Embed Size (px)

DESCRIPTION

Citation preview

A Compelling Iron Ore Investment Opportunity

Corporate Presentation

January 2014

TSX: BKI

TSX: BKI

2

Disclaimer Forward Looking Statement

This Presentation contains ‘‘forward-looking information’’ within the meaning of applicable Canadian securities legislation. Forward-looking information is based on what management

believes to be reasonable assumptions, opinions and estimates of the date such statements are made based on information available to them at that time, including those factors discussed

in the section entitled ‘‘Risk Factors’’ in the Company’s annual information form for the year ended December 31, 2011 (and dated March 26, 2012) or as may be identified in the

Company’s public disclosure from time to time, as filed under the Company’s profile on SEDAR at www.sedar.com. Forward-looking information may include, but is not limited to,

statements with respect to results of the Feasibility Study (as defined below) and the mineral reserve and resource estimate, the future financial or operating performance of the Company,

its subsidiaries and its projects, the development of and the anticipated timing with respect to the Shymanivske project, the ability to obtain financing; and the impact of concerns relating

to permitting, regulation, governmental and local community relations. Generally, forward looking information can be identified by the use of forward-looking terminology such as "plans",

"expects" or "does not expect", "is expected", "budget", "scheduled", "estimates", "forecasts", "intends", "anticipates" or "does not anticipate", or "believes", or variations of such words and

phrases or state that certain actions, events or results "may", "could", "would", "might" or "will be taken", "occur" or "be achieved". Estimates underlying the results of the Feasibility Study

arise from engineering, geological and costing work of Lycopodium Minerals Canada Ltd. (“Lycopodium”), Soutex Inc. (“Soutex”), Watts, Griffis and McOuat Limited (“WGM”), Consulting

Geologists and Engineers of Toronto, P&E Mining Consultants Inc. (“P&E”) and the Company. See the technical report relating to the feasibility study for a description of all relevant

estimates, assumptions and parameters. Forward-looking information is subject to known and unknown risks, uncertainties and other factors that may cause the actual results, level of

activity, performance or achievements of the Company to be materially different from those expressed or implied by such forward-looking information, including but not limited to: general

business, economic, competitive, geopolitical and social uncertainties; the actual results of current exploration activities; other risks of the mining industry and the risks described in the

annual information form of the Company. Although the Company has attempted to identify important factors that could cause actual results to differ materially from those contained in

forward-looking information, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such information will prove to be

accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward looking

information. The Company does not undertake to update any forward-looking information, except in accordance with applicable securities laws.

This Presentation does not constitute an offer to sell, or solicitation of an offer to buy, any securities by any person in any jurisdiction in which it is unlawful for such person to make such an

offering or solicitation. No representation or warranty, express or implied, is made as to the accuracy or completeness of the information set out herein, and nothing contained herein is, or

shall be relied upon, as a promise or representation, whether as to the past or future.

Bankable Feasibility Study (the “Feasibility Study”) – For additional information, please see the Company’s press release dated January 23, 2014.

*Resource estimate compiled using historic Soviet data by Hugues de Corta, who is an independent qualified person as defined by NI 43-101. Readers should not place undue reliance on

historical estimates.

*The mineral resource estimate for the Shymanivske Project is based on results from 185 historical drill holes totaling 37,316 meters and 60 Black Iron drill holes, which were drilled during

the Company’s Twin Hole drill program and the Definition Drill program, totaling 16,518 meters and is effective as of September 2012. Watts, Griffis and McOuat Limted (“WGM”),

Consulting Geologists and Engineers of Toronto, Canada, was retained to audit an in-house mineral resource estimate completed by Black Iron. Mr. Michael Kociumbas, P.Geo, Vice-

President of WGM and Mr. Richard Risto, P.Geo, Senior Geological Associate of WGM, were retained by Black Iron as independent technical consultants and are Qualified Persons as defined

by NI 43-101 and are responsible for reviewing and approving this mineral resource estimate. The Feasibility Study was prepared in accordance with the guidelines of National Instrument 43-101 by the independent firms of WorleyParsons Canada Services Ltd., Watts, Griffis and McOuat Limited and P&E Mining Consultants Inc.

*Matt Simpson President & CEO of Black Iron, a Qualified Person as defined by NI-43-101, has reviewed and approved the scientific and technical information in this presentation.

TSX: BKI

3

What Sets Black Iron Apart? Access to Skilled Labour & Infrastructure –

Two of the Most Challenging Iron Ore Project Development Risks

Key Development Risks

Taxes/Royalties

Human Resources

Access to Infrastructure

Community Opposition

Licensing/Permitting

Access to Water

Electricity Supply

Canada

Brazil

Africa

Australia

Ukraine

3

TSX: BKI

* Please see note on Page 2 4

Black Iron has ALL the Key Fundamentals for

a Successful Low Cost Project in Place

Exceptional Infrastructure

• Significant infrastructure

advantages (power, rail

and port) with confirmed

access and capacity

• Skilled local workforce

• Local partnerships

Compelling Economics

• Bankable Feasibility Study

(Shymanivske Project):

- 9.9Mtpa of 68% Fe Conc.

- Pre-tax NPV8 of US$3.3B

- Pre-tax IRR of 48%

• Pre-tax break even price of

$54/t (after-tax)

Sizable Resource

• Large NI 43-101 Compliant

Resource*

- Shymanivske

646Mt (M+I) @ 32% Fe

188Mt (Inf) @ 30% Fe

- Zelenivske (upside)

1.1 - 1.8Bt potential

Skilled

Leadership

• History of creating value

for shareholders

• Significant Ukrainian

political and iron ore

operations experience

Close to Target Markets

• Located in Kryviy Rih,

Ukraine a major iron ore

district, close to Europe,

Turkey, Russia, Asia and

Middle East

Metinvest Development Agreement

• Ukraine’s largest company,

9th globally in iron ore, 16th

in steel

• Committed to half of

project construction

financing (est. $250-$500M)

TSX: BKI

Board of Directors Key Management

Matt Simpson – President & CEO

• Former General Manager, Mining for Rio Tinto’s Iron Ore Company of Canada

• Worked for Hatch designing global metallurgical refineries

George Mover – COO

• Former Project General Director of Ferrexpo Yeristovo Mining, Ukraine

• Since 1994 worked on numerous mining projects in Former Soviet Union (Ukraine, Russia, Kazakhstan, Armenia)

Paul Bozoki – CFO

• Former CFO of CD Capital Partners, operating in Former Soviet Union & Ukraine

Aaron Wolfe – VP Corp Development

• Former investment banker with Macquarie

Nikolay Bayrak – VP Gov’t & Community Relations

• Former department head, Ukrainian Ministry of Emergencies and Public Protection; Former MP and President of MP’s Parliamentary Social Club

Bruce Humphrey – Chairman

• Former Chairman of Consolidated Thompson Iron Mines

Jaroslav Kinach

• Former Advisor to Ukraine Prime Minister and former Ukraine Country Head of EBRD

Chris Westdal

• Canadian Ambassador to Ukraine (1996-98) and to Russia (2003-06)

Pierre Pettigrew

• Former Canadian Minister for Foreign Affairs and international Trade

John Detmold

• Chairman & Founder of Invescture Group, S.A. de C.V. which owns Frontera Copper Corporation

Dave Porter

• Former VP for Rio Tinto’s Iron Ore Company of Canada and COO of Algoma Steel

Matt Simpson – President & CEO 5

A Track Record of Iron Ore Success with Consolidated Thompson Iron Mines, Rio Tinto’s Iron Ore Company

of Canada, and Ferrexpo

TSX: BKI

6

Project Backed by Forbes & Manhattan Success with Consolidated Thompson’s Bloom Lake Iron Mine

• World class 8Mtpa iron ore concentrate mine in Quebec

• Advanced from exploration stage through development to construction

− 8 mtpa capacity (66% Fe concentrate) expanding to 16 mtpa

− Completed scoping study, 3 feasibility studies, secured off-take with China’s third largest steel producer (WISCO)

• Raised over Cdn$1 bn in capital

• Attracted and put in place a qualified management team

Recently acquired for $4.9 billion

$1 mm market

cap

First F&M involvement

Forb

es

& M

anhatt

an I

nvolv

em

ent

2005 Q1-2011

Acquired for $4.9 billion

TSX: BKI

7

Major Local Development Partner: Metinvest Ukraine’s Largest Company and a Global Iron Ore & Steel Producer

• Over 100,000 employees; Generated US$12.6 billion of revenues and a 16% EBITDA margin in 2012

• Metinvest is owned by System Capital Management (SCM) and Smart Holding

• SCM has over US$28.4B in assets and operations across 13 different areas including ownership of:

• Global Commodity Ranking:

• DTEK >18GW of electricity production (~26%)

• Leman Trans, ~21% of railway cars

• Portinvest, ~13% of Ukraine’s port capacity

• 9th in Iron Ore with 33.9 MT • 16th in Steel with 18.4 MT • 33rd in Coal with 2.6 MT

TSX: BKI

Sound Capital Structure Attractive Valuation with Substantial Upside & Funding Support

8

Corporate Structure Capital Structure (TSX: BKI)

Shares Outstanding 141.5 million

Stock Options (1) 5.7 million

Fully Diluted Shares 147.2 million

Market Cap(2) ~US$29.3 million

Current Cash Balance(3) ~US$3.1 million

Debt Balance nil

1. 5,713,750 options exercisable at a weighted average price of $0.45 per share. 2. As at January 22, 2014, using a closing price of CAD $0.23 per share. 3. As at Sept 30, 2013 per Q3 Unaudited Financial Statements.

Metinvest Transaction Summary

Analyst Coverage

Black Iron Inc. (TSX: BKI)

Shymanivske Steel

Zelenivske Steel

Metinvest

Black Iron Cyprus

• Metinvest acquires 49% of Black Iron Cyprus for a total commitment up to US$535M

– US$20M due upon closing

– Matching of any further equity financed capital

• Metinvest option to increase ownership in Black Iron Cyprus to 51%

− Option vests after 3 consecutive months of production at nameplate capacity

− Option priced at a 30% premium to the fair market value as derived by an independent third party

TSX: BKI

9

Deposits In Mining Friendly Region Adjacent to existing Iron Ore Producers

• Two mining and exploration permits covering 5.92 km2

− Mining permit at Shymanivske, which has been extensively explored, covering 2.56 km2 valid until 2024

− Exploration permit at Zelenivske covering 3.36 km2 valid until 2014

• Adjacent to ArcelorMittal’s Kryviy Rih iron ore complex and Smart & Evraz’s YuGOK iron ore mine

• Plan to acquire a plot of land from Ukraine Government adjacent to the Shymanivske deposit for project waste dumps, concentrator and tailings

Black Iron’s Shymanivske Project

M&I: 646Mt @ 31.6% Inferred: 188Mt @ 30.1%

Black Iron’s Zelenivske

Project

ArcelorMittal’s Kryviy Rih Iron Ore Complex

Smart & Evraz’s YuGOK Iron Ore Mine

Railway lines

** See Black Iron’s website at www.blackiron.com for a Corporate Video highlighting the project location and infrastructure **

TSX: BKI

10

Large Ore Deposit with Growth Potential

• Banded iron formation consisting primarily of magnetite with some hematite

− Iron band thickness ranges from 40-80 m

− Only 9.7-21.2 m of overburden with a strip ratio of 1.63:1, life of mine; 1.36:1 for first 8 years

− Very clean ore body low in phosphorus, manganese and aluminum

• Resource defined by ~54,000 metres of drilling

― Black Iron completed a Twin Hole Drill Program consisting of 6,042 metres and a Phase II Drill Program consisting of 11,435 metres of infill drilling

― Total iron grade and band width align very well with 37,000 metres of historical drilled data

• Potential for total combined resource expansion of 1.1 to 1.8BT

− Additional drilling of Shymanivske at North end of deposit and to depth

− Exploration of the Zelenivske project

Shymanivske

Resource*

Tonnage

(Mt)

Fe Tot

(%)

Fe Mag

(%)

Measured 355.1 32.0 19.5

Indicated 290.7 31.1 17.9

Total Measured and Indicated

645.8 31.6 18.8

Inferred 188.3 30.1 18.4

* Please see note on page 2 Tonnage and grade rounded to first decimals. Cut-off grade of 10% Fe Mag

TSX: BKI

11

Potential Resource Extension at Shymanivske Ground Gravity Shows Iron Ore Mineralization at North End

• Ground gravity and magnetic surveys show potential extension of iron ore mineralization at North end of property as circled in red

• This area has not been included in the NI 43-101 resource as it has not yet been sufficiently drilled

• The identified area will be a target of a future drill program to allow for a second phase process plant expansion to increase production and project value

Potential resource upside to be drilled

Drill hole

Property boundary

Very likely Iron in ground

Likely just dirt in ground

TSX: BKI

Extensive Pit Shell Design and 3D Model

Completed (Property Overview)

12 * Bankable Feasibility Study complete by Lycopodium Minerals Canada Ltd.

TSX: BKI

Concentrator Footprint Compressed by

Staggering HPGRs and Stacking LIMS

13 * Bankable Feasibility Study complete by Lycopodium Minerals Canada Ltd.

TSX: BKI

14

Conventional Flowsheet Producing High Quality Iron Ore Products

Fe 68.0%

SiO2 4.5%

P 0.02%

S 0.05%

Al2O3 0.43%

Mn 0.03%

P80 32 µm

B.F. Concentrate

Fe 65.5%

SiO2 4.5%

S <0.01%

CaO/SiO2 0.15%

SiO2+Al2 O3 5.1%

CaO+MgO 1.0%

Compress. 318kg/pel

B.F. Pellets

Fe 69.5%

SiO2 1.3%

P 0.02%

S 0.05%

Al2O3 0.28%

Mn 0.03%

P80 32 µm

D.R. Concentrate

Fe 67.4%

SiO2 2.0%

S <0.01%

CaO/SiO2 0.34%

SiO2+Al2 O3 2.4%

CaO+MgO 1.2%

Compress. 283g/pel

D.R. Pellets

Co

re P

rod

uct

Va

lue

-Ad

d

Alt

ern

ati

ve

P

rod

ucts

TSX: BKI

15

Excellent Infrastructure with confirmed access Key to a Successful Iron Ore Project

• Paved roads to site, located 35km away from the major city of Kryviy Rih which has a skilled work force

• Surplus electricity readily accessible from high voltage power lines that run beside property

• ~2 km from main state-owned rail line

• Confirmation in July 2010 from Ukrainian Government that there is sufficient capacity to haul at least an additional 20 million tonnes of iron ore per annum

• 5 deep water ports accessible by rail with iron ore facilities available

• Preferred port option is Yuzhny located ~430 km away and providing access to the Black Sea and global seaborne iron ore markets

** See Black Iron’s website at www.blackiron.com for a Corporate Video highlighting the project location and infrastructure **

TSX: BKI

16

Strategic Global Location Close Proximity to Target Markets with Abundant Port and Rail Access

• Project is surrounded by steel mills in Europe, Turkey and the Middle East

• River barge & rail access to Western Europe.

• Five dry bulk tonnage ports accessible using railway running beside properties

• Approx 20% to 25% shorter transport distance to growth markets of India and China compared to North and South American producers

• Excellent Ukrainian logistical advantages

• Densely populated roadway infrastructure

• 468 million tonnes of cargo transported via rail

• 155 million tonnes of cargo transported via ship

TSX: BKI

17

Ukraine: A Mining Friendly Country in

Transition

• S&P Sovereign Risk rating of B

− Next Presidential election to occur in Q1-2015 (5 year term)

− GDP growth of 4.2% in 2010; 5.2% in 2011; 0.2% in 2012 (impacted by slowdown in global economy and steel production)

− Member of WTO

− Strong desire by citizens and business for European integration (and further separation from Russia) but government has delayed signing “Trade Agreement” over concerns of increased cost for Russian gas and trade restrictions

• Joining the “Trade Agreement” with Europe would benefit Black Iron due to lower construction costs via reduced duties. However not joining is neutral for Black Iron, as the Bankable Feasibility Study was completed without those cost savings assumptions

• Economy dominated by agriculture & commodities

― Steel production is Ukraine’s largest industry

― 60% of Ukraine’s total exports are commodity-related (the majority of which is steel)

• Large, highly skilled labour force (pop. 45.4 million)

− GDP per capita only $7600/yr

− Literacy rate >99%

• Mining friendly jurisdiction with strong local and national support

― ArcelorMittal and Ferrexpo plc have operated in-country for over 7 years

• Low corporate tax rate of 16% reduced from 21% in 2012

• Favourable mining royalties of $0.09 per tonne of ore mined (<1%) payable to the Government

$5Bn Investment in Integrated Iron Mine/Steel Mill

$3.2Bn Market Cap Iron Ore and Steel Production

in Ukraine

$1.8Bn Investment in Shale Gas Development

$10Bn Investment in Shale Gas Development

$10Bn Investment in Shale Gas Development

Major Foreign Corporate Investors

TSX: BKI

18

Source: Based on know production and reserves as listed in the USGS 2012 Iron Ore report

Globally Significant Iron Ore District 4th largest iron ore producer & 2nd largest reserve base

Global Distribution of Fe Reserves & Fe Production

• Black Iron’s projects are located in the heart of

Ukraine’s iron ore belt

– 35km from city of 750,000 people

• Iron ore district trends 300 km with sedimentary rock

hosted banded iron formations (Dnenpovskog complex)

• Historically well explored resource base but

substantially under-exploited due to historic Soviet

policy

• 15 iron ore mines in Ukraine produced 88 million

tonnes in 2012

Kiev

Yeristovskoye

Poltavsky GOK

Tsentralny Kryviy Rih Iron Ore Complex

Ingulestky GOK

Yuzhny GOK Kryviv Rih Ordzhonikize Gok

Shymanivske

Zelenivske

C Gok YuGok

0%

10%

20%

30%

40%

50%

60%

Asi

a

Aust

ralia

S.

Am

eri

ca

FSU

N.

Am

eri

ca

Oth

er

Afr

ica

% o

f W

orl

d P

roducti

on a

nd R

ese

rves

Production Reserves

Production Reserves

7%

21%

TSX: BKI

19

Permit Process for Shymanivske Deposit Black Iron Remains on Track

Exploration

Permit

Extraction

Permit

Land

Allotment

Construction

Approval

Operations

Approval

Deem deposit economical

• Complete Ukraine version of scoping study including evaluation of various mining methods & high level environmental impact

Pit shell reserves & environmental

impact Gov approval

• Complete field

environmental (OVOS) & archeological studies for Gov approval

• Submit pit shell design & mapped ground surface project for Gov. approval

Obtain surface rights for mine,

refinery & tailings

• Land use analysis

based on plot plan showing major buildings & agreed connections to utilities, rail and roads (Proekt)

• Approval of the project location

• Approval from all land owners & finalize lease

Start mine overburden

removal & plant construction

• Detailed design approved (Expertisa)

• Obtaining the construction permit

• Commissioning of the facility

• Registration of the ownership to the facility

Explore resource potential

• Conduct geophysical program

• Drill ore body

• State approval of explored deposit

Operate mine & refinery

• Ensure compliance with Ukraine Safety, Environment, Health and Employment laws as check by regular Gov inspections

• Finalize environmental permits

Mining

Allotment

Completed

TSX: BKI

BFS 2012 BFS 2014

Annual Production: 9.2 Mt 9.9 Mt

Iron Content: 68.0% 68.0%

Estimated Capital Investment:

(capital intensity)

US$1,094 million

US$119/t

US$1,097 million

US$111/t

Estimated Operating Expenses:

(average FOB)

(average at Mine Gate)

US$43.97/t

US$29.67/t

US$44.54/t

US$29.64/t

Long-Term CFR Benchmark Price(62%): US$95/t US$95/t

Net Present Value (8%): (pre-tax)

(after-tax)

US$3.5 billion

est. US$2.9 billion

US$3.3 billion

US$2.6 billion

Internal Rate of Return: (pre-tax)

(after-tax)

46%

est. 40%

48%

39%

Annual Average Cash Flow: (pre-tax)

(after-tax)

US$593 million

not reported

US$630 million

US$536 million

Projected Payback (8%): (pre-tax)

(after-tax)

2.2 years

not reported

2.0 years

2.5 years

Estimated Mine Life: modelled reserve

total defined resource

16 years

~21 years

14 years

~19 years

Projected Plant Start-Up Q4 2015 Q4 2016

Projected Revenue Commencement Q1 2016 Q1 2017

BFS Highlights – High Grade Concentrate High Value, Low Net Cost Iron Ore Development Project

20 ** See Disclaimer on page 2 ** * Bankable Feasibility Study completed by Lycopodium

TSX: BKI

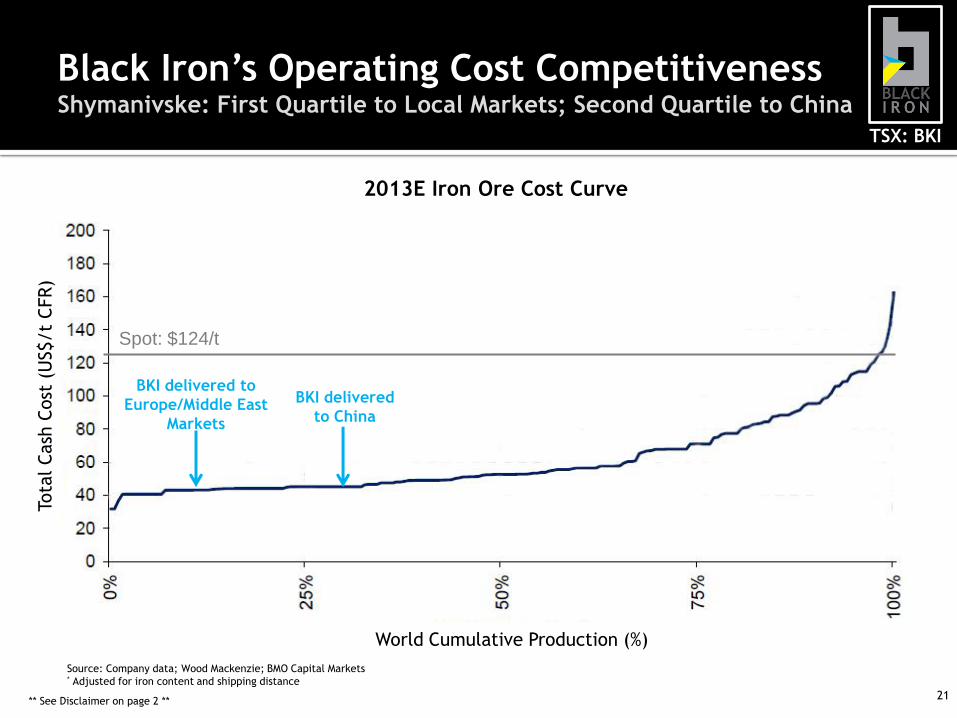

Black Iron’s Operating Cost Competitiveness Shymanivske: First Quartile to Local Markets; Second Quartile to China

21 ** See Disclaimer on page 2 **

Source: Company data; Wood Mackenzie; BMO Capital Markets * Adjusted for iron content and shipping distance

2013E Iron Ore Cost Curve

BKI delivered to

Europe/Middle East

Markets

BKI delivered

to China

World Cumulative Production (%)

Spot: $124/t

Tota

l Cash

Cost

(U

S$/t

CFR)

TSX: BKI

** See Disclaimer on page 2 **

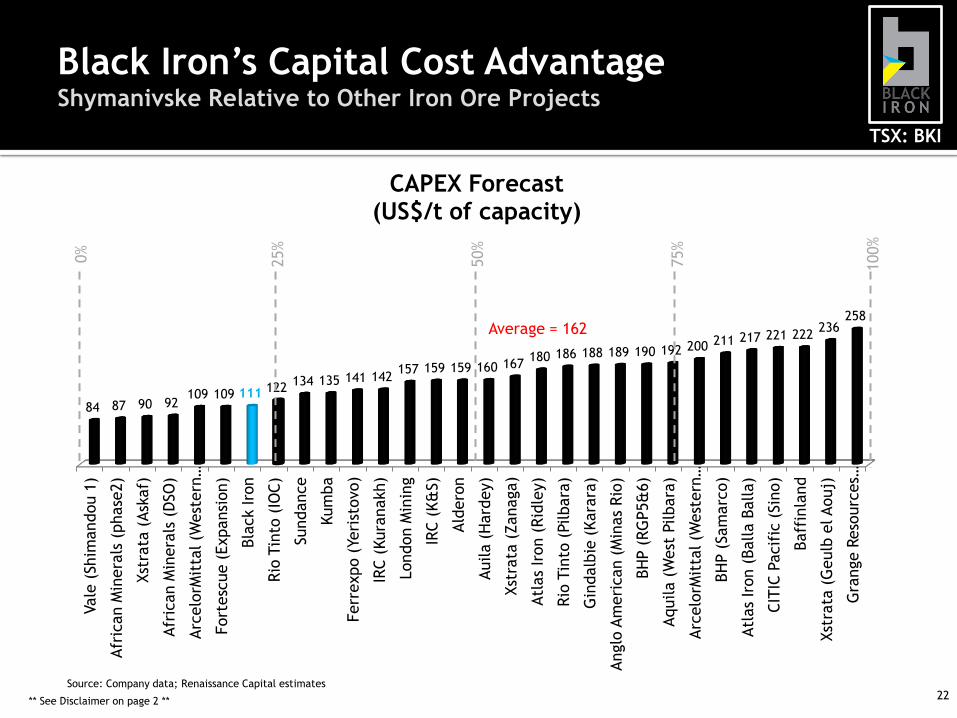

Black Iron’s Capital Cost Advantage Shymanivske Relative to Other Iron Ore Projects

22

Vale

(Shim

andou 1

)

Afr

ican M

inera

ls (

phase

2)

Xst

rata

(Ask

af)

Afr

ican M

inera

ls (

DSO

)

Arc

elo

rMit

tal (W

est

ern

…

Fort

esc

ue (

Expansi

on)

Bla

ck Iro

n

Rio

Tin

to (

IOC)

Sundance

Kum

ba

Ferr

expo (

Yeri

stovo)

IRC (

Kura

nakh)

London M

inin

g

IRC (

K&

S)

Ald

ero

n

Auila (

Hard

ey)

Xst

rata

(Zanaga)

Atl

as

Iron (

Rid

ley)

Rio

Tin

to (

Pilbara

)

Gin

dalb

ie (

Kara

ra)

Anglo

Am

eri

can (

Min

as

Rio

)

BH

P (

RG

P5&

6)

Aquila (

West

Pilbara

)

Arc

elo

rMit

tal (W

est

ern

…

BH

P (

Sam

arc

o)

Atl

as

Iron (

Balla B

alla)

CIT

IC P

acif

ic (

Sin

o)

Baff

inla

nd

Xst

rata

(G

eulb

el Aouj)

Gra

nge R

eso

urc

es …

84 87 90 92 109 109 111 122

134 135 141 142 157 159 159 160 167

180 186 188 189 190 192 200 211 217 221 222 236

258

CAPEX Forecast (US$/t of capacity)

Source: Company data; Renaissance Capital estimates

Average = 162

0%

25%

50%

75%

100%

TSX: BKI

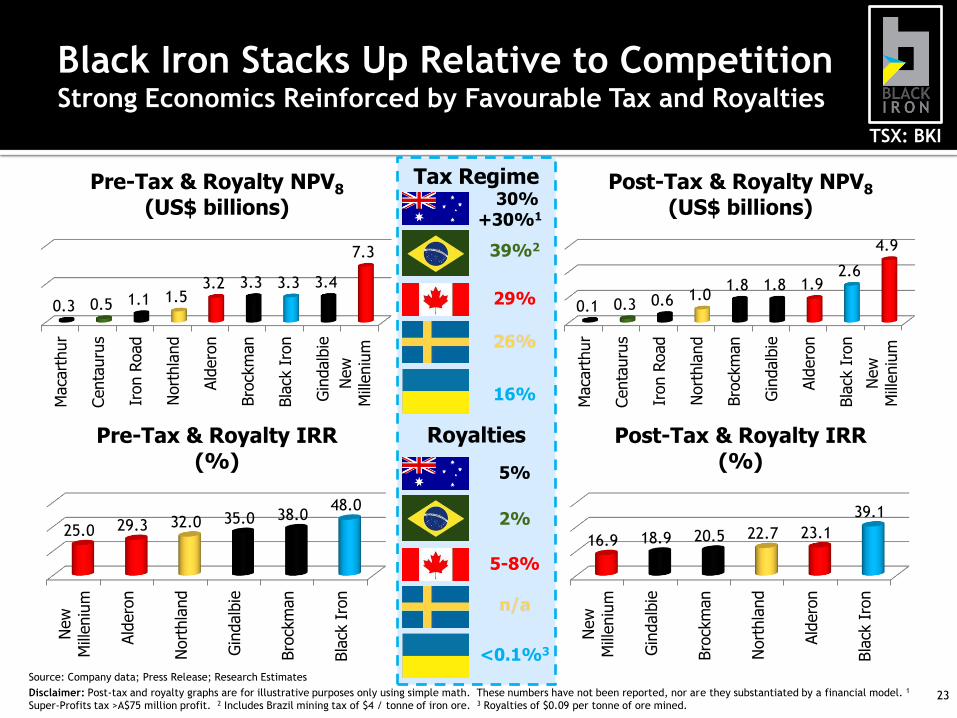

Disclaimer: Post-tax and royalty graphs are for illustrative purposes only using simple math. These numbers have not been reported, nor are they substantiated by a financial model. 1

Super-Profits tax >A$75 million profit. 2 Includes Brazil mining tax of $4 / tonne of iron ore. 3 Royalties of $0.09 per tonne of ore mined.

Maca

rthur

Centa

uru

s

Iron R

oad

Nort

hla

nd

Bro

ckm

an

Gin

dalb

ie

Ald

ero

n

Bla

ck I

ron

0.1 0.3 0.6 1.0 1.8 1.8 1.9

2.6

4.9

Post-Tax & Royalty NPV8

(US$ billions)

Source: Company data; Press Release; Research Estimates

New

M

illeniu

m

Ald

ero

n

Nort

hla

nd

Gin

dalb

ie

Bro

ckm

an

Bla

ck I

ron

25.0 29.3 32.0 35.0 38.0 48.0

Pre-Tax & Royalty IRR

(%)

New

M

illeniu

m

Gin

dalb

ie

Bro

ckm

an

Nort

hla

nd

Ald

ero

n

Bla

ck I

ron

16.9 18.9 20.5 22.7 23.1

39.1

Post-Tax & Royalty IRR

(%)

Tax Regime

Royalties

30% +30%1

39%2

29%

16%

5%

2%

5-8%

<0.1%3

New

M

illeniu

m

New

M

illeniu

m

Maca

rthur

Centa

uru

s

Iron R

oad

Nort

hla

nd

Ald

ero

n

Bro

ckm

an

Bla

ck I

ron

Gin

dalb

ie

0.3 0.5 1.1 1.5 3.2 3.3 3.3 3.4

7.3

Pre-Tax & Royalty NPV8

(US$ billions)

Black Iron Stacks Up Relative to Competition Strong Economics Reinforced by Favourable Tax and Royalties

23

TSX: BKI

Black Iron’s Target Capital Funding Strategy 49% of Equity Capital Solidified with Metinvest Transaction;

100% of Off-Take Still Available

** See Disclaimer on page 2 **

Estimated Capital Investment US$1.1 billion

Equity Investment Debt Investment

Black Iron Inc. (TSX: BKI)

Metinvest

9.9Mtpa Off-take

Export Credit Agencies

Bank Debt / High-Yield Bonds

Capital Markets

60% 40%

49% 51%

(US$250-300 million)

(US$0-50 million)

(US$300-400 million)

(US$250-350 million)

Significant Off-take Opportunity with Equity Funding Support from Metinvest ** % and $ amounts are indicative only and subject to negotiation **

(US$250-300 million)

24

TSX: BKI

Black Iron Continues to Deliver Shymanivske Project Development Timeline

2011-2012 2013

Scoping Study/PEA

Bankable Feasibility Study

Off-take

Construction

Drill metallurgical holes

Definition Drilling

Land Acquisition

Detailed Engineering

Production

Future

** See Disclaimer on page 2 **

Pilot Plant Test Work

2014

Permitting

Milestone Achieved 2014 Milestone

25

TSX: BKI

26

Black Iron Value Proposition

Close to Steel Mills in: W.Europe, Turkey, Russia, Asia and Middle East Close to

Target Markets

Large iron ore deposit with NI 43-101 compliant resource*

• 646 Mt Measured & Indicated resource @ 31.6% iron; additional 188 Mt of Inferred resource @ 30.1% iron, which will be concentrated to ~68% iron

• Potential for resource expansion to 1.1-1.8 Bt

Sizable Resource

Excellent access to skilled labour, power, rail & ports Exceptional

Infrastructure

Experienced management team and Board with history of creating value for shareholders of Consolidated Thompson, RioTinto and Ferrexpo

Skilled Leadership

High margins due to close proximity to multiple steel mills, skilled labour cost advantage and favourable corporate tax rate of 16% • Bankable Feasibility Study for 9.9Mt of high-grade 68% iron ore concentrate

– NPV of US$3.3 billion and 48% IRR (US$2.6 billion and 39% after-tax)

Compelling Economics

* Please see note on Page 2 26

Strategic Partners

Metinvest: Largest company in Ukraine; committed to half of project financing

TSX: BKI TSX: BKI

Shymanivske Project Site

CONTACT INFORMATION

65 Queen Street West

Suite 805, P.O. Box 71

Toronto, Ontario, Canada

M5H 2M5

www.blackiron.com

TSX: BKI

Investor Relations

Toronto: +1 (416) 309-2950 - Michael McAllister, IR Manager

London: +44 (0) 207 466 5000

Ukraine: +380 (56) 409-2536

[email protected] Follow us: