Embed Size (px)

Citation preview

TRADITIONALTRADITIONALPFM IS DEADPFM IS DEADWelcome to the New World ofDigital Money Management

You’ve seen theYou’ve seen themoney that financialmoney that financialinstitutions areinstitutions areinvesting in digital.investing in digital.

Bank of America CEO said they spend $500

million per year on their mobileonline platform and will continue toinvest at that rate.

BrianMoynihan

You know what’sYou know what’shappening in Siliconhappening in SiliconValley and LondonValley and Londonright now.right now.

“Global fintech investmentjumped

.”- CB INSIGHTS & ACCENTURE

201% between 2013and 2014

And you know thatAnd you know thatbanking models arebanking models arefundamentallyfundamentallychanging.changing.

“By 2020, more than 30 percentof banking revenues could be atrisk due to new competitorsand trends.”- ACCENTURE

Financial institutionsFinancial institutionsneed to get ahead ofneed to get ahead ofthese changes bythese changes byempowering theirempowering theiraccount holders.account holders.

“We need to reimagine how banks cantruly enrich customers’ lives.”

- BRADLEY LEIMER, HEAD OF INNOVATION, SANTANDER BANK U.S.

Banks and creditBanks and creditunions are recognizingunions are recognizingthe importancethe importanceof financialof financialempowerment.empowerment.

On a macro level, Americaneeds help.

Total student loan debt is now worthover $1 trillion

Healthcare costs are soaring

62% of Americans do not have anemergency fund to cover evenminor calamities

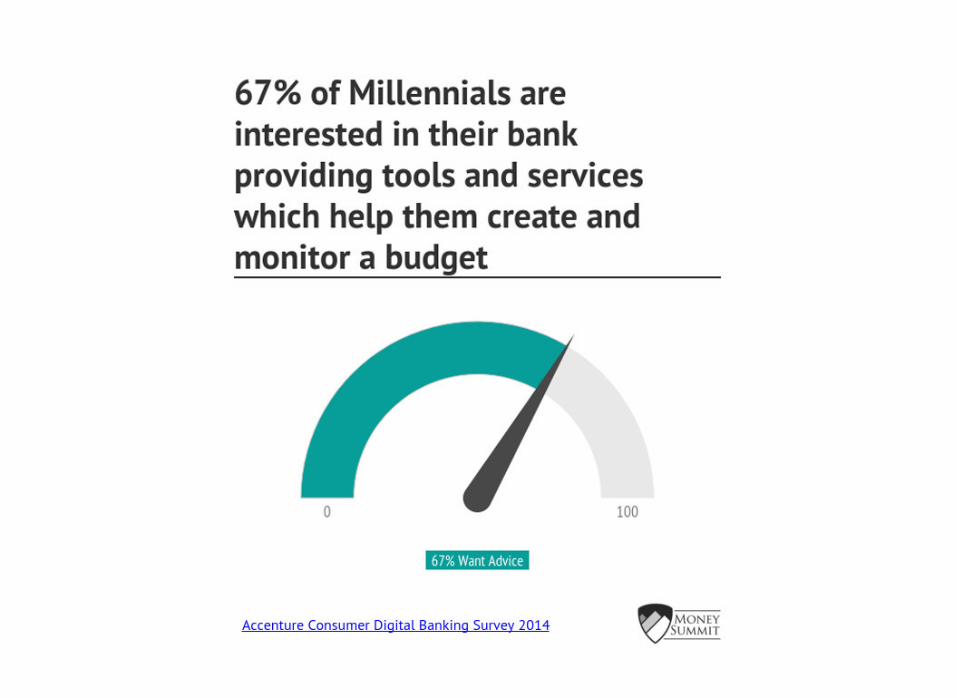

Americans are trying toAmericans are trying tomanage their finances,manage their finances,but they're not usingbut they're not usingthe best methods.the best methods.

82% of consumers keep track oftheir finances in some way, butover half do it through pen andpaper (36%) or in their head (18%)!

Financial institutionsFinancial institutionsneed to be at the heartneed to be at the heartof helping consumersof helping consumersmanage their financialmanage their financiallives better.lives better.

This is the futureThis is the futurebanking model!banking model!

“If you provide account holders withinsight, recommendations, andadvice, you build trust.”-MARK SCHWANHAUSSER, DIRECTOR OF OMNICHANNELFINANCIAL SERVICES, JAVELIN STRATEGY & RESEARCH

Some financialSome financialinstitutions say, “butinstitutions say, “butwe’ve tried PFM!”we’ve tried PFM!”

Traditional PFM hasn’tbeen effective because theexperience is broken.

Here’s why…

First of all,First of all,traditional PFM hastraditional PFM hasbeen hidden away,been hidden away,deep into a tab.deep into a tab.

That means account holderscan’t find it!

Secondly, it reliesSecondly, it relieson single-sourceon single-sourceaggregation.aggregation.

This means that if the singleconnection to the data providerbreaks, the account holder mustwait days, weeks, or even monthsfor their account and transactionsto update!

Third, data isThird, data isineffectively cleansed.ineffectively cleansed.

Most transaction feedstypically consist of a messystring of random-lookingcharacters:

COSTCxx 04ROCHESTERXXX726 XXX-XXX-1189 XXX027

What is an account holdersupposed to do with that mess?

Fourth,Fourth,transactions aretransactions areineffectivelyineffectivelycategorized.categorized.

If you’ve ever used standard PFMsolutions on the web, you know thepain of poor categorization.

Here is how two well knowntraditional PFM providers perform:

Fifth, the user hasFifth, the user hasto do too muchto do too muchwork themselves.work themselves.

If users have to set their ownbudget amounts or do multiplecalculations to see how theirfinances are tracking for themonth, they are not going to usethat PFM product.

“For the most part, a person’sobjective in decision making is toarrive at the best possible decisionoutcome with the least possibleeffort.”

-COLLEEN ROLLER, VP OF USABILITY ENGINEERING /DECISION ARCHITECTURE, BANK OF AMERICA

Lastly, PFM has failedLastly, PFM has failedbecause of unimaginativebecause of unimaginativeuser experience.user experience.

“Most financial service UIs are based onan accounting paradigm, which is notsurprising since that is how we are alltrained to think about our finances.”-MOHAMMAD KHALIL, HEAD OF PRODUCT,DATA & MARKETING, MOVEN

So how is digitalSo how is digitalmoney managementmoney management(DMM) different?(DMM) different?

“Over time, we believe moneymanagement will become notjust a feature of digital bankingbut digital banking itself.”-FORRESTER RESEARCH

According to Mapa research, manyPFM solutions globally are similar.In the examples that stood out,what was most distinctive was theability to facilitate integration andincrease both intuition andengagement.

With us so far? ;) Here’sWith us so far? ;) Here’swhat account holderswhat account holdersare looking for in DMM.are looking for in DMM.

A simple, personal andconvenient experiencethat is secure and works

A way to monitor allaccounts in one place

Anywhere, anytime access

View-it-and-do-it functionality

Predictive and advice-driven data

DMM best practice #1:DMM best practice #1:A simple, personalA simple, personaland convenientand convenientexperience that isexperience that issecure and workssecure and works

“Our emphasis has been rethinkingfinancial service UIs to accommodatenew paradigms that are eerilyfamiliar. These paradigms attempt tosimplify complex data or processesinto highly consumable interactionsthat are intuitive to the user.”-MOHAMMAD KHALIL, THE HEAD OF PRODUCT,DATA & MARKETING AT MOVEN

DMM best practice #2:DMM best practice #2:A way to monitor allA way to monitor allaccounts in one placeaccounts in one place

Celent Research found that 75percent of account holders saidthat the ability to view all theirfinances in one place was “highlyvaluable.”

DMM best practice #3:DMM best practice #3:Anywhere, anytimeAnywhere, anytimeaccessaccess

With smartphones enablingon-the-go services,consumers have an always-on mentality.

DMM best practice #4:DMM best practice #4:View-it-and-do-itView-it-and-do-itfunctionalityfunctionality

Consumers want clear, conciseinsights where they can see howtheir finances are tracking and theneasily be able to take action from it.

-RICK CLAYPOOLE, DIRECTOR, RETAIL PRODUCTMANAGEMENT AND MARKETING AT CADENCE BANK

"It has to be a very elegant solutionthat makes it very easy for clients toget smart about their financiallives."

DMM best practice #5:DMM best practice #5:Shift from historical toShift from historical topredictive and advice-predictive and advice-driven datadriven data

“Banks traditionally provide historicdata, such as last month’s bankstatement. We on the other hand willuse forward-looking data, such asnext month’s bank statement.”-ANTHONY THOMSON, THE FOUNDER ANDCHAIRMAN OF ATOM BANK

Now that you know whatNow that you know whata great DMM experiencea great DMM experiencelooks like, it’s time tolooks like, it’s time tounderstand how to getunderstand how to getthe most out of it!the most out of it!

4 steps to DMM success:

Tighter integration

Ongoing staff training

Continuous feedback

Better marketing and education

DMM success tip #1:DMM success tip #1:Tighter integration ofTighter integration ofDMM into homepageDMM into homepageand out of a tab leadsand out of a tab leadsto higher engagementto higher engagement

MACU Case Study:

40% adoption: After switching from PFM toDMM, adoption skyrocketed.

2x external accounts added daily: Once digitalmoney management was integrated into thehomepage, the number of external accountsadded daily more than doubled.

DMM success tip #2:DMM success tip #2:Better marketingBetter marketingand educationand education

“The marketing materials werecrucial in making Clarity [the namethey gave their DMM white-labelproduct] part of our brand... itsignificantly helped our adoptionrate and increased word of mouth.”

-RACHAEL SCHWARTZ, ELECTRONIC MARKETINGSPECIALIST OF FARMERS BANK & TRUST

Created an advertising campaign throughvarious marketing channels, including in thesidebar next to the customers' transactions

Used instructional videos to explainthe product's benefits

In order to increase adoption,Farmers Bank & Trust

Integrated the product into online banking,making the enrollment process easy

Helped users auto-populate their budgets

Created iPad prize draws to encourageusers to log in and use it

DMM success tip #3:DMM success tip #3:Ongoing staff trainingOngoing staff training

“The most effective training inspiresemployees to use the moneymanagement solution for themselves.”

-ERIN CALDWELL, TRAINING DIRECTOR, MX

DMM success tip #4:DMM success tip #4:Continuous feedbackContinuous feedback

“Société Générale in France ... not only solicits ideasfrom customers but also asks for their feedback onnew developments and asks them to vote to prioritizedifferent improvements.”

-FORRESTER RESEARCH

And finally… howAnd finally… howsuccessful hassuccessful hasDMM been?DMM been?Check out the and

MACU case study herethe Insight and Target case study here.

Empowering your account holders' financiallives through digital money management

Learn more at MX.com

Share