Embed Size (px)

DESCRIPTION

CEC 2010 Annual Report

Citation preview

1

COPPERBELT ENERGY CORPORATION PLC

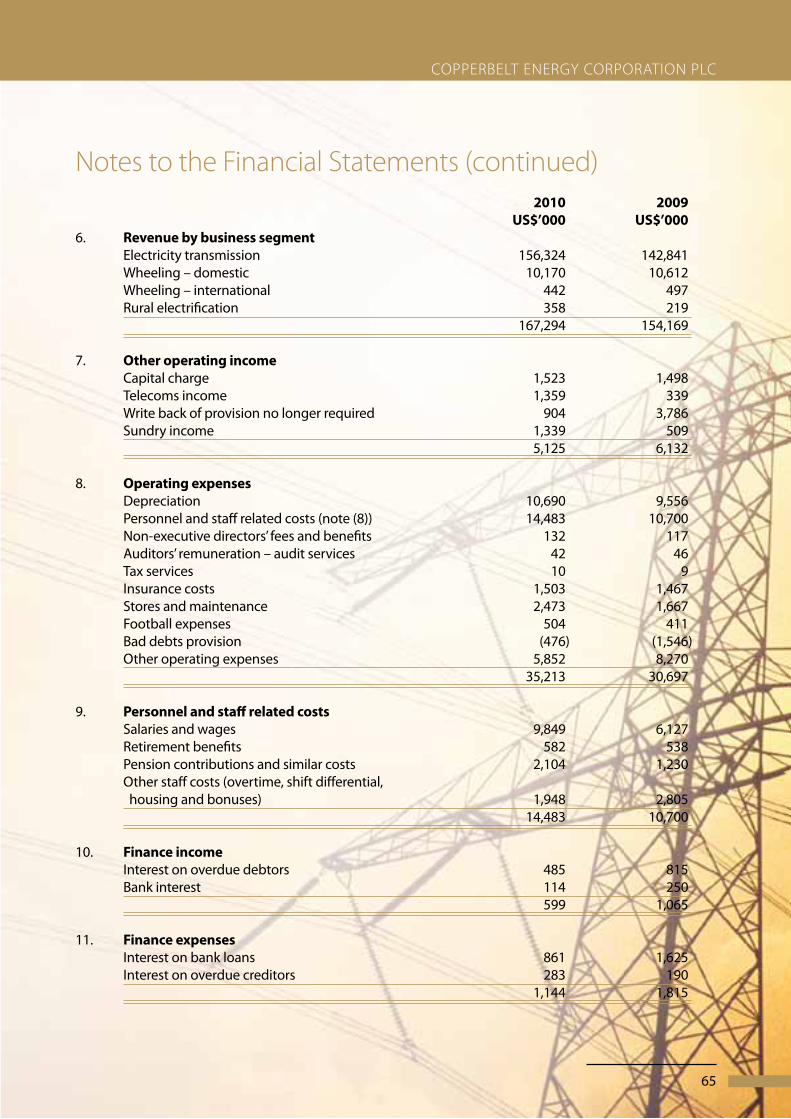

Copperbelt Energy Corporation Plc

Annual Report 2010

Copperbelt Energy Corporation Plc

Annual Report 2010

4

COPPERBELT ENERGY CORPORATION PLC

Miss

ion

Visio

nVa

lues

We are committed to: Supply reliable energy and high quality services to meet our customers’ unique and changing needs efficiently and proactively through robust infrastructure, diverse power sources and professional teams Increase value for our shareholders through responsible and transparent corporate conduct, innovation and investing prudently

To be the leading Zambian investor, developer and operator of energy infrastructure in Africa by providing innovative solutions and building strategic partnerships through committed professional teams

Being honest in all our dealings Supporting each other Building good team relationships Being open to new ideas Developing a ‘can do’ attitude

5

COPPERBELT ENERGY CORPORATION PLC

The Copperbelt Energy Corporation Plc (CEC) is the outcome of an evolutionary process that commenced more than 60 years ago – when the Rhodesia-Congo Border Company (CEC’s founding predecessor) was founded, with a mandate to provide power solutions to mining companies.

Majority owned by Zambian Energy Corporation (Zam-En), CEC has a deep insight into the mining industry, which enables it to provide quality electricity and other power products and services to the majority of the mines in Zambia.

In 2007, CEC extended its mandate beyond Zambia, and has since been providing a transmission service to a mining operation in the Democratic Republic of Congo.

In November 2009, CEC became a full member of the Southern African Power Pool and is, therefore, well placed to serve mines throughout Southern Africa. CEC is fast positioning itself as a developer of energy infrastructure in Africa and is well respected in the region for its skills in designing and operating transmission systems.

Listed on the Lusaka Stock Exchange since January 2008, CEC is a licensed carrier of

telecommunications traffic using broadband optic fibre and is now a competitive retail sector player in telecommunications through a joint venture with Realtime Zambia.

The Company owns and operates around 900 kilometres of 220kV and 66kV transmission lines, 520 kilometres of optic fibre on power lines, and 250km in trenches, 38 major substations and 80MW of gas turbine generation. CEC accounts for about 50% of power consumed in Zambia.

To ensure high quality of supply, the network has a number of reliability enhancing features that include a high degree of network redundancy, stand-by generation, a well-equipped control centre and multiple sourcing points.

CEC seeks to be a strategic partner in private power projects or public-private partnership power projects within the region and is focused on opportunities that create value for the Company and its investors.

To achieve that, we continue to build appropriate partnerships that provide us with the necessary support to pursue and participate in viable new business opportunities.

Corporate Profile

6

COPPERBELT ENERGY CORPORATION PLC

7

COPPERBELT ENERGY CORPORATION PLC

Chairman’s Statement 8

Report of the Managing Director - Operations 14

Report of the Managing Director – Corporate Development 20

Corporate Responsibility Report 29

Operational / Financial Highlights 32

Directors' Report 34

Statement on Corporate Governance 41

Statement Of Directors’ Responsibilities 44

Report of the Independent Auditors to the members of Copperbelt Energy Corporation Plc 45

Statement of Comprehensive Income 48

Statement of Changes In Equity 49

Statement of Financial Position 50

Statement of Cash flows 51

Notes to the Financial Statement 52

Corporate Governance Compliance Status 81

Directors 82

Corporate Contact Information 83

Bankers and Auditors 84

Contents

8

COPPERBELT ENERGY CORPORATION PLC COPPERBELT ENERGY CORPORATION PLC

Chairman’s StatementThe year 2010, whose results I am pleased to report, was eventful for the Copperbelt Energy Corporation Plc (CEC). Commendable progress was made on various fronts, building on the efforts of previous years. The period ended 31st December 2010 recorded increased turnover of 9% over the previous period, earnings per share were up by 7%, and average load sales volume rose 8% over the comparable period.

These results have been achieved, in large part, because CEC has been able to attract and retain highly skilled and motivated professional staff. The drive to recruit graduate talent, which the Company embarked on a few years back, is clearly bearing fruit as the crop of graduate professionals taken on from

Hanson Sindowe

9

COPPERBELT ENERGY CORPORATION PLC

about 2009 has gained considerable experience and with it, added responsibilities in line with the intention of the programme as well as the larger vision of the Company.

A deliberate decision was also taken to strengthen the availability, in the Company, of relevant skills capable of handling and delivering results with regard to the Company’s new business development.

This is an area that is becoming increasingly pivotal in respect of the future of CEC; hence it demands that professional staff with relevant skills and expertise in business development are available to drive this area of the business.

With such capabilities, we can be assured that the Company possesses the necessary skills and expertise to ably and successfully grow into its envisaged future.

Safety, Health and Environment (SHE)

During the year, the Company continued its pursuit of achieving SHE Excellence with emphasis on SHE Cultural Change, again, being the top most SHE driver.

Our focus in 2010 was twofold – cascading SHE training to all employees, following on the SHE training for Directors and Managers conducted in 2008; and operationalizing the SHE aspects of the business by improving our proactive and reactive SHE measures, continuing with the Managers’ SHE visibility tours and implementing the Tool Box Safety Talk – a system aimed at proactive incident prevention and used chiefly to demonstrate the involvement of frontline supervisors by ensuring that it (the Tool Box Safety Talk) was firmly embedded in the performance targets of all frontline supervisors.

Further, all the issues raised through the SHE Cultural Survey report are being addressed, and improving SHE communication internally is well in progress.

The pursuit of excellence entails an awareness of the challenges along the journey. Hence, it is a concern to the Company that statistics for road traffic incidents and accidents (RTIs/RTAs) were, in 2010, higher than the previous year. These are levels not desirable for the attainment of excellence in SHE across the business and measures, specifically a vehicle monitoring system to improve performance in this area, has been introduced as a positive reinforcement.

The one blot on an otherwise remarkable record was the unfortunate occurrence at Maposa substation in December, where an employee sustained burns due to non-compliance with system operations and safety procedures. Notwithstanding this, the Company’s SHE performance in 2010 was commendable; recording a laudable 1.3 million man-hours without a lost time accident (LTA) between August 2009 and December 2010.

Interventions in HIV and AIDS through provision of antiretroviral treatment, and malaria continued throughout 2010 with satisfactory results. To enhance our efforts in rolling back malaria, the Company purchased a fogging machine as an added measure to indoor residual spraying of homes and provision of subsidized insecticide treated bed nets to increase the effectiveness of the programme.

Business Environment & Performance Highlights

It was most encouraging to see growth returning across economic sectors, particularly mining, in 2010. Confidence within our mining customers continued to be buoyed by the prevailing high commodity prices, translating in increased production.

CEC posted positive results for the 2010 reporting period, during which capacity sales went up 8% on 2009, to an average of 470MW

10

COPPERBELT ENERGY CORPORATION PLC

from an average of 436MW. This positive shift is attributable to the resumption of operations at one of the mines placed under care and maintenance during the downturn, a return to full production and expansion projects by some of our customers, underpinned by the international copper price rally that continued throughout the year. Investments in new mining operations and the expansion of existing ones could be seen during 2010, and evidenced by our signing of a power supply agreement with Konnoco Zambia Limited, for redevelopment of the Konkola North Copper Mine by Brazil’s Vale and Africa Rainbow Minerals of South Africa. The operation will take up to 100MW when fully implemented in the next four to six years. The mine is, however, expected to start drawing down up to 40MW of power as early as 2012.

A connection agreement for the implementation of the Muliashi Mine project in Luanshya was, during the year, signed with owners CNMC Luanshya Copper Mine (CLM). Project implementation activities have since begun. Muliashi will add 30MW to the current power requirements of CLM over three years. I am glad to report that CEC and CLM have also executed a new power supply agreement (PSA), through which CEC will continue to supply all of CLM’s

existing and new (Muliashi) power requirements.

Technical proposals were submitted to Mopani Copper Mines Plc to provide a connection to the proposed Synclinorium project, which involves the construction of a new shaft in Kitwe. The Synclinorium project has a projected total demand of 27MW once fully operational.

Konkola Copper Mines Plc also progressed its Chingola Refractory Ore (CRO) project. Additional capacity will be required in order to meet the power requirements of all these projects, once completed.

The projected load growth and the economic growth witnessed across a number of sectors, again, brings to the fore the need for new generation and of tariffs moving to cost-reflectivity. Hence, on the request of ZESCO Ltd, we commenced negotiations to review the bulk power supply tariffs. Consequently, we initiated parallel negotiations of the PSA tariffs with our customers. The current tariffs were last substantively reviewed in 2008, for a three year period.

Considerable progress has been made with regard to the Kabompo Gorge Hydroelectric

11

COPPERBELT ENERGY CORPORATION PLC

project. The final feasibility study report was completed in early 2010 while the Environmental Impact Assessment report has been submitted to the Environment Council of Zambia for comments and approval. The project is expected to reach financial closure by the end of 2011.

Other developments of note during 2010 include the Government’s granting of authority to CEC to carry out feasibility studies of the hydro potential on the Luapula River sites. The Government of the Democratic Republic of Congo (DRC) has equally given support to the initiative.

Progress was made in respect of the construction of a new double circuit 220kV interconnector between Zambia and the DRC, whose construction is ongoing. The project is being undertaken jointly with the DRC’s national electric utility, SNEL.

The Company has established a unit to evaluate and develop renewable energy technologies. There is strong growth in such technologies world wide, and it is our view that Zambia is well placed to benefit from these technologies. By employing such proven technologies, CEC hopes to reduce its costs, particularly with regard to diesel. Initial successes include the commissioning of a bio-

diesel plant in Kitwe, and the securing of funding for feasibility studies in generation from bio-mass associated with working plantations on the Copperbelt.

The Company has invested further into optical fibre in metropolitan areas, and has secured a strong customer base with many of the country’s major institutions making use of the fibre to improve connectivity between different business sites, and to connect to the internet. There are plans to increase investment in this sector during 2011.

Stakeholder Relations

Two interim dividends, totaling US$10 million [K48.19 per share], were paid out to eligible shareholders of the company during the year, underscoring the Company’s desire to create value for our shareholders.

In a year that markets, the world over, were still trying to find their pre-2008 buoyancy, the CEC stock performed very well, posting increases month-on-month throughout the year, and closing the year at K615 per share (2009: K430) – the first time since the post-listing high of K1,200

12

COPPERBELT ENERGY CORPORATION PLC

per share that the stock has sustained such a consistently firm performance. The latter part of the year was especially positive, as the market’s appetite for the CEC stock increased. The 2010 closing price was 43% up on the 2009 close.

The Investor Relations function of the business strives at all times to improve the quality of communication between the Company and its shareholders. Automated procedures for issuing correspondence to our shareholders were developed in 2010, and the Company continued to capture more accurate records of shareholder details.

Corporate Responsibility

In 2010, the major part of our donation budget went to help young people through education sector assistance and sport, particularly the Power Dynamos Football Club, in so far as the latter was concerned.

The refurbishment of the Arthur Davies Stadium was completed at a cost US$860,000 and the stadium re-opened in July 2010.

The fitness centre and gymnasium for staff and the public that I reported on last year was, during the year, completed at a cost of US$478,000 and opened to public use.

The process of handing over the houses that were constructed for the relocated households in Chililabombwe was completed. A total of US$575,000 was spent on constructing better houses and relocating the eight affected households.

The Company is supporting the improvement of higher education through a partnership with the School of Engineering at the University of Zambia (UNZA), whereby a senior manager from CEC has been seconded to the school for two years on a full time basis to construct new high voltage laboratories and assist in curriculum development. Similar support is planned for the Copperbelt University.

Recognition

During the period under review, CEC added to its trophy cabinet – marking another year of local and international accolades for exceptional performance in different spheres of the business.

CEC picked up the Infrastructure Investment Award – 2010 Developer of the Year given by Africa Investor; the Investor Relations Award 2010 for the Best Online Annual Report in Africa conferred by World Finance and was once again recognised by the Zambia Revenue Authority for being exceptionally tax compliant.

Deserved recognition goes to everyone that contributed to the Company making these achievements.

Board Appointments & Operation

During the year, Helen Tarnoy, who served as Deputy Chairperson of the board resigned from the board while Peter Mumba, who represented the Zambian Government through the Ministry of Energy and Water Development, also left the board.

The board is grateful to both Helen and Peter for the enriching service they rendered throughout the period they served as members of the CEC Board of Directors.

Consequently, Jean Madzongwe has assumed the position of Deputy Chairperson of the CEC Board of Directors, while FMO and Aldwych International are now represented on the board by Robert Chestnutt. Teddy Kasonso now serves on the board as the representative of the Zambian Government.

On behalf of the board, I welcome Jean into her new role and extend a warm welcome to Robert and Teddy to the CEC Board of Directors. We look forward to benefitting from their vast experience.At the Annual General Meeting of the members of the Company, held on 26th March 2010, three

13

COPPERBELT ENERGY CORPORATION PLC

non-executive Directors (Munakupya Hantuba, Emmanuel Mutati and Jonathan Muke) retired from the board and were re-appointed to serve on the CEC Board of Directors.

The three members served the board diligently throughout the year and the Company has benefited much from their level and depth of knowledge and experience.

In November 2010, a board committee to undertake the task of reviewing the Company’s new business development projects was established. The Business Development Committee comprises 6 members – two Executive Directors, three Non-Executive Directors and an ex-officio.

Our board conducted itself in accordance with all relevant set and voluntary codes of corporate governance and standards relevant to the operations of the Company.

Business Outlook

We have a positive outlook for 2011, backed by the developments taking place on the mining landscape not only in Zambia but across the region and the impressive rally of the global metal prices, particularly copper and cobalt. We believe that the new investments made by our customers in more efficient operations have made Zambia a more competitive copper producer, which should ensure that the country is in a better position to withstand future reductions in the copper price.

With the supply and demand balance for energy within the Southern African Power Pool (SAPP) still being tight, and expected to remain so for the next few years, there is an ever present need to not only bring on stream new generation, but also to address transmission constraints so as to facilitate increased power trading within the SAPP. The long lead time to developing new generation plants is of concern, which may result in power shortages in the next few years, whilst the regional economies continue to grow without

adequate commissioned power generation infrastructure.

CEC is on the look out for projects in the region that make prudent investment sense and create value for our shareholders. We are already actively considering a number of projects, which the Company has been invited to invest in by various developers.

Closer to home, the new projects and expansions being undertaken by our existing and potential customers will demand a considerable level of additional capacity, which should be matched by a robust network capable of effectively and innovatively serving our customers’ needs for reliability and quality of supply.

The Company’s sustainability and continued growth is of paramount importance, hence, our strategy is that of continued investment in projects that provide an avenue for the business to diversify from its traditional supply of electricity to the mines on the Copperbelt, without compromising in any way the level and quality of service that the Company is known for. Developing the Company’s generation and transmission portfolio is of particular interest to the Company and I am pleased to report that steady progress is being made with respect to identifying viable projects in this new aspect of the business.

Conclusion

We are positive about the business going into 2011 and of the prospects already in the pipeline. We remain confident of the value that the projects being pursued will bring to the business and have a solid team, in all the Directors and staff, to deliver this value.

Hanson Sindowe

COPPERBELT ENERGY CORPORATION PLCNeil F. Croucher

15

COPPERBELT ENERGY CORPORATION PLC

Report of the Managing Director - Operations

Safety, Health and Environment

Safety, health and environment (SHE) remains CEC’s number one priority. The main areas of focus for the year in achieving SHE excellence were improving the SHE culture in the workplace through provision of SHE training to all employees, with emphasis being on the roles and responsibilities of employees in achieving a SHE cultural change. The second area of focus was aimed at operationalising SHE in the business by improving the SHE statistics and implementing Tool Box safety talks.

Owing to improved training, work procedures and emphasis on accountability, CEC achieved a reduction in lost time accidents from four (4) in 2009 to 1 in 2010; after going 1.3 million man hours without a lost time accident. There was also a reduction in system breaches and permit withdrawals. Notwithstanding these achievements, CEC’s safety record is not yet where we want it be. The topmost challenge was the escalating road traffic incidents (RTIs) and road traffic accidents (RTAs). CEC recorded 10 RTAs in 2010 compared to 7 in 2009, and 33 RTIs compared to 27 the previous year. One measure introduced to address this is the GEOTAB satellite vehicle monitoring system, which it is hoped, will help the company monitor vehicle usage.

CEC continued to implement its HIV and AIDS programme introduced in 2002. During the year, the company sustained its provision of free anti-retroviral medication, training of peer educators and counsellors and supporting community

based programmes. The roll back malaria programme was also carried out and it continues to yield positive results.

The company maintained its good performance in the various environmental management aspects that it monitors. CEC complied with all statutory requirements for licence renewal and reporting. Full compliance was also achieved for statutory emission limit for the emergency power plant.

Business overview

The performance of the Zambian economy in 2010 showed marked improvements over the previous two years. The growth was driven by, among other factors, the increased copper prices on the world market and with it, increased copper production. It is expected that this growth will continue to be driven by the plethora of mining projects that are coming on stream. Production levels for the key commodities of copper and cobalt should continue to steadily increase especially as the smelters and mines, which cut back or ceased operations in the wake of the global financial crisis, recommence and move to full production.

As a result, CEC’s mining customers, who consume much of the power produced in Zambia, resumed some of their expansion projects that were shelved during the period of the global financial and economic meltdown. Slow but steady increases in power demand were registered during 2010, compared to the

16

COPPERBELT ENERGY CORPORATION PLC

year before. Power availability in the country during the year generally improved, although a major power outage occurred in June 2010. Investment in the power sector remains critical as power availability will emerge as one of the key constraints for future growth and development in Zambia in the long term.

During the year, CEC continued to concentrate on achieving its mission and in doing this, focussed on responding to the unique needs of its customers, achieving excellence in its operational metrics, engaging constructively with policy makers and regulators, demonstrating environmental stewardship, adhering to safety standards and staying connected to its community.

Power Purchase and Sales

Power purchases and sales continue to be underpinned by the Bulk Supply Agreement (BSA) between CEC and ZESCO Ltd (ZESCO) and the various Power Supply Agreements (PSAs) between CEC and its customers. Power purchased from ZESCO accounted for 99.98% of CEC’s total requirements, with the balance being supplied from CEC’s gas turbine alternators (GTAs). ZESCO’s performance in respect of its role of supplying

bulk power was satisfactory throughout 2010, with only one blackout incident recorded on 18 June 2010, which affected the whole country. Apart from the high voltage experienced at system start up, management of the incident greatly improved in comparison to similar cases in the past. Subsequently, a combined team of engineers from CEC and ZESCO was formed to seek short and long term solutions to the problems that arise when there is a major disturbance affecting the Zambian power network. The team commenced its work during the year and many of its recommendations have been implemented. It was, therefore, most pleasing to note that when, on 26th August 2010, there was a major system disturbance in a neighbouring country’s power grid, which resulted in Zambia becoming separated from the Southern Power Pool (SAPP) grid, the Zambian system remained intact. Such incidents have previously resulted in the Zambian system being blacked out but, on this occasion, automated systems restored the supply/demand balance and quick operator responses reduced the extreme over-voltages within minutes; thereby resulting in a very minor impact on Zambian consumers.On the power sales front, energy consumption by CEC customers increased by 9% from 3,338 GWh in 2009 to 3,640 GWh during the year under

17

COPPERBELT ENERGY CORPORATION PLC

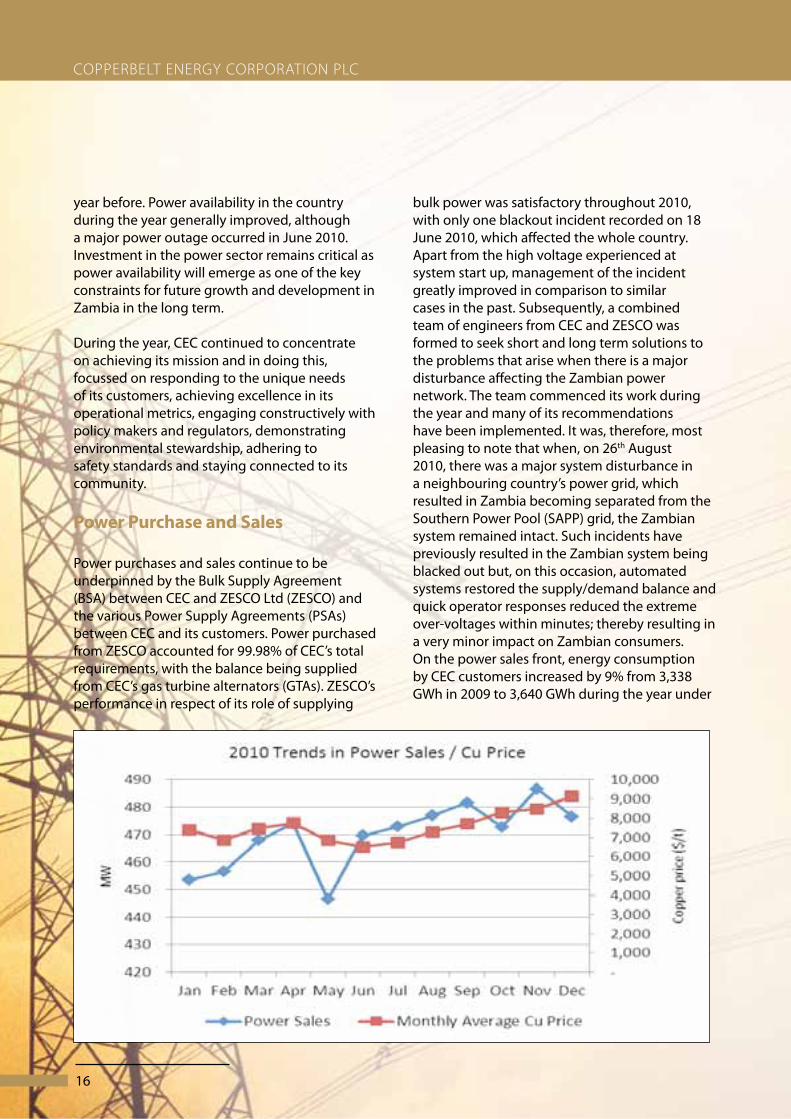

review. This recovery and ramp up in demand was also represented in increased capacity sales which rose by 8% from 436MW in 2009 to 470MW in 2010. A peak demand of 487MW was achieved in November 2010. The system load factor registered a 6% increase to 86%. The capacity sales performance was undoubtedly driven by the copper price improvements of about 24% throughout the year as shown in the graph below.

However, the noticeable dips in two months of the year were due to shut downs undertaken by some customers to overhaul equipment. Non-recovery of the total capacity sales to pre-economic downturn times of 520MW was mainly due to continued closure of the Chambishi Metal’s Cosak smelter, designed to produce cobalt, which has remained under care and maintenance to-date.

Wheeling for domestic and international customers continued to form an integral part of CEC’s business. Domestic wheeling, which involves transmission of power through the CEC system on behalf of ZESCO, was sustained at normal business levels throughout the year. Wheeled domestic energy was 1,660GWh compared to 1,611GWh the previous year. International wheeling, on the other hand, declined due to the expiration of power purchase agreements between the power utilities in the region on whose behalf CEC wheeled the power.

The entire fleet of six emergency Gas Turbine Alternators (GTAs) was available throughout the year. GTA reliability improved to 92% from 90% in 2009. The improvement was partly due to the replacement of auxiliary equipment and major refurbishment works on the GTA plant where frequent failures were previously experienced. However, plant availability was down at 97% compared to 98% the previous year. This was attributed to a two week outage of the Maclaren GTA on which exhaust rehabilitation works were being carried out. Further, the GTAs were operated to provide emergency power to CEC’s customers during the national power outage, which occurred in June and, glad to report, they

performed according to expectation.

System Maintenance

System capacity continued to be firm. However, system capacity constraints which include diminishing transformer capacity as a result of load growth, inadequate reactive power support and line capacity, have been identified as a cause for concern and a strategy developed to address them. As part of the strategy, higher capacity transformers were procured and installed where existing units were running out of capacity. Power factor correction capacitor banks were installed at major switching stations to improve capacity and aid voltage regulation. In addition, customers were encouraged to undertake similar installations downstream.

The system maintenance strategies that have been implemented over recent years continued to be employed during the year. Condition based maintenance, defect maintenance and system primary equipment testing continued as scheduled. Condition monitoring activities included transformer oil sampling, diagnostic SFRA tests and routine thermographic inspections. The company remains alert to the fact that there is need to invest in more test equipment especially for testing transformers which are aged and require stringent condition monitoring.

Significant progress was made on the power factor correction project. Some final works remain to be carried out before the equipment can be powered up. As reported last year, this project once completed, will greatly contribute towards stabilising the voltages on the Copperbelt.

Tariff review

Some of the Power Supply Agreements (PSAs) that CEC has with its customers are nearing the end of their term. Specifically, PSAs with four customers will expire in 2012. Therefore, during the year CEC undertook negotiations with two of these customers, with a view

18

COPPERBELT ENERGY CORPORATION PLC

to, among other things, extend the terms of these PSAs. This culminated in the signing of necessary amendments extending the PSAs for further periods of 10 and 15 years respectively. Negotiations with the other two customers will commence in quarter one of 2011.

At the request of ZESCO, a process to renegotiate the tariffs at which CEC purchases power commenced. CEC also commenced a parallel tariff renegotiation process with its customers. The two processes will run concurrently with the expectation that finality will be achieved in the coming year. The review of tariffs was last implemented in 2008. In addition, CEC has proposed to adjust tariffs at which it provides domestic wheeling to ZESCO.

During the year, CEC commissioned a Cost of Service study, which is expected to identify the cost elements involved in the Company’s provision of services to each customer. A South African based consultancy firm, NETGroup Solutions SA (Pty) Limited, has been engaged to carry out this study. This process is important as it will help CEC understand the cost of serving each of its customers and by extension, its ability to continue operating as a commercially sustainable

entity for the foreseeable future. The results from the study are expected during the first half of 2011.

Southern African Power Pool (SAPP) Membership

Following its admission to full membership of the SAPP in November 2009, CEC enhanced its participation in SAPP activities during the year. Some of the primary ongoing activities by SAPP include setting up of the day ahead market (DAM), revision of the operating guidelines, and monitoring of various transmission and generation projects that will help bridge the demand/supply gap in the region. In all these, CEC lent its support to the processes aimed at transforming the SAPP into a reliable competitive market.

Core business expansion

In line with our mission to meet customers’ unique demands, CEC has set out to diligently work with its customers to ensure that power requirements of their planned expansion projects

19

COPPERBELT ENERGY CORPORATION PLC

are adequately addressed. This is supported by CEC’s understanding that, as the copper prices recover, its customers’ confidence in progressing some of their expansion projects will grow. Therefore, notable progress was made during the year with targeted projects reaching advanced stages.

One key achievement was the signing of a power supply agreement of an initial term of 25 years, with a new mining customer on the Copperbelt, known as Konnoco Zambia Limited. Konnoco, which is redeveloping the Konkola North Mine located in Chililabombwe, is owned on an equal share basis by Africa Rainbow Minerals of South Africa and Vale of Brazil. This mine is expected to draw down 40MW from 2012 but has the potential to increase to 100 MW if all phases of the project are developed.

Significant progress was made on the Muliashi project, which is being undertaken by CNMC Luanshya Copper Mine (CLM) and is expected to take up to 30MW once fully operational. A connection agreement, through which the Muliashi project will be implemented, has been signed and project implementation activities have commenced. Completion is set to take place by the end of 2011. Furthermore, during the year, CEC and CLM executed a new PSA that will see CEC continue to supply all CLM power requirements, including additional power requirements as a result of the Muliashi Project. This new PSA will run up to 2024.

Network extensions associated with the planned development of a new mine shaft by Mopani Copper Mines (MCM) at Nkana in Kitwe was another project that achieved closure on technical aspects, with financial closure expected in 2011. This project, the Synclinorium project, has a projected total demand of 27MW. Its

location is in close proximity to the existing CEC infrastructure, and, as a result, minimal capital expenditure will be required to make power available to the project.

Various other projects were at early development stages by the end of the year.

Customer relations

CEC continued to engage its customers throughout the year through regular communication. This interaction yielded positive results.

Employee Relations

As always, CEC ensured that cordial employee relations were maintained throughout the organisation. A mentoring program was introduced in the company, whereby experienced members of staff were attached to new employees in a bid to share their expertise, professional knowledge and render support. The programme has worked well so far and it is the intention of the company to continue with it.

A skills-mapping exercise was conducted among all employees to assess training needs in the company. The results showed that the company has a sound skills base with generally well trained staff. However, CEC will continue to provide training where gaps exist and to ensure that the staff have the right skills to meet the ever changing technological and business environment.

Neil F. Croucher

COPPERBELT ENERGY CORPORATION PLCMichael J. Tarney

21

COPPERBELT ENERGY CORPORATION PLC

Financial Report for the Year Ended 31st December 2010

Statement of Comprehensive Income

Revenue arises primarily from the sale of power to the Company’s mining customers, and the provision of domestic and international wheeling services. Revenue increased by 8.5% to US$167.3m, mainly due a 7.8% increase in maximum demand from the Company’s mining customers (470MW in 2010 vs. 436MW in 2009), and tariff indexation in line with the US PPI index.

Cost of sales, which mainly comprises power purchased from ZESCO Limited [ZESCO] under the Bulk Supply Agreement increased by 8.5% to US$121.4m arising mainly from an increase in purchased power from ZESCO of 6% (438MW in 2010 vs. 413MW in 2009) and indexation of the ZESCO tariff to the Company in line with the US PPI index.

Gross profit increased by 8.3% to US$45.9m from US$42.4m in 2009, in line with the increase in sales to the Company’s mining customers described above.

Other operating income decreased by 16% to US$5.1m from US$6.1m the previous year. An explanation of the change is given below:

• Incomefromtelecommunications,mainlyarising from the sale of capacity on the

Report of the Managing Director – Corporate Development

Company’s national optical fibre network grew by a factor of 300% to US$1.4m from US$0.3m the previous year;

• Thecapitalcharge,comprisingpaymentsfrom Chambishi Metals PLC towards the capital cost of the substation at Chambishi remained constant at US$1.5m;

• Writebackofprovisionsnolongerrequired decreased by 76% to US$0.9m from US$3.8m the previous year. These items are by nature variable, and arise from risk sharing agreements with the Company’s customers whereby the Company’s level of contribution to the capital cost of substations constructed to supply new mining operations is linked to the quantity of additional power purchased by mining customers;

• Sundryincomeincreasedby163%toUS$1.3m from US$0.5m the previous year, and includes income derived from providing professional services to customers, such as the design, procurement and construction of new transmission assets.

Operating expenses increased by 14.7% to US$35.2m from US$30.7m the previous year. An explanation of the change is given below:

• Depreciationoffixedassetsincreasedby 14% to US$10.7m from US$9.6m the previous year;

• InsurancecostsremainedconstantatUS$1.5m. Insurance policies in place

22

COPPERBELT ENERGY CORPORATION PLC

cover the Company for property damage to primary and secondary equipment, public and employee liability, directors’ and officers’ insurance, and insurance for motor vehicles and moveable plant;

• Personnelandstaffrelatedcostsincreased by 35.5% to US$14.5m from US$10.7m the previous year. The factors that led to this increase included:

o a reduction in the amount of labour capitalised on projects of US$0.8m following the completion of the Northern Area transmission project;

o the effect of a stronger Kwacha during 2010 (average rate 4,797) compared to the previous year (average rate 5,047) which increased salary costs when converted into US Dollars. The majority of the Company’s employees are paid in Kwacha;

o an annual average pay increment to employees paid in Kwacha of 12% and enhancement of the salaries of certain grades of employees to reflect increased levels of skills and responsibilities; and

o the Company complies with IAS 19 in the preparation of its financial statements, and provides in full for deferred employee benefits. Personnel and staff related costs include a charge arising from an increase of US$1.1m in deferred employee benefits from US$2.8m at 31st December 2009 to US$3.9m at 31st December 2010. The provision is calculated by an independent actuary. A significant contributing factor to the increase in provision was a reduction in the discount rate applied by the actuary, which is linked to improved macro-economic stability in Zambia.

• Storesandmaintenancecostsincreasedby 47% to US$2.5m from US$1.7m the previous year. The increase was significant as certain activities had been curtailed during the first half of 2009 to conserve working capital, due to the low copper prices at that time;

• FootballexpensesincreasedbyUS$0.1mto US$0.5m. The Arthur Davis Stadium in Kitwe was refurbished and re-commissioned during the year;

• Otheroperatingexpensesreducedby30% to US$5.8m from US$8.3m the previous year. A reduction in legal costs in 2010 contributed significantly to the reduction, as well as the capitalization of development costs of the Kabompo Gorge Hydro Project during 2010 (US$1.4m included within fixed assets additions), whereas development costs in 2009 of US$1.4m had been expensed. The difference in treatment of costs arose due to the confirmation of the results of the feasibility study in 2010 that the project is considered to be technically and economically feasible.

Results from operating activities reduced by 11% from US$17.8m to US$15.8m with the increase in gross margin offset by an increase in operating expenses and a reduction in other operating income.

Finance income reduced by 44% to US$0.6m from US$1.1m the previous year. The reduction was attributable to an improvement in the timeliness of payments from the Company’s customers, as interest is charged only when payments are made after the due date under the relevant power supply agreement.

Finance expense reduced by 39% to US$1.1m from US$1.8m the previous year, mainly due to a reduction in the LIBOR rate applicable to the Company’s debt facilities, and a reduction in the quantum of outstanding loans compared to the previous year.

23

COPPERBELT ENERGY CORPORATION PLC

Profit before tax decreased by 11% from USUS$17.1m to USUS$15.2m.

Income tax expense (before tax on other comprehensive income) was US$5.0m compared to US$6.0m the previous year. The effective rate of tax on profit was 32.7% compared to a rate of 35.1% the previous year. The difference was mainly due to the effect of unrealised exchange differences in the tax computation arising from year on year movements in the exchange rate.

Other comprehensive income arising from gains on cash flow hedges was US$3.8m compared to US$1.3m the previous year. Both gains arose from the hedging policy of the Company, through which a more competitive rate than the prevalent spot rate for the conversion of dollars into Kwacha has been obtained.

Total comprehensive income increased by 7% to US$12.7m from US$11.9m the previous year.

Earnings per share increased by 7% to 1.27 US Cents per share from 1.19 US Cents per share the previous year.

Statement of Changes in Equity

Retained earnings increased by 8% to US$48.6m at 31st December 2010 compared to US$44.9m at the previous year end.

The adjustments to retained earnings were (i) retained profit of US$12.7m for the year (addition), (ii) dividends totaling US$10.0m declared and paid during the year (reduction) and (iii) depreciation added back to retained earnings of US$0.9m (addition) being the depreciation charged on the revalued portion of fixed assets in the statement of comprehensive income.

Total equity increased by 2% to US$161.0m from US$158.3m at the previous year end. Included in equity is the revaluation reserve, which reduced by US$0.9m to US$112.2m at 31st December 2010 from US$113.1m at the previous year end.

Statement of Financial Position

The net book value of fixed assets was US$239.3m at 31st December 2010 compared to US$236.2m at the previous year end. Total fixed asset additions were US$13.8m including:

• US$0.7mofbuildings;• US$4.0mofprimaryequipmentonthe

Company’s transmission network;• US$3.2mofsecondaryequipmentonthe

Company’s transmission network;• US$1.3mofgeneralequipmentand

fixtures;• US$0.6mofmotorvehicles;• US$3.8massetsincreaseincapitalworkin

progress, total US$9.6m at 31st December 2010. These include assets that are in the process of being commissioned, and include an amount of US$1.4m relating to the Kabompo Gorge Hydro project.

The depreciation charge was US$10.7m.

Total current assets were US$36.3m at 31st December 2010, a reduction of 1% compared to total current assets of US$36.5m at the previous year end.

Stock was largely unchanged from the previous year end at US$3.5m, the largest component of stock being liquid fuel held in stock for the Company’s fleet of gas turbine alternators and the Company’s vehicle fleet.

Trade and other receivables were US$24.1m at 31st December 2010, a 22% reduction to the previous year end total of $US30.7m. Within this balance, trade debts owed mainly by CEC’s mining customers reduced by 30% to US$16.9m as the customer payment record improved. An amount of US$2.7m over due from the Congolese utility SNEL has been provided for within trade receivables (provision at 31st December 2009 was US$3.2m). The Company has entered into an arrangement to fully recover this amount from SNEL in future as an off-set against a power trading transaction.

24

COPPERBELT ENERGY CORPORATION PLC

Cash and cash equivalents increased to US$8.8m compared to US$2.3m at the previous year end.

Total assets increased by 1% to US$277.6m at 31st December 2010 compared to US$274.7m at the previous year end.

Current liabilities increased by 25% to US$43.5m compared to US$34.8m at the previous year end. Key movements were:

• Tradeandotherpayablesincreasedby40% to US$34.5m from US$24.6m at the previous year end;

• AnamountofUS$1.4mpayabletoZambian Energy Corporation (Ireland) Limited, the Company’s largest shareholder, was re-paid during the year;

• TaxpayableincreasedtoUS$1.8mfromUS$1.7m the previous year.

Non-current liabilities decreased by 10% to US$73.1m compared to US$81.6m at the previous year end. Key movements were:

• Reductionininterestbearingloansby22% to US$24.9m at 31st December 2010 arising from debt repayments during the year;

• Reductioninnon-currenttradeandother payables by 16% to US$11.2m. The residual amount relates to an amount payable to First Quantum for the substation connecting Frontier mine;

• Anincreaseof40%indeferredemployeebenefits to US$3.9m in line with the actuarial valuation;

• AreductioninthedeferredtaxbalancetoUS$33.1m from US$33.4m the previous year.

Total loans outstanding at 31st December 2010 had decreased by 18% to US$32.1m compared to US$39.3m at the previous year end, thereby reducing the level of gearing of the Company. An amount of US$6.0m was repaid on the Company’s main loan facility with Citibank and DEG, and an

amount of US$1.2m was repaid to DBSA during the year. A further amount of $7.2m is scheduled to be re-paid on these facilities during 2011, although it is also anticipated that the Company will acquire new financing facilities during the year (see below).

Total equity and liabilities increased by 1% to US$277.6m at 31st December 2010 compared to US$274.7m at the previous year end.

The CEC Board approved the Company entering into a new three year amortising loan agreement with Citibank for US$10m in November 2010, for which a term sheet was signed on 1st December 2010. The loan is expected to become effective during the first quarter of 2011.

Statement of Cash Flows

Cash inflows before working capital changes increased by 6% to US$30.3m compared to US$28.6m for the previous year. The improvement was due to the increasing underlying profitability of the Company.

Net cash inflows on operating activities increased by 213% to US$36.4m compared to US$11.7m for the previous year. This movement demonstrates an improvement in the working capital of the Company, with debtor days decreasing. The tax payment was higher in 2009 at US$8.1m compared to US$6.5m in 2010 arising from the settlement of outstanding tax returns with Zambia Revenue Authority during 2009.

Net cash outflows from investing activities increased by 58% to US$13.1m from US$8.3m the previous year, mainly due to the increased investment in fixed assets undertaken by the Company at US$13.8m for the year compared to US$7.3m for the previous year.

Net cash outflows from financing activities increased to US$17.2m from US$17.0m during the year. The dividend paid during the year remained constant at US$10.0m.

25

COPPERBELT ENERGY CORPORATION PLC

There was a net increase in cash and cash equivalents of US$6.2m compared to a net decrease in cash and cash equivalents of US$13.6m during the previous year. Cash and cash equivalents were US$8.8m at 31st December 2010, compared to US$2.3m at 31st December 2009.

Share Price Performance on the Lusaka Stock Exchange

The share price, as at 31st December 2010, was K615 per share, compared to K430 per share at the previous year end, an increase of 43%. In comparison, the Lusaka Stock Exchange (LuSE) all share index recorded an increase of 19% in Zambian Kwacha terms and 15% in U.S. Dollar terms.

The dividend yield expressed in Kwacha as a percentage of the year end share price was 8%.

The Company was awarded an international prize for the quality of its on-line financial reporting during the year by the London based organization World Finance.

Development Activities

The main development activities undertaken by the Company during the year are summarized below.

Energy Sector – Key Trends

The need for increased investment in the energy sector is being widely supported by all Governments in the Southern African Development Community (SADC), as it is widely known that power utilities in the region do not possess sufficient generation and transmission capacity to meet the needs of their growing economies.

This has prompted regulators to approve increased tariffs, such that the tariff paid by consumers is considered to be cost reflective. In

practice, this means that the tariff will need to be sufficient to meet the marginal cost of new transmission and generation projects when they are commissioned, and regulatory systems will need to evolve to ensure that independent power producers are treated fairly and transparently along side the host national utilities.

There are abundant untapped energy resources in Southern Africa, with Zambia well placed to develop new hydro, thermal (coal) and renewable projects.

The Directors of the Company believe that the Company has a role to play in investing in new generation and transmission capacity, and some of the projects under development are listed below.

Second Zambia – DRC Interconnector Project

This project comprises the construction of a new dual circuit 220kV interconnector between the two countries that will enable the transmission of 550MW power between the two countries on a firm basis.

Works on the project in Zambia are currently being co-ordinated with the contractors on the (Democratic Republic of Congo) DRC side.

Kabompo Gorge Hydro Project

The final feasibility study for the project was issued by the consultant, Amanzi (a consortium of Arcus Gibb, Knight Piesold and SSI) in June 2010. The report indicates that the project is feasible, provided that geological and hydrological risk can be adequately addressed, and tariffs can migrate to cost reflective levels.

The proposed output of the power station is 40MW of capacity and 166GWh of energy per annum, and the project design specifies a roller compacted concrete dam that is 47.5m high and 123m long, a reservoir with an area of 3,485

26

COPPERBELT ENERGY CORPORATION PLC

hectares, an underground chamber for the power house, and 4km of tunneling. A transmission line will be constructed to connect to the national grid at Lumwana.

Consequently, the following additional activities were undertaken during the year:

(i) Submission of draft Implementation Agreement to the Office for Promoting Private Power Investment for further discussion.

(ii) Completion of the draft Environmental and Social Impact Assessment that was submitted to the Environmental Council of Zambia in December 2010.

(iii) Signature of Memoranda of Understanding with the Chiefs in the affected areas of North Western Province through which the Company has agreed to respect high standards of corporate social responsibility.

(iv) Request for Expressions of Interest from potential contractors through advertisement in the international media. Seventeen responses were received, from which a shortlist of five companies has been selected, who will be invited to submit a full bid. Final bids are expected

to be received during the third quarter of 2011.

(v) Appointment of financial and tax advisors.

(vi) Design of a new township at the project site. It is expected that significant further progress will be made in developing the project during 2011, with the selection of an Engineering, Procurement and Construction (EPC) contractor and project lenders, further development of project documentation and site preparation activities.

Hydro Projects on the Luapula River

The Company submitted a request to the Public Private Partnership (PPP Unit) of the Ministry of Finance and National Planning, under the provisions of the Public-Private Partnership Act No. 14 of 2009, to undertake feasibility studies on hydro sites on the Luapula River, as well as a transmission line connecting the Copperbelt Province to Luapula Province through the ‘Pedicle’ region of the DRC. The Government granted the Company the authority to undertake the studies; and work on the studies on the river schemes has commenced. The Company also obtained the written support of the Government of the DRC,

27

COPPERBELT ENERGY CORPORATION PLC

as the Luapula River defines the border between Zambia and the DRC, and the transmission line would traverse the Katanga region through the Pedicle. The long term intention is to develop these schemes under a public-private partnership arrangement where the power that is generated is made available for use in both Zambia and the DRC.

The work to be undertaken during 2011 relates to an assessment of the environmental and social, hydrological and topographical aspects of the whole river catchment area to ensure that the overall design and sequencing of the different potential schemes along the river is optimised. The details of the various studies to be undertaken are currently under discussion with the Governments of Zambia and the DRC.

Nansanga Farm Block

The Company responded to an invitation for expression of interest by the PPP Unit of the Ministry of Finance and National Planning to develop the power distribution network for the proposed Nansanga Farm Block. Following review of the Company’s expression of interest, the PPP unit pre-qualified the Company. This means that the Company will be eligible to submit a formal bid once the Request for

Proposals is issued out. This is likely to be done after the determination of the likely initial farming investment in the bloc, following invitations by the Zambia Development Agency.

CEC Renewables

A unit in the Company has been created to focus on the development of renewable energy projects. The initial scope of the unit has been to identify pilot projects in the areas of bio-fuels, and bio-mass and solar electricity generation that may lead to viable business units in future. Key developments during the year included:

(1) Commissioning of a bio-diesel plant in Kitwe

A plant capable of refining up to 1,000,000 litres of bio-diesel from jatropha oil has been commissioned in Kitwe. An agreement to purchase oil has been entered into with the Kapiri Mposhi Jatropha Growers’ Association, starting at a level of 200,000 litres per annum. The bio-diesel will be applied for use in the Company’s own vehicle fleet and generating plant in the first instance.

28

COPPERBELT ENERGY CORPORATION PLC

(2) Securing grant funding to evaluate options for the development of energy from bio-mass

The unit has been successful in securing grant funding with the Copperbelt Forestry Company to evaluate technologies for the conversion of wood waste into energy. There is much surplus bio-mass available on the Copperbelt, which currently is not used. The same technology solution may also be applied at the Kabompo Gorge hydro project in North-Western Province, as some woodland will require to be cleared in the area where the reservoir will be formed.

Telecommunications

The Company consolidated its investments in optical fibre infrastructure by purchasing the underground fibre in Lusaka and other commercial centres owned by Realtime in the final quarter of 2010. The total fibre network owned and operated by CEC now comprises 520km of fibre within the Copperbelt on power lines, and a further 250km of buried fibre throughout the country, mainly in the commercial centres. The network is currently being extended to cover new towns, including Livingstone, Kabwe and Solwezi.

The main customer base for the fibre is the banks, mining companies, mobile service providers and internet service providers that operate in Zambia. There is strong demand for fibre from these and other sectors, and the business is expected to grow steadily for the foreseeable future. Telecommunications is, by nature, a highly competitive and fast moving industry, and CEC’s objective is to operate effectively in the provision of fibre network services where it has a competitive advantage and is able to offer services to other entities with licenses issued by the regulatory authority, Zambia Information and Communications Technology Authority (ZICTA).

Realtime, which is operated as a joint venture under which CEC has a 50% interest, provides

direct services to customers. The main focus of Realtime is sales and customer service for corporate clients. The Realtime business operates in a manner that is complementary to CEC’s network fibre business.

Other Projects

The Company is investigating other opportunities to invest in the energy sector, both in Zambia and in other African countries.

The Company was awarded an international prize during the year for its development activities. The ‘Developer of the Year’ prize was given by African Investor.

The CEC Board has considered the possibility of establishing a special purpose vehicle to attract additional funding for development projects, so that the CEC balance sheet funding capacity is preserved in the interests of business prudence.

MICHAEL J TARNEY

29

COPPERBELT ENERGY CORPORATION PLC

Protecting our fellow human beings and the environment, and investing in communities around and beyond where we operate are at the core of the Company’s values to ensure our business and people are a positive influence on the community and the world through responsible behaviours, operations and service offerings.

Guided by our Corporate Social Responsibility policy, CEC pursues an integrated approach to corporate responsibility, ensuring consistency with the interests of our stakeholders.

CEC has traditionally supported education, health and young people. These form the Company’s core areas for social support and over the years, considerable resources have been invested in these key social development areas.

The major recipients and beneficiaries of CEC’s social investment have been children and young people. Orphans and vulnerable children are supported, for example, through construction of school infrastructure and provision of learning and teaching materials; improvement of the environment and facilities for children in, especially, public health institutions like the Kitwe Central Hospital.

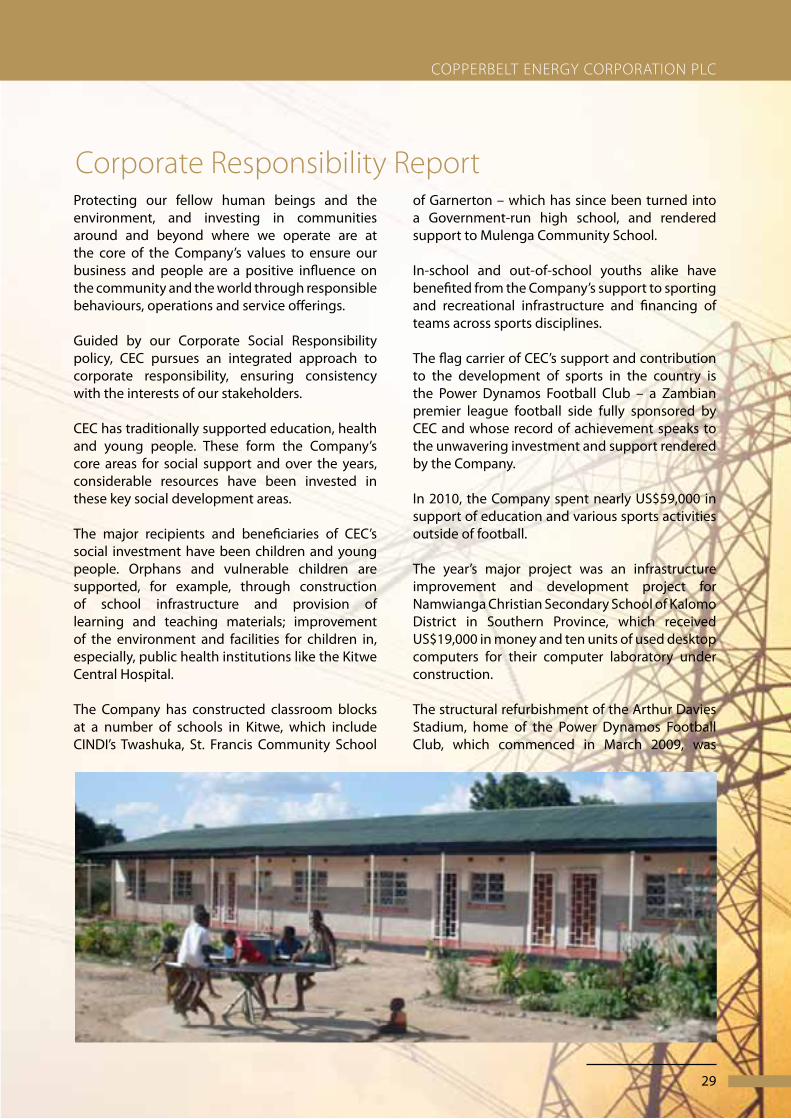

The Company has constructed classroom blocks at a number of schools in Kitwe, which include CINDI’s Twashuka, St. Francis Community School

of Garnerton – which has since been turned into a Government-run high school, and rendered support to Mulenga Community School.

In-school and out-of-school youths alike have benefited from the Company’s support to sporting and recreational infrastructure and financing of teams across sports disciplines.

The flag carrier of CEC’s support and contribution to the development of sports in the country is the Power Dynamos Football Club – a Zambian premier league football side fully sponsored by CEC and whose record of achievement speaks to the unwavering investment and support rendered by the Company.

In 2010, the Company spent nearly US$59,000 in support of education and various sports activities outside of football.

The year’s major project was an infrastructure improvement and development project for Namwianga Christian Secondary School of Kalomo District in Southern Province, which received US$19,000 in money and ten units of used desktop computers for their computer laboratory under construction.

The structural refurbishment of the Arthur Davies Stadium, home of the Power Dynamos Football Club, which commenced in March 2009, was

Corporate Responsibility Report

30

COPPERBELT ENERGY CORPORATION PLC

completed in July 2010 with a total investment of US$860,000. Nearly US$504,000 was spent on the team itself in 2010 to cover their operational expenses.

CEC has entered into a Memorandum of Understanding with the two major institutions of higher education in Zambia – the University of Zambia (‘UNZA’) and Copperbelt University (‘CBU’) – to support capacity building in the areas of power systems engineering, electronics and telecommunications.

The Company refurbished the lecture theatres at UNZA in 2009, provided modern furniture and installed electronic projection equipment that can be linked to the network servers in the institution. This has been of great assistance to lecturers and students alike, as lectures can now be delivered using the advantages of modern technology.

CEC has seconded a senior manager to UNZA and CBU on a full time basis, for two years, to assist in designing new laboratories, and developing project curricula that are fit for purpose in today’s rapidly evolving industrial environment.

Furthermore, the Managing Director – Corporate Development has been chosen to Chair the Zambian section of the Education Partnership for Africa (EPA), a broad based initiative through which a partnership has been created between the University of Manchester in the United Kingdom, UNZA and CBU to enhance all aspects of curriculum development, staff and student training in key areas of engineering competence.

Another focus of the EPA programme is fund raising, through which large corporates are invited to provide financial support for capacity building at the institutions, and to offer tailored project work in industry during the final year of degree courses.

In addition to seconding a senior person to the universities, CEC has made provision to support the construction of a high voltage laboratory during 2011. As CEC intends to recruit students from both UNZA and CBU in future, the initiative will have the added benefit of ensuring that new recruits have the necessary training to be considered for recruitment to the Company’s graduate training programme.

31

COPPERBELT ENERGY CORPORATION PLC

In its planning for the future construction of the Kabompo Gorge Hydro Project, the Company has taken the local community to heart. The project will bring development to an area that currently lacks many essential amenities, such as access to electricity and the provision of health care.

The creation of sustainable economic activity in the area will enable the establishment of a new town, which will enable both the Government and non-government institutions to develop institutional support for the local community.

The Company has also committed to opening a representative office in Mwinilunga, the local District centre, through which communication with the local community will be co-ordinated.

Memoranda of understanding have been signed with the local chiefs, ensuring that all developments will be undertaken in consultation with the local community, through a defined process.

The plans for the local community include the design of a new small town to house those working at the power station, which will provide for:Improvements to the access road;

Construction of a clinic;Construction of a school;Construction of social facilities such as shops.

The Company intends to enter into partnerships with non-governmental organisations and relevant Government agencies to facilitate capacity building in the local community in the areas of skills training and capacity development of small businesses.

Through our corporate responsibility and social investment efforts, the Company seeks to impact communities in a manner that spreads the benefit of our support to as many of the affected people as possible within a community.

Sustainability of assistance plays a major role in the Company’s corporate responsibility decisions as does the fit of the required assistance to our corporate values, policies and shareholder interests.

We value and encourage the involvement of all staff in the Company’s efforts to uphold, respect and carry out its responsibilities as a corporate citizen to the best standards possible and to the full benefit of other citizens.

32

COPPERBELT ENERGY CORPORATION PLC

Acid Test Ratio

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

2005 2006 2007 2008 2009 2010Year

Times

Debtor Days

-

10

20

30

40

50

60

70

2005 2006 2007 2008 2009 2010Year

No of Days

GP

-

10,000

20,000

30,000

40,000

50,000

60,000

2005 2006 2007 2008 2009 2010Year

Gross Profit

Return on Assets

0%

1%

2%

3%

4%

5%

6%

7%

2005 2006 2007 2008 2009 2010Year

Return on Assets

EBITDA

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

2005 2006 2007 2008 2009 2010Year

EBITDA

Earnings Per Share

-

0.20

0.40

0.60

0.80

1.00

1.20

1.40

2005 2006 2007 2008 2009 2010Year

EPS in Cents

Debtor Days

Acid Test Ratio

Gross Profit

Return on Assets

EBITDA

Earning Per Share

Operational / Financial Highlights

33

COPPERBELT ENERGY CORPORATION PLC

Revenue

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

200,000

2005 2006 2007 2008 2009 2010YEAR

US$`000

Revenue

Profit Before Interest and Tax

0

5,000

10,000

15,000

20,000

25,000

2005 2006 2007 2008 2009 2010Year

US$`000

PBIT

Load

505 514 521 533

436

470

050

100150200250300350400450500550600

2005 2006 2007 2008 2009 2010YEAR

LOAD (MW)

Load

Revenue

Profit before Interest and Tax

Load

34

COPPERBELT ENERGY CORPORATION PLC

Directors’ ReportThe Directors have pleasure in submitting to the shareholders their report and the financial statements for the year ended 31 December 2010.

The Company’s principal business is the generation, transmission, distribution and sale of electricity and telecommunication service provision. In the quest to develop the telecommunication business, the Company signed a joint venture agreement with RTAA (Proprietary) Limited on 11th February 2009 to acquire a 50% interest in Realtime Technology Alliance Africa Limited (‘Realtime’).

Financial resultsThe turnover for the year was US$167 million (2009: US$154 million). The gross profit was US$46 million (2009: US$42 million). The Table below presents a financial summary of key indicators for the five year period to 2010.

Key Statistics 2010 2009 2008 2007 2006

Sales ($’000) 167,294 154,169 177,486 131,746 127,280

Gross profit ($,000) 45,856 42,371 49,526 38,746 37,383

Profit before interest and taxes ($,000) 19,602 19,126 17,222 13,306 12,745

Acid test ratio (Times) 0.76 0.95 1.26 1.24 0.67

Return on equity 8% 8% 26% 16% 12%

EBITDA ($,000) 30,293 28,682 26,419 22,152 21,293

Total assets ($,000) 277,585 274,711 178,977 150,745 131,453

Earnings per share (Cents) 1.27 1.19 1.01 0.73 0.79

Return on assets 4.6% 4.4% 5.7% 4.6% 6.0%

Net profit ($,000) 12,719 11,920 10,143 7,251 7,915

Equity ($,000) 160,992 158,273 39,573 45,630 65,680

Current assets ($,000) 36,316 36,500 53,579 35,151 17,395

Inventory ($,000) 3,462 3,506 3,443 1,307 1,136

Current liabilities ($,000) 43,466 34,847 39,786 26,149 24,332

Working capital

The Directors have noted the negative working capital position as at 31 December 2010 of US$7.1 million. Therefore, the directors have made arrangements to increase the company’s current assets by US$10 million during the first quarter of 2011 by securing a loan from Citibank Zambia. The term sheet for the loan was signed and approved on 1 December 2010. This facility is repayable over a period of 36 months in equal quarterly instalments. The pricing of the facility is LIBOR plus 3.375% and first draw down is expected in the first quarter of 2011.

35

COPPERBELT ENERGY CORPORATION PLC

Capital Expenditure

CEC’s capital expenditure programme has been developed in line with the Company’s strategy of minimizing business risks, enhancing customer satisfaction and ensuring future business activities.

In this regard, the major categories of expenditure include emergency generation equipment, transmission and distribution equipment, protection and metering equipment, safety health and environmental (SHE) equipment, IT, vehicles and communication and control equipment.

Through its continuous capital expenditure programme, CEC continually refurbishes its Gas Turbine Alternators (GTAs) to improve the reliability of standby power plant, replaces system assets that have reached the end of their useful lives and invests in equipment that ensures that the Company will meet required high standards for SHE compliance.

In addition to its planned capital expenditure for the maintenance, renewal and refurbishment of its network and associated facilities, CEC undertook further projects related to (i) installation of power factor correction equipment (US$2,473,000), (ii) telecommunication optic fibre procurement and installation (US$2,283,000), (iii) procurement of Konkola Expansion project spares (US$882,000) and (iv) Feasibility studies and preparatory works on the Kabompo Hydro project site US$1,388,000. The total capital expenditure for the year was US$13.761 million.

Insurance

The Company has insured its operational assets against all significant business risks. The Company also maintains insurance for its Directors in respect of their duties as Directors of the Company. Besides the foregoing, the Company has cover for employer’s liability, public and product liability, group personal accident, motor vehicle insurance and group life assurance. These policies are renewable and run from 1st May to 30th April of the following year.

Directors’ Report (Continued)

Dividends and transfer to reserves

The policy of the Company in respect of the payment of dividends is a matter to be determined by the Board in accordance with the principles outlined below:

The Company’s actual accumulated profits arising from the business of the Company in respect of each year after: -

(i) provision of working capital as determined by the Board;

(ii) transfers to reserves as in the opinion of the Board ought reasonably to be made;

(iii) service of all debts and full compliance with any financing agreements to which the Company is party at the relevant time of payment; and

(iv) taking into account the interests of the shareholders in minimizing taxation liabilities.

shall be distributed by the Company to the shareholders by way of dividend.

The Company has a policy of declaring dividends twice a year; in March and August. Dividends of US$6,000,000 and US$4,000,000 were paid on 26th March and 25th October, 2010 respectively. Retained profit taken to reserves at 31 December 2010 was US$12.7 m.

Operations

During the year, all purchases of electrical power were from Zesco Limited (ZESCO) under the Bulk Supply Agreement. Electricity supplies from this source accounted for 99.98% of the total requirements.

The operations of the Company’s high-voltage

36

COPPERBELT ENERGY CORPORATION PLC

transmission and distribution system were maintained to a satisfactory standard.

A total of two hundred and twenty-two (222) faults occurred on the system in 2010 compared with one hundred and ninety-two (192) in 2009. The increase was attributed to more lightning related faults. There were two occurrences which resulted in interruptions of power supply to the Chililabombwe area. In each case, a disturbance was experienced on the Societe National d’Electricite (SNEL) system in the Democratic Republic of Congo (DRC) and at Luano substation, the Michelo 220kV line protection operated and tripped the line. This resulted in the SNEL import being channelled through the Luano – Bancroft area and Avenue – Bancroft 66kV lines via Michelo substation causing an over-load situation.

There were 36 faults on 220kV, 83 on 66kV and 8 on 11kV transmission networks; 6 on 220kV Transformers; 49 on 66kV Transformers; 9 on Rotating Plant; 1 on 220kV Busbars; 2 on 66kV Busbars; 1 on 11kV Busbars; 3 Major faults; 3 over frequency conditions and 21 through faults.

A satisfactory security of supply from ZESCO was generally maintained through out the review period. However, there was an interruption of ZESCO power supply to the entire Copperbelt for 4 hours 55 minutes on 18th June 2010 as a result of a fault on the Zesco 330kV transmission network.

The efficiency of the annual bush clearing exercise was maintained. However, a total of eleven (11) faults were experienced on the Michelo – Karavia 220kV tie line due to bush fires on the Congolese section of the tie line. In the year 2009, nineteen (19) faults were experienced.

Thefts and vandalism of the Company’s installations continued to be a major cause of concern. There were 18 incidents during the review period compared with 31 in the year 2009. There were 7 tower steel member thefts; four

Directors’ Report (Continued)thefts of overhead copper conductors; two thefts of copper earthing conductors and two cases of vandalism in the review period. Repairs were carried out as incidents were reported.

The stringent security measures that have been employed have been working well so far, thus the security of the power system has not been compromised.

Directors

The Directors who served during the year and at the date of this report were as follows:

Hanson Sindowe ChairpersonJean Madzongwe Deputy Chairperson

Teddy J Kasonso Appointed on 8 February 2010

Neil CroucherMichael TarneyIrene L Ng’andweStandwell C MaparaAbel MkandawireEmmanuel MutatiMunakupya HantubaJonathan M Muke

Robert Chestnutt Appointed on 18 August 2010

Peter Mumba Retired on 8 February 2010

Helen Tarnoy Retired on 18 August 2010

With the exception of (i) Madison General Insurance Company Limited, who provide insurance services in which Abel Mkandawire is a Director and (ii) Mopani Copper Mines Plc, which is a large customer of the Company and in which Emmanuel Mutati is Chief Executive Officer, the Company did not enter into contracts with any Company where a Director has material interests.

37

COPPERBELT ENERGY CORPORATION PLC

Share Capital

The authorised share capital of the Company is US$100,001, divided as follows:

1,000,000,000 Ordinary shares of a par value of US $0.0001 each1 Special Share of US $1.00 held in the Company by the Government of the Republic of Zambia

As at 31 December 2010, the shareholding was as follows:Zambian Energy Corporation (Ireland) Limited

520,000,000

ZCCM Investments Holdings PLC 200,000,000Private Individuals/Institutions 280,000,000Government of the Republic of Zambia (Golden Share)

1 Special Share

Average number and remuneration of employees

The total remuneration of employees during the year amounted to US$14.5 million (2009: US$10.7 million) after the capitalisation of labour, and US$14.6 million (2009: US$12.4 million) before the capitalisation of labour, and the average total number of employees was as follows:

Month NumberJanuary 355February 358March 358April 359May 358June 358July 356August 356September 358October 359November 360December 360Average 358

Power Dynamos Football Club

CEC continues to sponsor Power Dynamos Football Club through a direct funding.

Industrial Relations

A sound industrial relations climate prevailed in the Company during the year and no work stoppages were experienced. The Company will continue to pursue proactive dialogue and partnership with the Mineworkers Union of Zambia (MUZ).

Developments

The Company’s total demand continued to recover over the period under review with electricity consumption by CEC’s customers having increased by 8% on a year by year basis. The energy sales for CEC’s mining customers increased from 3,338 GWh in 2009 to 3,640 GWh in 2010 while capacity sales went up from 453 MW at the beginning of the year to a high of 487 MW. The good copper price continues to spur on measureable demand ramp up by the Company’s customers particularly Konkola Copper Mines Plc (KCM), Mopani Copper Mines Plc (MCM), NFC Africa Mining (NFC) and CNMC – Luanshya Copper Mines (CNMC-CLM). CEC’s capacity sales were, however, still lower than the pre-financial crisis high of about 520MW mainly due to the Chambishi (COSAK) smelter, which remained under care and maintenance.

On the power wheeling front, domestic wheeling on behalf of ZESCO, the national power utility, through the CEC system recorded a marginal increase from 1,657 GWh in 2009 to 1,660 GWh in 2010. International wheeling, on the other, hand showed a slump due to expiration of some international power purchase agreements involving SNEL and Zimbabwe Electricity Supply Authority (ZESA), and SNEL and Eskom. It is expected that international wheeling will rebound as SNEL completes rehabilitation of its generation facilities to restore capacity and

Directors’ Report (Continued)

38

COPPERBELT ENERGY CORPORATION PLC

Developments (continued)

the interconnection between CEC and SNEL is expanded to make it more reliable.

CEC is pleased to report the successful extension by the Company of the terms of the NFCA and Chibuluma Mines Power Supply Agreements (PSA) by a further 15 years and 10 years respectively. These PSAs were due to expire by the end of 2012.

During the year, CEC also commissioned a Cost of Service study, which will review the cost involved in the provision of services by CEC. NETGroup Solutions (Pty) Limited, a South African based consultant has been contracted to carry out the study, which will help CEC, as a going business, to understand its ability to continue operating on a commercial basis for the foreseeable future.

Various customer expansion projects were also commenced during the year. These include Muliashi by CNMC-CLM, Konkola North Mine by KONNOCO, Synclinorium by MCM and CRO by KCM. Upon completion, these projects will result in power sales increase of at least 107MW.