Embed Size (px)

Citation preview

45%

22%

11%

10%

7%

4%1%

Asia

Europe

North America

Latin America/ Carribian

Africa

Middle East

Oceania/Australia

Source: http://www.internetworldstats.com/stats.htm, ITU World Telecommunication /ICT Indicators database

In 2013, over 2.7 billion people are using the Internet, which corresponds to 39% of the world’s population

Internet User (%)Base:World Population

538.0

137.0101.2

74.540.3 33.6 31.0 29.1 20.1 17.7

40.1

11.4

79.5

30.1

82.5

32.4 33.9

15.3

30.0

60.7

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

100.0

-50.0

50.0

150.0

250.0

350.0

450.0

550.0

internet users (mio) internet penetration (%)

Source: http://www.internetworldstats.com/stats.htm, ITU World Telecommunication /ICT Indicators Database, MarkPlus Insight Analysis

In the developing world, 31% of the population is online, compared with 77% in the developed world

Internet User (mio)Base:World Population

74

29

37

80

33

41

developed country (%) developing country (%) world (%)

Women

Men

Globally, 37% of all women are online, compared with 41% of all men; it corresponds to 1.3 billion women and 1.5 billion men

Source: ITU World Telecommunication /ICT Indicators Database

Internet User (mio)Base:World Population

42.2

55.261.1

74.6

2010 2011 2012 2013In million 2010 2011 2012 2013

Urban Population 121.16 123.24 123.57 133.73

Urban Internet User 37.56 50.53 56.38 62.19

Internet User 42.16 55.23 61.08 74.57

Internet Penetration (Mio)Base: Indonesia Population

The number of Internet users grow significantly from 2010 to 2013; it has been grew by 13.5 million in 2013

Source: MarkPlus Insight, published on Marketeers Magazine Nov 2013 edition

42.2

55.2

61.1

74.6

8.0

13.8

24.2

31.7

18.98

24.99

39.6242.49

2010 2011 2012 2013

Internet Users Netizen (Access more than three hours per day) Netizen proportion (%)

Netizen Penetration (Mio)Base: Indonesia Population

The number of internet users in 2013 grew by 22% but the netizenpenetration growth is only 3% y-o-y

%

%

%%

Source: MarkPlus Insight, published on Marketeers Magazine Nov 2013 edition

233.48 236.33 239.14 242.02 244.81 247.57 250.34 253.09 255.79

43.3752.20

62.8474.57

91.04

109.59

131.91

158.79

191.13

8.00 13.8024.20

31.6939.79

47.9456.08

64.2372.38

2010 2011 2012 2013 2014* 2015* 2016* 2017* 2018*

Citizen of Indonesia (mio) Indonesia Internet User (mio) Indonesia Netizen (mio)

In 2013, 6 new internet users were born every a baby birth

*) Projection

Indonesia Population vs Internet User (mio)Base: Indonesia Population

Source: MarkPlus Insight, published on Marketeers Magazine Nov 2013 edition

1

2

3

To explore Netizen online habits and behaviors

To determine Netizen purchase behavior

To determine Netizen anxiety and desire

4 To understand Netizen media habits

This research is aimed to get insightful information for marketers toformulate an appropriate strategy to approach Netizen sub-culture

Source: MarkPlus Insight, published on Marketeers Magazine Nov 2013 edition

AREA RESPONDENTS

Jakarta 500Bandung 200Semarang 150Surabaya 300Medan 250Makassar 150Palembang 150Denpasar 150Pekanbaru 150Banjarmasin 150

Total 2150

*)Margin of error 2,11%

Quantitative Phase

Face to Face Interview

Multi Stage Random Sampling

• SEC A/B/C • Age 15 – 64 years old• Internet and/ or mobile internet users• Use internet for at least 3 hours a day• Not working or having family whose work at

market research company, advertising agency, and mass media.

Respondent Criteria

This survey was conducted by quantitative and qualitative research approach

Qualitative Phase

Focus Group Discussion

• Digital Immigrant (1 group)• Digital Native (1 group)

Source: MarkPlus Insight, published on Marketeers Magazine Nov 2013 edition

Gender (%)Base: All Respondents (n=2150)

49.950.1

Male Female

51.2

50.0

50.7

49.7

50.0

50.0

52.7

50.0

50.0

44.7

48.8

50.0

49.3

50.3

50.0

50.0

47.3

50.0

50.0

55.3

Jakarta (n=500)

Bandung (n=200)

Semarang (n=150)

Surabaya (n=300)

Medan (n=250)

Palembang (n=150)

Pekanbaru (n=150)

Denpasar(n=150)

Banjarmasin (n=150)

Makassar (n=150)

Gender (%)Base: All who live in particular city

The gender composition is balanced for all cities

Source: MarkPlus Insight, published on Marketeers Magazine Nov 2013 edition

27.7

20.916.8

17.9

10.7

6.0

15 – 22 y.o 23 – 30 y.o

31 – 35 y.o 36 – 45 y.o

46 – 55 y.o 56 – 64 y.o

Age (%)Base: All Respondents (n=2150)

17.9

21.7

23.6

23.0

13.8

A1 (More than Rp. 4.500.000)A2 (Rp. 3.000.001 - Rp. 4.500.000)B (Rp. 2.000.001 - Rp. 3.000.000)C1 (Rp. 1.500.001 - Rp. 2.000.000)C2 (Rp. 1.000.001 - Rp. 1.500.000)

Monthly Household Expenditure (%)Base: All Respondents (n=2150)

The respondents comes from SEC A – C; and mostly from younger segment (below 45 y.o)

Source: MarkPlus Insight, published on Marketeers Magazine Nov 2013 edition

Single45.5

Married and Have Kids

46.1

Married and have no kid

yet7.2

Marital Status (%)Base: All Respondents (n=2150)

Most of respondents are married and have kids

Source: MarkPlus Insight, published on Marketeers Magazine Nov 2013 edition

Key Findings

• 5 Netizen Species• Spending behavior• Online behavior• Social media• Anxieties & Desires• Media Habit• Netizen Favorite Brand

5 Species of Indonesian Netizens

32,6%

45,1% 5,1% 11,5%

5,5%

Those who has actively write an article, have a blog, upload video,social media buzzer, can’t be separated from the internet

Those passive users who only read other’s status or post in social media but never comment or share their own life

Those who loves to search and collect news for their own shake but don’t have any intention to share – research online, purchase offline

Those who love to chat by instant messaging

Those who are actively posting in social media, commenting other’s status or posts, criticize other’s idea

Source: MarkPlus Insight, published on Marketeers Magazine Nov 2013 edition

Passive Active

User Generation & Content

32,6%

45,1% 5,1% 11,5%

5,5%

Connection Level

Aware Appeal Ask Act Advocate

Active Passive

32,6%45,1% 5,1% 11,5% 5,5%

Currator CatalystCrawler Chatter Commentator

Co

nte

nt

Segmentation

Reading online news on website

“I rarely read newspaper. I’d

rather search news in detik.com”

{ Male, worker, digital immigrant }

Reading status on social media“I frequently

reading my friend’s Facebook comment or status silently”

{ Male, worker, digital immigrant }

Collecting Information

“My friend status always spot where she found a good place to eat and I

always noted down her location.”

{ Female, worker, digital native}

Get connected -chatting

“We’re using chat messenger (as the

main way) to communicate with

friend/family.”

{ Most respondents}

Make a call using Skype

“I am using Skype regulary to stay in

touch with my friend in England (1 am in a morning).”

{ Female, worker, digital native}

Post a comment“I state my

perspective with posting a comment

on one of Kaskus thread”

{ Male, high school student, digital

native }

Buy toys on Ebay

“Recently, i’ve bought McD minion toys on

eBay because I’m too lazy to search in McD

outlet.”

{ Male, first jobber digital native }

Sharing, sharing, sharing

“Tweet our thought, sharing photos of

our food pr activity, sharing music that we listened to or recommend good

place to eat.”{ Most respondents}

I tweet thereforeI am

“I speak my mind through online. I tweet a lot and has so many reply. Sometimes I also create my own meme

jokes on Path”{ Male, first jobber

digital native }

Amplify the enthusiasm

“I love to collect people writing about illuminati on Kaskus, which I am

is an illuminati enthusiast.”

{Male, high school student, digital native}

Digital natives crowds catalyst segment for their role as contentgenerator and also a creative content creator

Aware ShareAppeal Ask Act

Source: MarkPlus Insight, published on Marketeers Magazine Nov 2013 edition

Key Findings

• 5 Netizen Species• Spending behavior• Online behavior• Social media• Anxieties & Desires• Media Habit• Netizen Favorite Brand

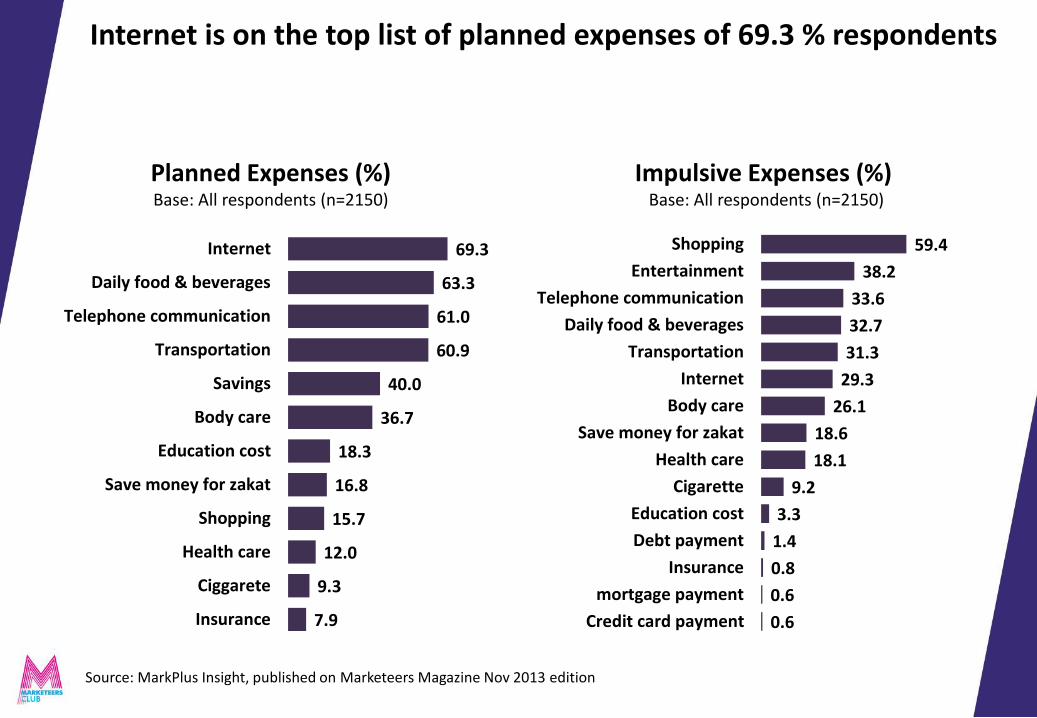

7.9

9.3

12.0

15.7

16.8

18.3

36.7

40.0

60.9

61.0

63.3

69.3

Insurance

Ciggarete

Health care

Shopping

Save money for zakat

Education cost

Body care

Savings

Transportation

Telephone communication

Daily food & beverages

Internet

Planned Expenses (%)Base: All respondents (n=2150)

0.6

0.6

0.8

1.4

3.3

9.2

18.1

18.6

26.1

29.3

31.3

32.7

33.6

38.2

59.4

Credit card payment

mortgage payment

Insurance

Debt payment

Education cost

Cigarette

Health care

Save money for zakat

Body care

Internet

Transportation

Daily food & beverages

Telephone communication

Entertainment

Shopping

Impulsive Expenses (%)Base: All respondents (n=2150)

Internet is on the top list of planned expenses of 69.3 % respondents

Source: MarkPlus Insight, published on Marketeers Magazine Nov 2013 edition

Do You Shop Online? (%)Base: Respondents (n=2148)

20.3

79.7

Yes No

The number of netizen who shop online increased by 5% compared to last year

Source: MarkPlus Insight, published on Marketeers Magazine Nov 2013 edition

3.7

4.2

7.6

8.3

9.3

12.1

12.4

17.0

56.4

79.2

Bus/train ticket

Glasses

Handphone accessories

Watch

Handphone

Book

Cinema ticket

Bags

Shoes

Apparel

Offline ShoppingBase: All respondent (n=2105)

1.8

2.3

2.8

3.0

5.1

5.1

7.6

20.0

20.2

67.1

Book

Cosmetic

Handphone accessories

Car accessories

Handphone

Airline ticket

Watch

Bags

Shoes

Apparel

Online ShoppingBase: Respondent ever bought online product (n=435)

Netizen are starting to buy primary items from the internet

Source: MarkPlus Insight, published on Marketeers Magazine Nov 2013 edition

Messenger group 27.0%

Online forum for shopping

26.6%

Social media 26.4%

Online shop20.0%

Online Shopping Channel (%) Base: respondents who shop online (n=434)

Most of respondents choose to do online shopping on messenger group and social media

Source: MarkPlus Insight, published on Marketeers Magazine Nov 2013 edition

Account transfer is the most widely used payment method for online shopping

Payment Methods of Online Shopping (%) Base: All respondents who bought a product/service through internet (n=435)

0.5

0.5

0.9

2.5

27.1

80.7

PayPal

KasPay

Rekening bersama (Rekber)

Credit card

Cash on Delivery (COD)

Account transfer

Source: MarkPlus Insight, published on Marketeers Magazine Nov 2013 edition

Key Findings

• 5 Netizen Species• Spending behavior• Online behavior• Social media• Anxieties & Desires• Media Habit• Netizen Favorite Brand

#1 SPENDING ON INTERNET SERVICE

Feel uneasy without internet

#1 CONTACT PEOPLE BY CHAT MESSENGER

Use chat messenger first (not SMS), make a phone call later

MODEM

UNLIMITED INTERNET PACKAGE

WHATSAPPLINE KAKAO TALK

Smartphone appealing so much not only for youngster; Netizenfirmly embrace hi-tech devices for supporting their online activities

#1 PROVIDER CONSIDERATION: INTERNET CONNECTION SPEED

Most activty rely on internet connection

COVERAGE AREA

INTERNET CONNECTION

SPEED

SIGNAL STRENGTH

Source: MarkPlus Insight, published on Marketeers Magazine Nov 2013 edition

Used Gadget To Access Internet (%)Base: All Respondent (n=2150)

86.0

42.3

15.210.6

Smartphone Own laptop laptop/pc at the office laptop/pc at home

Smartphone is the most widely used gadget to access internet for both men and women

Source: MarkPlus Insight, published on Marketeers Magazine Nov 2013 edition

Average Monthly Spending For Internet Access Through Smartphone/Tablet (%)

Base: All accessed internet through smartphone/tablet (n=1831)

75.544

111.386

85,43595,648 92,118

86,807 90,140

85,81897,184

74,743

91,808

78,924

62,581

80,290 81,620

61,96067,384

82,19176,579

72,618

0

50,000

100,000

150,000

Jakarta Denpasar Makassar Palembang Bandung Semarang Medan Surabaya Pekanbaru Banjarmasin

2012 (n=1831) 2013 (n=1374)

The average Netizen spending tends to be higher in particular cities compared to 2012

Source: MarkPlus Insight, published on Marketeers Magazine Nov 2013 edition

Only 11.5 % of respondents has purchased goods, most of them come from younger age

11.5

88.5

yes no

Have You Ever Bought A Product Because Of Online Ads? (%)Base: All respondents (n=2505)

Source: MarkPlus Insight, published on Marketeers Magazine Nov 2013 edition

82.7

31.8

11.1

4.1

Smartphone

Laptop/Notebook/Netbook

PC/Desktop

Tablet PC

Gadget USed to Access Internet Banking (%)Base: All respondents who have internet banking (n=387)

82.7% Netizen use their smartphone to access internet banking

Source: MarkPlus Insight, published on Marketeers Magazine Nov 2013 edition

For more Insights, please read Marketeers Magazine November 2013

To purchase full report, please email [email protected]