Embed Size (px)

Citation preview

Imperial Business in the City

The Long Term Underperformance of

the Chinese Stock Market, the

implications for UK investors

Prof. Franklin Allen

Professor Franklin AllenExecutive Director of the Brevan Howard Centre

Franklin Allen is the Executive Director

of the Brevan Howard Centre and

Professor of Finance and Economics at

Imperial College London. He received

his doctorate from Oxford University.

Dr. Allen's main areas of interest are

corporate finance, asset pricing, financial

innovation, comparative financial

systems, and financial crises.

The Long Term Underperformance of the

Chinese Stock Market and the Implications for

UK investors

Franklin Allen

Imperial College London

(Based on joint work with Jun Qian, Chenyu Shan and

Lei Zhu)

Imperial Business in the City

28 September 2016

Imperial means Intelligent BusinessImperial College Business School 4

Motivation

• China’s economic growth ‘miracle’:

– GDP growth rates highest among large countries over the past 3 decades

– Size of GDP overtook that of the US in 2014 (PPP terms, IMF’s World

Economic Outlook)

– Will double the size of US around 2035 (PPP) as long as its growth rate

remains twice as high as that of the US

• Development of China’s stock market:

– Started in 1990: ‘help SOEs to privatize and raise funds’

– Stock exchanges in Shanghai, Shenzhen; plus Hong Kong

– Total market cap second largest in the world (behind US)

Imperial means Intelligent BusinessImperial College Business School 5

Ranking Exchanges (2014) MktCap (US$M) Turnover

1 NYSE 19,351,417.2 82.00%

2 NASDAQ OMX 6,979,172.0 175.34%

3 Japan Exchange Group - Tokyo 4,377,994.4 124.35%

4 Shanghai SE 3,932,527.7 154.74%

5 Euronext 3,319,062.2 58.81%

6 Hong Kong Exchanges 3,233,030.6 47.04%

7 TMX Group 2,093,696.8 67.26%

8 Shenzhen SE 2,072,420.0 286.67%

9 Deutsche Börse 1,738,539.1 84.54%

10 BSE India 1,558,299.7 7.91%

11 National Stock Exchange India 1,520,925.1 41.62%

12 SIX Swiss Exchange 1,495,314.2 53.27%

China’s Stock Market

Imperial means Intelligent BusinessImperial College Business School 6

Buy-and-hold Returns of Major Stock Indices (1992-2014; inflation adjusted; cash dividends included)

0.0

1.0

2.0

3.0

4.0

5.0

6.0

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

SSE China S&P500 US BSE SENSEX Inida

IBOV Brazil Nikkei Japan

Imperial means Intelligent BusinessImperial College Business School 7

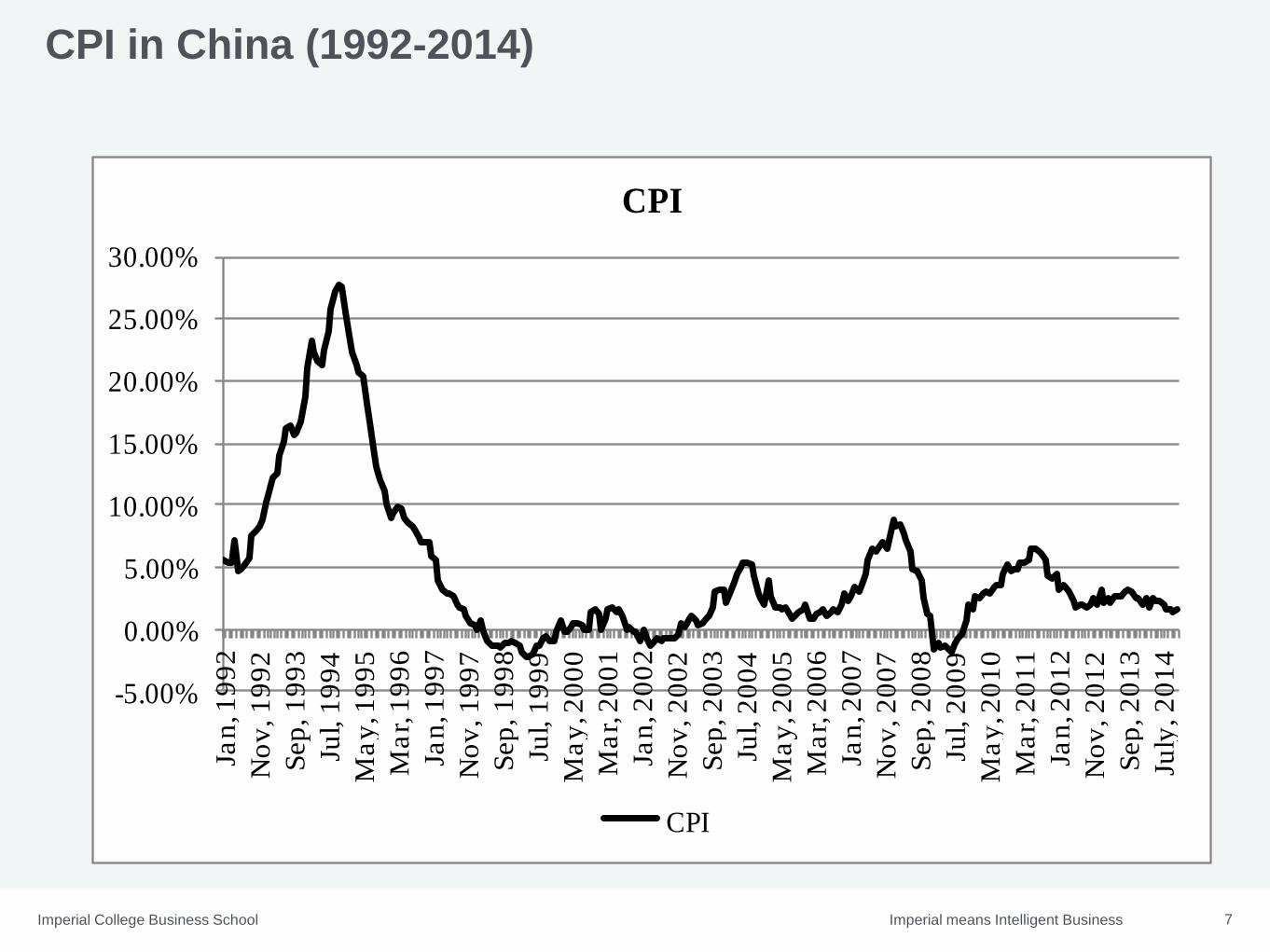

CPI in China (1992-2014)

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%Ja

n, 1

99

2

No

v, 1

99

2

Sep

, 1

99

3

Jul, 1

99

4

Ma

y, 1

99

5

Ma

r, 1

99

6

Jan

, 19

97

No

v, 1

99

7

Sep

, 1

99

8

Jul, 1

99

9

Ma

y, 2

00

0

Ma

r, 2

00

1

Jan

, 20

02

No

v, 2

00

2

Sep

, 2

00

3

Jul, 2

00

4

Ma

y, 2

00

5

Ma

r, 2

00

6

Jan

, 20

07

No

v, 2

00

7

Sep

, 2

00

8

Jul, 2

00

9

Ma

y, 2

01

0

Ma

r, 2

01

1

Jan

, 20

12

No

v, 2

01

2

Sep

, 2

01

3

July

, 2

01

4

CPI

CPI

Imperial means Intelligent BusinessImperial College Business School 8

GDP Growth in Large Countries(2000-2014; inflation adjusted)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Panel B. Real GDP in Large Countries from 2000 to 2014

China United States India Brazil Japan

Imperial means Intelligent BusinessImperial College Business School 9

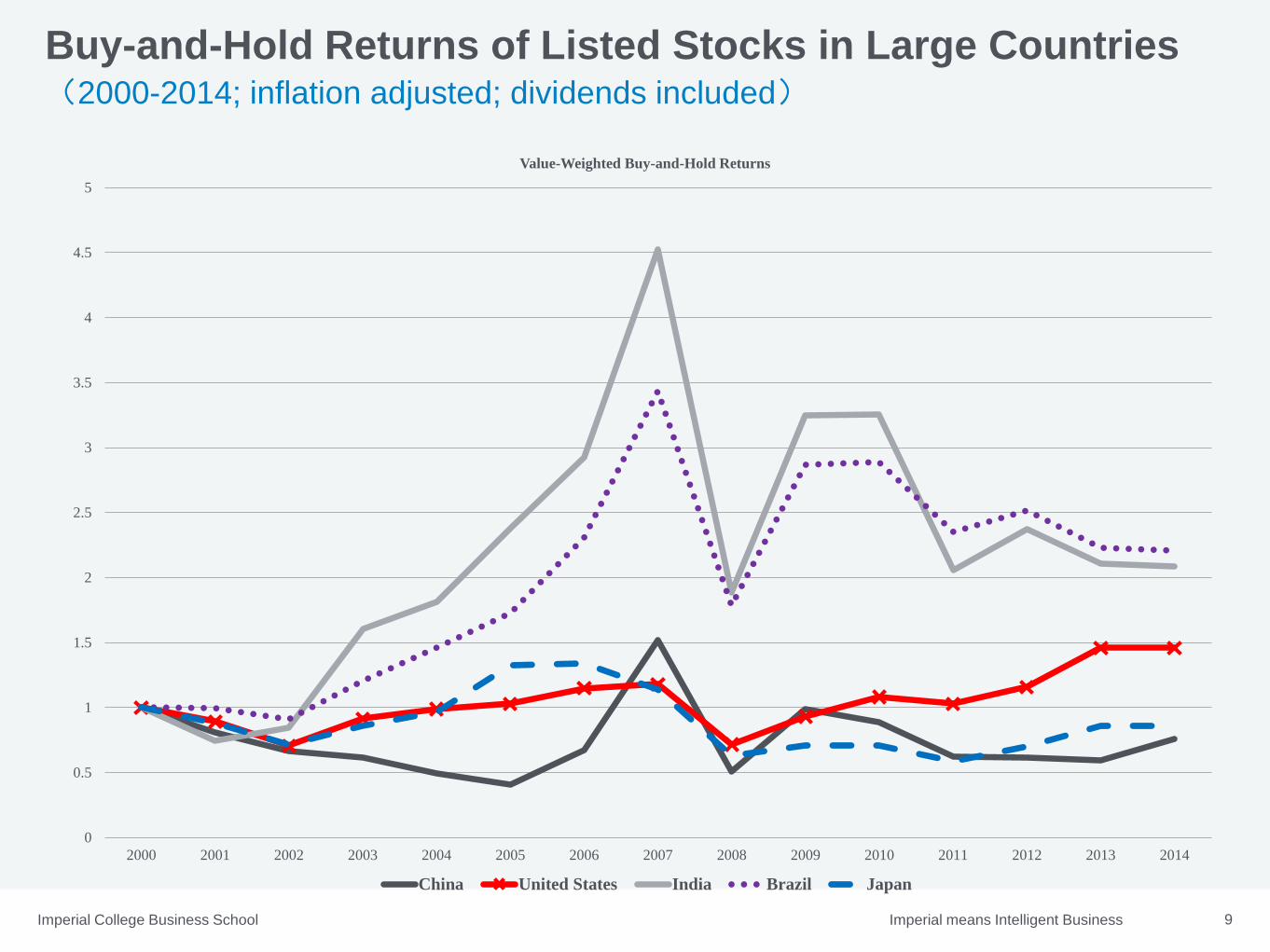

Buy-and-Hold Returns of Listed Stocks in Large Countries (2000-2014; inflation adjusted; dividends included)

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Value-Weighted Buy-and-Hold Returns

China United States India Brazil Japan

Imperial means Intelligent BusinessImperial College Business School 10

Buy-and-hold Returns of Stocks vs. Bank Deposits in China(2000-2014;inflation adjusted)

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Demand Deposit 1-Year Deposit 5-Year Deposit Buy-and-Hold Stock Returns

Imperial means Intelligent BusinessImperial College Business School 11

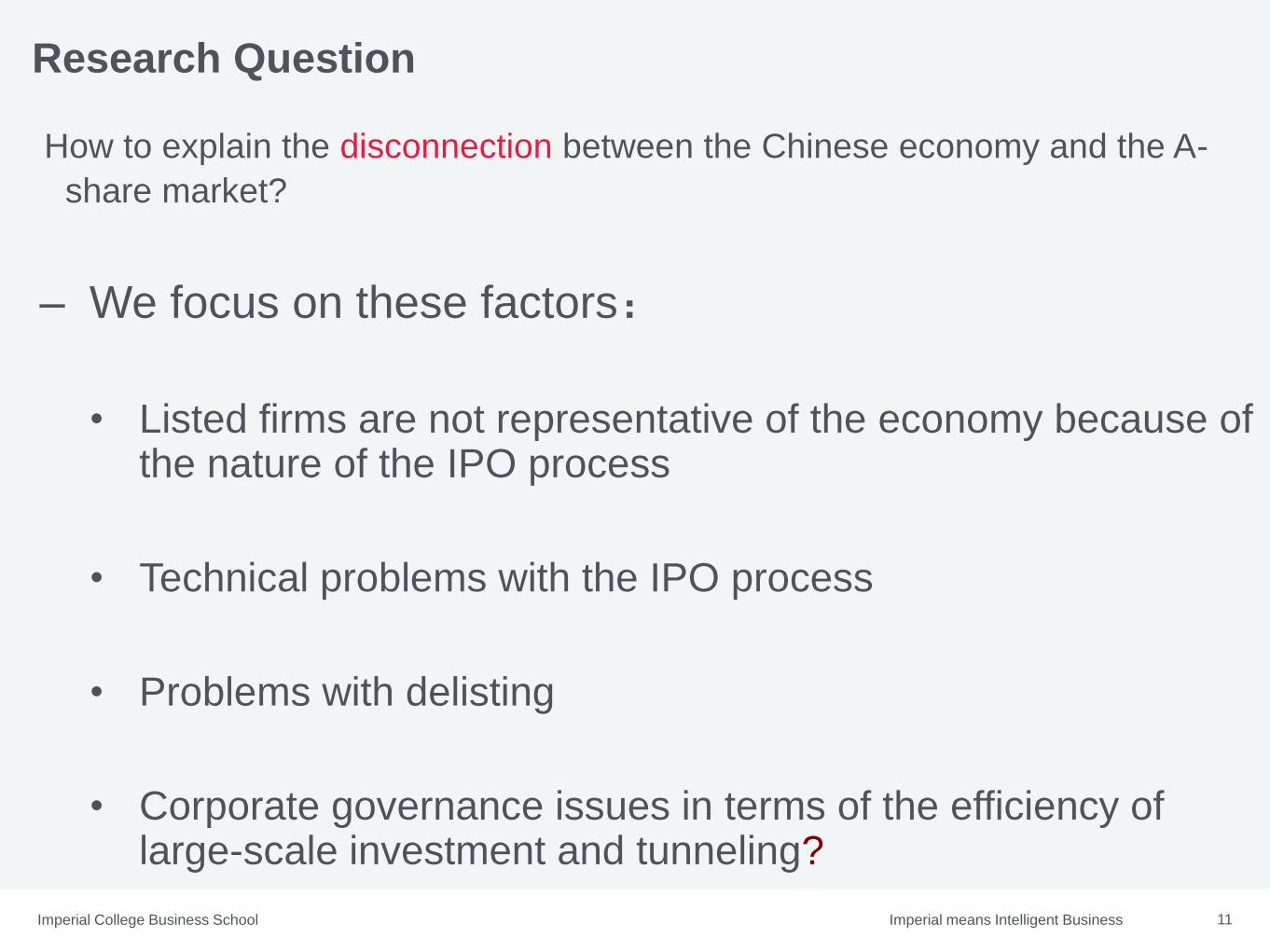

Research Question

How to explain the disconnection between the Chinese economy and the A-

share market?

– We focus on these factors:

• Listed firms are not representative of the economy because of the nature of the IPO process

• Technical problems with the IPO process

• Problems with delisting

• Corporate governance issues in terms of the efficiency of large-scale investment and tunneling?

Imperial means Intelligent BusinessImperial College Business School 12

Correlation between 5-Year Stock Returns and Future Growth

IMF GDP Ranking Country

Individual Stock

or Index Returns Sample Period Correlation p-value

1 United States Stock Return 1991-2014 0.565*** 0.004

2 China Stock Return 1991-2014 0.012 0.958

3 Japan Stock Return 1991-2014 0.418** 0.046

4 Germany Stock Return 1991-2014 0.697*** <0.001

5 United Kingdom Stock Return 1991-2014 0.322 0.133

6 France Stock Return 1991-2014 0.602*** 0.003

7 Brazil Stock Return 1995-2014 0.560** 0.012

8 Italy Stock Return 1991-2014 0.286 0.195

9 India Stock Return 1991-2014 0.573*** 0.006

10 Russian Federation Stock Return 1996-2014 0.547** 0.032

11 Canada Stock Return 1991-2014 0.524** 0.014

12 Australia Stock Return 1991-2014 0.469** 0.023

13 South Korea Index Return 1991-2014 -0.156 0.793

14 Spain Stock Return 1991-2014 0.593*** 0.002

15 Mexico Stock Return 1991-2014 0.322 0.143

16 Indonesia Stock Return 1991-2014 0.349 0.121

17 Netherlands Stock Return 1991-2014 0.735*** <0.001

18 Turkey Stock Return 1991-2014 0.414* 0.054

19 Saudi Arabia Index Return 1995-2014 0.196 0.524

20 Switzerland Stock Return 1991-2014 0.288 0.182

21 South Africa Stock Return 1991-2014 0.619*** 0.002

Difference Group Mean of Correlation China

Difference (Other

p-ValueCountries-China)

Developed 0.568 0.012 0.556*** <0.001

Emerging 0.567 0.012 0.555*** <0.001

Imperial means Intelligent BusinessImperial College Business School 13

Level and Growth of Net Income of Chinese Firms by Sector

Panel A. Net Income Percentage

Year SOE/All Listed/All Listed SOE/Listed All

Unlisted Non-

SOE/Unlisted All

2000 53.74% 35.10% 89.94% 65.84%

2001 49.03% 24.96% 94.50% 66.09%

2002 44.10% 24.23% 90.71% 70.81%

2003 43.66% 25.42% 88.31% 71.55%

2004 41.41% 25.85% 89.85% 75.47%

2005 39.58% 23.72% 92.46% 76.87%

2006 39.92% 22.15% 90.26% 74.40%

2007 36.63% 21.20% 86.68% 76.84%

2008 27.98% 17.45% 85.02% 84.07%

2009 26.02% 15.73% 80.97% 84.24%

2010 27.34% 15.14% 79.88% 82.04%

2011 25.65% 14.42% 77.43% 83.08%

2012 23.48% 13.70% 78.17% 85.20%

2013 21.25% 17.62% 79.20% 91.14%

2014 20.01% 19.32% 75.55% 82.31%

Imperial means Intelligent BusinessImperial College Business School 14

Level and Growth of Net Income of Chinese Firms by

Sector (cont.)

Panel B. Net Income Growth

Year All SOE Non-SOE Listed Unlisted

Listed

SOE

Listed

Non-SOE

Unlisted

Non-SOE

2001 0.060 -0.033 0.168 -0.246 0.225 -0.208 -0.588 0.230

2002 0.217 0.095 0.335 0.182 0.229 0.134 0.998 0.317

2003 0.474 0.459 0.485 0.546 0.451 0.505 0.944 0.466

2004 0.424 0.350 0.480 0.448 0.415 0.473 0.257 0.493

2005 0.243 0.188 0.282 0.141 0.279 0.174 -0.152 0.302

2006 0.336 0.347 0.328 0.247 0.363 0.217 0.611 0.319

2007 0.408 0.292 0.486 0.349 0.426 0.295 0.843 0.472

2008 0.128 -0.138 0.282 -0.071 0.182 -0.089 0.044 0.294

2009 0.145 0.064 0.176 0.031 0.168 -0.018 0.311 0.171

2010 0.552 0.631 0.524 0.494 0.563 0.474 0.579 0.522

2011 0.150 0.078 0.176 0.095 0.159 0.061 0.229 0.174

2012 0.005 -0.080 0.035 -0.045 0.014 -0.036 -0.077 0.040

2013 0.104 0.000 0.137 0.420 0.054 0.439 0.353 0.128

2014 0.019 .-0.115 0.019. 0.038 -0.073 -0.010 0.220 0.034.

Average 0.233 0.152 0.279 0.188 0.247 0.172 0.327 0.283

Correlation 0.687*** 0.554** 0.643** 0.390 0.713*** 0.361 0.411 0.627**

P-Value 0.007 0.049 0.018 0.168 0.004 0.204 0.144 0.022

Imperial means Intelligent BusinessImperial College Business School 15

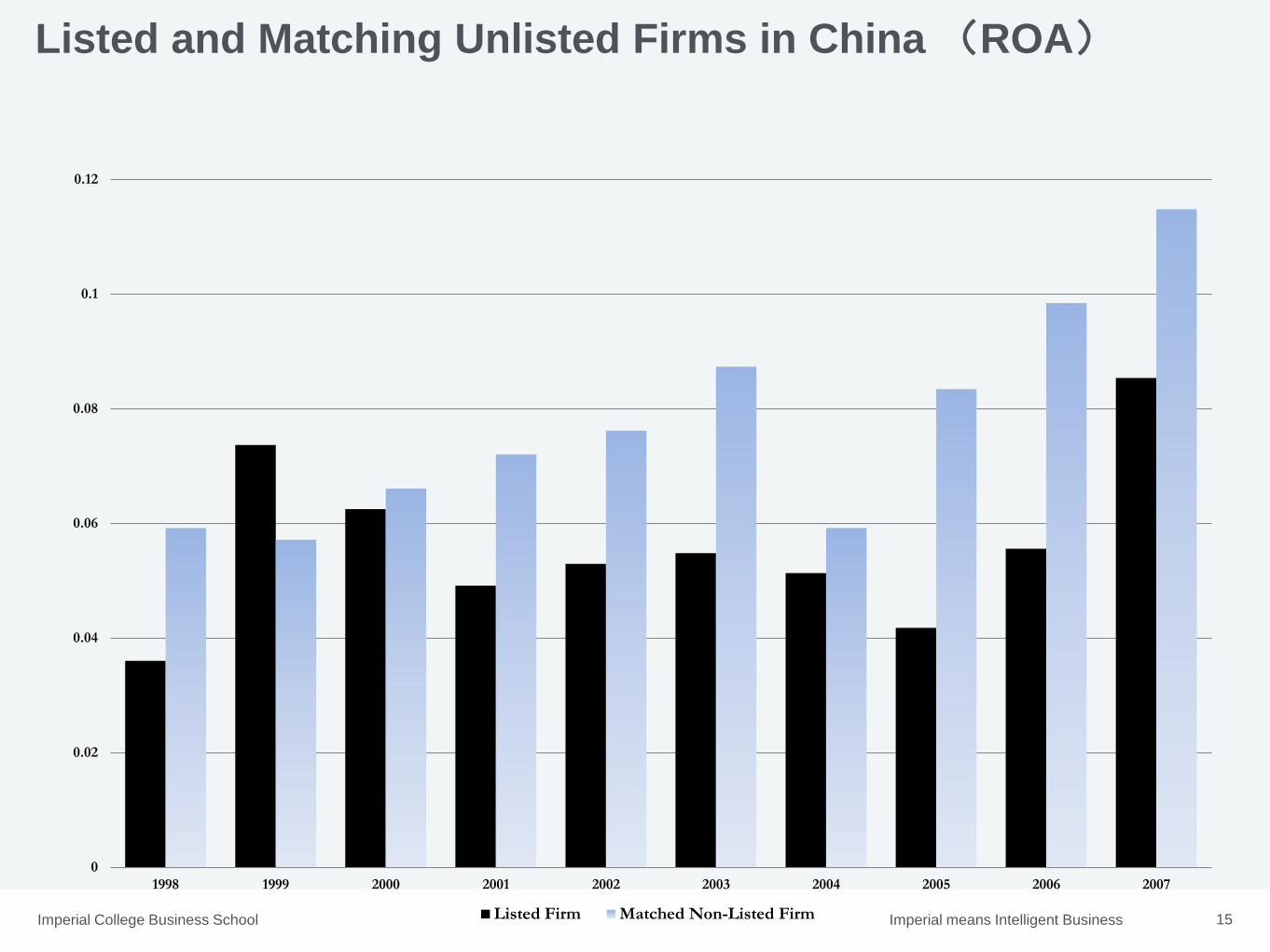

Listed and Matching Unlisted Firms in China (ROA)

0

0.02

0.04

0.06

0.08

0.1

0.12

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Listed Firm Matched Non-Listed Firm

Imperial means Intelligent BusinessImperial College Business School 16

• The evidence in the tables above suggest that the firms that are listed are not representative of

the economy as a whole

• The process for listing is different from other countries. Rather than firms with good prospects

being listed, the process has been political in nature:

– Each IPO must be approved by the CSRC

– In earlier years this took on the form of an explicit quota every year allocated to different

regions across the nation

– One of the main original purposes of the stock market was to provide funds for SOEs so firms

from mature industries with good political connections tended to be listed

• There are also technical problems with the conditions that firms must satisfy to be eligible for

an IPO such as positive earnings for three years prior to listing that lead to distorted incentives

Imperial means Intelligent BusinessImperial College Business School 17

ROA around IPO: Listed firms

0.04

0.05

0.06

0.07

0.08

0.09

0.1

0.11

0.12

0.13

-5 -4 -3 -2 -1 0 1 2 3 4 5

China US India Brazil South Africa

Imperial means Intelligent BusinessImperial College Business School 18

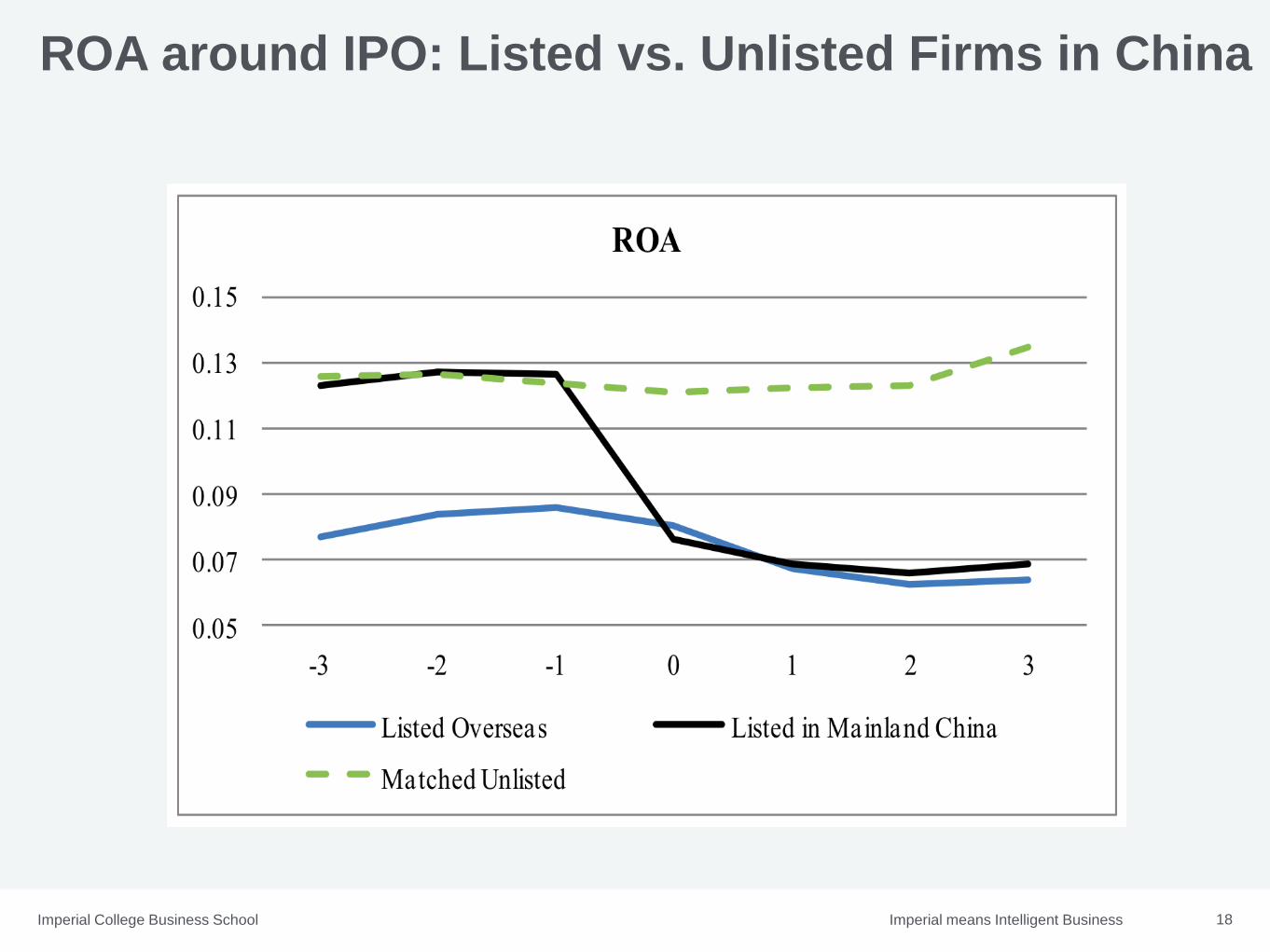

ROA around IPO: Listed vs. Unlisted Firms in China

Imperial means Intelligent BusinessImperial College Business School 19

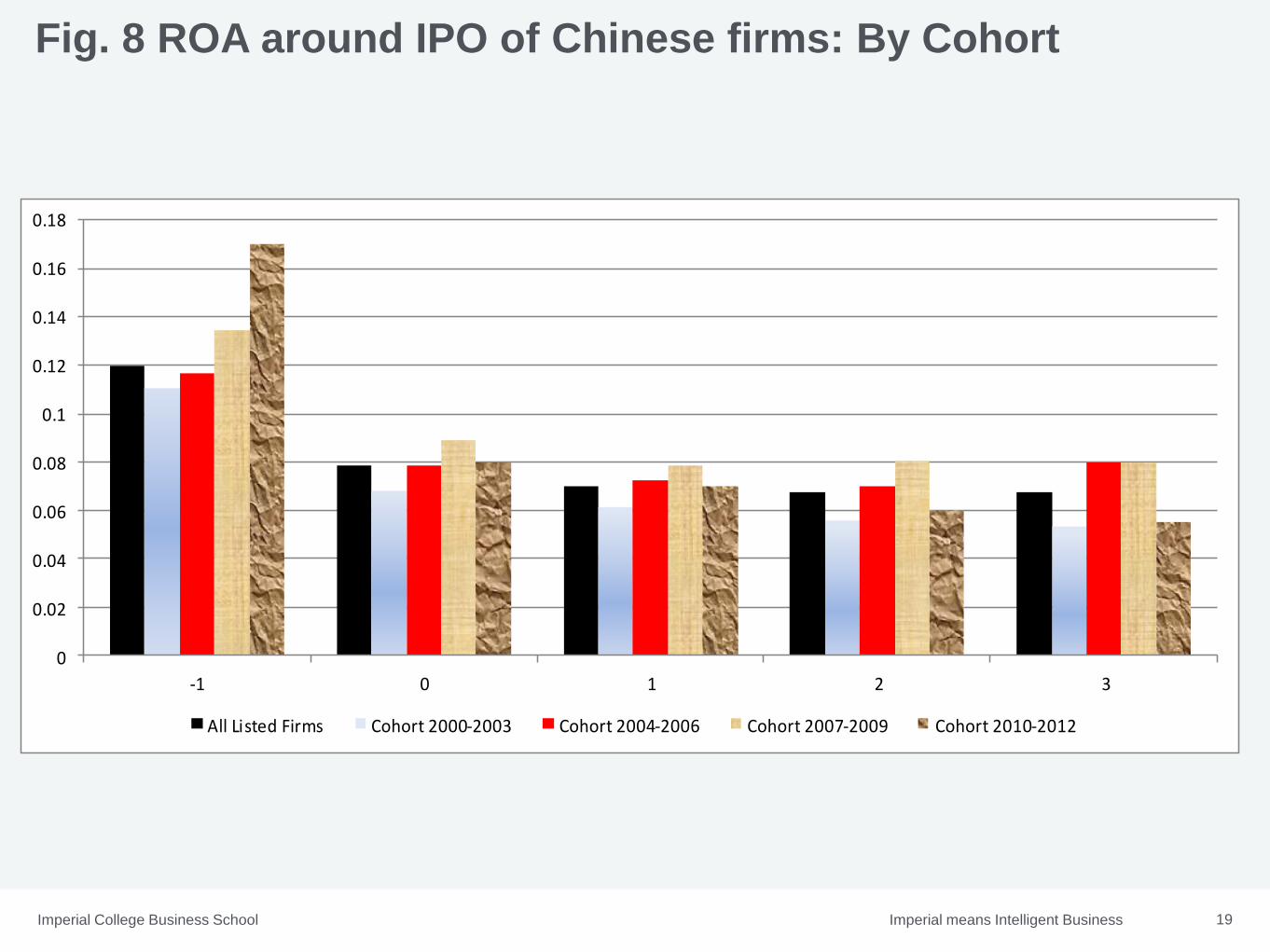

Fig. 8 ROA around IPO of Chinese firms: By Cohort

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

0.16

0.18

-1 0 1 2 3

All Listed Firms Cohort 2000-2003 Cohort 2004-2006 Cohort 2007-2009 Cohort 2010-2012

Imperial means Intelligent BusinessImperial College Business School 20

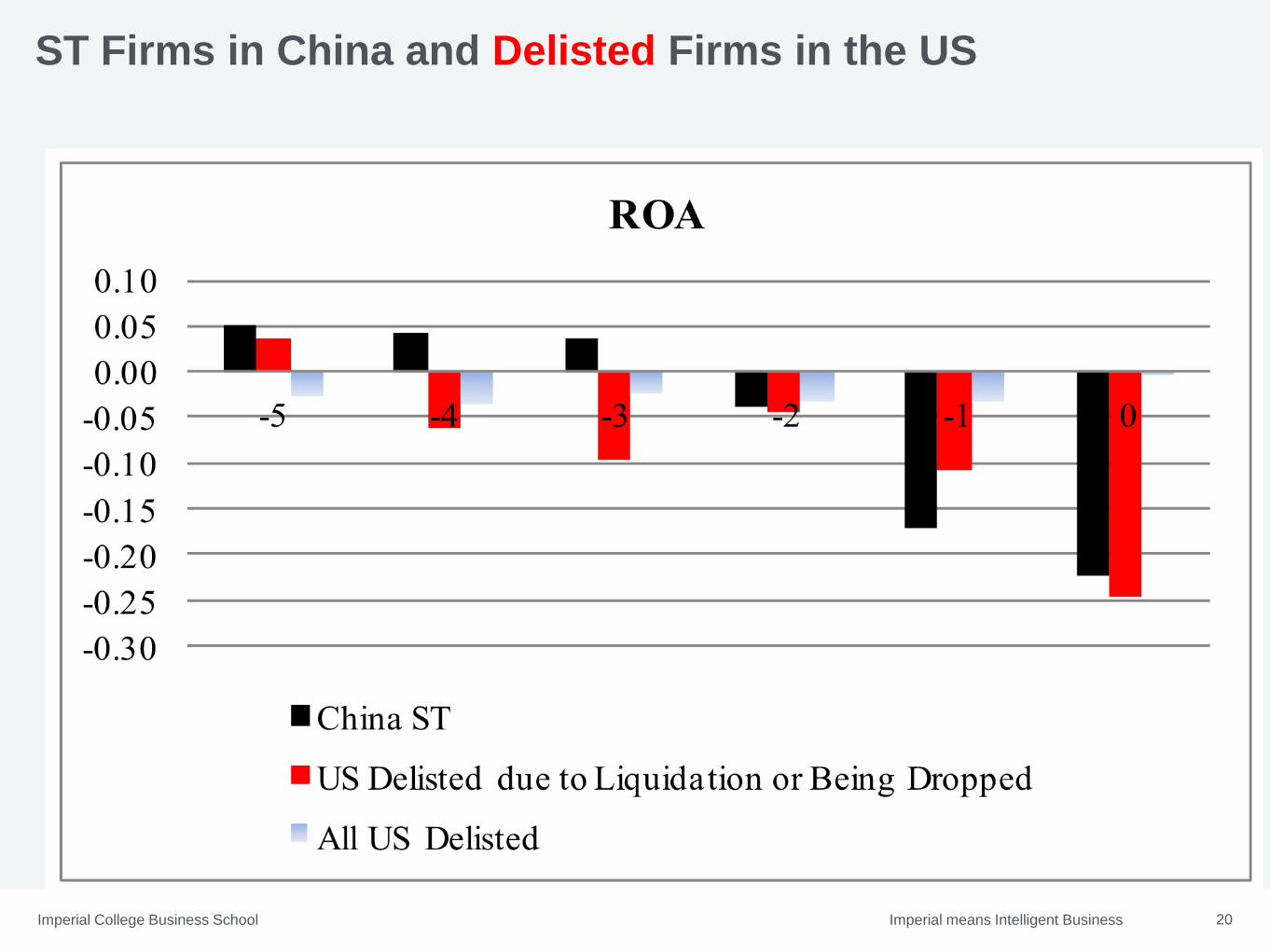

ST Firms in China and Delisted Firms in the US

Imperial means Intelligent BusinessImperial College Business School 21

Comparison of Investment of Listed Firms: Capital Expenditure/Assets

Imperial means Intelligent BusinessImperial College Business School 22

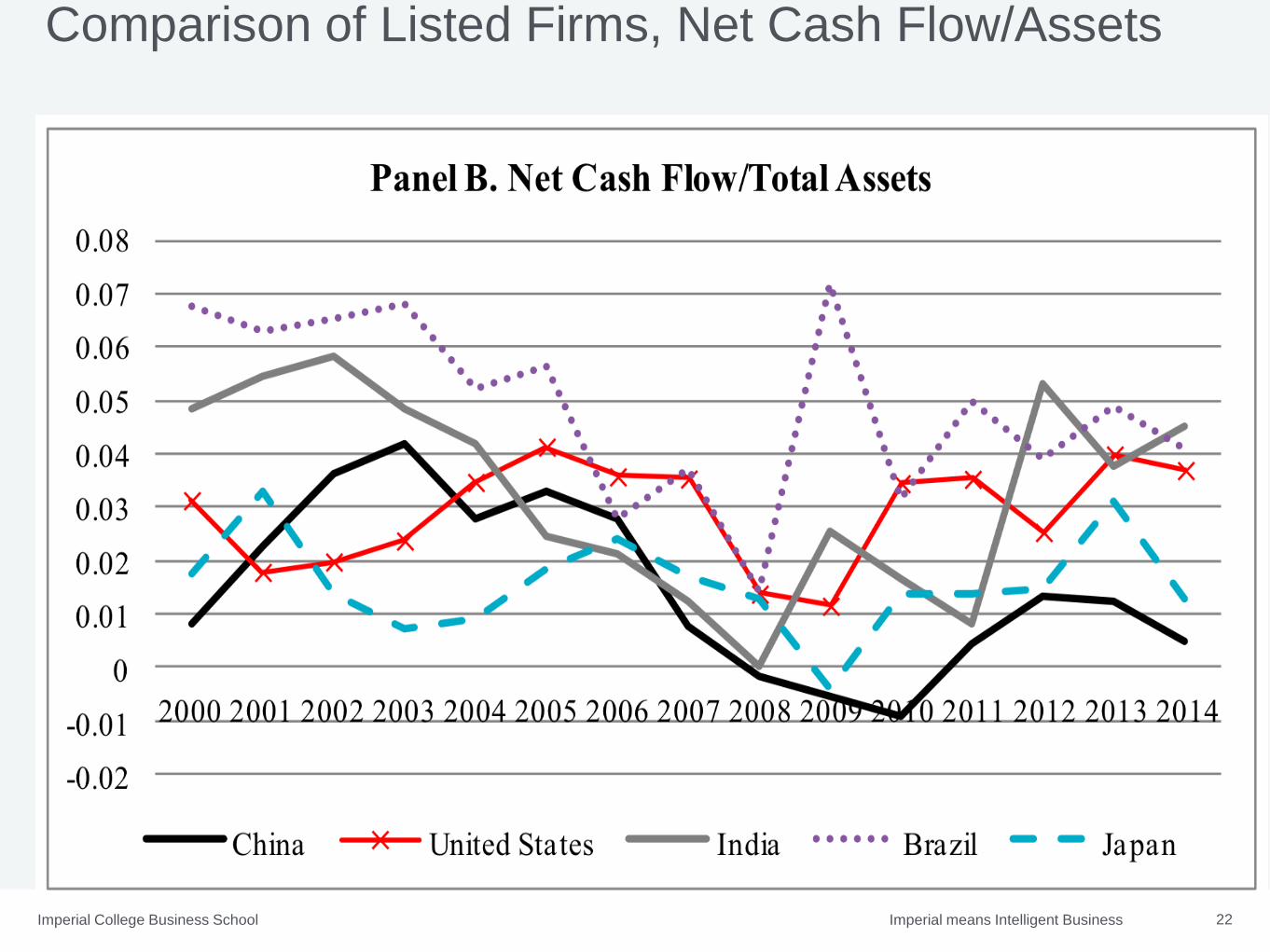

Comparison of Listed Firms, Net Cash Flow/Assets

Imperial means Intelligent BusinessImperial College Business School 23

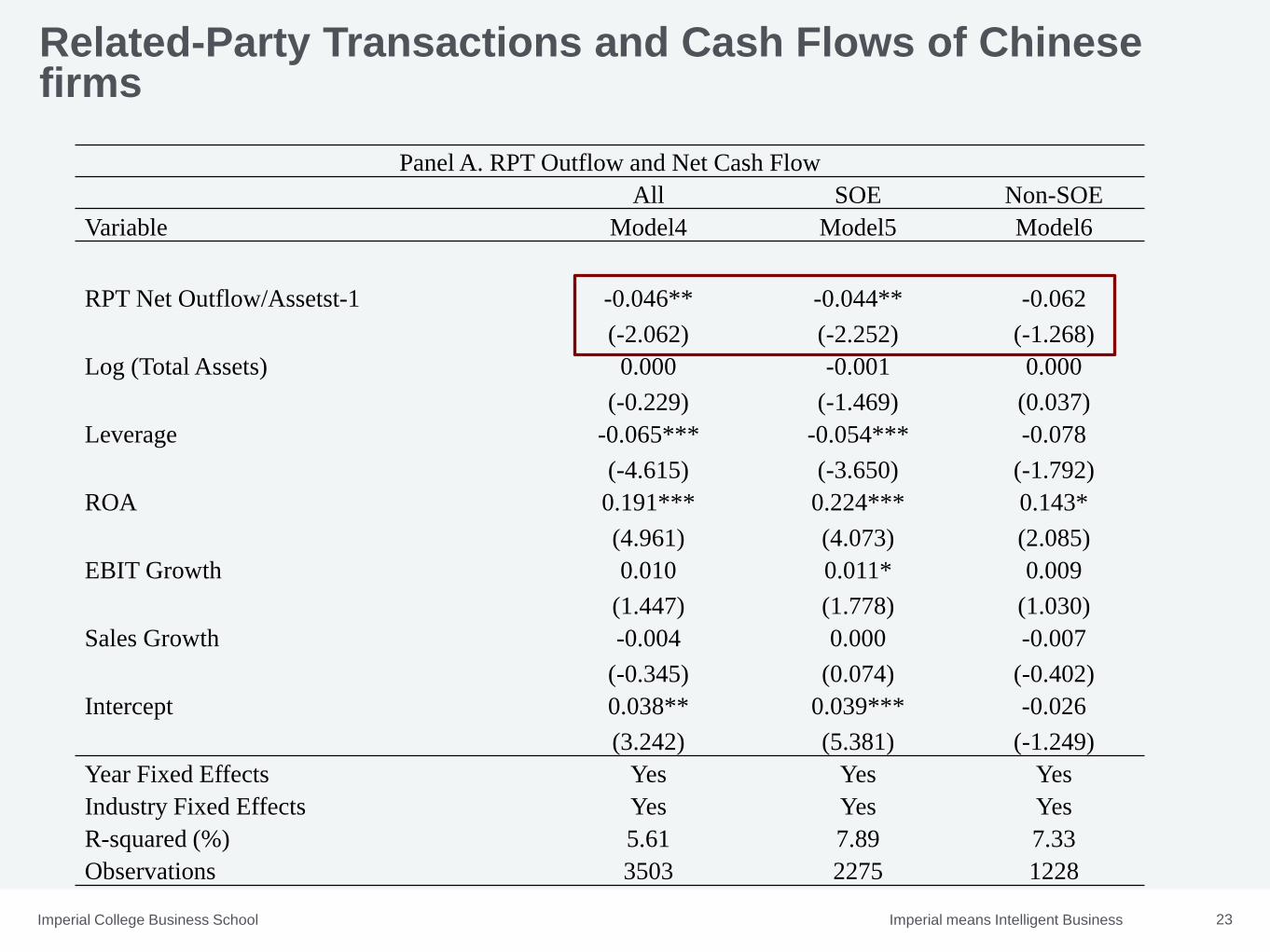

Related-Party Transactions and Cash Flows of Chinese firms

Panel A. RPT Outflow and Net Cash Flow

All SOE Non-SOE

Variable Model4 Model5 Model6

RPT Net Outflow/Assetst-1 -0.046** -0.044** -0.062

(-2.062) (-2.252) (-1.268)

Log (Total Assets) 0.000 -0.001 0.000

(-0.229) (-1.469) (0.037)

Leverage -0.065*** -0.054*** -0.078

(-4.615) (-3.650) (-1.792)

ROA 0.191*** 0.224*** 0.143*

(4.961) (4.073) (2.085)

EBIT Growth 0.010 0.011* 0.009

(1.447) (1.778) (1.030)

Sales Growth -0.004 0.000 -0.007

(-0.345) (0.074) (-0.402)

Intercept 0.038** 0.039*** -0.026

(3.242) (5.381) (-1.249)

Year Fixed Effects Yes Yes Yes

Industry Fixed Effects Yes Yes Yes

R-squared (%) 5.61 7.89 7.33

Observations 3503 2275 1228

Imperial means Intelligent BusinessImperial College Business School 24

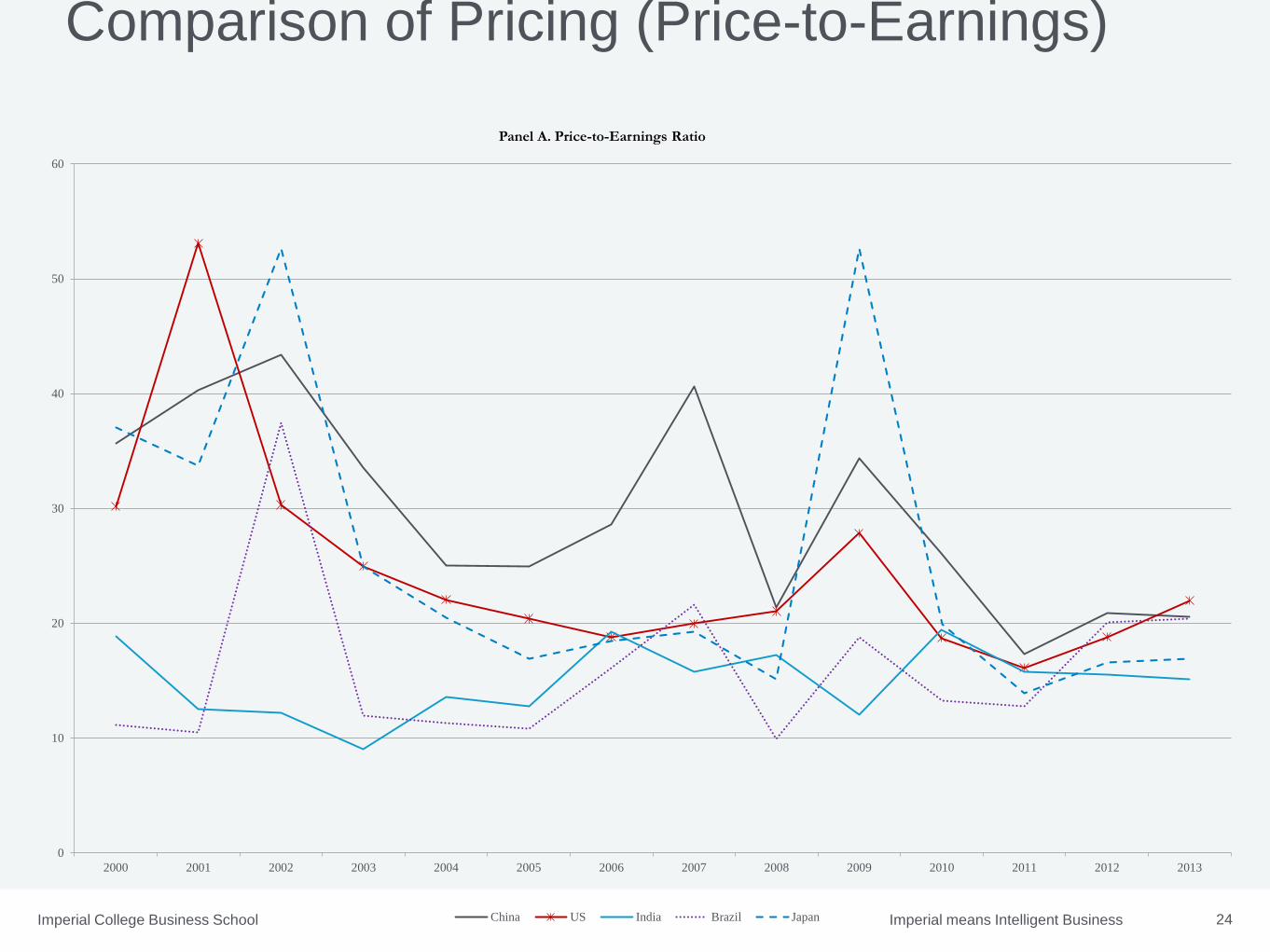

Comparison of Pricing (Price-to-Earnings)

0

10

20

30

40

50

60

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Panel A. Price-to-Earnings Ratio

China US India Brazil Japan

Imperial means Intelligent BusinessImperial College Business School 25

Comparison of Pricing (Market-to-Book)

0

1

2

3

4

5

6

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Panel B. Market-to-Book

China US India Brazil Japan

Imperial means Intelligent BusinessImperial College Business School 26

Concluding remarks

• Disconnection between economic growth and stock market in China

• Explaining the poor performance

– Firms that are listed are not representative of the economy as a whole

– Problems with the IPO listing process;

– Problems with the delisting process

– Corporate governance problems: either investment decisions are very bad

or there is tunneling or (probably) both

Imperial means Intelligent BusinessImperial College Business School 27

Concluding remarks (cont.)

• Implications:

– IPO listing process: Lowering standards, encourage the listing of more

privately owned and growth firms, administrative process => market

process

– Delisting process: Tougher regulations on delisting

– Improve corporate governance

• The 2015 bubble in the Chinese stock market

• Implications for UK investors