Embed Size (px)

Citation preview

2012

EXECUTIVE OVERVIEW & SURVEY FINDINGS

SALESPULSESURVEY

2012 Executive Summary

2012 SALES PULSE SURVEY RESULTS2

Each November Alexander Group conducts the Sales Pulse Survey (SPS) in conjunction with its Chief Sales Executive Forum. 2011/2012 SPS findings indicate that growth ambitions continue to ascend despite expectations for on-going weakness in the economy. With a median 2012 growth objective of 10% how do participating executives plan to grow much faster than GDP? Consider the following:

1. High growth companies are twice as likely to invest significant dollars in their sales organizations.

2. High growth companies are planning to convert new accounts as their primary source of sales growth.

3. New accounts will be acquired from both the Global and National account segments.

4. Solution selling will lead the way in closing business at new accounts in all segments.

5. High growth companies are NOT depending on new products to drive growth.

6. High growth companies are investing to enrich sales processes and sales tools to deliver more value in highly competitive markets.

With growth expectations high, sales executives are taking care to identify high potential growth opportunities and invest in sales resources that can close business by delivering more value and better ROI. In many cases this means transforming sales processes and tools to better deliver problem solving expertise to customers that demand more substance from the partners they choose to do business with.

Sales process improvement is at the center of 2012 growth strategies that focus on value delivery

92COMPANIES

14INDUSTRIES

PARTICIPANTS BYINDUSTRY

BUSINESS SERVICES

MEDIA

HEALTH CARE

TELECOMMUNICATIONSSERVICES

TELECOMMUNICATIONS EQUIPMENT

ELECTRONICS

COMPUTER SERVICES

COMPUTER SOFTWARE

COMPUTER HARDWARE

CHEMICALS

FOOD

OTHER

PHARMACEUTICALS MANUFACTURING

CONSTRUCTION

FINANCIAL SERVICES

INSURANCE

AUTOMOTIVE & TRANSPORT

INDUSTRIAL MANUFACTURING

TRANSPORTATIONSERVICES

CONSUMER PRODUCTS MANUFACTURERS

SECURITY PRODUCTS & SERVICES

AEROSPACE & DEFENSE

3 2012 SALES PULSE SURVEY RESULTS

PARTICIPANTS BYREVENUE IN 2012

$100 MILLION OR LESS

$501 MILLION - $1 BILLION$1.01 BILLION - $5 BILLION

>$5 BILLION

$101 MILLION - $500 MILLION

13%

18%

11%

37%

27%

75%WERE FROM COMPANIES WITH

MORE THAN $500 MILLIONIN REVENUE

4 2012 SALES PULSE SURVEY RESULTS

2012 Sales Leader Expectations

OVERALL BUSINESS CONDITIONS

MY COMPANY

OVERALL ECONOMY

DECLINE IN 2012

Sales Leaders are optimistic about their performance in 2012Less optimistic about the business environment and overall economy

5

3%10%

17%

REMAINS THE SAME

22%

55%52%

GROWTH IN 2012

75%

35% 31%

Looking ahead, do you think that a year from now

your company’s year-to-date sales will be greater

than, less than or about the same as right now?

When considering business conditions overall, do

you think that companies will see increased,

decreased or about the same amount of sales

opportunities over the next four quarters?

When considering business conditions in the

country as a whole, do you think that over the

next year we will see economic growth, decline or

no change?

2012 SALES PULSE SURVEY RESULTS

SALES RESULTS 2011 vs 2010

BETTER THAN THIS TIME LAST YEAR

ABOUT THE SAME

WORSE THANPREVIOUS YEAR

50%32%

18%

50%EXPECTED IMPROVED RESULTS IN

2011 COMPARED TO 2010

Q: When considering your

organization’s 2011 performance

against your annual 2011 sales

plan, would you say that current

sales outcomes are better than,

worse than, or about the same as

this time last year?

6 2012 SALES PULSE SURVEY RESULTS

PERCENT OF SALES LEADERS WHO…

82%

61%

75% 7%

35%

55% 31%

68% 58%

FOR 2011 FOR 2012 CHANGE

7

…Forecast growth compared to previous year

…Expect more sales opportunities for their businesses

…Expect overall economic conditions to improve

…Plan to invest more in sales

26%

24%

10%

Sales Leaders are less enthusiastic when compared to last yearExpectations for the general economy are the most pessimistic

2012 SALES PULSE SURVEY RESULTS

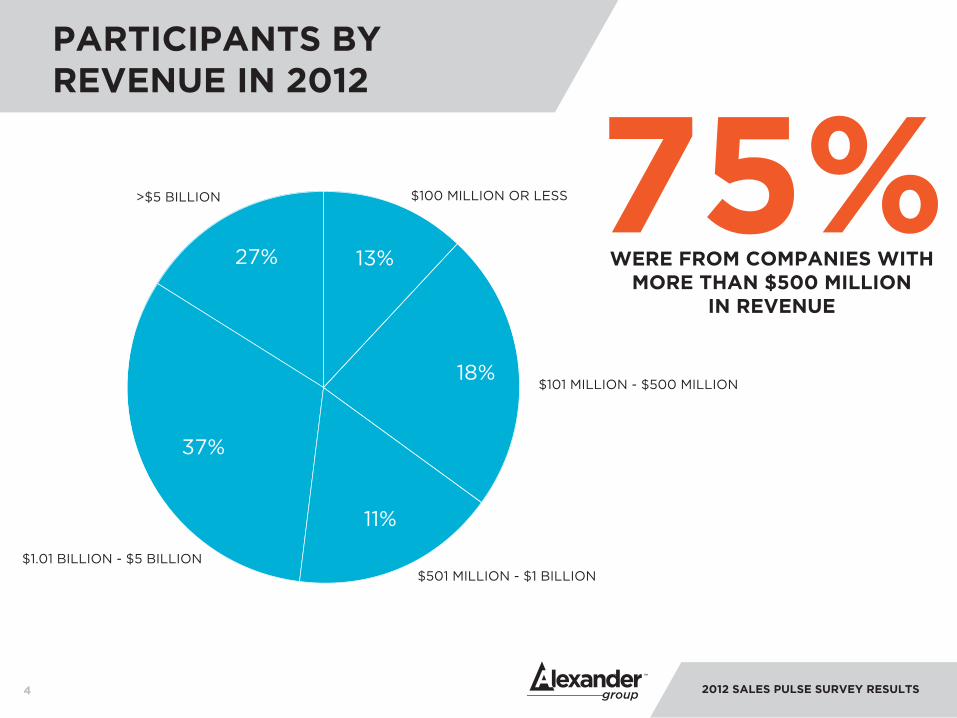

NUMBER OF COMPANIES BY 2012 GROWTH RATE

8

Sales Leaders overall expect a return to double-digit growth in 2012Though there continues to be a wide range of growth expectations

<=0

51-5%

28

6-10%

34

11-19%

20

>=20%

17

2012 SALES PULSE SURVEY RESULTS

PERCENT OF COMPANIES PLANNING TO INVEST MORE IN THEIR SALES ORGANIZATION

9

PLANNEDGROWTH RATE

<=0% 0%

1-5%

6-10%

11-19%

>=20%

High Growth companies are almost 2x as likely to invest in salesLow Growth companies will need a plan to return to higher revenue growth

39%

71%

70%

65%

2012 SALES PULSE SURVEY RESULTS

MEDIAN SALES INVESTMENTBY GROWTH CATEGORY

10

-10

-5

0

5

10

15

20

SALES BUDGET CHANGE SALES HEADCOUNT CHANGE

High Growth companies invest more in their sales budget and headcount, but this investment is still below growth goals

<=0% 1-5% 6-10% 11-19% >=20%

2012 SALES PULSE SURVEY RESULTS

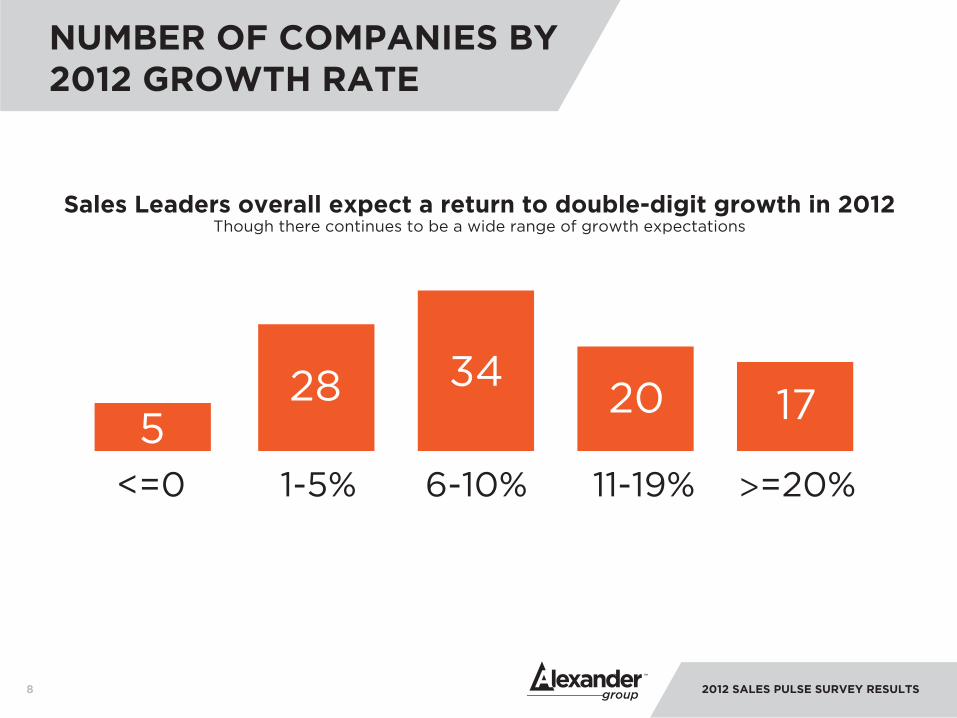

11

Sales Leaders will employ a mix of sales strategies for 2012New Business Acquisition and Cross-Selling are the most critical growth drivers

Global

SALES STRATEGY

NationalCustomerSegment

Small/MediumBusiness

5%

6%

5%

16%

23%

4%

15%

13%

13%

MAINTAIN A HIGHER PERCENTAGE OF

CURRENT CUSTOMERS

CROSS-SELL EXISTING

CUSTOMERS

NEW BUSINESS ACQUISITION

SALES STRATEGY

2012 SALES PULSE SURVEY RESULTS

12

High Growth companies expect new business acquisition to drive more growth, particularly

for global accounts

Low Growth companies are more focused on cross-selling to existing customers to

drive growth.

High Growth Companies (>10%) Low Growth Companies (<=10%)

HIGH GROWTH COMPANIESVS LOW GROWTH COMPANIES

Maintain a Higher Percentage of

Current Customers

Cross-sell Existing

Customers

NEW BUSINESS ACQUISITION

Global 0%

3%

3%

8%

19%

8%

25%

17%

17%

National

Small/MediumBusiness

Maintain a Higher Percentage of

Current Customers

CROSS-SELL EXISTING

CUSTOMERS

New Business Acquisition

Global 7%

7%

6%

21%

25%

1%

10%

10%

10%

National

Small/MediumBusiness

2012 SALES PULSE SURVEY RESULTS

13

More High Growth companies expect business to come from new customer acquisition

<=0

20%

20%

60%

1-5% 6-10% 11-19% >=20%

25%

29%

46% 47%

35%

18%45%

55%

13%

25%

62%

MAINTAIN A HIGH % OFCURRENT CUSTOMERS

CROSS-SELL EXISTING CUSTOMERS

NEW BUSINESS ACQUISITION

PLANNED GROWTH RATE

2012 SALES PULSE SURVEY RESULTS

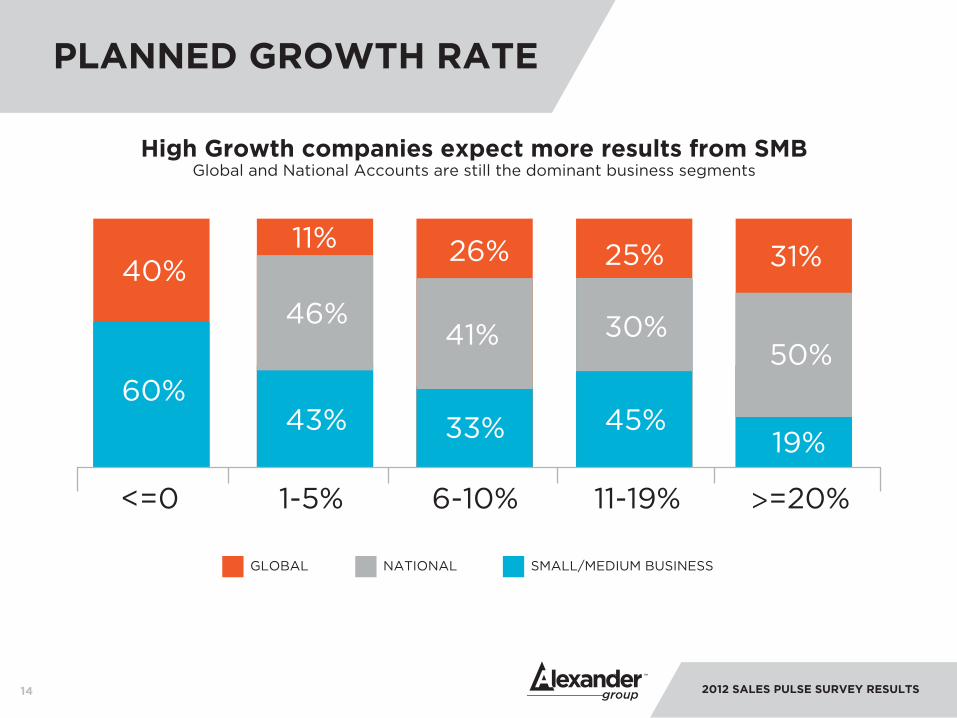

14

PLANNED GROWTH RATE

<=0

40%

60%

1-5% 6-10% 11-19% >=20%

11%

46%

43%

41%

33%

26% 25%

30%

45%

31%

19%

50%

GLOBAL NATIONAL SMALL/MEDIUM BUSINESS

High Growth companies expect more results from SMBGlobal and National Accounts are still the dominant business segments

2012 SALES PULSE SURVEY RESULTS

15

SOLUTION SELLING

Solution Selling is a major lever to “add value” for customersSales Leaders expect to better understand customer needs in 2012

36% of Executives specifically mentioned different aspects of “solution selling” as the way their organization will add value for customers in 2012.

2012 SALES PULSE SURVEY RESULTS

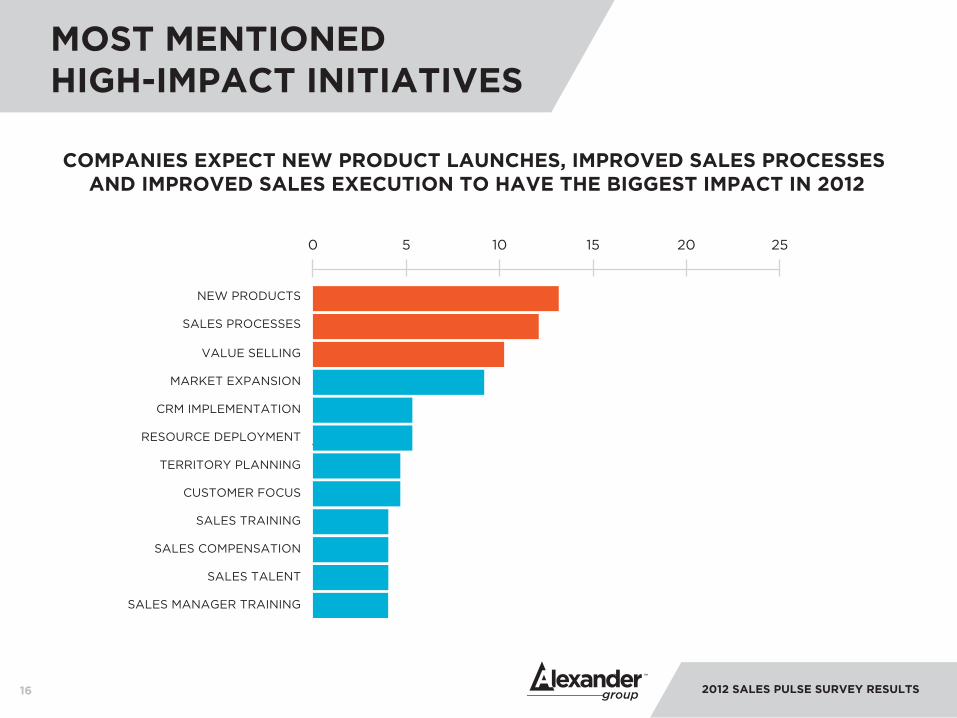

MOST MENTIONED HIGH-IMPACT INITIATIVES

NEW PRODUCTS

SALES PROCESSES

VALUE SELLING

MARKET EXPANSION

CRM IMPLEMENTATION

RESOURCE DEPLOYMENT

TERRITORY PLANNING

CUSTOMER FOCUS

SALES TRAINING

SALES COMPENSATION

SALES TALENT

SALES MANAGER TRAINING

COMPANIES EXPECT NEW PRODUCT LAUNCHES, IMPROVED SALES PROCESSES AND IMPROVED SALES EXECUTION TO HAVE THE BIGGEST IMPACT IN 2012

0 5 10 15 20 25

16 2012 SALES PULSE SURVEY RESULTS

17

MOST MENTIONED

NEW PRODUCTS

SALES PROCESSES

CRM IMPLEMENTATION

MARKET EXPANSION

TERRITORY PLANNING

VALUE SELLING

SALES MANAGER TRAINING

SALES PROCESSES

MARKET EXPANSION

NEW PRODUCTS

CRM IMPLEMENTATION

RESOURCE DEPLOYMENT

VALUE SELLING

PRICING

TERRITORY PLANNING

CUSTOMER FOCUS

VALUE SELLING

NEW PRODUCTS

SALES PROCESSES

SALES TALENT

SALES COMP

MARKET EXPANSION

NEW CHANNELS

RESOURCE DEPLOYMENT

NEW CUSTOMERSLEAST MENTIONED

Among High Growth companies customer focused sales processes and value selling are seen to be the keys to success

LOW GROWTH<6%

MEDIUM GROWTH6-10%

HIGH GROWTH>10%

THE KEYS TO SUCCESS

2012 SALES PULSE SURVEY RESULTS

ABOUT ALEXANDER GROUP

Alexander Group provides sales management consulting services to the

world’s leading sales organizations, serving Global 2000 companies from

across all industries. Founded in 1985, Alexander Group has a highly

sophisticated set of best practices to grow sales, as well as the industry’s

richest database, with detailed analytics on more than 100,000 sales

representatives from over 250 companies.

Alexander Group combines deep experience and data-driven insights to help

sales leaders make informed decisions that propel growth.

For more information on Alexander Group visit www.alexandergroup.com

2012 SALES PULSE SURVEY RESULTS28