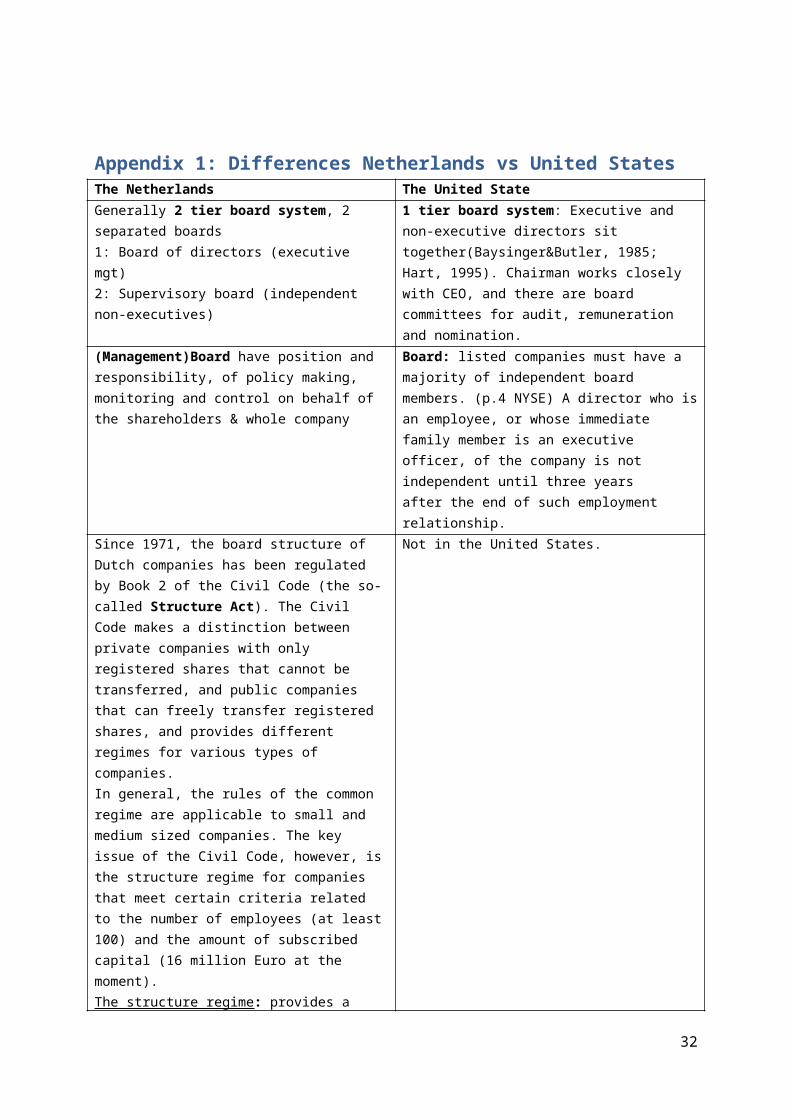

Appendix 1: Differences Netherlands vs United StatesThe Netherlands The United StateGenerally 2 tier board system, 2 separated boards1: Board of directors (executive mgt)2: Supervisory board (independent non-executives)

1 tier board system: Executive and non-executive directors sit together(Baysinger&Butler, 1985; Hart, 1995). Chairman works closely with CEO, and there are board committees for audit, remuneration and nomination.

(Management)Board have position and responsibility, of policy making, monitoring and control on behalf of the shareholders & whole company

Board: listed companies must have a majority of independent board members. (p.4 NYSE) A director who isan employee, or whose immediate family member is an executive officer, of the company is not independent until three yearsafter the end of such employment relationship.

Since 1971, the board structure of Dutch companies has been regulated by Book 2 of the Civil Code (the so-called Structure Act). The Civil Code makes a distinction between private companies with only registered shares that cannot be transferred, and public companies that can freely transfer registered shares, and provides different regimes for various types of companies.In general, the rules of the common regime are applicable to small and medium sized companies. The key issue of the Civil Code, however, isthe structure regime for companies that meet certain criteria related to the number of employees (at least100) and the amount of subscribed capital (16 million Euro at the moment). The structure regime: provides a

Not in the United States.

32

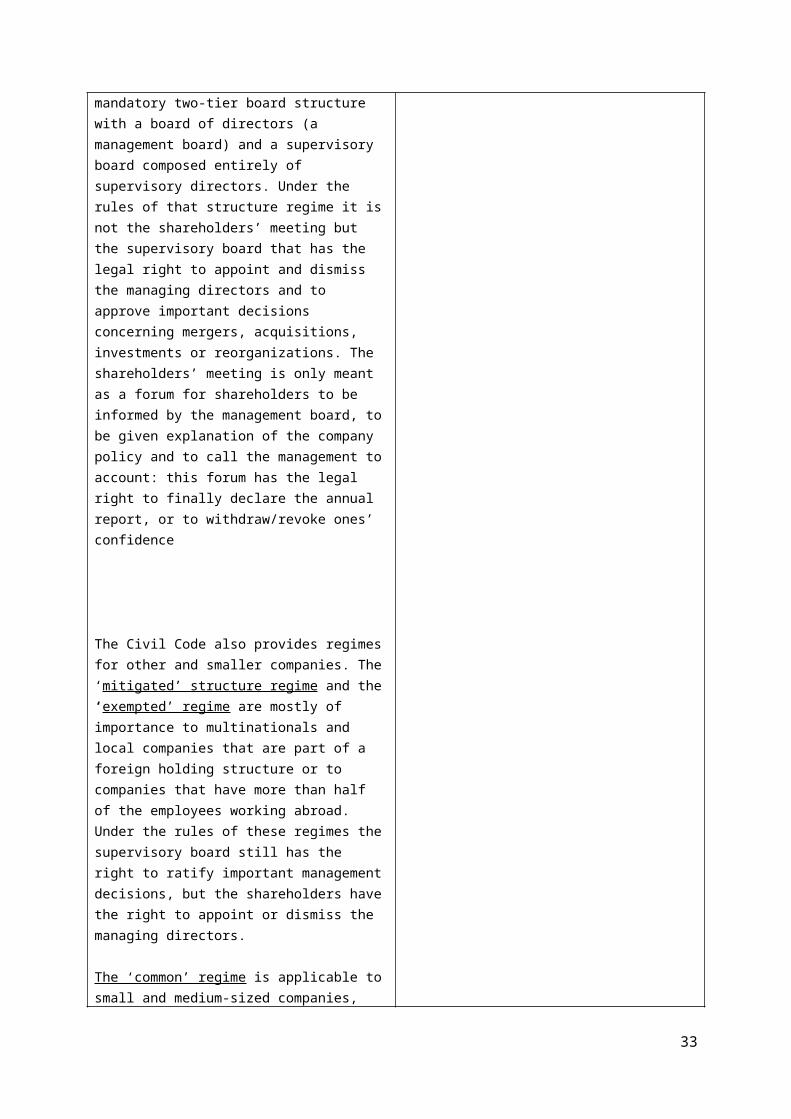

mandatory two-tier board structure with a board of directors (a management board) and a supervisory board composed entirely of supervisory directors. Under the rules of that structure regime it isnot the shareholders’ meeting but the supervisory board that has the legal right to appoint and dismiss the managing directors and to approve important decisions concerning mergers, acquisitions, investments or reorganizations. The shareholders’ meeting is only meant as a forum for shareholders to be informed by the management board, tobe given explanation of the company policy and to call the management toaccount: this forum has the legal right to finally declare the annual report, or to withdraw/revoke ones’ confidence

The Civil Code also provides regimesfor other and smaller companies. The‘mitigated’ structure regime and the‘exempted’ regime are mostly of importance to multinationals and local companies that are part of a foreign holding structure or to companies that have more than half of the employees working abroad. Under the rules of these regimes thesupervisory board still has the right to ratify important managementdecisions, but the shareholders havethe right to appoint or dismiss the managing directors.

The ‘common’ regime is applicable tosmall and medium-sized companies,

33

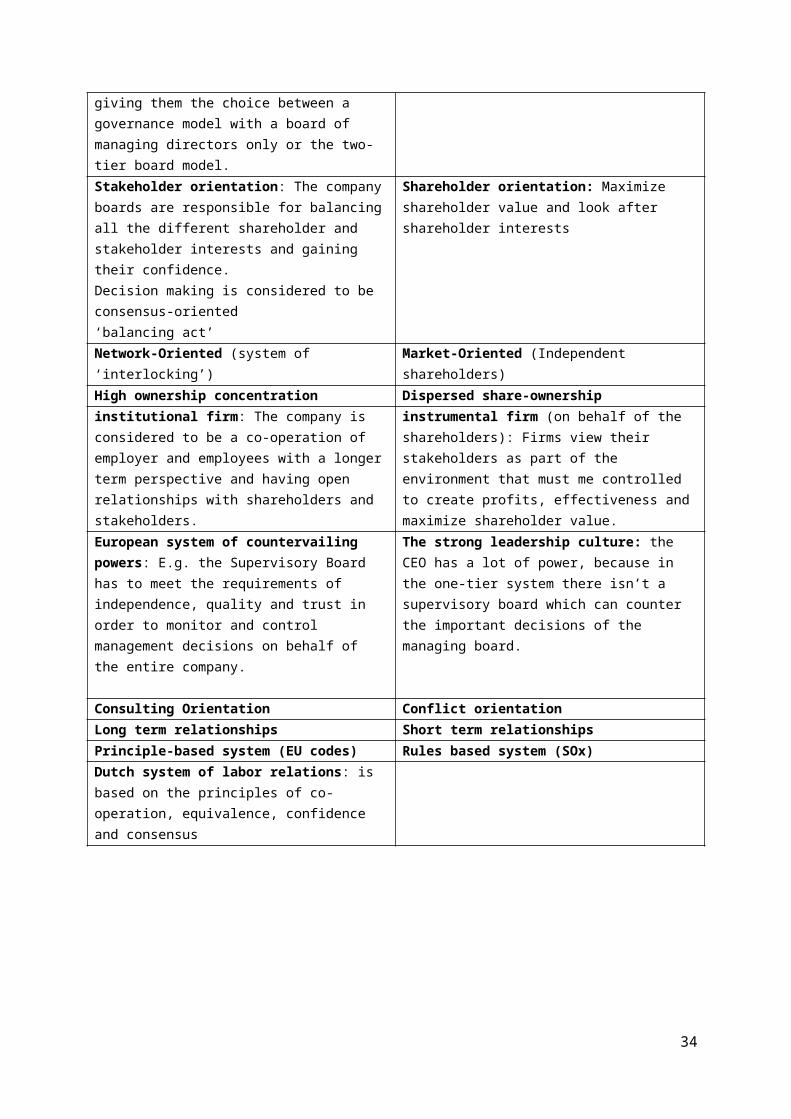

giving them the choice between a governance model with a board of managing directors only or the two-tier board model.Stakeholder orientation: The companyboards are responsible for balancingall the different shareholder and stakeholder interests and gaining their confidence.Decision making is considered to be consensus-oriented‘balancing act’

Shareholder orientation: Maximize shareholder value and look after shareholder interests

Network-Oriented (system of ‘interlocking’)

Market-Oriented (Independent shareholders)

High ownership concentration Dispersed share-ownershipinstitutional firm: The company is considered to be a co-operation of employer and employees with a longerterm perspective and having open relationships with shareholders and stakeholders.

instrumental firm (on behalf of the shareholders): Firms view their stakeholders as part of the environment that must me controlled to create profits, effectiveness and maximize shareholder value.

European system of countervailing powers: E.g. the Supervisory Board has to meet the requirements of independence, quality and trust in order to monitor and control management decisions on behalf of the entire company.

The strong leadership culture: the CEO has a lot of power, because in the one-tier system there isn’t a supervisory board which can counter the important decisions of the managing board.

Consulting Orientation Conflict orientationLong term relationships Short term relationshipsPrinciple-based system (EU codes) Rules based system (SOx)Dutch system of labor relations: is based on the principles of co-operation, equivalence, confidence and consensus

34

Appendix 2: Differences in responsibilitiesThe Netherlands The United States

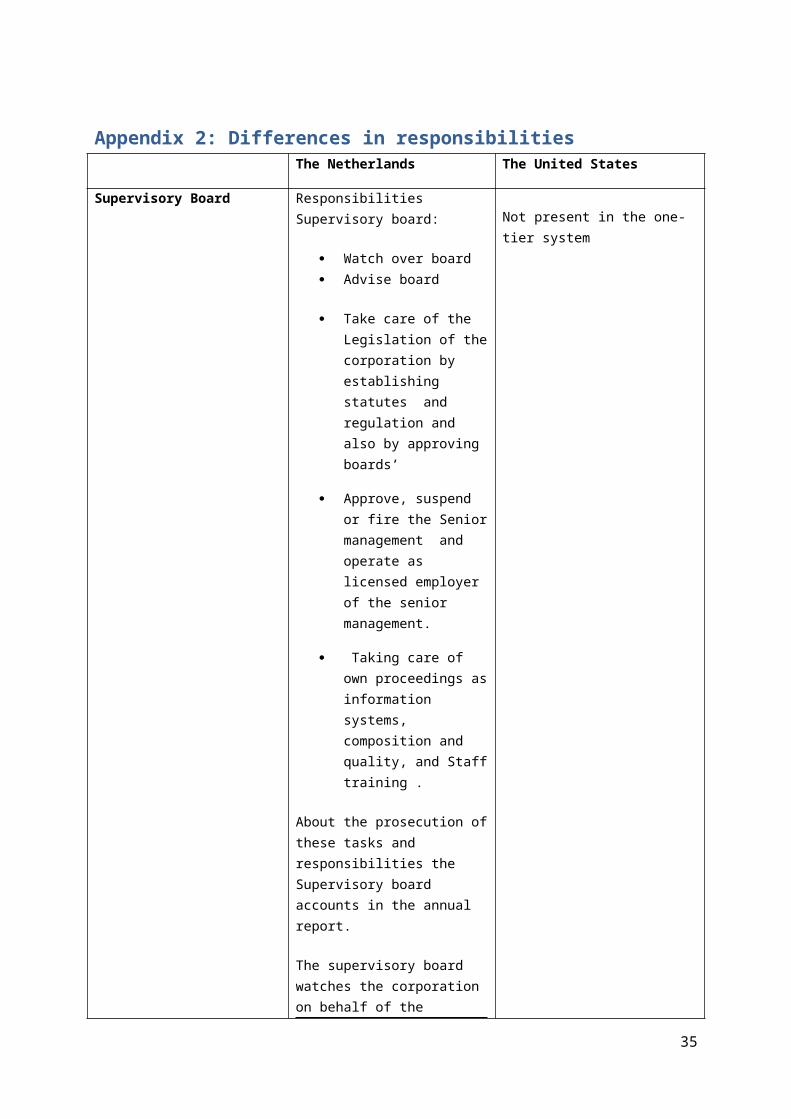

Supervisory Board Responsibilities Supervisory board:

Watch over board Advise board

Take care of the Legislation of thecorporation by establishing statutes and regulation and also by approving boards’

Approve, suspend or fire the Seniormanagement and operate as licensed employer of the senior management.

Taking care of own proceedings asinformation systems, composition and quality, and Stafftraining .

About the prosecution ofthese tasks and responsibilities the Supervisory board accounts in the annual report.

The supervisory board watches the corporation on behalf of the

Not present in the one-tier system

35

stakeholders, society and government

Has to control the boardof directors in the bestinterests of the company, operating independently from all the shareholders and stakeholders.

Appointed by shareholders after recommended by the board, and – the works council has the right toselect and nominate – atmost - a third of the board members.

Board of Directors

Managing the organization

Realization of goals

Set-up of the strategy includingrisk profile

Responsible for the results of thecorporation

Responsible for the social aspectsof the corporation(dec. 2008 code NL)

Represents & accounts the shareholders

Monitors & controls mgt for maximizing shareholder value

Hire, fire, compensate senior management

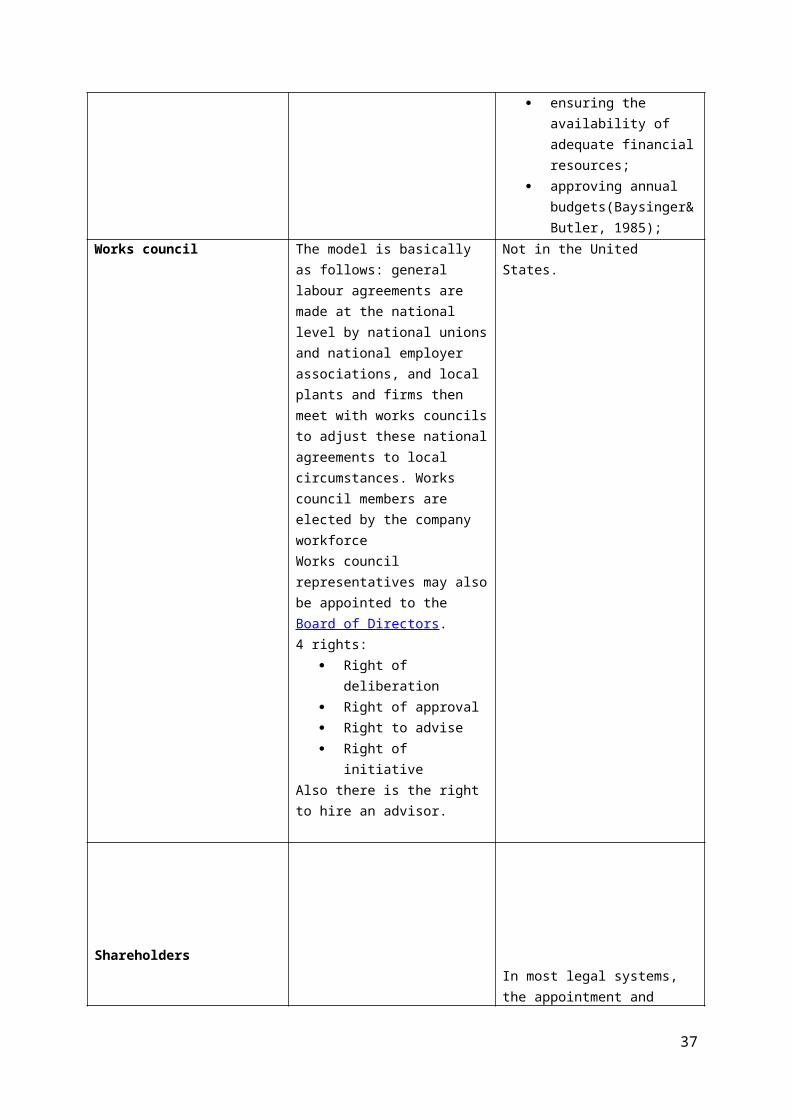

Governing the organization by establishing broadpolicies and objectives;

selecting, appointing, supporting and reviewing the performance of thechief executive;

36

ensuring the availability of adequate financialresources;

approving annual budgets(Baysinger&Butler, 1985);

Works council The model is basically as follows: general labour agreements are made at the national level by national unionsand national employer associations, and local plants and firms then meet with works councilsto adjust these nationalagreements to local circumstances. Works council members are elected by the company workforceWorks council representatives may alsobe appointed to the Board of Directors.4 rights:

Right of deliberation

Right of approval Right to advise Right of

initiativeAlso there is the right to hire an advisor.

Not in the United States.

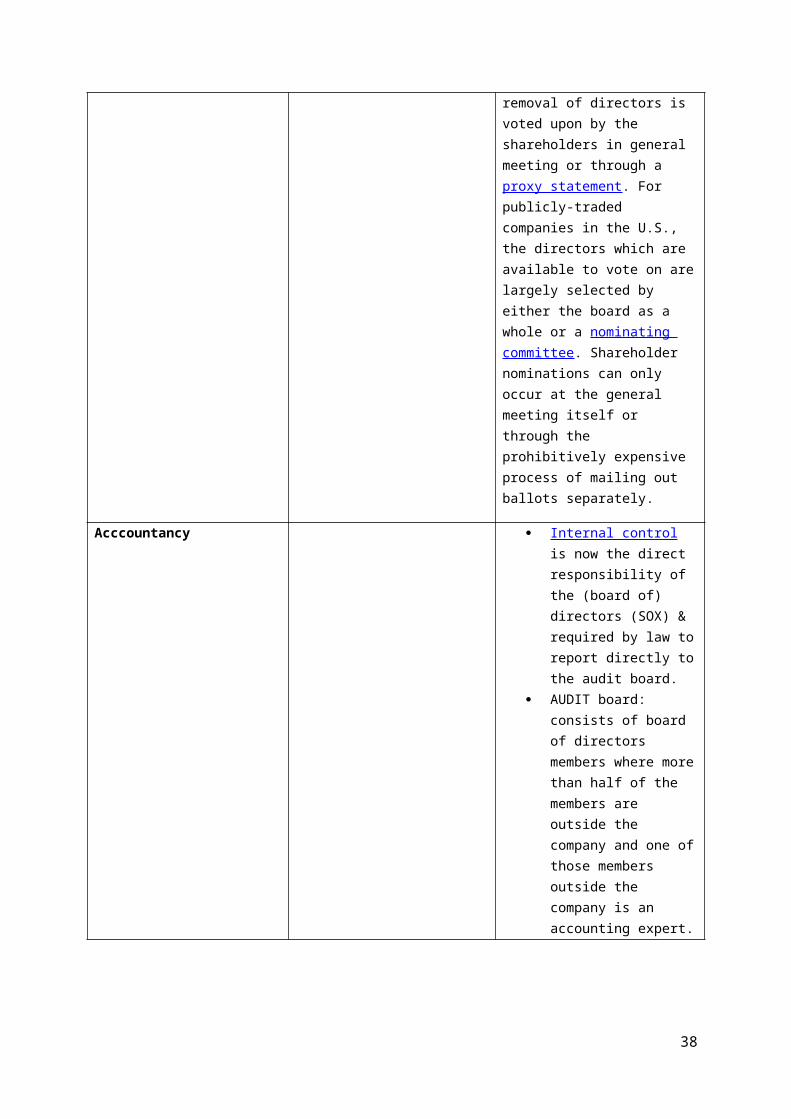

ShareholdersIn most legal systems, the appointment and

37

removal of directors is voted upon by the shareholders in general meeting or through a proxy statement. For publicly-traded companies in the U.S., the directors which are available to vote on arelargely selected by either the board as a whole or a nominating committee. Shareholder nominations can only occur at the general meeting itself or through the prohibitively expensive process of mailing out ballots separately.

Acccountancy Internal control is now the direct responsibility of the (board of) directors (SOX) & required by law toreport directly tothe audit board.

AUDIT board: consists of board of directors members where morethan half of the members are outside the company and one ofthose members outside the company is an accounting expert.

38

39

![Between the Actual and the Trivial World [Organon F]](https://img.dokumen.tips/doc/110x75/6352b72bcb577625920ddaf8/between-the-actual-and-the-trivial-world-organon-f.jpg)