Embed Size (px)

DESCRIPTION

Presented by Colin McNaught, AEA 19 September 2012

Citation preview

Financing Renewable Energy

Session 1

Colin McNaught

Aim

Introduction of main finance options and key concepts

How finance options shape a project

Increase your fluency in finance matters

In short: How would you like to pay for that?

2

Scope

Focus is on renewable energy

– Solar, Wind, Hydro, Biomass etc.

– Investment up to around £10 million:

Wind: Up to 7 MW

Solar: Up to 6 MW (small projects)

Hydro: Up to 3 MW

Key concepts also apply to energy efficiency

3

My Background

Energy sector experience over 20 years

Energy efficiency, CHP & renewables

Financial models for wind, solar, anaerobic digestion

Background in engineering – so presenting finance from a different perspective

4

Your Background

Internal Finance?

5

External Finance?

Renewable Energy?

Mortgage?

Agenda for Part 1

The Drivers – why invest and finance a project?

Risk and Reward

Finance Options

Decision Tree

6

Types of Drivers

Reduce energy bills

Invest capital and generate financial returns

Reduce greenhouse gas emissions

Improve corporate image

Enhance energy security

Address fuel poverty

7

8

Motivation Main benefits Influence on the set up of the project

Energy bills

Reduction in energy bills

Hedging against future rises in energy costs

Finance option which maximises and retains the value of energy generation potential should be selected.

Finance must be set up so that developers can use the energy for their own use.

Projects that supply onsite energy demand will inherently offer this.

Investment returns

Financial returns

Greater rate of return than investment in core activities

Finance option which maximises the rate of return on investment should be selected.

Different financing options and choices of incentive should be explored to determine the option that maximises such returns, without incurring significant risks.

Greenhouse gas emissions

Reduction in greenhouse gas emissions

Reduction in carbon footprint

The selected finance option, and any incentives claimed, will need to allow the carbon value of the renewable energy generated to be claimed.

Energy from waste or biomass electricity projects that recover heat as well as generate electricity may offer this.

Corporate image

Improved public perception of environmental values of the organisation

Finance option needs to allow the developer sufficient control over real or perceived environmental risks.

Finance should be setup so that local benefits are easily discernible and communicated in an appropriate manner.

Wind or solar PV projects may provide this opportunity.

Energy Security

Reduction in dependence on fossil fuels and electricity supplies

Reduction of UK imports of energy

If energy security required on site, systems should be engineered so that they can operate without a grid supply. This will add capital costs and should be weighed against the cost of energy supply interruptions.

For biomass and energy from waste this will require on site storage of sufficient fuel.

Fuel poverty

Energy security for poorer communities

Reduction in energy costs and impact of price rises

Finance set up should allow benefits of the project, e.g. lower energy prices or a profit share, to be passed on to the communities in need.

For example, the roll out of solar PV to housing stock.

See Copy of Guide: Page 4

Types of Drivers

Reduce energy bills

Invest capital and generate financial returns

Reduce greenhouse gas emissions

Improve corporate image

Enhance energy security

Address fuel poverty

9

Most of these drivers are based on the income that can be earned

Income from renewables

Feed in Tariff (FIT)

Electricity systems up to 5 MW

Solar PV, Wind, Hydro, Anaerobic Digestion…

Tariff for 20 years

Inflation indexed once registered

But reduces for new schemes in future years

Export tariff

10

Feed in Tariff – Non domestic schemes (since April 2010)

Income from renewables

11

12

Technology Band (kW) Tariff (p/kWh)

Hydro

≤15 21

15-≤100 19.6

100-≤500 15.5

500-≤2000 12.1

2000-≤5000 4.48

Wind

≤1.5 21

>1.5-≤15 21

>15-≤100 21

>100-≤500 17.5

>500-≤1500 9.5

>1500-≤5000 4.48

Solar

≤4 15.44

>4-≤10 13.99

>10-≤50 13.03

>50-≤100 11.5

>100-≤150 11.5

>150-≤250 11

>250-≤5000 7.1

Standalone 7.1

Export All 4.5

Current FIT Subject to change depending on rate of market growth Solar PV needs to be on a building with an EPC of D or better to earn > 7.1 p

Income from renewables

Renewable Heat Incentive (RHI)

Heat systems

Biomass, Ground Source Heat Pumps, Solar thermal...

Tariff for 20 years

Inflation indexed

13

14

Technology Band (kWth) Tariff (p/kWh)

Commercial Biomass

≤200 Tier 1 8.3

≤200 Tier 2 2.1

> 200 < 1000 Tier 1 5.1

> 200 < 1000 Tier 2 2.1

> 1000 1.0

Ground Source Heat Pumps

≤100 4.7

> 100 3.4

Solar Thermal all 8.9

Biomethane/biogas all 7.1

Current RHI Tier 1: < 1314 hours full load Tier 2: > 1314 hours

RHI – Non domestic schemes (since Dec 2011)

Income from renewables

15

Risk & Reward

Risk increases the cost of finance, restricts the options for finance and adds to the cost of obtaining finance.

Identifying and managing risk will improve all these finance issues.

Risk management may involve a partnership approach.

16

Types of Risk

Financial risks, capital costs, energy prices, credit risks and inflation

Development risks, the costs of undertaking feasibility and the risk of planning

Construction risks, construction costs and long lead in times

Technology risks, particularly around efficiency and reliability of the technology

Operational risks, operational and maintenance costs, fuel availability

Policy risks, changes to renewable energy policy and incentive structures = investment returns

17

18

Risk Description

Economic / Financial

Capital costs higher than budget

Operational costs higher than budget (including maintenance, interest rates and insurance)

Cost of finance higher than expected

Borrowing conditions breached and associated risks

Risks associated with energy price fluctuations

Carbon prices reduce

New competitors in the market

Rate of inflation

Currency risks (if cross-border projects, or if purchasing components in other currencies)

Development

Cost of resource assessment and feasibility studies

Cost of environmental impact studies, EIA reports etc.

Cost of grid connection assessments

Planning time longer – delay in generation income / possible lower incentive value received

Failure to gain planning consent

Development partners disagree and part company

Construction

Planning consent requires cost to comply with conditions

Construction costs higher than budget

Construction time longer, delaying income from generation

Connection to energy networks delayed

Environmental / social

Costs of impact assessment (often a legal requirement) higher than budgeted

Issues identified during impact assessment delay or prevent project development

Costs of mitigation actions higher than budgeted

Technology Technology less efficient than predicted, so less energy produced

Technology less reliable than expected, less energy produced and higher maintenance costs

Operational

Renewable energy resource is lower than predicted (e.g. lower wind speed)

Access to site prevents repair or maintenance

Replacement parts required

Delays in supply or installation of spare parts

Fuel costs higher than expected (e.g. biomass fuel costs higher or there is an increase in price of electricity for heat pump projects)

Fuel supply problems, (poor quality or interruptions in delivery)

Site energy use falls, reducing the value of avoided energy costs

Policy

Planning requirements changed

Capital grants removed or oversubscribed

Revenue incentive removed or reduced in value

Eligibility for capital grants or revenue incentives changed

Finance sector regulatory changes, reducing availability, and cost, of finance

Tax treatment changed

See Copy of Guide: Page 5

Assessing Risk

For each type of risk:

– How could your project be affected?

– How significant are the impacts?

– How could you reduce the risks?

– How could someone else reduce the risks?

19

Financing options

20

Type Examples

Own development

– Internal funding

– Debt finance

– Equity finance

– Leasing

Partnership structures

– Partnership – majority control

– Partnership – equal split

– Partnership – minority control

Third party

– Land lease agreements

– Service concessions

– Energy Service Companies (ESCOs)

Own Development

Greatest control + Rewards + Risks

Internal Funding

– Business Case and internal reviews

– May not be deemed core business

External Funding

– Grants or low cost loans

– May be incompatible with income from the FIT or RHI etc

21

Own Development

Debt Finance:

– Full ownership of rewards and risks

– Likely to be part of capex (so need internal funds)

– Added costs of interest payments

– Capital repayments

– May be step in-rights

22

Partnership Development

Many different forms of partnership

Different structures, benefits and risks

Majority control

– You closely control risks

– Partners bring niche skills or assets

Minority control

– Driver is not financial – reward share is low

– Partner controls

– Can you gain what you hope for without control?

23

Third Party

Transfer of almost all aspects

Best when you lack the skills and capital

Small income – e.g. land rent

24

Service Concessions

Useful for the public sector

Grant a right to develop and exploit a resource

Often long term (25 years)

Payments made to public authority

– (fixed + revenue elements)

Used for energy from waste contracts and other renewables

25

Choosing an Option

What are your drivers and expected outcomes?

Does the arrangement provide these outcomes?

Which risks are retained?

26

27

Own Development Partnership Third Party

Financial risks

Rate of inflation / Capital costs / Operational costs / Cost of finance / Borrowing conditions

All risks typically held by the developer.

Will depend on which party has access to the lowest cost of capital.

All risks typically held by the third party.

Construction risks

Longer planning time / Planning consent difficulties or costs / Construction costs / Construction delays

All risks typically held by the developer.

Potential to include some risks (e.g. construction time) in the contracts let.

Will depend on which party has responsibility for construction of the project.

All risks typically held by the third party.

Potential to include some risks (e.g. construction time) in the contracts let.

Environmental / social risks

Impact assessment costs / Delays due to impact assessment / Costs of mitigation

All risks typically held by the developer.

Will depend on which party has responsibility for construction of the project.

All risks typically held by the third party.

Technology risks

Lower technology efficiency / Lower technology reliability

All risks typically held by the developer.

Potential to manage these through warranty with the equipment supplier and through performance contracts with the equipment supplier.

Will depend on the setup arrangements for the project. Who has the experience of the technology and the allocation of benefits (in terms of energy savings and revenue streams from generation)?

All risks typically held by the third party.

Potential to manage these through warranty with the equipment supplier and through performance contracts with the equipment supplier.

Operational risks

Lower levels of resource / Repair or maintenance issues or delays / Higher fuel costs / Lower site energy use falls / Carbon prices / Market competition

All risks typically held by the developer.

Will depend on which party has responsibility for construction of the project, as well as on the setup arrangements for allocation of benefits.

All risks typically held by the third party.

Policy risks

Planning requirements changed

Changes in requirements or eligibility for: Capital grants / Revenue incentives / Tax treatment

All risks typically held by the developer.

Policy risks are out of the hands of the developer or a third party. Neither can manage these. So, appropriate to share these risks.

All risks typically held by the third party.

Some tax benefits for the third party – e.g. enhanced capital allowances.

See Copy of Guide: Page 11

Sources of Finance

Two main options – but many variants

On Balance Sheet:

– Part of normal activities of the organisation

Off Balance Sheet:

– Separate company who owns the asset

28

On Balance Sheet

Balance Sheet Debt

– Usually through a bank as a loan

– Banks have the first claim on the assets of a business (senior debt).

– Bank loans are lower risk = lower returns

– Two main types of bank debt:

Non recourse

Recourse

29

On Balance Sheet

Non recourse debt:

– Loan is secured on the value & income of the asset

– Bank focuses on the value and income of the asset

Will it perform? Will it break down?

– Added scrutiny on the asset

– Not as suitable for higher risk projects

– Lender will limit the risk e.g. 75% debt

– Fixed at outset, all consents etc. needed

– Often needs special purpose company

– Higher costs to set up

– Typically larger projects (> £25 million)

30

On Balance Sheet

Recourse debt:

– Loan is secured by the borrower

– Bank focuses on the credit status of the borrower

– May suit higher risk projects

– May not suit borrowers with high levels of existing borrowing

31

Practical example

Non recourse finance

– Large wind investments typically need 1 year of on site wind measurements + detailed analysis

– Cautious use of wind data

– Adds to development cost

– Adds to development timescale

– May miss higher incentives

Recourse finance

– Farmers securing loan for 1 MW wind turbines against the farm

– No met mast = saving 18 months + costs

32

Lessons from Non Recourse

The tests are tougher because they are external

Debt Service Cover Ratio: The operating cash flow compared to the debt payments?

– Aim for at least 1.3 : 1 in any operating year

Loan Life Cover Ratio: The operating cash flow compared to the debt payments over the entire term of the loan?

– Aim for at least 1:5 : 1

33

Lessons from Non Recourse

Debt Service Reserve: The cash kept to cover debt payments:

– In Project Finance – typically 6 months debt payments

Maintenance Service Reserve: The cash kept to cover maintenance:

– Often at least 3 months

P90 output: The output which will be exceeded 90% of the time.

34

Output and Cash Flow

Three hydro schemes in Argyll

Use bank thinking in the business case

35

Balance Sheet Equity

Raise funds by creating and selling new shares

Shareholders gain via:

– A share of the operating profits (dividends)

– Capital value in price of shares

– Must be possible to sell share – all investors need an exit strategy

36

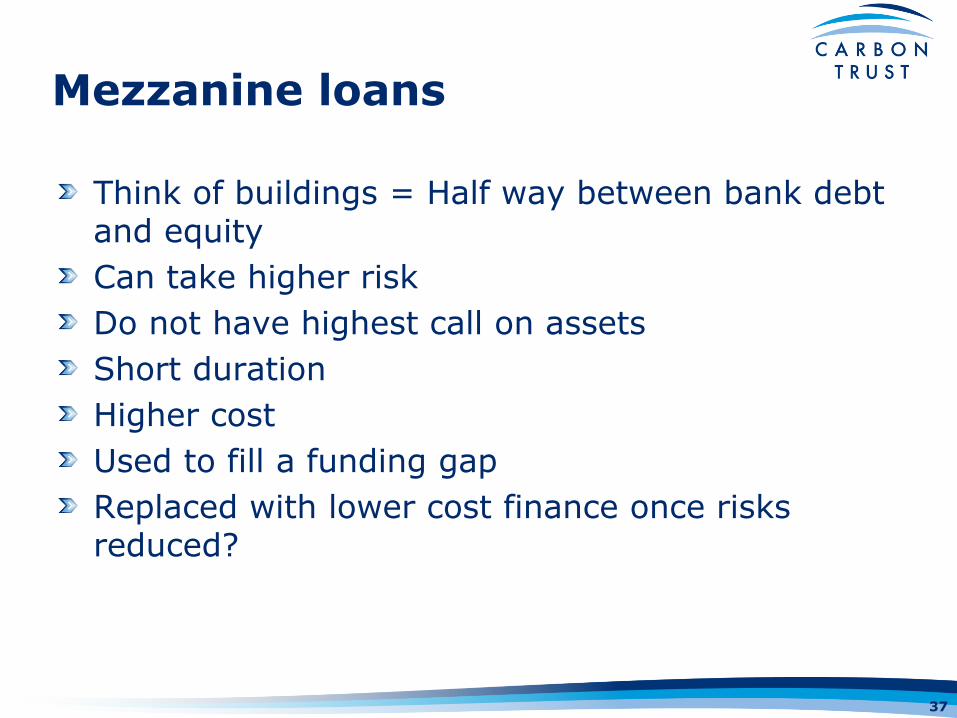

Mezzanine loans

Think of buildings = Half way between bank debt and equity

Can take higher risk

Do not have highest call on assets

Short duration

Higher cost

Used to fill a funding gap

Replaced with lower cost finance once risks reduced?

37

How much will finance cost?

38

Guide Page 14

Only an indication:

• Your project, your risks, your security, all influence the cost

Debt Equity

Type of finance Bank Senior Debt

Bank Mezzanine Debt*

Pension Funds* Infrastructure Funds*

Private Equity*

Type of risk typically taken

Proven technology

Established companies

Demonstrator / proven technology

New Companies

Proven technology

Proven technology

Private companies

Demonstrator technology

Typical level of return expected by the various types of lender / investor**

~5.5% to 6% ~7.5% to 10% ~15% IRR ~7% IRR ~35% IRR

39

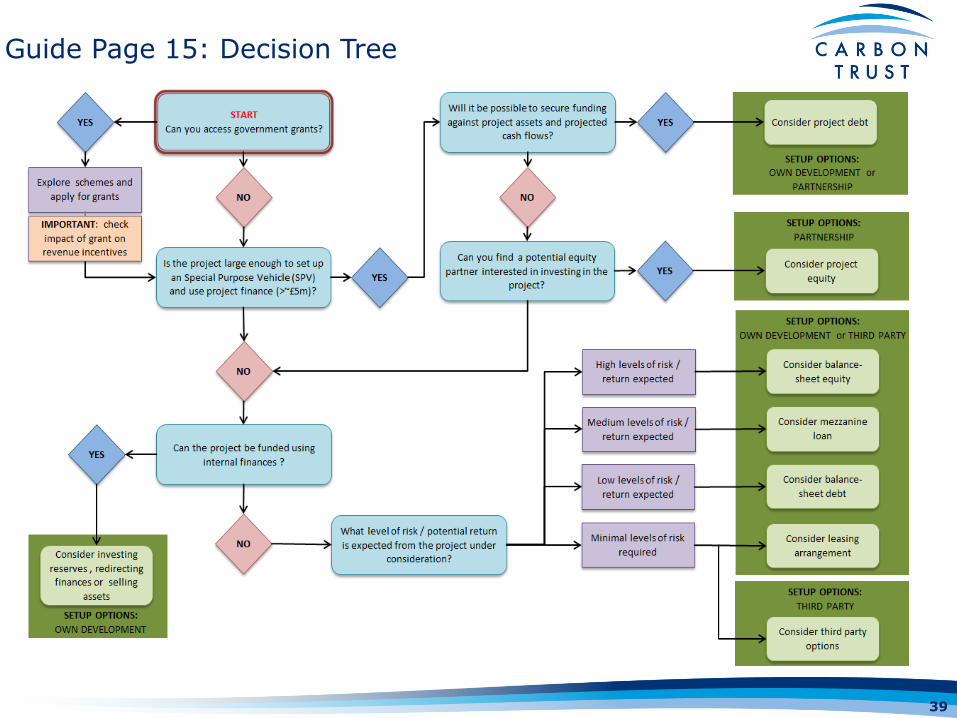

Guide Page 15: Decision Tree

QUESTIONS PLEASE

40

BREAK

41

Financing Renewable Energy

Session 2

Colin McNaught

Agenda for Part 2

Illustrations of the income and finance options for a renewable energy projects

More on incentives

Short case studies

Short exercise

43

Own Development

Risks

– Planning risk – upfront costs / 60% failure rate

– Requirement for equity can be as high as 30%

– Understanding project finance

– Selecting bankable technology –big issue under FIT

Benefits

– ‘Guaranteed’ income stream from electricity generation – regardless of use

– Energy Security – Generation of your own electricity for use on site

44

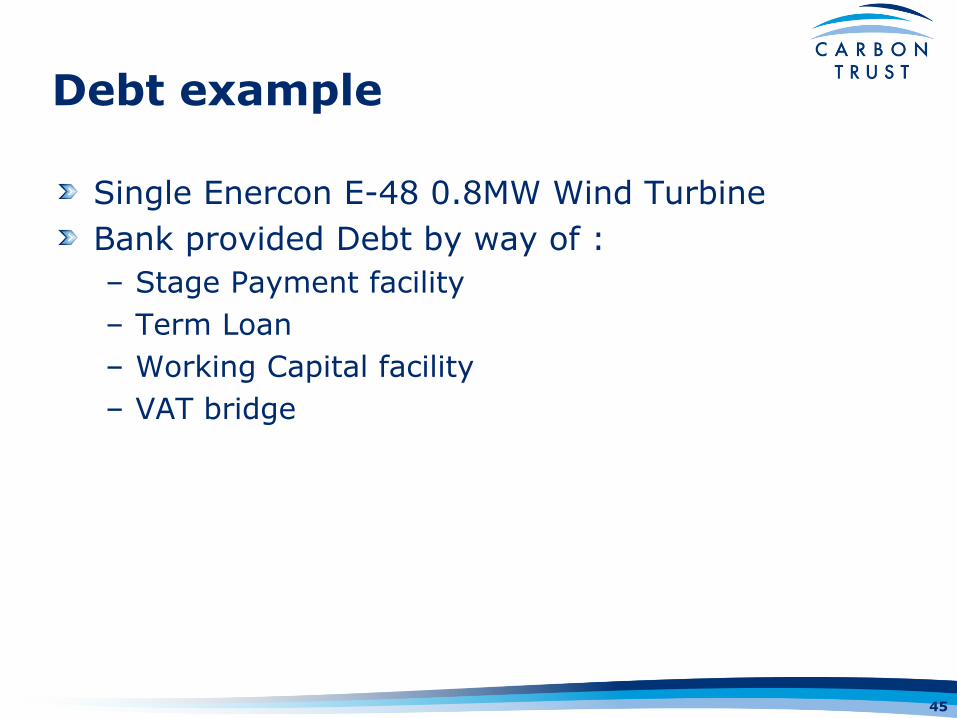

Debt example

Single Enercon E-48 0.8MW Wind Turbine

Bank provided Debt by way of :

– Stage Payment facility

– Term Loan

– Working Capital facility

– VAT bridge

45

Debt example (cont’d)

45 Documents to sign including :

– Banking documents

– Turbine Supply & Maintenance documents

– Land / Lease documents

– Grid Connection documents

– Planning documents (Section 75) / Decommissioning Bond

– Insurance documents

– Civils construction documents

46

Debt example (cont’d)

18 weeks to reach financial close

3 sets of lawyers (Bank, SPV and Landowners)

18 different Parties Involved

– Lawyers, Accountants, Technical Advisors, Insurance Advisors, PPA off takers, Turbine Suppliers, Civil Engineering Companies, Grid Connection provider, Project Manager /Planning Consultants, Wind Report Assessors.

Turbine/ project performance to be monitored continually

Which type of debt finance is this?

47

Project Finance Example

Bank will typically lend 70% - 90% of the project cost (dependant on technology )

Landowner will need to invest the remainder

Term of up to 15 years

Lend of between £1m and £25m

Lent against the forecast future cash flows

Bank will require legal, technical, financial and insurance overview

These costs to be met by the SPV – part of equity investment

48

More on Incentives

FIT & RHI – Covered in Part 1

Renewables Obligation – generally for projects > 5 MW

CCL – Renewables is exempt worth £4.85/MWh for electricity

CRC – Can be avoided – but better to claim FIT

49

More on Incentives

EU-ETS – Large sites only, renewable heat would avoid purchase of fossil fuel and need fewer EU-ETS allowances

CCA – Larger sites – Cant claim if earn FIT or RHI

Public Capital Grants – Cant claim FIT or RHI

– Some expenditure is eligible (development, heating network)

– Private sector grants are OK

50

More on Incentives

Enhanced Capital Allowances – a benefit against corporation tax paid. Not available if FIT or RHI is earned

Business rate relief – Stepped by scheme size, 100% relief for small schemes, to 2.5%

51

Example

300 kW wind turbine

27% load factor = 710 MWh pa

372 tonnes CO2 pa

Capex £450k

Operating & Maintenance £13.2k

52

Example

Interest of 6.5% pa

Deprecation of 10%

Corporation tax 30%

53

Example – Scenario 1

Earn CRC at £12/tonne

CRC worth £4.4k

Electricity used on site worth £64k

Payback in year 14

IRR 9.6%

54

Example – Scenario 2

Earn FIT at 17.5p/kWh + 3.1p export*

FIT worth £124k

Export worth £22k

Payback in year 6

IRR 25.2%

55

* Guide and its examples were drafted when export tariff was 3.1 – this is now higher at 4.5p

Example – Scenario 4

Earn FIT at 17.5p/kWh + 9 p/kWh on site use

FIT worth £124k

On site use worth £64k

Payback in year 5

IRR 38.9%

56

57

Scenario 1 Scenario 2 Scenario 3 Scenario 4

Electricity used on site 100% 0% 40% 100%

Electricity exported 0% 100% 30% 0%

Electricity wheeled 0% 0% 40% 0%

CRC savings £4,467 - - -

Electricity savings on site £63,860 - £25,544 £63,860

FIT - £124,173 £124,173 £124,173

Export - £21,996 £6,599 -

Extra for Wheeling - - £20,455 -

Exempt Services - - -£1,500

Total revenue (Year 1) £68,327 £146,169 £175,271 £188,033

Payback by: Year 14 Year 6 Year 5 Year 5

IRR 9.6% 25.2% 30.5% 32.9%

NPV £104,875 £727,786 £957,422 £1,058,483

ROI 12.3% 29.5% 36.0% 38.9%

Guide Page 22

Finance Options

Own Development (as per Scenarios 1 to 4)

Partnership 50:50

Third Party: Land lease:

– £3,200/MW + 6% of electricity sales

58

59

Own development with debt finance

Partnership development with 50-50 split of risk and reward

Land lease arrangement with third

party developer

Annual turbine output 710 MWh 710 MWh 710 MWh

FIT value (generation & export) £206/MWh £206/MWh £206/MWh

FIT £124,173 £62,087 -

Export £21,996 £10,998 -

Land rent per MW - - £3,200

Percentage of electricity sales - - 6%

Land rental income - - £13,673

Total revenue (Year 1) £146,169 £73,085 £13,673

Payback by: Year 6 Year 6 N/A

IRR 25.2% 25.2% N/A

NPV £727,786 £363,893 N/A

ROI 29.5% 29.5% N/A

Guide Page 23

Worked Example

Company plans to build a 1 MW wind turbine on their warehouse site costing £1.5 million

Expect to generate 2,600 MWh pa.

The relevant FIT is 9.5 p/kWh generated

The export tariff is 4.5 p/kWh generated

Operation costs are 1.7 p/kWh generated

They are offered a finance on 75%:25% debt equity basis at 7% pa.

60

Knowledge Review

How much did they borrow?

What was the annual interest payment?

How much income (£/yr) from the FIT is due?

What is the net annual income?

61

Knowledge Review

How much did they borrow? – £1.125 million (75% x £1.5 million)

What was the annual interest payment? – £78.8k pa (7% x £1.25 million)

How much income (£/yr) from the FIT is due? – £247k pa (9.5 p/kWh x 2,600,000 kWh)

What is the net annual income? – (FIT + Export – Interest – O&M)

– (£247k + £117k) – (£78.8k + £44.2k)

– (£364k) –(£123k) = £241k

62

NB this is a Simple Example which did not include: • Repayments, Insurance, Business rates, Land rent , P90

Output etc.

Further Resources

Co-operative Bank; project case studies

Financing renewable energy projects; A guide for developers

Financing Renewable Energy Projects for Farmers

Private Financing of Renewable Energy; A Guide for Policymakers

West Midlands Local Authority Low Carbon Economy Programme; Local authority funding guide

Scottish Future Trust; Report on the Commercial Aspects of Local Authority Renewable Energy Production

63

Questions

0

0.5

1

1.5

2

2.5

3

3.5

00:00 02:00 04:00 06:00 08:00 10:00 12:00 14:00 16:00 18:00 20:00 22:00