Embed Size (px)

Citation preview

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarket

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

1/ 126

International FinanceLectures

c.econ.sc.Alexander Borochkin

2018

International Finance

c.econ.sc.Alexander Borochkin

LiteratureManualsLegislatureInternet resources

The Foreign ExchangeMarket

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

2/ 126

Manuals

Claessens S., Kose M. A., Laeven L., Valencia F.Financial Crises: Causes, Consequences, and PolicyResponses..Washington D.C.: Intl Monetary Fund, 2014. 635 pages.

Madura J.International Financial Management.USA: Cengage Learning, 2011. 736 pages.

Melvin M.International Money and FinanceOxford, Academic Press, 2012. 336 pages.

Shapiro A. C.Multinational Financial ManagementHoboken, New Jersey: Wiley, 2009. 784 pages.

International Finance

c.econ.sc.Alexander Borochkin

LiteratureManualsLegislatureInternet resources

The Foreign ExchangeMarket

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

3/ 126

Legislature

Federal Law «On currency regulation and currencycontrol» dated 10.12.2003 173-FZ (amended12.03.2014 33-FZ) // SPS Konsul’tantPljus. URL:http://www.consultant.ru.

International Finance

c.econ.sc.Alexander Borochkin

LiteratureManualsLegislatureInternet resources

The Foreign ExchangeMarket

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

4/ 126

Internet resources I

MetaTrader 4. Trading Platform.URL: http://www.metaquotes.net/ru.

Vedomosti [Electronic resource]: newspaper.URL: http://www.vedomosti.ru/.

Kommersant [Electronic resource]: newspaper.URL:http://www.kommersant.ru/daily/.

World Economy and International Relations[Electronic resource]: scientific journal.URL:http://www.imemo.ru.

Financial Times [Electronic resource]: newspaper.URL:http://www.ft.com/home/uk.

International Finance

c.econ.sc.Alexander Borochkin

LiteratureManualsLegislatureInternet resources

The Foreign ExchangeMarket

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

5/ 126

Internet resources II

New York Times [Electronic resource]: newspaper.URL:http://www.nytimes.com/.

Wall Street Journal [Electronic resource]:newspaper.URL:http://europe.wsj.com/home-page.

International Monetary Fund [Electronic resource]:official site.URL:http://www.imf.org/external/russian/index.htm.

World Bank [Electronic resource]: official site.URL:http://web.worldbank.org.

World Trade Organization [Electronic resource]:official site.URL:http://www.wto.org/.

International Finance

c.econ.sc.Alexander Borochkin

LiteratureManualsLegislatureInternet resources

The Foreign ExchangeMarket

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

6/ 126

Internet resources III

United Nations (UN) [Electronic resource]: officialsite.URL:http://www.unrussia.ru/public.html.

United Nations Industrial DevelopmentOrganization (UNIDO) [Electronic resource]:official site.URL:http://www.unido.org.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

7/ 126

Content

1. The Foreign Exchange Market1.1 Forex definition1.2 International Market participants1.3 Financial centres1.4 Currency quote1.5 Long and short positions1.6 Currency Arbitrage1.7 Short-term and Long-term Forex Movements1.8 Russian forex market

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

7/ 126

Foreign Exchange Market definition

The foreign exchange market

is a place where large commercial banks tradeforeign-currency-denominated deposits with eachother. The foreign exchange market (forex, FX, orcurrency market) is a global decentralized market forthe trading of currencies. This includes all aspects ofbuying, selling and exchanging currencies at current ordetermined prices.

The modern foreign exchange market began formingduring the 1970s after three decades of governmentrestrictions on foreign exchange transactions.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

8/ 126

The foreign exchange marketcharacteristics

huge trading volume representing the largestasset class in the world leading to high liquidity;geographical dispersion;continuous operation: 24 hours a day exceptweekends, i.e., trading from 22:00 GMT onSunday (Sydney) until 22:00 GMT Friday (NewYork);the variety of factors that affect exchange rates;the low margins of relative profit compared withother markets of fixed income;the use of leverage to enhance profit and lossmargins with respect to account size.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

8/ 126

The foreign exchange marketcharacteristics

huge trading volume representing the largestasset class in the world leading to high liquidity;geographical dispersion;continuous operation: 24 hours a day exceptweekends, i.e., trading from 22:00 GMT onSunday (Sydney) until 22:00 GMT Friday (NewYork);the variety of factors that affect exchange rates;the low margins of relative profit compared withother markets of fixed income;the use of leverage to enhance profit and lossmargins with respect to account size.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

8/ 126

The foreign exchange marketcharacteristics

huge trading volume representing the largestasset class in the world leading to high liquidity;geographical dispersion;continuous operation: 24 hours a day exceptweekends, i.e., trading from 22:00 GMT onSunday (Sydney) until 22:00 GMT Friday (NewYork);the variety of factors that affect exchange rates;the low margins of relative profit compared withother markets of fixed income;the use of leverage to enhance profit and lossmargins with respect to account size.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

8/ 126

The foreign exchange marketcharacteristics

huge trading volume representing the largestasset class in the world leading to high liquidity;geographical dispersion;continuous operation: 24 hours a day exceptweekends, i.e., trading from 22:00 GMT onSunday (Sydney) until 22:00 GMT Friday (NewYork);the variety of factors that affect exchange rates;the low margins of relative profit compared withother markets of fixed income;the use of leverage to enhance profit and lossmargins with respect to account size.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

8/ 126

The foreign exchange marketcharacteristics

huge trading volume representing the largestasset class in the world leading to high liquidity;geographical dispersion;continuous operation: 24 hours a day exceptweekends, i.e., trading from 22:00 GMT onSunday (Sydney) until 22:00 GMT Friday (NewYork);the variety of factors that affect exchange rates;the low margins of relative profit compared withother markets of fixed income;the use of leverage to enhance profit and lossmargins with respect to account size.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

8/ 126

The foreign exchange marketcharacteristics

huge trading volume representing the largestasset class in the world leading to high liquidity;geographical dispersion;continuous operation: 24 hours a day exceptweekends, i.e., trading from 22:00 GMT onSunday (Sydney) until 22:00 GMT Friday (NewYork);the variety of factors that affect exchange rates;the low margins of relative profit compared withother markets of fixed income;the use of leverage to enhance profit and lossmargins with respect to account size.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

9/ 126

The size of the Forex market

Table 2.1: Global foreign exchange market turnover,daily averages in billions of US dollars and percentages

Instrument 1998 2001 2004 2007 2010 2013

Foreign exchangeinstruments

1527 1239 1934 3324 3971 5345

Spot transactions 37% 31% 33% 30% 37% 38%Outright forwards 8% 10% 11% 11% 12% 13%Foreign exchangeswaps

48% 53% 49% 52% 44% 42%

Currency swaps 1% 1% 1% 1% 1% 1%Options and otherproducts

6% 5% 6% 6% 5% 6%

Source: Bank for International Settlements. Triennial CentralBank Survey. Report on Global Foreign Exchange MarketActivity in 2013. Basel, December, 2013.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

10/ 126

Table 2.2: Global foreign exchange market turnover by currency pair,daily averages in billions of US dollars and percentages

2001 2007 2013

USD / EUR 372 (30%) 892 (26,8%) 1289 (24,1%)USD / JPY 250 (20,2%) 438 (13,2%) 978 (18,3%)USD / GBP 129 (10,4%) 384 (11,6%) 472 (8,8%)USD / AUD 51 (4,1%) 185 (5,6%) 364 (6,8%)USD / CAD 54 (4,3%) 126 (3,8%) 200 (3,7%)USD / CHF 59 (4,8%) 151 (4,5%) 184 (3,4%)USD / OTH 199 (16%) 612 (18,4%) 213 (4%)EUR / JPY 36 (2,9%) 86 (2,6%) 147 (2,8%)EUR / GBP 27 (2,1%) 69 (2,1%) 102 (1,9%)EUR / CHF 13 (1,1%) 62 (1,9%) 71 (1,3%)EUR / OTH 20 (1,6%) 83 (2,5%) 52 (1%)

All pairs 1239 (100%) 3324 (100%) 5345 (100%)

Source: Bank for International Settlements. Triennial Central BankSurvey. Report on Global Foreign Exchange Market Activity in 2013.Basel, December, 2013.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

11/ 126

Table 2.3: Geographical distributionof global foreign exchange market turnover,2 daily averages in billions of US dollars and percentages

2004 2010 2013

United Kingdom 835 (32%) 1854 (36,8%) 2726 (40,9%)United States 499 (19,1%) 904 (17,9%) 1263 (18,9%)Singapore 134 (5,1%) 266 (5,3%) 383 (5,7%)Japan 207 (8%) 312 (6,2%) 374 (5,6%)Hong Kong SAR 106 (4,1%) 238 (4,7%) 275 (4,1%)Switzerland 85 (3,3%) 249 (4,9%) 216 (3,2%)

Total 2608 (100%) 5043 (100%) 6671 (100%)

Source: Bank for International Settlements. Triennial Central BankSurvey. Report on Global Foreign Exchange Market Activity in 2013.Basel, December, 2013.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

12/ 126

The interbank market: the largest commercialbanks and securities dealers.Commercial companies.Central banks.Hedge funds.Investment management firms.Retail foreign exchange traders.Non-bank foreign exchange companies.Money transfer/remittance companies andbureaux de change.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

12/ 126

The interbank market: the largest commercialbanks and securities dealers.Commercial companies.Central banks.Hedge funds.Investment management firms.Retail foreign exchange traders.Non-bank foreign exchange companies.Money transfer/remittance companies andbureaux de change.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

12/ 126

The interbank market: the largest commercialbanks and securities dealers.Commercial companies.Central banks.Hedge funds.Investment management firms.Retail foreign exchange traders.Non-bank foreign exchange companies.Money transfer/remittance companies andbureaux de change.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

12/ 126

The interbank market: the largest commercialbanks and securities dealers.Commercial companies.Central banks.Hedge funds.Investment management firms.Retail foreign exchange traders.Non-bank foreign exchange companies.Money transfer/remittance companies andbureaux de change.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

12/ 126

The interbank market: the largest commercialbanks and securities dealers.Commercial companies.Central banks.Hedge funds.Investment management firms.Retail foreign exchange traders.Non-bank foreign exchange companies.Money transfer/remittance companies andbureaux de change.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

12/ 126

The interbank market: the largest commercialbanks and securities dealers.Commercial companies.Central banks.Hedge funds.Investment management firms.Retail foreign exchange traders.Non-bank foreign exchange companies.Money transfer/remittance companies andbureaux de change.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

12/ 126

The interbank market: the largest commercialbanks and securities dealers.Commercial companies.Central banks.Hedge funds.Investment management firms.Retail foreign exchange traders.Non-bank foreign exchange companies.Money transfer/remittance companies andbureaux de change.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

12/ 126

The interbank market: the largest commercialbanks and securities dealers.Commercial companies.Central banks.Hedge funds.Investment management firms.Retail foreign exchange traders.Non-bank foreign exchange companies.Money transfer/remittance companies andbureaux de change.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

13/ 126

Market maker

A market maker

or liquidity provider is a company, or an individual, thatquotes both a buy and a sell price in a financial instrument orcommodity held in inventory, hoping to make a profit on thebid-offer spread, or turn.

The U.S. Securities and Exchange Commission definesa "market maker" as a firm that stands ready to buy andsell stock on a regular and continuous basis at a publiclyquoted price.A Designated Primary Market Maker (DPM) is aspecialized market maker approved by an exchange toguarantee that he or she will take the position in aparticular assigned security, option or option index

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

13/ 126

Market maker

A market maker

or liquidity provider is a company, or an individual, thatquotes both a buy and a sell price in a financial instrument orcommodity held in inventory, hoping to make a profit on thebid-offer spread, or turn.

The U.S. Securities and Exchange Commission definesa "market maker" as a firm that stands ready to buy andsell stock on a regular and continuous basis at a publiclyquoted price.A Designated Primary Market Maker (DPM) is aspecialized market maker approved by an exchange toguarantee that he or she will take the position in aparticular assigned security, option or option index

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

14/ 126

Large market makers

General forex: Barclays Bank Plc (LSE: BARC.L),JPMorgan Chase & Co (JPM), Union Bank ofSwitzerland (UBS), Mizuho Financial Group, Inc.(MHFG), Deutsche Bank AG (DBK)USD/CHF: Union Bank of Switzerland (UBS), CreditSuisse Group (CS.N).Exotic currencies: Standard Chartered Bank(STAN.L). Russian ruble: Alfabank, Sberbank ect.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

15/ 126

Financial markets information

ReutersDow JonesBloomberg

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

15/ 126

Financial markets information

ReutersDow JonesBloomberg

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

15/ 126

Financial markets information

ReutersDow JonesBloomberg

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

16/ 126

Financial centres

A financial centre

is a location that is home to a cluster of nationally orinternationally significant financial services providers such asbanks, investment managers or stock exchanges.

The International Monetary Fund definition

International Financial Centers (IFCs)—such as London,New York, and Tokyo—are large international full-servicecenters with advanced settlement and payments systems,supporting large domestic economies, with deep and liquidmarkets where both the sources and uses of funds arediverse, and where legal and regulatory frameworks areadequate to safeguard the integrity of principal-agentrelationships and supervisory functions.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

17/ 126

(a) Global Financial CentresIndex (GFCI)

(b) International FinancialCentres Development Index(IFCDI)

Figure 2.1: Financial Centres ranking

GFCI - London-based British think-tank Z/Yen, Qatar Financial Centre Authority;IFCDI - The Xinhua News Agency of China, The Chicago Mercantile Exchange andDow Jones Company of the United States.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

18/ 126

Figure 2.2: New York City’s Financial District in LowerManhattan, which includes Wall Street. Many financial firmshave expanded northward to Midtown Manhattan.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

19/ 126

Figure 2.3: The City of London is one of the oldest financialcentres and today remains at the heart of London’s financialservices industry

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

20/ 126

Figure 2.4: Frankfurt’s banking district, home of theEuropean Central Bank.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

21/ 126

Figure 2.5: The Central District of Hong Kong, one of themain financial centres in Asia

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

22/ 126

Understanding currency quote

When a currency is quoted, it is done in relation toanother currency, so that the value of one isreflected through the value of another.USD/JPY = 102.50.The base currency is set to the left of the slash,while the currency on the right is referred to as thequote or counter currency

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

22/ 126

Understanding currency quote

When a currency is quoted, it is done in relation toanother currency, so that the value of one isreflected through the value of another.USD/JPY = 102.50.The base currency is set to the left of the slash,while the currency on the right is referred to as thequote or counter currency

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

22/ 126

Understanding currency quote

When a currency is quoted, it is done in relation toanother currency, so that the value of one isreflected through the value of another.USD/JPY = 102.50.The base currency is set to the left of the slash,while the currency on the right is referred to as thequote or counter currency

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

23/ 126

Direct and indirect quote

In a direct currency quote the domestic currency isthe base currency. The direct quote varies theforeign currency, and the quoted, or domesticcurrency, remains fixed at one unit.In an indirect quote the domestic currency is thequoted currency. The domestic currency isvariable and the foreign currency is fixed at oneunit.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

23/ 126

Direct and indirect quote

In a direct currency quote the domestic currency isthe base currency. The direct quote varies theforeign currency, and the quoted, or domesticcurrency, remains fixed at one unit.In an indirect quote the domestic currency is thequoted currency. The domestic currency isvariable and the foreign currency is fixed at oneunit.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

24/ 126

U.S. dollar as a base currency in the currency pair.The Queen’s currencies: the British pound,Australian Dollar and New Zealand dollar - are allquoted as the base currency against the U.S.dollar. The euro is quoted the same way as well.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

24/ 126

U.S. dollar as a base currency in the currency pair.The Queen’s currencies: the British pound,Australian Dollar and New Zealand dollar - are allquoted as the base currency against the U.S.dollar. The euro is quoted the same way as well.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

25/ 126

Example of the currency quotes

Figure 2.6: Currency quotes example

Most currency exchange rates are quoted out to fivedigits after the decimal place, with the exception of theJapanese yen (JPY), which is quoted out to threedecimal places.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

26/ 126

Cross currency pairs

When a currency quote is given without the U.S.dollar as one of its components, this is called across currency. The most common cross currencypairs are the EUR/GBP, EUR/CHF and EUR/JPY.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

27/ 126

Bid and Ask price

When buying a currency pair (going long), the askprice refers to the amount of quoted currency thathas to be paid in order to buy one unit of the basecurrency, or how much the market will sell one unitof the base currency for in relation to the quotedcurrency.When selling a currency pair (going short) the bidprice reflects how much of the quoted currencywill be obtained when selling one unit of the basecurrency, or how much the market will pay for thequoted currency in relation to the base currency.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

27/ 126

Bid and Ask price

When buying a currency pair (going long), the askprice refers to the amount of quoted currency thathas to be paid in order to buy one unit of the basecurrency, or how much the market will sell one unitof the base currency for in relation to the quotedcurrency.When selling a currency pair (going short) the bidprice reflects how much of the quoted currencywill be obtained when selling one unit of the basecurrency, or how much the market will pay for thequoted currency in relation to the base currency.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

28/ 126

Whichever currency is quoted first (the base currency)is always the one in which the transaction is beingconducted. Operator either buys or sells the basecurrency.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

29/ 126

Spread, pips and points

The difference between the bid price and the askprice.EUR/USD = 1.25155/035, the spread would be0.00035 or 35 pips, also known as points.The pip is the smallest amount a price can movein any currency quote. In the case of the U.S.dollar, euro, British pound or Swiss franc, one pipwould be 0.00001. With the Japanese yen, onepip would be 0.001, because this currency isquoted to two decimal places.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

29/ 126

Spread, pips and points

The difference between the bid price and the askprice.EUR/USD = 1.25155/035, the spread would be0.00035 or 35 pips, also known as points.The pip is the smallest amount a price can movein any currency quote. In the case of the U.S.dollar, euro, British pound or Swiss franc, one pipwould be 0.00001. With the Japanese yen, onepip would be 0.001, because this currency isquoted to two decimal places.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

29/ 126

Spread, pips and points

The difference between the bid price and the askprice.EUR/USD = 1.25155/035, the spread would be0.00035 or 35 pips, also known as points.The pip is the smallest amount a price can movein any currency quote. In the case of the U.S.dollar, euro, British pound or Swiss franc, one pipwould be 0.00001. With the Japanese yen, onepip would be 0.001, because this currency isquoted to two decimal places.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

30/ 126

Long and short positions

A long position in a security, such as a stock or a bond, orequivalently to be long in a security, means the holder of theposition owns the security and will profit if the price of thesecurity goes up.Short selling (also known as shorting or going short) is thepractice of selling securities or other financial instrumentsthat are not currently owned, and subsequentlyrepurchasing them ("covering").Net position is the difference between total open long(receivable) and open short (payable) positions in a givenasset (security, foreign exchange currency, commodity, etc.)held by an individual. This also refers to the amount ofassets held by a person, firm, or financial institution, as wellas the ownership status of a person’s or institution’sinvestments.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

30/ 126

Long and short positions

A long position in a security, such as a stock or a bond, orequivalently to be long in a security, means the holder of theposition owns the security and will profit if the price of thesecurity goes up.Short selling (also known as shorting or going short) is thepractice of selling securities or other financial instrumentsthat are not currently owned, and subsequentlyrepurchasing them ("covering").Net position is the difference between total open long(receivable) and open short (payable) positions in a givenasset (security, foreign exchange currency, commodity, etc.)held by an individual. This also refers to the amount ofassets held by a person, firm, or financial institution, as wellas the ownership status of a person’s or institution’sinvestments.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

30/ 126

Long and short positions

A long position in a security, such as a stock or a bond, orequivalently to be long in a security, means the holder of theposition owns the security and will profit if the price of thesecurity goes up.Short selling (also known as shorting or going short) is thepractice of selling securities or other financial instrumentsthat are not currently owned, and subsequentlyrepurchasing them ("covering").Net position is the difference between total open long(receivable) and open short (payable) positions in a givenasset (security, foreign exchange currency, commodity, etc.)held by an individual. This also refers to the amount ofassets held by a person, firm, or financial institution, as wellas the ownership status of a person’s or institution’sinvestments.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

31/ 126

Short positions on the stock exchange

Figure 2.7: Short trade scheme

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

32/ 126

Sources of short interest data

Time delayed short interest data (for legally shorted shares)is available in a number of countries, including the US, theUK, Hong Kong, and Spain.The number of stocks being shorted on a global basis hasincreased in recent years for various structural reasonsMarket data providers (Data Explorers, SunGard FinancialSystems) believe that stock lending data provides a goodproxy for short interest levels (excluding any naked shortinterest).SunGard provides daily data on short interest by trackingthe proxy variables based on borrowing and lending datawhich it collects.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

32/ 126

Sources of short interest data

Time delayed short interest data (for legally shorted shares)is available in a number of countries, including the US, theUK, Hong Kong, and Spain.The number of stocks being shorted on a global basis hasincreased in recent years for various structural reasonsMarket data providers (Data Explorers, SunGard FinancialSystems) believe that stock lending data provides a goodproxy for short interest levels (excluding any naked shortinterest).SunGard provides daily data on short interest by trackingthe proxy variables based on borrowing and lending datawhich it collects.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

32/ 126

Sources of short interest data

Time delayed short interest data (for legally shorted shares)is available in a number of countries, including the US, theUK, Hong Kong, and Spain.The number of stocks being shorted on a global basis hasincreased in recent years for various structural reasonsMarket data providers (Data Explorers, SunGard FinancialSystems) believe that stock lending data provides a goodproxy for short interest levels (excluding any naked shortinterest).SunGard provides daily data on short interest by trackingthe proxy variables based on borrowing and lending datawhich it collects.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

32/ 126

Sources of short interest data

Time delayed short interest data (for legally shorted shares)is available in a number of countries, including the US, theUK, Hong Kong, and Spain.The number of stocks being shorted on a global basis hasincreased in recent years for various structural reasonsMarket data providers (Data Explorers, SunGard FinancialSystems) believe that stock lending data provides a goodproxy for short interest levels (excluding any naked shortinterest).SunGard provides daily data on short interest by trackingthe proxy variables based on borrowing and lending datawhich it collects.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

33/ 126

Selling short on the currency markets

Currencies are traded in pairs, each currencybeing priced in terms of another. In this way,selling short on the currency markets is identicalto going long on stocks.A contract is always long in terms of one mediumand short another.When the exchange rate has changed, the traderbuys the first currency again; this time he getsmore of it, and pays back the loan. Since he gotmore money than he had borrowed initially, hemakes money.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

33/ 126

Selling short on the currency markets

Currencies are traded in pairs, each currencybeing priced in terms of another. In this way,selling short on the currency markets is identicalto going long on stocks.A contract is always long in terms of one mediumand short another.When the exchange rate has changed, the traderbuys the first currency again; this time he getsmore of it, and pays back the loan. Since he gotmore money than he had borrowed initially, hemakes money.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

33/ 126

Selling short on the currency markets

Currencies are traded in pairs, each currencybeing priced in terms of another. In this way,selling short on the currency markets is identicalto going long on stocks.A contract is always long in terms of one mediumand short another.When the exchange rate has changed, the traderbuys the first currency again; this time he getsmore of it, and pays back the loan. Since he gotmore money than he had borrowed initially, hemakes money.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

34/ 126

Table 2.4: Bank trades during the day

Currency trade RE Currency position

Bought Sold Long Short

100 000 EUR 119 040 USD 1.1904 100 000 EUR 119 040 USD100 000 USD 11 785 000 JPY 117.85 100 000 USD 11 785 000 JPY122 087 USD 70 000 GBP 1.7441 122 087 USD 70 000 GBP

Net position 103 047 USD 11 785 000 JPY100 000 EUR 70 000 GBP

Table 2.5: Next day currency quotes

EURUSD 1,2023 Bank closes down long EURUSDJPY 119.1464 Bank closes down short JPY

GBPUSD 1,7371 Bank closes down short GPB

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

35/ 126

Solution

100000EUR · (1.2023 − 1.1904) = 1190USD

− 11785000JPY · (1

119.1464−

1117.85

) = 1087.74USD

− 70000GBP · (1.7371 − 1.7441) = 490USD

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

35/ 126

Solution

100000EUR · (1.2023 − 1.1904) =

1190USD

− 11785000JPY · (1

119.1464−

1117.85

) = 1087.74USD

− 70000GBP · (1.7371 − 1.7441) = 490USD

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

35/ 126

Solution

100000EUR · (1.2023 − 1.1904) = 1190USD

− 11785000JPY · (1

119.1464−

1117.85

) = 1087.74USD

− 70000GBP · (1.7371 − 1.7441) = 490USD

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

35/ 126

Solution

100000EUR · (1.2023 − 1.1904) = 1190USD

− 11785000JPY · (1

119.1464−

1117.85

) =

1087.74USD

− 70000GBP · (1.7371 − 1.7441) = 490USD

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

35/ 126

Solution

100000EUR · (1.2023 − 1.1904) = 1190USD

− 11785000JPY · (1

119.1464−

1117.85

) = 1087.74USD

− 70000GBP · (1.7371 − 1.7441) = 490USD

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

35/ 126

Solution

100000EUR · (1.2023 − 1.1904) = 1190USD

− 11785000JPY · (1

119.1464−

1117.85

) = 1087.74USD

− 70000GBP · (1.7371 − 1.7441) =

490USD

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

35/ 126

Solution

100000EUR · (1.2023 − 1.1904) = 1190USD

− 11785000JPY · (1

119.1464−

1117.85

) = 1087.74USD

− 70000GBP · (1.7371 − 1.7441) = 490USD

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

36/ 126

Currency Arbitrage

Currency arbitrage

is the practice of taking advantage of exchange ratesdifference between two or more marketsArbitrage opportunity for USD/CHF: Citibank is quoting0.8745-55. Deutsche Bank is quoting 0.8725-35.

Trader could buy USD10 mln at Deutsche Bank’soffer price of 0.8735 and simultaneously sellUSD10 mln to Citibank at their bid price of 0.8745francs.

This would earn a profit of SF0.0010 per dollartraded, or SF10,000 would be the total arbitrageprofit.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

36/ 126

Currency Arbitrage

Currency arbitrage

is the practice of taking advantage of exchange ratesdifference between two or more marketsArbitrage opportunity for USD/CHF: Citibank is quoting0.8745-55. Deutsche Bank is quoting 0.8725-35.

Trader could buy USD10 mln at Deutsche Bank’soffer price of 0.8735 and simultaneously sellUSD10 mln to Citibank at their bid price of 0.8745francs.This would earn a profit of SF0.0010 per dollartraded, or SF10,000 would be the total arbitrageprofit.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

37/ 126

Triangular arbitrage

USDCHF GBPUSD GBPCHF

New York 0,9987 1,3947

1,3929

London – 1,3947 1,3920Geneva 0,9987 – 1,3920

Table appears to have no possible arbitrage opportunity.

Computing the implicit cross rate for New York, thearbitrageur finds the implicit cross rate to beGBPCHF = 0,9987 · 1,3947 = 1,3929.Thus the cost of GBP is high in New York, and the costof CHF is low.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

37/ 126

Triangular arbitrage

USDCHF GBPUSD GBPCHF

New York 0,9987 1,3947 1,3929London – 1,3947 1,3920Geneva 0,9987 – 1,3920

Table appears to have no possible arbitrage opportunity.

Computing the implicit cross rate for New York, thearbitrageur finds the implicit cross rate to beGBPCHF = 0,9987 · 1,3947 = 1,3929.Thus the cost of GBP is high in New York, and the costof CHF is low.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

38/ 126

Short-term and Long-term ForeignExchange Movements

Causes of short-term (throughout the day) FXmovements:• inventory control;• asymmetric information effects.

In the long run, economic factors affect theexchange rate movements:• demand/ supply of foreign and domestic goods);• Government policy change;• Economic growth and inflation.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

39/ 126

Russian foreign exchange market

Moscow Exchange Group (http://moex.com) is arouble liquidity centre and the oldest regulateddomestic FX trading venue, operating since 1992.The Central Bank of the Russian Federation setsthe official RUB exchange rate based onexchange trading results. FX Market memberspost full or partial collateral to execute their trades.Trades are settled on a payment vs. paymentbasis, whereby delivery is made when a memberfulfils all of its obligations to the the NationalClearing Centre (NCC) which acts as the centralcounterparty and is responsible for centralisedclearing.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

39/ 126

Russian foreign exchange market

Moscow Exchange Group (http://moex.com) is arouble liquidity centre and the oldest regulateddomestic FX trading venue, operating since 1992.The Central Bank of the Russian Federation setsthe official RUB exchange rate based onexchange trading results. FX Market memberspost full or partial collateral to execute their trades.Trades are settled on a payment vs. paymentbasis, whereby delivery is made when a memberfulfils all of its obligations to the the NationalClearing Centre (NCC) which acts as the centralcounterparty and is responsible for centralisedclearing.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

39/ 126

Russian foreign exchange market

Moscow Exchange Group (http://moex.com) is arouble liquidity centre and the oldest regulateddomestic FX trading venue, operating since 1992.The Central Bank of the Russian Federation setsthe official RUB exchange rate based onexchange trading results. FX Market memberspost full or partial collateral to execute their trades.Trades are settled on a payment vs. paymentbasis, whereby delivery is made when a memberfulfils all of its obligations to the the NationalClearing Centre (NCC) which acts as the centralcounterparty and is responsible for centralisedclearing.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

40/ 126

Moscow Exchange offers trading in thefollowing currencies

Settlement in Russian rubles (RUB): U.S dollar(USD), euro (EUR), U.S. dollar-euro basket (BKT),Chinese yuan (CNY), Ukrainian hryvnia (UAH),Kazakh tenge (KZT), and Belarusian ruble (BYR).Settlement in U.S. dollars: Euro.

In 2013 spot trades totalled RUB 57 trln and swaptrades amounted to RUB 99 trln.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

40/ 126

Moscow Exchange offers trading in thefollowing currencies

Settlement in Russian rubles (RUB): U.S dollar(USD), euro (EUR), U.S. dollar-euro basket (BKT),Chinese yuan (CNY), Ukrainian hryvnia (UAH),Kazakh tenge (KZT), and Belarusian ruble (BYR).Settlement in U.S. dollars: Euro.

In 2013 spot trades totalled RUB 57 trln and swaptrades amounted to RUB 99 trln.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

41/ 126

Trade-weighted Exchange Rate Indexes

An exchange rate index is a weighted average of acurrency’s value relative to other currencies, withthe weights typically based on the importance ofeach currency to international trade.The Russian Central Bank calculates the valuedual-currency busket as the sum of rouble valuesof 0.55 US dollars and 0.45 euros. The roublevalue of the dual-currency basket has been theoperational indicator of the Bank of Russiaexchange rate policy since February 2005.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

41/ 126

Trade-weighted Exchange Rate Indexes

An exchange rate index is a weighted average of acurrency’s value relative to other currencies, withthe weights typically based on the importance ofeach currency to international trade.The Russian Central Bank calculates the valuedual-currency busket as the sum of rouble valuesof 0.55 US dollars and 0.45 euros. The roublevalue of the dual-currency basket has been theoperational indicator of the Bank of Russiaexchange rate policy since February 2005.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarketForex definitionInternational MarketparticipantsFinancial centresCurrency quoteLong and shortpositionsCurrency ArbitrageShort-term andLong-term ForexMovementsRussian forex market

International MonetaryArrangements

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

42/ 126

Figure 2.8: The values of the dual currency basketcalculated by The Central Bank of Russian Federation

Source: The Central Bank of Russian Federation.2016. http://www.cbr.ru/

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarket

International MonetaryArrangementsThe Gold Standardand Interwar PeriodThe Bretton WoodsAgreementFloating ExchangeRatesPlaza and LouvreAccordThe EuropeanMonetary System

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

43/ 126

Content

2. International Monetary Arrangements2.1 The Gold Standard and Interwar Period2.2 The Bretton Woods Agreement2.3 Floating Exchange Rates2.4 Plaza and Louvre Accord2.5 The European Monetary System

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarket

International MonetaryArrangementsThe Gold Standardand Interwar PeriodThe Bretton WoodsAgreementFloating ExchangeRatesPlaza and LouvreAccordThe EuropeanMonetary System

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

43/ 126

The Gold Standard: 1880 to 1914. TheInterwar Period: 1918 to 1939

Under a gold standard, currencies are valued interms of their gold equivalent (an ounce of goldwas worth USD20.67 in terms of the U.S. dollarover the gold standard period).The I World War ended Britain’s financialpreeminence.The United States had risen to the status of theworld’s dominant banker country.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarket

International MonetaryArrangementsThe Gold Standardand Interwar PeriodThe Bretton WoodsAgreementFloating ExchangeRatesPlaza and LouvreAccordThe EuropeanMonetary System

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

43/ 126

The Gold Standard: 1880 to 1914. TheInterwar Period: 1918 to 1939

Under a gold standard, currencies are valued interms of their gold equivalent (an ounce of goldwas worth USD20.67 in terms of the U.S. dollarover the gold standard period).The I World War ended Britain’s financialpreeminence.The United States had risen to the status of theworld’s dominant banker country.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarket

International MonetaryArrangementsThe Gold Standardand Interwar PeriodThe Bretton WoodsAgreementFloating ExchangeRatesPlaza and LouvreAccordThe EuropeanMonetary System

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

43/ 126

The Gold Standard: 1880 to 1914. TheInterwar Period: 1918 to 1939

Under a gold standard, currencies are valued interms of their gold equivalent (an ounce of goldwas worth USD20.67 in terms of the U.S. dollarover the gold standard period).The I World War ended Britain’s financialpreeminence.The United States had risen to the status of theworld’s dominant banker country.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarket

International MonetaryArrangementsThe Gold Standardand Interwar PeriodThe Bretton WoodsAgreementFloating ExchangeRatesPlaza and LouvreAccordThe EuropeanMonetary System

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

44/ 126

Table 3.1: Leading central bank/treasury gold reserves(inmetric tons fine gold)

Year 1845 1850 1855 1860 1865 1870 1875 1880

UK 82 104 74 78 93 161 154 170France 2 3,5 32,8 105 194 217 337 242Germany n/a n/a n/a n/a n/a n/a 43 81Italy n/a n/a n/a n/a n/a 30,8 26 22Russia n/a n/a 81 n/a 57 160 230 195USA n/a n/a n/a n/a n/a 107 87 208

Source: World Gold Council. Historical Data - Annual time serieson World Official Gold Reserves since 1845. 10th August 2011.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarket

International MonetaryArrangementsThe Gold Standardand Interwar PeriodThe Bretton WoodsAgreementFloating ExchangeRatesPlaza and LouvreAccordThe EuropeanMonetary System

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

45/ 126

Table 3.2: Leading central bank/treasury gold reserves(inmetric tons fine gold)

Year 1885 1890 1895 1900 1905 1910 1913 1915

UK 141 166 305 198 199 223 248 585France 344 370 460 544 836 952 1030 1457Germany 99 186 252 211 267 240 437 876Italy 142 133 132 115 285 350 355 397Russia 195 312 695 661 654 954 1233 1250USA 371 442 169 602 1149 1660 2293 2568

Source: World Gold Council. Historical Data - Annual time serieson World Official Gold Reserves since 1845. 10th August 2011.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarket

International MonetaryArrangementsThe Gold Standardand Interwar PeriodThe Bretton WoodsAgreementFloating ExchangeRatesPlaza and LouvreAccordThe EuropeanMonetary System

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

46/ 126

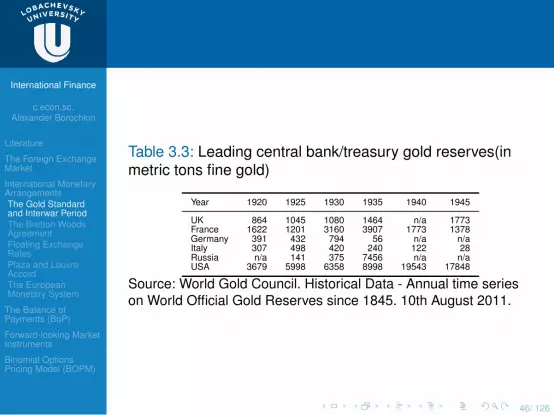

Table 3.3: Leading central bank/treasury gold reserves(inmetric tons fine gold)

Year 1920 1925 1930 1935 1940 1945

UK 864 1045 1080 1464 n/a 1773France 1622 1201 3160 3907 1773 1378Germany 391 432 794 56 n/a n/aItaly 307 498 420 240 122 28Russia n/a 141 375 7456 n/a n/aUSA 3679 5998 6358 8998 19543 17848

Source: World Gold Council. Historical Data - Annual time serieson World Official Gold Reserves since 1845. 10th August 2011.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarket

International MonetaryArrangementsThe Gold Standardand Interwar PeriodThe Bretton WoodsAgreementFloating ExchangeRatesPlaza and LouvreAccordThe EuropeanMonetary System

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

47/ 126

So a run on U.S. gold at the end of 1931 led to a15 percent drop in U.S. gold holdings. By 1933 theUnited States abandoned the gold standard.The early to mid-1930s was a period ofcompetitive devaluations and foreign exchangecontrols.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarket

International MonetaryArrangementsThe Gold Standardand Interwar PeriodThe Bretton WoodsAgreementFloating ExchangeRatesPlaza and LouvreAccordThe EuropeanMonetary System

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

47/ 126

So a run on U.S. gold at the end of 1931 led to a15 percent drop in U.S. gold holdings. By 1933 theUnited States abandoned the gold standard.The early to mid-1930s was a period ofcompetitive devaluations and foreign exchangecontrols.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarket

International MonetaryArrangementsThe Gold Standardand Interwar PeriodThe Bretton WoodsAgreementFloating ExchangeRatesPlaza and LouvreAccordThe EuropeanMonetary System

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

48/ 126

The Bretton Woods Agreement: 1944 to1973 and its breakdown

Bretton Woods agreement required each countryto fix the value of its currency in terms of ananchor currency, namely the dollar.The U.S. dollar was the key currency in thesystem, and USD1 was defined as being equal invalue to 1/35 ounce of gold.Since every currency had an implicitly defined goldvalue, through the link to the dollar, all currencieswere linked in a system of fixed exchange rates.

International Finance

c.econ.sc.Alexander Borochkin

Literature

The Foreign ExchangeMarket

International MonetaryArrangementsThe Gold Standardand Interwar PeriodThe Bretton WoodsAgreementFloating ExchangeRatesPlaza and LouvreAccordThe EuropeanMonetary System

The Balance ofPayments (BoP)

Forward-looking MarketInstruments

Binomial OptionsPricing Model (BOPM)

48/ 126

The Bretton Woods Agreement: 1944 to1973 and its breakdown