Embed Size (px)

Citation preview

Chapter 2. Basic accounting

concepts and principles

Instructor: Ng T Thuc Hien

Outline

1.Assets, liabilities and equity concepts

2.Recording financial transactions

3. Double-entry bookkeeping

Assets, liabilities and

equity concepts

01.

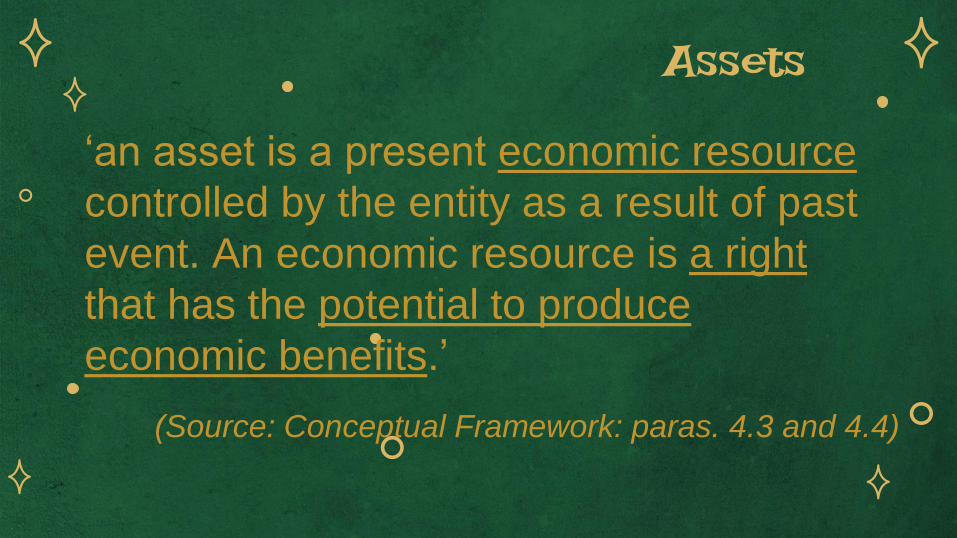

Assets

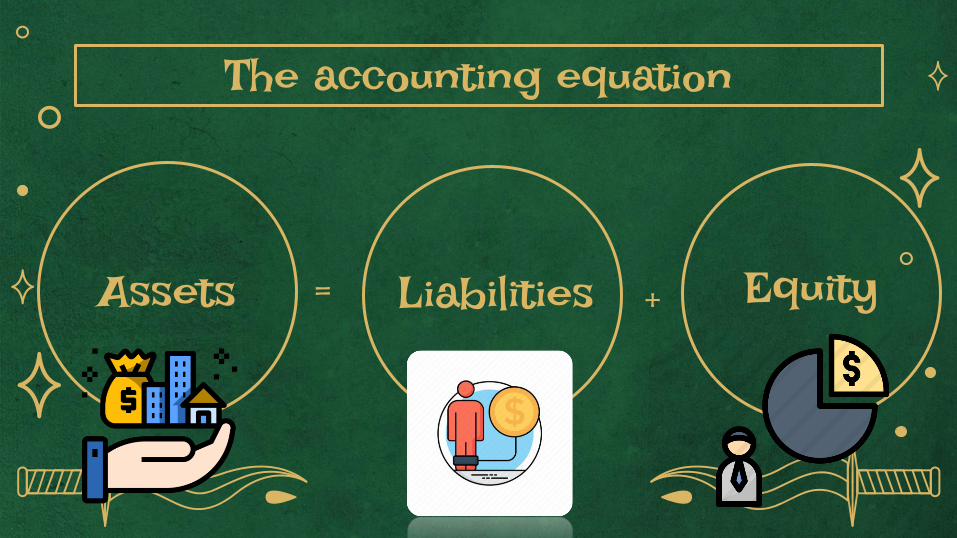

The accounting equation

+Liabilities= Equity

Assets

‘an asset is a present economic resource

controlled by the entity as a result of past

event. An economic resource is a right

that has the potential to produce

economic benefits.’

(Source: Conceptual Framework: paras. 4.3 and 4.4)

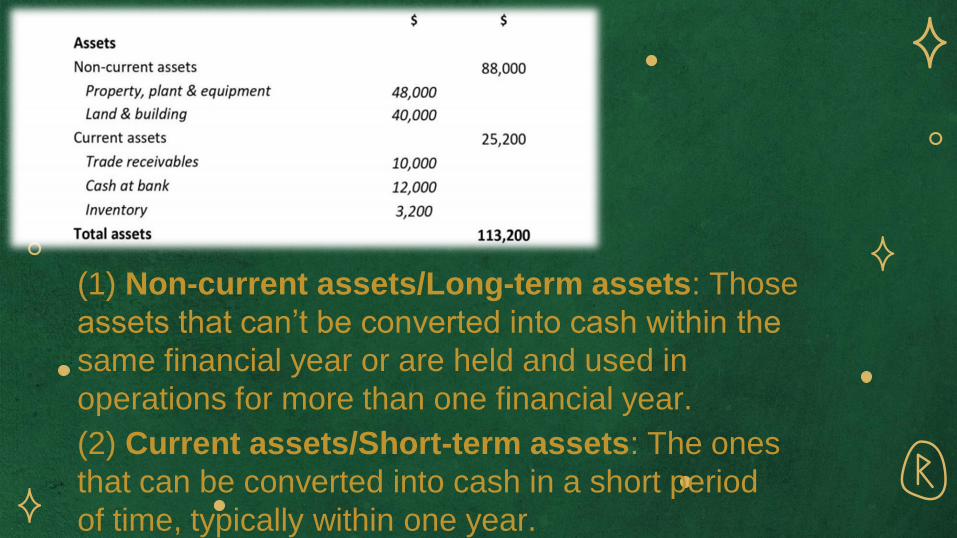

(1) Non-current assets/Long-term assets: Those

assets that can’t be converted into cash within the

same financial year or are held and used in

operations for more than one financial year.

(2) Current assets/Short-term assets: The ones

that can be converted into cash in a short period

of time, typically within one year.

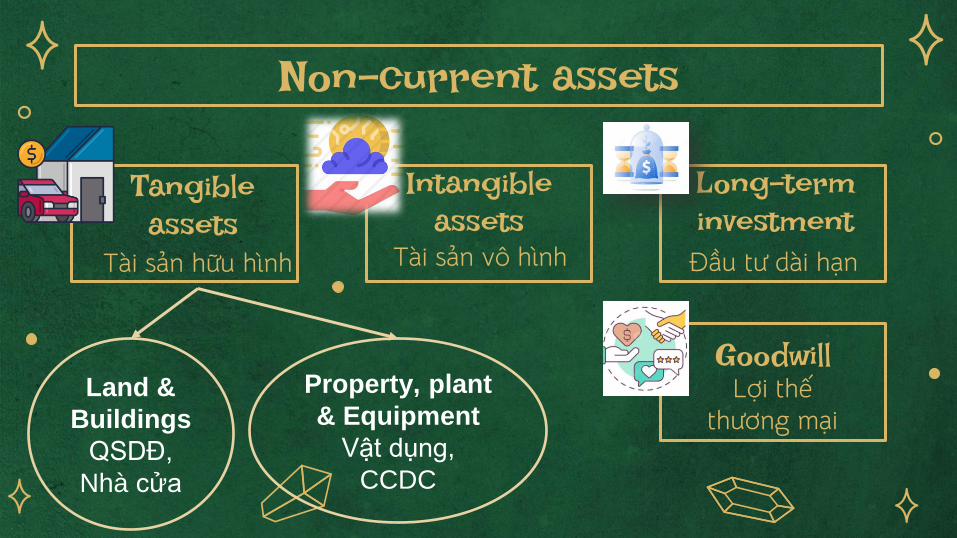

Tangible

assetsTài sản hữu hình

Intangible

assetsTài sản vô hình

Non-current assets

GoodwillLợi thế

thương mại

Long-term

investment

Đầu tư dài hạn

Land &

Buildings

QSDĐ,

Nhà cửa

Property, plant

& Equipment

Vật dụng,

CCDC

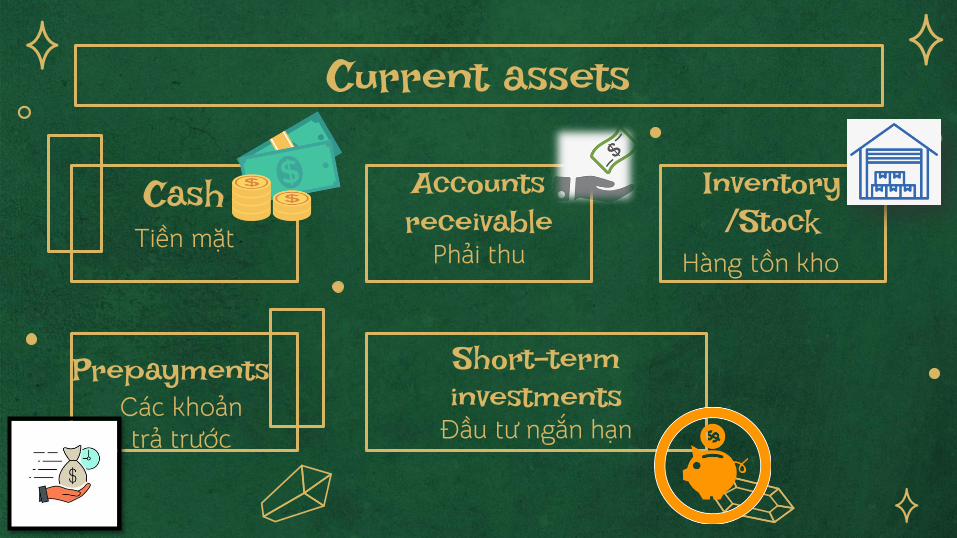

CashTiền mặt

Accounts

receivablePhải thu

Current assets

PrepaymentsCác khoản trả trước

Short-term

investmentsĐầu tư ngắn hạn

Inventory

/Stock

Hàng tồn kho

Liabilities

‘a liability is a present obligation of the entity to

transfer an economic resource as a result of

past events.’

(Conceptual Framework: para. 4.26)

Group work 1

(1)What are two types of

liabilities? (10 points)

(2)Examples of liability

items? (5 points/correct

answer)

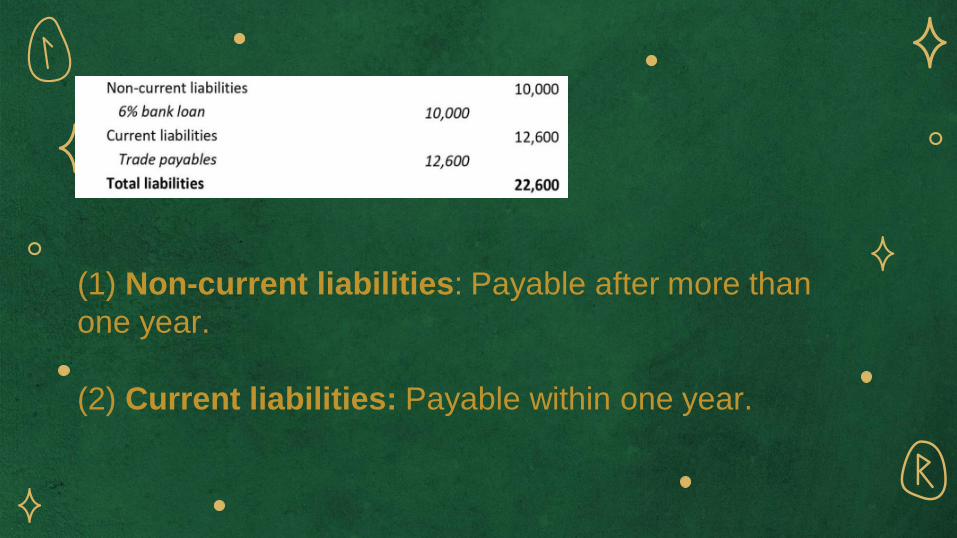

(1) Non-current liabilities: Payable after more than

one year.

(2) Current liabilities: Payable within one year.

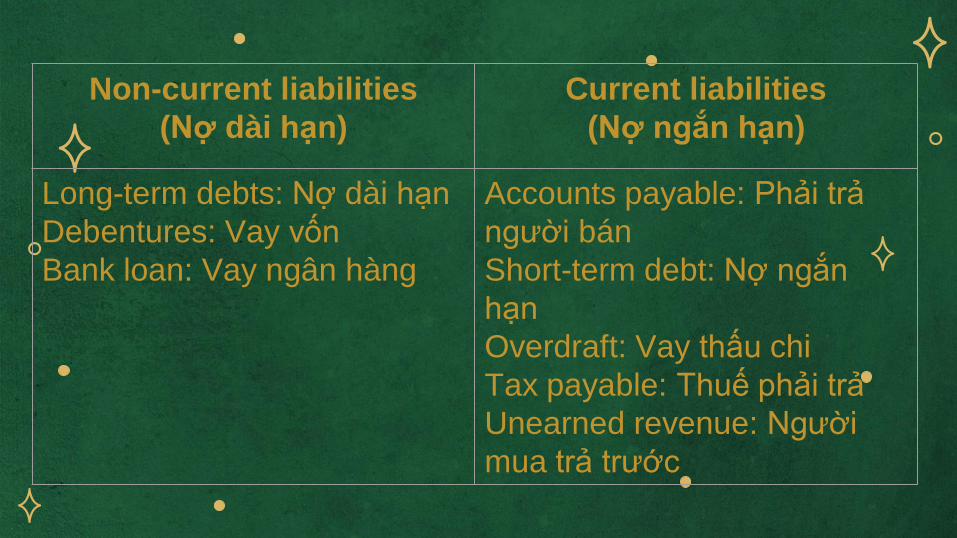

Non-current liabilities

(Nợ dài hạn)

Current liabilities

(Nợ ngắn hạn)

Long-term debts: Nợ dài hạn

Debentures: Vay vốn

Bank loan: Vay ngân hàng

Accounts payable: Phải trả

người bán

Short-term debt: Nợ ngắn

hạn

Overdraft: Vay thấu chi

Tax payable: Thuế phải trả

Unearned revenue: Người

mua trả trước

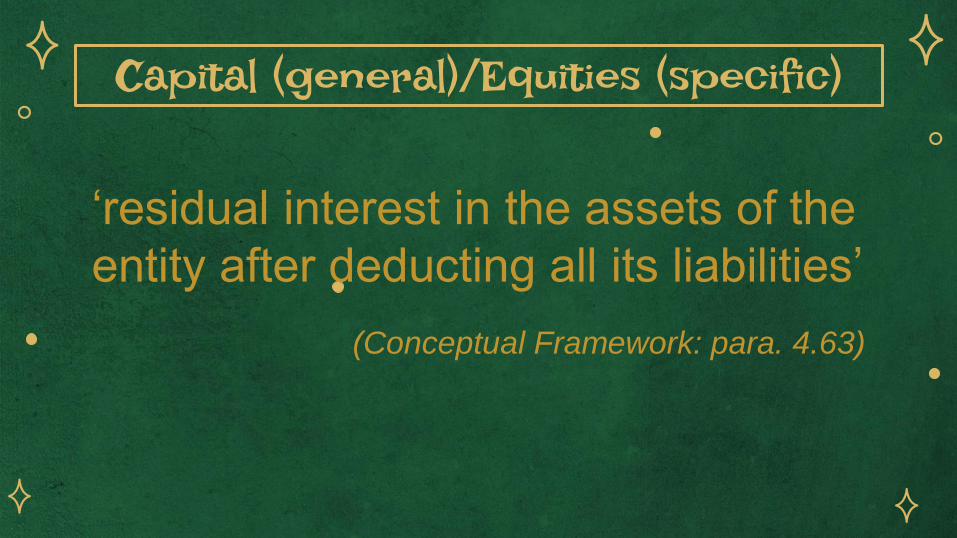

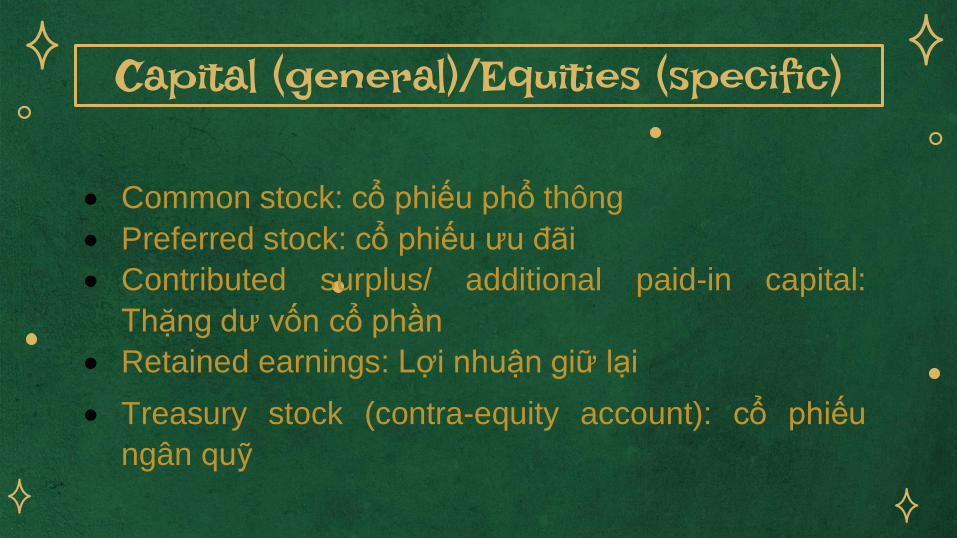

Capital (general)/Equities (specific)

‘residual interest in the assets of the

entity after deducting all its liabilities’

(Conceptual Framework: para. 4.63)

Capital (general)/Equities (specific)

• Common stock: cổ phiếu phổ thông

• Preferred stock: cổ phiếu ưu đãi

• Contributed surplus/ additional paid-in capital:

Thặng dư vốn cổ phần

• Retained earnings: Lợi nhuận giữ lại

• Treasury stock (contra-equity account): cổ phiếu

ngân quỹ

Group work 2

Which items in the accounting

system are affected by the

following transactions? (10

pts/item)

1. Lotus company records sale on credit of a

stationary bill for VND 110.000? Knowing that VAT

is 10%.

Group work 2

Which items in the accounting

system are affected by the

following transactions? (10

pts/item)

2. Lotus company records a cash payment for

internet service for the up coming year?

Recording financial

transactions

02.

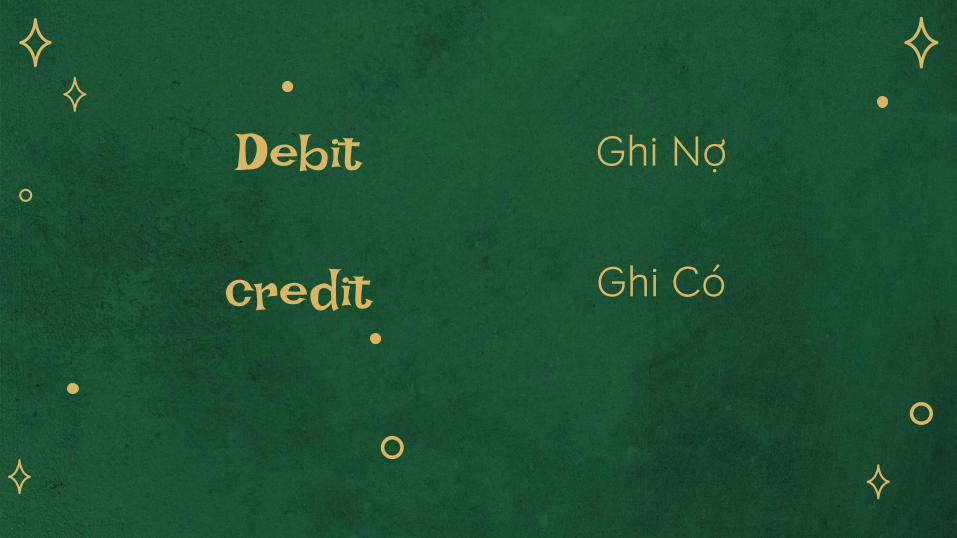

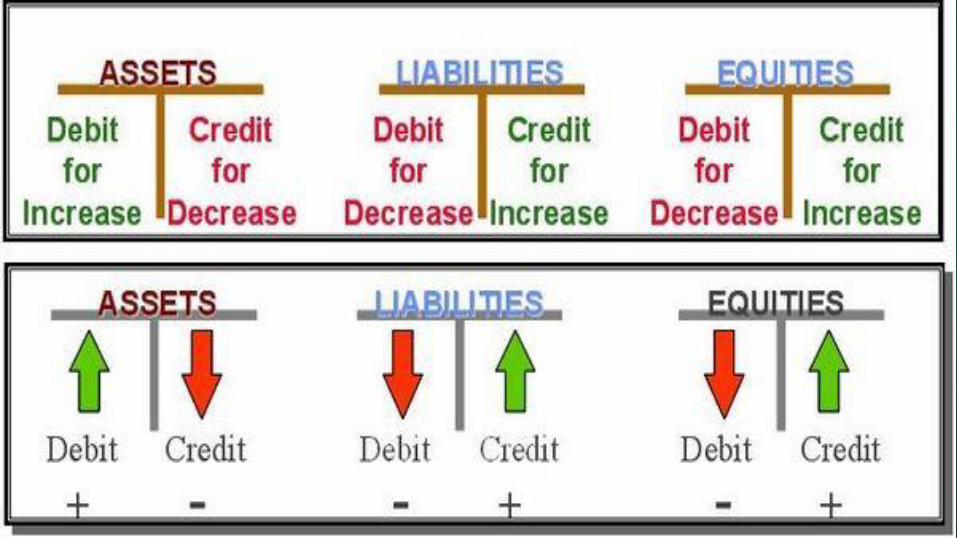

Debit Ghi Nợ

credit Ghi Có

Double entry

bookkeeping

03.

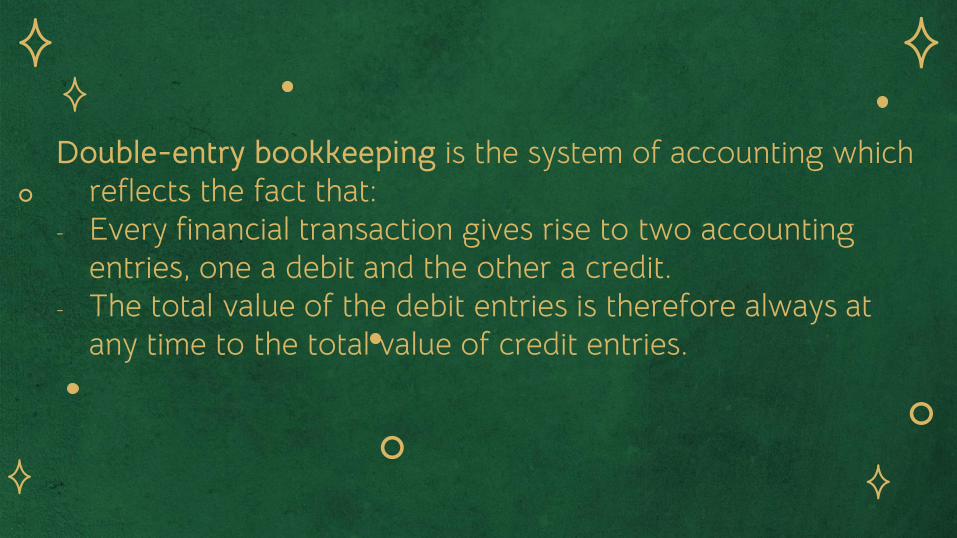

Double-entry bookkeeping is the system of accounting which reflects the fact that:

- Every financial transaction gives rise to two accounting entries, one a debit and the other a credit.

- The total value of the debit entries is therefore always at any time to the total value of credit entries.

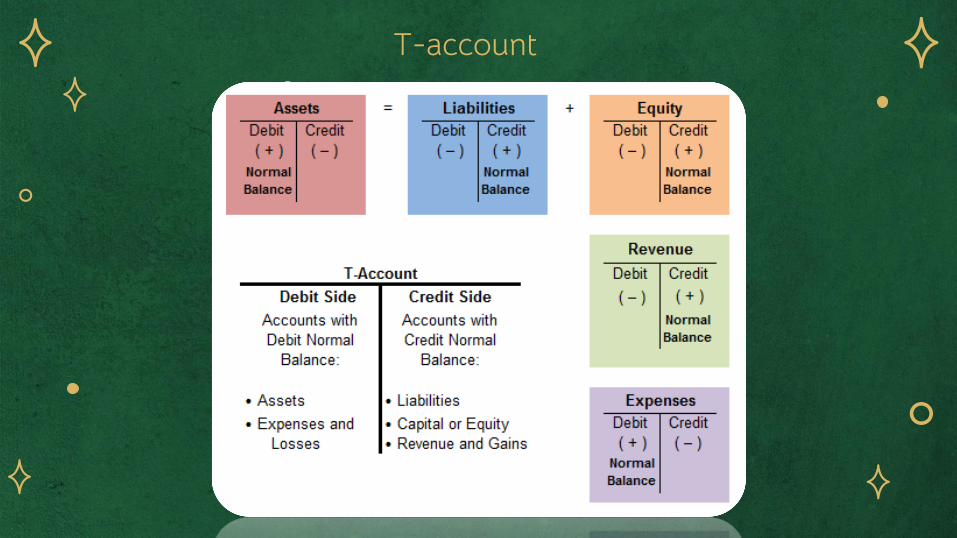

T-account

Double-entry bookkeeping: Hệ thống ghi sổ képT-account: Tài khoản chữ T

Have a nice day!