Embed Size (px)

Citation preview

Analysis of the North American Workwear and

Uniforms Market Fabric Innovations Hold the Future of the Mature Market

NBBE-39

March 2013

2 NBBE-39

Contents

Section Slide Numbers

Executive Summary 4

Market Overview 9

Total Workwear and Uniforms Market --

• Forecasts and Trends 30

• Market Share and Competitive Analysis 48

CEO's 360 Degree Perspective 59

General Workwear Market Breakdown 61

• Blue Workwear Market Breakdown 90

• White Workwear Market Breakdown 105

Corporate Workwear Market Breakdown 120

• Career Workwear Market Breakdown 148

• Casual Workwear Market Breakdown 163

Uniforms Market Breakdown 178

The Last Word (Conclusions and Implications) 198

Appendix 201

3 NBBE-39

Executive Summary

4 NBBE-39

Executive Summary

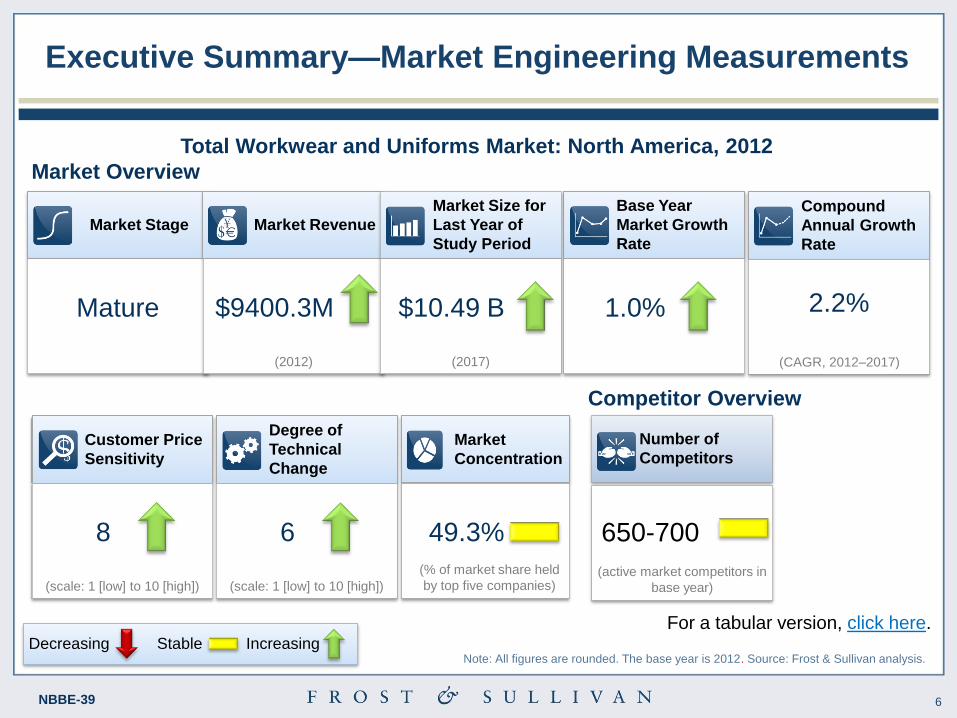

• The North American workwear and uniforms market generated revenue of $9400.3

million in 2012 and is expected to reach $10.49 billion in 2017.

• The North American workwear and uniforms market is mature, with a CAGR of 2.2

percent.

• The market is divided into three product groups: general workwear, corporate workwear,

and uniforms.

• The market revenue is divided into direct retail revenue and rental revenue. The

distribution structure is analyzed in detail for each category.

• Each workwear market segment is in a different stage of growth. White workwear, which

includes healthcare and hospitality workwear, is likely to experience the highest growth

in the forecast period.

• Innovations in fabric technologies and increasing awareness of end users for a multitude

of fabric enhancements promote price growth and, therefore, drive revenue.

Source: Frost & Sullivan analysis.

5 NBBE-39

Executive Summary (continued)

• Rental companies have dominated the North American market in the past.

• The continuing impact of the economic crisis and consequent changes in customer

preferences for direct buying restrain market growth for the rental channel.

• Price, inventory, and quality of service are expected to be the key competitive factors

throughout the forecast period.

• Participants range from small domestic manufacturers focused on a single type of workwear

to several large multinational corporations that manufacture and offer a wide range of

workwear products.

• Many rental companies and commercial launderers compete and collaborate with workwear

manufacturers and enjoy a leading market presence.

• With increasing customer demand for high-performance fabrics, the market is set to see

growth through increased collaborations with fabric manufacturers.

Source: Frost & Sullivan analysis.

6 NBBE-39

Executive Summary—Market Engineering Measurements

Base Year

Market Growth

Rate

1.0%

Market Stage

Mature

Market Revenue

$9400.3M

(2012)

Market Size for

Last Year of

Study Period

$10.49 B

(2017)

Total Workwear and Uniforms Market: North America, 2012

Market Overview

For a tabular version, click here. Stable Increasing Decreasing

Note: All figures are rounded. The base year is 2012. Source: Frost & Sullivan analysis.

Compound

Annual Growth

Rate

2.2%

(CAGR, 2012–2017)

Customer Price

Sensitivity

8

(scale: 1 [low] to 10 [high])

Degree of

Technical

Change

6

(scale: 1 [low] to 10 [high])

Market

Concentration

49.3%

(% of market share held

by top five companies)

Number of

Competitors

650-700

(active market competitors in

base year)

Competitor Overview

7 NBBE-39

Executive Summary—CEO's Perspective

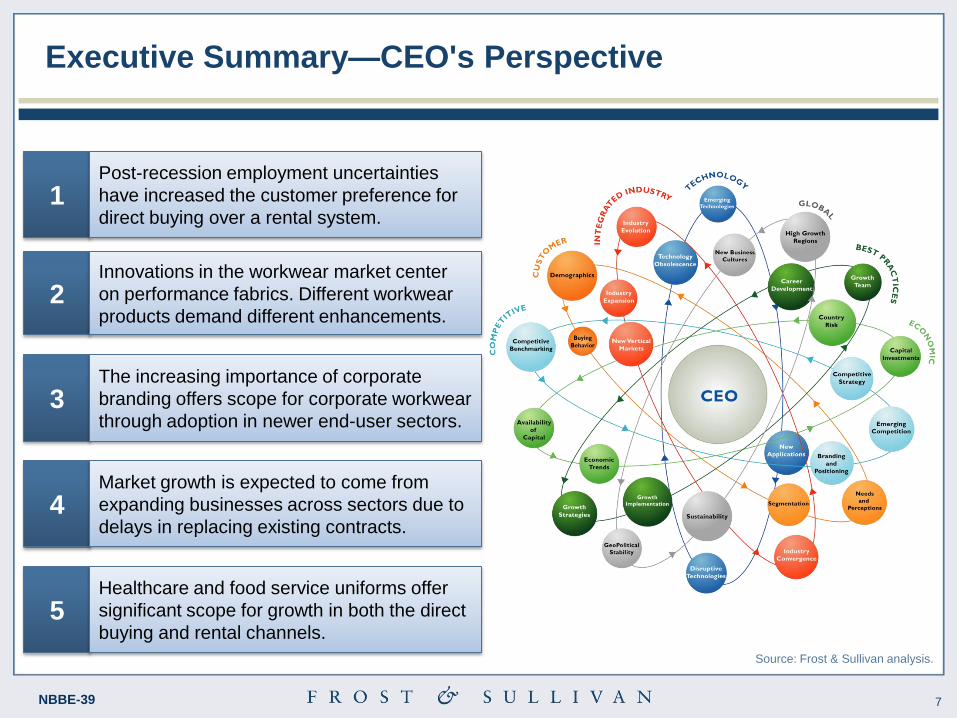

2

Innovations in the workwear market center

on performance fabrics. Different workwear

products demand different enhancements.

3 The increasing importance of corporate

branding offers scope for corporate workwear

through adoption in newer end-user sectors.

4

Market growth is expected to come from

expanding businesses across sectors due to

delays in replacing existing contracts.

5 Healthcare and food service uniforms offer

significant scope for growth in both the direct

buying and rental channels.

1 Post-recession employment uncertainties

have increased the customer preference for

direct buying over a rental system.

Source: Frost & Sullivan analysis.

8 NBBE-39

Market Overview—Segmentation

Note: All figures are rounded. The base year is 2012. Source: Frost & Sullivan analysis.

Uniforms 7.7%

General Workwear

62.5%

Corporate Workwear

29.8%

Percent Sales Breakdown by Product Type Total Workwear and Uniforms Market:

North America, 2012

9 NBBE-39

Direct Sales Channel Total Workwear and Uniforms

Market—Competitive Environment

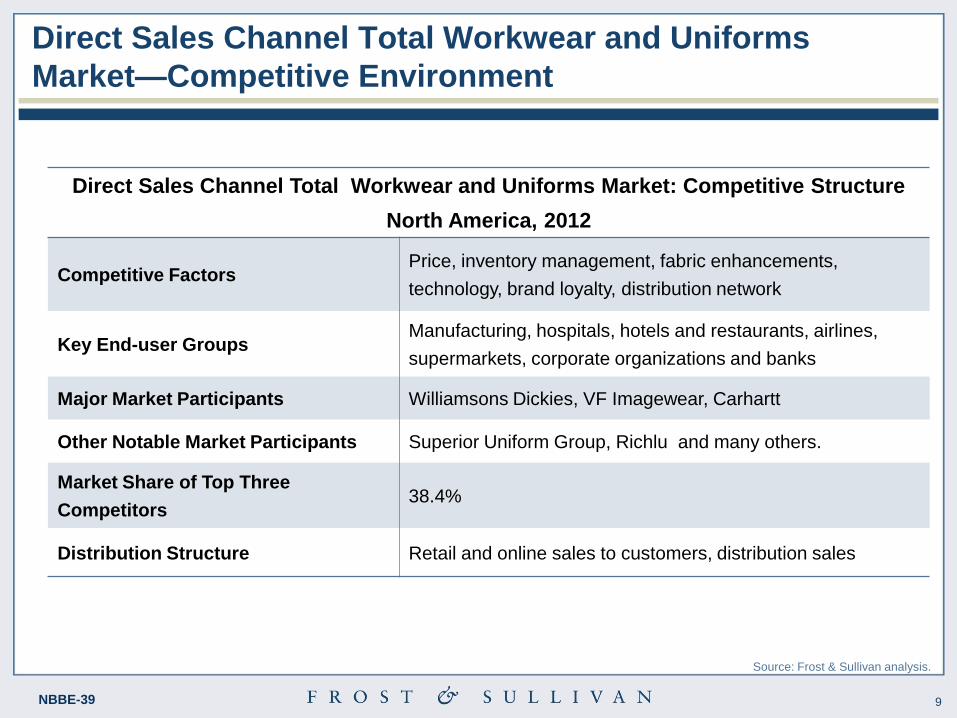

Direct Sales Channel Total Workwear and Uniforms Market: Competitive Structure

North America, 2012

Competitive Factors Price, inventory management, fabric enhancements,

technology, brand loyalty, distribution network

Key End-user Groups Manufacturing, hospitals, hotels and restaurants, airlines,

supermarkets, corporate organizations and banks

Major Market Participants Williamsons Dickies, VF Imagewear, Carhartt

Other Notable Market Participants Superior Uniform Group, Richlu and many others.

Market Share of Top Three

Competitors 38.4%

Distribution Structure Retail and online sales to customers, distribution sales

Source: Frost & Sullivan analysis.

10 NBBE-39

Rental Sales Channel Total Workwear and Uniform

Market—Competitive Environment

Rental Sales Channel Total Workwear and Uniforms Market: Competitive Structure

North America, 2012

Competitive Factors Robust laundry systems, reliability, customer relationships,

timely and high-quality service

Key End-user Groups Manufacturing, hospitals, hotels and restaurants, automotive

industry

Major Market Participants Cintas, ARAMARK Corporation, UniFirst, G&K Services

Other Notable Market Participants Alsco, Ameripride Services, and many others.

Market Share of Top Four

Competitors 68.5%

Distribution Structure Renting and leasing garments to customers

Source: Frost & Sullivan analysis.