29 DECEMBER 2004 PRESS RELEASE REPORT OF THE WORKING GROUP ON WAGE RESTRUCTURING FOR THE INSURANCE SECTOR

The Working Group on Wage Restructuring for the Insurance Sector (IWG)1 has

developed a set of recommendations2 to help companies in the insurance sector align key

components of its wage system with the recommendations of the Tripartite Taskforce on

Wage Restructuring. As the insurance sector has implemented wage restructuring since

July 2000, the IWG focused on making the existing wage system more flexible so that

companies with varying sizes and business models can implement the recommendations

based on their specific needs and circumstances.

2 The IWG provides broad guidelines for insurance companies to follow in their wage

restructuring recommendations. Firstly, companies are encouraged to standardise their

wage structure to three components, namely, basic salary, Monthly Variable Component

(MVC) and Annual Variable Component (AVC).

3 Based on today’s context, IWG also recommends that the Annual Wage Supplement

(AWS), which has always been part of guaranteed annual pay, be incorporated as part of

basic pay. Companies, however, may take their own decision on the payout. For example,

for a company that currently gives a 14-month package, it can either incorporate the AWS

into base pay through a clean wage package of 12 months, or spread the AWS over 14

equal installments, with the last 2 installments given out in the month of November or

December. As the incorporation of the AWS into base pay is a significant change, IWG has

1 The Working Group, formed in May 2004, comprises members from the Singapore Insurance Employees Union (SIEU), Singapore National Employers Federation, and representatives from 5 insurance companies. Please see Annex A for the full list of the members. 2 A summary of the recommendations by the IWG is at Annex B.

suggested that companies not ready to change by January 2005 can do so with effect from

the new Collective Agreement term3.

4 The IWG also recommends that the industry should have a full build-up of the MVC

to 10% by 2005 so as to enable the companies to respond nimbly to changing business

conditions.

5 Most insurance companies have a Variable Profit Bonus (VPB) in their wage system

based on a pre-determined formula on Key Performance Indicators (KPIs) such as Sales

Growth and/or Profits. However, it is not structured for all companies. Hence, the IWG

recommends that the industry rename the VPB as the Annual Variable Component (AVC)

and introduce a structure based on company KPIs. To enlarge the AVC component, the

IWG also encourages companies to consider moderating their built-in salary increases to

enhance the variable component.

6 Expressing confidence that the insurance industry will support the recommendations

of the group, Ms Jenny Wong, HR Director, Prudential Assurance Company Singapore Pte

Ltd and co-chair of the IWG, explained, “The insurance sector has been following closely

on the nation’s call for wage reform with its first attempt in 1986 when it adopted an

industry-wide Job Evaluation System to establish job grades and salary range for each

grade of job for its bargainable employees. Since then, a number of other initiatives to

streamline its wage structure followed.”

7 The IWG is mindful of the need to allow some flexibility for companies to implement

the recommendations. Mr Terry Lee, President of Singapore Insurance Employees Union

(SIEU) and co-chair of the IWG, expressed that the SIEU and IWG will jointly work at

3 Since the early 1970s, a Collective Agreement (CA) is signed once every 3 years between the Singapore Insurance Employees Union (SIEU) and the SNEF Insurance Group which comprises 47 insurance companies – both life and general business.

building personal KPI accomplishment into the formula for the payout of AVC so as to link

payment of the AVC to company as well as individual performance.

8 The full report is attached at Annex C and is also available on the MOM website at

www.mom.gov.sg.

Issued by the Working Group on Wage Restructuring for the Insurance Sector __________________________________________________________________

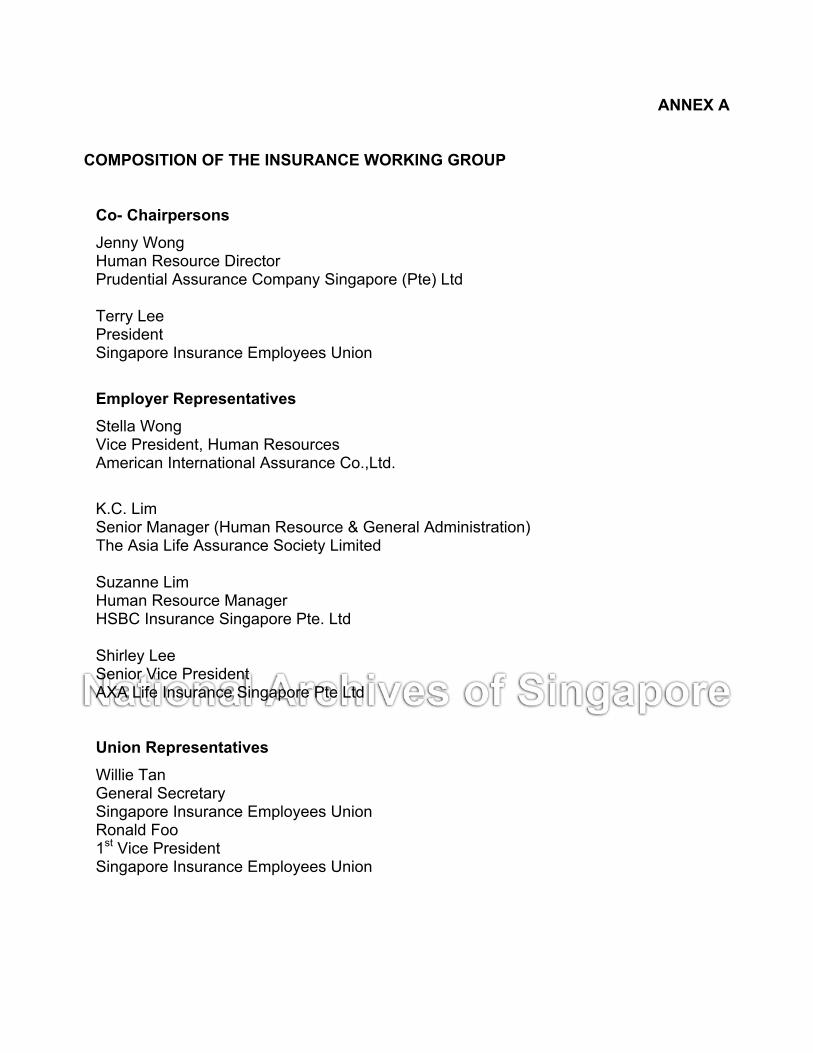

ANNEX A

COMPOSITION OF THE INSURANCE WORKING GROUP

Co- Chairpersons Jenny Wong Human Resource Director Prudential Assurance Company Singapore (Pte) Ltd Terry Lee President Singapore Insurance Employees Union

Employer Representatives Stella Wong Vice President, Human Resources American International Assurance Co.,Ltd.

K.C. Lim Senior Manager (Human Resource & General Administration) The Asia Life Assurance Society Limited Suzanne Lim Human Resource Manager HSBC Insurance Singapore Pte. Ltd Shirley Lee Senior Vice President AXA Life Insurance Singapore Pte Ltd

Union Representatives Willie Tan General Secretary Singapore Insurance Employees Union Ronald Foo 1st Vice President Singapore Insurance Employees Union

Jennifer Yap Treasurer Singapore Insurance Employees Union Goh Sor Imm Asst Director, Industrial Relations Dept National Trade Unions Congress Government Representatives from Ministry of Manpower Ong Yen Her Divisional Director, Labour Relations & Workplace Division Teo Seng Meng Senior Assistant Director Labour Relations Department Lau Weng Hong Senior IR Consultant/Conciliator Labour Relations Department Quek Jen Juan Senior IR Consultant/Conciliator Labour Relations Department

Secretariat Linda Ang Senior Consultant Singapore National Employers Federation James Pang IR Consultant/Conciliator Ministry Of Manpower

ANNEX B

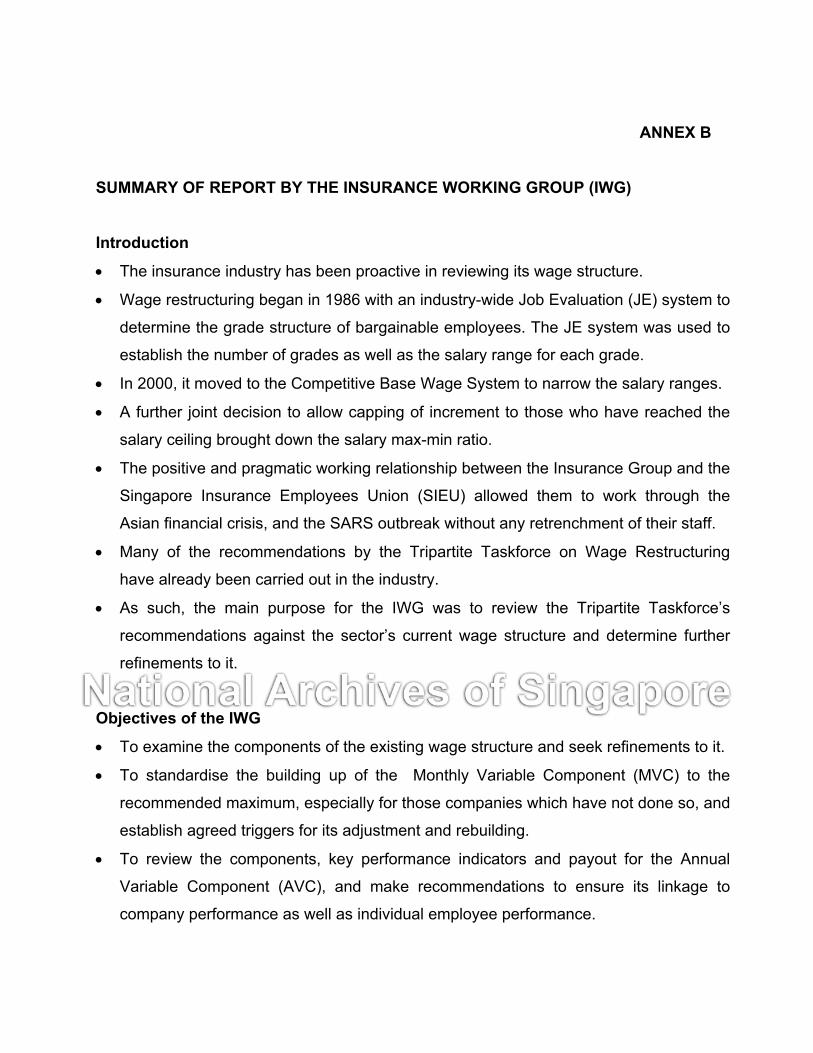

SUMMARY OF REPORT BY THE INSURANCE WORKING GROUP (IWG)

Introduction

• The insurance industry has been proactive in reviewing its wage structure.

• Wage restructuring began in 1986 with an industry-wide Job Evaluation (JE) system to

determine the grade structure of bargainable employees. The JE system was used to

establish the number of grades as well as the salary range for each grade.

• In 2000, it moved to the Competitive Base Wage System to narrow the salary ranges.

• A further joint decision to allow capping of increment to those who have reached the

salary ceiling brought down the salary max-min ratio.

• The positive and pragmatic working relationship between the Insurance Group and the

Singapore Insurance Employees Union (SIEU) allowed them to work through the

Asian financial crisis, and the SARS outbreak without any retrenchment of their staff.

• Many of the recommendations by the Tripartite Taskforce on Wage Restructuring

have already been carried out in the industry.

• As such, the main purpose for the IWG was to review the Tripartite Taskforce’s

recommendations against the sector’s current wage structure and determine further

refinements to it.

Objectives of the IWG

• To examine the components of the existing wage structure and seek refinements to it.

• To standardise the building up of the Monthly Variable Component (MVC) to the

recommended maximum, especially for those companies which have not done so, and

establish agreed triggers for its adjustment and rebuilding.

• To review the components, key performance indicators and payout for the Annual

Variable Component (AVC), and make recommendations to ensure its linkage to

company performance as well as individual employee performance.

Recommendations to Refine Existing Wage Structure

The IWG has made various recommendations to refine the present wage structure within

the insurance sector:

1. Standardise the components of the wage structure

• Basic Salary, Monthly Variable Component (MVC) and Annual Variable

Component (AVC).

2. Incorporate the Annual Wage Supplement (AWS) as part of basic pay.

• AWS is seen as no longer relevant in today’s context, since it has always been part

of guaranteed annual pay.

• IWG recommends that the companies concerned take their own decision on

payout. Take the example of a company that provides a 14-month package:

o The first step in this direction is to incorporate the AWS into base pay

through a clean wage package of 12 months.

o For those which prefer to continue to make the payment in 14 equal

installments, it will be base pay made over 14 equal installments, with the

last 2 installments to be given in the month of November or December.

• Incorporating AWS into base pay would move the basic monthly salary nearer to

the maximum of the salary range. Those reaching or at the maximum of their

salary range by 2005 would still be entitled to one final annual increment. Those

who have exceeded the maximum of their salary range shall not have any

increment.

• Incorporation of the AWS into base pay is a significant change for some of the

companies. Companies that are not ready to make the change by January 2005,

will do so with effect from the new Collective Agreement term (2006 to 2008).

3. Full Build Up of Monthly Variable Component (MVC)

• The MVC was implemented in the Group Annual Wage increase settlement in

2000 and both parties have built it up to 7% in 2003.

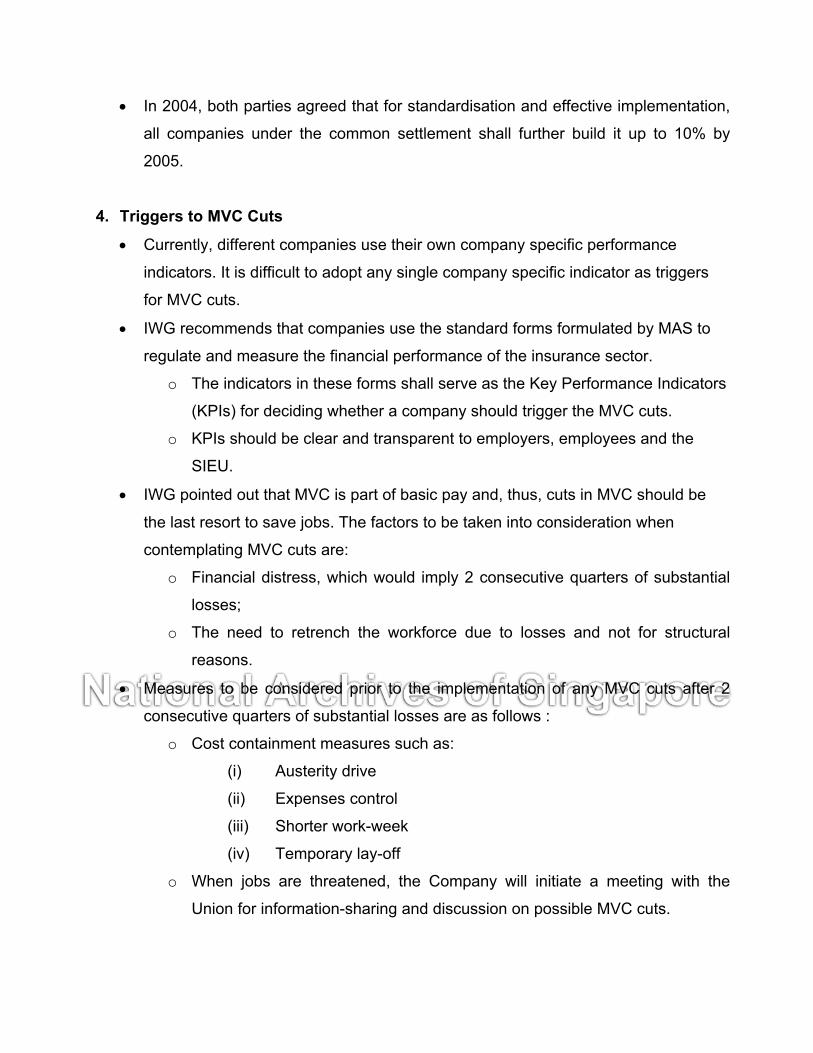

• In 2004, both parties agreed that for standardisation and effective implementation,

all companies under the common settlement shall further build it up to 10% by

2005.

4. Triggers to MVC Cuts

• Currently, different companies use their own company specific performance

indicators. It is difficult to adopt any single company specific indicator as triggers

for MVC cuts.

• IWG recommends that companies use the standard forms formulated by MAS to

regulate and measure the financial performance of the insurance sector. o The indicators in these forms shall serve as the Key Performance Indicators

(KPIs) for deciding whether a company should trigger the MVC cuts.

o KPIs should be clear and transparent to employers, employees and the

SIEU.

• IWG pointed out that MVC is part of basic pay and, thus, cuts in MVC should be

the last resort to save jobs. The factors to be taken into consideration when

contemplating MVC cuts are:

o Financial distress, which would imply 2 consecutive quarters of substantial

losses;

o The need to retrench the workforce due to losses and not for structural

reasons.

• Measures to be considered prior to the implementation of any MVC cuts after 2

consecutive quarters of substantial losses are as follows :

o Cost containment measures such as:

(i) Austerity drive

(ii) Expenses control

(iii) Shorter work-week

(iv) Temporary lay-off

o When jobs are threatened, the Company will initiate a meeting with the

Union for information-sharing and discussion on possible MVC cuts.

• It is only when such measures have failed and jobs are threatened that MVC cuts

would be exercised.

5. Rebuilding the MVC

• For full or partial MVC to be restored, the IWG recommends that:

o There should be 2 quarters of consecutive profits;

o The Company or SIEU may initiate a meeting to discuss the possible

restoration to the MVC that was cut either in full or partial;

o There will be no backdating of MVC cuts in the process of restoration.

6. AVC to replace the current Variable Bonus Payment II (VBP II)

• Most insurance companies have a variable wage component or some form of

variable bonus in their wage structures. Some are structured and given to all

employees, whilst others are less structured and not paid to all employees.

• Typically, this payout is based on a pre-determined formula on Key Performance

Indicators (KPIs) such as Sales Growth and/or Profits. For some, they have paid

out the bonus based on the pre-agreed formula with the SIEU.

• For consistency and standardisation in approach, the IWG recommends that AVC

will replace this payout.

• Owing to the different size of companies, sales growth and profitability, it is difficult

for the Insurance Workgroup to come up with a common formula for payout.

• Hence, the existing practice for this payout will be maintained. This means that:

o Individual companies continue to formulate their own KPIs to link the

payment of AVC closely to their company’s performance.

o The KPIs should be relevant to the company’s performance, attainable, and

transparent to the SIEU and their employees.

• For companies using the formula stipulated in the Collective Agreement, the SIEU

will work with the member companies to develop relevant and challenging KPIs

when the current CA expires by end 2005.

• Currently, the AVC forms about 10 to 13% of the bargainable employees’ total

annual compensation and up to 30% for the more senior executives.

o The proportion of variable versus fixed pay seems to be close to the

Tripartite Taskforce’s recommended level for the executives, but low for the

bargainable employees and junior level executives.

o IWG recommends that companies consider raising the maximum quantum

of variable bonus for the latter group of employees.

o To enlarge their variable component, the IWG also encourages companies

to consider moderating their built-in salary increases so that there is room

for enhancing the variable component.

o To link the AVC to both company and personal KPIs, IWG recommends that

both the Insurance Group and the SIEU jointly work at building personal KPI

accomplishment into the formula for payout of AVC.

Next Steps

• The SIEU will work with individual companies to make the necessary adjustments

to the recommendations as befitting the individual company’s situation.

• While allowing flexibility in implementation, IWG recommends the following

measures for companies to consider :

o To time the implementation of the recommendations starting in 2005, or

upon the renewal of the CA in 2006.

o To consider an upside for AVC with the inclusion of individual employee

performance KPIs for both the bargainable and non-bargainable staff.

o The review of the current common Performance Appraisal format to

facilitate the distribution of AVC based on individual employee performance

and contribution.

o To look into varying the level of service increments based on the company’s

performance as well as that of individual employees, instead of paying fixed

increments to all bargainable employees.

o To detail a communication plan and implementation roadmap for rolling out

the changes to all staff.

ANNEX C REPORT OF THE INSURANCE WORKING GROUP I OBJECTIVES OF THE INSURANCE WORKING GROUP (IWG)

1 The Insurance Working Group (IWG) was formed in May 2004 to review

the current wage structure of insurance companies and to look into

adopting the recommendations put up by the Tripartite Taskforce on Wage

Restructuring for a flexible and performance based system. The guiding

principles (detailed under Chapter 3 of Book 1 of the Tripartite Taskforce

Report on Wage Restructuring) for this process are:

a. Sustainable growth

b. Competitiveness

c. Flexibility

d. Motivation

e. Stability

2 Members of the IWG comprise representatives of employers, the SIEU,

Ministry of Manpower, NTUC and SNEF (see Appendix 2).

3 Over the years the insurance sector has been proactive in reviewing its

wage structure. Many changes had been made. In fact, much of the

recommendations made by the Tripartite Taskforce on Wage

Restructuring have been carried out way before its report was made public.

As such, the main purpose for the IWG was to review the Tripartite

Taskforce’s recommendations against the sector’s wage structure and

determine further refinements to it. Specifically, the objectives of the IWG

are as follows:

a. To examine the components of the existing wage structure and seek

refinements to it.

b. To standardize the building up of the Monthly Variable Component

(MVC) to the recommended maximum, especially for those

companies which have not done so, and establish agreed triggers

for its adjustment and rebuilding;

c. To review the components, key performance indicators and payout

for the Annual Variable Component (AVC), and make

recommendations to ensure its linkage to company performance as

well as individual employee performance.

II BACKGROUND 4 The insurance industry has come a long way in making its wage structure

more flexible and competitive. The SNEF Insurance Group comprises 47

insurance companies – both life and general business. Since the early

1970s, 30 out of the 47 companies (representing 64% of all insurance

companies) had been operating under one common Collective Agreement

(CA) that is signed once every 3 years with the Singapore Insurance

Employees’ Union (SIEU). Before the introduction of salary ranges for

different job positions, only minimum salaries were stated in the CAs as

follows:

Clerical (Without “O” levels) $520 no maximum

Clerical (With “O” levels or better) $550 no maximum

Non-Clerical $400 no maximum

As a result, workers with long years of service drew salaries much higher

than their younger counterparts in the same job.

5 First attempts at wage restructuring began in 1986, whereby it was agreed

that an industry-wide Job Evaluation (JE) system would be used to

determine the grade structure of bargainable employees for the 30

companies. The objective was to use the JE system to establish the

number of grades as well as the salary range for each grade. This

provided the structure for employees to be paid according to the job rate.

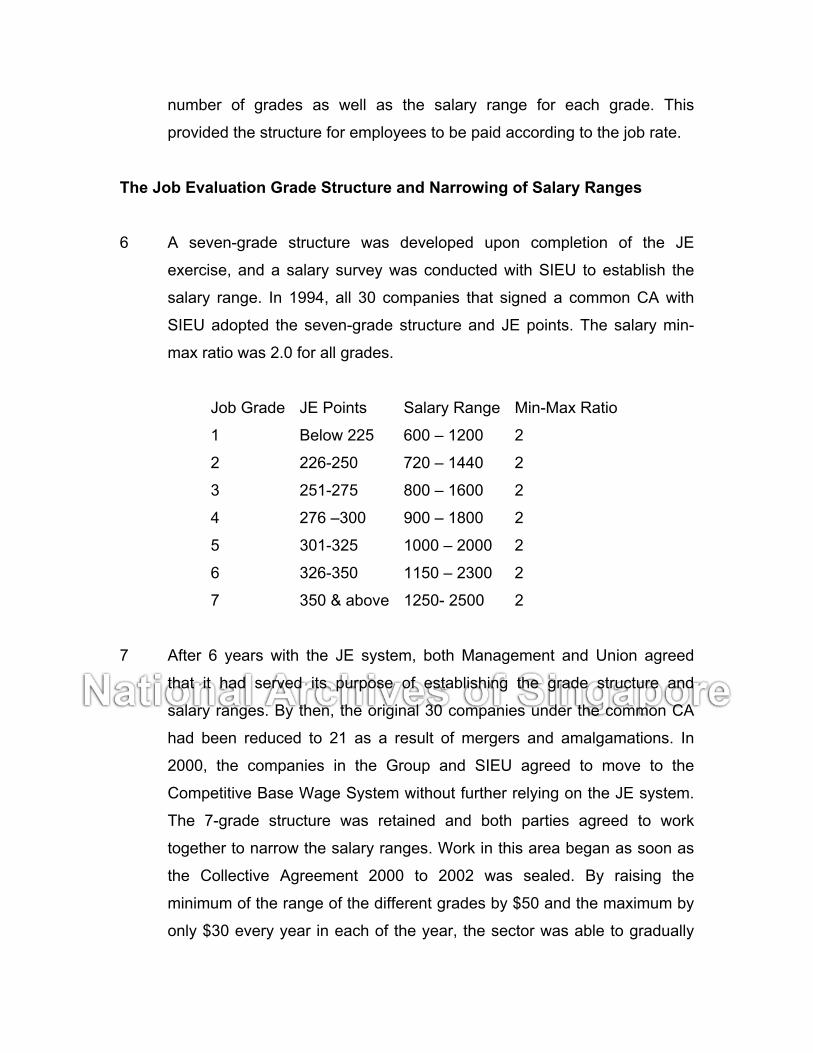

The Job Evaluation Grade Structure and Narrowing of Salary Ranges

6 A seven-grade structure was developed upon completion of the JE

exercise, and a salary survey was conducted with SIEU to establish the

salary range. In 1994, all 30 companies that signed a common CA with

SIEU adopted the seven-grade structure and JE points. The salary min-

max ratio was 2.0 for all grades.

Job Grade JE Points Salary Range Min-Max Ratio

1 Below 225 600 – 1200 2

2 226-250 720 – 1440 2

3 251-275 800 – 1600 2

4 276 –300 900 – 1800 2

5 301-325 1000 – 2000 2

6 326-350 1150 – 2300 2

7 350 & above 1250- 2500 2

7 After 6 years with the JE system, both Management and Union agreed

that it had served its purpose of establishing the grade structure and

salary ranges. By then, the original 30 companies under the common CA

had been reduced to 21 as a result of mergers and amalgamations. In

2000, the companies in the Group and SIEU agreed to move to the

Competitive Base Wage System without further relying on the JE system.

The 7-grade structure was retained and both parties agreed to work

together to narrow the salary ranges. Work in this area began as soon as

the Collective Agreement 2000 to 2002 was sealed. By raising the

minimum of the range of the different grades by $50 and the maximum by

only $30 every year in each of the year, the sector was able to gradually

narrow the salary ranges. A further joint decision to allow capping of

increment to those who have reached the salary ceiling brought the salary

max-min ratio from an average of 2.0 to 1.78. Adopting the same measure

for the period of the current CA (2003 to 2005), the average max-min ratio

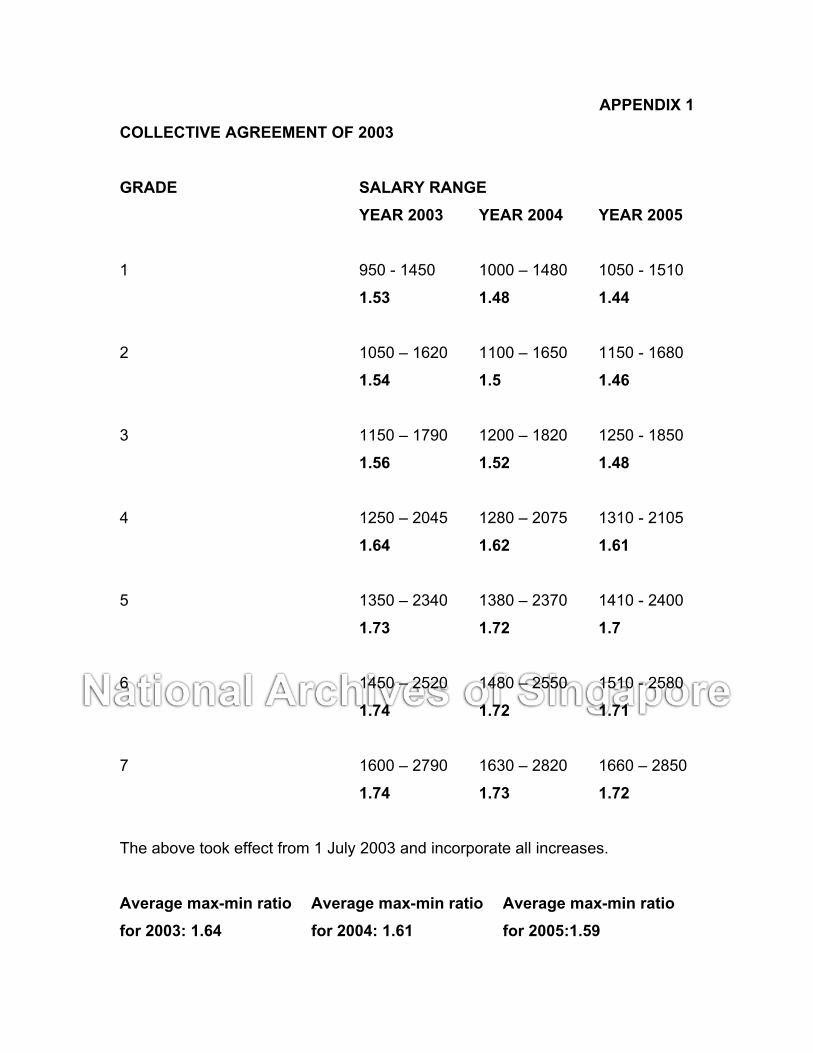

would be further reduced to 1.59 by 2005 (See Appendix 1).

Good Bipartite Relations as the Bedrock for Managing Change

8 The working relationship between the Insurance Group and the SIEU has

always been positive and pragmatic. The establishment of the job grades

with minimum and maximum salaries and the narrowing of the salary

ranges would not be possible if not for the harmonious and supportive

relationship between the Insurance Group and the SIEU. Both parties

have always been able to resolve their differences through bipartite

discussions based on open communication, good rapport and trust. In the

difficult years of the Asian financial crisis, and then the SARS outbreak,

the SIEU worked closely with the management of the Insurance Group to

provide modest but respectable salary increases to its employees. Except

for merger and acquisitions, the insurance sector did not have any

retrenchment of their staff. Further, on issues outside the Collective

Agreement, both the Insurance Group and the SIEU had signed

Memorandums of Understanding to enable companies and the union to

make references on the points of understanding in the memorandum so

that future cases could be appropriately dealt with. When the call for wage

restructuring came, both the Insurance Group and the SIEU

spontaneously took joint responsibility to review their wage structure.

III EXISTING WAGE STRUCTURE

9 The present wage structure within the insurance sector comprises the

following components:

a. Basic Salary

b. Monthly Variable Component (MVC)

c. Annual Wage Supplement (AWS)

d. Variable Profit Bonus I (VPB I)

e. Variable Profit Bonus II (VPB II)

Basic Salary 10 The annual basic salary package of employees in the Insurance Group is

typically paid over 14, 14.5 or in a few cases, 15-month equal installments.

This comprises 12 months salary and the AWS of 2 months, 2.5 months or

in some cases, 3 months salary. The AWS is typically paid in November or

December in each year. The Annual Wage Supplement (AWS) was

adopted for both the bargainable staff as well as the executives in the

majority of companies under the Group. It is observed that most

companies take the basic as well as the AWS as guaranteed payments as

the payment is stipulated in their employment contracts.

Monthly Variable Component

11 The Insurance Group is one of the pioneer group of companies to adopt

the Monthly Variable Component (MVC). First implemented in July 2000,

the Insurance Group has been building this component consistently with

each salary increase. To-date, most of the companies have already

achieved the full build-up of 10%, with a small number at 7%. It was

agreed that these companies will make it up to 10% by 2005.

Variable Profit Bonus I & II

12 The Wage Reform in 1986 paved the way for the payout of a variable

wage component that is tied to the company’s profits and productivity.

Through a bipartite agreement, one month of the AWS was transferred to

the item known as Variable Profit Bonus I (VPB I). VPB I is payable as

long as the company is not in “financial distress”. For most of the

companies, the AWS, as well as the VPB I have always been paid to the

employees.

13 The VPB II was introduced as a payout to employees if the company

performed well in the year. The formula for this payout was laid out in the

Collective Agreement as follows:

a) If the Service Increment (SI) is 4% and above, the formula shall be:

Current Profit x (8 – SI)% subject to a maximum of 13%

Benchmark Profit

to be paid as a lump sum

b) If the SI is below 4%, the formula shall be:

Current Profit x (6-SI)% subject to a maximum of 13%

Benchmark Profit

to be paid as a lump sum

Current profit refers to the profit for the preceding financial year.

14 The majority of Life and General Insurance companies adopted the

formula for payout of their variable profit bonus. However, with the SIEU’s

concurrence, some of the companies had been able to use their company

specific formula to calculate this payout to their employees. Although the

amount paid out may vary from year to year, it was observed that the

majority of the companies in the Insurance Group had been able to make

this payment to their employees. Even in the last 3 years when the

economy was sluggish, this payment was made to employees.

Open Appraisal System and Linkage to VPB II Payout

15 The Insurance Group made early attempts in linking bonus payout to

performance. This was made possible through the introduction of an Open

Appraisal System. From 1995, companies which adopted the Open

Appraisal System endorsed by SIEU could pay VPB II based on individual

KPIs. Currently, the individual KPI portion is limited to 30% of their VPB II

payout.

IV ANNUAL INCREMENT AND THE BASE UP WAGE INCREMENT

16 For the Insurance Group, annual increments have always been negotiated

on a yearly basis. Both the Insurance Group and the SIEU have been

pragmatic in giving salary increments on the basis that wage increases

should lag behind productivity growth. However, as per the negotiation

with the Union, member companies take a uniform approach in deciding

the quantum of salary increments for their bargainable employees, ie a flat

rate of market increase was given to each employee. The individual

companies have to pay on top of the negotiated increment, any merit or

promotional increments to the bargainable employees concerned.

17 In response to the weak economic situation which dampened the

employment market and when unemployment began to rise, the SIEU

made a bold step forward by proposing a Base Up Wage Increment

beginning with its Collective Agreement 2000 to 2002. The Base Up

Salary Increment was capped at $30 on the maximum of each salary

range. This means that over the 3-year period, each salary range only

increased by a maximum of $90. This was by no means an easy decision,

especially for the SIEU, but its adoption augured well for the industry in

holding salary increases at a modest rate during the economic downturns

and to some extent, helped preserve jobs.

V RECOMMENDATIONS OF THE IWG ON WAGE RESTRUCTURING

18 Reflecting on the Tripartite Taskforce’s recommendations, many of these

have been adopted by the Insurance Group. The IWG is of the opinion

that only refinements to their existing wage structure are necessary.

Incorporation of AWS into Basic Salary

19 The first recommendation is to standardize the components of the wage

structure to basic salary, MVC and AVC. It was felt that the AWS is no

longer relevant in today’s context, especially when it has always been part

of guaranteed annual pay. As such, it makes sense for it to be

incorporated into the wage component. Of the 3 components, by virtue

that MVC has reached its maximum of 10%, the AVC has its payout

critieria, and AWS has been deemed part of guaranteed pay, it therefore

follows that the AWS be treated as part of basic salary.

20 However, as companies in the Group have been paying a 14.5 or 15

months package as base pay, the first step in this direction is to

incorporate the AWS into base pay. Some companies surveyed however,

preferred to continue to make the payment in 14 equal installments. A few

member companies indicated preference for a clean wage package of 12

months. As this entails each company’s readiness for this change, the

IWG recommends that the companies concerned take its own decision on

payout. For those which maintain a 14 month payment, this shall be

deemed as base pay made over 14 equal installments, with the last 2

installments to be given in the month of November or December.

21 The IWG noted that with the incorporation of the AWS into the base pay –

whether paid over 12 or 14 months - the basic monthly salary of the

employees would be moved nearer to the maximum of the salary range.

As a goodwill gesture, as per the IWG’s recommendations, the Insurance

Group and the SIEU have agreed that those reaching or at the maximum

of their salary range by 2005 would still be entitled to one final annual

increment. Those who have already exceeded the maximum of their

salary range shall not have any increment.

22 The SIEU recognises that the incorporation of the AWS into base pay is a

significant change for some of the companies. They have agreed that

companies which are not ready to make the change by January 2005, will

do so with effect from the new CA term (2006 to 2008).

Full Build Up of Monthly Variable Component (MVC)

23 The MVC was implemented in the Group Annual Wage Increase

settlement in 2000 and both parties have built up it up to 7% in 2003. In

2004, both parties agreed that for standardization and effective

implementation, all companies under the common settlement shall further

build it up to 10%.

Triggers to MVC Cuts

24 The IWG recognizes that currently the different companies resort to the

use of their own company specific performance indicators. As such, it is

difficult to adopt any single company specific indicator for use as triggers

for MVC cuts. Since the MAS has regulated the insurance sector and

came up with new forms (financial performance indicators) for

submissions to them, the IWG recommends that companies use the

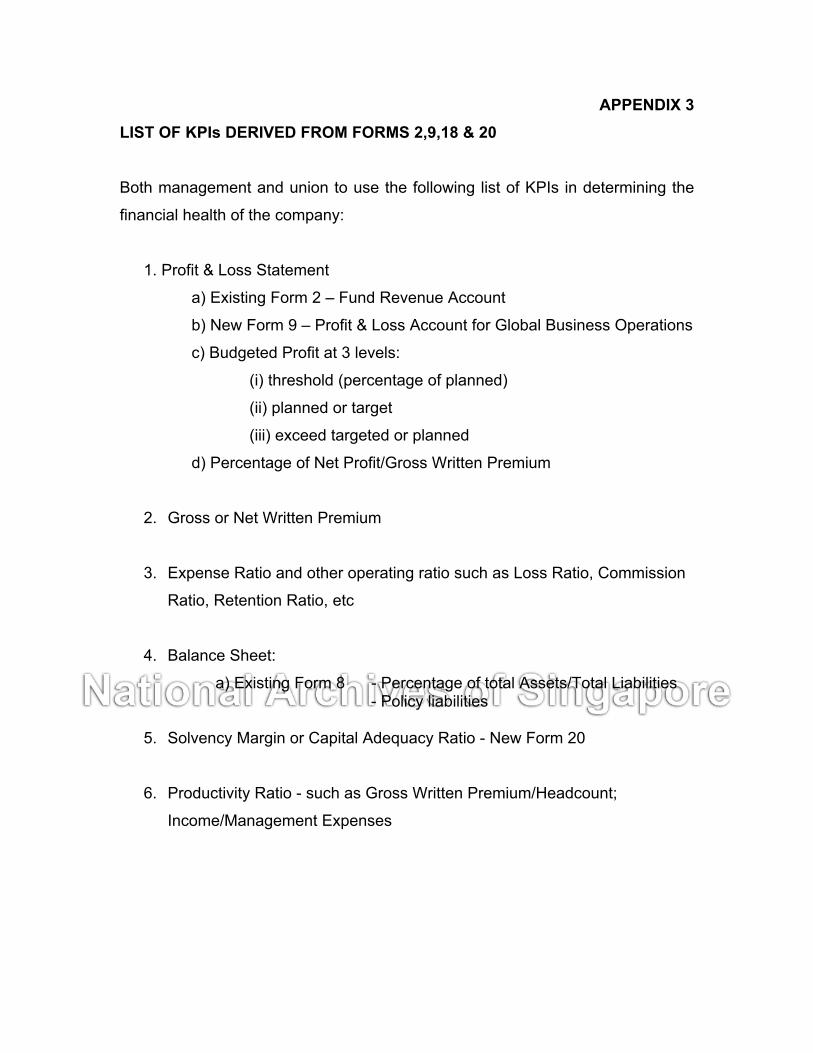

standard forms, in particular, Forms 2, 9, 18 and 20 (See Appendix 3).

The indicators in these Forms shall serve as the KPIs for deciding whether

a company should trigger the MVC cuts. KPIs should be clear and

transparent to employers, employees and the SIEU.

25 The IWG further pointed out to companies that MVC is part of basic pay

and agreed that if possible, MVC cuts should be the last resort to save

jobs. The factors to be taken into consideration when contemplating MVC

cuts are:

a) Financial distress, which would imply 2 consecutive quarters of

substantial losses based on Form 9;

b) The need to retrench the workforce due to losses and not for structural

reasons.

26 Measures to be taken prior to the implementation of any MVC cuts after 2

consecutive quarters of substantial losses are:

a) Implementation of other cost containment measures such as:

(i) Austerity drive

(ii) Expenses control

(iii) Shorter work-week

(iv) Temporary lay-off

b) When jobs are threatened, the Company will initiate a meeting with the

Union for information sharing and discussion on possible MVC cuts.

It is only when such measures have failed and jobs are threatened that

MVC cuts would be exercised.

Rebuilding the MVC

27 For full or partial MVC to be restored, the IWG recommends that:

a) There should be 2 quarters of consecutive profits based on Form 9;

b) The Company or SIEU may initiate a meeting to discuss the possible

restoration to the MVC that was cut either in full or partial;

c) There will be no backdating of MVC cuts in the process of restoration.

Renaming the VPB II to Annual Variable Component (AVC)

28 Most of the companies in the Insurance Group have a variable wage

component or some form of variable bonus in their wage structures. Some

are more structured and the payment is given to all employees, whilst

others are less structured and is not paid to all employees. Typically, this

payout is based on a pre-determined formula on key performance

indicators (KPIs) such as Sales Growth and/or Profits. For some, they

have paid out the bonus based on the pre-agreed formula with the SIEU,

as laid out in paragraph 13 above, currently termed as VPB II.

29 For consistency and standardization in approach, the IWG recommends

that this payout shall be called AVC henceforth. Owing to the different size

of companies, sales growth, profitability as well as their reporting

relationship with their Home Offices, it has been difficult for the Insurance

Workgroup, to come up with a common formula for payout. It is the IWG’s

view that the existing practice for this payout be maintained so as not to

cause undue stress on companies moving into the wage restructuring

process. This means that individual companies continue to formulate their

own KPIs to link the payment of AVC closely to their company’s

performance. The KPIs should be relevant to the company’s performance,

and should be attainable. They should also be transparent to the SIEU

and their employees.

30 For those companies using the formula stipulated in the CA, the SIEU has

agreed to review this and work with individual or group of companies on

relevant and challenging KPIs. As the current CA will expire by end 2005,

the SIEU will take the opportunity to work with the member companies in

this direction.

31 Currently, the AVC forms about 10 to 13% of the bargainable employees’

total annual compensation and up to 30% for the more senior executives.

The proportion of variable versus fixed pay seem to be close to the

Tripartite Taskforce’s recommended level for the executives, but low for

the bargainable employees and junior level executives. The IWG is of the

view that member companies consider raising the maximum quantum of

variable bonus for the latter group of employees. To enlarge their variable

component, the IWG also encourages companies to consider moderating

their built in salary increases so that there is room for enhancing the

variable component.

32 Having mentioned that there is an existing structured performance

appraisal process and forms in place within the Insurance Group, the IWG

contends that there is still scope for improvement in this area. This may

entail having a personal set of KPIs in addition to the company’s KPIs for

determination of the payout of the AVC. As the Insurance Group’s current

CA will expire in 2005, the IWG therefore recommends that both the

Insurance Group and the SIEU jointly work at building personal KPI

accomplishment into the formula for payout of AVC. This will truly

demonstrate the linking of payment of the AVC to company as well as

individual performance.

VI Conclusion and Next Steps

33 As the Insurance Group has always been cohesive and working towards a

unified stand, the IWG is confident that their recommendation would be

adopted by the member companies. However being pragmatic, the SIEU

will work with individual companies to make small adjustments to the

recommendations as befitting individual company’s situation. Since 2004

is coming to a close soon, the IWG further agrees to allow some flexibility

in the way member companies go about implementing its

recommendations:

a) To time implementation of the recommendations with the start of the

new year 2005, or for some to commence with the new CA term

starting Jan 2006.

b) To consider an upside for AVC with the inclusion of individual employee

performance KPIs especially for the bargainable staff.

c) The review of the current common Performance Appraisal format to

facilitate the distribution of AVC based on individual employee

performance and contribution;

d) To look into varying the level of service increments based on the

company’s performance as well as that of individual employees,

instead of paying fixed increments to all bargainable employees.

e) To detail a communication plan and implementation roadmap for rolling

out the changes to all staff.

APPENDIX 1 COLLECTIVE AGREEMENT OF 2003

GRADE SALARY RANGE YEAR 2003 YEAR 2004 YEAR 2005

1 950 - 1450 1000 – 1480 1050 - 1510

1.53 1.48 1.44

2 1050 – 1620 1100 – 1650 1150 - 1680

1.54 1.5 1.46

3 1150 – 1790 1200 – 1820 1250 - 1850

1.56 1.52 1.48

4 1250 – 2045 1280 – 2075 1310 - 2105

1.64 1.62 1.61

5 1350 – 2340 1380 – 2370 1410 - 2400

1.73 1.72 1.7

6 1450 – 2520 1480 – 2550 1510 - 2580

1.74 1.72 1.71

7 1600 – 2790 1630 – 2820 1660 – 2850

1.74 1.73 1.72

The above took effect from 1 July 2003 and incorporate all increases.

Average max-min ratio Average max-min ratio Average max-min ratio for 2003: 1.64 for 2004: 1.61 for 2005:1.59

APPENDIX 2 COMPOSITION OF THE INSURANCE WORKING GROUP Co- Chairpersons: Jenny Wong Human Resource Director

Prudential Assurance Company

Singapore (Pte) Ltd

Terry Lee President

Singapore Insurance Employees Union

Employers Representatives: Stella Wong Vice President, Human Resources

American International Assurance Co,

Ltd.

K.C. Lim Senior Manager (Human Resource &

General Administration)

The Asia Life Assurance Society Limited

Suzanne Lim Human Resource Manager

HSBC Insurance Singapore Pte. Ltd

Shirley Lee Senior Vice President

AXA Life Insurance Singapore Pte Ltd

Union Representatives: Willie Tan General Secretary

Singapore Insurance Employees Union

Ronald Foo 1st

Vice President

Singapore Insurance Employees Union

Jennifer Yap Treasurer

Singapore Insurance Employees Union

Goh Sor Imm Asst. Director, Industrial Relations Dept

National Trade Unions Congress

Government Representatives: Ong Yen Her Divisional Director, Labour Relations &

Workplace Division

Ministry Of Manpower

Teo Seng Meng Senior Assistant Director

Ministry Of Manpower

Lau Weng Hong Senior IR Consultant/Conciliator

Ministry Of Manpower

Quek Jen Juan Senior IR Consultant/Conciliator

Ministry Of Manpower

Secretariat: Linda Ang Senior Consultant

Singapore National Employers

Federation

James Pang IR Consultant/Conciliator

Ministry Of Manpower

APPENDIX 3 LIST OF KPIs DERIVED FROM FORMS 2,9,18 & 20

Both management and union to use the following list of KPIs in determining the

financial health of the company:

1. Profit & Loss Statement

a) Existing Form 2 – Fund Revenue Account

b) New Form 9 – Profit & Loss Account for Global Business Operations

c) Budgeted Profit at 3 levels:

(i) threshold (percentage of planned)

(ii) planned or target

(iii) exceed targeted or planned

d) Percentage of Net Profit/Gross Written Premium

2. Gross or Net Written Premium

3. Expense Ratio and other operating ratio such as Loss Ratio, Commission

Ratio, Retention Ratio, etc

4. Balance Sheet:

a) Existing Form 8 - Percentage of total Assets/Total Liabilities - Policy liabilities

5. Solvency Margin or Capital Adequacy Ratio - New Form 20

6. Productivity Ratio - such as Gross Written Premium/Headcount;

Income/Management Expenses

Recommended