Embed Size (px)

Citation preview

31 73

125

0 117 176

142 180 227

63 156 53

165 0

33

255 153

0

255 204

0

255 235 153

127 127 127

0 0 0

Body Text

OECD SENIOR BUDGET OFFICIALS MEETING

15th December 2016

2

31 73

125

0 117 176

142 180 227

63 156 53

165 0

33

255 153

0

255 204

0

255 235 153

127 127 127

0 0 0

Body Text

Various Fiscal reforms: to achieve fiscal sustainability and enhance nation's net worth

GST Implementation (1 April 2015)

The GST provides the government with a more comprehensive, transparent and efficient source of revenue

The GST is also likely to improve tax compliance, broaden and diversify the Government’s revenue base

Phase-by-phase rationalisation to better target allocation of subsidies towards more vulnerable groups

Subsidy Rationalisation Programme

Creation of a Fiscal Policy Committee (FPC)

High-level, strategic decision-making executive committee comprising key economic policymakers

Reviews regularly the Government’s fiscal performance, parameters used in the Medium Term Fiscal Framework (MTFF) and tracking to targets

Supported by a Fiscal Policy Office, set up concurrently to guide fiscal decision-making

Adopting Outcome-Based Budgeting (OBB)

An integrated performance framework with focus on detailed planning and outcome of budget initiatives

Emphasis on improving data quality across all ministries and federal agencies

2 Sources: Ministry of Finance

Adoption of the Medium Term Fiscal Framework (MTFF) for fiscal projections beyond annual budget horizon

Strategy include medium term rev-exp projections which is based on existing & new policies to achieve deficit targets.

Adopting Medium Term Fiscal Framework (MTFF)

Accrual accounting is essential to systematically determine the full costs of the government’s initiatives. Hence enhancing accountability and transparency of public financial management

Government will also be able to account for and assess all assets and liabilities and cost savings relevant to the overall stance of fiscal policy and sustainability

Shift from cash-based to accrual accounting is in line with requirements under the International Public Sector Accounting Standards (IPSAS)

Implementing Accrual Accounting Practices

3

31 73

125

0 117 176

142 180 227

63 156 53

165 0

33

255 153

0

255 204

0

255 235 153

127 127 127

0 0 0

Body Text

Prudence in public finances have helped to narrow fiscal deficit over the years. Total expenditure in 2016 is lower than the original budgeted expenditure, underscoring a tightening in budgetary discipline.

Demonstrable results of fiscal prudence

Consistently delivering deficit reduction

Improvement in government finances

% of GDP

Source: MoF

Source: MoF

Budget 2017: Prudent and Productive spending

MYR bn 2015 2016B 2016R 2017B

Revenue 219.1 225.7 212.6 219.7

Operating expenditure 217.0 215.2 207.1 214.8

Current balance 2.1 10.4 5.5 4.9

Development expenditure

40.8 50.0 45.0 46.0

Less: Loan recoveries 1.5 0.8 0.8 0.7

Overall balance -37.2 -38.8 -37.7 -40.3

% to GDP -3.2 -3.1 -3.1 -3.0

30.8% 32.4% 35.7% 36.0%

15.7% 17.2% 14.3% 14.9%

15.2% 12.3% 11.9% 10.4%

10.3% 11.4% 12.9% 13.4% 7.6% 8.5% 9.2% 10.1%

20.4% 18.2% 16.1% 15.0%

2010 2015 2016R 2017B

Development expenditure by sector

Operational expenditure by object

Others

Retirement charges

Debt service charges

Subsidies

Supplies & services

Emoluments

49.5% 39.4%

7.5%

3.6%

56.2%

26.5%

11.5%

5.8%

Economic Social Defence General administration

2010

2017B

(5.3) (4.7)

(4.3) (3.8)

(3.4) (3.2) (3.1) (3.0)

(0.6)

(3.4) (2.7) (2.3)

(1.7) (1.3) (1.1) (1.0) (0.9)

1.2

2010 2011 2012 2013 2014 2015 2016R 2017Budget

2020under11MP

Fiscal balance Primary balance

4

31 73

125

0 117 176

142 180 227

63 156 53

165 0

33

255 153

0

255 204

0

255 235 153

127 127 127

0 0 0

Body Text

Alongside cuts in recurrent spending, fiscal consolidation will be led by increased revenue generation from more diverse sources as well as enhanced tax efficiency and compliance – a strategy which will further ensure fiscal sustainability

Revenue sources have moved away from reliance on the oil sector

Share of oil-related and non-oil revenues, %

Diversification away from oil-related revenues as part of an ongoing long-term strategy

Incremental government revenues despite reduced dependency on oil sector reflects effectiveness in policies

Source: Ministry of Finance

41.3 35.4 35.8 33.7 31.2 30.0 21.5 14.6 13.8

58.7 64.6 64.2 66.3 68.8 70.0 78.5 85.4 86.2

2009 2010 2011 2012 2013 2014 2015 2016R 2017B

Oil-related Non-oil

Composition of total revenue

29.0 11.5 8.5 10.6

6.5

5.1 3.7 3.7

29.0

26.0 16.0 13.0

2014 2015 2016R 2017B

PITARoyaltiesDividend

65.2 63.7 63.2 69.2

24.4 26.3 28.2 29.8

17.2 35.2 38.6

40.0

2014 2015 2016R 2017B

CITA PIT SST / GST

66.3 bn

47.2 bn

106.9 bn

125.2 bn

35.3% 37.6% 42.6% 45.2% 45.7% 48.0% 50.1%

15.0% 15.0% 13.9% 12.2% 5.3% 4.0% 4.8%

13.1% 10.4% 9.1% 9.2% 8.4% 8.5% 9.0%

7.8% 7.4% 7.5% 7.8% 3.8%

12.3% 18.1% 18.2% 22.7% 23.3% 19.4% 18.3% 17.3% 12.7% 9.7% 6.1% 6.3% 7.5% 7.3% 7.2% 8.7% 8.2%

2005-08 2009-12 2013 2014 2015 2016R 2017B

Direct taxes (excl. PITA) Petroleum income tax Indirect taxes (excl. SST / GST) SST GST Petroleum royalties and returns on investments Others

132.4 bn 177.9 bn 213.4 bn 220.6 bn 219.1 bn 219.7 bn

30.9 bn

130 bn

212.6 bn

30.2 bn

139 bn

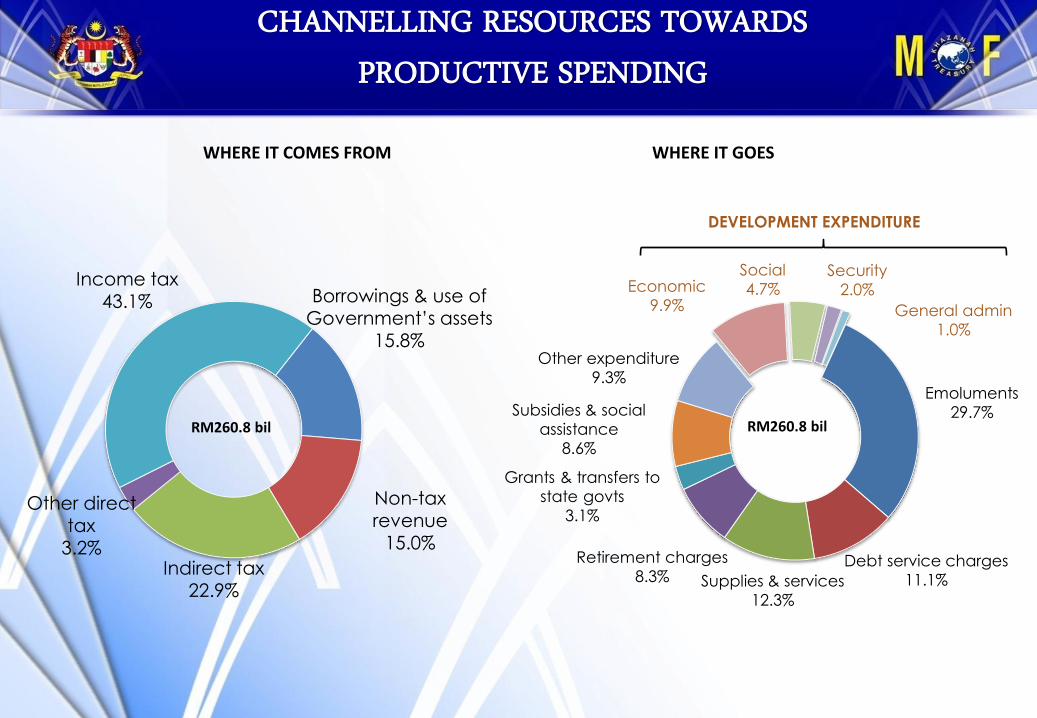

WHERE IT COMES FROM WHERE IT GOES

CHANNELLING RESOURCES TOWARDS PRODUCTIVE SPENDING

Income tax 43.1%

RM260.8 bil

Other direct tax

3.2% Indirect tax

22.9%

Non-tax revenue

15.0%

Borrowings & use of Government’s assets

15.8%

Debt service charges

11.1%

Emoluments

29.7%

General admin

1.0%

Security

2.0%

DEVELOPMENT EXPENDITURE

Economic

9.9%

Social

4.7%

Supplies & services

12.3%

Retirement charges

8.3%

Grants & transfers to

state govts

3.1%

Subsidies & social

assistance

8.6%

Other expenditure

9.3%

RM260.8 bil

2017 Budget Touchpoints

• 1Malaysia People’s Aid (BR1M) • Spurring Economic Growth

• Subsidies and Incentives • Inclusivity

• Generate additional income for B40

• Safety and Security

• Increase Home Ownership • Health and Sports

• Rakyat Centric Projects • NBOS and Transport

• Lifestyle Tax Relief • Human Capital

• Public Servants

31 73

125

0 117 176

142 180 227

63 156 53

165 0

33

255 153

0

255 204

0

255 235 153

127 127 127

0 0 0

Body Text

Appendix