Embed Size (px)

Citation preview

Final Project Report

June 2010

Recovering Value from the 5th Quarter and Reducing Waste

ADDING VALUE TO THE SCOTTISH RED MEAT SUPPLY CHAIN

This report summarises the activities MLCSL Consulting undertook during this project and details the resultsthat have been gained by the industry. 36 Scottish abattoirs were visited to evaluate the situation as regards tothe use or disposal of 5th Quarter materials in the abattoir. The main findings were:

• Significant amounts of Category 3 and edible products were leaving the abattoir as Category 1 by-products

• The abattoirs were charged about £70 per tonne for Category 1, although some smaller companies had to pay significantly more due to the small amounts requiring collection and their remote location

• Some of the industry was aware of the market potential of the animal by-products and offals, however, few companies seemed to have the time to capitalise on these opportunities. They needed a small amount of help on markets and clarification of product specifications to enable them to prioritise their activities

• Different veterinary and MHS attitudes, standards of inspection and acceptability was apparent within differentplants causing products to be classified as Category 1

Subsequent visits to the larger abattoirs identified issues that were relevant to the whole industry and were addressedby writing the Common Topic Factsheets. A report detailing specific advice on particular issues and relevant areas ofopportunity was written for the individual abattoirs.

During the 2 years that the project has been running significant changes have been experienced by the whole industry.

• The price of stock has escalated which has meant that the processors have been “squeezed”, and forced to lookat all opportunities to remain profitable

• There has been a “rendering war” which has meant the abattoirs have had to pay less for Category 1 to be removed and are getting paid more for fat and soft bones

• The export market has remained open allowing the Scottish industry to capitalize on the low pound and the good export markets for 5th Quarter outside the UK

• More companies are harvesting headmeat, tripes, hooves and red offal and selling them for human consumption

• Increased use for human consumption of typical product used for pet food raw materials has pushed up the value of these items

All of these factors have reduced costs and increased profitability which has culminated in a benefit to the industry of approximately £15.5 million per annum.

EXECUTIVE SUMMARY

June

201

0

1

1

INTRODUCTION2

From its commencement in August 2008 to Spring 2010 the industry led ‘Added Value’ project, has worked to helpScottish abattoirs to improve the value of their 5th Quarter products and reduce their costs of waste disposal.

The project was funded by the Scottish Government and managed by an industry steering group led by Quality MeatScotland. This is the final report which summarises the activity and details all the changes that have taken place.

ADDING VALUE TO THE SCOTTISH RED MEAT SUPPLY CHAIN

June

201

0

2

The project began with an Introductory Industry Seminar to which all the companies in Scotland involved in theslaughter of cattle and sheep were invited. This outlined the existing opportunities in recovering more value from the 5th Quarter (defined as all the residual material resulting from the slaughter of cattle and sheep) other than hidesand skins, reducing waste and mitigating costs. At the time of this project the hide and skin market was very poor. The European and Far East hide market was saturated with hides and extremely quiet.

This was followed by an Assessment of the situation at all those abattoirs in Scotland interested in working with theproject, reviewing the main issues that:

• prevented their better utilisation of 5th Quarter material

• affected waste disposal

The situation throughout the Scottish industry, varied from plant to plant, but the main findings were:

• Only a few of the larger plants, demonstrated that they were both aware of many of the new developments withinthe potential markets for 5th Quarter materials (e.g. the opening up of new markets for such as tripe in the new

Eastern European member states of the EU, and were collecting, washing, polishing and packing tripe) and had mostof their waste disposal problems under control

• Most abattoirs were recovering only a proportion of their red offal (e.g. livers, which were fit for human consumption, although in many abattoirs over 50% were contaminated by liver fluke). In many cases demand forsuch products was poor and seasonal (e.g. items used in the manufacture of haggis) and some product had to beconsigned either to the lower value pet food market or even in some remote plants to the animal by-products (ABP)waste skip or landfill where they had a derogation

• There were no major pet food companies in Scotland and few were collecting for the pet food market as a resultcompetition and prices were poor

• Many readily admitted that their experiences with the instability of the markets for 5th Quarter material, coupledwith problems associated with the remote location of some Scottish abattoirs, meant that they had adopted the easy(if costly) solution of disposing a large amount of material via the ABP waste skips

• Since the onset of the BSE crisis in 1996, a lot of the skills in harvesting and processing 5th Quarter material hadbeen lost

• Some were not even opening the stomachs to empty the contents but putting all into the ABP bin and paying forits disposal

• The large majority relied on outside service companies to dispose of their waste materials (e.g. Category 1 ABP’s),and were concerned by the lack of competition in the rendering sector. The lack of options meant they were forcedto consign all such waste to Category 1, and in 2008 the disposal charges ranged typically from £70 to £95 a tonne

• Few abattoirs were trimming the heads, removing the mandible, recovering cheek meat, lips, ears etc

• Many abattoirs were getting paid for the edible fats they collected, but if they went as a Category 3 product priceswere poor

• Only a very few were beginning to harvest the more exotic offal and carcase derivatives (e.g. paddywack, pizzles,oesophagus, trachea and tendons), for which there were growing markets e.g. Far East

Final Project Report

PROJECT DEVELOPMENT3

3.1 Opportunities and Assessment

3

June

201

0

ADDING VALUE TO THE SCOTTISH RED MEAT SUPPLY CHAIN

PROJECT DEVELOPMENT3

The project proceeded to address these issues through a combination of:

1. Follow up work with all interested plants on an individual basis

2. The development of a series of facts sheets on topics of common interest sent to all abattoirs in Scotland

3. Developing the response to the major market opportunities identified for Scottish abattoirs

3.1 Opportunities and assessment (cont’d)

12 of the larger abattoirs were visited as part of this follow up work but due to the commercial nature of these discussions, detailed elements cannot be disclosed.

The follow up work with interested abattoirs utilised a range of available expertise to provided advice on specific issues such as: standard processing timings for by product activity (e.g. to identify savings in processing proceduresin gut rooms); better operation of effluent plants; abattoir and cutting plant layout to enhance the ability to harvest5th Quarter material; waste disposal options (e.g. incineration, anaerobic/aerobic digestion), better ways to emptystomach and guts; novel material usage in lairages; practices to remove and utilise more edible offals. These visits highlighted common issues affecting most of the factories, therefore the common topic fact sheets were written anddistributed to all abattoirs in Scotland.

3.2 Follow up work with individual plants

Final Project Report

Fact sheets on eight major topics of common interest were distributed to the industry during the course of the project. These were on the following subjects:

1. An industry guide to the identification of Category 1, 2 and 3 material (to coincide with the proposal being

made by waste collectors servicing Scotland to provide separate collections for Category 1 and 3 material)

2. Inspection practices to retain value of livers, hearts and cheek meat (to help plant staff and MHS staff to work

more closely together to prevent the devaluing of material)

3. Edible offal, exploiting new market opportunities and improving preparation and packing processes

4. Controlling liver fluke. A fact sheet for abattoirs to use as a feed back to farmers supplying livestock with fluke

contamination

5. Processing tripe for human consumption

6. Producing casings

7. Making better use of blood

8. Processing cattle and sheep hooves

3.3 Topics of common interest

ADDING VALUE TO THE SCOTTISH RED MEAT SUPPLY CHAIN

4

June

201

0

Final Project Report

Following on from the opportunities identified in the Introductory Industry Seminar a further Meet the Buyerseminar helped the industry to look in more detail at the overseas markets for a variety of edible offals, as well as newopportunities for casings. It concluded with an informal ‘waste swapping’ workshop, organised by the National Industrial Symbiosis programme (the visuals of the main presentations were assembled and sent out as a Supplementary Note to the Common Topic information).

A Study Tour to observe the harvesting and preparation of edible offals in Spain (a country where, similar to someother parts of the EU, some plants are doing much more to add value to 5th Quarter material than is typical in plantsin Scotland), was also undertaken by a delegation from the larger plants.

Possible opportunities for individual plants were also looked at during the follow up visits. This included the development of opportunities for the smaller plants that individually have insufficient volumes of material to capitaliseon possible market opportunities, to collaborate through the Bulking Up Material for sale (e.g. through freezing material for the pet food market).

3.4 Developing the response to the major market opportunities Identified

By the conclusion of the project a company had been identified willing to collect, from a number of plants, frozenbulked-up material for the pet food market. Information was provided to abattoirs on details and cost of the freezingequipment they would need. The project activity in this area also prompted existing collectors of “fresh material” toreconsider the service they were offering to the abattoirs especially the smaller plants.

3.4.1 Bulking up material

As the project progressed additional activity was piloted to help with the growing need of the industry to address carbon emission and other environmental issues (e.g. such as energy benchmarking).

The project also alerted the Scottish Government and industry to the development of new technology that may changethe 5th Quarter landscape in the future. This included notably the microwave treatment of blood (which is being trialled in Scotland) and the use of novel enzyme technology to turn soft offal and bone into a protein powder thatcould be used in the human food chain (with a trial plant that may be located in Scotland).

The project team also advised a number of companies interested in locating anaerobic and aerobic digesters andcomposting plants in Scotland on the potential volumes of ‘waste’ (i.e. principally lairage, stomach and intestine contents and sludges) that may be available from the Scottish abattoir industry.

3.5 Additional activity

ADDING VALUE TO THE SCOTTISH RED MEAT SUPPLY CHAIN

5

June

201

0

In Scotland there were 27 cattle abattoirs killing approximately 500,000 animals. Seven abattoirs account for over80% of the kill. While 10 abattoirs slaughter less than 2% of the total kill. The markets for offal and variety meats hadbeen increasing since the export ban had been lifted in 2006, with both the European and Far Eastern markets look-ing for further sources of low value proteins. However, few Scottish companies were exploiting the export opportu-nities to sell products that were going to the renderers.

The difference between best and worst performers in the industry was due to a number of factors of which some wereoutside the control of these businesses. In the Scottish red meat sector the larger, more economically competent businesses tend to engage actively with the renderers and export programmes. However the poorest performers tendto include a large number of small independent businesses that operate in isolation and rarely actively seek out newinformation sources or they were too small or too remote to be able to dictate terms to the renderers and “took whatwas offered”.

In summer 2008 the Scottish Industry could be split into 3 distinct groups:

• Standard practice typical of the small and remote cattle abattoirs that kill about 7.5% of the cattle

• Good practice typical of most of the medium and some of the large abattoirs

• Best practice typical of some of the larger and a few of the medium sized abattoirs

BENCHMARK OF CATTLE OFFAL AND 5TH QUARTER MATERIAL4

4.1 Overview of the industry in Summer 2008

Final Project Report

The more remote the abattoir, the less economic sense it made for them to split their wastes and, in fact, more of theanimal was wasted than harvested. Where no derogation was available, the animal by-products had to be taken significant distances for disposal; sometimes across the sea. The renderers did not differentiate in costs to disposeCategory 1 and Category 3 by-products. Hardly any company collected pet food and therefore fat, stomachs with theircontents, heads, and potential pet food products all went in the Category 1 bins. However, all abattoirs collected goodlivers, kidneys, tongues etc.

These companies were visited individually and benefited by the following advice:

• Export market opportunities for fancy meats

• Separating fat and selling it separately

• Boning the head and selling cheek meat, lips, and snouts

• Joining up with the bulking up operation for supplying to pet food collectors

• Emptying and rough washing the stomachs for pet food

4.2 Standard practice (typical of small and remote abattoirs)

ADDING VALUE TO THE SCOTTISH RED MEAT SUPPLY CHAIN

6

June

201

0

Final Project Report

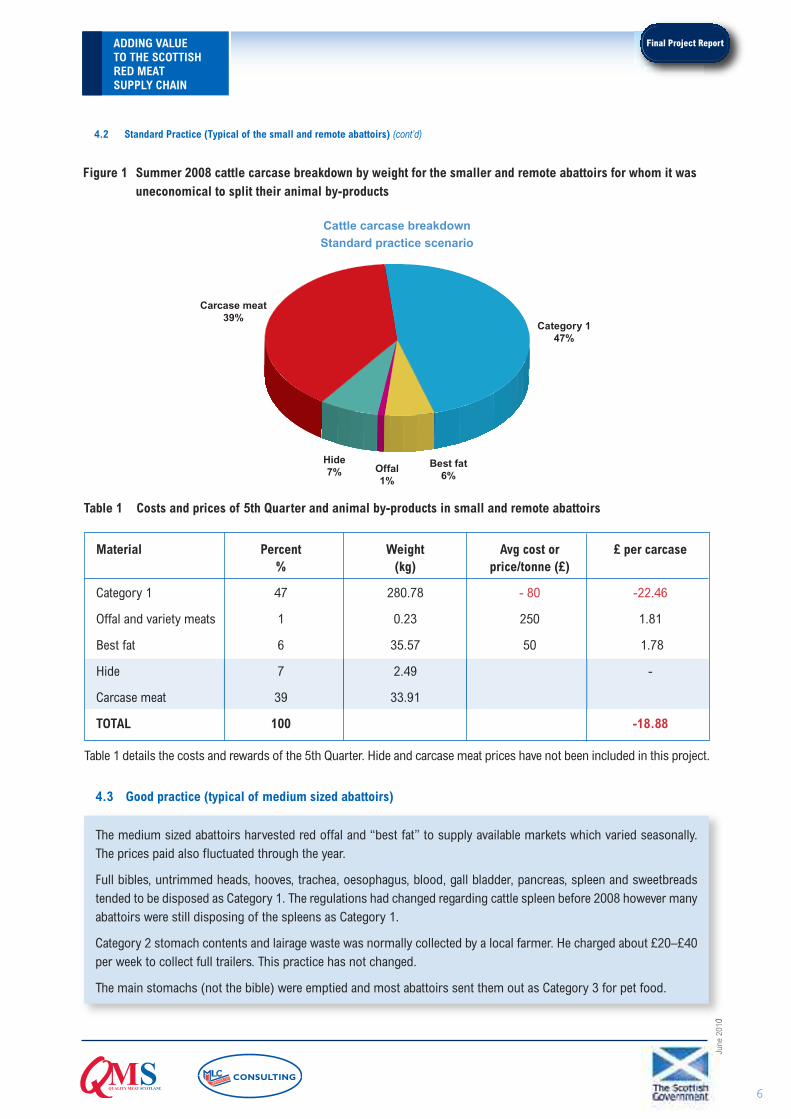

4.2 Standard Practice (Typical of the small and remote abattoirs) (cont’d)

Figure 1 Summer 2008 cattle carcase breakdown by weight for the smaller and remote abattoirs for whom it was uneconomical to split their animal by-products

Category 147%

Best fat6%

Offal1%

Hide7%

Carcase meat39%

Cattle carcase breakdown

Standard practice scenario

Table 1 Costs and prices of 5th Quarter and animal by-products in small and remote abattoirs

4.3 Good practice (typical of medium sized abattoirs)

Table 1 details the costs and rewards of the 5th Quarter. Hide and carcase meat prices have not been included in this project.

The medium sized abattoirs harvested red offal and “best fat” to supply available markets which varied seasonally. The prices paid also fluctuated through the year.

Full bibles, untrimmed heads, hooves, trachea, oesophagus, blood, gall bladder, pancreas, spleen and sweetbreadstended to be disposed as Category 1. The regulations had changed regarding cattle spleen before 2008 however manyabattoirs were still disposing of the spleens as Category 1.

Category 2 stomach contents and lairage waste was normally collected by a local farmer. He charged about £20–£40per week to collect full trailers. This practice has not changed.

The main stomachs (not the bible) were emptied and most abattoirs sent them out as Category 3 for pet food.

Material Percent Weight Avg cost or £ per carcase% (kg) price/tonne (£)

Category 1 47 280.78 - 80 -22.46

Offal and variety meats 1 0.23 250 1.81

Best fat 6 35.57 50 1.78

Hide 7 2.49 -

Carcase meat 39 33.91

TOTAL 100 -18.88

ADDING VALUE TO THE SCOTTISH RED MEAT SUPPLY CHAIN

7

June

201

0

Final Project Report

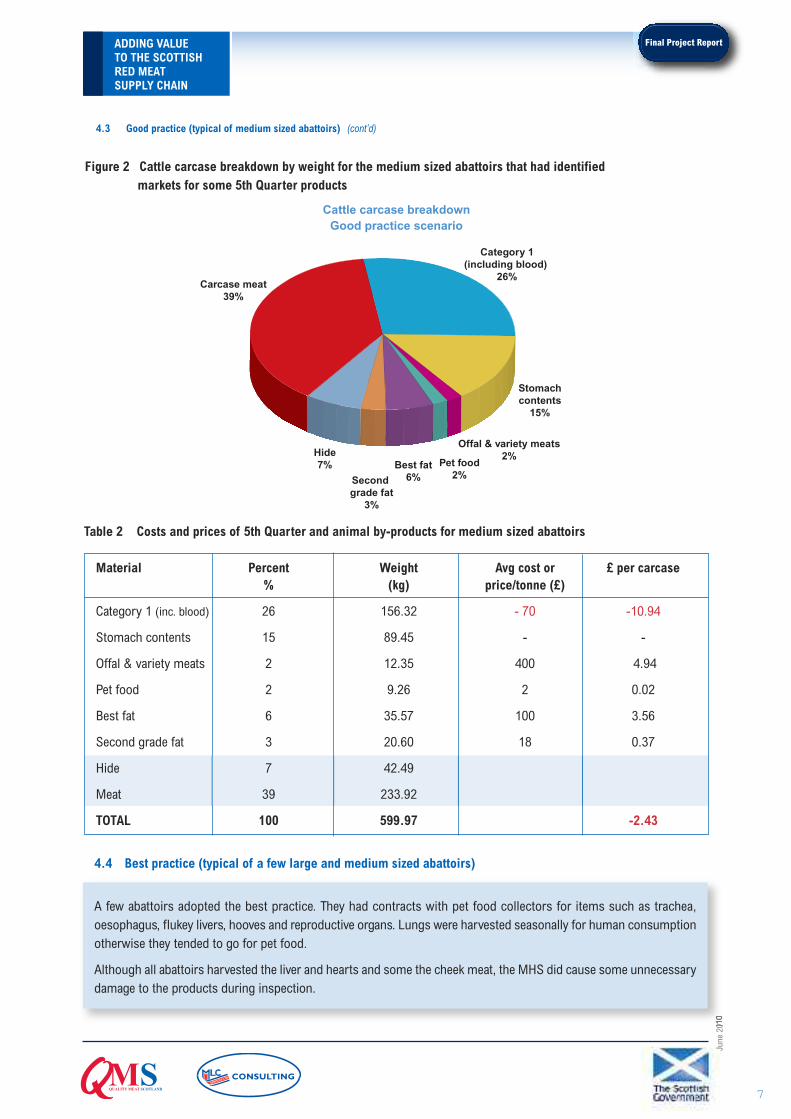

Figure 2 Cattle carcase breakdown by weight for the medium sized abattoirs that had identified markets for some 5th Quarter products

Category 1(including blood)

26%

Offal & variety meats2%Hide

7%

Carcase meat39%

Stomachcontents

15%

Pet food2%

Best fat6%Second

grade fat3%

Cattle carcase breakdownGood practice scenario

4.3 Good practice (typical of medium sized abattoirs) (cont’d)

Table 2 Costs and prices of 5th Quarter and animal by-products for medium sized abattoirs

4.4 Best practice (typical of a few large and medium sized abattoirs)

A few abattoirs adopted the best practice. They had contracts with pet food collectors for items such as trachea, oesophagus, flukey livers, hooves and reproductive organs. Lungs were harvested seasonally for human consumptionotherwise they tended to go for pet food.

Although all abattoirs harvested the liver and hearts and some the cheek meat, the MHS did cause some unnecessarydamage to the products during inspection.

Material Percent Weight Avg cost or £ per carcase% (kg) price/tonne (£)

Category 1 (inc. blood) 26 156.32 - 70 -10.94

Stomach contents 15 89.45 - -

Offal & variety meats 2 12.35 400 4.94

Pet food 2 9.26 2 0.02

Best fat 6 35.57 100 3.56

Second grade fat 3 20.60 18 0.37

Hide 7 42.49

Meat 39 233.92

TOTAL 100 599.97 -2.43

ADDING VALUE TO THE SCOTTISH RED MEAT SUPPLY CHAIN

8

June

201

0

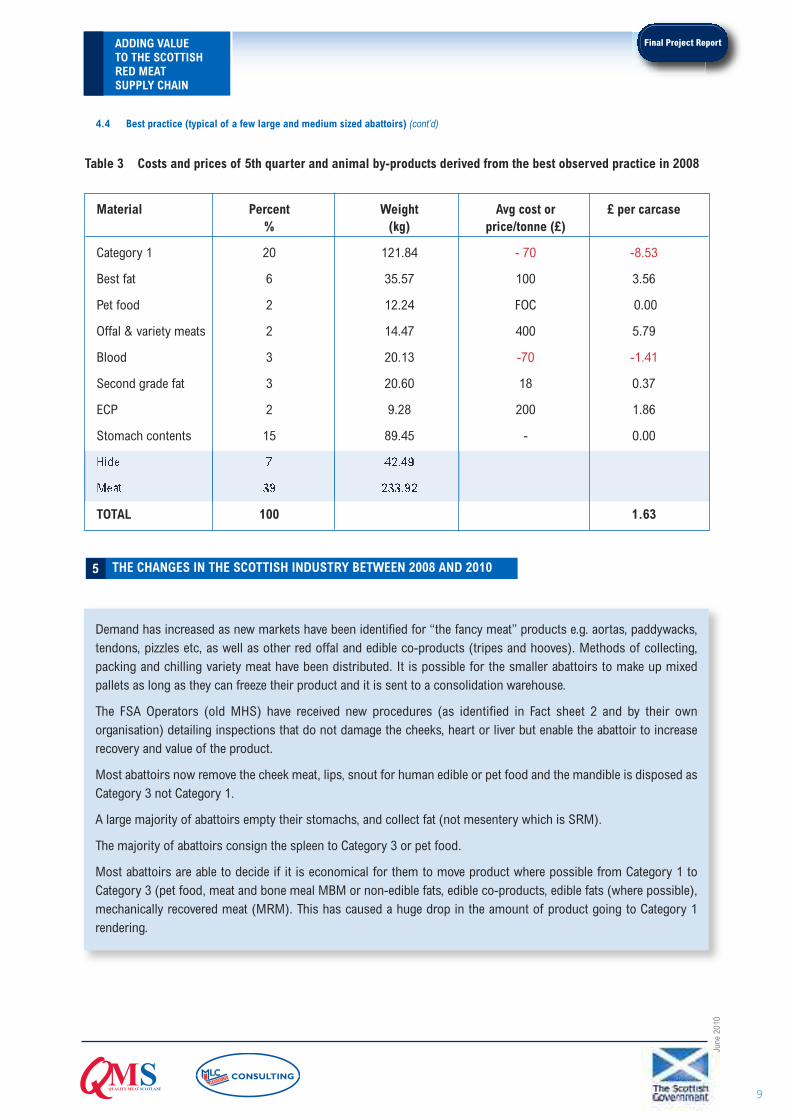

4.4 Best practice (typical of a few large and medium sized abattoirs) (cont’d)

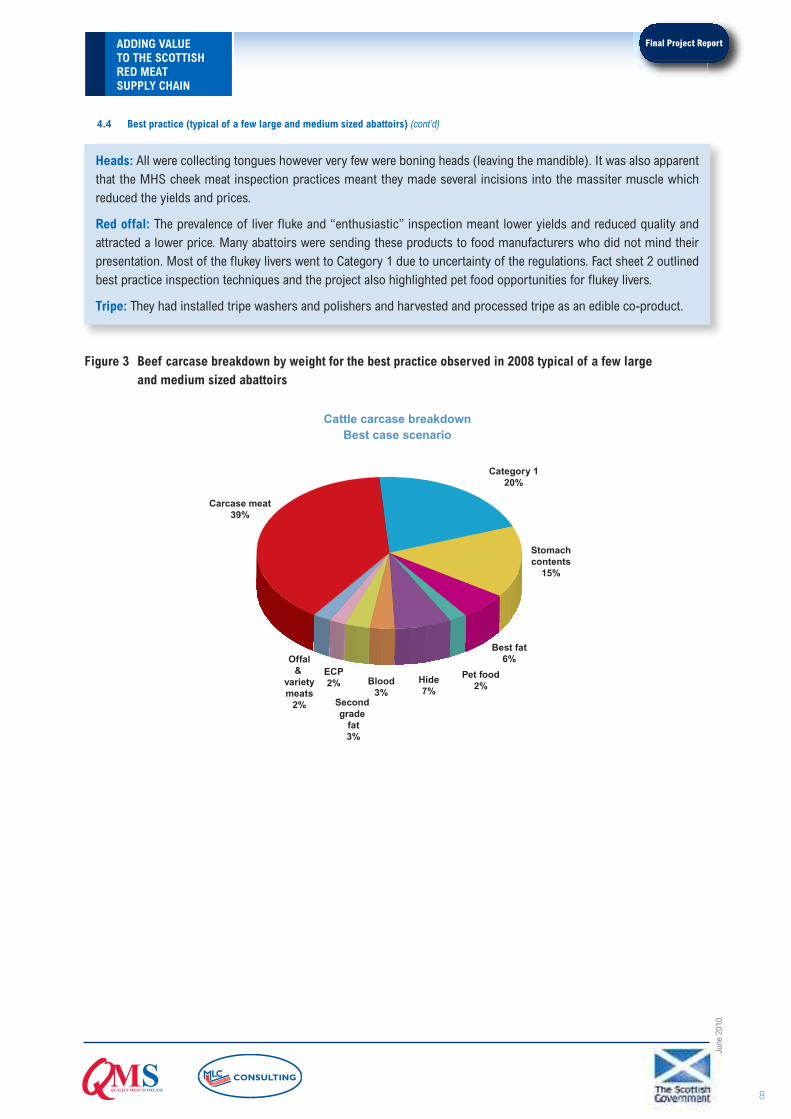

Heads: All were collecting tongues however very few were boning heads (leaving the mandible). It was also apparentthat the MHS cheek meat inspection practices meant they made several incisions into the massiter muscle which reduced the yields and prices.

Red offal: The prevalence of liver fluke and “enthusiastic” inspection meant lower yields and reduced quality and attracted a lower price. Many abattoirs were sending these products to food manufacturers who did not mind their presentation. Most of the flukey livers went to Category 1 due to uncertainty of the regulations. Fact sheet 2 outlinedbest practice inspection techniques and the project also highlighted pet food opportunities for flukey livers.

Tripe: They had installed tripe washers and polishers and harvested and processed tripe as an edible co-product.

Figure 3 Beef carcase breakdown by weight for the best practice observed in 2008 typical of a few largeand medium sized abattoirs

Category 120%

Best fat6%

Hide7%

Carcase meat39%

Stomachcontents

15%

Pet food2%Blood

3%Second grade

fat3%

ECP2%

Offal&

varietymeats

2%

Cattle carcase breakdownBest case scenario

Final Project Report

Material Percent Weight Avg cost or £ per carcase% (kg) price/tonne (£)

Category 1 20 121.84 - 70 -8.53

Best fat 6 35.57 100 3.56

Pet food 2 12.24 FOC 0.00

Offal & variety meats 2 14.47 400 5.79

Blood 3 20.13 -70 -1.41

Second grade fat 3 20.60 18 0.37

ECP 2 9.28 200 1.86

Stomach contents 15 89.45 - 0.00

Hide 7 42.49

Meat 39 233.92

TOTAL 100 1.63

ADDING VALUE TO THE SCOTTISH RED MEAT SUPPLY CHAIN

Final Project Report

9

June

201

0

4.4 Best practice (typical of a few large and medium sized abattoirs) (cont’d)

Table 3 Costs and prices of 5th quarter and animal by-products derived from the best observed practice in 2008

THE CHANGES IN THE SCOTTISH INDUSTRY BETWEEN 2008 AND 20105

Demand has increased as new markets have been identified for “the fancy meat” products e.g. aortas, paddywacks,tendons, pizzles etc, as well as other red offal and edible co-products (tripes and hooves). Methods of collecting,packing and chilling variety meat have been distributed. It is possible for the smaller abattoirs to make up mixed pallets as long as they can freeze their product and it is sent to a consolidation warehouse.

The FSA Operators (old MHS) have received new procedures (as identified in Fact sheet 2 and by their own organisation) detailing inspections that do not damage the cheeks, heart or liver but enable the abattoir to increase recovery and value of the product.

Most abattoirs now remove the cheek meat, lips, snout for human edible or pet food and the mandible is disposed asCategory 3 not Category 1.

A large majority of abattoirs empty their stomachs, and collect fat (not mesentery which is SRM).

The majority of abattoirs consign the spleen to Category 3 or pet food.

Most abattoirs are able to decide if it is economical for them to move product where possible from Category 1 to Category 3 (pet food, meat and bone meal MBM or non-edible fats, edible co-products, edible fats (where possible),mechanically recovered meat (MRM). This has caused a huge drop in the amount of product going to Category 1 rendering.

ADDING VALUE TO THE SCOTTISH RED MEAT SUPPLY CHAIN

Final Project Report

10

June

201

0

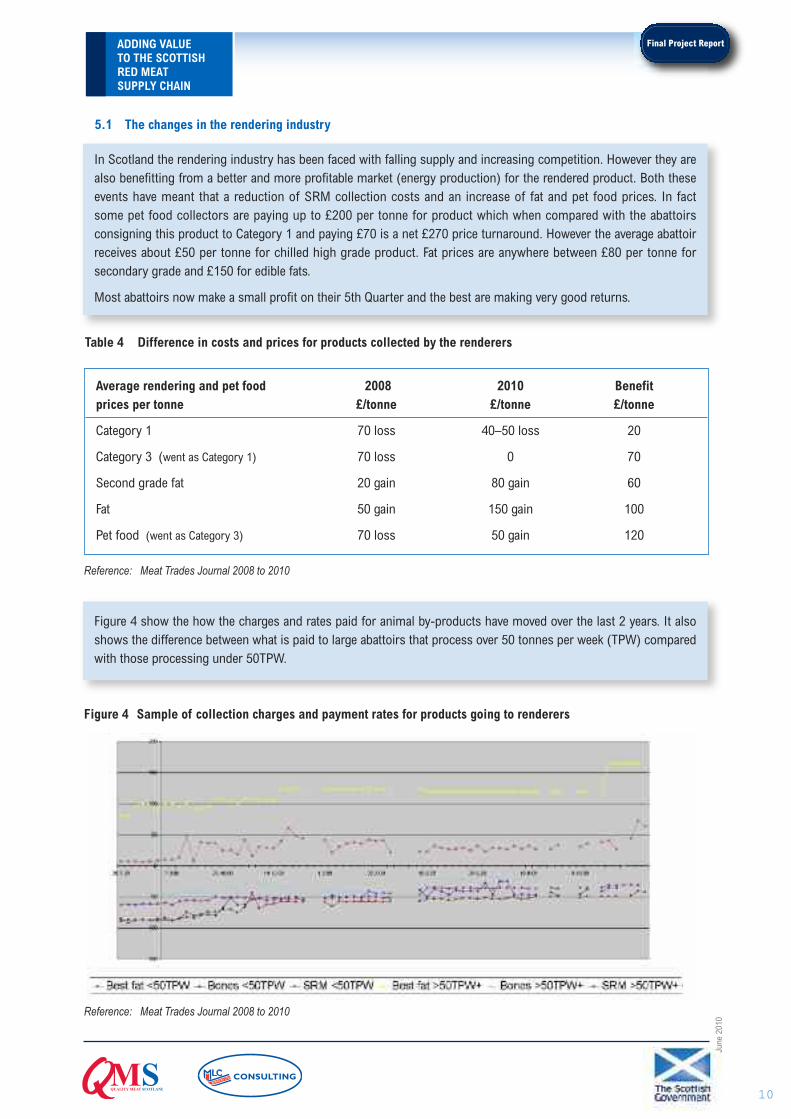

In Scotland the rendering industry has been faced with falling supply and increasing competition. However they arealso benefitting from a better and more profitable market (energy production) for the rendered product. Both theseevents have meant that a reduction of SRM collection costs and an increase of fat and pet food prices. In fact some pet food collectors are paying up to £200 per tonne for product which when compared with the abattoirs consigning this product to Category 1 and paying £70 is a net £270 price turnaround. However the average abattoirreceives about £50 per tonne for chilled high grade product. Fat prices are anywhere between £80 per tonne for secondary grade and £150 for edible fats.

Most abattoirs now make a small profit on their 5th Quarter and the best are making very good returns.

5.1 The changes in the rendering industry

Table 4 Difference in costs and prices for products collected by the renderers

Average rendering and pet food 2008 2010 Benefitprices per tonne £/tonne £/tonne £/tonne

Category 1 70 loss 40–50 loss 20

Category 3 (went as Category 1) 70 loss 0 70

Second grade fat 20 gain 80 gain 60

Fat 50 gain 150 gain 100

Pet food (went as Category 3) 70 loss 50 gain 120

Figure 4 show the how the charges and rates paid for animal by-products have moved over the last 2 years. It alsoshows the difference between what is paid to large abattoirs that process over 50 tonnes per week (TPW) comparedwith those processing under 50TPW.

Reference: Meat Trades Journal 2008 to 2010

Figure 4 Sample of collection charges and payment rates for products going to renderers

Reference: Meat Trades Journal 2008 to 2010

ADDING VALUE TO THE SCOTTISH RED MEAT SUPPLY CHAIN

Final Project Report

11

June

201

0

5.2 The best practice observed in 2010

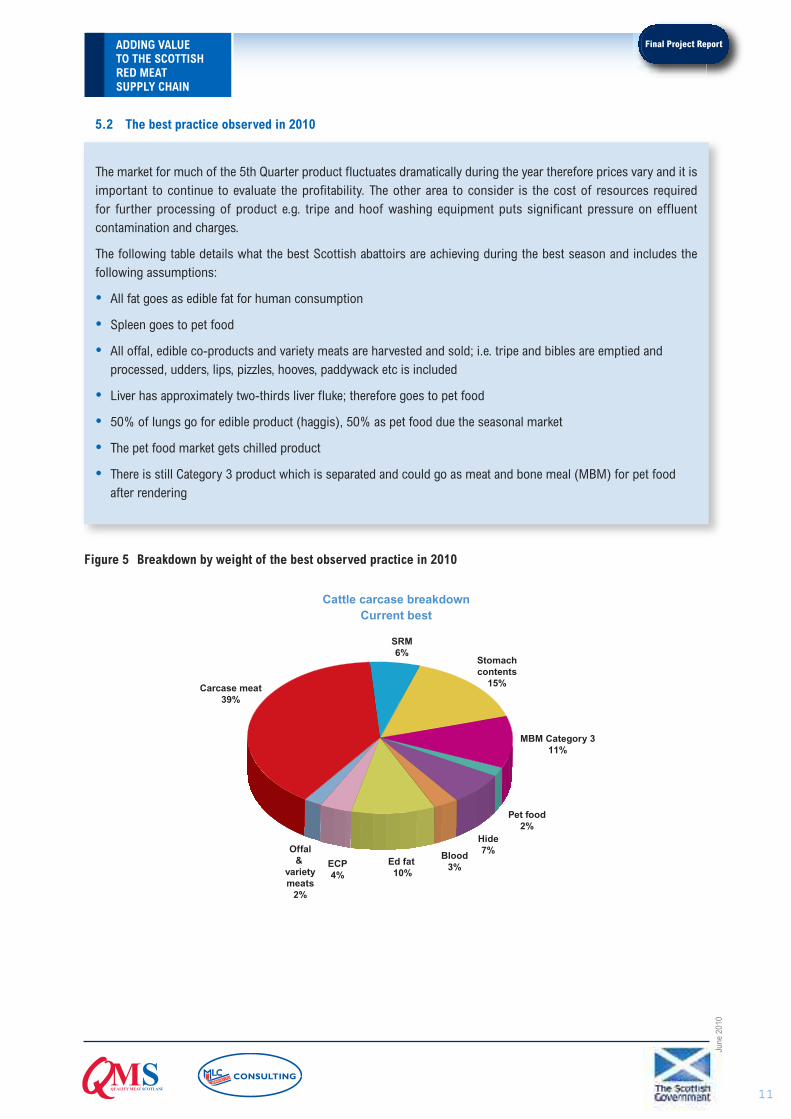

The market for much of the 5th Quarter product fluctuates dramatically during the year therefore prices vary and it isimportant to continue to evaluate the profitability. The other area to consider is the cost of resources required for further processing of product e.g. tripe and hoof washing equipment puts significant pressure on effluent contamination and charges.

The following table details what the best Scottish abattoirs are achieving during the best season and includes the following assumptions:

• All fat goes as edible fat for human consumption

• Spleen goes to pet food

• All offal, edible co-products and variety meats are harvested and sold; i.e. tripe and bibles are emptied and processed, udders, lips, pizzles, hooves, paddywack etc is included

• Liver has approximately two-thirds liver fluke; therefore goes to pet food

• 50% of lungs go for edible product (haggis), 50% as pet food due the seasonal market

• The pet food market gets chilled product

• There is still Category 3 product which is separated and could go as meat and bone meal (MBM) for pet food after rendering

Figure 5 Breakdown by weight of the best observed practice in 2010

SRM6%

Ed fat 10%

Hide7%

Carcase meat39%

Stomachcontents

15%

Pet food2%

Blood3%ECP

4%

Offal&

varietymeats

2%

MBM Category 311%

Cattle carcase breakdownCurrent best

ADDING VALUE TO THE SCOTTISH RED MEAT SUPPLY CHAIN

Final Project Report

12

June

201

0

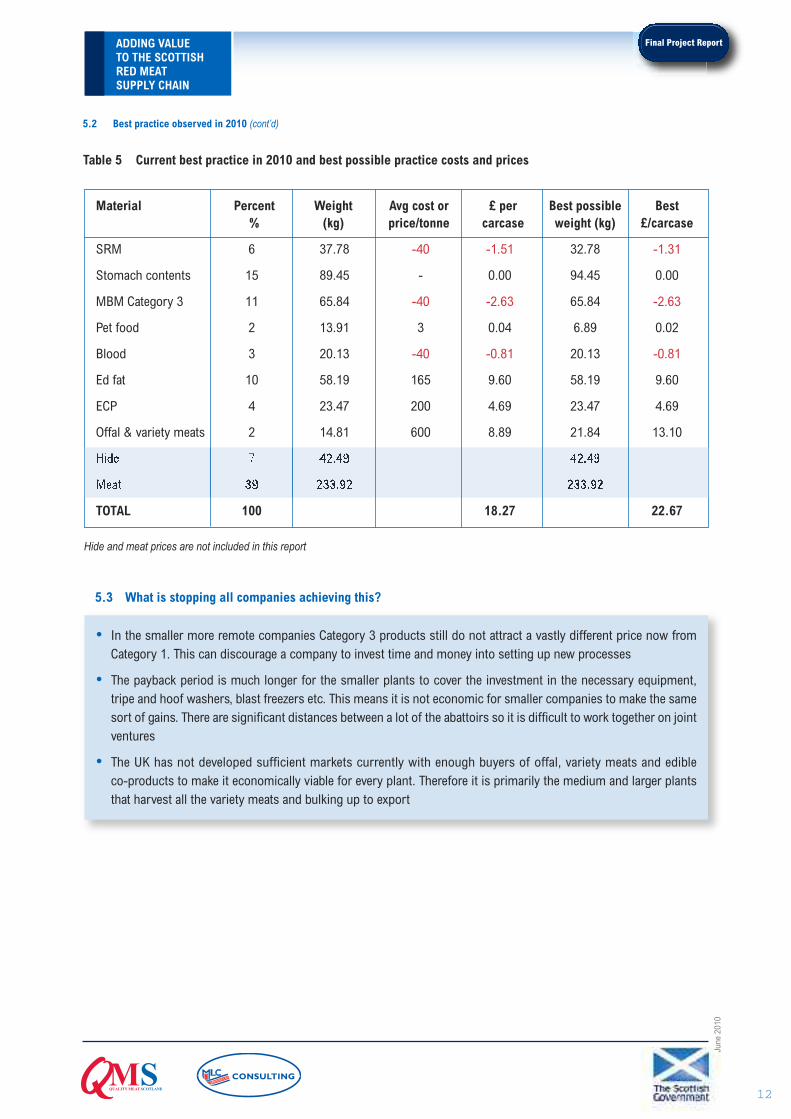

Table 5 Current best practice in 2010 and best possible practice costs and prices

Hide and meat prices are not included in this report

Material Percent Weight Avg cost or £ per Best possible Best% (kg) price/tonne carcase weight (kg) £/carcase

SRM 6 37.78 -40 -1.51 32.78 -1.31

Stomach contents 15 89.45 - 0.00 94.45 0.00

MBM Category 3 11 65.84 -40 -2.63 65.84 -2.63

Pet food 2 13.91 3 0.04 6.89 0.02

Blood 3 20.13 -40 -0.81 20.13 -0.81

Ed fat 10 58.19 165 9.60 58.19 9.60

ECP 4 23.47 200 4.69 23.47 4.69

Offal & variety meats 2 14.81 600 8.89 21.84 13.10

Hide 7 42.49 42.49

Meat 39 233.92 233.92

TOTAL 100 18.27 22.67

5.2 Best practice observed in 2010 (cont’d)

5.3 What is stopping all companies achieving this?

• In the smaller more remote companies Category 3 products still do not attract a vastly different price now fromCategory 1. This can discourage a company to invest time and money into setting up new processes

• The payback period is much longer for the smaller plants to cover the investment in the necessary equipment,tripe and hoof washers, blast freezers etc. This means it is not economic for smaller companies to make the samesort of gains. There are significant distances between a lot of the abattoirs so it is difficult to work together on jointventures

• The UK has not developed sufficient markets currently with enough buyers of offal, variety meats and edibleco-products to make it economically viable for every plant. Therefore it is primarily the medium and larger plantsthat harvest all the variety meats and bulking up to export

ADDING VALUE TO THE SCOTTISH RED MEAT SUPPLY CHAIN

Final Project Report

13

June

201

0

5.3 Further potential

On yields alone (no longer looking at changing selling prices) there is approximately a further £4.40 per carcase available.

The issues that would need to be addressed to achieve this are:

• There is a significant percentage of cattle with liver fluke especially in Western Scotland. If two thirds of the cattlehave liver fluke that reduces saleable weight by nearly 4kg per animal and fluked livers go to pet food

• The edible market for lungs is seasonal. Further markets are required to give an all round demand

• No companies in Scotland currently empty intestines. Intestinal contents are about 5kg which go as SRM. With thelow costs for disposing of SRM currently it is not economically practical to empty them

COMPANIES PROCESSING SHEEP6

Sheep abattoirs are more concentrated than the Cattle abattoirs with only 6 abattoirs (one-third of all lamb abattoirs)in Scotland killing 94% of the throughput.

Few of the abattoirs were harvesting any tripes or other fancy meats from sheep.

6.1 An overview of the industry at the start of the project in 2008

6.2 Best practice in 2008

Similarly this is only relevant in the larger abattoirs where economies of scale mean that it is practical to invest in tripewashing equipment. However, even without proper tripe washes the pet food market has become more lucrative andthey are actively looking for product.

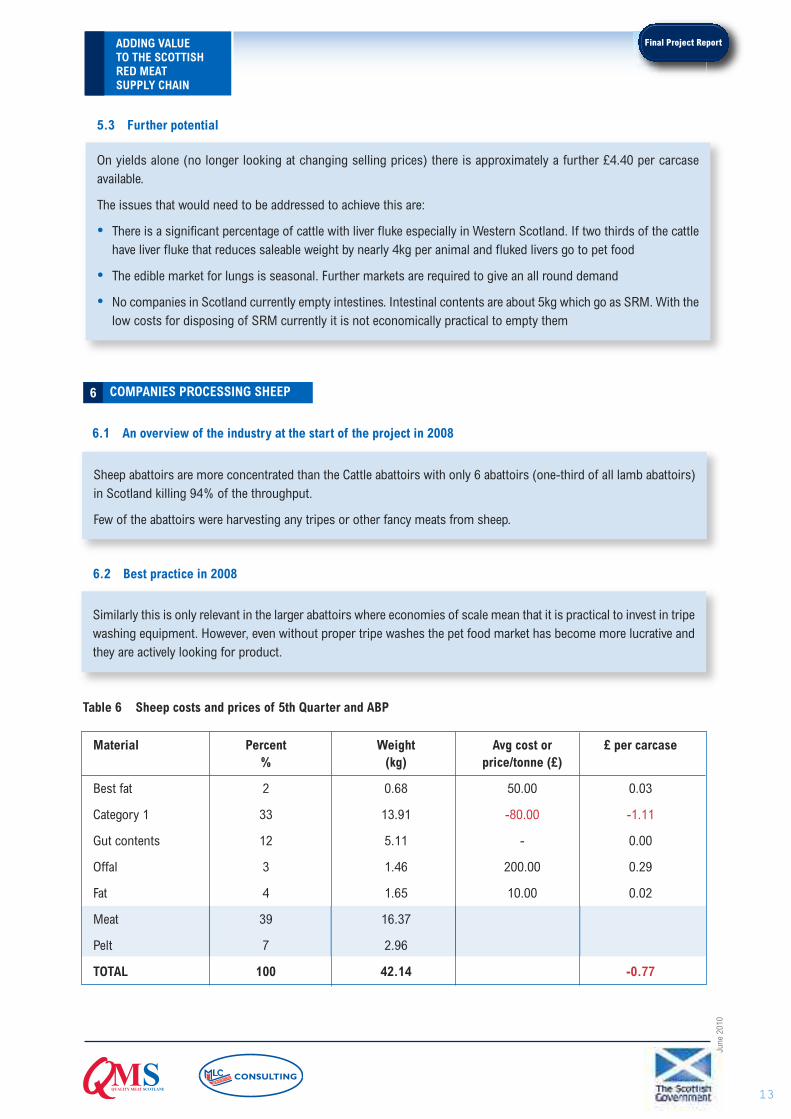

Table 6 Sheep costs and prices of 5th Quarter and ABP

Material Percent Weight Avg cost or £ per carcase% (kg) price/tonne (£)

Best fat 2 0.68 50.00 0.03

Category 1 33 13.91 -80.00 -1.11

Gut contents 12 5.11 - 0.00

Offal 3 1.46 200.00 0.29

Fat 4 1.65 10.00 0.02

Meat 39 16.37

Pelt 7 2.96

TOTAL 100 42.14 -0.77

ADDING VALUE TO THE SCOTTISH RED MEAT SUPPLY CHAIN

Final Project Report

14

June

201

0

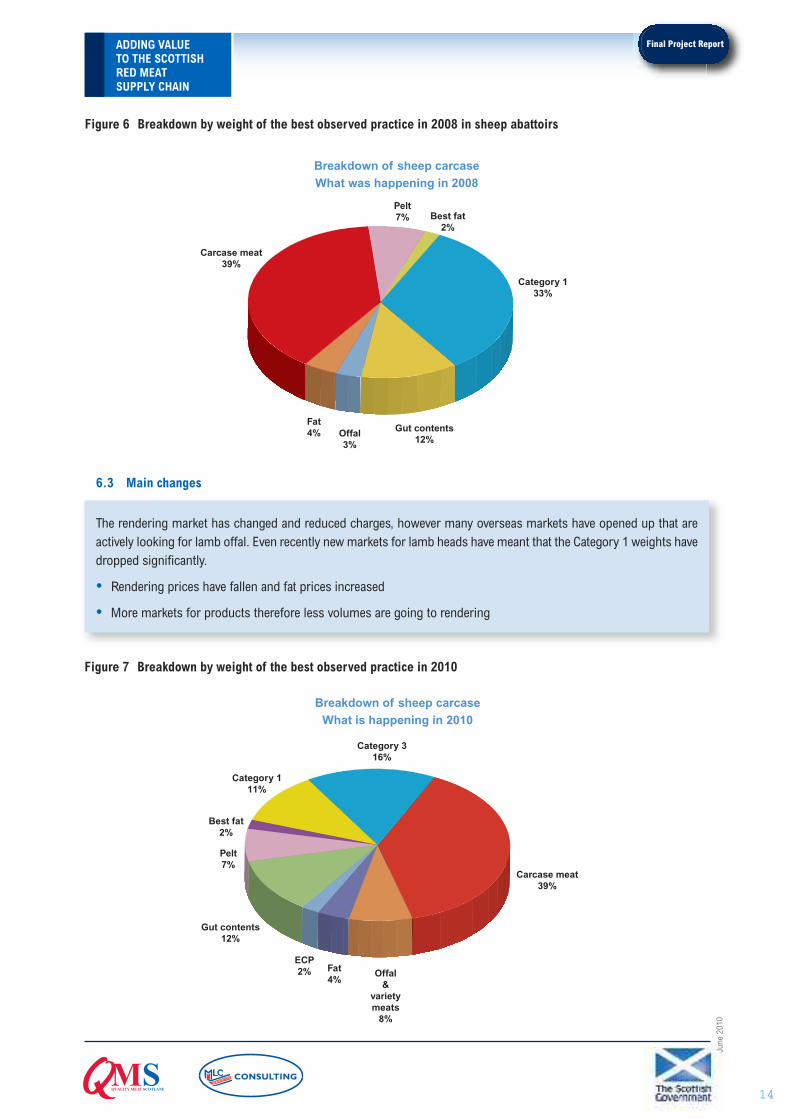

Figure 6 Breakdown by weight of the best observed practice in 2008 in sheep abattoirs

Pelt7%

Carcase meat39%

Best fat2%

Gut contents12%

Category 133%

Offal3%

Fat4%

Breakdown of sheep carcase

What was happening in 2008

6.3 Main changes

The rendering market has changed and reduced charges, however many overseas markets have opened up that are actively looking for lamb offal. Even recently new markets for lamb heads have meant that the Category 1 weights havedropped significantly.

• Rendering prices have fallen and fat prices increased

• More markets for products therefore less volumes are going to rendering

Figure 7 Breakdown by weight of the best observed practice in 2010

Pelt7%

Carcase meat39%

Best fat2%

Gut contents12%

Category 316%

Offal&

varietymeats

8%

Fat4%

Category 111%

ECP2%

Breakdown of sheep carcase

What is happening in 2010

ADDING VALUE TO THE SCOTTISH RED MEAT SUPPLY CHAIN

Final Project Report

15

June

201

0

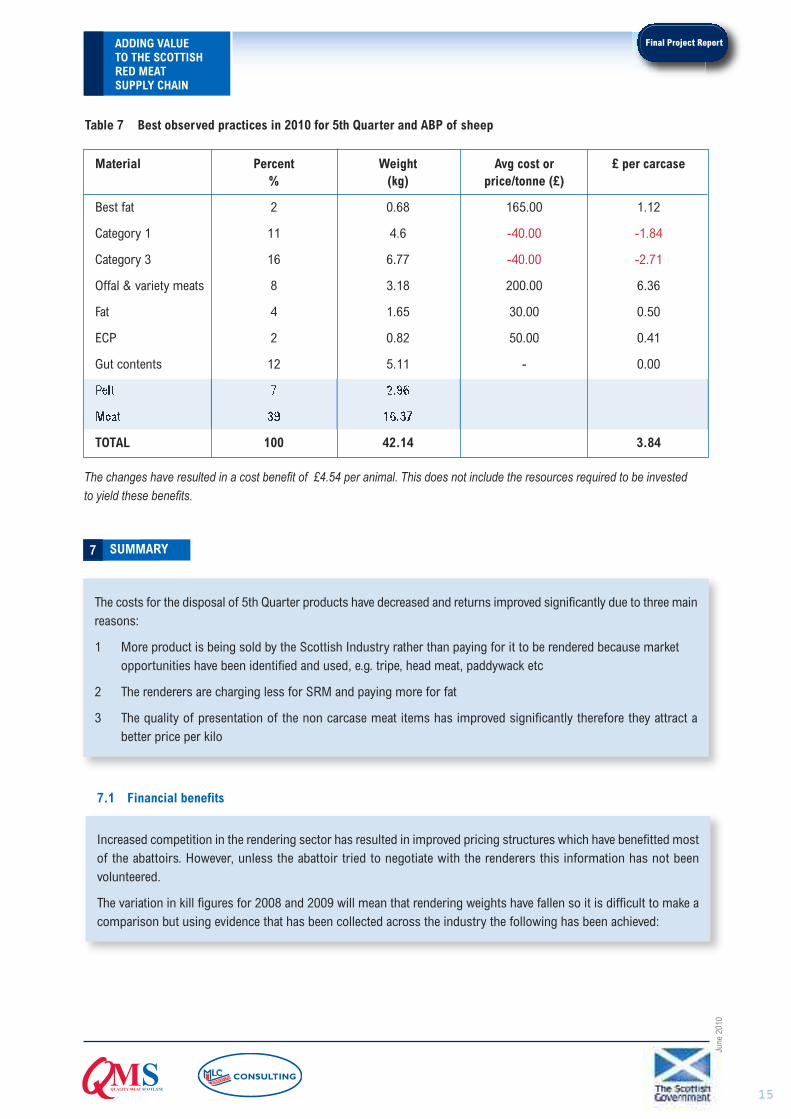

Table 7 Best observed practices in 2010 for 5th Quarter and ABP of sheep

The changes have resulted in a cost benefit of £4.54 per animal. This does not include the resources required to be invested

to yield these benefits.

Material Percent Weight Avg cost or £ per carcase % (kg) price/tonne (£)

Best fat 2 0.68 165.00 1.12

Category 1 11 4.6 -40.00 -1.84

Category 3 16 6.77 -40.00 -2.71

Offal & variety meats 8 3.18 200.00 6.36

Fat 4 1.65 30.00 0.50

ECP 2 0.82 50.00 0.41

Gut contents 12 5.11 - 0.00

Pelt 7 2.96

Meat 39 16.37

TOTAL 100 42.14 3.84

SUMMARY7

The costs for the disposal of 5th Quarter products have decreased and returns improved significantly due to three mainreasons:

1 More product is being sold by the Scottish Industry rather than paying for it to be rendered because market opportunities have been identified and used, e.g. tripe, head meat, paddywack etc

2 The renderers are charging less for SRM and paying more for fat

3 The quality of presentation of the non carcase meat items has improved significantly therefore they attract a better price per kilo

Increased competition in the rendering sector has resulted in improved pricing structures which have benefitted mostof the abattoirs. However, unless the abattoir tried to negotiate with the renderers this information has not been volunteered.

The variation in kill figures for 2008 and 2009 will mean that rendering weights have fallen so it is difficult to make acomparison but using evidence that has been collected across the industry the following has been achieved:

7.1 Financial benefits

ADDING VALUE TO THE SCOTTISH RED MEAT SUPPLY CHAIN

Final Project Report

16

June

201

0

Category 1 volumes and costs have dropped by approximately between 75% and 50%. This has reduced the cost paidto the renderers by at least 50% and in some cases nearly 80%.

Fat prices have doubled or in some cases tripled which gives the larger abattoirs more money per tonne.

Pet food companies have also started to pay for product.

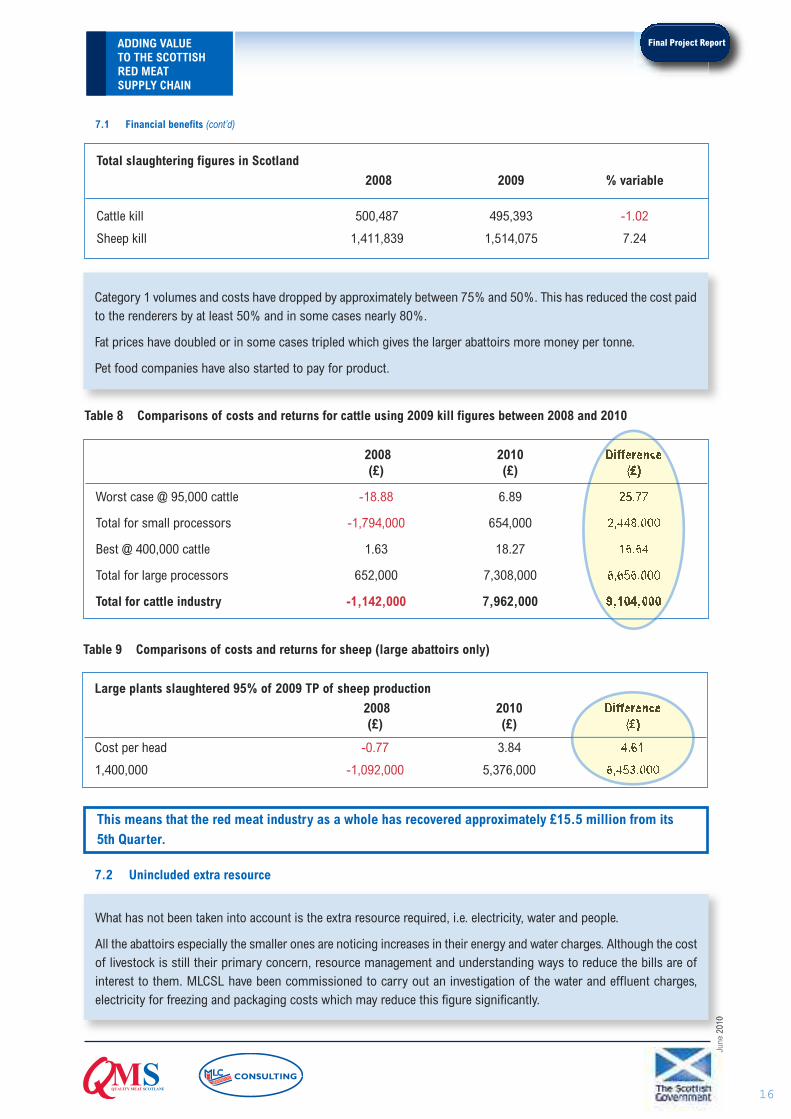

Table 8 Comparisons of costs and returns for cattle using 2009 kill figures between 2008 and 2010

7.1 Financial benefits (cont’d)

Total slaughtering figures in Scotland

2008 2009 % variable

Cattle kill 500,487 495,393 -1.02

Sheep kill 1,411,839 1,514,075 7.24

2008 2010 Difference(£) (£) (£)

Worst case @ 95,000 cattle -18.88 6.89 25.77

Total for small processors -1,794,000 654,000 2,448,000

Best @ 400,000 cattle 1.63 18.27 16.64

Total for large processors 652,000 7,308,000 6,656,000

Total for cattle industry -1,142,000 7,962,000 9,104,000

Table 9 Comparisons of costs and returns for sheep (large abattoirs only)

Large plants slaughtered 95% of 2009 TP of sheep production

2008 2010 Difference(£) (£) (£)

Cost per head -0.77 3.84 4.61

1,400,000 -1,092,000 5,376,000 6,453,000

This means that the red meat industry as a whole has recovered approximately £15.5 million from its5th Quarter.

What has not been taken into account is the extra resource required, i.e. electricity, water and people.

All the abattoirs especially the smaller ones are noticing increases in their energy and water charges. Although the costof livestock is still their primary concern, resource management and understanding ways to reduce the bills are of interest to them. MLCSL have been commissioned to carry out an investigation of the water and effluent charges,electricity for freezing and packaging costs which may reduce this figure significantly.

7.2 Unincluded extra resource

ADDING VALUE TO THE SCOTTISH RED MEAT SUPPLY CHAIN

Final Project Report

17

June

201

0

FUTURE ACTIONS8

Areas that were not thoroughly investigated during this project where potential opportunities may exist are listed below:

8.1 Further follow-up assistance

During our final interviews it was apparent that some of the smaller abattoirs were not using the new markets to reduce the weight in the SRM. The difference between best and worst performers in an industry also affects rate ofchange. The economically competent businesses tend to engage actively with KT programmes, but the poorest performers, a large number of small independent businesses tend to operate in isolation and rarely actively seek outnew information sources. It would be worth while giving each plant a further day of individual attention to bring themup to speed.

7.3 Resource management and carbon foot printing

The processing sector could look to establish a carbon footprint for the Scottish processing of beef and sheep. EBLEX,QMS and HCC are working jointly to fund some of the basic research and data collection needed for phase 2. The three organisations are also looking to fund some further detailed data collection on a 50:50 funding basis to install sub-metering into some typical processors to enable us to get a breakdown of where within the processing sector themost energy and water gets used. Action for Profits fact sheets will also be developed to pass on “top tips” to processors.

7.3.1 Objectives

• To understand energy and water use within the processing sector and how it is broken down within each plant against ELU’s or tonnes of meat produced

• To generate benchmark figures that can be used by individual processors

• To produce figures that demonstrate that the industry is taking action to reduce resource use

• To identify best practice, trial and measure the effects of best practice to reduce energy and water use and write fact sheets that can be sent out to all the meat processors

7 Summary (cont’d)

8.2 Increasing offal yields

Having worked with the abattoirs to identify different markets and better ways to make money from their offal, a morein-depth survey could be done with the abattoirs to understand current yields to human edible markets vs pet food markets through the year and understand their issues as to why they are unable to sell all of the products as human edible all of the year.

Set up an offal recovery data collection system with the larger abattoirs to understand reasons for lack of full recovery. Explore reasons such as adequate levels of trained staff, structural issues, market information, condemnations etc.

18

June

201

0

ADDING VALUE TO THE SCOTTISH RED MEAT SUPPLY CHAIN

Final Project Report

8.4 High value animal by-product opportunities and markets

Blood and leather with further processing could be a raw material for some pharmaceuticals and high value products.It could also be used as a pet food raw material. There are two areas that need further investigation to enable a comparison to be made between whether it would be viable to set-up or broker a pharmaceutical company set-up versus the opportunities in the pet food market.

Research size of total markets (volume and financials) for blood serum.

Actual cost to process these raw materials e.g. blood and collagen from hides into known high value items e.g. serumand pharmaceuticals.

8.5 Collection charges

Collection charges penalise the smaller companies significantly. During our investigations and using corroborating evidence from the MTJ it is apparent the difference is substantial. Cooperation between some of the medium sizedcompanies could yield significant benefits.

8.6 Further markets

Continue to identify and communicate opportunities in the Far East.

8.7 Opportunities that could be gained from revising the TSE regulations

There is an EU requirement that a country has to be clear for seven years before the BSE controls will be lifted, andonly then following further confirmation by the EU. This means that measures will remain and will limit the reductionand approach to conformity. There is, however, a belief that abattoirs in Europe are doing things differently. An opportunity to visit a couple of large abattoirs on the continent to review their TSE practices and compare and contrast them with those found in Scotland may highlight some different practices that enable improved profitability.

8.3 Anaerobic Digestion (AD) for effluent and blood

The industry is changing and most of the renderers are investigating the viability of building their own AD plants.Some abattoirs are very interested in investigating whether they can install their own systems. It would be beneficial to carry out a feasibility study working with interested partners e.g. municipal waste collectors, farmers, waterboards and the abattoirs etc. to explore opportunities in this area.

ADDING VALUE TO THE SCOTTISH RED MEAT SUPPLY CHAIN

Appendix 1

19

June

201

0

The current controls on Specified Risk Material are laid down in the EU TSE Regulation (EC999/2001). Over the yearsthere have been numerous changes and amendments. The latest applicable in this report was laid before the ScottishParliament and came into force 1 Jan 2009. Failure to comply with the Community legislation would leave the UK, asa member state, open to infraction proceedings by the EU Commission.

This review was undertaken by Quality Meat Scotland with funding from Scottish Government to assess the extent towhich the TSE controls are appropriate to the current levels of risk and recommend potential changes if required. This review was undertaken as a separate project by Alan Kirkwood. Within the following sections are quotes, opinions and statistics based on various studies, and meeting reports from EU, GB and other scientific agencies, linkedto statistical information on TSE result findings, and global research programmes.

A Review of Cattle and Sheep TSE Controls in Scotland

INTRODUCTION

OBJECTIVES

A Review TSE controls on cattle and sheep in abattoirs and cutting plants, including associated requirements

B Assess whether there is a continuing need for specific controls in light of progress made in eradicating BSE

C Assess whether those controls which are required need to be (or can be) adjusted or amended to reflect changes in circumstance’s since they were imposed

D Identify controls and procedures for industry to consider lobbying or action to achieve change. This should target Government and regulatory agencies

REVIEW OF CURRENT CONTROLSA

The following paragraphs give some indication to the background, and the flow of information required, ensuring thattransmissible spongiform encephalopathy’s (TSEs) agents are kept out of the food chain. The significant health effectsof TSE transfer to humans, from infected animals, has been the driver.

The current methods of controlling transmissible spongiform encephalopathy’s (TSE) are entrenched in EU legislation. The Food Standards Agency (FSA) is the Competent Authority (CA) who have ultimate responsibility andtheir highest priority is always consumer protection. Non–compliance by the Food Business Operator (FBO) triggers enforcement by the Competent Authority and failure to comply with TSE controls is an offence. The required TSE / SRMlegal controls are supported by a range of regulations and managed and policed by Food Standard Agency Operations(FSA Ops; previously the Meat Hygiene Service).

Applicable regulations:

• (EC) 999/2001 (as amended) specifies what SRM is, and that it shall be removed

• (EC) 854/2004 – specifies official controls are to verify continuous compliance with FBOs own procedures

concerning controls on SRM

• (EC) 1774/2002 – classifies SRM as Category 1 Animal By-Product and sets out the rules for its disposal.

ADDING VALUE TO THE SCOTTISH RED MEAT SUPPLY CHAIN

Appendix 1

20

June

201

0

These are transposed into Scottish law by The TSE (Scotland) Amendment (No2) 2008. FSA Ops presently operaterigidly in accordance with their Manual for Official Controls (known as the FSA Ops MOC) with TSE controls coveredby Chapter 2.7 Specified Risk Material Controls. All FSA Ops manuals are extremely detailed and very prescriptive, withOfficial Veterinarians and Meat Hygiene Inspectors expected to follow their duties and tasks to the letter, thus ensuring consistency across different sites. The existing procedures meet all the criteria as defined by law, with littleor no flexibility being permitted by FSA. Unfortunately in some plants, compliance and the operational relationshipscan vary between FSA Ops and Plant Management, depending on the levels of professionalism and the confidence ineach others capabilities.

In the case of cattle the current controls have proven effective as currently all susceptible animals show a continuingdecline in confirmed cases of BSE in the UK, this is in line with forecasted projections. Surveillance in sheep over 18months of age also shows that classical scrapie has declined and that atypical scrapie has remained relatively constant. The Veterinary Laboratories Agency (VLA) provides a summary of the statistics through active and passivesurveillance by species, which provides the ongoing evidence required under EU legislation.

ASSESSMENT OF THE NEED FOR CONTINUING CONTROLSB

The FSA indicate there are still basic breaches of SRM controls within plants. It is their role to limit any potential forthis to lead to human illness and ensure compliance with EU legislation.

It is a fact that TSE`s retain the capacity to surprise. Eradicating or limiting the damage to health and wellbeing fromTSE`s, both for humans and animals, has not been achieved yet. Science is evolving in greater detail but shows, in asmuch as there is a decline in BSE, that there is still an underlying range of possible public health concerns.

Recently identified TSE`s such as bovine amyloid spongiform encephalopathy (BASE), and atypical scrapie, whose potential to be a human health problem, are not yet fully understood. TSE diseases have a slow progression, andtherefore time is needed for the development of reliable answers to scientific questions. This makes TSE research along-term undertaking. TSE research in the UK remains a vibrant field, this research is supported by DEFRA fundingwith something in the region of £7 million being allocated to numerous projects across various Research Instituteswithin the UK. This research infrastructure has established strong international links not only within the EuropeanUnion but further afield to North America and Japan. These established contacts allow researchers to make realprogress on the various scientific models and complicated questions still needing answered.

The EU regulations dictate the protocol for the collection and control of TSE samples to ensure consistency of the dataprocessing across Member States.

The only opportunity for real change is when the levels of BSE infectivity drop or the science changes. There is an EUrequirement that a country has to be clear for seven years before the controls will be lifted, and only then followingfurther confirmation by the EU.

A Review of current controls (cont’d)

ADDING VALUE TO THE SCOTTISH RED MEAT SUPPLY CHAIN

Appendix 1

21

June

201

0

There have already been a number of amendments made to the EU TSE legislation. These have generally been technical amendments updating the detailed requirements of TSE monitoring arrangements, or in the case of scrapie,implementing a more proportionate approach to controls in line with the EU TSE Roadmap.

From an industry perspective (given the rapid decline in the number of cattle testing positive with BSE and the continuing research into atypical scrapie) it is logical to assess the species control needs separately:

Cattle

Progress has been made by FSA towards making the BSE controls for cattle more proportionate to the risk as agreedat the FSA Board Meeting in May 2009, (ref: FSA Board meeting paper 18 pages). In the case of the slaughter and handling of cattle carcases, a number of procedural changes have taken place, and continue to do so. These changeshave been fairly fluid recently, e.g. no requirements for Plant RMOP’s in specific cases, differentiating OTM (over 30month) and OFM (over 48 month) handling procedures.

Sheep

Atypical scrapie in sheep is not BSE. As yet, there is no evidence that it is harmful or can be transmitted to humans,although recently it has been shown that, like other TSE’s, it can be experimentally transmitted to mice and sheep.Through active surveillance, the vast majority of atypical cases have been identified in material submitted from agedslaughtered animals and very few clinical cases have been diagnosed. Most cases have been found in those sheep thatare genetically more resistant to classical scrapie but none have been identified in the genetically most susceptible.

The transition since January 2009, to complete FBO responsibility on detention checks for sheep and goats, appearsto have been successful. The initial pressure for a number of the TSE regulation changes being explored and negotiated came from industry but with the tight situation of Government finances, there is potential to examine theapplication of the current regulations to see whether efficiencies can be found in light of the reducing risk profile. Itwould appear outwardly to industry other Member States take a more pragmatic view and are prepared to operate ona more proportional risk basis, a hypothesis that should be investigated further.

ASSESSMENT OF THE POSSIBILITY TO ADJUST OR AMEND CONTROLSC

Industry accept that SRM controls have become a fact of life. All current TSE regulations are EU driven as describedin Section 2 under review of current controls.

BSE historical and risk status of the UK was the determining factor in many of the control measures implemented.

However, a seven year clear window in BSE is required by EU law which means that measures will remain and will limitthe reduction and approach to conformity.

1 January 2010 FCI information to be supplied to the abattoirs from supplier on all stock (cattle, sheep, calf and goat).Improved electronic recording of cattle passports will aid information flow.

IDENTIFY SPECFIC CONTROLS FOR FURTHER ATTENTIOND

ADDING VALUE TO THE SCOTTISH RED MEAT SUPPLY CHAIN

Appendix 1

22

June

201

0

Points for further explorations:

• Consider the statistic results from the surveillance programmes consult with Industry as an equal partner on specific issues

• Assist the drawing up of new guidelines on age sampling criteria by species traffic light system on enforcement in plants killing up to 48-month cattle

• Ensure prompt implementation of the measures outlined in the TSE Roadmap 2 expected to be published in July2010

• Acceptance and recognition by FSA OPS of third party external audit reports

• Changes in criteria and protocol procedures should be driven hard; the status quo is no longer an option, it is a lot of work and a costly waste of resource time

REFERENCE LIST

The reference information has been extracted from UK and EU government agencies as well as other organisations andcountries with an interest in the subjects covered in the report.

EU TSE Regulation (EC999/2001) (appendix 1)http://ec.europa.eu/food/fs/bse/legislation_en.html

Scottish Parliament (appendix 2)http://www.opsi.gov.uk/legislation/scotland/ssi2008/ssi_20080417_en_1

Spongiform Encephalopathy Advisory Committee (SEAC) (appendix 3)www.seac.gov.uk/statements/scrapiesstatement080207.pdf

European Food Safety Authority (EFSA) (appendix 4)www.efsa.europa.eu

World Organisation for Animal Health OIE (WOAH) (appendix 5)http://www.oie.int/eng/normes/mcode/en_chapitre_1.11.6.htm

World Health Organisation (WHO) (appendix 6)www.who.int

FSA OPS manual - Chapter 2.7. Specified Risk Material Controls (appendix 7)www.food.gov.uk/foodindustry/meat/FSA Opservice/FSA Opsmanual2006/

VLA (appendix 8)http://www.defra.gov.uk/vla/science/sci_tse_stats_intro.htm

EU TSE Roadmap (appendix 9)http://ec.europa.eu/food/food/biosafety/resources/publications_en.htm

FSA Board Meeting in May 2009 (appendix 10) www.food.gov.uk/multimedia/pdfs/board/fsa090505.pdf

D Identify specific controls for further attention (cont’d)