Embed Size (px)

Citation preview

1 Michael Chu’di Ejekam

Table of Contents

1

1) History of evolution of Malls – USA case study 2) Design advancements 3) Five Key Considerations

2 Michael Chu’di Ejekam

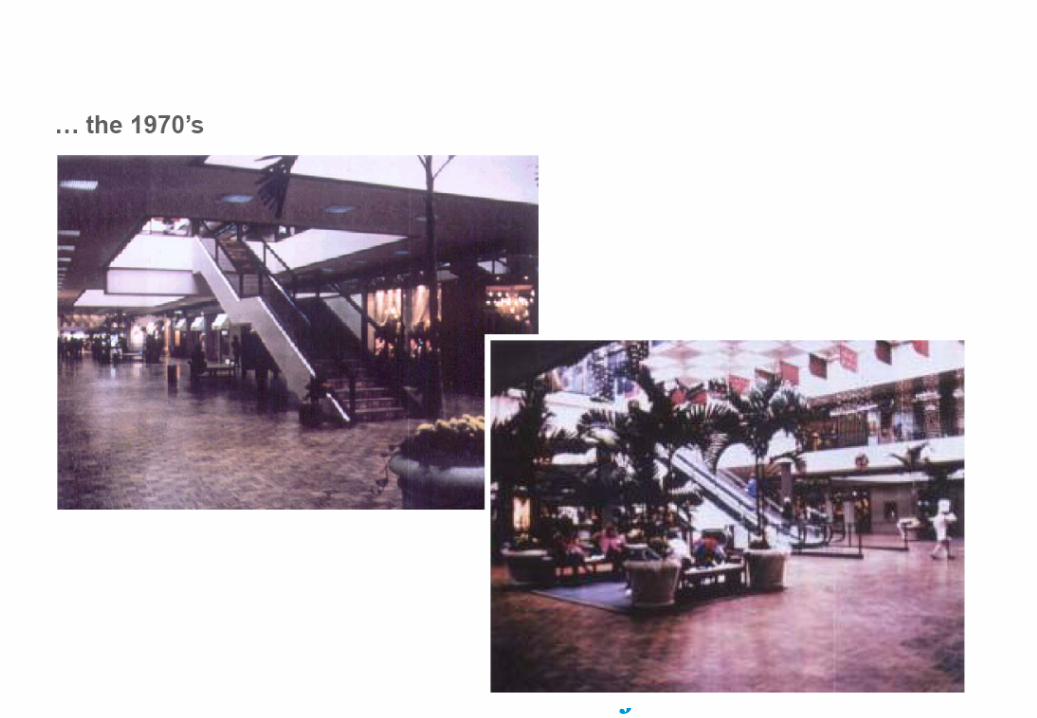

Evolution of Malls in the USA In 60 years, 12 types of malls 60 h i d h d 12 fIn 60 years, the industry has created 12 types of centers

1. Strip2. Neighbourhood3. Community4 Regional4. Regional5. Super Regional6. Power Center7. Urban Entertainment Center8. Factory Outlets Center9. Lifestyle Center10. The Mills11 S C i C t11. Super Convenience Center12. New Urbanism

2

Net Rents: $USD per SF per annum (2010)

2

3 Michael Chu’di Ejekam

4 Michael Chu’di Ejekam

5 Michael Chu’di Ejekam

6 Michael Chu’di Ejekam

7 Michael Chu’di Ejekam

8 Michael Chu’di Ejekam

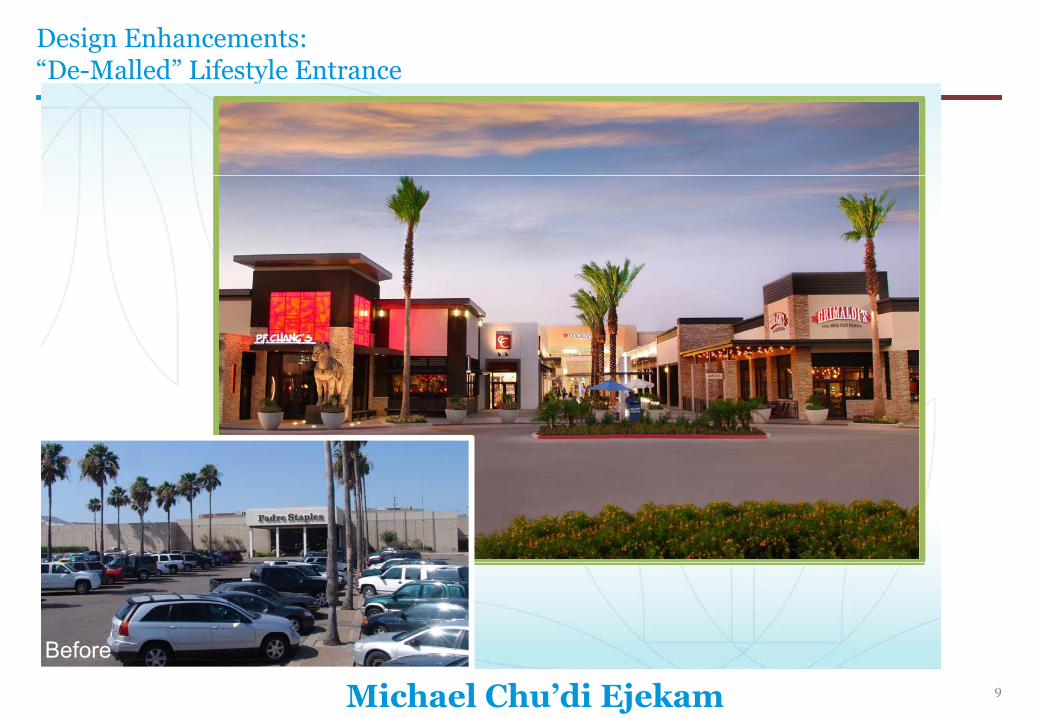

Transform from mall into “Urban Space” – a place of excitement, family, laughter

9 Michael Chu’di Ejekam

Design Enhancements: “De-Malled” Lifestyle Entrance

Before

New Contemporary Outdoor Lifestyle Entrance

10 Michael Chu’di Ejekam

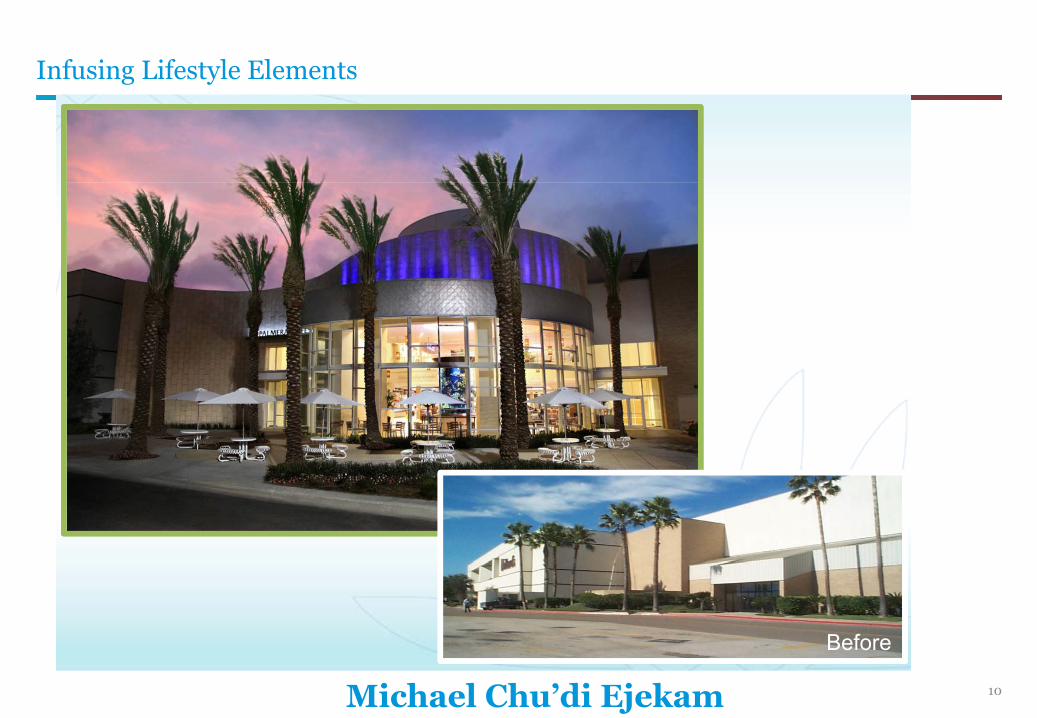

Infusing Lifestyle Elements

Before

Palm Court (Food Court Entrance)

11 Michael Chu’di Ejekam

More attractive – Food Court

Before

New Food Court

12 Michael Chu’di Ejekam

Emphasize Entertainment – e.g. Children’s Play Area

CAROUSEL REMOVED FROM CENTER COURT

New Children’s Play Area

13 Michael Chu’di Ejekam

Five Key Considerations (1) Investors and Returns

13

It’s about Returns, Returns, Returns

• Return requirements depend on the type of investor. • Type of Investor Drives Mall type and business plan • Typical PE returns proven achieveable - 25+% IRR, 2.5x - Ikeja

City Mall, Palms, Accra Mall • Non PE funds can handle lower initial yelds, longer hold periods • Will more "Longer Life" Investors emerge? • Will local investors play greater role? • Retailer developers (dual strategy) combine retail sales plus real

estate returns

Equity and debt are not widely available.

• 20K+ m2 mall costs $80-$180m each, requiring minimum $40-$90m equity per mall.

Dollar debt at 9+% rate, local currency debt at 17+% rate

• Is Naira debt feasible. Negative Leverage! • Will leases be quoted in Naira or Dollar

14 Michael Chu’di Ejekam

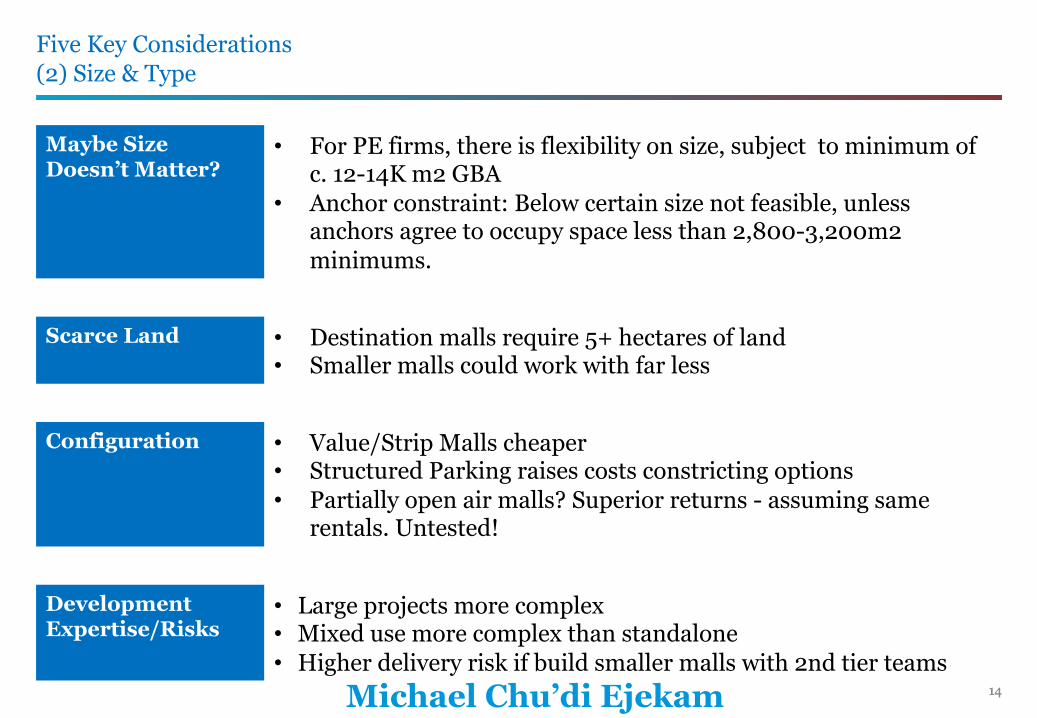

Five Key Considerations (2) Size & Type

14

Maybe Size Doesn’t Matter?

• For PE firms, there is flexibility on size, subject to minimum of c. 12-14K m2 GBA

• Anchor constraint: Below certain size not feasible, unless anchors agree to occupy space less than 2,800-3,200m2 minimums.

Scarce Land • Destination malls require 5+ hectares of land • Smaller malls could work with far less

Configuration • Value/Strip Malls cheaper • Structured Parking raises costs constricting options • Partially open air malls? Superior returns - assuming same

rentals. Untested!

Development Expertise/Risks

• Large projects more complex • Mixed use more complex than standalone • Higher delivery risk if build smaller malls with 2nd tier teams

15 Michael Chu’di Ejekam

Five Key Considerations (3) Demographics & Consumer Traits

15

Nuanced Feasibility Analysis

• Closer attention to trade area overlap, inflow • No longer the only game in town!

Geography • Destination malls more likely to struggle in secondary markets • Tradeoff of lower land costs vs lower buying power and lower

rentals • Riskier demographics in secondary locations

Cater to Consumer behaviour

• Typical Nigerian consumer purchase only 40-50 SKUs • Malls would need to cater to smaller basket sizes, narrow SKUs

and frequent shopping trips. • Convenience/Value is critical to access mass consumer

Decide Target Market

• Upscale, Value or both?? • In USA, need to decide • Ecommerce eating away value shopping

16 Michael Chu’di Ejekam

Five Key Considerations (4) Retailers

16

High Developments Cost, High Rents

• Grocery anchors perform very well. Are rents sustainable for line stores?

Paucity of Viable Tenants

• Certain tenants would not look at strip malls for example • Could Super Regional Work (Over 75,000 m2)

17 Michael Chu’di Ejekam

Five Key Considerations (5) Exit

17

Investors go in with eyes on Exit Door

• Returns Important Again • Type of mall driven by attractiveness to mall buyers • Major mall buyers have minimum mall size requirements • Small malls often below investment grade • Exit Yields unproven in secondary markets • More investors for bite-sized transaction sizes vs large • Typical PE 5 yr hold period realistic? • Will local pension funds become major buyers

18 Michael Chu’di Ejekam

Conclusion

18

1) Perhaps Nigeria malls would evolve like the USA 2) Introduce Design advancements 3) Five Key Considerations i) Investors ii) Size/Type iii) Demographics & Consumer Traits iv) Retailers v) Exit

Returns, Returns, Returns

19 Michael Chu’di Ejekam

19

Thank You

![Interactive Near-Field Illumination for Photorealistic Augmented Reality … · 2020-05-17 · etry captured by a RGB-D camera was presented by Lensing and Broll [35]. The captured](https://img.dokumen.tips/doc/110x75/5f038f687e708231d409a7c4/interactive-near-field-illumination-for-photorealistic-augmented-reality-2020-05-17.jpg)