Embed Size (px)

Citation preview

Risk Management Offer

Overview & Perspectives

2

Introduction

Chappuis Halder & Co A strong expertise dedicated to financial risks

Visit our website: www.chappuishalder.com

3

Chappuis Halder & Co experience and expertiseFrom risk identification to risk monitoring

IDENTIFICATION

ASSESS &MEASURE

ALIGN

MONITOR

IMPLEMENT

Managementinformation& businessintelligence

Risk profile& quantification

Risk assessment

Integratedaccountability& information

structures

Risk-informedperformance

indicators

What are my risks ? How can I define them ?Determine key business objectives based on company strategy, establishing risk appetite across the organization

High risk or low risk ? How much I can loose ? Fair Valuation ?Using risk profile, assess likelihood and potential impact of identified risks to establish risk tolerance levels across organization

Can I face my risks ? How I have to deal with them ?Based on risk assessment, align resources and accountability structure with initiatives that fall within company risk tolerance

Which organisation for me ? Which infrastructure ?

Execute on strategy, identifying key performance indicators to gauge financial

and operational progress

How to manage my risks ? To reduce them ? To follow them ?

To price them ?Using risk-informed

performance indicators, monitor progress and risks to business objectives to identify areas for

performance improvement

With our experience and our experts, Chappuis Halder & Co would provide appropriate incentives at every level of your organization. It could help you at the time to manage “modern” risk alongside performance

4

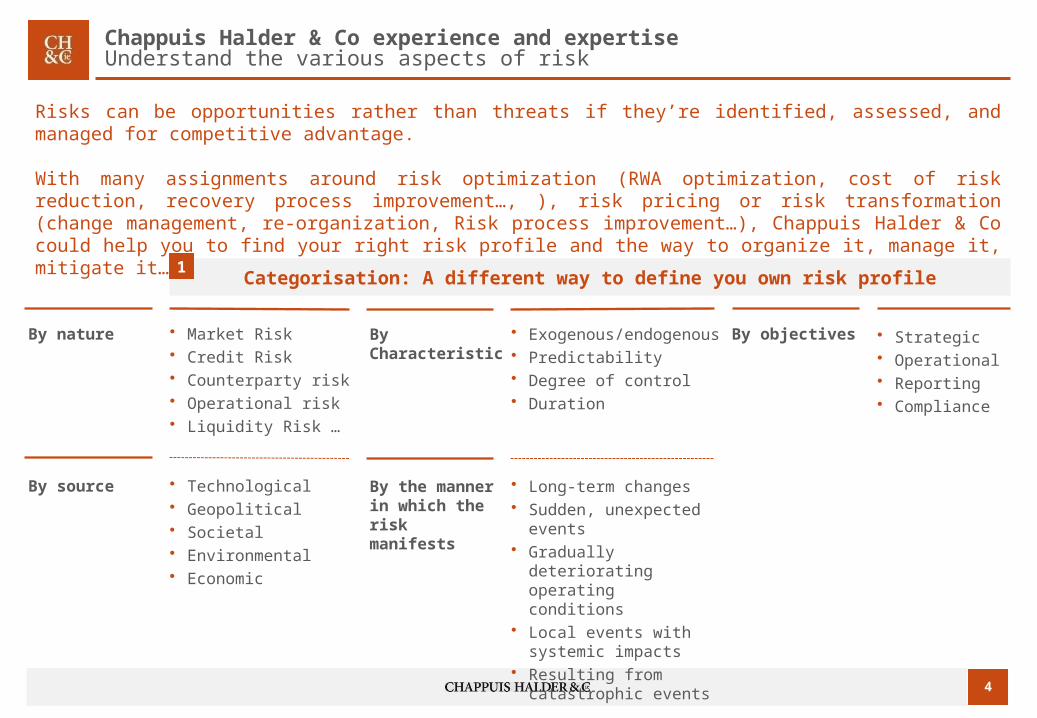

Chappuis Halder & Co experience and expertiseUnderstand the various aspects of risk

Risks can be opportunities rather than threats if they’re identified, assessed, and managed for competitive advantage.

With many assignments around risk optimization (RWA optimization, cost of risk reduction, recovery process improvement…, ), risk pricing or risk transformation (change management, re-organization, Risk process improvement…), Chappuis Halder & Co could help you to find your right risk profile and the way to organize it, manage it, mitigate it…

Categorisation: A different way to define you own risk profile1

• Market Risk• Credit Risk• Counterparty risk• Operational risk• Liquidity Risk …

By nature

• Technological• Geopolitical• Societal• Environmental• Economic

By source

• Exogenous/endogenous• Predictability• Degree of control• Duration

By Characteristic

• Long-term changes• Sudden, unexpected events• Gradually deteriorating

operating conditions• Local events with systemic

impacts• Resulting from catastrophic

events

By the manner in which the riskmanifests

• Strategic• Operational• Reporting• Compliance

By objectives

5

Why Risk Management is key for CH&CoRisk management at the heart of today’s banks business model

Financial institutions faced massive losses during the last crisis with dramatic impacts on the overall economy … During the financial crisis of 2007 – 2008, financial institutions faced significant losses that threatened

their own survival, and plunged the economy into a phase of turbulence

The causes of this turbulence were of different nature :> A confidence crisis> Liquidity and funding issues> Volatility and unpredictability of market parameters> High level of correlation between financial institutions

Context

Impacts

… As a consequence, new regulatory requirements were designed along with banks adjusting their business model• In order to restore trust in financial services, The Third Basel Accord came as an answer to the

shortcomings shown during the crisis with new liquidity and additional capital requirements

• In the same direction, banks are giving new trends to their business model, with risk modelling as a business integrated tool :

> Targeting and identifying new risk factors> Developing advanced and sophisticated modelling techniques to measure accurately risk levels in

an unpredictable world> Defining strategy and business trends based upon risk metrics consideration

6

Part 1

Banks’ business model in motionA business model driven by a risk culture

7

Agenda

Risk management : a multi-dimensional tool

Risk management : a large scope covering all banking activities

CH&Co risk management offer and nature of interventions

Credentials

1

2

3

4

8

Risk management functions in motionFrom a measurement tool to a more business oriented instrument with strategic guidance

1 RM* : instruments pricing & valuation• MTMarket• MtModel

2 RM : measuring and capturing market risks• Sensitivities• VaR models

RM : covering other financial risks • Credit IRB• Operational / AMA …

RM : developing advanced techniques for rare risks & complex instrum.• Stress Tests• Reputational risk• Very exotic products (CDO square…) / Securitization of securitizations

3

4

5

6

7

8

RM : optimizing profitability & managing business portfolio • ICAAP / Risk Appetite / RAROC• Scoring / collection• Funding/ Cash management

RM : computing for overall business purposes• Measure impacts on all dimensions (P&L, B/S, CT1,Treasury, ALM, stress testing)

RM : defining targets and steering strategy• EVA / Earnings Volatility • Strategic Plan, Risk Reserves

RM : solving complex multi-variable equations linked to strategy• Competitive positioning• Ideal target product mix, shareholder, asset-liability structure...

Futu

rePa

st

BUSINESS INTEGRATED modelling• Optimized algorithms and modules• Devices with enhanced computing capacity • Centralised, unlimited data storage capacity• Advanced modelling techniques, business

oriented

DYNAMIC modelling• Largely improved data storage capacity• Homogenisation of modelling practices• Regulatory incentives for modelling technique development

STATIC modelling• Low data storage capacity• Poor data quality• Devices with low computing power• Increase in banking transaction volumes• R&D development in CIB

Today’s average position

* RM refers to Risk Management including Risk Modelling

9

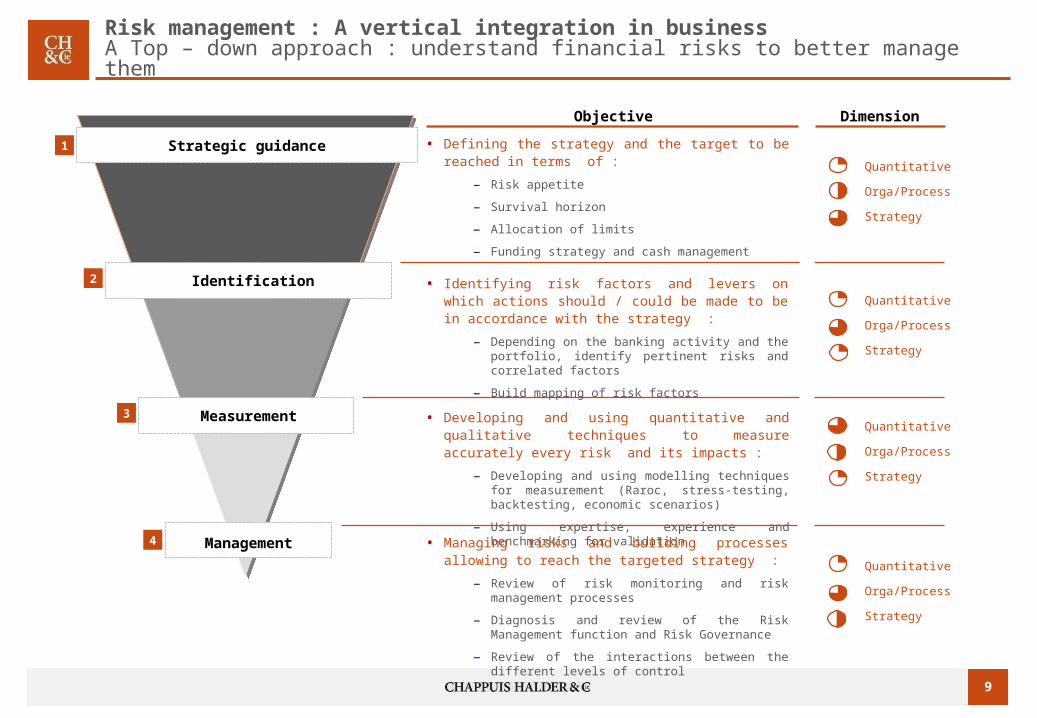

Risk management : A vertical integration in businessA Top – down approach : understand financial risks to better manage them

• Defining the strategy and the target to be reached in terms of :

– Risk appetite

– Survival horizon

– Allocation of limits

– Funding strategy and cash management

• Identifying risk factors and levers on which actions should / could be made to be in accordance with the strategy :

– Depending on the banking activity and the portfolio, identify pertinent risks and correlated factors

– Build mapping of risk factors

• Developing and using quantitative and qualitative techniques to measure accurately every risk and its impacts :

– Developing and using modelling techniques for measurement (Raroc, stress-testing, backtesting, economic scenarios)

– Using expertise, experience and benchmarking for validation

Measurement

Identification

Strategic guidance1

2

3

Management4 • Managing risks and building processes allowing to reach the targeted strategy :

– Review of risk monitoring and risk management processes

– Diagnosis and review of the Risk Management function and Risk Governance

– Review of the interactions between the different levels of control

Quantitative

Orga/Process

Strategy

Objective

Quantitative

Orga/Process

Strategy

Quantitative

Orga/Process

Strategy

Quantitative

Orga/Process

Strategy

Dimension

10

Agenda

Risk management : a multi-dimensional tool

Risk management : a large scope covering all banking activities

CH&Co risk management offer and nature of interventions

Credentials

1

2

3

4

11

All banking activities are concerned by managing and controlling risksCH&Co experiences and expertise cover the entire scope

Managing risks is about understanding all banking activities…

• During the crisis of 2007 – 2008, severe losses occurred across all banking activities

• Consequently, banks are considering to identify and control all types of risks in Retail Banking and Corporate and Investment Banking as well

• Whether it is about regulatory intent or simply for internal purposes, managing risks is now a major concern for banks affecting all banking activities and transactions

• Consequently, modelling and managing risks in banks are transversal and cross-disciplinary

… As well as understanding the dynamics of interactions between them

• Banking activities are not perfectly separated. They interact with each other (more or less, depending on the activities) which means that a risk within an activity can affect another and make risk contagion more likely

• Risk management can and must be an integrated tool for strategic decision making

• To do so, understanding the dynamics of interactions between banking activities is essential

• As an example, when a bank grant a credit for a counterparty, it must consider credit risk as well as funding and liquidity aspects

Financial purpose

Valuation

• Standard & Complex Instruments valuation

• Pricing (MtModel)• Parameters & Model Risk Reserves

Credit Risk

• Basel II : PD, LGD, CCF, EAD, RWA, UL• Basel III : CVA, DVA, Capital• Solvency II : Capital• Impairment, IFRS9• Stress testing,/ scenario

Market Risk ALM and Liquidity

• Sensitivities (Greeks, specific risks)• Stress Tests• Classic Var, Stress Var, Credit Var• Incremental / liquidity risk • Counterparty risk (CVA, DVA, FVA…)

• Basel III : LCR, NSFR, liquidity management, FVAA

• Securitization : SPV, collateral management

• Gap : cash flow patterns, survival horizon

Capital

• Economic Capital• ICAAP / Pillar II• Risk appetite

Strategic risks

Customer relationship management Business & strategies

• Credit granting model • Portfolio scoring model (recovery …)• Data quality• Data mining (descriptive statistics)• Big Data• Marketing

• Strategy guidance and decision• Reputation / Brand notoriety• Process optimization

Operational risk

• Fraud detection/ AMA models• Rogue trading

1

2

12

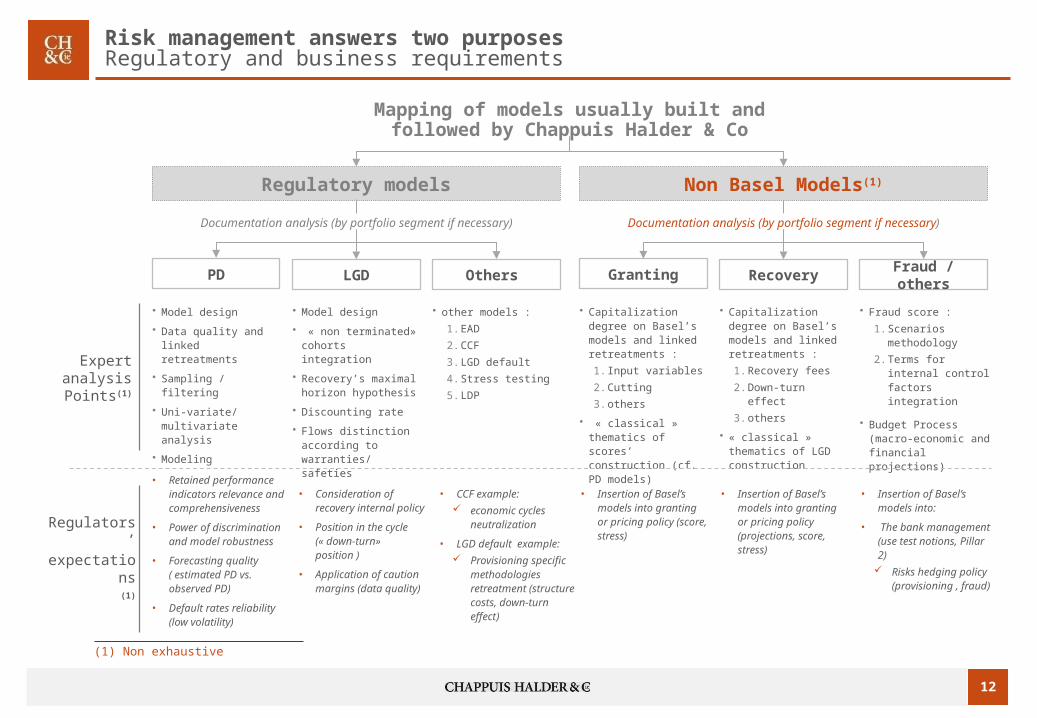

Risk management answers two purposesRegulatory and business requirements

Expert analysis Points(1)

Regulators’expectations

(1)

Regulatory models

PD

Non Basel Models(1)

LGD Others

(1) Non exhaustive

Granting Recovery Fraud / others

Mapping of models usually built and followed by Chappuis Halder & Co

Documentation analysis (by portfolio segment if necessary) Documentation analysis (by portfolio segment if necessary)

• Model design

• Data quality and linked retreatments

• Sampling / filtering

• Uni-variate/ multivariate analysis

• Modeling

• Division into classes

• PD Estimation

• Retained performance indicators relevance and comprehensiveness

• Power of discrimination and model robustness

• Forecasting quality ( estimated PD vs. observed PD)

• Default rates reliability (low volatility)

• other models :

1. EAD

2. CCF

3. LGD default

4. Stress testing

5. LDP

• Model design

• « non terminated» cohorts integration

• Recovery’s maximal horizon hypothesis

• Discounting rate

• Flows distinction according to warranties/ safeties

• Consideration of recovery internal policy

• Position in the cycle (« down-turn» position )

• Application of caution margins (data quality)

• CCF example: economic cycles

neutralization

• LGD default example: Provisioning specific

methodologies retreatment (structure costs, down-turn effect)

• Capitalization degree on Basel’s models and linked retreatments :

1. Input variables

2. Cutting

3. others

• « classical » thematics of scores’ construction (cf. PD models)

• Fraud score :

1. Scenarios methodology

2. Terms for internal control factors integration

• Budget Process (macro-economic and financial projections)

• Capitalization degree on Basel’s models and linked retreatments :

1. Recovery fees

2. Down-turn effect

3. others

• « classical » thematics of LGD construction

• Insertion of Basel’s models into granting or pricing policy (score, stress)

• Insertion of Basel’s models into granting or pricing policy (projections, score, stress)

• Insertion of Basel’s models into:

• The bank management (use test notions, Pillar 2)

Risks hedging policy (provisioning , fraud)

13

Risk function covers all types of portfolio and segmentsFrom retail to corporate passing by financial and sovereign counterparties

CH&Co expertise covers all types of portfolios with a benchmark of best practices on 3 different continents

By type of portfolio

2003 – Today

By activities

Today– 2017(*) 2003 – Today Today – 2017(*)

Decomposition of CH&Co expertise

Different methodologies for different types of underlying Different natures of missions for different types of clients

CIB 15%

RISK 37%

FINANCE 20%

STRATEGY 10%

IT 5%

BUSINESS / OPERATIONS 10%

HR 0%

MARKETING 3%

CIB 10%

RISK 15%

FINANCE 20%

STRATEGY 15%

IT 10%

BUSINESS / OPERATIONS 20%

HR

MARKETING 10%

EUROPE USASIA35% RETAIL (Mortgage incl.)

20% CORPORATE

15% BANK

15% SOVEREIGN

2% SPECIALISED LENDING

10% SECURITIZATION

3% OTHER (Funds, AM…)

High

Low

(*) CH&Co Analyses

Yesterday and today• Focus on retail portfolios due to better opportunities of RWA reduction • Focus on retail banking due to the massive use of statistical techniques• Development of heuristic models on Corporate portfolios • New models for banks and sovereigns as well as low default portfolios

Tomorrow ?• Geographic differences (Basel III,…) concerning risk modelling usage• Difference in timing due to different validation schedules according to local regulators• Importing European know-how in Asia and the US concerning Credit and operational models• Counterparty and liquidity risks seen as new form of modelling (particularly in Europe)

Yesterday and today • Managing risks is a key factor for modelling development (Basel II and III)• But financial issues are more and more concerned by modelling expertise (IAS 13, IAS39)• ICB have been dealing with counterparty credit risk since 2 / 3 years

Tomorrow?• Use of modelling techniques for strategic guidance and decision• Use of models to optimize business processes (recovery scores, anti fraud scores, granting)• Higher expectations for quantitative expertise demanded by regulators (CVA, funding risks…)• The “Big data” effect dictates the expansion of data mining and marketing

14

Agenda

Risk management : a multi-dimensional tool

Risk management : a large scope covering all banking activities

CH&Co risk management offer and nature of interventions

Credentials

1

2

3

4

15

A large scope of interventionWith expertise, experience and benchmarking at the heart of our business strategy

1. Finance 2. Pricing 3. ALM / Liquidity 4. Credit Risk 5. Market

Risk6. Operat. Risk

7. Business & Strategy

8. Customer relationship management

1.1 ICAAP / Pillar 2

1.2 Economic capital

1.3 Capital budgeting / RAPM

1.4 P&L and budget forecasting

2.1 Standard & Complex Models

2.2 Instrument pricing

2.3 Pricing Parameters control

3.1 Basel III : LCR, NSFR, liquidity

3.2 Securitization SPV, collat. manag.

3.3 Gap : CF patterns, survival horiz

3.4 Dynamic modelling

4.1 Basel II: PD, LGD, EAD, CCF, UL, RWA

4.2 Basel III, CVA, CCP, Capital

4.3 Solvency II : capital

4.4 Provision specific, collective

4.5 Stress & back testing

5.1 Classic & stress VaR, CVar

5.2 Risk reserves

5.3 Sensitivities Modelling & Calculation

5.4 Incremental and liquidity risk

6.1 Fraud detection

6.2 AMA models

6.3 Rogue trading

7.1 Strategy guidance and decision

7.2 Brand notoriety, reputation

7.3 Process optimization

8.1 Credit granting models

8.2 Portfolio scoring

8.3 Marketing and targeting

8.4 Data mining and descriptive statistics

0. Advanced Modelling, experience, expertise, benchmarking

Please, specify the subjects you are interested in, by checking the orange boxes

Legend

Business intentRegulatory intent

6.4 Operations structuring control

16

Modelling as an integrated business tool for great and diverse purposesA cross-disciplinary skills and decision-making facilitator tool

Modelling as a transversal tool

Risks1• Market : VaR computing, volatility,

liquidity, valuation• Credit : Basel II parameters,

Provisioning, stress, back testing• Operational : fraud, rogue trading...

Finance2• Manage Assets and Liabilities• Manage Economic capital (ICAAP)• Simulate P&L impacts• Capital Budgeting : RAROC etc…

Business3• Optimize operating model• Adapt marketing (CRM)• Scoring and targeting

customers

Strategy4• Build business strategy• Monitor reputation• Arbitrage between risk taking

and business development

Modelling allows Banks to forecast, anticipate, prevent, detect, measure, test, develop and decide… It is a powerful tool that requires a specific set of skills and knowledge

17

Modelling is more than just performing quantitative skills…… it is also about expertise, experience and benchmarking

The «New Way of Modelling » is about computing and using advanced technical and quantitative techniques as well as understanding banking activities environment, macro-impacts, dynamics of interactions, etc... It is much more that just performing quant techniques

What makes modelling a much powerful and greater tool… … for high level purposes and complex problems solving

A new way

of modelling

Solving complex quantitative problems in accordance with the banks environment and activity, and taking its characteristics into consideration

High level expertise & wide experience

Providing the bank with cutting-edge practices and placing it in a competitive environment where best practices are furnished as key strategic indicator

Benchmark & Best practices

Being in touch with a network of experts allows staying up to date with markets trends, strategic orientations and supervisor’s intentions and position

Network & People

1

« Model Validation »Validate models, methodologies or model implementation (in part or in full)

2

3

4

5

« Model Design »Design and build models / methodologies with advanced quantitative skills

« R&D » Promote R&D on academic / operational subjects and hot topics

« Task Force » Operate on confidential, touchy and highly sensitive subjects. Provide and perform targeted actions rapidly, whose results are to be quantified at the end of the assignment

«Business & Strategy modelling »Develop and use quantitative tools and instruments to improve strategy and define business orientations

18

What about modelling techniques and requirements ?The work tools

Main objectives• To give a quantitative perspective of a

specific context or for problem detections (by analysing data)

Underlying techniques• Data Mining• Statistics

Illustrations• Fraud detection• Portfolio analysis• Correlation analysis• Dashboard / reporting• Marketing …

Analyse1

Main objectives• To validate hypothesis and / or find the best

option of a specific strategy

Underlying techniques• Monte Carlo simulation• Bayesian networks• Fuzzy logic / Expertise

Illustrations• Capital planning• Strategic plan forecasting• Pricing• Stress testing …

Simulate2

Main objectives• To define and design a quantitative

methodology for strategy purposes or business decision

Underlying techniques• Benchmark• Experience/ Best practices

Illustrations• CVA desk implement.• « Cost of risk » hedging policy• Choice among different approaches …

Design5

Main objectives• To give a closed formula of a specific

problem

Underlying techniques• Mathematics• Statistics

Illustrations• RWA Calculation• Pricing• Marketing• Valuation (firm value)…

Solve3

Main objectives• To give an estimate or a prediction

(estimated probability of an event to happen under certain hypothesis)

Underlying techniques• Probability• Statistics

Illustrations• Risk parameter estimation (PD, LGD, EAD)• VaR / Credit VaR …

Predict4

19

Agenda

Risk management : a multi-dimensional tool

Risk management : a large scope covering all banking activities

CH&Co risk management offer and nature of interventions

Credentials

1

2

3

4

20

CH&Co credentials

Risk topics1

• Basel II - Market Risk• ALM• Collateral Management• Fraud prevention• Liquidity Risk

Organisation & process

References2

• Value at Risk model homologation• Review of the ALM model of a French bank• Collateral Management process review• Implementation of an anti-fraud unit to prevent rogue trading• Optimization of a liquidity follow-up process

• Basel II – Credit Risk

• Market Risk• Basel II – Op Risk• Basel III – Liquidity• Basel III – Capital• Impairment

(under IFRS)

Measurement & Validation

• Redesign of default probability model and implementation of the related rating tool

• LGD modelling for Corporate and Retail clients• Collective and specific provisions methodology review• VaR Backtesting through the hypothetical PNL• AMA methodology design• Impact assessment of Basel III liquidity ratios• CVA analysis under BIII, CCP (exposure and default fund) computation• Stress and back testing

• Risk Appetite• VaR & ES• CVA hedging• RWA• RAPM / RAROC

Strategy • Risk Appetite study• Comparative analysis between VaR and Expected Shortfall and impact

assessment of a model change• Opportunity study for a CVA hedging desk creation• RWA optimization and impacts simulation• Portfolio management optimization

21

Part 2

Banks’ organization restructuredAdapting to a changing environment

22

Agenda

A changing environment for financial institutions

By what banks transformation is driven ?

How to operate a successful transformation ?

1

2

3

23

All financial operators failed to foresee the scale and the magnitude of the crisis

• As monolines became important clients for rating agencies, a conflict of interest appeared and for too long, risks were underestimated

• As rating agencies are considered a risk barometer, an over-confidence was placed in information they gave

Rating agencies1

• Risk function had been put aside banks strategies because were not profit-only driven

• Risk managers did not have sufficient weight or knowledge to challenge front office models etc…

Risk managers 2

• Market participants were driven by profit regardless of risks they take

• It was a short term vision, not driven by durability or oriented toward a longer time scale

Market participants5

• Loopholes and shortcomings were revealed in rules defined by regulators to measure and identify accurately all risks

• Regulators put faith in markets self-regulation regardless of strong disturbance signals

Regulators 3

• As products became more and more complex, banks’ top managers did not always have a deep understanding of these products

• Knowing that they were highly profitable, top managers were blinded

Banks’ top management 4

24

There is an urgent need for restructuring banks…… Across all activities and business lines

The crisis had a significant impact on banks’ profitability …

… and more particularly CIB activities

2001 2006 20110%

4%

8%

12%

16% 15%17%

7%

BFI's ROE evolution - 2001 to 2011

CIB revenues are still too low…

• The economic context does not allow business expansion

• Economic growth is essentially at standstill in developed countries, and signs of slowing down are observed in emergent countries

• Fears of the European debt crisis make market participants unwilling to take risks and therefore limit their activities

• Banks focus on less risky activities and products which has an impact on the profitability

• Interest rates have reached historically low levels in both retail banking and CIB

Costs are still increasing …

• Taxes on financial transactions increase costs

• Risk cost have a direct impact on the P&L knowing that the euro crisis highly contributed in its increase tendency

New regulations will increase significantly banks capital

• With Basel 2.5 and Basel III, new capital charges are required to cover CVA risk as well as market risks

• Capital buffers must be constituted to neutralize systemic risks

Which can be explained by economic and political factors

2001 2006 20110%

5%

10%

15%

20%

15%

18%

8%

Banks' ROE evolution - 2001 to 2011

25

Agenda

A changing environment for financial institutions

By what banks transformation is driven ?

How to operate a successful transformation ?

1

2

3

26

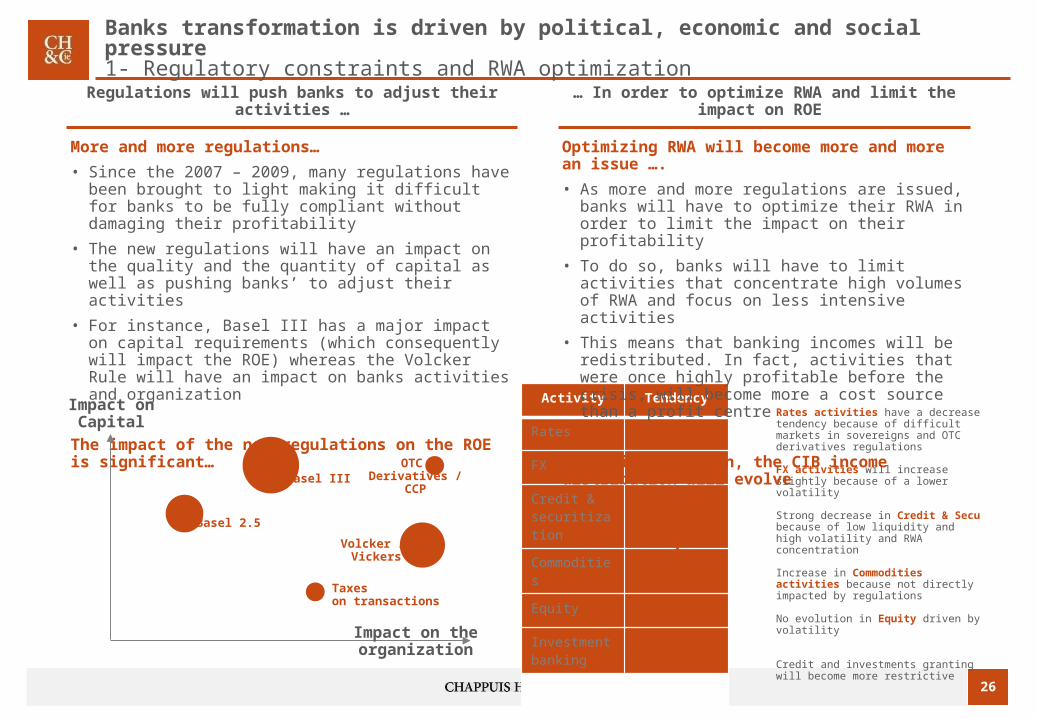

Banks transformation is driven by political, economic and social pressure1- Regulatory constraints and RWA optimization

Activity Tendency

Rates

FX

Credit & securitization

Commodities

Equity

Investment banking

Regulations will push banks to adjust their activities …

Optimizing RWA will become more and more an issue ….

• As more and more regulations are issued, banks will have to optimize their RWA in order to limit the impact on their profitability

• To do so, banks will have to limit activities that concentrate high volumes of RWA and focus on less intensive activities

• This means that banking incomes will be redistributed. In fact, activities that were once highly profitable before the crisis, will become more a cost source than a profit centre

As an illustration, the CIB income distribution will evolve

… In order to optimize RWA and limit the impact on ROE

More and more regulations…

• Since the 2007 – 2009, many regulations have been brought to light making it difficult for banks to be fully compliant without damaging their profitability

• The new regulations will have an impact on the quality and the quantity of capital as well as pushing banks’ to adjust their activities

• For instance, Basel III has a major impact on capital requirements (which consequently will impact the ROE) whereas the Volcker Rule will have an impact on banks activities and organization

The impact of the new regulations on the ROE is significant…

Impact on Capital

Impact on the organization

Basel III

Basel 2.5

Taxes on transactions

Volcker / Vickers

OTC Derivatives / CCP

Rates activities have a decrease tendency because of difficult markets in sovereigns and OTC derivatives regulations

FX activities will increase slightly because of a lower volatility

Strong decrease in Credit & Secu because of low liquidity and high volatility and RWA concentration

Increase in Commodities activities because not directly impacted by regulations

No evolution in Equity driven by volatility

Credit and investments granting will become more restrictive

27

Banks’ transformation is driven by political, economic and social pressure2- A structural change in the Risk management function

5 factors will lead to a major change in the risk management department, making it a more decision facilitator with strategic guidance …

Giving Risk managers more weight1

• Before the crisis, risk managers did not have sufficient power to make things change

• It is obvious that since the crisis, this has changed

• In fact, risk management is no more considered as a business killer but rather be used to enhance the quality of the business and reduce losses and identify profit opportunities

Giving Risk managers more talent2 A business integrated vision3

• All financial institutions have been strengthening their risk departments by recruiting new talents

• In fact, in order to challenge models and hypothesis used in the Front Office, banks understood that they need high-profile collaborators in their risk departments

• Moreover, as products became more and more complex, there was an urgent need for fully understanding risks driven by these products

• Managing risks correctly could no more be denied. In fact, as the “Too big Too fail” myth has been shattered forever, it was obvious that the strategy could no more be built without fully considering all risks

• Nowadays, in a changing and challenging environment, a good business strategy is driven by profit opportunities as well as taking acceptable risk levels

Instilling a risk culture4

• Banks faced massive losses because of unethical and irresponsible behaviours of some market operators, who neglected and underestimated risks they were taking

• One major change will concern changing mentalities and operational behaviours by instilling a culture of risk and therefore a more responsible and realistic attitude

Changing the way of managing risks5

• Risk management policy is also subject to evolution

• Credits granting policy is hardening with more selective criteria

• Moreover, risks will be managed in a dynamic way. For instance, pricing counterparty risk is more and more a common practice. In fact, OTC derivatives are no more considered as risk free and CVA is to be priced within the MtM of the deals

28

Banks’ transformation is driven by political, economic and social pressure3- Redefinition of strategic targets

Risk level

ROE

CIB activities

CIB activities

Retail Banking

Retail Banking

Redefinition of the Risk/Reward curve profile

• The Risk / Reward targets are to be revised because a business model oriented toward profit only is not viable as the crisis revealed

• Moreover, what was once highly profitable might not be today because of regulatory constraints

• Consequently, banks and financial institutions has to redefine their strategies in order to build up a new business model, viable on the long term with a good balance between risks taken and profitability, and by optimizing the impact of regulatory capital

Before the crisis

After the crisis

Banks’ strategy is now driven by more

considerations than before …

29

Banks’ transformation is driven by political, economic and social pressure4- Modifying the business approach : a more client oriented approach

The Business approach is also evolving by changing the client relationship management… From a short term relationship to a more long term relationship, based on client satisfaction

Change drivers

Long term relationships

• Fuelled by the need to limit conflict of interest, to reduce risks and to meet regulatory requirements, banks are building long term relationships, based on client satisfaction

1

Rebuild trust

• Banks are willing to rebuild confidence with their clients. These clients prefer relationship based on confidence and trust where transparency is a key element

Counselling and advising

• As a decline in ROE is witnessed because high profitable products are less popular, banks will have to return to a more advisory activity

Client strategy

• Optimizing business portfolio by managing accurately the client base : customized products by region, countries, age etc...

2 3

Products simplification

• As instruments became more and more complex, clients had been misled in their investments. Products simplification will enhance clarity as well as transparency

“Our first priority is and always has been to serve our clients’ interests” Goldman Sachs

“Our long-term, relationship-oriented approach has led clients to work with us on many of the most significant transactions in recent years”Morgan Stanley

Banks that can fully understand and meet client needs will reconquer trust and confidence, and therefore, create sustainable business

4 5

30

Agenda

A changing environment for financial institutions

By what banks transformation is driven ?

How to operate a successful transformation ?

1

2

3

31

Driving change management is key for a good transformation

Changing bad practices1

• Changing the “Golden Boy” attitude

• Refocusing on risks undertaken

• Challenging received ideas that are no more applicable in a new environment

• Rebuilding confidence and restoring a healthy image

• Working on clients loyalty by focusing primarily on maximizing clients profits and satisfaction

Adopting a risk culture2

• Moving from a profit culture to a more balanced culture driven by profit as well as risk considerations

• Accepting and understanding regulatory developments and requirements

• Considering risks as an integral part of business and strategy

• Giving risk managers more credibility and more importance

Raising consciousness3

• Understanding that every decision could lead to problems if not analysed nor fully understood

• Acting responsibly by respecting internal policies as well as client needs

• Building a sustainable and healthy business model that can last on the long term which will favour a stable banking industry and a viable sector

… for a more responsible and secure banking industry

Changing bad habits, changing minds, …

32

Making governance more reliable for a more transparent banking industry as well as for enhancing risk management

Enhancing reporting and clarity1

• Simplifying reporting dashboards to enhance clarity

• Building simple indicators for raising alerts in case limits are reached

• Alleviating processes for reporting production to enhance the availability of a clear information and fasten the flow and dissemination of information

• Building streams for relevant information to top management

Preventing and limiting frauds2

• Working and developing models and processes for limiting operational risk. For instance, Rogue trading must be subject to more work and research

• Preventing frauds by building reliable monitoring tools

• Fixing limits and maintaining follow-up

• Changing actual validation processes by making them more simple and efficient for a better judgement

• Optimizing these processes to accelerate decisions

• Redefining actors that are the most reliable and efficient for validation. For instance, validating hypotheses taken by the FO requires a specific knowledge and talent

• Making the validation step more than just a formality

Building efficient counter-powers4

• Strengthening counter-powers to guarantee a better risk management as well as limiting abuses

• Building efficient task forces teams (internal audit, risk managers, etc…) that have sufficient talents and weight to be able to challenge / criticize models and fully understand complex products as well as underlying risks

From a static approach to a more

proactive and dynamic approach for risk monitoring and governance…

Optimizing validation processes3

33

Rethinking organization to strengthen banks resilience as well as adapt business model to a changing and a complex environment

Restructuring the risk function1

• Giving the risk function more weight

• Recruiting new talents

• Including the risk function in business and strategy orientations

• Rethinking processes to make risk function a central actor

• Building a real time vision of consolidated risks

Reducing costs2

• Rethinking the organisation for cost cutting as business opportunities are more rare

• Reducing activities that are a great consumer of RWA and capital

• Deleveraging for risk cost reduction

• Moving to activities that are less taxed

• Building a flexible organization to withstand a rapidly evolving regulatory landscape

• Anticipating regulatory impacts and taking it into account within transformation programs

• Steering and monitoring transformation programs to meet with hot regulatory deadlines as well as political and social pressure

Standardizing organization4

• Standardizing organization across all geographic locations

• Standardizing organization across all business lines

• Standardizing organization across all products and asset types

A new flexible organization to meet with new needs and with a new business

model…

Adapting to regulatory constraints3

34

Part 3

Who are we ?CH&Co is more than just a consulting firm… it is an attitude

For more information: [email protected]

35

CH&Co is a worldwide network……With more than 60 consultants dispatched around the globe, over 3 continents

North America Europe Asia

New York• Established in 2011• 8 consultants• 7 projects in 2012

Montreal• Established in 2012• 1 consultant• 1 project in 2012

Paris• Established in 1996• 40 consultants• 40 projects since 2010

London• Established in 2010• 5 consultants• 6 projects in 2011

Hong Kong• Established in 2008• 15 consultants• 30 projects since 2010

Singapore• Established in 2011• 4 consultants• 4 projects in 2012

Shanghai• No office• 2 projects since 2011

Mumbai• No office• 2 projects since 2010

We are a global network, with specialized and dedicated teams, to provide high quality services at local and worldwide level, with the same quality and standards

For more information: [email protected]

36

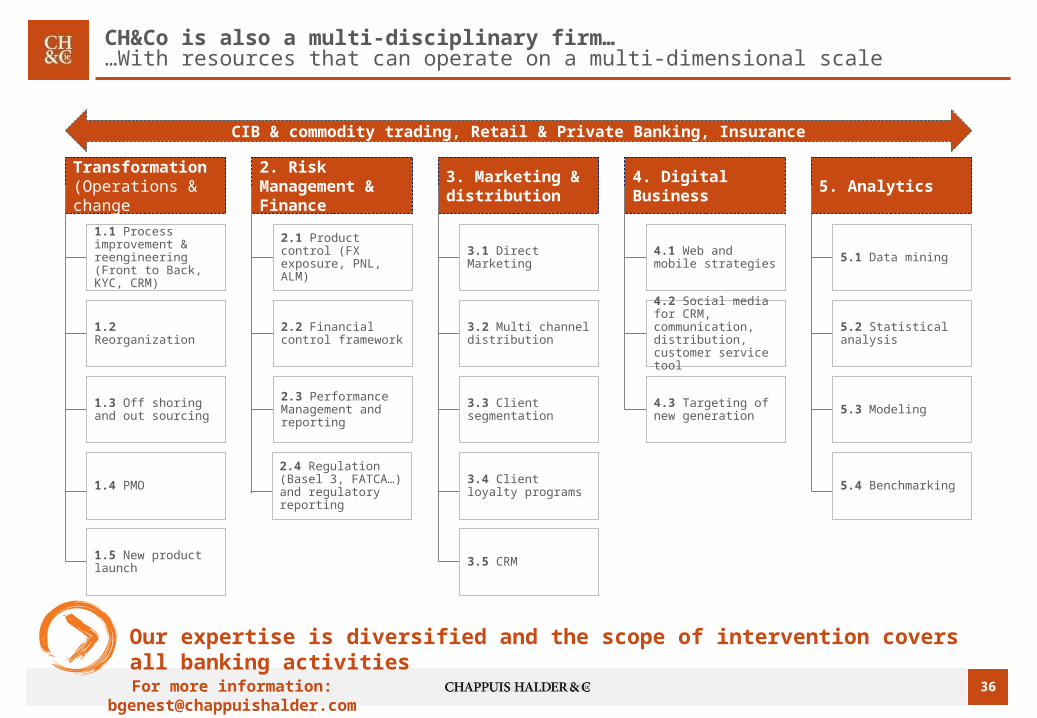

CH&Co is also a multi-disciplinary firm… …With resources that can operate on a multi-dimensional scale

Our expertise is diversified and the scope of intervention covers all banking activities

1. Transformation (Operations & change management)

2. Risk Management & Finance

3. Marketing & distribution 4. Digital Business 5. Analytics

1.1 Process improvement & reengineering (Front to Back, KYC, CRM)

1.2 Reorganization

1.3 Off shoring and out sourcing

1.4 PMO

1.5 New product launch

2.1 Product control (FX exposure, PNL, ALM)

2.2 Financial control framework

2.3 Performance Management and reporting

2.4 Regulation (Basel 3, FATCA…) and regulatory reporting

3.1 Direct Marketing

3.2 Multi channel distribution

3.3 Client segmentation

3.4 Client loyalty programs

3.5 CRM

4.1 Web and mobile strategies

4.2 Social media for CRM, communication, distribution, customer service tool

4.3 Targeting of new generation

5.1 Data mining

5.2 Statistical analysis

5.3 Modeling

5.4 Benchmarking

CIB & commodity trading, Retail & Private Banking, Insurance

For more information: [email protected]

37

CH&Co provided top-quality services for leading international companies

Corporate and Investment Banking / Asset Management Consumer

Commodity trading

For more information: [email protected]

38

NEW YORK600 Third Ave

2nd Flr, New YorkNY 10016, USA

PARIS44 rue du General Foy75 008, Paris, France

LONDONPalladia

60 Lombard streetLondon EC3V 9EA, UK

HONG KONG905, 9/F,

Kinwick Centre 32 Hollywood Road,

Central, Hong Kong

SINGAPORELevel 25, North Tower,

One Raffles Quay, Singapore 048583

MONTREAL19-18, boulevard René-

Lévesque O., Bureau 202Montrreal (Quebec)

H3P2P5 Canada

For more information: [email protected]