Embed Size (px)

Citation preview

MEAT AND PROTEIN ALTERNATIVESA LOOK INTO THE CURRENT AND FUTURE STATE OF MEAT, SUBSTITUTES, AND PLANT-BASED FOODS

September 2020

Contents

SECTION 1

Global landscape Growth drivers Regional zoom-in

Prospects How to win?

Understanding the historical and current

performance of meat and meat

substitutes

Page 2

Identifying the key factors stimulating

demand for meat substitutes and plant-

based foods

Page 9

A zoom-in to the largest and fastest-

growing meat substitutes markets in the

world

Page 18

Highlighting emerging developments in

meat and meat substitutes that are likely

to have an impact over the next five years

Page 24

A review of the main considerations for

businesses looking to tap into meat

substitutes

Page 31

SECTION 2 SECTION 3

SECTION 4 SECTION 5

SECTION 1

Global landscape

The global landscape

section provides an

understanding of

historical and current

trends in meat

consumption and the

current state of the

meat substitutes

market

SECTION 1

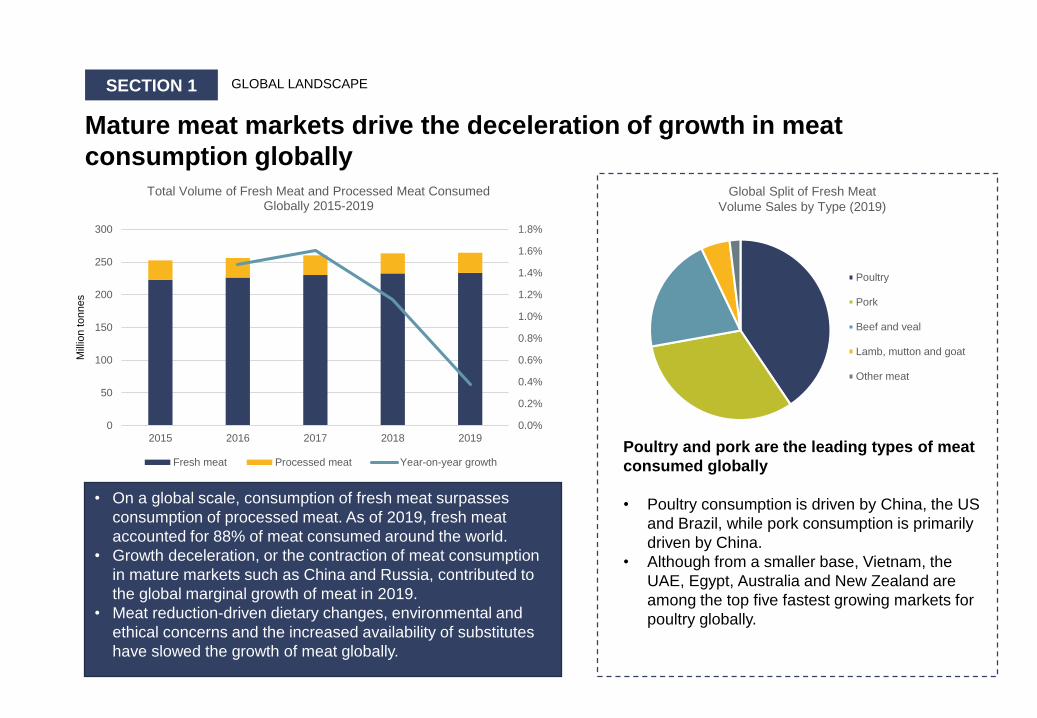

Mature meat markets drive the deceleration of growth in meat

consumption globally

GLOBAL LANDSCAPE

Poultry and pork are the leading types of meat

consumed globally

• Poultry consumption is driven by China, the US

and Brazil, while pork consumption is primarily

driven by China.

• Although from a smaller base, Vietnam, the

UAE, Egypt, Australia and New Zealand are

among the top five fastest growing markets for

poultry globally.

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

1.6%

1.8%

0

50

100

150

200

250

300

2015 2016 2017 2018 2019

Total Volume of Fresh Meat and Processed Meat Consumed Globally 2015-2019

Fresh meat Processed meat Year-on-year growth

Poultry

Pork

Beef and veal

Lamb, mutton and goat

Other meat

Global Split of Fresh Meat

Volume Sales by Type (2019)

• On a global scale, consumption of fresh meat surpasses

consumption of processed meat. As of 2019, fresh meat

accounted for 88% of meat consumed around the world.

• Growth deceleration, or the contraction of meat consumption

in mature markets such as China and Russia, contributed to

the global marginal growth of meat in 2019.

• Meat reduction-driven dietary changes, environmental and

ethical concerns and the increased availability of substitutes

have slowed the growth of meat globally.

Mill

ion tonnes

SECTION 1

Globally, China and the US are the largest consumers of fresh and

processed meat, respectively

GLOBAL LANDSCAPE

0.30.91.31.41.61.72.02.12.32.52.62.7

4.46.7

7.712.512.8

30.5

UAEMoroccoThailandAustralia

SpainUnited Kingdom

JapanItaly

FranceVietnam

South AfricaGermany

MexicoRussia

IndiaUSA

BrazilChina

Fresh Meat Retail Volume (million tonnes, 2019)

UAE

Vietnam

Morocco

Mexico

India

Fastest growing retail

markets for fresh meat

(year-on-year growth)

7.6%

4.2%

3.8%

3.2%

3.1% 0.20.20.20.20.30.30.30.30.30.4

0.60.60.70.8

1.31.3

2.44.0

ArgentinaSouth Korea

IndonesiaEgypt

CanadaBrazil

MexicoPhilippines

PolandSpainJapan

ItalyUnited Kingdom

FranceRussia

GermanyChinaUSA

Processed Meat Retail Volume (million tonnes, 2019)

India

Philippines

Russia

Thailand

Turkey

Fastest growing retail

markets for processed meat

(year-on-year growth)

8.8%

7.1%

7.1%

6.8%

6.1%

Developing markets such as India, Mexico and Vietnam are the driving forces for fresh and processed meat

• Large populations in countries such as China, Brazil and the US have been a key driver of meat consumption globally.

• However, it is developing markets that are supporting the current consumption levels of meat. Countries such as

Vietnam, India, Thailand and Mexico registered year-on-year growth rates ranging from 3% to 9% in the past year.

• Demand for fresh and branded pork and other types of meat is driving growth in overall meat consumption in India.

• Growing demand for poultry in Mexico is also supporting overall meat consumption in this Latin American country. Health

concerns around the consumption of red meat have led to poultry being the main meat consumed in Mexico.

• Premium and organic meat products are experiencing strong demand in developing countries, and this is expected to

continue being another driving factor in the fresh and processed meat categories.

SECTION 1

Consumption of fresh and processed meat falls in key Western markets

GLOBAL LANDSCAPE

-5.8%

0.9%

-0.7%-1.6%

-2.8%

-10%

-5%

0%

5%

10%

0

5

10

15

20

25

30

China USA Germany France Spain

2018/2

019 y

ear-

on-y

ear

gro

wth

Reta

il volu

me (

mill

ion tonnes)

Fresh Meat Consumption, Five Lowest Performing Markets in 2019

-1.5% -2.0%

-3.9%-3.0%

-1.2%

-10%

-5%

0%

5%

10%

0

1

2

3

4

5

Germany France Argentina Norway Greece

2018/2

019 y

ear-

on-y

ear

gro

wth

Reta

il volu

me (

mill

ion tonnes)

Processed Meat Consumption, Five Lowest Performing Markets in 2019

Health-consciousness is driving declines in fresh and processed meat consumption in Germany and France

• In Germany, the decline in meat consumption in 2019 was driven by reduced consumption of pork, the biggest type of

meat consumed. Pork is increasingly seen as less healthy than other meats, such as poultry. Furthermore, there are

early signs of sales cannibalisation of meat by meat substitutes.

• Unsustainability of meat agriculture and production, increased sensitivity towards animal welfare and the active reduction

of saturated fats have influenced the ongoing decline in meat consumption in France.

China is one of the few developing markets registering a strong decline in fresh meat consumption in 2019

• China’s recent decline in fresh meat consumption can mainly be attributed to large declines in pork consumption. African

swine fever has affected China’s pig farmers and supply levels. Similarly, awareness of African swine fever has affected

consumers’ perceptions, and this has contributed to declines in pork consumption.

SECTION 1

Global overview of meat substitutes

GLOBAL LANDSCAPE

-0.7%

7.6%4.8%

9.5%4.5% 4.3%

2.0%

8.3%4.7%

1.6%

21.5%

-2.3%

14.6%

2.1%

8.7%5.8%

-5.2%

7.4%11.5%

6.3%

13.8%

2.2%

8.8%6.1%

47.6%

9.5%

0.0%

21.4%

-10%

0%

10%

20%

30%

40%

50%

60%

0

20

40

60

80

100

120

Year-

on-y

ear

gro

wth

rate

(2018/2

019)

Reta

il volu

me (

‘000 t

onnes)

Meat Substitutes Consumption, Other Countries in 2019

60.5%25.5%

14.0%

Meat Substitutes Consumption,Top Two Largest Markets

(retail volume, ‘000 tonnes, 2019)

China

Japan

Other countries

4,259.4

• The maturity of meat substitutes in China and Japan is due to traditional

consumption of soy products and tofu.

• South Korea, the US, Indonesia, and the UK complete the top six

largest markets for meat substitutes globally.

• Of these, the UK registered the strongest growth in 2019, growing by

10%, driven by new product launches, negative press for red meat, and

an increasing number of consumers switching to plant-based diets.

• Finland, Canada, Norway and France are amongst the fastest

growing markets for meat substitutes. Canada has witnessed

increased consumer interest in chilled meat substitutes, driven by

changing diets and increased education. For example, the updated

Canadian Food Guide has a greater emphasis on plant-based proteins.

SECTION 1

Key product and brand highlights within meat substitutes globally

GLOBAL LANDSCAPE

Beyond Burger Impossible Burger Quorn pieces Veega meatballs

• Quorn is known for providing

meat-free mince, pieces,

fillets and nuggets.

• Quorn is one of the leading

meat substitute brands in the

world. It was acquired by

Monde Nissin, the world’s

largest noodle company.

• The company claims that its

products are a healthy

alternative protein that can

lower cholesterol levels.

• Within meat imitation products, burgers, fish

substitutes and chicken nuggets are emerging as

subcategories. Burgers is particularly contested, as

the grand fast-food prize, attracting investors’

attention.

• These burgers contain a range of non-meat protein,

such as from peas or soy, and often use beetroot

juice to mimic blood.

• Impossible Burger contains an ingredient called

Heme, considered the “magic ingredient” that makes

the burger taste like meat.

• Veega by San Miguel Foods

offers a wide range of meat-free

formats, including sausages,

burgers, nuggets, giniling

and meatballs.

USA EU /Philippines

SECTION 1

Who are the emerging leaders in plant-based products?

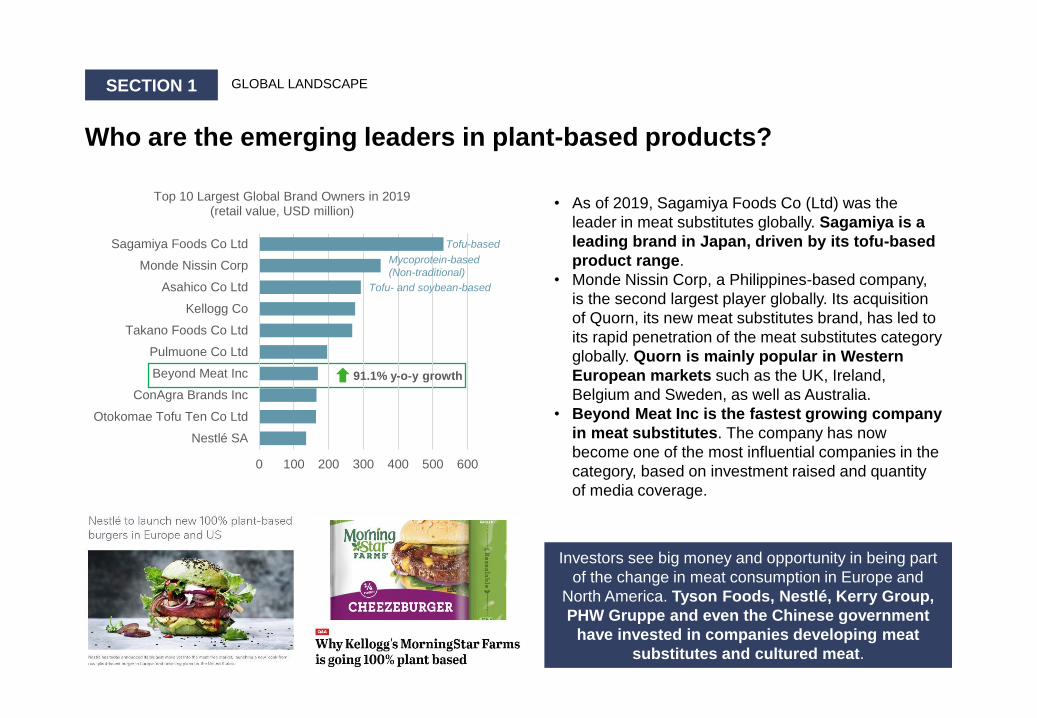

GLOBAL LANDSCAPE

• As of 2019, Sagamiya Foods Co (Ltd) was the

leader in meat substitutes globally. Sagamiya is a

leading brand in Japan, driven by its tofu-based

product range.

• Monde Nissin Corp, a Philippines-based company,

is the second largest player globally. Its acquisition

of Quorn, its new meat substitutes brand, has led to

its rapid penetration of the meat substitutes category

globally. Quorn is mainly popular in Western

European markets such as the UK, Ireland,

Belgium and Sweden, as well as Australia.

• Beyond Meat Inc is the fastest growing company

in meat substitutes. The company has now

become one of the most influential companies in the

category, based on investment raised and quantity

of media coverage.

0 100 200 300 400 500 600

Nestlé SA

Otokomae Tofu Ten Co Ltd

ConAgra Brands Inc

Beyond Meat Inc

Pulmuone Co Ltd

Takano Foods Co Ltd

Kellogg Co

Asahico Co Ltd

Monde Nissin Corp

Sagamiya Foods Co Ltd

Top 10 Largest Global Brand Owners in 2019 (retail value, USD million)

91.1% y-o-y growth

Investors see big money and opportunity in being part

of the change in meat consumption in Europe and

North America. Tyson Foods, Nestlé, Kerry Group,

PHW Gruppe and even the Chinese government

have invested in companies developing meat

substitutes and cultured meat.

Tofu-based

Mycoprotein-based

(Non-traditional)

Tofu- and soybean-based

SECTION 2

Growth drivers

This section identifies

the leading factors

supporting demand

for meat substitutes

globally. Some of the

growth drivers explored

in this section are

health awareness,

changing consumer

diets and environmental

considerations.

SECTION 2

The driving forces in plant-based protein and meat substitutes

GROWTH DRIVERS

Key factors

driving

growth of

meat

substitutes

Consumer lifestyles

Environmental impact✓ Livestock greenhouse gas emissions contribute to climate change

✓ There is a link between meet reducers and climate change worriers

Government policies✓ Health guidelines from

governments worldwide agree

that meat intake should be

limited/reduced

✓ Increasing product innovation and campaigns

are bringing the health and sustainability of

plant-based protein to the fore

Product innovation

✓ Flexitarian is a new term associated

with individuals who follow a flexible

vegetarian diet with the occasional

consumption of meat, typically for

health or other purposes

✓ The rise of flexitarianism helps to drive

the growth of plant-based foods and

meat substitutes

SECTION 2

Health and animal welfare concerns are leading motivations behind

consumers opting for a vegan diet

GROWTH DRIVERS

Source: Euromonitor International´s Health and Nutrition Survey, 2019

(Respondents that declared they follow a vegan diet n=691/20,166)

Blanks means no selection for such answer

• Health concerns and animal welfare concerns are

leading factors behind the adoption of a vegan diet.

Over 41% of global respondents choose vegan

options because it ‘makes them feel better’.

• Meat consumption (particularly red meat and

processed meat) is often associated with health

risks such as heart disease and cancer. Consumers

are therefore educating themselves on the health

benefits of reducing meat consumption and are

adjusting their diets accordingly.

• Ethical motivations such as animal welfare are also

influencing dietary changes among consumers

globally. Consumers are increasingly concerned

about the treatment of animals on large farms.

• Although the number of consumers who follow

a vegan diet is still growing from a small base,

the underlying motivations behind these dietary

requirements are also often applicable to

consumers opting for vegetarian and flexitarian

diets.

SECTION 2

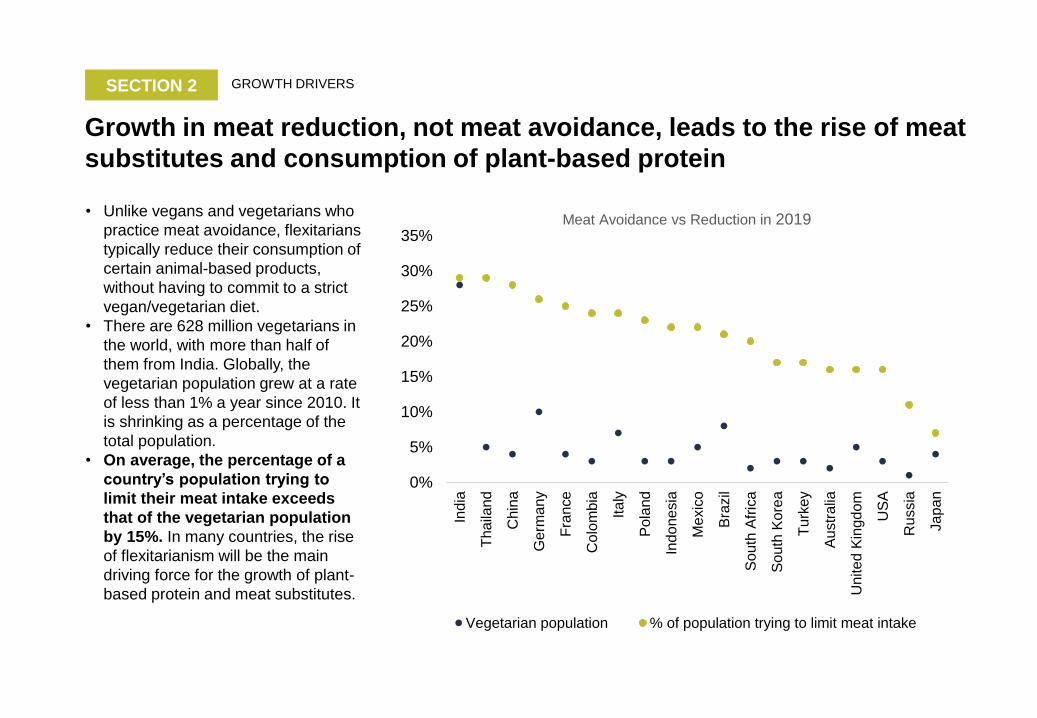

Growth in meat reduction, not meat avoidance, leads to the rise of meat

substitutes and consumption of plant-based protein

• Unlike vegans and vegetarians who

practice meat avoidance, flexitarians

typically reduce their consumption of

certain animal-based products,

without having to commit to a strict

vegan/vegetarian diet.

• There are 628 million vegetarians in

the world, with more than half of

them from India. Globally, the

vegetarian population grew at a rate

of less than 1% a year since 2010. It

is shrinking as a percentage of the

total population.

• On average, the percentage of a

country’s population trying to

limit their meat intake exceeds

that of the vegetarian population

by 15%. In many countries, the rise

of flexitarianism will be the main

driving force for the growth of plant-

based protein and meat substitutes.

0%

5%

10%

15%

20%

25%

30%

35%

India

Tha

iland

Chin

a

Ge

rma

ny

Fra

nce

Co

lom

bia

Ita

ly

Po

land

Indo

ne

sia

Me

xic

o

Bra

zil

So

uth

Afr

ica

So

uth

Ko

rea

Turk

ey

Au

str

alia

Un

ite

d K

ingd

om

US

A

Ru

ssia

Ja

pa

n

Meat Avoidance vs Reduction in 2019

Vegetarian population % of population trying to limit meat intake

GROWTH DRIVERS

SECTION 2

Vegan-labelled products are benefiting from the rise of flexitarianism

• Besides meat substitutes, vegan-

labelled products are also benefiting

from the rise of flexitarianism across

multiple continents, although there is no

visible increase in full-time vegans.

• Globally, the UK is the world leader

for sales of vegan-labelled products,

followed by the US and Germany.

• Although falling behind the US and the

UK in sales of vegan-labelled packaged

food, Germany is among the leaders

globally for sales of vegan-labelled

products. This can in part be attributed

to the association Proveg, which has

contributed to taking veganism from

negative to trendy connotations in many

parts of Germany, especially in Berlin.

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

UnitedKingdom

USA Germany Australia ItalyU

SD

mill

ion

Vegan-labelled packaged food

2016-2019

2016 2017 2018 2019

Sainsbury’s was the first UK

supermarket to launch vegan

BBQ Ribs, made from tempeh

(fermented whole beans), in

May 2019, aiming to combine

convenience with taste.

GROWTH DRIVERS

SECTION 2

Environmental messages generate more awareness around meat

consumption and its impact on the planet

GROWTH DRIVERS

SECTION 2

Meat reducers often worry about climate change

GROWTH DRIVERS

BrazilChinaFrance

Germany

India

Japan

Russia

United Kingdom

USA

Mexico

Australia

ColombiaIndonesia

Italy

Poland

South Africa

South Korea

Thailand

Turkey

Middle East

Canada

-10%

0%

10%

20%

30%

40%

50%

0% 10% 20% 30% 40%

% m

ore

lik

ely

to

be

wo

rrie

d a

bo

ut clim

ate

Share of population reducing meat

Note: Based on the answers of 28,487 respondents globally

Meat Reduction vs Concern about Climate Change▪ UN figures state that the

livestock industry has an adverse impact

on climate change, since it creates more

greenhouse gases than the

transport industry. Currently, there are

almost 22 billion animals bred for the

industry, with cattle accounting for 1.4

billion.

▪ Research indicates that meat reducers

are more likely to show more concern

about climate change.

▪ For example, developed markets such

as the US, the UK, Australia, Germany,

France and Poland stand out as

markets in which people who are

reducing their meat consumption are

more likely to be motivated by

environmental concerns.

▪ Environmentally concerned consumers

who are reducing their meat intake are

still a minority. However, this consumer

group is expected to grow over the next

five years.

SECTION 2

Pioneering innovations in meat substitutes drive supply

GROWTH DRIVERS

• Many meat processors are keeping a close eye on the meat substitutes category, and some meat processors are even

investing in it. Tyson, Nestlé, ABP, Hilton, JBS and Maple Leaf have all done so. In recent years there have been many

product launches, such as Nestlé’s Incredible Burger, Gold&Green’s Pulled Oats and Vivera’s Quarter Pounder.

• It is also worth noting that competition is not only arising from large food companies, but also from local and smaller

companies. Some markets, such as those in Western Europe, are currently witnessing market fragmentation in meat

substitutes, allowing potential consolidation opportunities.

• With more companies getting involved and launching new product concepts, consumers will continue to have access to a

wide selection of meat alternative products, boosting consumption.

Gold&Green’s Pulled Oats Vivera’s Quarter Pounder

An advantage which appeals to investors is that meat substitute products can be patented, unlike meat. As such,

there is room for new business models and greater margins. Creating tasty products with good mouthfeel also requires

a great deal of know-how, which serves as a barrier to entry for potential new competitors.

SECTION 2

A move towards policies that actively seek to lower meat consumption

GROWTH DRIVERS

According to the latest food

pyramid released by the Danish

Consumers Cooperative Society

in 2011, animal protein sources

were moved to the top of the

pyramid, whilst vegetables were

moved to the bottom of the

pyramid. Research is currently

underway in Denmark, looking

at ways to adapt quinoa to the

Danish climate and grow it in

the country in order to have a

better supply of meat-free

protein alternatives.

Scientists from the National

Institute for Public Health and

the Environment in the

Netherlands have advised

people to avoid eating too

much animal protein, as a

debate over increasing the tax on

meat gathers pace. Whilst the

report did not recommend an

optimum level of meat

consumption, spokesperson

Toon van Wijk said people

should not eat more than 500g of

meat per week. Only 300g

should come from red or

processed meat.

The Chinese government has

outlined a plan to reduce its

citizens’ meat consumption by

50% by 2030. New dietary

guidelines drawn up by China’s

health ministry recommend that

the nation’s 1.3 billion population

should consume between 40g

and 75g of meat per person each

day. These measures are

designed to improve public

health, but could also lead to a

significant cut in greenhouse gas

emissions.

The French food safety

agency, ANSES, has issued

national updated dietary

guidelines urging consumers

to “considerably reduce” their

consumption of meat.

ANSES has recommended that

the consumption of delicatessen

produce such as ham, sausage

and pâté “does not exceed 25g

per day”, and the consumption of

meat, excluding poultry, such as

beef, pork and lamb, “should not

exceed 500g per week”.

A global consensus is forming on the desirability of reducing meat intake, formed around the recommendations of

the World Health Organization (WHO), which says that red meat intake should be limited to around 500g per week.

It also recommends that processed meat should be avoided totally, or consumed in very small amounts.

SECTION 3

Regional zoom-in

Understanding some of

the largest and

fastest-growing meat

substitutes markets

across the globe, their

key success drivers,

and other market

dynamics.

SECTION 3

Meat substitutes in Japan and China is expected to witness a larger

contribution from non-traditional meat substitutes

REGIONAL ZOOM-IN

Meat substitutes in China and Japan is currently dominated by

tofu- and soy-based products

• In 2019, a local Chinese start-up launched the Zhen brand of

mooncake, with a meat substitute filling made with protein

extracted from peas. This meat substitute, which is mainly

distributed online, is catering to the growing interest in non-

traditional meat substitutes amongst younger consumers.

• Tofu- and soybean-based products in Japan have reached

maturity, leading to projected stagnant growth in the overall meat

substitutes category. This will open up opportunities for non-

traditional meat substitutes, as this type of substitute product is

expected to expand, satisfying emerging demand from millennials

and gen Z.

• However, tofu is expected to continue contributing to the forecast

performance of meat substitutes in both Japan in China, as it is

perceived as naturally healthy. The premium quality and superior

hygiene of packaged tofu is expected to resonate with those

consumers who shy away from wet markets.

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Th

ousands o

f to

nnes

Consumption of Meat Substitutes in China 2015-2024

Meat substitutes retail volume Meat substitutes y-o-y growth

-15%

-10%

-5%

0%

5%

10%

15%

950

1,000

1,050

1,100

1,150

1,200

1,250

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Th

ousands o

f to

nnes

Consumption of Meat Substitutes in Japan, 2015-2024

Meat substitutes retail volume Meat substitutes y-o-y growth

Coronavirus (COVID-19) considerationsIn 2020, meat substitutes has seen a spike in demand due to excess

purchasing and stockpiling activity across both Japan and China. This is

aligned with similar observations in other staple food categories.

Consequently, in 2021, meat substitutes is expected to register a strong year-

on-year decline in volume consumption as demand levels revert to normal.

SECTION 3

Tofu remains the dominant meat substitute in Southeast Asia

REGIONAL ZOOM-IN

4.8%

8.5%

4.5%

2.1%1.6%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

0

10

20

30

40

50

60

70

Indonesia Vietnam Malaysia Philippines Singapore

Th

ousands o

f to

nnes

Consumption of Meat Substitutes in Southeast Asia (2019)

Meat substitutes retail volume Meat substitutes y-o-y growth

In Southeast Asia, both tofu and tempeh are part of

daily consumption, with tofu contributing 98% of

packaged meat substitutes in the region. Both tofu and

tempeh are part of several traditional dishes in the region,

such as Tempeh Penyet in Indonesia, Adobong Tokwa in

Philippines, and Laksa in Singapore and Malaysia.

Source : https://omnipork.co/

With consumers’ habits and taste preferences for these

traditional flavours and formats, it is somewhat difficult for

new-age meat substitutes to penetrate the market.

• Indonesia and Vietnam are amongst the fastest growing markets

for meat substitutes in Southeast Asia. Growth in these

countries has primarily been driven by habit persistence of

consumption of tofu and tempeh.

• Formalisation of unpackaged tofu and its increased

availability in modern retail has been another growth driver.

• For example, Yun Yi tofu is still mainly sold as unpackaged tofu in

Indonesia, but due to increased demand for packaged products, it

is now also available in many major modern retailers.

• Singapore and Vietnam are emerging markets showing

consumer interest in non-traditional substitutes. Health-

conscious consumers are purchasing vegetarian products offered

by domestic players such as Omn!pork, Vissan and CJ Cau Tre.

• Indonesia and Vietnam are expected to register 5% and 10% retail

volume CAGRs respectively over the forecast period (2020-2024).

Source: The Impossible Wellington at Bread

Street Kitchen, Singapore

SECTION 3

Product innovation in Western European markets to drive growth of

meat substitutes over the forecast period (2020-2024)

REGIONAL ZOOM-IN

Substitution potential is high in France, the UK and Germany, all markets in which meat consumption is forecast to fall

• In the UK, besides consumers’ health-driven dietary changes, the increasing prices of meat and seafood

have also contributed to a slight shift from meat to meat substitutes. Similarly, the UK has seen new

product launches from Quorn, Tesco’s Wicked Kitchen and Beyond Meat. Large meat corporations such as

Anglo Beef Processors have also expanded their product range by launching meat substitute products.

• In France, consumers are interested in meat substitutes, but remain cautious about the products being

highly transformed and not clean label. Whilst meat is very clean label, meat substitutes are considered in

the same light as ready meals.

• Meat substitute products that are positioned as ‘healthy’ are gaining traction from new consumers in

Germany. Brand manufacturers have implemented innovation-led strategies to improve the taste and

texture of their products, as these are also key considerations in consumers’ decision-making. Furthermore,

discounters such as Aldi introduced meat substitutes to their shelves, with Aldi launching a veggie burger

called Wonderburger in the past year.

2

3318

7

48

2013

70

23

0

20

40

60

80

France UK Germany

Th

ousands o

f to

nnes (

reta

il) Meat Substitutes Consumption in Key Western European Markets 2015/2019/2024

2015 2019 2024

SECTION 3

Canada to become one of the fastest-growing meat substitute markets

in the Americas

REGIONAL ZOOM-IN

0

1,000

2,000

3,000

4,000

Fresh meat

2015 2019 2024

0

500

1,000

1,500

2,000

Processed meat

2015 2019 2024

0

50

100

150

200

Meat substitutes

2015 2019 2024

12.4% CAGR (2020-2024)

Th

ou

sa

nd

s o

f to

nn

es

Consumption of Meat and Substitutes

in Canada

(total volume)

1.8% CAGR (2020-2024)

5.1% CAGR (2020-2024)

• Over the past five years, Canadians have increased their

consumption of meat substitutes, with one of the key reasons

being wanting to limit or reduce their current meat

consumption.

• Weight management, animal welfare and gut health are other

leading considerations by Canadian consumers when opting to

diversify their protein intake and purchasing meat substitutes.

• Meat substitutes is expected to grow faster compared with fresh and

processed meat; forecast to register a 12% CAGR over the forecast

period.

• Industry sources suggest that Canada is responsible for only less

than 5% of new product launches globally, meaning that there is

significant investment opportunity for new players to enter meat

substitutes in the country.

Maple Leaf Foods, a leading

player in processed meat and

seafood in Canada, acquired

its new plant-based Lightlife

brand in 2017, and has

launched new plant-based

product formats across both

retail and foodservice.

Source : https://lightlife.com/en-ca/

The next slide also shows a similar breakdown for other

important meat substitutes markets

SECTION 3

Summary of other meat substitutes markets

REGIONAL ZOOM-IN

Thousands o

f to

nnes

Consumption of Meat and Substitutes in Key Markets

2015/2019/2024

(total volume)

10,000

15,000

20,000

25,000

Fresh meat

2015 2019 2024

1.3% CAGR (2020-2024)

9,500

9,600

9,700

9,800

Processed meat

2015 2019 2024

3.3% CAGR (2020-2024)

0

200

400

600

Meat substitutes

2015 2019 2024

24.3% CAGR (2020-2024)

0

1,000

2,000

3,000

Fresh meat

2015 2019 2024

3.3% CAGR (2020-2024)

500

750

1,000

1,250

1,500

Processed meat

2015 2019 2024

0.8% CAGR (2020-2024)

0

40

80

120

Meat substitutes

2015 2019 2024

7.0% CAGR (2020-2024)

2,000

2,500

3,000

3,500

Fresh meat

2015 2019 2024

1.9% CAGR (2020-2024)

0

500

1,000

1,500

Processed meat

2015 2019 2024

-2.5% CAGR (2020-2024)

0

5

10

15

20

Meat substitutes

2015 2019 2024

15.0% CAGR (2020-2024)

200

250

300

350

400

Fresh meat

2015 2019 2024

2.4% CAGR (2020-2024)

20

40

60

80

Processed meat

2015 2019 2024

3.9% CAGR (2020-2024)

0

2

4

6

Meat substitutes

2015 2019 2024

3.2% CAGR (2020-2024)

SECTION 4

Prospects

Exploring long-term

potential

developments in meat

and meat substitutes,

while understanding

how these will influence

the way consumers

approach meat

consumption in the

future.

SECTION 4

China and the US will play an important role in supporting the growth of

meat substitutes over the forecast period

PROSPECTS

Global retail volume sales of meat substitutes are expected

to see moderate growth over the forecast period (2021-

2024), registering a 3% CAGR

• The projected healthy growth of meat substitutes in China

and the US will help support the growth of meat substitutes

globally over the forecast period.

• In China, meat substitutes consists mainly of soy products

such as tofu. Soy products are seeing a notable shift from

small factories and artisanal shops to larger-scale production,

contributing to future growth. China is likely to remain the

market leader for the next five years, with more than a 50%

share of total volume sales of meat substitutes.

• The US was the third biggest consumption market for meat

substitutes in 2019, and the leader in terms of innovation.

Processed meat and seafood manufacturers have also begun

looking more closely at the opportunities in alternative

seafood production, which offers great opportunities for

overall meat substitutes.

2,577 2,886

2,772

2,859 2,938 3,013

1,0881,207

1,074 1,075 1,077 1,079524

563578 605 636 671

71

9293 98 105 111

-10%

-5%

0%

5%

10%

15%

0

1,000

2,000

3,000

4,000

5,000

6,000

2019 2020 2021 2022 2023 2024

Reta

il volu

me (

‘000 t

onnes)

Global Meat Substitutes Consumption Forecast, 2019-2024

China Japan Rest of the world

USA Global y-o-y growth

COVID-19 considerationsIn 2020, meat substitutes has seen a spike in demand due to stockpiling

activity across markets all over the world. Consequently, in 2021 meat

substitutes is expected to register a strong year-on-year decline in volume

consumption, as demand levels revert to normal towards 2024.

SECTION 4

Despite being categorised as processed food, meat substitutes suppliers

attempt to create a healthier image

PROSPECTS

• Meat substitutes technology could potentially usher in a new

era of sustainable food that could help to slow down the rate of

consumption of the Earth’s resources and mitigate the effects

of climate change.

• However, meat substitutes (unlike fresh meat) are processed

products, mostly built from isolates of natural ingredients,

whereby only about 60% of the protein contained in the plant

can be extracted. In addition to the loss of several useful

nutrients, most meat substitute products also have a very high

sodium content, containing about 16% of the recommended

daily value.

• For this reason, many consumers are likely to become more

selective and careful when buying meat substitute products,

given their health concerns.

• In response to this, many manufacturers are already thinking

of ways to best cater to the expected wave of consumer

demand by highlighting their products’ natural ingredients, and

health claims such as being organic and having no artificial

ingredients, among others.

• Health and wellness needs to be a key consideration for

producers of meat substitutes in the future, to create

competitive advantages and unique selling points that

attract not only consumers who are conscious about

sustainability, but also consumers who are conscious

about their health.

Smoky Maple Bacon

Tempeh from Tofurky Organic Teriyaki from

TofuBaked

Soybean sausages from

Polsoja

Organic Jackfruit Meatballs

from Edward & Sons

SECTION 4

Product innovation in meat substitutes expected to be driven by growing

consumer health concerns

PROSPECTS

Rising concerns about health and wellness will drive the plant-based protein industry to innovate and offer opportunities for

suppliers and manufacturers to enter the market with new healthy meat substitute products

• Originally, plant-based foods were mostly served as a substitute for red meat and poultry. However, health-conscious consumers of

meat substitutes are demanding variations of flavours, textures and formats, opening up opportunities for new product development in

seafood-inspired meat substitutes. For example, Tyson Foods, a key player within processed meat and seafood, has already begun to

invest in an alternative seafood start-up called New Wave Foods, which focuses on creating plant-based shrimp products.

• In order to appeal to both health- and sustainability-conscious consumers, meat substitutes globally has started to see numerous

brands that position themselves as organic, natural and meatless, claiming to contribute to a more nutritious diet with low or no carbs,

as well as high protein. This is expected to resonate not only amongst vegan, vegetarian and flexitarian populations, but also amongst

mass-market consumers who are trying to reduce their meat intake due to health concerns or disease prevention.

• As consumers’ interest in plant-based foods grows, companies should consider incorporating health and wellness into their current

business model and investing in product innovations around this topic.

Hilary’s organic veggie burgers New Wave’s plant-based shrimp Tuno’s plant-based seafood

SECTION 4

Blended meat products perceived as a step-transition to plant-based

protein and meat substitutes

PROSPECTS

• Besides being the key driver of sales of plant-based protein, flexitarianism has also opened up another avenue for

blended meat products, with meat as a key ingredient, but combined with more plant-based content.

• This is the epitome of “meat reduction” (as opposed to cutting out meat altogether), and satisfies consumers who are

seeking healthier options without sacrificing taste.

• These blended products, which are seeing increased availability, are perceived as a gradual transition to help

consumers reduce meat before moving on to the next stage with plant-based protein. As such, these launches

have received positive feedback from the majority of consumers who identify as flexitarians, or who are pursuing

healthier choices.

In June 2019, Tyson

announced a new Raised

and Rooted brand,

featuring “patties blended

with beef and plants”, that

hit shelves at the end of

2019.

In June 2019, Perdue Foods

launched Chicken Plus - a line

of chicken nuggets, tenders

and burgers made from

chicken and cauliflower,

chickpeas, and plant protein.

Misfit Foods launched

meat-blended sausages,

with the starring

ingredients being kale,

gold squash and sweet

potato.

SECTION 4

Cultured meat has the potential to be the “future of food”

PROSPECTS

Cultured meat is lab meat created by using muscle

stem cells from a fully-grown animal, cultivating

them in a nutrient-rich growth medium to become

muscle tissues.

• Advocates of cultured meat claim several

advantages of lab meat over fresh meat and

consider it as the future of food. Although fresh

meat is seen as a better protein source because of

its perception as a more “natural” source of protein,

cultured meat positions itself as the ideal solution to

provide a more ethical, sustainable and healthier

protein source.

• Since 2013, cultured meat exploratory work and

development has increased. In 2020, there are

nearly 30 start-ups working on cultured meat

production around the world. They expect to get

their products to market within the next few years.

• Cultured meat is expected to become an important

sector within the meat industry over the next 10

years, when it will begin to become a viable

alternative to the conventional meat industry.

Lower environmental impact

Less strain on natural resources

Hormone-free

Antibiotic-free

Customised nutrition

High protein

“Clean” meat

Healthy living

Sustainability

Animal welfareAnimal-friendly

Slaughter-free

Cultured meat

New

meat substitutes

Current

meat substitutes

SECTION 4

18.2%

Cultured meat could profit from “safer” claims

PROSPECTS

Amongst the main aspects which cultured meat could capitalise on

are food safety and avoiding disease, thanks to the exclusion of

slaughterhouses from the meat production process

In 1997, many countries were hit by an outbreak of bird flu, when

governments worldwide had to order the slaughter of more than a billion

chickens, ducks, pigeons and other birds to contain the spread of the

virus. Fast track to 2020, and the global pandemic COVID-19, caused by

animal-hosted viruses, has spread to 213 countries and caused hundreds

of thousands deaths.

Historically, there have been many diseases caused by close contact

with animals, through the hunting, trading or consumption of these

animals, such as bird flu, SARS, Spanish flu, COVID-19, etc. Such

activities place the world at an increased risk of contracting new

diseases. For this reason, consumers are more likely to be attracted

to cultured meat as a safer and more sustainable option, with

COVID-19 being an influencing factor.

Looking forward, cultured meat brands see great opportunities

surrounding health and wellness attitudes, as consumers are becoming

more active in seeking healthier options that can improve their health and

boost their immune system. Potentially being able to offer a

personalised and individualised nutrition profile that caters to

various nutritional deficiencies, cultured meat shows great

possibilities in being a new food revolution and mitigating some of

the health, environmental and social costs that traditional meat

consumption brings.

SECTION 5

How to win?

This section further

highlights key

business

considerations

companies should

review when making

decisions concerning

meat substitutes,

whether these are

marketing, product

innovation or pricing

decisions.

SECTION 5

Euromonitor International’s plant-based scorecard inputs

Animal

welfare

Dairy

alternatives

Edible

insects

Lab-cultured

meat

Meat

analogues

Categories Key metrics

analysed

• Market size (value and

volume)

• Historic and forecast

growth

• Consumer survey data

• Socio-demographic

data

• Substitutes

• Retailing

Countries

54 researched countries

within Euromonitor

Passport database(Note: Country coverage may

vary based on data availability

and by each category)

Time period

2013 to 2023

2019 (base year)

HOW TO WIN?

SECTION 5

Besides the US and China, Western Europe has potential – offering

opportunities for meat substitute companies in the future

THE FUTURE

501 483 493 472 449371 361

459369

190 201 181 198 217215 217 66

75

691 684 674 670 666586 578

525444

0

200

400

600

800

1000

USA France UnitedKingdom

Germany China Australia Thailand Spain Vietnam

Index s

core

Meat substitutes: Key markets based on scorecard

Market size & growth Consumer & socio-demographic

Top performing Other high

performers

• While the US is known as one of the

market leaders for meat substitutes, due

to market consumption and innovation,

Western Europe’s performance is strongly

influenced by consumers’ tendency to

avoid meat, which has been developed

over the years through the efforts of

NGOs propagating veganism and

vegetarianism within the region.

• Environmental concern, the adoption

of a flexitarian diet and new product

innovation are key drivers of meat

substitutes in the US and many Western

European countries.

• Rising demand for clean labels,

alongside healthier branding and

nutritional profiles for processed food,

are also contributing to the growth of meat

substitutes in markets in Asia, as well as

other parts of the world.

Source: Euromonitor International

HOW TO WIN?

SECTION 5

New Zealand companies looking to launch new meat substitutes should

focus on aligning their products with the right market

• In order to better penetrate new

markets, food suppliers need to be

aware of the existing food culture

within their target market. This is

true for both lab-grown meat and

plant-based meat products which

aim to be direct replacements for

meat products.

• In 2019, China, the US, Brazil and

India formed the four largest meat

consumer markets globally.

• Globally, poultry accounted for 41%

of the total meat volume, followed

by pork (31%) and beef and veal

(21%).

• In the next five years, the total

meat volume globally is expected to

register a CAGR of 1.8%, of which

poultry forms 42% of the future total

meat volume, followed by pork

(32%) and beef and veal (20%).

• Growth in beef and veal is

expected to slow down compared

with past years, as beef-heavy

markets are becoming more

saturated and consumption in

Western Europe is set to see a

marginal decline.

• With the rise of meat reducers, it is

likely to be easier for producers to

introduce specific types of meat

substitutes to markets that have a

high demand for that specific type

of meat, i.e. producers could

potentially introduce pork-based

meat substitutes to markets that

have high demand for pork, such

as China.

HOW TO WIN?

Beef and Veal Lamb, Mutton

and Goat

Pork Poultry

China India BrazilUSA Australia

SECTION 5

New Zealand companies also need to provide competitive price points,

as consumers have a wider product choice in stores

HOW TO WIN?

• An interesting innovation in 2018 was the German insect burger. It was a timely introduction,

as insect protein has been on the agenda and is positioned as high in protein, free from

additives and sustainable. However, at EUR30 per kilo, it was not priced attractively. Unlike

the insect burger, The Frozen Butcher Angus Burger, a meat-based substitute competitor in

the premium range, was only priced at EUR16 per kilo.

• A Euromonitor International storecheck producing a rough average of unit prices in

processed meat and meat substitutes from a selection of 15 German supermarkets,

discounters and online retailers came to the same conclusion: although the price per SKU

is in many cases slightly lower for comparable meat substitutes, the smaller pack

sizes mean that the price per kg is 43% higher for meat substitutes – a barrier for

reaching the mass market.

Picture from bugfoundation.com

Picture from frozenbutcher.com

As new players join meat substitutes globally, companies must have competitive

pricing strategies while still highlighting any health or functional benefits

• Increasing demand for meat substitutes across many markets around the world is attracting

small and large players alike to enter the category and launch new products.

• Companies are launching new flavours, ingredients, formats and meals in order to

differentiate their products and maintain high premium price points in certain markets.

However, as these products become more available, and the choice is vast, it is expected

that consumers will keep a closer eye on prices, whilst also focusing on value propositions.

• Private label is expected to play a larger role in the price competition, with countries such

as Germany and Australia starting to see more private label plant-based products in stores.

SECTION 5

New players should think about a health and wellness positioning when

developing marketing strategies for meat substitutes

HOW TO WIN?

Beyond Meat launched a new advertising campaign in 2019

focusing on fitness, featuring a range of well-known sports men

and women. Toning down the ethical and sustainable and

including more happy meat eaters in the target group is a

skilled approach to brand-building that has not quite been

seen in the sector before. Claims about the superior quality

of plant protein for athletes have been used before, by Swedish

retailer Coop in 2017 and Danish Naturli’ in 2018, yet Beyond

Meat’s campaign goes further in the direction of a fitness

positioning. The campaign also connects meat substitutes to

athletes outside the sports arena, depicting their daily lives full

of love, care for the planet and new generations, and focuses

on healthy eating.

Macros is a ready-made meal delivery service provider in

Australia which is gaining popularity among consumers due to

its healthy positioning. More recently, Macros intensified its

marketing and promotional efforts for its plant-based meal

range. The company positions its meals as dietitian-

approved and as free from preservatives, additives,

artificial ingredients and others. This further suggests that

marketing and positioning around health benefits and

meal functionality is an increasing way of communicating

a message to consumers. Highlighting key ingredients,

providing transparent information on product manufacturing

and verification or certification with health organisations are

becoming common practice amongst brand manufacturers or

foodservice providers of meat substitutes.

Source : https://www.macros.com.au/

SECTION 5

The permanent shift in consumer preference to health and wellness-

related products may help spur growth for plant-based products

Source: Euromonitor International (Voice of the Industry Survey COVID-19, n=4819)

HOW TO WIN?

▪ The recent global pandemic boosted

consumers’ interest in staying healthy. More

than 31% of respondents expect a permanent

change in their purchasing habits, whereby they

purchase more health and wellness-related

products following the emergence of the

COVID-19 pandemic.

▪ The availability of general functional products to

enhance health is seen as one biggest concerns

for consumers during and after the COVID-19

lockdown.

▪ COVID-19 will put natural and healthy

ingredients back under the spotlight.

Incorporating health and wellness messaging

into brand images would help plant-based

protein suppliers to generate consumer interest.

▪ An emphasis on the affordability of plant-based

protein products will also be critical as

consumers look to reduce their overall spending

either permanently or over the mid-term.

0% 25% 50% 75% 100%

Buy more health and wellness-relatedproducts

Buy more products to improve life athome

Reduce overall spending

COVID-19 changes views of health and spending

Permanent change

Mid-term change, but will eventually return to pre-crisis norms

Short-term change only (Q1 and Q2 2020)

No Change

Not Sure

Key takeaways and recommendations

1New Zealand companies looking to explore overseas opportunities in meat substitutes are encouraged to focus not only

on markets that have a large size, but also those that are witnessing rapid expansion. Fast-growing meat substitute

markets such as Canada, the US, Vietnam, Australia, France and others are good starting points to look for market entry

opportunities.

2As discussed in this report, globally meat substitutes is being driven by multiple factors. Nevertheless, the growing number of

flexitarians across the world is an important consumer shift that businesses must consider when developing food products and

meal solutions moving forward. Consumers are not necessarily trying to cut out all meat, but rather have a smooth transition to a

low meat consumption diet. Understanding the right occasions, cooking habits and flavour preferences will continue to be

important in targeting flexitarian consumers.

3China and Japan are expected to remain the largest meat substitutes markets globally. These are expected to remain driven by

tofu- and soybean-based products. However, New Zealand companies looking to develop non-traditional meat substitutes

are recommended to focus on those markets that are seeing the growing presence of non-traditional products. Markets

such as the US, Canada, Western Europe, Vietnam, Singapore and Australia provide opportunities for the further penetration of

non-traditional meat substitute products.

4New Zealand manufacturers of meat producers and meat substitutes are encouraged to look further into upcoming

potential disruptors such as innovations in cultured meat, blended products and health-driven meat substitutes. These

are likely to play an important role in the future development of the meat substitutes category. As technology improves, it is

expected that brand manufacturers will tap into meat substitutes by providing unique solutions to growing concerns about ultra-

processed foods, animal welfare and climate change.

5Business considerations around target countries, marketing, price and product positioning are very important and can

determine the success of products introduced in meat substitutes. Aligning these business strategies to consumers’

frustrations (e.g. health concerns) will be key to successfully introducing a product to a particular market. Similarly, choosing the

right countries to introduce meat substitute product ranges will be another important factor to consider. Targeting fast-growing

meat substitutes markets is likely to facilitate rapid consumer awareness and exposure.

Disclaimer: This information statement contains statistical data, estimates and forecasts concerning the industry in which NZTE and its members participates that

are based on independent industry publications, including those published by Euromonitor International Limited (“Euromonitor”) as well as NZTE’s

general knowledge of, and expectations concerning, the industry. The industry market and sales positions, shares, market sizes and growth estimates included in

this information statement are based on estimates using the foregoing independent industry publications and estimates based on data from various industry

analyses, our internal research and adjustments and assumptions that we believe to be reasonable. Although NZTE has no reason to believe this industry

information is not reliable, we have not independently verified data from industry publications and analyses and cannot guarantee their accuracy or completeness.

In addition, NZTE believes that data regarding the industry and industry market and sales positions, shares, market sizes and growth provide general guidance

but are inherently imprecise. Further, these estimates and assumptions involve risks and uncertainties and are subject to change based on various factors,

including those discussed in the “Risk Factors” section of this information statement. These and other factors could cause results to differ materially from those

expressed in the estimates and assumptions. Accordingly, investors should not place undue reliance on this information.

New Zealand Trade and Enterprise (NZTE) is the Government agency

charged with a single purpose: growing companies internationally, bigger,

better and faster, for the good of New Zealand.

We employ 600 people, have over 200 private sector partners and draw on

a global network of thousands more.

We have people based in 50 offices, working across 24 time zones and 40

languages to support New Zealand businesses in over 100 countries.

Our global presence lets us deliver value to the businesses we support,

through our unique know-how (knowledge and experience) and know-who

(networks and connections).

Our know-how and know-who is expressed in our Māori name:

Te Taurapa Tūhono.

Te Taurapa is the stern post of a traditional Māori waka, which records

valuable knowledge, and stabilises and guides the craft forward.

Tūhono represents connections to people and an ability to build

relationships.

We provide customised services and support to ambitious businesses

looking to go global. We help them build their capability, boost their

global reach, connect to other businesses and invest in their growth.

We also connect international investors with opportunities in

New Zealand through a global network of investment advisors.

We call on our Government network and work closely with our NZ Inc

partners and the business community, to grow our national brand and

help businesses to open doors in global markets.

nzte.govt.nz

Disclaimer: This document only contains general information and is not formal advice. The New Zealand Government and its associated agencies (‘the

New Zealand Government’) do not endorse or warrant the accuracy, reliability or fitness for any purpose of any information provided. It is recommended that

you seek independent advice on any matter related to the use of the information. In no event will the New Zealand Government be liable for any loss or

damage whatsoever arising from the use of the information. While every effort is made to ensure the accuracy of the information contained herein, the

New Zealand Government, its officers, employees and agents accept no liability for any errors or omissions or any opinion expressed, and no responsibility is

accepted with respect to the standing of any firms, companies or individuals mentioned.