Embed Size (px)

Citation preview

Is the Indian Automation and Process Control Industry on the Verge of Rapid Growth?

Srivatsan Murali,Research Analyst

Economics Research and AnalyticsSeptember 11, 2008

2

Focus Points

2. Political Overview

1. Industry Segmentation

4. Manufacturing Overview

Metals and Mining

Power, Oil and Gas

5. End User Analysis

Automobiles

Chemicals, Pharmaceuticals and Food Processing

6. Growth Opportunities

3. Economic Overview

3

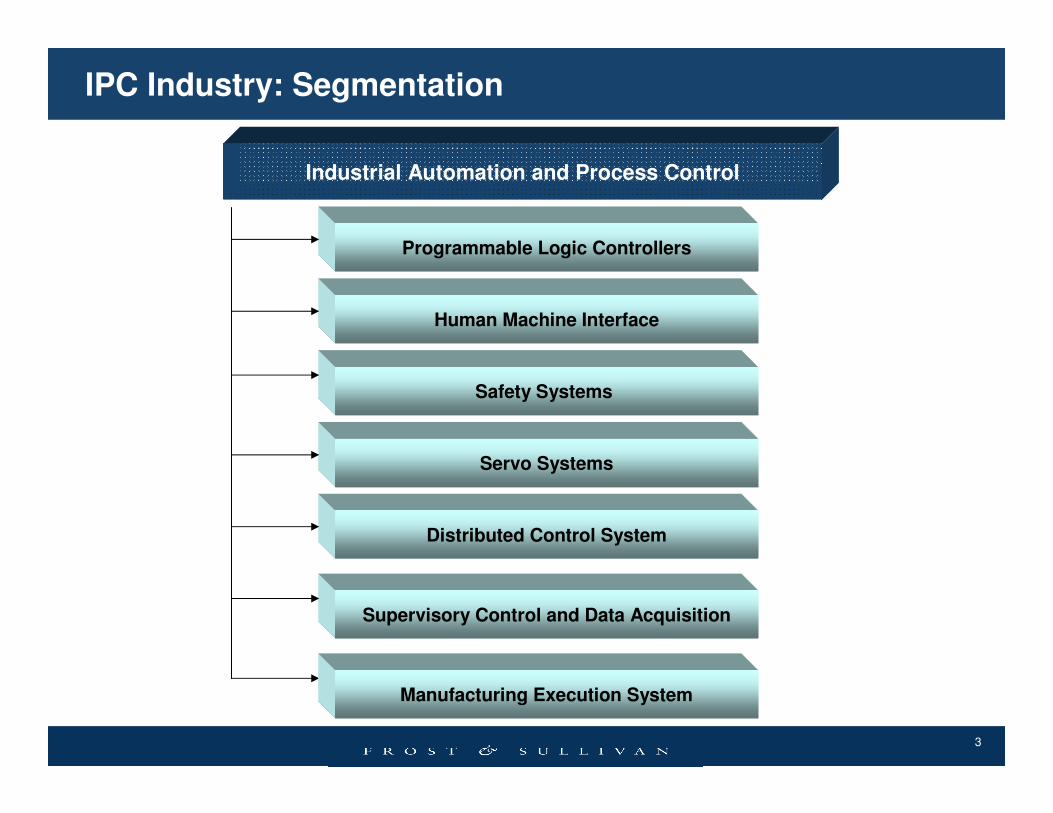

IPC Industry: Segmentation

Industrial Automation and Process Control

Programmable Logic Controllers

Human Machine Interface

Safety Systems

Servo Systems

Distributed Control System

Manufacturing Execution System

Supervisory Control and Data Acquisition

4

Political Overview

Composition of the Parliament (2008)

Elections 2009

� Hung Assembly � Emergence of BSP on the national stage� Coalition Government: Holding up reforms, � Slowdown in growth� Unlikely to see progress on key reform area of

labor laws.

Key Areas for Governance

� Currently infrastructure requires $ 300 Billion

� Investment reforms� Reforming labor laws � Pension reforms� Banking reforms� Reign in inflation

Current Situation

� Prospect of reforms being passed because left not in government.

� Political uncertainty and current coalition holding up key reforms essential for growth.

� Government adopting socialist policy with a view towards elections.

� Interest groups pressurizing government.

Source: Frost & Sullivan

Left Front

NDA

Others

UPA Plus

Allies

•UPA: United Progressive Alliance

•NDA: National Democratic Alliance

•Others: BSP, TDP and Independents

5

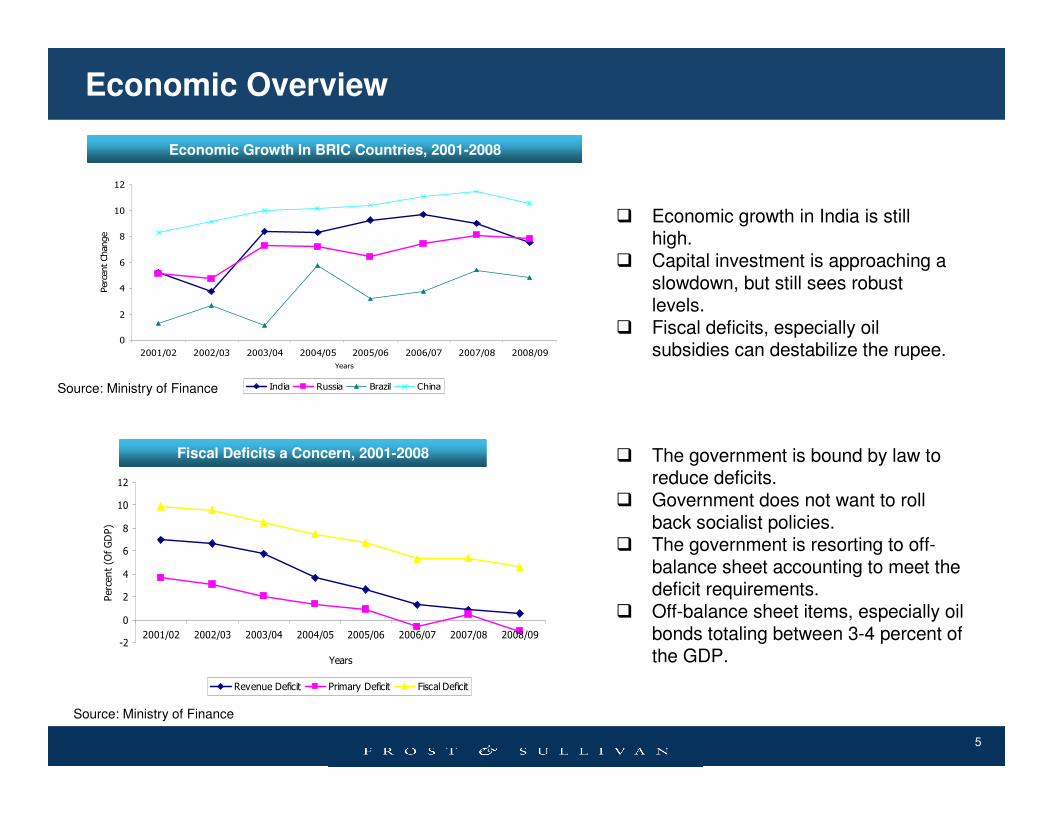

Economic Overview

� Economic growth in India is still high.

� Capital investment is approaching a slowdown, but still sees robust levels.

� Fiscal deficits, especially oil subsidies can destabilize the rupee.

Fiscal Deficits a Concern, 2001-2008

Economic Growth In BRIC Countries, 2001-2008

0

2

4

6

8

10

12

2001/02 2002/03 2003/04 2004/05 2005/06 2006/07 2007/08 2008/09

Years

Perc

en

t C

han

ge

India Russia Brazil China

-2

0

2

4

6

8

10

12

2001/02 2002/03 2003/04 2004/05 2005/06 2006/07 2007/08 2008/09

Years

Pe

rce

nt

(Of

GD

P)

Revenue Deficit Primary Deficit Fiscal Deficit

Source: Ministry of Finance

Source: Ministry of Finance

� The government is bound by law to reduce deficits.

� Government does not want to roll back socialist policies.

� The government is resorting to off-balance sheet accounting to meet the deficit requirements.

� Off-balance sheet items, especially oil bonds totaling between 3-4 percent of the GDP.

6

0

2

4

6

8

10

12

14

5/1/2008 2/2/2008 1/3/2008 29/03/2008 26/04/2008 24/05/2008 21/06/2008 19/07/2008

Percent

Inflation CRR Repo Rate

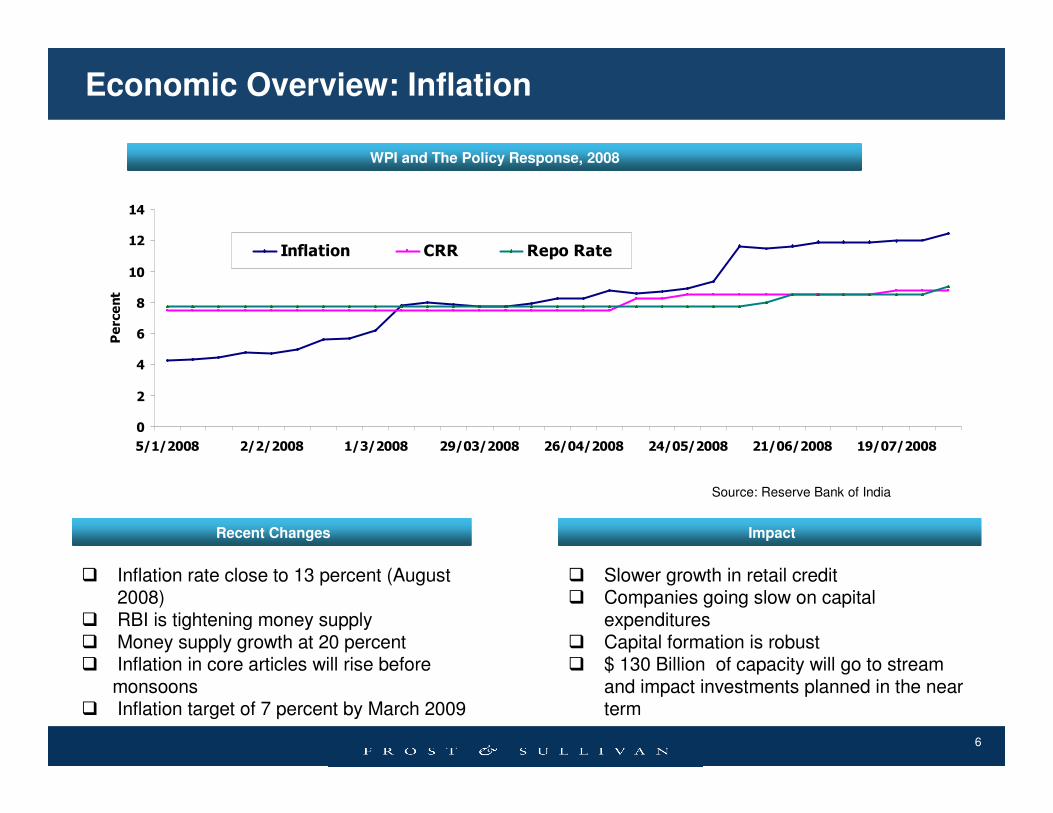

Economic Overview: Inflation

WPI and The Policy Response, 2008

� Inflation rate close to 13 percent (August 2008)

� RBI is tightening money supply� Money supply growth at 20 percent� Inflation in core articles will rise before

monsoons� Inflation target of 7 percent by March 2009

� Slower growth in retail credit � Companies going slow on capital

expenditures� Capital formation is robust� $ 130 Billion of capacity will go to stream

and impact investments planned in the near term

Impact

Source: Reserve Bank of India

Recent Changes

7

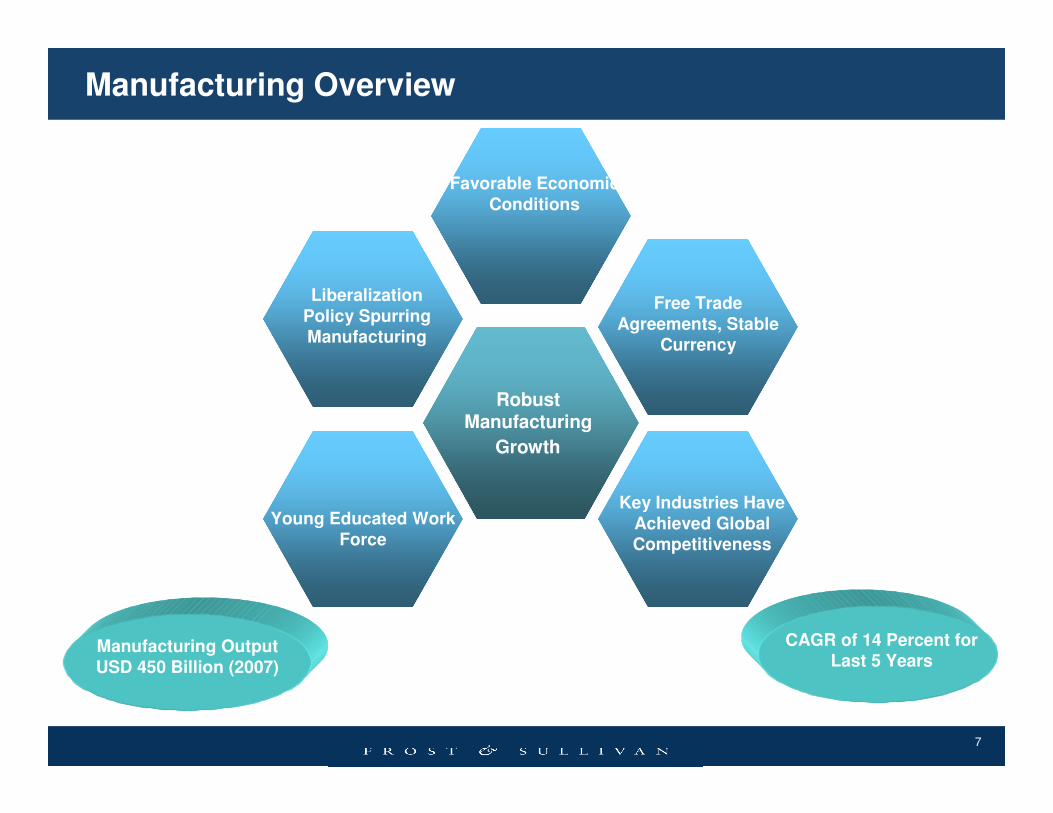

Manufacturing Overview

Liberalization

Policy Spurring Manufacturing

Favorable Economic

Conditions

Free Trade

Agreements, Stable Currency

Key Industries Have

Achieved Global Competitiveness

Young Educated Work

Force

Rapid Expansion in Manufacturing. High Growth anticipated

Manufacturing Output

USD 450 Billion (2007)

CAGR of 14 Percent for Last 5 Years

Robust Manufacturing

Growth

8

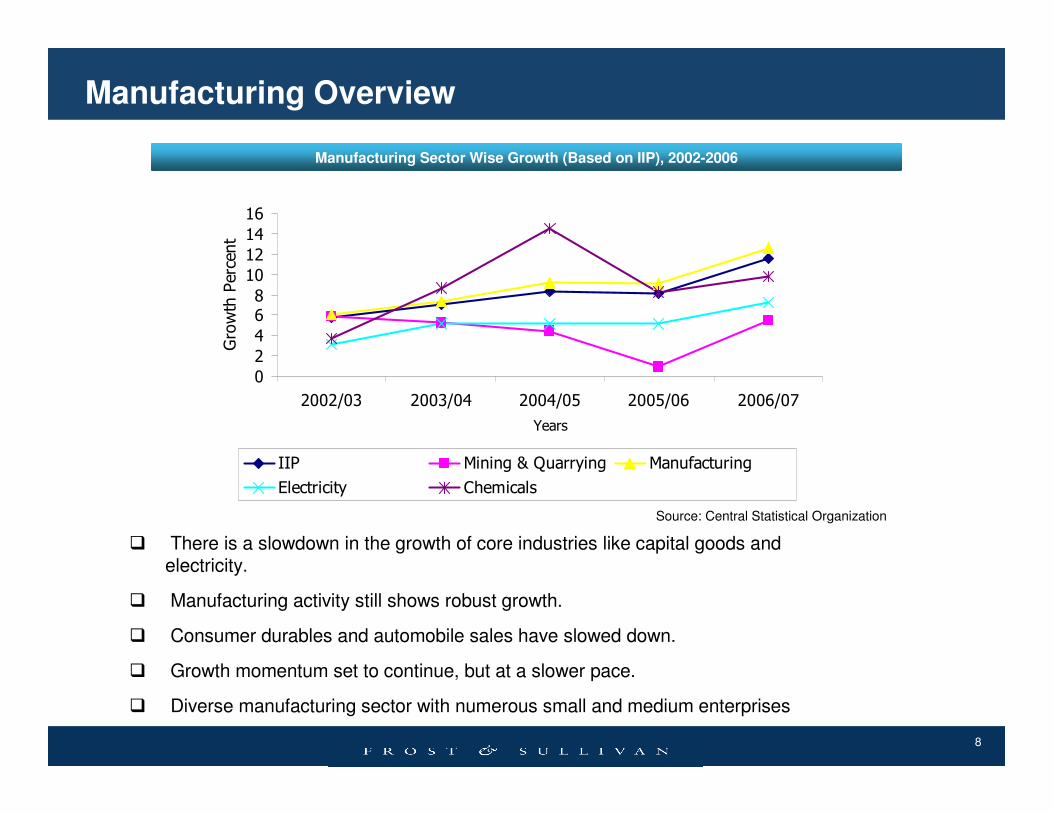

Manufacturing Overview

� There is a slowdown in the growth of core industries like capital goods and electricity.

� Manufacturing activity still shows robust growth.

� Consumer durables and automobile sales have slowed down.

� Growth momentum set to continue, but at a slower pace.

� Diverse manufacturing sector with numerous small and medium enterprises

Manufacturing Sector Wise Growth (Based on IIP), 2002-2006

0

2

4

68

10

12

14

16

2002/03 2003/04 2004/05 2005/06 2006/07

Years

Gro

wth

Pe

rce

nt

IIP Mining & Quarrying Manufacturing

Electricity Chemicals

Source: Central Statistical Organization

9

Manufacturing Investment

Investment, 2000-2008

Source: Ministry of Finance

-40

-20

0

20

40

60

80

100

120

2000/01 2001/02 2002/03 2003/04 2004/05 2005/06 2006/07 2007/08 2008/09

Percent

Gross Domestic Capital Formation Private Capital Formation

� Investment has been volatile to interest rates.

� Private investment has been the engine of capital formation in the country.

� Capital expenditure by listed firms showed a 40 percent increase last year.

� Capital expenditure is anticipated to drop by 30 percent in the year 2009.

� This slowdown is on the account of increasing cost of capital and global liquidity conditions.

� Liberalized mining law key stimulus for automation end-users.

10

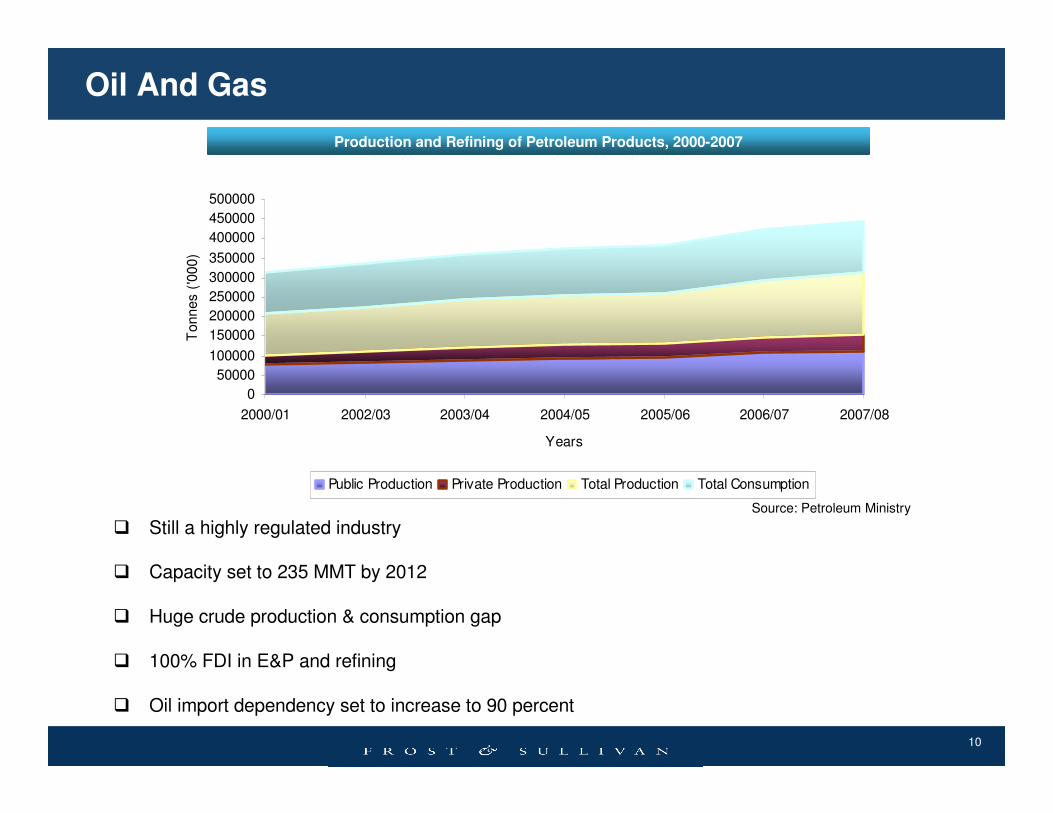

Oil And Gas

� Still a highly regulated industry

� Capacity set to 235 MMT by 2012

� Huge crude production & consumption gap

� 100% FDI in E&P and refining

� Oil import dependency set to increase to 90 percent

Production and Refining of Petroleum Products, 2000-2007

0

50000

100000

150000

200000

250000

300000

350000

400000

450000

500000

2000/01 2002/03 2003/04 2004/05 2005/06 2006/07 2007/08

Years

Tonn

es (

'000

)

Public Production Private Production Total Production Total Consumption

Source: Petroleum Ministry

11

Oil And Gas

� Demand supply gap in gas set to rise to 154.9 MMSCMD in 2011 and to 221.0 & MMSCMD in 2025

� 100% FDI in exploration and production

� Huge demand for gas from captive power plants

� Pricing issue for gas still remains to be sorted out

� The development of a national grid creates huge investment opportunity.

Natural Gas Snapshot,2002-2007

0

500

1000

1500

2002 2003 2004 2005 2006 2007

Years

Qu

an

tity

(B

illio

n

Cu

bic

Me

ters

)

Onshore (Reserves) Offshore (reserves)

Total (Reserves) Total Production

Total Consumption

Source: Petroleum Ministry

12

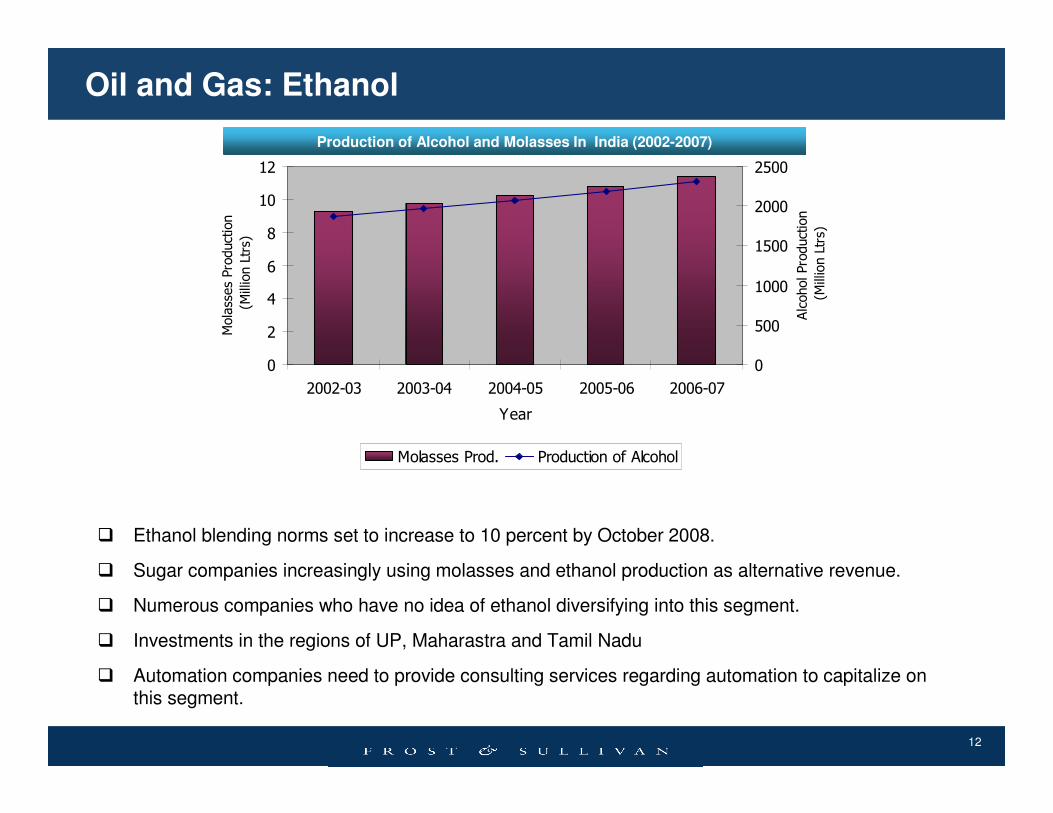

Oil and Gas: Ethanol

0

2

4

6

8

10

12

2002-03 2003-04 2004-05 2005-06 2006-07

Year

Mo

lass

es

Pro

du

ctio

n

(M

illio

n L

trs)

0

500

1000

1500

2000

2500

Alc

oh

ol

Pro

du

ctio

n

(M

illio

n L

trs)

Molasses Prod. Production of Alcohol

Production of Alcohol and Molasses In India (2002-2007)

� Ethanol blending norms set to increase to 10 percent by October 2008.

� Sugar companies increasingly using molasses and ethanol production as alternative revenue.

� Numerous companies who have no idea of ethanol diversifying into this segment.

� Investments in the regions of UP, Maharastra and Tamil Nadu

� Automation companies need to provide consulting services regarding automation to capitalize on this segment.

13

0

20000

40000

60000

80000

100000

120000

2000/01 2001/02 2002/03 2003/04 2004/05 2005/06 2006/07

Years

Qu

an

tity

(M

Ws)

0

2

4

6

8

10

12

14

16

Pe

rce

nta

ge

Peak Demand Peak Met Peak Shortage

30538

40425 41110

78700

1083219119 21180

16423

0

20000

40000

60000

80000

100000

8th Plan 9th Plan 10th Plan 11th Plan

Period

Ta

rge

t (M

Ws)

0

10

20

30

40

50

60

Pe

rce

nt

Target Achieved Achievement Percent

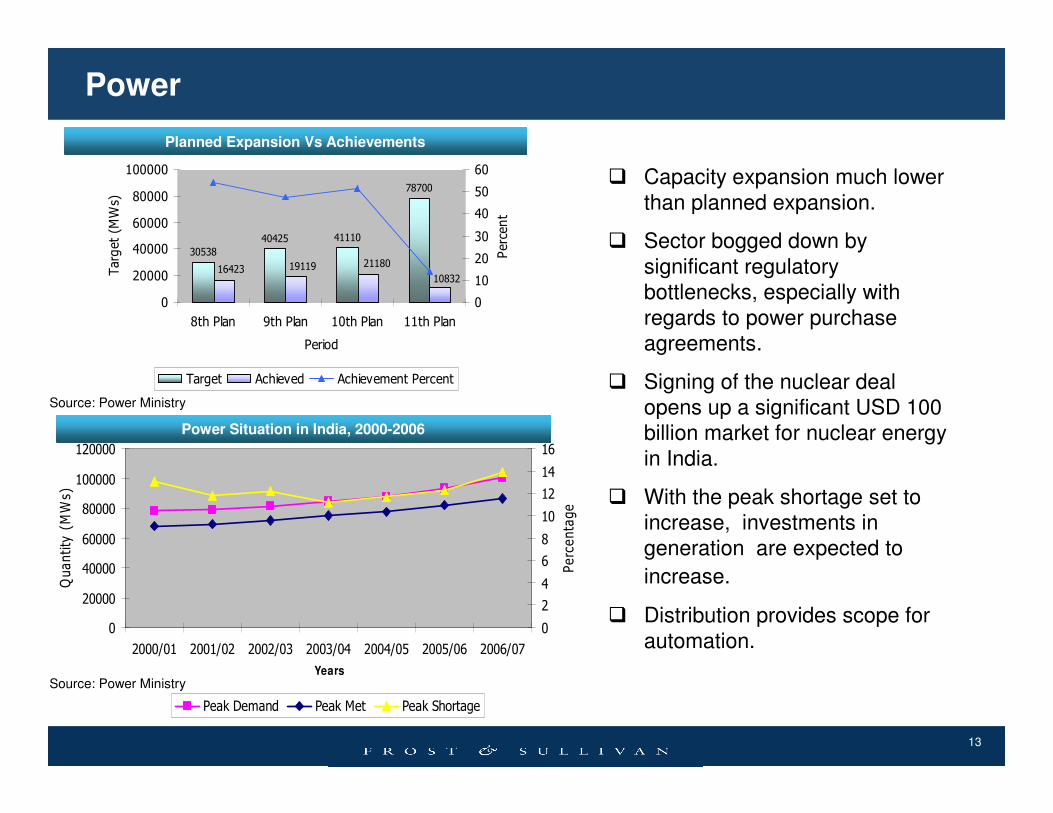

Power

Planned Expansion Vs Achievements

Power Situation in India, 2000-2006

Source: Power Ministry

Source: Power Ministry

� Capacity expansion much lower than planned expansion.

� Sector bogged down by significant regulatory bottlenecks, especially with regards to power purchase agreements.

� Signing of the nuclear deal opens up a significant USD 100 billion market for nuclear energy in India.

� With the peak shortage set to increase, investments in generation are expected to

increase.

� Distribution provides scope for automation.

14

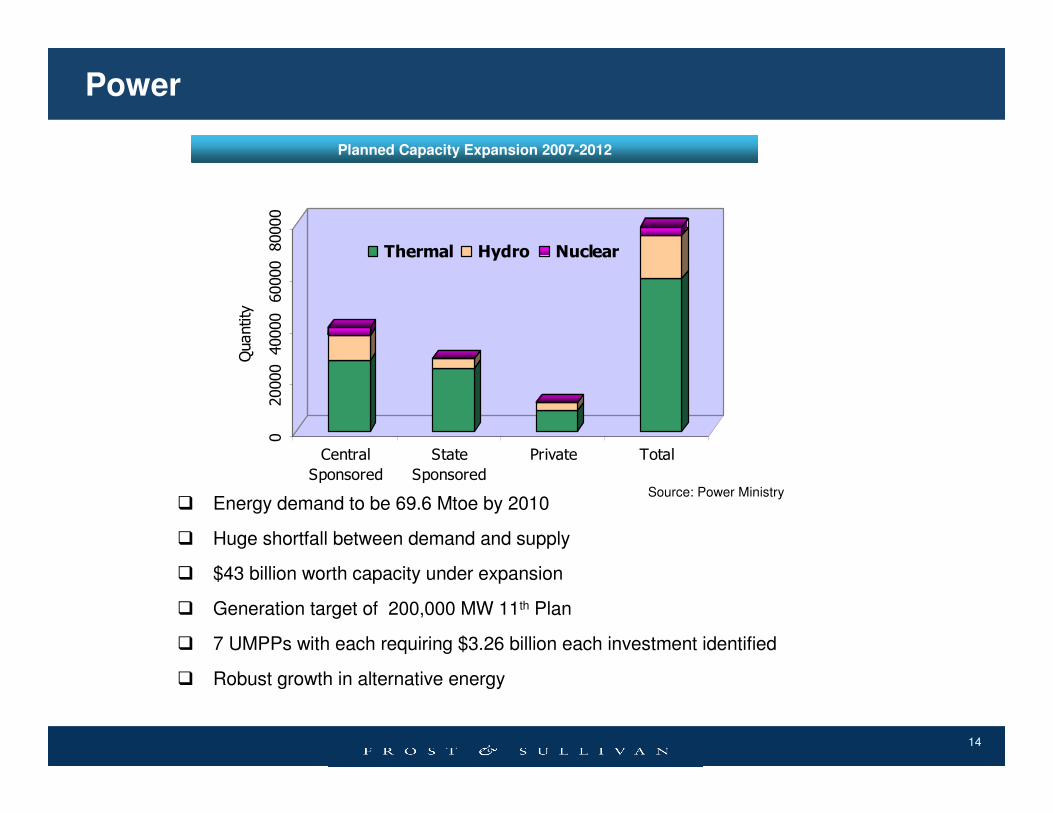

Power

Planned Capacity Expansion 2007-2012

� Energy demand to be 69.6 Mtoe by 2010

� Huge shortfall between demand and supply

� $43 billion worth capacity under expansion

� Generation target of 200,000 MW 11th Plan

� 7 UMPPs with each requiring $3.26 billion each investment identified

� Robust growth in alternative energy

Source: Power Ministry

02

00

00

40

00

06

00

00

80

00

0

Qu

an

tity

Central

Sponsored

State

Sponsored

Private Total

Thermal Hydro Nuclear

15

Metals

0

10

20

30

40

50

60

2002/03 2003/04 2004/05 2005/06 2006/07 2007/08 (April-

December)

Years

Ou

tpu

t ('

00

00

00

) T

on

ne

s

Crude Steel Production Finished Steel Including Alloys Production Finished Steel Including Alloys Consumption

Finished Steel Including Alloys Import Finished Steel Including Alloys Export

� Set to become second largest producer of steel

� Capacity expansion to 124 million Tons by 2011-12

� 194 MOUs signed to establish new plants

� Total Investment USD 140 billion by 2012

Steel Production,2002-2007

Non Ferrous Metals Production, 2002-2006

� Power sector attracting investments leading to increased aluminum demand

� Copper demand boosted by electronics industry

� Consolidation and expansion in non-Ferrous Metals

� Reduction in import duties� Growth in steel production leading to

zinc demand

0

500000

1000000

1500000

2000000

2500000

3000000

2002/03 2003/04 2004/05 2005/06 2006/07

Year

Pro

du

ctio

n (

To

nn

es)

Zinc Production Copper Production Aluminium Production

Source: Steel Ministry

Source: Ministry of Mines & Minerals

16

0

200000

400000

600000

800000

1000000

1200000

1400000

1600000

1800000

2001 2002 2003 2004 2005 2006 2007

Years

Ou

tpu

t (U

nit

s)

0

5

10

15

20

25

30

35

Perc

en

t

Cars Commercial Vehicles Growth

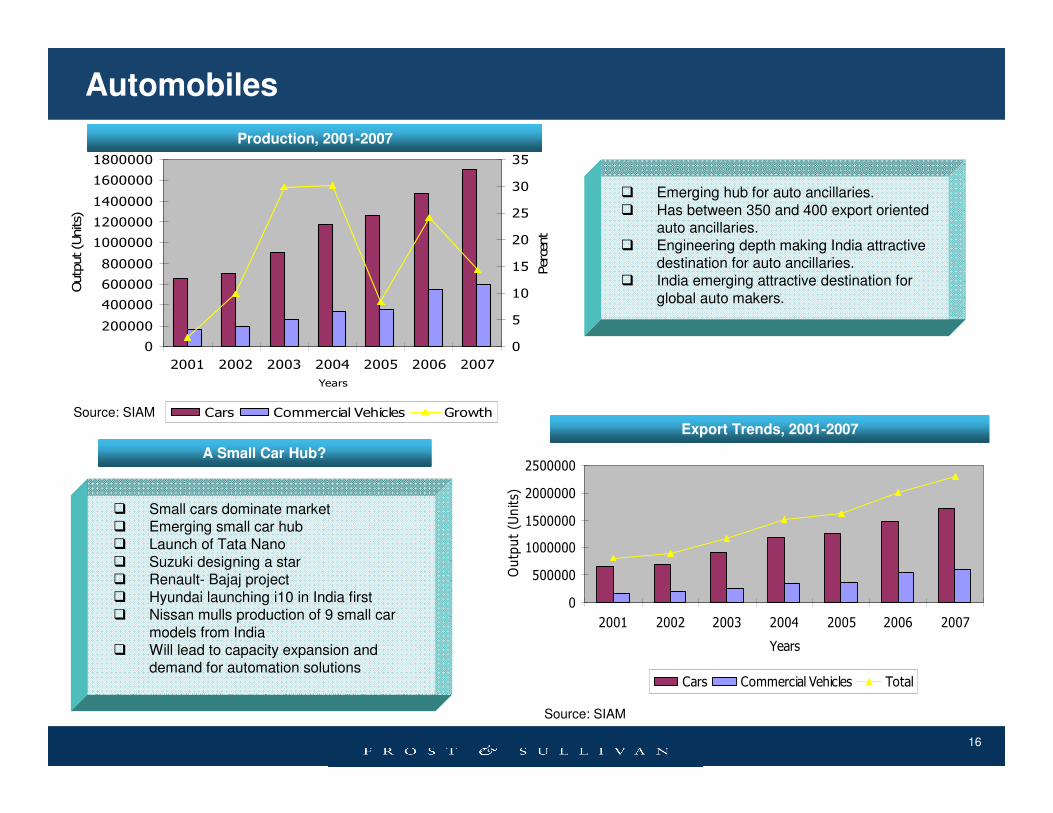

Automobiles

� Small cars dominate market � Emerging small car hub � Launch of Tata Nano� Suzuki designing a star � Renault- Bajaj project � Hyundai launching i10 in India first� Nissan mulls production of 9 small car

models from India� Will lead to capacity expansion and

demand for automation solutions

� Emerging hub for auto ancillaries. � Has between 350 and 400 export oriented

auto ancillaries. � Engineering depth making India attractive

destination for auto ancillaries. � India emerging attractive destination for

global auto makers.

A Small Car Hub?

Production, 2001-2007

Export Trends, 2001-2007

0

500000

1000000

1500000

2000000

2500000

2001 2002 2003 2004 2005 2006 2007

Years

Ou

tpu

t (U

nit

s)

Cars Commercial Vehicles Total

Source: SIAM

Source: SIAM

17

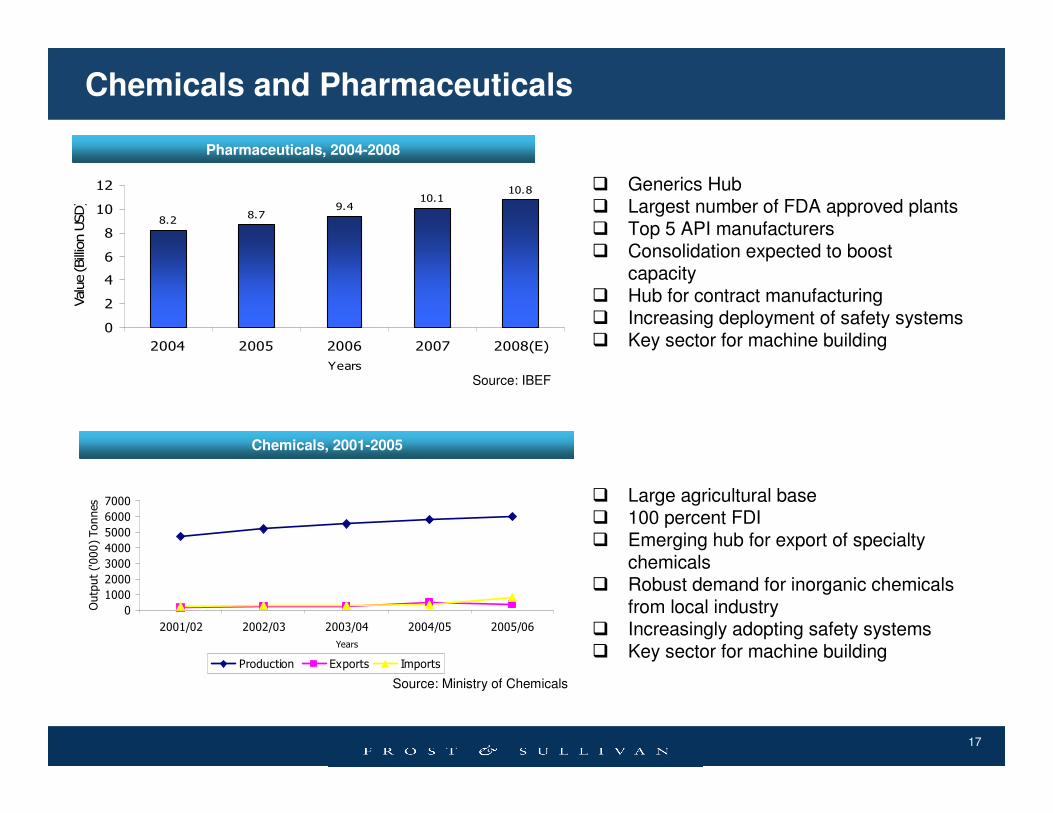

8.28.7

9.410.1

10.8

0

2

4

6

8

10

12

2004 2005 2006 2007 2008(E)

Years

Valu

e (

Bill

ion

US

D)

0

1000

2000

3000

4000

5000

6000

7000

2001/02 2002/03 2003/04 2004/05 2005/06

Years

Ou

tpu

t ('

00

0)

To

nn

es

Production Exports Imports

Chemicals and Pharmaceuticals

� Generics Hub � Largest number of FDA approved plants � Top 5 API manufacturers� Consolidation expected to boost

capacity � Hub for contract manufacturing � Increasing deployment of safety systems� Key sector for machine building

Pharmaceuticals, 2004-2008

� Large agricultural base � 100 percent FDI � Emerging hub for export of specialty

chemicals � Robust demand for inorganic chemicals

from local industry� Increasingly adopting safety systems� Key sector for machine building

Chemicals, 2001-2005

Source: Ministry of Chemicals

Source: IBEF

18

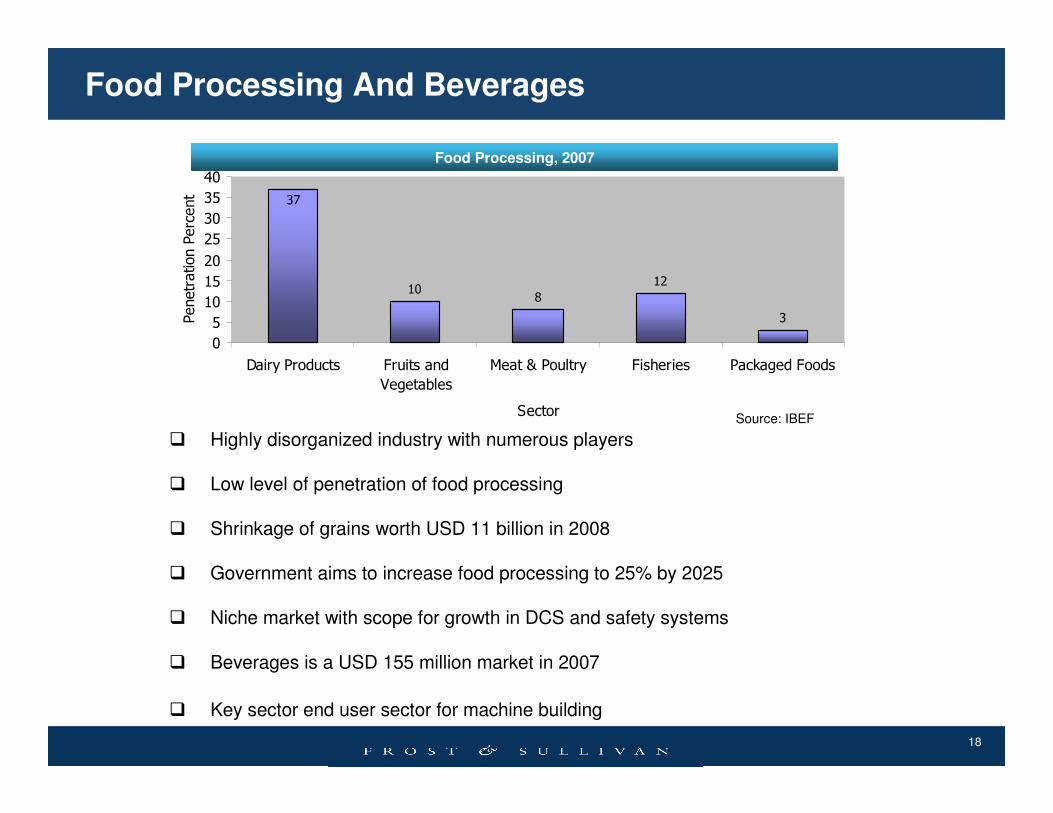

Food Processing And Beverages

Food Processing, 2007

� Highly disorganized industry with numerous players

� Low level of penetration of food processing

� Shrinkage of grains worth USD 11 billion in 2008

� Government aims to increase food processing to 25% by 2025

� Niche market with scope for growth in DCS and safety systems

� Beverages is a USD 155 million market in 2007

� Key sector end user sector for machine building

Source: IBEF

108

12

3

37

0

5

10

15

20

25

30

35

40

Dairy Products Fruits and

Vegetables

Meat & Poultry Fisheries Packaged Foods

Sector

Pe

ne

tra

tio

n P

erc

en

t

19

Growth Opportunities

PLC DCS SCADASafety Systems

MES

Oil and Gas Low High High Moderate High

Metals Moderate High HighNo ImpactNo Impact

Power Low High High No Impact High

Automotive High LowHigh Low Moderate

Chemicals High High Moderate HighHigh

Food Processing

High No Impact No Impact Moderate Moderate

High Low No Impact High Moderate

Key Sectors and Impact on Demand (Segment wise), 2008-2010

OEMS High No Impact No Impact No Impact No Impact

Servo Systems

High

No Impact

No Impact

No Impact

Moderate

No Impact

No Impact

No Impact

Pharma

20

Your Feedback is Important to Us

Growth Forecasts?

Competitive Structure?

Emerging Trends?

Strategic Recommendations?

Other?

Please inform us by taking our survey.

What would you like to see from Frost & Sullivan?

21

For Additional Information

• To leave a comment, ask the analyst a question, or receive the free audio segment that accompanies this presentation, please contact Stephanie Ochoa, Social Media Manager at (210) 247-2421, via email, [email protected], or on Twitter at http://twitter.com/stephanieochoa.