Embed Size (px)

Citation preview

05/01/2023

FOREIGN INVESTMENT IN REAL PROPERTY TAX ACT OF 1980, as

amended

Presented by Jane M. Shields, EsquireMary R. LaSota, Esquire

1

05/01/2023

FIRPTAWHEN DOES IT APPLY?

Applies to the disposition of US real property interest made by a non-resident alien individual(s) or a foreign entity.

Section 897 of IRS Tax Code 2

05/01/2023

FIRPTA’S PURPOSE?

A foreign person should be subject to US tax on the sale of a USRPI and should not be able to avoid that tax through the use of a US holding entity or a nonrecognition transaction.

Prior to Section 897(a): The General Rule and the Section 897(a) Exception.

3

05/01/2023

FIRPTA DEFINITIONS

• Disposition• US Real Property Transfer• Interest in Real Property• US Resident• Amount Realized• Transferor

• Transferee• Transferor’s Agent• Transferee’s Agent• Qualified Substitute

4

05/01/2023

FIRTPA DEFINITIONS

• What is a DISPOSITION?• Sale or Purchase • Gift, Redemption or Capital Contribution

• What is a US real property interest?• Real property: Property located in the US and Virgin

Islands• Land and unserved natural products of land,

improvements and personal property associated with the use of real property. Treas. Reg. Section 1.897-1 5

05/01/2023

FIRPTA DEFINITIONS

• What is a US real property interest (continued)?• Options to buy or sell a US Real Property Interest. Treas.

Reg. § 1.897- 1(d)(2)(ii)(B) • A domestic corporation unless it is established that the

corporation was not a U.S. real property holding corporation within the period described in section 897(c)(1)(A)(ii).• State law definitions of real property does not

control

6

05/01/2023

FIRPTA DEFINITIONS

• Interest in Real Property?• Fee Ownership, Co-Ownership, Time sharing interest, a life

estate, remainder interest, or reversionary interest in real property even if the option is currently exercisable. Treas. Reg. Section 1.897-1(d)(2)(i), 2(ii)(B).

• An interest in an entity, other than solely as a creditor?• Stock of a corporation, Partnership interest, interest in a

trust or estate as a beneficiary or an ownership in a grantor trust

7

05/01/2023

FIRPTA DEFINITIONS

8

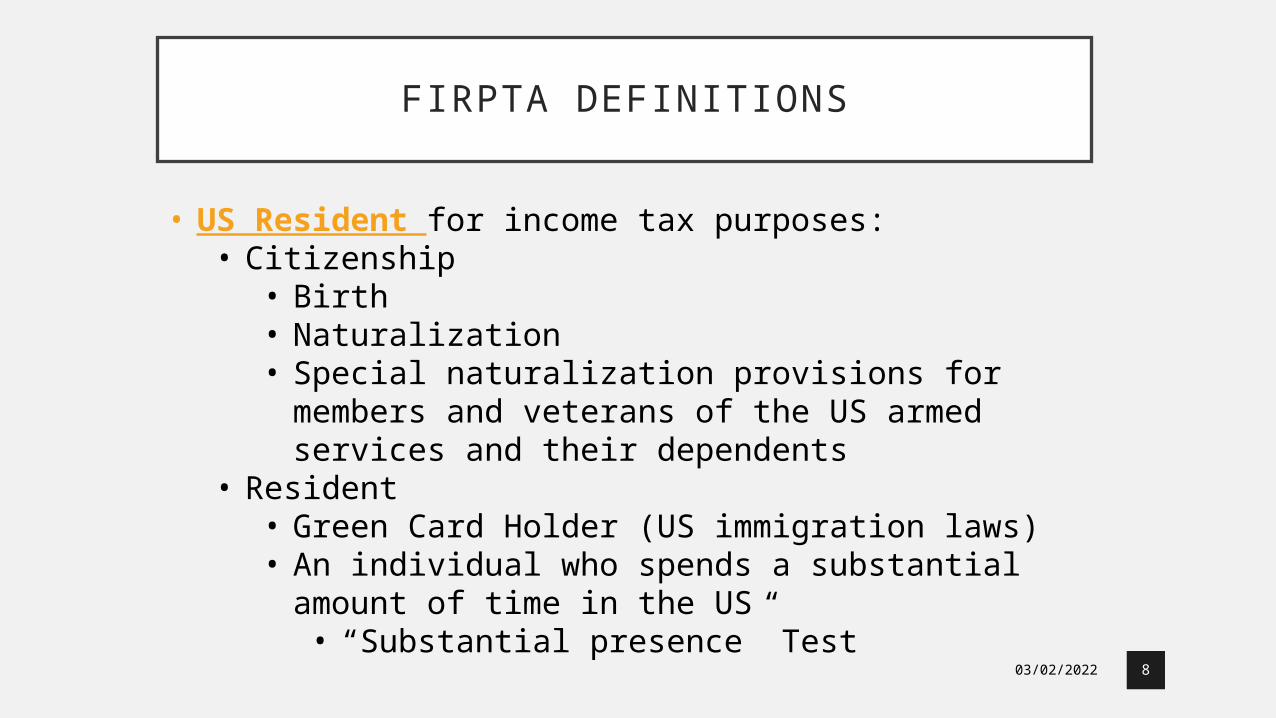

• US Resident for income tax purposes:• Citizenship• Birth• Naturalization• Special naturalization provisions for members

and veterans of the US armed services and their dependents

• Resident• Green Card Holder (US immigration laws)• An individual who spends a substantial amount

of time in the US• “Substantial presence” Test

05/01/2023

FIRPTA DEFINITIONS

• US Resident for estate tax purposes:• A person will be a US estate and gift tax resident if the US is

that person’s domicile. • Amount Realized – is the sales price of the real property, not

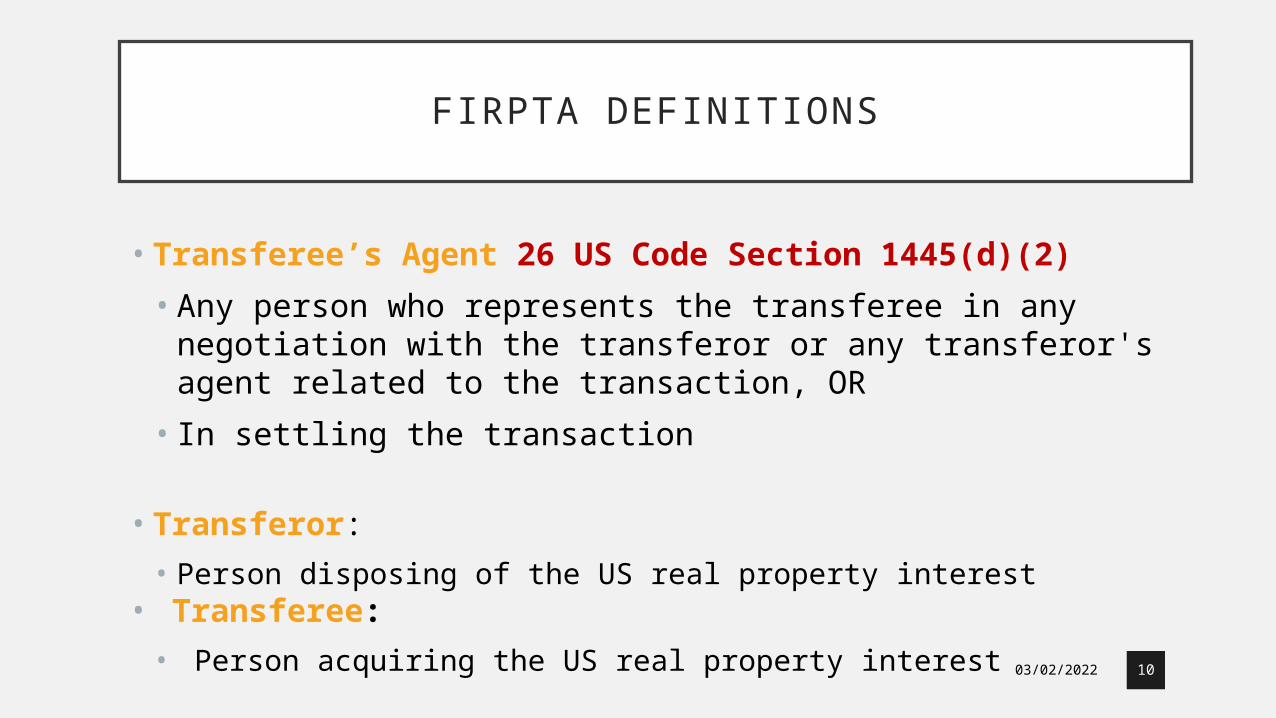

the net proceeds• Transferor’s Agent 26 US Code Section 1445(d)(2)• Any person who represents the transferor in any negotiation with

the transferee's agent related to the transaction, OR• In settling the transaction

9

05/01/2023

FIRPTA DEFINITIONS

• Transferee’s Agent 26 US Code Section 1445(d)(2)• Any person who represents the transferee in any negotiation

with the transferor or any transferor's agent related to the transaction, OR• In settling the transaction

• Transferor: • Person disposing of the US real property interest• Transferee: • Person acquiring the US real property interest 10

05/01/2023

FIRPTA DEFINITIONS

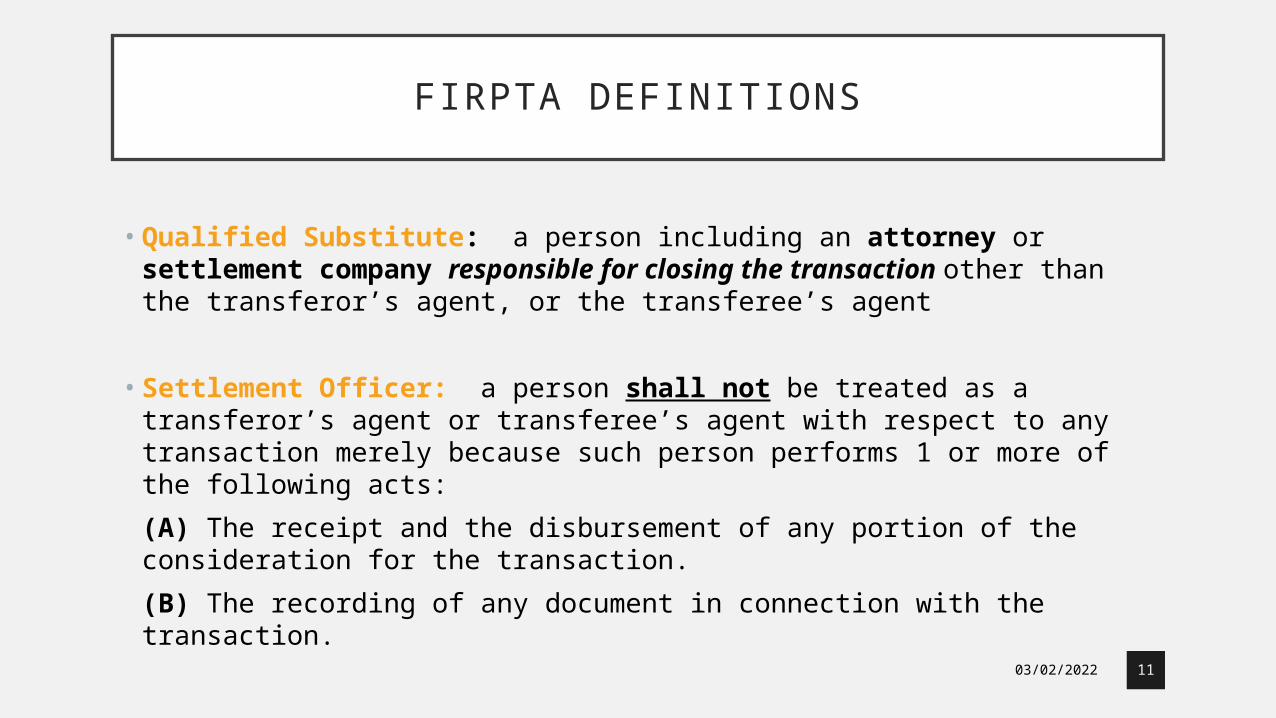

• Qualified Substitute: a person including an attorney or settlement company responsible for closing the transaction other than the transferor’s agent, or the transferee’s agent

• Settlement Officer: a person shall not be treated as a transferor’s agent or transferee’s agent with respect to any transaction merely because such person performs 1 or more of the following acts:(A) The receipt and the disbursement of any portion of the consideration for the transaction.(B) The recording of any document in connection with the transaction.

11

05/01/2023

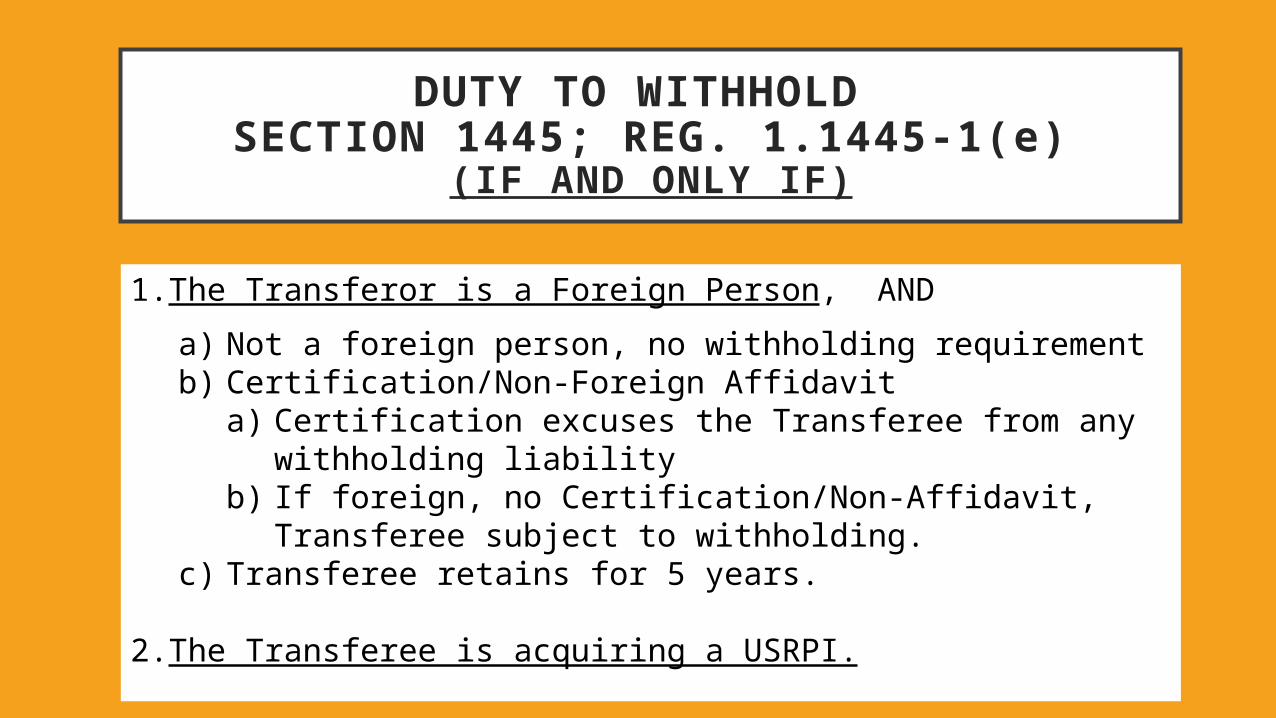

DUTY TO WITHHOLD SECTION 1445; REG. 1.1445-1(e)

(IF AND ONLY IF)

12

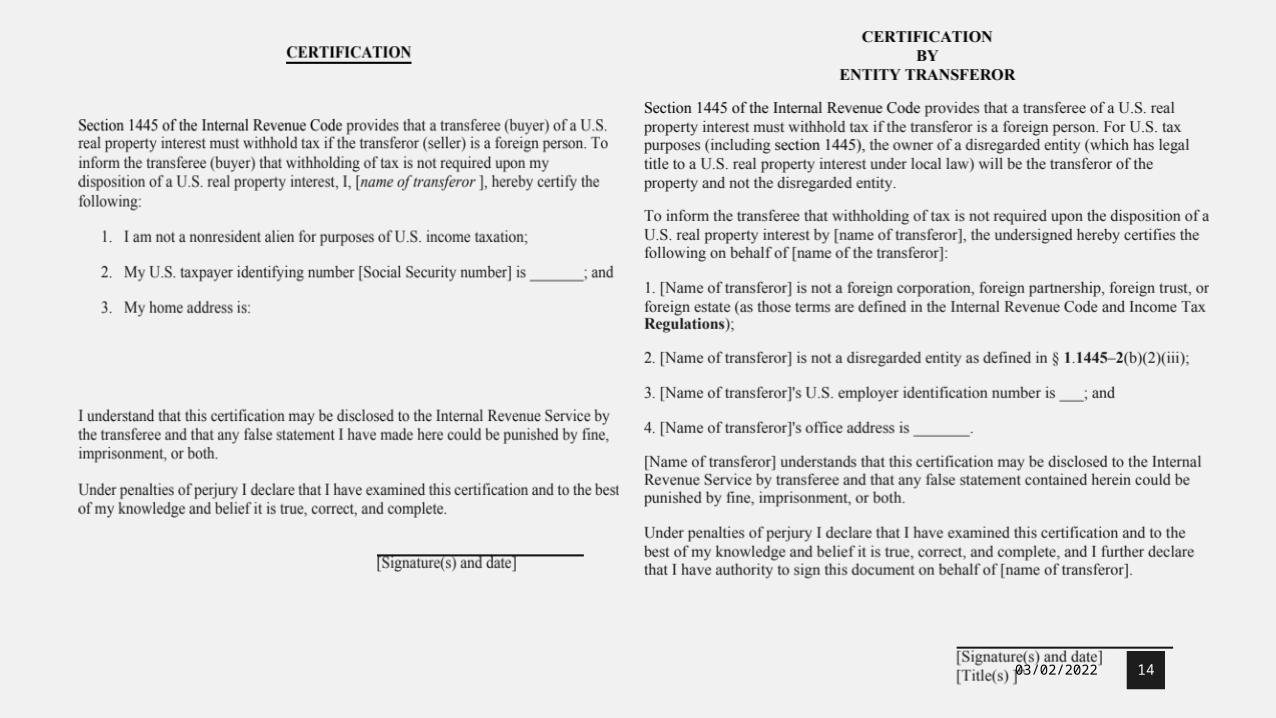

1. The Transferor is a Foreign Person, ANDa) Not a foreign person, no withholding requirementb) Certification/Non-Foreign Affidavit

a) Certification excuses the Transferee from any withholding liability

b) If foreign, no Certification/Non-Affidavit, Transferee subject to withholding.

c) Transferee retains for 5 years.

2. The Transferee is acquiring a USRPI.

05/01/2023

EXAMPLETransferor Furnishes Nonforeign Affidavit

• Treas. Reg use the term “certification”, not affidavit, (notary public not needed)

• Executed under penalties of perjury• Transferee may rely on the

affidavit/certification without conducting an investigation verifying truthfulness.

• Liability of “actual knowledge” of untruthfulness or notice that its false

26 US Code Section 1445 (2); Reg.1.1445-2(b)(2)(i)

Joe, the seller of a piece of property, gives Lenny his Agent, a Non-Foreign Status Certification. Lenny knows that the Certification is false. What are Lenny’s obligations?

13

DUTY TO WITHHOLD SECTION 1445; REG. 1.1445-1(e)

(IF AND ONLY IF)

05/01/2023 14

05/01/2023

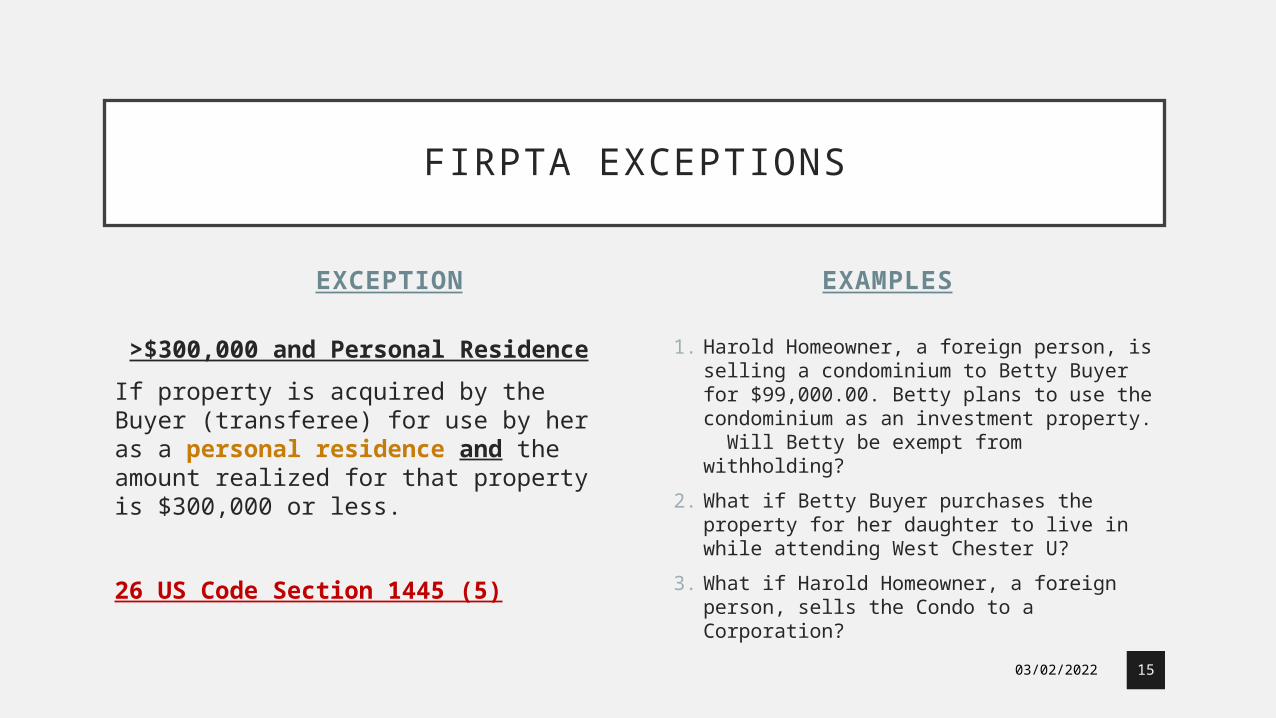

EXCEPTION

>$300,000 and Personal ResidenceIf property is acquired by the Buyer (transferee) for use by her as a personal residence and the amount realized for that property is $300,000 or less.

26 US Code Section 1445 (5)

1. Harold Homeowner, a foreign person, is selling a condominium to Betty Buyer for $99,000.00. Betty plans to use the condominium as an investment property. Will Betty be exempt from withholding?

2. What if Betty Buyer purchases the property for her daughter to live in while attending West Chester U?

3. What if Harold Homeowner, a foreign person, sells the Condo to a Corporation?

EXAMPLES

15

FIRPTA EXCEPTIONS

05/01/2023

EXCEPTION

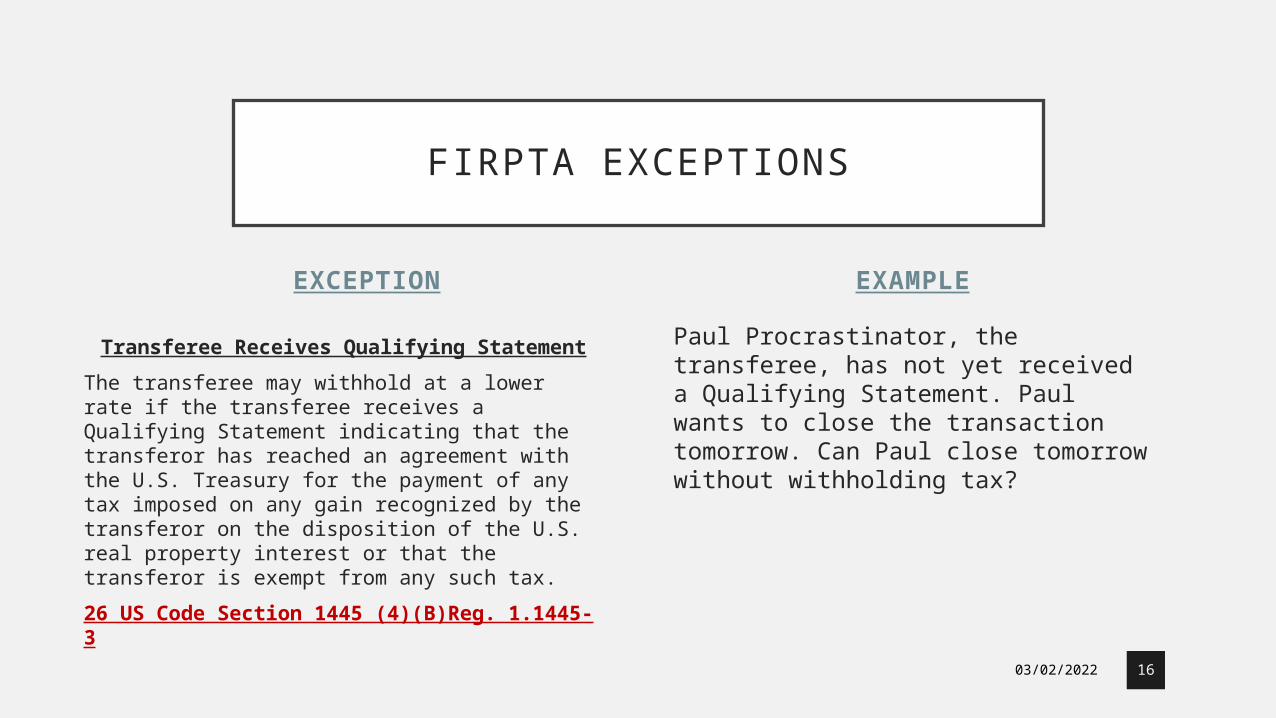

Transferee Receives Qualifying StatementThe transferee may withhold at a lower rate if the transferee receives a Qualifying Statement indicating that the transferor has reached an agreement with the U.S. Treasury for the payment of any tax imposed on any gain recognized by the transferor on the disposition of the U.S. real property interest or that the transferor is exempt from any such tax.26 US Code Section 1445 (4)(B)Reg. 1.1445-3

Paul Procrastinator, the transferee, has not yet received a Qualifying Statement. Paul wants to close the transaction tomorrow. Can Paul close tomorrow without withholding tax?

EXAMPLE

16

FIRPTA EXCEPTIONS

05/01/2023

FIRPTA EXCEPTIONS

OTHER EXCEPTIONS

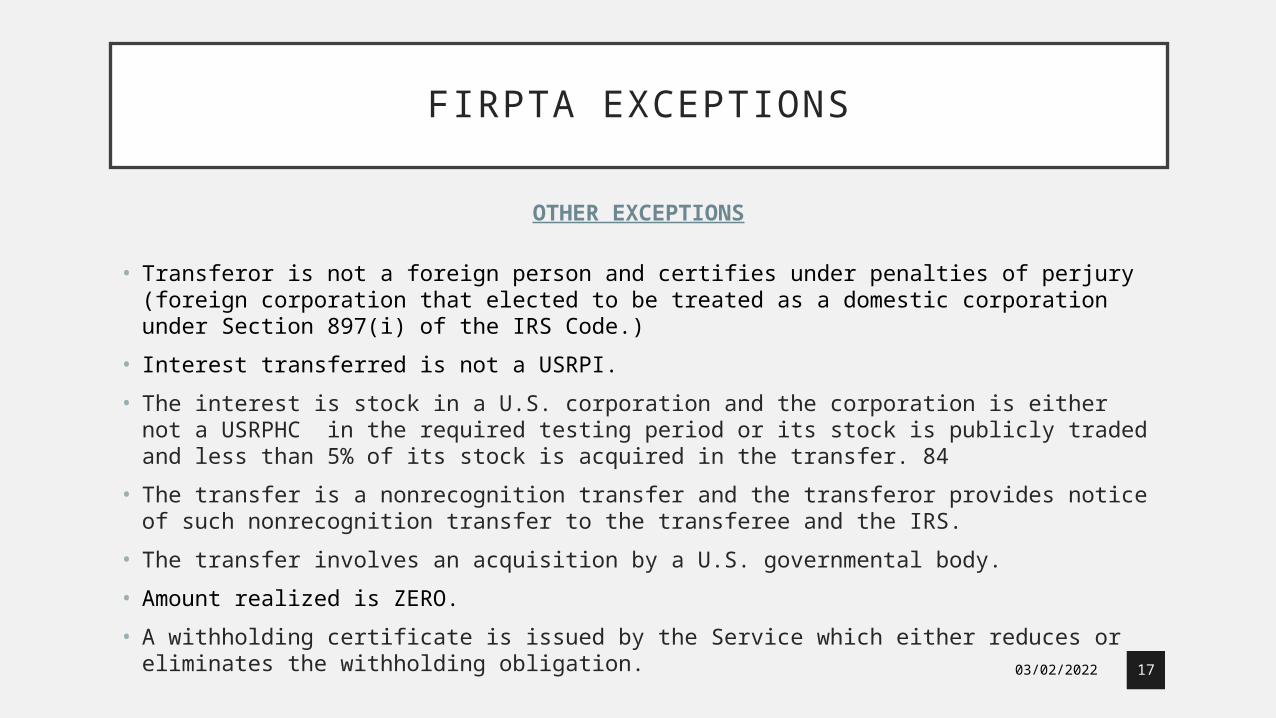

• Transferor is not a foreign person and certifies under penalties of perjury (foreign corporation that elected to be treated as a domestic corporation under Section 897(i) of the IRS Code.)

• Interest transferred is not a USRPI.• The interest is stock in a U.S. corporation and the corporation is either not a USRPHC in the

required testing period or its stock is publicly traded and less than 5% of its stock is acquired in the transfer. 84

• The transfer is a nonrecognition transfer and the transferor provides notice of such nonrecognition transfer to the transferee and the IRS.

• The transfer involves an acquisition by a U.S. governmental body. • Amount realized is ZERO. • A withholding certificate is issued by the Service which either reduces or eliminates the

withholding obligation. 17

05/01/2023

MUST WITHHOLDNOW WHAT??

• 10% or 15% of the sale price collected at closing • IRS within 20 days of the closing date

OR • withholding certificate is submitted

before closing • Who requests withholding

certificate? Transferee, Transferee’s Agent, or Transferor

• 90 days (currently 200 days)• Form 8288 and Form 8288a• 10% or 15% is held by the closing

agent. 18

05/01/2023

NO PROFIT! MUST I WITHHOLD

• File a withholding certificate• Closing Agent files a Form 8288 and Form

8288-B • Show original deed with doc stamps

(original purchase price)• Original closing statements• Showing improvements which increases

the basis of the home• Show proposed closing statements and

new sale agreement• Must be submitted before closing takes

place• No submittal then you must withhold

19

05/01/2023

CLIENT NEEDS AN ITIN

IRS Acceptance Agent Program:

Felix R. Strater IIId/b/a Liberty Tax Service 5351

323 East Gay StreetWest Chester, PA 19380Phone: (610) 696-5540

https://www.irs.gov/Individuals/Acceptance-Agents---Pennsylvania

20

05/01/2023

LIABILITY: AGENTS AND QUALIFIED SUBSTITUTES

Remember – “Who is the Agent?”• Transferor’s Agent? • Transferee’s Agent?• Qualified Substitute?

Bears the Risk of Liability?• >$300,000 and Personal Residence – Transferee Liable • Failure to Furnish Notice• Notice of False Affidavit• “Actual Knowledge”• Duty To Notify

21

![storage.googleapis.com · (f) Is Seller a "foreign person" as described in the Foreign Investment in Real Property Tax Act (FIRPTA)? C] Yes g NO A "foreign person" is a nonresident](https://img.dokumen.tips/doc/110x75/5ffe11986864516dc947e909/f-is-seller-a-foreign-person-as-described-in-the-foreign-investment.jpg)