Embed Size (px)

Citation preview

7/11/2016

1

1

2

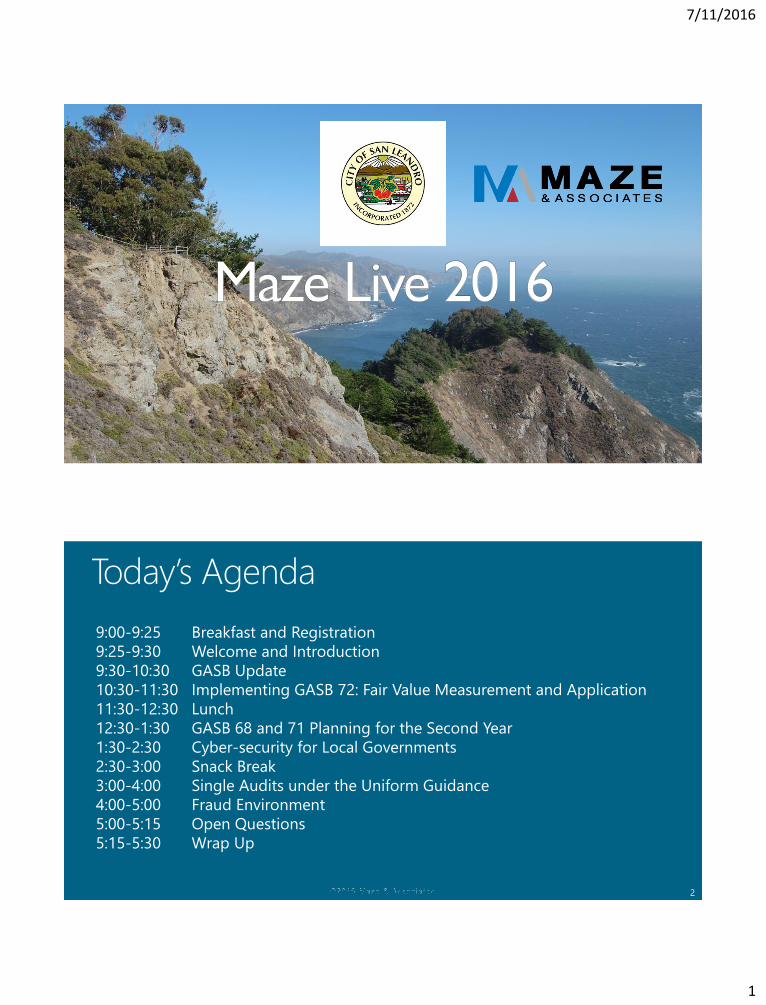

9:00-9:25 Breakfast and Registration

9:25-9:30 Welcome and Introduction

9:30-10:30 GASB Update

10:30-11:30 Implementing GASB 72: Fair Value Measurement and Application

11:30-12:30 Lunch

12:30-1:30 GASB 68 and 71 Planning for the Second Year

1:30-2:30 Cyber-security for Local Governments

2:30-3:00 Snack Break

3:00-4:00 Single Audits under the Uniform Guidance

4:00-5:00 Fraud Environment

5:00-5:15 Open Questions

5:15-5:30 Wrap Up

7/11/2016

2

3

4

7/11/2016

3

5

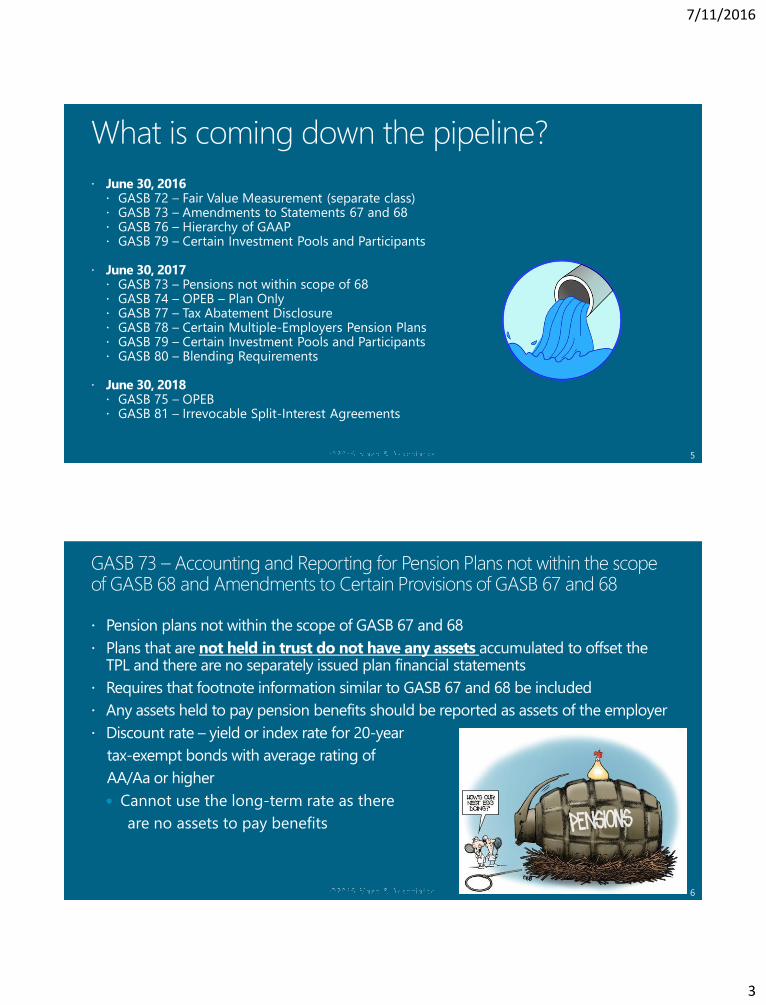

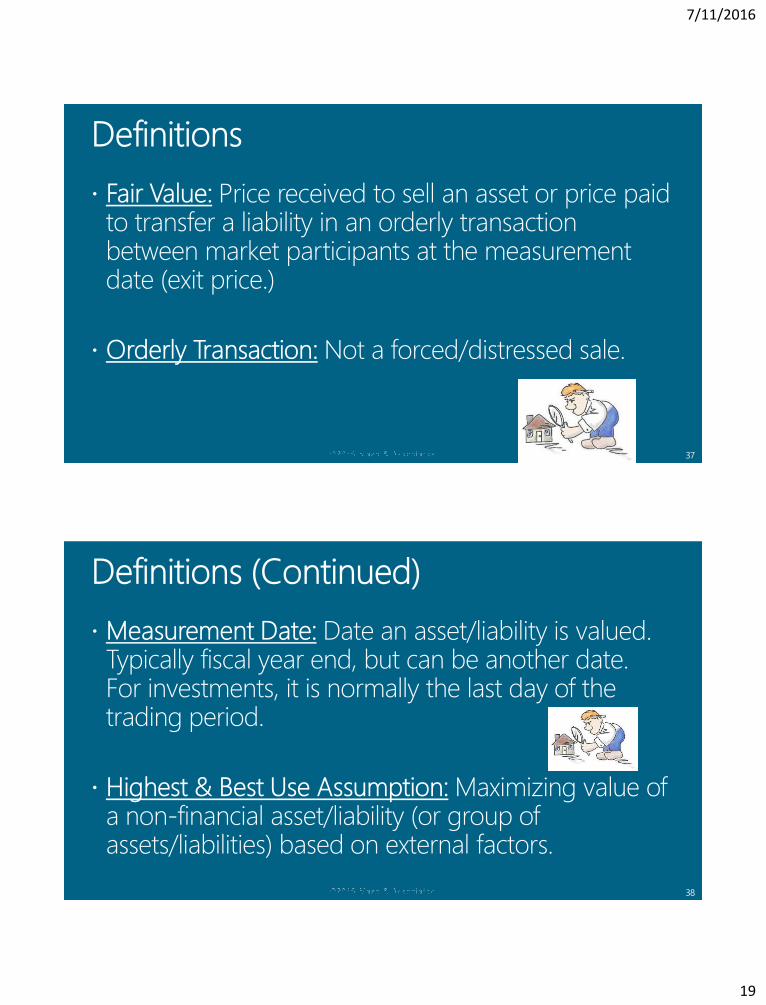

GASB 72 – Fair Value Measurement (separate class)

GASB 76 – Hierarchy of GAAP GASB 79 – Certain Investment Pools and Participants

GASB 74 – OPEB – Plan Only GASB 77 – Tax Abatement Disclosure GASB 78 – Certain Multiple-Employers Pension Plans GASB 79 – Certain Investment Pools and Participants GASB 80 – Blending Requirements

GASB 75 – OPEB GASB 81 – Irrevocable Split-Interest Agreements

6

Cannot use the long-term rate as there

are no assets to pay benefits

7/11/2016

4

7

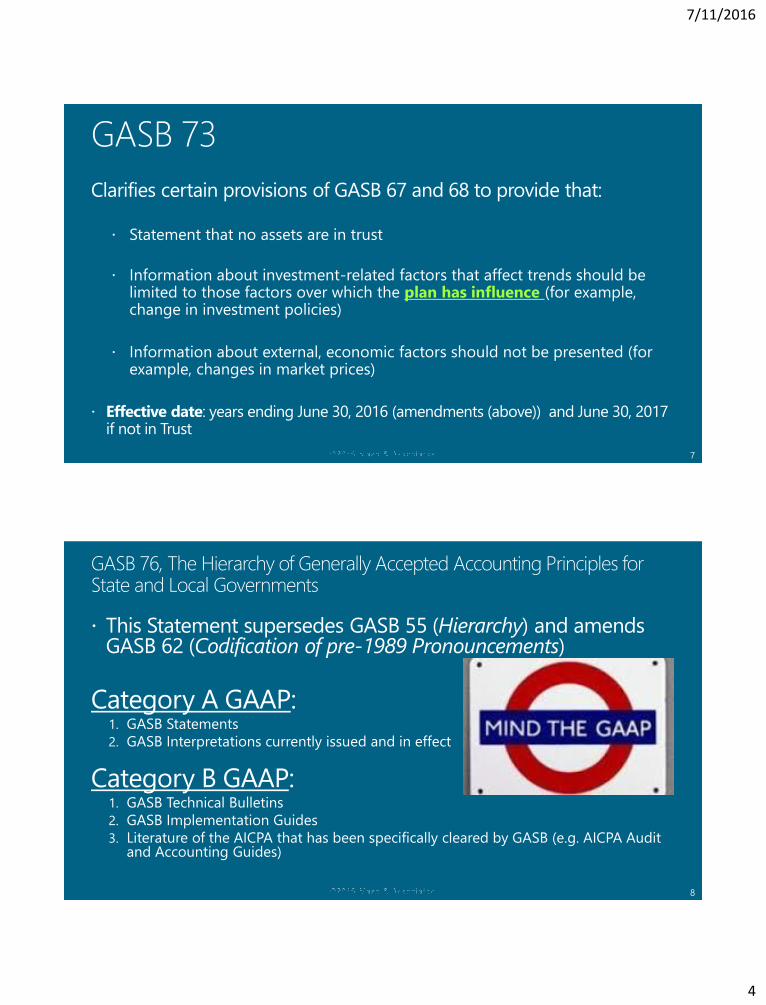

Statement that no assets are in trust

Information about investment-related factors that affect trends should be limited to those factors over which the plan has influence (for example, change in investment policies)

Information about external, economic factors should not be presented (for example, changes in market prices)

8

1. GASB Statements

2. GASB Interpretations currently issued and in effect

1. GASB Technical Bulletins

2. GASB Implementation Guides

3. Literature of the AICPA that has been specifically cleared by GASB (e.g. AICPA Audit and Accounting Guides)

7/11/2016

5

9

1. Consider non-authoritative accounting literature from other sources that does not conflict or contradict and authoritative GAAP. Sources of these items:

10

Not a State or Local Government Pension Plan

Provide benefits to both Government and Non Government employees

No identifiable predominate Government employer

7/11/2016

6

11

GASB 43-Financial Reporting for Postemployment Benefit Plans Other than Pension Plans and Statement

GASB 57-OPEB Measurements by Agent Employers

12

7/11/2016

7

13

14

7/11/2016

8

15

16

7/11/2016

9

17

18

promise to forgo tax

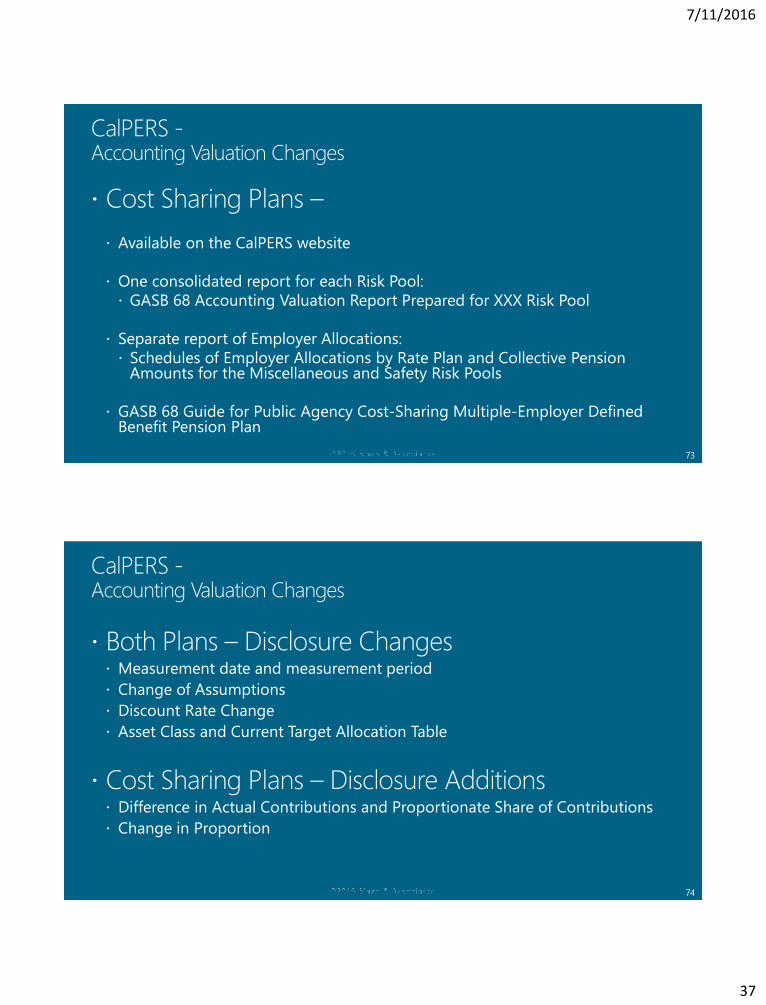

specificaction

7/11/2016

10

19

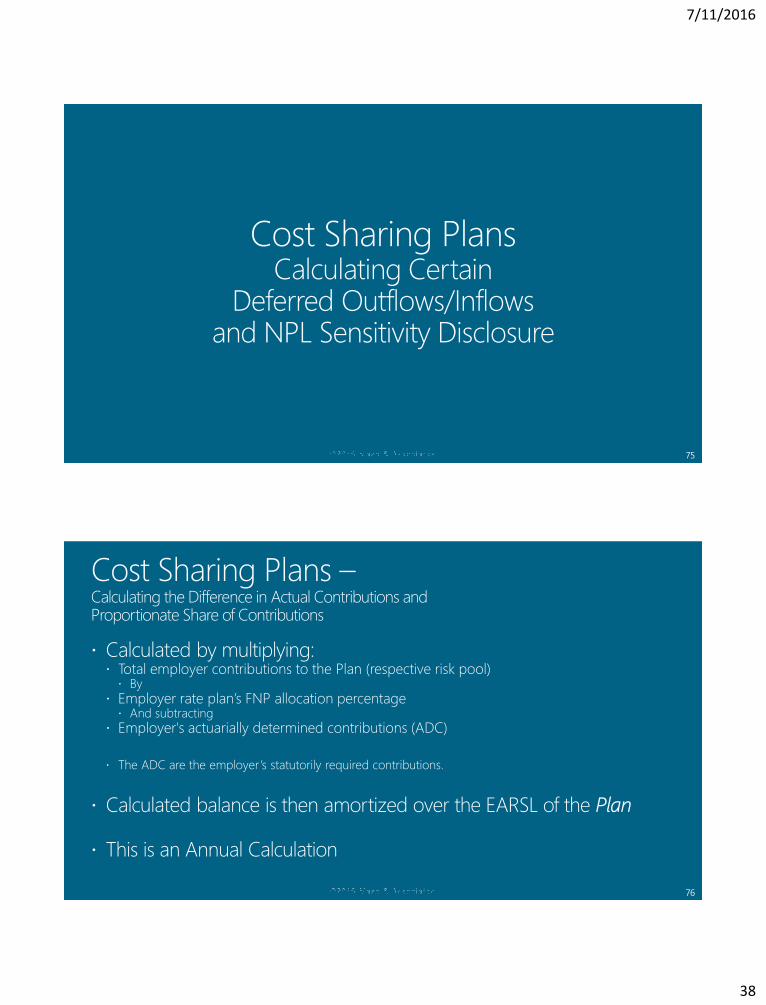

• Distinguish between government’s OWN agreements and agreements by OTHER GOVERNMENTS that affect the reporting entity

• Can be individually disclosed or aggregated

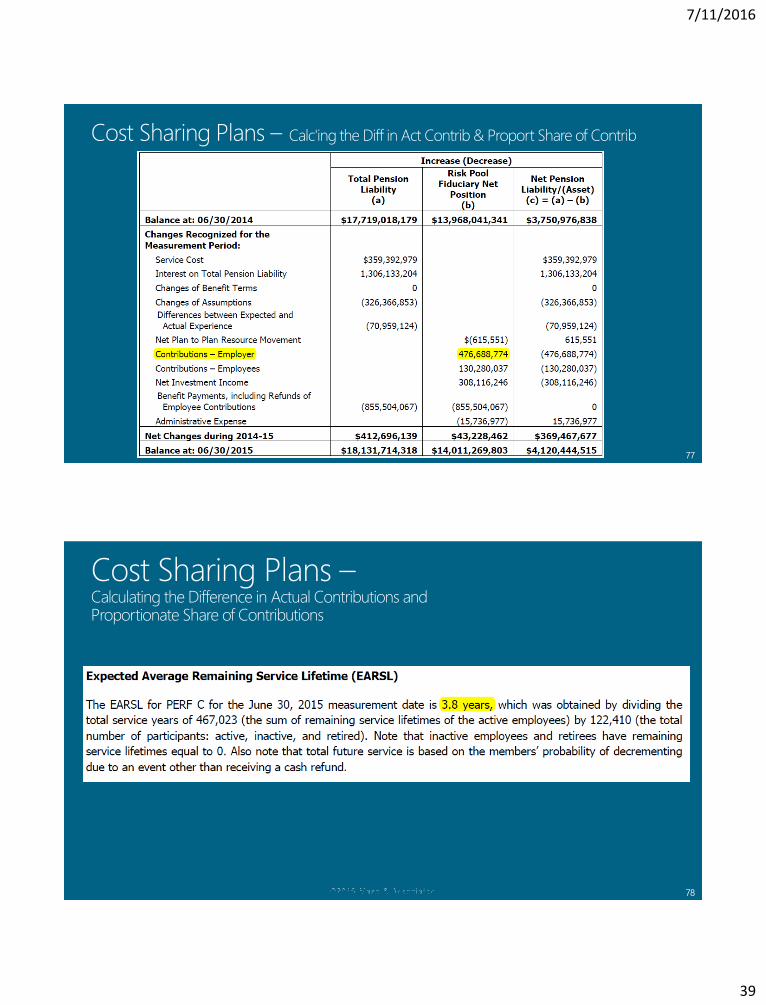

• Organized by abatement type or program (e.g. income tax vs. property tax incentive)

• Disclosures required from the date of agreement and should continue through the abatement expiration date.

Effective date: years ending June 30, 2017

20

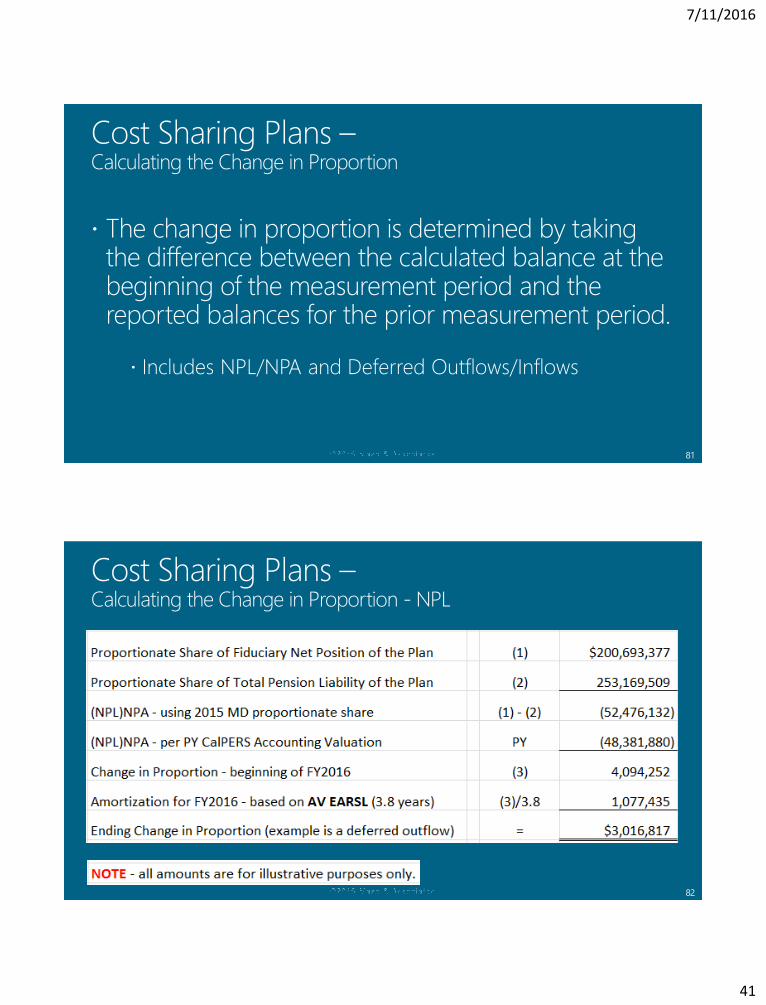

Description of Disclosure Government's Own

Imposed by other

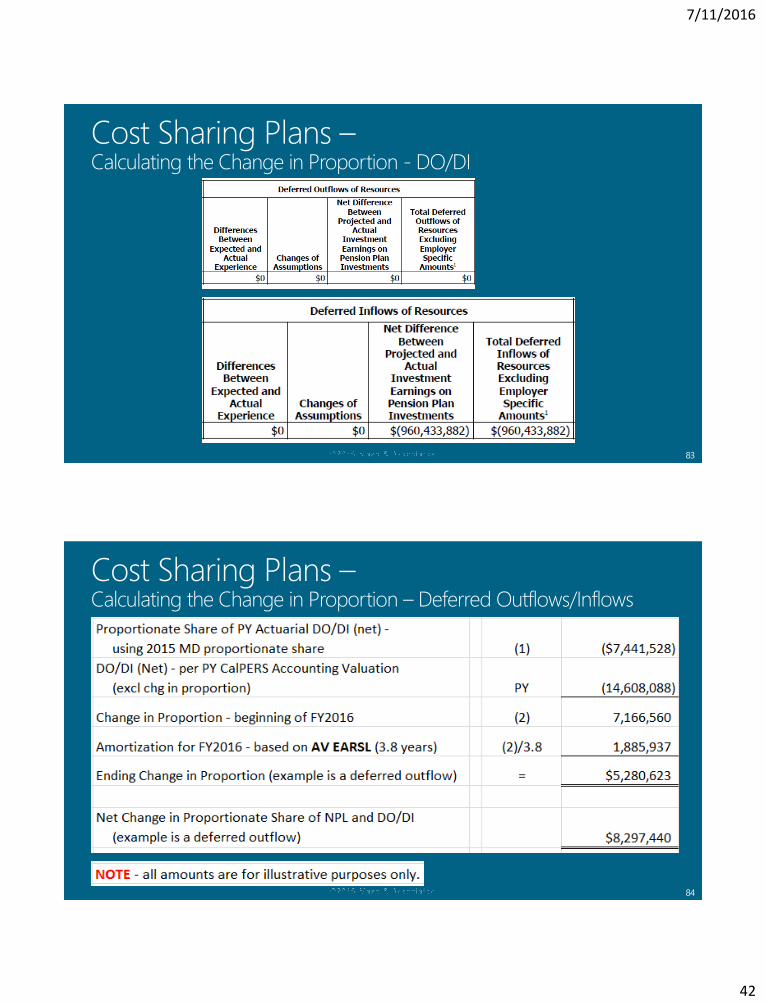

Government

Name of program <

Purpose of program <

Name of government <

Type of tax being abated < <

Dollar amount of taxes abated < <

Authority of abate taxes <

Eligibility criteria <

Abatement mechanism <

Recapture clause, if any <

Type of recipient commitments <

Any received/receivable from other governments < <

Other commitments by government <

Quantitative threshold for individual disclosure < <

7/11/2016

11

21

aturity

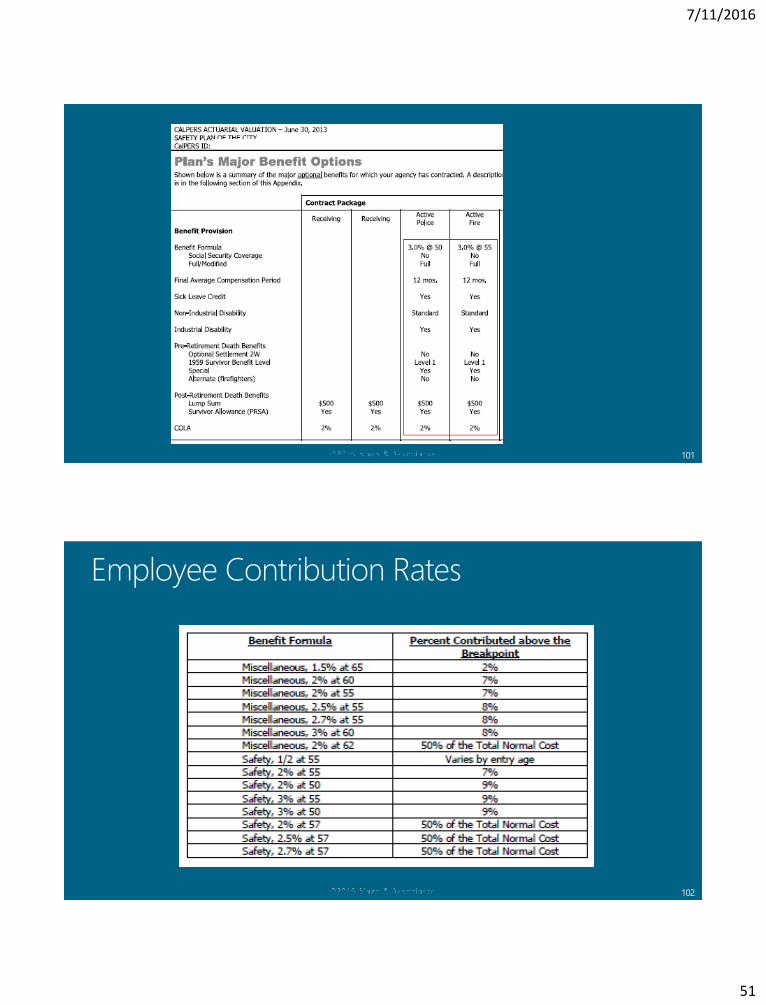

• Diversification

• Shadow pricing

22

Diversification No more than 5% of portfolio in one issuer

Excludes US Treasury, certain Agency Securities and CDs

Includes securities underlying repurchase agreements

7/11/2016

12

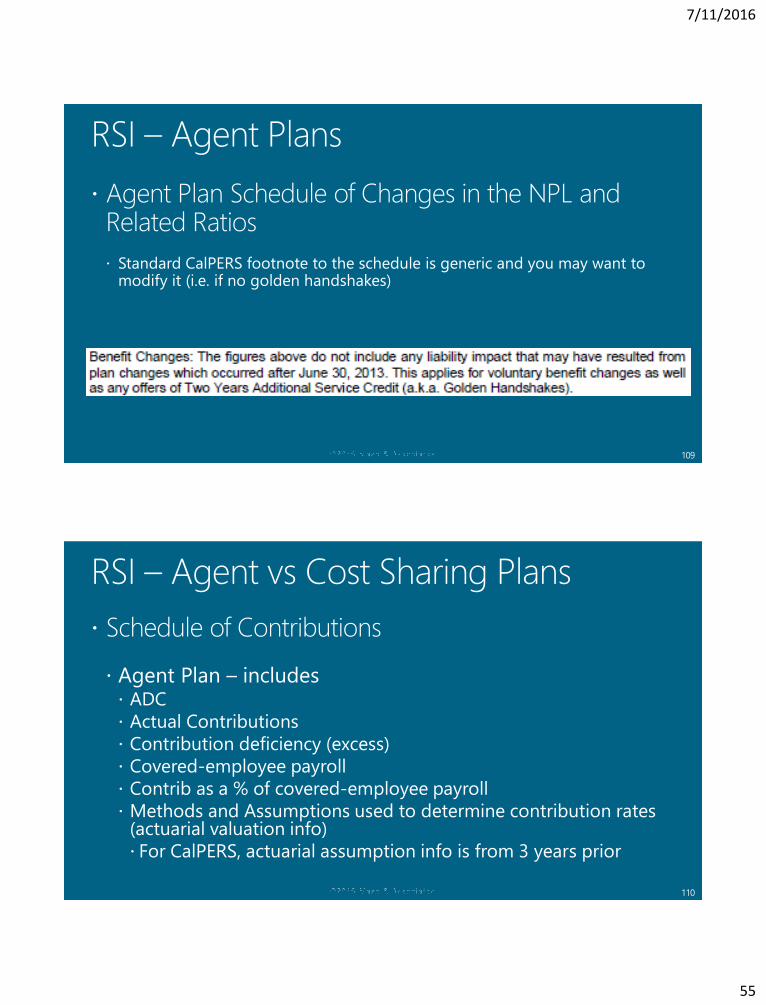

23

24

Effective date: years ending June 30, 2016 or June 30, 2017 (certain exceptions for pools regarding portfolio quality, custodial credit risk and shadow pricing)

7/11/2016

13

25

Effective date: years ending June 30, 2017

26

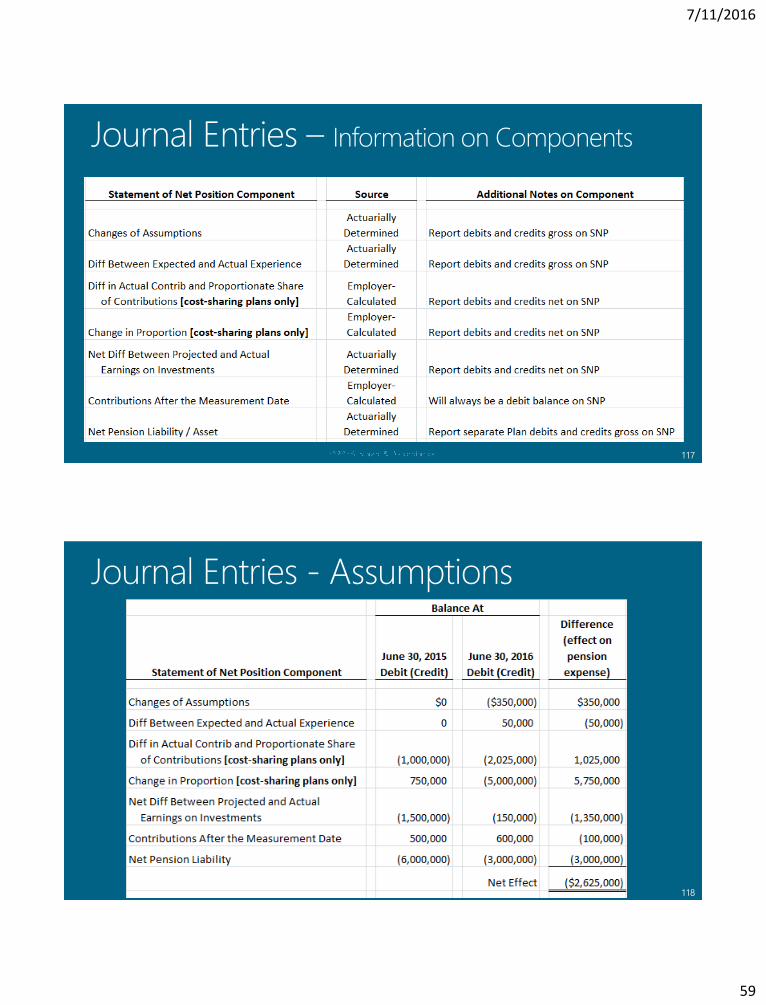

7/11/2016

14

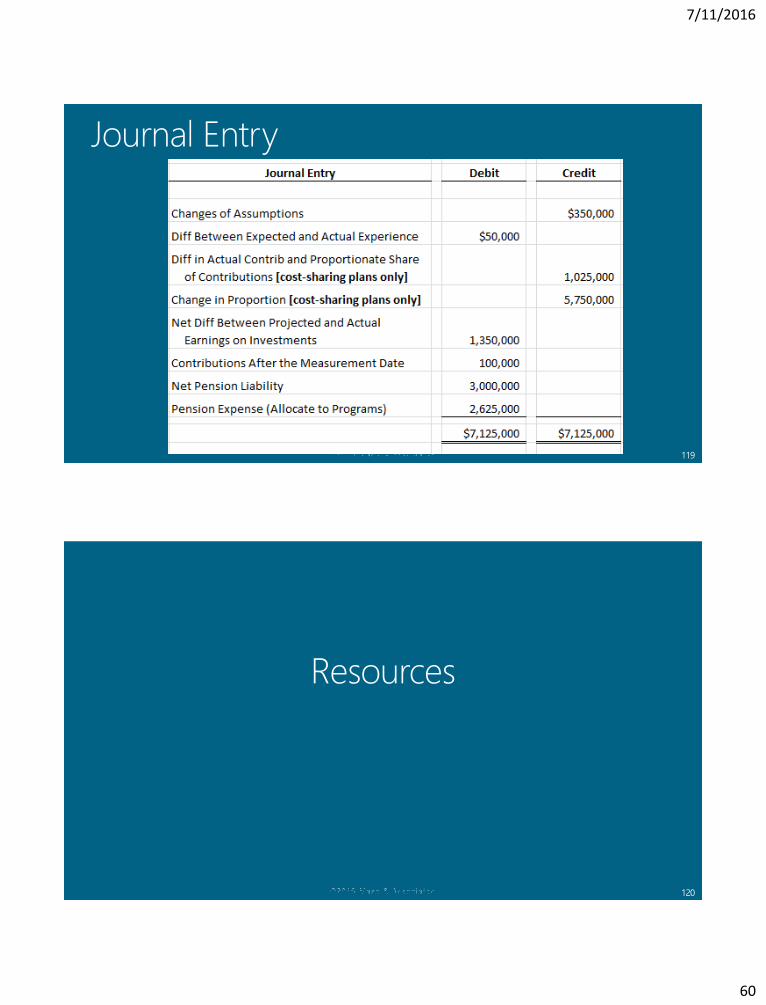

27

28

7/11/2016

16

31

32

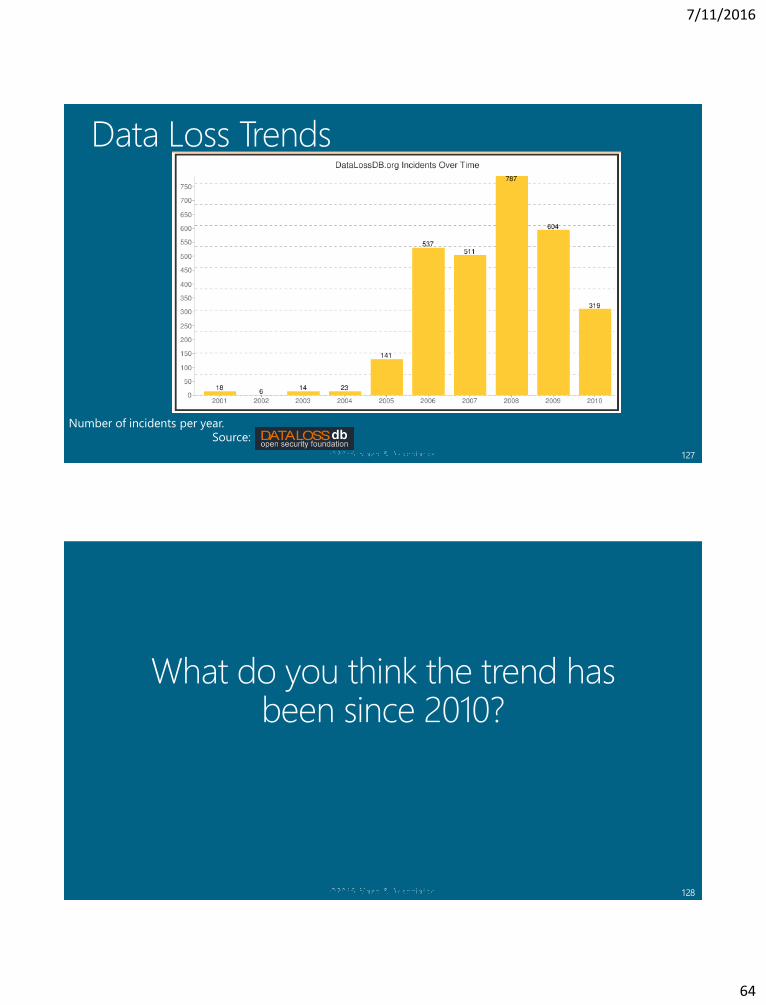

7/11/2016

17

33

34

7/11/2016

18

35

36

7/11/2016

19

37

38

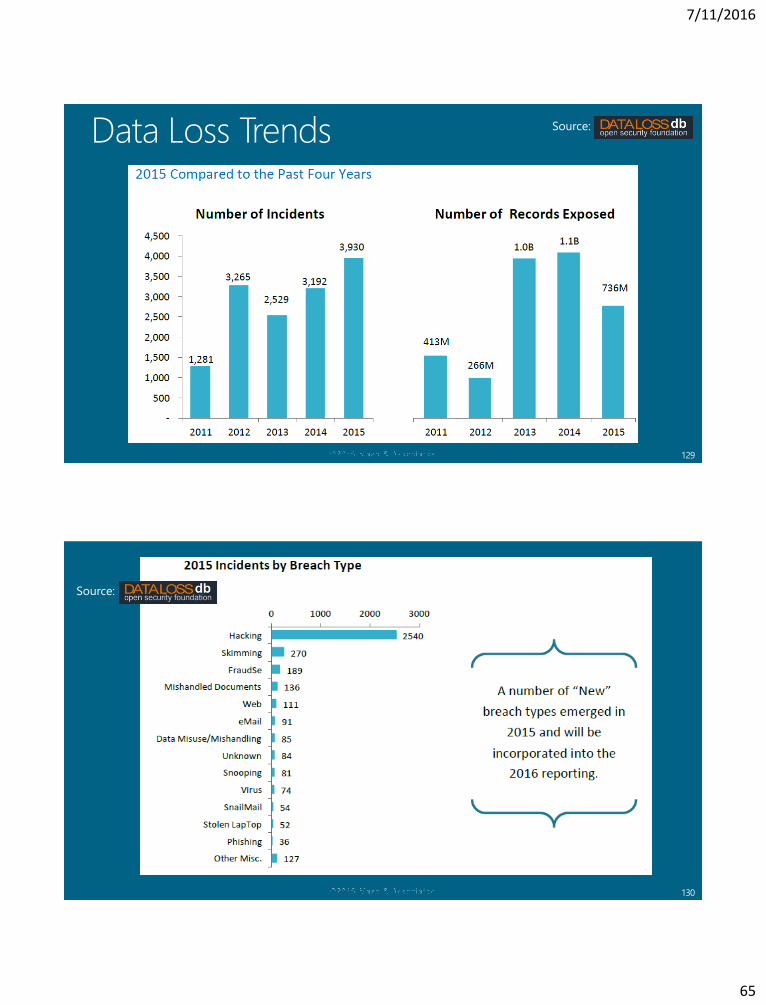

7/11/2016

20

39

40

7/11/2016

21

41

42

Entry Price

7/11/2016

22

43

44

7/11/2016

23

45

46

7/11/2016

24

47

48

7/11/2016

25

49

50

7/11/2016

26

51

52

7/11/2016

27

53

54

7/11/2016

28

55

56

7/11/2016

29

57

58

7/11/2016

30

59

60

7/11/2016

31

61

62

http://www.gasb.org/jsp/GASB/Page/GASBSectionPage&cid=1176160042391

http://gasb.org/cs/ContentServer?c=Document_C&pagename=GASB%2FDocument_C%2FGASBDocumentPage&cid=1176165839556

7/11/2016

32

63

64

7/11/2016

33

65

66

7/11/2016

34

67

68

7/11/2016

35

69

70

7/11/2016

36

71

Changes to the Accounting Valuations

72

7/11/2016

37

73

74

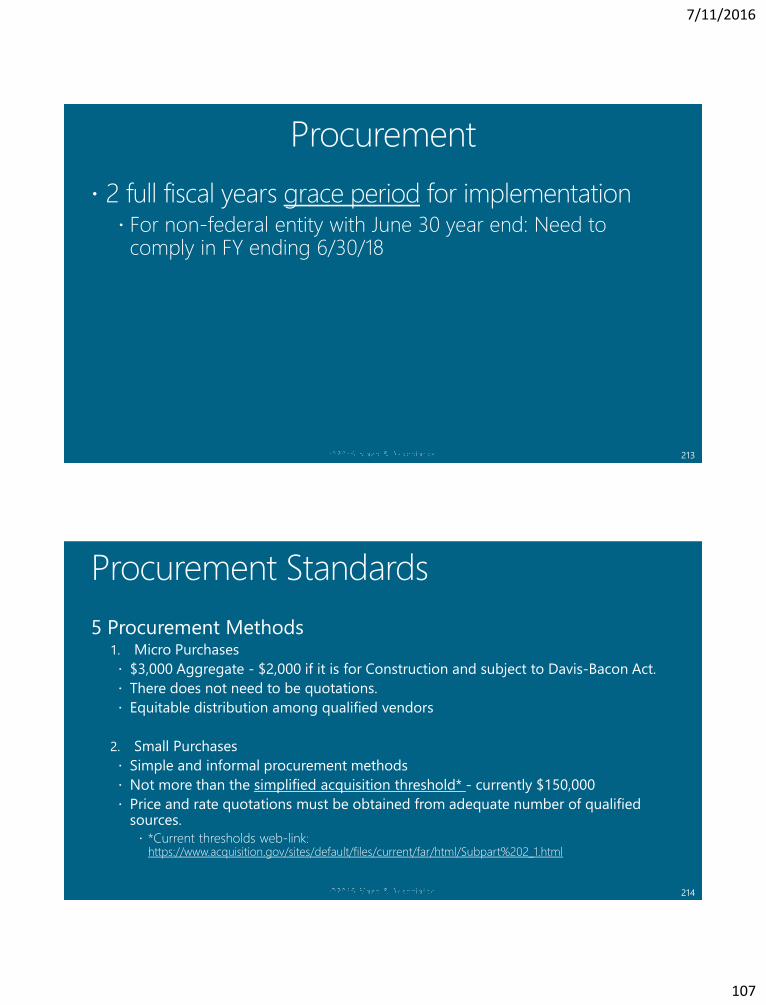

7/11/2016

38

75

Calculating CertainDeferred Outflows/Inflows

and NPL Sensitivity Disclosure

76

7/11/2016

39

77

78

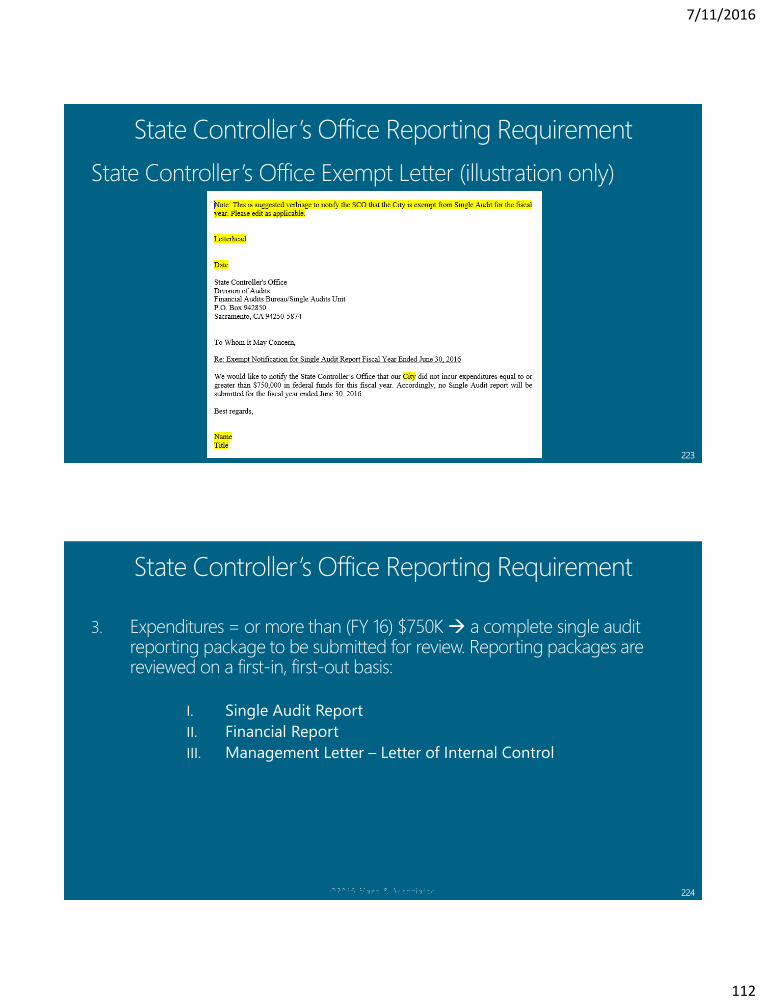

7/11/2016

40

79

80

7/11/2016

41

81

82

7/11/2016

42

83

84

7/11/2016

43

85

86

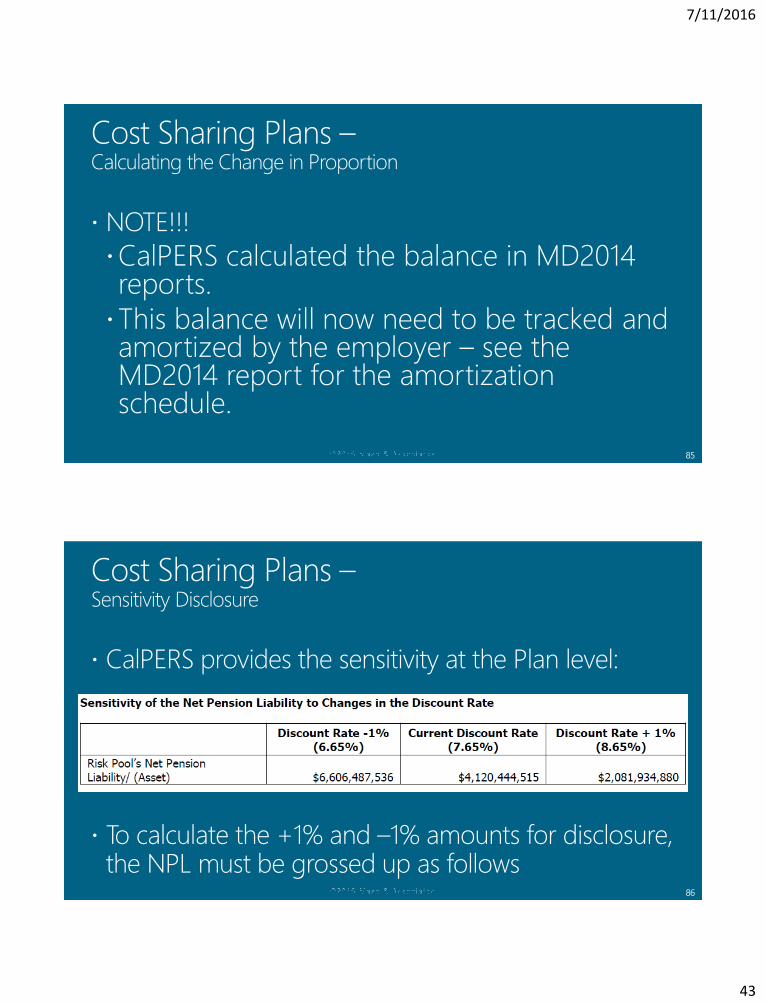

Sensitivity Disclosure

To calculate the +1% and –1% amounts for disclosure, the NPL must be grossed up as follows

7/11/2016

44

87

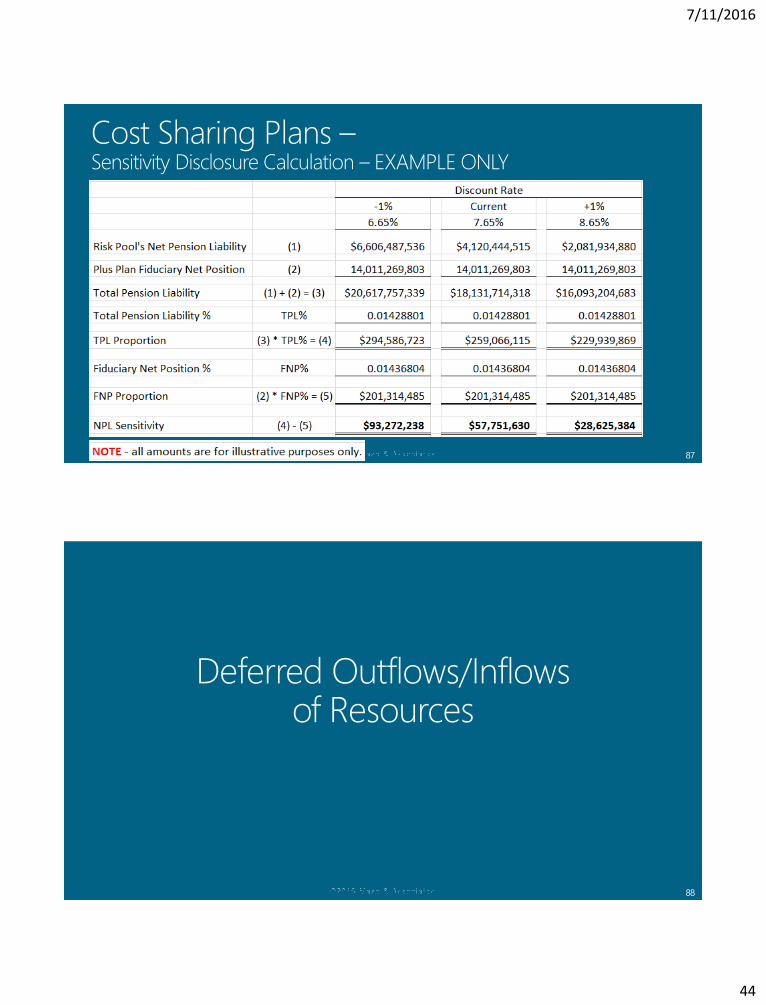

Sensitivity Disclosure Calculation – EXAMPLE ONLY

88

7/11/2016

45

89

90

7/11/2016

46

91

92

7/11/2016

47

93

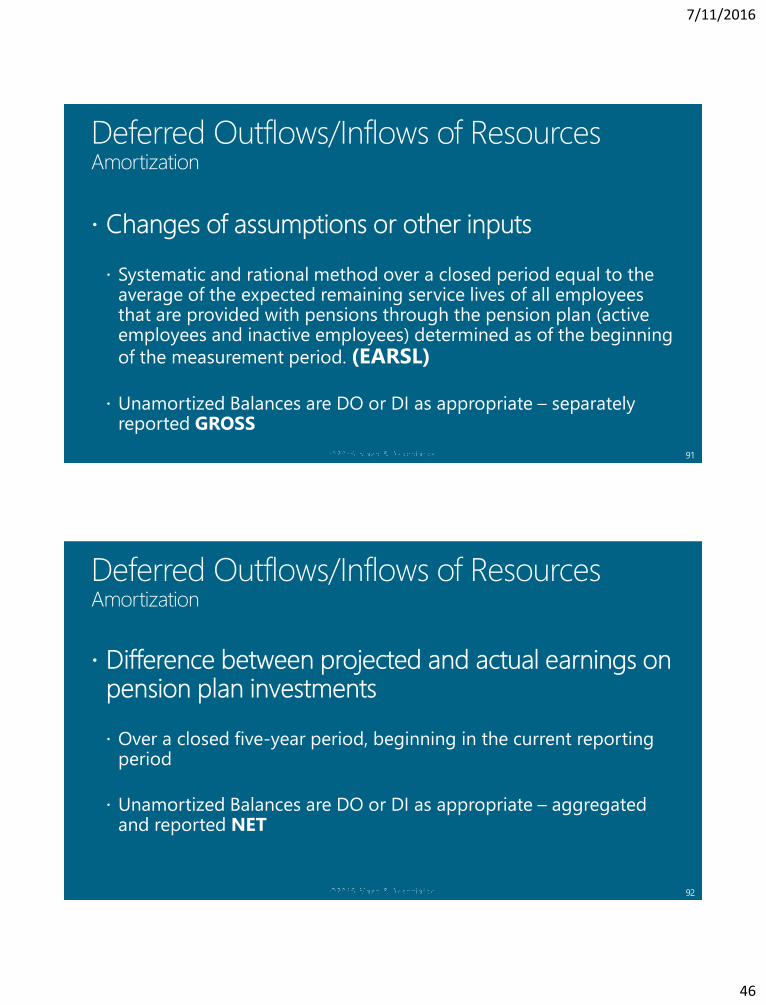

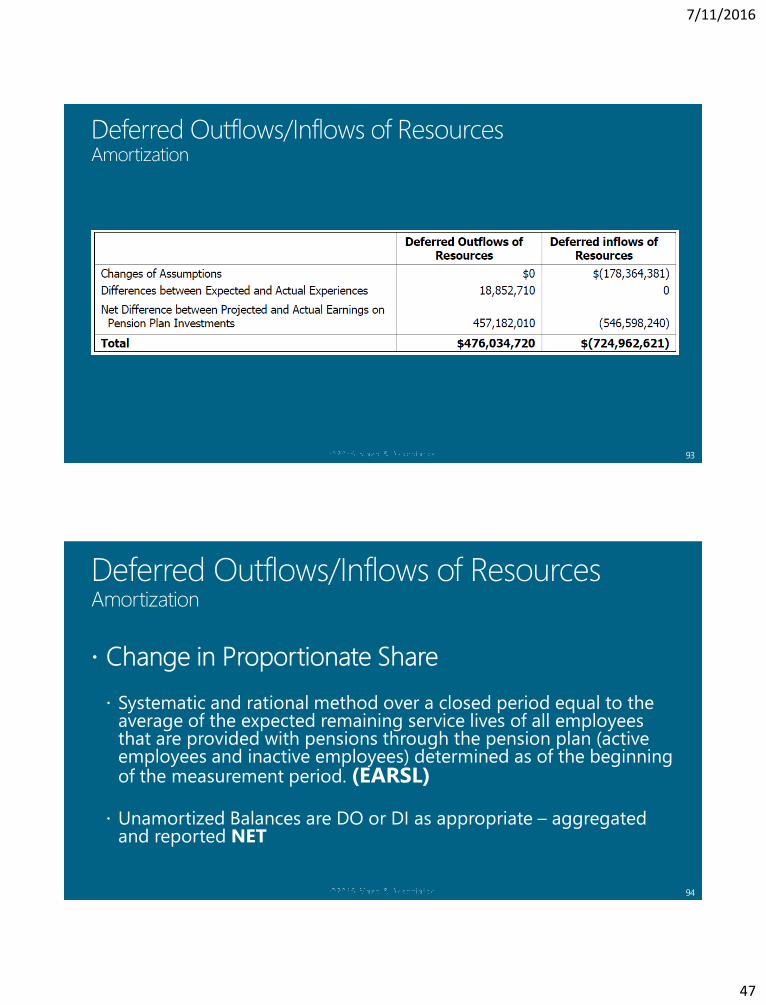

Deferred Outflows/Inflows of ResourcesAmortization

94

(EARSL)

7/11/2016

48

95

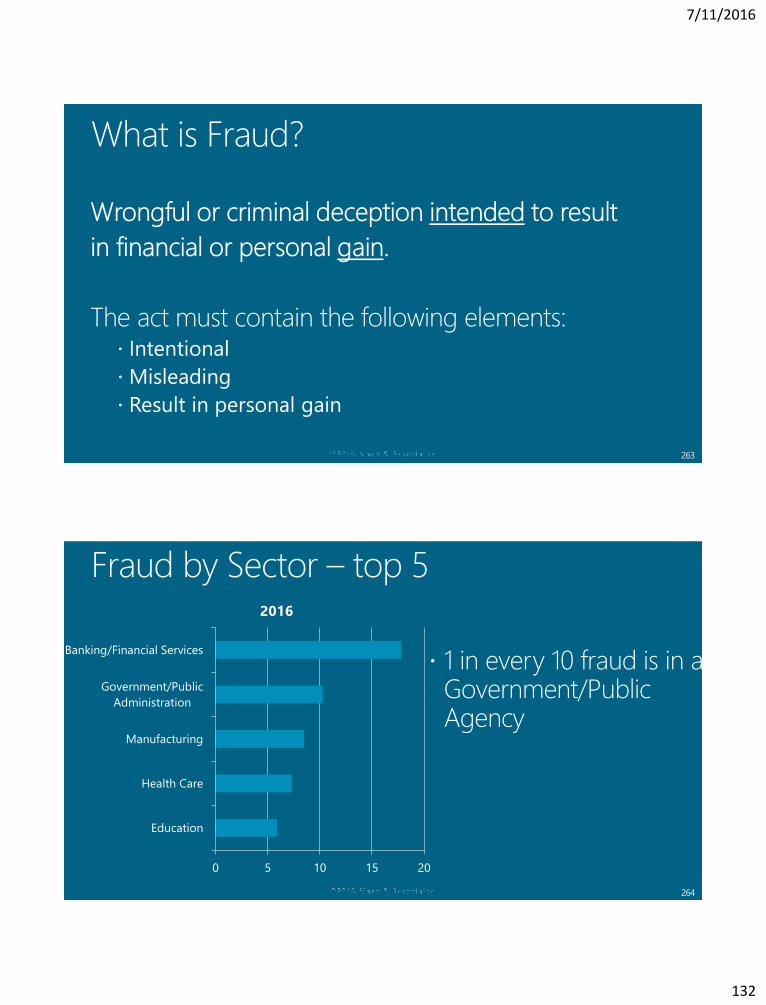

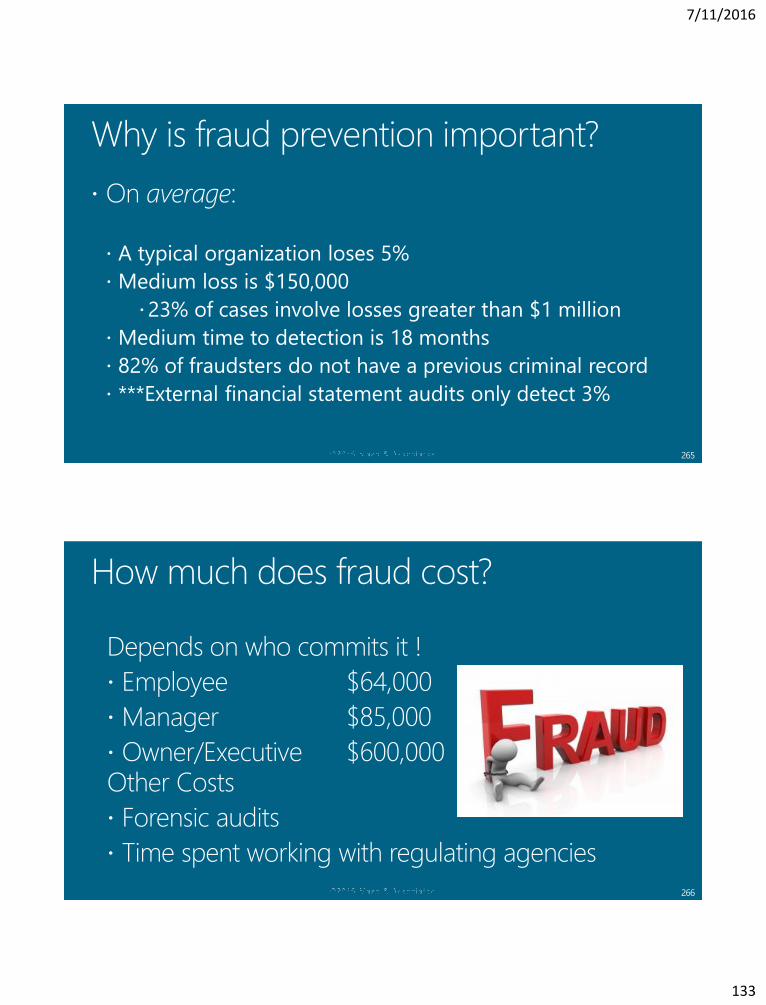

Proportionate Share of Contributions

96

Disclosure Sources

7/11/2016

49

97

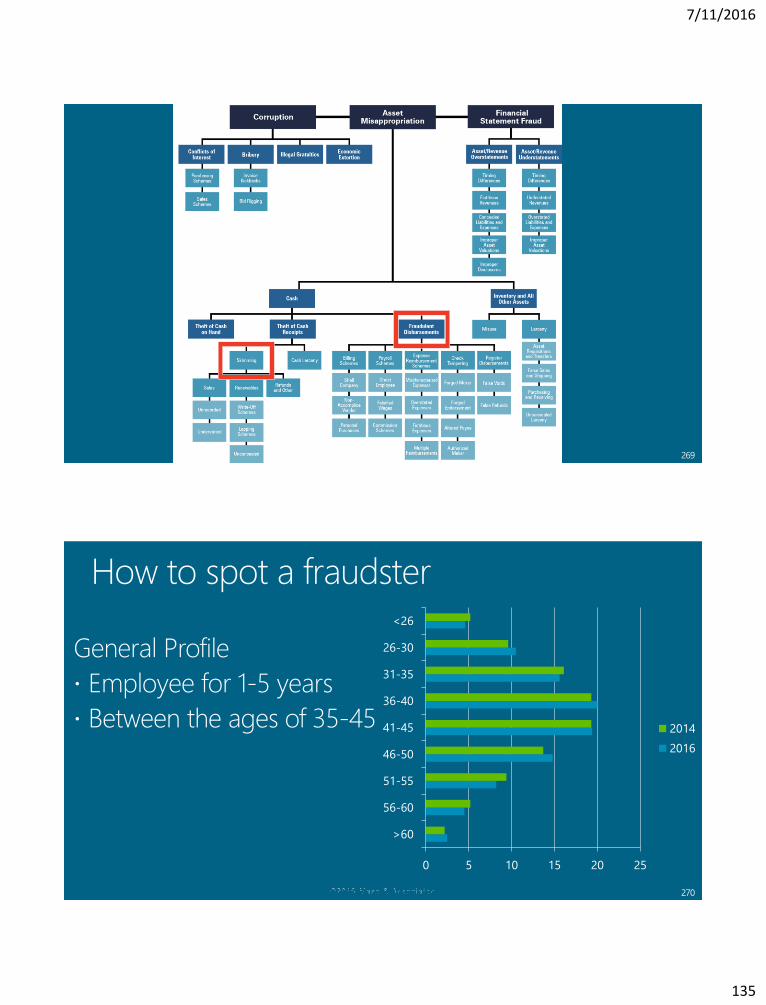

98

7/11/2016

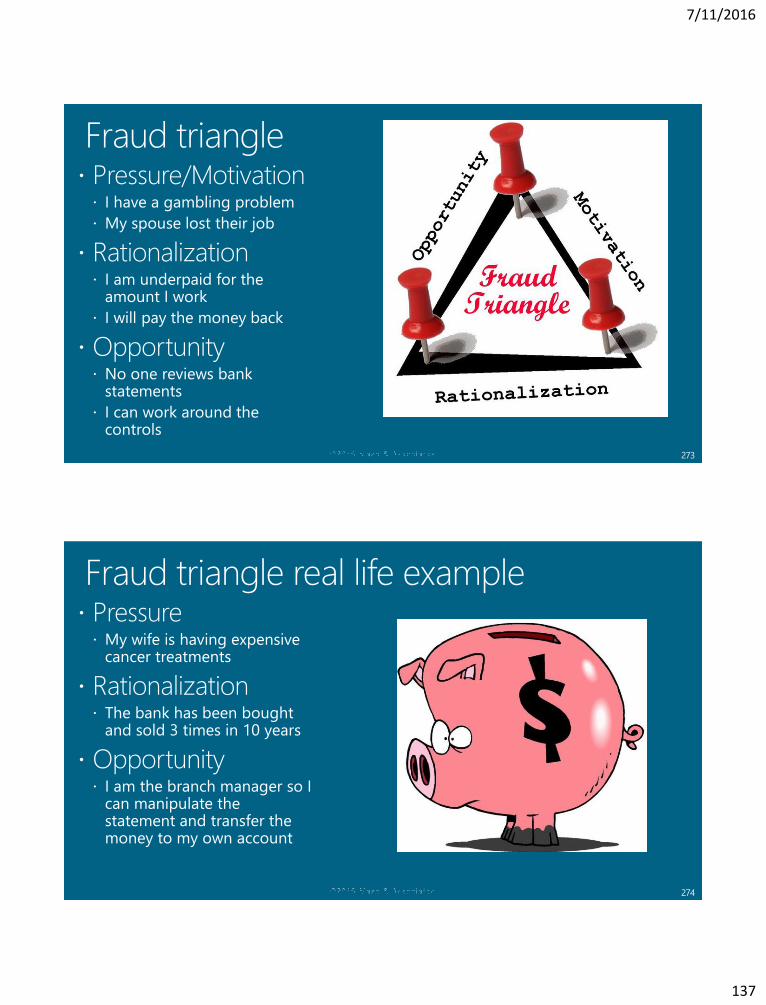

50

99

100

7/11/2016

51

101

102

7/11/2016

52

103

Clarifications

104

7/11/2016

53

105

106

7/11/2016

54

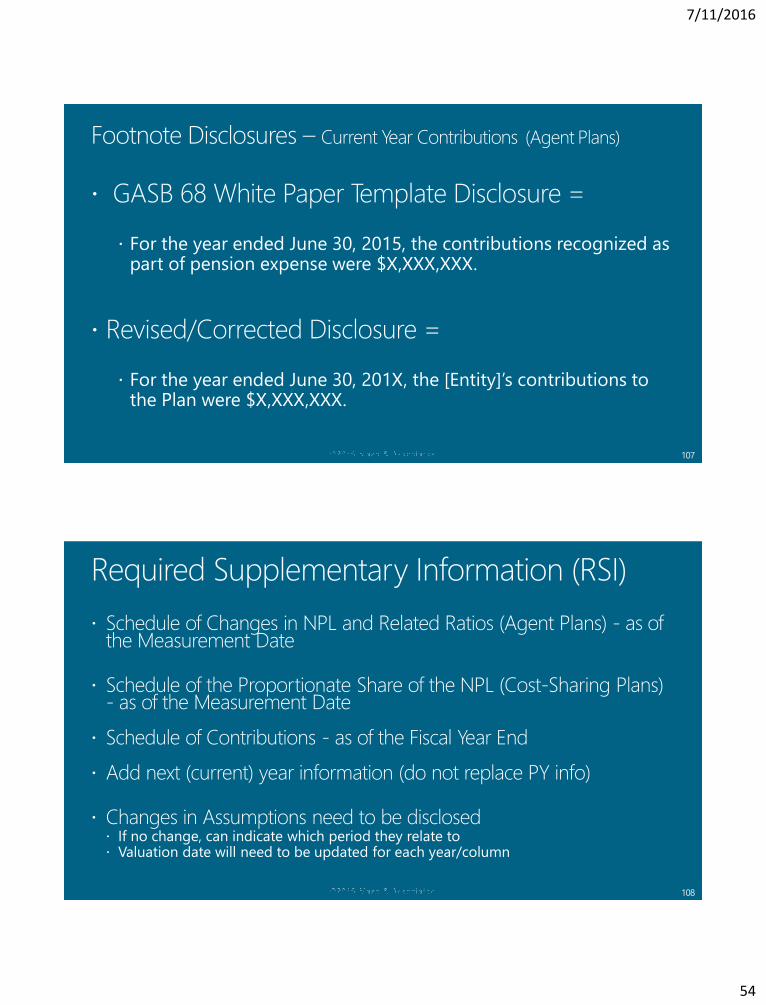

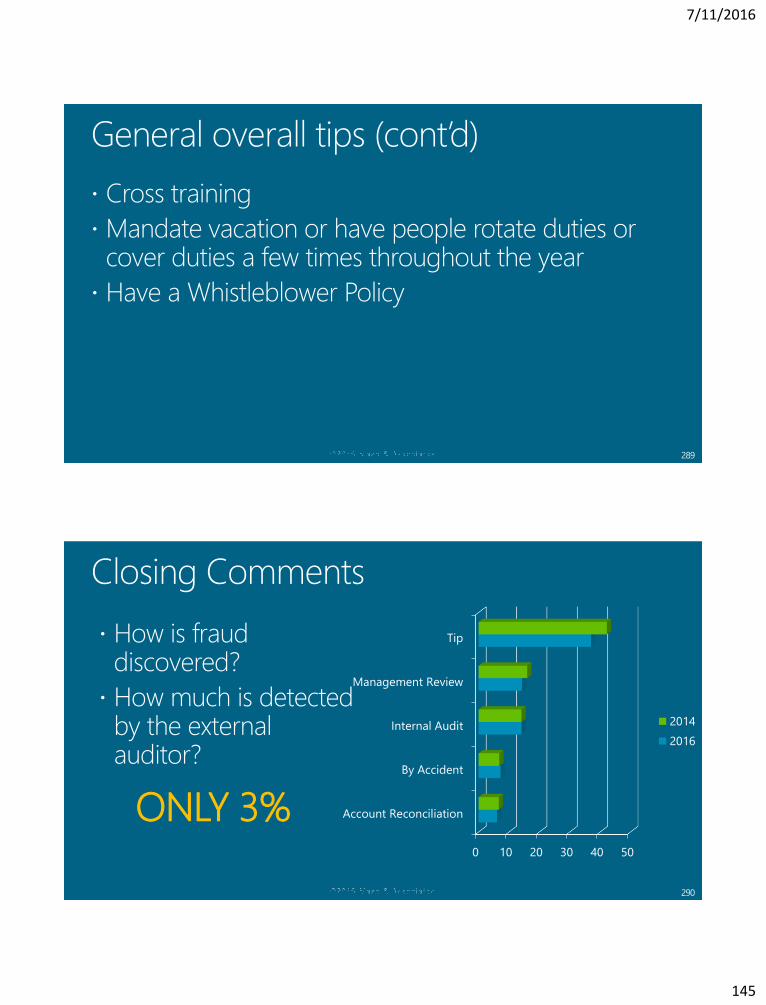

107

108

7/11/2016

55

109

110

7/11/2016

56

111

112

CEP = The total payroll of employees that are provided with pensions through the pension plan, including pensionable and non-pensionable amounts.

7/11/2016

57

113

114

7/11/2016

58

115

116

7/11/2016

59

117

118

7/11/2016

60

119

120

7/11/2016

61

121

http://www.gasb.org/jsp/GASB/Page/GASBSectionPage&cid=1176160042391#gasbs75

https://www.calpers.ca.gov/page/employers/actuarial-services/gasb

122

https://www.calpers.ca.gov/docs/gasb-68-cost-sharing-guide.pdf

CCMA White Paper – Implementing GASB No. 68 Accounting and Financial Reporting for Pensions: http://www.calcpa.org/members/technical-resources/gaa-white-papers

7/11/2016

62

123

124

7/11/2016

63

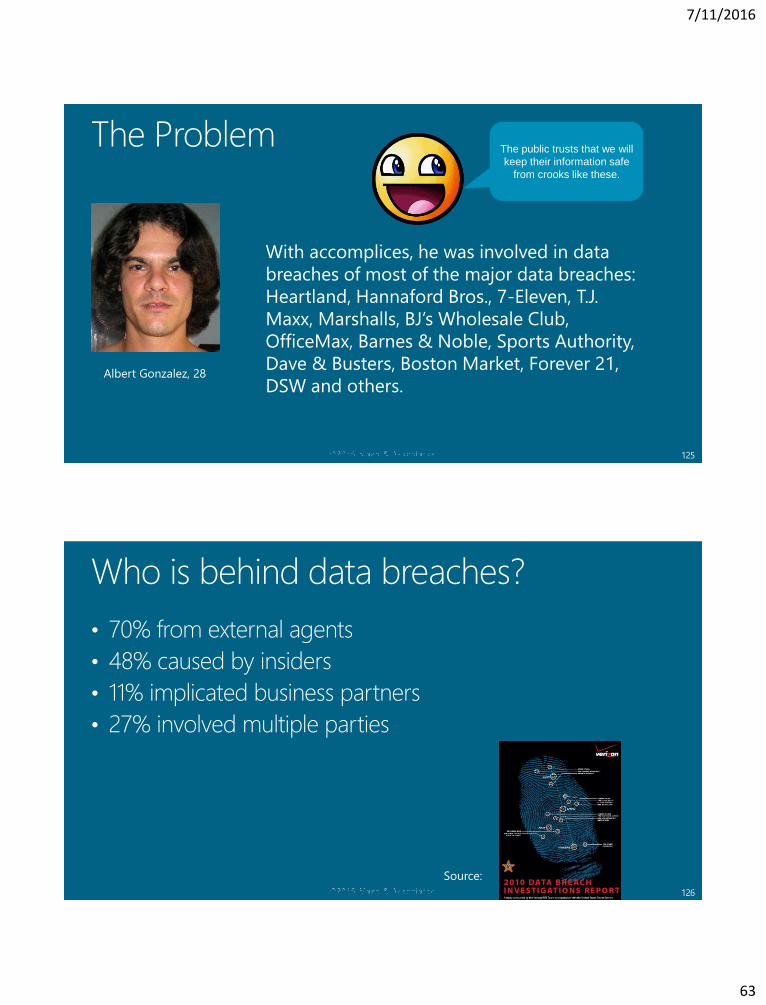

125

Albert Gonzalez, 28

With accomplices, he was involved in data

breaches of most of the major data breaches:

Heartland, Hannaford Bros., 7-Eleven, T.J.

Maxx, Marshalls, BJ’s Wholesale Club,

OfficeMax, Barnes & Noble, Sports Authority,

Dave & Busters, Boston Market, Forever 21,

DSW and others.

The public trusts that we will

keep their information safe

from crooks like these.

126

Source:

7/11/2016

69

137

1. Securing the IT environment

2. Managing and retaining data

3. Managing IT risk and compliance

4. Ensuring privacy

6. Managing System Implementations

7. Preventing and responding to computer fraud

10. Managing vendors and service providers

http://www.aicpa.org/InterestAreas/InformationTechnology/Resources/TopTechnologyInitiatives/Pages/2013TTI.aspx

Orange text are all

PCI related

138

7/11/2016

70

139

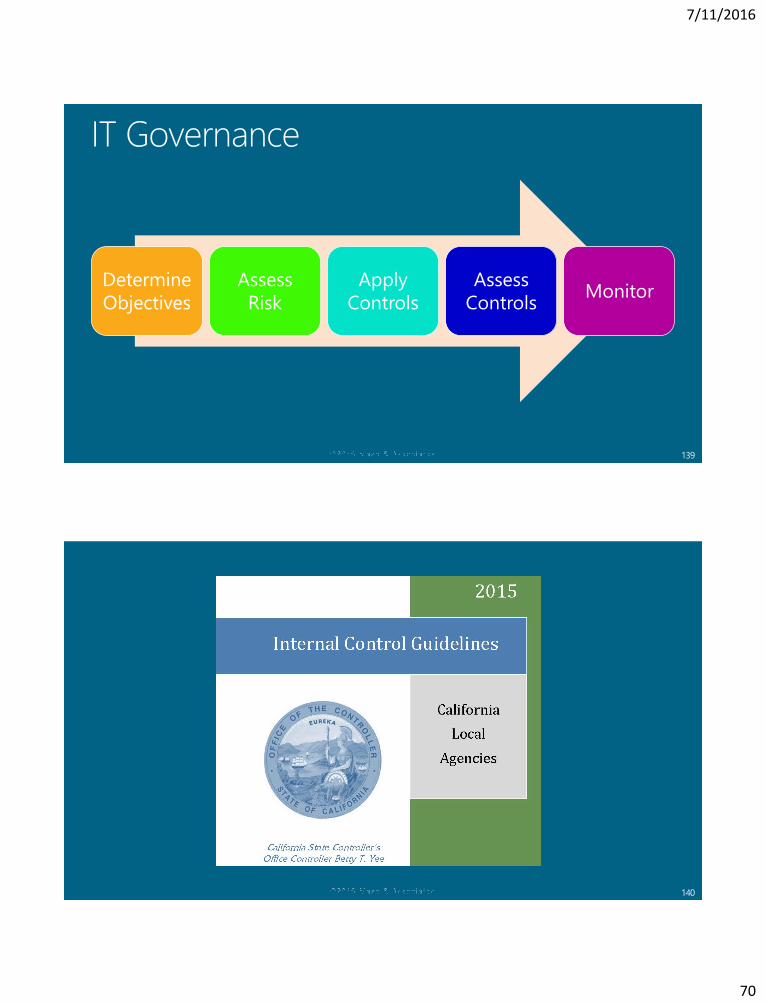

Determine

Objectives

Assess

Risk

Apply

Controls

Assess

ControlsMonitor

140

7/11/2016

71

141Source: Internal Control Guidelines California Local Agencies 2015 SCO

142

Source: AICPA’s Auditing Standard AU-C §315.A91

7/11/2016

72

143

144

7/11/2016

73

145

146

7/11/2016

74

147

utility model

148

7/11/2016

75

149

150

Efficiency

Agility

Innovation

7/11/2016

76

151

152

7/11/2016

77

153

154

7/11/2016

78

155

156

7/11/2016

79

157

158

7/11/2016

80

159

160

7/11/2016

81

161

162

7/11/2016

82

163

164

7/11/2016

83

165

166

7/11/2016

84

167

168

7/11/2016

85

169

170

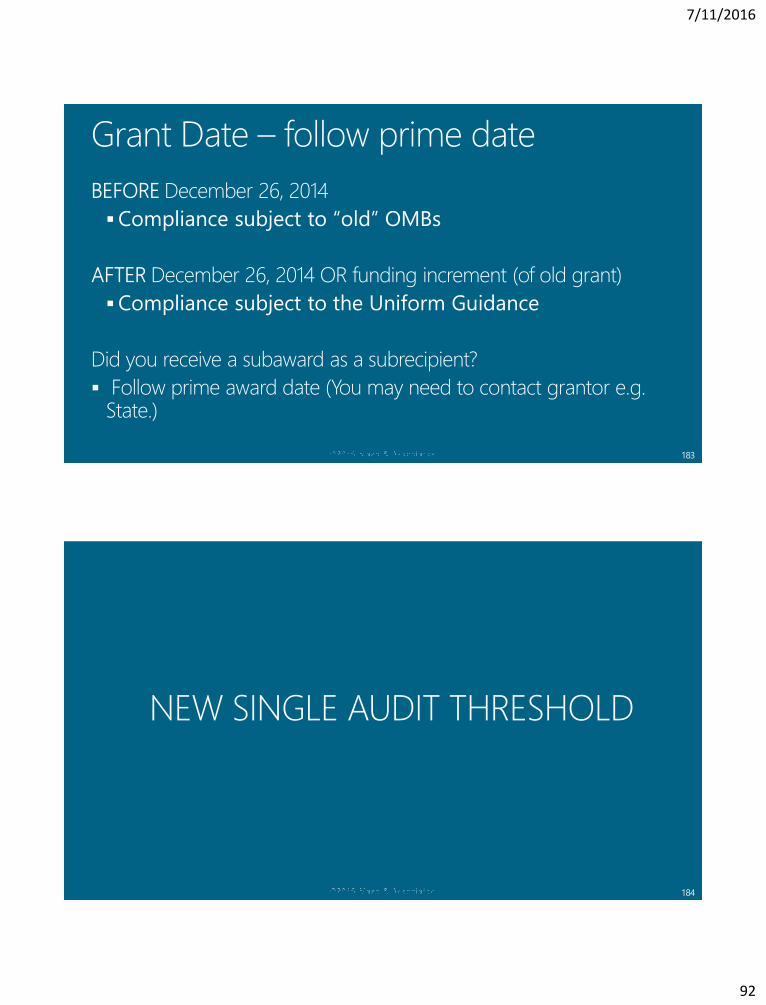

Uniform Guidance

New Single Audit Threshold

Grant Agreement Dates

Type A/B Threshold

2016 Compliance Supplement

Internal Control

Indirect Costs

Subrecipient Monitoring Documentation

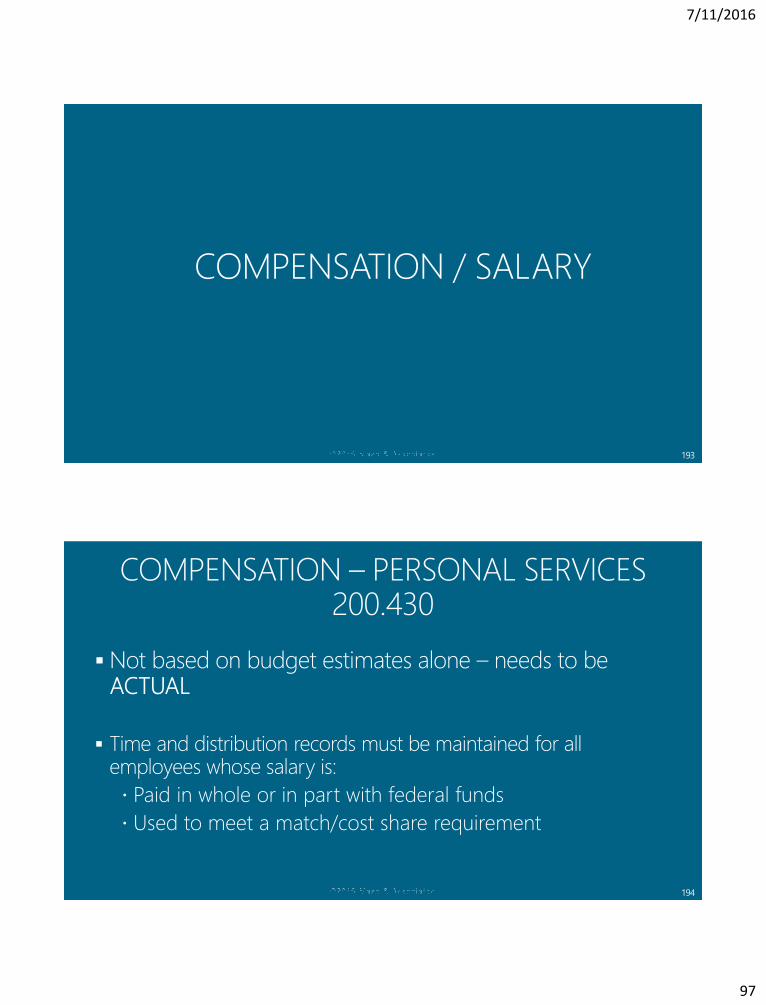

Compensation/salary

7/11/2016

86

171

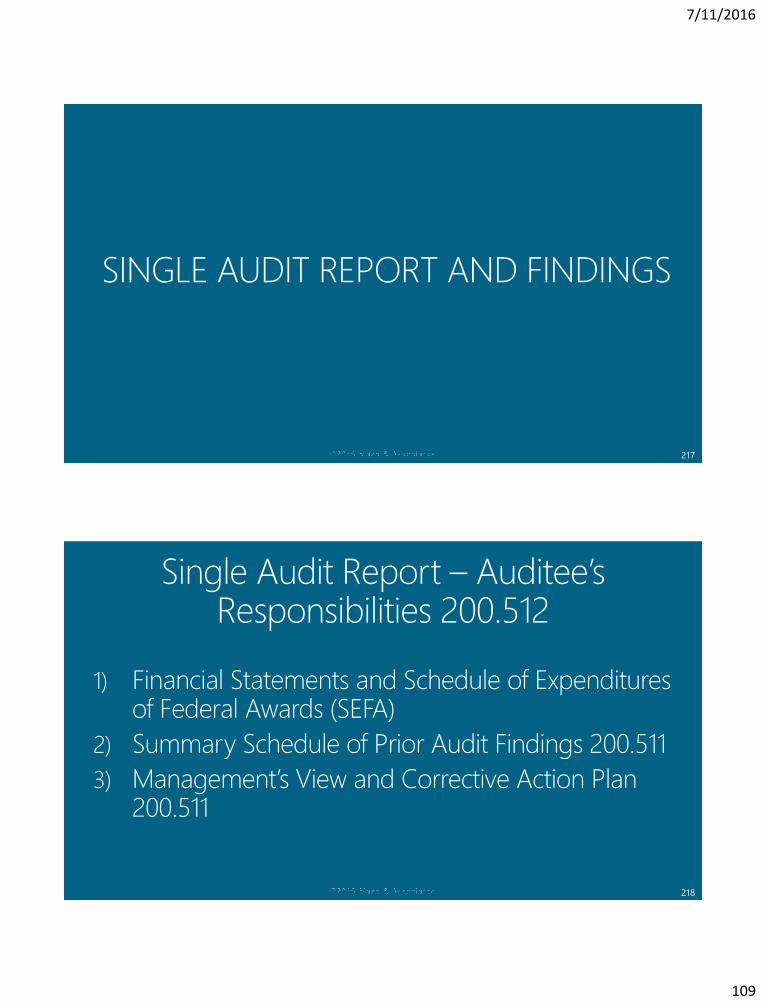

Procurement Standard

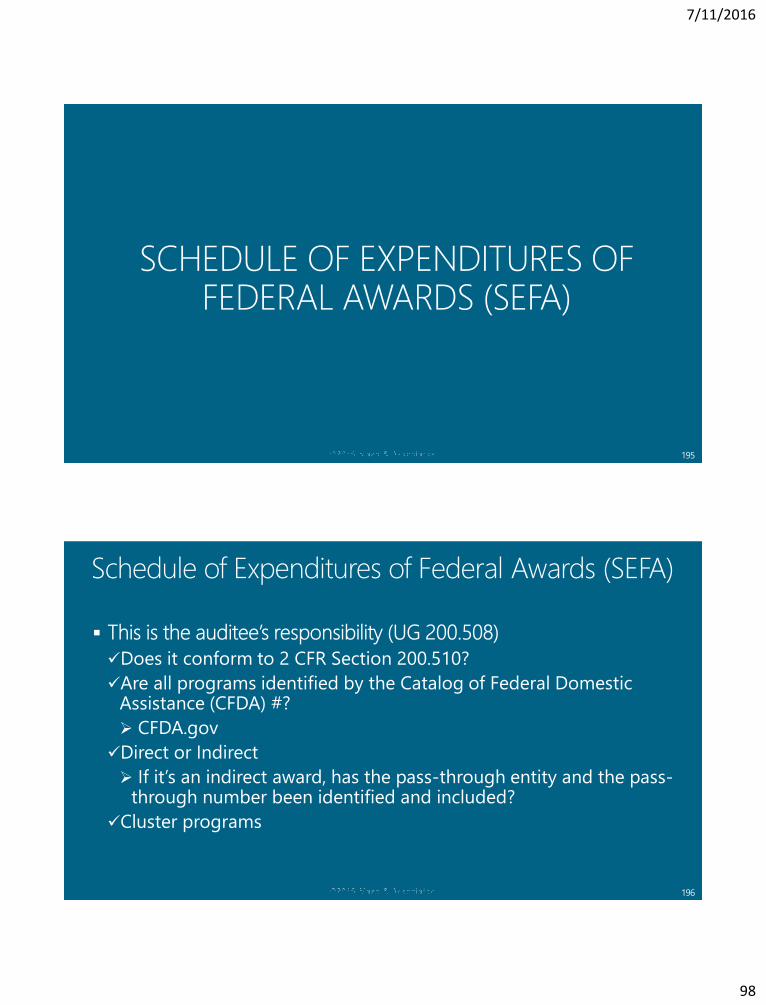

Schedule of Expenditures of Federal Awards (SEFA) – auditee responsibilities

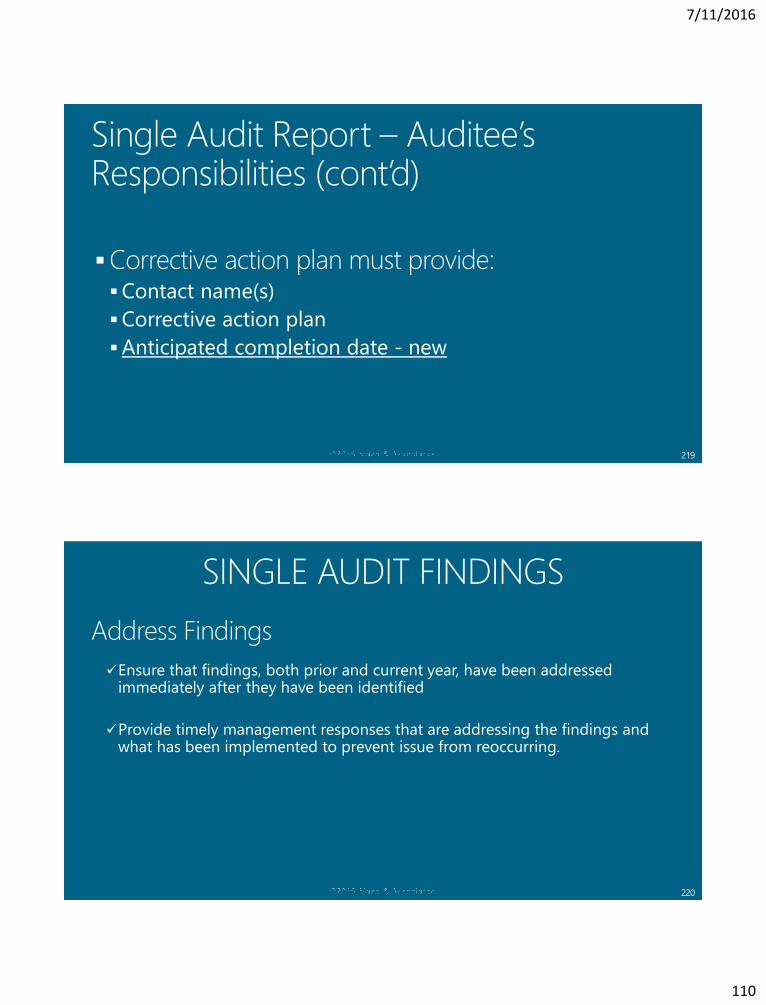

Addressing findings – auditee responsibilities - both current and prior year

Data Collection Form

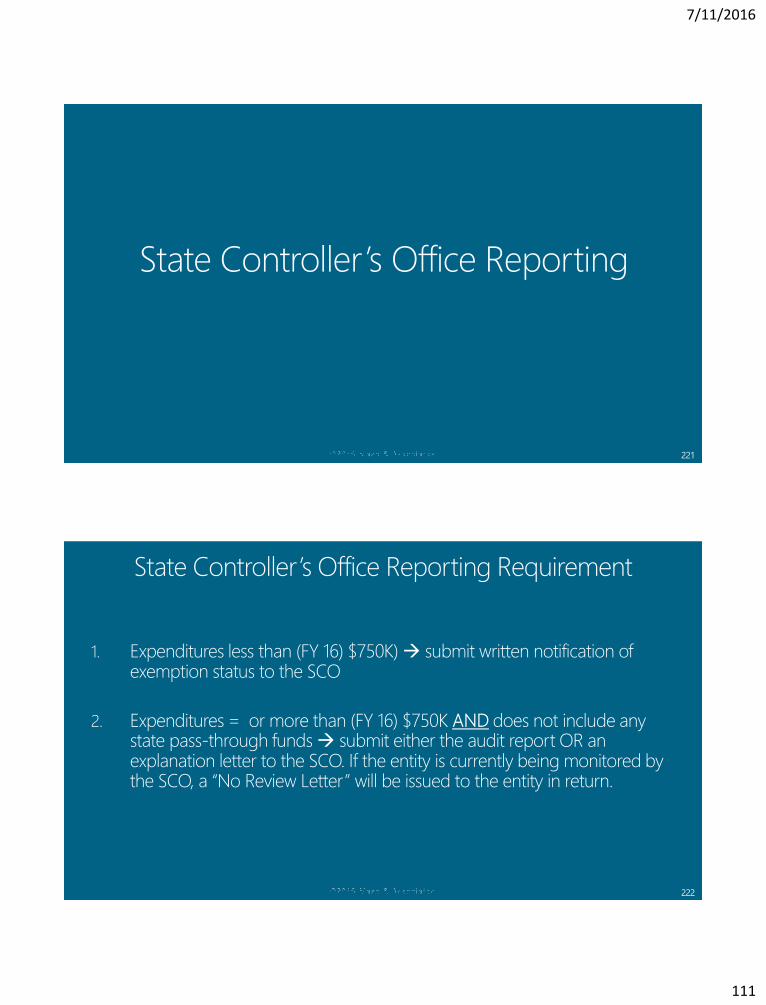

State Controller’s Office Reporting Package

172

7/11/2016

87

173

Web-link: Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards at 2 CFR 200 (UG or Uniform Guidance)

174

7/11/2016

88

175

176

White House OMB Compliance Supplement.

7/11/2016

89

177

178

Tip: As an auditee, utilize this document to obtain a goal of an unqualified report with no findings on compliance.

7/11/2016

90

179

180

7/11/2016

91

181

182

SOURCE: HTTP://WWW.ECFR.GOV/ AND SEARCH TITLE 2 CHAPTER II PART 200

PDF VERSION: HTTP://WWW.GPO.GOV/FDSYS/PKG/FR-2013-12-26/PDF/2013-30465.PDF

7/11/2016

92

183

184

7/11/2016

93

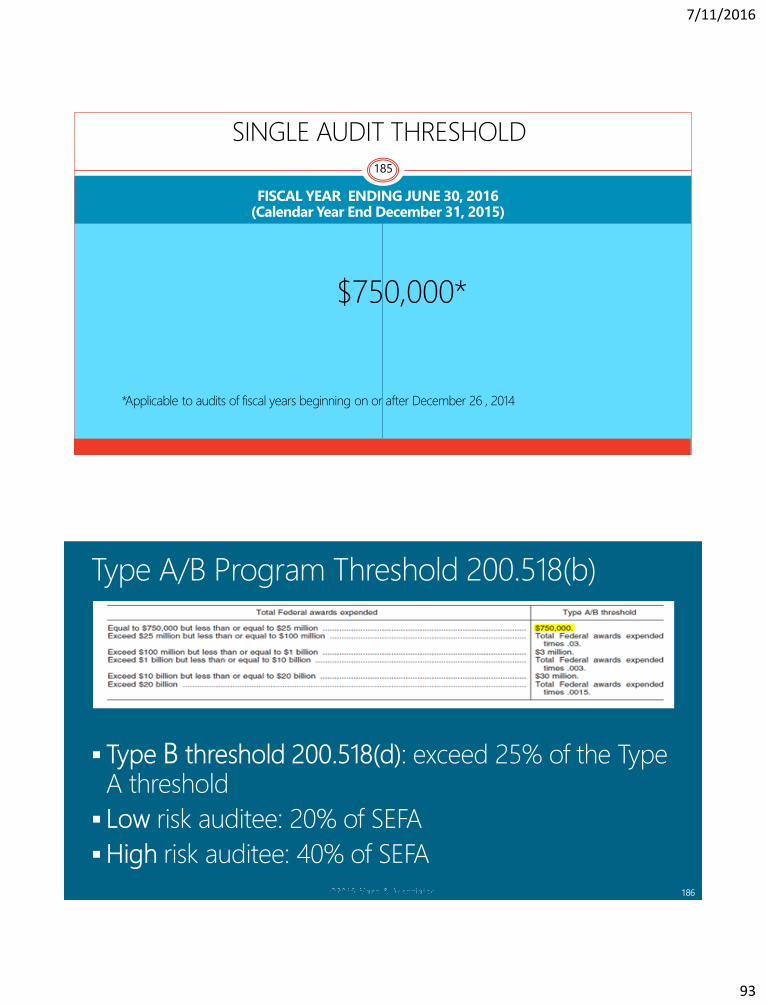

FISCAL YEAR ENDING JUNE 30, 2016 (Calendar Year End December 31, 2015)

185

186

7/11/2016

94

187

188

7/11/2016

95

189

190

7/11/2016

96

191

192

7/11/2016

97

193

194

7/11/2016

98

195

196

Schedule of Expenditures of Federal Awards (SEFA)

7/11/2016

99

197

Federal Grantor/Pass Through

Grantor/Program Title

Federal

CFDA

Number

Pass Through

Entity

Identifying

Number

Federal

Expenditures

Expenditures

to

Subrecipients

Department of Education Direct

Program – Title I Grants to Local

Educational Agencies 84.010 N/A $1,000,000 $800,000

198

7/11/2016

100

199

200

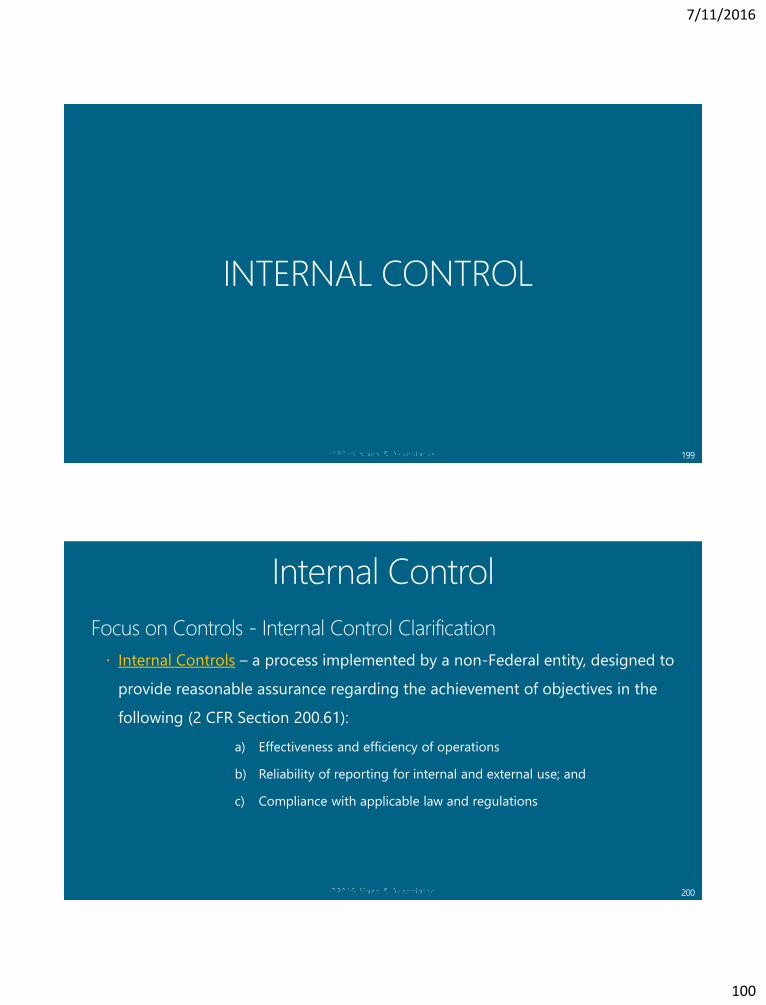

Internal Controls – a process implemented by a non-Federal entity, designed to

provide reasonable assurance regarding the achievement of objectives in the

following (2 CFR Section 200.61):

a) Effectiveness and efficiency of operations

b) Reliability of reporting for internal and external use; and

c) Compliance with applicable law and regulations

7/11/2016

101

201

202

7/11/2016

102

203

204

7/11/2016

103

205

(Tip – use this as checklist)

206

7/11/2016

104

207

208

7/11/2016

105

209

210

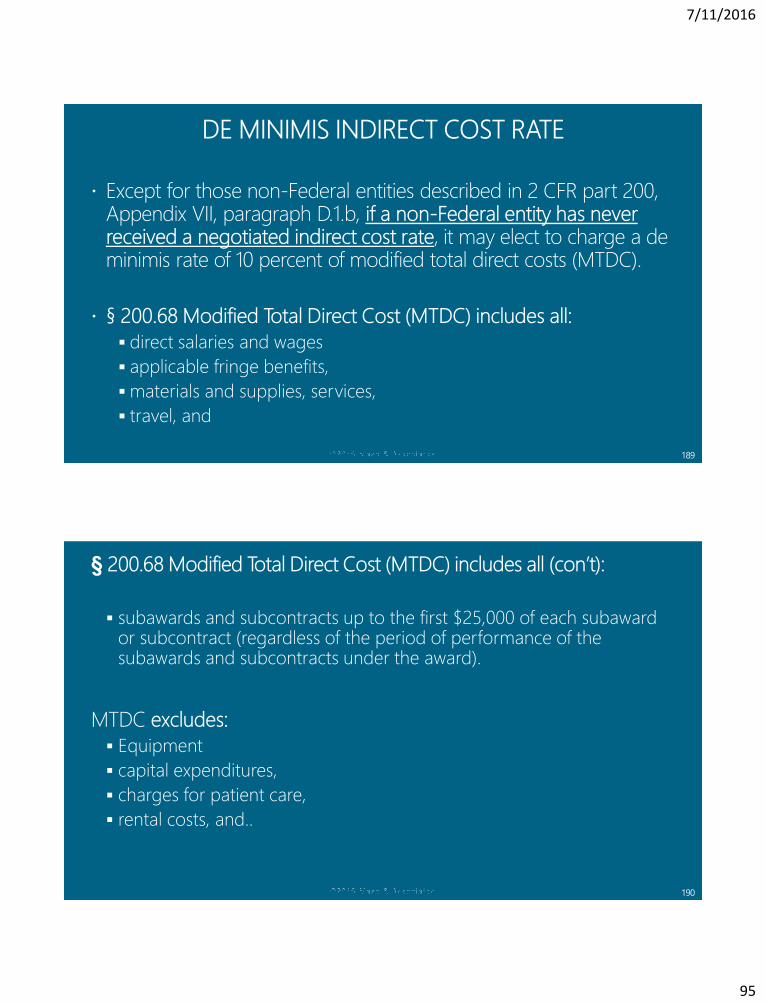

Indirect cost rate for the federal award, including if de minimis rate is charged

7/11/2016

106

211

212

7/11/2016

107

213

214

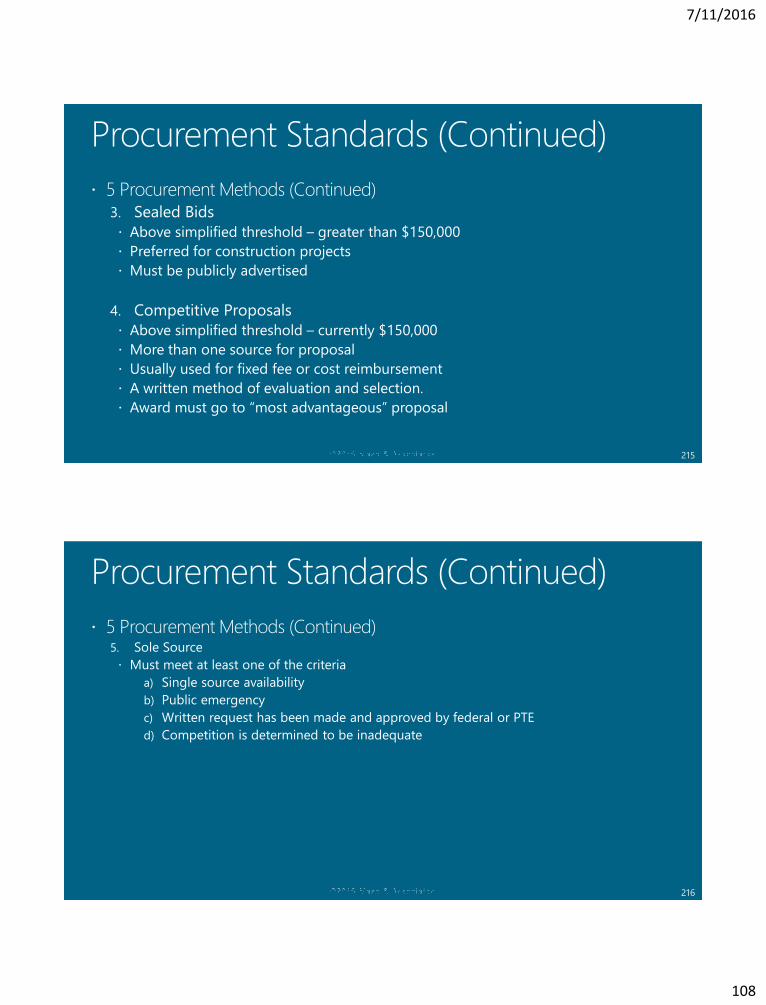

https://www.acquisition.gov/sites/default/files/current/far/html/Subpart%202_1.html

7/11/2016

108

215

216

7/11/2016

109

217

218

7/11/2016

110

219

220

7/11/2016

111

221

222

7/11/2016

112

223

224

7/11/2016

113

225

226

7/11/2016

114

227

228

7/11/2016

115

229

230

http://www.sco.ca.gov/Files-AUD/2015_internal_control_guidelines.pdf

7/11/2016

116

231

232

7/11/2016

117

233

234

7/11/2016

118

235

236

7/11/2016

119

237

238

7/11/2016

120

239

240

7/11/2016

121

241

242

7/11/2016

122

243

244

7/11/2016

123

245

246

7/11/2016

124

247

248

• Application controls

• General IT controls

7/11/2016

125

249

250

7/11/2016

126

251

252

7/11/2016

127

253

254

7/11/2016

128

255

256

7/11/2016

129

257

258

7/11/2016

130

259

http://www.gao.gov/products/GAO-01-1008G

http://www.coso.org/IC.htm

260

7/11/2016

131

261

262

7/11/2016

132

263

264

0 5 10 15 20

Education

Health Care

Manufacturing

Government/Public

Administration

Banking/Financial Services

2016

7/11/2016

133

265

266

7/11/2016

134

267

268

7/11/2016

135

269

270

0 5 10 15 20 25

>60

56-60

51-55

46-50

41-45

36-40

31-35

26-30

<26

2014

2016

7/11/2016

136

271

272

7/11/2016

137

273

274

7/11/2016

138

275

276

7/11/2016

139

277

Authorization

Record

keeping

Custody of

asset

278

7/11/2016

140

279

280

7/11/2016

141

281

282

7/11/2016

142

283

284

7/11/2016

143

285

286

7/11/2016

144

287

288

7/11/2016

145

289

290

ONLY 3%0 10 20 30 40 50

Account Reconciliation

By Accident

Internal Audit

Management Review

Tip

2014

2016

7/11/2016

146

291

292