Embed Size (px)

Citation preview

IntroductionThis white paper gives an overview of the mobile payments landscape in Central & Eastern Europe. It covers 10 of the biggest countries in the region by population: Russia, Ukraine, Poland, Romania, Czech Republic, Hungary, Azerbaijan, Belarus, Bulgaria and Serbia. While equal in size to the EU5 (France, Germany, Italy, Spain & UK) or US by population, they are significantly more fragmented. Localization of both the digital service provided and payment methods is a key to succeed in the region.

Central & Eastern Europe is in an intermediate phase between Western markets and quickly growing emerging markets. There is relatively high ownership of traditional desktop devices, which means traditional software vendors and PC game developers have significant potential in the region. At the same time, access to bank-based payments remains low.

It is also interesting to note that the markets profiled in this report fall into two categories in terms of spending behavior. In countries like Russia and Poland, transaction volumes have declined compared to the last year, while average user spending has increased. At the same time, in countries like Azerbaijan and Belarus, carrier billing’s popularity is quickly growing, indicated by a significant jump in transaction volumes and decline in spend per user. This signals a broader demographic access to carrier billing.

Fortumo’s Central & Eastern European white paper gives a high-level overview of the biggest markets in the region as well as insights on user spending behavior, device preferences and the mobile operator ecosystem. Data presented in the white paper has been taken from Fortumo’s cross-platform mobile payment solution as well as external public sources of information.

Andrea BoettiVP of Global Business Development & SalesFortumo

Mattias LiivakHead of Marketing & PRFortumo

If you have any questions about the data in this report, please reach out to us at [email protected].

Carrier billing in 2016: Central & Eastern Europe

Carrier billing in 2016: Central & Eastern EuropeMarket report by Fortumo

RussiaMarket profile

GDP per capita(IMF 2014 estimate):

$24,000

Median age:

39 years

Carrier billing in 2016: Central & Eastern Europe

46%

75%

15%

22%

146 million

Debit card penetration:

Credit card penetration:

Smartphone penetration:

Population:

age15-24

age 25+

age 25+

Carrier billing in 2016: Central & Eastern Europe

Share of carrier billing in payment mix: 22.3% (2nd most popular after eWallets)

Carriers in market:

Payment types:

Localization:

Traffic sources:

Important note: The exchange rate of Russian ruble has significantly declined in value compared to USD which should be accounted for when planning expansion to the market.

RussiaCarrier billing landscapeDecember 2015 - February 2016

Quarterly ARPPU: $12

one-off transactionssubscriptions (weekly and monthly billing)

MTS (34%) Beeline (25%) Megafon (24%) Tele2 (14%)

+71% compared to December 2014 - February 2015)

Average transaction size: $2 +50% compared to December 2014 - Februay 2015

79% mobile

18% desktop

3% tablet Recommended, 86% of paying users have browser locale set to Russian

Motiv (2%) Smarts (1%)

Transaction volume change: -28% compared to December 2014 - February 2015

UkraineMarket profile

GDP per capita(IMF 2014 estimate):

$8600

Median age:

40 years

Carrier billing in 2016: Central & Eastern Europe

39%

50%

20%

29%

43 million

Debit card penetration:

Credit card penetration:

Smartphone penetration:

Population:

age15-24

age 25+

age 25+

Carrier billing in 2016: Central & Eastern Europe

Share of carrier billing in payment mix: 6.7%

Carriers in market:

Payment types:

Localization:

Traffic sources:

Important note: Web-money services and services with political content are forbidden in Ukraine. The exchange rate of Ukrainian hryvnia has significantly declined in value compared to USD which should be accounted for when planning expansion to the market.

Ukraine Carrier billing landscapeDecember 2015 - February 2016

Quarterly ARPPU: $7.5

one-off transactionssubscriptions (weekly and monthly billing)

Kyivstar (43%) Vodafone (35%) life:) (21%) TriMob (1%)

-28% compared to December 2014 - February 2015)

Average transaction size: $1.1 -23% compared to December 2014 - Februay 2015

47% mobile

48% desktop

5% tablet Recommended, paying user browser locale is mostly Russian (79%) and Ukrainian (13%)

Transaction volume change: +21% compared to December 2014 - February 2015

(4th most popular after eWallets, bank cards and bank transfers)

PolandMarket profile

GDP per capita(IMF 2014 estimate):

$23,000

Median age:

38 years

Carrier billing in 2016: Central & Eastern Europe

50%

72%

9%

18%

38 million

Debit card penetration:

Credit card penetration:

Smartphone penetration:

Population:

age15-24

age 25+

age 25+

T-Mobile (30% Orange (28%) Plus (26%) Play Mobile (16%)

Carrier billing in 2016: Central & Eastern Europe

Share of carrier billing in payment mix: 19.4% (2nd most popular after eWallets)

Carriers in market:

Payment types:

Localization:

Traffic sources:

PolandCarrier billing landscapeDecember 2015 - February 2016

Quarterly ARPPU: $30

one-off transactionssubscriptions (weekly and monthly billing)

+65% compared to December 2014 - February 2015)

Average transaction size: $4.5 +27% compared to December 2014 - Februay 2015

59% mobile

36% desktop

5% tablet 97% of paying users have browser locale set to Polish

Transaction volume change: -20% compared to December 2014 - February 2015

RomaniaMarket profile

GDP per capita(IMF 2014 estimate):

$17,000

Median age:

38 years

Carrier billing in 2016: Central & Eastern Europe

47%

34%

8%

12%

20 million

Debit card penetration:

Credit card penetration:

Smartphone penetration:

Population:

age15-24

age 25+

age 25+

Carrier billing in 2016: Central & Eastern Europe

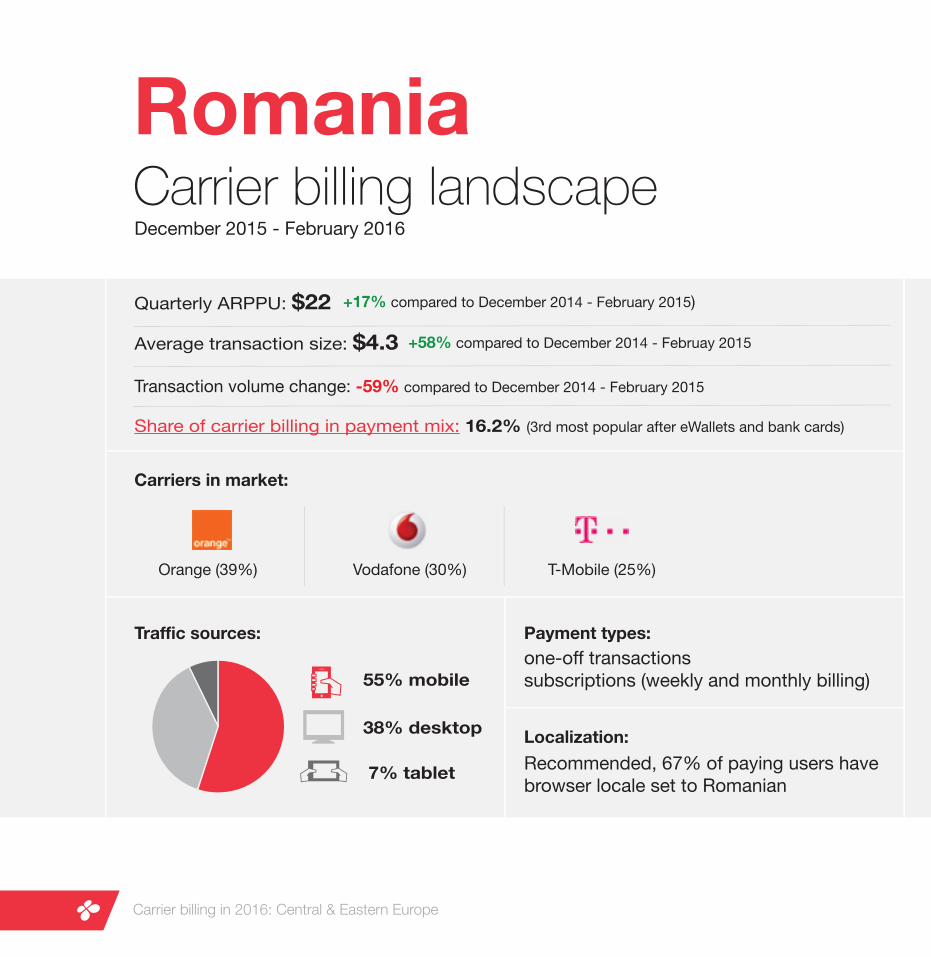

Share of carrier billing in payment mix: 16.2% (3rd most popular after eWallets and bank cards)

Carriers in market:

Payment types:

Localization:

Traffic sources:

RomaniaCarrier billing landscapeDecember 2015 - February 2016

Quarterly ARPPU: $22

one-off transactionssubscriptions (weekly and monthly billing)

Orange (39%) Vodafone (30%) T-Mobile (25%)

+17% compared to December 2014 - February 2015)

Average transaction size: $4.3 +58% compared to December 2014 - Februay 2015

55% mobile

38% desktop

7% tablet Recommended, 67% of paying users have browser locale set to Romanian

Transaction volume change: -59% compared to December 2014 - February 2015

Czech RepublicMarket profile

GDP per capita(IMF 2014 estimate):

$27,000

Median age:

40 years

Carrier billing in 2016: Central & Eastern Europe

66%

75%

14%

28%

10 million

Debit card penetration:

Credit card penetration:

Smartphone penetration:

Population:

age15-24

age 25+

age 25+

Carrier billing in 2016: Central & Eastern Europe

Share of carrier billing in payment mix: 20.9% (3rd most popular after prepaid cards and eWallets)

Carriers in market:

Payment types:

Localization:

Traffic sources:

Czech RepublicCarrier billing landscapeDecember 2015 - February 2016

Quarterly ARPPU: $18

one-off transactionssubscriptions (weekly and monthly billing)

T-Mobile (39%) O2 (36%) Vodafone (25%)

-5% compared to December 2014 - February 2015)

Average transaction size: $3.5 -6% compared to December 2014 - Februay 2015

62% mobile

29% desktop

9% tablet 90% of paying users have browser locale set to Czech

Transaction volume change: +55% compared to December 2014 - February 2015

HungaryMarket profile

GDP per capita(IMF 2014 estimate):

$17,000

Median age:

41 years

Carrier billing in 2016: Central & Eastern Europe

63%

34%

7%

13%

10 million

Debit card penetration:

Credit card penetration:

Smartphone penetration:

Population:

age15-24

age 25+

age 25+

Carrier billing in 2016: Central & Eastern Europe

Carriers in market:

Payment types:

Localization:

Traffic sources:

HungaryCarrier billing landscapeDecember 2015 - February 2016

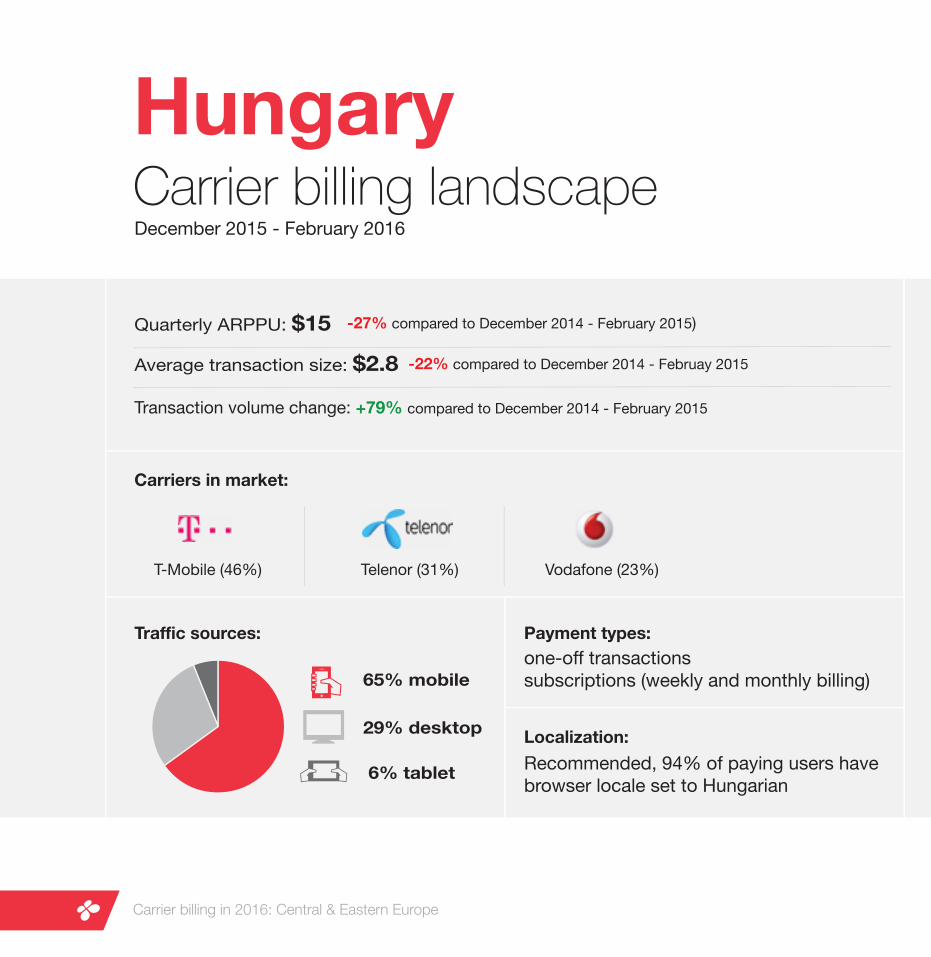

Quarterly ARPPU: $15

one-off transactionssubscriptions (weekly and monthly billing)

T-Mobile (46%) Telenor (31%) Vodafone (23%)

-27% compared to December 2014 - February 2015)

Average transaction size: $2.8 -22% compared to December 2014 - Februay 2015

65% mobile

29% desktop

6% tablet Recommended, 94% of paying users have browser locale set to Hungarian

Transaction volume change: +79% compared to December 2014 - February 2015

AzerbaijanMarket profile

GDP per capita(IMF 2014 estimate):

$17,000

Median age:

28 years

Carrier billing in 2016: Central & Eastern Europe

20%

60%

6%

10%

10 million

Debit card penetration:

Credit card penetration:

Smartphone penetration:

Population:

age15-24

age 25+

age 25+

Carrier billing in 2016: Central & Eastern Europe

Carriers in market:

Payment types:

Localization:

Traffic sources:

AzerbaijanCarrier billing landscapeDecember 2015 - February 2016

Quarterly ARPPU: $15

one-off transactionssubscriptions (weekly and monthly billing)

Azercell (55%) Bakcell (35%) Nar Mobile (10%)

-48% compared to December 2014 - February 2015)

Average transaction size: $2 -52% compared to December 2014 - Februay 2015

49% mobile

50% desktop

1% tablet Recommended, 58% of paying users have browser locale set to Russian

Transaction volume change: +89% compared to December 2014 - February 2015

Important note: e-Wallet services are forbidden in Azerbaijan.

BelarusMarket profile

GDP per capita(IMF 2014 estimate):

$18,000

Median age:

38 years

Carrier billing in 2016: Central & Eastern Europe

41%

8%

14%

9 million

Debit card penetration:

Credit card penetration:

Smartphone penetration:

Population:

age15-24

age 25+

age 25+

40%

Carrier billing in 2016: Central & Eastern Europe

Carriers in market:

Payment types:

Localization:

Traffic sources:

BelarusCarrier billing landscapeDecember 2015 - February 2016

Quarterly ARPPU: $15

one-off transactionssubscriptions (weekly and monthly billing)

MTS (47%) Velcom (41%) Life:) (11%)

-17% compared to December 2014 - February 2015)

Average transaction size: $1.6 -28% compared to December 2014 - Februay 2015

41% mobile

54% desktop

5% tablet Recommended, 98% of paying users have browser locale set to Russian

Transaction volume change: +219% compared to December 2014 - February 2015

BulgariaMarket profile

GDP per capita(IMF 2014 estimate):

$17,000

Median age:

42 years

Carrier billing in 2016: Central & Eastern Europe

60%

3%

13%

7 million

Debit card penetration:

Credit card penetration:

Smartphone penetration:

Population:

age15-24

age 25+

age 25+

33%

Carrier billing in 2016: Central & Eastern Europe

Carriers in market:

Payment types:

Localization:

Traffic sources:

BulgariaCarrier billing landscapeDecember 2015 - February 2016

Quarterly ARPPU: $15

one-off transactionssubscriptions (weekly and monthly billing)

M-tel (45%) Telenor (40%) Vivacom (15%)

-35% compared to December 2014 - February 2015)

Average transaction size: $2.6 -10% compared to December 2014 - Februay 2015

21% mobile

76% desktop

3% tablet Recommended, 78% of paying users have browser locale set to Bulgarian

Transaction volume change: +11% compared to December 2014 - February 2015

Important note: Employment (e.g. hiring), medical, juridical and accounting related services are forbidden in Bulgaria.

SerbiaMarket profile

GDP per capita(IMF 2014 estimate):

$13,000

Median age:

41 years

Carrier billing in 2016: Central & Eastern Europe

58%

14%

16%

7 million

Debit card penetration:

Credit card penetration:

Smartphone penetration:

Population:

age15-24

age 25+

age 25+

36%

Carrier billing in 2016: Central & Eastern Europe

Carriers in market:

Payment types:

Localization:

Traffic sources:

SerbiaCarrier billing landscapeDecember 2015 - February 2016

Quarterly ARPPU: $14

one-off transactionssubscriptions (weekly and monthly billing)

mt:s (53%) Telenor (31%) VIP (16%)

-18% compared to December 2014 - February 2015)

Average transaction size: $2.3 -14% compared to December 2014 - Februay 2015

35% mobile

38% desktop

27% tablet Recommended, 55% of paying users have browser locale set to Serbian

Transaction volume change: +54% compared to December 2014 - February 2015

Local payment methods beyond carrier billing

Yandex Moneyhttps://money.yandex.ru/new/

QIWIhttps://qiwi.ru/

WebMoneyhttp://www.wmtransfer.com/

Przelewy24http://www.przelewy24.pl/en

PaysafeCardhttps://www.paysafecard.com/

Skrillhttps://www.skrill.com/en/home/

Carrier billing in 2016: Central & Eastern Europe

Additional reading

Uber proves merchants need to go beyond credit cards in emerging marketsRead now

Free e-book: crash course into direct carrier billingRead now

India & Pakistan lead in Fortumo’s Emerging Markets Payment IndexRead now

https://fortumo.comhttps://facebook.com/fortumohttps://twitter.com/fortumohttps://www.linkedin.com/company/fortumo-ltd.

Fortumo is a mobile payments company that enables direct carrier billing with more than 350 mobile operators in 90+ countries. Fortumo's payment products work across a wide range of platforms including desktop devices, smartphones, feature phones, tablets and smart TV-s. These products give consumers a simple, 1-click payment method to charge online purchases to their phone bill. For app stores, digital media companies and game developers, Fortumo provides one integration with 350 mobile operators as well as a single point of contact for settlements, reporting, support and infrastructure upgrades. Founded in 2007, Fortumo has offices in Estonia, San Francisco, Beijing, Delhi, Mumbai, Singapore and London and is backed by Intel Capital and Greycroft Partners.

This document is for informational purposes only. Fortumo and the authors make no expressed or implied warranties in this document.

Fortumo and the author(s) make no representation or warranty in relation to the accuracy, completeness or reliability of the information contained in this document. Any opinions expressed in this document are subject to change without notice. This document may be based on a number of assumptions and different assumptions could result in materially different results.

This document should not be regarded by recipients as a substitute for obtaining independent advice and/or the exercise of their own judgement, and is not to be relied upon by recipients. Fortumo and the authors, and any of their members, directors, employees or agents do not accept any liability for any loss or damage arising out of the use of all or any part of this document.

Copyright © 2016 Fortumo | All rights reserved.

![Direct Carrier Billing - MarketResearch.com: Market ... · Direct carrier billing: giving CSPs a share of the mobile payments market Executive summary [1] Direct carrier billing (DCB)](https://img.dokumen.tips/doc/110x75/5f01ee857e708231d401be76/direct-carrier-billing-market-direct-carrier-billing-giving-csps-a-share.jpg)