Embed Size (px)

Citation preview

Eurasia Regional EITI Data Analysis Workshop

22-24 June, 2015Istanbul, Turkey

What is the importance of EITI data analysis?•Creates neutral space for building trust and facilitating discussion

Multi-Stakeholder Dialogue(MSG, CSOs)

• Links EITI to broader national policy priorities

Objective Setting(Work plan)

• Useful in evaluating pressing policy questions & challenges

Disclose Relevant Information(Scoping, Reconciler TOR &

EITI Report)

• Enables informed public understanding & policy debates

Analysis of Information

• Increases accountability & developmentLinks to Policymaking & Institution building

Legal framework & fiscal regime

(§3.2 )

Exploration activities

(§3.3)

Taxes & Primary

Revenues(§4.2(a))

SOE level of beneficial ownership (§3.6(c))

Direct payments/

receipts (§4.2(d))

Employment §3.4(d)

Revenues in & not recorded

in budget (§3.7)

License award/transfer

process & deviations(§3.1

0)

Production volumes &

values (§3.5(a) & §3.4(e))

In-kind revenues(§4.1(c))

Government transfers by

SOEs(§4.2(c))

Mandated national/

subnational transfers(§4.2(e))

Social payments(§4.1(e))

Earmarked revenues &

budget/audit processes

(§3.8)

Register of licenses(§3.9)

Export volumes &

values (§3.5(b))

Infrastructure/barter

provisions(§4.1(d))

SOE quasi-fiscal

expenditures(§3.6(b))

Beneficial ownership

(§3.11)

Economiccontribution(§3.4(a)-(c))

Transport Revenues

(§4.1(f)

Contract/license

disclosure(§3.12)

Allocation of Rights Production

Data Revenue Collection

SOERevenue Management

Sub-National

Social Impact

What is “EITI data”?

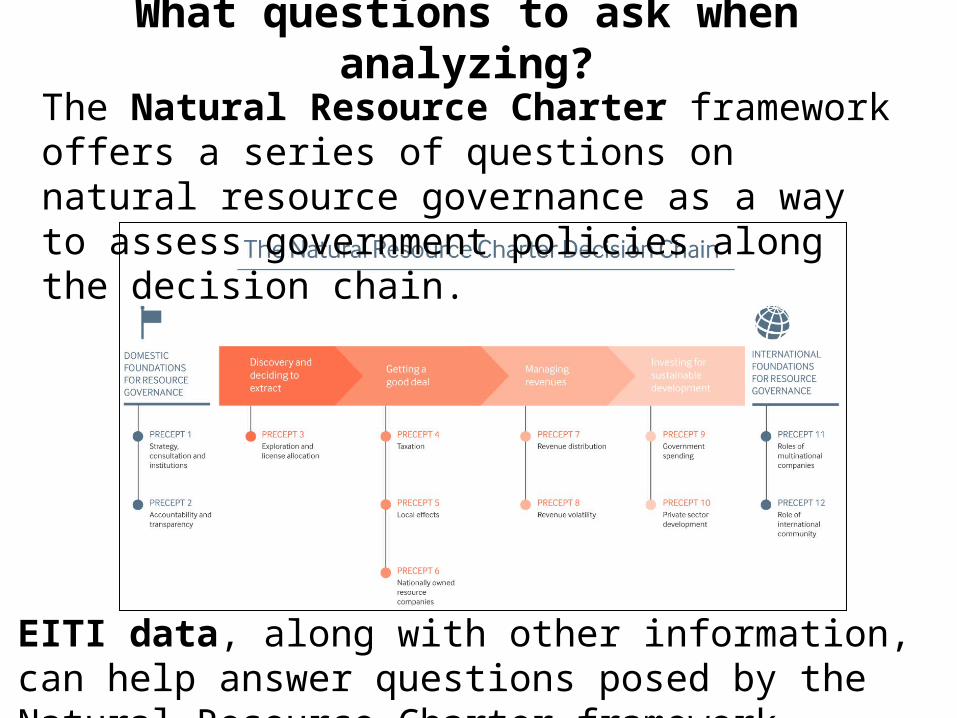

What questions to ask when analyzing?

EITI data, along with other information, can help answer questions posed by the Natural Resource Charter framework

The Natural Resource Charter framework offers a series of questions on natural resource governance as a way to assess government policies along the decision chain.

Limitations of Analysis

However, it is important to note the limitations of EITI report analysis. EITI reports usually do not provide all the information needed to fully analyze the costs and benefits of extractive policies.

But, EITI disclosures can raise important questions about natural resource revenue management and expose areas where greater transparency is needed.

Step A. Information Gathering: What are the relevant NRC framework questions and what information from EITI reports and other sources will help answer them?

Step B. Policy Evaluation: What does analysis of EITI information using the NRC framework questions indicate about the country’s natural resource policies and systems?

Step C. Recommendations: How can the government improve policies and systems to better manage resource wealth?

Framework for Analysis

Three steps to using EITI information to analyze Natural Resource Charter framework questions:

State-owned Enterprises

Issue for Analysis

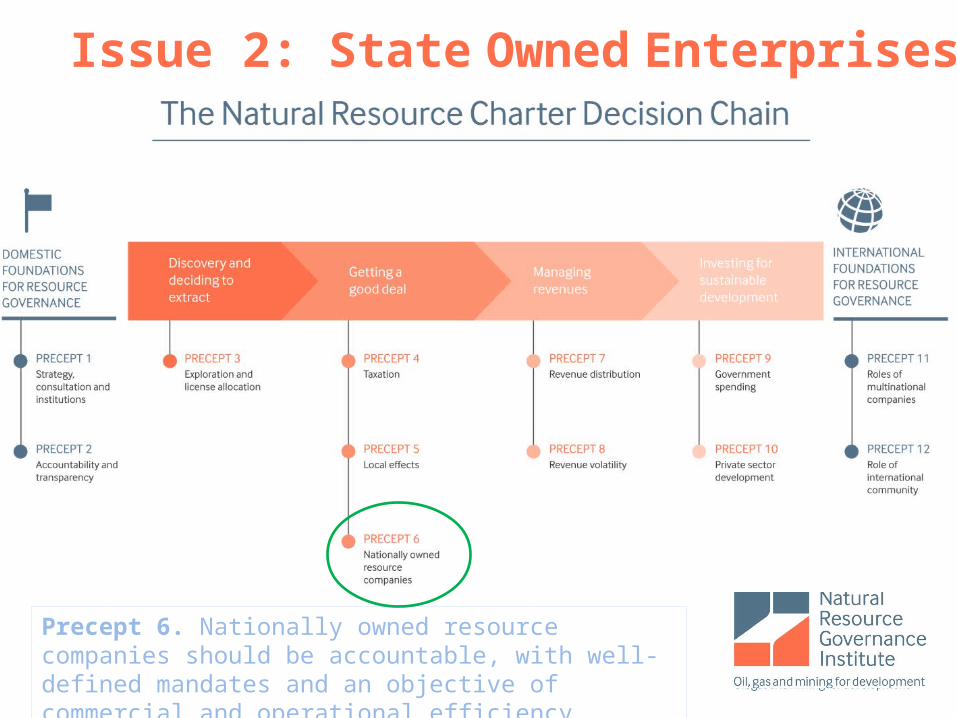

Issue 2: State Owned Enterprises

Precept 6. Nationally owned resource companies should be accountable, with well-defined mandates and an objective of commercial and operational efficiency.

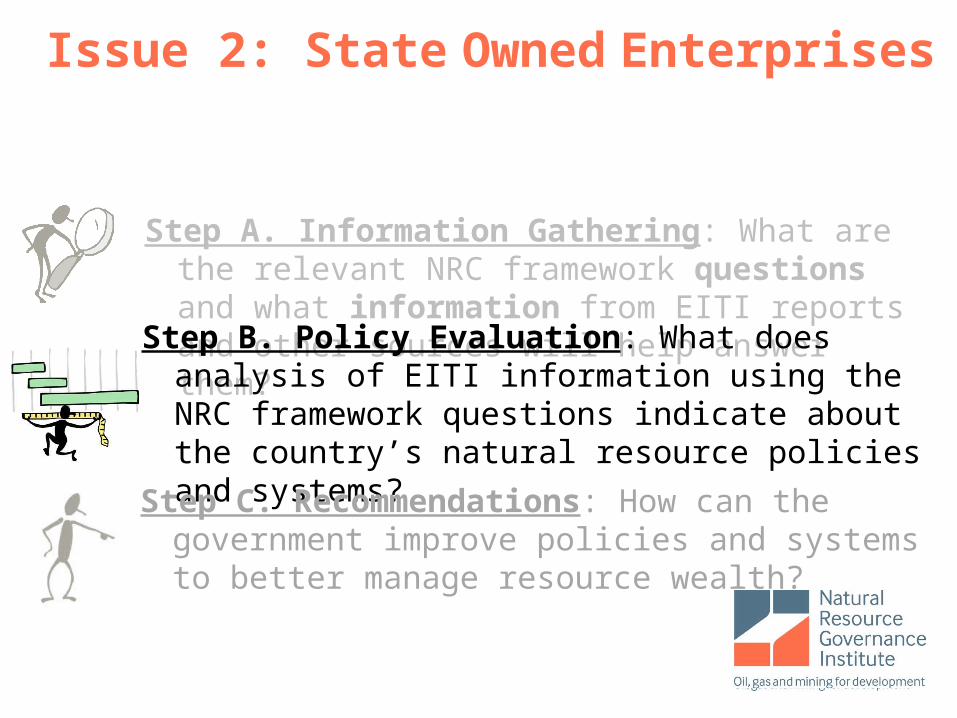

Step A. Information Gathering: What are the relevant NRC framework questions and what information from EITI reports and other sources will help answer them?

Step B. Policy Evaluation: What does analysis of EITI information using the NRC framework questions indicate about the country’s natural resource policies and systems?

Step C. Recommendations: How can the government improve policies and systems to better manage resource wealth?

Issue 2: State Owned Enterprises

Step A. Information Gathering: Primary QuestionsState Owned Enterprises

Primary Questions6.1 SOE Role. Do the extractive sector state-owned enterprises have clearly defined roles?

6.2 SOE Funding and Financing. Does the extractive sector state-owned enterprises have appropriate funding and financing models?6.3 Political Interference. Is there limited political interference in extractive sector state-owned enterprises technical decisions?6.4 SOE Accountability. Is the extractive sector state-owned enterprises transparent and subject to oversight?

6.5 Long-term outlook. What is the long-term outlook for governance of extractive state owned enterprises and institutions governing on extractive resources?

Secondary Questions• Transparency?• Audits?• Oversight?

What are the relevant NRC framework questions?

Precept 6. Nationally owned resource companies should be accountable, with well-defined mandates and an objective of commercial and operational efficiency.

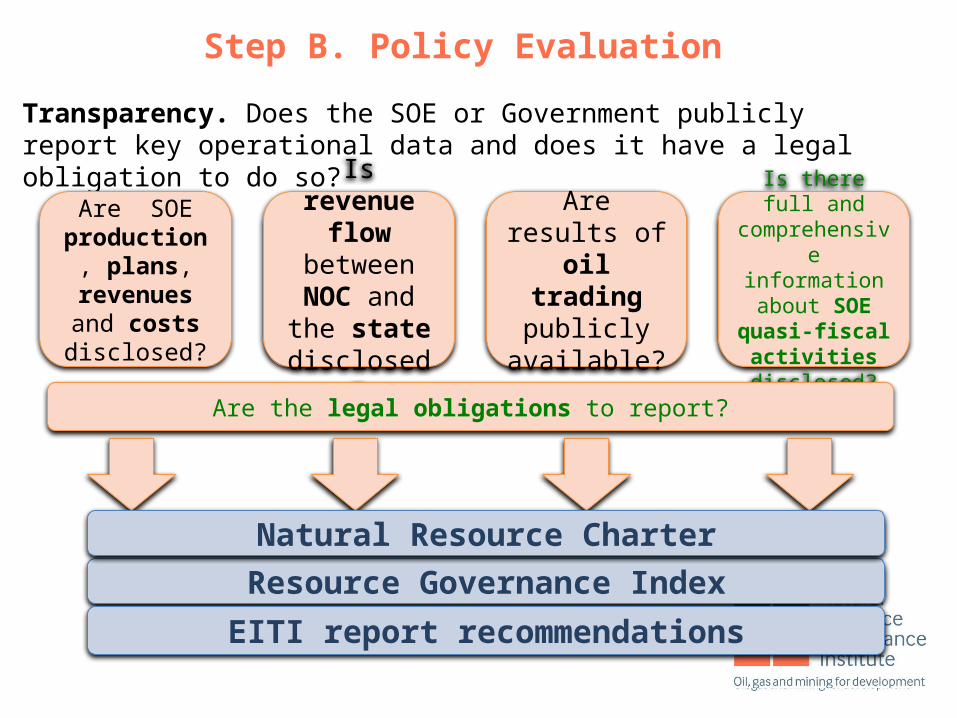

Transparency. Does the SOE or Government publicly report key operational data and does it have a legal obligation to do so?

Audits. Is the SOE subjected to independent financial audits by skilled independent professionals, and are the results publicly disclosed?

Oversight. Is the SOE subject to an appropriate level of legislative oversight without unduly constraining decision-making?

6.4 SOE Accountability. Is the extractive sector state-owned enterprises transparent and subject to oversight?

Step A. Information Gathering: Secondary Questions

Transparency. Does the SOE or Government publicly report key operational data and does it have a legal obligation to do so?

Are SOE production,

plans, revenues and costs disclosed?

Is revenue flow between NOC and the

state disclosed?

Are results of oil trading

publicly available?

Step A. Information Gathering: Tertiary Questions

Is there full and comprehensive

information about SOE quasi-fiscal

activities disclosed?

Are the legal obligations to report?

Transparency. Does the SOE or Government publicly report key operational data and does it have a legal obligation to do so?

Are SOE production,

plans, revenues and costs disclosed?

Is revenue flow between NOC and the

state disclosed?

Are results of oil trading

publicly available?

Step A. Information Gathering: Tertiary Questions

Is full and comprehensive

information about SOE quasi-

fiscal activities disclosed?

EITI reportRGI

EITI reportRGI

EITI reportRGI

EITI reportRGI

Official website (Government Ministry, National Oil Company, Oil Fund etc.)

Are the legal obligations to report?

SOEs: EITI Standard §3.6 Where state participation in the extractive industries gives rise to material revenue payments, the EITI Report must include:

b) Disclosures from SOE(s) on their quasi-fiscal expenditures such as payments for social services, public infrastructure, fuel subsidies and national debt servicing. The multi-stakeholder group is required to develop a reporting process with a view to achieving a level of transparency commensurate with other payments and revenue streams, and should include SOE subsidiaries and joint ventures.

If this information is published on government

websites, the EITI report may simply

provide a link

EITI Report

Step A. Information Gathering: SourcesIs full and

comprehensive information

about SOE quasi-fiscal activities

disclosed?

QuestionIs full and

comprehensive information about SOE

quasi-fiscal activities disclosed?

EITI Report

EITI Standard §3.6b Disclosures from SOE(s) on their quasi-fiscal expenditures such as payments for social services, public infrastructure, fuel subsidies and national debt servicing

AzerbaijanSOCAR website

2013 EITI report, page 30

2013 SOCAR financial report, page 22

SOCAR website, Social

Responsibility

QuestionIs full and

comprehensive information about

SOE quasi-fiscal activities disclosed?

RGI: Azerbaijan

Step A. Information Gathering: What are the relevant NRC framework questions and what information from EITI reports and other sources will help answer them?

Step B. Policy Evaluation: What does analysis of EITI information using the NRC framework questions indicate about the country’s natural resource policies and systems?

Step C. Recommendations: How can the government improve policies and systems to better manage resource wealth?

Issue 2: State Owned Enterprises

Transparency. Does the SOE or Government publicly report key operational data and does it have a legal obligation to do so?

Are SOE production,

plans, revenues and costs disclosed?

Is revenue flow between NOC and the

state disclosed?

Are results of oil trading

publicly available?

Step B. Policy Evaluation

Is there full and comprehensive

information about SOE quasi-

fiscal activities disclosed?

Resource Governance IndexNatural Resource Charter

EITI report recommendations

Are the legal obligations to report?

The national company should maintain public accounts in accordance with international standards and subject to independent audit, and clearly identify any private ownership interests and related transactions.

A system of checks and balances helps address the inevitable conflicts of interest

The national company should face at least the same standards of disclosure that private companies do.

Step B: Policy Evaluation: Natural Resource Charter

Precept 6. Nationally owned resource companies should be accountable, with well-defined mandates and an objective of commercial and operational efficiency.

QuestionWhat are the

safeguards that ensure publishing of information about

SOE quasi-fiscal activities disclosed?

Natural Resource Charter Azerbaijan government policy

A system of checks and balances helps address the inevitable conflicts of interest

Officials of the SOCAR are not required to disclose information about their financial interest in any extractive activities or projects

The national company should face at least the same standards of disclosure that private companies do.

According to the Charter of SOCAR on reporting, accounting and control in the Company, the SOCAR keeps accounts according to the law, and compiles a statistical report which it submits to the relevant state bodies.

The national company should maintain public accounts in accordance with international standards and subject to independent audit

SOCAR management is responsible for the preparation of consolidated financial statements in accordance with international financial reporting standards, such as IASB or GAAP accounting standards.

Step B: Policy Evaluation: Compare Azerbaijan’s transparency practices to the Charter’s recomendations

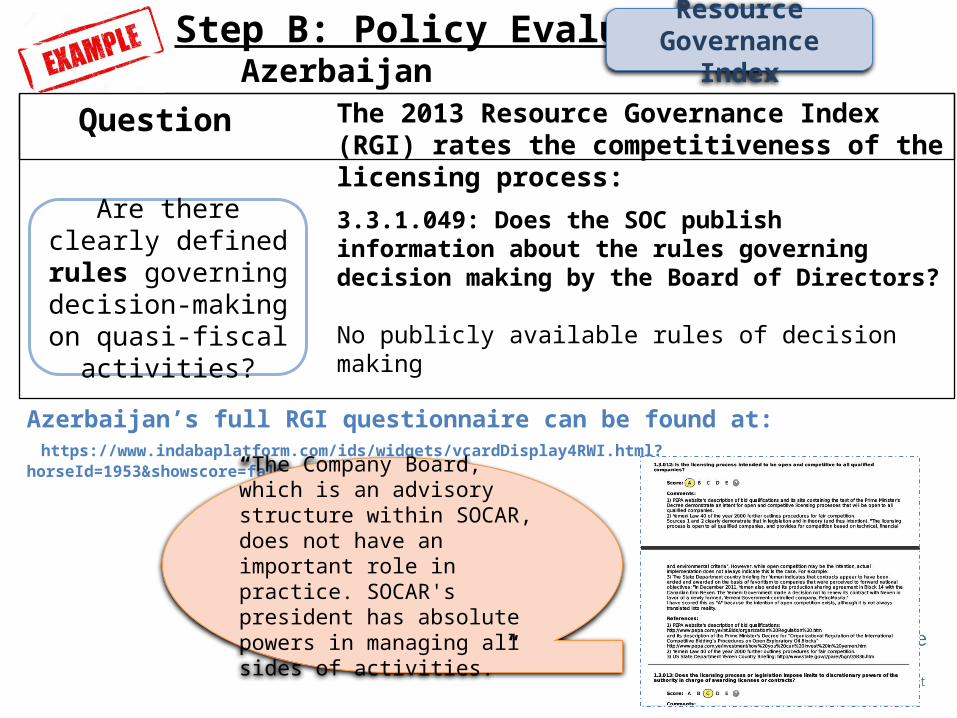

Step B: Policy Evaluation:

Question The 2013 Resource Governance Index (RGI) rates the competitiveness of the licensing process:

3.3.1.049: Does the SOC publish information about the rules governing decision making by the Board of Directors?

No publicly available rules of decision making

Azerbaijan’s full RGI questionnaire can be found at: https://www.indabaplatform.com/ids/widgets/vcardDisplay4RWI.html?horseId=1953&showscore=false

Resource Governance Index

Are there clearly defined rules

governing decision-making on quasi-fiscal

activities?

Azerbaijan

“The Company Board, which is an advisory structure within SOCAR, does not have an important role in practice. SOCAR's president has absolute powers in managing all sides of activities.”

Step B. Policy Evaluation: Azerbaijan

SOCAR is wholly owned by the government of Azerbaijan and takes part in all oil and gas activities. It publishes regular reports on production volumes, the value of exports, estimates of investments in exploration and development, production costs, the names of companies operating in the country, production data by company, quasi-fiscal activities, and the government’s portion of production-sharing contracts. SOCAR’s annual financial reports are audited by an independent external auditor and include the consolidated accounts of all SOCAR’s subsidiaries, however data is incomplete. Moreover there is no clear definition of rules governing non-commercial activities, namely quasi-fiscal activities. Additionally information about conducted quasi-fiscal activities is not fully available for public.

Rights Allocation Method. Does the government use an appropriate allocation method to allocate rights?

Step A. Information Gathering: What are the relevant NRC framework questions and what information from EITI reports and other sources will help answer them?

Step B. Policy Evaluation: What does analysis of EITI information using the NRC framework questions indicate about the country’s natural resource policies and systems?

Step C. Recommendations: How can the government improve policies and systems to better manage resource wealth?

Issue 2: State Owned Enterprises

“The national company should maintain public accounts in accordance with international standards and subject to independent audit, and clearly identify any private ownership interests and related transactions… legislature or appropriate oversight agency should conduct regular and systematic oversight of the national company.”

NATURAL RESOURCE CHARTER

6.4.1.Transparency

Step C. RecommendationsHow can government policies and systems be improved to meet the goals expressed in the Natural Resource Charter?

Transparency. Does the SOE or Government publicly report key operational data and does it have a legal obligation to do so?

“When citizens, investors and even other public institutions lack basic knowledge of what these companies are doing and how they are making decisions, the likelihood of management in the long-term public interest decreases significantly. ”

3. RecommendationsThe most effective SOEs have carefully-defined commercial and non-commercial roles.

NRGI: 9 Recommendations

for NOCs

Ensuring Transparency and

Effective Oversight

Transparency. Does the SOE or Government publicly report key operational data and does it have a legal obligation to do so?

“Public disclosure of key data on company finances and activities in a consistent and timely fashion is critical. Relevant information for publication includes expenditures by the company on quasi-fiscal activities”

3. RecommendationsThe most effective SOEs have carefully-defined commercial and non-commercial roles.

NRGI: 9 Recommendations

for NOCs

Ensuring Transparency and

Effective Oversight

Transparency. Does the SOE or Government publicly report key operational data and does it have a legal obligation to do so?

Recommendation 7.Maximize public reporting of key data.

“As is regularly demonstrated in the private sector, rigorous accounting standards that include independent audits are one of the most powerful tools creating incentives for strong performanceand corporate governance…”

3. RecommendationsThe most effective SOEs have carefully-defined commercial and non-commercial roles.

NRGI: 9 Recommendations

for NOCs

Ensuring Transparency and

Effective Oversight

Transparency. Does the SOE or Government publicly report key operational data and does it have a legal obligation to do so?

Recommendation 8.Secure independent financial audits, and publish them.

“Legislators should also take seriously their key role in policy-making, including via legislation that establishes major strategies for the petroleum sector, defines the roles of the NOC and other institutional actors, and sets reporting requirements. ”

3. RecommendationsThe most effective SOEs have carefully-defined commercial and non-commercial roles.

NRGI: 9 Recommendations

for NOCs

Ensuring Transparency and

Effective Oversight

Transparency. Does the SOE or Government publicly report key operational data and does it have a legal obligation to do so?

Recommendation 9.Choose an effective level of legislative oversight.

3. Recommendations: Azerbaijan

Actions for Azerbaijan’s government:

• Establish clear rules for SOCAR quasi-fiscal activities

• Require transparency in decision making on SOCAR quasi-fiscal activities

• Full disclose financial information on SOCAR quasi-fiscal activities

30

INSTRUCTIONS FOR GROUP WORK

Based on the proposed methodology take 3 STEPS of ANALYSIS on following issues:

Do the roles and responsibilities of KMG suit the national context (Ukraine)

Is there political interference in KMG technical decisions? (Kyrgyzstan)

Does KMG have an appropriate funding model? (Azerbaijan)

Is KMG transparent and subject to oversight? (Kazakhstan)

Does KMG have clearly defined roles? (Tadjikistan)