Embed Size (px)

Citation preview

Speaker Firms and Organization:

Greenberg Traurig, LLPCarl J. RileyShareholder

DLA Piper LLPRobert J. Le Duc

Partner, Co-Chair, National REIT Tax Practice

Seyfarth Shaw LLPJohn P. Napoli

Partner

Thank you for logging into today’s event. Please note we are in standby mode. All Microphones will be muted until the event starts. We will be back with speaker instructions @ 11:55am. Any Questions? Please email: [email protected]

Group Registration Policy

Please note ALL participants must be registered or they will not be able to access the event. If you have more than one person from your company attending, you must fill out the group registration form. We reserve the right to disconnect any unauthorized users from this event and to deny violators admission to future events.

To obtain a group registration please send a note to [email protected] or call 646.202.9344.

Presented By:

March 17, 2014

1

Partner Firms:

March 17, 2014

2

If you experience any technical difficulties during today’s WebEx session, please contact our Technical Support @ 866-779-3239.

You may ask a question at anytime throughout the presentation today via the chat window on the lower right hand side of your

screen. Questions will be aggregated and addressed during the Q&A segment.

Please note, this call is being recorded for playback purposes.

If anyone was unable to log in to the online webcast and needs to download a copy of the PowerPoint presentation for today’s

event, please send an email to: [email protected]. If you’re already logged in to the online webcast, we will post a link

to download the files shortly.

If you are listening on a laptop, you may need to use headphones as some laptops speakers are not sufficiently amplified enough to

hear the presentations. If you do not have headphones and cannot hear the webcast send an email to

and we will send you the dial in phone number.

March 17, 2014

3

About an hour or so after the event, you'll be sent a survey via email asking you for your feedback on your experience with this

event

today - it's designed to take less than two minutes to complete, and it helps us to understand how to wisely invest your time in future

events. Your feedback is greatly appreciated. If you are applying for continuing education credit, completions of the surveys are

mandatory as per your state boards and bars. 6 secret words (3 for each credit hour) will be given throughout the presentation. We

will ask you to fill these words into the survey as proof of your attendance. Please stay tuned for the secret word.

Speakers, I will be giving out the secret words at randomly selected times. I may have to break into your presentation briefly to read

the secret word. Pardon the interruption.

March 17, 2014

4

Welcome to the Knowledge Group Unlimited Subscription Programs. We have Two Options Available for You: FREE UNLIMITED: This program is free of charge with no further costs or obligations. It includes:

Unlimited access to over 15,000 pages of course material from all Knowledge Group Webcasts. Subscribers to this program can download any slides, white papers, or supplemental material covered during all live webcasts.

50% discount for purchase of all Live webcasts and downloaded recordings.

PAID UNLIMITED: Our most comprehensive and cost-effective plan, for a one-time fee:

Access to all LIVE Webcasts (Normally $199 to $349 for each event without a subscription). Including: Bring-a-Friend – Invite a client or associate outside your firm to attend for FREE. Sign up for as many webcasts as you wish.

Access to all of Recorded/Archived Events & Course Material includes 1,500+ hours of audio material (Normally $299 for each event without a subscription).

Free CLE/CPE/CE Processing (Normally $49 Per Course without a subscription). Access to over 15,000 pages of course material from Knowledge Group Webcasts. Ability to invite a guest of your choice to attend any live webcast Free of charge (Exclusive benefit only available for PAID UNLIMITED

subscribers). 6 Month Subscription is $299 with No Additional Fees Other options are available. Special Offer: Sign up today and add 2 of your colleagues to your plan for free Check the “Triple Play” box on the sign-up sheet

contained in the link below.

https://gkc.memberclicks.net/index.php?option=com_mc&view=mc&mcid=form_157964

March 17, 2014

5

Knowledge Group UNLIMITED PAID Subscription Programs Pricing: Individual Subscription Fees: (2 Options)Semi-Annual: $299 one-time fee for a 6 month subscription with unlimited access to all webcasts, recordings, and materials. Annual: $499 one-time fee for a 12 month unlimited subscription with unlimited access to all webcasts, recordings, and materials.

Group plans are available. See the registration form for details.

Best ways to sign up:1.Fill out the sign up form attached to the post conference survey email.2.Sign up online by clicking the link contained in the post conference survey email. 3. Click the link below or the one we just posted in the chat window to the right. https://gkc.memberclicks.net/index.php?option=com_mc&view=mc&mcid=form_157964

Discounts: Enroll today and you will be eligible for the “Triple Play” program and 3% off if you pay by credit card. Also we will waive the $49 CLE/CPE processing fee for today’s conference. See the form attached to the post conference survey email for details.

Questions: Send an email to: [email protected] with “Unlimited” in the subject.

Partner Firms:

March 17, 2014

6

Greenberg Traurig, LLP (GT) is an international, multi-practice law firm with approximately 1750 attorneys serving clients from 36 offices in the United States, Latin America, Europe, the Middle East and Asia. GT is among the Top 10 law firms on The National Law Journal's 2013 NLJ 350, an annual

ranking of the largest firms in the U.S.

GT provides integrated legal services for clients worldwide. It offers a multidisciplinary team, including senior lawyers who have been the chief

legal officers at major multinational companies and have spent years solving real-world problems in the business, political and legal environments of

major commercial centers. GT’s experience in more than 100 practice areas and network of contacts throughout the world position the firm to help clients

achieve their objectives both domestically and in the global marketplace.

DLA Piper is a global law firm, with approximately 4,200 lawyers located in more than 30 countries throughout the Americas, Asia Pacific, Europe and

the Middle East.

Partner Firms:

March 17, 2014

7

Seyfarth Shaw LLP has more than 800 attorneys in the U.S., London, Shanghai, Melbourne and Sydney, and provides a broad range of legal services in the areas of corporate, real estate, labor and employment,

employee benefits, and litigation. The firm is a recognized leader in delivering value and innovation for legal services, and its acclaimed

SeyfarthLean client service model has earned numerous accolades from a variety of highly respected third parties, including industry associations,

consulting firms and media.

Seyfarth Shaw’s REIT practice is interdisciplinary, comprised of attorneys with corporate, securities, real estate and tax law expertise who represent

public and private REITs as outside general counsel and in specific finance, development, acquisition and disposition transaction, as well as advising on reporting obligations under Sarbanes-Oxley and SEC filings. Attorneys in the

practice have comprehensive experience in all stages of REIT operations, and represent every type of REIT including equity, mortgage, hybrid, special purpose REITs, public and private REITs, and funds that invest in REITs.

Brief Speaker Bios:

Carl J. Riley

Carl J. Riley is a Shareholder in Greenberg Traurig's New York Office. Carl focuses his practice on complex tax matters, specializing in real estate-related matters, including initial public offerings, formations and other securities issuances, with particular emphasis on transactions involving REITs. He is experienced with tax rulings and treaties, administrative practice before taxing authorities, and the Foreign Investment in Real Property Tax Act (FIRPTA). In addition, Carl advises clients regarding mergers and acquisitions, securities offerings, and transactions involving regulated investment companies (RICs), partnerships, pension funds and other tax exempt entities, and sovereign wealth funds. He is also experienced in the formation, diligencing, structuring and implementation of various investments and acquisitions involving private equity funds. He received his J.D. and LL.M. from the New York University School of Law.

March 17, 2014

8

Robert J. Le Duc

Robert J. Le Duc concentrates his practice in federal and international income taxation. Mr. Le Duc also has extensive experience in the real estate and mortgage-related areas, including representation of real estate funds, debt funds, and publicly traded and privately owned equity and mortgage real estate investment trusts (REITs). He has structured dozens of debt and equity offerings, REIT mergers and acquisitions, formations of private REITs, partnership roll-ups and various mortgage REIT transactions. In addition, Mr. Le Duc has provided tax advice regarding numerous cross border real estate investments and cross border financing transactions, with particular focus on advising non-US governmental investors.Legal 500 names Mr. Le Duc for his REIT practice, calling him "extremely responsive."

Brief Speaker Bios:

John P. Napoli

John Napoli is co-managing partner of Seyfarth Shaw’s New York office, where he practices in the areas of federal, state and local taxation and chairs the firm’s national Tax practice group. Mr. Napoli advises public and private clients on tax issues relating to corporate mergers and acquisitions, restructurings, consolidations, financing, real estate (including REITs), tax free like kind 1031 exchanges, subchapter S corporations, partnerships, joint ventures, and limited liability companies. Mr. Napoli has been instrumental in structuring numerous tax-efficient real estate transactions, including the formation, operation and liquidation of REITs and UPREITs. He also represents clients before the Internal Revenue Service, United States Tax Court, and various state and local authorities on a variety of controversy matters. Mr. Napoli has an AV rating in Martindale Hubbell, has been selected for inclusion in Super Lawyers–NY Metro every year since 2006, and in 2011, was named to the NACD Directorship’s “Directorship 100” list of “people to watch” in corporate America.

March 17, 2014

9

► For more information about the speakers, you can visit: http://theknowledgegroup.org/event_name/us-reits-for-foreign-investment-understanding-advantages-under-firpta-proposed-reforms-live-webcast/

Real estate investment trusts (REITs) have long been considered to be tax-efficient vehicles for foreign investments in U.S. real estate. Recently, the Obama administration and members of Congress have issued various legislative proposals that encourage private infrastructure investment. These proposals are intended to attract foreign capital to the U.S. real estate market by reducing existing tax barriers to investment, primarily under the Foreign Investment in Real Property Tax Act of 1980 (commonly known as FIRPTA).

Many (but not all) of these reforms could enhance the value of REITs as vehicles for foreign investment in the United States. However, since REITs are subject to complex rules related to income, assets, share ownership, and distribution of income, they can represent challenges to adopters and investors.

In this 2-hour live webcast, our panel of key thought leaders and practitioners will offer insight with respect to the latest and significant issues surrounding foreign investment in U.S. real estate through REITs.

March 17, 2014

10

Featured Speakers:

March 17, 2014

11

Carl J. RileyShareholderGreenberg Traurig, LLP

Robert J. Le DucPartner, Co-Chair, National REIT Tax PracticeDLA Piper LLP

John P. NapoliPartnerSeyfarth Shaw LLP

Introduction

Carl J. Riley is a Shareholder in Greenberg Traurig's New York Office. Carl focuses his practice on complex tax matters,

specializing in real estate-related matters, including initial public offerings, formations and other securities issuances, with

particular emphasis on transactions involving REITs. He is experienced with tax rulings and treaties, administrative practice

before taxing authorities, and the Foreign Investment in Real Property Tax Act (FIRPTA). In addition, Carl advises clients

regarding mergers and acquisitions, securities offerings, and transactions involving regulated investment companies

(RICs), partnerships, pension funds and other tax exempt entities, and sovereign wealth funds. He is also experienced in

the formation, diligencing, structuring and implementation of various investments and acquisitions involving private equity

funds. He received his J.D. and LL.M. from the New York University School of Law.

March 17, 2014

12

Corey ParkerSenior ConsultantBaker Tilly Virchow Krause, LLP

Carl J. RileyShareholderGreenberg Traurig, LLP

Introduction

Robert J. Le Duc concentrates his practice in federal and international income taxation. Mr. Le Duc also has extensive experience in the real estate and mortgage-related areas, including representation of real estate funds, debt funds, and publicly traded and privately owned equity and mortgage real estate investment trusts (REITs). He has structured dozens of debt and equity offerings, REIT mergers and acquisitions, formations of private REITs, partnership roll-ups and various mortgage REIT transactions. In addition, Mr. Le Duc has provided tax advice regarding numerous cross border real estate investments and cross border financing transactions, with particular focus on advising non-US governmental investors.

Legal 500 names Mr. Le Duc for his REIT practice, calling him "extremely responsive."

March 17, 2014

13

Reshma Patel - JacksonManagerBaker Tilly Virchow Krause, LLP

Robert J. Le DucPartner, Co-Chair, National REIT Tax PracticeDLA Piper LLP

Introduction

John Napoli is co-managing partner of Seyfarth Shaw’s New York office, where he practices in the areas of federal, state

and local taxation and chairs the firm’s national Tax practice group. Mr. Napoli advises public and private clients on tax

issues relating to corporate mergers and acquisitions, restructurings, consolidations, financing, real estate (including

REITs), tax free like kind 1031 exchanges, subchapter S corporations, partnerships, joint ventures, and limited liability

companies. Mr. Napoli has been instrumental in structuring numerous tax-efficient real estate transactions, including the

formation, operation and liquidation of REITs and UPREITs. He also represents clients before the Internal Revenue

Service, United States Tax Court, and various state and local authorities on a variety of controversy matters. Mr. Napoli

has an AV rating in Martindale Hubbell, has been selected for inclusion in Super Lawyers–NY Metro every year since 2006,

and in 2011, was named to the NACD Directorship’s “Directorship 100” list of “people to watch” in corporate America.

March 17, 2014

14

Reshma Patel - JacksonManagerBaker Tilly Virchow Krause, LLP

John P. NapoliPartnerSeyfarth Shaw LLP

Table of Contents

15

Roadmap 16

U.S. Source Income•Foreign Investors 18

•Investment (“FDAP”) Income 19•Business Income 20•FDAP or ECI? 21

•Comparison of Income Categories 22•Tax Treaties 23•Taxation of Gains 24

Foreign Investments in U.S. Real Estate•Gains from USRPIs 29

•What is a USRPI? 30•What is a REIT? 31•REIT Requirements 32

•Taxation of REIT Distributions 33•FIRPTA Tax Triggers 34

•FIRPTA Exceptions 35

•Notice 2007-55 36•Dividends for 5% or Less Exception 37

•Section 892 – Foreign Government Exceptions 38

•Requirements of Section 892 39•Investment Vehicle Comparison 40

•Summary 41

Commonly Used Structures

•Base Case Real Estate Fund Structure 44•Base Case REIT Structure 45•Mini REIT Strategy 46

•Leveraged Blocker Structure 47•Portfolio Interest Summary 48

Recent Legislative Proposals•Obama Administration Proposal 51•Real Estate Investment and Jobs Act of 2013 (REIJA) 52

•Senate Finance Committee Discussion Draft 54•Camp Proposals 55•Summary of the Various Proposals 57

Circular 230 Notice 58

Roadmap

• First, we’ll discuss general tax rules relating to non-U.S. persons with U.S.-source income (slides 17-24)

• Then, we’ll turn to specific rules relating to foreign investments in U.S. real estate, including the use of REITs (slides 28-41)

• We will then examine certain common structures that are used for foreign investments in U.S. real estate (slides 42-48)

• Finally, we’ll look at recent tax reform proposals and how they would impact these rules (slides 49-57)

March 17, 2014

16

March 17, 2014

17

U.S. Source IncomeU.S. Source Income

Corey ParkerSenior ConsultantBaker Tilly Virchow Krause, LLP

Carl J. RileyShareholderGreenberg Traurig, LLP

U.S. Source Income

• Non-U.S. persons – two types of income from U.S. sources, with different rules:

– Investment income– Business income

• Categories are mutually exclusive

March 17, 2014

18

Foreign InvestorsForeign Investors

Corey ParkerSenior ConsultantBaker Tilly Virchow Krause, LLP

Carl J. RileyShareholderGreenberg Traurig, LLP

U.S. Source Income

• Investment income:– Interest, dividends, rents, salaries, wages, premiums, annuities, compensations,

remunerations, emoluments, and other “fixed or determinable annual or periodical” gains, profits, and income (“FDAP”)

– Don’t be misled

• Certain interest, dividends and gains can be business income rather than investment income

• Most rents, salaries and wages are considered to be business income rather than investment income

March 17, 2014

19

Investment (“FDAP”) IncomeInvestment (“FDAP”) Income

Corey ParkerSenior ConsultantBaker Tilly Virchow Krause, LLP

Carl J. RileyShareholderGreenberg Traurig, LLP

U.S. Source Income

• Business income:– Income which is effectively connected with the conduct of a trade or business within the United

States (so-called “effectively connected income”, or “ECI”)

March 17, 2014

20

Business IncomeBusiness Income

Corey ParkerSenior ConsultantBaker Tilly Virchow Krause, LLP

Carl J. RileyShareholderGreenberg Traurig, LLP

U.S. Source Income

• Although investment income (FDAP) and business income (ECI) are subject to different tax treatment (as discussed below), it is not always easy to categorize a given item of income. Examples:

– Rental income is generally business income• However, income from property that is net leased may be investment income

– Interest income is often investment income• However, interest received by a foreign person on loans that it originated may be business

income

March 17, 2014

21

FDAP or ECI?FDAP or ECI?

Corey ParkerSenior ConsultantBaker Tilly Virchow Krause, LLP

Carl J. RileyShareholderGreenberg Traurig, LLP

U.S. Source Income

• So which is better – investment income or business income?– Hint: it depends

• Comparison of Income Categories:

March 17, 2014

22

Comparison of Income CategoriesComparison of Income Categories

Type of incomeMaximum

tax rate

Is income offset by

expenses?

Can treaties reduce the tax

rate?

Must foreign recipient file a

U.S. tax return?

Investment income (FDAP)

30%;0% on “portfolio

interest”*No Yes No

Business income (ECI)

35% (corporate)39.6% (non-corporate)

Yes No** Yes

*Generally, interest paid to a foreign person who holds less than 10% of the voting stock of the payor.

**Most treaties raise the threshold of necessary connections to the US to make business income subject to US taxation. In the case of real estate investments, this higher threshold will likely be met anyway.

Corey ParkerSenior ConsultantBaker Tilly Virchow Krause, LLP

Carl J. RileyShareholderGreenberg Traurig, LLP

U.S. Source Income

• U.S. tax treaties– Where applicable, can lower the U.S. withholding tax rate on certain types of investment income

(e.g., interest and dividends)– Can only help; can’t hurt– Don’t help with gains from sale of U.S. real estate– Generally don’t help with treatment of business income in the context of real estate investments

– “Limitation on benefits” provisions designed to combat “treaty shopping”

March 17, 2014

23

Tax TreatiesTax Treaties

Reshma Patel - JacksonManagerBaker Tilly Virchow Krause, LLP

Robert J. Le DucPartner, Co-Chair, National REIT Tax PracticeDLA Piper LLP

U.S. Source Income

• But how are GAINS treated?– Most gains from sales of investment assets would be treated as investment income

• Example: foreign person holds Apple stock as an investment; sells it at a gain– In general, this would be investment income and not business income– However, better still, most gains on investment assets (intangible personal property)

are sourced to the seller’s jurisdiction – i.e., not treated as U.S. source income; no U.S. tax

• BIG exception: gains from sale of interests in U.S. real estate

March 17, 2014

24

Taxation of GainsTaxation of Gains

Reshma Patel - JacksonManagerBaker Tilly Virchow Krause, LLP

Robert J. Le DucPartner, Co-Chair, National REIT Tax PracticeDLA Piper LLP

May 30, 2013

25

CLE PROCESSINGThe Knowledge Group offers complete CLE processing solutions for your webcasts and land events. This comprehensive service includes everything you need to offer CLE credit at your conference: Complete end-to-end CLE credit SolutionsSetting up your marketing collateral properly.Completing and filing all of the applications to the state bar.Guidance on how to structure content meet course material requirements for the state Bars.Sign up forms to be used to check & confirm attendance at your event. Issuing official Certificates of Attendance for credit to attendees. Obtaining CLE credit varies from state to state and the rules can be complex. The Knowledge Group will help you navigate the complexities via complete cost effective CLE solutions for your conferences. Most CLE processing plans are just $499 plus filing fees and postage.

To learn more email us at [email protected] or CALL 646-202-9344

May 30, 2013

26

PRIVATE LABEL PROGRAM & INTERNAL TRAINING The Knowledge Group provides complete private label webcasts and in-house training solutions. Developing and executing webcasts can be a huge logistical nightmare. There are a lot of moving parts and devolving a program that is executed smoothly and cost effectively can prove to be a significant challenge for companies who do not produce events on a regular basis. Live events require a high level of proficiency in order to execute proficiently. Our producers will plan and develop your webcast for you and our webcast technicians will execute your live event with expert precision. We have produced over 1000 live webcasts. Put our vast expertise to work for you. Let us develop a professional webcast for your firm that will impress all your clients and internal stakeholders. Private Label Programs Include: Complete Project ManagementTopic DevelopmentRecruitment of Speakers (Or you can use your own)Marketing Material DesignPR CampaignMarketing CampaignEvent Webpage DesignSlides: Design and Content DevelopmentSpeaker coordination: Arranging & Executing Calls, Coordinating Slides & ContentAttendee RegistrationComplete LIVE Event Management for Speaker and Attendees including:

o Technical Supporto Event Moderatoro Running the Live event (All Aspects)o Multiple Technical Back-ups & Redundancies to Ensure a Perfect Live Evento Webcast Recording (MP3 Audio & MP4 Video)o Post Webcast Performance Survey

CLE and CPE Processing Private Label Programs Start at just $999

May 30, 2013

27

RESEARCH & BUSINESS PROCESS OUTSOURCING The Knowledge Group specializes in highly focused and intelligent market and topic research. Outsource your research projects and business processes to our team of experts. Normally we can run programs for less than 50% of what it would cost you to do it in-house. Here are some ideal uses for our services: Market Research and Production

o List Research (Prospects, Clients, Market Evaluation, Sales Lists, Surveys)o Design of Electronic Marketing Collateralo Executing Online Marketing Campaigns (Direct Email, PR Campaigns)o Website Designo Social Media

Analysis & Research

o Research Companies & Produce Reportso Research for Cases o Specialized Research Projects

eSales (Electronic Inside Sales – Email and Online)

o Sales Leads Developmento eSales Campaigns

Inside Sales people will prospect for leased, contact them and coordinate with your sales team to follow up. Our Inside eSales reps specialize in developing leads for big-ticket enterprise level products and services.

o Electronic Database Building – Comprehensive service which includes deveolment od sales leads, contacting clients, scoring leads, adding notes and transferring the entire data set to you for your internal sales reps.

eCustomer Service (Electronic Inside Sales – Email and Online)

o Real-Time Customer Service for Your clients Online Chat Email

o Follow-Up Customer Service Responds to emails Conducts Research Replies Back to Your Customer

Please note these are just a few ways our experts can help with your Business Process Outsourcing needs. If you have a project not specifically listed above please contact us to see if we can help.

March 17, 2014

28

Foreign Investments in U.S. Real Estate

Foreign Investments in U.S. Real Estate

Reshma Patel - JacksonManagerBaker Tilly Virchow Krause, LLP

John P. NapoliPartnerSeyfarth Shaw LLP

Foreign Investments in U.S. Real Estate

• Gains from the sale of U.S. real property interests (“USRPIs”)– Pursuant to the Foreign Investment in Real Property Tax Act (“FIRPTA”), gains from sales of

USRPIs by foreign persons are taxed as U.S. source business income

March 17, 2014

29

Gains from USRPIsGains from USRPIs

Reshma Patel - JacksonManagerBaker Tilly Virchow Krause, LLP

John P. NapoliPartnerSeyfarth Shaw LLP

Foreign Investments in U.S. Real Estate

• USRPIs subject to FIRPTA include:

– Buildings, land, leasehold interests, easements, options to acquire U.S. real estate, certain mineral interests, etc.

– Interests other than solely as a creditor (e.g., loans with equity kickers such as shared appreciation mortgages)

– Stock of U.S. real property holding corporations (“USRPHCs”)• A USRPHC is a U.S. corporation, 50% or more of the assets of which consist of USRPIs

March 17, 2014

30

What is a USRPI?What is a USRPI?

Reshma Patel - JacksonManagerBaker Tilly Virchow Krause, LLP

John P. NapoliPartnerSeyfarth Shaw LLP

Foreign Investments in U.S. Real Estate

• Use of Real Estate Investment Trusts (“REITs”) to hold U.S. real estate – what is a REIT?

– Creature of the tax law– Special type of U.S. corporation – so it generally blocks receipt of business income by its

shareholders – that is focused on real estate

• Subject to various qualification requirements / tests• Must distribute substantially all of its ordinary income each year (at least 90%)• Allowed a tax deduction for dividends paid (so pays little or no income tax)

March 17, 2014

31

What is a REIT?What is a REIT?

Corey ParkerSenior ConsultantBaker Tilly Virchow Krause, LLP

Carl J. RileyShareholderGreenberg Traurig, LLP

Foreign Investments in U.S. Real Estate

• Key requirements for REIT qualification:– Gross asset and income tests

• at least 75% must generally be real estate-related (e.g., rental real estate or mortgages), and

• at least 95% of the income must be real estate-related and/or passive investment income– Shareholder requirements

– Distribution requirements– Generally can’t be considered a dealer (e.g., condo developer)– Other requirements

March 17, 2014

32

REIT RequirementsREIT Requirements

Corey ParkerSenior ConsultantBaker Tilly Virchow Krause, LLP

Carl J. RileyShareholderGreenberg Traurig, LLP

Foreign Investments in U.S. Real Estate

• Tax treatment of distributions by REITs– Dividends (e.g., attributable to rental income) generally treated by foreign investors as

investment income; not business income– However, if a REIT has a capital gain (e.g., from selling U.S. real estate) and pays a dividend,

the character passes through to shareholders

• Good for U.S. individuals, because capital gain income is taxed at a lower rate than dividend income paid by a REIT (20% max v. 39.6% max)

• Sucks for foreign investors because generally subject to FIRPTA (Boo!!!)

March 17, 2014

33

Taxation of REIT DistributionsTaxation of REIT Distributions

Corey ParkerSenior ConsultantBaker Tilly Virchow Krause, LLP

Carl J. RileyShareholderGreenberg Traurig, LLP

Foreign Investments in U.S. Real Estate

• So remind me again – how can FIRPTA tax arise (deemed business income)? Three ways:

– Foreign person sells interest in U.S. real estate• Directly, or via a sale through a pass-through entity such as a partnership

– Foreign person sells stock of a USRPHC

– REIT sells U.S. real estate and pays a dividend to foreign person

March 17, 2014

34

FIRPTA Tax TriggersFIRPTA Tax Triggers

Reshma Patel - JacksonManagerBaker Tilly Virchow Krause, LLP

Robert J. Le DucPartner, Co-Chair, National REIT Tax PracticeDLA Piper LLP

Foreign Investments in U.S. Real Estate

• Important exceptions – no FIRPTA tax on sale of corporate stock if:– the corporation is a REIT that is “domestically controlled”

• Domestically controlled means less than 50% foreign ownership, directly and indirectly• This exception is only available for a REIT (or a regulated investment company, or “RIC”

(i.e., a mutual fund)), but not for a regular taxable C corporation

– Also an exception if the class of stock (whether of a REIT or C corporation) is publicly traded, and the foreign investor holds 5% or less of that class

March 17, 2014

35

FIRPTA ExceptionsFIRPTA Exceptions

Reshma Patel - JacksonManagerBaker Tilly Virchow Krause, LLP

Robert J. Le DucPartner, Co-Chair, National REIT Tax PracticeDLA Piper LLP

Foreign Investments in U.S. Real Estate

• Notice 2007-55 provides for an unfortunate exception to this exception– Normally, liquidating distributions or distributions in excess of earnings and profits are treated as

proceeds from the sale of the stock for tax purposes

• Therefore, such distributions from a domestically controlled REIT should be exempt from FIRPTA

– But Notice 2007-55 says that these distributions are subject to FIRPTA• Recent legislative proposals would repeal this rule

March 17, 2014

36

Notice 2007-55Notice 2007-55

Reshma Patel - JacksonManagerBaker Tilly Virchow Krause, LLP

Robert J. Le DucPartner, Co-Chair, National REIT Tax PracticeDLA Piper LLP

Foreign Investments in U.S. Real Estate

• Where a REIT pays a dividend attributable to a sale of U.S. real estate, FIRPTA will also not apply if the stock is publicly traded and the foreign recipient owns 5% or less

– In this case, the income is taxed as regular dividend investment income• 30% statutory withholding tax rate• Possibly lower if a treaty applies

March 17, 2014

37

Dividends for 5% or Less ExceptionDividends for 5% or Less Exception

Reshma Patel - JacksonManagerBaker Tilly Virchow Krause, LLP

Robert J. Le DucPartner, Co-Chair, National REIT Tax PracticeDLA Piper LLP

Foreign Investments in U.S. Real Estate

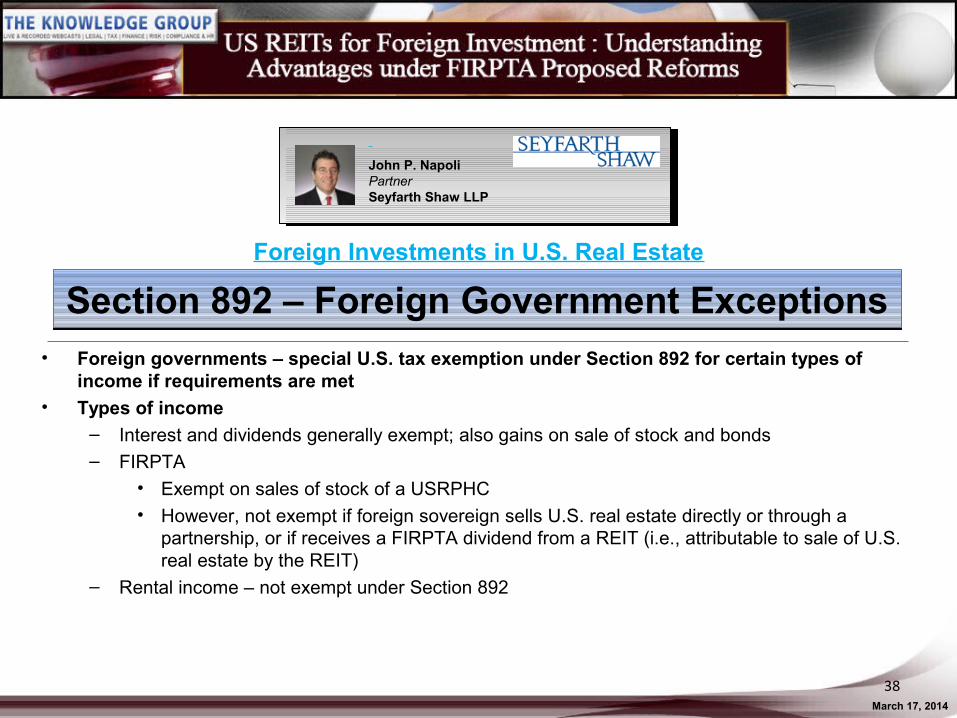

• Foreign governments – special U.S. tax exemption under Section 892 for certain types of income if requirements are met

• Types of income– Interest and dividends generally exempt; also gains on sale of stock and bonds– FIRPTA

• Exempt on sales of stock of a USRPHC• However, not exempt if foreign sovereign sells U.S. real estate directly or through a

partnership, or if receives a FIRPTA dividend from a REIT (i.e., attributable to sale of U.S. real estate by the REIT)

– Rental income – not exempt under Section 892

March 17, 2014

38

Section 892 – Foreign Government ExceptionsSection 892 – Foreign Government Exceptions

Reshma Patel - JacksonManagerBaker Tilly Virchow Krause, LLP

John P. NapoliPartnerSeyfarth Shaw LLP

Foreign Investments in U.S. Real Estate

• Key requirements for exemption for foreign sovereigns under Section 892:– Limited to certain types of income (see prior slide)

– Income is either:• Not attributable to “commercial activity” (not precisely defined, but generally similar to the

concept of business income as discussed above), or• If attributable to commercial activity (e.g., most rents), it is done through a blocker entity

(REIT or C corporation) that is not “controlled” by the foreign sovereign– Standard for “control” is 50% or more of vote or value, or other “effective control”

(e.g., certain contractual governance rights might create effective control and preclude reliance on 892)

March 17, 2014

39

Requirements of Section 892Requirements of Section 892

Reshma Patel - JacksonManagerBaker Tilly Virchow Krause, LLP

John P. NapoliPartnerSeyfarth Shaw LLP

Foreign Investments in U.S. Real Estate

March 17, 2014

40

• Comparison of Investment Vehicles:

Partnership REIT C Corporation

Entity level income tax? No

Generally no (if all income is distributed)

Yes

Does it block the flow-through of business income (ECI)?

NoGenerally yes (except FIRPTA in certain cases)

Yes

State taxes for investor (filing and payment obligations)?

Generally yes No No

Corey ParkerSenior ConsultantBaker Tilly Virchow Krause, LLP

Carl J. RileyShareholderGreenberg Traurig, LLP

Foreign Investments in U.S. Real Estate

• Recap of certain approaches to reduce U.S. tax:– Treaty (lowers the tax rate of withholding tax on investment income where qualify for benefits)– Use of a REIT as a blocker entity (i.e., generally blocks recognition by foreign shareholders of

taxable business income) while incurring little or no entity-level tax– Certain gains are not U.S. source and therefore not taxable (e.g., stocks and bonds generally;

also straight mortgage loans; but not real estate)– No FIRPTA tax if sell corporate stock:

• of domestically-controlled REIT (or RIC), or• of public company where own 5% or less

– Foreign sovereigns exempt under Section 892 on certain types of investment income where requirements are satisfied

– Corporate blocker entity pays deductible interest to foreign investors that is exempt as portfolio interest (described below)

March 17, 2014

41

SummarySummary

Reshma Patel - JacksonManagerBaker Tilly Virchow Krause, LLP

Robert J. Le DucPartner, Co-Chair, National REIT Tax PracticeDLA Piper LLP

March 17, 2014

42

Commonly Used StructuresCommonly Used Structures

Reshma Patel - JacksonManagerBaker Tilly Virchow Krause, LLP

John P. NapoliPartnerSeyfarth Shaw LLP

Commonly Used Structures

Now that we’ve digested all the relevant rules, the following slides show some typical investment structures

March 17, 2014

43

Typical Investment StructuresTypical Investment Structures

Reshma Patel - JacksonManagerBaker Tilly Virchow Krause, LLP

John P. NapoliPartnerSeyfarth Shaw LLP

March 17, 2014

44

Base Case Real Estate Fund StructureBase Case Real Estate Fund Structure

• Flexible private fund structure:

Reshma Patel - JacksonManagerBaker Tilly Virchow Krause, LLP

John P. NapoliPartnerSeyfarth Shaw LLP

Commonly Used Structures

March 17, 2014

45

Base Case REIT StructureBase Case REIT Structure

Corey ParkerSenior ConsultantBaker Tilly Virchow Krause, LLP

Carl J. RileyShareholderGreenberg Traurig, LLP

Commonly Used Structures

March 17, 2014

46

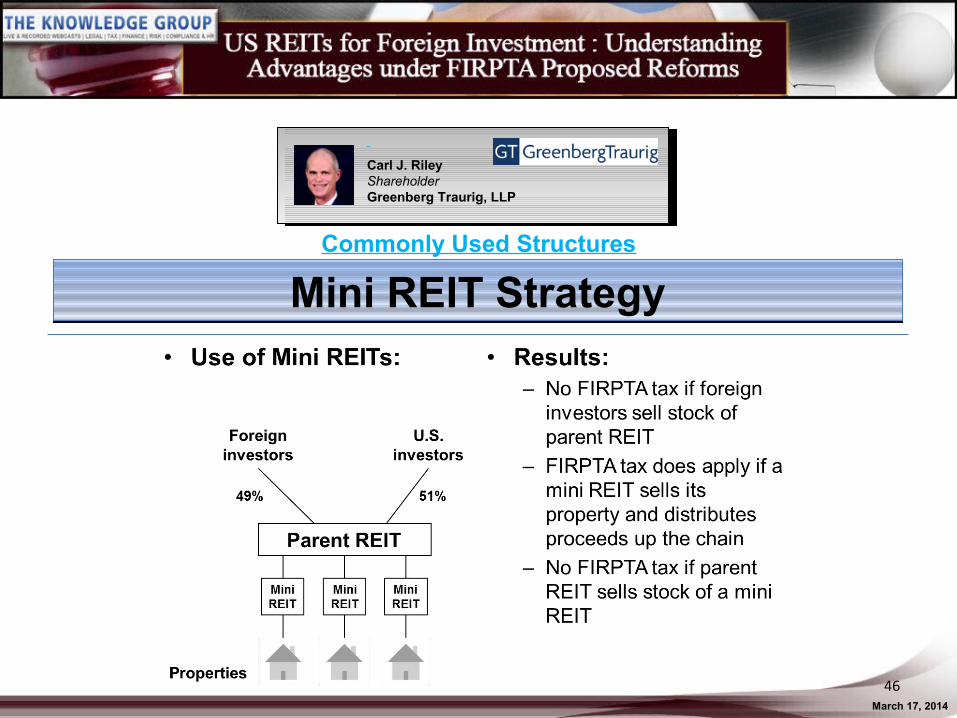

Mini REIT StrategyMini REIT Strategy

Corey ParkerSenior ConsultantBaker Tilly Virchow Krause, LLP

Carl J. RileyShareholderGreenberg Traurig, LLP

Commonly Used Structures

March 17, 2014

47

Leveraged Blocker StructureLeveraged Blocker Structure

Reshma Patel - JacksonManagerBaker Tilly Virchow Krause, LLP

Robert J. Le DucPartner, Co-Chair, National REIT Tax PracticeDLA Piper LLP

Commonly Used Structures

• Portfolio interest – where properly executed, enables corporate payor to deduct interest, which is exempt from tax by foreign recipient

• Key requirements:

– Foreign shareholder holds less than 10% of the payor’s voting stock– Debt instrument must be in “registered form” (not bearer paper)– Not applicable to contingent interest

• Certain constraints on deductibility of interest

– Interest stripping rules in Section 163(j) if too highly leveraged– Applicable high yield discount obligations (“AHYDO”) that fail certain tests

March 17, 2014

48

Portfolio Interest SummaryPortfolio Interest Summary

Reshma Patel - JacksonManagerBaker Tilly Virchow Krause, LLP

Robert J. Le DucPartner, Co-Chair, National REIT Tax PracticeDLA Piper LLP

March 17, 2014

49

Recent Legislative Proposals

Recent Legislative Proposals

Reshma Patel - JacksonManagerBaker Tilly Virchow Krause, LLP

John P. NapoliPartnerSeyfarth Shaw LLP

• Obama Administration Proposal – Released March 2013

• Real Estate Investment and Jobs Act of 2013 – Senate version (S. 1181) introduced June 18, 2013

– House version (H.R. 2870) introduced July 31, 2013 • Senate Finance Committee Discussion Draft

– Released by Sen. Max Baucus on November 19, 2013

• Tax Reform Act of 2014– Released by David Camp, Chairman of the House Ways and Means on February 26, 2014 (the

“Camp Proposals”)

March 17, 2014

50

Recent Legislative Proposals at a Glance

Recent Legislative Proposals at a Glance

Reshma Patel - JacksonManagerBaker Tilly Virchow Krause, LLP

John P. NapoliPartnerSeyfarth Shaw LLP

Recent Legislative Proposals

• Under current law, gain of a U.S. tax-exempt pension fund from the disposition of U.S. real estate generally is exempt from U.S. tax (subject to certain UBTI rules), but gain of a foreign pension fund from U.S. real estate is generally taxable under FIRPTA

• The Obama Administration has proposed exempting gains that a foreign pension fund derives from the disposition of U.S. real estate from FIRPTA rules

– A “foreign pension fund” would be defined as a trust, corporation, or other organization or arrangement that is organized or created outside of the United States and that is generally exempt from income tax in its home jurisdiction

– The foreign pension fund must generally be engaged in administering or providing pension or retirement benefits

March 17, 2014

51

Obama Administration Proposal – Released March 2013

Obama Administration Proposal – Released March 2013

Reshma Patel - JacksonManagerBaker Tilly Virchow Krause, LLP

John P. NapoliPartnerSeyfarth Shaw LLP

Recent Legislative Proposals

The following proposals are in the two REIJA bills:•Expand the FIRPTA exemptions for publicly traded REITs from the existing threshold of 5% (see slides 35 and 37) to 10%

•Legislative repeal of Notice 2007-55 (see slide 36)

•Assumption that small (i.e. <5%) shareholders of a publicly traded REIT are U.S. persons (absent actual knowledge to the contrary); stock of a REIT held by a second REIT would be presumed to be held by a foreign shareholder unless the second REIT is itself domestically controlled

March 17, 2014

52

Real Estate Investment and Jobs Act of 2013 (REIJA)

Real Estate Investment and Jobs Act of 2013 (REIJA)

Corey ParkerSenior ConsultantBaker Tilly Virchow Krause, LLP

Carl J. RileyShareholderGreenberg Traurig, LLP

Recent Legislative Proposals

• Exempt from FIRPTA stock of public and private REITs held by certain “qualified shareholders” – namely publicly traded (with certain record requirements) “qualified collective investment vehicles” in treaty jurisdictions

– A “qualified collective investment vehicle” is an entity that:• qualifies for a reduced rate of withholding on ordinary REIT dividends even though the

entity holds more than 10% of the stock of the REIT;

• is a taxable corporation, primarily engaged in an active real estate trade or business; OR • is designated as such by the Department of the Treasury (and is either fiscally transparent

or entitled to something akin to a “dividends paid deduction” (similar to that of a U.S. REIT))

March 17, 2014

53

Real Estate Investment and Jobs Act of 2013 (REIJA) (cont’d)

Real Estate Investment and Jobs Act of 2013 (REIJA) (cont’d)

Corey ParkerSenior ConsultantBaker Tilly Virchow Krause, LLP

Carl J. RileyShareholderGreenberg Traurig, LLP

Recent Legislative Proposals

The Senate Finance Committee Discussion Draft contained the following proposals:•Restrict definition of “domestically controlled REIT”•Exempt foreign pension plans from FIRPTA

•Expand the FIRPTA exemptions for publicly traded REITs from the existing threshold of 5% to 10%•Legislative repeal of Notice 2007-55•Dividends received from foreign corporations attributable to dividends from REITs not treated as U.S.-source dividends eligible for the dividends received deduction under Section 245

March 17, 2014

54

Senate Finance Committee Discussion DraftSenate Finance Committee Discussion Draft

Corey ParkerSenior ConsultantBaker Tilly Virchow Krause, LLP

Carl J. RileyShareholderGreenberg Traurig, LLP

Recent Legislative Proposals

The Camp proposals contains several changes to the REIT rules unrelated to FIRPTA:•For purposes of the REIT asset and income tests, only assets with useful lives of at least 27.5 years would qualify as real estate assets •Rents and interest would not include amounts based on percentages of receipts or sales where (i) the tenant is a C corporation and (ii) the amounts received from this tenant constitute more than 25% of the total amounts based on percentages of receipts or sales •REITs that have to distribute C corporation E&P would have to do so in cash •Reversion of Taxable REIT Subsidiary securities limit to 20% •Immediate tax on unrealized gain upon the conversion or transfer of C corporation built-in gain asset to a REIT or the acquisition of property by a REIT from a C corporation in an otherwise tax-free transaction•Prevent REITs from being a party to a tax-free spin-off transaction

March 17, 2014

55

Camp ProposalsCamp Proposals

Reshma Patel - JacksonManagerBaker Tilly Virchow Krause, LLP

Robert J. Le DucPartner, Co-Chair, National REIT Tax PracticeDLA Piper LLP

Recent Legislative Proposals

The following is Camp’s proposal relating to FIRPTA:•Interests in certain REITs not excluded from the definition of U.S. real property interests

– Under current law, any USRPHC that disposes of all its US real property in taxable dispositions ceases to be treated as a USRPHC

– Under the proposal, this beneficial rule would not apply to REITs – i.e., if a REIT sells all its US real property, it still has the status as a USRPHC for a five year period

March 17, 2014

56

Camp Proposals (cont’d)Camp Proposals (cont’d)

Reshma Patel - JacksonManagerBaker Tilly Virchow Krause, LLP

Robert J. Le DucPartner, Co-Chair, National REIT Tax PracticeDLA Piper LLP

Recent Legislative Proposals

* The Camp proposals contain a number of additional points including the following: certain short-life property not treated as real property for purposes of REIT provisions; limitation on fixed percentage rent and interest exceptions for REIT income tests; non-REIT earnings and profits required to be distributed by REIT in cash; and interests in certain REITs not excluded from definition of United States real property interests

March 17, 2014

57

Reshma Patel - JacksonManagerBaker Tilly Virchow Krause, LLP

John P. NapoliPartnerSeyfarth Shaw LLP

Recent Legislative Proposals

In compliance with U.S. Treasury Regulations, please be advised that any tax advice given herein (or in any attachment) was not intended or written to be used, and cannot be used, for the purpose of (i) avoiding tax penalties or (ii) promoting, marketing or recommending to another person any transaction or matter addressed herein.

March 17, 2014

58

Circular 230 NoticeCircular 230 Notice

► You may ask a question at anytime throughout the presentation today. Simply click on the question mark icon located on the floating tool bar on the bottom right side of your screen. Type

your question in the box that appears and click send.

► Questions will be answered in the order they are received.

Q&A:

March 17, 2014

59

Carl J. RileyShareholderGreenberg Traurig, LLP

Robert J. Le DucPartner, Co-Chair, National REIT Tax PracticeDLA Piper LLP

John P. NapoliPartnerSeyfarth Shaw LLP

May 30, 2013

60

Welcome to the Knowledge Group Unlimited Subscription Programs. We have Two Options Available for You: FREE UNLIMITED: This program is free of charge with no further costs or obligations. It includes:

Unlimited access to over 15,000 pages of course material from all Knowledge Group Webcasts. Subscribers to this program can download any slides, white papers, or supplemental material covered during all live webcasts.

50% discount for purchase of all Live webcasts and downloaded recordings.

PAID UNLIMITED: Our most comprehensive and cost-effective plan, for a one-time fee:

Access to all LIVE Webcasts (Normally $199 to $349 for each event without a subscription). Including: Bring-a-Friend – Invite a client or associate outside your firm to attend for FREE. Sign up for as many webcasts as you wish.

Access to all of Recorded/Archived Events & Course Material includes 1,500+ hours of audio material (Normally $299 for each event without a subscription).

Free CLE/CPE/CE Processing3 (Normally $49 Per Course without a subscription). Access to over 15,000 pages of course material from Knowledge Group Webcasts. Ability to invite a guest of your choice to attend any live webcast Free of charge. (Exclusive benefit only available for PAID UNLIMITED

subscribers.) 6 Month Subscription is $299 with No Additional Fees. Other options are available. Special Offer: Sign up today and add 2 of your colleagues to your plan for free. Check the “Triple Play” box on the sign-up sheet

contained in the link below.

https://gkc.memberclicks.net/index.php?option=com_mc&view=mc&mcid=form_157964

May 30, 2013

61

Knowledge Group UNLIMITED PAID Subscription Programs Pricing: Individual Subscription Fees: (2 Options)Semi-Annual: $299 one-time fee for a 6 month subscription with unlimited access to all webcasts, recordings, and materials. Annual: $499 one-time fee for a 12 month unlimited subscription with unlimited access to all webcasts, recordings, and materials.

Group plans are available. See the registration form for details.

Best ways to sign up:1.Fill out the sign up form attached to the post conference survey email.2.Sign up online by clicking the link contained in the post conference survey email. 3. Click the link below or the one we just posted in the chat window to the right. https://gkc.memberclicks.net/index.php?option=com_mc&view=mc&mcid=form_157964

Discounts: Enroll today and you will be eligible for the “Triple Play” program and 3% off if you pay by credit card. Also we will waive the $49 CLE/CPE processing fee for today’s conference. See the form attached to the post conference survey email for details.

Questions: Send an email to: [email protected] with “Unlimited” in the subject.

May 30, 2013

62

ABOUT THE KNOWLEDGE GROUP, LLC.

The Knowledge Group, LLC is an organization that produces live webcasts which examine regulatory

changes and their impacts across a variety of industries. “We bring together the world's leading

authorities and industry participants through informative two-hour webcasts to study the impact of

changing regulations.”

If you would like to be informed of other upcoming events, please click here.

Disclaimer:

The Knowledge Group, LLC is producing this event for information purposes only. We do not intend to provide or offer business advice. The contents of this event are based upon the opinions of our speakers. The Knowledge Congress does not warrant their accuracy and completeness. The statements made by them are based on their independent opinions and does not necessarily reflect that of The Knowledge Congress' views. In no event shall The Knowledge Congress be liable to any person or business entity for any special, direct, indirect, punitive, incidental or consequential damages as a result of any information gathered from this webcast.

Certain images and/or photos on this page are the copyrighted property of 123RF Limited, their Contributors or Licensed Partners and are being used with permission under license. These images and/or photos may not be copied or downloaded without permission from 123RF Limited

![삼성누버거버먼미국리츠부동산자투자신탁 H[REITs-재간접형 … · 삼성누버거버먼미국리츠부동산자투자신탁h[reits-재간접형] ... ⑤전자등록기관은](https://img.dokumen.tips/doc/110x75/5f0529607e708231d411942c/eeeeeeeeeef-hreits-e-eeeeeeeeeefhreits-e.jpg)