Embed Size (px)

Citation preview

GASB 77: a New Municipal Finance

Safeguard

Greg LeRoy ~ Good Jobs First

Southern Municipal Finance SocietySeptember 29, 2017 ~Dallas

Good Jobs First:Since 1998, a Fiscal-Policy Resource forPolicymakers, Grassroots, Journalists

Independent, non-partisan, non-profit Model Research and Publications 50-state “report card” studies Subsidy Tracker & Violation Tracker Testimony, Training and Speaking

>$70 Billion per Year! Property Tax Abatements Tax Increment Financing (TIF) Districts Corporate Income Tax Credits Personal Income Tax Diversions Sales Tax Exemptions & Diversions Tax-free Loans Enterprise Zones Training Grants Dedicated Infrastructure

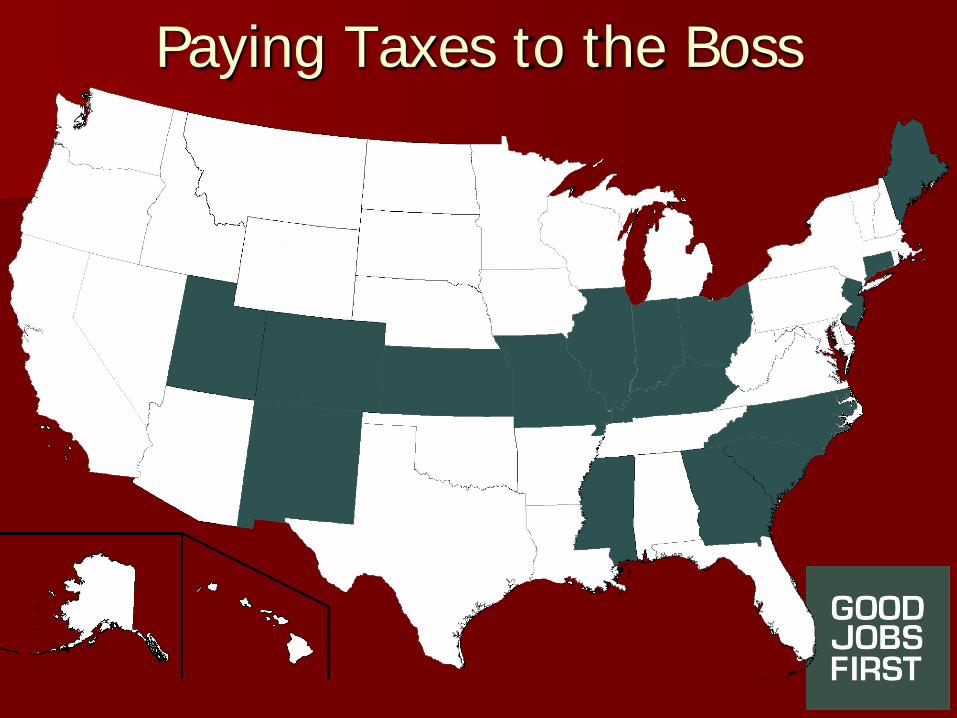

Paying Taxes to the Boss

Memphis Budget Erosion

TIF vs. Chicago Schools

Detroit MSA Shutdowns 2001-04

MEGA Deals 2001-2004

Intergovernmental Free Lunch

School boards usually powerless against abatements, TIFs, EZs

$1.2B and Counting

And Right Behind at $1.1 Billion…

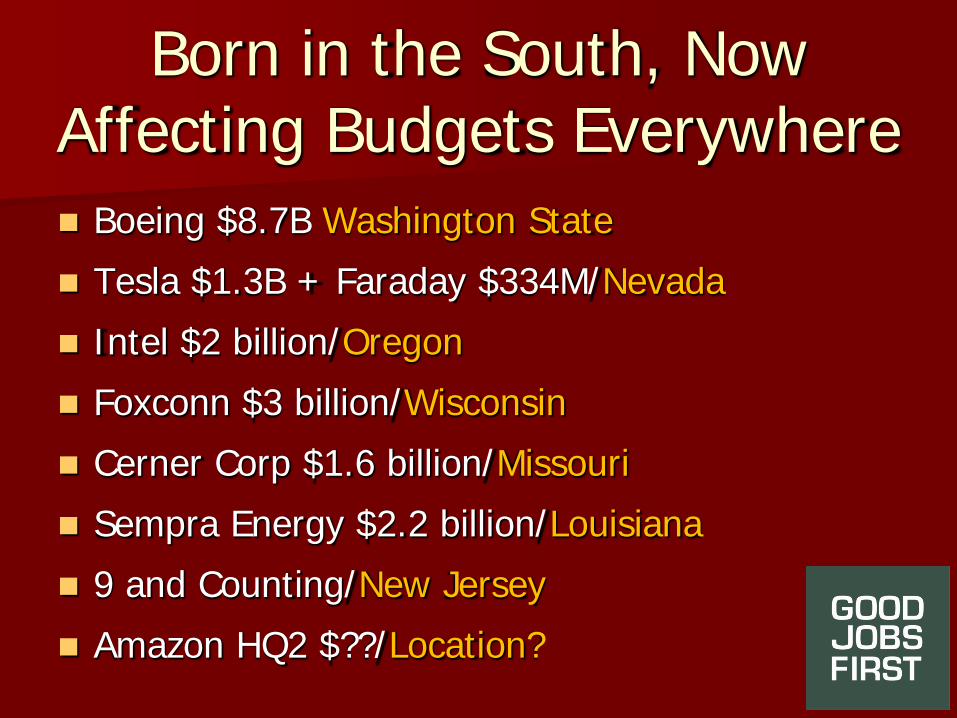

Born in the South, NowAffecting Budgets Everywhere Boeing $8.7B Washington State Tesla $1.3B + Faraday $334M/Nevada Intel $2 billion/Oregon Foxconn $3 billion/Wisconsin Cerner Corp $1.6 billion/Missouri Sempra Energy $2.2 billion/Louisiana 9 and Counting/New Jersey Amazon HQ2 $??/Location?

363 Megadeals

$658,000/job

Data Centers: How Costly? 10 states with specific “cloud” tax breaks

fail to disclose even aggregate cost!

Alabama, Indiana, Iowa, Mississippi, Missouri, Nebraska, Oklahoma, South Carolina, Tennessee, & Virginia

Florida Megadeal, Gone Awry

North Carolina Megadeal Dell – Winston-Salem Record state package of $242M, plus

$37M local, after state-sanctioned intraregional competition

Jobs lasted less than four years

But What’s the Total Cost?

~$70 Billion per Year = Old Estimate, Based Mostly on Extrapolations

Enter GASB!(Governmental Accounting Standards Board)

Determines 2010-2014 that tax abatements are of sufficient prevalence and magnitude to merit a Statement

Exposure Draft late Oct 2014 draws ~300 comments from non-profit, tax & budget, academic, labor and public officials.

120 substantive, >2/3rds pro-disclosure

Subsidy Tracker

Company-specific and searchable 50 states + DC + localities

+ federal deals

August 2015:Statement No. 77 Issued Covers GAAP-compliant budgets calendar

2016 and beyond

~50,000 state & local government bodies will newly report

CAFR Note: how much revenue was lost to each tax abatement program

“Tax Abatement” 3 Elements1) Agreement between government and

taxpayer (not broad exemption)

2) Government agrees to less revenue

3) Taxpayer agrees to perform quid pro quo

Data Will be Crude For abating governments, one dollar figure

per program per year

For passive income losers (e.g., school districts), one dollar figure per tax, per source

Missing: # of deals, names of recipients, future-year losses

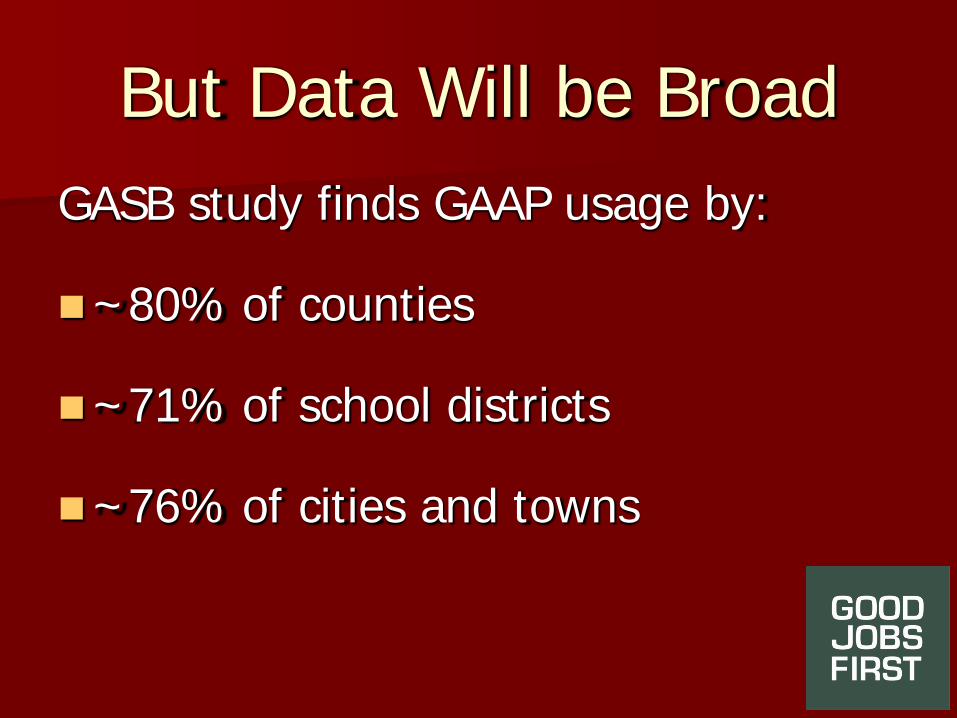

But Data Will be BroadGASB study finds GAAP usage by:

~80% of counties

~71% of school districts

~76% of cities and towns

Intergovernmental Disclosures

Bernalillo County, $210

City of Albuquerque,

$280

Albuquerque Public Schools,

$250

UNM Hospital, $150

CNM (community

college), $80

State of New Mexico, $30

Hypothetical $1,000 Bernalillo County property tax abatement

Associated Obligations

Example: new infrastructure promised to abated project

Compliance to Date:One Hot Mess

Some localities missed the memo

Some go above and beyond

Some don’t look right

Ohio ruling: a precursor?

Tiff over TIF Tax Increment Financing (TIF) was

flagged by many commenters

GASB clarified in April 2017 Implementation Guide

2 of 3 kinds of TIF covered

Problems persist…

New! Subsidy Tracker 2 Unveiled two days ago -- for GASB 77 data

Standardized template

Go-to hub

Now seeking partners!

51 State “Roadmaps” AvailableWho collects CAFRs?

Are CAFRs posted online?

Are CAFRs stress-tested?

Who else commented pro or con?

When do first big cities, counties, school districts report?

A Cottage Industry is Born! Journalists

Non-profits

Ratings Agencies

Academics

State Agencies

Learn More @

www.goodjobsfirst.org/GASB

![WV GASB Conference GAAP Update [Read-Only]wvde.state.wv.us/finance/documents/GASBUpdatePresentation.pdf · The Great GASB Conference ... implementation of GASB 47 • All other termination](https://img.dokumen.tips/doc/110x75/5b2a1f147f8b9ad6458b9054/wv-gasb-conference-gaap-update-read-onlywvdestatewvusfinancedocumentsga.jpg)