Embed Size (px)

Citation preview

Hol van Magyarorszag helyea globalis beszallıtoi lancban?

Koren MiklosCEU es MTA KRTK

Dr. Gaspar PalKozgazdasagtudomanyi Emlekalapıtvany

2016

Bevezetes

A masodik szetvalas

“Globalization’s second unbundling” (Baldwin)

1. A globalizacio elso szetvalasa:I A csokkeno szallıtasi koltsegek hatasara a termeles es a

fogyasztas szetvalik egymastol.I Vasut, gozhajo, kontener, repulogep.

2. A masodik szetvalas:I A csokkeno kommunikacios koltsegek hatasara a termeles

szetvalik a tervezestol es iranyıtastol.I A beszallıtoi lancok globalissa valnak (GBL).

1

A masodik szetvalas

“Globalization’s second unbundling” (Baldwin)

1. A globalizacio elso szetvalasa:I A csokkeno szallıtasi koltsegek hatasara a termeles es a

fogyasztas szetvalik egymastol.I Vasut, gozhajo, kontener, repulogep.

2. A masodik szetvalas:I A csokkeno kommunikacios koltsegek hatasara a termeles

szetvalik a tervezestol es iranyıtastol.I A beszallıtoi lancok globalissa valnak (GBL).

1

A kontener lecsokkentette a tavolsagot termelo esfogyaszto kozott

2

Izzo-ar egy magyar webshopban

3

Egy hasonlo kınai izzo szallıtassal egyutt negyedannyibakerul

4

Miben mas a GBL-ok idoszaka?

1. Az iparosodas konnyebb es gyorsabb.I Nincs szukseg nagy, tokeintenzıv iparfejlesztesre.I Eleg egy meglevo GBL-hoz csatlakozni.

2. De kevesebbet jelent.I Az exportsiker kevesbe meri a hazai teljesıtmenyt.I A technologia nem biztos, hogy atterjed.

3. Gazdasagpolitikai kihıvasok.

4. Nyitott kerdesek.

5

Miben mas a GBL-ok idoszaka?

1. Az iparosodas konnyebb es gyorsabb.I Nincs szukseg nagy, tokeintenzıv iparfejlesztesre.I Eleg egy meglevo GBL-hoz csatlakozni.

2. De kevesebbet jelent.I Az exportsiker kevesbe meri a hazai teljesıtmenyt.I A technologia nem biztos, hogy atterjed.

3. Gazdasagpolitikai kihıvasok.

4. Nyitott kerdesek.

5

Miben mas a GBL-ok idoszaka?

1. Az iparosodas konnyebb es gyorsabb.I Nincs szukseg nagy, tokeintenzıv iparfejlesztesre.I Eleg egy meglevo GBL-hoz csatlakozni.

2. De kevesebbet jelent.I Az exportsiker kevesbe meri a hazai teljesıtmenyt.I A technologia nem biztos, hogy atterjed.

3. Gazdasagpolitikai kihıvasok.

4. Nyitott kerdesek.

5

Tenyek

A gazdag orszagok GDP- (es export-) reszesedese csokken(Baldwin 2013)

Trade and Industrialization after Globalization’s Second Unbundling 167

G7 are share- losers over this period.5 Apart from India, all of their manu-facturing sectors are heavily involved in the international supply chains of Japan (the East Asians) or Germany (Poland and Turkey).

The right panel of figure 5.2 suggests that the standard culprit in global-

Fig. 5.1 Globalization changed: G7 share of world income and exportsSources: (Left) World Bank from 1960, Maddison pre- 1960; (middle) WTO online database; (right) UNSTAT online database.

5. Taiwan is not in the UN data used for the calculation, but would almost surely qualify if it were.

Fig. 5.2 Global manufacturing shares and trade cost trendsSources: (Left) unstat.un .org, 2005 prices; 6 EMs = China, India, Indonesia, Thailand, Tur-key, and Poland; Korea (which gained 3 points) is in RoW. (Right) Jacks, Meissner, and Novy (2011).

6

A helyi hozzaadott ertek aranya egyre csokken afeldolgozoipari exportban (Johnson es Noguera 2014)

Figure 1: World VAX Ratio between 1970 and 2009

Figure 2: World VAX Ratio between 1970 and 2009, by Sector

36

7

A GBL-kereskedelem erzekenyebb a tavolsagra (Johnson esNoguera 2014)Figure 12: Panel Regressions with Time-Varying Country Fixed E↵ects

0.0

5.1

.15

.2.2

5

1970 1980 1990 2000 2010

Distance coefficient for VAX ratio

-1.2

-1-.8

-.6

1970 1980 1990 2000 2010

Distance coefficient for value added exportsDistance coefficient for exports

-.1-.0

50

.05

.1.1

5

1970 1980 1990 2000 2010

Contiguity coefficient for VAX ratio

-.6-.4

-.20

.2.4

.6

1970 1980 1990 2000 2010

Contiguity coefficient for value added exportsContiguity coefficient for exports

-.15

-.1-.0

50

.05

1970 1980 1990 2000 2010

Language coefficient for VAX ratio 0.2

.4.6

.8

1970 1980 1990 2000 2010

Language coefficient for value added exportsLanguage coefficient for exports

-.2-.1

5-.1

-.05

0

1970 1980 1990 2000 2010

Colony coefficient for VAX ratio

.2.4

.6.8

1

1970 1980 1990 2000 2010

Colony coefficient for value added exportsContiguity coefficient for exports

Note: See (8) for regression specification. Solid lines indicate time-varying coe�cients on trade costproxies, and dashed lines indicate 90% confidence intervals. Standard errors are clustered by countrypair.

42

8

A kereskedelmi egyezmenyek novelik a GBL-kereskedelemaranyat (Johnson es Noguera 2014)Figure 13: Bilateral Fragmentation Before and After Regional Trade Agreements

.65

.7.7

5.8

.85

.9

-20 -15 -10 -5 0 5 10 15 20Normalized year of adoption of RTA

TreatmentControl

43

9

Az ipari termekek kereskedelme regionalis 1. (Baldwin2013) 170 Richard Baldwin

national supply chains are quite different than selling intermediates (export-ing) to them. The sourcing share rises up to about $25,000 and then declines (figure 5.5, left panel). Selling intermediates falls for low income levels but rises beyond a point near $15,000 (right panel). Combining the two mea-sures, a nation’s total involvement in supply chain is tilde shaped.

While this research is very recent and needs further testing, the top- line message is very intuitive. When a nation like China moved up from making clothing to assembling electronics and machinery, the import content of its exports rose, but at the other extreme, a nation like Finland has all but exited from the fabrication end of manufacturing, so domestic value added content of its exports tends to be higher.

These charts paint a picture of two transformations: one in globalization itself, and one in developing nations’ experiences with industrial exports. The next task is to suggest how the two might be connected.

Fig. 5.4 The tight geographical clustering of manufactures export swingsSource: Author’s calculations on World Bank data.Note: Data for all nations with (1) population over 10 million, (2) manufacturing export share over 50 percent in 2007– 2008, (3) at least 90 percent data coverage from 1985 to 2008.

10

Az ipari termekek kereskedelme regionalis 2. (Baldwin2013) 180 Richard Baldwin

5.2.2 Transformed International Commerce

The second unbundling transformed trade for a very simple reason. Pro-duction dispersion did not end the need to coordinate production stages—it internationalized it (rightmost illustration in figure 5.7). This gave rise to twenty- first century trade—the heart of which might be called the trade- investment- services- intellectual property (IP) nexus (Baldwin 2011). Specifically, the nexus reflects the intertwining of: (a) trade in parts and com-ponents; (b) international movement of investment in production facilities, personnel training, technology, and long- term business relationships; and (c) services to coordinate the dispersed production, especially infrastructure services such as telecoms, Internet, express parcel delivery, air cargo, trade- related finance, customs clearance, and so forth.

The most radical change in terms of theory and outcomes was the way the second unbundling made it easy for rich- nation firms to combine the high technology they developed at home with low- wage workers abroad.

Fig. 5.9 Distance of engine part factories from DetroitSource: www .chicagofed .org, 2005_aos_klier .pdf. 11

Magyarorszag a GBL-ban

Magyarorszagon meg a visegradi orszagoknal isalacsonyabb a hozzaadott ertek aranya az exportban(OECD TiVA)

4050

6070

1995 2000 2005 2010year

EU_15Visegrád_3Magyarország

12

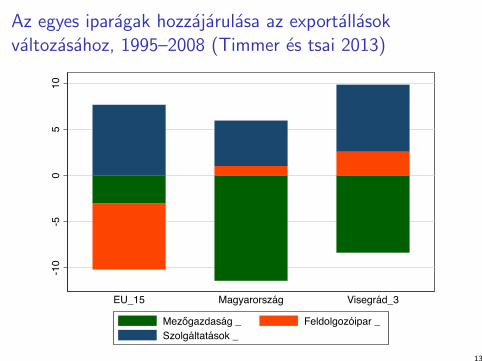

Az egyes iparagak hozzajarulasa az exportallasokvaltozasahoz, 1995–2008 (Timmer es tsai 2013)

-10

-50

510

EU_15 Magyarország Visegrád_3

Mezőgazdaság _ Feldolgozóipar _Szolgáltatások _

13

A GBL-export kereslete az egyes tenyezok irant,1995–2008 (Timmer es tsai 2013)

-20

-10

010

20

EU-15 Magyarország Visegrád-3

Tőke FelsőfokúÉretségizett Alapfokú+szakmunkás

14

Magyar trendek

1. Az export hozzaadott erteke sokkal lassabban novekedett,mint a termekexport.

2. Magyarorszagon meg a visegradi orszagoknal is alacsonyabb ahozzaadott ertek aranya az exportban.

3. Az exportallasok osszesegeben stagnaltak, egyedul aszolgaltatasokban nottek jelentosen.

4. A tenyezok kozul a toke (kulfoldi?) es a magasan kepzettmunkasok nyertek leginkabb.

15

Gazdasagpolitikai kihıvasok

Gazdasagpolitikai kihıvasok

1. A kulkerpolitika nem “piacert piacot,” nem zeroosszegujatszma.

I WTO, Brexit, keleti nyitas

2. A kulker-, befektetes-, ipar- es szellemitulajdon-politikakiegeszıtik egymast.

I mely megallapodasok: TPP, TTIP

3. Uj protekcionista fegyver: helyi (“behind-the-border”)szakpolitika.

I diszkriminacio nehezebben merheto

4. A hosszu GBL megnoveli a komplex szabalyozas koltsegeit.I adminisztracio, szabvanyosıtas, harmonizacio

16

Gazdasagpolitikai kihıvasok

1. A kulkerpolitika nem “piacert piacot,” nem zeroosszegujatszma.

I WTO, Brexit, keleti nyitas

2. A kulker-, befektetes-, ipar- es szellemitulajdon-politikakiegeszıtik egymast.

I mely megallapodasok: TPP, TTIP

3. Uj protekcionista fegyver: helyi (“behind-the-border”)szakpolitika.

I diszkriminacio nehezebben merheto

4. A hosszu GBL megnoveli a komplex szabalyozas koltsegeit.I adminisztracio, szabvanyosıtas, harmonizacio

16

Gazdasagpolitikai kihıvasok

1. A kulkerpolitika nem “piacert piacot,” nem zeroosszegujatszma.

I WTO, Brexit, keleti nyitas

2. A kulker-, befektetes-, ipar- es szellemitulajdon-politikakiegeszıtik egymast.

I mely megallapodasok: TPP, TTIP

3. Uj protekcionista fegyver: helyi (“behind-the-border”)szakpolitika.

I diszkriminacio nehezebben merheto

4. A hosszu GBL megnoveli a komplex szabalyozas koltsegeit.I adminisztracio, szabvanyosıtas, harmonizacio

16

Gazdasagpolitikai kihıvasok

1. A kulkerpolitika nem “piacert piacot,” nem zeroosszegujatszma.

I WTO, Brexit, keleti nyitas

2. A kulker-, befektetes-, ipar- es szellemitulajdon-politikakiegeszıtik egymast.

I mely megallapodasok: TPP, TTIP

3. Uj protekcionista fegyver: helyi (“behind-the-border”)szakpolitika.

I diszkriminacio nehezebben merheto

4. A hosszu GBL megnoveli a komplex szabalyozas koltsegeit.I adminisztracio, szabvanyosıtas, harmonizacio

16

Nyitott kerdesek

Kutatasi kerdeseim:

1. Tanulunk-e a fejlett technologia kolcsonzese soran?

2. Miert csokkenti erosebben a tavolsag a GBL-kereskedelmet?

17

Tanulas

I Kozep-europai Beszallıtoi Felmeres (Bekes, Koren, Murakozyes Telegdy)

I 600-600 vallalat Magyarorszagon, Romaniaban esSzlovakiaban

I beszallıtoi es vevoi kapcsolatok, kovetelmenyek, tanulas

I Kibol lesz multi-beszallıto?

I Miben fejlodnek a beszallıtok?

18

Tanulas

I Kozep-europai Beszallıtoi Felmeres (Bekes, Koren, Murakozyes Telegdy)

I 600-600 vallalat Magyarorszagon, Romaniaban esSzlovakiaban

I beszallıtoi es vevoi kapcsolatok, kovetelmenyek, tanulas

I Kibol lesz multi-beszallıto?

I Miben fejlodnek a beszallıtok?

18

Tavolsag

I Az uzleti utazas hatasa a kulfoldi befektetesekre es akulkereskedelemre (Bekes, Javorcik es Koren)

I A Malev csodjevel tobb varossal megszunt a kozvetlen legiosszekottetes.

I Hogyan alakult a befektetes es kereskedelem ezek[be/bol] avarosok[ba/bol]?

19

Tavolsag

I Az uzleti utazas hatasa a kulfoldi befektetesekre es akulkereskedelemre (Bekes, Javorcik es Koren)

I A Malev csodjevel tobb varossal megszunt a kozvetlen legiosszekottetes.

I Hogyan alakult a befektetes es kereskedelem ezek[be/bol] avarosok[ba/bol]?

19

Osszegzes

Osszegzes

I Magyarorszag elhelyezkedesenel fogva nagyon szorosanintegralodik az Europa Gyarba.

I Meddig?I Mit tanulunk belole?

I A kereskedelem- es fejlesztes-politika sokkal komplexebb aGBL-ok rendszereben.

I A hagyomanyos “harcos” kulkerpolitika kontraproduktıv lehet.I A GBL nem elsosorban szakmunkasokra teremt keresletet.

20