Embed Size (px)

Citation preview

NOTE:

1. THIS IS A DRAFT BUSINESS RESCUE PLAN, BASED ON A RESTRUCTURED SAA PROPOSAL,

WHICH IS STILL IN THE PROCESS OF BEING SUPPLEMENTED WITH FURTHER INFORMATION

(INDICATED IN THE BODY OF THIS DOCUMENT WITH DRAFTING NOTES) AND WHICH IS

ALSO SUBJECT TO CONSULTATION.

2. IN PARTICULAR, THE BRPs:

2.1. ARE IN THE PROCESS OF OBTAINING VALUATIONS OF THE COMPANY’S ASSETS,

WHICH WILL BE INSERTED AND ATTACHED TO THIS DOCUMENT.

2.2. WILL PROVIDE FURTHER INFORMATION IN THIS DOCUMENT DETAILING THE

RESTARTING OF THE AIRLINE PURSUANT TO THE OUTBREAK OF COVID-19.

2.3. WILL PROVIDE THE COMPLETE LIST OF ANNEXURES TO THIS DOCUMENT AT A

LATER STAGE.

3. THIS DRAFT BUSINESS RESCUE PLAN IS FOR DISCUSSION PURPOSES AND MAY NOT BE

CIRCULATED TO ANY OTHER PARTY.

2

(Registration No. 1997/022444/30)

(in business rescue)

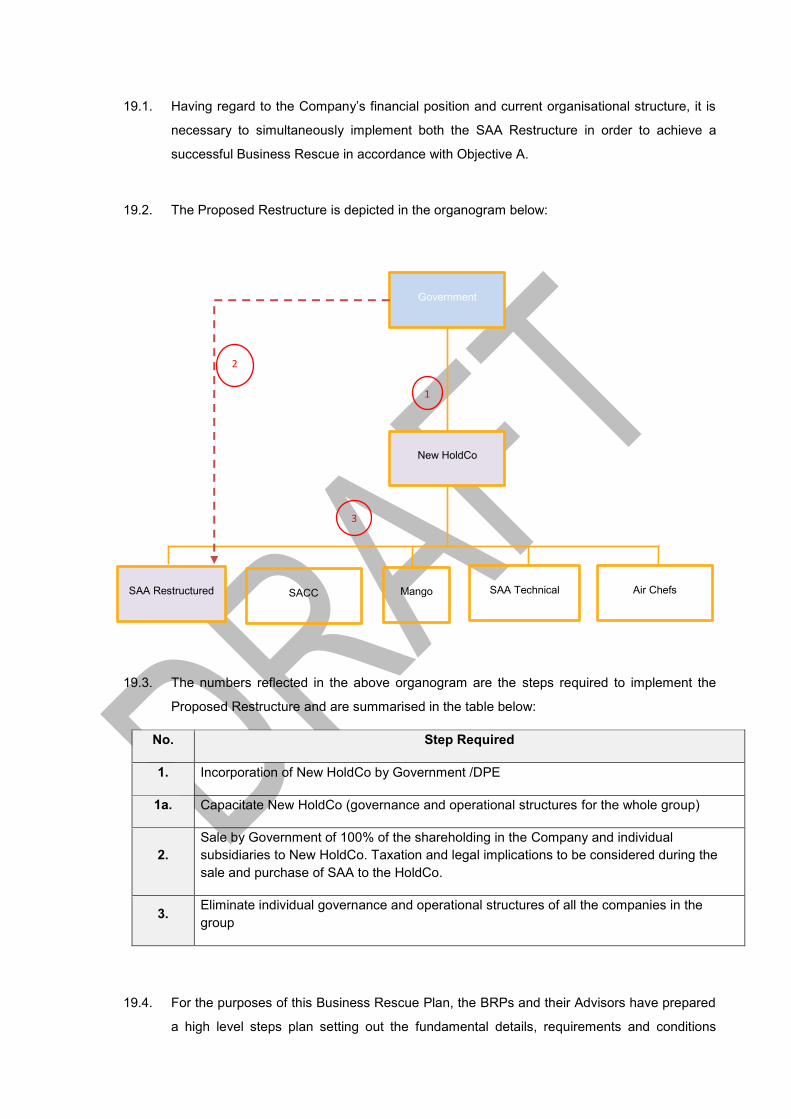

BUSINESS RESCUE PLAN Prepared in terms of section 150 of the Companies Act No. 71 of 2008 (as amended)

Prepared by:

SIVIWE DONGWANA

(joint business rescue practitioner)

and

LESLIE MATUSON

(joint business rescue practitioner)

PUBLICATION DATE: []

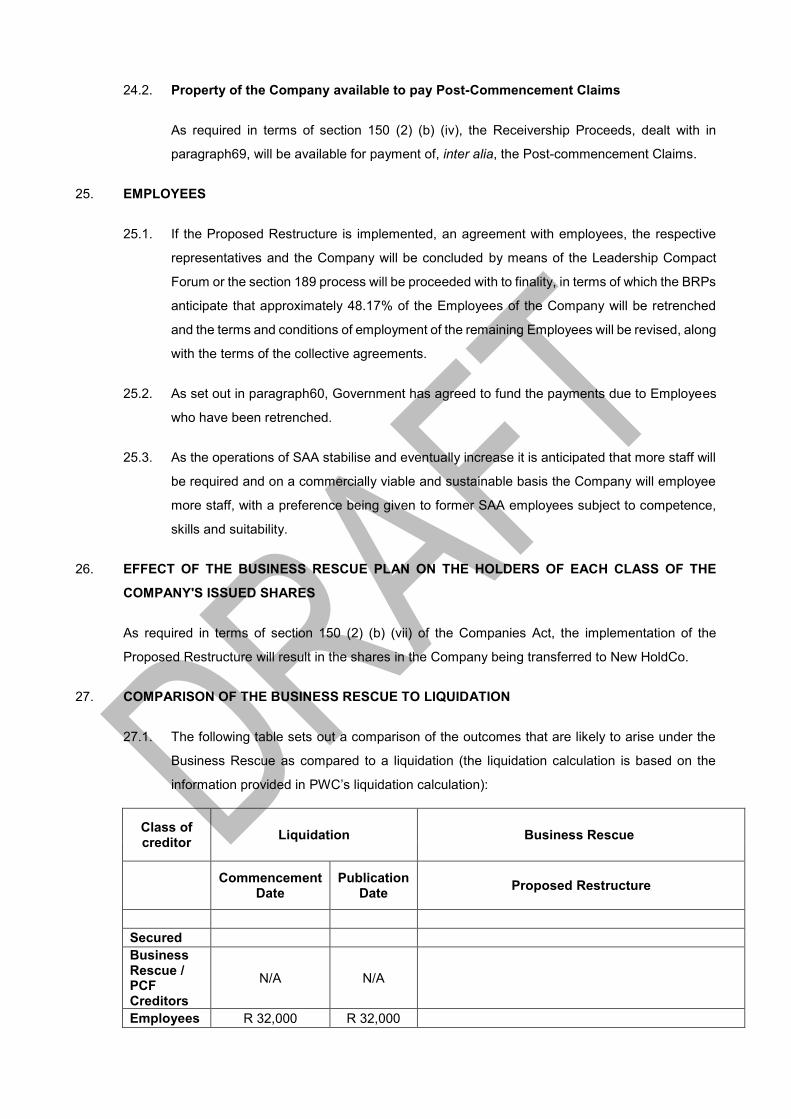

TABLE OF CONTENTS

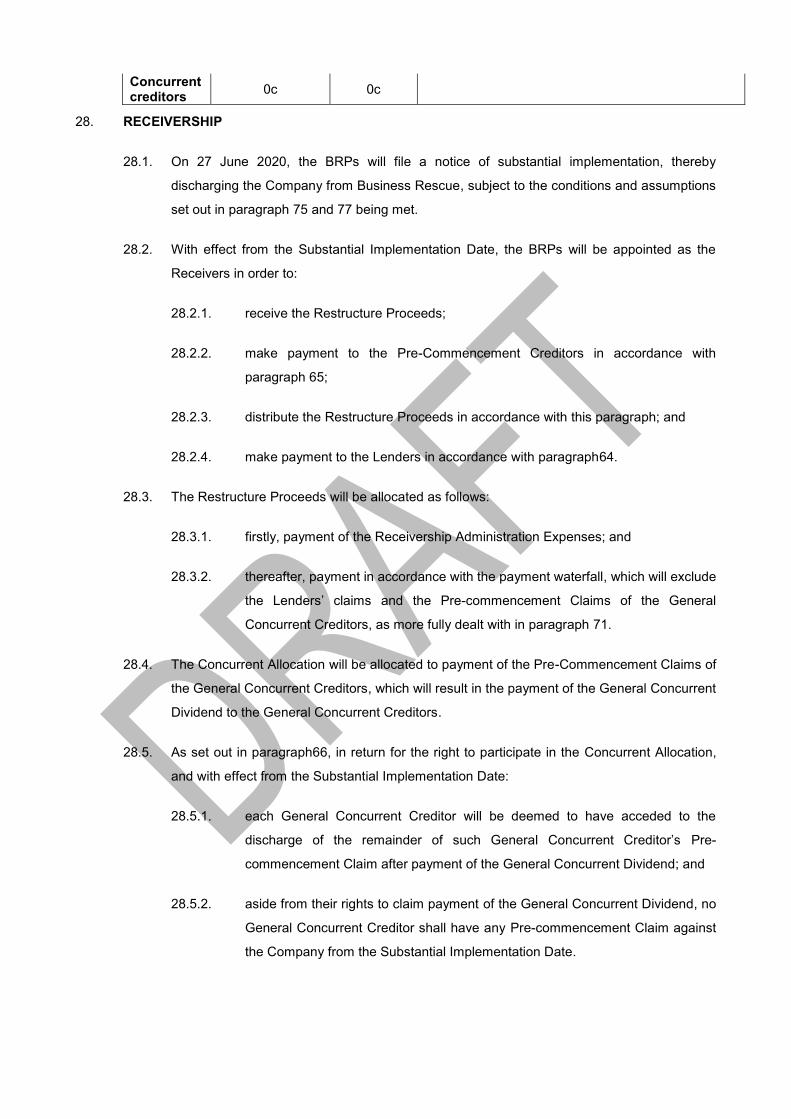

Paragraph number and description Page

1. INTERPRETATION AND PRELIMINARY .................................................................................................. 3

2. ACTION TO BE TAKEN BY AFFECTED PERSONS .............................................................................. 12

3. STRUCTURE OF THE PLAN ................................................................................................................... 12

PART A – BACKGROUND .............................................................................................................................. 13

4. COMPANY INFORMATION ..................................................................................................................... 13

5. COMPANY BACKGROUND .................................................................................................................... 15

6. SUMMARY OF THE BUSINESS RESCUE.............................................................................................. 19

7. STEPS TAKEN SINCE THE APPOINTMENT OF THE BRPS ................................................................ 20

8. MARKET CONDITIONS AND TRADING FOLLOWING THE COMMENCEMENT DATE ...................... 45

9. MATERIAL ASSETS AND SECURITY OF THE COMPANY AS AT THE COMMENCEMENT DATE.... 51

10. CREDITORS OF THE COMPANY AS AT THE COMMENCEMENT DATE ........................................ 52

11. CREDITORS VOTING INTEREST AND VOTING BY PROXY ............................................................ 52

12. PROBABLE DIVIDEND ON LIQUIDATION .......................................................................................... 53

13. HOLDERS OF THE COMPANY’S ISSUED SECURITIES................................................................... 54

14. THE PRACTITIONERS’ REMUNERATION ......................................................................................... 54

15. STATEMENT ABOUT WHETHER THE BUSINESS RESCUE PLAN INCLUDES A PROPOSAL

MADE INFORMALLY BY A CREDITOR ......................................................................................................... 54

PART B – PROPOSALS.................................................................................................................................. 55

16. PURPOSE AND OBJECTIVE OF BUSINESS RESCUE ..................................................................... 55

17. SUMMARY OF THE PROPOSAL IN TERMS OF THIS BUSINESS RESCUE PLAN ......................... 55

18. THE PROPOSED RESTRUCTURE ..................................................................................................... 57

19. GOVERNMENT APPROPRIATION AND FUNDING ........................................................................... 60

20. RECEIVERSHIP ................................................................................................................................... 69

21. EFFECT ON CREDITORS ................................................................................................................... 65

22. EFFECT ON EMPLOYEES .................................................................................................................. 67

23. EFFECT OF THE BUSINESS RESCUE PLAN ON THE HOLDERS OF EACH CLASS OF THE

COMPANY'S ISSUED SHARES ..................................................................................................................... 68

24. COMPARISON OF THE BUSINESS RESCUE TO LIQUIDATION ..................................................... 68

25. ORDER OF DISTRIBUTION – PAYMENT WATERFALL IN BUSINESS RESCUE & RECEIVERSHIP

69

26. PROOF OF CLAIMS BY CREDITORS................................................................................................. 72

27. MORATORIUM ..................................................................................................................................... 55

28. BENEFITS OF ADOPTING THE BUSINESS RESCUE PLAN COMPARED TO LIQUIDATION ........ 72

29. RISKS OF THE BUSINESS RESCUE .................................................................................................. 74

30. ASSUMPTIONS MADE WITH REGARD TO FORECAST OF THE BUSINESS RESCUE DIVIDEND 75

PART C – ASSUMPTIONS AND CONDITIONS ............................................................................................. 77

31. CIRCUMSTANCES IN WHICH THE BUSINESS RESCUE PLAN WILL END AND THE DURATION

OF BUSINESS RESCUE................................................................................................................................. 77

32. CONDITIONS FOR THE BUSINESS RESCUE PLAN TO COME INTO OPERATION AND BE FULLY

IMPLEMENTED ............................................................................................................................................... 77

33. EFFECT OF THE BUSINESS RESCUE PLAN ON EMPLOYEES ...................................................... 77

34. PROJECTED BALANCE SHEET AND PROJECTED STATEMENT OF INCOME AND EXPENSES

PREPARED ON THE ASSUMPTION THAT THE BUSINESS RESCUE PLAN IS ADOPTED ...................... 78

35. EXISTING LITIGATION ........................................................................................................................ 78

36. DISPUTE RESOLUTION ...................................................................................................................... 78

37. ABILITY TO AMEND THE BUSINESS RESCUE PLAN ...................................................................... 80

38. SEVERABILITY .................................................................................................................................... 80

39. CONCLUSION ...................................................................................................................................... 80

40. BRPS' CERTIFICATE ........................................................................................................................... 80

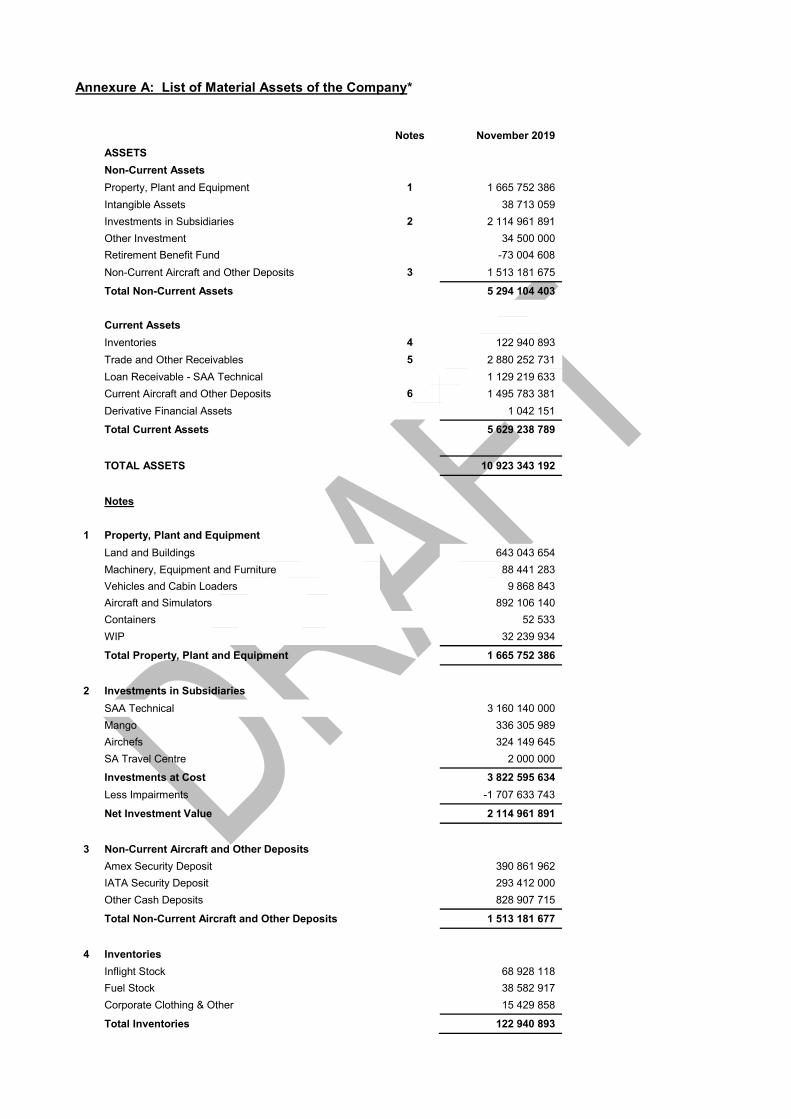

Annexure A: List of the material assets of the Company

Annexure B: List of the Creditors of the Company

Annexure [] : Steps Plan

Annexure [] : Income statement, balance sheet and cash flow

Annexure [] :

Annexure [] :

1. INTERPRETATION AND PRELIMINARY

The headings of the paragraphs in this Business Rescue Plan are for the purpose of convenience and

reference only and shall not be used in the interpretation of nor modify nor amplify the terms of this

Business Rescue Plan nor any paragraph hereof. Unless a contrary intention clearly appears:

1.1. words importing –

1.1.1. any one gender includes the other gender;

1.1.2. the singular includes the plural and vice versa; and

1.1.3. persons include natural persons, created entities (incorporated and un-

incorporated and the State) and vice versa,

1.2. the following terms and/or expressions shall have the meanings assigned to them hereunder

and cognate expressions shall have corresponding meanings –

1.2.1. “Absa” means Absa Bank Limited (acting through its Corporate and Investment

Banking division), Registration No. 1986/004794/06, a company incorporated in

accordance with the laws of South Africa;

1.2.2. “Adamantem” means Adamantem (Pty) Limited, Registration

No. 2017/292632/07, a company incorporated in accordance with the laws of

South Africa;

1.2.3. “Adoption Date” means the date upon which the Business Rescue Plan is

approved in accordance with section 152(2), read with section 152(3)(b) and

section 152(3)(c)(ii)(aa), of the Companies Act;

1.2.4. “Advisors” means the advisors to the BRPs, namely Matuson & Associates,

Adamantem, Alvarez & Marsal Europe Limited, PricewaterhouseCoopers

Advisory Services (Pty) Limited and Edward Nathan Sonnenbergs Inc., and their

respective employees or representatives;

1.2.5. “Affected Person” or “Affected Persons” shall bear the meaning ascribed

thereto in section 128(1)(a) of the Companies Act, being shareholders, creditors,

employees of the Company and the registered trade unions representing

employees of the Company;

1.2.6. “Air Chefs” means Air Chefs SOC Limited, Registration No. 1990/006277/30, a

state owned company incorporated in accordance with the laws of South Africa;

1.2.7. “Ashburton” means [];

1.2.8. “BRPs” means the joint business rescue practitioners of the Company, appointed

in terms of section 129(3)(b) of the Companies Act, being Dongwana and

Matuson, and shall include a reference to “Receivers” as the context requires in

this Business Rescue Plan;

1.2.9. “Business” means the business of the Company from time to time including, inter

alia:

1.2.9.1. operating as a national airline carrier, providing passenger and cargo

transport services, over various domestic, regional and international

routes;

1.2.9.2. operating the Divisions; and

1.2.9.3. the holding of shares in the following wholly owned subsidiaries

(whose businesses are more fully described in paragraph [5.5]):

1.2.9.3.1. Mango;

1.2.9.3.2. SAA Technical;

1.2.9.3.3. Air Chefs; and

1.2.9.3.4. SACC.

1.2.10. “Business Day” means any day other than a Saturday, Sunday or official public

holiday in South Africa;

1.2.11. “Business Rescue” means proceedings to facilitate the rehabilitation of the

Company, which is financially distressed, as more fully defined in section

128(1)(b) of the Companies Act and paragraph [] herein;

1.2.12. “Business Rescue Costs” means the remuneration and expenses of the BRPs

and other claims arising out of the costs of the Business Rescue, including the

costs of the Advisors;

1.2.13. “Business Rescue Plan” means this document together with all of its annexures,

as amended from time to time, and prepared in accordance with section 150 of

the Companies Act;

1.2.14. “CCMA” means the Commission for Conciliation, Mediation and Arbitration

established in terms of section 112 of the LRA;

1.2.15. “CIPC” means the Companies and Intellectual Property Commission, established

in terms of section 185 of the Companies Act;

1.2.16. “Claims” means Pre-commencement Claims and Post-commencement Claims;

1.2.17. “Commencement Date” means 5 December 2019, being the date upon which

Business Rescue commenced in accordance with section 129(1), read with

section 132(1)(a)(i), of the Companies Act;

1.2.18. “Company” means South African Airways SOC Limited, Registration

No. 1997/022444/30, a state owned company incorporated in accordance with

the laws of South Africa, at present under Business Rescue;

1.2.19. “Companies Act” means the Companies Act, No. 71 of 2008, as amended;

1.2.20. “Concurrent Allocation” means an amount of [] allocated to payment of the

General Concurrent Creditors, as more fully dealt with in paragraph [];

1.2.21. “Concurrent Creditors” means all unsecured Pre-commencement Creditors;

1.2.22. “Conditions” means the conditions which must be satisfied for the business

rescue plan to come into full operation and to be fully implemented, as

contemplated in section 150(c)(i) of the Companies Act, more fully dealt with in

paragraph [];

1.2.23. “Contracts” means those contracts entered into by the Company and third

parties, either prior to or after the Commencement Date;

1.2.24. “Creditors” means Pre-commencement Creditors and Post-commencement

Creditors;

1.2.25. “Creditors’ Committee” means the committee formed in terms of section 145(3)

of the Companies Act;

1.2.26. “DBSA” means the Development Bank of Southern Africa, Registration No. [], a

public entity established in terms of the Development Bank of

Southern Africa Act, No. 13 of 1997;

1.2.27. “Disputed Claims” means any and all Claims which are disputed by the BPRs,

including Pre-commencement Claims which may have been lodged by Pre-

commencement Creditors and whose Pre-commencement Claims have been

rejected either in whole or in part by the BRPs or Receivers, and which dispute

shall be determined in favour of or against such Creditors in terms of the Dispute

Mechanism contained in paragraph [];

1.2.28. “Distribution/s” means distributions to be made to Creditors by the BRPs and/or

the Receivers;

1.2.29. “DPE” means the Department of Public Enterprises of South Africa;

1.2.30. “Dongwana” means Siviwe Dongwana, the joint business rescue practitioner

appointed by the Company in terms of section 129(2)(b) of the Companies Act;

1.2.31. “Employees” means employees of the Company;

1.2.32. “Employees’ Committee” means the committee formed in terms of

section 144(3)(c) of the Companies Act and also for the purposes of consulting

with the Employees in terms of section 189(3), read together with section 189A,

of the LRA;

1.2.33. “ENSAfrica” means Edward Nathan Sonnenbergs Incorporated, attorneys

practising as such at 129 Rivonia Road, the Marc, Tower 2, Sandown, Sandton;

1.2.34. “Financially Distressed” shall bear the meaning ascribed thereto in

section 128(1)(f) of the Companies Act;

1.2.35. “Final Claims Date” means the final date for the filing of Pre-commencement

Claims, being [];

1.2.36. “FirstRand” means FirstRand Bank Limited (acting through its Rand Merchant

Bank division), Registration No. 1929/001225/06, a company incorporated in

accordance with the laws of South Africa;

1.2.37. “General Concurrent Creditors” means the Pre-commencement Creditors

excluding the Lenders;

1.2.38. “General Concurrent Dividend” means the guaranteed dividend of [] ([]) cents

in the Rand payable to the General Concurrent Creditors if this Business Rescue

Plan is adopted and the Proposed Restructure is fully implemented, as more fully

dealt with in paragraph [];

1.2.39. “Government” means the Government of the Republic of South Africa;

1.2.40. “Guarantees” means the guarantees issued by Government in favour of the

Lenders for the obligations of the Company, more fully dealt with in paragraph [];

1.2.41. “IAM” means Investec Asset Management, Registration No. [], a company

incorporated in accordance with the laws of South Africa;

1.2.42. “IATA” means the International Air Transport Association, incorporated in terms

of an Act of the Canadian Parliament;

1.2.43. “Insolvency Act” means the Insolvency Act No. 24 of 1936, as amended;

1.2.44. “Investec” means Investec Bank Limited, Registration No. 1969/004763/06, a

company incorporated in accordance with the laws of South Africa;

1.2.45. “Lenders” means the Pre-commencement Lenders and PCF Lenders;

1.2.46. “Lessors” means the lessors of aircraft to the Company, as more fully dealt with

in [];

1.2.47. “LRA” means the Labour Relations Act, No. 66 of 1995, as amended;

1.2.48. “Management” means members of the Company’s board and/or pre-existing

management as at the Commencement Date;

1.2.49. “Mango” means Mango Airlines SOC Limited, Registration No. 2006/018129/30,

a state owned company incorporated in accordance with the laws of South Africa;

1.2.50. “Matuson” means Leslie Matuson, the joint business rescue practitioner

appointed by the Company in terms of section 129(2)(b) of the Companies Act;

1.2.51. “Matuson & Associates” means Matuson & Associates (Pty) Limited,

Registration No. 2009/008967/07, a company incorporated in accordance with

the laws of South Africa;

1.2.52. “Momentum” means [];

1.2.53. “National Treasury” means the Department of the National Treasury of

South Africa;

1.2.54. “Nedbank” means Nedbank Limited, Registration No. 1951/000009/06, a

company incorporated in accordance with the laws of South Africa;

1.2.55. “New HoldCo” means the new holding company to be established as a

State Owned Company by Government in terms of the Proposed Restructure;

1.2.56. “NPE” means a national public entity established in terms of the PFMA;

1.2.57. “Notice of Meeting” means the notice of the meeting to consider the Business

Rescue Plan delivered to all Affected Persons as contemplated in terms of

section 151(2) of the Companies Act;

1.2.58. “PCF” means post-commencement finance as contemplated in section 135 of the

Companies Act;

1.2.59. “PCF Bank Lenders” means Absa, FirstRand, Investec, Nedbank and Standard

Bank;

1.2.60. “PCF Lenders” means DBSA and the PCF Bank Lenders;

1.2.61. “PFMA” means the Public Finance Management Act, No. 1 of 1999, as amended;

1.2.62. “Post-commencement Claims” means any claim against the Company, the

cause of action in respect of which arose after the Commencement Date;

1.2.63. “Post-commencement Creditors” means all persons, including legal entities

and natural persons, having Post-commencement Claims, excluding the PCF

Lenders;

1.2.64. “Pre-commencement Claims” means any claim against the Company, the

cause of action which arose prior to the Commencement Date;

1.2.65. “Pre-commencement Creditors” means all persons, including legal entities and

natural persons, having Pre-commencement Claims;

1.2.66. “Pre-commencement Lenders” means Absa, FirstRand, Investec, Nedbank,

Standard Bank, IAM, Ashburton, Sanlam and Momentum;

1.2.67. “Proposed Restructure” means the restructure proposed by the BRPs, as more

fully dealt with in paragraph [];

1.2.68. “Publication Date” means the date on which this Business Rescue Plan is

published to Affected Persons in terms of section 150(5) of the Companies Act,

being [] 2020;

1.2.69. “Rand” or “R” or “ZAR” means the lawful currency of South Africa;

1.2.70. “Receivers” means the receivers to be appointed in terms of paragraph [], being

Dongwana and Matuson;

1.2.71. “Receivership” means the process which will commence on the Substantial

Implementation Date, more fully dealt with in paragraph [];

1.2.72. “Receivership Administration Expenses” means the remuneration and

expenses of the Receivers and other claims arising out of the costs of the

Receivership;

1.2.73. “Receivership Proceeds” means the Restructure Proceeds, the proceeds

received from any recovery or related process instituted by the BRPs and/or the

Receivers and any additional proceeds to be included in the Receivership

Proceeds in terms of the Business Rescue Plan;

1.2.74. “Restructure Proceeds” means the proceeds received by the Company or value

attributed to the Transfer Shares or the transfer of any other asset in terms of the

Proposed Restructure, as more fully dealt with in paragraph [];

1.2.75. “SA Airlink” means SA Airlink (Pty) Limited, Registration No. 1969/002554/07, a

company incorporated in accordance with the laws of South Africa;

1.2.76. “SAA Cargo” means the division of the Company which operates as an airfreight

service provider;

1.2.77. “SAA Lounges” means the division of the Company which operates as a lounge

service provider to premium passengers;

1.2.78. “SAA Technical” means SAA Technical SOC Limited, Registration

No. 1999/024058/30, a state owned company incorporated in accordance with

the laws of South Africa;

1.2.79. “SAA Voyager” means the division of the Company which operates the

Company’s loyalty programme;

1.2.80. “SAA Restructure” means the proposed restructure of the Business of the

Company, as more fully dealt with in paragraph [];

1.2.81. “SACC” means South African Airways City Centre SOC Limited, Registration

No. 1997/003282/30, a state owned company incorporated in accordance with

the laws of South Africa;

1.2.82. “SA Express” means South African Express Airways SOC Limited (in business

rescue), Registration No. 1990/007412/30, a state owned company incorporated

in accordance with the laws of South Africa;

1.2.83. “Sanlam” means [], Registration No. [], a company incorporated in accordance

with the laws of South Africa;

1.2.84. “Secured Creditors” means those Creditors who hold security for their Claims

against the Company;

1.2.85. “South Africa” means the Republic of South Africa;

1.2.86. “Standard Bank” means The Standard Bank of South Africa Limited,

Registration No. 1962/000738/06, a company incorporated in accordance with

the laws of South Africa;

1.2.87. “Subsidiaries” means the wholly owned subsidiaries of the Company,

comprising:

1.2.87.1. SAA Technical;

1.2.87.2. Mango;

1.2.87.3. Air Chefs; and

1.2.87.4. SACC.

1.2.88. “Substantial Implementation Date” means the earlier of:

1.2.88.1. [], or such later date as may be notified by the BRPs to

Affected Persons,

upon which date the BRPs will file with CIPC a notice of substantial

implementation in terms of section 152(8) of the Companies Act whereupon

Business Rescue will end in terms of section 132(2)(c)(ii);

1.2.89. “Tax/Taxation” means:

1.2.89.1. levies payable to Government authorities;

1.2.89.2. normal taxation;

1.2.89.3. capital gains tax;

1.2.89.4. value-added tax;

1.2.89.5. donations tax;

1.2.89.6. customs duty;

1.2.89.7. securities transfer tax;

1.2.89.8. all Pay-As-You-Earn taxation (PAYE) not paid over;

1.2.89.9. all other forms of taxation, other than deferred tax; and

1.2.89.10. any penalties or interest on any of the aforegoing;

1.2.90. “Trade Unions” means the following registered trade unions representing

employees of the Company:

1.2.90.1. National Transport Movement;

1.2.90.2. National Union of Metalworkers of South Africa;

1.2.90.3. South African Airways Cabin Crew Association;

1.2.90.4. Aviation Union of South Africa;

1.2.90.5. South African Transport and Allied Workers Union;

1.2.90.6. Solidarity; and

1.2.90.7. South African Airways Pilots Association;

1.2.91. “Transfer Shares” means the shares to be transferred by the Company to

New HoldCo in terms of the Proposed Restructure;

1.2.92. “Value-Added Tax Act” means the Value Added Tax Act, No. 89 of 1991, as

amended;

1.2.93. “VAT” means the value-added tax levied in terms of the Value-Added Tax Act;

1.3. any reference to any statute, regulation or other legislation in this Business Rescue Plan shall

be a reference to that statute, regulation or other legislation as at the Publication Date, and as

amended or substituted from time to time;

1.4. any reference in this Business Rescue Plan to any other agreement or document shall be

construed as a reference to such other agreement or document as same may have been, or

may from time to time be, amended, varied, novated or supplemented;

1.5. if figures are referred to in numerals and in words and if there is any conflict between the two,

the words shall prevail;

1.6. if any provision in a definition in this Business Rescue Plan is a substantive provision

conferring a right or imposing an obligation on any person or entity then, notwithstanding that

it is only in a definition, effect shall be given to that provision as if it were a substantive provision

in the body of this Business Rescue Plan;

1.7. where any term is defined in this Business Rescue Plan within a particular paragraph other

than this paragraph 0, that term shall bear the meaning ascribed to it in that paragraph

wherever it is used in this Business Rescue Plan;

1.8. where any number of days is to be calculated from a particular day, such number shall be

calculated as excluding such particular day and commencing on the next day. If the last day

of such number so calculated falls on a day which is not a Business Day, the last day shall be

deemed to be the next succeeding day which is a Business Day;

1.9. any reference to days (other than a reference to Business Days), months or years shall be a

reference to calendar days, months or years, as the case may be; and

1.10. words or terms that are capitalised and not otherwise defined in the narrative of this Business

Rescue Plan (excluding capitalised words or terms used for the purpose of tables) shall bear

the meaning assigned to them in the Companies Act.

2. ACTION TO BE TAKEN BY AFFECTED PERSONS

2.1. If any Affected Person is in doubt as to what action should be taken arising from the contents

of this Business Rescue Plan, such Affected Person or Affected Persons are advised to

consult an independent attorney, accountant or other professional advisor in addition to any

consultation with or direction received from the BRPs.

2.2. Nothing contained in this Business Rescue Plan shall constitute legal or Tax advice to any

Affected Person, nor do the BRPs make any representations in respect thereof.

3. STRUCTURE OF THE PLAN

For the purposes of section 150(2) of the Companies Act, this Business Rescue Plan is divided into 3

(three) parts as follows –

3.1. PART A - BACKGROUND

This part sets out the background to the Company and the factors that resulted in the

Company being Financially Distressed and being placed under Business Rescue. The

Company’s financial distress is described more fully in paragraph [] below.

3.2. PART B - PROPOSALS

This part describes the terms of the proposals and includes, inter alia, the benefits and/or

effect of adopting the Business Rescue Plan as opposed to the Company being placed into

liquidation.

3.3. PART C – ASSUMPTIONS AND CONDITIONS

This part sets out, inter alia, what conditions need to be fulfilled in order for the Business

Rescue Plan to become effective, and to be implemented.

_____________________________________________________________________________________

PART A – BACKGROUND

______________________________________________________________________________________

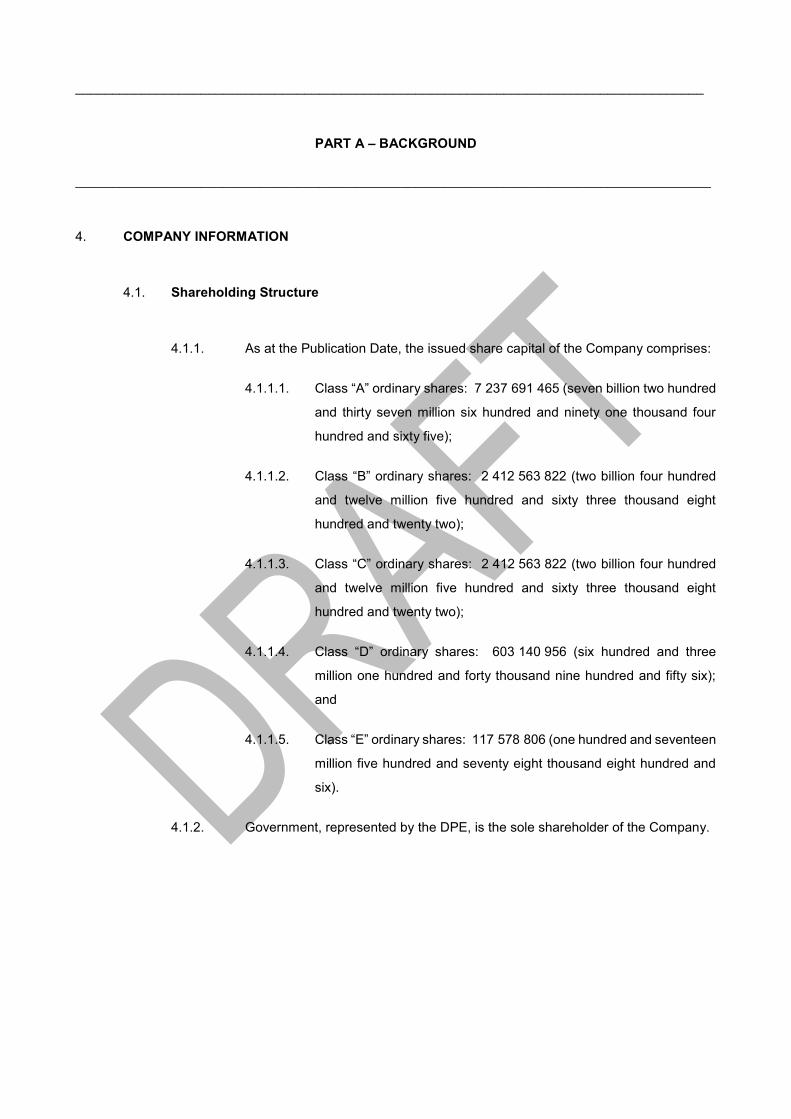

4. COMPANY INFORMATION

4.1. Shareholding Structure

4.1.1. As at the Publication Date, the issued share capital of the Company comprises:

4.1.1.1. Class “A” ordinary shares: 7 237 691 465 (seven billion two hundred

and thirty seven million six hundred and ninety one thousand four

hundred and sixty five);

4.1.1.2. Class “B” ordinary shares: 2 412 563 822 (two billion four hundred

and twelve million five hundred and sixty three thousand eight

hundred and twenty two);

4.1.1.3. Class “C” ordinary shares: 2 412 563 822 (two billion four hundred

and twelve million five hundred and sixty three thousand eight

hundred and twenty two);

4.1.1.4. Class “D” ordinary shares: 603 140 956 (six hundred and three

million one hundred and forty thousand nine hundred and fifty six);

and

4.1.1.5. Class “E” ordinary shares: 117 578 806 (one hundred and seventeen

million five hundred and seventy eight thousand eight hundred and

six).

4.1.2. Government, represented by the DPE, is the sole shareholder of the Company.

4.2. Directors

4.2.1. As at the Commencement Date, the directors of the Company, according to

CIPC, were:

Name of Director Date of

Appointment

Deon Jeftha Fredericks 29/10/2018

Zukisa Millicent Ramasia 11/06/2019

Ahmed Ismail Bassa (non-executive) 03/11/2017

Martin Lawrence Kingston (non-executive) 03/11/2017

Holmes Peter Maluleka (non-executive) 01/09/2016

Thandeka Nozipho Mgoduso (non-executive) 01/09/2016

Akhter Hoosen Moosa (non-executive) 01/09/2016

Geoffrey Rothschild (non-executive) 03/11/2017

Matsidiso Peter Tshisevhe (non-executive) 01/09/2016

4.2.2. The records of the Company are in the process of being updated with CIPC,

however, according to the Company records, the following are the directors of the

Company as at the Publication Date:

Name of Director Date of

Appointment

Ahmed Ismail Bassa (non-executive) 03/11/2017

Holmes Peter Maluleka (non-executive) 01/09/2016

Thandeka Nozipho Mgoduso (non-executive) 01/09/2016

Akhter Hoosen Moosa (non-executive) 01/09/2016

Geoffrey Rothschild (non-executive) 03/11/2017

Matsidiso Peter Tshisevhe (non-executive) 01/09/2016

4.3. Company Information

Financial Year End: 31 March

Registered Address: Airways Park

1 Jones Road

OR Tambo International Airport

Kempton Park

Gauteng

1620

Postal Address: Private Bag X13

OR Tambo International Airport

Kempton Park

Gauteng

1627

Auditors / Accountants: Auditor General South Africa:

Polani Sokombela

5. COMPANY BACKGROUND

5.1. Background to the Company

5.1.1. The Company was established in February 1934, when Government took over

Union Airways of South Africa, being the first commercial airline of South Africa.

It has been state-owned since then, except from 1999 to 2002, when Swissair

held 20% of the equity in the Company.

5.1.2. The Company's Business involves operating as a national airline carrier,

providing passenger and cargo transport services over various domestic, regional

and international routes. The Company is a member of Star Alliance, the largest

international airline alliance.

5.1.3. As at the Commencement Date, the Company:

5.1.3.1. Provided aviation transport services to [21] routes, comprising:

5.1.3.1.1. 9 international routes;

5.1.3.1.2. 15 regional routes; and

5.1.3.1.3. 6 domestic routes.

5.1.3.2. Held a fleet of 49 aircraft, comprising:

5.1.3.2.1. Owned aircraft:

5.1.3.2.1.1. 5 x A340-300 aircraft; and

5.1.3.2.1.2. 4 x A340-600 aircraft.

5.1.3.2.2. Leased aircraft:

5.1.3.2.2.1. 7 x A319 aircraft;

5.1.3.2.2.2. 10 x A320 aircraft;

5.1.3.2.2.3. 3 x A340-300 aircraft;

5.1.3.2.2.4. 3 x A340-600 aircraft;

5.1.3.2.2.5. 6 x A330-200 aircraft;

5.1.3.2.2.6. 5 x A330-300 aircraft;

5.1.3.2.2.7. 4 x A350-900 aircraft; and

5.1.3.2.2.8. 2 x B737-300F aircraft (freighters).

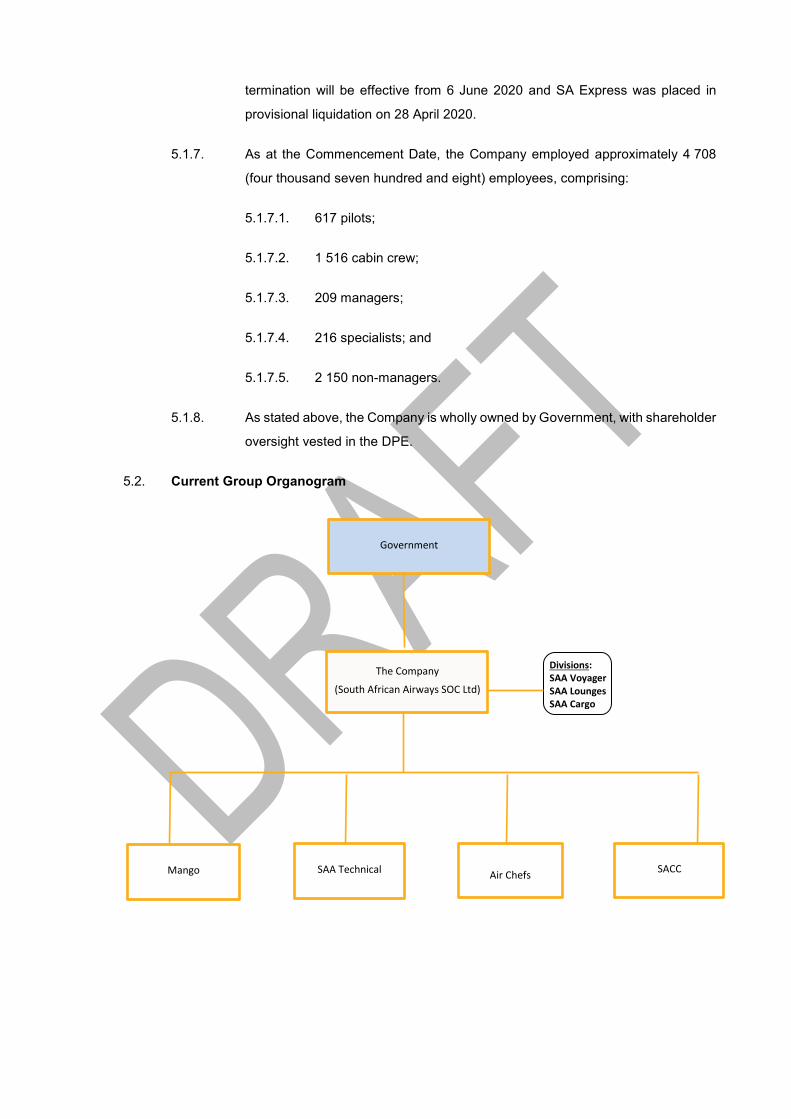

5.1.4. The Company has the following three non-corporate businesses (i.e. the

Divisions):

5.1.4.1. SAA Cargo, an air cargo service provider with capacity primarily

sourced from the “belly space” of SAA’s passenger aircraft fleet.

5.1.4.2. SAA Lounges, which provides lounge services to premium

passengers in the major cities in South Africa (Johannesburg,

Cape Town, Durban, East London and Port Elizabeth) and Africa

(Harare and Lusaka).

5.1.4.3. SAA Voyager, an airline loyalty programme.

5.1.5. In addition, the Company wholly owns the Subsidiaries, namely:

5.1.5.1. Mango, a global best-practice low-cost carrier, primarily operating in

the South African domestic market, and a feeder airline to the

Company;

5.1.5.2. SAA Technical, Africa’s largest aircraft Maintenance, Repair and

Overhaul (“MRO”) business;

5.1.5.3. Air Chefs, a catering business primarily supplying catering services

to the Company’s fleet and SAA Lounges in Johannesburg,

Cape Town and Durban; and

5.1.5.4. SACC, which is currently dormant but operated as a retail travel

business with franchises in South Africa and some other African

states.

5.1.6. The Company licenses its airline code to two feeder airlines, namely, SA Express

and SA Airlink. During the Company’s Business Rescue, however, SA Airlink

terminated the license agreement concluded with the Company, which

termination will be effective from 6 June 2020 and SA Express was placed in

provisional liquidation on 28 April 2020.

5.1.7. As at the Commencement Date, the Company employed approximately 4 708

(four thousand seven hundred and eight) employees, comprising:

5.1.7.1. 617 pilots;

5.1.7.2. 1 516 cabin crew;

5.1.7.3. 209 managers;

5.1.7.4. 216 specialists; and

5.1.7.5. 2 150 non-managers.

5.1.8. As stated above, the Company is wholly owned by Government, with shareholder

oversight vested in the DPE.

5.2. Current Group Organogram

Air Chefs

SAA Technical

The Company

(South African Airways SOC Ltd)

Mango

Government

SACC

Divisions: SAA Voyager SAA Lounges SAA Cargo

5.3. Background to the Company's Financial Distress

5.3.1. The main reasons for the Company’s financial distress are the following:

5.3.1.1. The Company has suffered significant losses in each financial year

since the 2014 financial year.

5.3.1.2. There has been a lack of adequate recapitalisation which resulted in

the Company experiencing severe liquidity constraints, which was

exacerbated by:

5.3.1.2.1. The confirmation by Government that it would not

continue supporting the Company financially in the

manner that it had previously done, but would

provide financial support to facilitate a radical

restructuring of the Company.

5.3.1.2.2. The grounding of SAA aircraft by the Civil Aviation

Authorities, in October 2019, due to technical none

compliance which negatively affected the reputation

of the airline with travel agents and passengers

5.3.1.2.3. The industrial action that occurred over an eight day

period in November 2019 which had the effect of

severely hampering the cash flow of the Company.

5.3.1.2.4. The Company lost significant revenue during

November 2019 where the Company should have

been ramping up to its busiest period.

5.3.1.2.5. The issuing of an application to commence business

rescue proceedings by one of the Trade Unions.

The adverse publicity in the media shortly after the

commencement of business rescue proceedings

had the following consequences:

5.3.1.2.5.1. the withdrawal of travel insurance

by various insurers;

5.3.1.2.5.2. various travel agents halting the

sale of the Company’s tickets to

their customers and preferring to

use other carriers; and

5.3.1.2.5.3. customers that had already booked

flights started cancelling their flights

and requesting refunds.

5.3.1.2.6. The governance issues at the Company which

resulted in a high turnover of executive management

over the last ten years;

5.3.1.2.7. In adequate capitalisation of the subsidiaries with

increasing dependency on the Company to provide

them with working capital; and

5.3.1.2.8. Increased competition with a significant pressure on

the Company’s pricing for tickets.

5.3.2. The aforesaid adversely affected the Company’s cash flow and caused the

Company to become illiquid and therefore financially distressed in that is was

unable to pay its liabilities to lenders and creditors as they fell due.

6. SUMMARY OF THE BUSINESS RESCUE

6.1. Introduction

Business Rescue, as defined in section 128 (1) (b) of the Companies Act, refers to

proceedings to facilitate the rehabilitation of a company that is financially distressed by

providing for –

6.1.1. the temporary supervision of a company by one or more business rescue

practitioners, and of the management of its affairs, business and property;

6.1.2. a temporary moratorium on the rights of claimants against a company or in

respect of property in its possession; and

6.1.3. the development and implementation, if approved, of a plan to rescue the

company in question by restructuring its affairs, business, property, debt and

other liabilities, and equity in a manner that maximises the likelihood of the

company in question continuing in existence on a solvent basis or, if it is not

possible for the company to so continue in existence, results in a better return for

the company's creditors or shareholders than would result from the immediate

liquidation of the company.

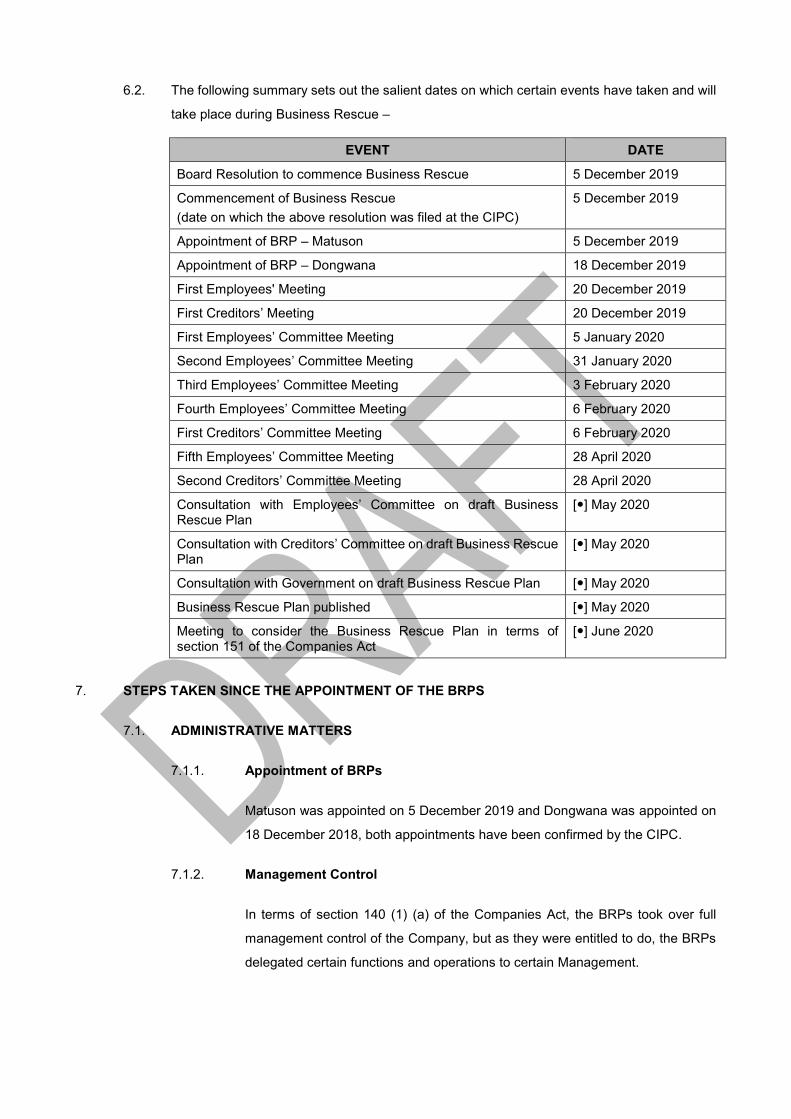

6.2. The following summary sets out the salient dates on which certain events have taken and will

take place during Business Rescue –

EVENT DATE

Board Resolution to commence Business Rescue 5 December 2019

Commencement of Business Rescue

(date on which the above resolution was filed at the CIPC)

5 December 2019

Appointment of BRP – Matuson 5 December 2019

Appointment of BRP – Dongwana 18 December 2019

First Employees' Meeting 20 December 2019

First Creditors’ Meeting 20 December 2019

First Employees’ Committee Meeting 5 January 2020

Second Employees’ Committee Meeting 31 January 2020

Third Employees’ Committee Meeting 3 February 2020

Fourth Employees’ Committee Meeting 6 February 2020

First Creditors’ Committee Meeting 6 February 2020

Fifth Employees’ Committee Meeting 28 April 2020

Second Creditors’ Committee Meeting 28 April 2020

Consultation with Employees’ Committee on draft Business Rescue Plan

[] May 2020

Consultation with Creditors’ Committee on draft Business Rescue Plan

[] May 2020

Consultation with Government on draft Business Rescue Plan [] May 2020

Business Rescue Plan published [] May 2020

Meeting to consider the Business Rescue Plan in terms of section 151 of the Companies Act

[] June 2020

7. STEPS TAKEN SINCE THE APPOINTMENT OF THE BRPS

7.1. ADMINISTRATIVE MATTERS

7.1.1. Appointment of BRPs

Matuson was appointed on 5 December 2019 and Dongwana was appointed on

18 December 2018, both appointments have been confirmed by the CIPC.

7.1.2. Management Control

In terms of section 140 (1) (a) of the Companies Act, the BRPs took over full

management control of the Company, but as they were entitled to do, the BRPs

delegated certain functions and operations to certain Management.

7.1.3. Notices

The BRPs have been publishing notices to affected persons in terms of the

Companies Act.

7.1.4. Reporting to CIPC

The BRPs have complied with all statutory obligations under the Companies Act

and will render monthly reports to CIPC as contemplated in section 132 (3) of the

Companies Act.

7.1.5. Appointment of Alvarez & Marsal as Global Aviation Restructuring Experts

The BRPs appointed and mandated Alvarez & Marsal to provide:

7.1.5.1. Independent and objective advice, from an aviation operations

perspective, on opportunities to reduce cash burn, including cost

reduction and operations improvement opportunities;

7.1.5.2. to provide the restructuring plan options for the airline which would

then be developed into a BR plan once Government has chosen their

preferred plan and

7.1.5.3. based on their aviation industry contacts, to assist in sourcing a SEP

for the Company.

7.1.6. Appointment of PWC as Independent Experts

7.1.6.1. The BRPs appointed and mandated PWC:

7.1.6.1.1. to provide cash flow forecasts to show the liquidity

requirements for each of the restructuring scenarios

for SAA;

7.1.6.1.2. to develop an integrated financial forecasting and

business model [based on the Proposed

Restructuring Plan] (“Financial Model”); and

7.1.6.1.3. as independent experts for purposes of calculating

the estimated liquidation dividend that would be

received by Creditors, in their specific classes, if the

Company were to be immediately placed in

liquidation.

7.1.6.2. The Financial Model was used, inter alia, to prepare the projected

balance sheet and statement of income and expenses for the

Company for the ensuing three years, dealt with in paragraph []

below.

7.1.6.3. The liquidation dividend is dealt with in paragraph [] below.

7.1.7. Extension for Publication of Business Rescue Plan

In terms of section 150 (5) of the Companies Act, the Business Rescue Plan was

required to be published within 25 (twenty five) Business Days from the

appointment of the BRPs. The BRPs ultimately obtained an extension from the

Creditors as contemplated in section 150 (5) (b) of the Companies Act for the

publication of the Business Rescue Plan to [29 May 2020].

7.1.8. Publication of Business Rescue Plan and Notice of Meeting

7.1.8.1. The Business Rescue Plan will be published to all Affected Persons

on the Publication Date.

7.1.8.2. The Notice of Meeting will be delivered to all Affected Persons

simultaneously with the publication of the Business Rescue Plan.

7.1.8.3. The publication of the Business Rescue Plan and delivery of the

Notice of Meeting will take place in accordance with the provisions of

the Companies Act and the Regulations thereto.

7.1.9. Cash Resources

7.1.9.1. In order to preserve the cash resources of the Company, the BRPs

implemented immediate cash relief initiatives and explored broader

cost optimisation initiatives, which are dealt with further in

paragraph [].

7.1.9.2. The BRPs also obtained PCF from the PCF Lenders, which is dealt

with further in paragraph [].

7.2. LABOUR

7.2.1. Employees’ Meetings

7.2.1.1. A first meeting of Employees, as contemplated in section 148 (1) of

the Companies Act, was convened on 20 December 2019.

7.2.1.2. At this meeting, inter alia:

7.2.1.2.1. the business rescue process was explained;

7.2.1.2.2. Employees were informed of the BRPs’ opinion

regarding the reasonable prospect of rescuing the

Company;

7.2.1.2.3. Employees were informed of the BRPs’ actions since

the Commencement Date;

7.2.1.2.4. assistance was also given to the Employees by

providing answers to their various queries; and

7.2.1.2.5. nominations were requested for the establishment of

the Employees’ Committee.

7.2.2. Employees’ Committee

7.2.2.1. Pursuant to the first meeting of Employees, the Employees’

Committee was duly established.

7.2.2.2. The Employees’ Committee comprises the following:

7.2.2.2.1. representatives from the Trade Unions; and

7.2.2.2.2. representatives for the independent employees

(being those employees unrepresented by trade

unions).

7.2.2.3. The members of the Employees’ Committee appointed Cloete Murray

as the independent chairperson of the Employees’ Committee.

7.2.2.4. The Employees' Committee met with the BRPs on 5 January 2020,

31 January 2020, 4 February 2020,6 February 2020, 12 March 2020

and 28 April 2020.

7.2.3. Consultation on the Draft Business Rescue Plan

7.2.3.1. On 31 May 2020, the BRPs provided the draft Business Rescue Plan

to, inter alia, representatives on the employees’ committee to:

7.2.3.1.1. enable them to make representations to the BRPs

for consideration, subject to the BRPs’ overall

responsibility to publish a Business Rescue Plan

which they regard as representing the best

prospects of rescuing the Company as contemplated

in the Companies Act; and

7.2.3.1.2. afford them sufficient opportunity to review the draft

Business Rescue Plan and prepare a submission as

contemplated in section 152 (1) (c) of the Companies

Act.

7.2.3.2. On [], the BRPs consulted with the employees’ committee and [].

[D/N: Insert outcome of consultation].

7.2.4. Section 189 of the LRA Process

7.2.4.1. It became apparent that for the Business Rescue efforts to be

successful, and for liquidation to be avoided, it was necessary for the

Company to restructure its operations and also reduce its costs

significantly.

7.2.4.2. The Company has formed the view that, alongside other cost savings

measures to be implemented, the best way for the Company to

reduce its costs significantly in order for the Business Rescue efforts

to be successful, and for liquidation to be avoided, is by the Company:

7.2.4.2.1. reducing the number of its employees in line with the

optimal operations; and

7.2.4.2.2. revising the terms and conditions of employment of

the remaining employees to align them with the

market related conditions, preferably through

collective agreements concluded with those Trade

Unions representing the majority of the Company’s

remaining employees.

7.2.4.3. As a result, on 9 March 2020, the Company, having contemplated the

possibility of such dismissals and a possible new structure, issued

notices in terms of section 189 (3) read together with section 189A of

the LRA (“section 189 (3) notices”) to all Employees and their trade

unions.

7.2.4.4. In terms of those section 189 (3) notices, all of the positions with the

Company would be potentially affected. All employees would be

displaced, and the selection criteria would be applied to offer

employees new jobs in the new proposed structure, at revised terms

and conditions of employment. In the event that an employee does

not accept a job offered to them, then it is proposed that they would

be selected for retrenchment, and another displaced employee will

be offered that position. 2 440 positions were made available in terms

of the proposed new structure on significantly revised terms and

conditions of employment. Representative Trade Unions will be

required to conclude new collective agreements giving effect to the

proposed changes and cancelling existing collective agreements

insofar as same are at variance with the proposed changes.

7.2.4.5. It must be mentioned that both NUMSA and SACCA withdrew from

the section 189 process initially citing health concerns in the context

of the COVID-19 pandemic and later in protest for inadequacy of

information provided by the Company.

7.2.4.6. The issuance of the section 189 (3) notices was the first step in a

statutory facilitated consultation process which commenced on 20

March 2020 under the auspices of facilitation at the CCMA. The

Company and the consulting parties held consultation meetings

and/or bilateral meetings on the following dates 20 March 2020,

23/03/2020, 24/03/2020, 26/03/2020, 01/04/2020, 02/04/2020,

03/04/2020, 13/04/2020, 14/04/2020, 15/04/2020, 16/04/2020,

17/04/2020, 18/04/2020, 20/04/2020, 23/04/2020, 28/04/2020 and

29/04/2020..

7.2.4.7. Following the declaration by the President of the Republic of South

on 15 March 2020 of a National State of Disaster, a s189

Supplementary Notice was issued to all employees on 19 March

2020. The restrictions of movement imposed as a result of the

declaration was expected to have a severe impact on the revenue

and cash generating ability of the Company which, in the opinion of

the Company and BRPs, necessitated an expedited s189

consultation process. Furthermore, the Company requested that the

parties consult and reach agreement on measures to mitigate the

adverse effects of the Covid-19 pandemic, such as the

implementation of short time and a rotational lay off

7.2.4.8. The section 189 (3) notices were issued after consultation with the

DPE, and notification to National Treasury.

7.2.4.9. The Company, for a minimum period of 60 (sixty) days as prescribed

in terms of the LRA, consulted with the consulting parties, on all the

issues set out in the section 189 (3) notices. This consultation

process was facilitated by two commissioners from the CCMA and

ended on 8 May 2020.

7.2.4.10. Mutual separation agreements were offered to the employees on the

terms set out below. The period for acceptance of the agreements

will be set out in more detail in paragraph [] .

7.2.5. On or about 22 November 2019, the Company had concluded a salary agreement

with a coalition of two of the recognised unions (NUMSA and SACCA) within its

workplace to regulate salaries and other conditions until 31 March 2020. In terms

of these salary agreements, the Company agreed to pay salary increases and

back pay to employees in separate tranches subject to the Company securing

funding for such purposes and such funding being available in February, March

and April 2020. The trade unions have enquired on and demanded the payment

of such salary increases and back-pay. To date, the funding required for such

salary increases has not been provided and accordingly the BRPs have not

authorised such payment of these salary increases and back-pay.

7.3. CREDITORS

7.3.1. Creditors’ Meeting:

7.3.1.1. A first meeting of Creditors, as contemplated in section 147 (1) of the

Companies Act, was convened on 20 December 2019

(“the First Meeting”).

7.3.1.2. At the First Meeting, inter alia:

7.3.1.2.1. the business rescue process was explained;

7.3.1.2.2. Creditors were informed of the BRPs’ opinion

regarding the reasonable prospect of rescuing the

Company;

7.3.1.2.3. Creditors were informed of the BRPs’ actions since

the Commencement Date;

7.3.1.2.4. assistance was given to the Creditors by providing

answers to their various queries;

7.3.1.2.5. the BRPs received proof of Pre-commencement

Claims by Pre-commencement Creditors; and

7.3.1.2.6. nominations were requested for the establishment of

the Creditors’ Committee.

7.3.2. Creditors' Committee

7.3.2.1. Pursuant to the First Meeting, a Creditors Committee was duly

established.

7.3.2.2. The members of the Creditors’ Committee appointed

Juliette de Hutton as the independent chairperson of the

Creditors’ Committee.

7.3.2.3. The Creditors' Committee met with the BRPs on 6 February 2020 and

28 April 2020.

7.3.3. Consultation on the draft Business Rescue Plan

7.3.3.1. On 28 May 2020, the BRPs provided the draft Business Rescue Plan

to, inter alia, representatives on the creditors’ committee to:

7.3.3.1.1. enable them to make representations to the BRPs

for consideration, subject to the BRPs’ overall

responsibility to publish a Business Rescue Plan

which the BRPs regarded as representing the best

prospects of rescuing the Company as contemplated

in the Companies Act; and

7.3.3.1.2. afford them sufficient opportunity to review the draft

Business Rescue Plan.

7.3.3.2. On [], the BRPs consulted with the creditors’ committee.

[D/N: Insert outcome of consultation].

7.4. LEGAL

7.4.1. Court Applications:

7.4.1.1. SA Airlink:

7.4.1.1.1. On 17 January 2020, SA Airlink issued an urgent

application seeking, inter alia:

7.4.1.1.1.1. a declarator that the flown and

unflown revenue in respect of flights

which occurred prior to the

Company’s Business Rescue did

not amount to a “debt owed” as

contemplated in terms of section

154 (2) of the Companies Act, or are

not debts owed by the Company

immediately before the beginning of

Business Rescue; and

7.4.1.1.1.2. an order that the Company makes

payment of the aforesaid flown

revenue within five days of the order

sought.

7.4.1.1.2. The Company and BRPs opposed the urgent

application.

7.4.1.1.3. The urgent application was heard on

11 February 2020.

7.4.1.1.4. On 2 March 2020, the urgent application was

dismissed with costs, including the costs of two

counsel.

7.4.1.1.5. On 5 March 2020, SA Airlink applied for leave to

appeal.

7.4.1.1.6. On 13 March 2020, SA Airlink were granted leave to

appeal to the Supreme Court of Appeal.

7.4.1.1.7. SA Airlink and the Company have filed heads of

argument and are awaiting confirmation of the

hearing date.

7.4.1.2. Black Management Forum (“BMF”) Application:

7.4.1.2.1. On or about 13 January 2020, the BMF launched an

application challenging the appointment of Mr Nico

Bezuidenhout as the Chief Executive Officer of

Mango Airlines (SOC) Limited (“Mango”). The

Company is cited as the Second Respondent in its

capacity as Mango’s holding company.

7.4.1.2.2. On 5 February 2020, the Company filed its notice of

opposition.

7.4.1.2.3. On 2 March 2020 the Company filed its record of

proceedings.

7.4.1.2.4. The other respondents in the matter have also filed

their records of proceedings.

7.4.1.2.5. The BMF is now required to either supplement its

founding papers or to notify the respondents that it

will not supplement its founding papers.

7.4.1.2.6. Upon the BMF supplementing its papers or notifying

the respondents that it will not supplement its

papers, the respondents, including the Company will

be required to file their answering papers.

7.4.1.3. NUMSA and SACCA application 1

7.4.1.3.1. On 10 February 2020 NUMSA and SACCA filed an

urgent application in the Labour Court for an order in

the order following terms:

7.4.1.3.1.1. That the Company’s and the

Business Rescue Practitioners’

announcement on 6 February 2020

in respect of the purported

dismissals of NUMSA and SACCA’s

members due to changes in the

flight network of the Company be

declared null and avoid for non-

compliance with the LRA and be set

aside;

7.4.1.3.1.2. That the Company’s and the

Business Rescue Practitioners’

failure to engage in meaningful joint-

consensus seeking consultations as

envisaged in section 189 and 189A

of the LRA be declared as unlawful

and/or unfair;

7.4.1.3.1.3. That the Company be interdicted

and restrained from taking any

steps towards terminating the

employment of NUMSA and

SACCA members in terms of the

restructuring process until it has

complied with the procedural

requirements in the LRA; and

7.4.1.3.1.4. That the Company be directed to

place NUMSA and SACCA

members on a trainee lay-off

scheme in terms of a collective

agreement between the parties.

7.4.1.3.1.5. The matter was heard on 13

February 2020 and judgment was

handed down on 14 February 2020.

The application was dismissed and

no order as to costs was made.

7.4.1.3.1.6. On the same day (14 February

2020), NUMSA and SACCA

launched an application for leave to

appeal on an urgent basis. The

matter was heard on the same day

and judgement was reserved.

7.4.1.3.1.7. On 20 February 2020, the

application for leave to appeal was

dismissed.

7.4.1.3.1.8. On 21 February NUMSA and

SACCA petitioned the Labour

Appeal Court on an urgent basis for

leave to appeal.

7.4.1.3.1.9. On 26 February 2020, SAA filed a

notice of intention to oppose and

answering affidavit.

7.4.1.3.1.10. On 27 February 2020, NUMSA and

SACCA filed their replying affidavit.

7.4.1.3.1.11. The matter currently awaits a

decision from the Labour Appeal

Court. However, in circumstances

where the section 189 (3) notice has

already been issued by the BRPs on

9 March 2020, this petition is moot

and is unlikely to be pursued further.

7.4.1.4. NUMSA and SACCA application 2

7.4.1.4.1. On 30 April 2020 NUMSA and SACCA delivered

another urgent application in the Labour Court for an

order in the order following terms:

7.4.1.4.1.1. declaring that the Company’s and

the BRPs’ issuing of the section

189(3) notices was unlawful,

alternatively, that the issuing of the

section 189(3) notices and/or

continuation with the consultative

process is unfair;

7.4.1.4.1.2. directing the Company and the

BRPs to withdraw the section

189(3) notices, alternatively, to

suspend the consultative process

until a business rescue plan has

been presented;

7.4.1.4.1.3. directing the Company and the

BRPs not to terminate the services

of any employee pursuant to the

notices and not to process any

applications for voluntary severance

packages, alternatively, not to

terminate services of any employee

pursuant to the section 189(3)

notices until the prayer sought in

the aforesaid paragraph has been

complied with;

7.4.1.4.1.4. declaring that the Company’s and

BRPs’ suspension of the

contractual right of the members of

NUMSA and SACCA to be

considered for placement in the

Training Lay-Off Scheme as an

alternative to retrenchment is

unlawful; and

7.4.1.4.1.5. directing the Company and the

BRPs to uplift such suspension and

to take all necessary steps towards

giving effect to their reciprocal

obligations in respect of the

aforesaid contractual rights.

7.4.1.4.2. The application was set down for hearing on

7 May 2020. The Court found in favour of the

applicants on 8 May 2020.

7.4.1.4.3. On 25 May 2020, the Company applied for leave to

appeal.

7.4.1.4.4. On May 2020, the Company was granted leave to

appeal to the Labour Appeal Court.

7.4.2. Suspension and Cancellation of Contracts:

7.4.2.1. Section 136 (2) (2) of the Companies Act authorises the BRPs during

Business Rescue to entirely, partially or conditionally suspend, for the

duration of the business rescue proceedings, any obligation of the

Company that arises under an agreement to which that the Company

was a party at the Commencement Date and would otherwise

become due during the Business Rescue.

7.4.2.2. The BRPs suspended the Company’s obligations in terms of some of

the aircraft lease agreements concluded with Lessors, as detailed in

paragraph [], whereafter the Lessors exercised their contractual

rights to begin termination proceedings on the applicable lease

agreements.

7.4.2.3. The BRPs also suspended certain of the Company’s obligations and

cancelled certain contracts concluded by the Company prior to the

Commencement Date in terms of section 136 (2) of the

Companies Act or in accordance with the terms of the respective

contracts.

7.4.3. Investigation into the affairs of the Company

In terms of section 141 (1) (c) of the Companies Act, the BRPs must investigate

the Company’s affairs, business, property and financial situation. This is dealt

with further under the review of procurement contracts in paragraph36.

7.4.4. General:

The BRPs were required to engage attorneys to advise on, inter alia, issues

relating to employment, Tax, regulatory issues, contractual disputes, PCF, post-

commencement agreements, the Proposed Restructure, Claims against the

Company and various issues arising out of the Business Rescue.

7.5. BUSINESS RESCUE INITIATIVES

7.5.1. The Proposed Restructure

7.5.1.1. The BRPs, together with the Advisors and Management, conducted

an objective assessment of the Company and evaluated various

business rescue scenarios to optimise the Company’s business

model, flight network and cost base.

7.5.1.2. Pursuant to conducting the aforesaid assessment and evaluation,

and after consultation with the Government, the BRPs developed a

proposal to restructure the Company’s affairs, business, property,

debt and other liabilities, and equity in a manner that would maximise

the likelihood of the Company continuing in existence on a solvent

basis.

7.5.1.3. The details of the Proposed Restructure are set out in paragraph57.

7.5.2. Post-Commencement Finance

7.5.2.1. On 7 December 2019, the PCF Bank Lenders granted a PCF

revolving credit facility to the Company in the amount of

R2 000 000 000.00 (two billion Rand) (which debt is secured by

Government Guarantees in favour of the PCF Bank Lenders).

7.5.2.2. On 27 January 2020, DBSA granted a PCF term loan facility to the

Company in the amount of R3 500 000 000.00 (three billion five

hundred million Rand) (which debt is secured by a Government

Guarantee in favour of DBSA).

7.5.3. Government Funding and Guarantees

7.5.3.1. In terms of the 2020 Budget Speech, Government has allocated an

amount of R16.4 billion to the Company in order to repay Lenders

who are secured by way of the Guarantees for legacy debt, PCF and

the applicable interest, as detailed in paragraph60.

7.5.3.2. Additional funding will be required for the Proposed Restructure in

order to address the working capital requirements and the

retrenchment costs.

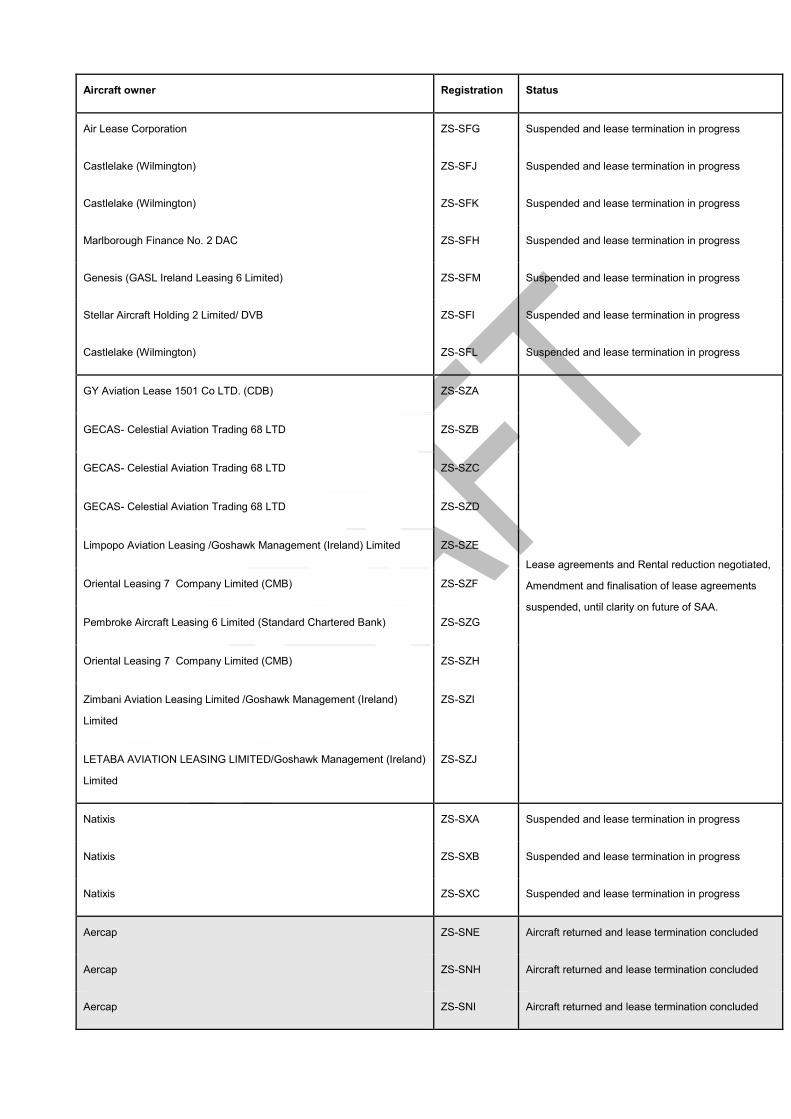

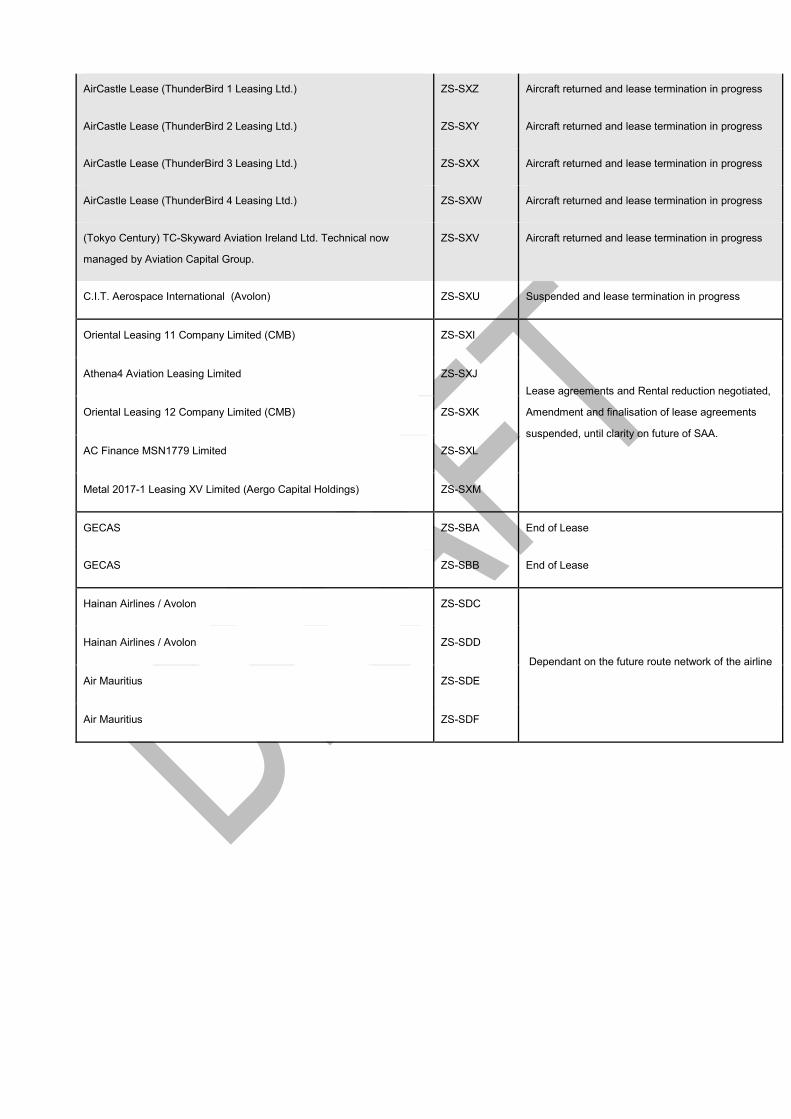

7.5.4. Lessors and Fleet Optimisation

7.5.4.1. In order to address liquidity constraints, the BRPs negotiated

deferred payments with the Lessors in terms of which:

7.5.4.1.1. Lessors were paid 50% of the amounts due to them

since the Commencement Date on

31 December 2019 and the remaining 50% was paid

on 15 January 2020;

7.5.4.1.2. Lessors were, and continued to be, paid on a weekly

basis from 1 February 2020 until end of March 2020.

7.5.4.2. The BRPs then proceeded to identify which aircraft are necessary for

the Business and issued suspension notices to the Lessors of those

aircraft which are not necessary for the Business going forward.

7.5.4.3. Pursuant to the aforesaid suspension notices, certain lessors opted

to terminate their agreements as detailed in annexure [].

7.5.4.4. The negotiated lease agreements will take effect after the Adoption

Date.

7.5.4.5. The aforesaid actions will result in substantial savings of aircraft lease

charges to the Company.

7.5.5. Cash Conservation and Management Office

7.5.5.1. The BRPs established a Cash Conservation and Management Office

(“CCMO”).

7.5.5.2. The role of the CCMO is to:

7.5.5.2.1. enforcement of discipline to optimise cash resources

through review and authorisation of all

expenses/costs excluding costs related to fuel and

leasing of aircrafts;

7.5.5.2.2. holistic monitoring of the cash resources to ensure

that there is sufficient liquidity for the execution of

critical operations;

7.5.5.2.3. ;

7.5.5.2.4. ensure that the allocation of cash flow within the

Company yields the most optimal results for the

Company;

7.5.5.2.5. identify and implement real time cost reduction

opportunities;

7.5.5.2.6. identify and eliminate costs not necessary for the

safe and efficient day-to-day operations of the

Company; and

7.5.5.2.7. review and approve the Company’s daily cash run

prior to payment execution.

7.5.5.3. All expenditure, whether previously provided for or not, needs to be

approved by the CCMO, after compliance with the cost authorisation

procedures set out by the CCMO.

7.5.5.4. The CCMO is comprised of 10 members, mainly from the BRPs’

teams and Management, who meet every weekday.

7.5.6. Review of Procurement Contracts

7.5.6.1. The BRPs established a fleet management work stream, which

performed the following:

7.5.6.1.1. Review of all contracts for leasing of aircrafts.

7.5.6.1.2. Review of contracts for the supply of fuel.

7.5.6.2. Contracts which were deemed as not commercially viable were

cancelled and the affected Lessors were advised to take back the

aircrafts. This resulted in the return of 3 passenger aircrafts and

2 cargo aircrafts.

7.5.6.3. For the remaining aircraft, terms of the various contracts were

renegotiated with a particular focus on the lease charges which

resulted in reductions. This is dealt with in paragraph35.

7.5.6.4. The BRPs also developed a work stream to review contracts and

assess the value for money for each contract, which work stream

was responsible for the following activities:

7.5.6.4.1. Obtaining the Company’s payment records for the

period 1 March 2018 to 30 April 2019, and

performing an analysis of same.

7.5.6.4.2. Obtaining a list of suppliers from the group

procurement department.

7.5.6.4.3. Reviewing supplier contracts other than those

relating to aircraft and fuel.

7.5.6.5. The approach adopted by the team was to start by reviewing the top

twenty contracts by spend, based on the payment records for the

period 1 March 2018 to 30 April 2019. A significant number of the

contracts related to the procurement of ITS services. These

contracts were then reviewed systematically.

7.5.6.6. The team also reviewed the nature and frequency of the costs and/or

expenditure submitted for approval at CCMO and verified same

against the contract list.

7.5.6.7. In the instances where the contracts were deemed to be priced above

the market rates, they were renegotiated with the suppliers to reduce

the costs to market rates.

7.5.6.8. In the instances where the contracts were deemed to be priced above

the market rates, and the suppliers were not amenable to a

negotiated reduction of rates to market rates, those contracts we

cancelled.

7.5.6.9. In all instances where the contracts were deemed to be prices

significantly higher than the market, those contracts were submitted

to the Special Investigating Unit for investigation for any potential

fraud and/or corruption.

7.5.6.10. During this process, it was identified that there are numerous services

that are outsourced by the Company, which, in the BRPs’ view, do

not need to be outsourced, because there is either capability to

perform those services within the Company, or, with a small capital

investment, it would be more beneficial for the Company to insource

those services. The process of insourcing these services would have

commenced at the end of March 2020.

7.5.7.

7.5.8. Stakeholder Engagement and Management

7.5.8.1. In order for the Business Rescue to succeed, it was, and remains,

imperative that the BRPs constantly engage with and manage the

various stakeholders involved in the Company’s Business Rescue.

7.5.8.2. To this extent, and in addition to what has been set out in paragraph

[] above, the BRPs have had various engagements with, inter alia:

7.5.8.2.1. DPE and National Treasury;

7.5.8.2.2. Trade Unions;

7.5.8.2.3. Regulatory authorities including the Civil Aviation

Authority, Air Services Licensing Council, IATA; and

7.5.8.2.4. Association of South African Travel Agents, other

trade partners and insurers to the travel industry.

7.5.8.3. The BRPs continue to engage with all stakeholders throughout the

Business Rescue.

7.5.9. Operational Review

7.5.9.1. The BRPs conducted an operational review of the Business and

mandated Alvarez & Marsal to provide an objective and impartial

insight into the operations of the Company. The approach that was

adopted is as follows;

7.5.9.1.1. Assuming the severe cash constraints and survival

as the key objective so as to identify a portfolio of

profitable routes to maintain SAA branded flights and

retain as may jobs as possible;

7.5.9.1.2. Applying a fact based, objective assessment of the

impacts on fleet, people and facilities;

7.5.9.1.3. Withdrawing from unprofitable routes and increase

overall SAA Group profitability;

7.5.9.1.4. Identified aircraft and routes that could be better

utilised or reassigned to increase yield and capacity.

Identify regional routes that would help increase

aircraft utilisation so as to improve overall

profitability;

7.5.9.1.5. Assess the ancillary businesses to achieve a more

viable business model with potential to attract SEPs.

7.5.9.2. The outcomes of its review as set out in paragraph [] below.

7.5.10. PFMA Application

7.5.10.1. In an attempt to expedite and facilitate critical decision making

required to effect cost-savings during the Company’s Business

Rescue, the BRPs applied to the DPE on 18 December 2019 for:

7.5.10.1.1. a partial exemption from the requirements of section

54 (2) of PFMA, and

7.5.10.1.2. an exemption from the requirements of various

clauses of the Company’s Memorandum of

Incorporation (“MoI”).

7.5.10.2. On 19 December 2019, the DPE granted the Company:

7.5.10.2.1. an exemption from the requirements of section 54 (2)

of the PFMA insofar as the following transactions are

concerned:

7.5.10.2.1.1. acquisition or disposal of a

significant shareholding in a

company;

7.5.10.2.1.2. acquisition or disposal of a

significant asset, unless the value of

the transaction exceeds R1 billion

(in the case of disposals);

7.5.10.2.1.3. commencement or cessation of a

significant business activity; and

7.5.10.2.1.4. significant change in the nature or

extent of its interest in a significant

partnership, trust, unincorporated

joint venture or similar arrangement,

7.5.10.2.2. approval to:

7.5.10.2.2.1. commence proceedings in terms of

section 189 of the LRA, to

implement any retrenchment of the

Company’s employees;

7.5.10.2.2.2. conclude voluntary severance

agreements with the Company’s

employees; and

7.5.10.2.2.3. conclude transactions covered by

clauses 3.4 and 3.5 of the

Company’s MoI.

7.5.10.3. On 26 December 2019, the Minister of Finance granted a similar

exemption due to certain conditions to Government guarantees

issued by the Minister of Public Enterprises and concurred to by the

Minister of Finance to secure debts of the Company.

7.5.10.4. This exemption was subsequently withdrawn by the Department of

Public Enterprise on xxx

7.5.11. Financial Stability of Subsidiaries

[D/N: To be updated closer to publication]

7.5.11.1. The Company’s Business Rescue had various consequences on the

Subsidiaries and various intra-group transactions were required, both

for the successful Business Rescue of the Company and in order to

sustain the financial viability of the Subsidiaries.

7.5.11.2. Pursuant to the grant of the supplementary exemption referred to in

[], [the BRPs proceeded with / intend to proceed with the

following intra-group transactions]:

7.5.11.2.1. the capitalisation of SAA Technical, Air Chefs and

Mango through subscription by the Company of

ordinary shares in these entities to ensure financial

stability during [the Proposed Restructure]; and

7.5.11.2.2. [the transfer of rights, duties, assets and/or liabilities

between the Company and the Subsidiaries as part

of the Proposed Restructure].

7.5.11.3. [The grant of the supplementary exemption will also allow the

Subsidiaries to conclude transactions and will further ensure their

financial stability and will limit the Company from having to continue

funding them post-Business Rescue. These transactions included

proceedings in terms of section 189 of the LRA and the sale / disposal

of assets to generate liquidity to fund operational costs.]

7.5.12. Route Retention and Closures

7.5.12.1. During the 2019 calendar year, only eight routes were profitable at

the C5 level (one International & seven Regional).

7.5.12.1.1. The International market (57% revenue) route losses

for FY19 were (R3,040m).

7.5.12.1.2. The Regional market (29% revenue) route losses for

FY19 were (R315m).

7.5.12.1.3. The Domestic market (14% revenue) route losses for

FY19 were (R868m).

7.5.12.2. In order to have a sustainable and profitable SAA, significant cost

reductions are required across labour, aircraft costs, maintenance,

property and supplier contracts.

7.5.12.3. Analysis showed that even by cutting costs by 25% and reducing

revenue by 10%, there were routes that still remained significantly

loss making with no option to optimise further at the C5 level and

these routes were:

7.5.12.3.1. Three of the international destinations (Hong Kong,

Munich, Sao Paulo).

7.5.12.3.2. Four of the regional destinations (Luanda, Entebbe,

Dakar and Abidjan)

7.5.12.3.3. All four of the domestic destinations (Cape Town,

Durban, Port Elizabeth and East London)

7.5.12.4. Taking account of the above and the objective of the having a

sustainable National Carrier that is independent and not reliant on

fiscal support, in the long term, the following is the proposed route

network for SAA:

7.5.12.5. [D/N: insert slide with route selection, please ensure that the

domestic routes CPT and DBN are included in the current route

network]

7.5.12.6. [D/N: we should also include the following routes that can be

brought back online post the implementation of the plan and on

a strategic basis and to be operated differently so as to minimise

the losses and eventually strive for profitability:

7.5.12.6.1. Domestic (More frequencies in Cape Town-

Durban and Port Elizabeth)

7.5.12.6.2. Regional (Blantyre, Entebbe, Gaborone,

Libreville, Luanda, Ndola)

7.5.12.6.3. International (Munich)].

7.5.13. Temporary Suspension of Flights

7.5.13.1. On 06 February 2020 the BRPs announced the suspension of all

loss-making routes with a clear objective of saving cash in the short

run in order to ensure the survival of SAA in the immediate term and

extend its cash runway until it receives the funds it requires to

restructure.

7.5.13.2. It was announced that SAA would be flying the following routes in

light of its current cash position:

7.5.13.2.1. International Routes:

7.5.13.2.1.1. New York;

7.5.13.2.1.2. Washington via Accra;

7.5.13.2.1.3. Perth;

7.5.13.2.1.4. Frankfurt; and

7.5.13.2.1.5. London.

7.5.13.2.2. Regional Routes:

7.5.13.2.2.1. Mauritius;

7.5.13.2.2.2. Dar es Salaam;

7.5.13.2.2.3. Victoria Falls;

7.5.13.2.2.4. Lagos;

7.5.13.2.2.5. Maputo;

7.5.13.2.2.6. Harare;

7.5.13.2.2.7. Lusaka;

7.5.13.2.2.8. Lilongwe;

7.5.13.2.2.9. Windhoek;

7.5.13.2.2.10. Kinshasa; and

7.5.13.2.2.11. Nairobi.

7.5.13.2.3. Domestic Route:

7.5.13.2.3.1. Cape Town

7.5.13.3. Re-assessment of routes

7.5.13.3.1. Subsequent to the announcement and with the

progress of the business rescue process, new

information came to light which allowed BRPs to re-

evaluate their decision on the routes going forward.

Some of the new information included:

7.5.13.3.1.1. A number of the lessors having

since committed to the reduction of

their aircraft lease costs subject to

the approval of the Business

Rescue Plan by the creditors and

lenders;

7.5.13.3.1.2. The cost reduction initiatives started

under the business rescue process

started bearing fruit;

7.5.13.3.1.3. The initiation of the section 189

process was intended to reduce

headcount and revise terms and

conditions of employment, which

would go a long way in the reduction

of both route and overhead costs.

7.5.13.3.2. The Company is also working on a structured plan

for the re-instatement of any one of routes which

become profitable after taking into account the

effects of a broader revenue enhancement strategy

and implementation of the BR Plan.

7.5.13.4.

7.5.14. Ad hoc arrangements

7.5.14.1. As mentioned above, the Company licenses its airline code on two

feeder airlines, namely, SA Express and SA Airlink.

7.5.14.2. The BRPs negotiated ad hoc arrangements with SA Express and

SA Airlink in respect of those tickets which were purchased through

the Company’s airline code and flown after the Commencement

Date.