Embed Size (px)

Citation preview

Report of the Central Board of Directors on the working of the Reserve Bank of India

for the year ended June 30, 2009 submitted to the Central Government in terms of

Section 53(2) of the Reserve Bank of India Act, 1934

RESERVE BANK OF INDIA ANNUAL REPORT2008-09

GOVERNOR

D. Subbarao

DEPUTY GOVERNORS

Shyamala Gopinath

Usha Thorat

K.C. Chakrabarty

DIRECTORS NOMINATED UNDERSECTION 8 (1) (b) OF THE RBI ACT, 1934

Y.H. Malegam

Suresh D. Tendulkar

U.R. Rao

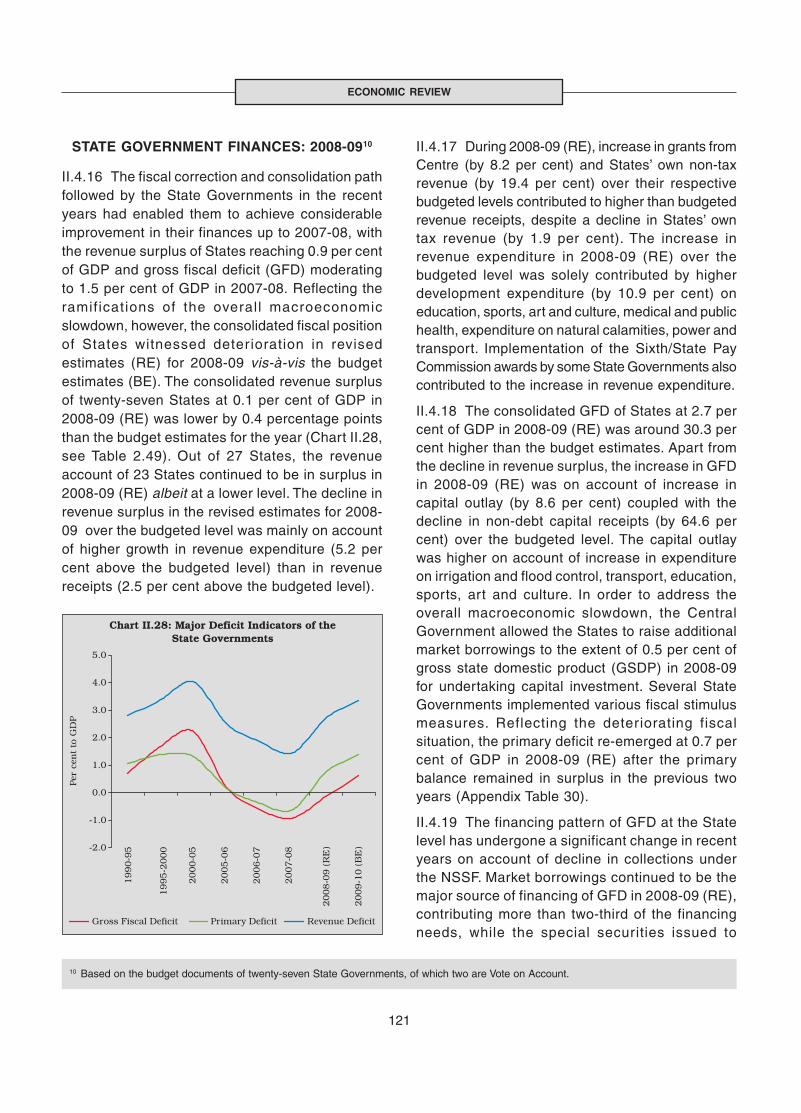

Lakshmi Chand

DIRECTORS NOMINATED UNDERSECTION 8 (1) (c) OF THE RBI ACT, 1934

H. P. Ranina

Ashok S. Ganguly

Azim Premji

Kumar Mangalam Birla

Shashi Rajagopalan

Suresh Neotia

A. Vaidyanathan

Man Mohan Sharma

D. Jayavarthanavelu

Sanjay Labroo

DIRECTOR NOMINATED UNDERSECTION 8 (1) (d) OF THE RBI ACT, 1934

Ashok Chawla

MEMBERS OF LOCAL BOARDS

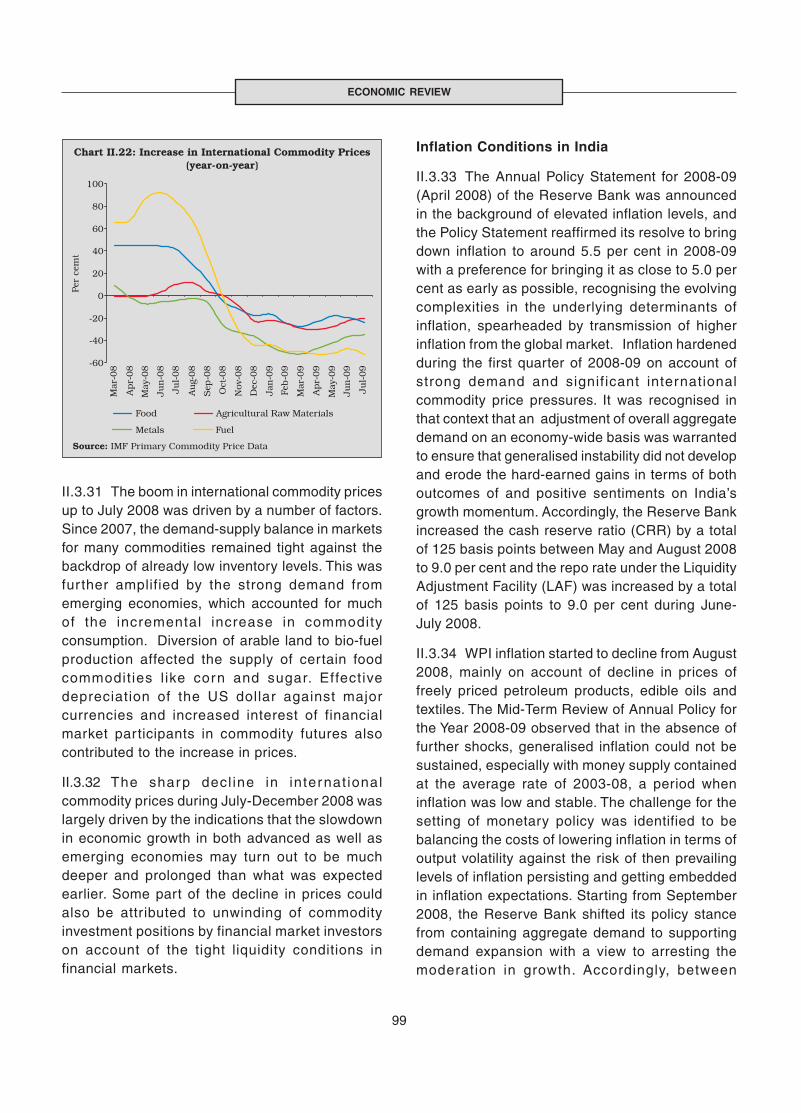

WESTERN AREA

Y.H. Malegam

K. Venkatesan

Dattaraj V. Salgaocar

Jayantilal B. Patel

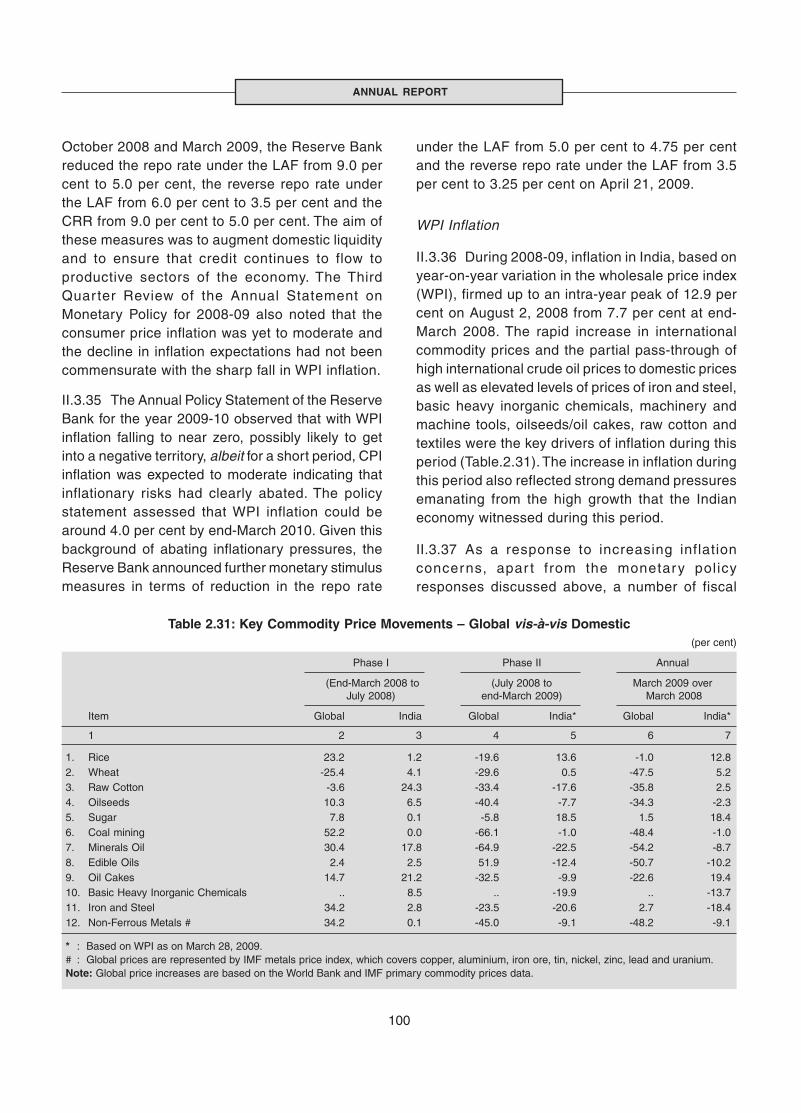

EASTERN AREA

Suresh D. Tendulkar

A. K. Saikia

Sovan Kanungo

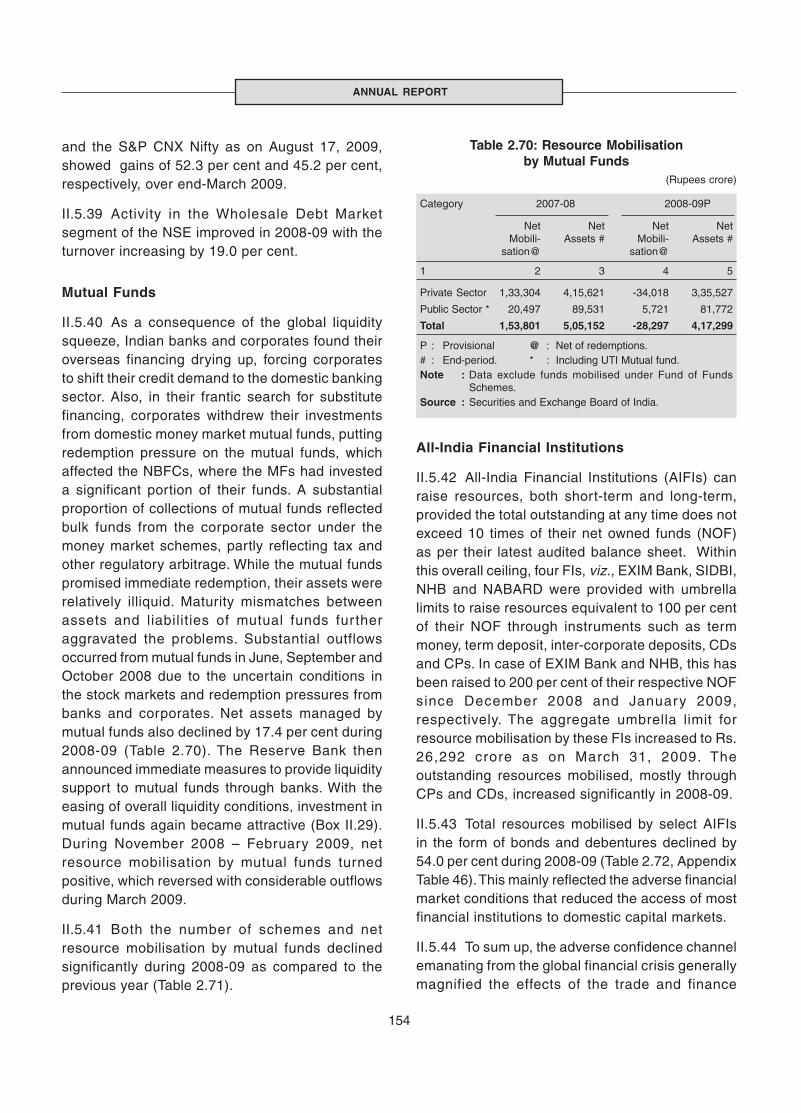

NORTHERN AREA

U.R. Rao

Mitha Lal Mehta

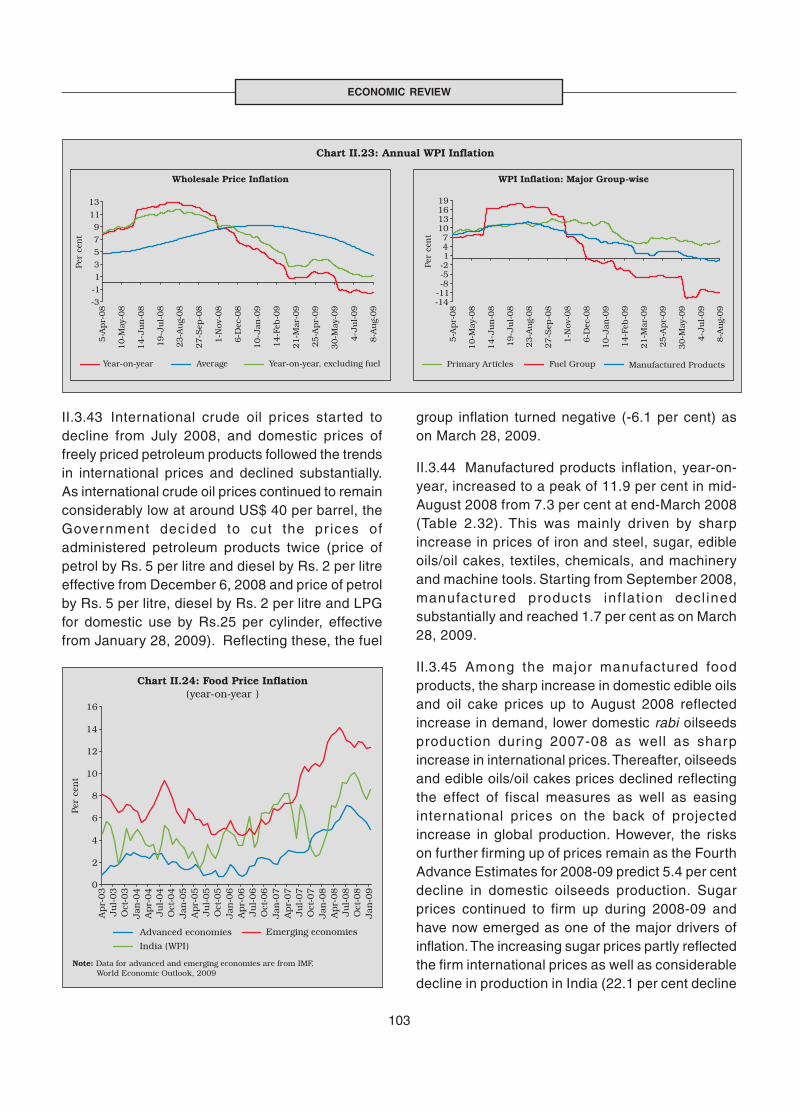

Ram Nath

Pritam Singh

SOUTHERN AREA

Lakshmi Chand

C. P. Nair

M. Govinda Rao

Devaki Jain

CENTRAL BOARD / LOCAL BOARDS

AS ON JUNE 30, 2009

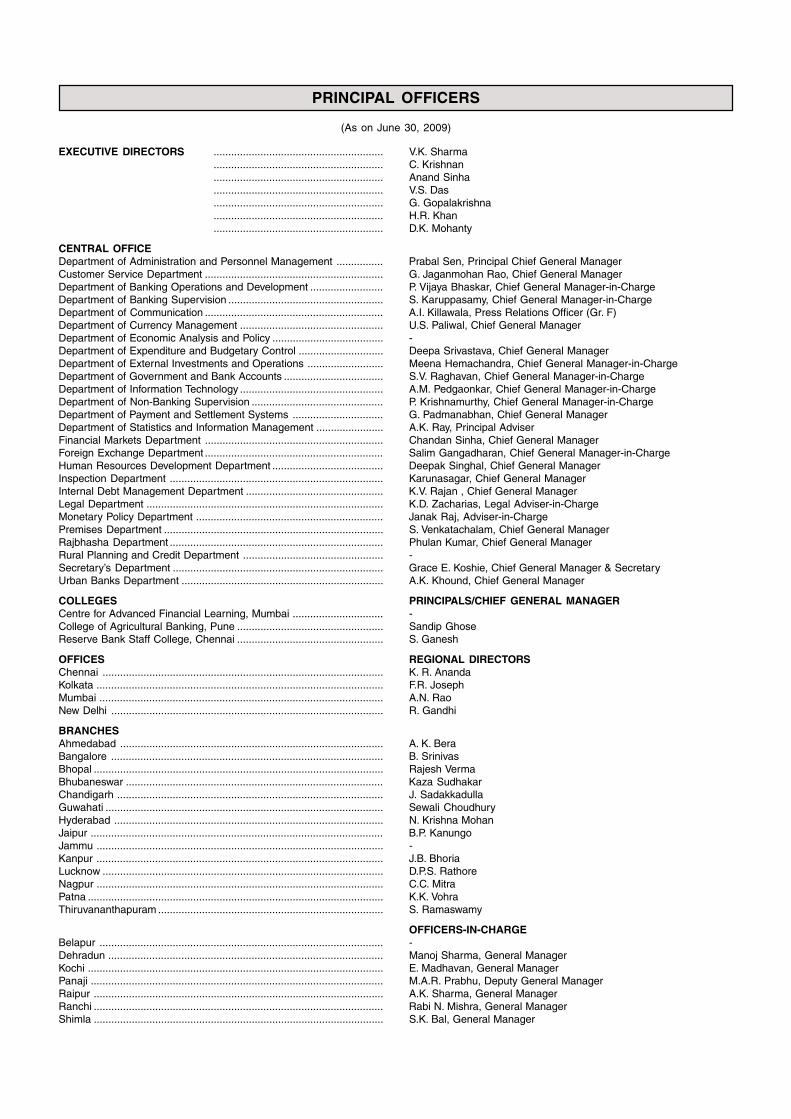

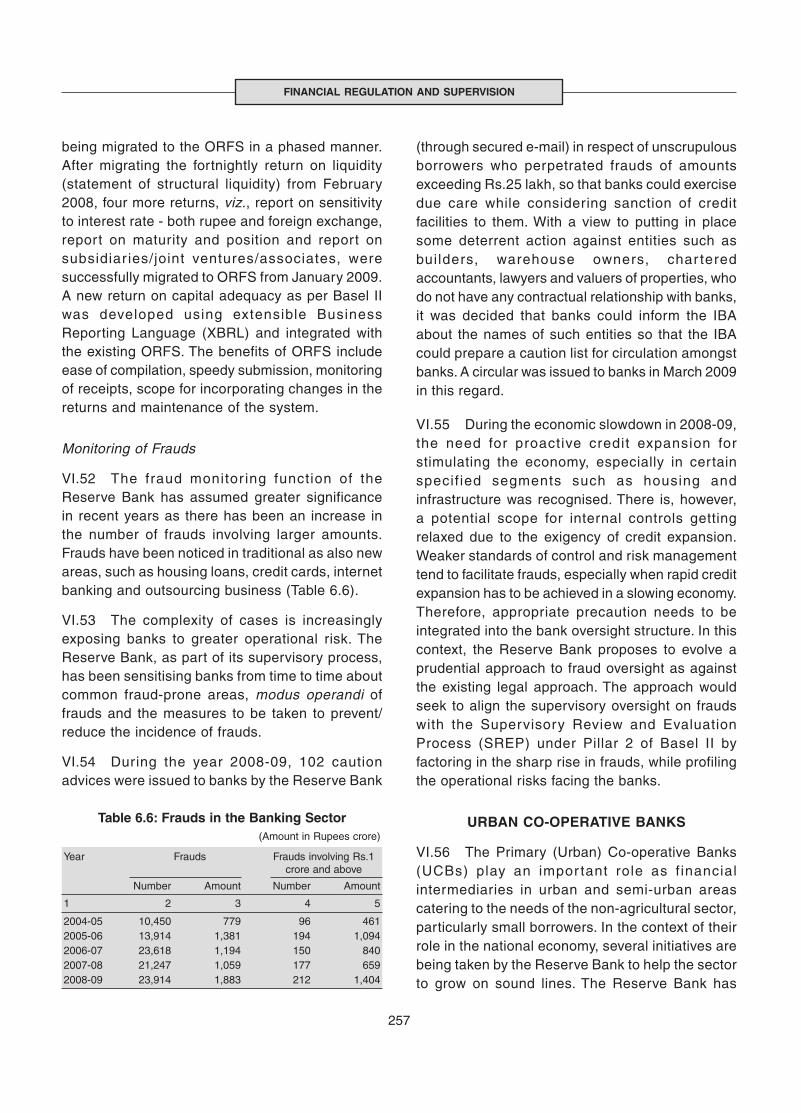

PRINCIPAL OFFICERS

(As on June 30, 2009)

EXECUTIVE DIRECTORS .......................................................... V.K. Sharma.......................................................... C. Krishnan.......................................................... Anand Sinha.......................................................... V.S. Das.......................................................... G. Gopalakrishna.......................................................... H.R. Khan.......................................................... D.K. Mohanty

CENTRAL OFFICEDepartment of Administration and Personnel Management ................ Prabal Sen, Principal Chief General ManagerCustomer Service Department ............................................................. G. Jaganmohan Rao, Chief General ManagerDepartment of Banking Operations and Development ......................... P. Vijaya Bhaskar, Chief General Manager-in-ChargeDepartment of Banking Supervision ..................................................... S. Karuppasamy, Chief General Manager-in-ChargeDepartment of Communication ............................................................. A.I. Killawala, Press Relations Officer (Gr. F)Department of Currency Management ................................................. U.S. Paliwal, Chief General ManagerDepartment of Economic Analysis and Policy ...................................... -Department of Expenditure and Budgetary Control ............................. Deepa Srivastava, Chief General ManagerDepartment of External Investments and Operations .......................... Meena Hemachandra, Chief General Manager-in-ChargeDepartment of Government and Bank Accounts .................................. S.V. Raghavan, Chief General Manager-in-ChargeDepartment of Information Technology ................................................. A.M. Pedgaonkar, Chief General Manager-in-ChargeDepartment of Non-Banking Supervision ............................................. P. Krishnamurthy, Chief General Manager-in-ChargeDepartment of Payment and Settlement Systems ............................... G. Padmanabhan, Chief General ManagerDepartment of Statistics and Information Management ....................... A.K. Ray, Principal AdviserFinancial Markets Department ............................................................. Chandan Sinha, Chief General ManagerForeign Exchange Department ............................................................. Salim Gangadharan, Chief General Manager-in-ChargeHuman Resources Development Department ...................................... Deepak Singhal, Chief General ManagerInspection Department ......................................................................... Karunasagar, Chief General ManagerInternal Debt Management Department ............................................... K.V. Rajan , Chief General ManagerLegal Department ................................................................................. K.D. Zacharias, Legal Adviser-in-ChargeMonetary Policy Department ................................................................ Janak Raj, Adviser-in-ChargePremises Department ........................................................................... S. Venkatachalam, Chief General ManagerRajbhasha Department ......................................................................... Phulan Kumar, Chief General ManagerRural Planning and Credit Department ................................................ -Secretary’s Department ........................................................................ Grace E. Koshie, Chief General Manager & SecretaryUrban Banks Department ..................................................................... A.K. Khound, Chief General Manager

COLLEGES PRINCIPALS/CHIEF GENERAL MANAGERCentre for Advanced Financial Learning, Mumbai ............................... -College of Agricultural Banking, Pune .................................................. Sandip GhoseReserve Bank Staff College, Chennai .................................................. S. Ganesh

OFFICES REGIONAL DIRECTORSChennai ................................................................................................ K. R. AnandaKolkata .................................................................................................. F.R. JosephMumbai ................................................................................................. A.N. RaoNew Delhi ............................................................................................. R. Gandhi

BRANCHESAhmedabad .......................................................................................... A. K. BeraBangalore ............................................................................................. B. SrinivasBhopal ................................................................................................... Rajesh VermaBhubaneswar ........................................................................................ Kaza SudhakarChandigarh ........................................................................................... J. SadakkadullaGuwahati ............................................................................................... Sewali ChoudhuryHyderabad ............................................................................................ N. Krishna MohanJaipur .................................................................................................... B.P. KanungoJammu .................................................................................................. -Kanpur .................................................................................................. J.B. BhoriaLucknow ................................................................................................ D.P.S. RathoreNagpur .................................................................................................. C.C. MitraPatna ..................................................................................................... K.K. VohraThiruvananthapuram ............................................................................. S. Ramaswamy

OFFICERS-IN-CHARGEBelapur ................................................................................................. -Dehradun .............................................................................................. Manoj Sharma, General ManagerKochi ..................................................................................................... E. Madhavan, General ManagerPanaji .................................................................................................... M.A.R. Prabhu, Deputy General ManagerRaipur ................................................................................................... A.K. Sharma, General ManagerRanchi ................................................................................................... Rabi N. Mishra, General ManagerShimla ................................................................................................... S.K. Bal, General Manager

i

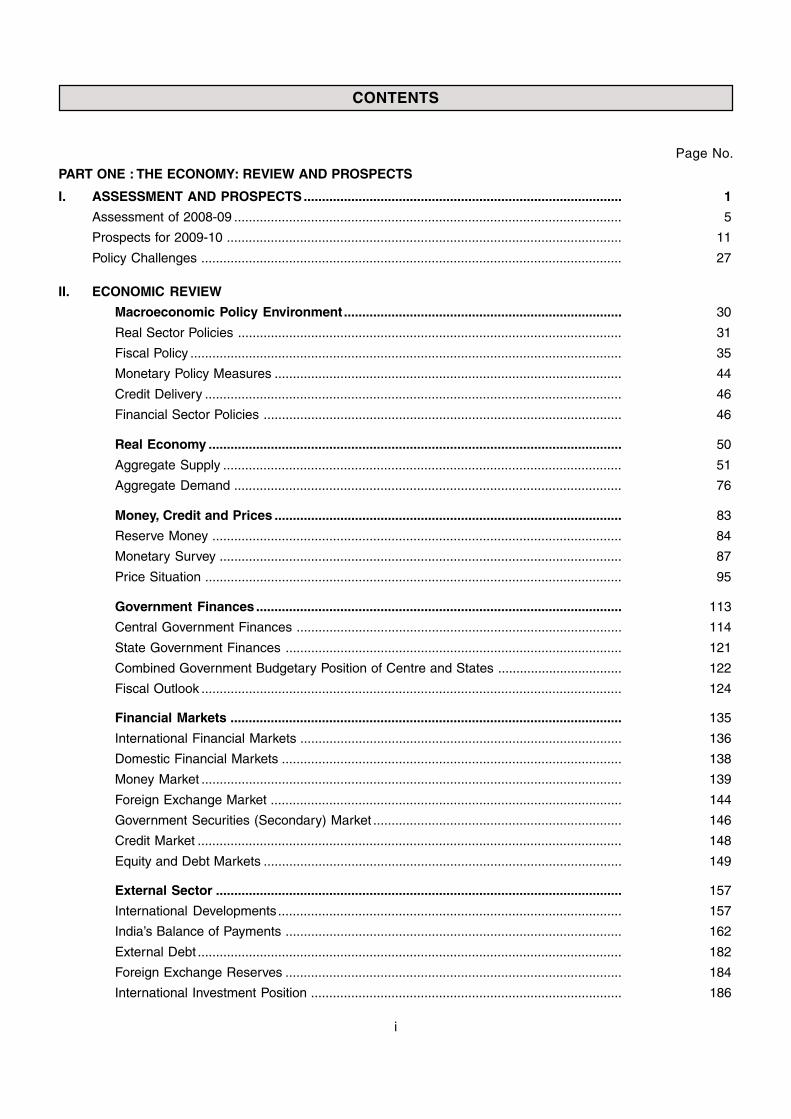

PART ONE : THE ECONOMY: REVIEW AND PROSPECTS

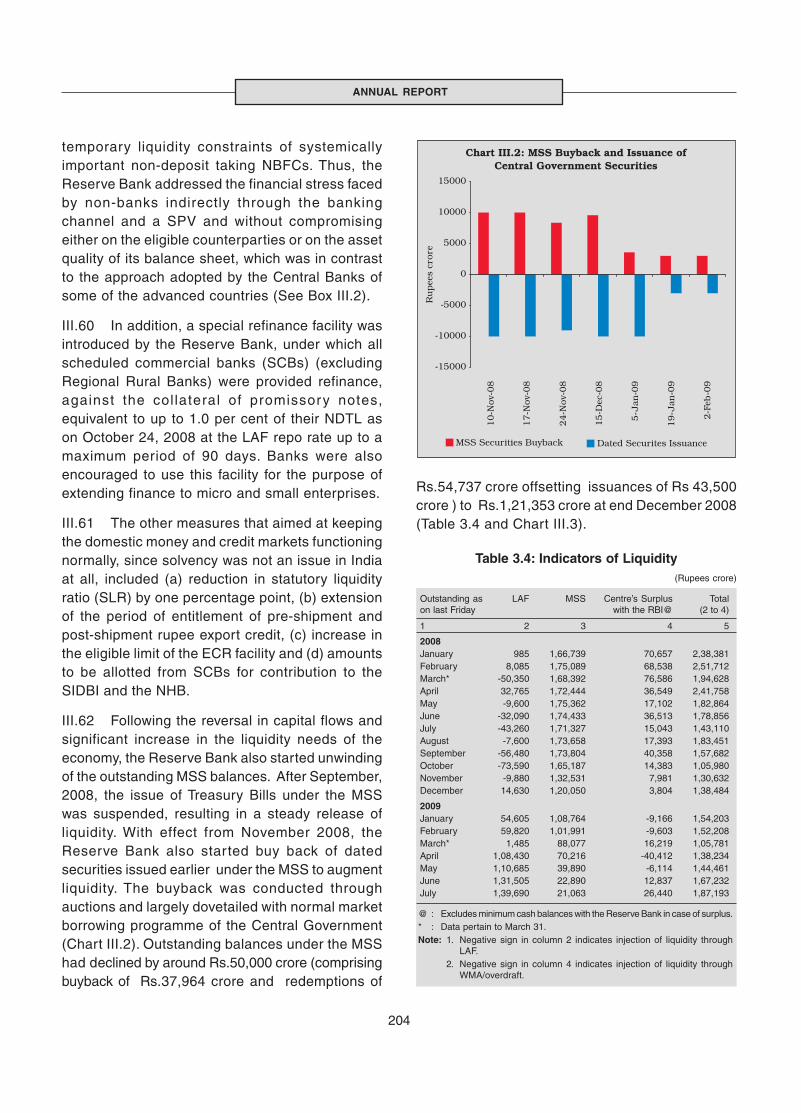

I. ASSESSMENT AND PROSPECTS....................................................................................... 1

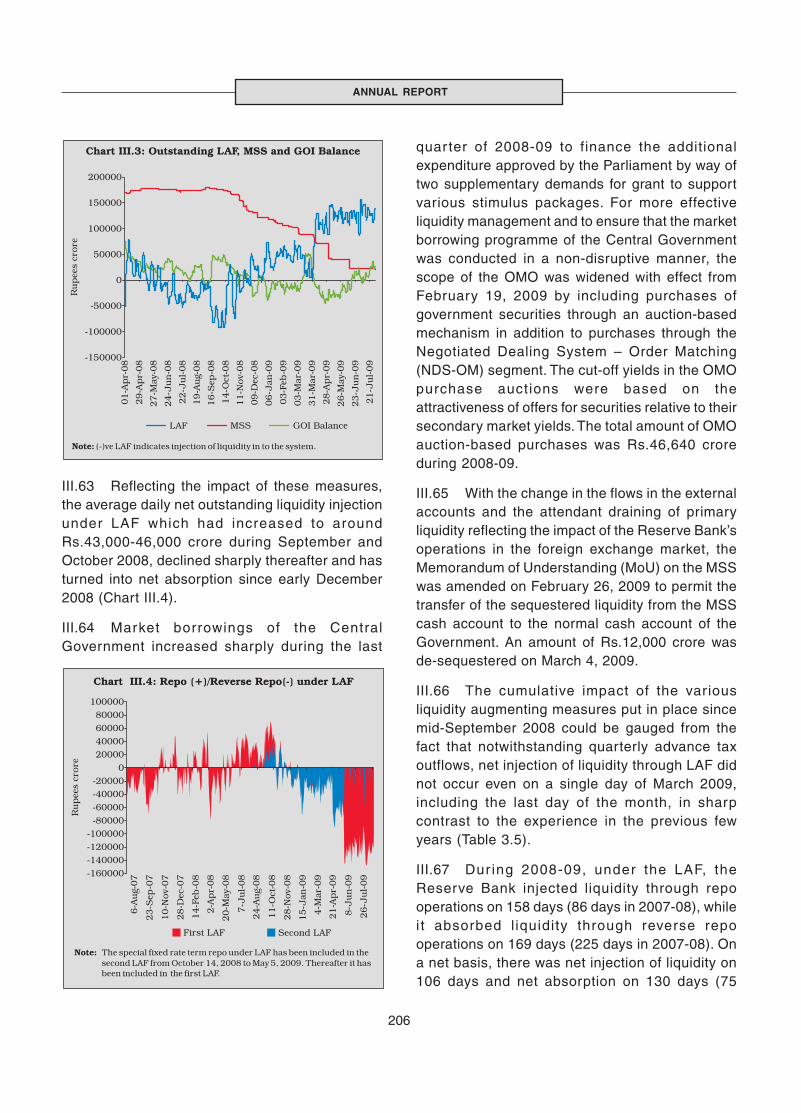

Assessment of 2008-09 .......................................................................................................... 5

Prospects for 2009-10 ............................................................................................................ 11

Policy Challenges ................................................................................................................... 27

II. ECONOMIC REVIEW

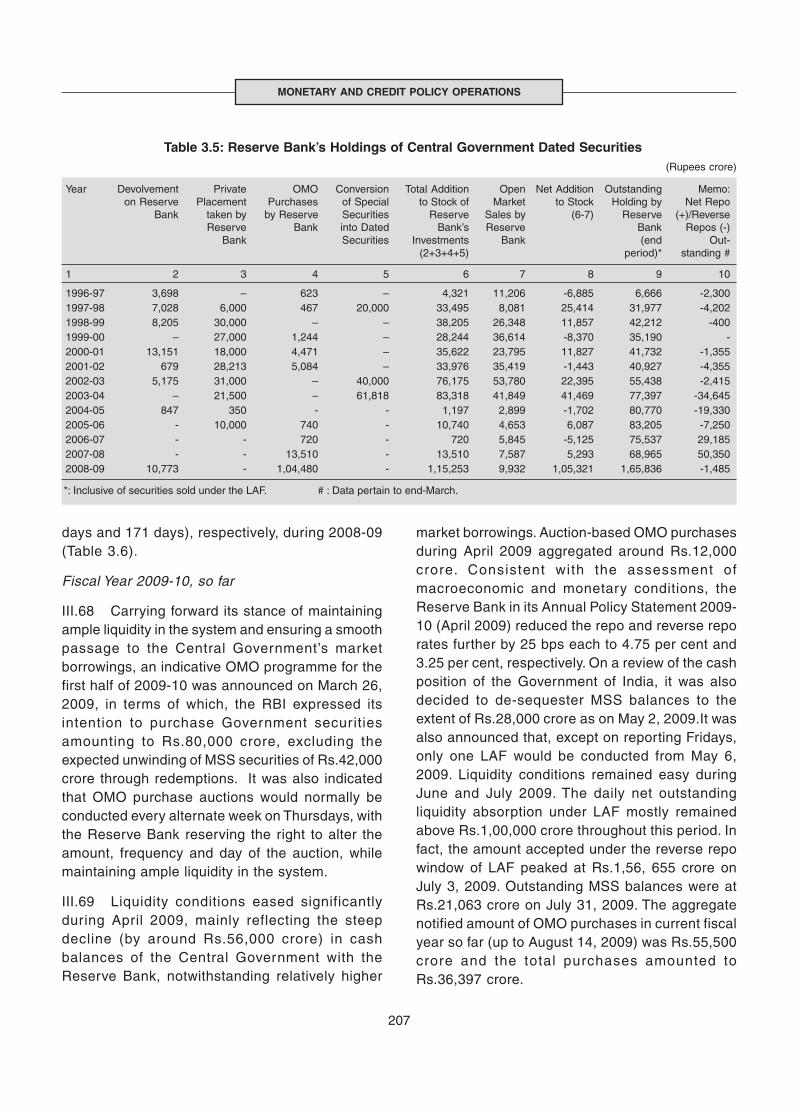

Macroeconomic Policy Environment............................................................................ 30

Real Sector Policies ......................................................................................................... 31

Fiscal Policy ...................................................................................................................... 35

Monetary Policy Measures ............................................................................................... 44

Credit Delivery .................................................................................................................. 46

Financial Sector Policies .................................................................................................. 46

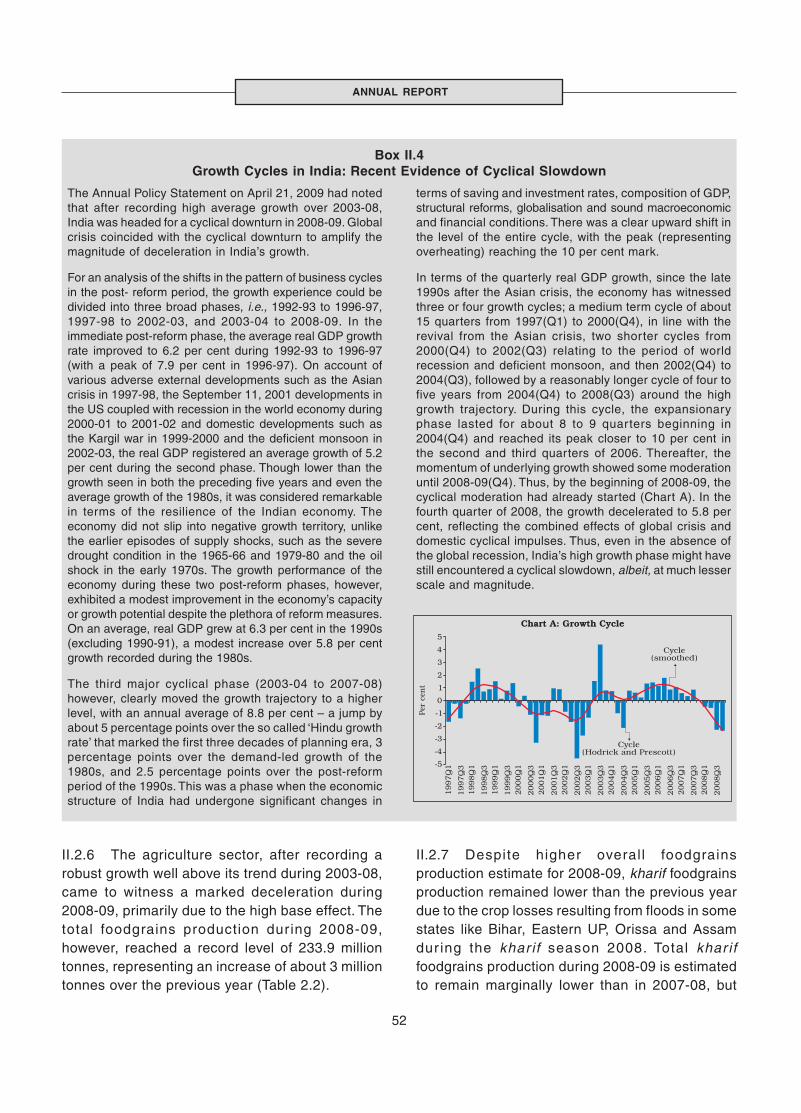

Real Economy ................................................................................................................. 50

Aggregate Supply ............................................................................................................. 51

Aggregate Demand .......................................................................................................... 76

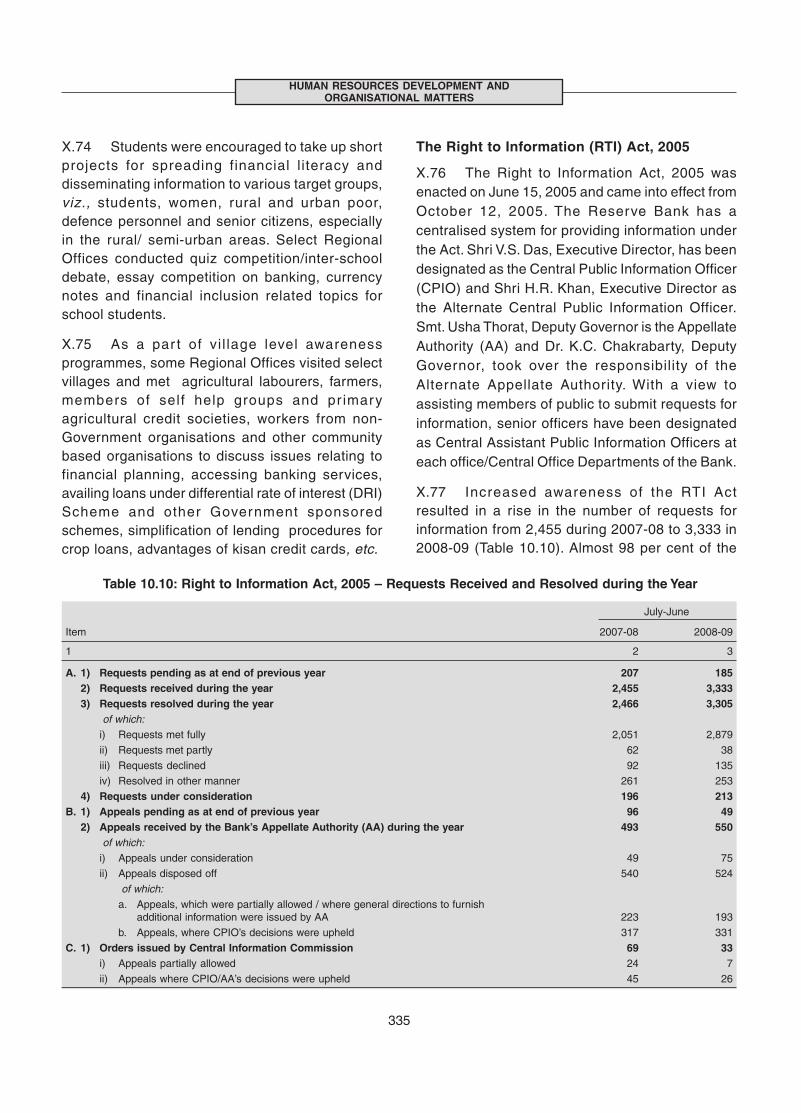

Money, Credit and Prices ............................................................................................... 83

Reserve Money ................................................................................................................ 84

Monetary Survey .............................................................................................................. 87

Price Situation .................................................................................................................. 95

Government Finances .................................................................................................... 113

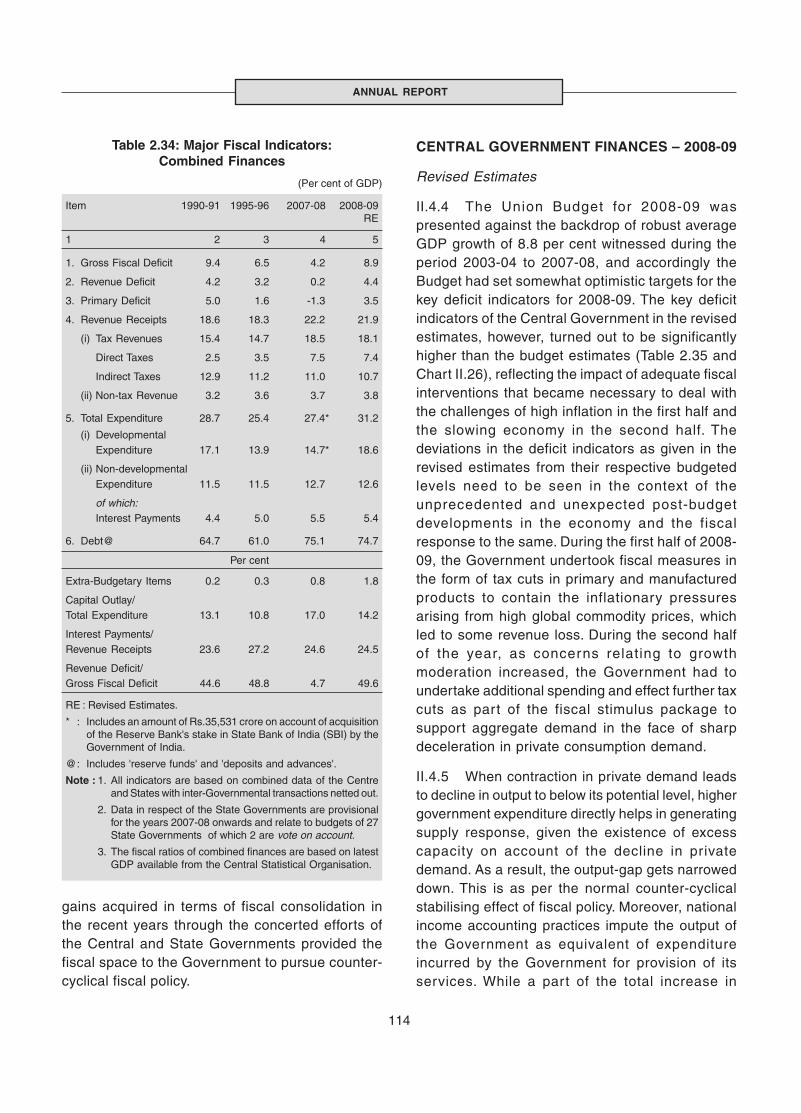

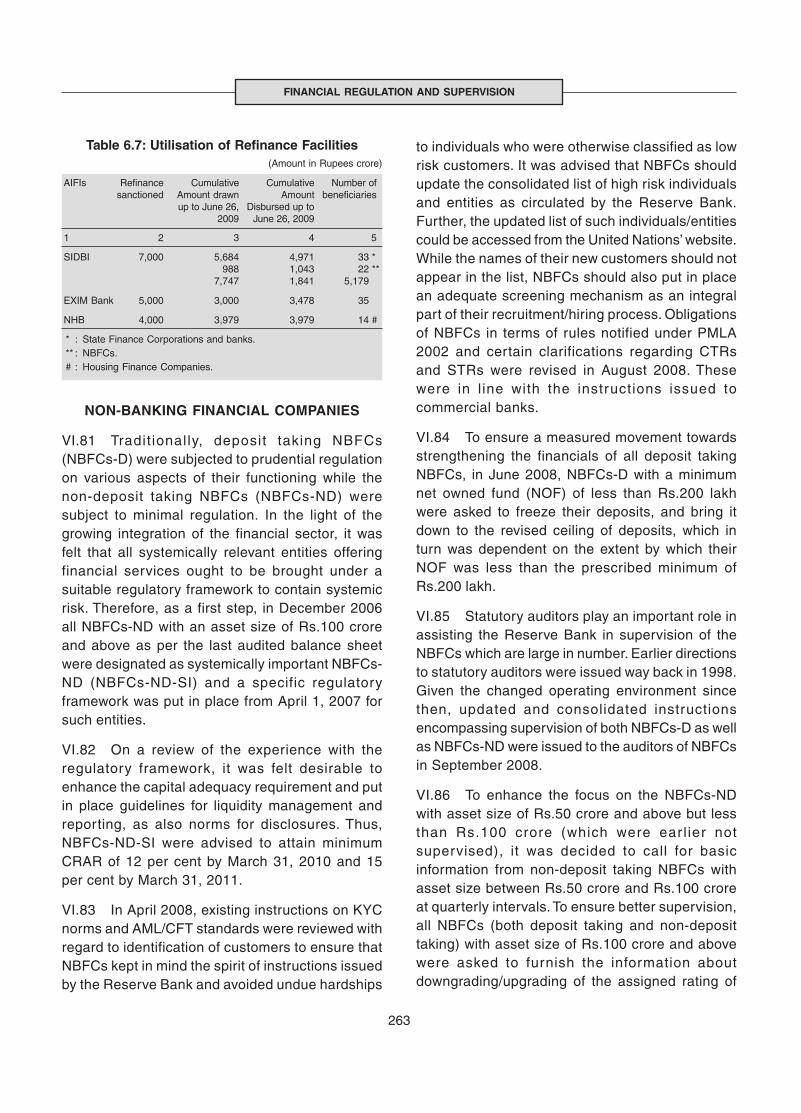

Central Government Finances ......................................................................................... 114

State Government Finances ............................................................................................ 121

Combined Government Budgetary Position of Centre and States .................................. 122

Fiscal Outlook ................................................................................................................... 124

Financial Markets ........................................................................................................... 135

International Financial Markets ........................................................................................ 136

Domestic Financial Markets ............................................................................................. 138

Money Market ................................................................................................................... 139

Foreign Exchange Market ................................................................................................ 144

Government Securities (Secondary) Market .................................................................... 146

Credit Market .................................................................................................................... 148

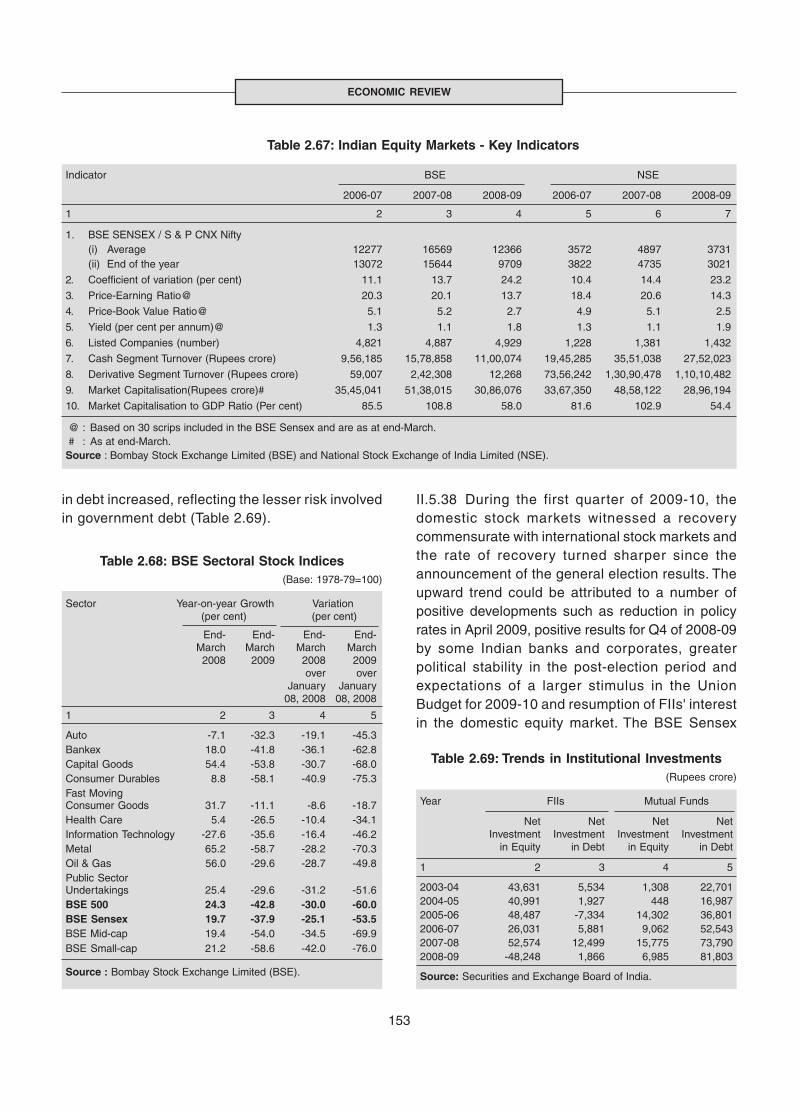

Equity and Debt Markets .................................................................................................. 149

External Sector ............................................................................................................... 157

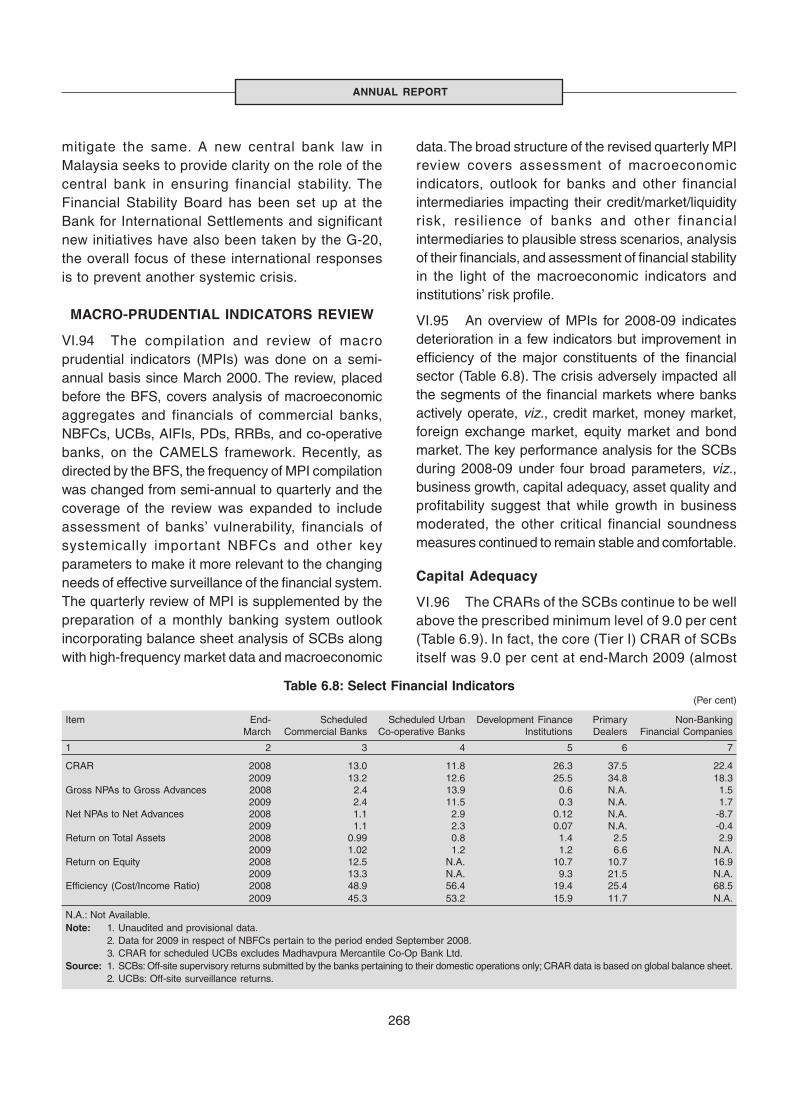

International Developments.............................................................................................. 157

India’s Balance of Payments ............................................................................................ 162

External Debt .................................................................................................................... 182

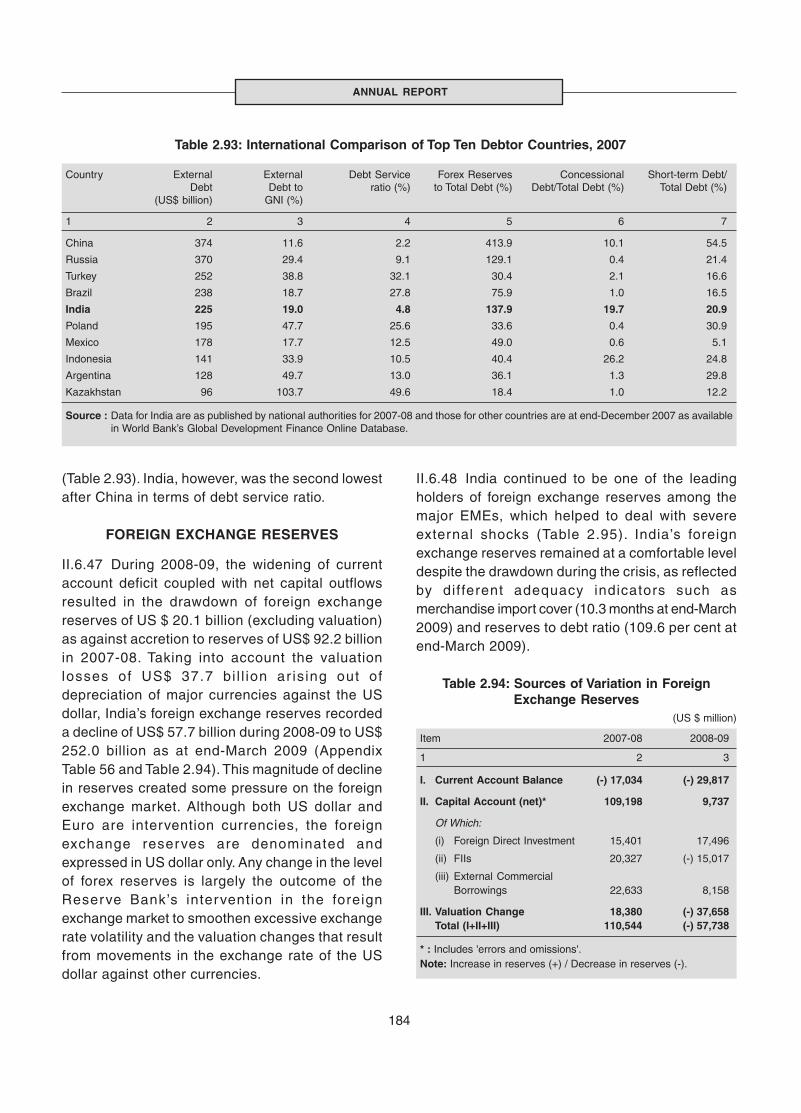

Foreign Exchange Reserves ............................................................................................ 184

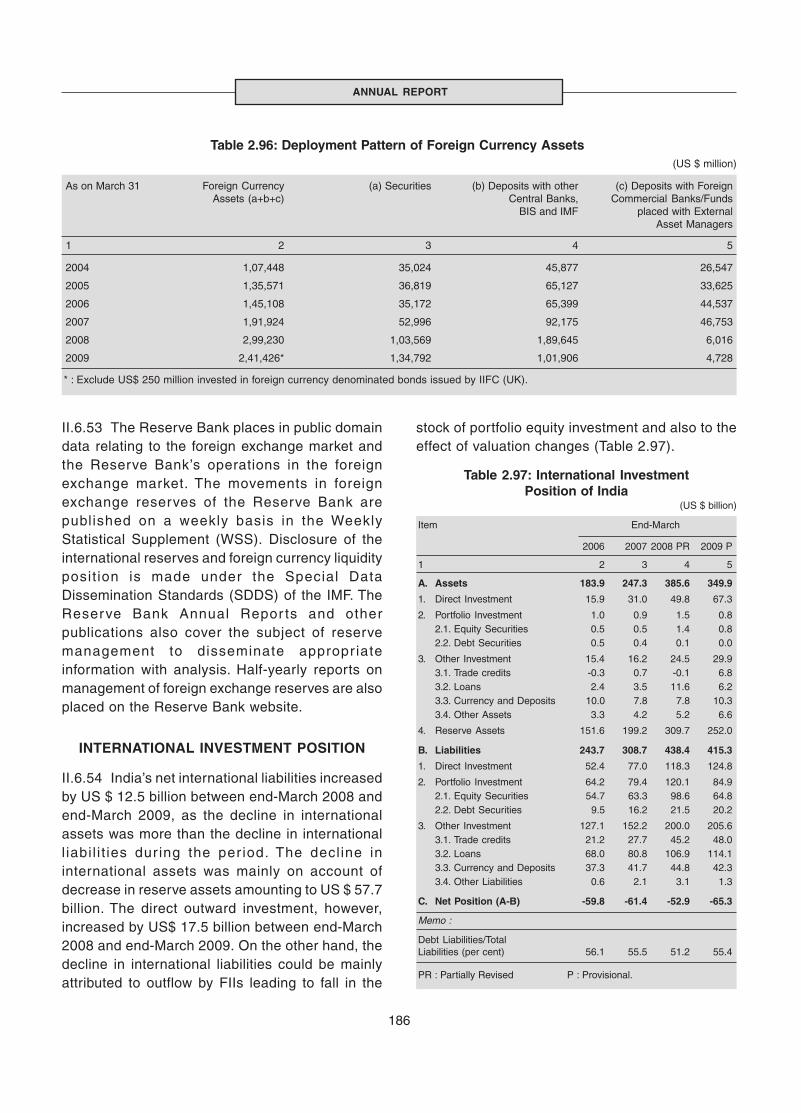

International Investment Position ..................................................................................... 186

CONTENTS

Page No.

ii

PART TWO: THE WORKING AND OPERATIONS OF THE RESERVE BANK OF INDIA

III. MONETARY POLICY OPERATIONS .................................................................................... 188

Monetary Policy Operations: 2008-09 .................................................................................... 189

Monetary Policy Operations: 2009-10 .................................................................................... 196

Liquidity Management ............................................................................................................ 201

IV. CREDIT DELIVERY ............................................................................................................... 210

Priority Sector Lending ........................................................................................................... 211

Micro Finance ......................................................................................................................... 221

Financial Inclusion .................................................................................................................. 222

Financial Literacy and Credit Counselling .............................................................................. 226

Export Credit ........................................................................................................................... 227

Extension of Collateral Facility – Savings Bonds ................................................................... 229

Non-banking Financial Companies ........................................................................................ 229

Scheduled Commercial Banks ............................................................................................... 230

V. DEVELOPMENT AND REGULATION OF FINANCIAL MARKETS ..................................... 231

Money Market ......................................................................................................................... 232

Government Securities Market ............................................................................................... 233

Foreign Exchange Market ...................................................................................................... 235

VI. FINANCIAL REGULATION AND SUPERVISION ................................................................. 241

Regulatory Framework for the Indian Financial System ........................................................ 243

Committee on Financial Sector Assessment ......................................................................... 245

Commercial Banks ................................................................................................................. 247

Urban Co-operative Banks ..................................................................................................... 257

Rural Co-operatives ................................................................................................................ 259

Regional Rural Banks ............................................................................................................. 260

All India Financial Institutions (AIFIs) ..................................................................................... 262

Non-Banking Financial Companies ........................................................................................ 263

Deposit Insurance and Credit Guarantee Corporation of India .............................................. 266

Macro-Prudential Indicators Review....................................................................................... 268

VII. PUBLIC DEBT MANAGEMENT ............................................................................................ 276

Central Government ............................................................................................................... 277

State Governments ................................................................................................................. 286

VIII. CURRENCY MANAGEMENT ................................................................................................ 293

Banknotes in Circulation ......................................................................................................... 293

Coins in Circulation ................................................................................................................. 294

Currency Operations .............................................................................................................. 295

Page No.

CONTENTS

iii

IX. PAYMENT AND SETTLEMENT SYSTEMS AND INFORMATION TECHNOLOGY ............ 302

Payment and Settlement Systems ......................................................................................... 302

Developments in Payments and Settlement Systems ............................................................ 304

Developments in Use of Information Technology ................................................................... 312

X. HUMAN RESOURCES DEVELOPMENT AND ORGANISATIONAL MATTERS ................ 316

Human Resource Initiatives.................................................................................................... 316

Other Initiatives ....................................................................................................................... 321

Research Activities ................................................................................................................. 337

Central Board and its Committees ......................................................................................... 345

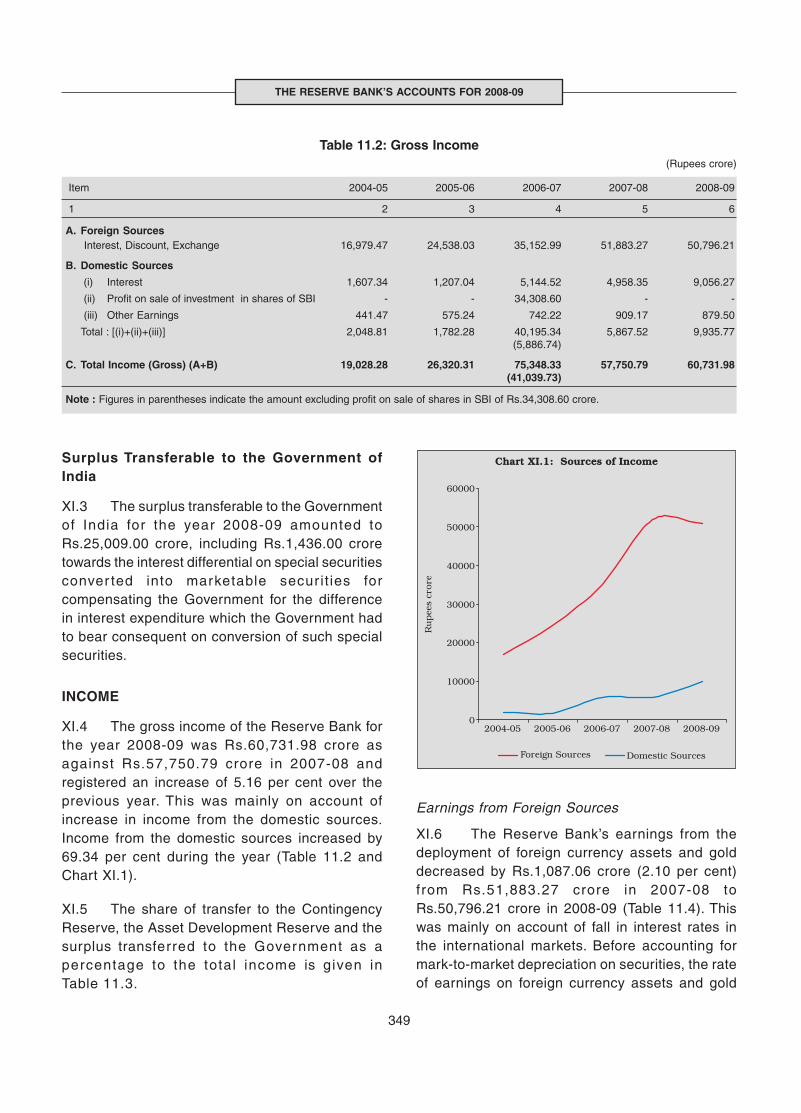

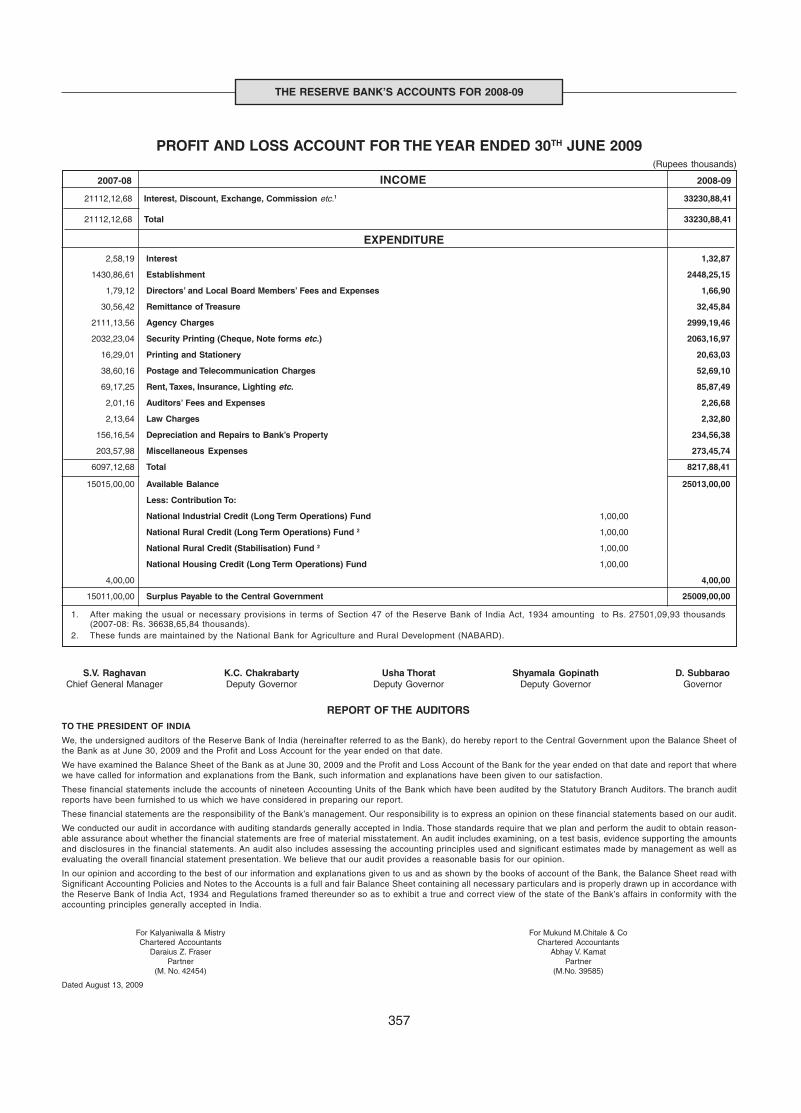

XI. THE RESERVE BANK’S ACCOUNTS FOR 2008-09 ........................................................... 348

Income and Expenditure......................................................................................................... 348

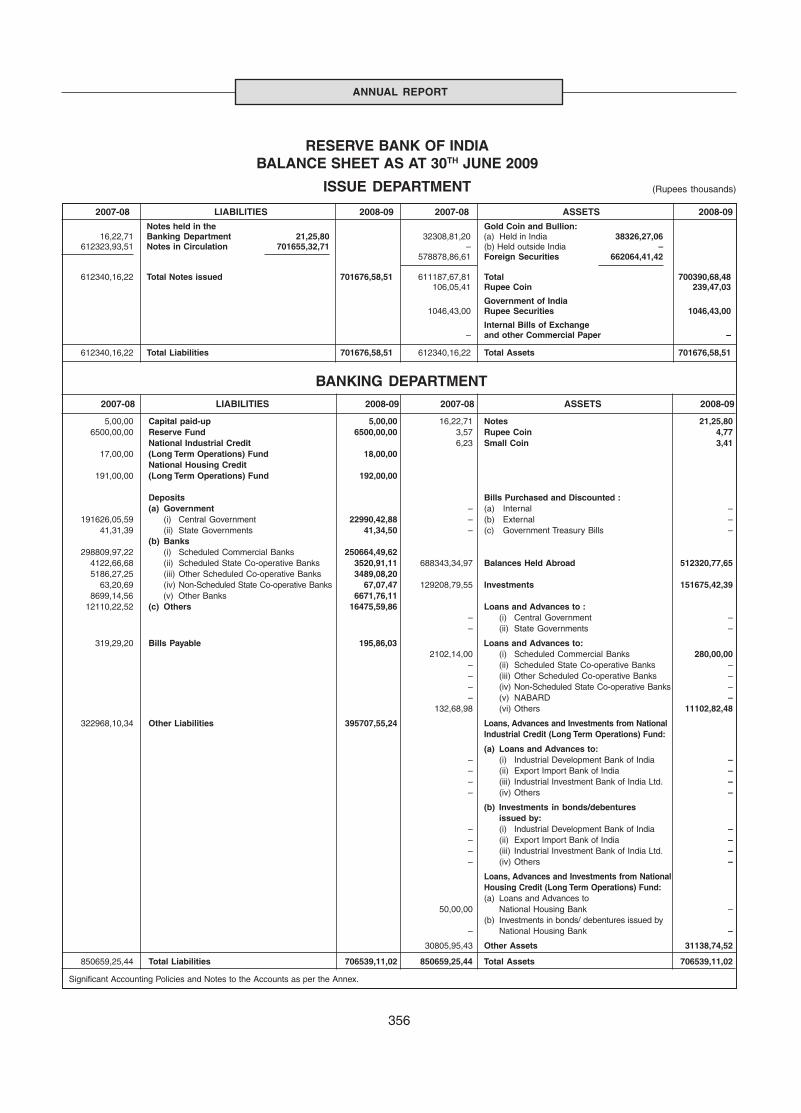

Balance Sheet ........................................................................................................................ 352

Significant Accounting Policies and Notes to the Accounts for 2008-09 ................................ 358

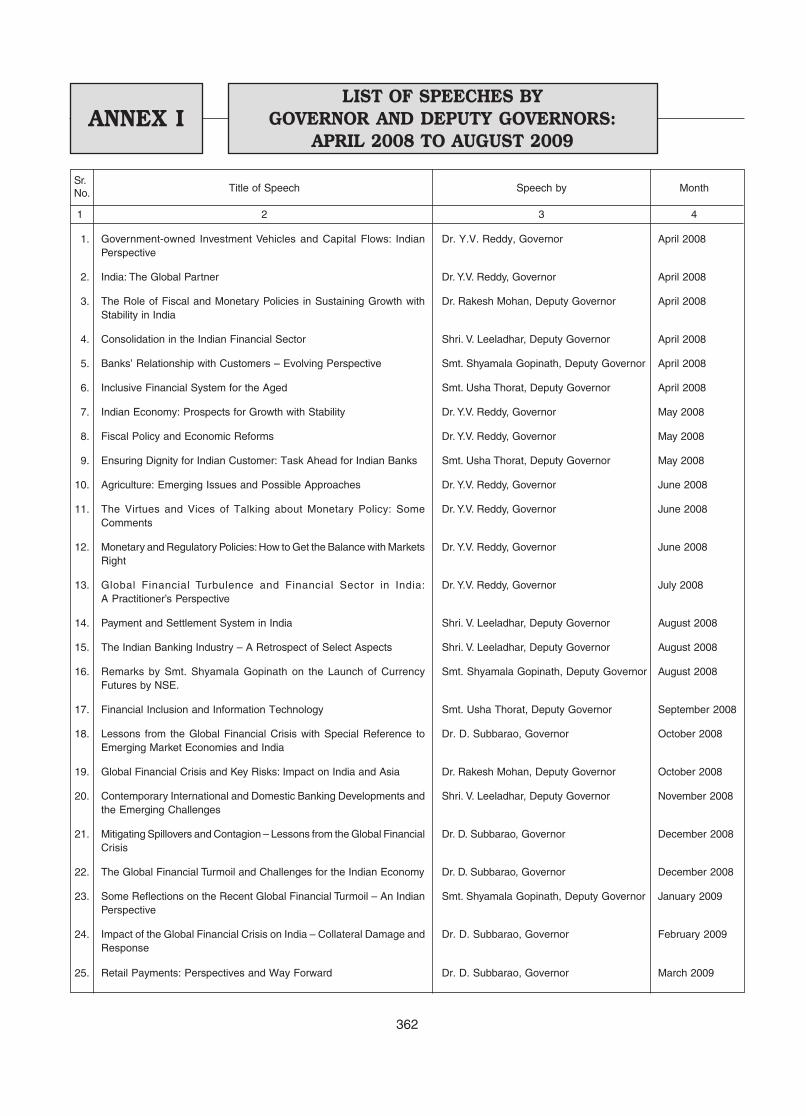

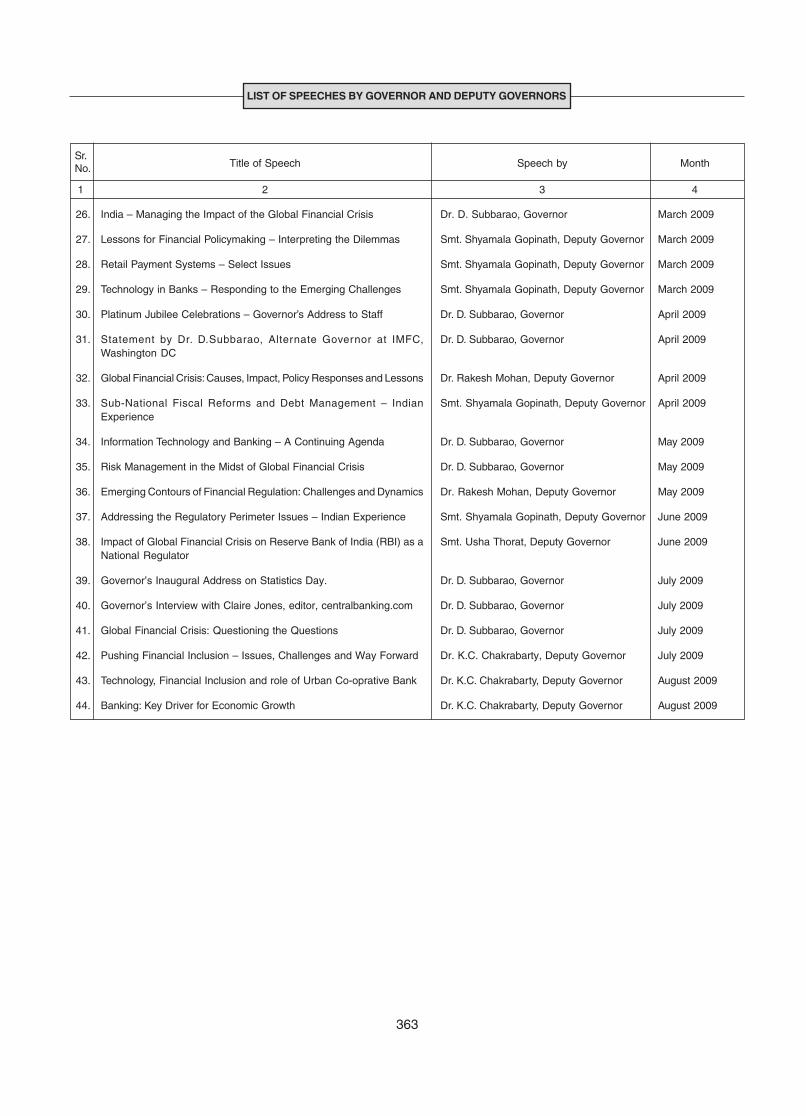

Annex I : List of Speeches by Governor and Deputy Governors ................................ 362

Annex II : List of Reports of Groups/Committees ......................................................... 364

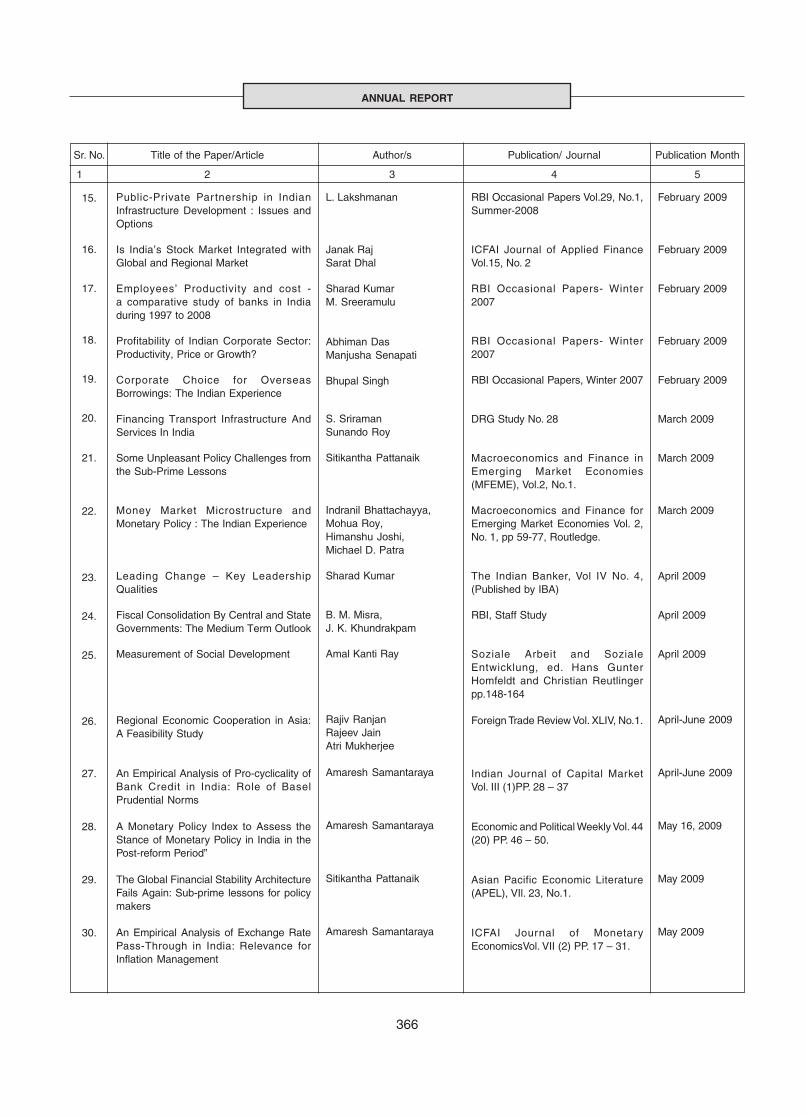

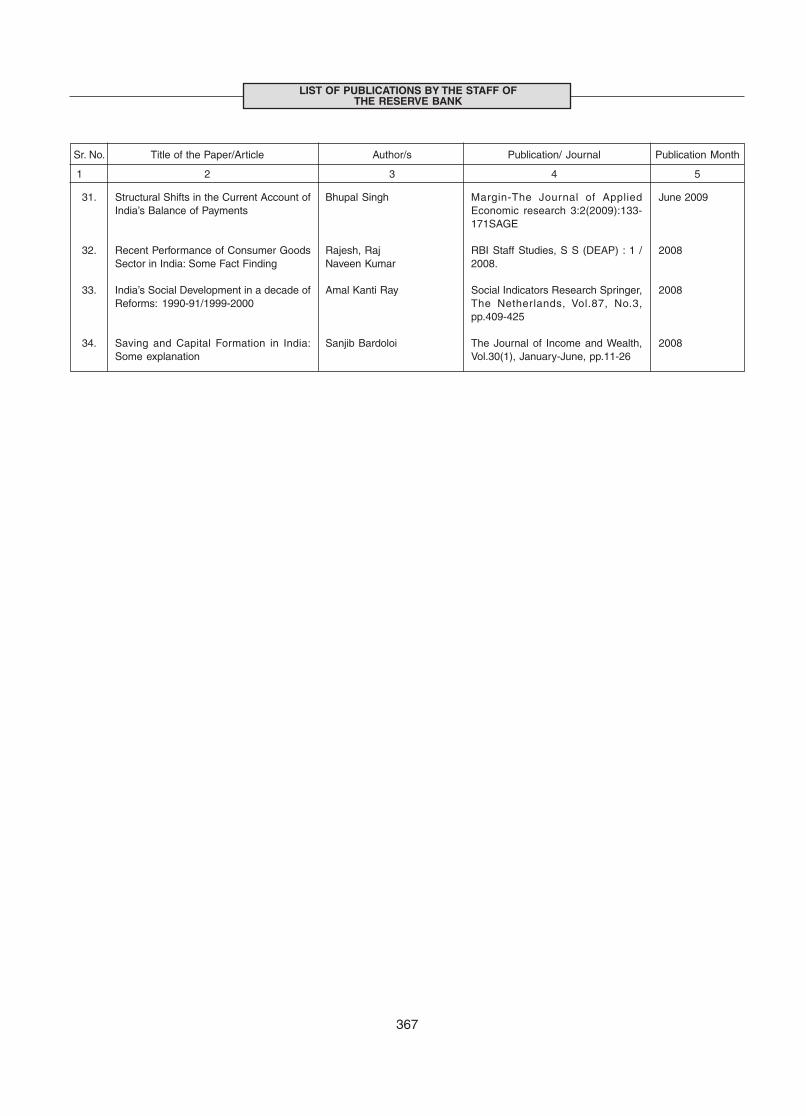

Annex III : List of Publications by the Staff of the Reserve Bank:June 2008 to July 2009 .................................................................................... 365

Annex IV : Visits of Foreign Delegations to The Reserve Bank .................................... 368

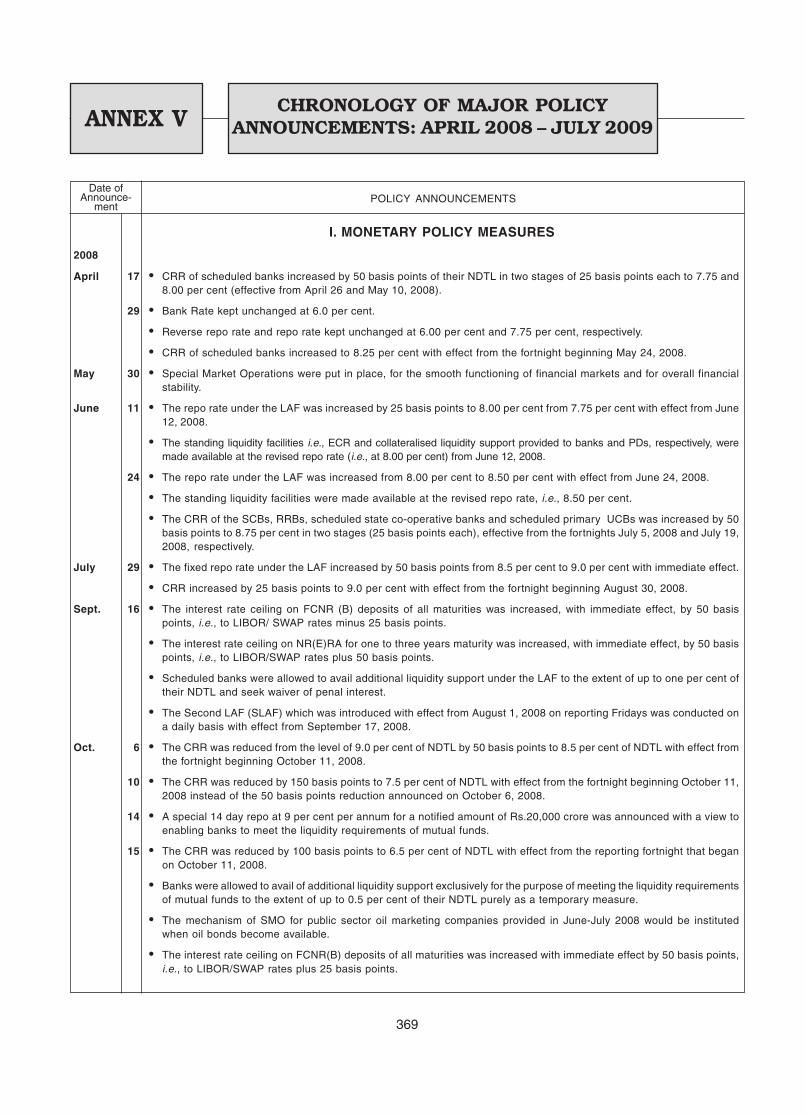

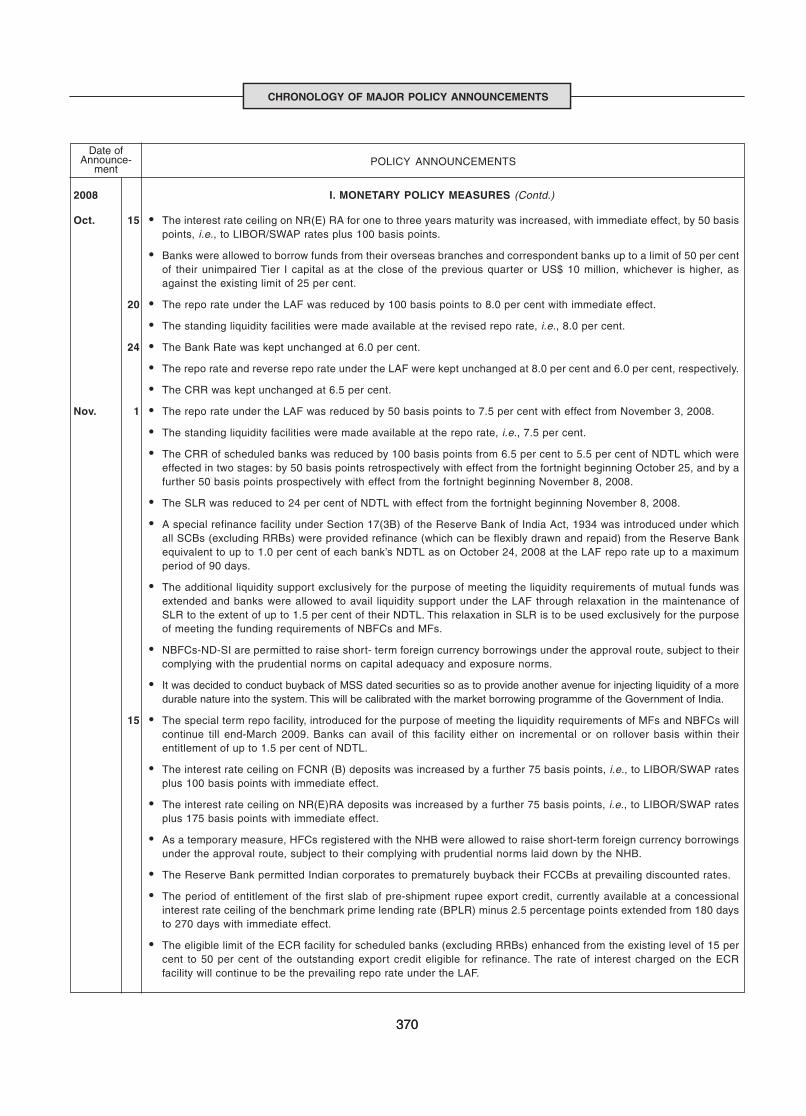

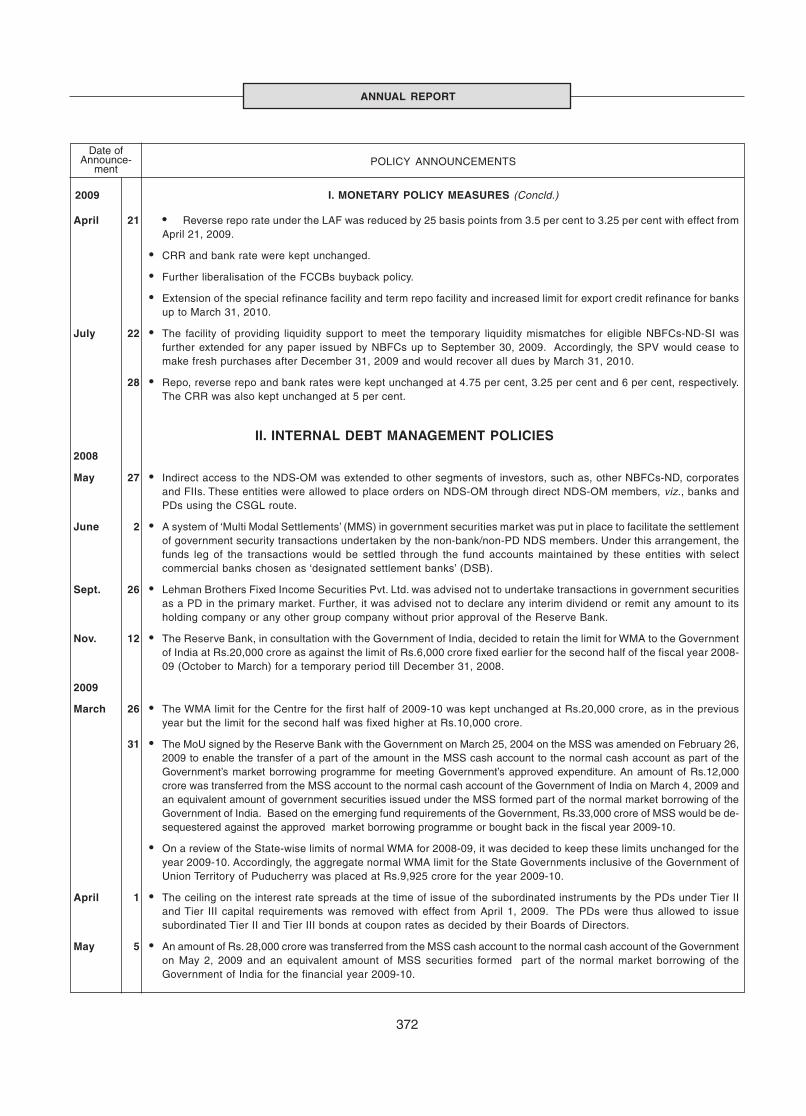

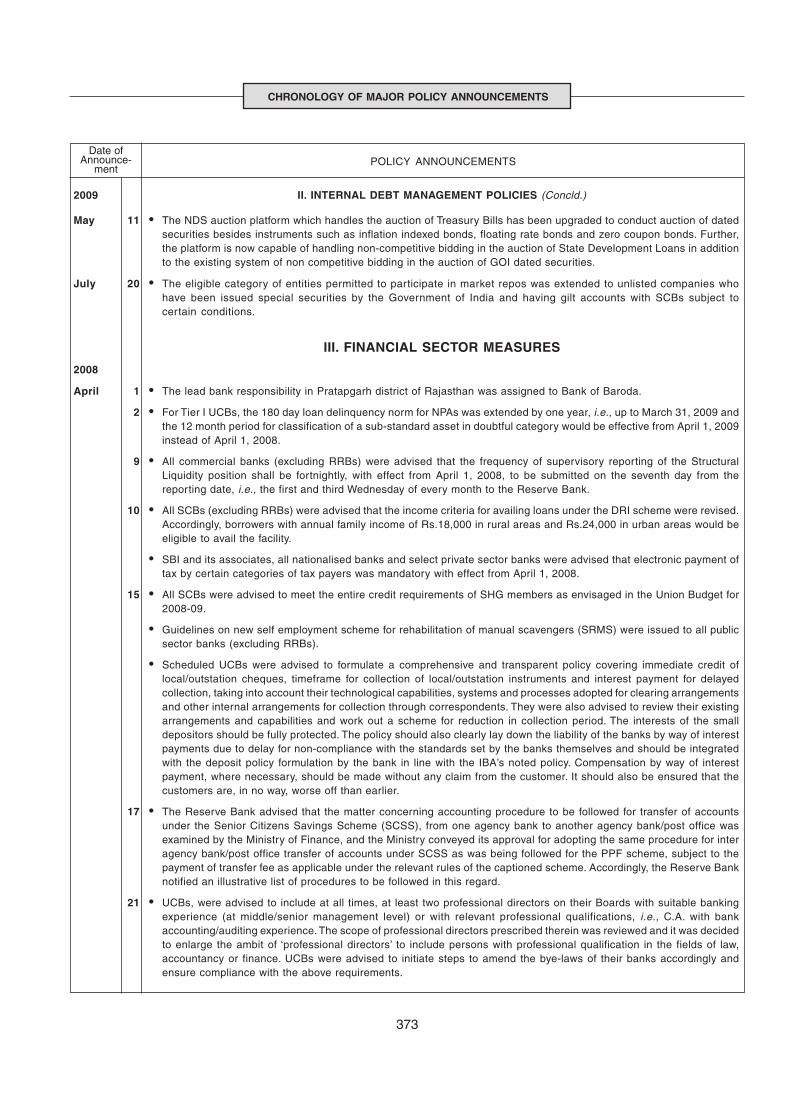

Annex V : Chronology of Major Policy Announcements: April 2008-July 2009 .......... 369

BOXES

II.1 Counter-Cyclical Fiscal Policy in the Current Economic Scenario ................................... 37

II.2 Fiscal Transparency at the State Level ............................................................................ 42

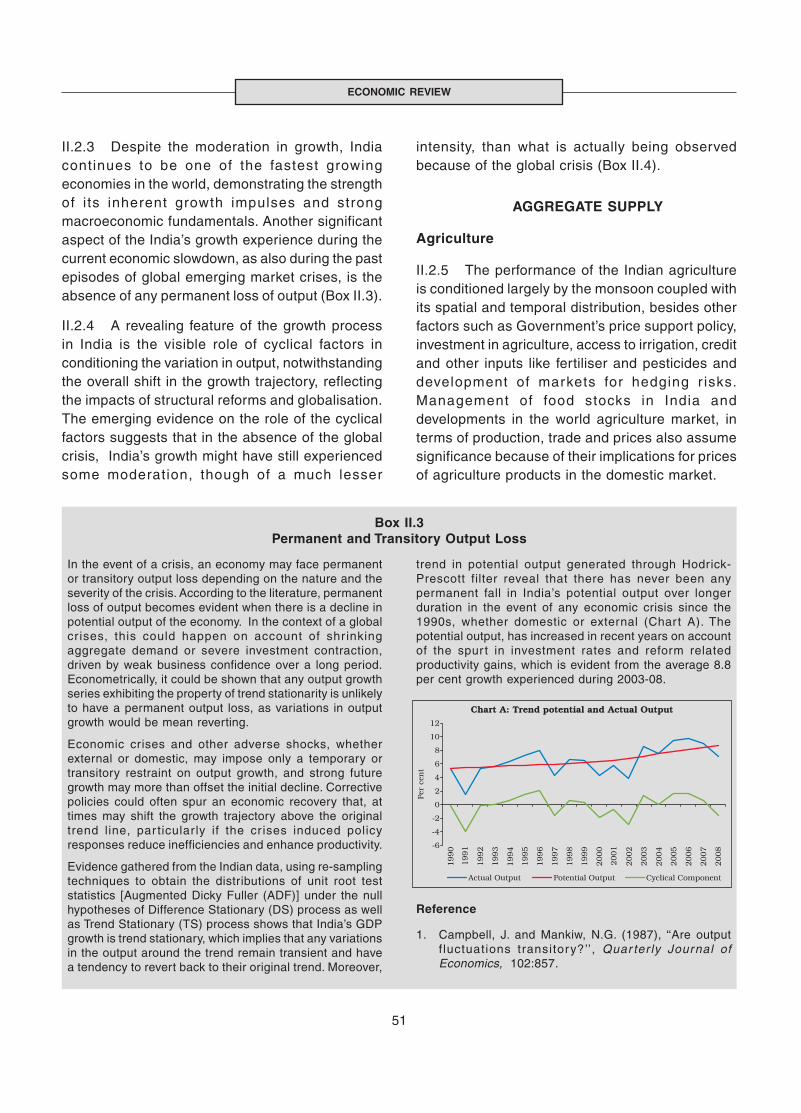

II.3 Permanent and Transitory Output Loss ............................................................................ 51

II.4 Growth Cycles in India: Recent Evidence of Cyclical Slowdown ..................................... 52

II.5 Rationalisation of MSP Computation ............................................................................... 56

II.6 Global Agricultural Outlook .............................................................................................. 60

II.7 Global Climate Change: Emerging Challenges for Indian Agriculture ............................. 62

II.8 Performance of the Electricity Sector ............................................................................... 68

II.9 Industrial Performance – Select Economies .................................................................... 71

II.10 Global Recession and the Services Sector ..................................................................... 73

II.11 Effects of Global Recession on Unemployment in India .................................................. 75

II.12 Financial Crisis and Economic Growth: An Inter-temporal Perspective ........................... 78

II.13 The Management of Economic Slowdown: Rebalancing of Growth ................................ 79

II.14 Report of the High Level Committee on Estimation of Saving andInvestment ........................................................................................................................ 81

Page No.

CONTENTS

iv

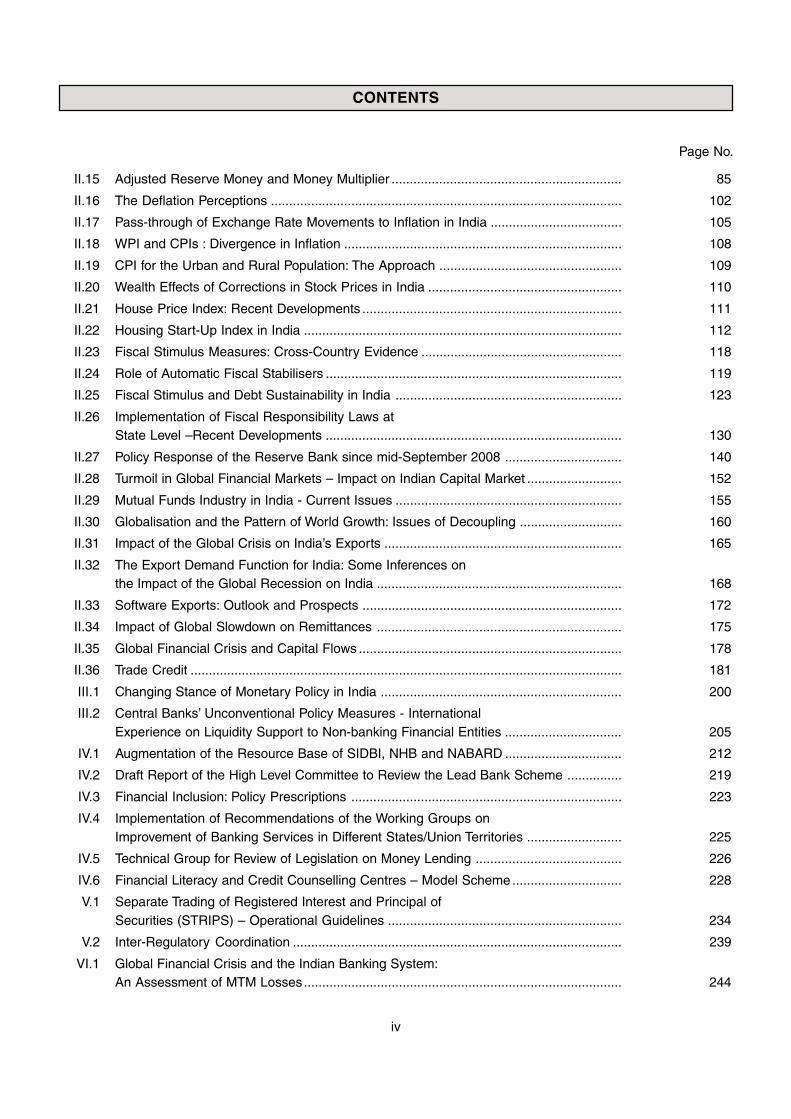

II.15 Adjusted Reserve Money and Money Multiplier ............................................................... 85

II.16 The Deflation Perceptions ................................................................................................ 102

II.17 Pass-through of Exchange Rate Movements to Inflation in India .................................... 105

II.18 WPI and CPIs : Divergence in Inflation ............................................................................ 108

II.19 CPI for the Urban and Rural Population: The Approach .................................................. 109

II.20 Wealth Effects of Corrections in Stock Prices in India ..................................................... 110

II.21 House Price Index: Recent Developments ....................................................................... 111

II.22 Housing Start-Up Index in India ....................................................................................... 112

II.23 Fiscal Stimulus Measures: Cross-Country Evidence ....................................................... 118

II.24 Role of Automatic Fiscal Stabilisers ................................................................................. 119

II.25 Fiscal Stimulus and Debt Sustainability in India .............................................................. 123

II.26 Implementation of Fiscal Responsibility Laws atState Level –Recent Developments ................................................................................. 130

II.27 Policy Response of the Reserve Bank since mid-September 2008 ................................ 140

II.28 Turmoil in Global Financial Markets – Impact on Indian Capital Market .......................... 152

II.29 Mutual Funds Industry in India - Current Issues .............................................................. 155

II.30 Globalisation and the Pattern of World Growth: Issues of Decoupling ............................ 160

II.31 Impact of the Global Crisis on India’s Exports ................................................................. 165

II.32 The Export Demand Function for India: Some Inferences onthe Impact of the Global Recession on India ................................................................... 168

II.33 Software Exports: Outlook and Prospects ....................................................................... 172

II.34 Impact of Global Slowdown on Remittances ................................................................... 175

II.35 Global Financial Crisis and Capital Flows ........................................................................ 178

II.36 Trade Credit ...................................................................................................................... 181

III.1 Changing Stance of Monetary Policy in India .................................................................. 200

III.2 Central Banks’ Unconventional Policy Measures - InternationalExperience on Liquidity Support to Non-banking Financial Entities ................................ 205

IV.1 Augmentation of the Resource Base of SIDBI, NHB and NABARD ................................ 212

IV.2 Draft Report of the High Level Committee to Review the Lead Bank Scheme ............... 219

IV.3 Financial Inclusion: Policy Prescriptions .......................................................................... 223

IV.4 Implementation of Recommendations of the Working Groups onImprovement of Banking Services in Different States/Union Territories .......................... 225

IV.5 Technical Group for Review of Legislation on Money Lending ........................................ 226

IV.6 Financial Literacy and Credit Counselling Centres – Model Scheme.............................. 228

V.1 Separate Trading of Registered Interest and Principal ofSecurities (STRIPS) – Operational Guidelines ................................................................ 234

V.2 Inter-Regulatory Coordination .......................................................................................... 239

VI.1 Global Financial Crisis and the Indian Banking System:An Assessment of MTM Losses....................................................................................... 244

Page No.

CONTENTS

v

Page No.

CONTENTS

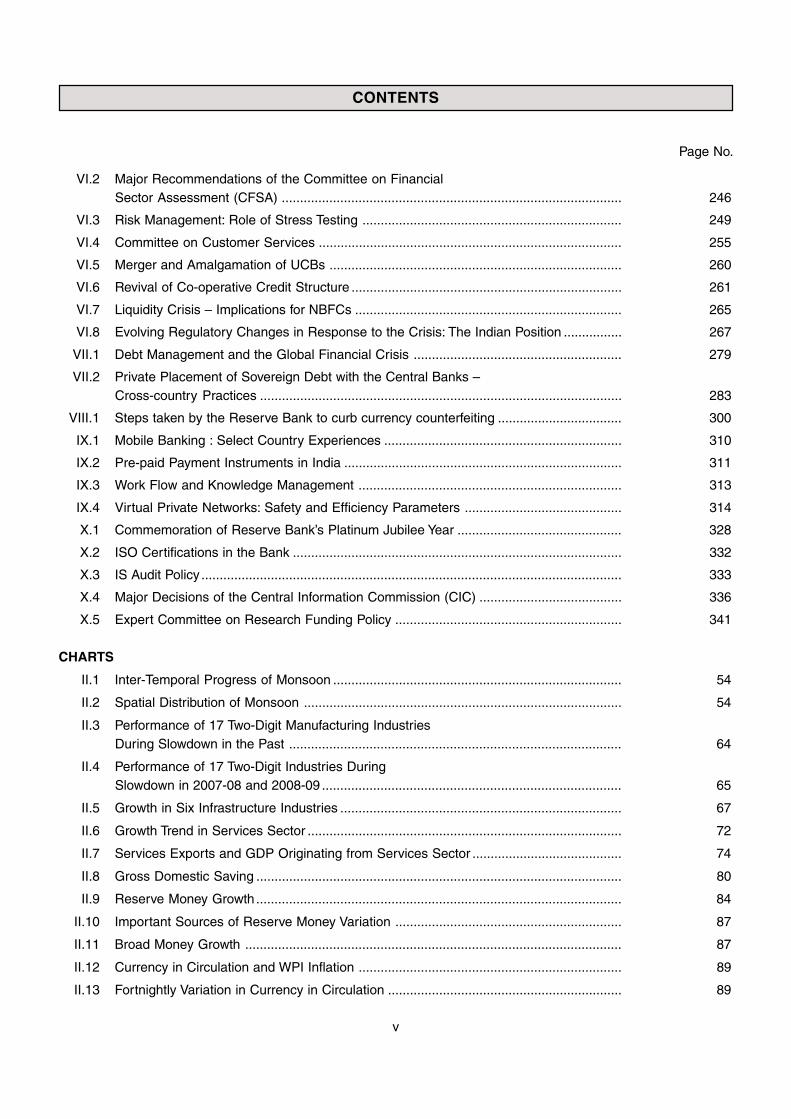

VI.2 Major Recommendations of the Committee on FinancialSector Assessment (CFSA) ............................................................................................. 246

VI.3 Risk Management: Role of Stress Testing ....................................................................... 249

VI.4 Committee on Customer Services ................................................................................... 255

VI.5 Merger and Amalgamation of UCBs ................................................................................ 260

VI.6 Revival of Co-operative Credit Structure .......................................................................... 261

VI.7 Liquidity Crisis – Implications for NBFCs ......................................................................... 265

VI.8 Evolving Regulatory Changes in Response to the Crisis: The Indian Position ................ 267

VII.1 Debt Management and the Global Financial Crisis ......................................................... 279

VII.2 Private Placement of Sovereign Debt with the Central Banks –Cross-country Practices ................................................................................................... 283

VIII.1 Steps taken by the Reserve Bank to curb currency counterfeiting .................................. 300

IX.1 Mobile Banking : Select Country Experiences ................................................................. 310

IX.2 Pre-paid Payment Instruments in India ............................................................................ 311

IX.3 Work Flow and Knowledge Management ........................................................................ 313

IX.4 Virtual Private Networks: Safety and Efficiency Parameters ........................................... 314

X.1 Commemoration of Reserve Bank’s Platinum Jubilee Year ............................................. 328

X.2 ISO Certifications in the Bank .......................................................................................... 332

X.3 IS Audit Policy ................................................................................................................... 333

X.4 Major Decisions of the Central Information Commission (CIC) ....................................... 336

X.5 Expert Committee on Research Funding Policy .............................................................. 341

CHARTS

II.1 Inter-Temporal Progress of Monsoon ............................................................................... 54

II.2 Spatial Distribution of Monsoon ....................................................................................... 54

II.3 Performance of 17 Two-Digit Manufacturing IndustriesDuring Slowdown in the Past ........................................................................................... 64

II.4 Performance of 17 Two-Digit Industries DuringSlowdown in 2007-08 and 2008-09 .................................................................................. 65

II.5 Growth in Six Infrastructure Industries ............................................................................. 67

II.6 Growth Trend in Services Sector ...................................................................................... 72

II.7 Services Exports and GDP Originating from Services Sector ......................................... 74

II.8 Gross Domestic Saving .................................................................................................... 80

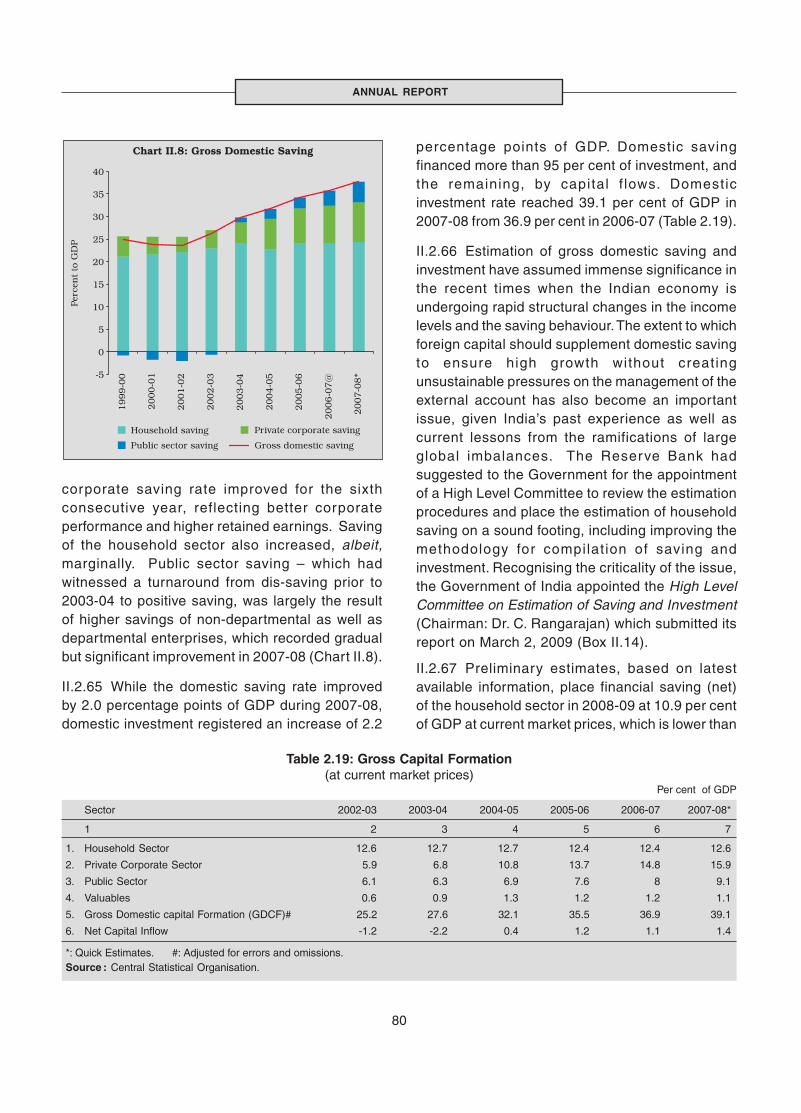

II.9 Reserve Money Growth .................................................................................................... 84

II.10 Important Sources of Reserve Money Variation .............................................................. 87

II.11 Broad Money Growth ....................................................................................................... 87

II.12 Currency in Circulation and WPI Inflation ........................................................................ 89

II.13 Fortnightly Variation in Currency in Circulation ................................................................ 89

vi

Page No.

CONTENTS

II.14 Time Deposits Growth Rates ........................................................................................... 89

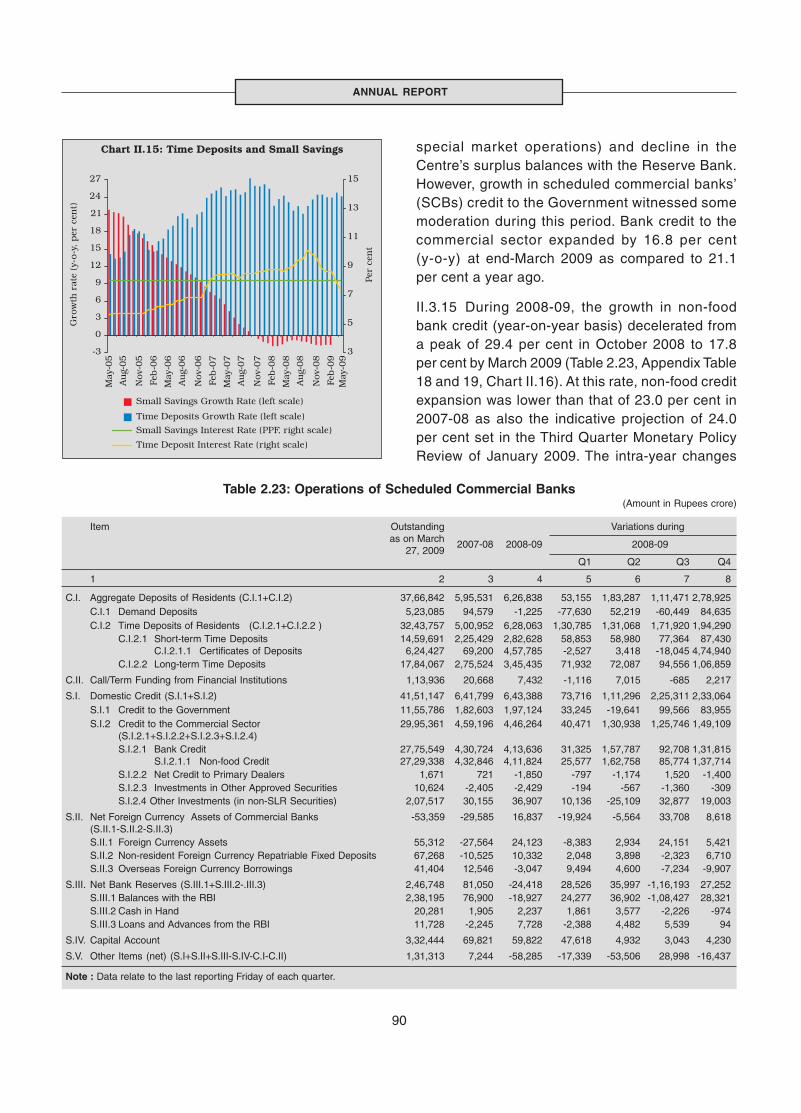

II.15 Time Deposits and Small Savings ................................................................................... 90

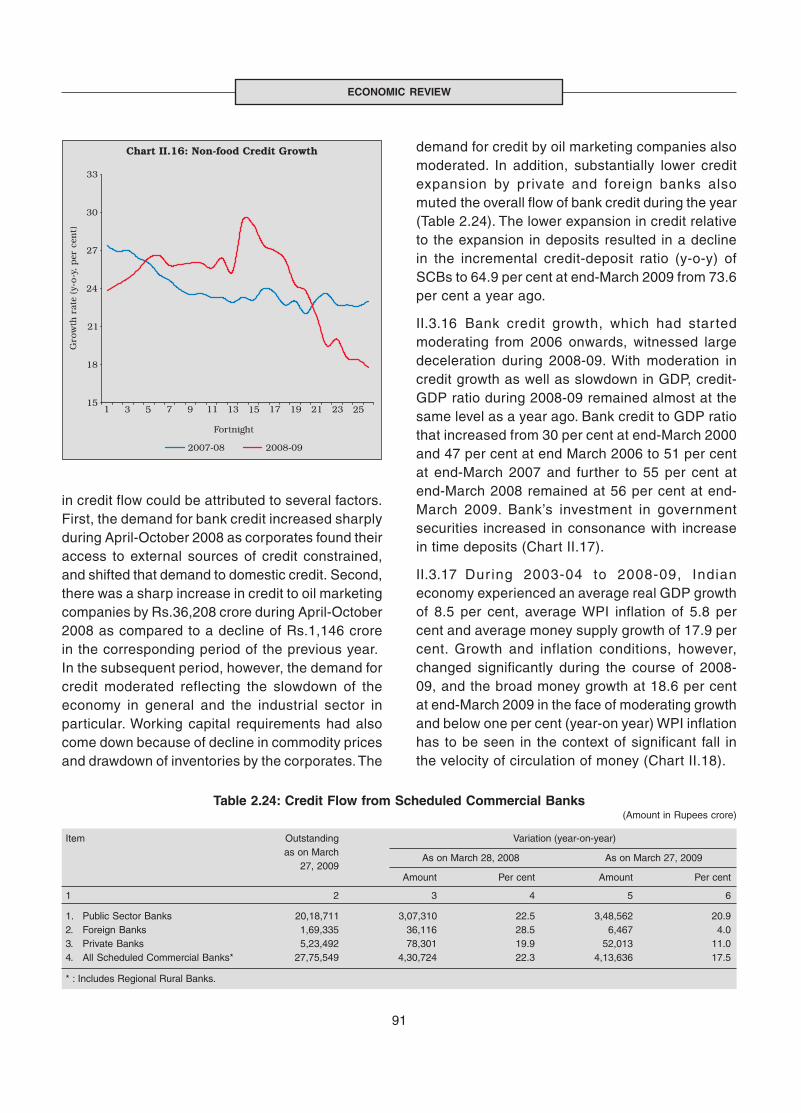

II.16 Non-Food Credit Growth .................................................................................................. 91

II.17 Bank Credit and Investment in Government Securities ................................................... 92

II.18 Income Velocity of Money ................................................................................................. 92

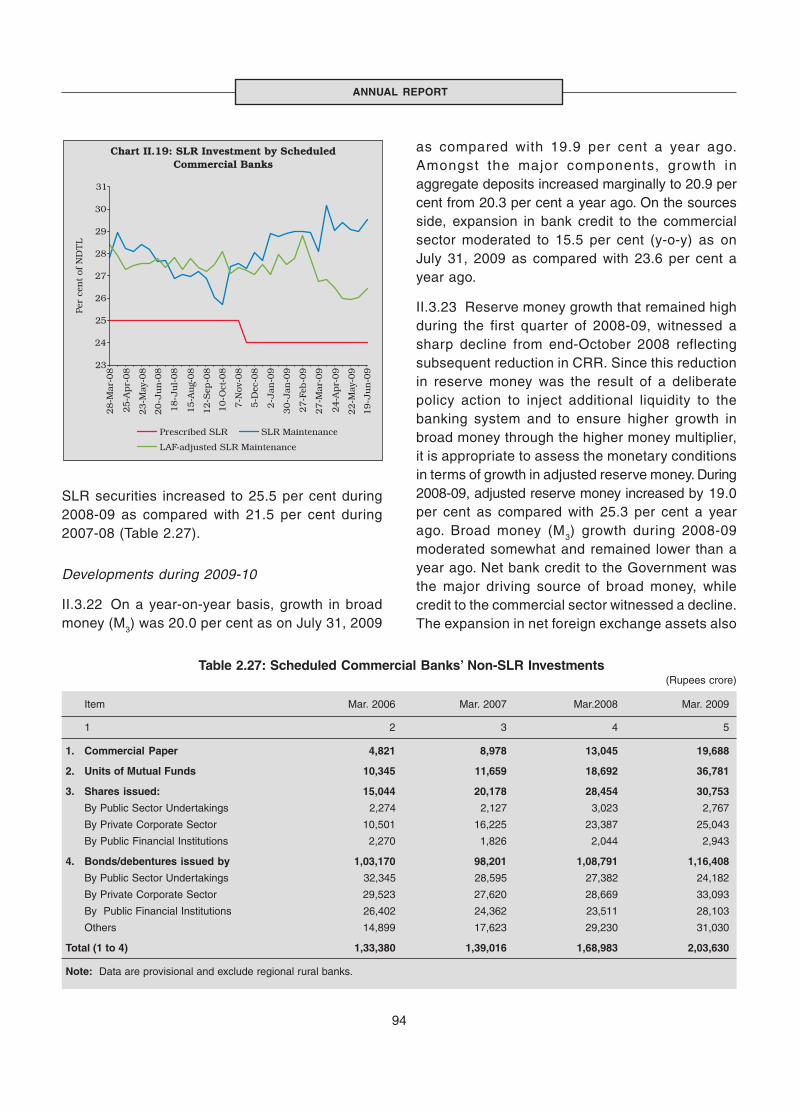

II.19 SLR Investment by Scheduled Commercial Banks ......................................................... 94

II.20 Global Inflation ................................................................................................................. 95

II.21 Volatility in CPI Inflation .................................................................................................... 97

II.22 Increase in International Commodity Prices (year-on-year) ............................................ 99

II.23 Annual WPI Inflation ......................................................................................................... 103

II.24 Food Price Inflation .......................................................................................................... 103

II.25 Asset Price Movements .................................................................................................... 109

II.26 Deficit Indicators of the Central Government ................................................................... 115

II.27 Debt Service Burden of the Central Government ............................................................ 120

II.28 Major Deficit Indicators of the State Governments .......................................................... 121

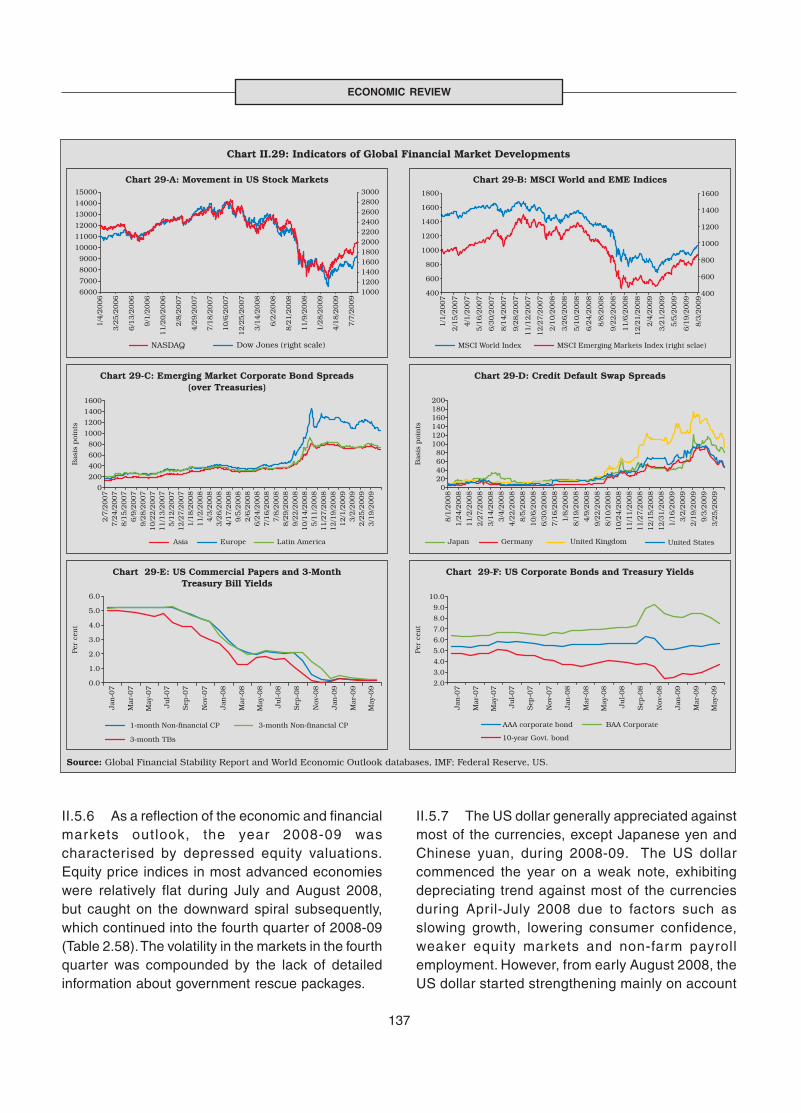

II.29 Indicators of Global Financial Market Developments ....................................................... 137

II.30 Movement of the LAF and Call Money Rate .................................................................... 142

II.31 Volumes and Rates in the Money Market ........................................................................ 142

II.32 Movement of WADR of CD and Average Call Money Rate ............................................. 144

II.33 Movement of WADR of CPs and Average Call Money Rate ............................................ 144

II.34 Nominal and Real Exchange Rates of Indian Rupee ...................................................... 145

II.35 Rupee-US Dollar Forward Premia ................................................................................... 146

II.36 Average Daily Turnover in the Foreign Exchange Market ................................................ 146

II.37 Yield on Government Bonds ............................................................................................ 147

II.38 Yield and Trading Turnover in Government Securities ..................................................... 148

II.39 Resource Mobilisation in Primary Market ........................................................................ 151

II.40 Key Global Indicators ....................................................................................................... 159

II.41 Key Balance of Payments Indicators ................................................................................ 163

II.42 External Demand and India’s Export Growth ................................................................... 164

II.43 Exports Growth of India vis-a-vis Advanced Economies andEMEs during October 2008-April 2009 ............................................................................ 166

II.44 India’s Export Growth - Principal Commodities (April-February) ..................................... 166

II.45 India’s Import Growth - Principal Commodities (April-February) ..................................... 167

II.46 Monthly Movements in Exports, Imports and Trade Balance ........................................... 169

II.47 India’s Gross Invisible Receipts ....................................................................................... 169

II.48 Growth of India's Software Services Exports ................................................................... 171

II.49 Movements in Oil Price and Remittance Inflows to India ................................................. 174

vii

Page No.

CONTENTS

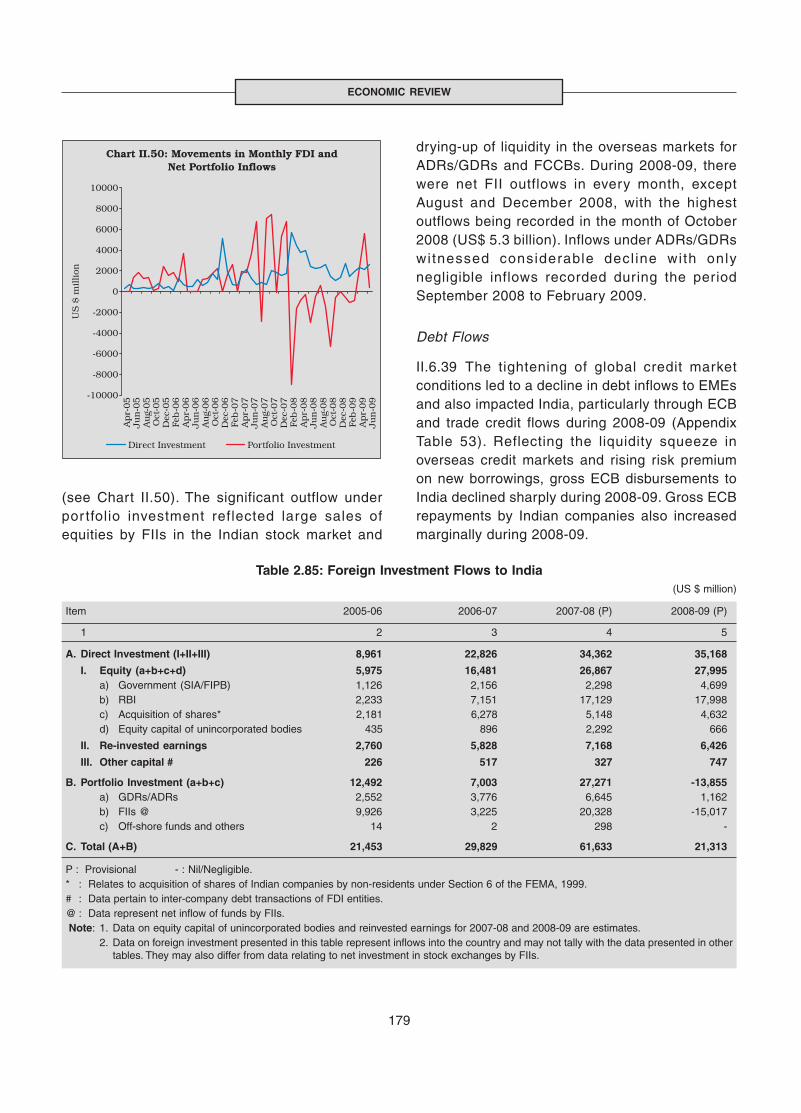

II.50 Movements in Monthly FDI and Net Portfolio Inflows ...................................................... 179

III.1 Cash Reserve Ratio ......................................................................................................... 201

III.2 MSS Buyback and Issuance of Central Government Securities...................................... 204

III.3 Outstanding LAF, MSS and GOI Balance ........................................................................ 206

III.4 Report(+)/Reverse Repo(-) Under LAF ............................................................................ 206

VI.1 Extension of Protection Accorded to the Depositors ....................................................... 266

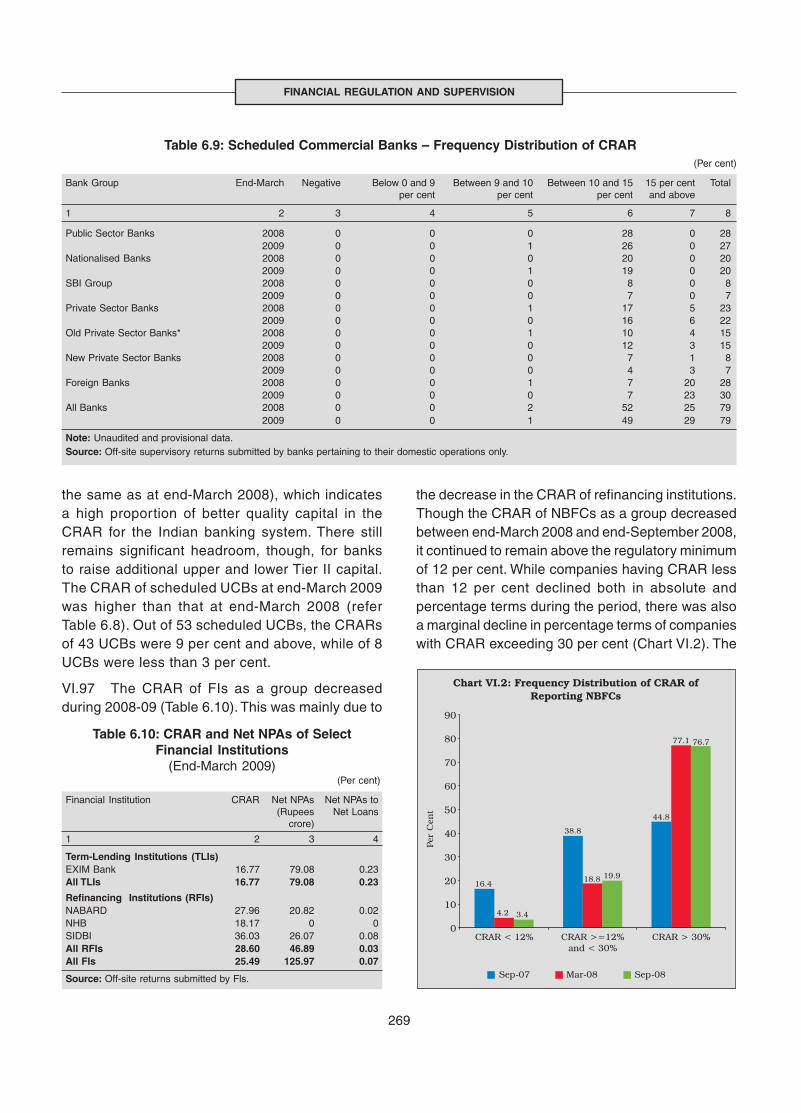

VI.2 Frequency Distribution of CRAR of Reporting NBFCs .................................................... 269

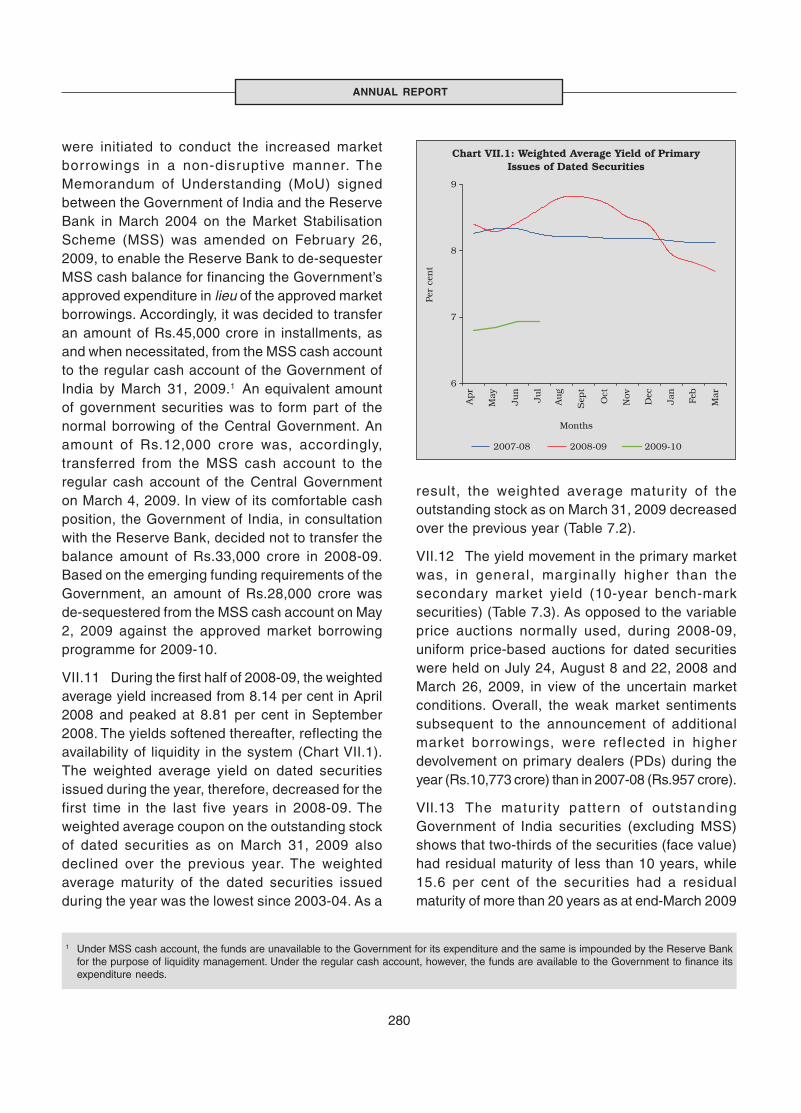

VII.1 Weighted Average Yield of Primary Issues of Dated Securities ...................................... 280

VII.2 Primary Market Yields of Treasury Bills ............................................................................ 284

VII.3 Cash Balances of the Central Government ..................................................................... 285

VII.4 Weighted Average Yield on SDLs and Yield to Maturity (YTM) on10-year Central Government Security .............................................................................. 288

VIII.1 Currency and Major Aggregates ...................................................................................... 294

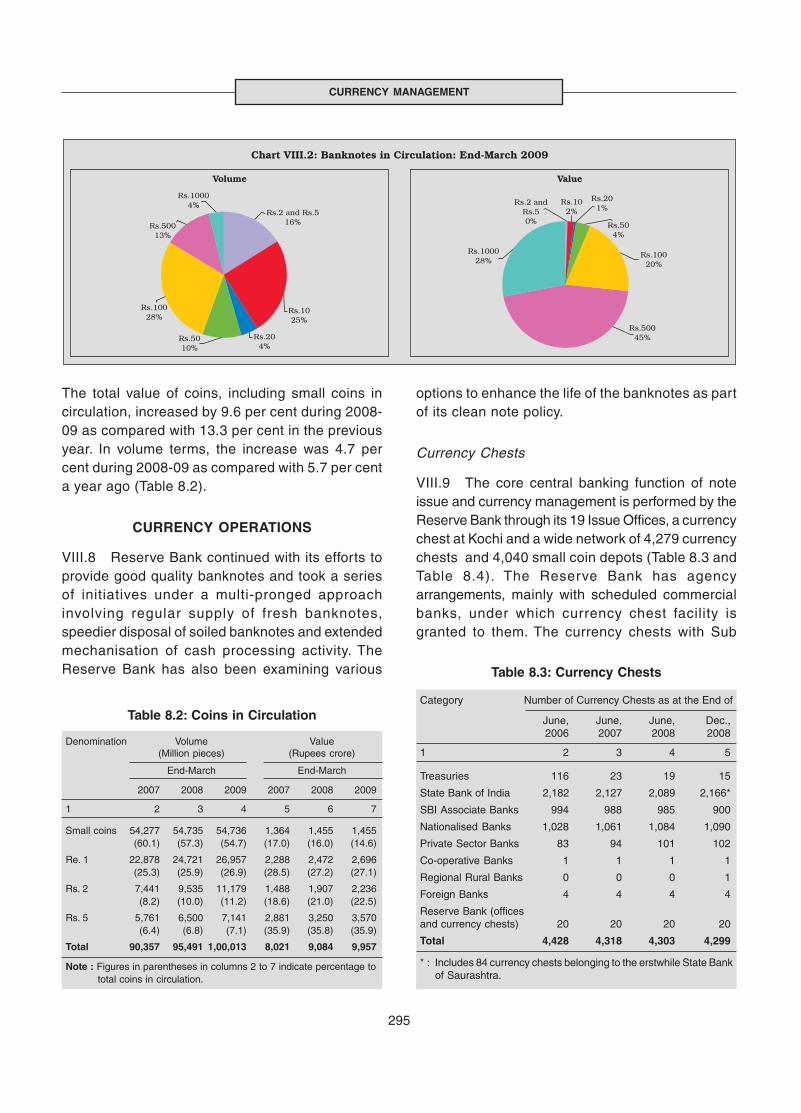

VIII.2 Banknotes in Circulation : End-March 2009 ..................................................................... 295

IX.1 Share of Paper-based versus Electronic Transactions .................................................... 306

IX.2 Trends in Real time Gross Settlement (RTGS) Transactions ........................................... 308

X.1 Total Staff Strength of the Reserve Bank ......................................................................... 324

XI.1 Sources of Income ........................................................................................................... 349

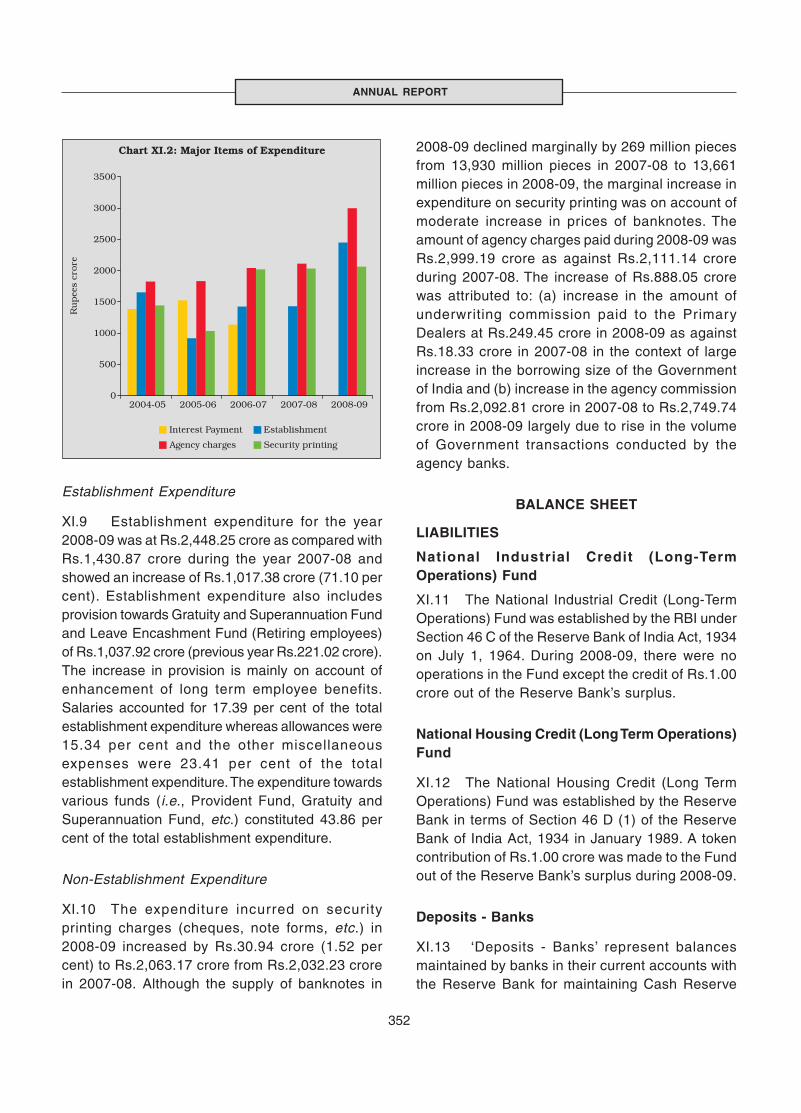

XI.2 Major Items of Expenditure .............................................................................................. 352

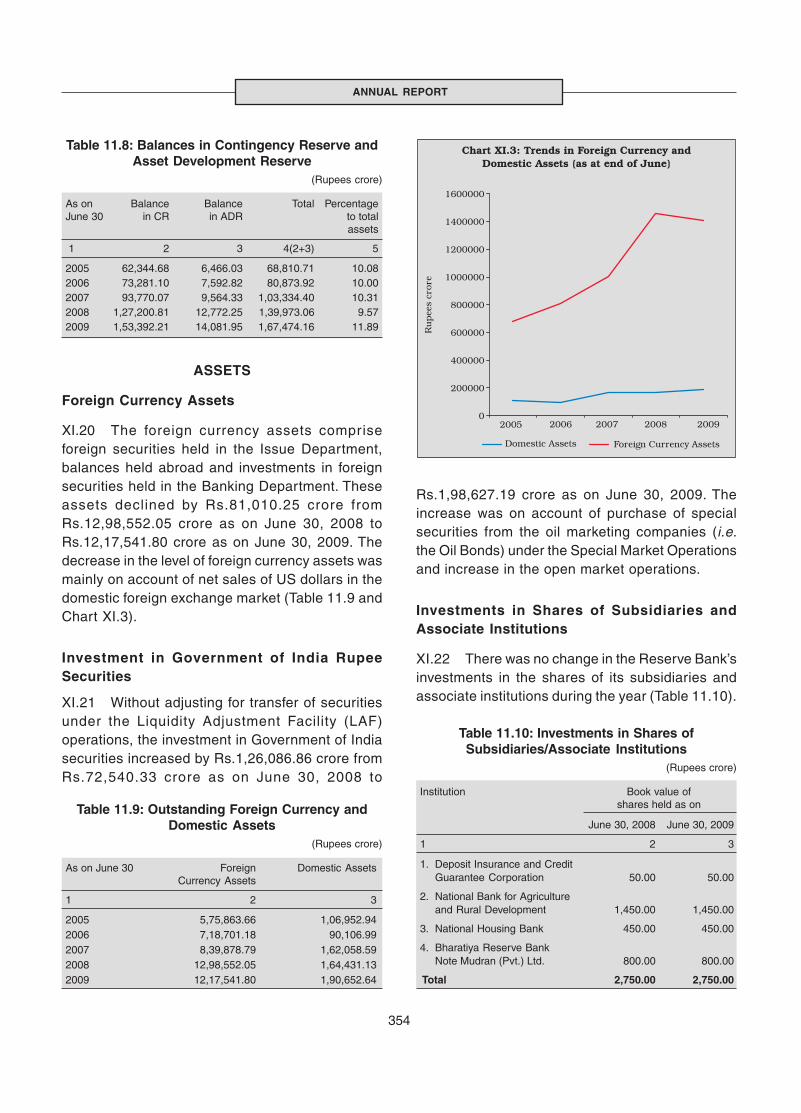

XI.3 Trends in Foreign Currency and Domestic Assets (as at end of June) ........................... 354

TEXT TABLES

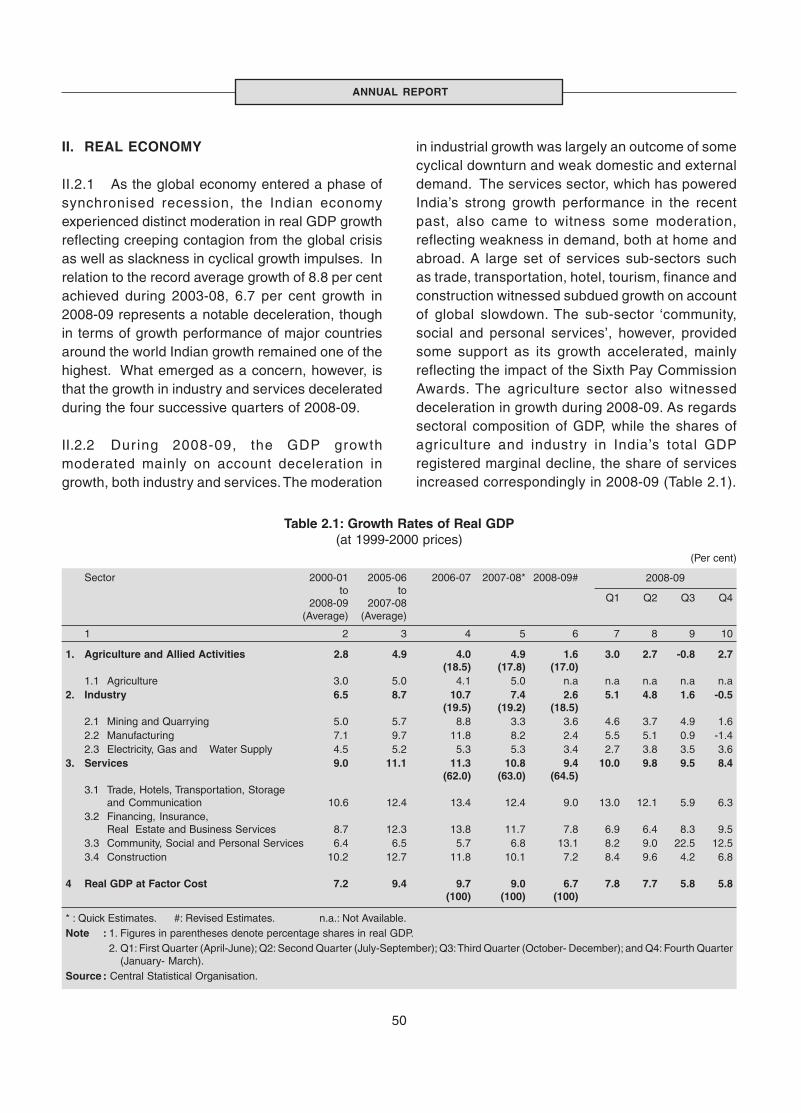

2.1 Growth Rates of Real GDP .............................................................................................. 50

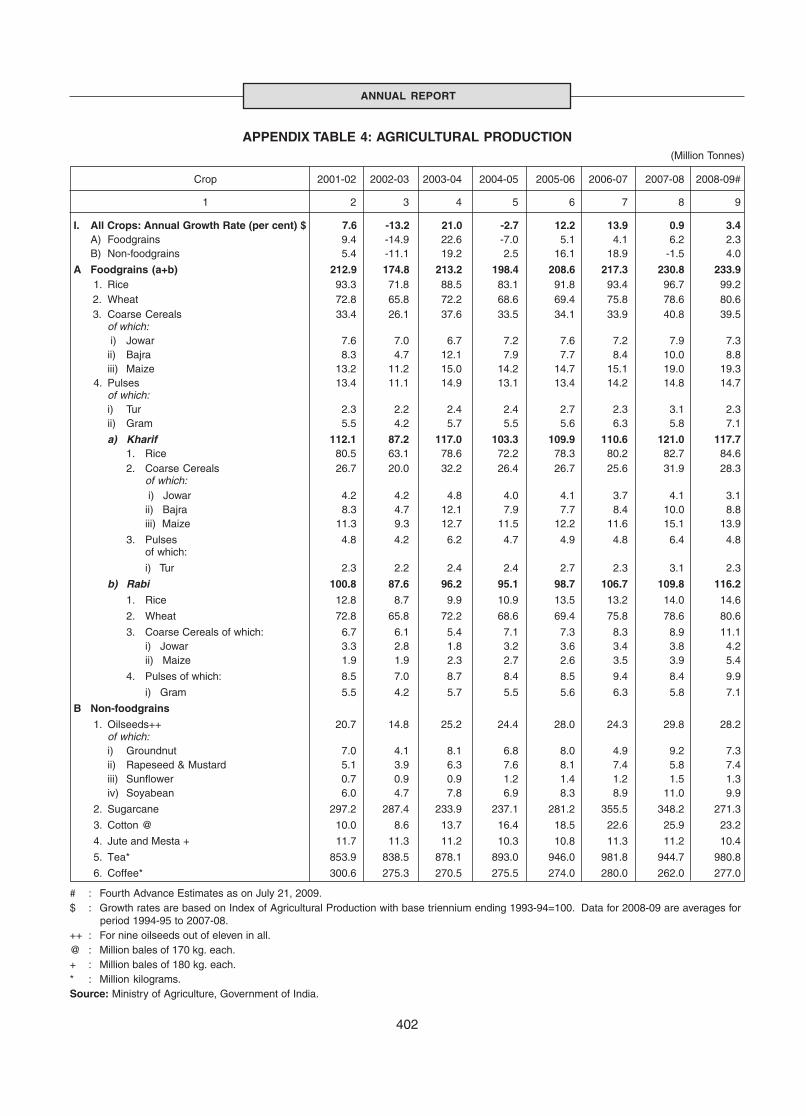

2.2 Agricultural Production ..................................................................................................... 53

2.3 Season-wise Agricultural Production ............................................................................... 53

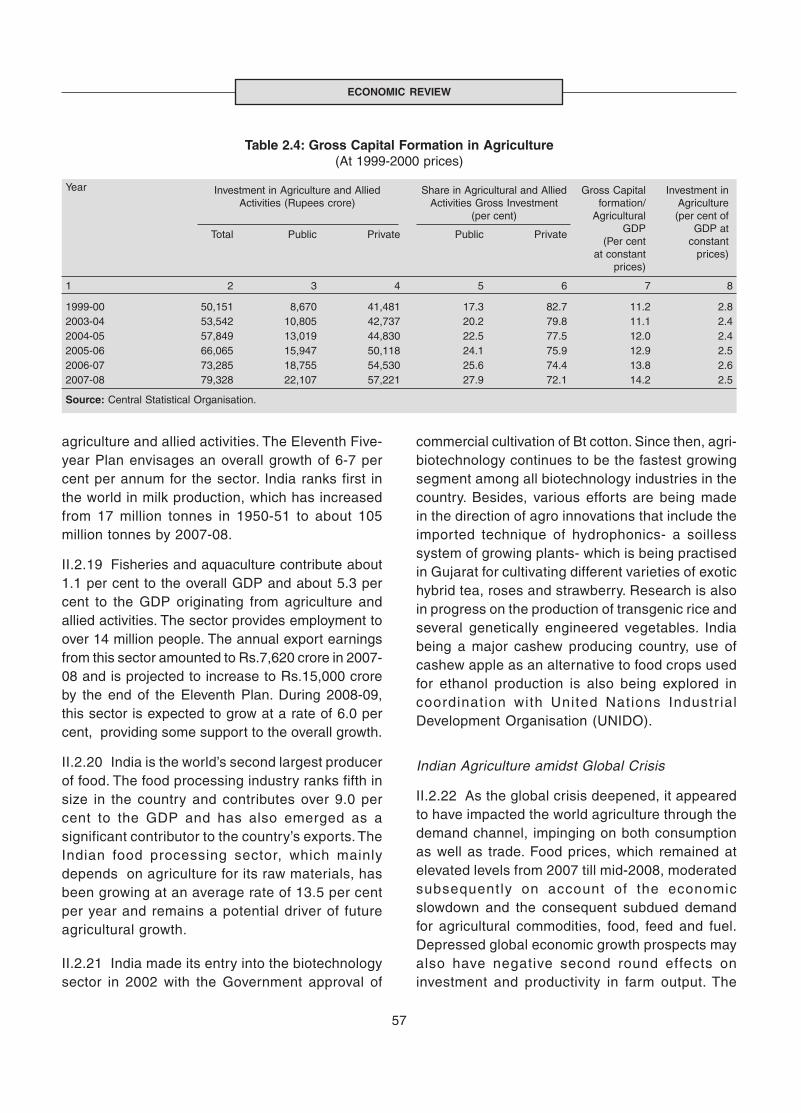

2.4 Gross Capital Formation in Agriculture ............................................................................ 57

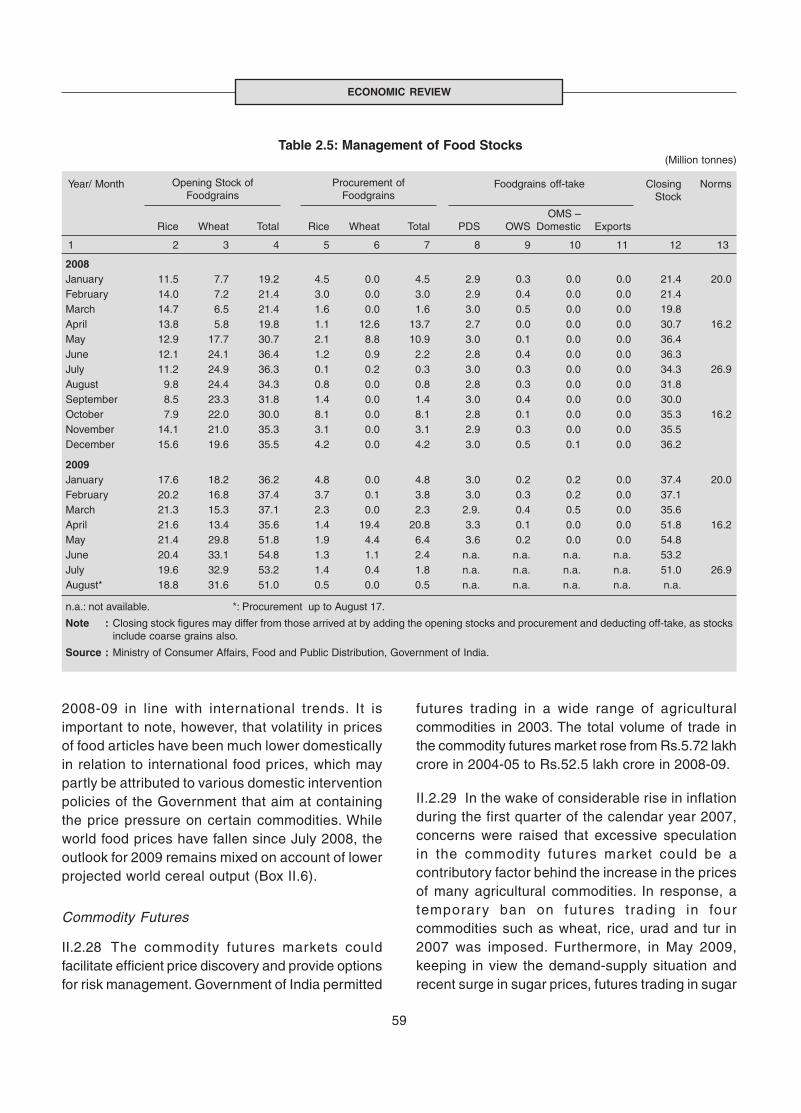

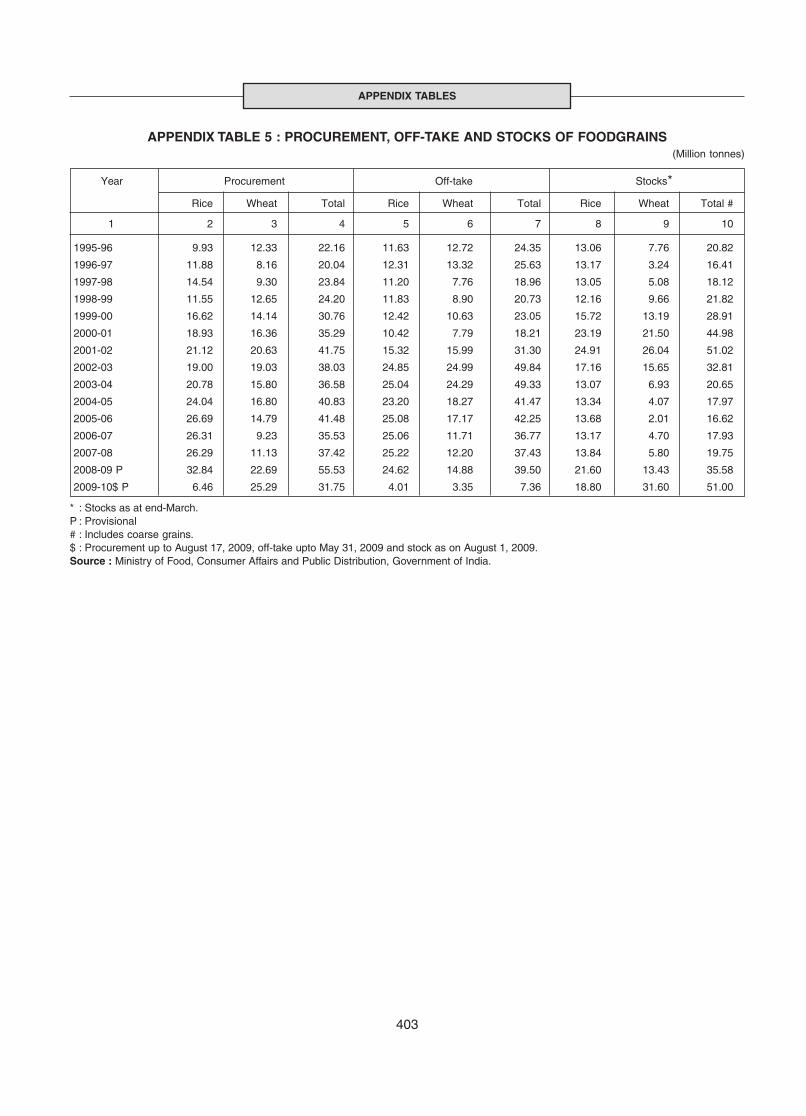

2.5 Management of Food Stocks ........................................................................................... 59

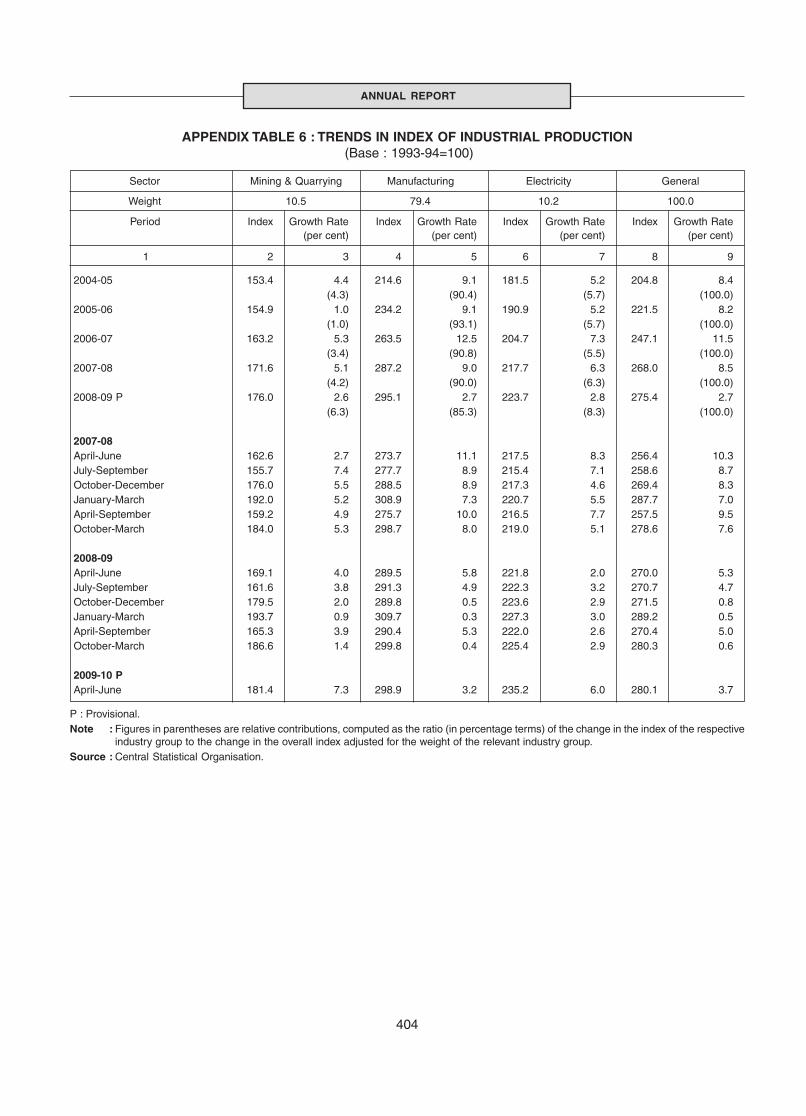

2.6 Growth Performance of Industrial Sector based onIndex of Industrial Production (IIP) ................................................................................... 63

2.7 Phases of Slowdown in Indian Industry ........................................................................... 63

2.8 Index of Industrial Production: Sectoral and Use-basedClassification of Industries ............................................................................................... 65

2.9 Trends in Growth of Consumer Goods ............................................................................. 66

2.10 Capacity Utilisation ........................................................................................................... 67

2.11 Targets and Achievements of Infrastructure Industries .................................................... 69

2.12 Performance of Central Sector Projects ........................................................................... 69

2.13 Industrial Investment Proposals ....................................................................................... 70

viii

CONTENTS

Page No.

2.14 Performance of Micro, Small and Medium Enterprises.................................................... 71

2.15 Performance of the Services Sector ................................................................................ 74

2.16 Indicators of Services Sector Activity ............................................................................... 74

2.17 Demand Side of GDP-Shares .......................................................................................... 76

2.18 Demand Side of GDP - Growth Rates ............................................................................. 77

2.19 Gross Capital Formation .................................................................................................. 80

2.20 Household Saving in Financial Assets ............................................................................. 82

2.21 Reserve Money – Variations ............................................................................................ 86

2.22 Monetary Indicators .......................................................................................................... 88

2.23 Operations of Scheduled Commercial Banks .................................................................. 90

2.24 Credit Flow from Scheduled Commercial Banks ............................................................. 91

2.25 Non-food Bank Credit - Sectoral Deployment .................................................................. 92

2.26 Flow of Resources to Commercial Sector ........................................................................ 93

2.27 Scheduled Commercial Banks’ Non-SLR Investments .................................................... 94

2.28 Global Inflation Indicators ................................................................................................. 97

2.29 Nominal and Real Policy Rates : Select Countries .......................................................... 98

2.30 International Commodity Prices ....................................................................................... 98

2.31 Key Commodity Price Movements – Global vis-à-vis Domestic ...................................... 100

2.32 Wholesale Price Inflation in India ..................................................................................... 104

2.33 Consumer Price Inflation - Major Groups......................................................................... 107

2.34 Major Fiscal Indicators: Combined Finances ................................................................... 114

2.35 Major Fiscal Indicators of the Central Government ......................................................... 115

2.36 Subsidies of the Centre .................................................................................................... 116

2.37 Key Deficit Indicators of the Centre for 2008-09 - Provisional Accounts ......................... 120

2.38 Average Interest Rates on Outstanding Domestic Liabilities of the Centre ..................... 120

2.39 Indicators of Combined Finances of the Centre and States ............................................ 122

2.40 Combined Liabilities of the Centre and States ................................................................. 123

2.41 Outstanding Government Guarantees ............................................................................. 124

2.42 Decomposition of the GFD of the Central Government .................................................. 125

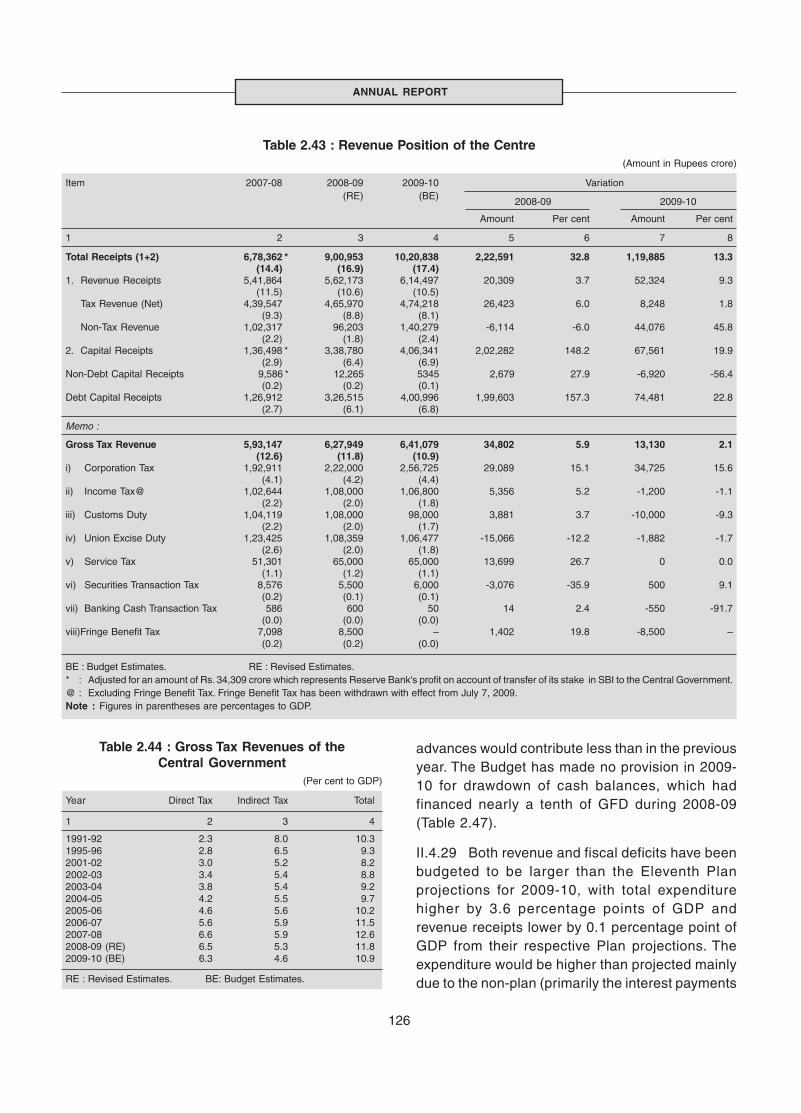

2.43 Revenue Position of the Central Government .................................................................. 126

2.44 Gross Tax Revenues of the Central Government ............................................................. 126

2.45 Expenditure Pattern of the Central Government .............................................................. 127

2.46 Expenditure on Select Development Heads of the Central Government ......................... 127

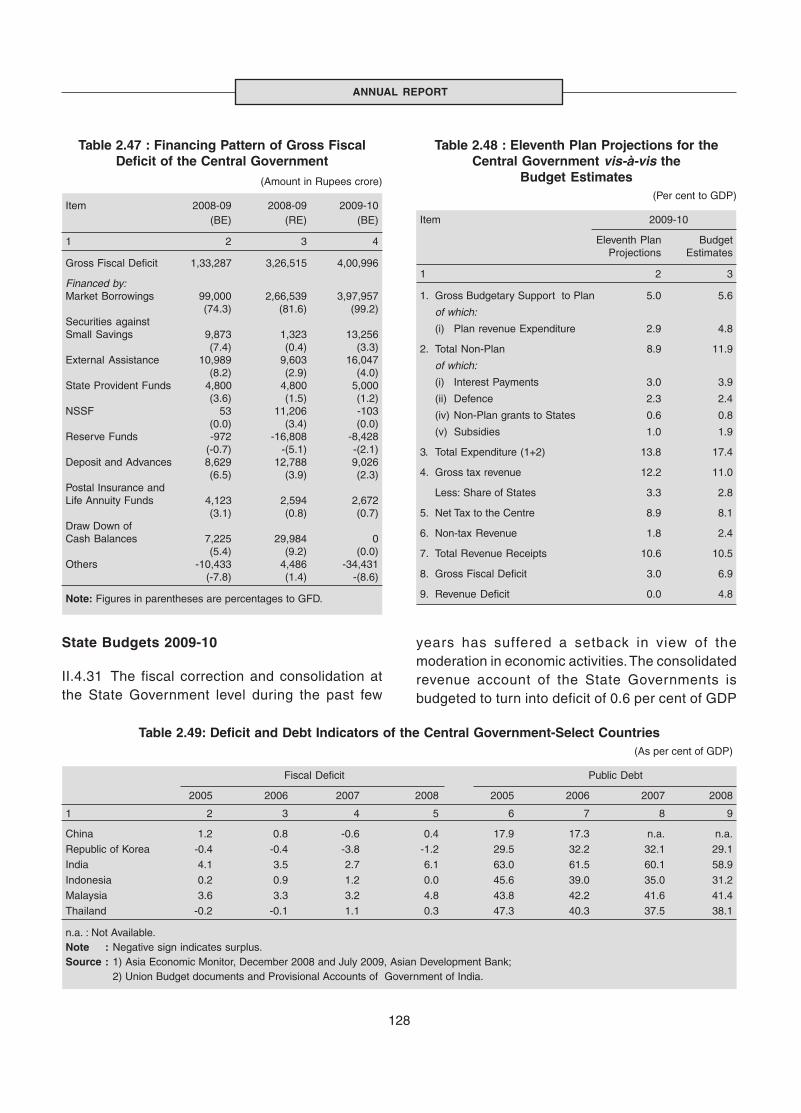

2.47 Financing Pattern of Gross Fiscal Deficit of the Central Government ............................. 128

2.48 Eleventh Plan Projections for the Central Government vis-à-vis the Budget Estimates .. 128

2.49 Deficit and Debt Indicators of the Central Government-Select Countries ....................... 128

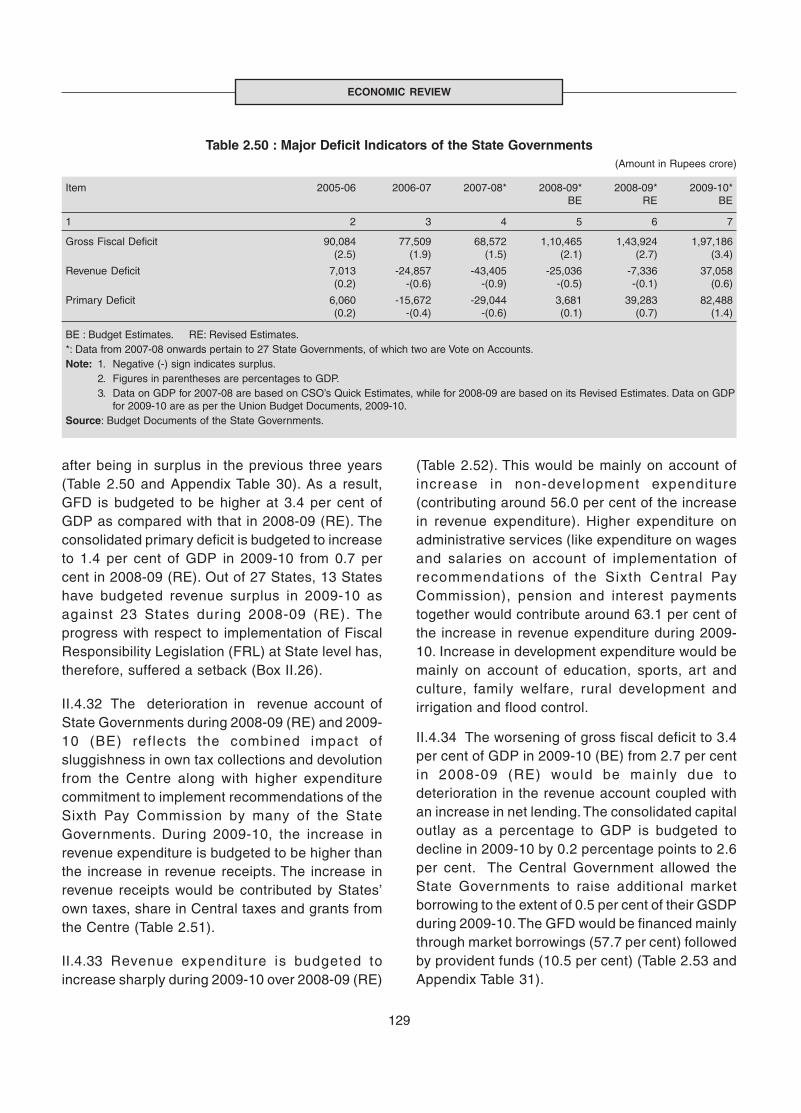

2.50 Major Deficit Indicators of the State Governments .......................................................... 129

ix

CONTENTS

Page No.

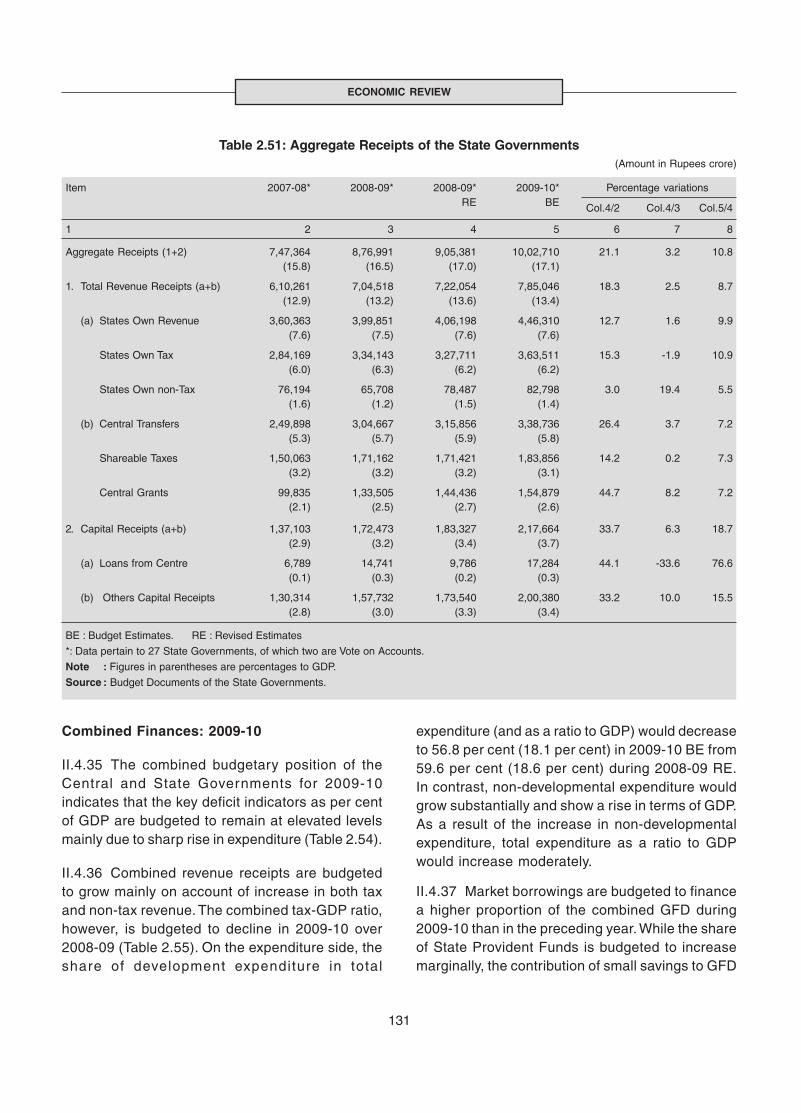

2.51 Aggregate Receipts of the State Governments ............................................................... 131

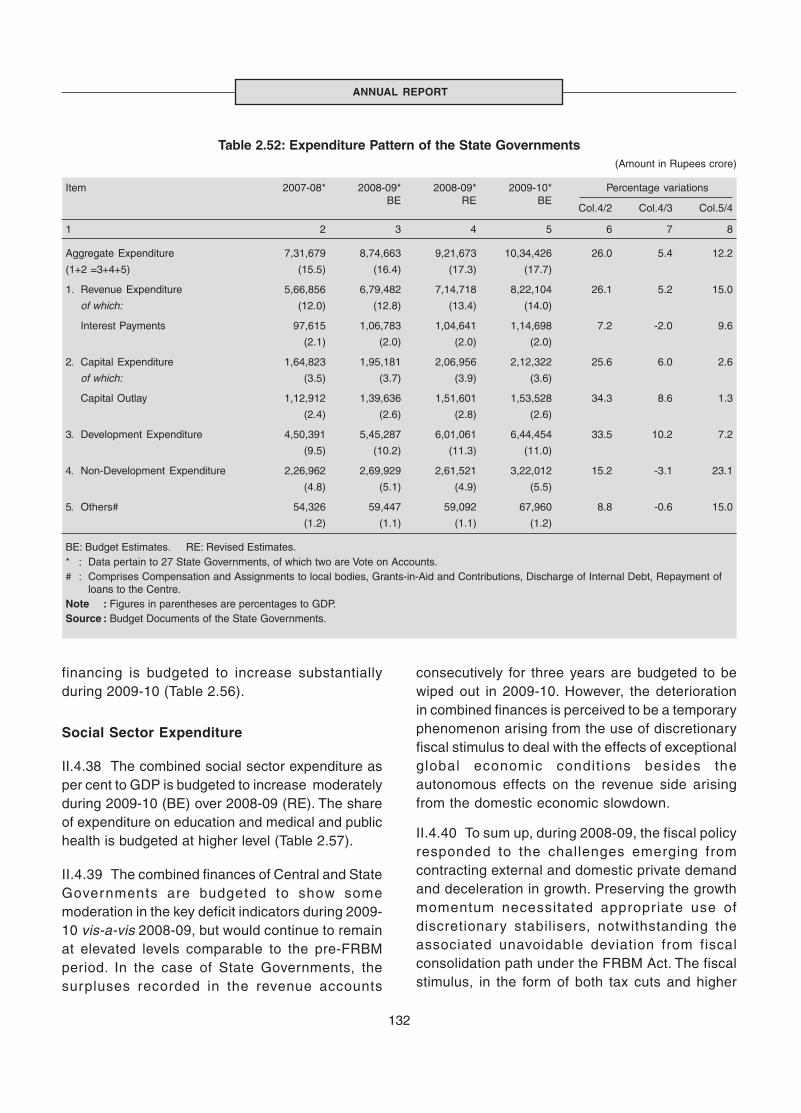

2.52 Expenditure Pattern of the State Governments ............................................................... 132

2.53 Decomposition and Financing Pattern of Gross Fiscal Deficit of States ......................... 133

2.54 Measures of Deficit of the Central and State Governments ............................................ 133

2.55 Combined Receipts and Disbursement of the Centre and States ................................... 134

2.56 Financing of Gross Fiscal Deficit of the Centre and States ............................................. 134

2.57 Combined Expenditure of the Centre and States on Social Sector ................................. 135

2.58 International Stock Markets .............................................................................................. 138

2.59 Appreciation (+)/Depreciation (-) of the US dollar vis-à-vis other Currencies ................. 138

2.60 Domestic Markets at a Glance ......................................................................................... 141

2.61 Activity in Money Market Segments ................................................................................. 143

2.62 Commercial Paper-Major Issuers ..................................................................................... 144

2.63 Purchase and Sales of US dollar by the Reserve Bank .................................................. 145

2.64 Movements in Deposit and Lending Rate ........................................................................ 148

2.65 Changes in Deposit and Lending Rates .......................................................................... 149

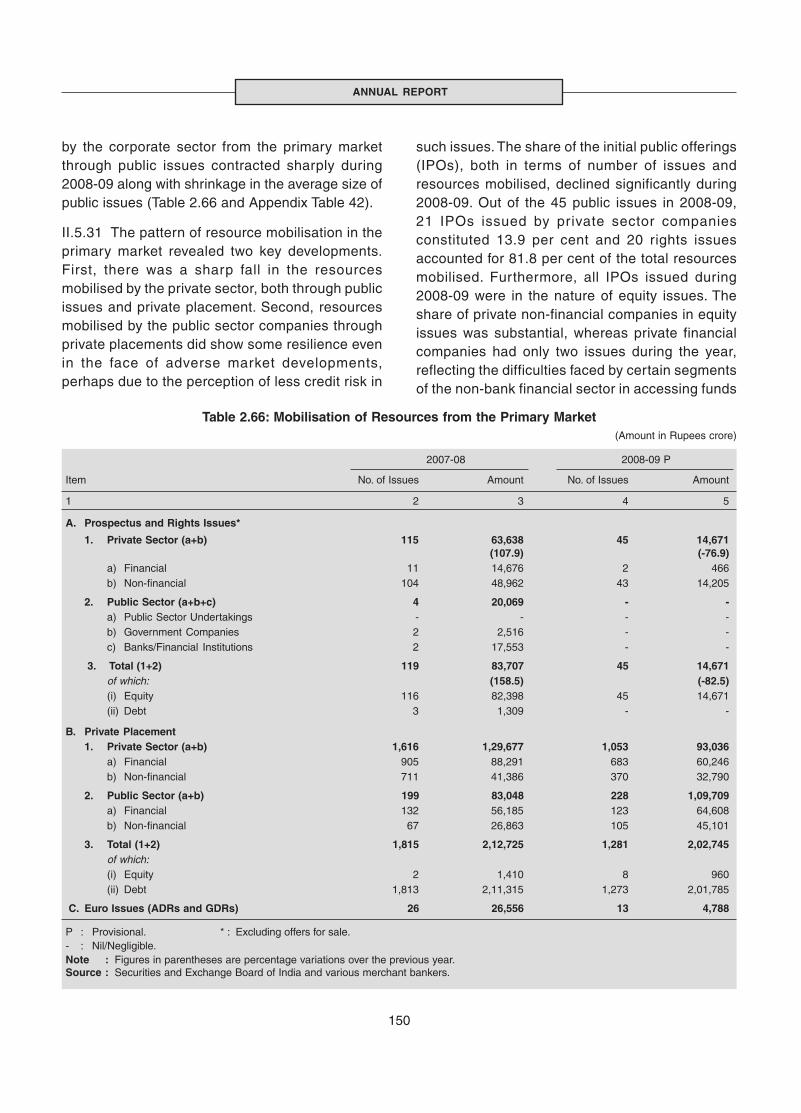

2.66 Mobilisation of Resources from the Primary Market ........................................................ 150

2.67 Indian Equity Markets - Key Indicators ............................................................................. 153

2.68 BSE Sectoral Stock Indices.............................................................................................. 153

2.69 Trends in Institutional Investments ................................................................................... 153

2.70 Resource Mobilisation by Mutual Funds .......................................................................... 154

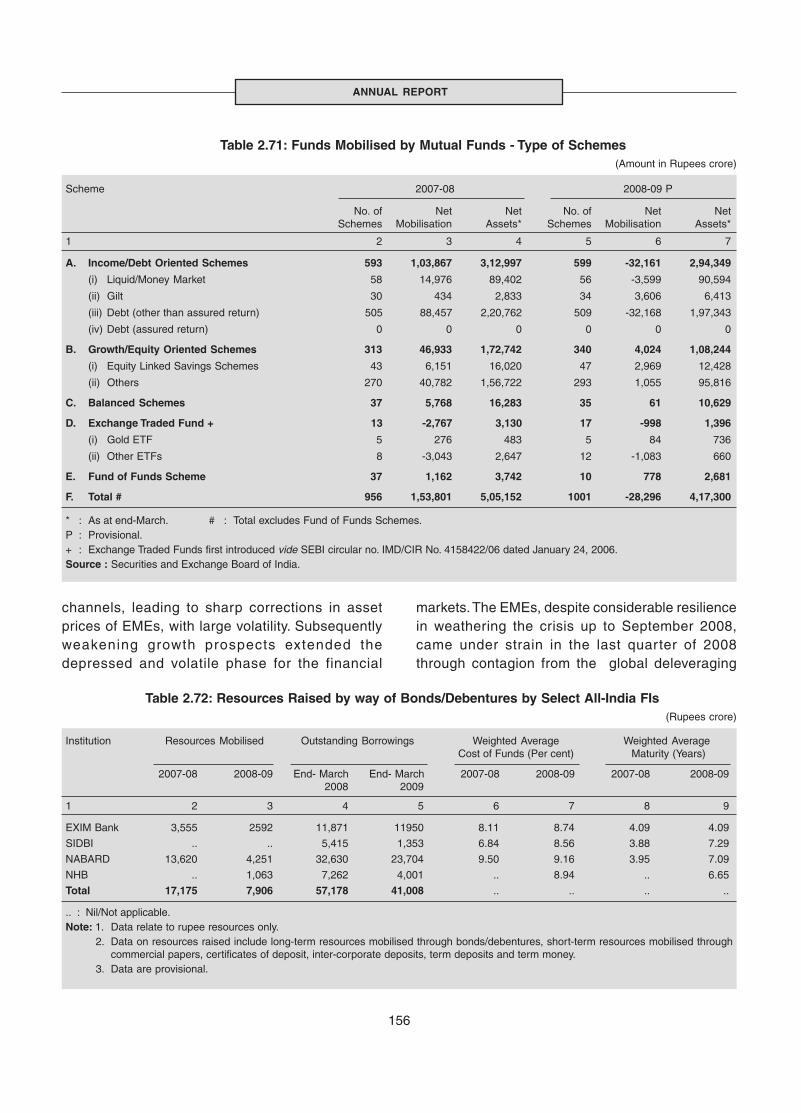

2.71 Funds Mobilised by Mutual Funds - Type of Schemes .................................................... 156

2.72 Resources Raised by way of Bonds/Debentures by Select All-India FIs ......................... 156

2.73 Direction of India’s Exports .............................................................................................. 166

2.74 Direction of India’s Imports ............................................................................................... 167

2.75 Balance of Payments : Key Indicators .............................................................................. 170

2.76 Structure of India’s Service Exports ................................................................................. 171

2.77 India’s Share in World Exports of Goods and Services ................................................... 171

2.78 Computer & Information Services Exports ....................................................................... 173

2.79 Foreign Tourists Arrival in India and Outbound Tourist Traffic .......................................... 173

2.80 Non-Software Miscellaneous Receipts & Payments ........................................................ 173

2.81 Composition of Private Transfers to India......................................................................... 174

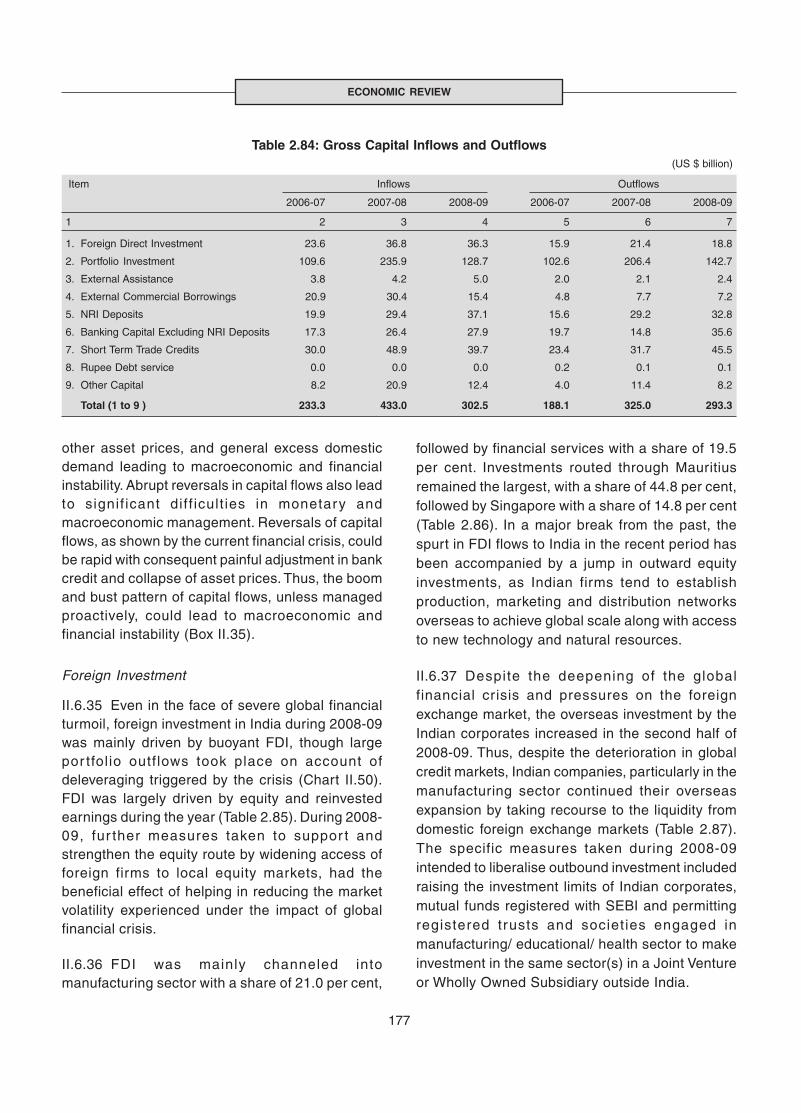

2.82 Migrant Remittances: Top Recipients ............................................................................... 174

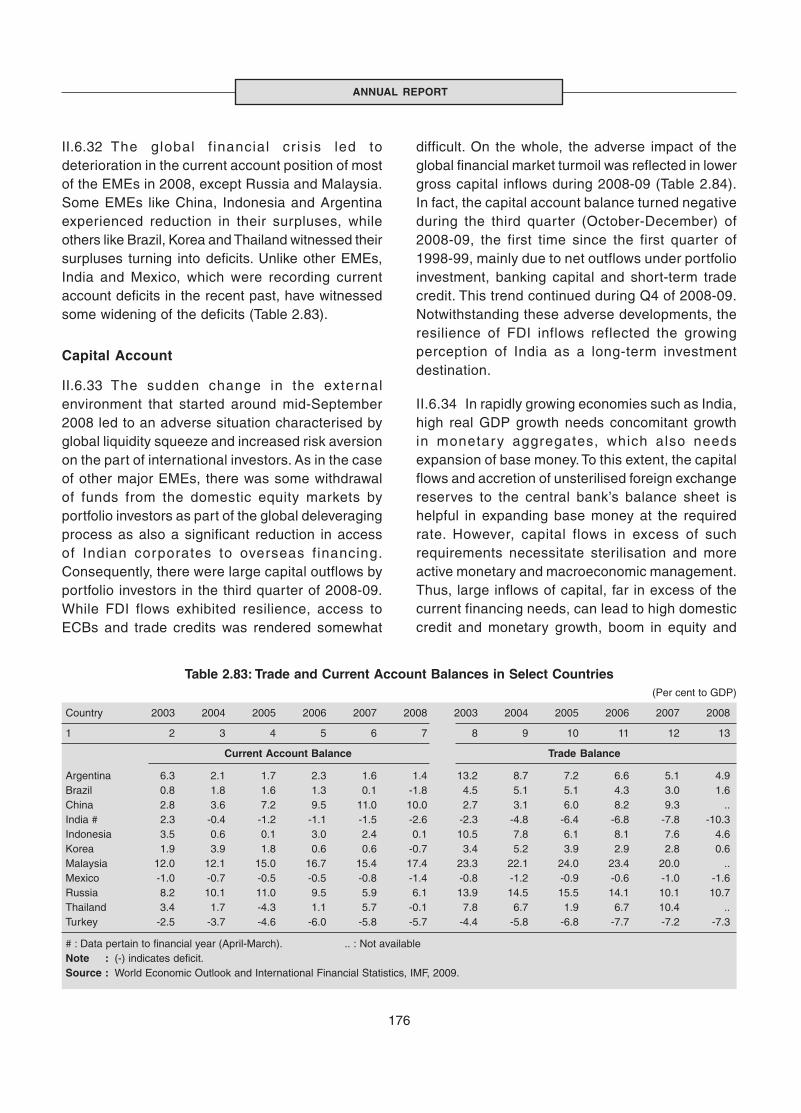

2.83 Trade and Current Account Balances in Select Countries ............................................... 176

2.84 Gross Capital Inflows and Outflows ................................................................................. 177

2.85 Foreign Investment Flows to India ................................................................................... 179

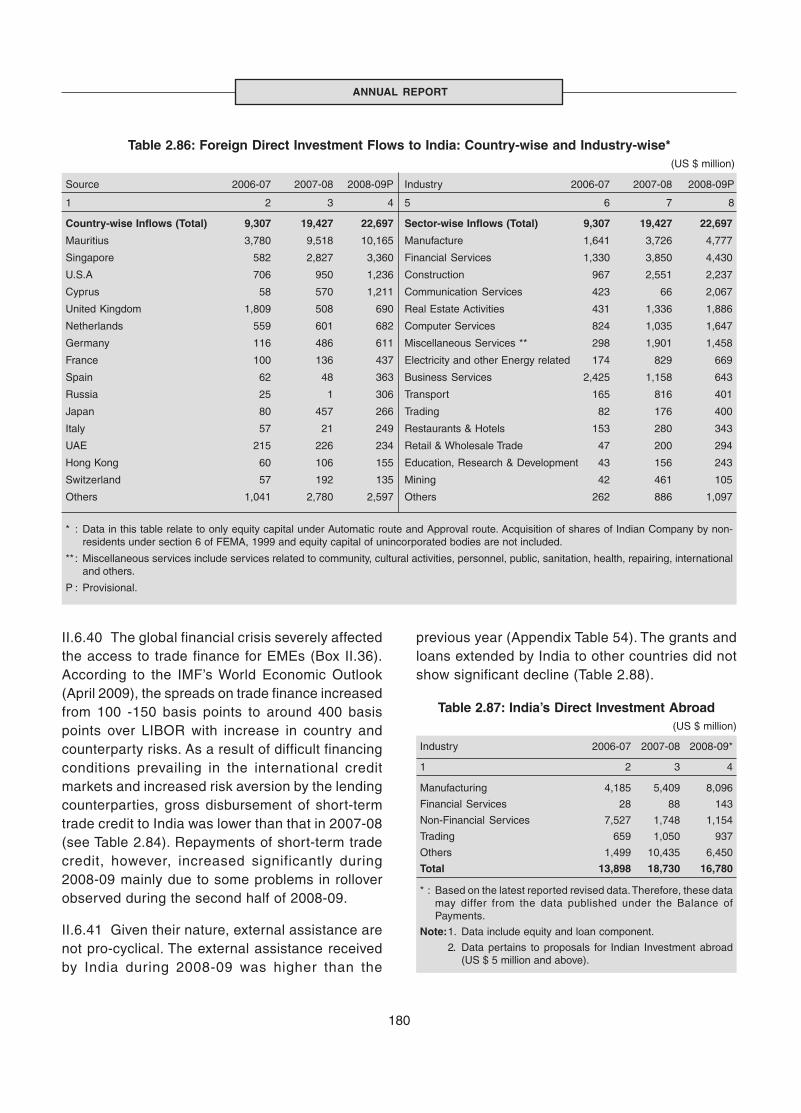

2.86 Foreign Direct Investment Flows to India: Country-wise and Industry-wise .................... 180

2.87 India’s Direct Investment Abroad ..................................................................................... 180

x

CONTENTS

Page No.

2.88 India’s Grants and Loans to Foreign Governments ......................................................... 182

2.89 Balances under NRI Deposit Schemes ............................................................................ 182

2.90 Ceiling Interest rates on NRI Deposits ............................................................................. 182

2.91 India’s External Debt ........................................................................................................ 183

2.92 External Debt Service Payments ..................................................................................... 183

2.93 International Comparison of Top Ten Debtor Countries, 2007 ......................................... 184

2.94 Sources of Variation in Foreign Exchange Reserves ....................................................... 184

2.95 Foreign Exchange Reserves of the Major EMEs ............................................................. 185

2.96 Deployment Pattern of Foreign Currency Assets ............................................................. 186

2.97 International Investment Position of India ........................................................................ 186

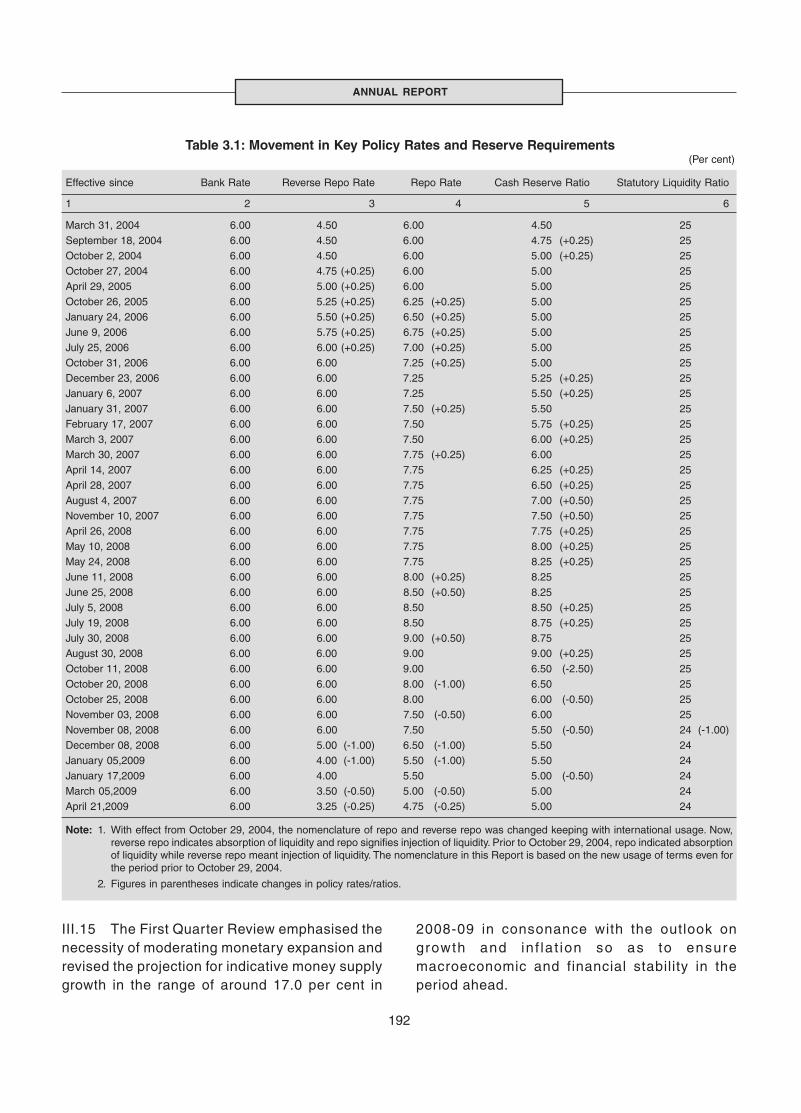

3.1 Movement in Key Policy Rates and Reserve Requirements ............................................ 192

3.2 Reserve Bank’s Liquidity Management Operations ......................................................... 202

3.3 Monthly Primary Liquidity Flows and Open Market Operations ....................................... 202

3.4 Indicators of Liquidity ........................................................................................................ 204

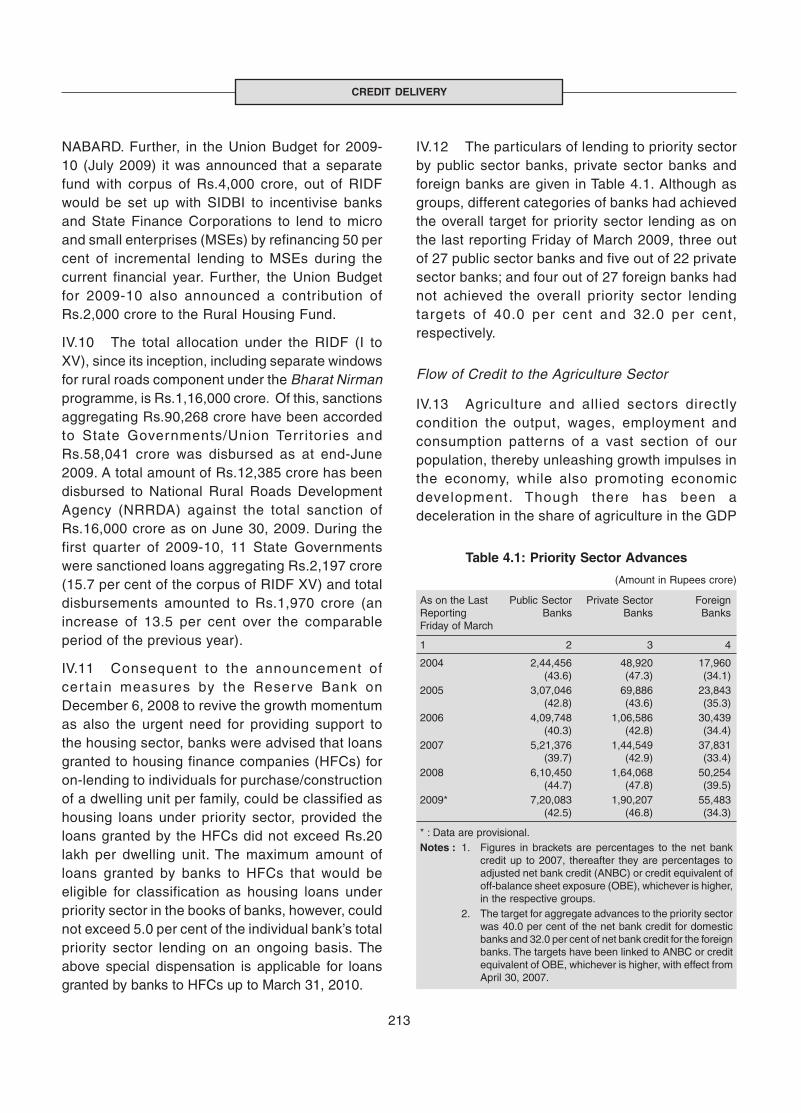

3.5 Reserve Bank’s Holdings of Central Government Dated Securities ................................ 207

3.6 Reverse Repo/Repo Bids under LAF ............................................................................... 208

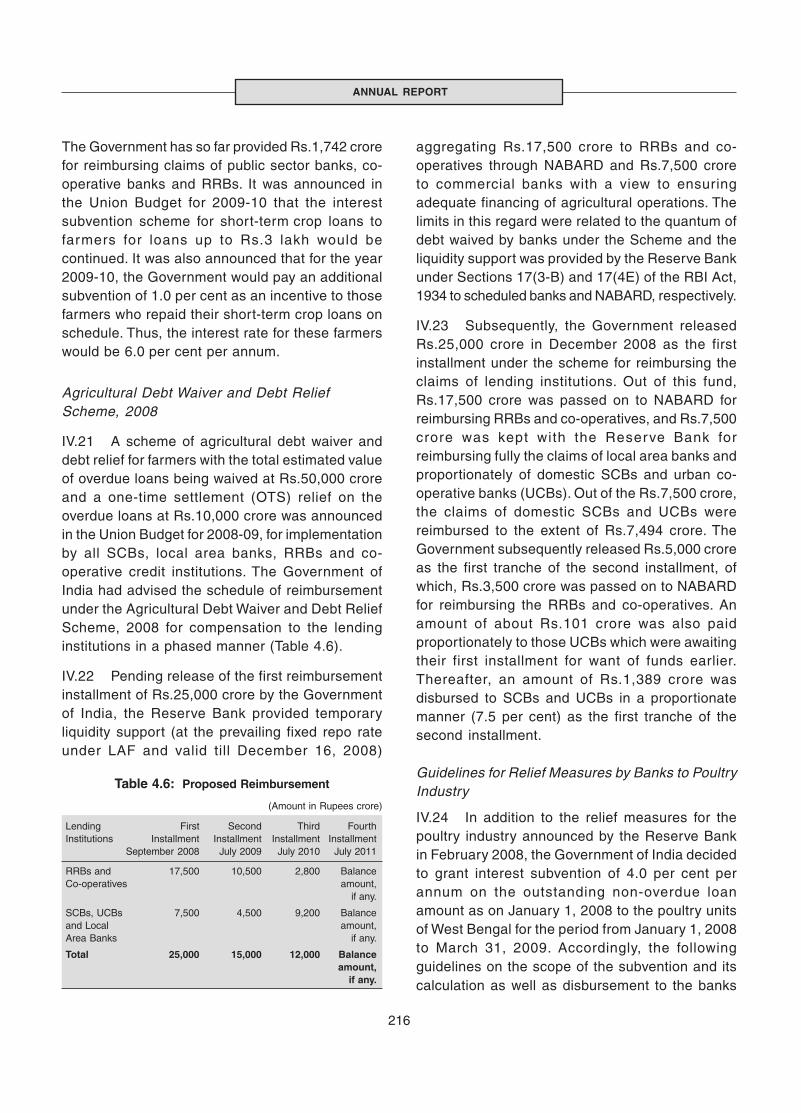

4.1 Priority Sector Advances .................................................................................................. 213

4.2 Disbursements under Special Agricultural Credit Plans .................................................. 214

4.3 Targets and Actual Disbursement to Agriculture by Banks .............................................. 214

4.4 Outstanding Agricultural Advances .................................................................................. 215

4.5 Public Sector Banks – Recovery of Direct Agricultural Advances ................................... 215

4.6 Proposed Reimbursement ................................................................................................ 216

4.6 Outstanding Credit to Micro and Small Enterprises ......................................................... 217

4.7 Credit to Sick Micro and Small Enterprises ..................................................................... 217

4.8 Bank Credit to Minority Communities by SCBs under Priority Sector Advances ............ 221

4.9 Bank Loans Outstanding against SHGs as on March 31, 2008 ...................................... 221

6.1 Health of Scheduled Commercial Banks in India ............................................................. 242

6.2 Offices of Indian Banks Opened Abroad – Between July 2008 and June 2009 .............. 247

6.3 Offices of Foreign Banks Opened in India – Between July 2008 and June 2009 ............ 248

6.4 Timeframe for Implementation of Advanced Approaches in India ................................... 248

6.5 Resolution of NPAs ........................................................................................................... 250

6.6 Frauds in the Banking Sector ........................................................................................... 257

6.7 Utilisation of Refinance Facilities ...................................................................................... 263

6.8 Select Financial Indicators ............................................................................................... 268

6.9 Scheduled Commercial Banks – Frequency Distribution of CRAR ................................. 269

6.10 CRAR and Net NPAs of Select Financial Institutions (End-March 2009) ........................ 269

xi

CONTENTS

Page No.

6.11 Scheduled Commercial Banks - Performance Indicators ................................................ 270

6.12 Net NPA to Net Advances of Scheduled Commercial Banks ........................................... 271

6.13 Net NPAs to Net Advances of SUCBs.............................................................................. 271

6.14 Scheduled Commercial Banks – Cost of Funds and Return on Funds ........................... 272

6.15 Operational Results of Scheduled Commercial Banks – Key Ratios ............................... 272

6.16 Operational Results of Scheduled Commercial Banks: 2008-09 ..................................... 273

6.17 Operational Results of SUCBs – Key Ratios ................................................................... 273

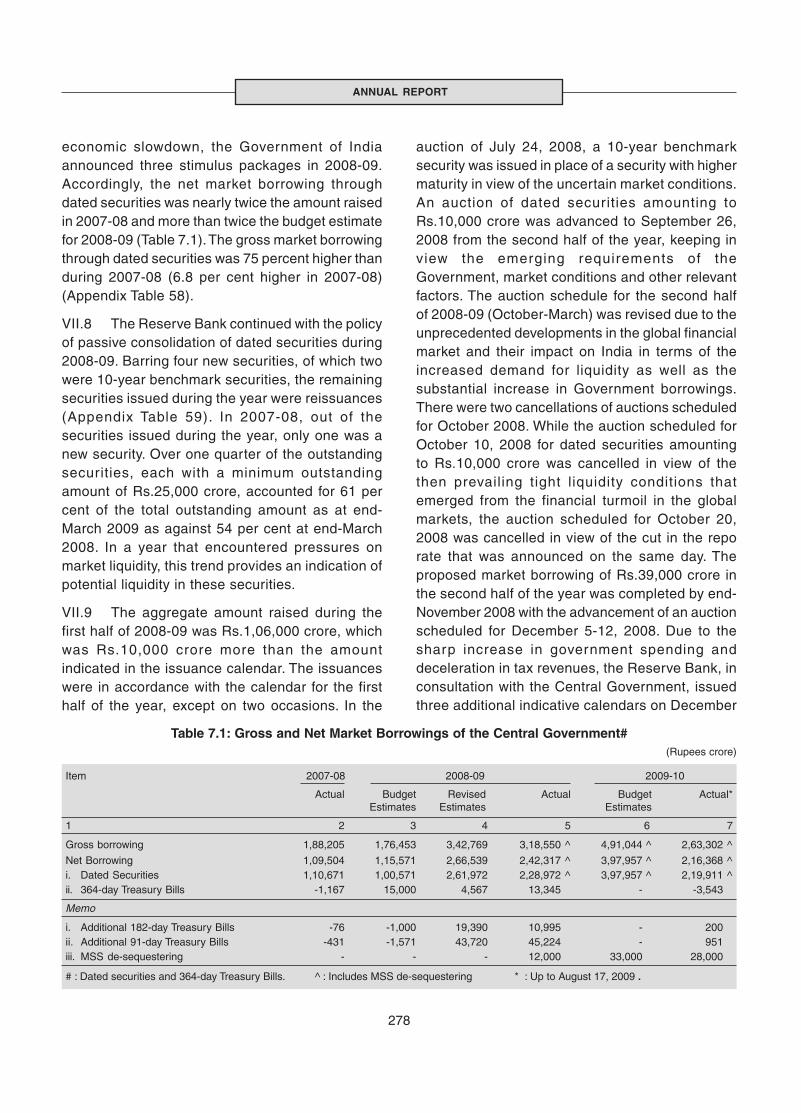

7.1 Gross and Net Market Borrowings of the Central Government ....................................... 278

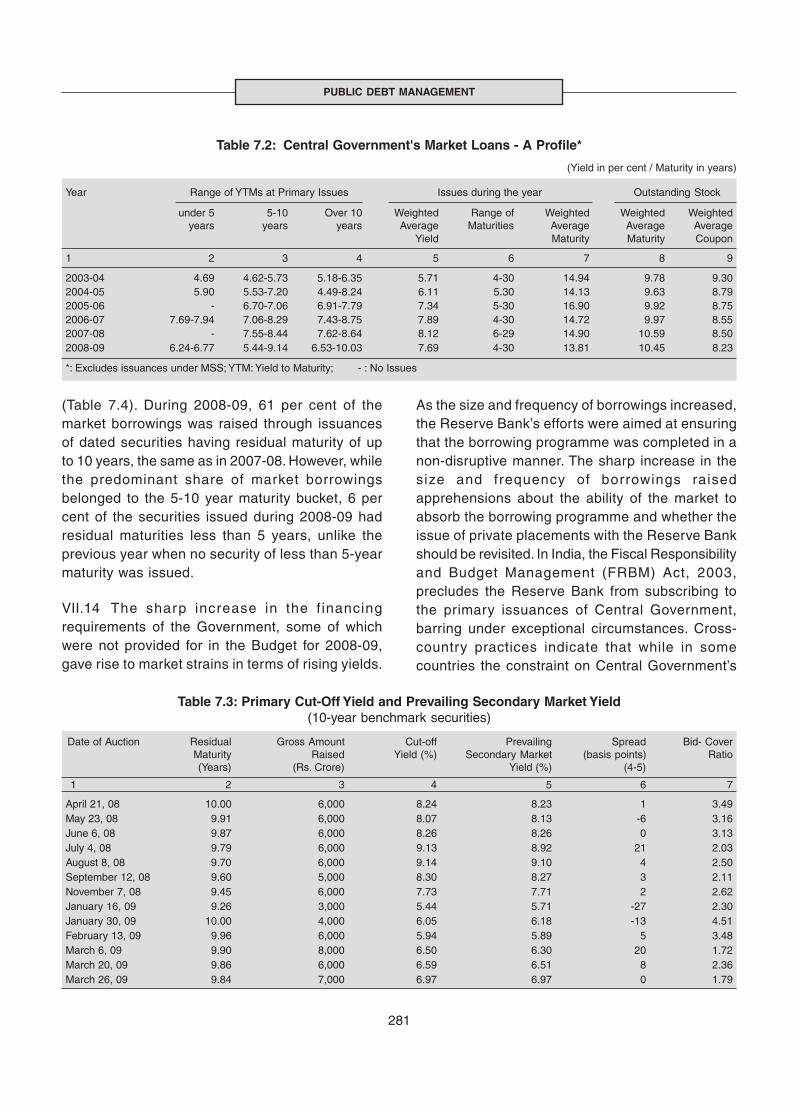

7.2 Central Government’s Market Loans- A Profile ................................................................ 281

7.3 Primary Cut-Off Yield and Prevailing Secondary Market Yield ........................................ 281

7.4 Maturity Profile of Central Government Dated Securities ................................................ 282

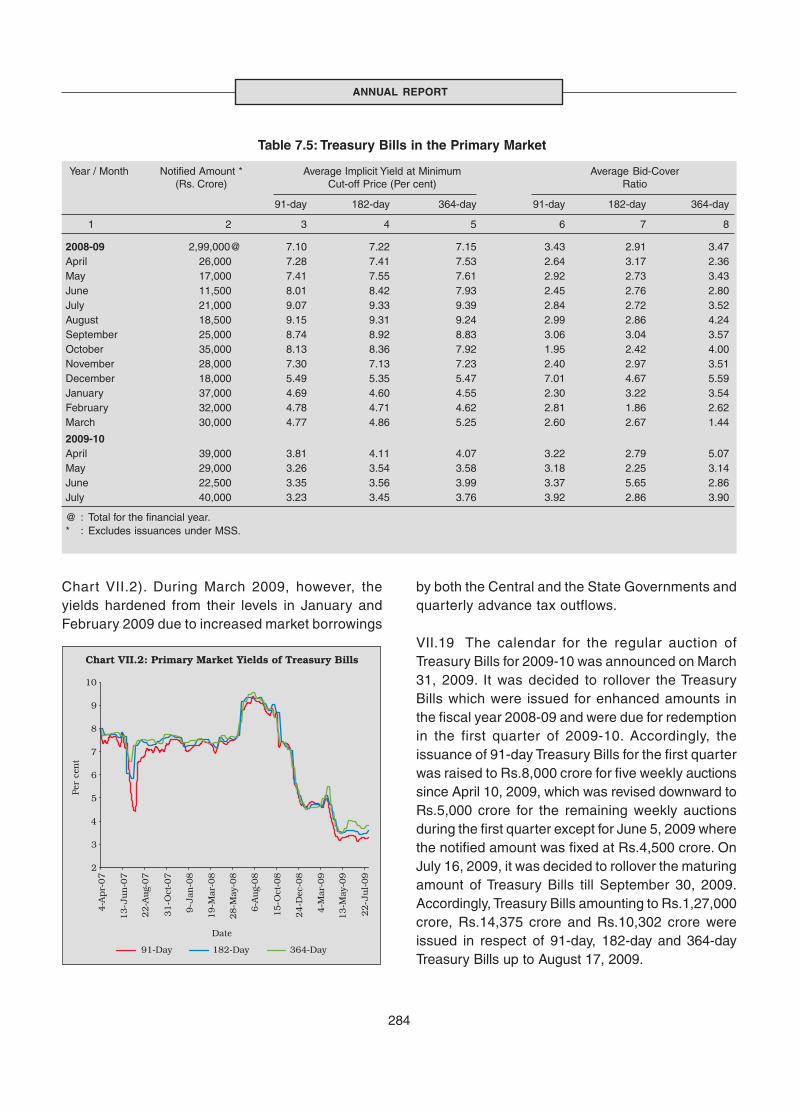

7.5 Treasury Bills in the Primary Market ................................................................................ 284

7.6 Annual Market Borrowings of State Governments ........................................................... 286

7.7 Yield on State Government Securities ............................................................................. 287

7.8 Month-wise Market Borrowings of State Governments ................................................... 287

7.9 Weighted Average Spreads during 2008-09 .................................................................... 288

7.10 Frequency Distribution of Tranches of Auctions during 2008-09...................................... 288

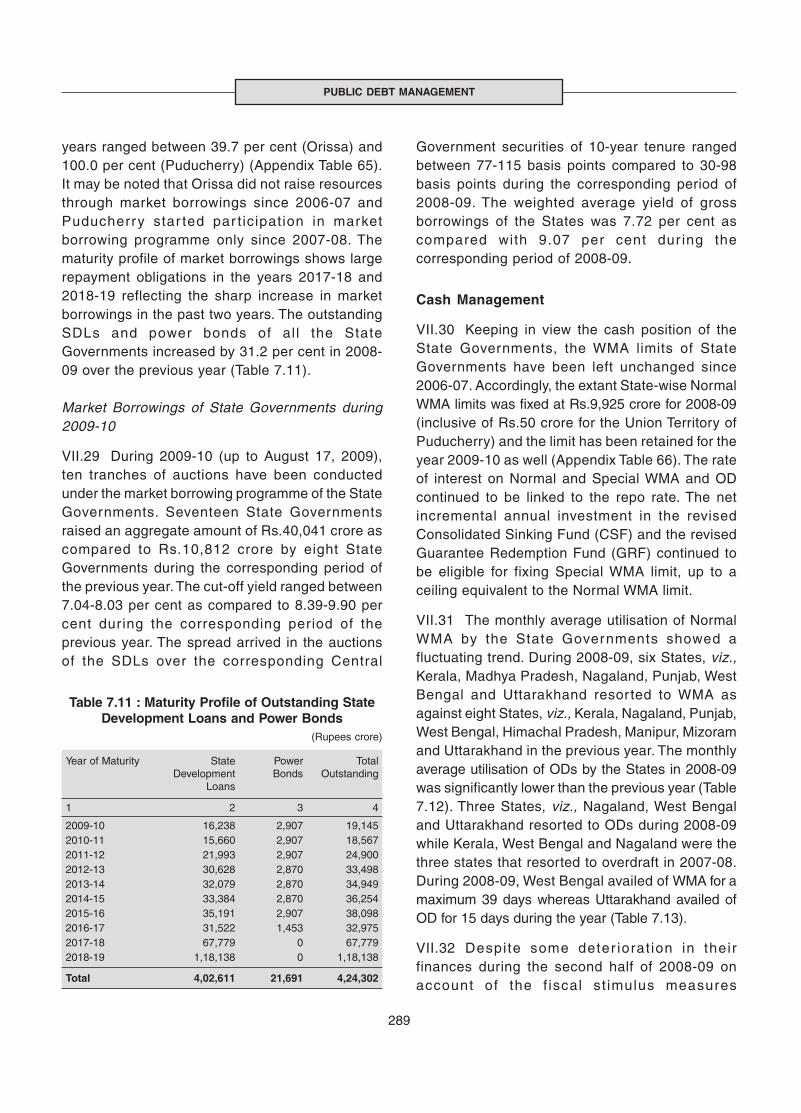

7.11 Maturity Profile of Outstanding State Development Loans and Power Bonds ................. 289

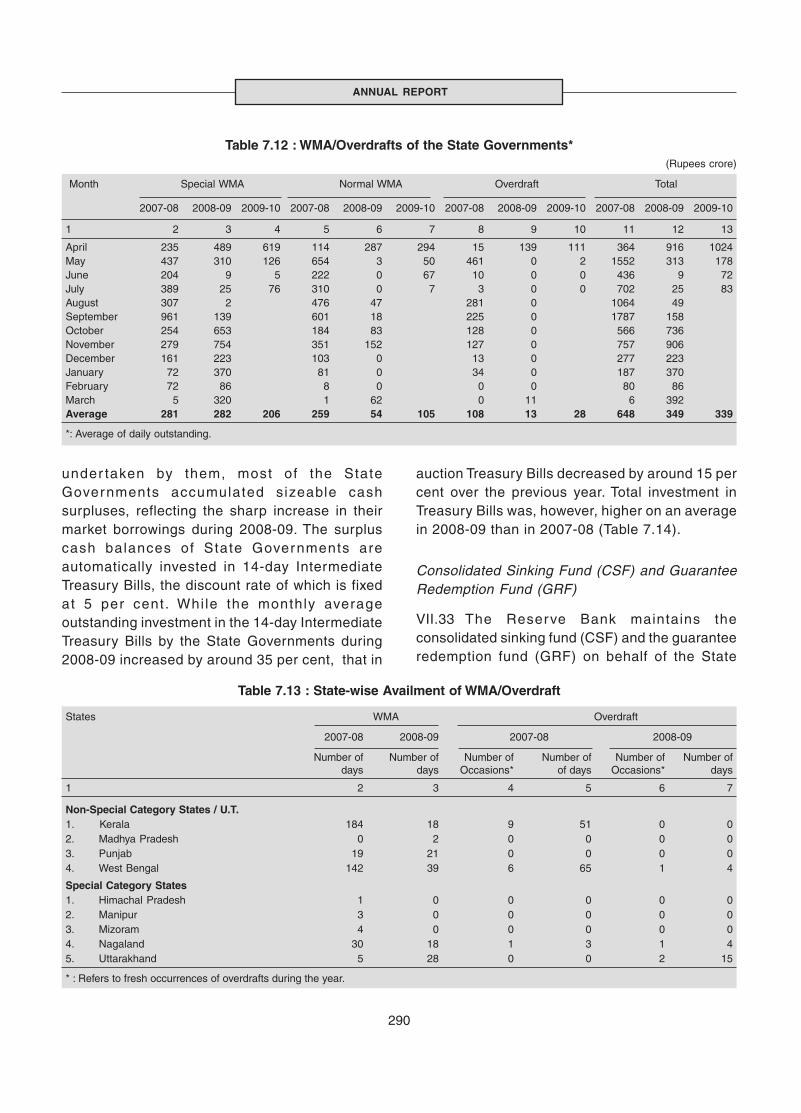

7.12 WMA/Overdrafts of the State Governments .................................................................... 290

7.13 State-wise Availment of WMA/Overdraft .......................................................................... 290

7.14 Investments of the State Governments/UT ...................................................................... 291

8.1 Banknotes in Circulation .................................................................................................. 294

8.2 Coins in Circulation .......................................................................................................... 295

8.3 Currency Chests ............................................................................................................... 295

8.4 Small Coin Depots ............................................................................................................ 296

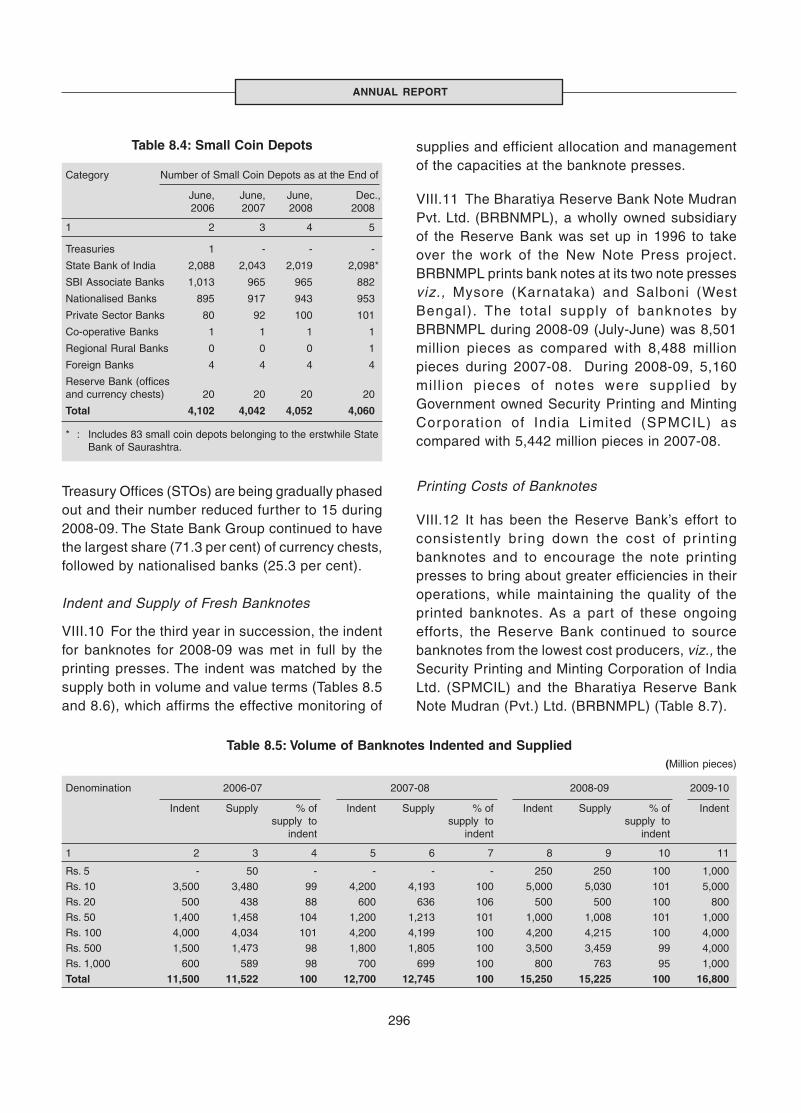

8.5 Volume of Banknotes Indented and Supplied .................................................................. 296

8.6 Value of Banknotes Indented and Supplied ..................................................................... 297

8.7 Supply and Cost of Banknotes ......................................................................................... 297

8.8 Indent and Supply of Coins (Volume) ............................................................................... 298

8.9 Indent and Supply of Coins (Value) .................................................................................. 298

8.10 Disposal of Soiled Notes and Supply of Fresh Banknotes............................................... 299

8.11 Counterfeit Notes Detected .............................................................................................. 299

8.12 Number of Counterfeit Notes Detected at the Reserve Bank and Bank Branches ......... 299

9.1 Payment System Indicators - Annual Turnover ................................................................ 304

9.2 Retail Electronic Funds Transfer Systems........................................................................ 307

xii

Page No.

CONTENTS

9.3 Card-Based Payment Transactions .................................................................................. 307

9.4 Evaluation of Critical IT Implementation: 2008-09 ........................................................... 314

10.1 Reserve Bank Training Establishments - Programmes Conducted ................................. 317

10.2 Select Programmes/ Seminars/ Workshops Conducted byTraining Colleges during 2008-09 .................................................................................... 318

10.3 Number of Officers Trained in External Training Institutions in India and Abroad ............ 319

10.4 Courses Conducted under Joint India- IMF Training Programme-Pune .......................... 319

10.5 Recruitment by the Reserve Bank - 2008 ........................................................................ 323

10.6 Staff Strength of Reserve Bank ....................................................................................... 324

10.7 Category-wise Actual Staff Strength (As on December 31, 2008) .................................. 325

10.8 Department-wise Staff Strength of the Reserve Bank ..................................................... 326

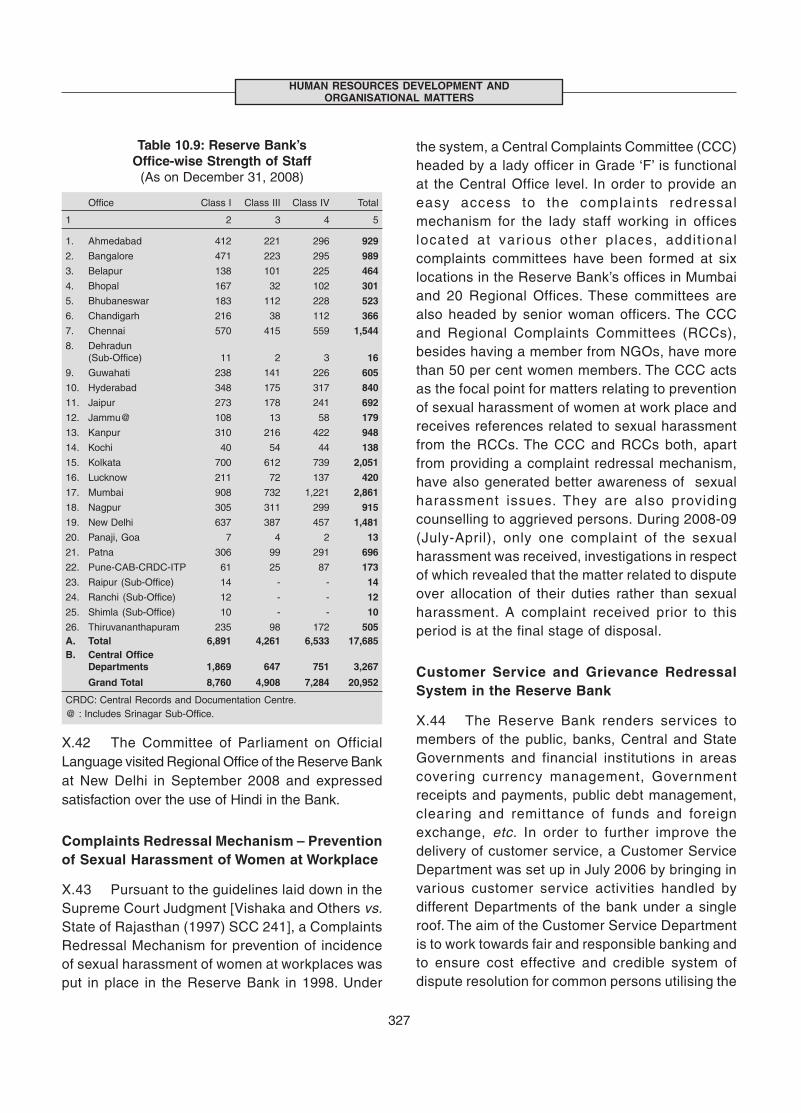

10.9 Reserve Bank’s Office-wise Strength of Staff .................................................................. 327

10.10 Right to Information Act, 2005 – Requests Received and Resolved during the year ...... 335

11.1 Trends in Gross Income, Expenditure and Net Disposable Income ................................ 348

11.2 Gross Income ................................................................................................................... 349

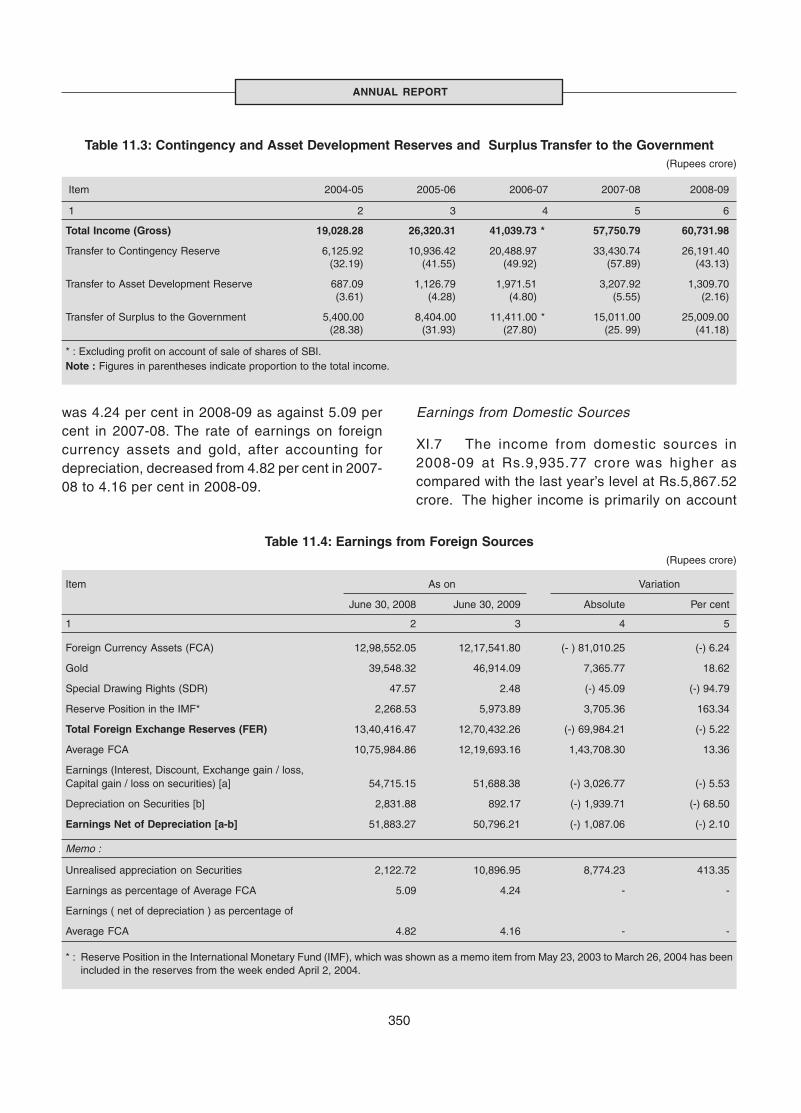

11.3 Contingency and Asset Development Reserves andSurplus Transfer to the Government ................................................................................ 350

11.4 Earnings from Foreign Sources ....................................................................................... 350

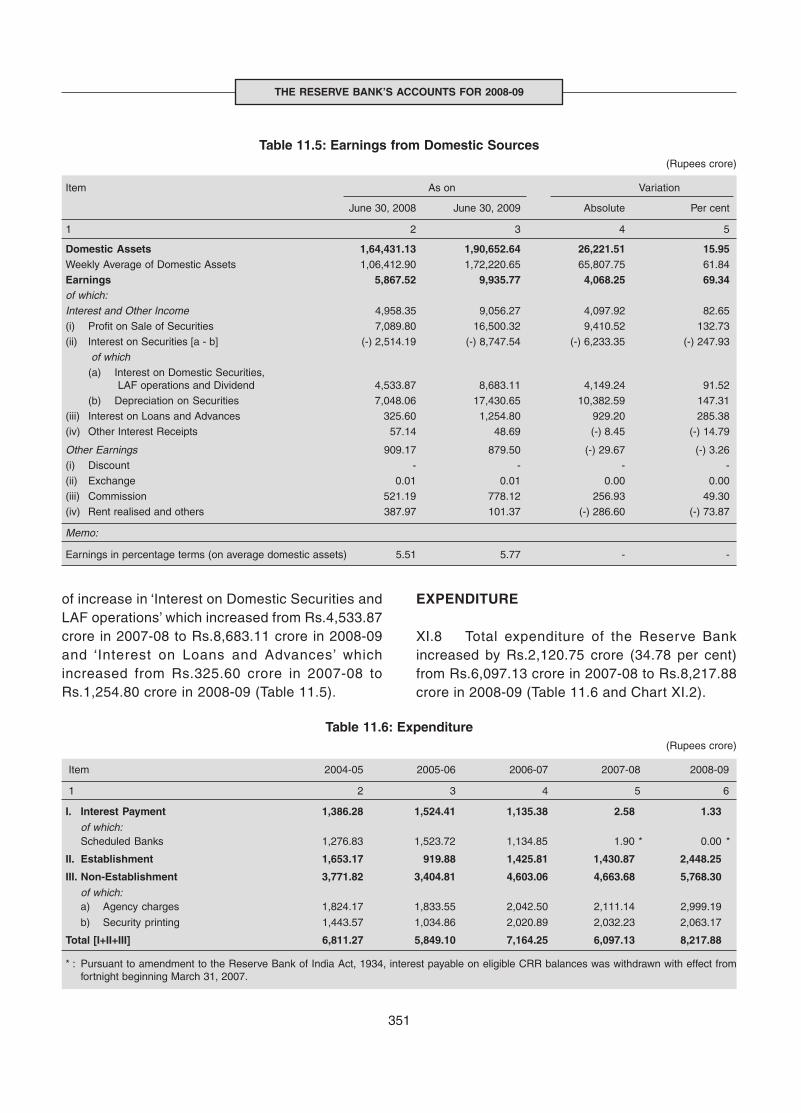

11.5 Earnings from Domestic Sources .................................................................................... 351

11.6 Expenditure ...................................................................................................................... 351

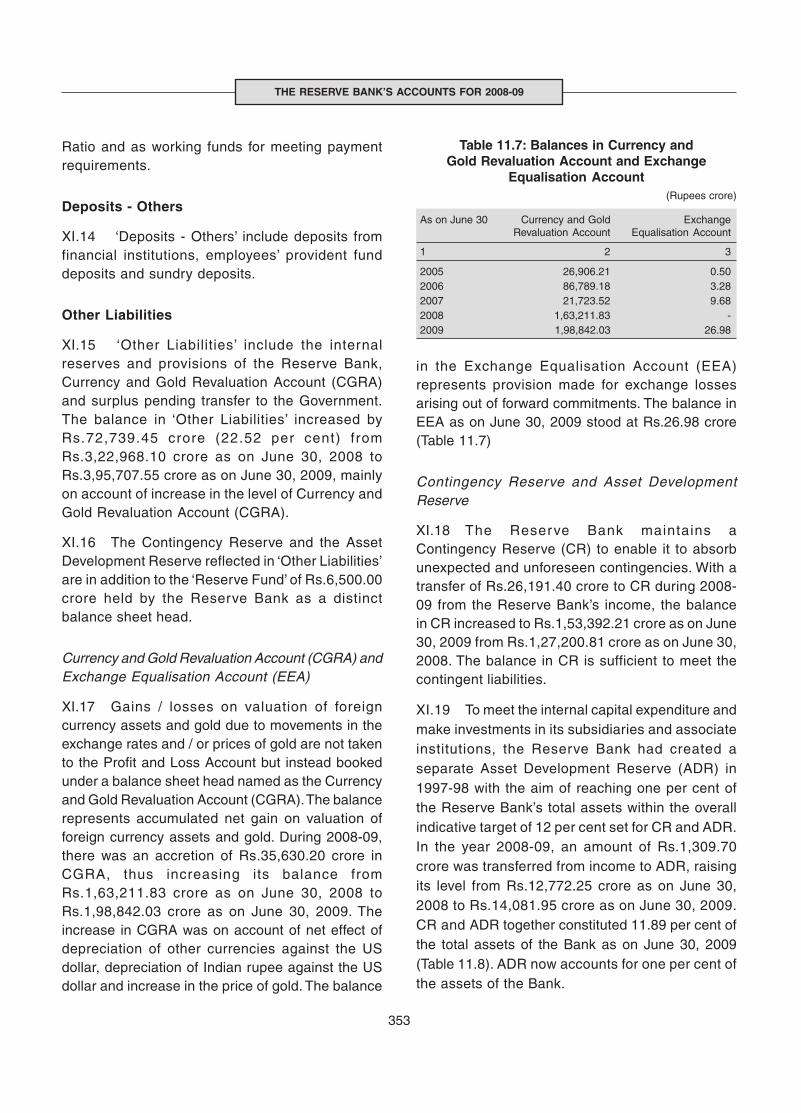

11.7 Balances in Currency and Gold Revaluation Account andExchange Equalisation Account ....................................................................................... 353

11.8 Balances in Contingency Reserve and Asset Development Reserve ............................. 354

11.9 Outstanding Foreign Currency and Domestic Assets ...................................................... 354

11.10 Investments in Shares of Subsidiaries/Associate Institutions .......................................... 354

APPENDIX TABLES

1 Select Macroeconomic and Financial Indicators.............................................................. 399

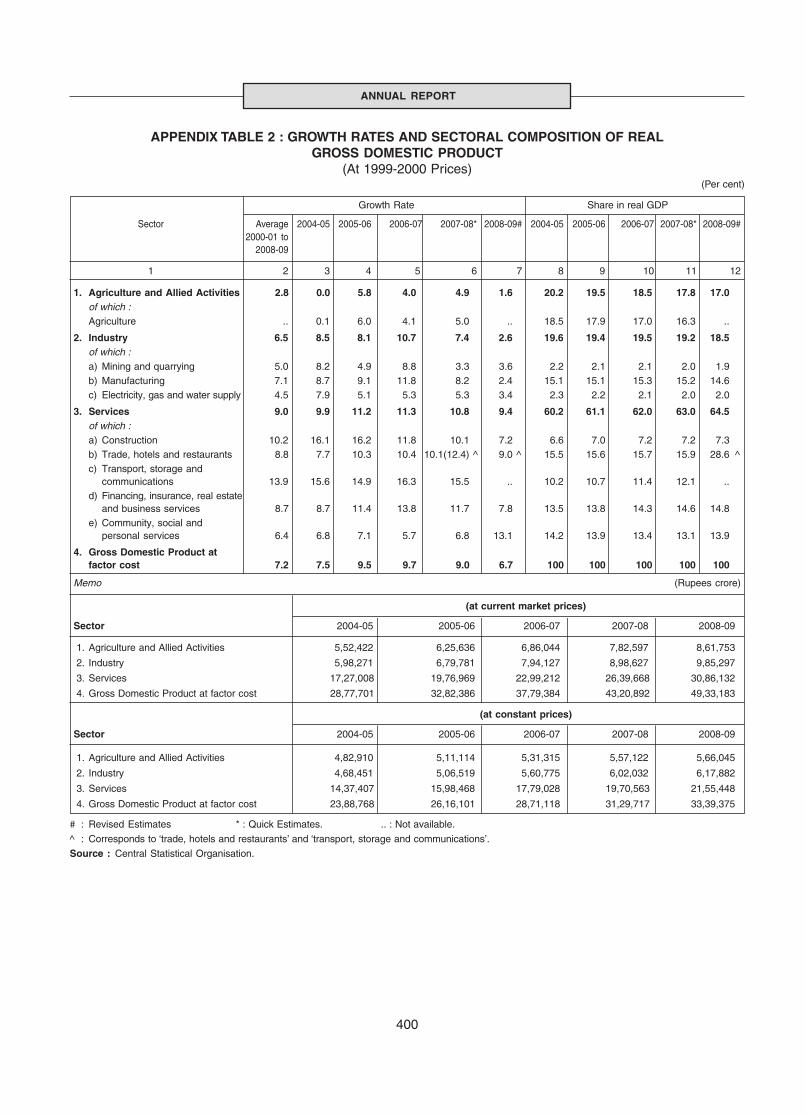

2 Growth Rates and Sectoral Composition ofReal Gross Domestic Product (At 1999-2000 prices) ...................................................... 400

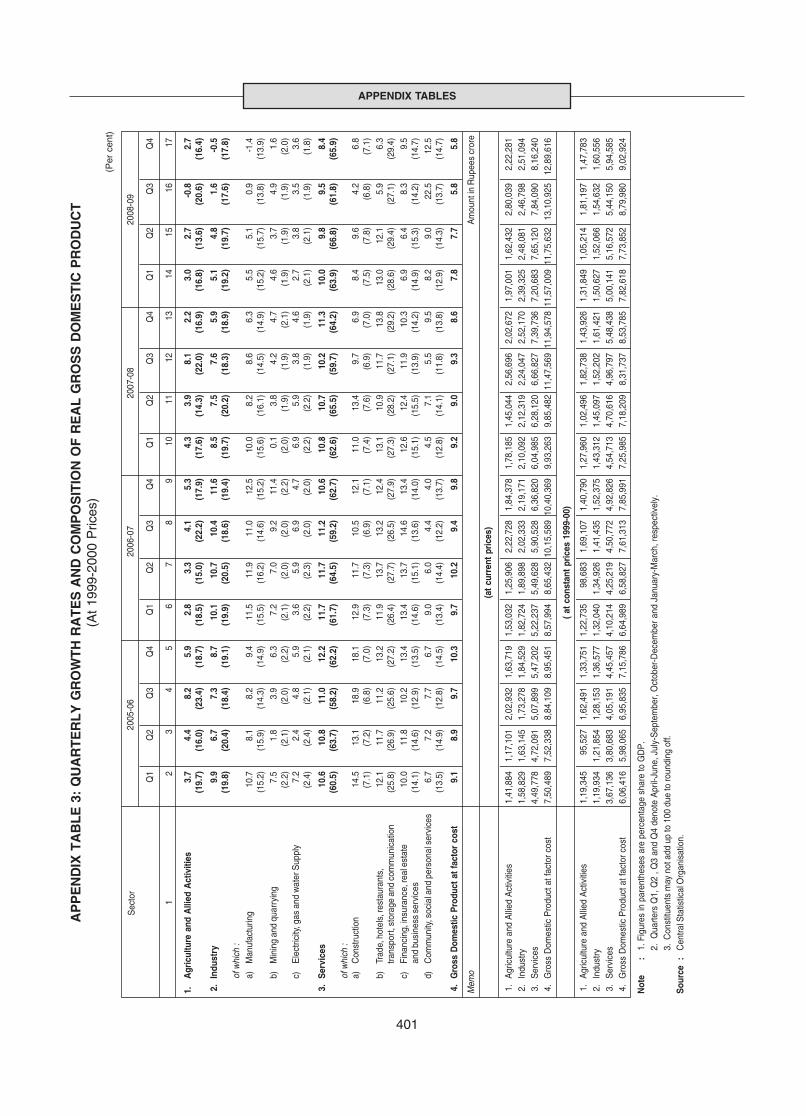

3 Quarterly Growth Rates and Composition of Real Gross Domestic Product(At 1999-2000 prices) ....................................................................................................... 401

4 Agricultural Production ..................................................................................................... 402

5 Procurement, Off-take and Stocks of Foodgrains ............................................................ 403

6 Trends in Index of Industrial Production (Base: 1993-94=100) ........................................ 404

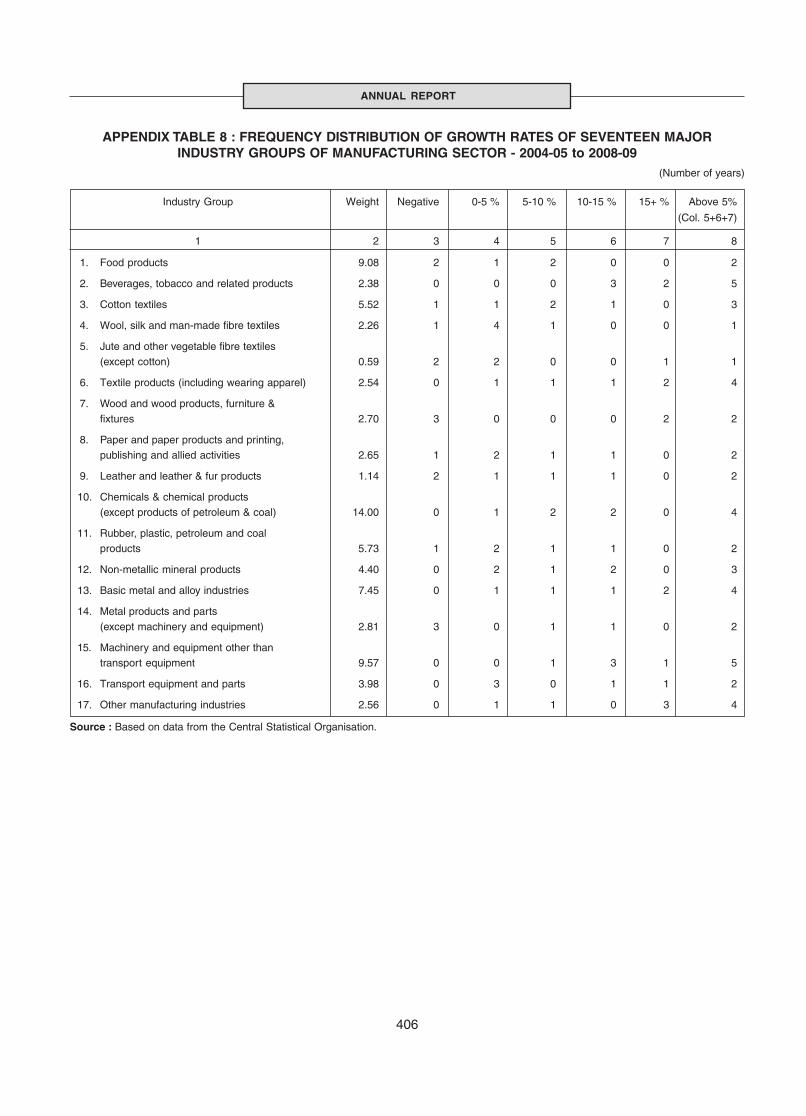

7 Growth in Index of Seventeen Major Industry Groups of Manufacturing Sector(Base : 1993-94=100) ....................................................................................................... 405

8 Frequency Distribution of Growth Rates of Seventeen Major IndustryGroup of Manufacturing Sector - 2004-05 to 2008-09 ..................................................... 406

xiii

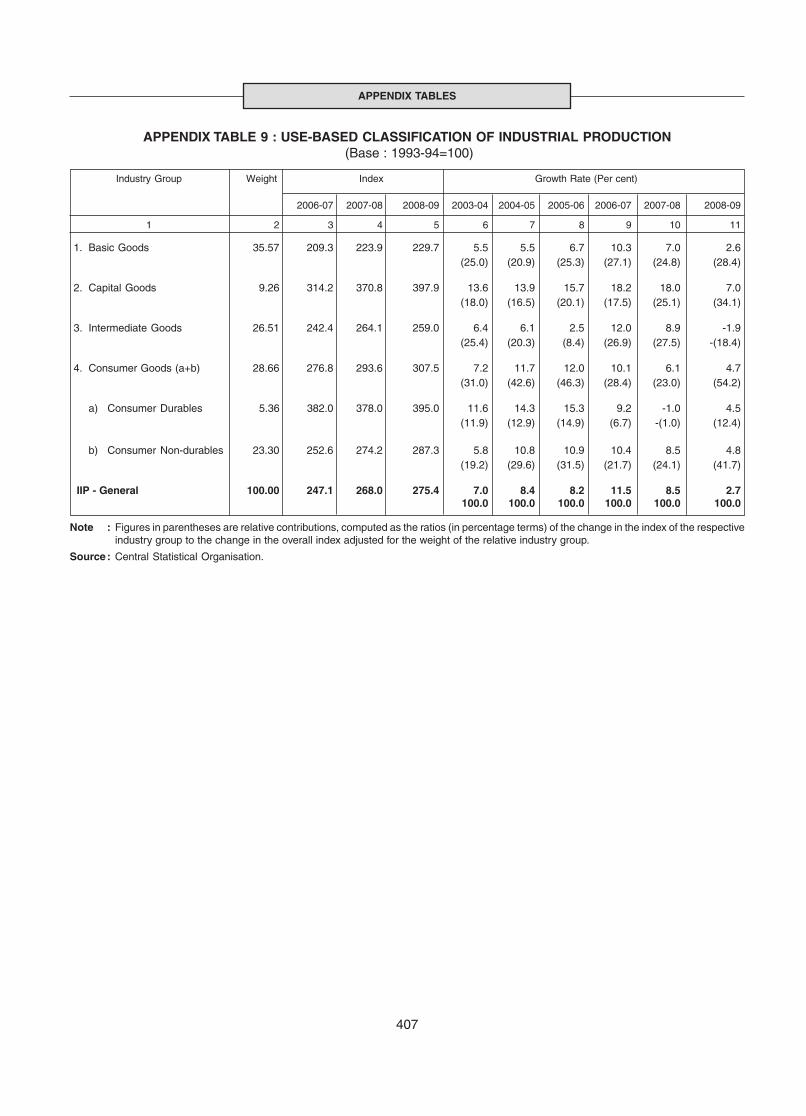

9 Use-Based Classification of Industrial Production (Base: 1993-94=100) ........................ 407

10 Growth of Six Infrastructure Industries (Base: 1993-94=100) ......................................... 408

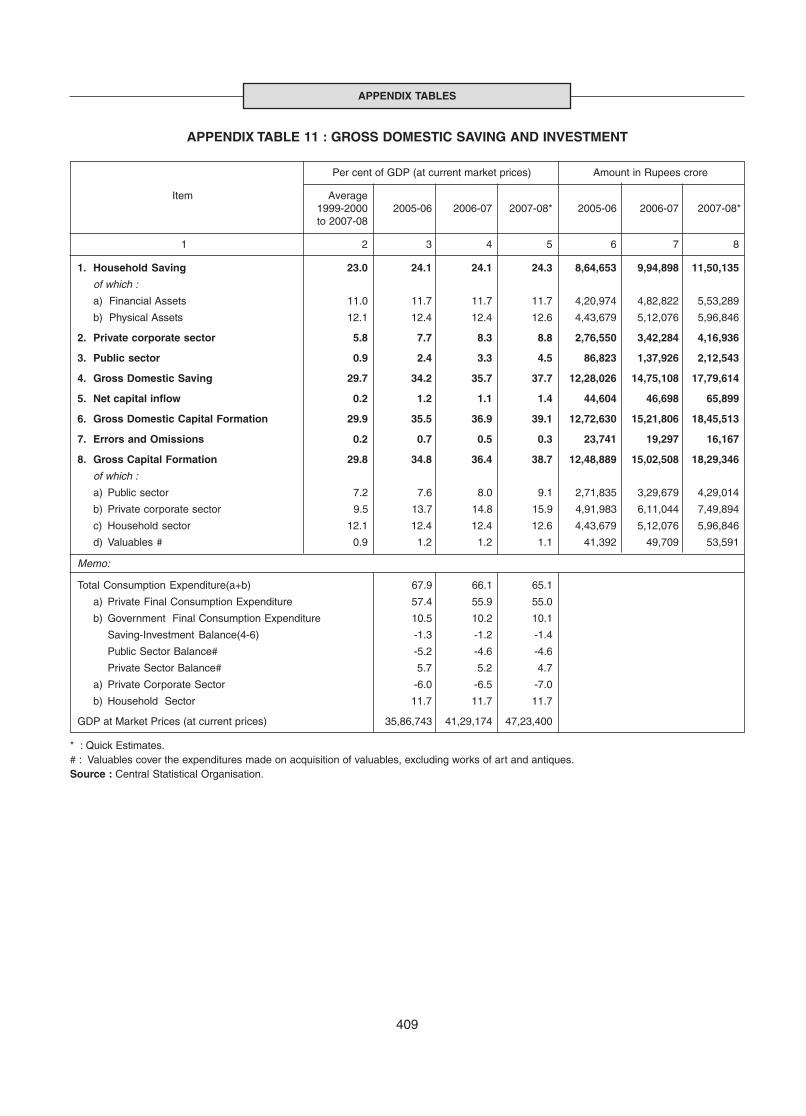

11 Gross Domestic Saving and Investment .......................................................................... 409

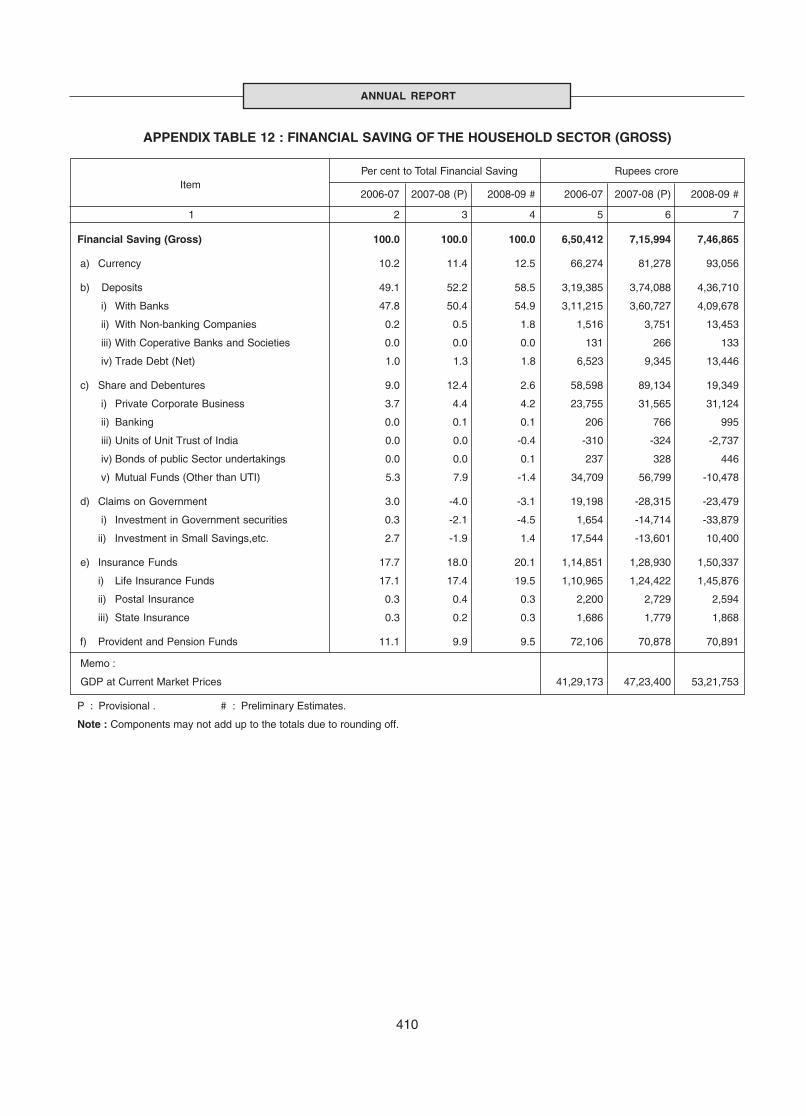

12 Financial Saving of the Household Sector (Gross) .......................................................... 410

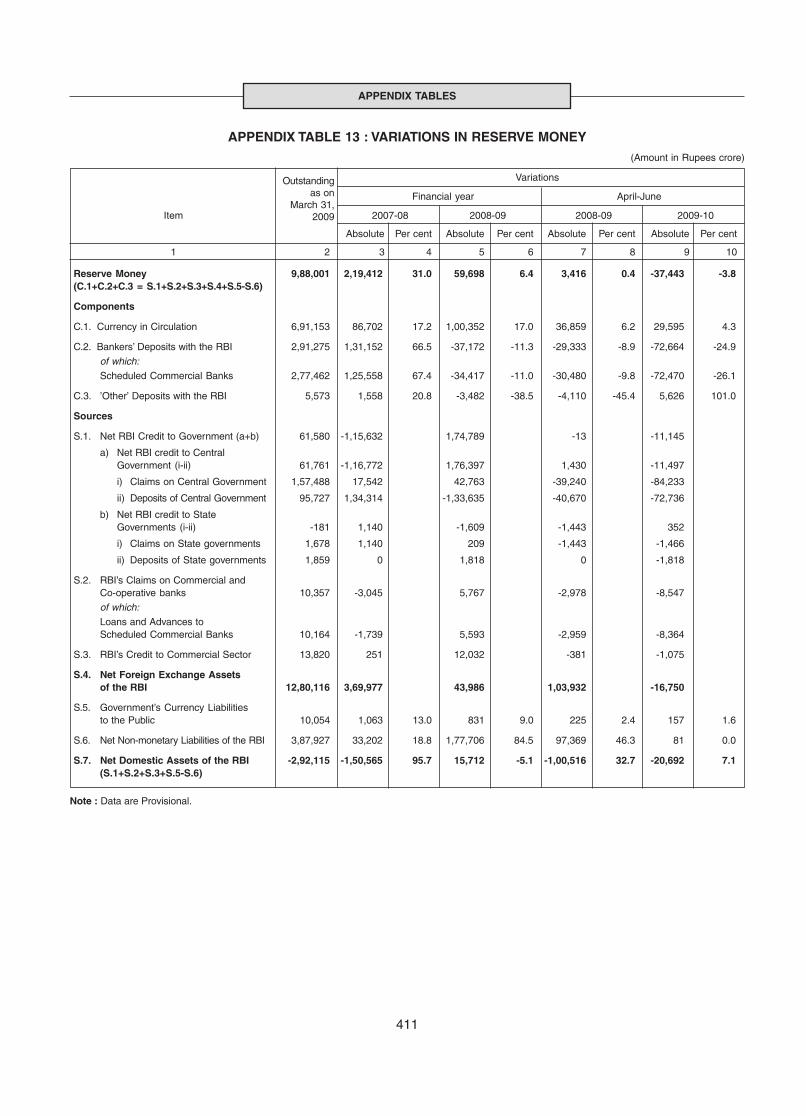

13 Variations in Reserve Money ........................................................................................... 411

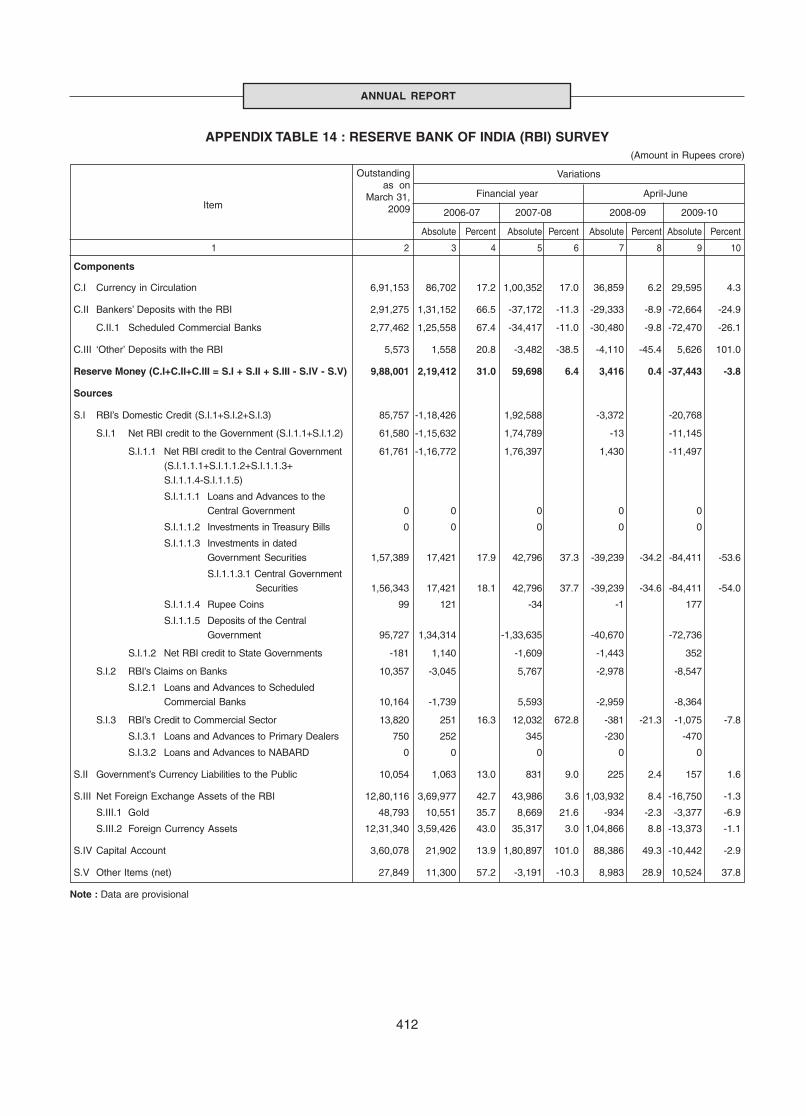

14 Reserve Bank of India (RBI) Survey ................................................................................ 412

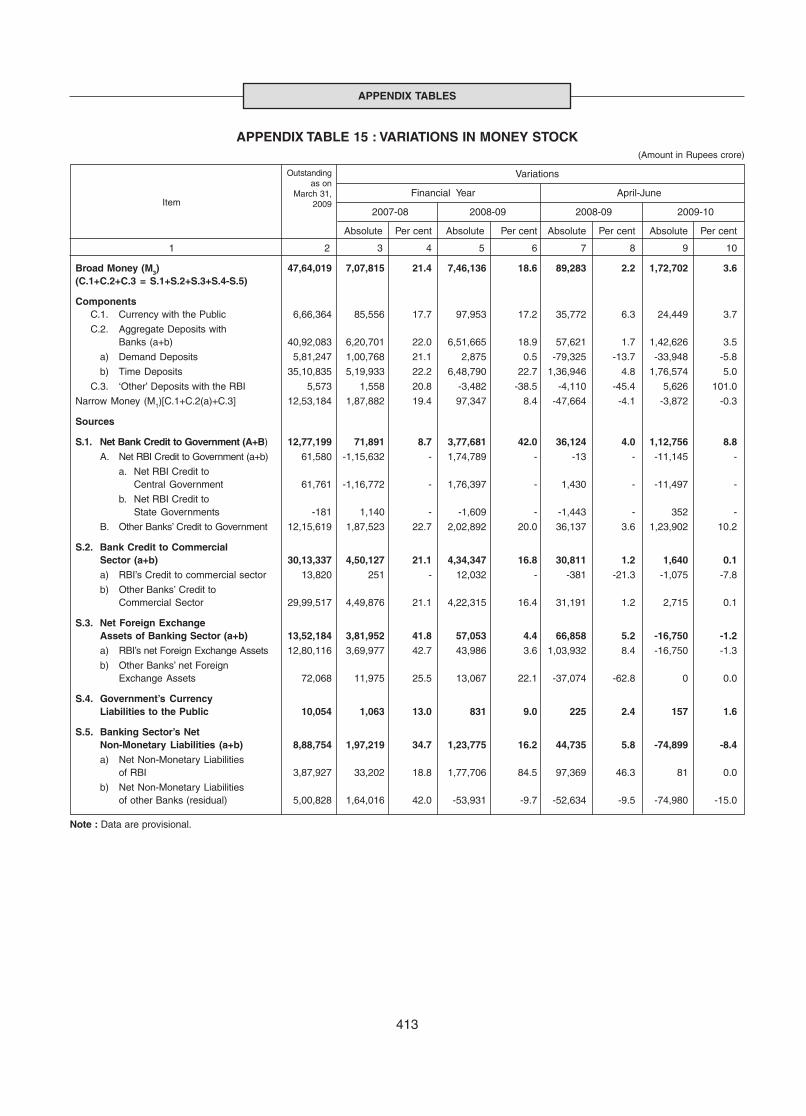

15 Variations in Money Stock ................................................................................................ 413

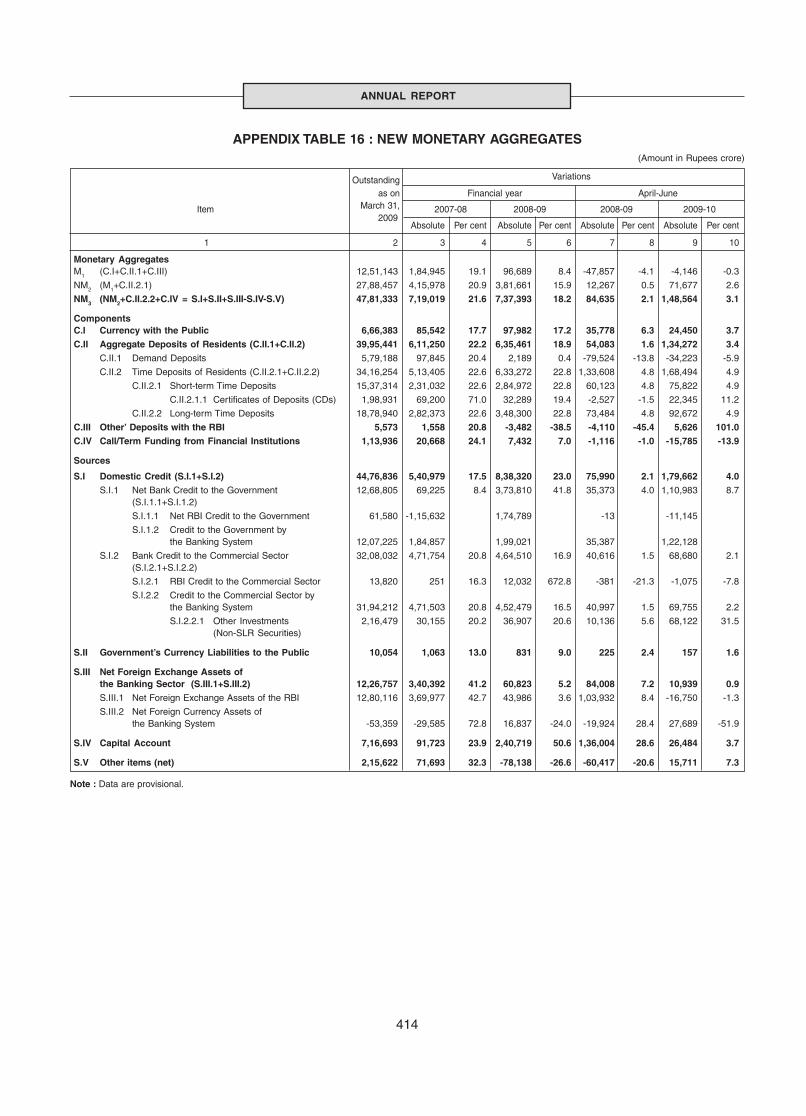

16 New Monetary Aggregates ............................................................................................... 414

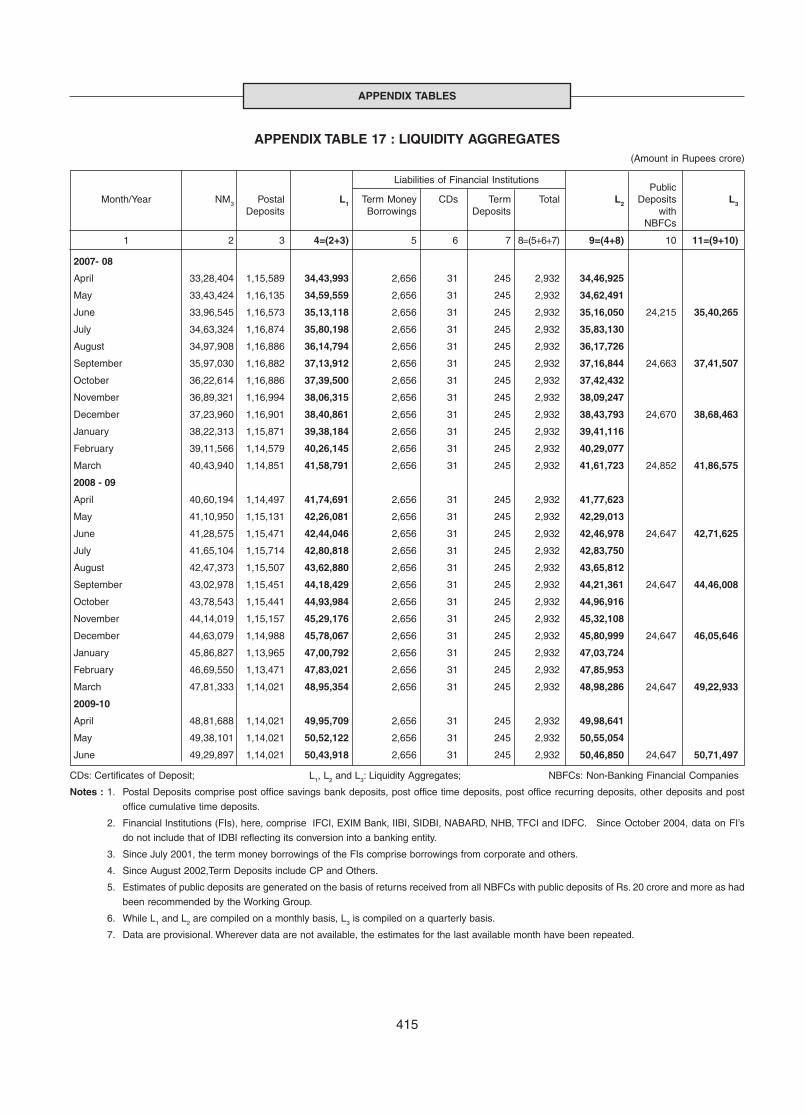

17 Liquidity Aggregates ......................................................................................................... 415

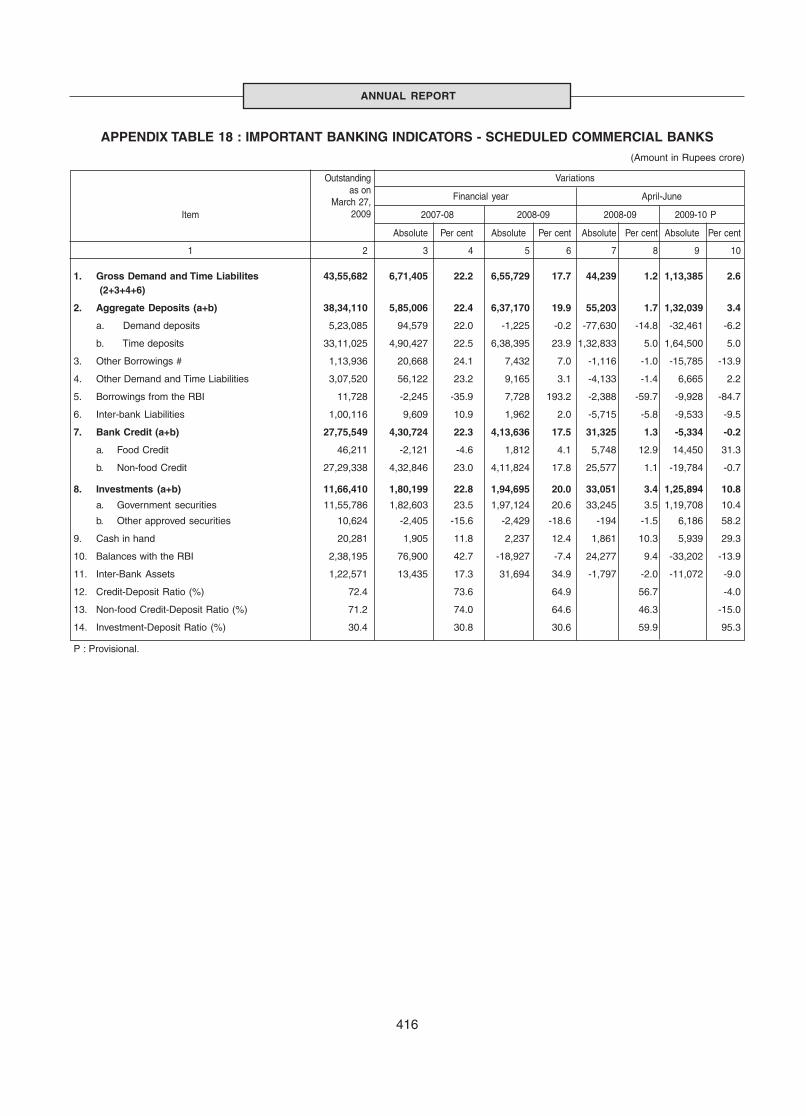

18 Important Banking Indicators - Scheduled Commercial Banks ....................................... 416

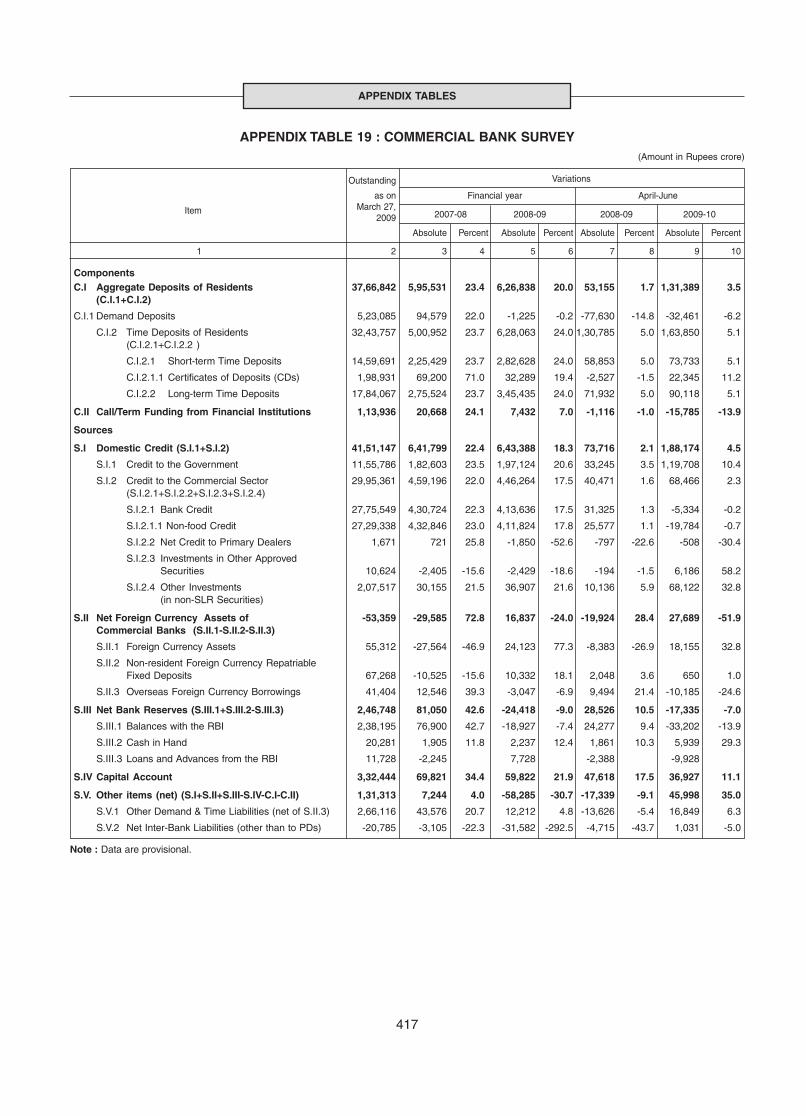

19 Commercial Bank Survey ................................................................................................. 417

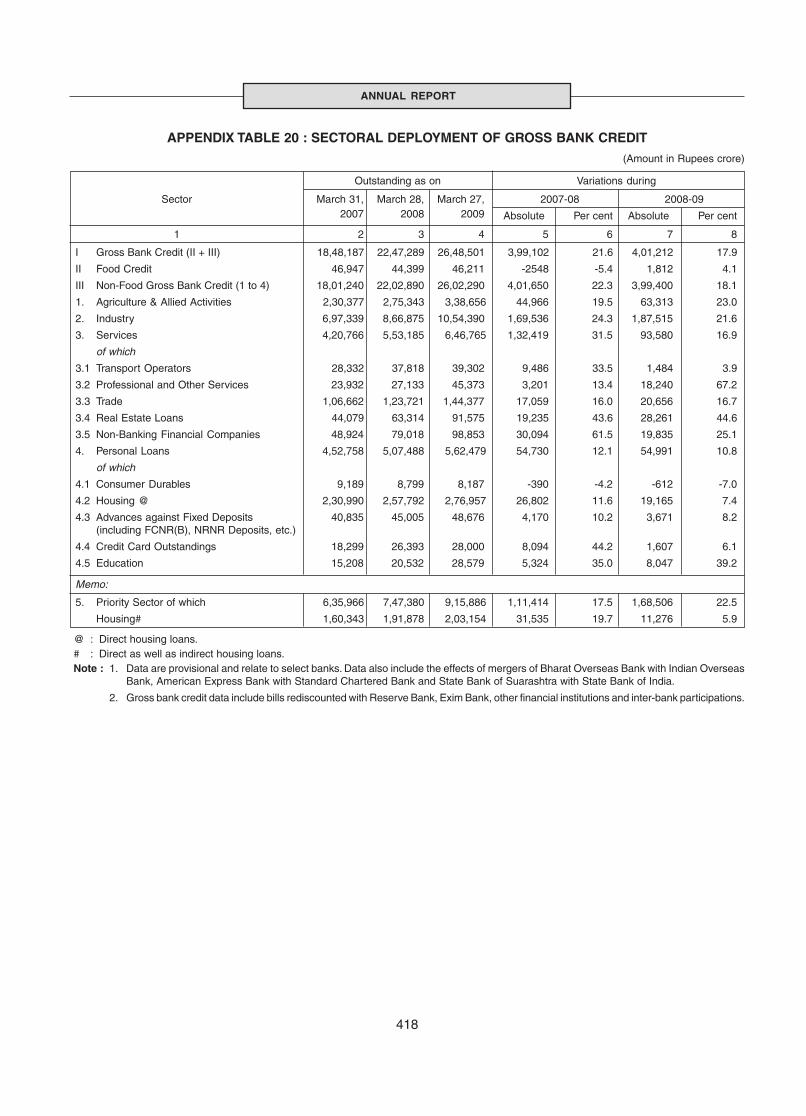

20 Sectoral Deployment of Gross Bank Credit ..................................................................... 418

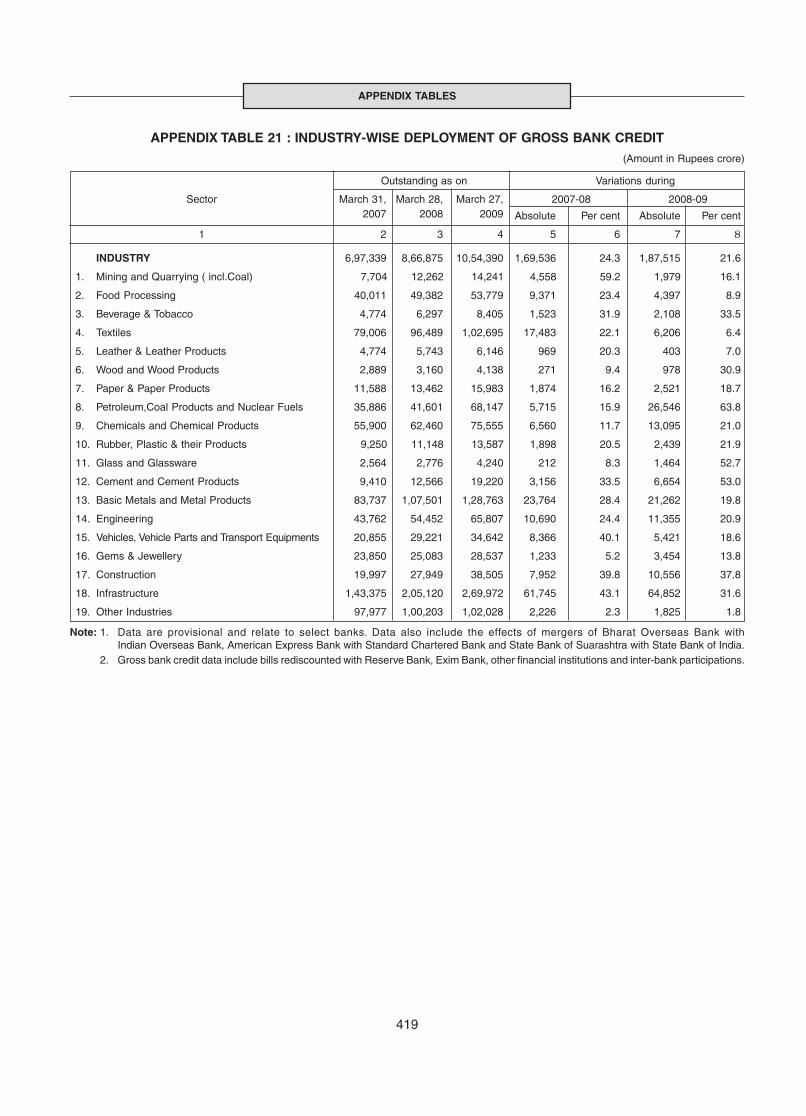

21 Industry-Wise Deployment of Gross Bank Credit ............................................................ 419

22 Reserve Bank’s Accommodation to Scheduled Commercial Banks ................................ 420

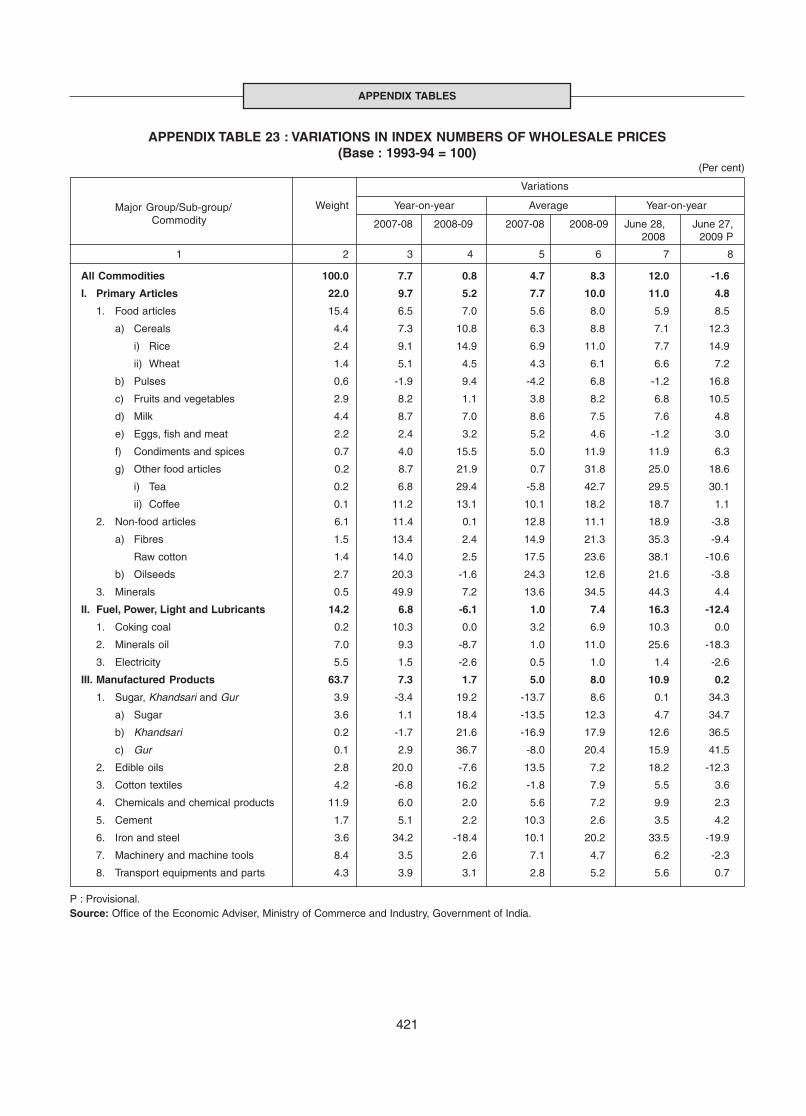

23 Variations in Index Numbers of Wholesale Prices ........................................................... 421

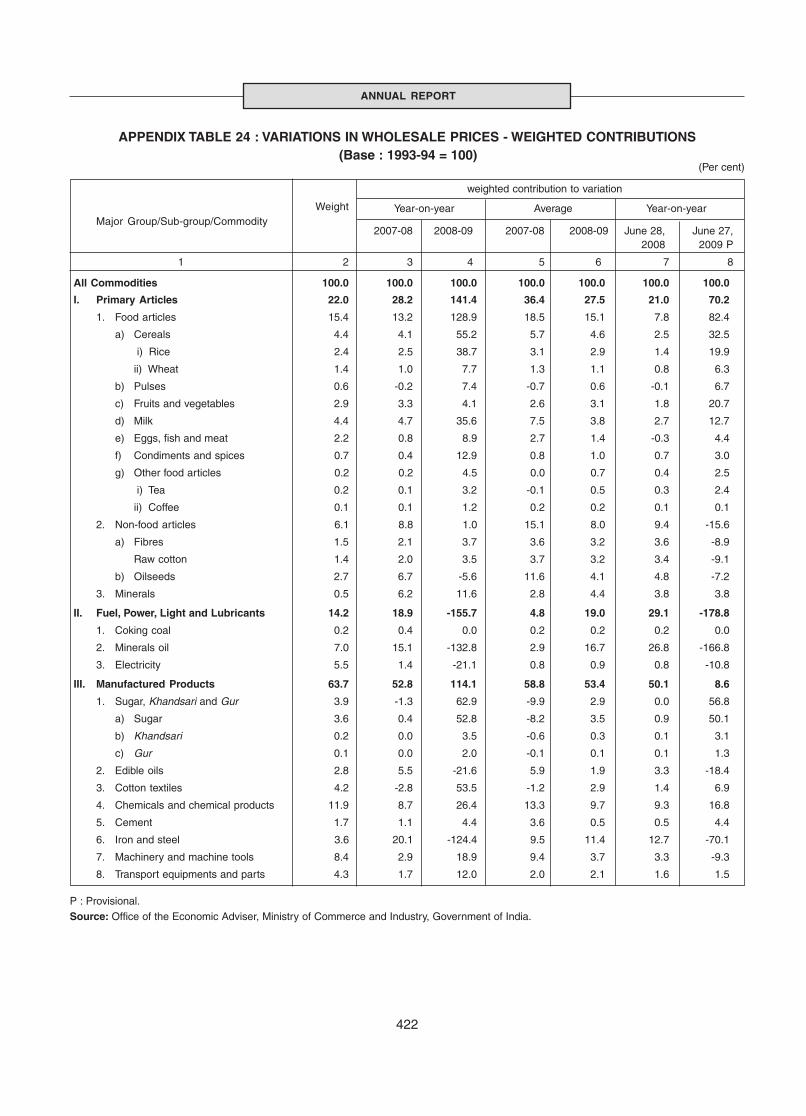

24 Variations in Wholesale Prices - Weighted Contributions ................................................ 422

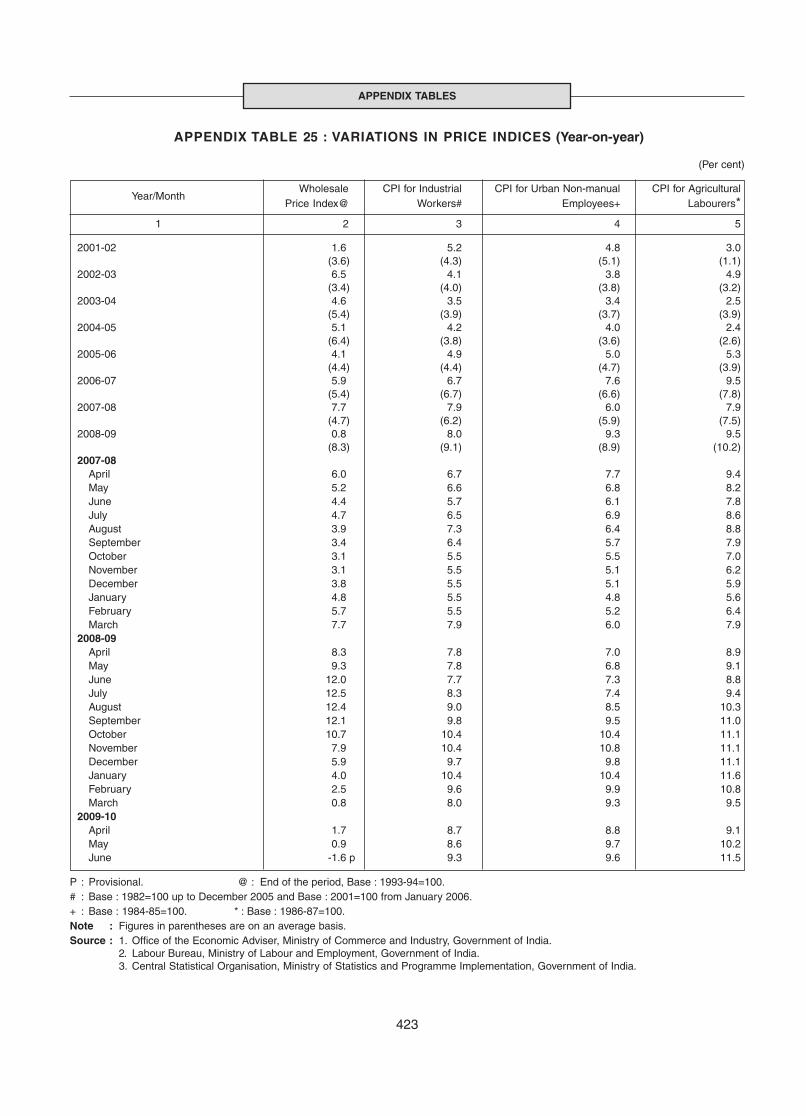

25 Variations in Price Indices (Year-on-Year) ........................................................................ 423

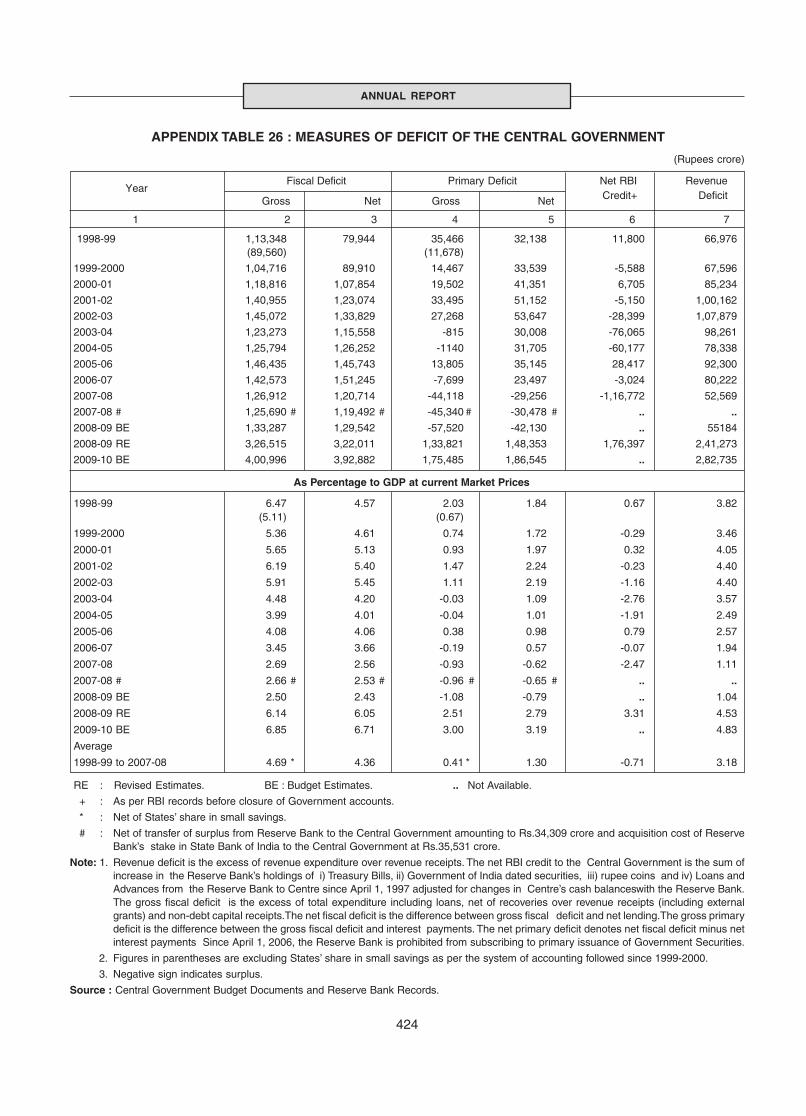

26 Measures of deficit of the Central Government ............................................................... 424

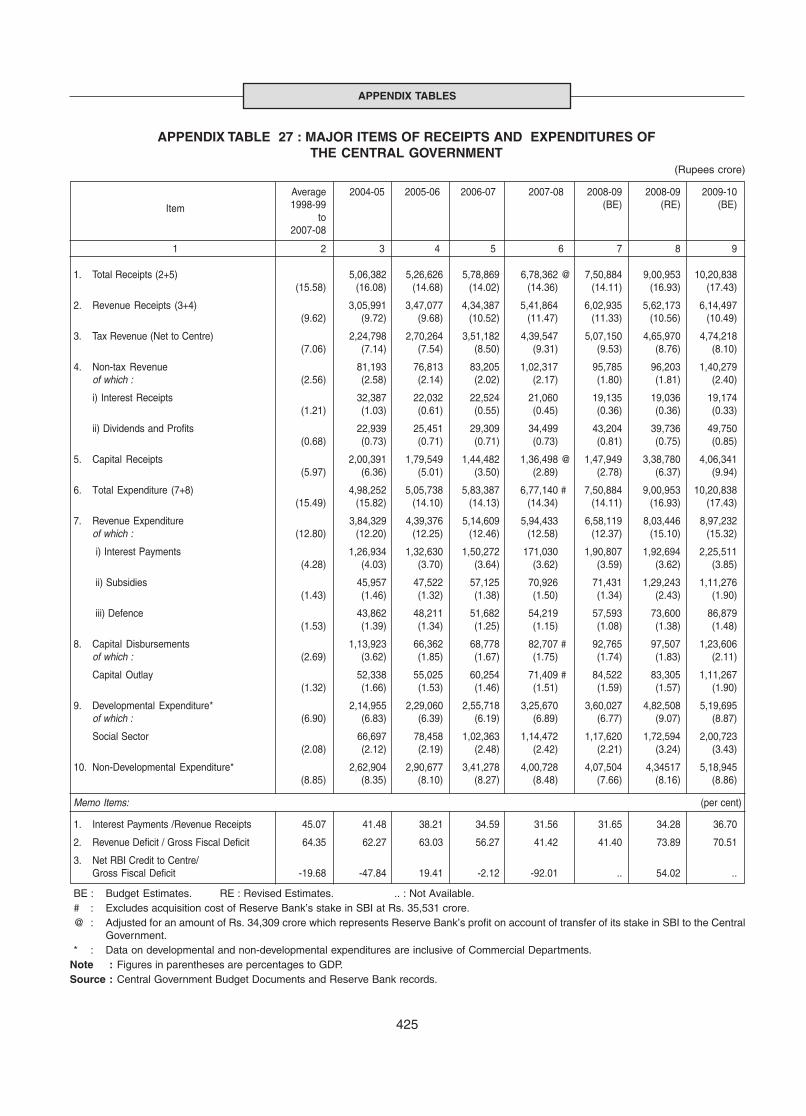

27 Major Items of Receipts and Expenditures of the Central Government .......................... 425

28 Financing of Gross Fiscal Deficit of the Central Government .......................................... 426

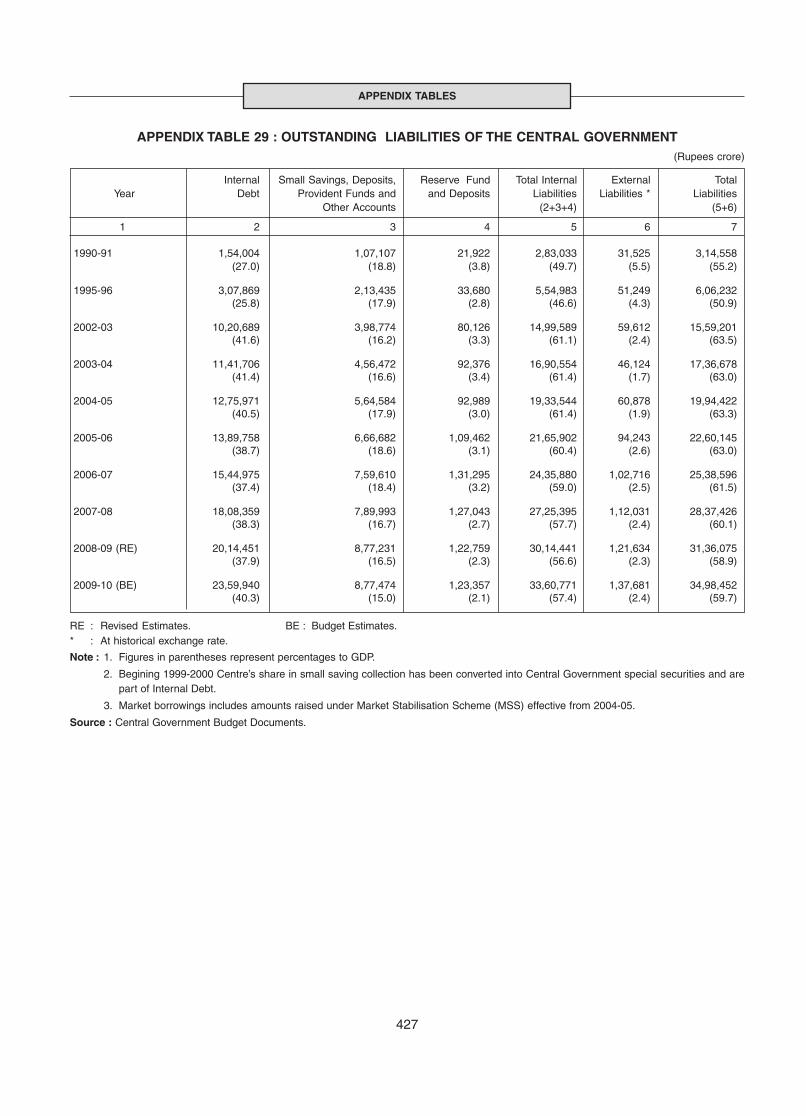

29 Outstanding Liabilities of the Central Government .......................................................... 427

30 Budgetary Operations of the State Governments ............................................................ 428

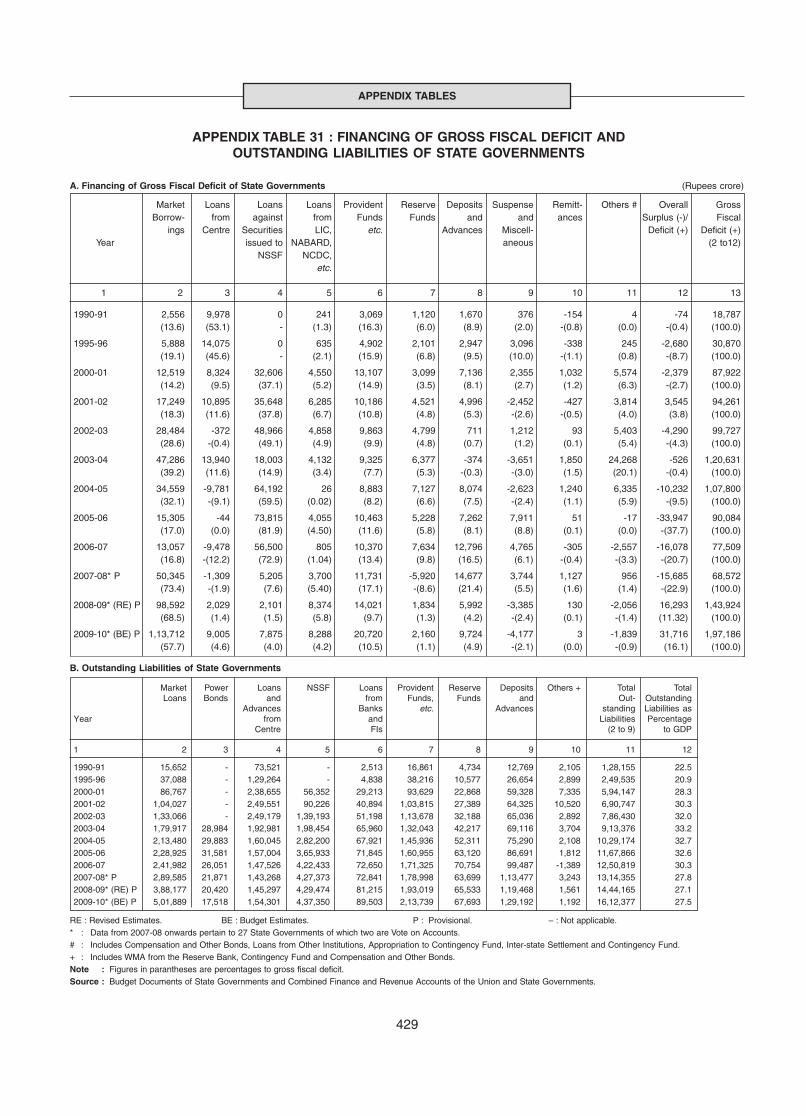

31 Financing of Gross Fiscal Deficit andOutstanding Liabilities of State Governments .................................................................. 429

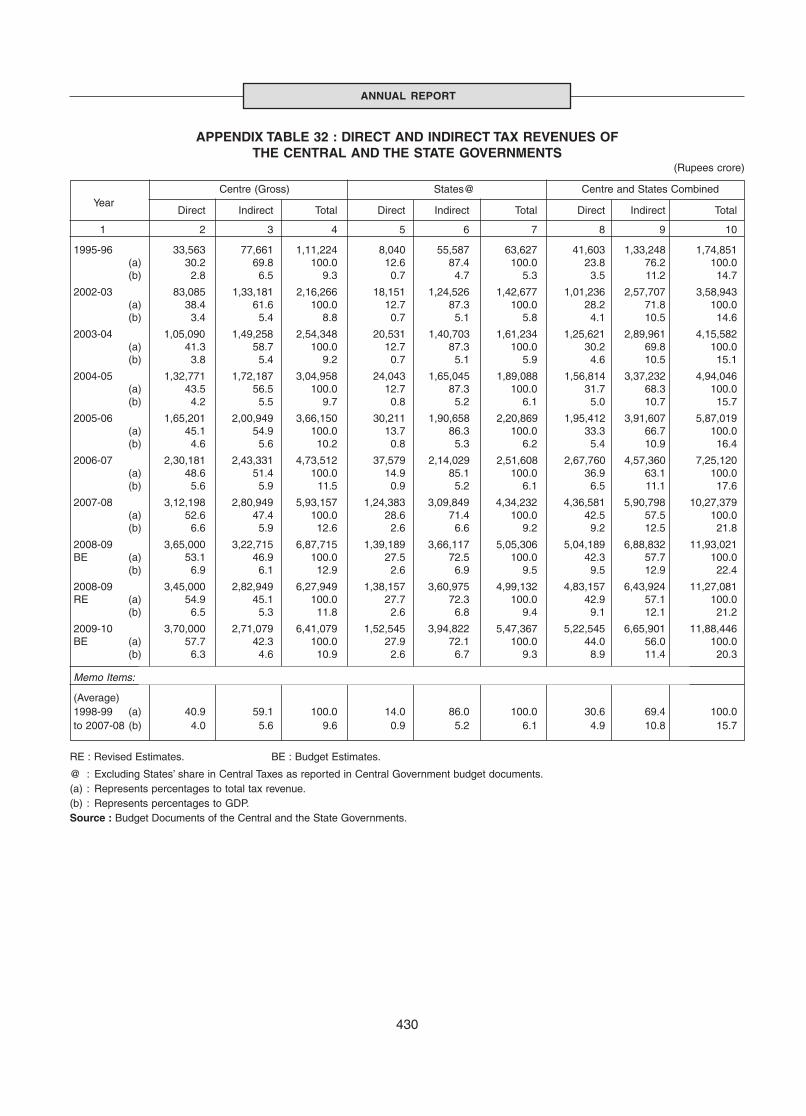

32 Direct and Indirect Tax Revenues of the Central and the State Governments ................ 430

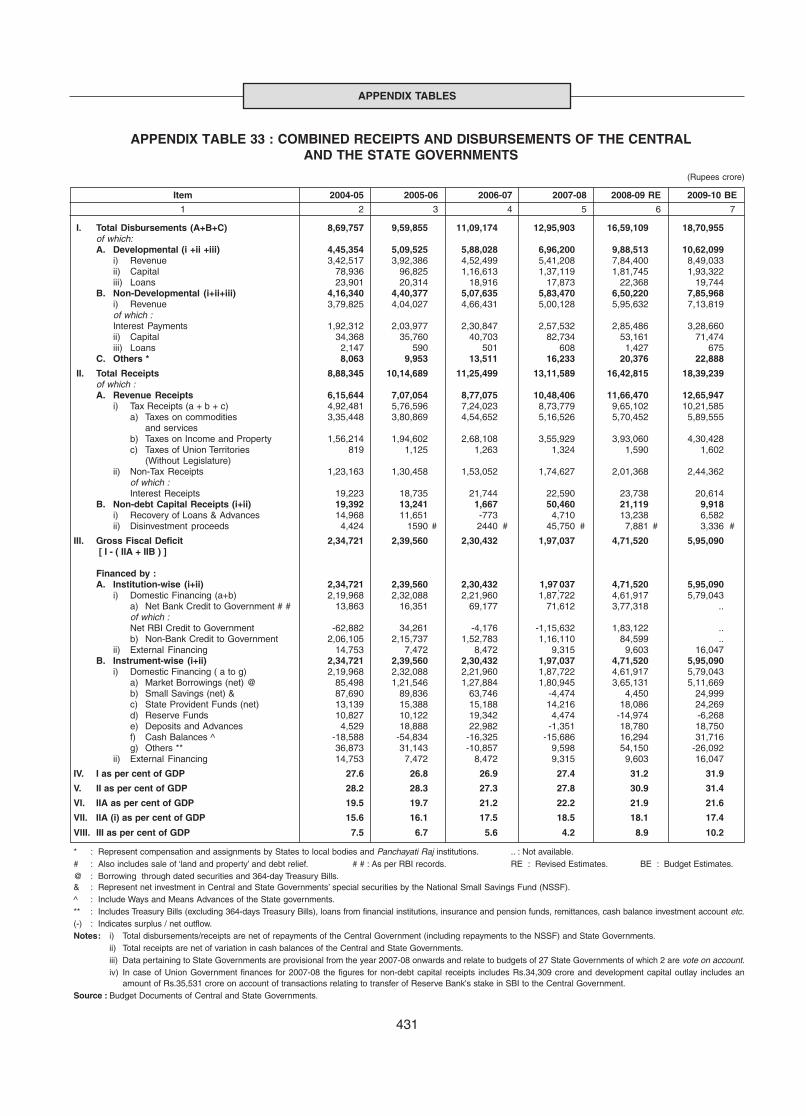

33 Combined Receipts and Disbursements of the Central and State Governments ........... 431

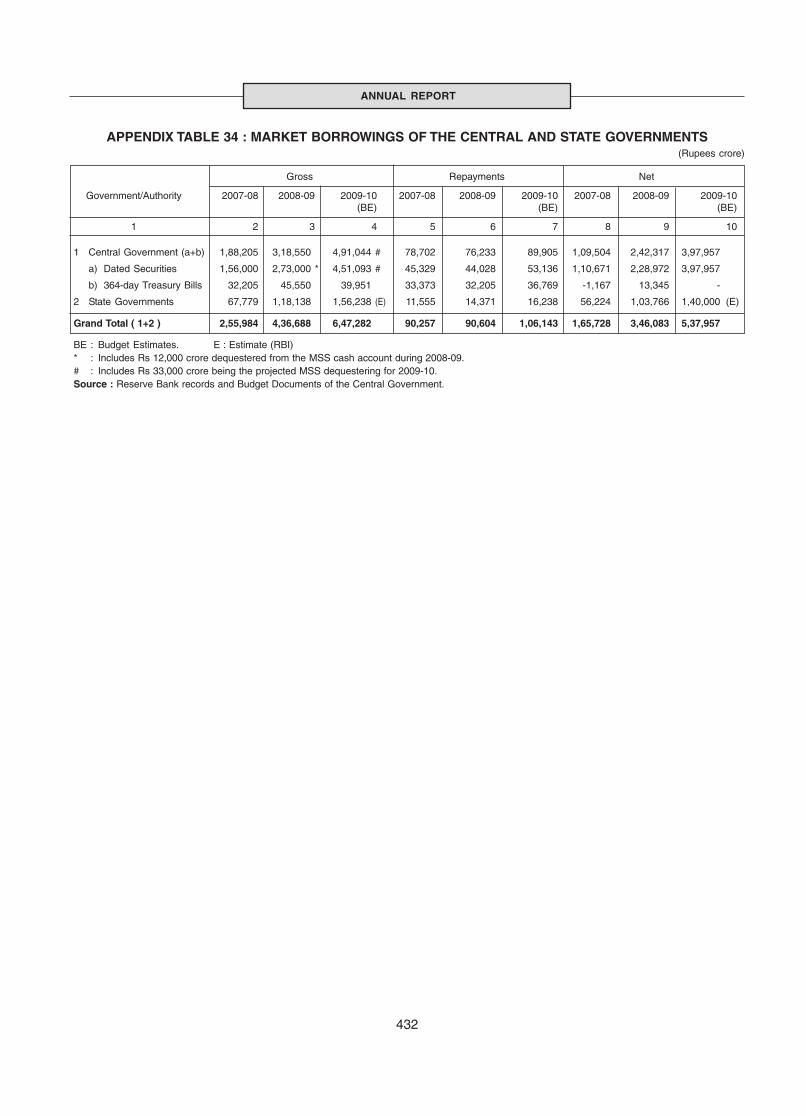

34 Market Borrowings of the Central and State Governments ............................................. 432

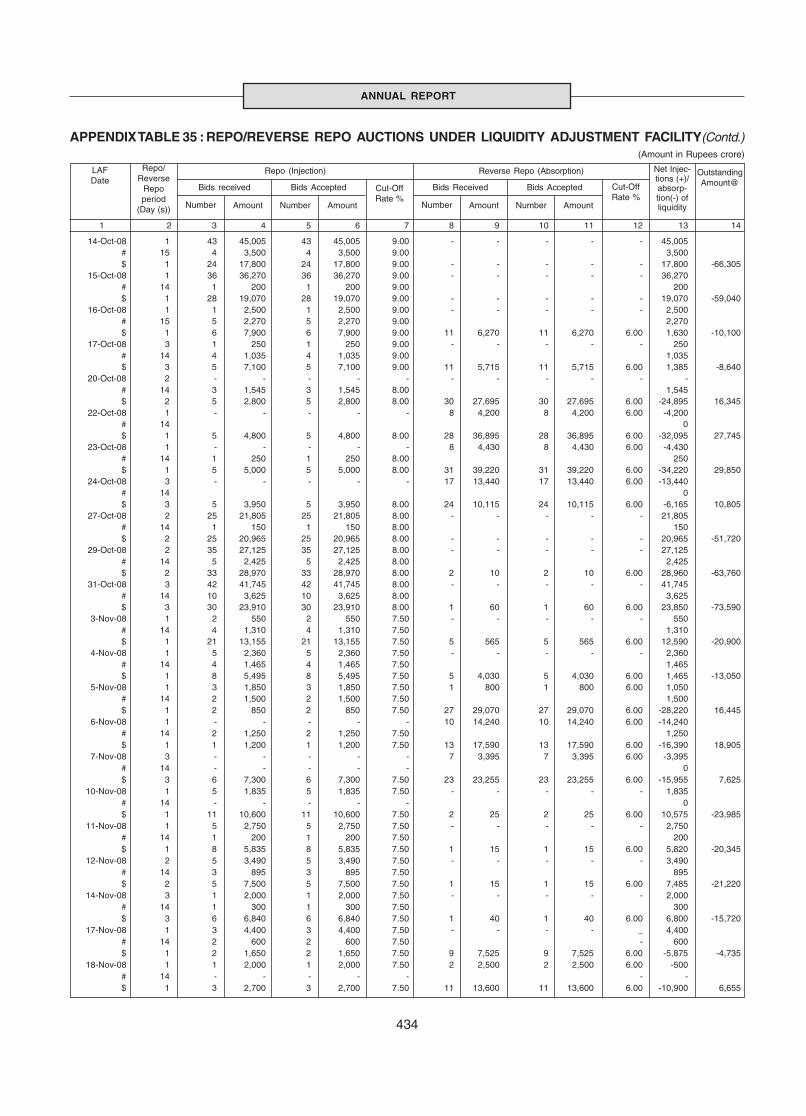

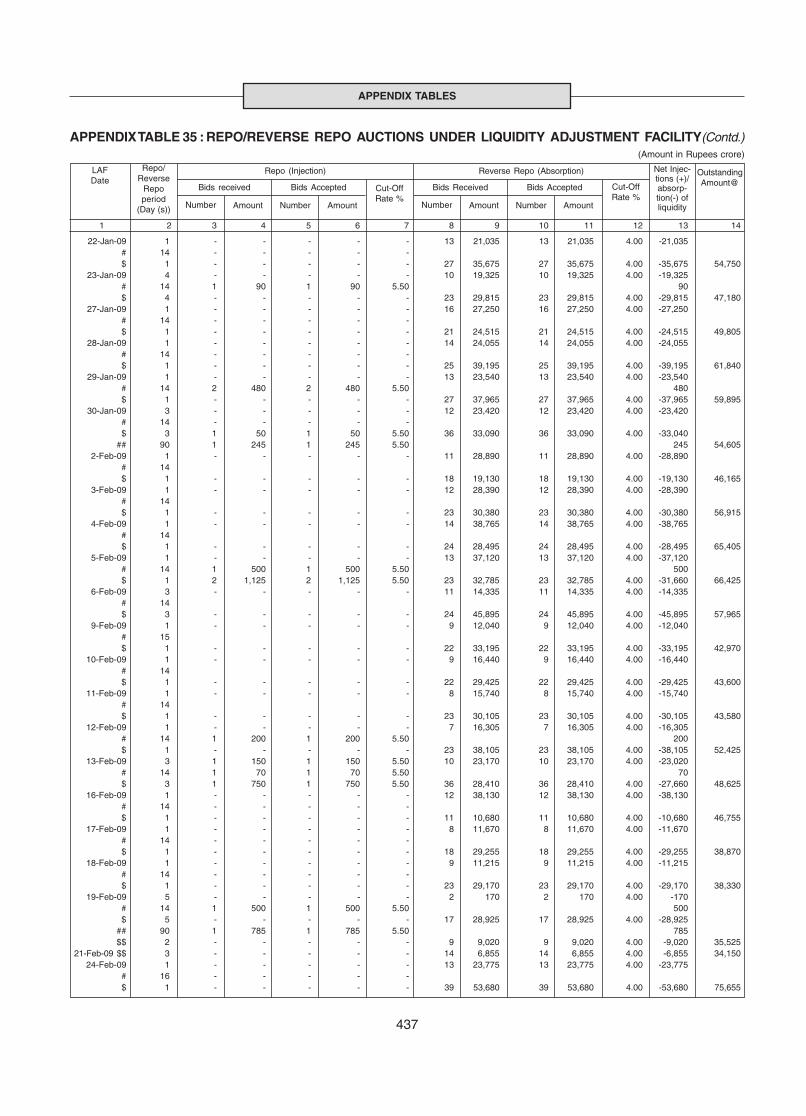

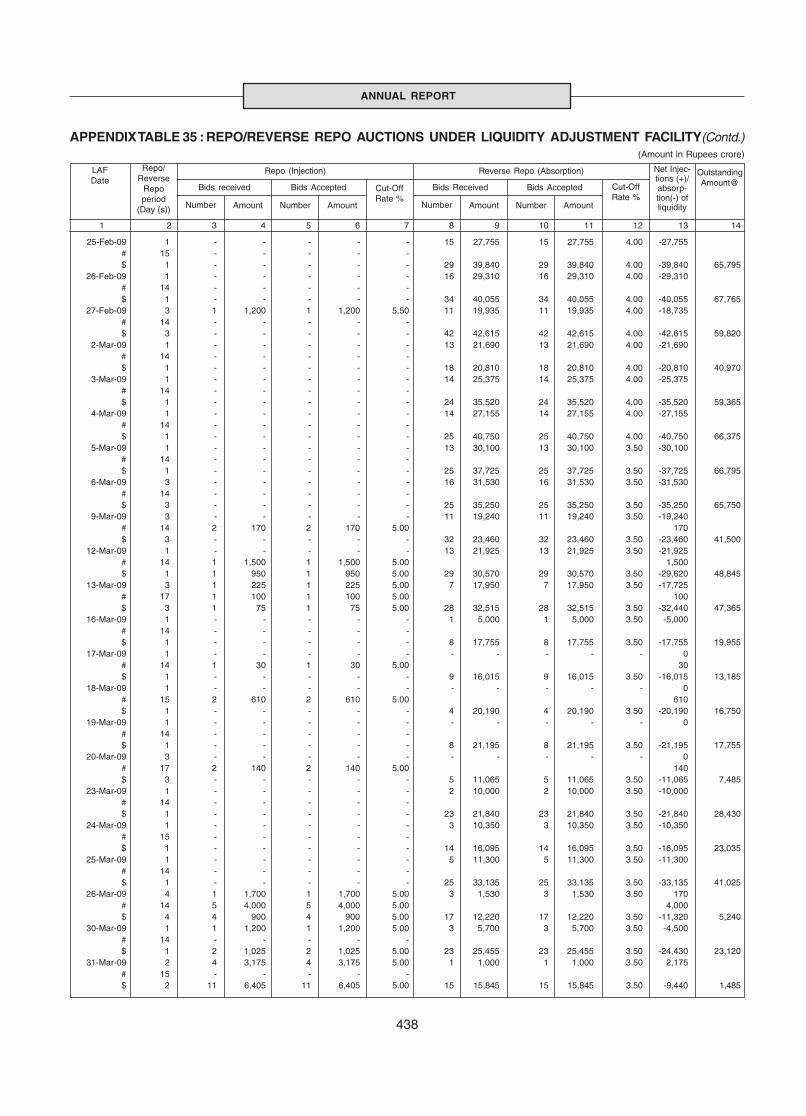

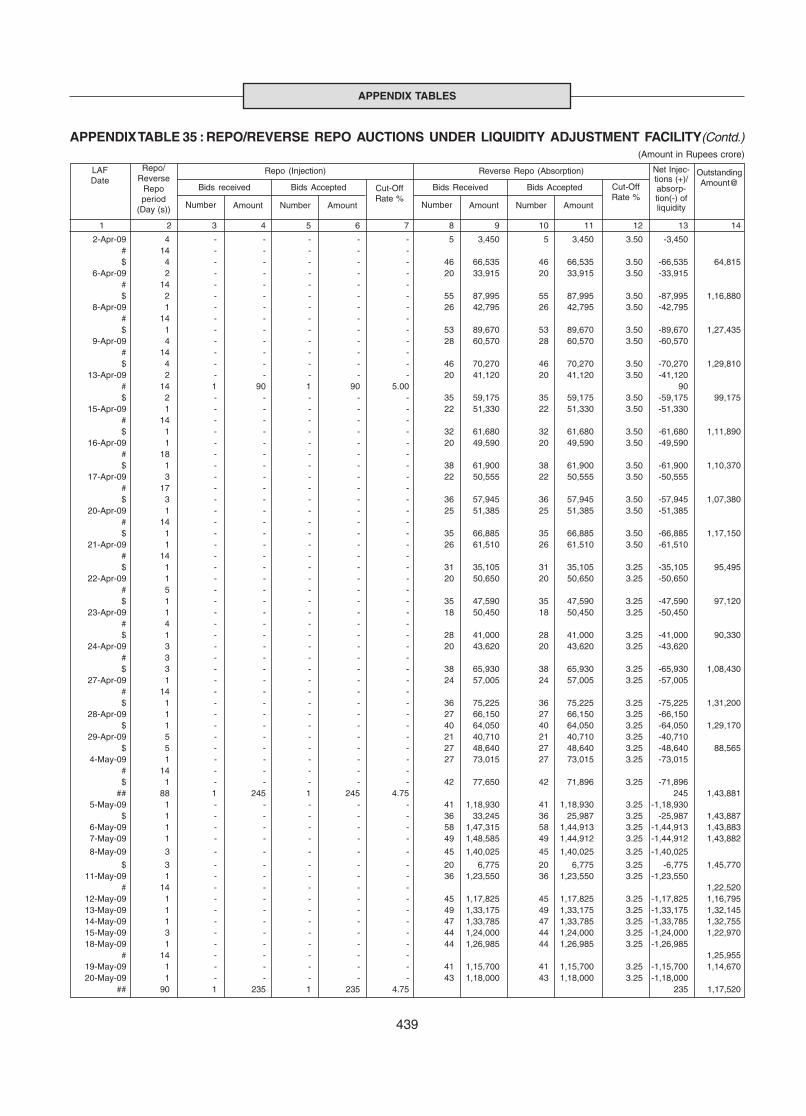

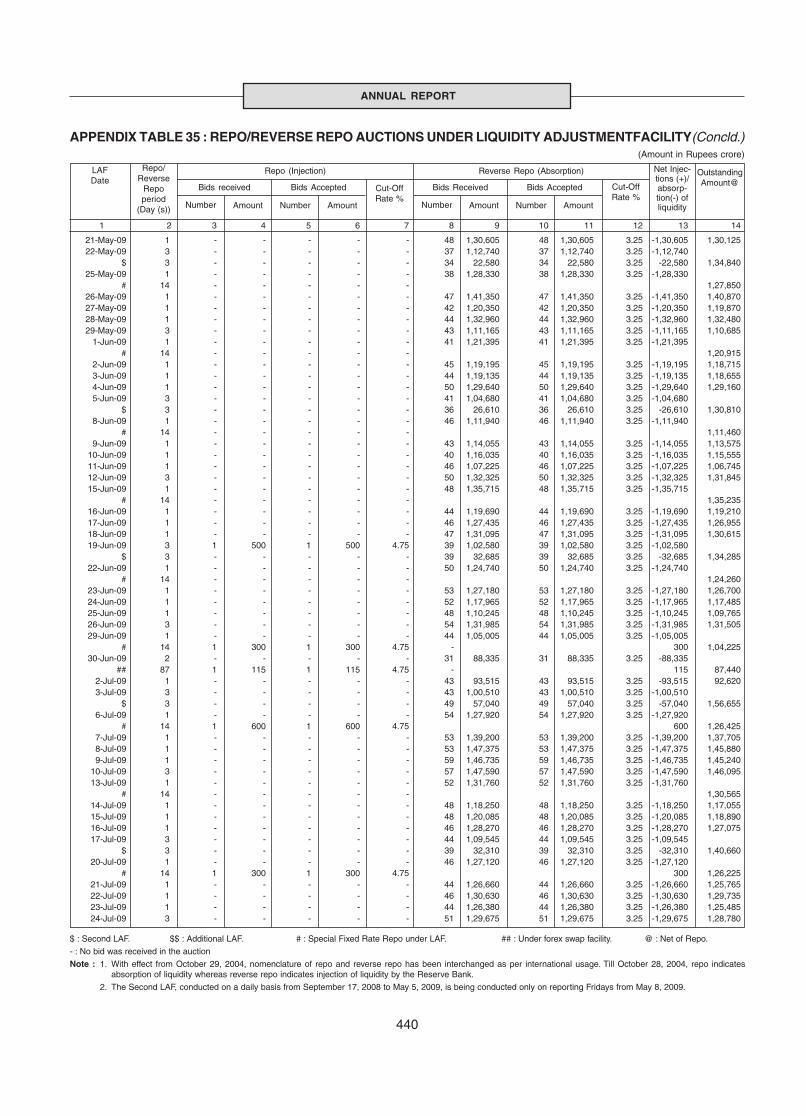

35 Repo/Reverse Repo Auctions Under Liquidity Adjustment Facility ................................. 433

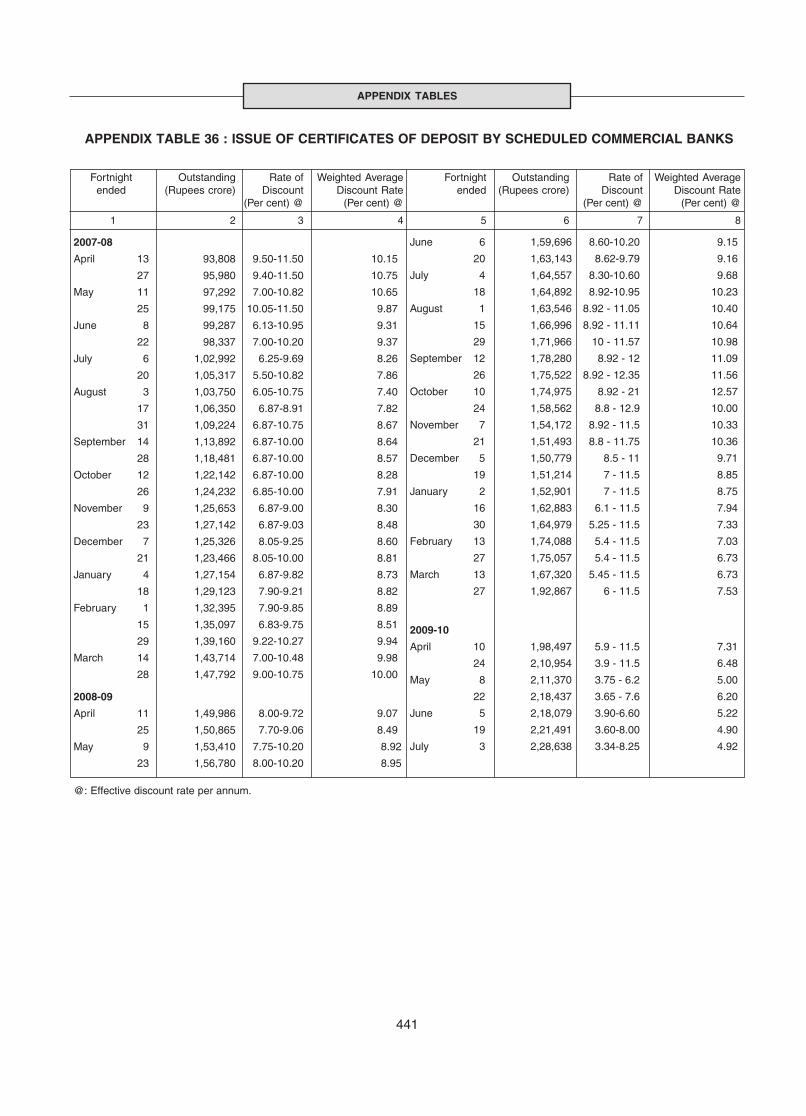

36 Issue of Certificates of Deposit by Scheduled Commercial Banks .................................. 441

37 Commercial Paper ............................................................................................................ 442

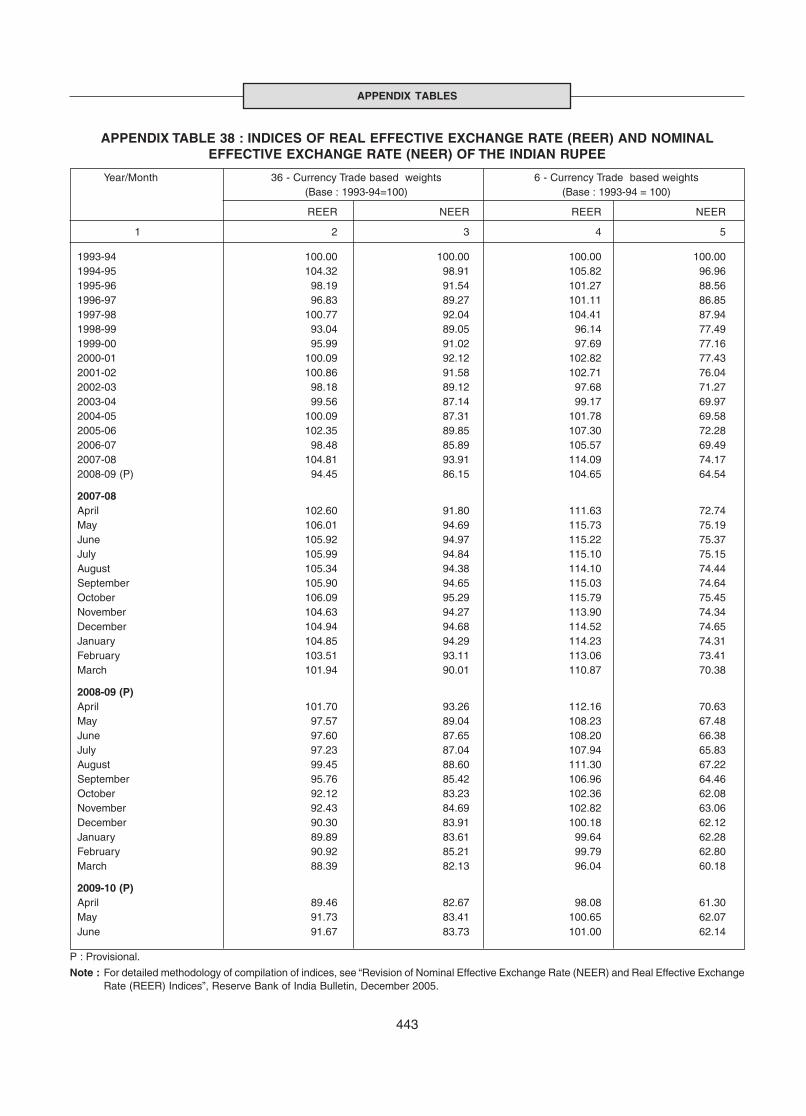

38 Indices of Real Effective Exchange Rate (REER) andNominal Effective Exchange Rate (NEER) of the Indian Rupee ..................................... 443

39 Inter-Bank and Merchant Transactions in the Foreign Exchange Market ........................ 444

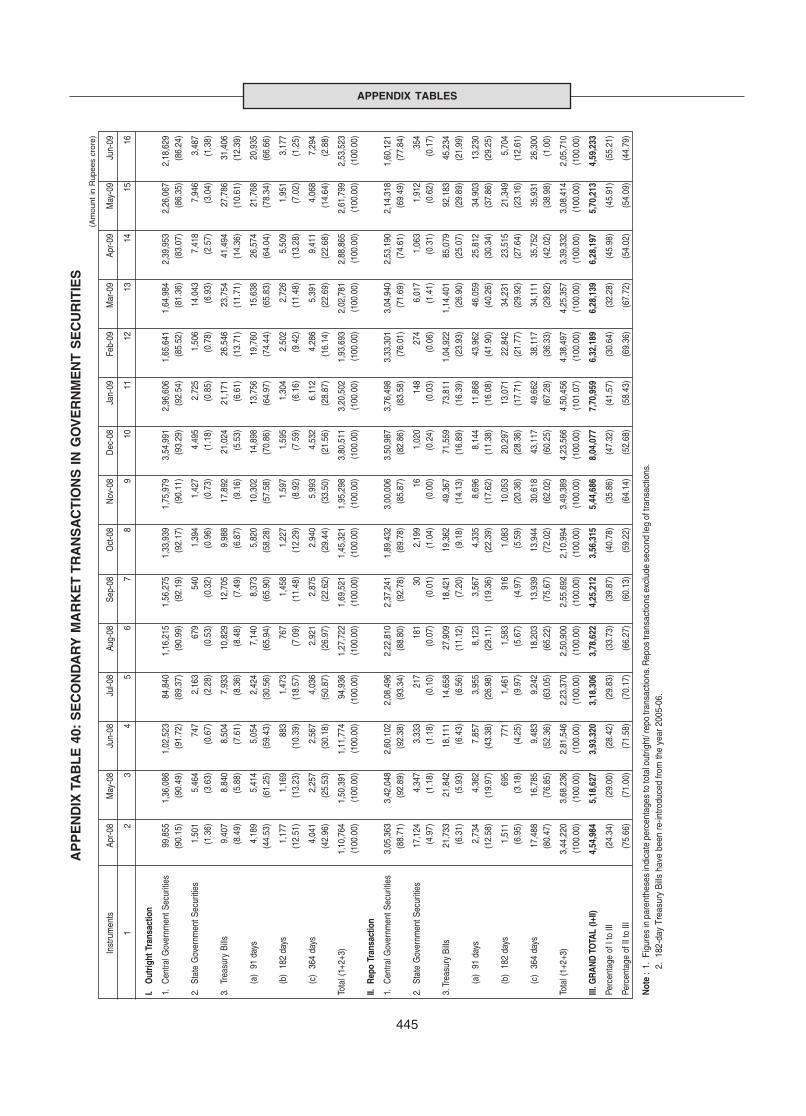

40 Secondary Market Transactions in Government Securities ............................................. 446

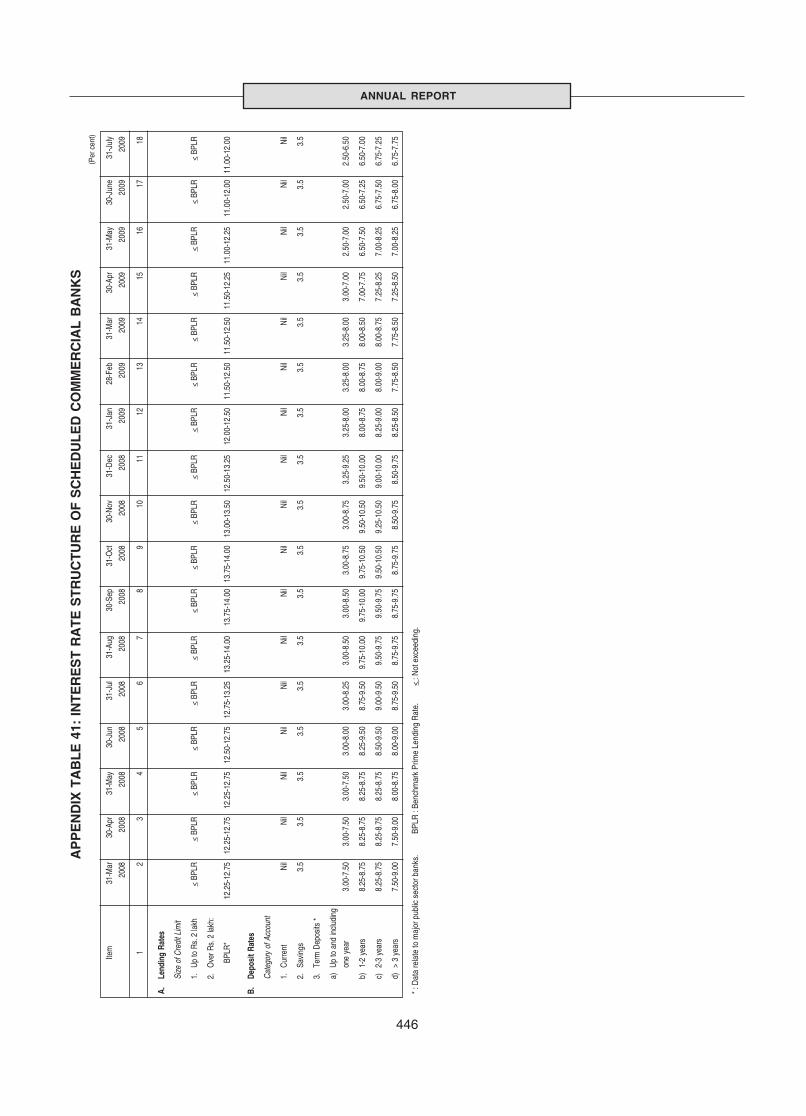

41 Interest Rate Structure of Scheduled Commercial Banks ............................................... 446

Page No.

CONTENTS

xiv

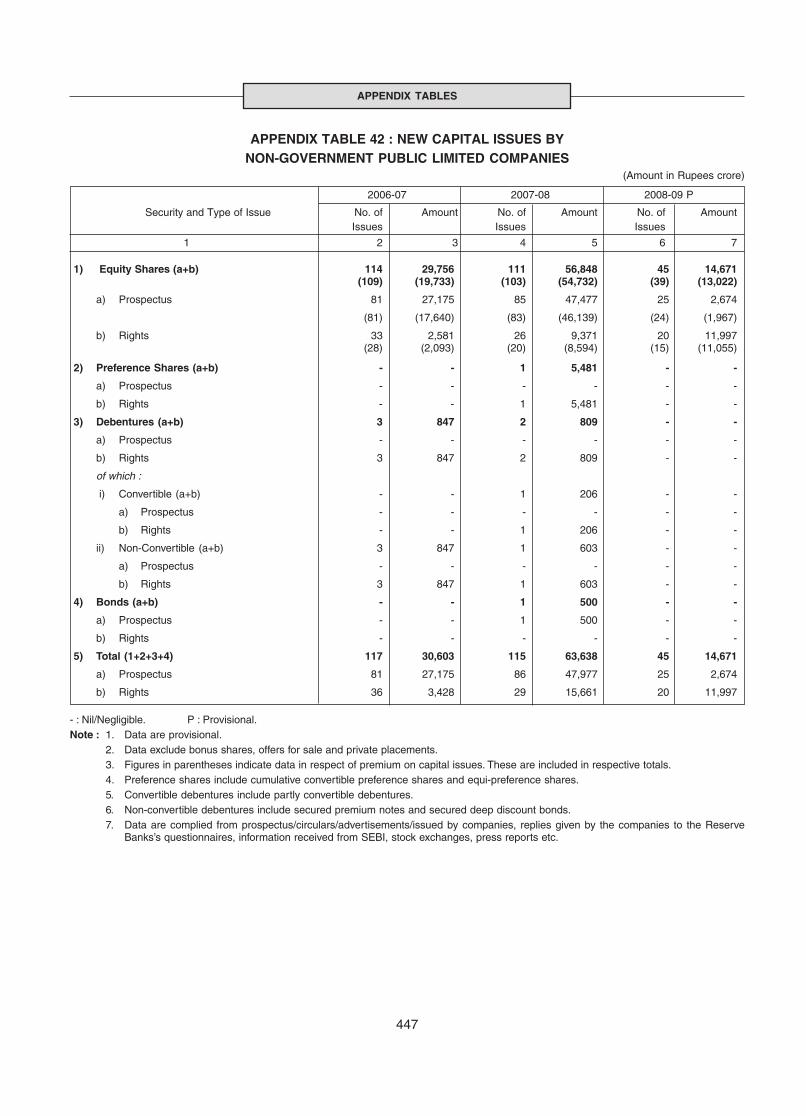

42 New capital Issues by Non-Government Public Limited Companies ............................... 447

43 Domestic Stock Indices .................................................................................................... 448

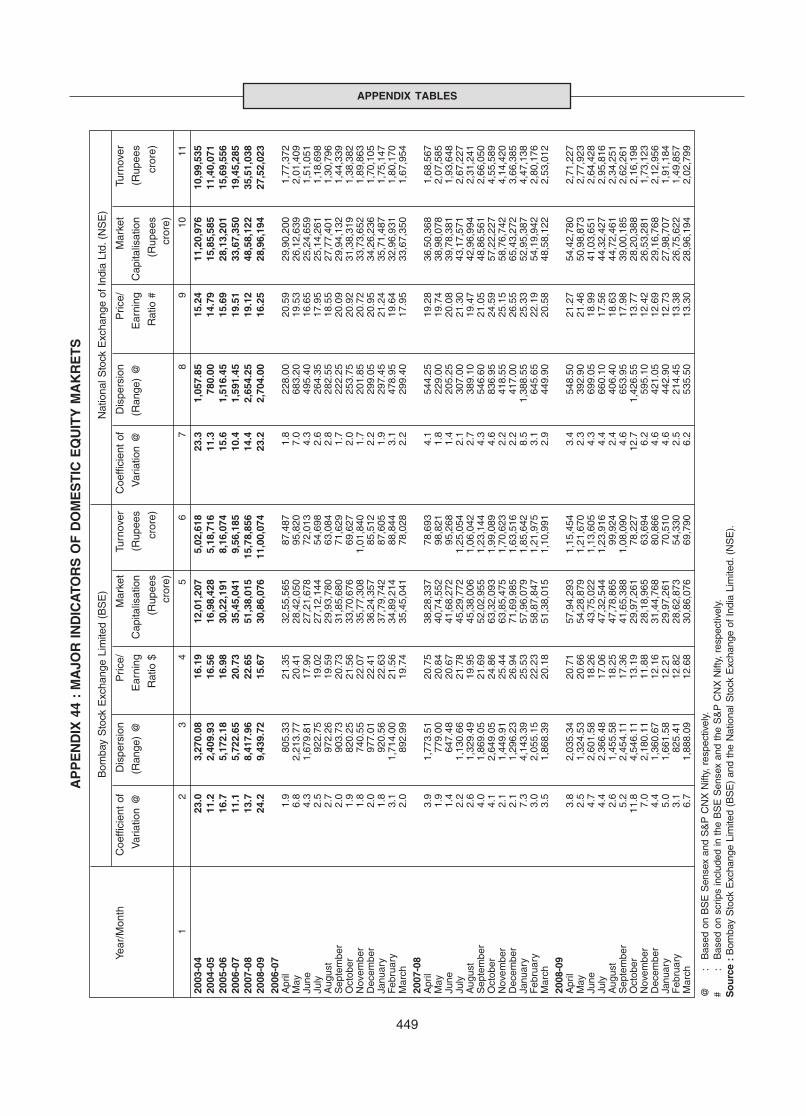

44 Major Indicators of Domestic Equity Markets................................................................... 449

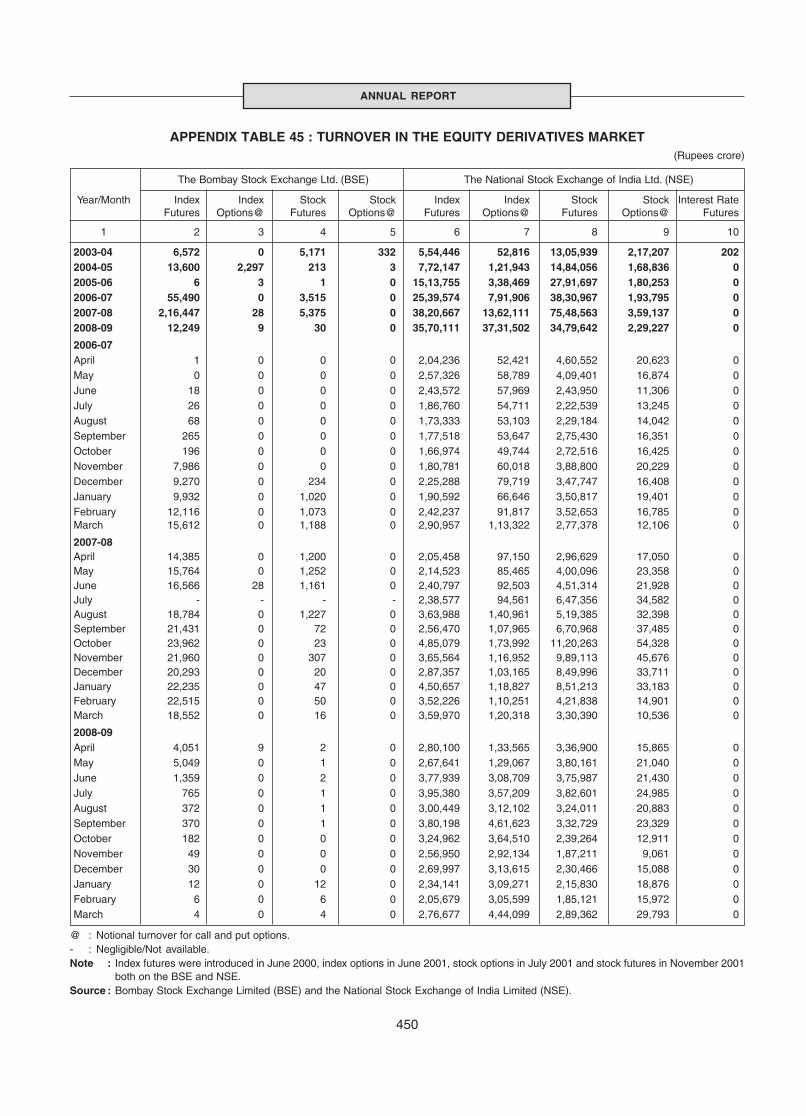

45 Turnover in the Equity Derivatives Market ........................................................................ 450

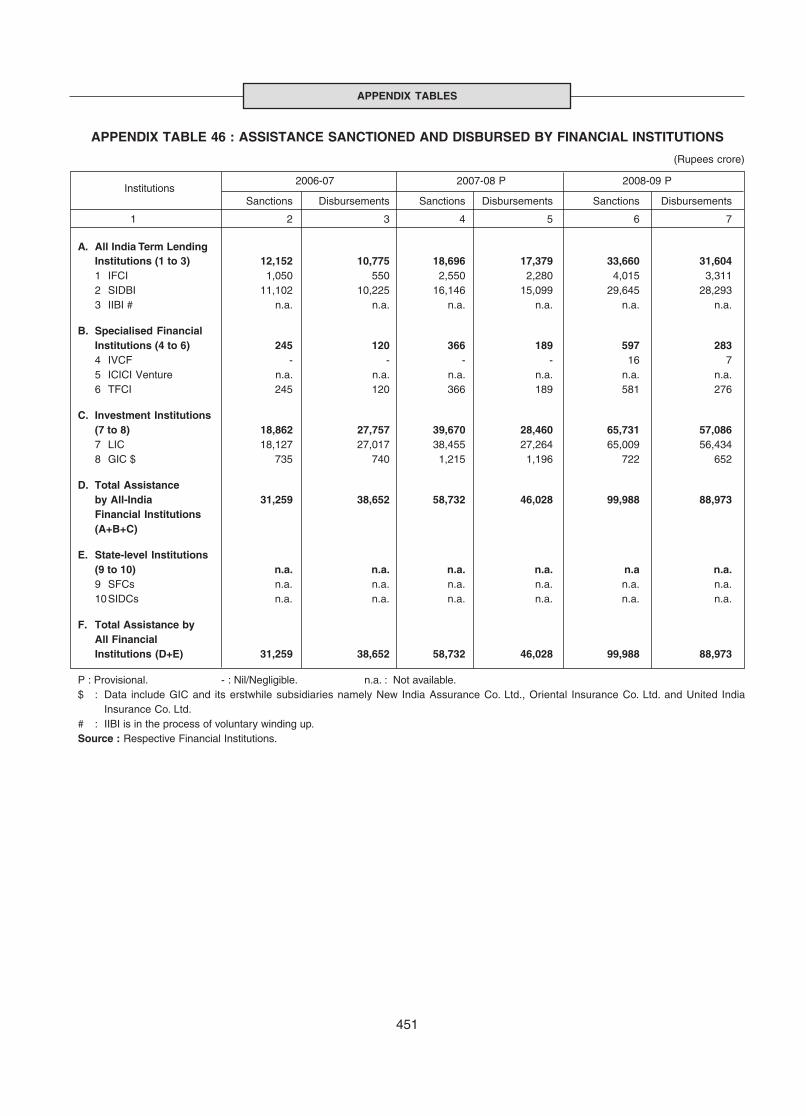

46 Assistance Sanctioned and Disbursed by Financial Institutions ...................................... 451

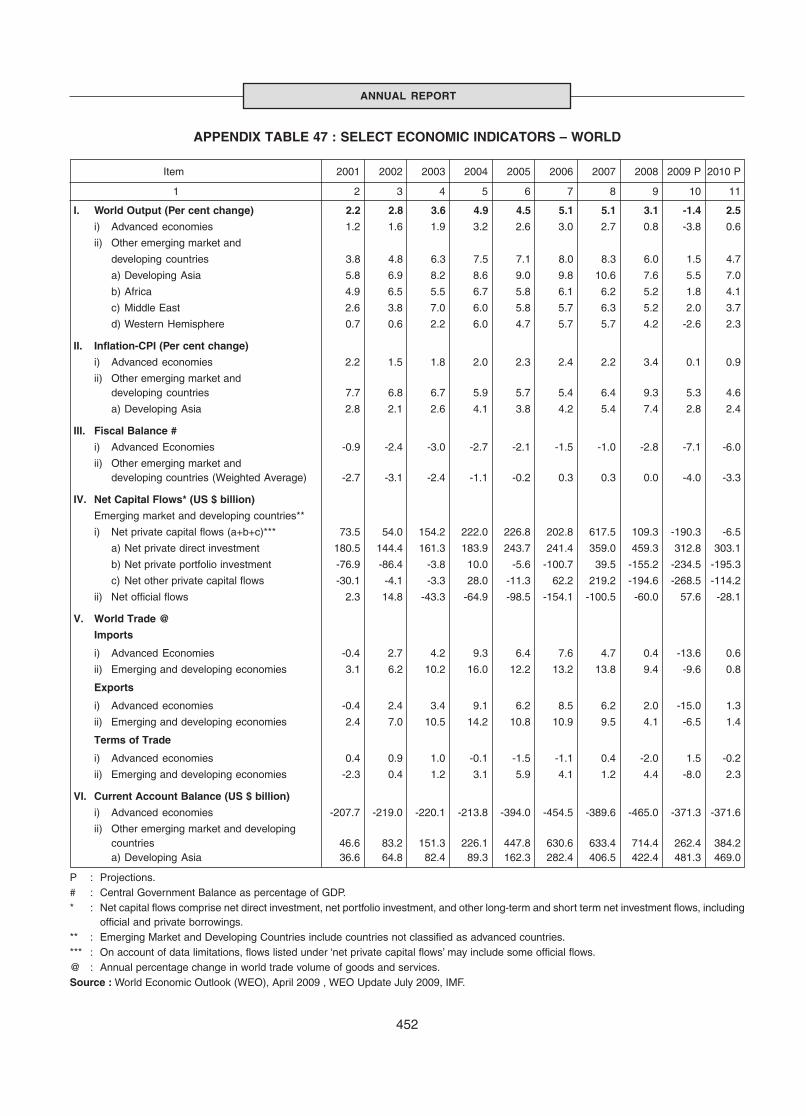

47 Select Economic Indicators - World ................................................................................. 452

48 India’s Foreign Trade ........................................................................................................ 453

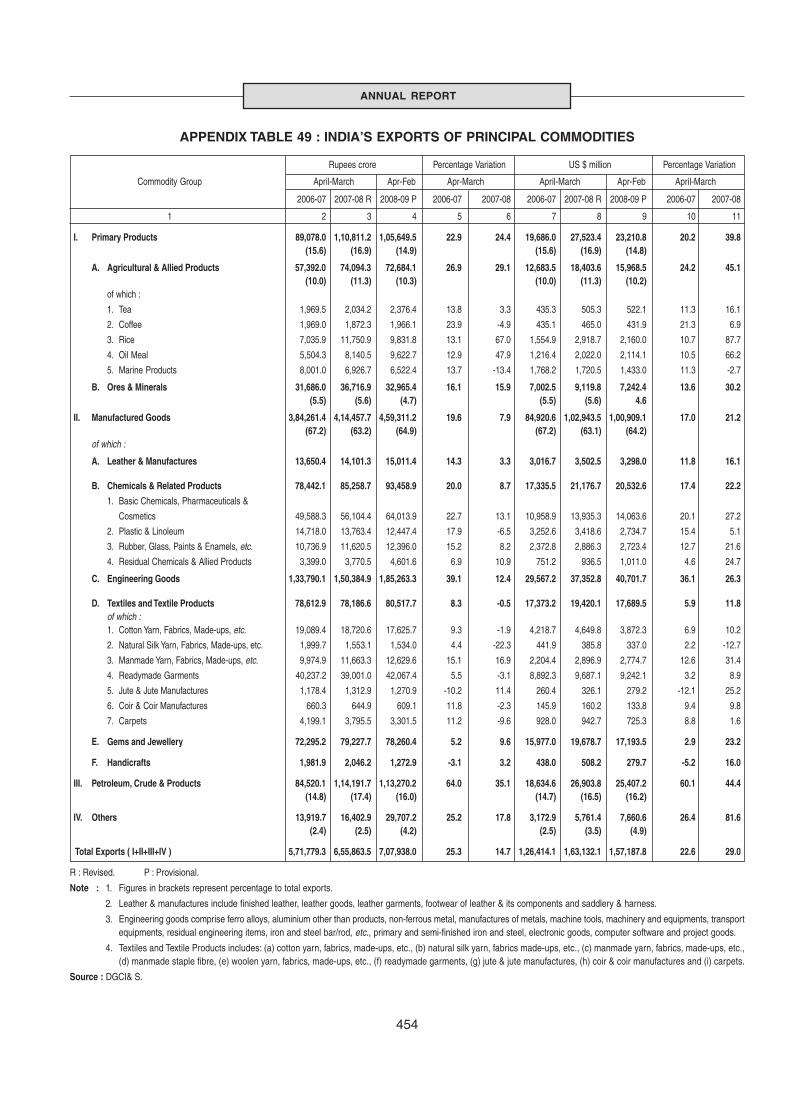

49 India’s Exports of Principal Commodities ......................................................................... 454

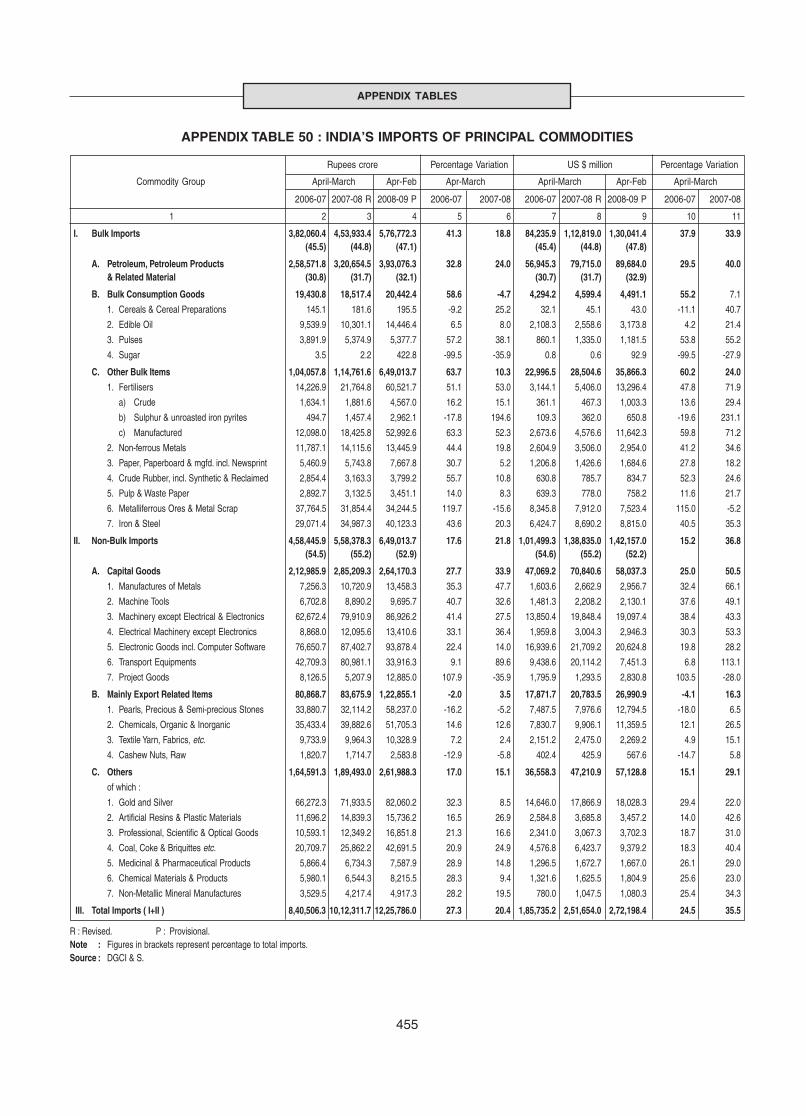

50 India’s Imports of Principal Commodities ......................................................................... 455

51 India’s Overall Balance of Payments ................................................................................ 456

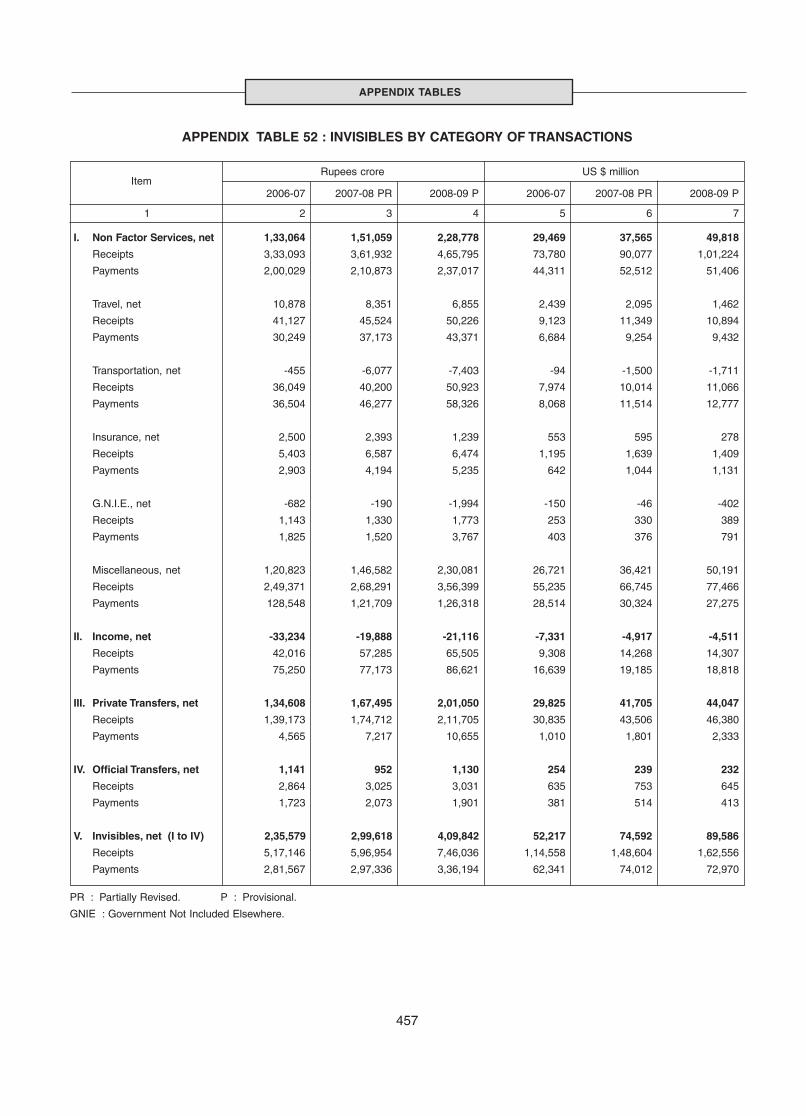

52 Invisibles by Category of Transactions ............................................................................. 457

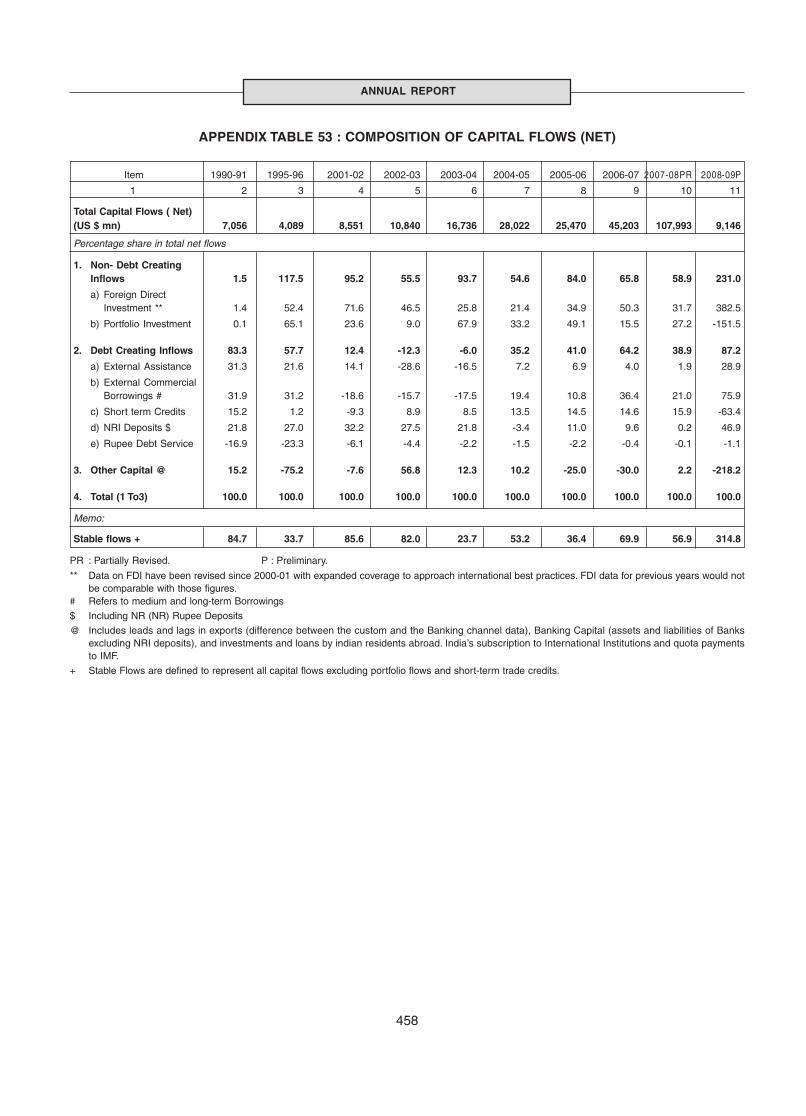

53 Composition of Capital Flows (Net).................................................................................. 458

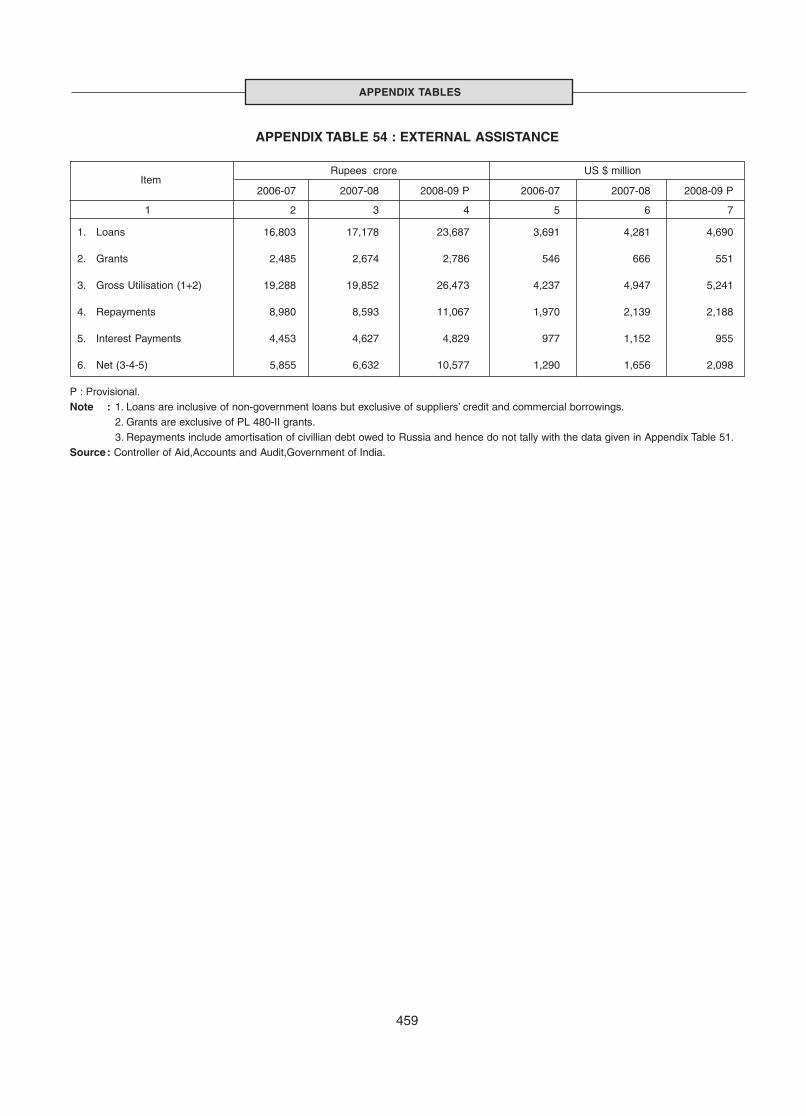

54 External Assistance .......................................................................................................... 459

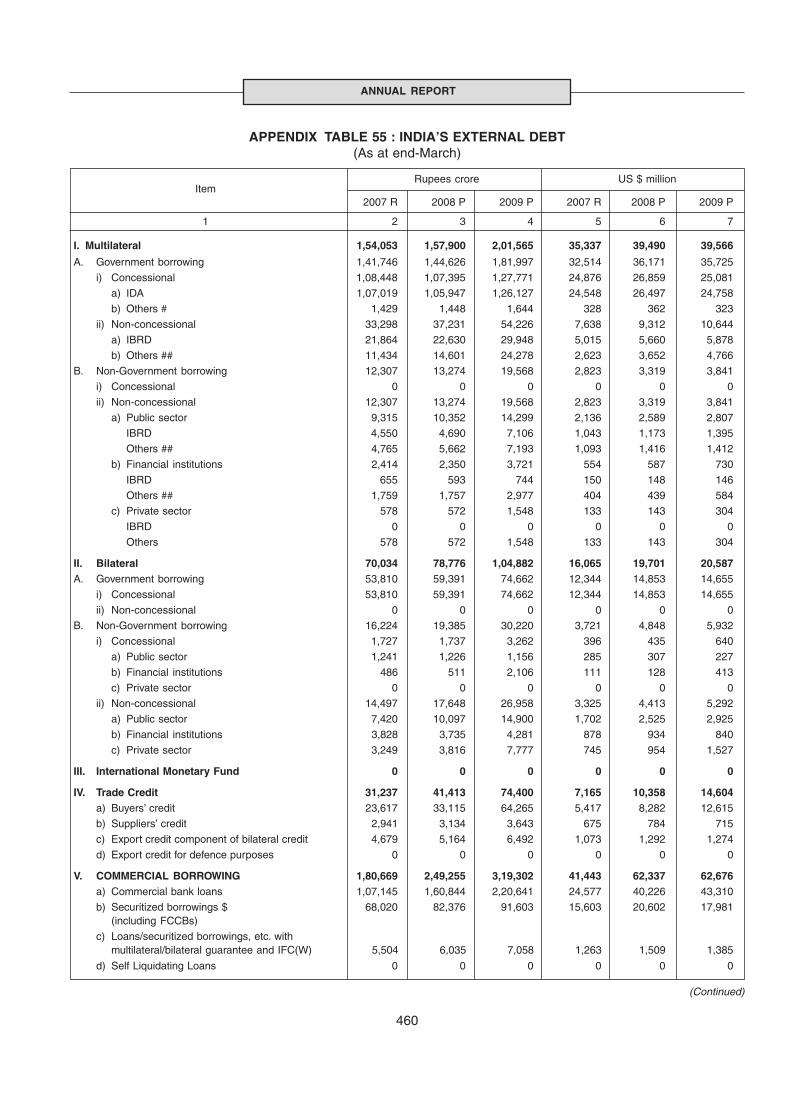

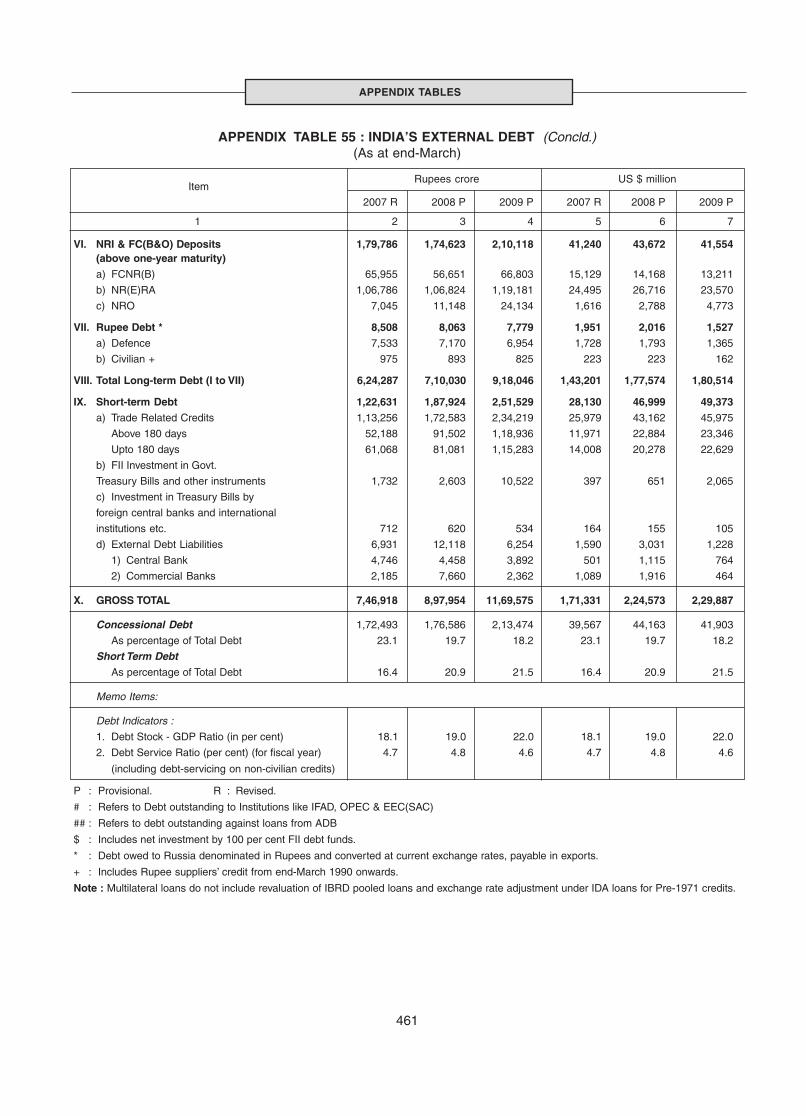

55 India’s External Debt (As at end-March) .......................................................................... 460

56 India’s Foreign Exchange Reserves ................................................................................. 462

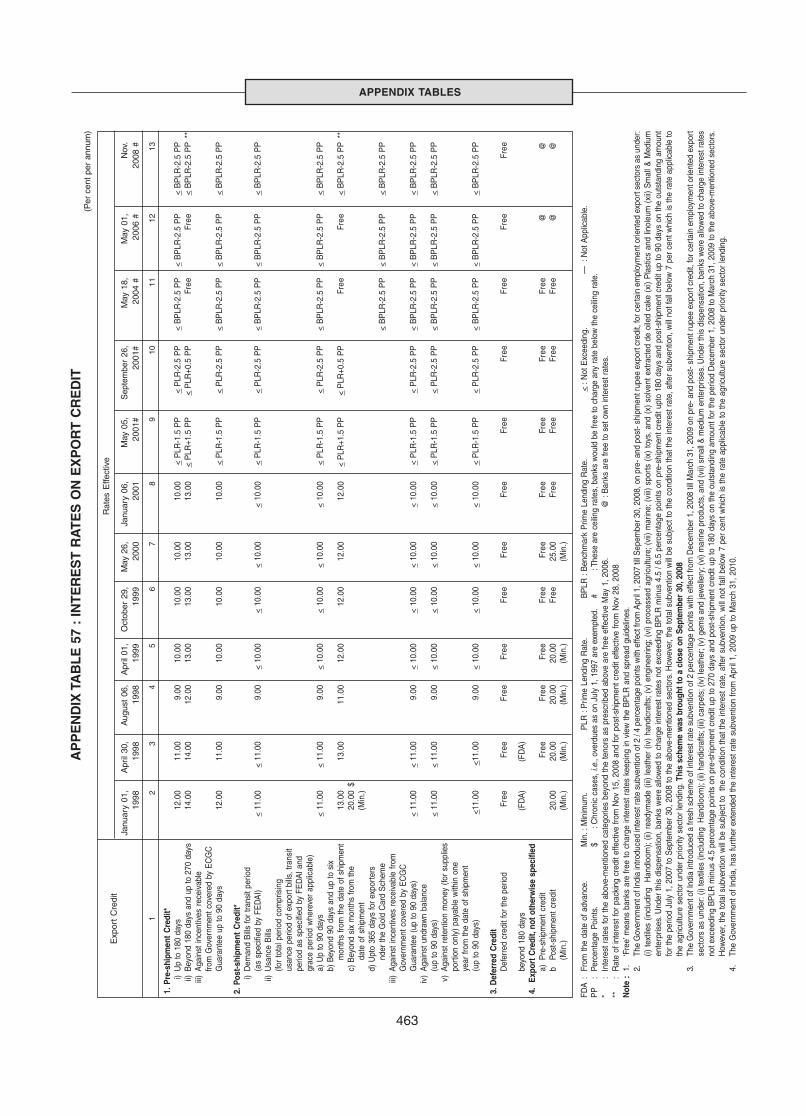

57 Interest Rates on Export Credit ........................................................................................ 463

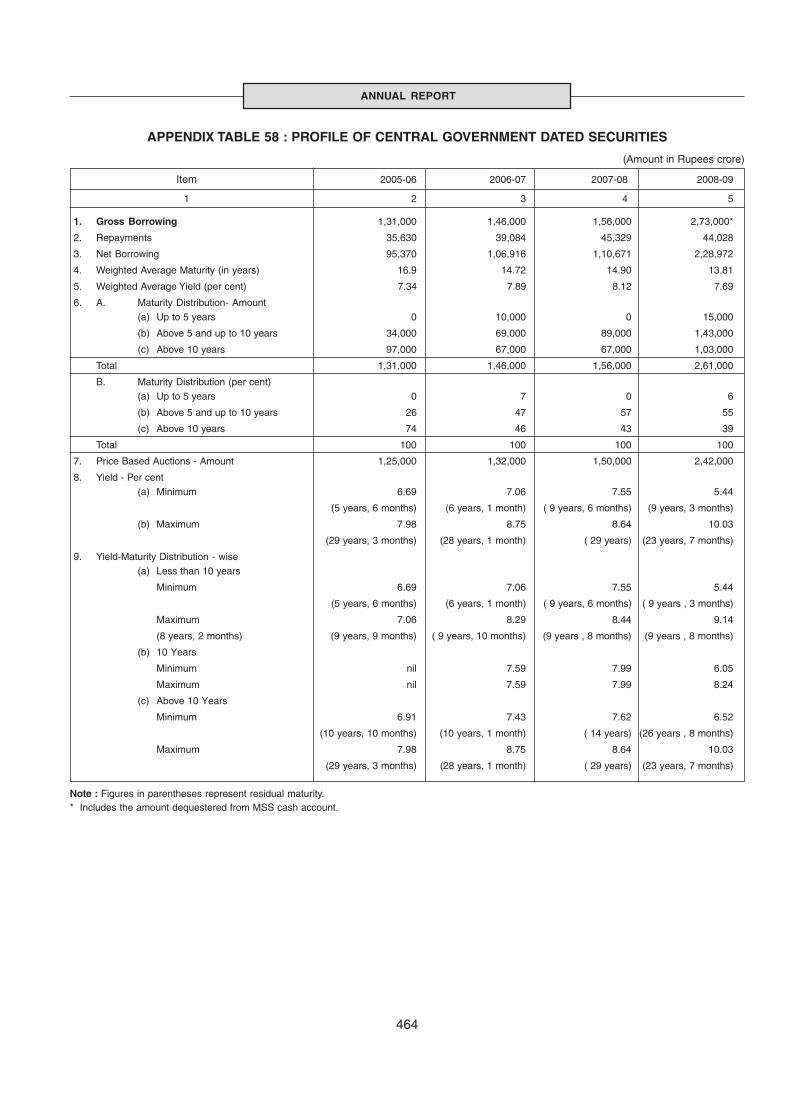

58 Profile of Central Government Dated Securities .............................................................. 464

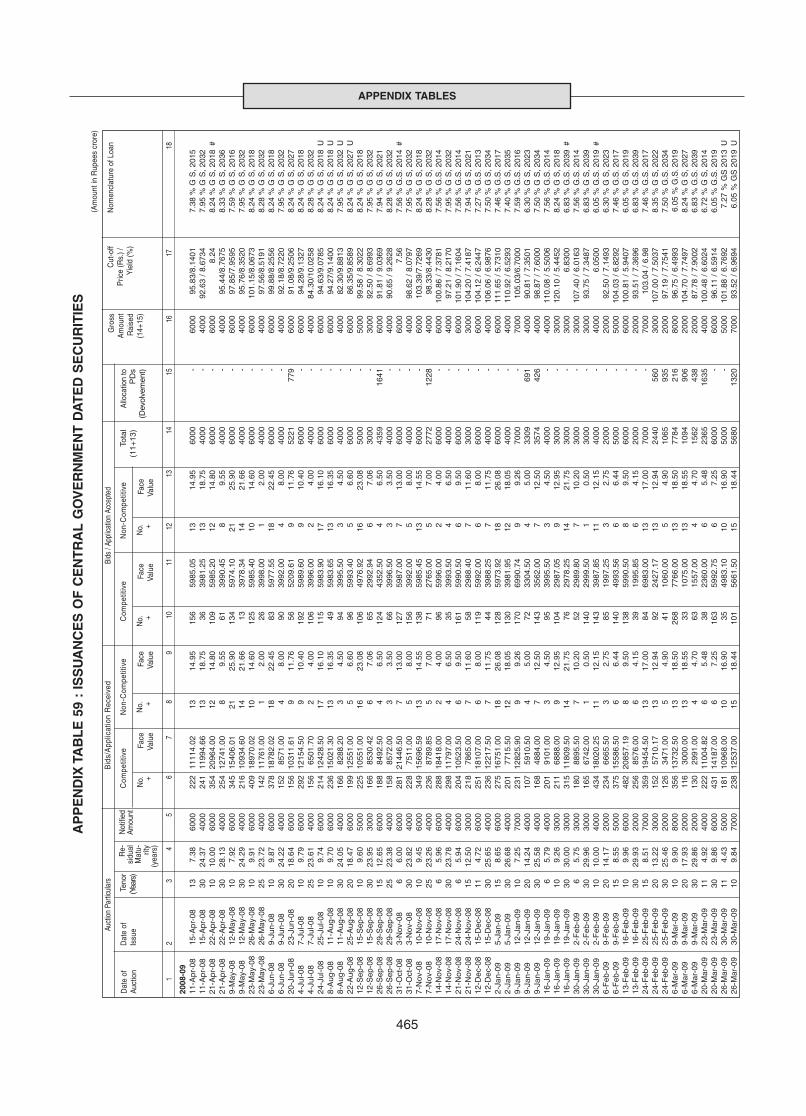

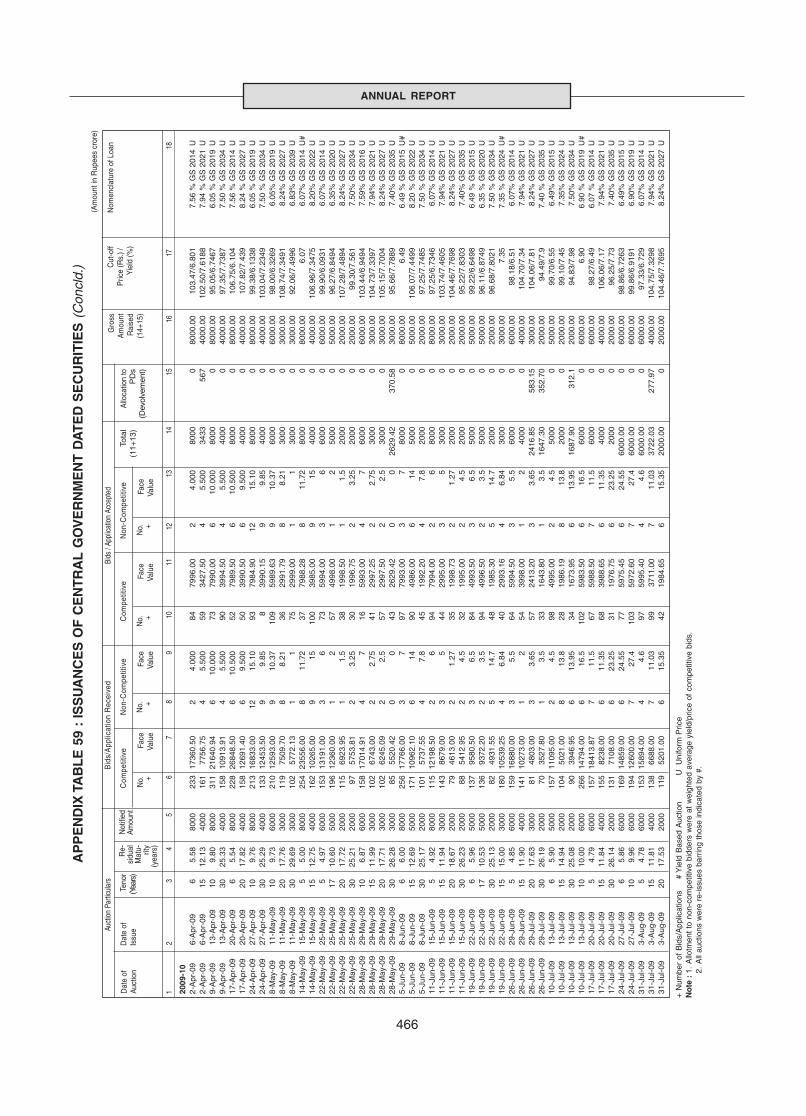

59 Issuances of Central Government Dated Securities ........................................................ 465

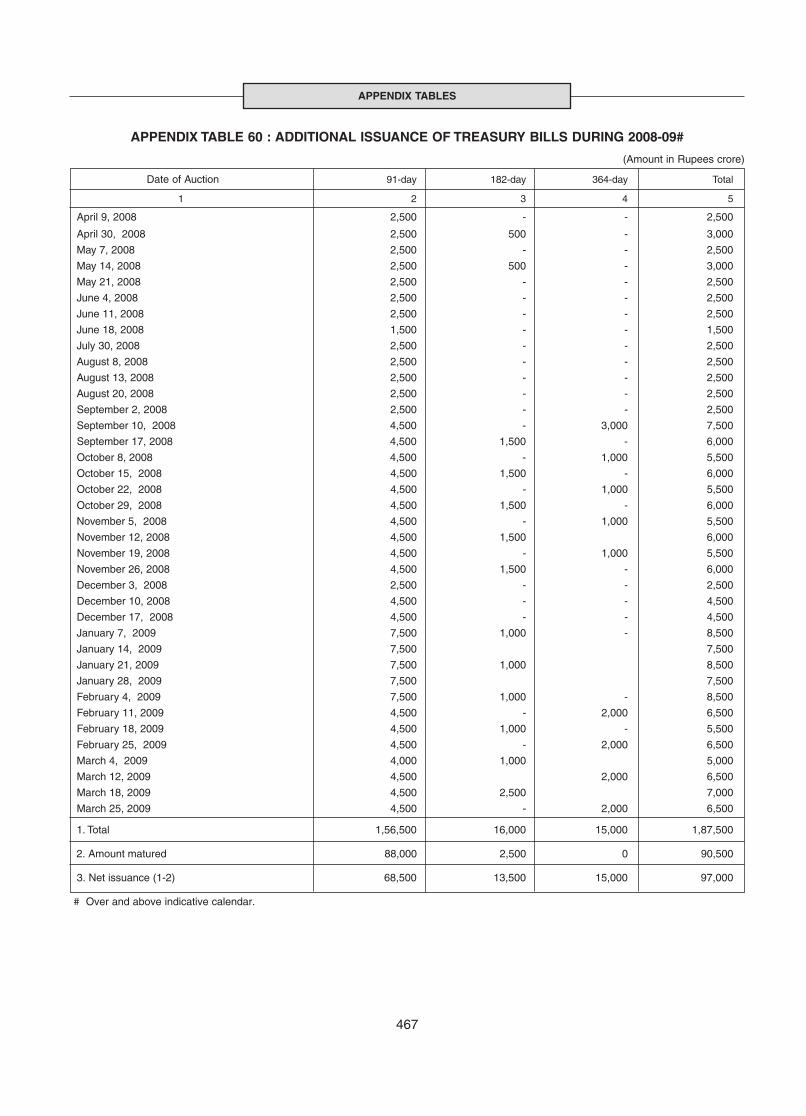

60 Additional Issuance of Treasury Bills during 2008-09 ...................................................... 467

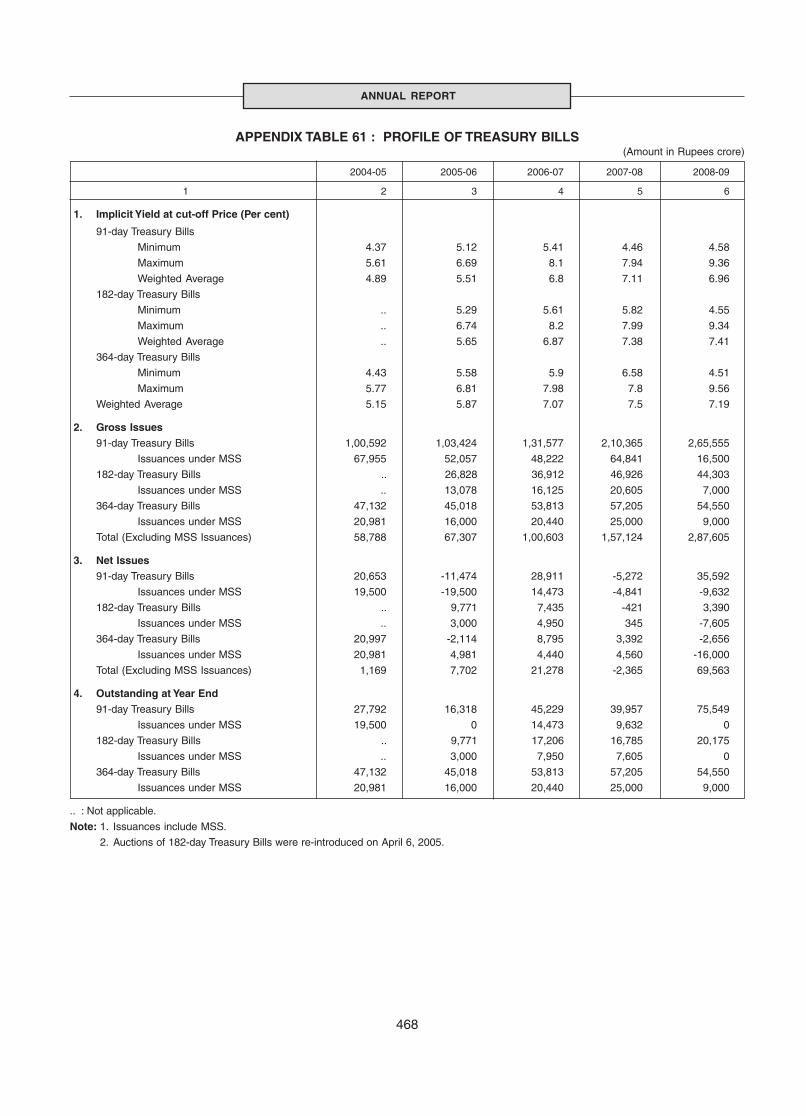

61 Profile of Treasury Bills ..................................................................................................... 468

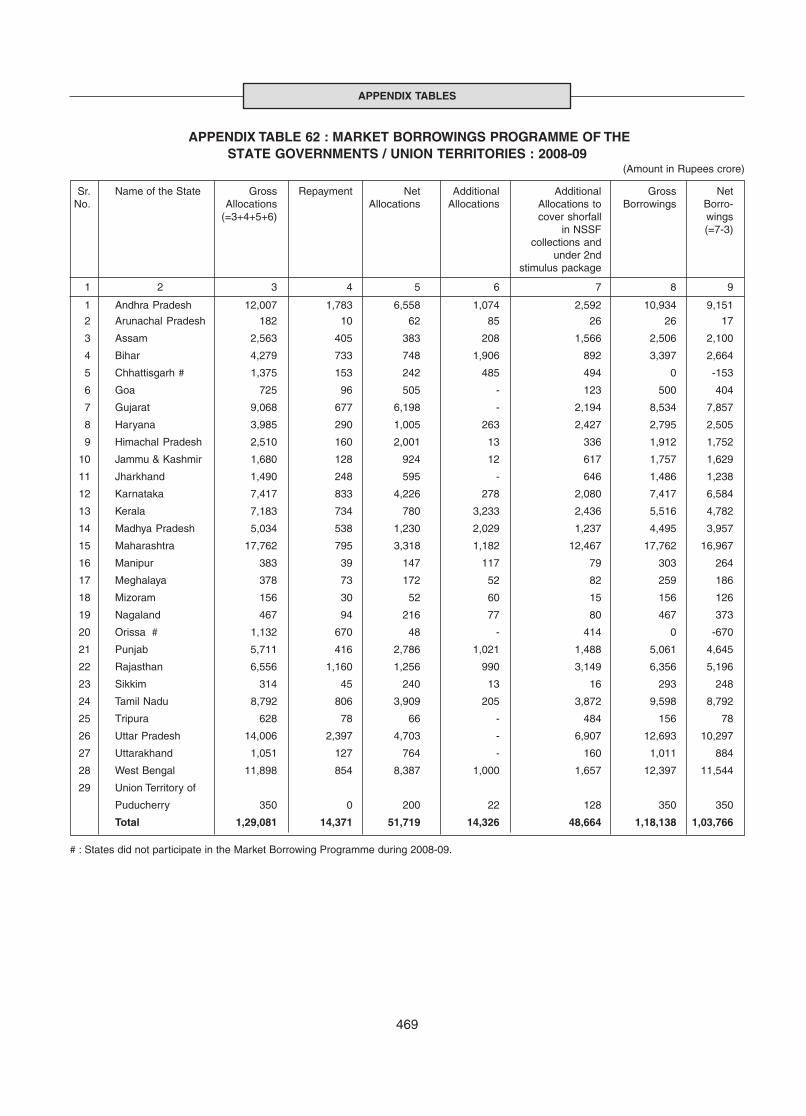

62 Market Borrowings Programme of the State Governments/Union Territories - 2008-09 . 469

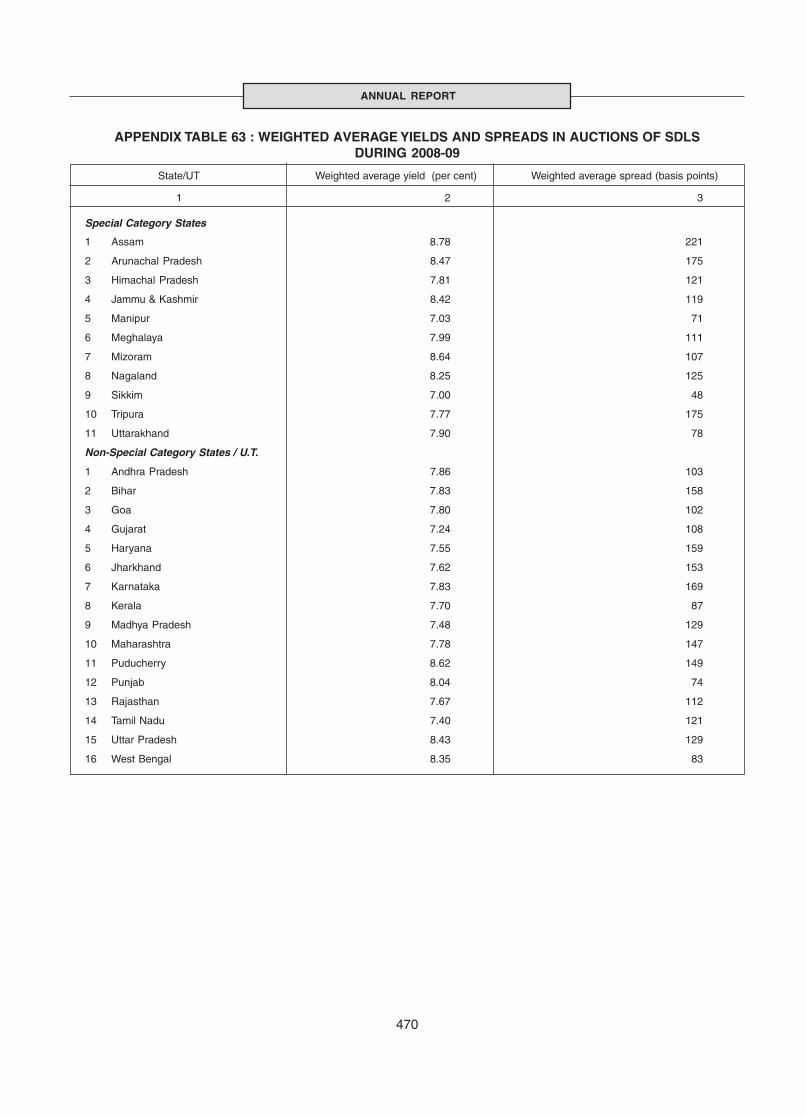

63 Weighted Average Yields and Spreads in Auction of SDLs during 2008-09 .................... 470

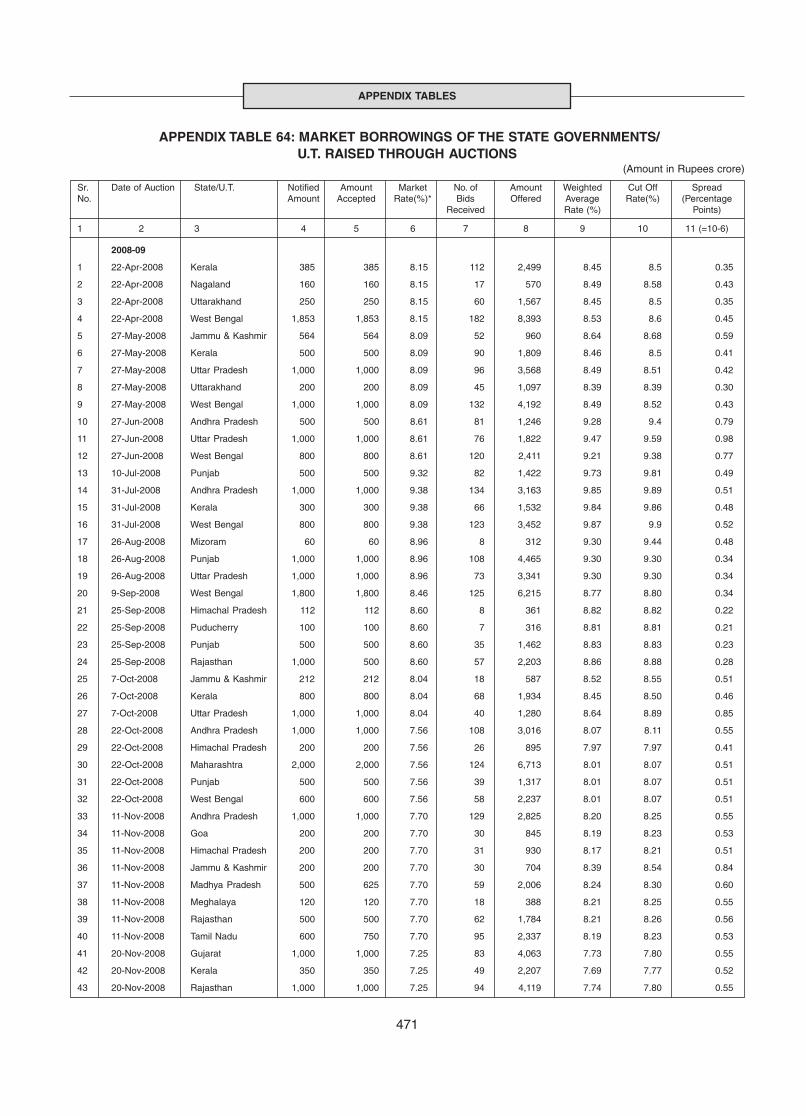

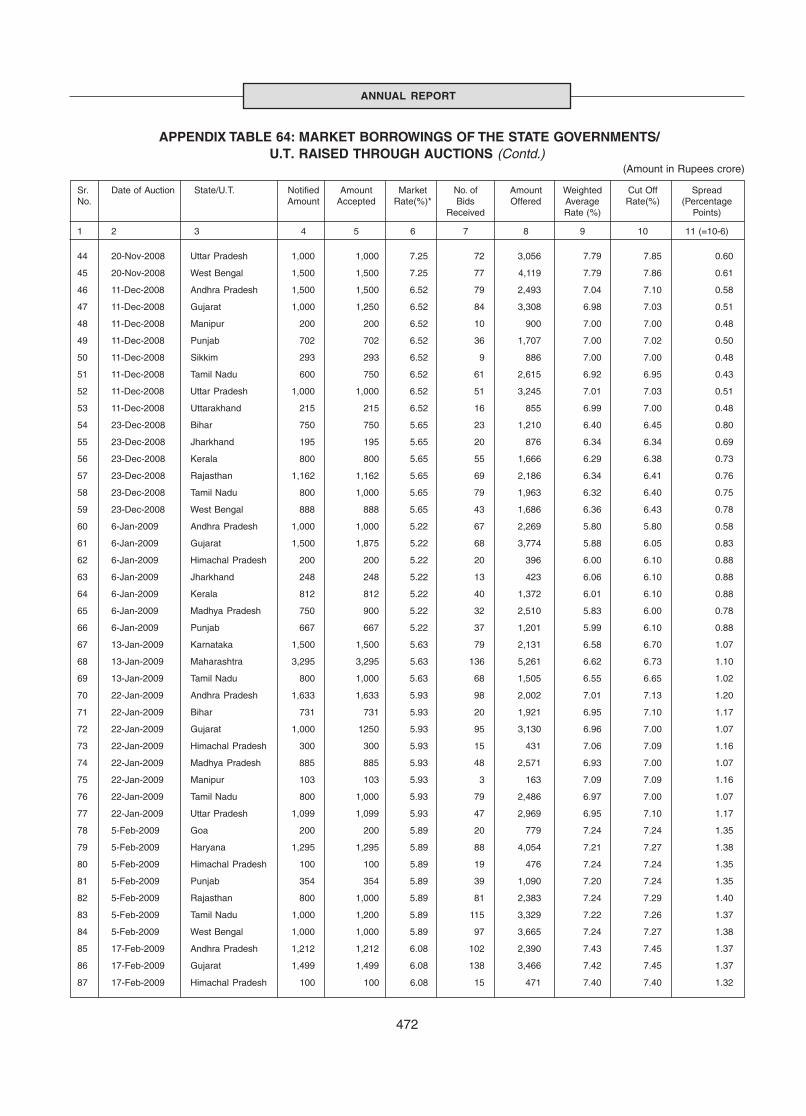

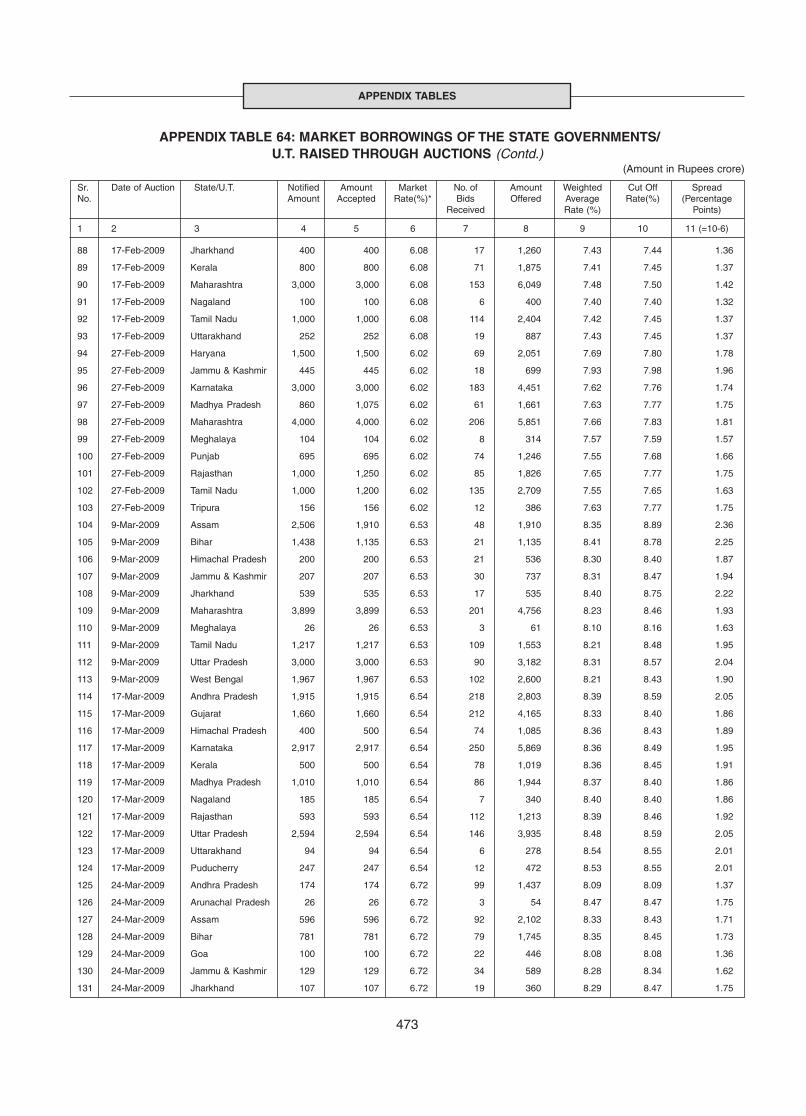

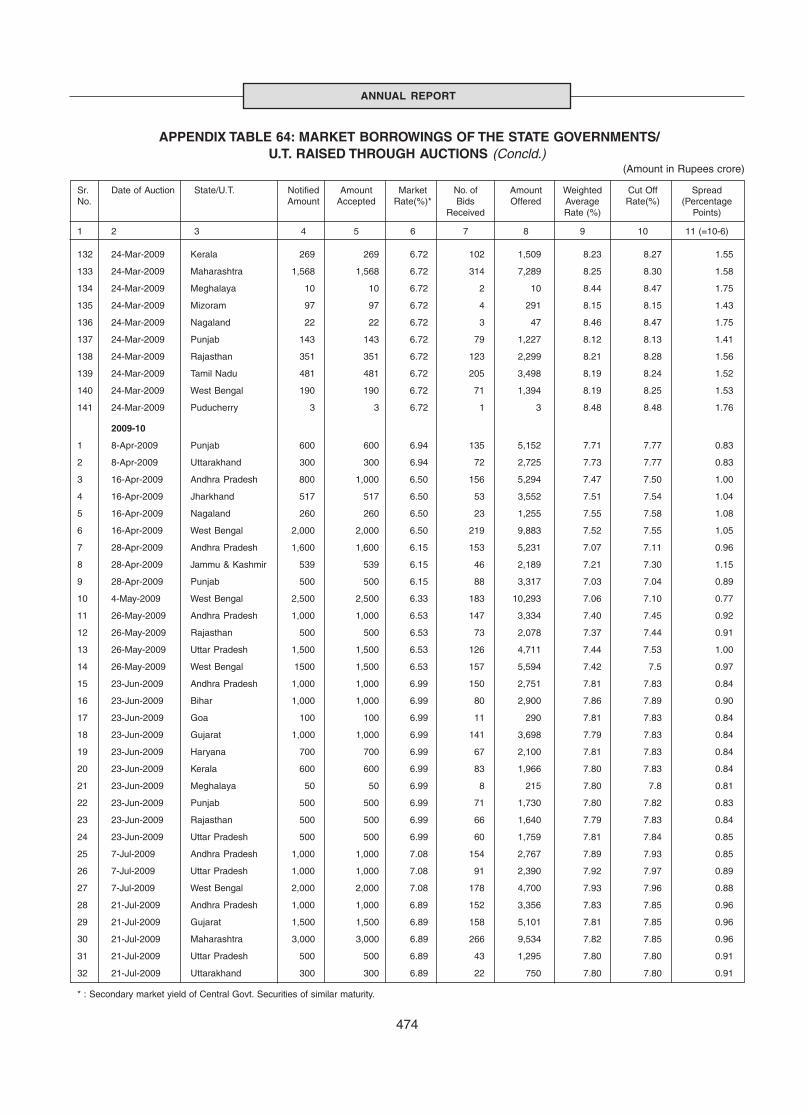

64 Market Borrowings of the State Governments/U.T. Raised Through Auctions ................ 471

65 Maturity Profile of Outstanding Securities of State Governments/U.T. ............................ 475

66 Normal WMA Limits of States/UT .................................................................................... 476

Page No.

CONTENTS

LIST OF ABBREVIATIONS

xv

ABCI - Association of Business Communicatorsof India

ABCP - Asset Backed Commercial Paper

ACU - Asian Clearing Union

ADB - Asian Development Bank

ADF - Augmented Dicky Fuller

ADR - Asset Development Reserve

ADRs - American Depository Receipts

ADs - Authorised Dealers

AERA - Airport Economic Regulatory Act

AFI - Annual Financial Inspection

AIFI - All India Financial Institution

AIMSCS - Advanced Institute of Mathematics,Statistics and Computer Science

ALM - Asset Liability Management

AMA - Advanced Measurement Approach

AMFI - Association of Mutual Funds in India

AML - Anti-Money Laundering

AMU - Asian Monetary Unit

ANBC - Adjusted Net Bank Credit

APS - Annual Policy Statement

AS - Accounting Standard

ATM - Automated Teller Machine

BAFT - Bankers’ Association for Finance &Trade

BC - Business Correspondent

BCBS - Basel Committee on Banking Supervision

BCP - Business Continuity Planning

BCSBI - Banking Codes and Standards Board ofIndia

BE - Budget Estimates

BF - Business Facilitator

BFS - Board for Financial Supervision

BFSI - Banking Financial Services and Insurance

BIS - Bank for International Settlements

BMP - Basic Management Programme

BoP - Balance of Payments

BPLR - Benchmark Prime Lending Rate

BPSS - Board for Regulation and Supervision ofPayment and Settlement Systems

BRBNMPL - Bharatiya Reserve Bank Note MudranPrivate Limited

BSA - Bilateral Swap Arrangements

BSE - Bombay Stock Exchange, Mumbai

BSR - Basic Statistical Returns

BTC - Bankers’ Training College

CA - Concurrent Audit

CAB - College of Agricultural Banking

CACP - Commission for Agricultural Costs andPrices

CAD - Current Account Deficit

CAMELS - Capital Adquacy, Asset Quality,Management, Earnings, Liquidity,Systems and Control

CAS - Central Account Section

CBDT - Central Board of Direct Taxes

CBLO - Collateralised Borrowing and LendingObligation

CBS - Consolidated Banking Statistics

CBS - Core Banking Solutions

CC - Cubic Capacity

CCB - Central Co-operative Bank

CCC - Central Complaints Committee

CCIL - Clearing Corporation of India Limited

CCR - Counterfeit Currency Report

CCRS - Currency Chest Reporting System

CD - Certificate of Deposit

C-D - Currency-Deposit

CDBMS - Centralised Data Base ManagementSystem

CDOs - Collateralised Debt Obligations

CDR - Corporate Debt Restructuring

LIST OF ABBREVIATIONS

xvi

CDS - Credit Default Swap

CENVAT - Central Value Added Tax

CFMS - Centralised Funds Management System

CFSA - Committee on Financial SectorAssessment

CFT - Combating Financing of Terrorism

CGFTMSE - Credit Guarantee Fund Trust for Microand Small Enterprises

CGRA - Currency & Gold Revaluation Account

CIC - Central Information Commission

CICs - Credit Information Companies

CIS - Commonwealth of Independent States

CMCPS - Compulsorily and MandatorilyConvertible Preference Shares

CMIS - Currency Management InformationSystem

CoBoSAC - Corporate Bonds and SecuritisationAdvisory Committee

CODs - Central Office Departments

CoR - Certificate of Registration

CP - Commercial Paper

CPADS - Centralised Public Accounts DepartmentSystem

CPC - Cheque Processing Centre

CPDO - Centralised Public Debt Office

CPFF - Commercial Paper Funding Facility

CPI - Consumer Price Index

CPI-AL - Consumer Price Index-Agricultural Labourers

CPI-RL - Consumer Price Index-Rural Labourers

CPI-IW - Consumer Price Index for IndustrialWorkers

CPIO - Central Public Information Officer

CPIs - Consumer Price Indices

CPMG - Corporate Performance MonitoringGroup

CPPC - Central Pension Payment Cell

CPSEs - Central Public Sector Enterprises

CR - Contingency Reserve

CRAR - Capital to Risk-Weighted Assets Ratio

CRCS - Central Registar of Co-operativeSocieties

CRR - Cash Reserve Ratio

CSAA - Control Self Assessment Audit

CSD - Customer Services Department

CSF - Consolidated Sinking Fund

CSGL - Constituant Subsidiary General Ledger

CSO - Central Statistical Organisation

CTR - Cash Transaction Receipt

CTS - Cheque Truncation System

CTS - Complaint Tracking System

CVD - Countervailing Duty

CVPS - Currency Verification and ProcessingSystem

CWC - Central Water Commission

DAD - Deposit Accounts Department

DAP - District Agricultural Plan

DAPM - Department of Administration andPersonnel Management

DBOD - Department of Banking Operations andDevelopment

DBS - Department of Banking Supervision

DCC - District Consultative Committee

DCCB - District Central Cooperative Bank

DCM - Department of Currency Management

DEAP - Department of Economic Analysis andPolicy

DEBC - Department of Expenditure andBudgetary Control

DEIO - Department of External Investments andOperations

DEPB - Duty Entitlement Pass Book

DGBA - Department of Government and BankAccounts

LIST OF ABBREVIATIONS

xvii

DGCI & S - Directorate General of CommercialIntelligence and Statistics

DIC - District Industries Centre

DICGC - Deposit Insurance and Credit GuaranteeCorporation

DIP - Disclosure and Investor Protection

DIT - Department of Information Technology

DMIS - Document Management InformationSystem

DNBS - Department of Non-Banking Supervision

DOC - Department of Communication

DoT - Department of Telecommunication

DRG - Development Research Group

DRI - Differential Rate of Interest

DRT - Debt Recovery Tribunal

DS - Difference Stationary

DSB - Designated Settlement Banks

DSIM - Department of Statistics and InformationManagement

DvP - Delivery versus Payment

EACB - European Association of Co-operativeBanks

EBT - Electronic Benefit Transfer

ECB - European Central Bank

ECBs - External Commercial Borrowings

ECGC - Export Credit Guarantee Corporation

ECR - Export Credit Refinance

ECS - Electronic Clearing Services

EEA - Exchange Equalisation Account

EEFC - Exchange Earners’ Foreign Currency

EFT - Electronic Funds Transfer

EMEs - Emerging Market Economies

EOU - Export Oriented Unit

EPCG - Export Promotion Capital Goods

ESOS - Employees Stock Option Scheme

EU - European Union

EXIM Bank - Export Import Bank

FAO - Food & Agriculture Organisation

FAQs - Frequently Asked Questions

FATF - Financial Action Task Force

FBT - Fringe Benefit Tax

FC - Financial Conglomerate

FCAs - Foreign Currency Assets

FCCB - Foreign Currency Convertible Bond

FCI - Food Corporation of India

FCNR(B) - Foreign Currency Non-Resident (Banks)

FDI - Foreign Direct Investment

FED - Foreign Exchange Department

FEDAI - Foreign Exchange Dealers’ Associationof India

FI - Financial Institutions

FIEO - Federation of Indian ExportOrganisation

FIIs - Foreign Institutional Investors

FIPB - Foreign Investment Promotion Board

FITL - Funded Interest Term Loan

FIU-IND - Financial Intelligence Unit-India

FLCCs - Financial Literacy and Credit CounselingCentres

FMCG - Fast Moving Consumer Goods

FMD - Financial Markets Department

FOF - Flow of Funds

FPS - Focus Product Scheme

FRBM - Fiscal Responsibility and BudgetManagement

FRBs - Floating Rate Bonds

FRL - Full Reservoir Level

FRLs - Fiscal Responsibility Legislations

FSB - Financial Stability Board

FSF - Financial Stability Forum

LIST OF ABBREVIATIONS

xviii

FST - Financial Sector Technology

FVCIs - Foreign Venture Capital Investors

GCC - Gulf Cooperation Council

GCCs - General-purpose Credit Cards

GDP - Gross Domestic Product

GDRs - Global Depository Receipts

GFCE - Government Financial ConsumptionExpenditure

GFD - Gross Fiscal Deficit

GFSR - Global Financial Stability Report

GIPSA - General Insurer’s (Public Sector)Association of India

GoI - Government of India

GRF - Guarantee Redemption Fund

GSDP - Gross State Domestic Product

GST - Goods and Services Tax

HFCs - Housing Finance Companies

HLAC - High Level Advisory Committee

HLCCFM - High Level Coordination Committee onFinancial Markets

HLG - High Level Group

HR - Human Resources

HRDD - Human Resources DevelopmentDepartment

HRMS - Human Resources ManagementSystem

HSUI - Housing Start Up Index

HTM - Held-to-Maturity

IAS - Integrated Accounting Systems

IASC - Inspection and Audit Sub-Committee

IBA - Indian Banks’ Association

ICAC - International Cotton AdvisoryCommittee

ICAI - Institute of Chartered Accountants ofIndia

ICAR - Indian Council for Agricultural Research

ICCOMS - Integrated Computerised CurrencyOperations and Management System

ICT - Information and CommunicationTechnology

IDMD - Internal Debt Management Department

IDR - Indian Depository Receipt

IDRBT - Institute for Development & Research inBanking Technology

IEM - Industrial Entrepreneurs Memoranda

IES - Integrated Establishment System

IGIDR - Indira Gandhi Institute of DevelopmentResearch

IIA - Institute of Internal Auditors

IIBM - Indian Institute of Bank Management

IIFCL - India Infrastructure Finance CompanyLimited

IIFT - Indian Institute of Foreign Trade

IIP - Index of Industrial Production

ILO - International Labour Organisation

IMA - Internal Models Approach

IMD - India Millennium Deposits

IMD - India Meteorological Department

IMF - International Monetary Fund

IMFC - International Monetary and FinancialCommittee

IODP - Integrated Officers DevelopmentProgrammes