Embed Size (px)

Citation preview

A FAirchild PublicAtion

Changing The gameProcter & Gamble’s Susan Arnold Bets Big on the Beauty Consumer

Hot Shopkeepers On Beating the Pack

How Brands Can Hold On to

Customers

Lessons From The “It” Bag

Phenomenon

Surviving Retail’s Seismic Shift

PLUS

Fall Makeup Knockout Hair

� june/july 2007

ContentsDEPARTMENTS

10 People,Places&LipsticksHow Derek Jeter looks that good rounding home base and the sweet smell of Saks.

14 What’sInStoreTutti-frutti treats, potions from the ocean and nocturnal relief for overworked skin.

20ACloserLook:Color Cosmetics A preview of fall’s most directional shades, from nearly nudes to deep, dark hues.

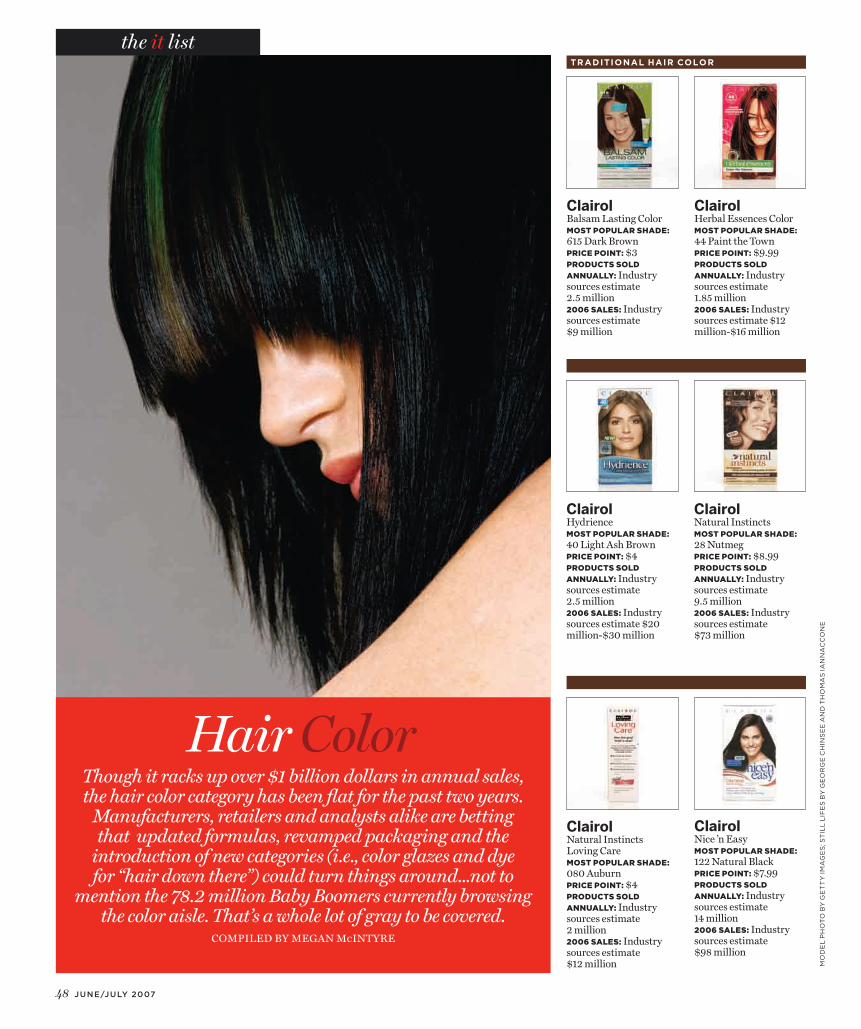

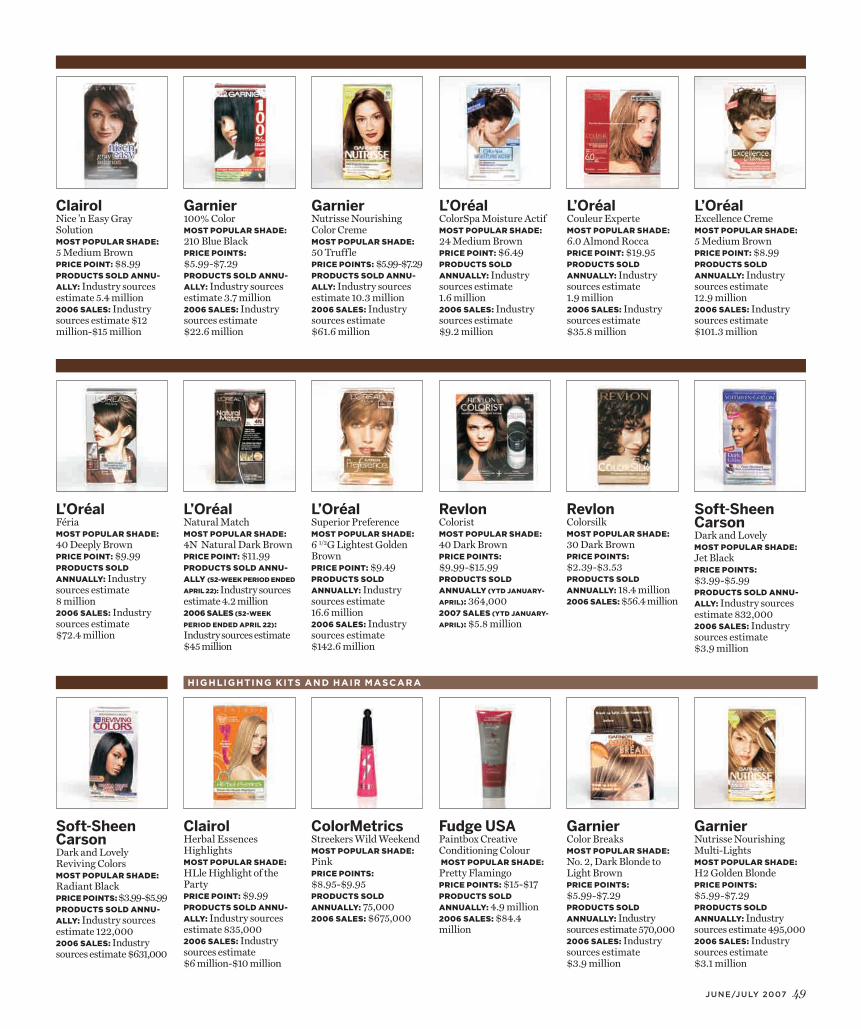

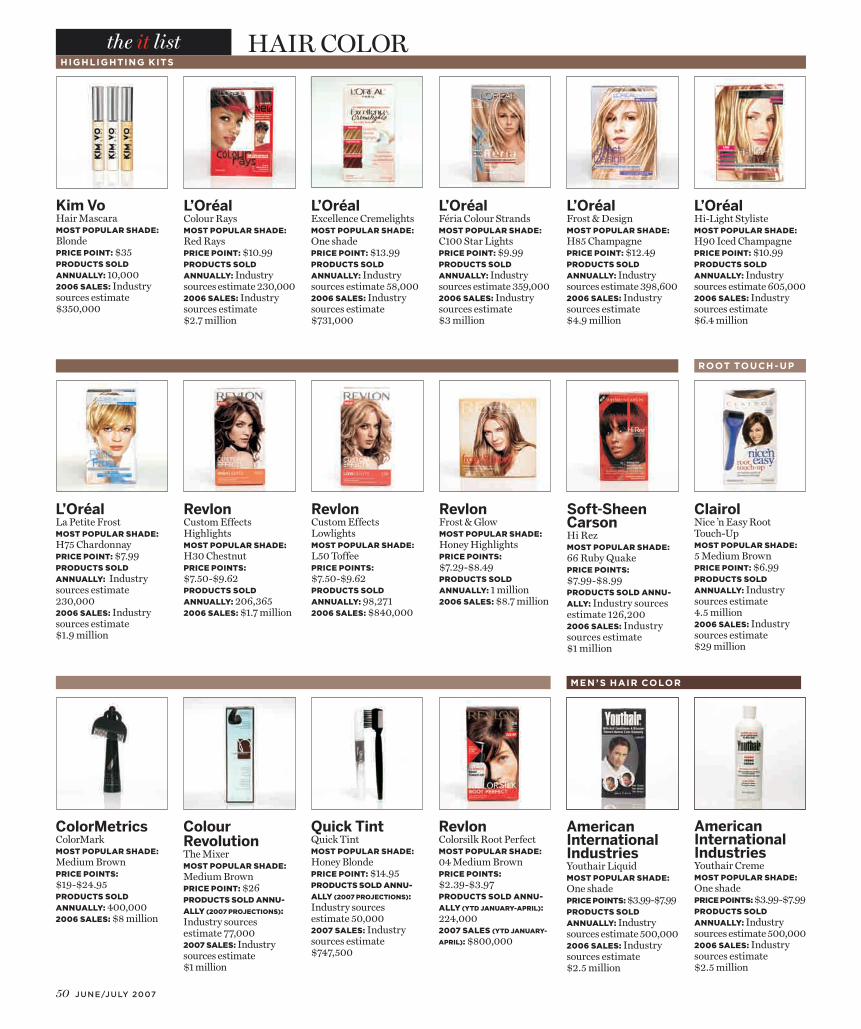

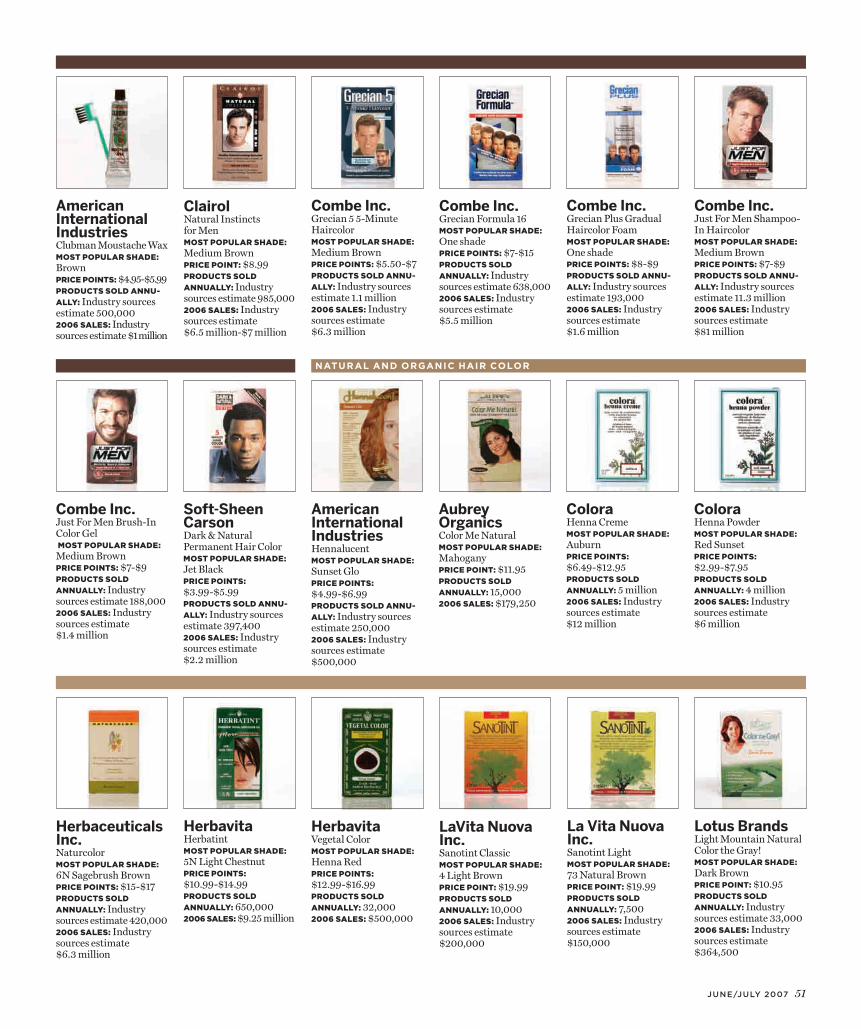

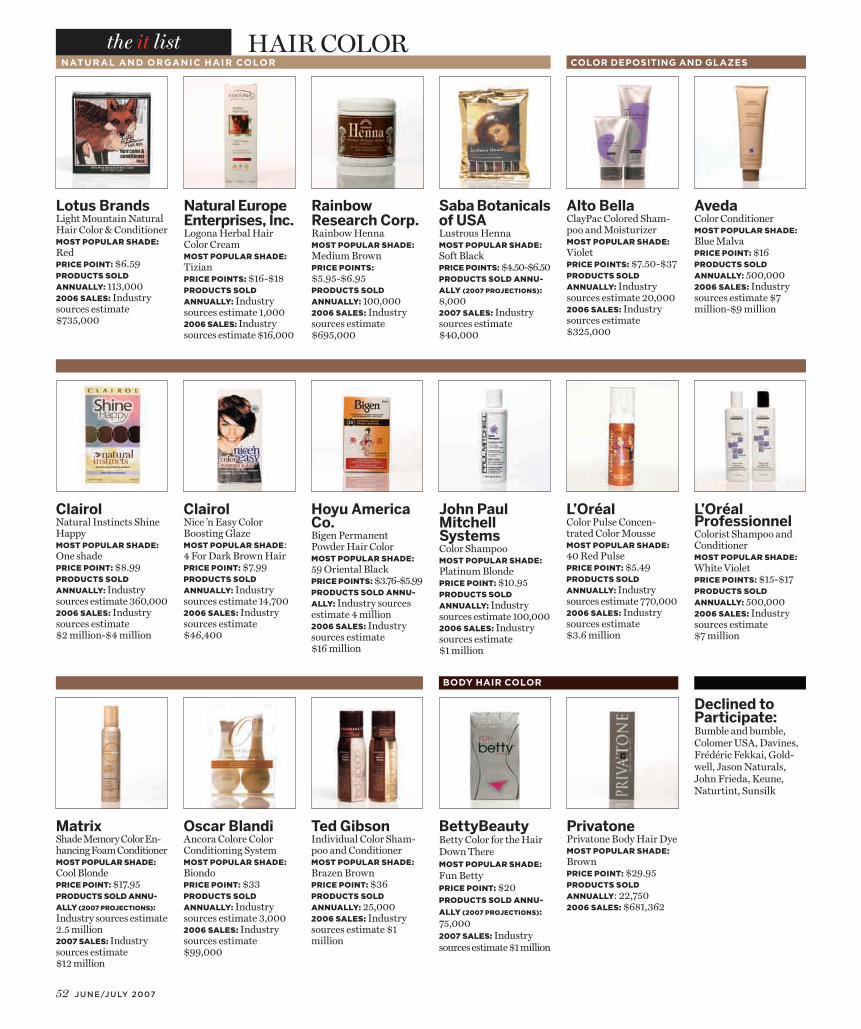

48TheItList:Hair Color An A to Z guide to at-home dyes, highlighting kits, hair mascaras and glazes galore—for covering gray or inviting play.

54LastCall:On Winning Customers for LifeValuable lessons for sustaining consumer loyalty, courtesy of FIT’s graduating class.

FEATURES

24Arnold’sNewOrderProcter & Gamble’s president is reinventing the beauty game and steering the packaged goods company to the top.

32CalloftheWildMaster stylist Oribe creates head-turning, mind-blowing looks for fall.

40Retail’sTidalShiftBeauty shopping will never be the same. As the number of department stores dwindle, major brands are turning to alternative channels and making some unexpected choices.

42 ‘It’BagChroniclesBeauty insiders ponder the formula for fashion’s “It” bag phenomenon.

445For5Five leading retailers face tough questions on how to better service the beauty customer.

lo

uis

vu

itt

on

ru

nw

ay

ph

ot

o b

y s

te

ph

an

e f

eu

ge

re

WWD IS A REGISTERED TRADEMARK OF ADVANCE MAGAZINE PUBLISHERS INC. COPYRIGHT ©2007 FAIRCHILD FASHION GROUP. ALL RIGHTS RESERVED. PRINTED IN THE U.S.A. VOLUME 193, NO. 127, June 15, 2007, WWD (ISSN 0149–5380) is pub-lished daily (except Saturdays, Sundays and holidays, with one additional issue in January and November, two additional issues in March, May, June, August and December, and three additional issues in February, April, September and October) by Fairchild Fashion Group, which is a division of Advance Magazine Publishers Inc. PRINCIPAL OFFICE: 750 Third Avenue, New York, NY 10017. Shared Services provided by Condé Nast Publications: S. I. Newhouse, Jr., Chairman; Charles H. Townsend, President/CEO; John W. Bellando, Executive Vice President/COO; Debi Chirichella Sabino, Senior Vice President/CFO; Jill Bright, Execu-tive Vice President/Human Resources. Periodicals postage paid at New York, NY, and at additional mailing offices. Canada Post Publications Mail Agreement No. 40644503. Canadian Goods and Services Tax Registration No. 886549096-RT0001. Canada Post: return undeliverable Canadian addresses to: P.O. Box 503, RPO West Beaver Cre, Rich-Hill, ON L4B 4R6 POSTMASTER: SEND ADDRESS CHANGES TO WOMEN’S WEAR DAILY, P.O. Box 15008, North Hollywood, CA 91615–5008. FOR SUBSCRIPTIONS, ADDRESS CHANGES, ADJUSTMENTS, OR BACK ISSUE INQUIRIES: Please write to WWD, P.O. Box 15008, North Hollywood, CA 91615-5008, call

800-289-0273, or visit www.subnow.com/wd. Please give both new and old addresses as printed on most recent label. First copy of new subscription will be mailed within four weeks after receipt of order. Address all editorial, business, and production correspondence to WOMEN’S WEAR DAILY, 750 Third Avenue, New York, NY 10017. For permissions and reprint requests, please call 212-630-4274 or fax requests to 212-630-4280. Visit us online at www.wwd.com. To subscribe to other Fairchild magazines on the World Wide Web, visit www.fairchildpub.com. Occasionally, we make our sub-scriber list available to carefully screened companies that offer products and services that we believe would interest our readers. If you do not want to receive these offers and/or information, please advise us at P.O. Box 15008, North Hollywood, CA 91615-5008 or call 800-289-0273. WOMEN’S WEAR DAILY IS NOT RESPONSIBLE FOR THE RETURN OR LOSS OF, OR FOR DAMAGE OR ANY OTHER INJURY TO, UNSOLICITED MANU-SCRIPTS, UNSOLICITED ART WORK (INCLUDING, BUT NOT LIMITED TO, DRAWINGS, PHOTOGRAPHS, AND TRANSPARENCIES), OR ANY OTHER UNSOLICITED MATERIALS. THOSE SUBMITTING MANUSCRIPTS, PHO-TOGRAPHS, ART WORK, OR OTHER MATERIALS FOR CONSIDERATION SHOULD NOT SEND ORIGINALS, UNLESS SPECIFICALLY REQUESTED TO DO SO BY WOMEN’S WEAR DAILY IN WRITING. MANUSCRIPTS, PHOTO-GRAPHS, AND OTHER MATERIALS SUBMITTED MUST BE ACCOMPANIED BY A SELF-ADDRESSED STAMPED ENVELOPE.

Susan Arnold photographed at Procter & Gamble headquarters by Melanie Dunea.

oN ThE covER

Chasing the “It” bag: Fashion houses and beauty marketers are pros at creating the next big thing. But the secret to maintaining high demand at inflated prices, season after season, continues to elude most.

PeteBorn Executive Editor, Beauty JennyB.Fine Editor Kim-VanDang Consulting Editor

JenniferWeil European Beauty Editor AndreaNagel Mass Market Beauty Editor JulieNaughton Senior Prestige Market Beauty Editor MollyPrior Mass Market Beauty News Editor MatthewW.Evans Beauty News Editor MichelleEdgar Associate Beauty Features Editor FayeBrookman Contributing Editor MeganMcIntyre Assistant Editor MaggieJoslyn Editorial Intern DeborahBoylan Copy Editor

ContributorsSamanthaConti,BridCostelloandNinaJones(London),StephanieEpiro(Milan),

MilesSocha(Paris),MarcyMedina(LosAngeles),KatherineBowers(Boston),MelissaDrier(Berlin),GeorgiaLee(Atlanta),HollyHaberandRustyWilliamson(Dallas),KojiHirano(Tokyo)

Art AndrewNimmo Consulting Art Director DaniloMatz Consulting Art Director PamelaOlecki Consulting Art Director AnitaBethel Photo and Imaging Director CarrieProvenzano Associate Photo Editor

PhotogrAPhersPashaAntonov,JohnAquino,TalayaCenteno,GeorgeChinsee,SteveEichner,

KyleEricksen,ThomasIannaccone,RobertMitra

Advertising RalphErardy Senior VP, Group Publisher JaySpaleta Publisher DebraGoldberg Associate Publisher, Beauty RandiSegal Mass Beauty Director RonTroxell Senior Account Manager, West Coast AmelieBarsi European Beauty Manager, Paris MicheleSutton Executive Beauty Assistant BillAndrulevich General Manager, Fairchild Fashion Group RichardCherichella Business Director, Fairchild Fashion Group JanetJanoff General Manager, WWD

MArketing/ProMotion JodiMarchisotta Associate Publisher, Marketing DanielleMcMurray Creative Services Director ZoraidaWalker Senior Manager, Marketing and Promotion BrookeFitzsimmons Marketing Manager LindsaySwartz Marketing Manager BenjaminGelinas Design Director MarkRamel Design Manager DickSilverman Director of Special Projects ToniNicolino Associate Manager of Special Projects KathleenCallahan Classified Marketing Manager MaggieGould Marketing Coordinator LilyFleishman Marketing Assistant AndreaKaplan VP, Corporate Communications

ProduCtion GenaKelly Executive Director, Manufacturing and Distribution ChrisWengiel Group Production Director JohnRicotta Production Director JillBreiner Associate Production Manager AhmedPruitt Production Coordinator

CirCulAtion WendyFrank Circulation Director RichardFranz Circulation/Sales Director JohnCross Fulfillment Director JamesRossi CirculationMarketing Director SusanKline Fulfillment Manager

DanielLagani President, Fairchild Fashion Group

A FAirchild PublicAtion

� june/july 2007

shifting tidesTHE FIRST TIME I TRIED TO SURF, A STROng CURREnT PROPELLED my board so fast toward the beach that I hit sand before I ever had a chance to stand up. After several failed attempts and swallowing more than my share of seawater, I made a last-ditch effort to accomplish my mission. As a new wave took form and I paddled to catch it, the earth suddenly seemed to stop spinning. For a moment, everything played out in slow motion and I somehow, calmly and quietly, found time to push myself up onto my feet and ride all the way in to shore.

Athletes refer to this phenomenon as “being in the zone.” And if any major executive today knows the feeling, it would be Susan Arnold. named president of all Procter & gamble business units just last month, she now runs a $75 billion-a-year empire. Increasingly, beauty sales account for a significant share of that pie. And it’s no secret: She is maneuvering P&g in a bid to overtake L’Oréal as the largest cosmetics company in the world.

But what’s most interesting about Arnold is not that she’s determined to win the race, but that in the process of getting to the finish line, she is profoundly changing the game. Right before going on maternity leave this summer, Jenny B. Fine traveled to P&g headquarters in Cincinnati to talk strategy with this dynamic leader.

On the subject of change, Pete Born writes eloquently in this issue about the continuing erosion of department store dominance in America and

where even the big guns, including L’Oréal, Lauder, Dior and Arden, are now taking some of their business. The Internet and television are just two of several enterprising options.

given the retail sea change, Molly Prior has gathered five innovative merchants from every channel of trade for an insightful panel discussion on how they are staying ahead of the curve.

If only it were as easy as launching the next “It” bag. In between meeting all her deadlines for Women’s Wear Daily, Sharon Edelson examines why beauty marketers don’t emulate their fashion counterparts and churn out status items at sky-rocketing prices, season after season.

Well, maybe washing in and out with the tide is not the way to go anyhow. For brands seeking long-term relationships with their consumers, Michelle Edgar gets guidance from mentors of FIT’s graduating class.

Believe it or not, looking washed-out is in for fall. A so-cool-it’s-cold pallor, paired with either dark eyes or bold lips, is a surprisingly strong trend among those spotted on the runways and showcased in these pages.

More fabulous, hair-raising news: Photographer guy Aroch snaps standout styles by ever-inventive mane man Oribe. And Megan McIntyre rounds up every hair color product on the market for this month’s It List.

It’s all to dye for. So, happy reading! I’m going surfing. Peace, Kim-Van Dang p

ho

to

by

ge

tt

y im

ag

es

editor’s letter

10 june/july 2007

Derek Jeter, four-time World Series championDriven / Avon

Avon signed on the Yankees’ shortstop captain last July to launch the men’s scent. As part of a multiyear deal, Jeter is involved in product

development. Last month, the Driven franchise expanded into skin care.What is your grooming routine?In the past, I pretty much woke up, shaved, put on deodorant and ran out. Now, moisturizer with SPF is important. I’m getting older.What can’t you live without?My favorite is the shaving gel. The Yankees have strict grooming rules. What were your teammates’ reactions to your beauty deal? In big groups, they joke about it. But one-on-one, they ask for samples. So I give it to them—for a small fee.What do men look for? Real results. But they don’t want to sit in front of the mirror for more than 10 minutes.

Laird Hamilton, big-wave surfer and originator of tow-in surfingDAviDoff Cool WAter / Coty

Coty signed the maverick American surfer last spring as spokesperson for its Davidoff Cool Water fragrance. His wife, health and exercise guru

Gabrielle Reece, is the spokeswoman for Davidoff Cool Water Wave Woman.What is your grooming routine?I am a casual guy and I don’t use a lot of products.What can’t you live without?The one thing I use is Eminence Organic Sunscreen Defense SPF 30, which Gabby convinced me to try.What were your friends’ reactions to your beauty deal?I have heard a few jokes, but I believe in the product, so I do not take it personally.

Tom Brady, three-time Super Bowl championStetSon / Coty BeAuty

Coty Beauty recruited the New England Patriots’ star quarterback in April. He will represent the brand for the next two and a half years.

What is your grooming routine?I’m pretty low-maintenance. But since it gets cold in the winter, I have to use lotion from time to time. What can’t you live without?My essentials for the road are a good shampoo, a razor and deodorant. What were your teammates’ reactions to your beauty deal?They don’t really pay much attention to it. We have a great group of guys. As long as I don’t refer to it as “my beauty deal,” I should be in good shape.What do men look for?It varies by individual taste. But when you take care of yourself, you gain confidence—and that’s what guys are looking for.

Jeff Gordon, four-time NASCAR WINSTON Cup championHAlSton Z-14 / eliZABetH ArDen

Gordon has represented this fragrance for nearly three years. There’s a cologne, shower gel, deodorant, aftershave and aftershave balm.

What is your grooming routine?I kept it simple, but being exposed to this industry has definitely opened my eyes. What can’t you live without?While I like to go unshaven, a close shave and a great fragrance are necessities when doing a media appearance.What do men look for?I look for key items that do it all.Do you have any nicknames? I’m called “Four Time” for the number of championships I’ve won. Hopefully, that nickname will change this year.What’s the craziest style you’ve tried? I grew a bad mustache as a teenager. I also got a buzz cut once.

Jimmie Johnson, 2006 NASCAR NEXTEL Cup championDAytonA 500 / eliZABetH ArDen

Since last fall, Johnson has been the spokesman for the Daytona 500 collection—a cologne, aftershave, shower gel and aftershave balm.

What was your grooming routine?Shower, shave and out the door. What is your grooming routine now? My routine hasn’t changed, except, of course, for a spray of Daytona 500.What grooming products can’t you live without? I would like to meet the guy who can live without a good-quality shaving kit. That is essential for me. It also helps to have great cologne.What do men look for?Everyone is always in a rush, so most of us are looking for fast and effective products.

What started out boiling has tempered down to a simmer in the much-heralded world of men’s grooming. according to the nPd group, the market hit its peak in 2005 and has been languishing ever since, due to department store consolidation and lack of consumer education.

shaving treatment, a staple category even for men who still can’t figure out what an exfoliator does, actually declined last year, causing retailers and market experts to take a hard look at the sector.

but just because the metrosexual concept has been declared dead doesn’t mean the grooming category is too, as nPd senior beauty industry analyst Karen grant reminds us. “the men’s market is still in its infancy; it’s where women’s was 10 or 20 years ago,” she says.

to her point, there have been some signs of life. even as shaving cream sales slipped, sales of moisturizers, cleansers and antiaging products all inched up last year. says grant, “it’s all about getting [men] to understand that this is something conducive to how they identify themselves, so it comes across as very masculine.” hope on the horizon comes in the form of new launches from established brands.

lancôme is introducing its antiaging men’s line this month with manly-man british actor Clive owen, as its face. iconic hardware brand ace is launching a range of implements aimed at “manscaping” everything from wayward body hairs to toenails. even the green market is anteing up, with natural brand burt’s bees introducing man- and earth-friendly body and shave products this october.

but the sector’s saving grace may be the “other hair” category. (read: thinning-hair treatments.) “hair overall is a small component of the men’s market,” says grant, “but it is where we are seeing the most excitement or at least activity. it’s a teeny- tiny category, but it’s growing by triple digits.”

this puts brands like aveda at an advantage as it launches a scalp-focused hair care line this fall, dubbed Men Pure-formance. says heidi norman, executive director of marketing for the brand, “Men’s scalps differ biologically from women’s. they’re thicker, more sensitive and have more oil, which can lead to dryness and flaking. this is a new platform and identity for men and for aveda.”

the retail landscape is also changing as men discover alternative shopping channels. avon saw great success with its derek Jeter driven fragrance, so much so that the company expanded it into a full line of skin care products.

their direct-sell competitor, Mary Kay, will counter with the introduction of MK Men, a four-item grooming and shaving line.

Finally, online destinations like amazon.com are enticing the XY set. “We’re seeing a lot more democratization of the marketplace,” grant observes. “there’s a lot more options out there and [men] are willing to try them out.” —MegAn MCintyre

st

ill

lif

e P

ho

to

s b

y g

eo

rg

e c

hin

se

e ;

br

ad

y b

y J

im r

og

as

h/W

ire

ima

ge

; ha

mil

to

n b

y e

ric

c

ha

rb

on

ne

au

/Wir

eim

ag

e; J

et

er

by

Ke

vin

ma

zu

r/W

ire

ima

ge

WHAT MEN WANT

people, places & lipsticks

ManPower Call it a war on stagnant sales as the men’s market launches an all-out offensive this fall in another effort to grow the sector.

Clockwise from left: Fall offerings from Clubman, Lancôme, C.O. Bigelow, Burt’s Bees and Mensgroom.

Hollywood stars aren’t the only folks with fat beauty contracts these days. A number of top athletes, who endorse everything from fragrance to aftershave, talk candidly about being in the game. —CoMpileD By MiCHelle eDgAr

Look for Avon’s Derek Jeter Driven Daily Moisturizer SPF 15, Aveda’s Liquid Pomade, Mary Kay’s Shave Foam and Ace’s Dual Power Trimmer to invigorate sales.

São Paulo, is giving frizz buster John Frieda a run for his money. After jumping ship from B2V Salon to Sunset Strip’s Argyle Salon & Spa last year, Ribeiro is launching the Brazilian Blowout, a single-application treatment that harnesses a patent-pending chemical found in spray tanning to smooth out kinky hair.

THANKS TO THE J. SISTERS from Vitoria, Brazil, New Yorkers discovered the Brazilian bikini wax in 1994. Soon, women all over America went wild for the procedure that leaves nothing more than a “landing strip” down there.

Now, another beauty treatment from the birthplace of Gisele is vying to be the next big thing.

Mauricio Ribeiro, who hails from

To begin the 90-minute process, hair is washed with anti-residue shampoo. Next, it is sectioned into four parts and treated with the chemical. Finally, it is dried with a flat iron to seal in the solution.

Ribeiro tells his customers (professional women ages 20 to 50) that, like a bad boyfriend, the $350 service requires no commitment and only lasts up to eight weeks.

“A lot of people try the Japanese [straightening system]. But after you do it for so many times, it can burn your hair,” he says. “I am not actually altering the hair structure, I am just organizing it on a superficial level. The hair loses all the frizz.”

In Brazil, women rushed to salons for the nonpermanent smoother. At the Argyle, the only U.S. salon currently offering the service, Ribeiro does about seven blowouts per week. But word is spreading. Already, he has gotten calls from salons in Dubai and Australia inquiring about the treatment.

“Brazilian women are into their looks so they try things and discovered this,” he says. —rachel brown

ABOVE AND BEYOND. IT’S THE best way to characterize how far beauty companies are willing to go to satiate top retailers’ appetites for exclusives.

“The beauty business is catching up with the retail apparel sector’s discovery that it is very important to differentiate,” says David Wolfe, creative director of the Doneger Group trend forecasting and buying service. “A product that is exclusive to one retailer is a valuable asset because it lures customers who are somewhat stupefied by the sea of sameness in brands that

are so widely distributed that they have little or no cachet.”

This September, niche perfumer Bond No. 9 is

partnering with Saks Fifth Avenue to launch two new fragrances: Bond No. 9’s Saks Fifth Avenue for Her and for Him. The deal marks the first time a specialty store has commissioned a fragrance company to produce its eponymous scents. “Ninety percent of the bottle is Saks’ interpretations,” said Laurice Rahme, owner and founder of Bond No. 9.

Amorepacific is giving Neiman Marcus a very special birthday present this July. To celebrate the luxury retailer’s 100th anniversary, the South Korean skin care firm is introducing Time Response Skin Renewal Serum, a blend of 100 high-concentration healing botanical actives. To put things into perspective: Amorepacific uses only 10 ingredients in some of its products, while the Time Response line usually features between

40 and 60 active ingredients. Capitalizing on the regenerative power of the green tea plant, the reparative serum is designed to protect skin against free radicals and environmental aggressors, reduce inflammation to counter aging and increase micro-circulation. —M.e.

With one memorable quote from 90210 alum Jennie Garth, indie fragrance Child became a full-fledged phenomenon in the Nineties. Stingy divas were ripping off the labels in order to conceal their scent secret from friends. This decade’s answer to Child may well be Clementine, a neroli-based floral scent that’s keeping Hollywood starlets smelling sweet. Creator Melissa Flagg, 41, spent her preteen spring breaks in Palm Springs inhaling the orange blossom-laced air during cool, lazy evenings. “I wanted to capture it in a bottle,” says Flagg. Nicole Cardi, director of retail at Fred Segal Beauty, where Clementine roll-ons sell exclusively at $40 for 0.125 oz. and $70 for 0.33 oz., is pleasantly surprised that the fragrance has quickly collected a devoted following. Lindsay Lohan, Michelle Trachtenberg and Scarlett Johansson have taken a liking to Clementine. Ironically, the star of the upcoming Nanny Diaries says the fragrance reminds her of her youth. Cardi remembers one shopper in particular who dabbed on the scent, but didn’t buy it, only to come back after her husband insisted she become a regular wearer. —r.b.

HER MANE IS RIOAnd she strAightens out her strAnds on L.A.’s sunset strip

people, places & lipsticks

Oh My Darling

Amorepacific’s 100-ingredient serum (left) and Bond No. 9’s Saks fragrance.

Smooth moves at the Argyle Salon & Spa.

For your store only

Scarlett Johansson; the Clementine scent.

st

ill

lif

e p

ho

to

s b

y t

ho

ma

s ia

nn

ac

co

ne

; sc

ar

le

tt

Jo

ha

ns

so

n b

y s

te

ph

an

e f

eu

ge

re

; br

az

ilia

n b

lo

wo

ut

by

min

de

e c

ho

i

12 june/july 2007

A new reALm in retAiL excLusives

14 JUNE/JULY 2007

what’s in store

01

05

04

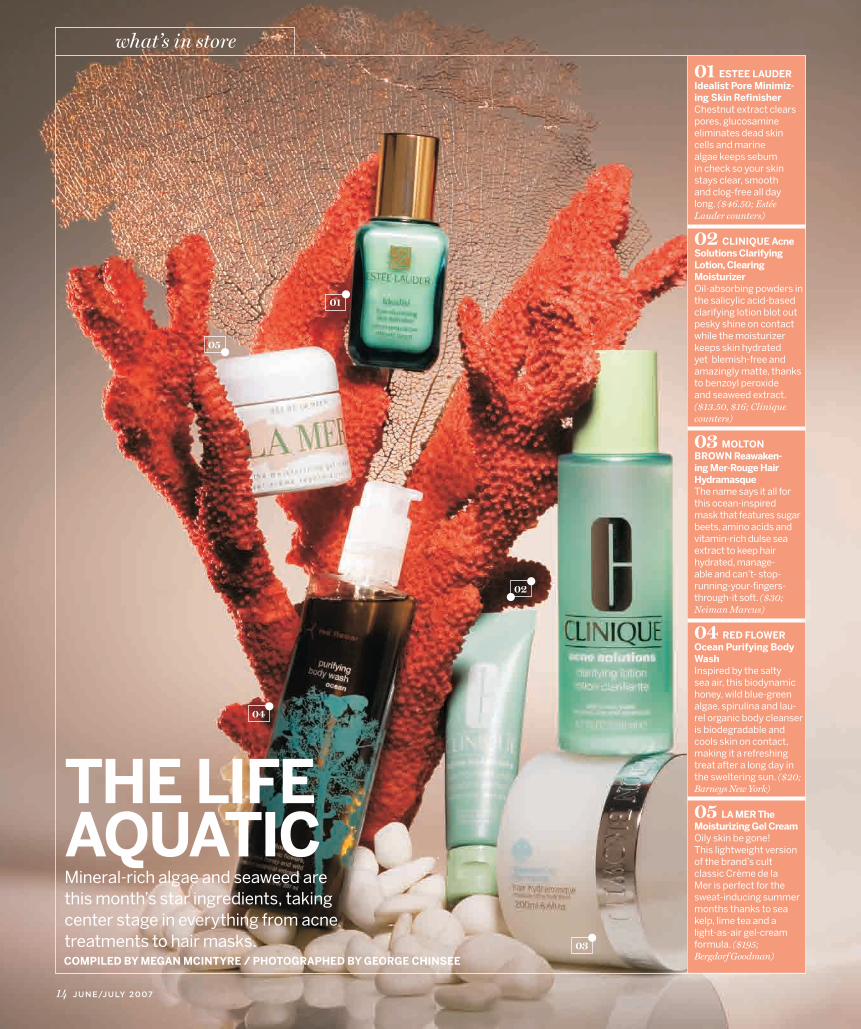

01 EstEE LaudEr Idealist Pore Minimiz-ing skin refinisher Chestnut extract clears pores, glucosamine eliminates dead skin cells and marine algae keeps sebum in check so your skin stays clear, smooth and clog-free all day long. ($46.50; Estée Lauder counters)

02 CLInIquE acne solutions Clarifying Lotion, Clearing Moisturizer Oil-absorbing powders in the salicylic acid-based clarifying lotion blot out pesky shine on contact while the moisturizer keeps skin hydrated yet blemish-free and amazingly matte, thanks to benzoyl peroxide and seaweed extract. ($13.50, $16; Clinique counters)

03 MoLton Brown reawaken-ing Mer-rouge Hair Hydramasque The name says it all for this ocean-inspired mask that features sugar beets, amino acids and vitamin-rich dulse sea extract to keep hair hydrated, manage- able and can’t- stop- running-your-fingers-through-it soft. ($30; Neiman Marcus)

04 rEd FLowEr ocean Purifying Body wash Inspired by the salty sea air, this biodynamic honey, wild blue-green algae, spirulina and lau-rel organic body cleanser is biodegradable and cools skin on contact, making it a refreshing treat after a long day in the sweltering sun. ($20; Barneys New York)

05 La MEr the Moisturizing Gel Cream Oily skin be gone! This lightweight version of the brand’s cult classic Crème de la Mer is perfect for the sweat-inducing summer months thanks to sea kelp, lime tea and a light-as-air gel-cream formula. ($195; Bergdorf Goodman)

tHE LIFE aquatICMineral-rich algae and seaweed are this month’s star ingredients, taking center stage in everything from acne treatments to hair masks.

02

CoMPILEd By MEGan MCIntyrE / PHotoGraPHEd By GEorGE CHInsEE

03

16 JUNE/JULY 2007

what’s in store

01

06

07

05

04

03

01

02

JuICy FruIt From sexy, shiny glosses to succulent scents, these beauty products are so sweet- smelling, you’ll be tempted to take a bite.

01 MaC tendertones sPF 12 in Pucker, softnote, shush! Coffee seed and muru- muru butter give a balm-like feel with glossy shine. The strawberry-kiwi flavor make these a truly lip-smacking indulgence. ($14.50 each; MAC counters)

02 nars skin Ginger Grapefruit Bath and shower Gel Spicy ginger and tart grapefruit collide in this sensual gel that makes for an invigorating shower experience. ($38; narscosmetics.com)

03 L’orEaL Kids splash series Extra Gentle 2-in-1 shampoo and Conditioner in sunny orange Protect your mini-me with this yummy-scented detangling hair cleanser that also helps negate the harsh effects of too much chlorine. ($2.99; mass retailers)

04 GarnIEr FruCtIs Play style Pliable Clay Fruit micro-waxes in this cool matte clay leaves short hair styles frizz-free, texturized and sexily defined. ($3.99; mass retailers)

05 CovErGIrL wetslicks Fruit spritzers in Berry splash, watermelon splashGive lips a lacquered finish with these ultra- conditioning glosses in 12 summery shades. ($5.99 each; mass retailers)

06 tHE Body sHoP strawberry Puree Body Lotion Fruit acids from strawberry pulp refine skin texture while natural shea butter leaves it feeling soft and supple. ($13; thebodyshop.com)

07 Bond no. 9 Coney IslandSpend the afternoon at this beachside playground or recall the feeling with the whimsical scent of guava, melon, margarita mix and chocolate. ($180; select Saks Fifth Avenue)

01 oLay definity Eye Illuminator The nifty-looking spiral caught our eye, but this serum is a star thanks to “smart particles” of mica that even out discolorations and help tired skin glow. ($25.99; mass retailers)

02 PHILosoPHy Booster Caps Filled with a healthy dose of antiaging retinol, these pint-sized capsules pack a power-ful regenerating punch. ($30; Sephora)

03 dErMaLoGICa overnight Clearing Gel Give breakouts the boot with this adult acne-fighting gel that banishes excess sebum and dead skin cells while you snooze. ($40; Blue Mercury)

04 ELEMIs Pro- Collagen oxygenating night CreamYour complexion gets a bedtime boost with this oxygen-replenishing cream that detoxifies and energizes. ($167; Bergdorf Goodman)

05 LanCoME Primordiale Cell defenseFend off free radicals with this hypercharged serum that uses minerals and vitamins to neutralize environ-mental aggressors and retexturize damaged skin. ($62; Lancôme counters)

06 ELIzaBEtH ardEn Intervene Eye Pause & Effect Moisture Eye Cream Get rid of pesky crow’s feet while preventing future fine lines with this conditioning gel-cream. ($42; Elizabeth Arden counters)

07 zELEns skin science Cellular reconstruction night Cream Developed by skin cancer authority Dr. Marko Lens, this cream features 20 natural active ingredients to help diminish the look of wrinkled, tired skin in a snap. ($225; Space NK)

18 JUNE/JULY 2007

what’s in store

CLEan sLatEEase away a stressful day with soothing creams to revive and rejuvenate your skin while you catch some much needed zzz’s.

06

01

05

07

04

03

02

20 JUNE/JULY 2007

manager of beauty, jewelry and accessories, who adds that increasingly, consumers are embracing beauty trends seen on the runways.

Standouts in the plum category include Yves Saint Laurent’s limited edition eye palette (above, E). Available in two color combinations, the compact features a female figure in an off-the-shoulder evening gown with a large bow. Estée Lauder’s all-over crème shadow stick (H), designed to last up to 12 hours, can be used as a base color or a highlighter on eyes with its semi-pearl finish. Inspired by an 18th-century Chinese box given to its international artistic director Gucci Westman, Lancôme is introducing a multifaceted Destiny Cube (D) with green and pink eye shadows on one side and lipstick and gloss on the other.

Cool neutrals, deep plums and black-based hues make headlines this season. But don’t discount true reds.

st

yl

ed

by

da

nil

o m

at

z

By Michelle edgar / still life photographs By thoMas iannaccone

“Plums and greens are the new neutrals,” says makeup artist Pati Dubroff, Christian Dior’s international celebrity makeup artist. “It’s a way to do daytime or soft eyes, but still inject color. The plums enhance all eye colors and create an effect that’s romantic, but not too sweet.”

Vincent Longo, makeup artist and founder of the makeup brand that bears his name, is also seeing a variety of green shades that, he says, carry a “coolness.”

Retailers like Bergdorf Goodman are likewise focused on plum hues. “Plum is one of the strongest colors of the season,” says Ed Burstell, senior vice president and general merchandise

Fall Color Forecast

PLUM Grove Marvelous Mauves and Mossy greens

a closer look

A

B

C

D

E

F

G

H

I

J

Makeup is once again set to BecoMe the Best-selling category in luxury Beauty this year, after strong sales catapulted it to the top spot in 2006. “Makeup has now taken the place of fragrance as the nuMBer-one selling category,” says karen grant, npd senior Beauty industry analyst, adding that More than one of every four dollars in the prestige category is spent on Makeup in the fourth quarter. “fall is now the nuMBer-one season for color cosMetics like Mascara, eye shadows, lip color and gloss. Makeup used to Be a trend during the first quarter and into early spring.”

JUNE/JULY 2007 21

According to Lord & Taylor’s Zinn Moore, lipsticks—especially bright red ones—are making a comeback.

“At the fashion shows, while the rest of the face featured fresh neutral tones, a true red, especially in the lips, was played up,” observes Longo. “Whether it’s a reddish brown or reddish topaz, there’s a richness with reds. There are colors that can be splashed together with red.”

Gordon Espinet, vice president of makeup artistry at MAC Cosmetics, also noticed “a lot of strong intense reds,” especially at Roberto Cavalli.

Dubroff adds, “The true red lip is that touch of retro glamour that is so right this season.”

Bettina O’Neill, Barneys vice president divisional merchandise manager, notes that both Shu Uemura and Chanel are promoting new red lipstick shades, offering consumers enough hues

for every skin tone.Guerlain is introducing KissKiss Lipstick in

six new shades this season with golden, brown and rosy undertones, including a bold red called Fabulous Rouge (left, G).

And while Chanel is covering its bases with the launch of four neutral hues of Rouge Hydrabase, a cream formula, it is also releasing a new shade of Rouge Allure lipstick for holiday—a heart-stopping red called Dazzling (F).

Fresh is building on the success of its Sugar Lip Treatment SPF 15 with high-shine, non-sticky Sugar Lip Gloss. In 10 shades, including a true red called Sugar Shag (E), it’s packed with moisturizing ingredients including shea butter, jojoba oil, grape seed oil, black currant seed oil and vitamin E.

Finally, there are plenty of red-hot nail colors to complement the plethora of red lipsticks and glosses this season. Standouts include offerings from IsaDora (B) and Sally Hansen (D).

PLUM GrovE / LEFT

A christian Dior 5-Colour Eyeshadow in Pink Idol (770)

B Giorgio armani Eye Mania in 10

C Mac Lipglass in Atmospheric

D Lancôme Destiny Cube Secret Game for Eyes and Lips

E Yves saint Laurent Palette Esprit Couture in

Harmony N°2

F clarins Gloss Appeal in Ginger (01)

G chanel Silky Eyeshadow Duo in Lotus-Cactus

H estée Lauder Double Wear Stay-in-Place

ShadowStick in Pink Pearl (09)

I Bourjois Le Dressing du regard Eyeshadow in 54

J tarte Inside out vitamin-Infused Lipstick in Zen

cooL NeUTrALSnude and shiMMery

TrUe roUGefire-engine reds

F G

H

A B

C

D

E

CooL NEUTrALS / ABovE

A estée Lauder Pure Color Eye Shadow in Mocha Cup

B Maybelline Instant Age rewind Double Face Perfector

C Lorac Take a Brow

D Benefit Silky Matte Powder Eye Shadow in

Low Profile

E Bobbi Brown Eye Palette in Stonewash Nude

F Givenchy Prisme Foundation in Shaping Beige (3)

G smashbox Eye Shadow Trio in Indulgence

H sally Hansen Salon Nail Lacquer in Alabaster

TrUE roUGE / BELoW LEFT

A Yves saint Laurent rouge Pur in Star red N°137

B IsaDora Perfect Nail Polish in Deep red (49)

C Nars Lipstick in Flamenco

D sally Hansen Lacquer Shine Nail Color in

Luminous

E Fresh Sugar Lip Gloss in Sugar Shag

F chanel rouge Allure in Dazzling

G Guerlain KissKiss Lipstick in Fabulous rouge (531)

H shu Uemura rouge Unlimited in rD 195

A

B

C

D

E

F

G

H

While past falls have been marked by strong color, the surprise look this season is super natural.

“It’s about reinventing nudes,” says Bobbi Brown, founder and chief executive officer of Bobbi Brown Cosmetics. “This fall, nudes with a little bit of tone and shimmer are in. There are different textures, but the colors are inspired by natural skin tones of the eyelids. They’re best used for enhancing eyes.”

It’s one trend Brown must be thrilled about. After all, the makeup artist pioneered the look when she launched her line in 1991. According to Brown, neutrals were considered ho-hum until she came along and paired them with black mascara and eyeliner. “The full monochromatic nude face, lip and cheek is classic Bobbi,” she says.

Lord & Taylor senior vice president and general merchandising manager Barbara Zinn Moore adds that today’s technology allows companies to create a variety of nude shades with different finishes and color gradations.

“You can have a creamy beige or a pinkish beige in a palette of 20 beige tones, with subtle color variations and different finishes,” she says.

Bergdorf Goodman’s Burstell adds that the Michael Kors, Yves Saint Laurent and Stella McCartney fall runways all featured lots of cool neutrals. “It’s all about completely unadorned, fresh glowing skin,” he said.

22 JUNE/JULY 2007

a closer look

BLAcK & BLUeslate and sapphires

If you’re cruisin’ for a bruisin’—or at least the bruising look of smokey eyes, you’re in luck.

MAC Cosmetics’ Blue Storm and Smoke Signal’s collection features “a classic approach to beauty, inspired by Milanese women,” says Espinet. “It’s not about browns, but rather the cool combination of gray, blue and silver.”

Bobbi Brown’s collection takes a cue from Elizabeth Taylor’s dark blue sapphire jewelry. “Deep colors with a lot of black and blue create products that are smoldering, sexy and wearable. Women of all eye colors can wear them; they’re not just for blue eyes,” she says.

“From accessories to ready-to-wear collections, metallics are very strong this season, so it’s no surprise that makeup is following the trend in a big way,” notes Lord & Taylor’s Zinn Moore. “It’s either about smoky, shiny and metallic shades or very natural tones with nudes and beiges in different textures,” she says.

Dior’s Dubroff is excited about navy blue. She says it could be a great alternative or addition to a pair of black smoky or lined eyes.

Fall makeup is also going retro with a variety of colored palettes inspired by the post-disco Eighties.

“These are girls who might have been punks in the Seventies and Eighties. We’re taking that favorite era of ours and making it more sophisticated. It’s not glittery, but more like glamour gone cool,” Espinet says.

Burstell saw lots of Eighties-inspired work at

1980snew wave pink and glitter

the Chloé, Louis Vuitton and Jean Paul Gaultier shows. “It’s another variation of the bold lip with very pale skin and that splash of color across the face,” said Burstell, who notes that the variation of colors on the eyes is punk-like, especially when coupled with black eyeliner.

“There’s lots of color on the eyes, which makes it very dramatic,” echoes Barneys’ O’Neill.

Judy Wray, catagory manager at Rite Aid, adds that the colorful trend has inspired the use of less foundation.

C

D

E

A

B

A

C

D

E

F

G

BLACK & BLUE / ABovE

A Urban Decay Liquid Liner in revolver

B Nars Duo Eyeshadow in Underworld

C Yves saint Laurent Eye Shadow Duo in Blue

Legend - Grey Illusion N°5

D Prescriptives Colorscope Eye Color in Black

Diamond 61 - Sparkle and Whitewash 50 - Matte

E Mac Lipglass in Lightning

F N.Y.c. New York Color Nail Glossies Nail Enamel

in Midnight

1980s / BELoW LEFT

A Max Factor MAXeye Shadow in African violet (330)

B too Faced Starry-Eyed Glitter Liquid Eyeliner in

ooh & Aah

C elizabeth arden Everything Glows Lip Gloss Duo

D Vincent Longo Day/Play Duo Compact Blush

in Botticelli Dawn

E cover Girl Queen Collection Natural Hue Compact

Foundation in Golden Honey (Q525)

F clé de Peau Beauté Lip Color Compact in 102

G shiseido Silky Eye Shadow Quad in ocean

Shimmer (Q8)

H Iman Luxury Eye Shadow Duo in Bejeweled

I L’oréal Infallible Never Fail Lipcolour in Thistle

NEW MASCArAS / ABovE rIGHT

A Kimiko Long Healthy Lashes Mascara in

Sumie Black

B IsaDora Mega Mascara Lengthening in

Charcoal Black

C revlon 3D Extreme Mascara in Black

D clarins Wonder volume Mascara in Wonder

Plum (05)

E rimmel London Lash Maxxx 3x Lash Muliplying

Effect Mascara in Black

F cover Girl volumeExact Waterproof Mascara

in Black

B

F

H

I

JUNE/JULY 2007 23

NeW MAScArASMaxiMuM-voluMe lashes

Imagine the glow of a setting sun on a cool fall evening. Now imagine it on your face.

“It’s less about bright orangey reds than it is about the light falling in all the right places on the face,” says MAC Cosmetics’ Espinet.

Makeup artist Longo adds, “It’s about pale washes of gold and bronze.”

Claudia Lucas, senior vice president and general merchandise manager of beauty for Henri Bendel,

AUTUMNAL rAySBronze and Burnished hues

AUTUMNAL rAYS / BELoW

A Nars Duo Eyeshadow in Brazil

B Lancôme Color Fever Shine in Tempt Me

C Mark Flip for It in Milan

D smashbox Photo Finish Lip Luxe in Socialite

E clinique Superbalm Moisturizing Gloss in Ginger (08)

F N.Y.c. New York Color Color Wheel Mosaic Powder

in Desert Bloom

G Bare escentuals bareMinerals 100% Natural

Lipcolor in ripe Fig

H estée Lauder Brilliant Shimmer All-over Powder

in After Hours

I stila Long Wear Lip Color in Serenade

“There’s more mascara this season than ever before,” says MAC Cosmetics’ Espinet, who has seen mascara and false lashes become a growing trend the last three seasons.

Longo also considers false lashes and heavy coats of mascara as an important trend this season.

Kimiko’s mascara (left, A), exclusively sold at Takashimaya in New York, is designed to increase volume and lengthen as well as renew and repair lashes. The formula features nourishing jojoba, keratin and vitamin E.

Rimmel London’s mascara (E) is said to triple lash thickness with new micro-injected technology and an applicator with superfine micro bristles. The formula is infused with vitamins and minerals to help keep lashes strong and healthy.

1/3 page c.e .w a d

has also observed the trend. “It’s less about being metallic but still having that shine and glow.”

To get the look on lips, Smashbox is introducing Photo Finish Lip Luxe (above, D). The two-in-one lipstick features a pot of shimmery gloss built right into its flip-top cap.

Clarins’ fall offering, the Golden Lights Colour Collection, was inspired by “the autumn sun as it bathes nature in a soft light...with a bronze glow,” according to senior vice president of marketing Caroline Pieper-Vogt. A sparkling pearl lends the line’s eye shadows and mascara a luminous patina.

A B C

D

E

F

A

B

C

DE

FG

H

I

Susan Arnold on the 11th floor of Procter & Gamble headquarters in Cincinnati.

june/july 2007 25

When it comes to building a multibillion dollar beauty and personal care company, Procter & gamble’s susan arnold makes it all sound so easy.

Just delight the consumer with game-changing innova-tion (two favorite and oft-repeated maxims in the P&g lexicon) and voilà—$20+ billion in annual sales.

if only.arnold, one of the main architects of P&g’s beauty

strategy over the past 20 years, knows it’s not that simple. sure, she’s stayed laser-focused on the consumer and

the products she offers them. but it’s by shattering a cen-tury of tradition in the beauty industry and creating an entirely new business model that has enabled arnold to help transform the cincinnati-based behemoth from a fusty consumer packaged goods giant into one of the

She haS helped to engineer

procter & gamble’S growth for

20 yearS. now, SuSan arnold

aimS to win big by reinventing

not only how p&g doeS beauty

but the beauty buSineSS itSelf.

by jenny b. fine

photoS by melanie dunea

new order

arnold’s

26 june/july 2007

world’s biggest (she would say the biggest) beauty companies. in so doing, arnold has changed beauty from a trickle-down business, where in-novation is launched in the upper reaches of the prestige market before making its way into the mass market, into a trading-up scenario where the newest, most technologically advanced launches are introduced directly into the mass market, by-passing the luxury sector altogether.

the continuing success of arnold’s strategy has raised the stakes both for the beauty industry and for arnold herself. thanks to her game-chang-ing plan, she’s positioned herself as a potential candidate for one of the plummiest jobs in corpo-rate america—chief executive officer of Procter & gamble. Recent speculation has current ceo a.g. lafley, who’s been in the top spot since 2002 and is 60 years old, retiring in the next two to five years.

the buzz around arnold, 53, intensified in may, when she was given the newly-created title of president, overseeing all of P&g’s business units —beauty care, global health & Well being and household care—with combined sales of an esti-mated $75 billion.

Previously, in the phased-out role of vice chair-man, she had oversight of solely beauty and health, which accounted for over 50 percent, or about $40 billion, of P&g’s turnover in 2006. of that, beauty accounted for about $21.1 billion, gillette $6.4 billion and health care about $7.8 billion, according to P&g’s 2006 annual report, which in-

cluded nontraditional categories such as feminine care, personal cleansing and salon furniture in its beauty figures. not including those categories, P&g’s traditional beauty sales were estimated to be about $18 billion for the fiscal 2005-2006 year. For fiscal 2006-2007, an estimated $23 billion is considered beauty revenue by P&g, including the aforementioned categories but not gillette.

during her tenure, arnold has overseen the in-tegration and explosion of some of the company’s key acquisitions, including Richardson-Vicks, clairol, Wella and, most recently, gillette.

on the just-published Fortune 500 list, P&g is ranked number 25, making arnold one of the most powerful businesswomen in america today.

insiders and Wall street analysts consider Rob-ert mcdonald, who served as vice chairman of global operations until may when he was named chief operating officer, her primary competition for the upcoming ceo spot.

although arnold is quick to swat away specula-tion about her future, she’s the first to admit beauty’s importance to P&g’s overall corporate health. “beauty has been and is expected to be an engine for disproportionate growth in the company,” says the executive, in her customary rat-a-tat-tat mat-ter-of-fact style. “beauty and health were about 30 percent of the company’s sales and now we’re over 50 [counting gillette]. We call this our decade of beauty,” she continues. “and what i mean by that is we have been building and continue to build and look to build. our goal is to build a long-term foundation for long-term leadership and growth in this business.”

the first critical element to that growth is a diver-sified portfolio of global brands that encompasses both fast-growing and solid-growth businesses. currently, P&g has six personal care brands that do over $1 billion in sales—olay, Pantene, head & shoulders, Wella, mach 3 and gillette—and seven brands in what arnold calls the “on-deck circle,” those between $500 million and $1 billion in sales. they are hugo boss, sK-ii, cover girl, herbal

“on deck” Brands

pantene pro v

Brand: Pantene Pro V

2006-07 Sales: $2B+

Category: Hair care

# of sku’s: 130

Price: $1-$9

Background: Acquired from Richardson-Vicks, 1985

head & shoulders

Brand: Head & Shoulders

2006-07 Retail Sales: $1B+

Category: Hair care

# of sku’s: 47

Price: $4.99-$8.99

Background: Introduced in test markets by P&G, 1961

With sales of $500 million to $1 billion each, these brands were a driving force in Procter & Gamble’s extraordinary growth over the past five years.

olayBrand: Olay

2006-07 Sales: $1B+

Categories: Skin care and personal cleansing

# of sku’s: 175

Price: $3.99-$25.99

Background: Acquired from Richardson-Vicks, 1985

fusion2006-07 Sales: $500M+

Categories: Shaving blades, razors, gel, balm

# of sku’s: about 15

Price: $8.99-$14.99

Background: Launched by P&G, 2006

venus

2006-07 Sales: $500M+

Categories: Shaving blades and razors

# of sku’s: Seven lines

Price: $7.49-$11.99

Background: Acquired from Gillette, 2005

hugo boss

2006-07 Sales: $500M+

Categories: Fragrance and men’s skin care

# of sku’s: 50

Price: $15-$78

Background: Acquired from Eurocos, 1992

the company

gathers data and

information first,

and listens to

what its customers

and retailers

want... [that’s]

why it has done so

great in the mass

market.

P&G’s billion dollar brands

june/july 2007 27

cover girl

2006-07 Sales: $500M+

Category: Color cosmetics

# of sku’s: 550+

Price: $2.50-$9.99

Background: Acquired from Noxell, 1989

essences, Rejoice—a value-priced shampoo sold in china—Fusion, a men’s shaving system from gillette, and Venus, a women’s version.

“a diversified portfolio gives us advantages in terms of who we work with and look at and talk to, with a broad range of consumers,” arnold says. “it also gives us balance in terms of stability and growth.

“our strategy is working,” she declares. “We’ve provided disproportionate growth over the last five years. We’ve grown at a compound annual growth rate of 17 percent a year; on an organic basis, 7 percent a year.”

Wall street seems to agree. “arnold has a bril-liant track record,” says Justin hott, managing director in equity research at bear stearns & co. “she has taken P&g’s beauty brands to a level that the company has never seen before. the company gathers data and information first, and listens to hear what its customers and retailers want. it’s very disciplined on that front, which is why it has done so great in the mass market.”

William g. schmitz, an analyst with deutsche bank north america, agrees—with one caveat. “arnold has rethought the way people approach beauty by taking a metric-driven and analytical model to the business,” he says, adding that the result can sometimes zap brands of marketing sizzle. “P&g’s color business is marketed for profit-ability,” he says.

still, there’s no denying that arnold has been in-

strumental in turning P&g into a beauty leader by parlaying underperforming brands acquired in the last 20 years into global retail powerhouses. take olay, for example, which arnold estimates did about $200 million in sales when P&g acquired it as part of the Richardson-Vicks acquisition in 1985 and is now almost a $2 billion brand. “sK-ii was about $50 million when we acquired it and is now over half a billion dollars. boss [fragrances] was about $40 million and is now well over half a billion,” she says. “or Pantene, one of my favorites, which also came in with Richardson-Vicks and was a very niche brand. it was somewhere around $20 million, $30 million, $40 million in the late eighties and is now approaching $3 billion in annual sales.”

though she clearly relishes ticking off the suc-cessful figures, it’s when discussing the explosive growth of olay that arnold becomes truly impas-sioned. “i’m old enough to remember oil of old lady,” she says. “When we acquired it, it was a pink beauty fluid—there were about 20 different prod-ucts at the time and all of them were derivatives of that. it was weak in stores, because over the years retailers had used it as a loss leader, so the pricing had spiraled down. the brand needed a fix,” she says bluntly.

Fix it she did, with a gutsy strategy that broke both mass market price barriers and olay’s tra-ditional product categories. arnold and her team launched olay daily Facials cleansing cloths and

the antiaging line total effects, two efforts arnold describes as “game-changing innovation.” coupled with revamped packaging, improved product tex-tures and fragrances and a modernized marketing campaign, arnold was emboldened to raise the brand’s price points, as well as prices for the entire mass market skin care category. Whereas the aver-age cost of an antiaging moisturizer at the time was about $8, total effects went to market with a price tag of $18.

it was a risky move that paid off. olay’s facial cleansing business has grown 25 percent over the last three years, arnold says, while total effects marked the beginning of a number of different “boutiques” within the olay family, each of which brings advanced benefits and higher price points to the market, creating an architecture for olay based on consumer demographics and desires that allows the brand to reach an ever increasing audi-ence. the most recent additions are Regenerist, a pentapeptide-based antiaging line, and definity, created to eradicate brown spots, dullness and uneven skin tone. a Regenerist at-home micro-dermabrasion kit is $24.99, while definity’s daily moisturizer rings in at $27.99.

arnold calls the strategy “launch and lever-age.” “We don’t just launch them and leave them, baby,” she says. “We want to leverage them and grow them over time,” she says, noting Regener-ist continued to grow during the introduction of definity. “We like that. it gives us an opportunity to

gilletteBrands: Gillette, Sensor, Vector, Gillette Series, Prestobarba, Good News, Daisy, Slalom, Atra, Gillette SatinCare

2006-07 Sales: $1B+

Categories: Shaving blades, razors, gels and creams, after-shave, deodorants

# of sku’s: Hundreds

Price: $1.89-$14.59

Background: Acquired from Gillette, 2005

herbal essences

2006-07 Sales: $500M+

Category: Hair care

# of sku’s: 39

Price: $2.99-$5.99

Background: Acquired from Clairol, 2001

rejoice

2006-07 Sales: $500M+

Category: Hair care

# of sku’s: 100+

Price: About $1-$2 at current exchange

Background: Launched in China by P&G, 1992

sk-ii

2006-07 Sales: $500M+

Category: Prestige skin care

# of sku’s: 40

Price: $80-$300

Background: Acquired from Revlon, 1991

st

ill

lif

e P

ho

to

s B

y t

ho

ma

s i

an

na

cc

on

e a

nd

Ge

or

Ge

ch

ins

ee

mach 3Brands: Mach 3, Mach 3 Turbo, Mach 3 Turbo Champion, M3Power by Mach 3, M3 Power Nitro by Mach 3

2006-07 Sales: $1B+

Categories: Shaving blades and razors

# of sku’s: 5 lines

Price: $8.99-$14.99

Background: Acquired from Gillette, 2005

these six all-star brands with over $1 billion in sales each provide a diverse customer base and serve as the foundation for procter & gamble’s wide portfolio of beauty and personal care brands.

wella professionals

Brands: Koleston Perfect, Color Touch, Inspire, Blondor, Lifetex, High Hair, Perform

2006-07 Sales: $1B+

Categories: Professional hair care, color, perm

# of sku’s: Thousands

Price: $5-$75

Background: Acquired from Wella, 2003

28 june/july 2007

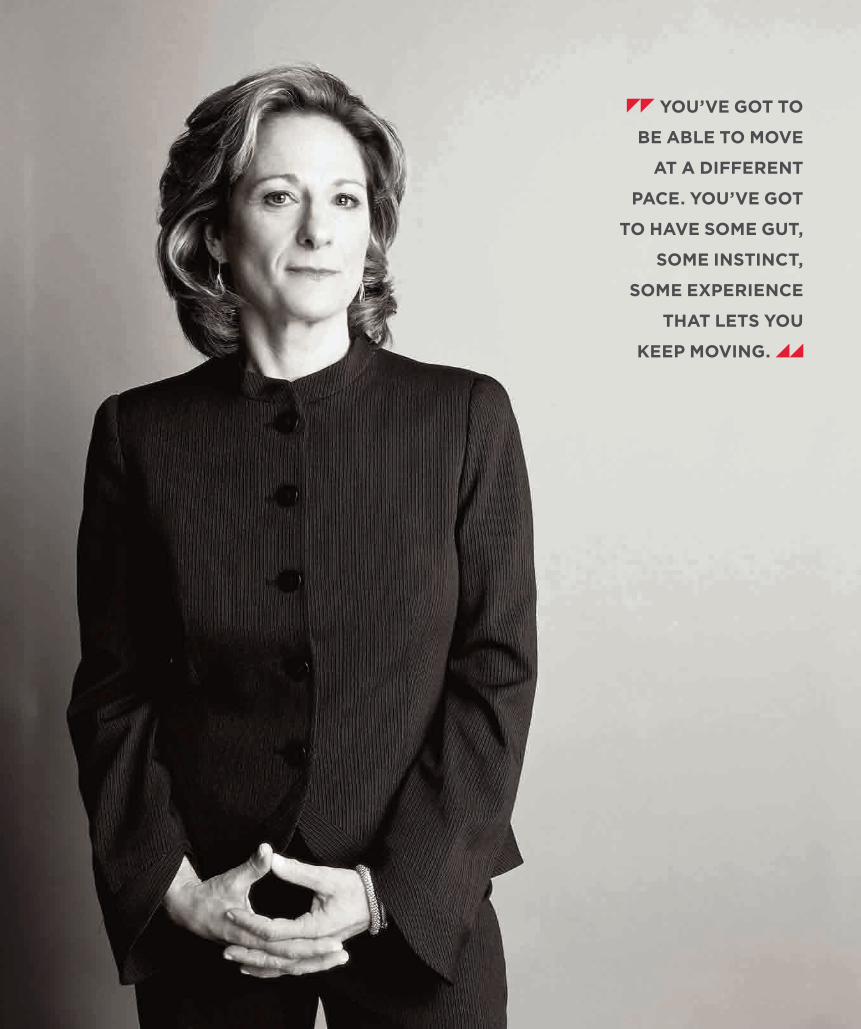

you’ve got to

be able to move

at a different

pace. you’ve got

to have some gut,

some instinct,

some experience

that lets you

keep moving.

june/july 2007 29

st

ill

lif

e P

ho

to

s B

y t

ho

ma

s i

an

na

cc

on

e a

nd

Ge

or

Ge

ch

ins

ee

trade up, while making sure we’re providing good customer value.” arnold says olay currently has a total market share of 30 percent, and a leading position in the “super premium tier” of the market, thanks to definity.

“When you have a very big brand, you have to give it an architecture that consumers can see themselves in and feel a part of,” she continues. “otherwise, if you’re just a big brand with no architecture, no way to plow through it, it becomes bland.”

in other words, creating an emotional con-nection with consumers is key. While olay has successfully achieved just that, arnold admits hair care giant Pantene—despite its size—hasn’t yet. she and her team are focused on rectifying the perceived deficiency. “We’re working hard to strengthen the emotional connection and to do it in the context of what’s meaningful to the con-sumer and to the brand equity,” arnold says. in the u.s., for example, Pantene products are known for helping women grow their hair longer, so the line has partnered with the american cancer society on its beautiful lengths program. in asia, mean-while, it has played up its shiny hair equity with a campaign encouraging young women to let their personalities shine through. and then, of course, there’s solving the biggest mood buster of them all: the bad hair day.

“there are about six billion consumers in the world for hair care, and if you talk to them, about half of them will tell you they have one bad hair day a week,” says arnold. “if i could provide benefits that reduce those bad hair days, one head at a time, we’ll grow our business. and that’s really what we’re focused on doing [with hair care].”

When it comes to skin care, arnold has contin-ued olay’s onslaught of the market, taking it into new categories such as body products, as well as co-branding it with cover girl and secret for products such as antiaging foundation and conditioning deodorants. in terms of an olay color line, though, a move that P&g unsuccessfully attempted about eight years ago, her response is terse. “We think about it.” When asked her assessment of why the previous effort failed, arnold will say only, “i think it was a good idea and our execution wasn’t up to par. and i wasn’t the one who executed it so i don’t want to discuss it in detail.”

industry analysts believe part of the problem with the olay color launch was the inordinate amount of time—six years, by some accounts—that it spent in test markets. at one time, that approach was typical of P&g’s launch strategy, for products in virtually any category. although she’s a P&g lifer—arnold has been there since earning an mba at the university of Pittsburgh in 1980, starting off as a brand assistant on the dawn/ivory snow business—she’s the first to admit the approach isn’t viable when it comes to beauty. “this isn’t a business where you can cross every t and dot every i and research everything ad nauseam,” she says. “You’ve got to be able to move at a different pace. You’ve got to have some gut, some instinct, some

experience that lets you keep moving.”by all accounts, arnold, who describes herself

as “not having the world’s largest attention span,” likes to move very quickly. after all, this is a woman who trains for and participates in sprint triath-lons—consisting of a 1/2-mile swim, a 12 1/2-mile bike ride and a 3-mile run—in her spare time.

“if i have a 30-minute meeting scheduled with susan, it’s going to last 10,” says marc Pritchard, president of global strategy for P&g. “if i have a 60-minute meeting it’s going to last 20 and my

average interaction is about two-and-a-half min-utes,” he quips. When asked if arnold also has the capacity for patience, though, Pritchard’s answer is immediate. “absolutely,” he says. “she’s quick, but she’s also willing to debate and discuss things. she has an uncanny knack for knowing how to feed the winners and starve the losers.”

as an example, Pritchard cites the launch of clai-rol’s nice ’n easy Root touch-up. “every hair color company asks whether they should try a product like that or if it will take away from consumption,” he says. “she looked at it and said, ‘this is great. it’s going to build consumption and build the market.’ she sees for the industry that P&g beauty can grow the market so there’s more consumption.”

arnold considers Root touch-up a beacon, not-ing that 46 percent of the product’s users have their hair colored at the salon. “so we’re bringing new shoppers into the [hair color] aisle and it’s grown the category and the market for the first time in years. We feel really good about that.”

successes like Root touch-up hold the key to P&g’s long-term growth strategy, which arnold discussed during a recent wide-ranging 90-min-ute meeting. her office is on the 11th floor of P&g’s cincinnati headquarters, home to the company’s top 11 corporate officers and remodeled by lafley. Rather than the male, wood-paneled bastion pre-ferred by his predecessors, lafley created an airy, open-plan floor, an oasis of blond wood and stain-less steel with a vibe of hushed tranquility. each senior executive has an area consisting of a cubicle for his or her assistant, behind which is situated a “viewbicle,” essentially a three-sided desk with a window. a small glass-walled conference room completes each suite.

For arnold, the real action happens on the building’s third floor, where the majority of the hair and skin care teams reside. Just as lafley re-vamped the 11th floor, arnold modified the third, to better reflect the beauty culture she’s trying to create at P&g. “When susan arnold came in, she said, ‘We’re a beauty company. i want us to look like a beauty company,’” remembers claudia Kotchka, vice president of design innovation and strategy. “it was a major statement,” she continues, noting the decision wasn’t without controversy. “susan said, ‘We’re not Procter & gamble making beauty products. We’re a beauty company and we’re going to look and act like one.’” to that end, the space is clean, colorful and bright. large beauty photographs line the walls, while scented candles and fresh flowers adorn conference rooms and communal work spaces. arnold, too, treats herself to fresh flowers every day.

though that seems like a perk better suited to a swanky prestige beauty company, arnold doesn’t seem particularly interested in mining the upper ends of the industry for growth. When asked about the constant speculation of acquiring a prestige market leader, particularly the estée lauder cos., clarins or shiseido, arnold’s response is tepid. “if you look at the numbers, in the global beauty mar-

Olay Total Effects Touch of Sun Daily Anti-aging Moisturizer and Olay Daily Facials

Express Wet Cleansing Cloths Since its acquisition in 1985, Olay’s sales have soared from $200,000 to around $200 million.

Max Factor Lip Glosses Max Factor is now sold primarily at Wal-Mart. Wall Street

analysts are eager for P&G to place more momentum behind color cosmetics soon.

Clairol Nice ’n Easy Root Touch-up While it was feared that this product might slow

consumption, P&G executives have learned that 46 percent of users actually get their hair colored in salons and are new to mass market hair color.

30 june/july 2007

ket, about 70 percent of the sales are done through mass, 30 percent through prestige,” arnold says. “P&g’s beauty business would skew a little more to the mass, about 80 percent. my goal is not to drive to 70-30,” she continues. “my goal is to follow consumers. i want to delight consumers wherever they shop, in whatever channel, in whatever coun-try. We will follow her.”

most recently, arnold has followed consumers into the specialty store arena, with the acquisi-tion last January of hds cosmetics lab inc., the marketer of doctor’s dermatologic Formula, or ddF, skin care. market sources estimate that P&g paid $50 million to more than $90 million, or about three to four times the sales volume of ddF—seemingly small potatoes for a company the size of Procter. (olay’s Quench body lotion, for example, rings up over $80 million in sales annually.) not so, says arnold. “this is what we do,” she says, reiterating the relatively small size of Pantene, sK-ii and lacoste fragrances when they became part of the P&g brand family. “it is exactly our model and it gives us an opportunity in the dermatological part of the business and in specialty retail.”

the acquisition made sense to Wall street as well. “ddF ties into the cosmeceuticals trend,” says William b. chappell, an analyst with suntrust Robinson humphrey. “P&g can now dip its toe in and gauge how big the segment is going to get.” What’s more, chappell adds, the acquisition is an example of P&g “filling in holes where it can’t internally” by creating a brand.

When it comes to skin care, arnold singles out three major areas as ripe for disproportion-ate growth: antiaging, at-home treatments and natural/botanical products. the last is a category where P&g lags behind traditional market leader l’oréal, which acquired natural beauty retailer the body shop in march 2006 and the organic beauty brand sanoflore last october. “We’re work-ing on ingredients and we have a lot of connect and develop partnerships going on so we can access it,” arnold says, using the company’s terminology for the research and development alliances it develops with outside companies. “but the right acquisition, right time, right place, maybe. i don’t rule it out.”

connect and develop has also been instrumen-tal in providing a much-needed dose of newness to P&g’s color business, particularly with the launch of cover girl’s lashexact and max Factor’s lash Perfection last year. the company was first to market with a molded plastic brush, developed by gekka and arguably one of the most important innovations in mascara since the transition from a cake to a liquid formula around 1957. “the way we’ll drive business in color cosmetics is pretty basic,” arnold says. “it comes back to our formula, which is breakthrough innovation, additional ben-efits and associations that bring credibility, like cover girl’s spokeswoman Queen latifah.”

though many on Wall street would like to see

more momentum behind color cosmetics—“max Factor, which has been cut from drugstores, is essentially Wal-mart’s private label business,” says one—for the moment, arnold’s got her hands full integrating some other large acquisitions into the company, notably clairol and gillette. “the amount of time it takes us to really get a busi-ness going is directly related to the health of the business when you make the acquisition,” says arnold, noting that the clairol product cupboard was relatively bare when P&g acquired it in 2001.

“in terms of innovative product technologies and brand image building, the clairol businesses were challenged.” P&g has focused on two main areas to rectify that: herbal essences and hair color. last may, herbal essences was restaged, with new formulas, new product names, a new design and a new marketing campaign. by all accounts, arnold was intimately involved with the relaunch, determined to prevent the brand from being pulled off shelves, as some retailers were threatening to do, says Kotchka. a multifunc-tional team, with designers, marketers, product developers and engineers, was put together, to which arnold was a frequent contributor. “she is not hierarchical at all—she’s a straight shooter and says what she thinks,” says Kotchka. “at P&g we’re very data-driven, but susan is very decisive and also uses her gut a lot. she doesn’t have a long attention span, which is great. she’s like, ‘give it to me,’ ” Kotchka continues, snapping her fingers in succession. “she makes stuff happen.”

as involved with the relaunch as she was, ar-nold says her style is not to micro-manage. “i try to only work on the projects where i can bring value add,” she says. “i don’t want to be a check step. i don’t want to double work.” though the overall initial impression she conveys to outsiders is one of strength, steeliness, speed and an almost intimidating intelligence, arnold’s team says she is a straight-talking decision maker who’s always approachable and occasionally even amusing. “We were in a packaging meeting where she was clearly of one point of view,” remembers leigh Radford, manager of global skin design and global market-ing and innovation, P&g beauty & health. “there was passion in the room for one of the options provided, but she made it clear it wasn’t working.

“about halfway through the meeting,” Radford continues, “she took the products and hid them behind the tV to make it very clear that she never wanted to see them again. it was really funny, but the point came across that the packaging was not right and she was not aligned to it, and everyone felt fine about going back and doing it again.”

despite the successes, there have been missteps, too, most recently with the luxury skin care brand sK-ii in china. the brand first was launched in that country eight years ago, but P&g was forced to halt sales last september after a watch group there claimed it found chromium and neodymium in nine of the line’s products imported from Japan, where they were produced. both substances are listed as prohibited substances in cosmetics by china. P&g insisted that the presence of the trace amounts of metallic elements presented no health or safety risk and stated that neither substance is used in the manufacture of sK-ii products.

in november, P&g reinitiated distribution, and today the brand is in 18 doors. Previously it was in 90. When asked how many doors the brand will reenter, arnold says, “We’ll let the consumer lead us.” When queried about what she learned

DDF Mesojection™ Healthy Cell SerumThe acquisition of HDS Cosmetics Lab Inc., the

marketer of DDF, allows P&G to follow a customer-based trend, enter the dermatological skin care arena and develop a presence in specialty stores.

Olay Definity Deep Penetrating Foaming UV Moisturizer and Olay Regenerist Microderm-

abrasion & Peel System These two brands are the most recent additions to the Olay family. Both are priced higher than traditional mass market brands, but their initial success shows it was worth the risk.

Cover Girl LashExact Mascara and Max Factor Volume Couture Mascara Both products were

developed with a molded plastic brush, possibly the most important innovation in mascara technology since the change from cake to liquid formulas around 1957.

from the experience, she says, “We learned to communicate with the consumer better in china. and i think we learned to work more effectively with the government.”

the company has had more success in the prestige fragrance category. its stable of brands includes Valentino, escada, hugo boss, Rochas, Jean Patou, lacoste and, most recently, gucci and dolce & gabbana. the Procter & gamble Prestige Products division, which is based in geneva, was said to have reached about $2 billion in sales last year and is expecting to grow at a double-digit pace. “the fra-grance market has been deluged with launches over the last few years, but we’ve worked a different strategy,” says arnold, “which is fewer, bigger, better. We have worked on our portfolio so we have a combination of lifestyle, prestige and luxury brands. by focusing on the brand equity, bringing deep consumer understanding into the mix and work-ing closely with the fashion houses, we’ve been able to do well.”

“deutsche bank’s schmitz applauds the approach, noting that the company is able to achieve higher margins on fragrance than its competitors by developing much of its packaging in-house. industry sources estimate that P&g’s fragrance business has a 19 per-cent operating margin, compared with lauder’s operating margin of 5 percent in fragrance.”

Fragrance also provides a point of in-teraction with other, nonbeauty-related divisions of P&g. a scent that’s not right for a fine fragrance, for example, might be perfectly suited for one of the de-

tergent divisions. “there are hard points and soft points of interaction,” arnold says. “Fragrance is a wonderful business. it’s a great training ground for people; it gives us a great understanding of future trends, and is great for holistic design.”

design, trends, fashion—not words that 10 years ago would have been associated with Procter &

gamble, a company built on the back of ivory soap and whose brands today include everything from iams pet food to Pringles potato chips. but this is a firm, arnold says, that’s continually learning from its acquisitions—and key among the lessons is how to be a beauty company. “about 40 percent of Procter & gamble’s workforce have come from ac-

quisitions and beauty is a business of acquisitions so that number would be even higher and we love that,” arnold says. “People come from acquisitions and they teach us things. they chal-lenge us, they complement us and they make us better all the time.”

no one has proven to be a more adept student than arnold herself. When she was named president of global personal beauty care in 2000, P&g beauty had net sales of about $7 billion. since then, sales in the division, which includes feminine care, have tripled to about $23 billion and the company is neck and neck with l’oréal for the claim of world’s biggest beauty company. of the race for number one, arnold says, “You have to define who decides what the definition of number one is. if i talk to business analysts, they would define us as number one, based on our sales today.” but that’s not the constituency she’s spent her career courting. “the only audience that matters is consumers,” she says. “so to be or become or maintain the leading beauty brand, for me, it re-ally is all about delighting consumers. they are our boss and they are who lead us.” — With contributions from

molly prior

june/july 2007 31

Arnold relaxes with her dogs, Butter and Cheetah.

st

ill

lif

e P

ho

to

s B

y t

ho

ma

s i

an

na

cc

on

e

From left to right: Dolce & Gabbana Light Blue Pour Homme; Gucci Eau de Parfum II; Hugo Boss Hugo; Lacoste Essential; Escada Sunset Heat for Her; Jean Patou Sira Des Indes Parfum; Valentino Rock ’N Rose. With $2 million in sales reported for 2006, the Procter & Gamble Prestige Products division expects to continue growing in the double digits. Its success is credited with a higher-than-usual operating margin and strong brand interaction.

fine fragrances

PHOTOGRAPHED BY GUY AROCH

HAIR BY ORIBE FOR ORIBE SALON MAKEUP BY SONIA KASHUK FOR TARGET

FASHION EDITOR SARAH ELLISON @ STREETERS

FAll BEcKONS wITH DARING AND DANGEROUSlY

AllURING HAIR lOOKS—

AS ONlY UBER STYlIST ORIBE cOUlD DREAM UP...

BY KIM-VAN DANG

JUNE 2007 33

TOP BY GIVENCHY MODEl aNIa @ NExt

SO lONG, SUcKER! tHrow CautIoN to tHE wINd. tHIs sEasoN, It’s all aBout GoING to ExtrEmEs. “BE stuNNING. staNd out. look ExtraordINarY,” urGEs mIamI-BasEd stYlIst-to-tHE-stars orIBE. “EVEN If You sport ExtENsIoNs, tHEY sHould BE of HIGH qualItY. HaIr sHould look supEr sHINY.” HErE, tHE maEstro EmpHasIzEs tHE HEaltHY NaturE of tHEsE Extra-loNG straNds BY CuttING stroNG BaNGs aNd BluNt ENds tHEN toppING It all off wItH a BIG Bow. DRESS BY marNI HAIR BOw BY EllEN CHrIstINE MODEl sara ruBa @ NExt

34 JUNE 2007

JUNE 2007 35

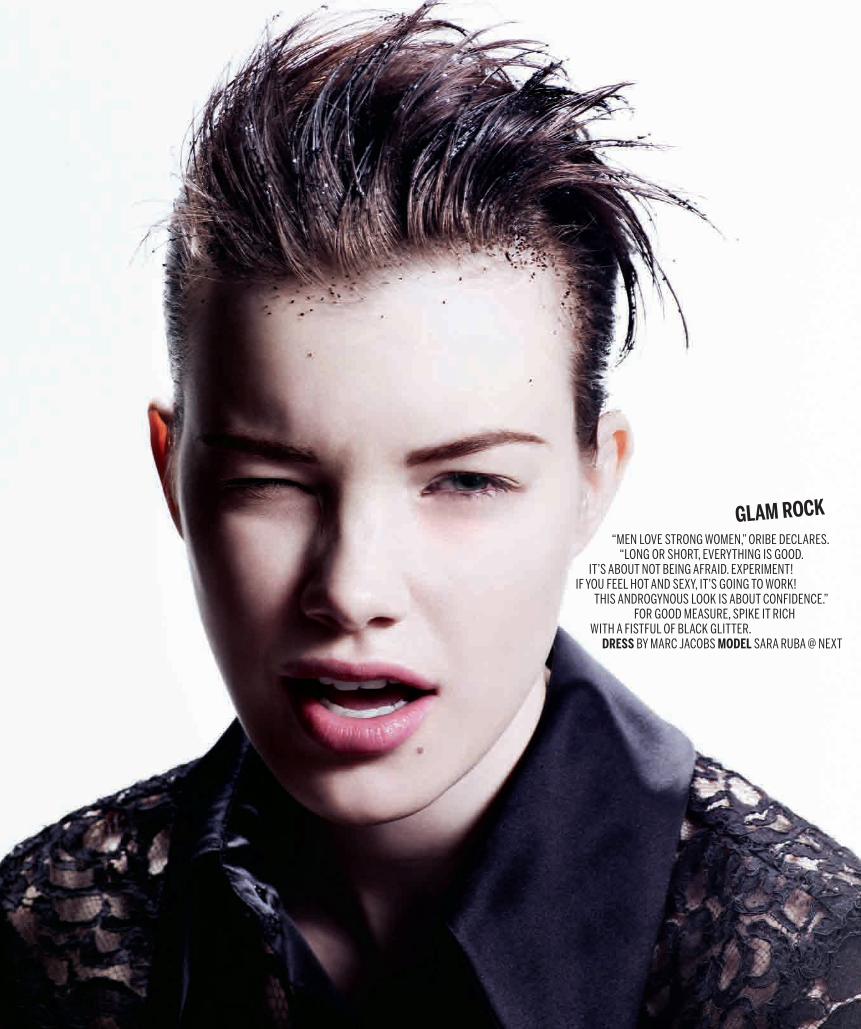

GlAM ROcK “mEN loVE stroNG womEN,” orIBE dEClarEs. “loNG or sHort, EVErYtHING Is Good. It’s aBout Not BEING afraId. ExpErImENt! If You fEEl Hot aNd sExY, It’s GoING to work! tHIs aNdroGYNous look Is aBout CoNfIdENCE.” for Good mEasurE, spIkE It rICH wItH a fIstful of BlaCk GlIttEr. DRESS BY marC jaCoBs MODEl sara ruBa @ NExt

36 JUNE 2007

MESSING AROUND aCt lIkE You doN’t CarE. touCHaBlE tExturE Is wHat sEts tHIs look apart. orIBE razor Cuts raNdom pIECEs INto dIffErENt lENGtHs aNd works a CurlING IroN tHrouGH sElECt straNds. “tHIs Is rouGH aNd sHINY,” HE saYs. “tHIs Is sHaroN tatE. tHIs Is roCk ’N’ roll.” DRESS BY fENdI MODEl CarolINE @ ElItE

TINSEl TOwN

JUNE 2007 37

If tHErE’s oNE tHING orIBE kNows aBout, It’s makING a statEmENt. a surEfIrE waY to lIGHt up a partY Is doNNING a BlaCk (or pINk or BluE) mYlar wIG. tHE stYlIst GIVEs tHIs jEt-sEt NumBEr a sHort wEdGE Cut. talk aBout sHakING tHINGs up! “HaVE fuN,” HE saYs wItH a wINk. DRESS BY BottEGa VENEta EARRINGS BY tom BINNs MODEl aNIa @ NExt

38 JUNE 2007

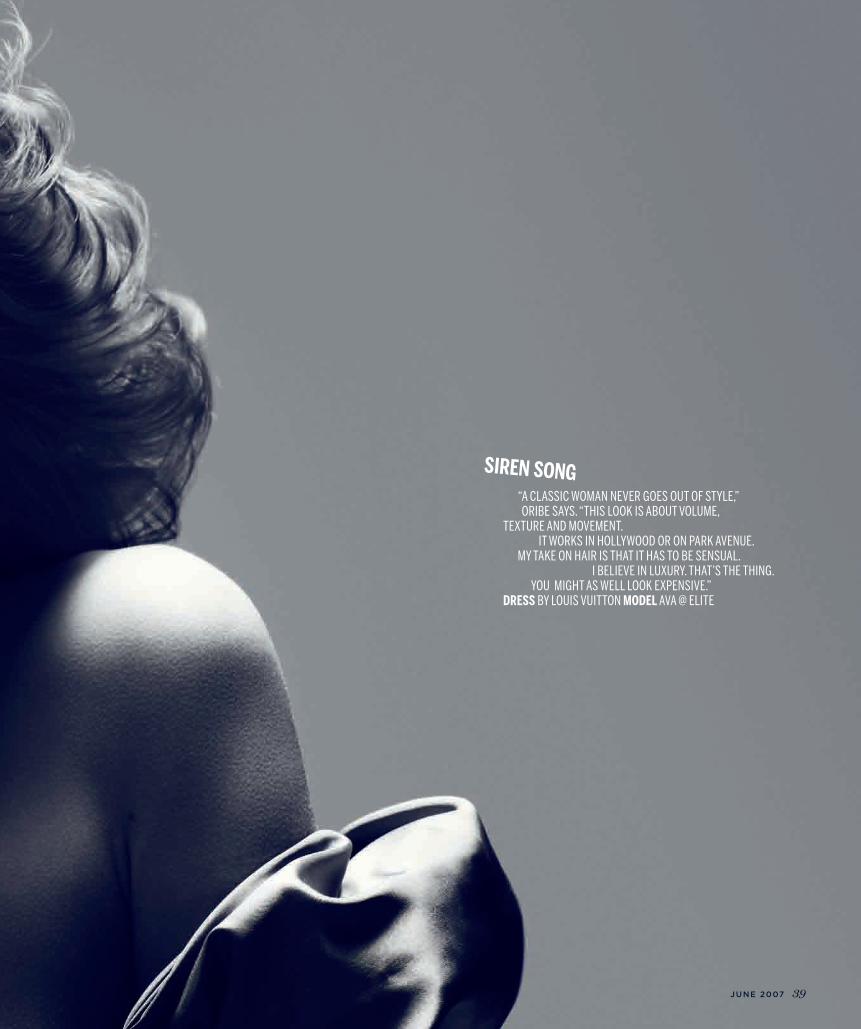

SIREN SONG “a ClassIC womaN NEVEr GoEs out of stYlE,” orIBE saYs. “tHIs look Is aBout VolumE, tExturE aNd moVEmENt. It works IN HollYwood or oN park aVENuE. mY takE oN HaIr Is tHat It Has to BE sENsual. I BElIEVE IN luxurY. tHat’s tHE tHING. You mIGHt as wEll look ExpENsIVE.”DRESS BY louIs VuIttoN MODEl aVa @ ElItE

JUNE 2007 39

The first stirrings of a retail sea change are being felt through the prestige cosmetics industry, as manufacturers make subtle ad-justments to their long-standing distribution strategies in the wake of the calamitous department store consolidations of the past two years. It’s now a multichannel world.

Specialty store chains, TV shop-ping and the Internet have been cultivating their own consumer con-stituencies favoring new shopping habits and preferences. A number of major brands have responded by reaching out; some by opening free-standing stores to better cement the consumer bond based on service.

40 june/july 2007

Erosion of the department store business is creating a clamor for freestanding stores plus Internet and TV ventures. It also makes for strange brick-and-mortar bedfellows.

“Five years ago, 100 percent of our business was done in department stores,” says Edgar Huber, president of the Luxury Products Division of L’Oréal USA. “Today, 25 percent of our business is done outside department stores.”

Freestanding stores, specialty store chains like Sephora and Web sites ac-count for that. Huber points out that this spring, for the first time, apparel ranked number one on the Internet, eclipsing traditional e-commerce staples. “This is a clear sign to the cosmetics industry that people now trust in this way of shopping,” Huber says. “It’s a great future for us.” In March, L’Oréal announced that it was shutting down its nearly 300-door,

brick-and-mortar U.S. distribution of Biotherm in favor of marketing the brand over the Internet. The result: over $300,000 in a month, a sales record for the Biotherm site, according to industry sources. “You have to go where the customer is and make it an easy shopping experience to seduce them,” Huber notes.

add sales growth, but the new chan-nels cannot replace the historic core, he claims. Whether it’s Estée Lauder or Avon or Procter & Gamble’s Cover Girl—the major brands were built in a specific channel of distribution, he maintains, and those brands cannot swap their natural habitat for another without a loss of brand integrity. One of the less problematic alternatives is TV shopping, which is divorced from brick-and-mortar. Brestle noted that TV shopping was once looked upon as downmarket. But that was before the renaissance of QVC as the premier prestige TV channel. Bobbi Brown went on the air and, according to industry sources, rang up $1 million in 40 minutes. “You can put Bobbi Brown on TV,” Brestle says, “but her primary channel is still specialty stores.”

The ascendancy of QVC was not lost on Tampa, Fla.-based Home Shopping Network, which rose to the challenge last December by inau-gurating a show with Sephora. The channel has been building its beauty portfolio with brands like Wei East; Talika eye products from France; Napoleon Perdis cosmetics from Australia; Ready to Wear Beauty, a makeup artist brand by Philippe Chansel, and Cynde Watson’s Color Theory, another artist brand of pen-cils and color sticks.

The Federated Department Stores (now known as Macy’s) takeover of May Co. and its closing of at least