Embed Size (px)

Citation preview

1

TSX:MNDNOV 2017

2

This presentation contains "forward-looking statements" within the meaning of applicable securities laws, including statements relating to life ofmine production plans, exploration plans and the growth and strategy of Mandalay. Actual results and developments may differ materially fromthose contemplated by these statements depending on, among other things: exploration results or production results not meeting management’sexpectations; capital, production and operating cost results not meeting current plans; and changes in commodity prices and general market andeconomic conditions. The factors identified above are not intended to represent a complete list of the factors that could affect Mandalay. Adescription of additional risks that could result in actual results and developments differing from those contemplated by forward lookingstatements in this news release can be found under the heading “Risk Factors” in Mandalay’s annual information form dated March 31, 2017 andin its final prospectus dated July 18, 2016, copies of which are available under Mandalay's profile at www.sedar.com. Although Mandalay hasattempted to identify important factors that could cause actual actions, events or results to differ materially from those described in forward-looking statements, there may be other factors that cause actions, events or results not to be as anticipated, estimated or intended. There can beno assurance that forward-looking statements will prove to be accurate, as actual results and future events could differ materially from thoseanticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking statements.

Quality Control and Assurance

Quality control and assurance programs are implemented in line with the standards of National Instrument 43-101.

The exploration programs at Costerfield and Björkdal are supervised by Chris Gregory (Member, Australian Institute of Geoscientists, VP ofOperational Geology for Mandalay and a “Qualified Person” as defined under National Instrument 43-101. Mr. Gregory regularly visits Costerfieldand Björkdal, and supervises the collection and interpretation of scientific and technical information contained in this presentation.

The exploration programs at the Cerro Bayo and Challacollo projects are supervised by Scott Manske, Chief Cordilleran Geologist of MandalayResources, and an Oregon registered Professional Geologist. A “Qualified Person” as defined by NI 43-101, he has reviewed and approved thetechnical and scientific information on these projects contained in the presentation.

Dr. Mark Sander (Member: AusIMM), President and CEO of Mandalay, has visited the Costerfield, Cerro Bayo, Challacollo, and Björkdal andhas supervised the preparation of this presentation.

All currency references in US$ unless otherwise indicated.

Forward-looking Statements

3

A Values-Based and Value-Focused Company

WE ARE SUCCESSFUL WHEN:

Our employees live and work safely and experience the

personal satisfaction that comes with high performance

and recognition

The communities in which we operate value our

presence

Our environmental impact is minimized and causes no

permanent harm

We have a large, diversified set of customers who are

delighted with and compete for our products

Our shareholders realize a superior total return on their

investment and support our corporate values

Our values are visibly demonstrated by strong local

management, at the point of impact with our stakeholders,

and coordinated across the Company for maximum effect

4

Designed for Value: How We are Different

Acquire only when we see possibility of an immediately accretive transaction with

strong value uplift in 3-5 years

Target cash cost of production: 50% of ‘reversion to mean’ metal price

100% ownership; no private royalties, no streams

Flat, virtual, low-cost organizational structure; local GM accountability

Direct relationships and sales contracts with customers

Return cash to shareholders when possible

No hedging of metal prices

Stingy with equity

Reasonably levered

(PRODUCTION SUSPENDED)

5

1.7

32

79.967.7 64.4 68

50.9

-0.8

30.6

61.275.9

52.4

73.4

53.7

20.6

92.2

171.8

166.9

184.6194.5

185.51,224

1,570

1,670

1,411

1,2651,160 1,248

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

-50

0

50

100

150

200

250

2010 2011 2012 2013 2014 2015 2016

1. The Company defines EBITDA as earnings before interest, taxes and non cash charges/ (income). EBITDA should not be considered by an investor as

an alternative to net income or cash flow as determined in accordance with IFRS – EBITDA figures reflect adjusted EBITDA, please see the Company’s

Management’s Discussion and Analysis.

Mandalay Acquisition Timeline

2009

• Costerfield, Australia

• Gold & Antimony

2010

• Cerro Bayo, Chile

• Silver & Gold

2014

• Challacollo, Chile

• Silver & Gold

2014

• Björkdal, Sweden

• Gold

• No acquisition

• Optimize operations

• Pay down debt

• Exchange warrants

• Begin dividends

2011-2013

Revenue EBITDA Cash from Operations Gold Price

Mandalay Financial Performance 2010-2016

Results: Consistent Performance Across the Price CycleU

S$ M

M

Go

ld P

rice (

US

$)

6

Based on Matched Production and Reserves Growth

With Continuing Capital and Overhead Spending Discipline

15,854 63,351

107,941 126,908

154,810 166,679

114,000-128,000254,000

520,000 633,000

772,000

1,123,000

1,054,000 1,024,000

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

0

50,000

100,000

150,000

200,000

250,000

300,000

2010 2011 2012 2013 2014 2015 2016 2017E

Oz A

u E

q.

Ye

ar-

En

d R

es

erv

es

Oz A

u E

q.

An

nu

al

Pro

du

cti

on

145,497

12.8

24.9

35.9 34.4

40.3 39.5

29.5

810

392333

271 260237 203

- 100

200

300

400

500

600

700

800

900

2010 2011 2012 2013 2014 2015 2016-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

CapexspendingperozAuEq.$/oz

Capexspending($m)

Mandalaycapitalspendingatoperatingmines(excludingexploration)

3.6 3.4

5.3 5.1

6.7

4.44.8

224

54 49 40 4426 33

-

50

100

150

200

250

2010 2011 2012 2013 2014 2015 2016- 1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

OverheadspendingperAuEq.$/oz

Overheadspending($m)

Mandalaycorporateoverheadspending

Acquisition

7

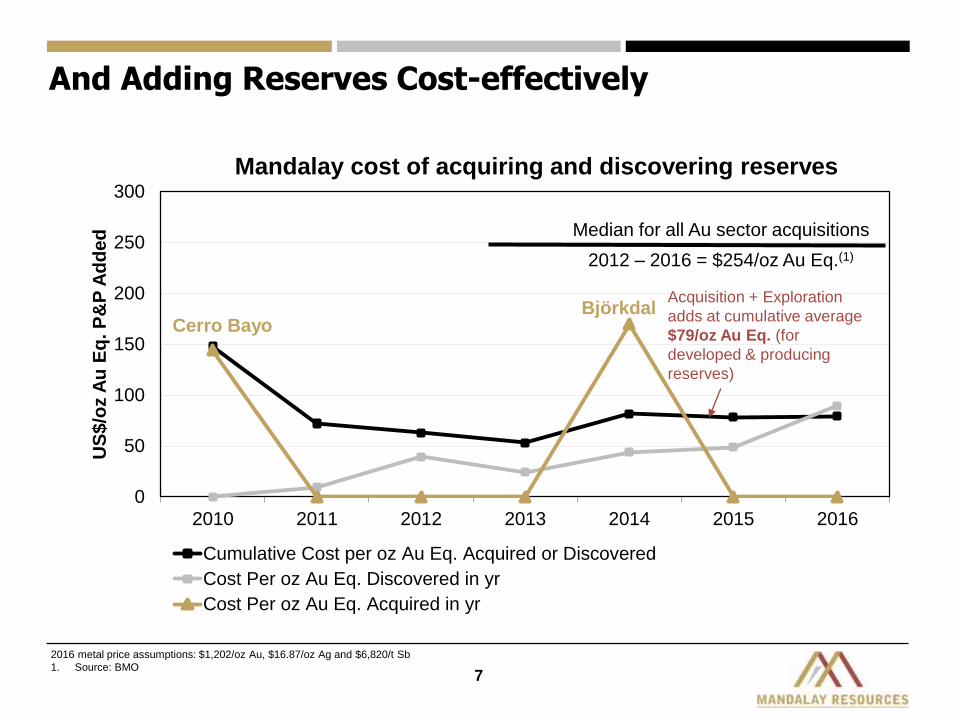

0

50

100

150

200

250

300

2010 2011 2012 2013 2014 2015 2016

US

$/o

z A

u E

q. P

&P

Ad

de

d

Mandalay cost of acquiring and discovering reserves

Cumulative Cost per oz Au Eq. Acquired or Discovered

Cost Per oz Au Eq. Discovered in yr

Cost Per oz Au Eq. Acquired in yr

And Adding Reserves Cost-effectively

2016 metal price assumptions: $1,202/oz Au, $16.87/oz Ag and $6,820/t Sb

1. Source: BMO

Acquisition + Exploration

adds at cumulative average

$79/oz Au Eq. (for

developed & producing

reserves)

Cerro BayoBjörkdal

Median for all Au sector acquisitions

2012 – 2016 = $254/oz Au Eq.(1)

8

Creating and Delivering Value for Shareholders

$0

$2,000,000

$4,000,000

$6,000,000

$8,000,000

$10,000,000

$12,000,000

$14,000,000

Dividends Paid (USD)*

6% of revenues (dividend contribution)

A $10,000 investment on Sept. 24, 2009

would be worth on Sept. 19, 2017(1-4):

• Mandalay: $23,373

• Peer Index: $12,894

• Gold Seniors: $7,645

Record

Dividends

Since 2009, Mandalay has returned cash to

shareholders via:

• Warrant redemptions

• Share buybacks

• Dividends

(1) Adjusted for reinvested dividends. Assumes investment in Mandalay made as part of private placement announced on 24-Sep-09 to fund acquisition of Costerfield and accounts for

warrant exchange offer of 0.47 shares per warrant. (2) Peer Index: Alacer, Argonaut, Dundee PM, Kirkland Lake, Klondex, Perseus, Primero, Richmont. (3) Gold Seniors: Agnico Eagle,

AngloGold, Barrick, Goldcorp, Gold Fields, Kinross, Newcrest, Newmont, Polyus, Randgold. (4) End date as at Sept 19, 2017.

*Annual cash dividend paid quarterly, based on 6% of the Company’s trailing quarter’s gross revenue and the future cash requirements of the Company

0.0

5.0

10.0

15.0

20.0

25.0

$0

$20,000

$40,000

$60,000

$80,000

$100,000

Sep-09 Sep-10 Sep-11 Sep-12 Sep-13 Sep-14 Sep-15 Sep-16

Volu

me (

mill

ions)

Invest

ment

Valu

e

Mandalay(1) Peer Index(2) Gold Senior(3)

Total Return vs. Peers and Seniors through Sept. 19, 2017

Dividend

Suspended

9

Major Shareholders(1)

Holders Shares (Million) Shares (Percentage)

GMT Capital 72.6

Ruffer LLP 56.5

CI Investments 46.1

AzValor 31.8

Plinian + Management + Directors 30.5

Large Holders (Top-5) 237.5

Other Holders 213.8

TOTAL 451.3

16.1%

12.5%10.2%

7.0%

6.8%

47.4%

Broader Ownership and Higher Liquidity Over Time

Analyst Coverage

Firm Analyst

BMO Brian Quast

Raymond James Chris Thompson

Scotia Trevor Turnbull

Volume

30-day Average Daily Volume 859,264

100-day Average Daily Volume 1,076,243

Average Daily Volume across all trading platforms (as of September 19, 2017)

1. Known ownership positions are estimates - as at September 18, 2017 - Ownerships and percentages rounded to one decimal place.

1. Exercise Price: C$0.60 – C$1.13 expiry dates ranging from Mar 18, 2018 – Jun 30, 20242. Market Capitalization converted to US$ using exchange rate of 1 CAD = 0.79 USD (Nov. 8, 2017)

3. Cash and Cash Equivalents and Interest-Bearing Debt as at end of Q3-2017 (Sept 30, 2017)

10

Strong Balance Sheet as of Sept 30, 2017

Millions

(Except Share Price Info)

Share price (Nov. 8, 2017 - close) (C$) $0.315/shr

Shares Outstanding 451.3

Stock Options(1) 21.1

RSUs 0.7

Fully Diluted Shares Outstanding 473.1

Market Capitalization (C$) $142.2

Cash and Cash Equivalents (US$)(3) $24.8

Total Interest-Bearing Debt (US$)(3) $39.6

Total Enterprise Value (US$)(2,3) $126.5

Mandalay secured US$40 million revolving credit facility July 25, 2017

US$25 million undrawn

Mandalay is well-capitalized to fund its capital plans and acquisitions

11

Björkdal Gold Mine: Investment Thesis Demonstrated

Land package 12,949 hectares

Ownership 100%

P&P Reserves(1) 10,600,000 t @ 1.68 g/t Au for 574 koz

2016 Production 48,143 oz Au

Key for 2017:

Grade control working properly and debottlenecking mine

operations has increased rate of delivery of high-grade ore

Phase 1 of low-grade ore sorting program (crushing and screening)

implemented with 50% grade upgrade; design and detailed

engineering for Phase 2 complete

Flotation expansion project completed on time and on budget,

performing as planned (1.7% recovery increase)

Continued exploration success

(1) Source: Roscoe Postle Associates, Effective September 30, 2016, documented in an independent NI 43-101 Technical Report filed Jan. 27, 2017

12

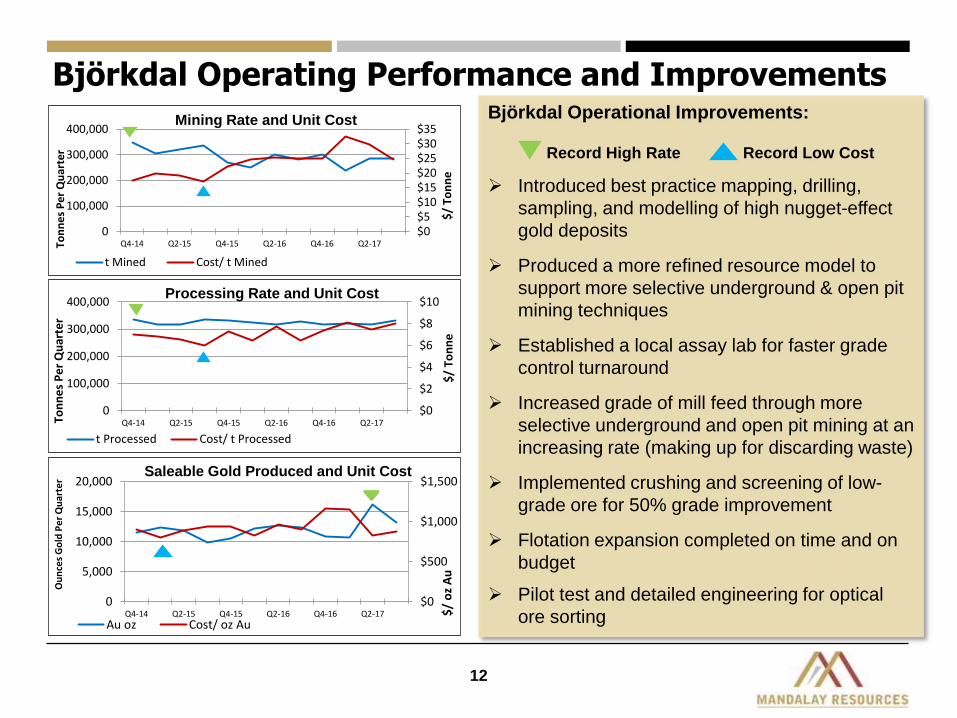

Björkdal Operating Performance and Improvements

$0$5$10$15$20$25$30$35

0

100,000

200,000

300,000

400,000

Q4-14 Q2-15 Q4-15 Q2-16 Q4-16 Q2-17

$/

Ton

ne

Ton

ne

s P

er Q

ua

rter

Mining Rate and Unit Cost

t Mined Cost/ t Mined

$0

$2

$4

$6

$8

$10

0

100,000

200,000

300,000

400,000

Q4-14 Q2-15 Q4-15 Q2-16 Q4-16 Q2-17

$/

Ton

ne

Ton

ne

s P

er

Qu

arte

r

Processing Rate and Unit Cost

t Processed Cost/ t Processed

Björkdal Operational Improvements:

Record High Rate Record Low Cost

Introduced best practice mapping, drilling,

sampling, and modelling of high nugget-effect

gold deposits

Produced a more refined resource model to

support more selective underground & open pit

mining techniques

Established a local assay lab for faster grade

control turnaround

Increased grade of mill feed through more

selective underground and open pit mining at an

increasing rate (making up for discarding waste)

Implemented crushing and screening of low-

grade ore for 50% grade improvement

Flotation expansion completed on time and on

budget

Pilot test and detailed engineering for optical

ore sorting$0

$500

$1,000

$1,500

0

5,000

10,000

15,000

20,000

Q4-14 Q2-15 Q4-15 Q2-16 Q4-16 Q2-17 $/

oz

Au

Ou

nce

s G

old

Pe

r Q

uar

ter

Saleable Gold Produced and Unit Cost

Au oz Cost/ oz Au

13

Björkdal Debottlenecking: Lifted Mill OutputConsistently-delivered higher-grade ore results in demonstrated higher production

0

0.5

1

1.5

2

2.5

3

3.5

-

5,000

10,000

15,000

20,000

25,000

30,000

g/t

Au

Pro

ce

sse

d

To

nn

es p

roce

sse

d

Björkdal plant throughput – tonnes and grade

Throughput - tonnes Throughput - grade

Consistent tonnes processed each week

75

80

85

90

95

100

-

500

1,000

1,500

2,000

2,500

Au

re

co

ve

ry %

Sa

lea

ble

Au

oz

pro

du

ce

d

Björkdal processing output and recovery – saleable ounces

Throughput - Saleable ounces Throughput - Recovery

(Before commissioning of flotation expansion in early July)

Output - Saleable ounces Au

14

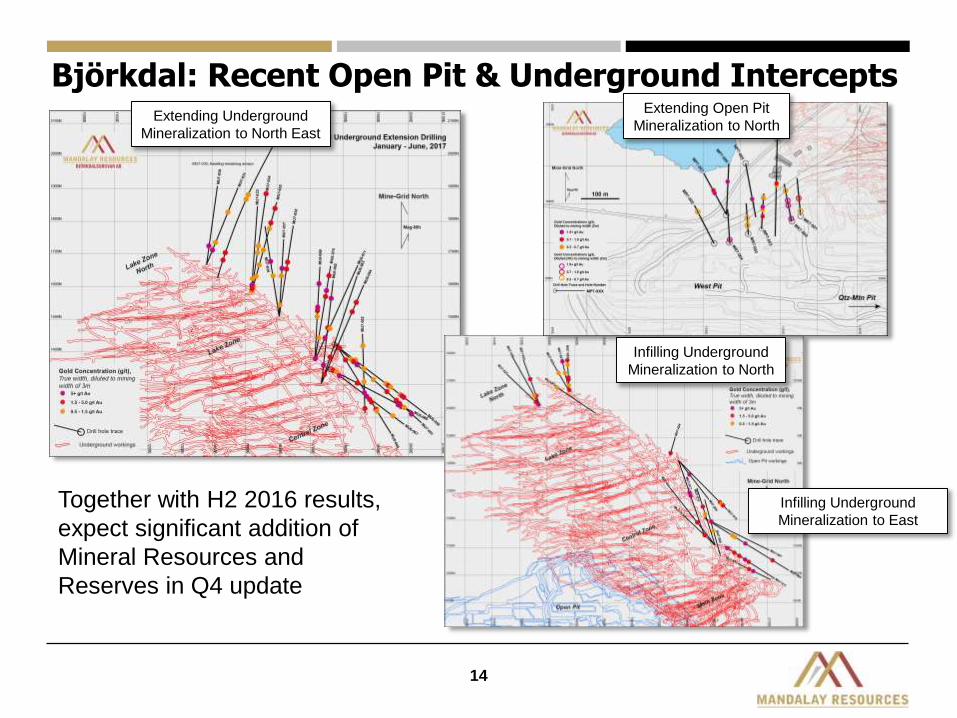

Björkdal: Recent Open Pit & Underground Intercepts Extending Open Pit

Mineralization to NorthExtending Underground

Mineralization to North East

Infilling Underground

Mineralization to East

Infilling Underground

Mineralization to North

Together with H2 2016 results,

expect significant addition of

Mineral Resources and

Reserves in Q4 update

15

Emerging High-Grade Skarn Intercepts at Björkdal

Continuous

volumes of skarn

Smaller shoots of

high-grade within

skarn

A few ‘000 tonnes

of high-grade

skarn mined and

processed in Q2

with both high

reconciled grades

and good recovery

16

Costerfield Gold-Antimony Mine:Turnaround Complete; Dependable Performance

Land package 1,293 hectares

Ownership 100%

P&P Reserves(1) 619,000 t @ 6.5 g/t Au; 2.8% Sb

2016 Production 41,310 oz Au, 3,598 t Sb

Key for 2017:

May 2017 – Completed the capital development to access near-mine

shoots and support next few years of production

July 2017 – Completed tailings lift construction for current LOM tailings

September 2017 – Positive initial results of low-cost aquifer injection test

End 2017 – Expected end of year 2017 Mineral Reserve increases at

Brunswick and further exploration upside (expected release Feb. 2018)

(1) Source: SRK Consulting (Australia), Effective December 31, 2016, documented in an independent NI 43-101 Technical Report filed March 31, 2017

17

Costerfield Operational Improvements:

Record High Rate Record Low Cost

Improved mine output/mill throughput from

170 tpd to 450 tpd (capped by grid power

and site grinding capacity)

Changed mining method from cut-and-fill to

blast-hole stoping with cemented rock fill

(greater production, lower unit costs)

Increased sub-level spacing from 5 to 10 m

Introduced contract capital development for

faster and lower cost results

Replaced mechanized mining fleet

Introduced mobile crusher to decrease

particle size of mill feed (better recoveries,

higher throughput)

Grew mine life from zero reserves to roughly

4 years while mining continuously for 7

years – discovered Cuffley and N-lode

Costerfield: Continuous Improvement

$0

$100

$200

$300

$400

0

20,000

40,000

60,000

Q4-09(Dec. only)

Q4-10 Q4-11 Q4-12 Q4-13 Q4-14 Q4-15 Q4-16

USD

/ To

nn

e

Ton

nes

Pe

r Q

uar

ter

Mining Rate and Unit Cost

t Mined Cost/ t Mined

$0

$50

$100

$150

0

20,000

40,000

60,000

Q4-09(Dec.only)

Q4-10 Q4-11 Q4-12 Q4-13 Q4-14 Q4-15 Q4-16

USD

/ To

nn

e

Ton

ne

s P

er

Qu

arte

r

Processing Rate and Unit Cost

t Processed Cost/ t Processed

$0

$1,000

$2,000

$3,000

0

5,000

10,000

15,000

20,000

Q4-09(Dec. only)

Q4-10 Q4-11 Q4-12 Q4-13 Q4-14 Q4-15 Q4-16

USD

/ O

z A

u E

q.

Ou

nce

s P

er

Qu

arte

r

Au Equivalent Production and Unit Cost

Oz Au Eq. Cost/ Au Eq. Oz

18

Brunswick Resource Enlarged by Recent Drilling

Ready for Mineral

Resource and Reserve

estimation in Q3/Q4

19

Emerging Costerfield Deeps High-Grade Shoot

Emerging mineralized shoot

below historic workings

Very high-grade gold

• 60 to >100 g/t Au

At least:

• 400 m on strike

• 100 m vertical

Open

20

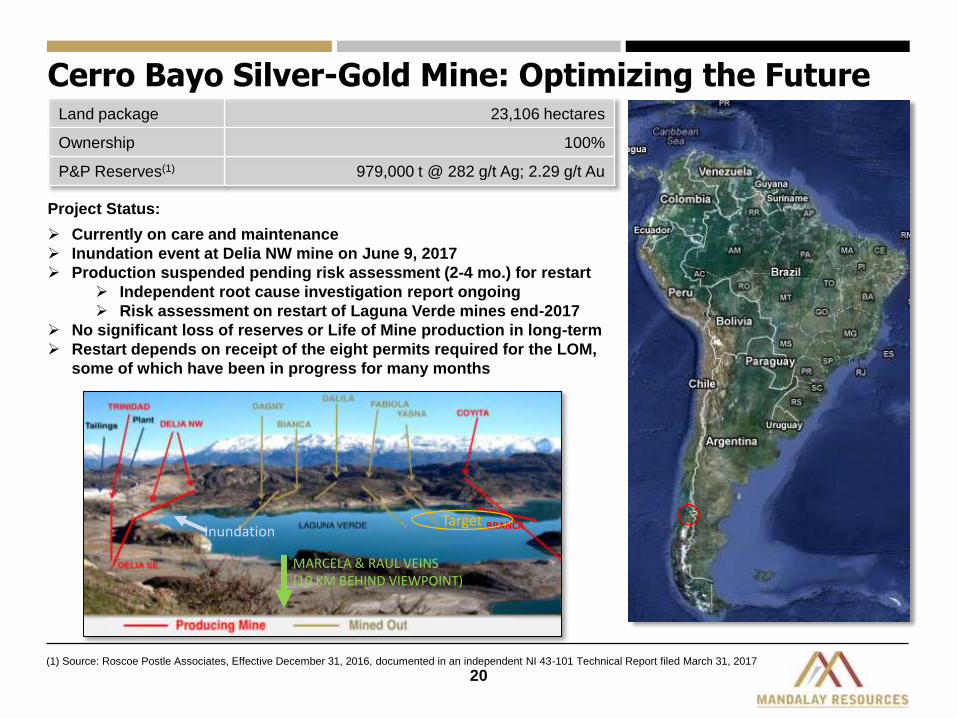

Cerro Bayo Silver-Gold Mine: Optimizing the FutureLand package 23,106 hectares

Ownership 100%

P&P Reserves(1) 979,000 t @ 282 g/t Ag; 2.29 g/t Au

Project Status:

Currently on care and maintenance

Inundation event at Delia NW mine on June 9, 2017

Production suspended pending risk assessment (2-4 mo.) for restart

Independent root cause investigation report ongoing

Risk assessment on restart of Laguna Verde mines end-2017

No significant loss of reserves or Life of Mine production in long-term

Restart depends on receipt of the eight permits required for the LOM,

some of which have been in progress for many months

(1) Source: Roscoe Postle Associates, Effective December 31, 2016, documented in an independent NI 43-101 Technical Report filed March 31, 2017

BRANCATarget

MARCELA & RAUL VEINS (10 KM BEHIND VIEWPOINT)

Inundation

21

Cerro Bayo Operational Improvements:

Shifted the mining method from

shrinkage stoping to completely

mechanized blast hole open stoping;

Ramped up throughput from 0 tpd –

1,400 tpd from three mines

Installed flotation automation system to

maximize silver and gold recoveries

Extended mine life from 3 years at

1,200 tpd to 4 years at 1,400 tpd while

mining continuously for 6 years

Production suspended pending risk

assessment (2-4 mo.) and subsequent

permitting for restart. Mine on care and

maintenance

Record High Rate Record Low Cost

Cerro Bayo Operating Performance

$0

$50

$100

0

50,000

100,000

150,000

Q4-10 Q2-11 Q4-11 Q2-12 Q4-12 Q2-13 Q4-13 Q2-14 Q4-14 Q2-15 Q4-15 Q2-16 Q4-16 Q2-17

$/

Ton

ne

Ton

ne

s P

er Q

ua

rter

Mining Rate and Unit Cost

t Mined Cost/ t Mined

$0

$50

0

50,000

100,000

150,000

Q4-10 Q2-11 Q4-11 Q2-12 Q4-12 Q2-13 Q4-13 Q2-14 Q4-14 Q2-15 Q4-15 Q2-16 Q4-16 Q2-17

$/

Ton

ne

Ton

ne

s P

er

Qu

arte

r

Processing Rate and Unit Cost

t Processed Cost/ t Processed

$0

$5

$10

$15

$20

0

500,000

1,000,000

1,500,000

Q4-10 Q2-11 Q4-11 Q2-12 Q4-12 Q2-13 Q4-13 Q2-14 Q4-14 Q2-15 Q4-15 Q2-16 Q4-16 Q2-17

$/

oz

Ag

Ne

t B

ypro

du

ct

Oz

Ag/

Qu

arte

r

Saleable Silver Produced & Unit Cost

Ag oz Cost/ oz Ag net Au

22

Challacollo Silver-Gold Project 2017

Key for 2017:

May 2017 – Water sufficient to support eventual operation discovered

Permitting for production well in process

Option to optimize project for lower CAPEX

Land package 20,378 hectares

Ownership 100%

Location 130 km SE of Iquique, Chile

Indicated Resource 4.7 MM t @ 200 g/t Ag for 30 MM oz Ag

Elevation Approx. 1,500 ASL

23

Invest With Us: How We Will Deploy Your Capital1. Acquire new assets counter-cyclically – at discount to value

• Acquire only when we see possibility of an immediately accretive transaction with strong value

uplift in 3-5 years

• Keep portfolio evergreen – exit assets that do not fit

2. Execute focused operational improvement projects at each site

3. Apply relentless, disciplined financial management

• Restart Cerro Bayo with optimized, risk-assessed plan• Maintain good Björkdal performance; further upside includes complete commissioning of flotation

expansion; add optical sorting; extend mine life with exploration

• Extend Costerfield life with Brunswick lode if prudent and beyond with further exploration

• Optimize Challacollo feasibility with lower capital and operating costs

• Mining – projects focused on safer, more mechanised mining with higher extraction, lower dilution

and reduced cost

• Metallurgical – projects focused on higher recovery, higher availability, higher quality products with

higher payables and reduced costs

• Commercial – more diverse customers paying better terms

• Low cash cost and overheads for high EBITDA margins

• Low DD&A for high P&L margins – low acquisition cost, focused CAPEX & exploration

• Prudent, low-cost leverage to fund growth when needed

• Minimize shareholder dilution

• Compare all potential uses of cash to the benefits of returning cash to shareholders

4. Engage all stakeholders in a values-based and value-focused organization

TSX:MND

For more information, please contact:

Greg DiTomaso

Director, Investor Relations

Tel: 647.260.1566

Email: [email protected]

Company Website: www.mandalayresources.com

Twitter: @MandalayAuAg